?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study investigates the association between employee-friendly schemes and firm financial performance using a frontier market, Vietnam, as a research context. We employ Anphabe’s “Top 100 Vietnam Best Places to Work” lists to identify companies with ideal employee-friendly practices. Using a data sample of more than 3,800 firm-year observations, we document a strong and positive relationship between employee welfare and firm performance measured by Tobin’s q. Our result is robust to a battery of sensitivity tests, including an alternative indicator of financial performance, alternative selection criteria, and different econometric techniques.

1. Introduction

The question of whether corporations gain benefits when they improve employee-friendly practices has long has attracted enormous attention from scholars and practitioners (Edmans, Citation2012).Footnote1 In parallel, competition in labor markets encourages firms to enhance workplace standards to attract and retain talent (Ghaly et al., Citation2015), subsequently facilitating corporate competitive advantages (Porter, Citation1985). Therefore, answering the denoted question would explain various vital decisions, including human resource management and other employee relations practices.

Existing theories offer contradictory predictions regarding the effect of employee-friendly practices on firm performance. While the traditional theory proposed by Taylor (Citation1911) suggests that generous employee treatment would dampen firm performance, the modern management theories (Maslow, Citation1943; McGregor & Cutcher-Gershenfeld, Citation1960; Pfeffer & Veiga, Citation1999; Zingales, Citation2000) demonstrate the opposing prediction. Moreover, empirical studies also depict that employee-friendly practices are associated with various financial decisions and behaviors which are beneficial to corporate performance such as cash holdings (Ghaly et al., Citation2015), innovation (Wei et al., Citation2020; J. Chen et al., Citation2016), or investment efficiency (Cao & Rees, Citation2020).

Relying on those denoted theoretical grounds, various studies have emerged investigating the roles of employee welfare on corporate value and performance. Notwithstanding, most studies targeting the influence of employee welfare focus on the U.S. market, where firm-level data on employee satisfaction is widely available. For instance, pioneering research popularly utilizes Fortune’s “100 Best Companies to Work for in America” (Bae et al., Citation2011; Edmans, Citation2012, Citation2011; Faleye & Trahan, Citation2011) or rich information from the Kinder, Lydenberg, and Domini Research and Analytics, Inc. Socrates database (KLD) (Boubaker et al., Citation2019; C. Chen et al., Citation2016; Faleye & Trahan, Citation2011; Ghaly et al., Citation2015).Footnote2

What receives modest attention is whether employee-friendly practices are beneficial or detrimental to financial performance for firms operating in non-U.S. and less-developed economies. We aim to fill this gap by investigating whether employee-friendly practices are beneficial or detrimental to the financial performance of Vietnamese firms. To the best of our knowledge, this is the first study that investigates this association in a typical frontier market like Vietnam using firm-level data.

After the Doi Moi, a national economic revolution in 1986, Vietnam achieved remarkable success in economic development and living conditions. Nonetheless, similarly to China, such achievement is based on cheap labor (Revilla Diez, Citation2016), raising the question of whether there is a trade-off between employee benefits and competitive advantage. Against this critique, Vietnam has been developing and strengthening legal frameworks, including the Labour Code, which targets various facets of employee treatment.Footnote3 In addition, the recent free trade agreements with the U.S. and Europe (e.g., the Trans-Pacific Partnership) urge the country and enterprises to practise corporate social responsibility (CSR) (M. Nguyen et al., Citation2018), in which employee relations are an important dimension. Thus, if a positive role of employee welfare is found in our study, there would be good reasons to continuously improve the Labour Code and CSR activities in Vietnam.

We employ the list of “Top 100 Vietnam Best Places to Work” by Anphabe to collect information about companies that offer superior employee-friendly schemes. Using a sample of more than 3,800 firm-year observations spanning seven waves of Anphabe’s reports, this study confirms a positive association between employee friendliness and corporate financial performance measured by Tobin’s q. Our finding is insensitive to alternative measures of financial outcome, different sampling criteria, and various econometric techniques.

We contribute to the extant literature in several aspects. First, unlike most of the recent literature, which heavily focuses on the U.S. market, we target a typical frontier market—Vietnam. This direction should merit the recent literature since the consequences of improving employee welfare is an essential issue for not only advanced but also emerging and frontier markets. Second, the effects of employee welfare on various facets of firm operations are ambiguous in less developed countries due to the lack of measures (Xu et al., Citation2020). As a response to this call, we retrieve data from the “Top 100 Vietnam Best Places to Work” reports. Thus, our study contributes to the growing strand of literature that attempts to propose alternative measures of employee welfare rather than using Fortune’s list or data from the KLD.Footnote4 Third, we provide evidence to support the notion that the modern management theories (Maslow, Citation1943; McGregor & Cutcher-Gershenfeld, Citation1960; Pfeffer & Veiga, Citation1999; Zingales, Citation2000) can be applied in the context of a less-developed market, subsequently fostering the potential implementations of practices which improve employee welfare.

The remainder of this paper is organized as follows. Section 2 shows the literature review and hypothesis development. In Section 3, we describe in detail the data and methodology used. Section 4 presents the empirical results. Finally, Section 5 concludes.

2. Literature review and hypothesis development

Employee welfare is a comprehensive term that includes a satisfying workplace (e.g., flexible working schedules, good working conditions, and attractive retirement plans) and employee benefits (e.g., career promotion and job security).Footnote5 Accordingly, employee welfare consists of both explicit contractual claims (e.g., regular salary or remuneration) and implicit/non-contractual agreements between a firm and its employees. Ghaly et al. (Citation2015) and C. Chen et al. (Citation2016) consider that employee welfare will be present if a company provides favorable policies such as better relations with unions, an efficient cash profit sharing scheme, employee involvement in decision making, work–life balance and so on.

There is no consensus on whether employee-friendly practices are detrimental or beneficial for corporate financial performance from the theoretical perspective.Footnote6 For instance, the traditional theory by Taylor (Citation1911) considers workers without special skills and social position as tangible inputs, such as raw materials. Under this view, employee welfare appears if those employees are overpaid or underworked, implying that generous employee treatment would dampen firm performance. In contrast, modern management theories (Maslow, Citation1943; McGregor & Cutcher-Gershenfeld, Citation1960; Pfeffer & Veiga, Citation1999; Zingales, Citation2000) consider human capital (i.e. employees) a vital asset. From this viewpoint, employees can contribute novel ideas or build strong ties with customers. Enhancing employee welfare is necessary to boost employee engagement and motivation, subsequently leading to better firm performance. In addition, a satisfying working environment ensures the attachment of talented employees who help firms gain advantages over competitors (Edmans, Citation2012).

Although built on conflicting theoretical grounds, empirical findings tend to document the benefits of employee-friendly practices to firm financial performance. For instance, Lau and May (Citation1998) compare two groups of companies. The first group contains 58 public companies in Fortune’s “100 Best Companies to Work for in America”. The second group consists of 88 companies listed in the S&P 100. The result depicts that the first group has higher asset growth, sale growth and profitability when compared to the second group. In a similar vein, Fulmer et al. (Citation2003) compare publicly traded companies in the Fortune list with a matched group and a large number of publicly traded companies in the U.S. market. The authors find that firms in the Fortune list outperform the matched group (broad market) in terms of return on assets and market-to-book ratio (cumulative returns).

Edmans (Citation2011) suggests that firms with higher levels of employee satisfaction (e.g., named in the “100 Best Companies to Work for in America”) gain significantly superior long-horizon returns over various benchmarks. Later, Edmans (Citation2012) uses the data sample of U.S firms spanning 1984 to 2011 to study the relationship between employee satisfaction and firm value. The author shows that companies in the “100 Best Companies to Work for in America” generate greater stock returns (approximately 3.8% per year) than their peers.

Faleye and Trahan (Citation2011) utilize a data sample of U.S. firms from 1998 to 2005 to explore the relation between employee-friendly practices and shareholder outcomes. Using Fortune’s list to capture firms with superior employee welfare, Faleye and Trahan (Citation2011) show that firms selected in the list have greater stock returns, financial performance, profitability and productivity. The result holds when using the KLD as an alternative for Fortune’s list. Meanwhile, Carvalho and Areal (Citation2016) show that firms selected in the “100 Best Companies to Work for in America” are more resilient during crises since their performance is not affected during “bear” markets. More recently, Chang and Jo (Citation2019) support the positive relation between employee-friendly practices for U.S. firms when using a sample of 19,089 firm-year observations from 1991 to 2012. Enhancing employee welfare can also mitigate the moral hazard problem resulting from an enhancement in unemployment insurance benefits. For instance, Darrough et al. (Citation2019) document a negative relationship between unemployment insurance benefits and firm productivity. However, the reductive effect of unemployment insurance benefits on productivity is mitigated by policies that benefit workers’ welfare.

Interestingly, a modern strand of research proposes alternative measures of employee welfare rather than using the Fortune’s list or data from the KLD. For example, Fauver et al. (Citation2018) retrieve information from the Asset4 dataset to construct a firm-level employee-friendly index (EF-index) which focuses on five aspects; namely, employment quality, health and safety, training, diversity, and human rights. The authors then find that firms treating their employees well tend to be highly evaluated (Tobin’s q) and have better performance (return on assets, return on equity). In a similar vein, Gupta and Krishnamurti (Citation2020) construct a firm-level indicator called the Employee Treatment Index (ETI) and find a positive link between ETI and Tobin’s q. Au et al. (Citation2021) develop an employee-flexibility score (FLEX) using textual analysis of online job reviews (obtained from a career-intelligence website). Using a sample of over 1.2 million reviews of S&P 1500 firms published between 2011 and 2017, the authors add that firms with a high flexibility score tend to have better stock returns. Fatmy et al. (Citation2022) focus on workforce diversity by using an indicator of LGBT friendliness. The result depicts that firms with more LGBT-friendly performance have better profitability and market valuation.

Using a machine learning approach, Ylinen and Ranta (Citation2021) employ a large dataset of approximately 250,000 crowdsourced employee reviews to investigate which dimensions of employee-friendly corporate culture can predict firm value and performance. Ylinen and Ranta (Citation2021) conclude that various employee-related dimensions can be seen as useful predictors of firm outcome, such as job security, attitude towards older colleagues, work–life balance, office/work environment, environmental friendliness, and workplace safety.

Moreover, there is also a rich strand of literature suggesting that enhancing employee satisfaction will lead to various financial decisions, which in turn create positive repercussions for firm overall performance. Specifically, some studies document the positive role of employee-friendly practices on innovation, which is a critical driver of performance (Koellinger, Citation2008; Thornhill, Citation2006). Using a sample of more than 8,900 firm-year observations between 1998 and 2010, J. Chen et al. (Citation2016) find that firms with employee-friendly workplaces tend to invest more in innovation and also gain more innovative success. C. Chen et al. (Citation2016) add that firms with better employee treatment schemes have more and better patents through improving employee satisfaction and teamwork. Wei et al. (Citation2020) show that employee welfare is conducive to corporate innovation in a large sample of all A-share listed manufacturing corporations on the Shanghai and Shenzhen stock markets over the period 2010 to 2017. Liu et al. (Citation2020), using a sample of 2,698 listed firms on the Shanghai and Shenzhen stock markets, add that firms with more employee-related CSR generate more innovation success.

Similarly, empirical studies depict that employee welfare is linked with the financial health of firms. For example, Ghaly et al. (Citation2015) suggest that a firm’s commitment to fair employee treatment positively influences cash holdings, using a sample of 13,752 firm-year observations in the U.S. market. Xu et al. (Citation2020) add that corporations named in the “China’s Best Employer Award 100” list tend to have lower leverage, suggesting that firms can credibly demonstrate their commitment to stakeholders and re-shape their capital structure by improving job satisfaction. Using a sample of more than 3,000 U.S. firms, Cao and Rees (Citation2020) document a positive association between employee-friendly treatment and labor investment efficiency. Focusing on corporate financing decisions, Saeed (Citation2021) confirms that employee-friendly policies negatively affect dividend payments. Therefore, “treating one group of stakeholders (e.g., employees) ethically may also influence the outcomes for other stakeholders—by undertaking the investment opportunities that improve firm value for shareholders” (Saeed, Citation2021, p. 604).

The above theories and empirics allow us to develop two opposing hypotheses as follows:

H1: Employee-friendly practices are positively associated with financial performance.

H2: Employee-friendly practices are negatively associated with financial performance.

3. Data and research method

3.1. Data

This study employs the list of “Top 100 Vietnam Best Places to Work” by Anphabe to collect information about companies that offer ideal employee-friendly practices.Footnote7 The “Top 100 Vietnam Best Places to Work” report was first introduced in 2013 by Anphabe, based on a nationwide survey.Footnote8 The annual reports and surveys have attracted thousands of employees from various industries, positions, departments and geographies. All surveys are conducted independently through a rigorous process, combining in-depth interviews, group and large-scale surveys.

The primary purpose of Anphabe’s surveys is to collect information on job motivation and expectations about ideal working conditions, including promotion opportunities, culture and value, financial benefits, reputation, management/leadership, and work and life quality. Anphabe’s lists are superior for our research purposes, especially when the level of employee satisfaction is difficult to measure (Edmans, Citation2011). In addition, the total number of respondents for Anphabe’s reports is enormous (from 9,032 respondents in 2013 to 71,460 in 2020) and far higher than any individual-level surveys conducted in the same context.

Our use of the “Top 100 Vietnam Best Places to Work” has both benefits and drawbacks. Regarding the benefits, the reports and lists are free and widely available on Anphabe’s website and popular media in Vietnam. In addition, the surveys and reports are done in consultation with large market research companies (e.g., Nielsen), facilitating the accuracy and validity of the questionnaires and their associated results . Nonetheless, detailed information on various facets of employee-friendly practices for each firm in the Top 100 cannot be obtained. Therefore, we cannot disaggregate employee welfare into separated dimensions as in Melián-González et al. (Citation2015), who used the Glassdoor website. In addition, Anphabe’s report does not have a fixed announcement date like Fortune’s “100 Best Companies to Work for in America”. Thus, the application of an event study as in Hannon and Milkovich (Citation1996) is infeasible.

In a similar vein to Lau and May (Citation1998) and Fulmer et al. (Citation2003), our objective is to investigate whether firms that appear on Vietnam’s Top 100 list have superior financial performance to firms that are not considered the “best places to work”. First, we retrieve the list of companies from Anphabe’s lists. Second, we gather information for all firms listed in two major stock exchanges, namely the Ho Chi Minh City Stock Exchange (HSX) and the Hanoi Stock Exchange (HNX), from Datastream. We extract financial data for seven years corresponding to seven surveys by Anphabe (i.e. 2013 to 2018 and 2020).Footnote9 Third, we remove firms with missing information on key variables proven to be associated with firm performance (such as firm size, cash holdings ratio, leverage, capital intensity). Our final data sample consists of 685 listed firms (356 and 329 firms listed on the HSX and HNX, respectively). Of these, the companies in Anphabe’s “Top 100 Vietnam Best Places to Work” are shown in .

Table 1. List of companies with favorable employee-friendly practices in the data sample

Some may worry that all the companies in Anphabe’s reports are listed on the HSX, and the inclusion of HNX listings may be redundant. Arguably, Anphabe’s surveys are widely available from the media, and indeed, the large number of respondents is strong evidence for the coverage and popularity of the “Top 100 Vietnam Best Places to Work” surveys and reports. Therefore, the absence of firms listed on the HNX in Anphabe’s list merely comes from interviewees’ perceptions.Footnote10

presents the 12 publicly listed companies (with available data) named in the “Top 100 Vietnam Best Places to Work” (according to year) in our sample.Footnote11

3.2. Research method

We employ the following model to investigate the relationship between employee welfare and firm financial performance:

where i, j, and t represent firm, industry and year, respectively. In model (1), we include industry fixed effects, σj, to control for unobserved and time invariant industry characteristics. In addition, we employ time fixed effects, θt, to take into account macroeconomics variables which influence firm financial performance.Footnote12

To measure firm performance, we use Tobin’s q. This indicator is computed as the market value of equity plus the book value of debt, all divided by the book value of total assets (e.g., T. Nguyen et al., Citation2015). We use the natural logarithm of Tobin’s q (LnQ) to enhance the normality of this variable.

We identify the firm-years in which a firm is included in the “Top 100 Vietnam Best Places to Work” list and code these firms with a value of one (i.e. D_BPTW = 1). All remaining firm-years equal zero.

F is the matrix of control variables at the firm-level.Footnote13 Following related studies (e.g., Faleye & Trahan, Citation2011), we employ the following controls: (i) firm size measured by the natural logarithm of total assets (in thousands VND); (ii) leverage indicated by the share of total debt on total assets; (iii) capital intensity measured by the share of capital expenditures on total assets; and (iv) cash holdings measured by the ratio of cash and short-term investments on total assets. All variables are winsorized at the first and 99th percentiles to reduce the influence of outliers. The definition and source of all variables are presented in .

Table 2. Variable definition and source

4. Empirical findings

4.1. Descriptive statistics and preliminary result

shows the descriptive statistics of all variables. The mean (standard deviation) of Tobin’s q is 0.846 (0.561). The mean value of Ln (Total assets) is approximately 20.580. On average, firms in our sample have a leverage ratio of 0.223, capital expenditures ratio of 0.045, and cash holdings ratio of 0.156. Lastly, the mean (standard deviation) of ROA is 7.157% (6.336%).

Table 3. Summary statistics and sample distribution

presents the correlation test. It is observed that the correlation coefficient of LnQ and D_BPTW is 0.148 (significant at the 1% level). In addition, firm size is negatively associated with financial performance. Next, firms with higher leverage ratio, capital expenditures ratio and cash holdings ratio tend to have higher financial performance. The correlation coefficient between ROA (%) and LnQ is 0.617 (1% level of significance), and between MTB and LnQ is 0.744 (1% level of significance). Thus, ROA (%) and MTB can be seen as appropriate alternative indicators for LnQ. The coefficients of correlation for pairs of variables are far less than 0.8, indicating that multicollinearity is less likely an issue in our study.

Table 4. Correlation matrix

For preliminary checking purposes, we aim to compare the mean of LnQ for two groups (firms named in Anphabe’s list and those unnamed) following a standard procedure described in Lau and May (Citation1998). In the first step, we conduct an F-test for the equality of variance of LnQ between two groups (null hypothesis: the variances are equal). We employ Brown and Forsythe (Citation1974)’s test, which is robust under nonnormality and skewed populations for the equality of variances. The F-test statistics (with p-value ranging from 0.306 to 0.509) suggest that we cannot reject the null hypothesis. Thus, a t-test with an equal variances assumption is suitable in the second step.

In the second step, we conduct a t-test for the difference between the mean of LnQ between two groups: firms named (D_BPTW = 1) and unnamed (D_BPTW = 0) in Anphabe’s list. The result shows that the group with higher levels of employee-friendly practices (D_BPTW = 1) have better financial performance than the remaining group, and the difference is statistically significant (p-value = 0.000).Footnote14

4.2. Main findings

shows regression results on the relationship between employee welfare and firm performance. We pay attention to the estimate on D_BPTW. If it is positive and significant, we find evidence confirming the positive role of employee-friendly practices on firm financial performance.

Table 5. The relationship between employee welfare and firm performance

In column (1), D_BPTW is the only explanatory variable, while all controls are included in column (2). It is observed that the estimates on D_BPTW are positive and significant at the 99% level of confidence in columns (1) and (2); that is, with and without other controls. Thus, the effect of employee-friendly schemes on firm performance is not driven by spurious correlations between other variables.

The empirical evidence suggests a positive relationship between employee welfare and firm performance, measured by Tobin’s q. Using the result in column (2) for illustration, we find that ceteris paribus, firms in the “Top 100 Vietnam Best Places to Work” perform 56.3% better than firms not on the list.

Our result is consistent with modern management theories (Maslow, Citation1943; McGregor & Cutcher-Gershenfeld, Citation1960; Pfeffer & Veiga, Citation1999; Zingales, Citation2000), which raise the importance of human resources on corporate performance. In addition, this positive relation is in accordance with empirical studies which employ the “100 Best Companies to Work for in America” list for the U.S. market, such as Faleye and Trahan (Citation2011), Fulmer et al. (Citation2003), Edmans (Citation2011), and Edmans (Citation2012).

Next, we employ alternative measures of financial outcome. Specifically, following Faleye and Trahan (Citation2011) and Fulmer et al. (Citation2003), in column (3) and column (4), we apply ROA and Market-to-book value as the dependent variable, respectively. It is observed that the estimates on D_BPTW are positive and significant in the last two specifications of , suggesting a positive relationship between employee-friendly practices and other firm financial outcomes (i.e. return on assets and market-to-book value).

4.3. Sensitivity tests

In this section, we conduct a battery of sensitivity tests to re-check the positive role of employee-friendly practices on firm performance. First, we estimate model (1) with industry fixed effects for each year the “Top 100 Vietnam Best Places to Work” report is available (2013 to 2018 and 2020). shows the result of this test.

Table 6. Sensitivity test: regression result for each year

It is evident that the estimates of the BPTW dummy are all positive and significant (at least at the 10% level of significance). The estimates on the D_BPTW variable vary from 0.366 (2020) to 0.755 (2013). Thus, the positive association between employee satisfaction and firm performance holds even when disaggregating our sample into separate years.

Next, we employ alternative sample selection criteria and present the tests in .

Table 7. Sensitivity tests using alternative sample selection criteria and alternative techniques

In column (1), we utilize a sub-sample of firms listed on the HSX. The rationale for this is that all Vietnamese listed companies in the “Top 100 Vietnam Best Places to Work” are on the HSX. In column (2), we focus on 2013–2018, which forms a standard panel dataset. The results using alternative sample selection criteria are consistent with the previous finding. Specifically, the coefficients of D_BPTW are positive and statistically significant at the 1% level, as shown in columns (1) and (2).

From column (3) through column (6), we apply alternative econometric techniques as follows. First, in column (3), we estimate model (1) using time-varying industry fixed effects (i.e. a dummy for each industry–year pair). By applying this technique, we are able to control time-varying factors across industries, such as industrial competition, which can alter the employee satisfaction−firm performance nexus (Chang & Jo, Citation2019). In column (4) and column (5), we respectively use time fixed effects and pooled ordinary least squares (OLS). Although the statistics of the Hausman test show that the fixed effects technique is superior, we still apply random effects for robustness testing purposes (column 6). As can be seen, the positive association between employee welfare and financial performance holds.

However, the results in this study may suffer from the reverse causality issue. Generally speaking, firms with superior financial performance tend to have conditions and resources to invest in various employee-friendly practices such as favorable salary and benefits, which subsequently enhance employee satisfaction. In other words, better performance leads to the higher possibility of being listed in the “Top 100 Vietnam Best Places to Work”.

In the following test, presented in , we aim to convincingly conclude that there is a causal effect of employee welfare on firm performance. We treat D_BPTW as an endogenous variable. Following Faleye and Trahan (Citation2011), we estimate a two-stage treatment effects model. In the first stage, we regress firm size (natural logarithm of total assets) and ROA (%) over D_BPTW using the Probit technique because D_BPTW is a binary variable.Footnote15 In the second stage, the predicted probabilities of being in the “Top 100 Vietnam Best Places to Work” (hereafter, Predicted BPTW) is used as the key predictor of financial performance measured by Tobin’s q. Note that in the second stage, industry and time fixed effects are applied.

Table 8. Sensitivity test using two-stage treatment effects model

In column (1), it is evident that the estimates on Ln (Total assets) and ROA (%) are statistically significant, implying that the utilization of those variables in predicting the probability of being in the “Top 100 Vietnam Best Places to Work” is suitable. From column (2), we observe that the coefficient of Predicted BPTW is positive and significant at the 1% level. Therefore, when using a two-stage treatment effects model, the positive role of employee-friendly schemes on financial performance is unchanged.

4.4. Additional analysis: falsification test

The main finding of this study indicates that firms listed in Anphabe’s “Top 100 Vietnam Best Places to Work” experience superior financial performance than those not on those lists. There are possible concerns that the findings could be driven by chance (e.g., the positive association may be attributable to other unobservable factors), or the information from Anphabe is somewhat misleading (e.g., cannot appropriately indicate ideal employee-friendly practices). To ease those concerns, we perform additional analysis, namely the falsification test.Footnote16

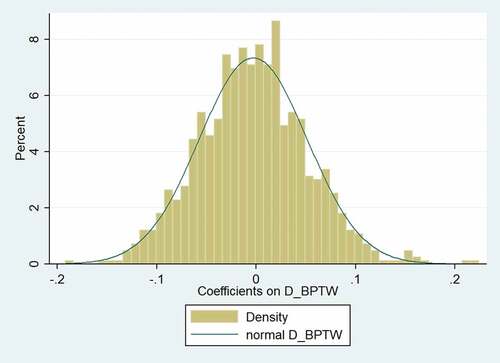

In the first step, we randomly select some pseudo best-place-to-work firms (those not on the list, but we assume they are on the list). In other words, we assign D_BPTW = 1 for firms even they are not recognized as “best places to work”. In the second step, we replicate the baseline regression (model 2) using the pseudo firms instead of the “real” best-place-to-work firms and obtain the estimated coefficients on D_BPTW. We reiterate this procedure 1,000 times. presents the distribution of coefficients of D_BPTW.

Figure 1. The distribution of estimated coefficients on D_BPTW for pseudo firms.

The figure documents that pseudo firms cannot create a strong and positive effect on financial performance, as can firms on Anphabe’s lists. Specifically, among the 1,000 pseudo samples, the coefficient on D_BPTW is far less than the coefficient on D_BPTW (0.563) shown in specification 2 of . Notably, the coefficient on D_BPTW in fluctuates from—0.192 to 0.213, indicating that a negative relationship is recorded for pseudo firms. The evidence is sharply different for firms on the lists because in all specifications of the main analysis, we observe the consistently positive association between D_BPTW and LnQ.

5. Conclusion

In this study, we revisit the relationship between employee welfare and firm financial performance. Unlike prior research, which extensively focuses on the U.S. market using Fortune’s “100 Best Companies to Work for in America” or the KLD database, we target a frontier market—Vietnam—where labor laws are still developing. In addition, CSR practices in Vietnam, such as improved employee relations, are still at an early stage.

Using the “Top 100 Vietnam Best Places to Work” by Anphabe, we document a positive relationship between employee welfare and firm performance measured by Tobin’s q. Our result is robust when employing alternative indicators of performance, alternative sample selection criteria and econometric techniques.

The finding in our study provides important policy implications for the design of Vietnam’s Labour Code and related regulations which aim to enhance the welfare of corporate employees. The result also offers a strong rationale for potential investment in CSR activities at the firm level, including improving employee-friendly schemes. Our study also validates and indicates the necessity of enhancing employee-friendly practices to gain better financial performance as suggested by a rich strand of management theory (e.g., Maslow, Citation1943; McGregor & Cutcher-Gershenfeld, Citation1960; Pfeffer & Veiga, Citation1999; Zingales, Citation2000).

Our paper cannot avoid some shortcomings. First, we cannot explicitly check possible channels through which employee welfare positively affects firm performance. Firm innovation is a candidate, as suggested by C. Chen et al. (Citation2016). Nevertheless, information on Vietnamese firms’ innovative activities (such as number of patents or citations of patents) is unavailable. Second, we are unable to disaggregate the level of employee-friendly practices since data on its various dimensions is not accessible. Thus, we were unable to capture the impact of each dimension on firm performance.

Acknowledgements

We would like to thank David McMillan (Senior Editor) and two reviewers for instructive suggestions. The authors thank Dalat University for financial support. Duc Nguyen greatly appreciates Robert Faff for his invaluable instruction during the “Pitching Research” section at Western Sydney University, Australia. Duc Nguyen dedicates this paper to his two sons (Bond and Pi). All remaining errors are our own responsibility.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Duc Nguyen Nguyen

Duc Nguyen Nguyen is a lecturer at the Faculty of Economics and Business Administration, Dalat University, Vietnam. He has published his work in peer-reviewed journals such as the Journal of International Financial Markets, Institutions and Money; Journal of Behavioral and Experimental Finance; Emerging Markets Finance and Trade; Economic Analysis and Policy; and Cogent Economics and Finance.

Quang Thai Truong

Quang Thai Truong has served as a lecturer at the Faculty of Economics and Business Administration, Dalat University, Vietnam. His recent studies have been accepted by Technological Forecasting and Social Change, Emerging Markets Finance and Trade, Review of Quantitative Finance and Accounting, Journal of Behavioral and Experimental Finance, and Journal of Asian Business and Economic Studies (JABES).

Nhat Thien Tran

Nhat Thien Tran is currently researching and teaching at the Faculty of Economics and Business Administration (from 2000 to now), Dalat University, Vietnam, where he is also Vice-Dean of the Faculty of Economics and Business Administration, and leads a research group in Economics and Finance. Research topics and publications include optimal growth in economics, and macroeconomic modelling.

Thuy T. Dang

Thuy T. Dang is currently Head of Department of International Relations and Integration Studies, Vietnam Institute for Indian and Southwest Asian Studies, Vietnam Academy of Social Sciences (VASS); and a lecturer at Vietnam Graduate Academy of Social Sciences, Vietnam. Dr. Dang has published in some of the world’s most prestigious journals and proceedings of international conferences on banking and finance.

Notes

1. The·extant literature on this topic uses “employee welfare” (Ghaly et al., Citation2015), “employee satisfaction”, “employee-friendly practices” or “employee-friendly schemes” (C. Chen et al., Citation2016; Edmans, Citation2012) interchangeably to avoid duplication. Edmans (Citation2011) and Edmans (Citation2012) consider that employees of firms listed in Fortune’s “100 Best Companies to Work for in America” tend to have higher levels of satisfaction. Ghaly et al. (Citation2015) consider that employees in firms with higher scores in “employee relations” (from the KLD database) will have higher levels of employee welfare.

2. KLD is the largest source of data for research on CSR. See, Mattingly (Citation2015) for a review of empirical papers using KLD.

3. The National Assembly passed the country’s first Labour Code in 1994. On 2 April 2002, a law amending and supplementing some articles of the 1994 Labour Code was passed by the National Assembly (effective 1 January 2003). On 29 November 2006, another law amending several articles of the Labour Code was introduced and took effect on 1 July 2007.

4. Such as Xu et al. (Citation2020), Fauver et al. (Citation2018), Gupta and Krishnamurti (Citation2020), Au et al. (Citation2021), and Fatmy et al. (Citation2022), and Ylinen and Ranta (Citation2021).

5. See more detail in Cornell and Shapiro (Citation1987) and C. Chen et al. (Citation2016).

6. Interestingly, traditional studies at the individual level find no significant relationship between job satisfaction and performance. For example, Brayfield and Crockett (Citation1955), Vroom (Citation1964), and Locke (Citation1976) suggest that employee satisfaction is not related to individual performance.

7. Also, see Xu et al. (2020) for the utilization of the “China’s Best Employer Award 100” list.

8. Anphabe is one of the leading companies in human resources in Vietnam. See more detail at https://www.anphabe.com/; reports are freely accessible at https://www.anphabe.com/survey-report.

9. Unfortunately, a survey from 2019 is not available.

10. In a sensitivity test, we use a sub-sample of firms listed on the HSX only.

11. Unfortunately, several banks are excluded from the sample (e.g. VCB, TCB, ACB, MBB, VPB, TPB) due to missing values. Prior studies targeting the impact of employee-friendly practices such as Ghaly et al. (Citation2015) also drop financial institutions from the data sample.

12. Following the guidance in Torres-Reyna (Citation2007), we conduct an F-test to determine whether time fixed effects are needed in the model. The statistics (F = 9.25, p = 0.000) reject the null that the coefficients for all years are jointly equal to zero. Thus, time fixed effects are required in this study. Next, we also perform the Breusch–Pagan Lagrange multiplier test to observe whether the OLS or random effects technique is suitable. The result supports the utilization of random effects instead of pooled OLS (chi-squared = 3,851, p-value = 0.000). Lastly, we use the Hausman test to determine between fixed and random effects. We find that the fixed effects technique as in model (1) is suitable for our analysis purpose (chi-squared = 662.58, p-value = 0.000).

13. For all variables, we employ Vietnam’s domestic currency (VND) to eliminate the influence of foreign exchange risk.

14. For brevity, the detail of the preliminary test is not shown, but it is available on request.

15. Faleye and Trahan (Citation2011) use firm size, ROA and R&D expenditures. Unfortunately, most Vietnamese firms do not report their investment in R&D projects.

16. This test is widely used in finance literature, for example Gao et al. (Citation2020).

References

- Au, S.-Y., Dong, M., & Tremblay, A. (2021). Employee flexibility, exogenous risk, and firm value. Journal of Financial and Quantitative Analysis, 56(3), 853–18. https://doi.org/10.1017/S0022109019001066

- Bae, K.-H., Kang, J.-K., & Wang, J. (2011). Employee treatment and firm leverage: A test of the stakeholder theory of capital structure. Journal of Financial Economics, 100(1), 130–153. https://doi.org/10.1016/j.jfineco.2010.10.019

- Boubaker, S., Chourou, L., Haddar, M., & Hamza, T. (2019). Does employee welfare affect corporate debt maturity? European Management Journal, 37(5), 674–686. https://doi.org/10.1016/j.emj.2019.08.004

- Brayfield, A. H., & Crockett, W. H. (1955). Employee attitudes and employee performance. Psychological Bulletin, 52(5), 396–424. https://doi.org/10.1037/h0045899

- Brown, M. B., & Forsythe, A. B. (1974). Robust tests for the equality of variances. Journal of the American Statistical Association, 69(346), 364–367. https://doi.org/10.1080/01621459.1974.10482955

- Cao, Z., & Rees, W. (2020). Do employee-friendly firms invest more efficiently? Evidence from labor investment efficiency. Journal of Corporate Finance, 65, 101744. https://doi.org/10.1016/j.jcorpfin.2020.101744

- Carvalho, A., & Areal, N. (2016). Great places to work®: Resilience in times of crisis. Human Resource Management, 55(3), 479–498. https://doi.org/10.1002/hrm.21676

- Chang, S., & Jo, H. (2019). Employee-friendly practices, product market competition and firm value. Journal of Business Finance & Accounting, 46(1–2), 200–224. https://doi.org/10.1111/jbfa.12353

- Chen, C., Chen, Y., Hsu, P.-H., & Podolski, E. J. (2016). Be nice to your innovators: Employee treatment and corporate innovation performance. Journal of Corporate Finance, 39, 78–98. https://doi.org/10.1016/j.jcorpfin.2016.06.001

- Chen, C., Chen, Y., Hsu, P.-H., & Podolski, E. J. (2016). Be nice to your innovators: Employee treatment and corporate innovation performance. Journal of Corporate Finance, 39, 78–98. https://doi.org/10.1016/j.jcorpfin.2016.06.001

- Chen, J., Leung, W. S., & Evans, K. P. (2016). Are employee-friendly workplaces conducive to innovation? Journal of Corporate Finance, 40, 61–79. https://doi.org/10.1016/j.jcorpfin.2016.07.011

- Cornell, B., & Shapiro, A. C. (1987). Corporate stakeholders and corporate finance. Financial Management, 16(1), 5–14. https://doi.org/10.2307/3665543

- Darrough, M., Kim, H., & Zur, E. (2019). The impact of corporate welfare policy on firm-level productivity: evidence from unemployment insurance. Journal of Business Ethics, 159(3), 795–815. https://doi.org/10.1007/s10551-018-3817-2

- Edmans, A. (2011). Does the stock market fully value intangibles? Employee satisfaction and equity prices. Journal of Financial Economics, 101(3), 621–640. https://doi.org/10.1016/j.jfineco.2011.03.021

- Edmans, A. (2012). The link between job satisfaction and firm value, with implications for corporate social responsibility. Academy of Management Perspectives, 26(4), 1–19. https://doi.org/10.5465/amp.2012.0046

- Faleye, O., & Trahan, E. A. (2011). Labor-friendly corporate practices: Is what is good for employees good for shareholders? Journal of Business Ethics, 101(1), 1–27. https://doi.org/10.1007/s10551-010-0705-9

- Fatmy, V., Kihn, J., Sihvonen, J., & Vähämaa, S. (2022). Does lesbian and gay friendliness pay off? A new look at LGBT policies and firm performance. Accounting & Finance, 62(1), 213–242. https://doi.org/10.1111/acfi.12787

- Fauver, L., McDonald, M. B., & Taboada, A. G. (2018). Does it pay to treat employees well? International evidence on the value of employee-friendly culture. Journal of Corporate Finance, 50, 84–108. https://doi.org/10.1016/j.jcorpfin.2018.02.003

- Fulmer, I. S., Gerhart, B., & Scott, K. S. (2003). Are the 100 best better? An empirical investigation of the relationship between being a “Great place to work” and firm performance. Personnel Psychology, 56(4), 965–993. https://doi.org/10.1111/j.1744-6570.2003.tb00246.x

- Gao, H., Hsu, P.-H., Li, K., & Zhang, J. (2020). The real effect of smoking bans: evidence from corporate innovation. Journal of Financial and Quantitative Analysis, 55(2), 387–427. https://doi.org/10.1017/S0022109018001564

- Ghaly, M., Dang, V. A., & Stathopoulos, K. (2015). Cash holdings and employee welfare. Journal of Corporate Finance, 33, 53–70. https://doi.org/10.1016/j.jcorpfin.2015.04.003

- Gupta, K., & Krishnamurti, C. (2020). Do countries matter more in determining the relationship between employee welfare and financial performance? International Review of Finance, 20(2), 415–450. https://doi.org/10.1111/irfi.12231

- Hannon, J. M., & Milkovich, G. T. (1996). The effect of human resource reputation signals on share prices: An event study. Human Resource Management, 35(3), 405–424. https://doi.org/10.1002/(SICI)1099-050X(199623)35:3<405::AID-HRM7>3.0.CO;2-0

- Koellinger, P. (2008). The relationship between technology, innovation, and firm performance—Empirical evidence from e-business in Europe. Research Policy, 37(8), 1317–1328. https://doi.org/10.1016/j.respol.2008.04.024

- Lau, R. S. M., & May, B. E. (1998). A win-win paradigm for quality of work life and business performance. Human Resource Development Quarterly, 9(3), 211–226. https://doi.org/10.1002/hrdq.3920090302

- Liu, B., Sun, P.-Y., & Zeng, Y. (2020). Employee-related corporate social responsibilities and corporate innovation: Evidence from China. International Review of Economics & Finance, 70, 357–372. https://doi.org/10.1016/j.iref.2020.07.008

- Locke, E. A. (1976). The nature and causes of job satisfaction. Handbook of Industrial and Organizational Psychology. https://cir.nii.ac.jp/crid/1573105975115113600

- Maslow, A. H. (1943). A theory of human motivation. Psychological Review, 50(4), 370–396. https://doi.org/10.1037/h0054346

- Mattingly, J. E. (2015). Corporate social performance: a review of empirical research examining the corporation–society relationship using kinder, lydenberg, domini social ratings data. Business & Society, 56(6), 796–839. https://doi.org/10.1177/0007650315585761

- McGregor, D., & Cutcher-Gershenfeld, J. (1960). The human side of enterprise (Vol. 21). McGraw-Hill New York.

- Melián-González, S., Bulchand-Gidumal, J., & González López-Valcárcel, B. (2015). New evidence of the relationship between employee satisfaction and firm economic performance. Personnel Review, 44(6), 906–929. https://doi.org/10.1108/PR-01–2014-0023

- Nguyen, M., Bensemann, J., & Kelly, S. (2018). Corporate social responsibility (CSR) in Vietnam: A conceptual framework. International Journal of Corporate Social Responsibility, 3(1), 9. https://doi.org/10.1186/s40991-018-0032-5

- Nguyen, T., Locke, S., & Reddy, K. (2015). Ownership concentration and corporate performance from a dynamic perspective: Does national governance quality matter? International Review of Financial Analysis, 41, 148–161. https://doi.org/10.1016/j.irfa.2015.06.005

- Pfeffer, J., & Veiga, J. F. (1999). Putting people first for organizational success. Academy of Management Perspectives, 13(2), 37–48. https://doi.org/10.5465/ame.1999.1899547

- Porter, M. E. (1985). Competitive advantage: Creating and sustaining competitive advantage. Free Press.

- Revilla Diez, J. (2016). Vietnam 30 years after Doi Moi: Achievements and challenges. Zeitschrift für Wirtschaftsgeographie, 60(3), 121–133. https://doi.org/10.1515/zfw-2016-0035

- Saeed, A. (2021). The impact of employee friendly practices on dividend payments: Evidence from emerging economies. Journal of Business Research, 135, 592–605. https://doi.org/10.1016/j.jbusres.2021.07.009

- Taylor, F. W. (1911). The principles of scientific management. Harper Brothers.

- Thornhill, S. (2006). Knowledge, innovation and firm performance in high- and low-technology regimes. Journal of Business Venturing, 21(5), 687–703. https://doi.org/10.1016/j.jbusvent.2005.06.001

- Torres-Reyna, O. (2007). Panel data analysis fixed and random effects using Stata (v. 4.2). Data & Statistical Services, Priceton University, 112.

- Vroom, V. H. (1964). Work and motivation. Wiley.

- Wei, Y., Nan, H., & Wei, G. (2020). The impact of employee welfare on innovation performance: Evidence from China’s manufacturing corporations. International Journal of Production Economics, 228, 107753. https://doi.org/10.1016/j.ijpe.2020.107753

- Xu, H., Ni, X., Li, C., & Liu, Y. (2020). Job satisfaction and firm leverage: Evidence from the “China’s best employer award 100” winners. China Journal of Accounting Research, 13(3), 309–325. https://doi.org/10.1016/j.cjar.2020.07.003

- Ylinen, M., & Ranta, M. (2021). Employee-friendly corporate culture and firm performance: Evidence from a machine learning approach. Available at SSRN 3813075. http://dx.doi.org/10.2139/ssrn.3813075; https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3813075

- Zingales, L. (2000). In Search of New Foundations. The Journal of Finance, 55(4), 1623–1653. https://doi.org/10.1111/0022-1082.00262