?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Non-performing loans (NPL) for banking are a necessity but a frightening specter. A high NPL indicates a bank’s failure to manage its business. The increasingly uncontrollable NPL with a net position of above 5% will make the bank a patient regulator in the category of banks under intensive or special supervision. Therefore, corporate governance (audit committee, CEO duality, and independent commissioners) is needed to stabilize and even minimize non-performing loans in banks’ 440 annual financial statements of emerging markets sourced from Bloomberg during 2016–2020. All research data will be processed by structural equation modeling based on partial least squares. The results of this study indicate that the audit committee, CEO duality, and independent commissioners do not affect non-performing loans. At the same time, financial performance positively affects non-performing loans. In other words, the financial performance variable cannot mediate the effect of good corporate governance on non-performing loans. Therefore, this research implies that the banking industry is expected to minimize the ratio of non-performing loans to create a healthy financial performance.

PUBLIC INTEREST STATEMENT

Non-performing loans are still terrifying things for banks. It is because the banking industry is an industry that is subject to the risk of an economic crisis, especially it involves public money and playing it in the form of various investments, such as credit, purchasing securities, and investing other funds. Therefore, banks must carry out their functions properly. The function includes a liaison function (financial intermediary) between savers (parties with excess funds) and lenders (parties who lack funds), development functions, service functions, and transmission functions. In addition, corporate governance is needed to oversee all banking business activities to minimize the ratio of non-performing loans so the bank’s health can be maintained.

1. Introduction

The banking industry grows rapidly because a bank is an agency that acts as a driving force for a country’s economy. Vetrova (Citation2017) defines a bank as a financial institution which deals with debits and credits. It lends, accepts and deposits money, builds the gap between the lenders and the borrowers. Banks are not only dealing with money but are also producers of money. Banks are required to compete to maintain the viability of the company. It aims to gain profits and avoid the existing risks. The banking sector is efficient if it can withstand negative impacts and contribute to financial system stability. One key indicator to assess bank function performance is the non-performing loan (NPL). A high NPL is an indicator of a bank’s failure to manage its business, including liquidity problems (inability to pay third parties), profitability (uncollectible debts), and solvency (decreased capital). Mingaleva et al. (Citation2014) stated that NPL is the most serious concern regarding the global financial crisis for many countries. Akomeah et al. (Citation2020) found a significant relationship between the credit risk management variables (NPL, CAR and SIZE) and the profitability of listed banks in Ghana. Al Zaidanin (Citation2020) concluded that the ranking approach shows that Bank of Jordan was in the top position followed by the Capital Bank of Jordan which related with NPL. Catherine (Citation2020) proved that strong credit appraisal puts the milestones for an effective management of credit risk and gives the firms a competitive advantage in the marketplace. Hence it can be concluded that credit appraisal defines a bank’s survival and profitability.

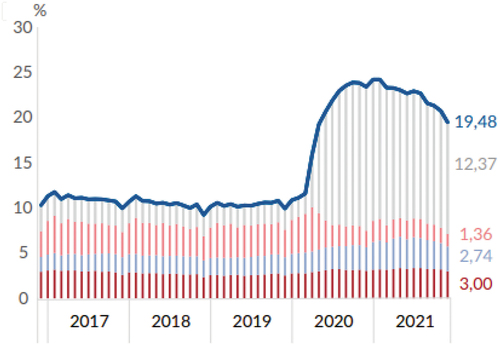

According to the International Monetary Fund, NPLs are those with a delay in interest payment and the loan itself of 90 days or more. The World Bank describes NPL as the ratio between non-performing loans to the total loan portfolio. If non-performing loans are high, it will disrupt bank profitability and operations (www.worldbank.org). China is one of the countries experiencing the impact of NPLs during the spread of Covid-19. It affected NPLs such as slowing credit distribution, declining asset quality, and tightening net interest margins. Apart from China, Hong Kong, and Taiwan also experienced growth in credit and fee income. The asset quality problem of Taiwanese banks is limited to a few sectors, including tourism, retail, and transportation. Meanwhile, Hong Kong banks may face more challenges from the spread of the COVID-19 virus and conflict in the country. Hong Kong’s economy is also more fragile due to China’s slowing economy than Taiwanese banks. Banks in Singapore, Malaysia, and Thailand are projected to be the most affected by the central bank’s policy of lowering its benchmark interest rate (www.worldbank.org).

An increase in the ratio of non-performing loans and credit costs is also a risk amid the COVID-19 outbreak, particularly in the banking, food and beverage, tourism, supply chain, shipping, retail, and domestic transportation sectors. Banks in Thailand and Malaysia also can be affected, while banks in Indonesia, Vietnam, and the Philippines are relatively overweight, so NPLs need to be emphasized to avoid losses. When the NPL continues to increase, it will negatively affect the bank. Dao and Kang (Citation2022) proved that NPL as a sharp increase in the lending spread, a reduction in output and a depreciation in the real exchange rate of the developing country. Lee (Citation2020) showed a positive interrelationship between bank profitability and loan growth.

Graphic 1. NPL Development during the Covid-19 Pandemic

Therefore, it is to minimize NPL through corporate governance and financial performance. Corporate governance (CG) is a set of principles that help an organization carry out its activities with integrity, fairness, and transparency. CG also helps an organization make the necessary disclosures and decisions about its transactions ethically. Balagobei (Citation2019) suggested that CG is the broadest control device, a hybrid of internal and external control mechanisms to utilize corporate resources efficiently.

Corporate governance that is consistently implemented can build public and international trust to positively impact the development of a good and healthy banking world. Implementing CG can provide a solid foundation for prudent and professional business practices in banking. This CG concept as a modern corporate management model is believed to bring change for better bank management in facing current and future challenges marked by intense competition between banks in winning customer trust and developing bank business. However not all good corporate governance in a company is carried out by what is aspired and expected. So far, many assumptions from various parties state that with the implementation of CG in a company, it can be ascertained that corporate governance has been running well without any shortcomings. In fact, it is not that simple because realizing CG requires extra struggle and support from several internal and external parties.

Liem (Citation2016) added that CG is crucial for the banking industry because it helps prevent banks from financial fraud causing financial difficulties and bankruptcy (Liem, Citation2016). GCG is a good shield for companies to fight corporate fraud (Salleh & Othman, Citation2016). Another phenomenon states that implementing good governance in banking is categorized into three parts: “Very Good, Good and Fair.” Still, the implementation of CG has not been able to prevent fraud in banking (Liem, Citation2016). Previous research has examined the impact of corporate governance on bank risk-taking, such as the findings of DeYoung et al. (Citation2013) that CEO risk-taking incentives lead to riskier business policy decisions concerning lending to businesses, non-interest-based banking activities, and investing in mortgage-backed securities in commercial banks. Calomiris and Carlson (Citation2016) examined bank ownership and risk-taking in banks in the 1890s and found that higher managerial ownership was associated with lower bank default risk.

Several studies have examined how banks with corporate governance regimes fared differently during crises. Anginer et al. (Citation2018) demonstrated that shareholder-friendly corporate governance results in higher risk for larger banks and banks in countries with large financial safety nets as banks try to shift risk to taxpayers. Berger et al. (Citation2016) found that high shareholding by lower-level management led to a much higher probability of default for commercial banks during 2007–2010. Beltratti and Stulz (Citation2012); Fahlenbrach and Stulz (Citation2011) found that banks with more shareholder-friendly boards and CEO compensation contracts experience worse stock market performance during financial crises. On the other hand, Ellul and Yerramilli (Citation2013) showed that the company had a strong and independent risk management function before the financial crisis. Anginer et al. (Citation2016) explained that CG negatively affects bank capitalization. Erkens et al. (Citation2012) described that financial institutions with more independent boards and higher institutional ownership experienced worse stock returns during the global financial crisis. Thus, weak corporate governance and excessive risk-taking can lead to severe banking instability and huge losses.

Corporate governance is believed to reduce non-performing loans, including the audit committee, CEO duality, and independent commissioners. The audit committee is tasked with internal supervision of the company on implementing audits, risk management, financial reporting processes, and corporate governance in the company. Supervision carried out by the audit committee is expected to improve financial performance, especially in banking. The bank’s financial performance is a picture of the success achieved by the bank in its operational activities. Therefore, a bank’s financial performance is the main and crucial factor in assessing the overall performance of the banking system itself. The performance of a bank can be assessed by analyzing its financial statements. Based on research by Ekinci and Poyraz (Citation2019) show that the audit committee significantly positively influences financial performance (ROA). Poudel and Hovey (Citation2012) added that the audit committee significantly affects the financial performance carried out in Nepal. However, Darwanto and Chariri (Citation2019) stated that the audit committee has a negative effect on the company’s financial performance.

Additionally, Magembe et al. (Citation2017) and Awan and Jamali (Citation2016) explained that the audit committee has a negative impact on non-performing loans (NPL). Finally, supported by Bussoli et al. (Citation2015) determined the effect of corporate governance on the quality of Italian cooperative bank loans. The results indicated that the board dimensions and loan quality were significantly and negatively related. It means more board members ensuring the quality of bank management and the presence of committees slowing down the loan quality and performance of Italian banks. Lee et al. (Citation2011) also stated that the audit committee has a negative effect on non-performing loans. Awan and Jamali (Citation2016) researched corporate governance as proxied by management size, CEO duality, and the size of the audit committee on financial performance. They found that the GCG mechanism affects financial performance. Layola and Sophia (Citation2016) explained that CEO duality has a negative effect on NPL with their empirical results. When corporate governance does not have strong regulations, the level of credit risk increases. According to Magembe et al. (Citation2017), CEO duality positively impacts non-performing loans. In other words, the loan quality will be quite good when the number of members increases. Thus, the separation of powers roles (chairman of the board and managing director will be two different people) is needed to speed things up.

Adnan et al. (Citation2013) stated that independent commissioners within banks play the role of balancing executives and management. They promote the proper functioning of the board and trigger internal dialogue to reduce larger areas of conflict of interest. Adnan et al. (Citation2013) proved that independent commissioners have a relationship with bank efficiency. Moreover, Awrey (Citation2013) claimed that independent commissioners influence loan quality. They elaborated that when independent board members work independently, it is possible to provide loans by conducting proper investigations. Even other board characteristics, audit committees, and board members also impact prices and non-performing loans. The finding is supported by research from Tahir et al. (Citation2018) explained that the corporate governance structure related to bank credit risk exposure is measured by the help of a bank’s credit growth. When independent board members help manage the bank’s management and reduce bank risk exposure, it significantly affects non-performing loans.

Meanwhile, Poudel and Hovey (Citation2012) argued that the size of independent commissioners has a negative effect on bank efficiency as measured by the NPL ratio. It is because independent commissioners are considered ineffective for this credit risk exposure due to their short tenure at the bank—on a short-term basis. Layola and Sophia (Citation2016) found similarly that independent commissioners have a negative effect on non-performing loans.

Balagobei and Velnampy (Citation2017) added a positive relationship between financial performance and non-performing loans. Likewise, with the results of Sheefeni’s research (Sheefeni, Citation2015), the impact of bank-specific predictors on NPL concludes that ROA, ROE, the ratio between loans and assets, and Logged Total Assets are the key factors for bank-specific Non Performing Loans in Namibia. On the other hand, Nenu et al. (Citation2018) stated that financial performance negatively impacts non-performing loans. The novelty of this research lies in the research model, which focuses on the effect of corporate governance mechanisms on non-performing loans with financial performance as a mediating variable. Therefore, the findings of this study are useful for banks to pay attention to corporate governance and the results of their financial performance to minimize non-performing loans to create a healthy bank.

2. Literature review

Agency theory considers company management as an agent for shareholders that will act with full awareness of their interests, not as a wise and prudent party and fair to shareholders (Jensen & Meckling, Citation1976). The bank itself has several risks, namely the risk that arises from counterparty failure to fulfill obligations. This risk causes a non-performing loan (NPL). NPL or credit risk is a risk caused by the inability of debtors to fulfill their obligations as required by creditors (Sheefeni, Citation2015). The higher the NPL, the worse the quality of bank credit, which causes the number of non-performing loans. As a result, the possibility of a bank being in a problematic condition is even greater. Darwanto and Chariri (Citation2019) added that the amount obtained of the Non-performing loan ratio is 5%, if it exceeds 5%, it will affect the soundness of the bank concerned.

Cadbury (Citation1992) defines corporate governance as a system used to direct and control an organization. It includes relationships between, and accountability of, the organization’s stakeholders, as well as the laws, policies, procedures, practices, standards, and principles which may affect the organization’s direction and control. Chen (Citation2021) add that corporate governance is the system of rules, practices, and processes by which a firm is directed and controlled. Corporate governance essentially involves balancing the interests of a company’s many stakeholders, such as shareholders, senior management executives, customers, suppliers, financiers, the government, and the community. The implementation of corporate governance practices includes five principles: transparency, independence, accountability, responsibility, and fairness, that arranged by the G20/OECD, where it is the international standard for corporate governance. The Principles help policy makers evaluate and improve the legal, regulatory and institutional framework for corporate governance, with a view to supporting economic efficiency, sustainable growth and financial stability (https://www.oecd.org/corporate/principles-corporate-governance/).

The formation of audit committees by public companies has been carried out in many countries (Darwanto and Chariri (Citation2019). The audit committee operates as a representative of the board of directors from whom it receives its powers to perform its corporate governance responsibilities which include overseeing and monitoring the organization’s financial reporting, disclosure, internal and external audit, internal control, regulatory compliance, and risk management activities; this applies to public, private, and mix sectors, as well as some non-governmental and not-for- profit organizations (Al-Baidhani, Citation2014). Along with the demand for companies to be more transparent and reliable regarding their performance, the role of audit committees has become increasingly important. An audit committee is exclusively composed of non-executive members, with at least one of them being independent. It illustrates that the independent member of the audit committee must have the necessary expertise in the field of accounting and auditing and has to fulfill the new independence criteria set out by the law (https://www2.deloitte.com/be/en/pages/risk/articles/audit-committee.html). Finally, the audit committee capable to enhance their supervision so that the company’s performance and the integrity of financial reports can be better.

Effective April 2003, the Securities and Exchange Commission (SEC) adopted a rule directing the national securities exchanges and national securities associations to prohibit the listing of any security of an issuer that is not in compliance with the audit committee requirements mandated by the Sarbanes-Oxley Act of Citation2002. The requirements relate to (1) the independence of audit committee members; (2) the audit committee’s responsibility to select and oversee the issuer’s independent accountant; (3) procedures for handling complaints regarding the issuer’s accounting practices; (4) the authority of the audit committee to engage advisors; and (5) funding for the independent auditor and any outside advisors engaged by the audit committee.

CEO duality is a person who serves in 2 roles, namely the CEO (board of directors) and chairman of the board (board of commissioners) in the company (Elvin et al., Citation2016). The CEO manages all the organisation’s resources with the power given by the board of commissioners. On the other hand, the board of commissioners is the supervisor of the CEO. CEO duality harms the company in terms of agency theory perceptions because it can hinder the board of directors in managing and the board of commissioners in assessing and supervising their performance (Grove et al., Citation2011). Moreover, management will not be separated from the element of conflict of interest so that it can influence decision-making for personal interests. This situation creates agency costs which result in less effective board work and a lack of independence, and it impacts the company’s overall performance (Johnson & Peterson, Citation2014). The monitoring function of the commissioners is also less effective because the person concerned must supervise the board of directors, including himself. In this supervision, there may be a conflict of interest and a higher risk of business operations (Elvin et al., Citation2016).

Independent commissioners demonstrate their existence as representatives of independent (minority) shareholders and represent investors’ interests (Elvin et al., Citation2016). Therefore, to protect the interests of independent shareholders, there must be a proper system, namely good corporate governance, which requires independent commissioners. These gives a signal that an independent board of commissioners in the company is essential in realizing good corporate governance.

The purpose of bank operations is to obtain optimal profits by providing financial services to the public. These objectives are met if the bank has and can maintain its performance well. Banks with good performance will increase the value of shares in the secondary market and can increase the number of funds from third parties. An indicator of good bank performance is the increase in public confidence in the bank, namely the increase in the value of shares and the number of funds from third parties. Customer trust and loyalty to the bank are necessary for bank management to formulate a business strategy. A bank’s financial performance is the result achieved by managing existing resources in the bank as effectively and efficiently as possible to achieve the goals set by the bank’s management. Therefore, the bank’s financial performance is part of the bank’s performance. The bank’s overall performance is a description of its operations regarding aspects of finance, marketing, fundraising and distribution, technology and human resources (Zaidanin et al., Citation2021).

3. Hyphotesis development

3.1. Audit committee and financial performance

The audit committee is a committee consisting of elected members of the board of commissioners whose responsibility is to assist in establishing an independent auditor on management’s proposals (Al-Baidhani, Citation2014). Thus, an audit committee is a group that is independent or has no interest in management and is specially appointed. They comprehend the field of accounting and other matters related to the company’s internal control system, which will have a good influence on the financial performance of the banking sector.

In line with agency theory, audit committee meetings function as a medium to correct mistakes that have been made and conduct evaluations of the company and evaluation of financial performance. The supervisory function on the audit committee will be more effective when they can contribute to the company’s internal control function because it can assist accountants in reducing their work time which will have an impact on the financial statements that will be produced faster. The frequency of audit committee meetings in a company can be influenced by various things, such as the tasks that the committee must carry out and the audit committee’s responsibilities to the company, especially those related to improving the company’s financial performance.

Ekinci and Poyraz (Citation2019), showed that the audit committee significantly positively affects financial performance as measured by ROE. In addition, the audit committee can influence the profitability of banks. The more effective the supervision of the audit committee will make the company’s performance optimal; it will affect the profitability of banks. This result is supported by Poudel and Hovey (Citation2012) that the audit committee positively affects financial performance.

H1: The audit committee has a positive effect on financial performance

3.2. CEO duality and financial performance

CEO duality harms the company in terms of agency theory perceptions because it can hinder the board of directors in managing management and the board of commissioners in assessing and supervising the board of directors’ performance (Coles et al., Citation2011). Moreover, management will not be separated from the element of conflict of interest so that it can influence decision-making for personal interests. This situation creates agency costs which result in less effective board work and a lack of independence, and it impacts the company’s overall performance (Fama & Jensen, Citation1983). The monitoring function of the commissioners is also less effective because the person concerned must supervise the board of directors, including himself. In this supervision, there may be a conflict of interest and a higher risk of business operations (Dechow et al., Citation1996). Finkelstein et al. (Citation1994) added that it would be difficult for the board of commissioners to report or dismiss a CEO with poor performance because the CEO is also his relative. Grove et al. (Citation2011) found that the dual leadership of the Chairman of the board with the CEO has a negative effect on financial performance. CEO duality can hinder the board of commissioners from their duties and responsibilities, including assessing and supervising the company’s performance, and it declines the performance. This study is in line with Sheefeni (Citation2015), who found a negative relationship between CEO duality and financial performance. They stated that it would be difficult for the board of commissioners to report or dismiss a CEO with poor performance because the CEO is also his relative.

H2: CEO duality has a negative effect on financial performance

3.3. Independent commissioner and financial performance

Independent Commissioners are members of the Board of Commissioners from outside the Issuer or Public Company and meet the requirements as independent commissioners. Independent commissioners act as representatives of stakeholders to oversee the company’s activities. Therefore, independent commissioners are in the best position to monitor and create good corporate governance. In line with agency theory, independent commissioners act as mediators in disputes with internal managers, oversee management policies, and advise management. The benefits of corporate governance can be seen from the premium paid by investors at the market price. The market value of companies that implement good corporate governance will be higher than companies that do not implement good corporate governance practices. However, good corporate governance is not enough if the board of commissioners carries out only supervision because members of the board of commissioners can come from the company’s shareholders or the board of directors. The minimum proportion of independent board of commissioners is 30% of the members of the board of commissioners. The more independent commissioners will be able to encourage the board of commissioners to act objectively and protect the interests of the company’s stakeholders, the better the supervision so that it can optimally control the company’s financial performance. The results of this study are in line with previous research conducted by Li et al. (Citation2014); Darwanto and Chariri (Citation2019) indicated the proportion of independent commissioners affects the company’s financial performance.

H3: Independent commissioners have a positive effect on financial performance

3.4. Audit committee and non-performing loan

In carrying out its duties, the board of commissioners is assisted by several committees, including the audit committee. The audit committee plays a crucial role in assessing credit risk. The main task is to provide an overview of accounting issues, financial reporting and explanations, internal control systems and independent auditors. The audit committee’s effectiveness can be measured by the number of meetings, attendance, size, and expertise in accounting and finance. Additionally, the average age of the audit committee and the different structural systems of each country’s board of commissioners and directors also show its effectiveness (Magembe et al., Citation2017).

In line with agency theory, audit committee meetings are also believed to become a means for its members to conduct discussions on the credit assessment process of third parties. It also supervises the possibility of problems in distributing credit to third parties. Accordingly, the more often the audit committee members hold intensive meetings, the better the credit quality will be, supporting the reduction of NPLs. Awan and Jamali (Citation2016) suggested that the audit committee can improve banking activities in identifying, controlling, and managing critical financial risks such as non-performing loans. It is expected that the audit committee can take into account risk assessments, control risks through contingency plans and take other risk management measures. Bussoli et al. (Citation2015) and Lee et al. (Citation2011) also explained that the audit committee negatively influences non-performing loans.

H4: The audit committee has a negative effect on non-performing loans

3.5. CEO duality and non-performing loan

Balagobei (Citation2019) believed that the impact of corporate governance variables on loan loss provisions is mixed. CEO duality has a negative effect on inventory loan losses. When corporate governance is not strong enough in regulation, the level of credit risk increases, resulting in an allowance for loan losses and vice versa. Based on agency theory, CEO duality can inhibit the board of directors from their duties and responsibilities, including assessing and supervising the loans of company management. This situation will create agency costs, resulting in the board’s work being less effective and reducing the company’s overall loans (Fama & Jensen, Citation1983). Grove et al. (Citation2011), Sivasubramaniam (Citation2020), and Elvin et al. (Citation2016) show that the effect of CEO duality and loan quality is significant and negatively related. It means more duality in CEO members who ensure the quality of bank management and members without reason, thereby slowing down loan quality and bank performance.

H5: CEO duality has a negative effect on non-performing loans

3.6. Independent commissioner and non-performing loan

An Independent Commissioner is a member of the board of commissioners who have no relationship in terms of financial, management, shared ownership and/or family with members of the board of directors, other members of the board of commissioners and/or controlling shareholder. They also have no relationship with the Bank that may affect the person concerned’s ability to act independently. Elvin et al. (Citation2016), The Independent Board of Commissioners is a supervisory agent with authority to supervise and protect minority shareholders and plays an important role in the decision-making process. Independent commissioner optimizes the implementation of banking governance, so it lowers the risk of bad loans in banks. When board members work independently, it is possible to make loans with proper investigation.

In line with agency theory, the supervision carried out by the board of commissioners has not been able to control the company, especially in distributing loans to third parties. In conclusion, the more independent commissioners will be able to encourage the board of commissioners to act objectively and protect the interests of the company’s stakeholders. It also results in better supervision to properly control the company’s loans. Balagobei (Citation2019) claimed that bank board members affect loan quality. Even other board characteristics, audit committee, and the number of board members also impact the lending price and non-price terms. Poudel and Hovey (Citation2012) and Layola and Sophia (Citation2016) also explained that independent commissioners have a negative effect on non-performing loans.

H6: Independent Commissioner has a negative effect on non-performing loans

3.7. Financial performance and non-performing loan

Tahir et al. (Citation2018) concluded that state-owned banks reduce bank performance and increase the risk of having dispersed ownership. For private banks, it improves company performance and reduces banks’ risk of concentrated ownership. The level of non-performing loans determines risk. All loan categories are described by the level of non-performing loans from a sample of banks. They inferred that increasing non-performing loans would reduce bank performance in the long run. Teshome et al. (Citation2018) conducted an analysis using the general technique moment method and concluded that non-performing loans have a negative impact on bank performance and lending behaviour. A high level of NPL worsens asset quality, and that is the cause of low profitability. In addition, it can reduce the ability to offer more or new loans in the future. Sheefeni’s research (Sheefeni, Citation2015) explained the specific impact of predictor banks on NPL. Nenu et al. (Citation2018) also illustrated that financial performance negatively influences non-performing loans.

H7: Financial performance has a negative effect on non-performing loans

illustrates the role of financial performance as a mediating variable in influencing corporate governance, which includes audit committees, duality of CEOs, and independent commissioners in controlling non-performing loans in the banking industry.

Figure 1. Research model.

4. Research method

This research involved all banks in emerging markets (China, India, Indonesia, Kazakhstan, Malaysia, Pakistan, Philippines, Thailand, Vietnam) from Bloomberg, a total of 427 banks in the 2016–2020 period. Sampling used purposive sampling with the following criteria: (1) emerging market banks that issued annual financial reports during the observation period; (2) banking in emerging markets that have complete data related to research variables; and (3) banking in emerging markets that did not experience losses during the observation period. Based on these criteria, the sample in this study is 440 banks’ annual financial statements during the observation period (88 banking x 5 years).

This study consists of 3 variables: the dependent variable (non-performing loan-NPL). NPL is measured by the ratio between non-performing loans and total loans. Independent variables (audit committee, CEO duality and independent commissioner). The audit committee is used to measure how effective the audit committee is in overseeing the company’s performance through financial reports (Darwanto and Chariri (Citation2019). The audit committee variable indicator is measured using the meetings of audit committee. The proxy for the CEO duality variable uses a dummy indicator, which is coded “1” if the chairman holds the position of CEO and “0” otherwise, while the independent commissioner variable is measured by adding up the independent directors. In addition to the dependent and independent variables, this study uses an intervening variable, financial performance. Financial performance is measured using return on assets (ROA) ROA to measure how well the company’s financial performance is obtained from the ratio between net income after tax and total assets (Ekinci & Poyraz, Citation2019).

The data analysis technique in this study used structural equation modelling based on partial least square with the WrapPLS application (Hair et al., Citation2017). The reason for using WrapPLS is (1) it can automatically estimate p-values for path coefficients. It can be seen that most other PLS software only gives the T value so that the user must compare it with the table T value or look for the p-value again; (2) can provide several indicators of model fit that can be useful for comparing the best model between different models. The resulting fit indicators include the R-squared average (ARS), average path coefficient (APC), and average variance inflation factor (AVIF); and (3) can provide output value of indirect effect and total effect along with p-value, standard error, and effect size. Here is the following equation:

Information:

η1 : Financial Performance

η2 : Non-Performing Loan

γ1-γ6 : Coefficient

ξ1 : Audit Committee

ξ2 : CEO Duality

ξ3 : Independent Commissioner

ς1- ς2 : Residual Value

4.1. Convergent validity and Average Variance Extracted (AVE)

4.1.1. Measurement model results (outer model)

Measurement model testing (outer model, often also called external relation or measurement model) shows how the observed variables are measured (Hair et al., Citation2017).

4.1.2. Validity test

The convergent validity test is related to the principle that the manifest variables of a construct should be highly correlated. The reflexive indicator can be seen from the loading factor value for each construct indicator. The rule of thumb is used to assess convergent validity. The rule is the loading factor value must be greater than 0.7. Another method to measure convergent validity is the Average Variance Extracted (AVE). If the AVE value of each variable has a value above 0.5, then it has met the convergent validity criteria (Hair et al., Citation2017).

The discriminant validity test relates to the principle that the different constructs (manifest variables) should not be highly correlated. Discriminant validity is measured from the value of the cross-loadings of each indicator and under the Fornell-Larcker criteria; namely, the AVE square root value of each construct must be greater than the correlation between constructs. Discriminant validity is considered valid if the loadings value of each indicator has a value greater than the loadings value of other variables (Hair et al., Citation2017).

4.1.3. Reliability test

The reliability test was conducted to prove the accuracy and consistency of the instrument in measuring the construct. There is a way to measure reliability, namely with composite reliability. In assessing construct reliability, the composite reliability value must be greater than 0.7. For example, suppose all latent variable values have a composite reliability value of 0.7. In that case, it means that the construct has good reliability, or the questionnaire used as a tool in this study is reliable or consistent (Hair et al., Citation2017).

4.1.4. Structural model testing

Structural model testing is carried out to see whether or not a relationship between variables in the model is strong and to test whether the hypotheses formulated in the study can be “rejected” or “not rejected” (Hair et al., Citation2017).

5. Result

5.1. Descriptive statistics

Table shows that the audit committee has a minimum score of 1,000 with a maximum value of 27,000, a median value of 10,000, an average value of 10,361 and a standard deviation of 5,121. CEO duality has a minimum value of 0.000 with a maximum value of 1,000, the mean value of this variable is 0.000, the average value is 0.056, and the standard deviation is 0.231. The independent commissioner has a minimum value of 0.000, maximum value of 10,000, a median value of 5,000 with an average value of 4,865 and a standard deviation of 1,753. Financial performance has a minimum value of −15,600, a maximum value of 442,000, and the mean value of this variable is 92,000. The mean value is 48,000, and the standard deviation is 7,541. Non-performing loans have a minimum value of 0.000, a maximum value of 70.100, and a median value of 288.000 with an average value of 823,000 and a standard deviation of 46,179.

Table 1. Descriptive Statistic

5.2. Measurement model results (outer model)

5.2.1. Convergent validity and Average Variance Extracted (AVE)

Table shows that the value of the outer loading generated is more than 0.70; hence each variable has a good convergent validity value, and the convergent validity requirements have been met. On the other hand, the average output variance extracted indicates a good AVE value for each construct because it has a value greater than 0.50 and is said to be eligible.

Table 2. Outer loadings and Average Variance Extracted (AVE)

5.3. Discriminant validity and composite reliability

Table describes that each construct with its indicators has a higher cross-loading value than the other. In other words, each indicator can predict latent constructs better than indicators from other constructs. The results of the composite reliability and Cronbach alpha values have more than 0.70, that is, 1,000. Each latent construct has good reliability because it has met the requirements of the composite reliability test and Cronbach’s alpha.

Table 3. Cross Loadings, Composite Reliability and Cronbach Alpha

5.4. Structural model test results (inner model)

5.4.1. Coefficient of determination (R2)

Table shows that the R-Square value on the financial performance variable is 0.004 or 0.04%. These results show that the financial performance variable can be explained by the audit committee, CEO duality and independent commissioner variables of 0.04% %. Meanwhile, the remaining 99.6% is explained by other variables. For example, the NPL variable has an R-square value of 0.523 or 52.3%. . The results demonstrate that the audit committee can define the NPL variable, CEO duality and independent commissioner variables, as well as the financial performance of 52.3% and other variables explain the remaining 47.7%.

Table 4. R-Square (R2)

5.5. Hypothesis test result

The inner model of hypothesis testing is carried out to answer the problems posed in this study with the results of the data analysis. Hypothesis testing was carried out according to the research framework to analyze and test directly and indirectly between exogenous variables and endogenous variables with a moderation model. The significance level of testing this hypothesis is done by looking at the p-value.

The results in Table and Figure show that in hypothesis 1, the audit committee does not affect financial performance with a p-value = 0.13. In conclusion, hypothesis 1 is rejected because the condition is p values > 0.05 and has a path coefficient of 0.05. The figure shows that if there is an increase in the audit committee, the financial performance will increase by 0.05 and vice versa; every time there is a decrease in the audit committee, the financial performance will decrease by 0.05. In effect size, where the value is 0.003, the audit committee affects the financial performance by 0.3%, and other variables influence the remaining 99.7%.

Table 5. Path Coefficients

Figure 2. WrapPLS.

Hypothesis 2 states that CEO duality does not affect financial performance with a p-value of 0.38. Hence hypothesis 2 is rejected because the condition is p values > 0.05 and has a path coefficient of −0.02. The figure implies that if there is an increase in CEO duality, financial performance will decrease by 0.05, and vice versa; if there is a decrease in CEO duality, financial performance will increase by 0.05. Therefore, CEO duality does not affect financial performance in the effect size, where the value is 0.000.

Hypothesis 3 believes independent commissioners have no effect on financial performance and have a p-value of 0.27. Therefore, hypothesis 3 is rejected because the condition is p values > 0.05 and has a path coefficient of 0.03. The figure shows that if there is an increase in the independent commissioner, the financial performance will increase by 0.03, and vice versa; if there is a decrease in the independent commissioner, the financial performance will decrease by 0.03. In effect size, where the value is 0.03, the audit committee affects the financial performance by 0.1%, and other variables influence the remaining 99.9%.

Hypothesis 4 explains that the audit committee has no effect on non-performing loans and has a p-value of 0.16. Thus hypothesis 4 is rejected because the condition is p values > 0.05 and has a path coefficient of 0.05. The figure shows that if there is an increase in the audit committee, the non-performing loan will increase by 0.05 and vice versa; every time there is a decrease in the audit committee, the non-performing loan will decrease by 0.05. In effect size, where the value is 0.02, the audit committee influences non-performing loans by 0.2%, and other variables influence the remaining 99.8%.

Hypothesis 5 indicates CEO Duality does not affect non-performing loans and has a p-value of 0.42. So, it can be concluded that hypothesis 5 is rejected because the condition is p values > 0.05 and has a path coefficient of −0.01. The figure shows that if there is an increase in CEO duality, non-performing loans will decrease by 0.01, and vice versa; if there is a decrease in CEO duality, non-performing loans will increase by 0.01. Therefore, in the effect size, where the value is 0.000, CEO duality does not affect non-performing loans.

Hypothesis 6 describes that independent commissioners do not affect non-performing loans having a p-value of 0.08. As a result, hypothesis 6 is rejected because the condition is p values > 0.05 and has a path coefficient of −0.07. The figure shows that if there is an increase in the independent commissioner, the non-performing loan will decrease by 0.07, and vice versa; if there is a decrease in the independent commissioner, the non-performing loan will increase by 0.07. In effect size, where the value is 0.06. It means the independent commissioner affects non-performing loans by 0.6%, and other variables influence the remaining 99.4%.

Hypothesis 7 explains that financial performance affects non-performing loans with a p-value of P < 0.1. Hence, hypothesis 7 is accepted because the condition is p values > 0.05 and has a path coefficient of −0.72. The figure shows that if there is an increase in financial performance, non-performing loans will decrease by 0.72, and vice versa; if there is a decrease in performance, non-performing loans will increase by 0.72. In effect size, where the value is 0.514. Accordingly, financial performance affects non-performing loans by 51.4%, and other variables influence the remaining 48.6%.

The results in Table of the effect size show that the effect of the audit committee on financial performance has a value of 0.003. It means that the audit committee affects the financial performance by 0.3%, and other variables influence the remaining 99.7%. The effect of CEO duality on financial performance has a value of 0.000; it reflects that CEO duality does not affect financial performance. Finally, the relationship between independent commissioners and financial performance has a value of 0.03. Accordingly, the independent commissioner affects the financial performance by 0.1%, and other variables influence the remaining 99.9%.

Table 6. Effect sizes for path coefficients

With the influence of the audit committee on non-performing loans, getting a value of 0.02, it can be concluded that the audit committee has an effect on non-performing loans by 0.2%, and other variables influence the remaining 99.8%. The relationship between CEO duality and non-performing loans is 0.000; this means that CEO duality does not affect non-performing loans. The influence of independent commissioners on non-performing loans, where the value is 0.06, means that the independent commissioners influence non-performing loans by 0.6%, and other variables influence the remaining 99.4%. Finally, the effect size between financial performance and non-performing loans, where the value is 0.514, means that financial performance affects non-performing loans by 51.4%, and other variables influence the remaining 48.6%.

6. Discussion

6.1. Audit committee and financial performance

The audit committee has a negative influence on financial performance. The direction of the negative relationship explains that the greater the meetings of audit committees, the lower the financial performance of banks. This research is in line with previous research conducted by Darwanto and Chariri (Citation2019), Ekinci and Poyraz (Citation2019), and Awrey (Citation2013). They believed that the audit committee had a negative effect on financial performance. In this study, the average meetings of bank audit committees is 10. It is in contrast with agency theory that the more the meetings of audit committees, the more control and supervision will be carried out; this will consider many decisions from audit committees that come from different educations. The possibility that can affect the decline in the ROA value due to the addition of an audit committee is that not all audit committees have expertise in accounting and finance, thus affecting the supervision of financial statements.

The practical implication of this study is that banks do not have to expand the number of audit committees because increasing audit committees will reduce financial performance. Efforts that the company must make are to reduce the number of audit committees and maximize their functions and duties so that supervision and consideration of company policies are not too strict so that financial performance is getting better even with a small number of audit committees.

6.2. CEO duality and financial performance

The results showed that CEO duality significantly negatively affected financial performance. As a result, companies with a duality leadership structure tend to have low financial performance. The results of this study are supported by Elvin et al. (Citation2016) and Grove et al. (Citation2011). They believed that the family relationship between the board of commissioners and the board of directors could hinder the board of commissioners from the duties and responsibilities of overseeing the company’s performance so that that performance could worsen. This research is also in line with Sheefeni (Citation2015). Moreover, management will not be separated from the element of conflict of interest; thus, it can influence decision-making for personal interests. This situation creates agency costs, making the board’s work less effective and lacking independence. Accordingly, it reduces the overall performance of the company. These empirical results are supported by agency theory which holds that structure.

6.3. Independent commissioner and financial performance

The proportion of independent commissioners does not affect financial performance. The size of independent commissioners’ proportion in the company does not affect the company’s financial performance. The results of this study are in line with previous research conducted by (Ga, 2010), Li et al. (Citation2014) and Darwanto and Chariri (Citation2019), stating that the proportion of independent commissioners does not affect the company’s financial performance. The results of this study can occur because there are many proportions of independent commissioners in banking. The supervision carried out by independent commissioners will minimize management actions that only think of the company’s interests and reduce fraudulent activities that can harm the company. The proportion of independent commissioners in the 440 banking samples is only 48% on average. Therefore, this result contradicts agency theory, it is considered not to make a positive contribution to financial performance because the provisions for the proportion of independent commissioners have not been fully implemented. As a result, it cannot guarantee the immaculate function of supervision, management, decision-making, and accurate decisions within a company.

6.4. Audit committee and non-performing loan

The results of the audit committee analysis appear to have not an impact on credit risk. The results of this study contradict the agency theory, the more the number of audit committees, the more control and supervision will be carried out; this will consider many decisions from audit committees that come from different educations. Audit committee meetings are also believed to be a means for its members to conduct discussions on the credit assessment process of third parties. It can also supervise the possibility that problems will arise in distributing credit to third parties. Unfortunately, the large number of meetings held by the audit committee did not affect the decrease in NPL. According to Shaoib et Awan and Jamali (Citation2016), the audit committee can improve banking activities by identifying, controlling, and managing critical financial risks such as non-performing loans. It is expected that the audit committee can take into account risk assessments in the form of the main risks faced by banks, control risks through planning contingencies and take other risk management. Different with Magembe et al. (Citation2017) that effective credit risk management requires an increase in the meetings number of audit committee and an increase in the number of independent members on the audit committee.

6.5. CEO duality and non-performing loan

Grove et al. (Citation2011) argued that the impact of corporate governance variables on loan loss provisions is mixed. CEO duality has a negative effect on inventory loan losses. Their relationship status is also mixed; some relationships are significant, and some are not. They concluded with their empirical results that when corporate governance is not strongly regulatory, the level of credit risk increases. It results in an allowance for loan losses. Italian bank cooperative loan quality shows that board dimensions and loan quality are significant and negatively related, and the number of committee members negatively impacts loan quality. This is contrary to agency theory, it extends, meaning that more and more members of CEO duality ensure the quality of bank management and committees without reason to slow down loan quality and bank performance. Layola and Sophia (Citation2016) explained that CEO duality negatively influences non-performing loans.

6.6. Independent commissioner and non-performing loan

A negative relationship is identified between the independent board, bank performance, and non-performing loans in banks. The study also found that management tried to reduce the company’s non-performing loans. The study findings prove that management effectiveness depends on shareholders’ decisions through voting rights. On the other hand, Balagobei (Citation2019) found a non-significant relationship between dependent boards and non-performing loans. The Independent Board of Commissioners is the supervisory agency with the authority to supervise and protect minority shareholders and plays an essential role in the decision-making process. The existence of an independent commissioner and the implementation of banking governance is considered optimal for reducing the risk of bad loans in banks (Sivasubramaniam, Citation2020). In contrast to agency theory, when board members can work independently, it is possible to make loans with proper investigation. It is supported by research from Poudel and Hovey (Citation2012) and Layola and Sophia (Citation2016), which explain that independent commissioners significantly influence non-performing loans.

6.7. Financial performance and non-performing loan

In the context of Namibia, (Sheefeni, Citation2015) described the impact of bank-specific predictors on NPL. ROA is the main bank-specific factor of Non-Performing Loans. European Central Bank (ECB; Citation2017) stipulates that the ratio of non-performing loans (NPL) is 5%. It encourages banks to overcome non-performing loans. ECB has issued various regulations that rescue credit, often called “Credit Restructuring.” Banks make an effort in credit business activities so that debtors can fulfill their obligations again. The bank’s business is to provide credit; hence it does not deposit capital as a shareholder or a pawning institution (Nenu et al., Citation2018). Credit is temporary and must be paid in full. Therefore, credit risk is lower than shareholder risk. The bank is also not a place for foreclosure and the sale of collateral.

It is in line with agency theory; banks with higher incomes are less attracted to riskier investments (Possible NPL) because ROA and ROE are negatively related to NPL. However, the research shows the opposite fact; the average of 440 banking samples shows a non-performing loan value of 8.23%. Furthermore, it shows that the average non-performing loan in banking in emerging markets is considered high, which can be concluded to have a low ROA and bad credit. The empirical results of this study can be helpful and may have significant implications for policymakers and bankers. Policymakers can develop policies to ensure that bankers monitor non-performing loans. In addition, policymakers must reform new policies directed at the correct dimensions of corporate governance. An increase in NPLs will move the economy in a less stable direction and encourage declining growth in the banking sector. This result consistent with Le (Citation2020) that bank profitability has a positive interrelationship with loan growth.

7. Conclusion

Based on 440 annual financial reports of the banking industry in the Emerging Market sourced from Bloomberg for 2016–2020, it shows that financial performance affects NPL. While the audit committee, CEO duality, and independent commissioners do not affect financial performance and NPL. Thus, the banking industry that has implemented GCG in its operational activities has no impact on financial performance and NPL.

This research has implications: (1) theoretically, it can be a reference and literature for further research; (2) practically, for banks in emerging markets, it can be a form of evaluation so that the existing corporate governance can be consistent. In addition, the results of this study influence banking managers to always pay attention to the extent to which the soundness of the company’s financial performance can minimize the level of the NPL ratio. For regulators, it can improve the quality of standardization in establishing regulations regarding governance implementation. Finally, for investors, this can be a guide for investing.

The limitations of this study are the low ability of the corporate governance variable (audit committee, CEO duality, and independent commissioner) to explain the financial performance variable, which is only 0.04% %. Furthermore, the ability of the corporate governance variable (audit committee, CEO duality, and independent commissioner) to explain the NPL variable is quite large, namely 52.3%. Future research is expected to examine other variables that can reduce the NPL ratio with different research samples and observation periods to enrich the financial accounting literature.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Indri Kartika

Indri Kartika is a lecturer at the Faculty of Economics, Universitas Islam Sultan Agung. Her areas of interest are financial accounting, corporate social responsibility, corporate governance, and banking.

Sri Sulistyowati

Sri Sulistyowati is a lecturer at the Faculty of Economics, Universitas Islam Sultan Agung. Her areas of interest are financial accounting, auditing, accounting information system, and taxation.

Budi Septiawan

Budi Septiawan is a lecturer at the Faculty of Economics and Business, Universitas Pasundan. His areas of interest are financial accounting, accounting information system, informationyt system, digital accounting, digital business and accounting for MSME.

Maya Indriastuti

Maya Indriastuti is a lecturer at the Faculty of Economics, Universitas Islam Sultan Agung. Her areas of interest are financial accounting, green accounting, corporate social responsibility, corporate governance, sharia finance, banking, and taxation.

References

- Cadbury. (1992). Report of the Committee on the Financial Aspects of Corporate Governance. London: Gee.

- Adnan, M. A., Htay, S. N. N., Rahid, H. M. A., & Meera, A. K. M. (2013). A panel data analysis on the relationship between corporate governance and bank efficiency. Journal of Accounting Finance and Economics, 1(1), 1–43. https://www.academia.edu/5925034/A_Panel_Data_Analysis_on_the_Relationship_between_Corporate_Governance_and_Bank_Efficiency

- Akomeah, J., Agumeh, R., & Siaw, F. (2020). Credit risk management and financial performance of listed banks in Ghana. Research Journal of Finance and Accounting, 11(6), 39–48. https://doi.org/10.7176/RJFA/11-6-05

- Al-Baidhani, A. M. (2014). The effects of corporate governance on bank performance: Evidence from the Arabian Peninsula. Evidence from the Arabian Peninsula. Putra Business School: Nurturing Human Leaders, 1–30. https://ssrn.com/abstract=2284814orhttp://doi.org/10.2139/ssrn.2284814

- Al Zaidanin, J. S. (2020). A study on financial performance of the Jordanian commercial banks using the CAMEL model and panel data approach. International Journal of Finance & Banking Studies, 9(4), 111–130. https://doi.org/10.20525/ijfbs.v9i4.978

- Anginer, D., Demirguc-Kunt, A., Huizinga, H., & Ma, K. (2016). Corporate governance and bank capitalization strategies. Journal of Financial Intermediation, 26, 1–27. https://doi.org/10.1016/j.jfi.2015.12.002

- Anginer, D., Demirguc-Kunt, A., Huizinga, H., & Ma, K. (2018). Corporate governance of banks and financial stability. Journal of Financial Economics, 130(2), 327–348. https://doi.org/10.1016/j.jfineco.2018.06.011

- Awan, A. W., & Jamali, J. A. (2016). Impact of corporate governance on financial performance: Karachi stock exchange, Pakistan. Business and Economic Research, 6(2), 401. https://doi.org/10.5296/ber.v6i2.9772

- Awrey, D. (2013). Toward a supply-side theory of financial innovation. Journal of Comparative Economics, 41(2), 401–419. https://doi.org/10.1016/j.jce.2013.03.011

- Balagobei, S. (2019). Corporate governance and non - performing loans: Evidence from listed banks in Sri Lanka. International Journal of Accounting and Business Finance, 5(1), 72–85. http://doi.org/10.4038/ijabf.v5i1.40

- Balagobei, S., & Velnampy, T. (2017). A study on ownership structure and financial performance of listed beverage food and tobacco companies in Sri Lanka. International Journal of Accounting and Financial Reporting, 7(2), 36–47. https://doi.org/10.5296/ijafr.v7i2.11518

- Beltratti, A., & Stulz, R. (2012). The credit crisis around the globe: Why did some banks perform better? Journal of Financial Economics, 105(1), 1–17. https://doi.org/10.1016/j.jfineco.2011.12.005

- Berger, A., Imbierowicz, B., & Rauch, C. (2016). The roles of corporate governance in bank failures during the recent financial crisis. Journal of Money, Credit, and Banking, 48(4), 729–770. https://doi.org/10.1111/jmcb.12316

- Bussoli, C., Gigante, M., & Tritto, M. B. (2015). The impact of corporate governance on banks performance and loan quality : Evidence from Italian cooperative bank. 9th International Scientific Conference “Economic and Social Development” Istanbul, 9-10 April, 432–441. Economic and Social Development: Book of Proceedings. https://www.proquest.com/openview/6976866f04db3974712fdb6d89438495/1?pq-origsite=gscholar&cbl=2033472

- Calomiris, C., & Carlson, M. (2016). Corporate governance and risk management at unprotected banks: National banks in the 1890s. Journal of Financial Economics, 119(3), 512–532. https://doi.org/10.1016/j.jfineco.2016.01.025

- Catherine, N. (2020). Credit risk management and financial performance. Open Journal of Business and Management, 8(1), 30–38 https://www.scirp.org/journal/paperinformation.aspx?paperid=96563.

- Chen, J. (2021). Corporate governance. Definition: How It Works, Principles, and Examples, Investopedia: Business-Corporate Finance, 1-14. https://www.investopedia.com/terms/c/corporategovernance.asp

- Coles, J. W., McWilliams, V. B., & Sen, N. (2001). An examination of the relationship of governance mechanisms to performance. Journal of Management, 27(1), 23–50. https://doi.org/10.1177/014920630102700102

- Dao, H. T., & Kang, T. (2022). Non-performing loans and the lending channel of shock transmission across countries. Cogent Business & Management, 9(1), 1–23. https://doi.org/10.1080/23311975.2022.2046239

- Darwanto, & Chariri, A. (2019). Corporate governance and financial performance in Islamic banks: The role of the sharia supervisory board in multiple-layer management. Banks and Bank Systems, 14(4), 183–191. https://doi.org/10.21511/bbs.14(4).2019.17

- Dechow, P. M., Sloan, R. G., & Sweeney, A. P. (1996). Causes and Consequences of Earnings Manipulation: An Analysis of Firms Subject to Enforcement Actions by the SEC. Contemporary Accounting Research, 13(1), 1–36. https://doi.org/10.1111/j.1911-3846.1996.tb00489.x

- DeYoung, R., Peng, E., & Yan, M. (2013). Executive compensation and business policy choices at US commercial banks. Journal of Financial and Quantitative Analysis, 48(1), 165–196. https://doi.org/10.1017/S0022109012000646

- Ekinci, R., & Poyraz, G. (2019). The effect of credit risk on financial performance of deposit banks in Turkey. Procedia Computer Science, 158, 979–987. https://doi.org/10.1016/j.procs.2019.09.139

- Ellul, A., & Yerramilli, V. (2013). Stronger risk controls, lower risk: Evidence from US bank holding companies. Journal of Finance, 68(5), 1757–1803. https://doi.org/10.1111/jofi.12057

- Elvin, P., Intan, N., Bt, N., & Hamid, A. (2016). Ownership structure, corporate governance and firm performance. International Journal of Economics and Financial Issues, 6(S3), 5–6. http://www.econjournals.com

- Erkens, D., Hung, M., & Matos, P. (2012). Corporate governance in the 2007–2008 financial crisis: Evidence from financial institutions worldwide. Journal of Corporate Finance, 18(2), 389–411. https://doi.org/10.1016/j.jcorpfin.2012.01.005

- European Central Bank (ECB). (2017). Guidance to banks on non-performing loans. https://www.bankingsupervision.europa.eu/ecb/pub/pdf/guidance_on_npl.en.pdf

- Fahlenbrach, R., & Stulz, R. (2011). Bank CEO incentives and the credit crisis. Journal of Financial Economics, 99(1), 11–26. https://doi.org/10.1016/j.jfineco.2010.08.010

- Fama, E. F., & Jensen, M. C. (1983). Separation of ownership and control.The. Journal of Law & Economics, 26(2), 301–325. https://doi.org/10.1086/467037

- Finkelstein, S. and D’aveni, R.A. (1994) CEO Duality as a Double-Edged Sword: How Boards of Directors Balance Entrenchment Avoidance and Unity of Command. Academy of Management Journal, 37(5), 1079–1108. http://dx.doi.org/10.2307/256667

- Grove, H., Patelli, L., Victoravich, L. M., & Xu, P. T. (2011). Corporate governance and performance in the wake of the financial crisis: Evidence from us commercial banks. Corporate Governance: An International Review, 19(5), 418–436. https://doi.org/10.1111/j.1467-8683.2011.00882

- Hair, J. J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2017). A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM) (Second ed.). SAGE. https://www.oecd.org/corporate/principles-corporate-governance/

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the Firm : Managerial behavior, agency costs, and capital structure. Journal of Finance Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Johnson, D. S., & Peterson, M. (2014). Consumer financial anxiety US regional financial service firms’ trust building response to the financial crisis. International Journal of Bank Marketing, 32(6), 515–533. https://doi.org/10.1108/IJBM-08-2013-0080

- Layola, M. A., & Sophia, S. M. A. (2016). Effect of corporate governance on loan loss provision in Indian Public Bank. Amity Journal of Governance Governance, 1(1), 1–15. https://amity.edu/UserFiles/admaa/183Paper/201.pdf

- Le, T. D. Q. (2020). The interrelationship among bank profitability, bank stability, and loan growth: Evidence from Vietnam. Cogent Business & Management, 7(1), 1–18. https://doi.org/10.1080/23311975.2020.1840488

- Le, T. D. Q. (2020). The interrelationship among bank profitability, bank stability, and loan growth: Evidence from Vietnam. Cogent Business & Management, 7(1), 1–18. https://doi.org/10.1080/23311975.2020.1840488

- Lee, T. D., Chung, W., & Taylor, R. E. (2011). A strategic response to the financial crisis: An empirical analysis of financial services advertising before and during the financial crisis. Journal of Services Marketing, 25(3), 150–164. https://doi.org/10.1108/08876041111129146

- Liem, M. C. (2016). Corporate governance in banking industry: An explanatory study. Research Journal of Finance and Accounting, 7(6), 30–48. https://core.ac.uk/download/pdf/234631303.pdf

- Li, X., Xie, H., Chen, L., Wang, J., & Deng, X. (2014). News impact on stock price return via sentiment analysis. Knowledge-Based Systems, 69, 14–23. https://doi.org/10.1016/j.knosys.2014.04.022

- Magembe, J. M., Ombuki, C., & Kiweu, M. (2017). An empirical study of corporate governance and loan performance of commercial banks in Kenya. International Journal of Economics, Commerce and Management, 11, 580–604. http://ir.mksu.ac.ke/bitstream/handle/123456780/383/jane%20magembe.pdf?sequence=1&isAllowed=y

- Mingaleva, Z., Zhumabayeva, M., & Karimbayeva, G. (2014). The reasons of non-performing loans and perspectives of economic growth. Life Science Journal, 11(5s), 157–161. https://www.researchgate.net/publication/286758400_The_reasons_of_non-performing_loans_and_perspectives_of_economic_growth

- Nenu, E., Vintilă, G., & Gherghina, Ş. (2018). The impact of capital structure on risk and firm performance: Empirical evidence for the Bucharest stock exchange listed companies. International Journal of Financial Studies, 6(2), 1–39. https://doi.org/10.3390/ijfs6020041

- Poudel, R., & Hovey, M. (2012). Corporate governance and efficiency in Nepalese commercial banks. Econometric Studies of Corporate Governance, 1–9. https://dx.doi.org/10.2139/ssrn.2163250

- Salleh, S. M., & Othman, R. (2016). Board of Director’s attributes as deterrence to corporate fraud. Procedia Economics and Finance, 35(16), 82–91. https://doi.org/10.1016/s2212-5671(16)00012-5

- Sarbanes-Oxley Act. (2002). Sarbanes-Oxley Act. Government Printing Office.

- Sheefeni, J. P. S. (2015). The impact of macroeconomic determinants on nonperforming loans in Namibia. International Review of Research in Emerging Markets and the Global Economy (IRREM), 1(4), 612–632. https://tarjomefa.com/wp-content/uploads/2017/09/7731-English-TarjomeFa.pdf

- Sivasubramaniam, S. (2020). Corporate governance and non -performing loans: Evidence from listed banks in Sri Lanka. Journal of Business Finance & Accounting, 5(1), 72–85. https://doi.org/10.4038/ijabf.v5i1.40

- Tahir, S. H., Shah, S., Arif, F., Ahmad, G., Aziz, Q., & Ullah, M. R. (2018). Does financial innovation improve performance? An analysis of process innovation used in Pakistan. Journal of Innovation Economics, 27(3), 195. https://doi.org/10.3917/jie.027.0195

- Teshome, E., Debela, K., & Sultan, M. (2018). Determinant of financial performance of commercial banks in Ethiopia: Special emphasis on private commercial banks. African Journal of Business Management, 12(1), 1–10. https://doi.org/10.5897/ajbm2017.8470

- Vetrova, T. N. (2017). Effectiveness of banking: Evaluation and Measuring. Social-Economic Phenomena and Process, 12(2), 30–35. https://doi.org/10.20310/1819-8813-2017-12-2-30-35

- Zaidanin, A., Salem, J., Zaidanin, A., & Jamil, O. (2021). The impact of credit risk management on the financial performance of United Arab Emirates commercial banks. International Journal of Research in Business and Social Science, 10 (3), 303–319. (2147- 4478) https://doi.org/10.20525/ijrbs.v10i3.1102