?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Studies on involuntary pension participation in general and among farmers, in particular, are scanty. Therefore, this paper aims at investigating cocoa farmers’ awareness of pension schemes as well as assessing their willingness to participate in a cocoa pension scheme. A sample of 450 cocoa farmers were interviewed using a structured questionnaire. The discrete choice experiment (DCE) comprising conditional logit (CL) and random parameter logit (RPL) models were used to analyse farmers’ willingness to pay for pension schemes. From the study, only 43 percent of farmers were aware of the cocoa pension scheme. The results of DCE analysis revealed that farmers’ decision and willingness to pay for pension scheme were influenced by the scheme attributes such as premium, payment period, payment method and pension pay. For pension institutions, the revelation that farmers are less likely to participate in a pension scheme that takes longer years to realise the benefits should be crucial in developing schemes for cocoa farmers. Therefore, it is suggested that actuarial calculations should relax the cap for being declared due for pension and reduce the premium payment period for pension benefits.

1. Introduction

The majority of working Ghanaians are into agriculture and related activities (Ghana Statistical Service [GSS], 2019). As such, the sector is ascribed as fundamental towards Gross Domestic Product (GDP) contribution in the country. Again, agriculture can help achieve Sustainable Development Goals One and Two, thus, eradicating poverty and hunger in Ghana. For instance, in 2019, the agricultural sector contributed 19% to the country’s GDP and employed more than half of Ghanaians (Service, Citation2019). It should be emphasised that cocoa production continues to cushion agriculture’s contribution to economic growth in Ghana. Globally, Ghana is ranked as the second-largest cocoa producer, tailing only Côte d’Ivoire (Bakang et al., Citation2021). In 2019, cocoa production contributed 1.4% to agriculture’s share of GDP (Service, Citation2019a). It is further underscored that cocoa is the largest export earner of the country (Avane et al., Citation2021). In terms of income, cocoa production is estimated to contribute 60–90% of producers’ household revenue (World Cocoa Foundation, Citation2014).

Despite the aforementioned fortunes of the cocoa subsector, it is acknowledged that production is mainly undertaken by aged smallholder farmers with an average age of 50 years (Ali et al., Citation2018; Akrofi-Atitianti et al., Citation2018; Kos and Lensink, 2017; Lowe, Citation2017). This situation—coupled with old plantations, low-yielding varieties, climate change, amongst others—threatens the projected potential of the cocoa sector (Onyeiwu et al., Citation2011). In most cases, these aged farmers do not continuously invest in their cocoa farms, and they usually employ farmhands to practise sharecropping (Bymolt et al., Citation2018). Simultaneously, these aged farmers are likely to be in poverty or poor (Agyeman-Boaten & Fumey, Citation2021; Wongnaa et al., Citation2021). Age, in correlation with poverty among farmers, even goes beyond cocoa, and the same is acknowledged in other jurisdictions (see, Garza-Rodríguez, Citation2016; Sekhampu, Citation2013; Tuyen, Citation2015).

The Organisation (Citation2017) revealed that poverty incidence among the aged in sub-Saharan Africa could be attributed to lack of pension benefits. Likewise, United Nations Development Programme (Citation2012) espoused that the pension system can eradicate income insecurity among individuals when they retire—a possible strategy to support aged cocoa farmers and reduce poverty. As such, several studies have probed pension schemes for farmers across the globe, in Africa (Miti et al., Citation2021; Ning et al., Citation2016; Walczak & Pieńkowska-Kamieniecka, Citation2015) and particularly in Ghana (Asare, Citation2019; Kos and Lensink, 2017; Mensah, Citation2016; Adzawla et al., Citation2015; Yeboah, Citation2015; Afenyadu, Citation2014). A section of these studies investigated farmers’ willingness to enrol into pension systems and their habits towards pension contribution (Kos and Lensink, 2017; Mensah, Citation2016) with none on the use of DCE in analysing the willingness to partake in cocoa pension schemes.

Meanwhile, the Government of Ghana (GoG) launched a pension scheme for cocoa farmers. The scheme is expected to enrol over a 1.5million cocoa farmers and also foresee the provision of retirement payments for beneficiaries(Cocoa Health and Extension Division, Citation2020). Thus, despite the GoG’s effort to roll out a pension scheme for cocoa farmers, there is scanty literary evidence to support the decision. Additionally, among all the pension studies on informal sector only Kos and Lensink (2017) studied the cocoa subsector. As such, findings from the previous works might be very generic when used for decision-making. Moreover, currently, there is not enough evidence in the literature on the potential factors that will stimulate participation in a cocoa pension scheme or the modalities of the pension scheme preferred. Also, most pension studies among farmers on the reasons for participation in pension schemes relied on qualitative case studies (Miti et al., Citation2021), subject literature and secondary research analysis (Walczak & Pieńkowska-Kamieniecka, Citation2015), qualitative and descriptive statistics (Yeboah, Citation2015), and dichotomy choice questions (Mensah, Citation2016). However, the present study used the Discrete Choice Experiment (DCE) method to improve the robustness of the results. Further, though, the pioneer study on contribution towards a cocoa pension in Ghana was done by Kos and Lensink (2017) using Randomised Control Trial (RCT). Nevertheless, the study considered only fixed (pension) or flexible (part of the money can be withdrawn to take care of emergency financial situation) savings as a precursor for contribution without considering the payment period, premium, payment method and maturity, as done in this study. Additionally, in this study, the authors used DCE which, to the best of their knowledge, had not been used by any study on pension in the subsector. Hence, the following questions remain largely unanswered (i) what is cocoa farmers’ level of awareness of the cocoa pension scheme? (ii) what attributes of the pension scheme will the cocoa farmers prefer? (iii) are farmers’ decisions to join contingent on the pension scheme attributes? Given these, the present study seeks to analyse farmers’ awareness of the cocoa pension scheme and to use the DCE to assess cocoa farmers’ willingness to join cocoa pension schemes.

2. Literature review

2.1. Determinants of participation in pension schemes among informal workers and farmers

Synthesised literature suggests that various factors influence an individual’s decision to partake in a pension scheme or otherwise. These factors span from the individual’s socioeconomic characteristics, institutional factors and pension product characteristics (Mensah, Citation2016). For instance, Collins-Sowa (Citation2013) investigated the drivers of pension contribution among informal workers and found that age, education, marital status, household size, pension type and multiple streams of income significantly influence respondents’ willingness to pay for a pension scheme. The study further explained that farm location and possession of assets negatively influence payment for a pension scheme. Again, FBO membership, payment mode, household size and knowledge of the pension system significantly drive farmers’ willingness to participate in the micro-pension scheme (Collins-Sowa, Citation2013). Consistently, a study by Adzawla et al. (Citation2015) further affirmed that age, education, marital status (single), income and household size significantly and positively determine informal sector workers’ willingness to contribute to pension schemes. The authors expatiated that aged, educated, single and, workers with larger family sizes have a higher tendency to partake in pension schemes.

Moreover, a study by Castel (Citation2008) found that pension packages, saving capacity, access to credit, education, and knowledge about the pension system significantly and positively determine workers’ willingness to contribute towards pension. Furthermore, it was observed that gender, number of children, education and income were statistically significant in determining farmers’ readiness to contribute towards pension scheme (Zhang, Citation2015). Relatively, individuals with higher income and access to credit have enough disposable income to save a portion for future uncertainties. Likewise, Karamcheva and Sanzenbacher (Citation2014) elaborated that married and educated workers are more likely to participate in pension schemes whilst younger workers and women are unlikely to participate in the same. Probably, educated workers are well informed and knowledgeable about the benefits of pension packages, thereby influencing their decision to partake in the scheme.

A similar study by Withanage et al. (Citation2000) in Sri Lanka indicated that farmers who are older, single with full-time employment, members of an insurance scheme and who have higher farm sizes are more willing to partake in pension schemes. The authors further underscore that married individuals’ unwillingness to partake in insurance schemes could be attributed to their higher household income expenditure, leaving a token or no revenue to contribute towards pension. Recently, Miti et al. (Citation2021) looked into factors influencing informal sector workers to pay for insurance and pension schemes in developing countries. Their study concluded that income, trust, family size, age, education and the residential area are statistically significant in explaining workers’ willingness to pay for pension and insurance schemes. The authors further specified that low and flexible contribution rates, benefits packages, government subsidies and quality of the schemes influenced participation and payment for pension schemes.

A more specific study on pension savings by Ghanaian cocoa farmers highlighted that education and old age are positively correlated to contribution toward pension schemes (Kos and Lensink, 2017). Thus, educated and aged cocoa farmers are more likely to save for their retirement. The study further probed the determinants of farmers’ choice of flexible pension savings and underlined that younger, female and non-remittance receiving cocoa farmers prefer flexible pension saving modality.

Given these, the following two hypotheses have been developed for the study;

Hypothesis 1: Pension attributes influence the willingness of farmers to participate in cocoa pension schemes.

2.2. Informal voluntary pension scheme in Ghana and cocoa pension

A pension scheme is a financial arrangement for the old-aged to enjoy some benefits after retirement (Boyetey et al., Citation2021; Summers et al., Citation2005). It is, therefore, recognised as an investment approach to enjoying future benefits till death. Thus, the pension scheme is regarded as a social protection tool against the risk of post-retirement poverty. Globally, the pension system in the formal sector is well organised, relative to the informal sector where there are challenges to its implementation. It is said that the informal sector workers are generally poor, and lack access to a resource pool and adequate knowledge and information about pension systems (Mensah, Citation2016). Also, universally, the majority of workers are in the informal economy, most especially in low and middle-income countries (Organisation, Citation2017; Patankar & Patwardhan, Citation2016). Yet, just like mainstream financial exclusion, voluntary pension schemes have been limited to a few workers (Guven, Citation2019; Park et al., Citation2019; Sharma, Citation2016). Thus, pension coverage in the informal sector has been steadily slow over the years despite its 30%-40% contribution to Ghana’s economic growth (Adzawla et al., Citation2015; International Monetary Fund, Citation2017). The GoG, in 1965, passed Act 27 which requires all workers (both formal and informal sector workers) to join a contributory pension scheme.

The National Pension Act 766 was passed in 2008 to ensure that every working Ghanaian enjoy pension benefit after retirement. The contribution is mandatory for both private and public sector organisations. The Act mandates contributions to be in a three-tier system. The first two tiers are compulsory for formal workers whiles the third tier is non-restrictive; meaning both formal and informal workers can take advantage of it to secure their future (Agblobi, Citation2011). All the tiers are regulated by the Government through the National Pensions Regulatory Authority (NPRA) and managed by private entities. A key difference between formal and informal voluntary pension schemes in Ghana is the absence of floors and ceilings for informal contributors. Thus, depending on the strength of the informal contributor, the person is allowed to save any amount at any time (no cap on amount and frequency of payment) Also, this regulation is optional for self-employed individuals like farmers (National Pensions Regulatory Authority, Citation2008). Thus, farmers do not need to contribute any percentage of their earnings to the national pension scheme. However, farm owners who have employees working on their farms are mandated to contribute a quota (18.5%) of their workers’ basic salary to the national pension scheme (National Pensions Regulatory Authority, Citation2008).

Nevertheless, Collins-Sowa (Citation2013) reported that Ghana’s social security policies have not lived up to expectations of providing inclusive social protection for the population, especially the labour force in the informal sector, and seem to have secluded informal workers from any form of social protection. This is because Ghana’s state-based pension scheme tends not to favour the majority of the populace as it leans towards the participation of formal workers (Asante, Citation2017).

As mentioned previously, aside from the generalised voluntary informal pension scheme in Ghana, there is currently no dedicated pension initiative for farmers. Therefore, to secure the future of farmers, the GoG has begun rolling out a farmer pension scheme programme in segments starting with cocoa farmers. It is also envisaged that the Pension Scheme for cocoa farmers in the country will enable them to make voluntary contributions towards their retirement, while COCOBOD makes a supplementary contribution on behalf of the farmers (CHED, 2020). Currently, the piloting of the project is ongoing in some selective cocoa-producing communities in the country. It is expected that the actual implementation will follow right after the piloting. To this end, the COCOBOD and the NPRA will together have to vigorously embark on an education and sensitisation programme to bring all cocoa farmers as individuals and as groupings to enrol on the scheme (CHED, 2020).

2.3. Theoretical framework

The design and conceptualisation of pension products are rooted in economic theories. Ergo, many theories have been used to explain pension schemes according to relevant literature. Some of these theories include the rational prodigality theory, permanent income and life-cycle hypothesis, retirement insurance theory, overlapping generation theory, and random utility theory. However, the scope of this study is concentrated on the need for pension uptake because cocoa farmers are ageing, hence, the need to secure their future. In lieu of this, the Overlapping Generation Theory (OLG) is regarded as relatively suitable to underpin this work. Thus, the model considers why people save presently for future benefits. However, an underlying principle of the theory is the factor of age and demographic factors which influence savings.

The theory is acknowledged as a classical economic growth theory to explain the habit of savings and to analyse pension schemes (Miyazaki, Citation2013). A glut of studies has similarly used the theory in population dynamic change and its influence on social security, savings and pension schemes (Cipriani & Fioroni, Citation2021; Cremers, Citation2005; Hualei et al., Citation2018; Miles, Citation1999; Tosun, Citation2003; Wolf & Caridad Yocerin, Citation2021). Theoretical as well as applied OLG models have since proved particularly widespread in analysing the long-term economic consequences of the gradual ageing of nations, a demographic process characterised by the increasing population share of the elderly. As the world population continues to increase with a corresponding increase in aged people, modelling of demographics within the OLG framework became increasingly realistic.

In relation, the population of aged cocoa farmers in Ghana is projected to increase, making it very prudent to model this expected change within the OLG framework. In application, the model assumes a cocoa farmer’s life in two phases. The first phase considers a younger and economically active farmer while the second phase involves an aged and economically inactive farmer (Mensah, Citation2016). During phase one, the farmer is expected to work and earn income for consumption and savings. But in the second phase, the farmer becomes inactive and anticipates depending on the accumulated capital during phase one for survival. In essence, the OLG model—in part—encapsulates the random utility theory in the sense that, farmers will prefer saving in anticipation of better future benefits. This model suggests that farmers are faced with a utility function (Fanti, Citation2014), which shows that how farmers spend their income during their youthful stage determines resources available at their disposal when they retire. In other words, farmers must spread their farm income and the return on their assets over their lifetime such that they can continue to consume even after they are too old to work.

3. Methodology

3.1. Study area and sampling

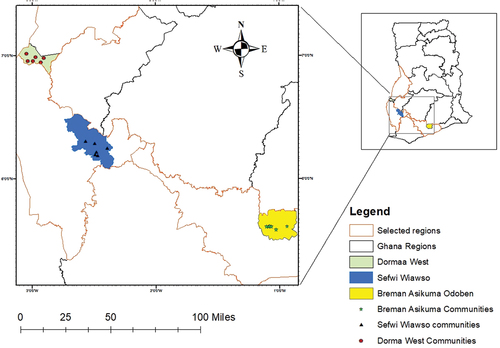

The study was conducted in Ghana’s Central, Western North and Bono Regions. The major cocoa-producing districts in these regions were selected (see, Figure for the geographical location of the study areas). For instance, about 54% of cocoa production is from the Western North Region (Bannor et al., Citation2019; Ghana Cocoa Board, Citation2018), while Central Region is known for its increasing cocoa production, particularly the study area Asikuma-Odoben-Brakwa District. One of the critical reasons supporting cocoa production in these regions is the fertile lands amidst cocoa production incentives (subsidised inputs, mass spraying, cocoa rehabilitation programme, hand pollination) provided by government and other NGOs (COCOBOD, Citation2018; Abbey et al., Citation2016). The Sefwi-Wiawso, Dormaa East and Asikuma-Odoben-Brakwa districts were purposively selected from the Western North, Bono and Central regions of Ghana, respectively. These districts were selected because of their known intense production of cocoa in Ghana. Next, six cocoa-producing communities were randomly selected. One hundred and fifty farmers (150) apiece were selected from six communities within each region. Lastly, based on the list of cocoa farmers in these communities from purchasing clerks of Licensed Cocoa Buying Companies (LBCs), 25 farmers were randomly selected from each community. Cumulatively, 450 farmers were interviewed across Ghana for this study. The study was done from May 2020 to January 2021.

Figure 1. Map of the study area.

3.2. Method of data analysis

Descriptive statistics, Conditional Logit (CL) and Random Parameter Logit (RPL) models were used in the analysis.

3.3. Choice experiment design

In this study, the mean willingness to pay (WTP) and preferences of cocoa farmers for pension were analysed using the discrete choice experiment (DCE) approach, based on farmers’ stated preferences. This technique was utilised because it is frequently used to analyse situations where market data is unreliable or non-existent (Asante‐Addo & Weible, Citation2020; Tonsor et al., Citation2009), such as the cocoa farmers’ pension scheme in Ghana. Furthermore, in literature for agriculture, marketing, health and environmental studies, the choice experiment approach has been applied extensively (Hensher, Citation2010; Holmes et al., Citation2017; Martey et al., Citation2021). Additionally, respective authors have employed the DCE in empirical studies. For example, Ruto and Garrod (Citation2009) used DCE in determining farmers’ preferences for agri-environment schemes. Sarfo et al. (Citation2021) examined farmers’ willingness to pay for digital and conventional credit using the discrete choice experiment. Asante‐Addo and Weible (Citation2020) adopted the choice experiment approach to assess consumers’ willingness to pay (WTP) and preferences for domestic or imported chicken meat attributes. Applying the discrete choice experiment, Martey et al. (Citation2021) investigated average willingness to pay and farmers’ preferences for attributes of cowpea varieties. The willingness to pay for retirement benefits among teachers was analysed using a stated preferences experiment from national data (Fuchsman et al., Citation2020). Ragasa et al. (Citation2020) investigated competition among local and imported products using this method.

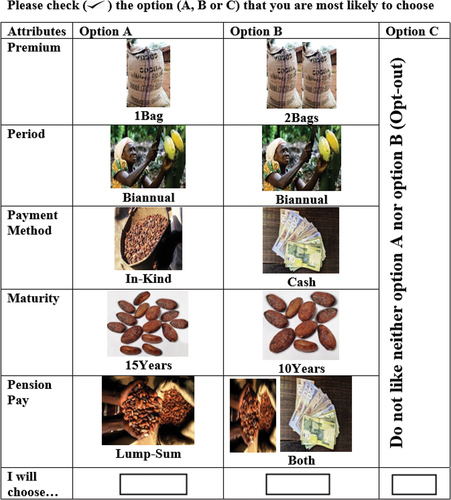

In choice experiments, researchers stimulate and present hypothetical scenarios of marketing and production settings to individuals. Basically, two or three alternatives consisting of several attributes having different levels make up each scenario. Through multiple decision making, respondents select their preferred alternative from the choice set presented. This study presented cocoa farmers pension attributes with their respective levels in an experimental design obtained from expert consultations and literature review. The attributes included premium, period, payment method, maturity and pension pay. Table gives a summary of the attributes with their respective levels applied in the choice experiment. It is important to note that the few attributes in the choice set ensure that the farmer makes the actual decision, thereby eliminating attribute non-attendance (ANA), where one or more attributes are disregarded (Hensher & Greene, Citation2010).

Table 1. Attributes and level for cocoa pension scheme

The premium attribute refers to the amount farmers contribute towards the pension scheme, equivalent to the cost of a bag of cocoa as US$119.78 (GH¢660). Also, the period attribute is the timeframe for a farmer to contribute a premium for a pension until reaching maturity. The mode of payment farmers use in making their contributions towards a pension scheme is attributed to the payment method. Similarly, the maturity attribute explains the payment duration qualifying a farmer to start enjoying benefits, which is represented by annual and biannual. However, the minimum contribution for maturity in the public sector is 15 years. Likewise, the pension pay attribute describes how farmers can receive pension benefits after maturity. Pension benefits received in the public sector are regular monthly payments and lump-sum payments.

From , the explained levels and attributes are presented. The OPTEX procedure in SAS was employed to determine the optimal experimental design for this study. In effect, the possible combination of attributes and levels from two attributes differing across three levels, and three attributes differing across two levels were determined as 72; that is, 32*23. As a result, two blocks comprising eight choice sets were established using the D-optimal design with an adjusted Federov search algorithm having a complete factorial design. Consequently, three categories of choice set scenarios were attained for each block, including the opt-out (none of these) option. Each cocoa farmer was assigned randomly to a block comprising three independent choice sets. An example of a choice set presented to cocoa farmers is shown in below.

Figure 2. A sample of choice set presented to respondents.

3.4. Econometric modelling

In understanding studies related to choices, researchers used the random utility theory (McFadden, 1973) as the theoretical context for this study. Following the utility framework, the most derived utility among several alternatives is chosen by an individual. Supposing a cocoa farmer is to select a pension package among several schemes to secure his old age in the future, and considering his budget constraints, he will choose the one from which he expects to attain maximum utility. In line with the random utility theory, it is stated as follows, assuming a poultry farmer p selects pension option f:

where denotes the vector for pension attributes associated with alternatives (premium, period, payment method, maturity and pension pay)

signifies the vector interacting with farmer characteristics and choice variables, whiles

is the random error term. The models employed in this study for cocoa farmer’s preferences for pension attributes were the conditional logit (CL) and random parameter logit (RPL). Subsequently, the RPL model was preferred to the CL model since the CL model is associated with the assumption of independence of irrelevant alternatives (IIA); preference homogeneity and independent error over time (Asante‐Addo & Weible, Citation2020; Benson et al., Citation2016; Martey et al., Citation2021; Train, Citation2009). The RPL model, on the contrary, permits random variation within a specified distribution sample while estimating preference heterogeneity (Martey et al., Citation2021; McFadden & Train, Citation2000). As a result, this study proposed heterogeneity among cocoa farmers; hence, they are likely to have varied preferences for pension attributes.

Following studies of Martey et al. (Citation2021) and Krah et al. (Citation2019), the utility framework permits interaction between pension attributes and key demographic characteristics. Therefore, the expected utility of a cocoa farmer p in selecting pension attributes f is specified as:

where is the vector for pension attributes that are previously defined

is the marginal utility of money (price for a bag of cocoa)

represents smallholder-specific random terms capturing the heterogeneity preference of pension attributes;

are the coefficients of each pension attribute to be estimated involving an alternative specific constant (ASC)

represents the coefficients to be estimated related to the interacting terms

and

is the independently and identically distributed error term (Train, Citation2009).

In estimating a specific attribute’s average marginal willingness to pay (WTP), we calculate the ratio of the marginal utility of income to the coefficient of the attribute (Martey et al., Citation2021). Assuming the random parameter having a normal distribution is well known, the distribution expected to fit the parameters determined could be selected in principle (Nahuelhual et al., Citation2004). However, a normal distribution was assumed since the pension attributes used in this study are not predictable, permitting positive as well as negative coefficients. The model is empirically specified as follows:

where is premium

represents period

signifies payment method;

denotes maturity period; and

means pension pay. These pension attributes are presented and described in Table .

4. Results and discussion

4.1. Personal and household characteristics of cocoa farmers

Table presents cocoa farmers’ demographic characteristics. Cocoa production is dominated by men in the study area. Cocoa production in Ghana is highly manual with little or no use of mechanisation. Men usually have the required strength and production resources like land for cocoa farming. Most women assist their husbands in cocoa cultivation. On average, a cocoa farmer was close to 50 years. Therefore, cocoa production is dominated by farmers of advanced ages. About 40% of the respondents were native cocoa farmers while the rest were either permanent (54%) or temporary (4%) migrants. This implies that migrant cocoa farmers dominate in the area. Due to differences in weather conditions and soil fertility, many people migrate from northern Ghana to the southern part to either farm or serve as farm labour. Most of these migrants end up settling permanently in the receiving communities. Close to 60% of the cocoa farmers had completed basic education (Junior High School) while a quarter had no formal education. The majority of the cocoa farmers had married and were household heads. On average, a household comprised seven members.

Table 2. Cocoa farmers’ demographic characteristics

Also, Table presents cocoa farmers’ production characteristics. The main economic activity for more than 90% of the respondents is farming. According to GSS (2019), the majority of rural households in Ghana are crop farmers of which cocoa is a major perennial/tree crop cultivated. However, few of the respondents had farming (cocoa production) as a secondary source of income. On average, a farmer had 20 years of experience in cocoa production. This implies that the farmers have amassed ample knowledge in cocoa production and understand dynamics in the industry. About 80% of the farmers received extension visits in the 2020/2021 cocoa season, and about a third belonged to Farmer Based Organisations (FBOs). This means that about two-thirds of the cocoa farmers lack benefits associated with FBOs like group loans, extension education, training services and knowledge sharing among group members. This could have adverse impacts on cocoa production.

Table 3. Cocoa farmers’ production characteristics

Land ownership for half of the cocoa farmers is inheritance (Table ). In this case, some of the farmers inherited cocoa farms while others cultivated cocoa on inherited lands. About 60% of the farmers produce cocoa through the sharecropping system. This is done by farmers who do not own farmlands. The average number of cocoa farms owned by the respondents is three, with a maximum of 10. Due to land fragmentation, many farmers have multiple farms which could be a mixture of land ownerships: inheritance, purchase and/or sharecropping. The average cocoa farm size was three and a half hectares. Cocoa production in Ghana is predominantly on small-scale basis and ranges between two and five hectares (Aneani & Padi, Citation2016). Also, productivity (yield per hectare) was 147 kg. According to Aneani and Padi (Citation2016), cocoa productivity is low in Ghana, with a mean of 234 kg per hectare. This could be due to inadequate management of cocoa farms, pest and disease infestations, low soil fertility, and climate change. Less than half of the cocoa farmers have off-farm economic activities, which contributes an average of US$755 to their income annually.

4.2. Farmers’ awareness and willingness to join cocoa pension schemes in Ghana

presents farmers’ awareness of cocoa pension schemes in Ghana, and their willingness to join. About 60% of the cocoa farmers had bank accounts for their transactions, and only 13% were members of Village Savings and Loans Associations (VSLAs). VSLA boosts farmers’ off-farm income (Bannor et al., Citation2020a), food security (Ksoll et al., Citation2016), household consumption expenditure and empowerment of women (Mwansakilwa et al., Citation2017). Saving with banks and participation in VSLA enable farmers and the rural poor to obtain loans in times of financial crises (Brannen & Sheehan-Connor, Citation2016). Thus, VSLA enables the rural poor to mitigate the volatility of farm income and improve their welfare (Cameron & Ananga, Citation2015). Furthermore, one-third of the cocoa farmers had savings towards their retirements (old age). These farmers save a portion of their income with banks, VSLAs or other financial institutions to provide them with a means of living when they are old and do not have the strength to farm.

Table 4. Farmers’ awareness and willingness to join cocoa pension schemes in Ghana

Cocoa farmers have multiple engagements to take care of themselves during their old ages: investment in children (89%), investment in farms (61%), savings with a bank (31%), investment in an off-farm business (17%), life insurance (9%), and pension contribution (6%). Cocoa farmers invest in their children by providing them with quality education, apprenticeship and other means of securing a better future for them. Farmers invest in farms by cultivating perennial/tree crops like cocoa, oil palm, coconut, citrus (orange) and cashew to provide them with a lasting source of income. Others train their children to take over management of their farms at old ages. Savings with a bank, life insurance and pension contribution enable cocoa farmers to withdraw from the contributions when old and cannot work. However, few of the cocoa farmers are into these.

Half of the cocoa farmers were aware of the general pension scheme for formal sector workers in Ghana (Table ). Awareness of the cocoa pension scheme was generally low in the study area (43%). Cocoa farmers become aware of pension schemes through the media (radio and television), insurance companies, Ghana Cocoa Board (COCOBOD), Licensed Buying Companies, non-governmental organisations (NGOs) and colleague farmers, with radio (63%) forming the majority. Almost all the farmers were willing to join pension schemes from the formal sector or cocoa pension scheme. This implies that cocoa farmers have anticipated the adverse effects of not saving ample money towards their old age. Cocoa farmers would want to join pension schemes by the Social Security and National Insurance Trust (SSNIT), insurance companies, farmer organisations or Licensed Buying Companies. SSNIT is a Government of Ghana agency in charge of the administration of national pension schemes, making it a popular and trusted pension company in Ghana. Though not in existence, some cocoa farmers would want farmer organisations and Licensed Buying Companies to manage pension schemes for cocoa farmers in Ghana.

4.3. Results from the choice experiment

The findings obtained from conditional logit (CL) as well as random parameter logit (RPL) are shown in Table . To generate stable results, the 1000 Halton draws was used to estimate the simulations of the RPL model. The results for the conditional logit model are shown in Model 1. The results for RPL models are presented from Model 2 to Model 5. Models 2 and 3 estimates are from the RPL model without non-random parameters. However, in Model 2, the estimates do not correlate with attributes, whereas in Model 3, the estimates correlate with attributes. Again, models 4 and 5 are RPL estimates having non-random parameters; even though Model 4 does not consider the correlation between attributes, Model 5 reports for the correlation among attributes.

Table 5. Estimates of CL and RPL models for choice of cocoa pension

From the results, CL and RPL display consistent signs for the coefficients of all the attributes in the respective models and are statistically significant, suggesting that the choice of attributes is suitable for this study. Meanwhile, variations in the average values exist since the mean estimates for the CL model are lower than those of the RPL models (Revelt & Train, Citation1998). This result suggests possible underestimation effects in the CL model (Martey et al., Citation2021). Also, the results of the standard deviations for the RPL were significant. This supports the preference for heterogeneity hypothesis of variation among the preferences for pension attributes among cocoa farmers. Under conditions where heterogeneity in the attributes of pension preferences were not accounted for, possible invalid assumptions about cocoa farmers’ preferences for pension attributes can occur.

The log-likelihood and Akaike Information Criterion (AIC) estimates for the RPL models reveal that they were relatively low in Model 5, thus, they fit best for the data. Therefore, we focus our discussion on Model 5. Regarding Model 5, cocoa farmers consider premium (i.e. one bag vs two bags), period (i.e. annual vs biannual), payment method (i.e. cash vs in-kind) and pension pay (i.e. regular vs lump-sum vs both) as important attributes in selecting pension packages. It is worth noting that, the maturity (i.e. 1–5 vs 6–10 vs 11–15) attribute was not statistically significant. This concurs with the finding of Kitamura and Nakashima (Citation2021) who found that people, especially males, have an insignificant preference for long-term pension schemes (deferred annuities). They highlighted that long-term pension schemes are regarded as a gamble, making such schemes unattractive to a segment of contributors. The results for the payment method are contrary to findings, suggesting that respondents will delay claiming benefits if lump-sum were offered to them as incentives (Maurer & Mitchell, Citation2021). Meanwhile, the findings for the payment period are consistent with a study that suggests that contribution periods are very important in pension schemes (Bonnet et al., Citation2019). Relatively, the coefficient on payment method is of higher magnitude compared to all the other attributes. Usually, payments towards pension schemes are in cash; however, cocoa production is seasonal, hence, farmers might not be able to make monthly contributions towards the scheme. Likewise, it is asserted that farmers prefer in-kind transactions to in-cash (Grima et al., Citation2016; Navrud & Vondolia, Citation2020). Given this, it would be appropriate for farmers to provide the price equivalent of the number of bags for premium payment during harvest, spread annually, ergo, their preference for in-kind. Also, cocoa farmers’ average willingness to pay (WTP) for a pension scheme is US$ 55.19 (GH¢ 304.11), which is lower than a bag of cocoa. One plausible reason could be that cocoa farmers are predominantly smallholder farmers who get their income seasonally, and are, therefore, unlikely to pay premiums beyond the mean WTP.

The non-random parameters used in the RPL model were age, sex, experience, educational level and per capita expenditure. Among the non-random parameters, only age and per capita expenditure were significant determinants of pension participation. The per capita expenditure was positive and significant, indicating that with higher per capita expenditure farmers are likely to contribute towards a pension scheme. Farmers within this criterion are likely to have a large farm size which generates more income (R. K. Bannor et al., Citation2020b; Bannor & Oppong-Kyeremeh, Citation2018; Kos and Lensink, 2017)—therefore, they can contribute to a pension scheme to their benefit in future. In detail, the results of the per capita expenditure as a proxy for poverty revealed that, with an increase in the per capita expenditure of a farmer, the farmers are more likely to participate in the cocoa pension scheme. Similarly, Miti et al. (Citation2021) and Zhang (Citation2015) reported that informal workers’ willingness to participate in pension schemes was based on their income. The result suggests that, the cocoa pension scheme should be in tandem with other poverty alleviation programmes and policies to better the lives of cocoa farmers lest the necessary impact may not be achieved. Moreover, aged farmers are less likely to participate in a pension scheme. Inconsistently, Adzawla et al. (Citation2015) reported that age is a significant and positive predictor of willingness to participate in pension schemes. However, the results on age and per capita from this study buttresses the Overlapping Generation Theory (OLG). Thus, cocoa farmers’ pension contribution should be done from an early and youthful age to when old. This is because it is at their early ages that they can generate enough income with the knowledge and physical strength to increase farm size and increase production and productivity. The results also mean that, for a specific pension scheme for cocoa farmers to be sustainable, there is a need to have several young cocoa farmers participate as the aged are less likely to save for a pension. Thus, OLG theory seems to explain farmers’ willingness to participate in a cocoa pension scheme.

5. Conclusions and recommendations

This study investigated farmers’ awareness of cocoa pension schemes in Ghana and their willingness to pay for a pension scheme. About half of the cocoa farmers knew the formal workers’ general pension scheme. However, only about 43% of farmers were aware of the cocoa pension scheme yet to be scaled up, suggesting a low level of awareness in the study area. Almost all (97%) farmers were willing to join pension schemes from the formal sector or cocoa pension scheme. Specifically, cocoa farmers preferred joining pension schemes of the Social Security and National Insurance Trust (SSNIT) and insurance companies. Also, the discrete choice experiment (DCE) was used to analyse cocoa farmers’ preferences and willingness to pay for pension schemes. The findings of this study revealed significant heterogeneity among cocoa farmers’ preferences for pension schemes, suggesting the importance of permitting preference heterogeneity in choice modelling. Empirically, the results demonstrated that premium, period, payment method and pension pay were significant attributes considered by cocoa farmers in choosing a pension scheme. Also, socioeconomic characteristics such as per capita expenditure positively influence willingness to participate in the cocoa pension scheme whereas influence negatively. Notably, cocoa farmers showed high preferences for a pension scheme with an equivalent cost of one cocoa bag as premium, annual payment, in-kind payment method, and regular and lump-sum payment methods. These attributes are crucial for developing any pension scheme for cocoa farmers. However, the maturity period attribute did not significantly influence farmers’ choice for the pension scheme, indicating that farmers are indifferent to the years of maturity of the premium paid for pension schemes in the choice experiment. Comparing the attributes for pension, the payment method had the highest effect over premium, period and pension pay whereas pension pay had the lowest effect over the other attributes. On average, cocoa farmers were willing to pay (WTP) US$ 55.19 (GH¢ 304.11) as a premium for pension schemes.

Also, per capita expenditure as a non-random parameter was significant. This finding signifies that most cocoa farmers are poor and willing to make small contributions towards a pension scheme to secure their future in old age. This and the age factor result bolster the application of the Overlapping Generation Theory (OLG) in developing the cocoa pension scheme.

6. Implication for policy

The finding that most farmers are not aware of the cocoa pension scheme suggests that the Government of Ghana, through the Ghana COCOBOD, should educate and sensitise cocoa farmers on the new pension scheme to enable them to make informed decisions towards securing their old age. Although most cocoa farmers are ageing, they are willing to join the pension scheme; therefore, policymakers should find seed money to top up for fewer farmers who meet the allowable pension age to qualify for the same. Also, the Government should lobby pension scheme institutions to relax the age due for pension, given the average age of farmers.

7. Implication for practice

For pension institutions, the revelation that farmers are less likely to participate in a pension scheme that takes longer years to realise the benefits should be crucial in developing schemes for cocoa farmers. Therefore, it is suggested that actuarial calculations should relax the cap for being declared due for pension and reduce the premium payment period for pension benefits. Also, pension institutions in developing pension schemes for cocoa farmers should find possible means of attracting the contribution of the farmers (in-kind payment) during the sales of cocoa at various LBCs to ensure consistency in payment and reliable pension payment. Additionally, as evidenced in the results, unlike formal workers, farmers do not draw monthly salaries and wouldn’t be able to contribute monthly pension scheme. Therefore, actuarial calculations should consider possible ways of deducting appropriate premium (in-kind payment from cocoa beans), which can be spread for the whole year.

8. Implication for theory

Participation in cocoa pension schemes among cocoa farmers can be explained by the Overlapping Generation Theory (OLG). Therefore, pension practitioners should endeavour to have more young cocoa farmers in the pension scheme to ensure the sustainability of the scheme.

9. Implication for future research

One limitation of the study is the inability to calculate the exact benefit (amount of money) farmers are likely to have given the amount they are willing to pay. Therefore, future studies should undertake the actuarial analysis of the possible benefit both in a lump sum and monthly pension given the payment period, the premium and maturity date to add to this study. Such a study will be more revealing if the authors use non-hypothetical choice experiments, such as experimental auctions, to validate WTP estimates in this study since hypothetical bias cannot be ruled out completely.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Ghana Cocoa Board. (2018). “49th Annual Report and Financial Statements”, Ghana Cocoa Board Accra, Ghana Available at. Accra. February 6, 2022 https://cocobod.gh/resource_files/49th-annual-report-and-financial-statements-2017-2018.pdf

- Abbey, P., Tomlinson, P. R., & Branston, J. R. (2016). Perceptions of governance and social capital in Ghana’s cocoa industry. Journal of Rural Studies, 44, 153–21. http://doi.org/10.1016/j.jrurstud.2016.01.015

- Adzawla, W., Baanni, S. A., & Wontumi, R. F. (2015). Factors influencing informal sector workers’ contribution to pension scheme in the Tamale Metropolis of Ghana. Journal of Asian Business Strategy, 5(2), 37–45. https://doi.org/10.18488/journal.1006/2015.5.2/1006.2.37.45

- Afenyadu, A. (2014), Official Retirement Can Wait: A Study of Petty Traders in Ghana to Identify Barriers to Participation in ISF Pension Scheme”, Master’s Thesis, University of Guelph.

- Agblobi, A. D. (2011). Pensions: The new investment perspective for retirement planning. Mork Impressions, Accra-Ghana.

- Agyeman-Boaten, S. Y., & Fumey, A. (2021). Effects of cocoa swollen shoot virus disease (CSSVD) on the welfare of cocoa farmers in Ghana: Evidence from Chorichori community of the Sefwi Akontombra district. SN Business Economics, 1(11), 1–3. https://doi.org/10.1007/s43546-021-00152-8

- Akrofi-Atitianti, F., Ifejika Speranza, C., Bockel, L., & Asare, R. (2018). Assessing Climate smart agriculture and its determinants of practice in Ghana: a case of the cocoa production system. Land, 7(1), 30. https://doi.org/10.3390/land7010030

- Ali, E. B., Awuni, J. A., Danso-Abbeam, G., & Yildiz, F. (2018). Determinants of fertiliser adoption among smallholder cocoa farmers in the Western Region of Ghana. Cogent Food & Agriculture, 4(1), 1538589. https://doi.org/10.1080/23311932.2018.1538589

- Aneani, F., & Padi, F. 2016. Baseline farmer survey of smallholder cocoa farming systems in Ghana”, Sustainable Agriculture Research. 6(1): 13–23. https://doi.org/10.5539/sar.v6n1p13

- Asante, B. O. (2017), Perception and willingness to participate in social security insurance by the informal sector: a case study of commercial drivers in the Kumasi metropolis, master’s thesis, Department of Economics, Kwame Nkrumah University of Science and Technology. http://ir.knust.edu.gh/bitstream/123%20456789/10247/1/Bmy%2520project%2520work%2520msc2FINAL-SAT-23-10-2016.pdf

- Asante‐Addo, C., & Weible, D. (2020). Is there hope for domestically produced poultry meat? A choice experiment of consumers in Ghana. Agribusiness, 36(2), 281–298. https://doi.org/10.1002/agr.21626

- Asare, F. (2019), Consumer Behaviour towards Pension Scheme Acquisition in the Informal Sector in Ghana, Master’s Thesis, University of Ghana. http://ugspace.ug.edu.gh/handle/123456789/33379, accessed January 2, 2022.

- Avane, A., Amfo, B., Aidoo, R., & Mensah, J. O. (2021). Adoption of organic fertilizer for cocoa production in Ghana: Perceptions and determinants. African Journal of Science, Technology, Innovation and Development, 1–12. https://doi.org/10.1080/20421338.2021.1892254

- Bakang, J. E., Frimpong, A. A., Etuah, S., Tham-Agyekum, E. K., Sowah, I. N., Doodo, E. A., … Iddrisu, M. (2021). Competitive strategies for purchasing of cocoa by licensed buying companies in Ghana: The determinants and performance implications. Journal of Development and Agricultural Economics, 13(4), 295–303. https://doi.org/10.5897/JDAE2021.1303

- Bannor, R. K., Kumar, G. A. K., Oppong-Kyeremeh, H., & Wongnaa, C. A. (2020b). Adoption and impact of modern rice varieties on poverty in Eastern India. Rice Science, 27(1), 56–66. https://doi.org/10.1016/j.rsci.2019.12.006

- Bannor, R. K., & Oppong-Kyeremeh, H. (2018). Extent of poverty and inequality among households in the Techiman municipality of Brong Ahafo region. Ghana. Journal of Energy and Natural Resource Management, 1(1), 26–36. https://jenrm.uenr.edu.gh/index.php/uenrjournal/article/view/122/72

- Bannor, R. K., Oppong-Kyeremeh, H., Atewene, S., & Wongnaa, C. A. (2019). Influence of non-price incentives on the choice of cocoa licensed buying companies by farmers in the Western North of Ghana. Journal of Agribusiness in Developing and Emerging Economies, 9(4), 402–418. https://doi.org/10.1108/JADEE-11-2018-0151

- Bannor, R. K., Oppong-Kyeremeh, H., Derkyi, M., Adombila, A. Y., & Amrago, E. C. (2020a). Village savings and loans association participation and impact on off-farm income among rural women. Journal of Enterprising Communities: People and Places in the Global Economy, 14(4), 539–562. https://doi.org/10.1108/JEC-04-2020-0058

- Benson, A. R., Kumar, R., & Tomkins, A. (2016), On the relevance of irrelevant alternatives, Proceedings of the 25th International Conference on World Wide Web. Montreal.

- Bonnet, C., Meurs, D., & Rapoport, B. (2019). Gender pension gaps along the distribution: An application to the French case. Journal of Pension Economics & Finance, 21(1), 1–23. https://doi.org/10.1017/S1474747220000177

- Boyetey, D. B., Boampong, O., & Enu-Kwesi, F. (2021). Effect of institutional mechanisms on micropension saving among informal economy workers in the Greater Accra Region of Ghana. Heliyon, 7(9), e08004. https://doi.org/10.1016/j.heliyon.2021.e08004

- Brannen, C., & Sheehan-Connor, D. (2016). Evaluation of the impact of village savings and loan associations using a novel survey instrument. Development Southern Africa, 33(4), 502–517. https://doi.org/10.1080/0376835X.2016.1179097

- Bymolt, R., Laven, A., & Tyzler, M. (2018). Demystifying the cocoa sector in Ghana and Côte d’Ivoire. In The Royal Tropical Institute.

- Cameron, S., & Ananga, E. D. (2015). Savings groups, livelihoods and education: Two case studies in Ghana. Journal of International Development, 27(7), 1027–1041. https://doi.org/10.1002/jid.3067

- Castel, P. (2008). Voluntary Defined Benefit Pension System Willingness to Participate: The Case of Vietnam.

- Chang, H. H., Wang, J. H., & Mishra, A. K. (2015). Do farmers’ old age pension programs affect farm production? Empirical evidence of dairy farms in Taiwan. Agricultural Economics, 61(11), 533–541. https://doi.org/10.17221/244/2014-AGRICECON

- Cipriani, G. P., & Fioroni, T. (2021). Social security and endogenous demographic change: Child support and retirement policies. Journal of Pension Economics & Finance, 1–19. https://doi.org/10.1017/S1474747220000402

- Cocoa Health and Extension Division. (2020). “Launch of cocoa farmer’s pension scheme.” Ghana Cocoa Board. Available at https://www.ched.com.gh/applications/newwebsite/farmers_pension.html, accessed February 4

- Collins-Sowa, P. A. (2013). Willingness to participate in micro pension schemes: Evidence from the informal sector in Ghana. Journal of Economics and International Finance, 15(1), 21–34. https://doi.org/10.5897/JEIF12.097

- Cremers, E. T. (2005). Intergenerational welfare and trade. Macroeconomic Dynamics, 9(5), 585–611. https://doi.org/10.1017/S136510050504037X

- Fanti, L. (2014). Raising the mandatory retirement age and its effect on long-run income and pay-as-you-go (PAYG) pension. Metroeconomica, 65(4), 619–645. https://doi.org/10.1111/meca.12055

- Fuchsman, D., McGee, J. B., & Zamarro, G. (2020), Teachers’ Willingness to Pay for Retirement Benefits: A National Stated Preferences Experiment, Sinquefield Center for Applied Economic Research Working Paper, (20-03).

- Garza-Rodríguez, J. (2016). The determinants of poverty in the Mexican states of the US-Mexico border. Estudios fronterizos, 17(33), 141–167. https://doi.org/10.21670/ref.2016.33.a06

- Ghana Statistical Service. (2019). ”Rebased 2013-2019 Annual Gross Domestic Product”, Ghana Statistical Services, Accra-Ghana. available at https://statsghana.gov.gh/gssmain/fileUpload/National%20Accounts/Annual_2013_2019_GDP.pdf. accessed on February 8

- Grima, N., Singh, S. J., Smetschka, B., & Ringhofer, L. (2016). Payment for Ecosystem Services (PES) in Latin America: Analysing the performance of 40 case studies. Ecosystem Services, 17, 24–32. https://doi.org/10.1016/j.ecoser.2015.11.010

- Guven, M. U.(2019), “Extending Pension Coverage to the Informal Sector in Africa (English)', Social Protection and Jobs Discussion Paper, No. 1933. Washington, DC: World Bank Group. http://documents.worldbank.org/curated/en/153021563855893271/Extending-Pension-Coverage-to-the-Informal-Sector-in-Africa

- Hensher, D. A. (2010). Hypothetical bias, choice experiments and willingness to pay. Transportation Research Part B: Methodological, 44(6), 735–752. https://doi.org/10.1016/j.trb.2009.12.012

- Hensher, D. A., & Greene, W. (2010). Non-attendance and dual processing of CommonMetric attributes in choice analysis: A latent class specification. Empirical Economics, 39(2), 413–426. https://doi.org/10.1007/s00181-009-0310-x

- Holmes, T. P., Adamowicz, W. L., & Carlsson, F. (2017). Choice Experiments. In P. Champ, K. Boyle, & T. Brown. (Eds.), A Primer on Nonmarket Valuation”, The Economics of Non-Market Goods and Resources (pp. 133–186). Springer. https://doi.org/10.1007/978-94-007-7104-8_5

- Hualei, Y., Zheng, S., & Haoyu, H. (2018). Will Delayed Retirement Occupy Family Fertility? Journal of Finance and Economics, 44(10), 53–66. https://qks.sufe.edu.cn/J/CJYJ/Article/Details/A0cf3aa277-3c24-4c29-9bc4-34ccdae97a77

- International Monetary Fund. (2017). ”Regional Economic Outlook: Sub-Saharan Africa, Restarting the Growth Engine”, World Economic and Financial Surveys (April 17). Washington, DC: International Monetary Fund, Publication Services.

- Karamcheva, N. S., & Sanzenbacher, G. (2014). Bridging the gap in pension participation: How much can universal tax-deferred pension coverage hope to achieve? Journal of Pension Economics & Finance, 13(4), 439–459. https://doi.org/10.1017/S147474721400002X

- Kitamura, T., & Nakashima, K. (2021). Preferences for deferred annuities in the Japanese retirement market. Journal of Financial Economic Policy, 13(6), 810–830. https://doi.org/10.1108/JFEP-06-2020-0138

- Krah, K., Michelson, H., Perge, E., & Jindal, R. (2019). Constraints to adopting soil fertility management practices in Malawi: A choice experiment approach. World Development, 124, 104651. https://doi.org/10.1016/j.worlddev.2019.104651

- Ksoll, C., Lilleør, H. B., Lønborg, J. H., & Rasmussen, O. D. (2016). Impact of village savings and loan associations: Evidence from a cluster randomised trial. Journal of Development Economics, 120, 70–85. https://doi.org/10.1016/j.jdeveco.2015.12.003

- Lowe, A. (2017), Creating opportunities for young people in Ghana’s cocoa sector, Working Paper 511, Overseas Development Institute, London.

- MacKeller, L. (2009). “Pension systems for the informal sector in Asia”. World Bank.

- Martey, E., Etwire, P. M., Adogoba, D. S., & Tengey, T. K. (2021). Farmers’ preferences for climate-smart cowpea varieties: Implications for crop breeding programmes. Climate and Development, 1–16. https://doi.org/10.1080/17565529.2021.1889949

- Maurer, R., & Mitchell, O. S. (2021). Older peoples’ willingness to delay social security claiming. Journal of Pension Economics & Finance, 20(3), 410–425. https://doi.org/10.1017/S1474747219000404

- McFadden, D., & Train, K. (2000). Mixed MNL models for discrete response. Journal of Applied Econometrics, 15(5), 447–470. https://doi.org/10.1002/1099-1255(200009/10)15:5<447::AID-JAE570>3.0.CO;2-1

- Mensah, N. O. (2016), “Willingness of Poultry Agribusiness Workers To Participate in the Informal Voluntary Pension Scheme in the Kumasi Metropolis of the Ashanti Region in Ghana”, Masters Thesis, University of Ghana, Accra-Ghana.

- Miles, D. (1999). Modelling the Impact of Demographic Change upon the Economy. Economic Journal, 109(452), 1–36. https://doi.org/10.1111/1468-0297.00389

- Miti, J. J., Perkio, M., Metteri, A., & Atkins, S. (2021). Factors associated with willingness to pay for health insurance and pension scheme among informal economy workers in low- and middle-income countries: A systematic review. International Journal of Social Economics, 48(1), 17–37. https://doi.org/10.1108/IJSE-03-2020-0165

- Miti, J. J., Perkiö, M., Metteri, A., & Atkins, S. (2021). “Case study M: Extension of the contributory pension scheme to small-scale farmers in Zambia”, Handbook on Social Protection Systems. Edward Elgar Publishing. https://www.elgaronline.com/view/edcoll/9781839109102/9781839109102.00053.xml

- Miyazaki, K. (2013). Pay-as-you-go social security and endogenous fertility on neoclassicalgrowthmodel. Journal of Population Economics, 26(3), 1233–1250. https://doi.org/10.1007/s00148-012-0451-7

- Mwansakilwa, C., Tembo, G., Zulu, M. M., & Wamulume, M. (2017). Village savings and loan associations and household welfare: Evidence from Eastern and Western Zambia. African Journal of Agricultural and Resource Economics, 12(1), 85–97. http://dx.doi.org/10.22004/ag.econ.258601

- Nahuelhual, L., Loureiro, M. L., & Loomis, J. (2004). Using random parameters to account for heterogeneous preferences in contingent valuation of public open space. Journal of Agricultural and Resource Economics, 29(3), 537–552. https://www.jstor.org/stable/40987248

- National Pensions Regulatory Authority. (2008), National Pensions Act, 2008 (Act 766) https://npra.gov.gh/assets/documents/NPRA_2008_Act_766.pdf 15 September 2022.

- Navrud, S., & Vondolia, G. K. (2020). Farmers′ preferences for reductions in flood risk under monetary and non-monetary payment modes. Water Resources and Economics, 30, 100151. https://doi.org/10.1016/j.wre.2019.100151

- Ning, M., Gong, J., Zheng, X., & Zhuang, J. (2016). Does new rural pension scheme decrease elderly labor supply? Evidence from CHARLS. China Economic Review, 41, 315–330. https://doi.org/10.1016/j.chieco.2016.04.006

- Onyeiwu, S., Pallant, E., & Hanlon, M. (2011), Sustainable and Unsustainable Agriculture in Ghana and Nigeria: 1960-2009, 211–222. https://smartech.gatech.edu/bitstream/handle/1853/35263/1238272590_SO.pdf

- Organisation, I. L. (2017), “World Social Protection Report 2017-19”, Universal Social Protection to Achieve the Sustainable Development Goals.

- Park, K. G., Stańko, D., & McShane, D. (2019). Supervision of lost pension accounts and unclaimed benefits. Journal of Financial Regulation and Compliance, 27(3), 266–279. https://doi.org/10.1108/JFRC-03-2018-0045

- Patankar, A., & Patwardhan, A. (2016). Estimating the uninsured losses due to extreme weather events and implications for informal sector vulnerability: A case study of Mumbai, India. Natural Hazards, 80(1), 285–310. https://doi.org/10.1007/s11069-015-1968-3

- Ragasa, C., Andam, K. S., Asante, S. B., & Amewu, S. (2020). Can local products compete against imports in West Africa? Supply-and demand-side perspectives on chicken, rice, and tilapia in Ghana. Global Food Security, 26, 100448. https://doi.org/10.1016/j.gfs.2020.100448

- Revelt, D., & Train, K. (1998). Mixed logit with repeated choices: Households’ choices of appliance efficiency level. Review of Economics and Statistics, 80(4), 647–657. https://doi.org/10.1162/003465398557735

- Ruto, E., & Garrod, G. (2009). Investigating farmers‘ preferences for the design of agri-environment schemes: A choice experiment approach. Journal of Environmental Planning and Management, 52(5), 631–647. https://doi.org/10.1080/09640560902958172

- Sarfo, Y., Musshoff, O., Weber, R., & Danne, M. (2021). Farmers’ willingness to pay for digital and conventional credit: Insight from a discrete choice experiment in Madagascar. PloS one, 16(11), e0257909. https://doi.org/10.1371/journal.pone.0257909

- Sekhampu, T. S. (2013). Determinants of poverty in South African township. Journal of Social Sciences, 34(2), 145–153. https://doi.org/10.1080/09718923.2013.11893126

- Service, G. S. (2019a), “Rebased 2013-2019 Annual Gross Domestic Product”, Accra-Ghana. available at https://statsghana.gov.gh/gssmain/fileUpload/National%20Accounts/Annual_2013_2019_GDP.pdf. on February 8, 2019a.

- Service, G. S. (2019b). 2017/18 Ghana census of agriculture: National report. Accra, Ghana.

- Sharma, D. (2016). Nexus between financial inclusion and economic growth: Evidence from the emerging Indian economy. Journal of Financial Economic Policy, 8(1), 13–36. https://doi.org/10.1108/JFEP-01-2015-0004

- Summers, B., Ironfield-Smith, C., Duxbury, D., Hudson, R., & Keasey, K. (2005). Informed choice: Consumer preferences for information on pensions. Journal of Financial Regulation and Compliance, 13(3), 260–267. https://doi.org/10.1108/13581980510622117

- Tonsor, G. T., Olynk, N., & Wolf, C. (2009). Consumer preferences for animal welfare attributes: The case of gestation crates. Journal of Agricultural and Applied Economics, 41(3), 713–730. https://doi.org/10.1017/S1074070800003175

- Tosun, M. S. (2003). Population Aging and Economic Growth: Political Economy and Open Economy Effects. Economics Letters, 81(3), 291–296. https://doi.org/10.1016/S0165-1765(03)00195-2

- Train, K. E. (2009). Discrete choice methods with simulation. Cambridge University Press.

- Tuyen, T. Q. (2015). Socio-economic determinants of household income among ethnic minorities in the North-West Mountains, Vietnam. Croatian Economic Survey, 17(1), 139–159. https://doi.org/10.15179/ces.17.1.5

- United Nations Development Programme. (2012), 2010 Millennium Development Goal Report, UNDP, Ghana and NDPC/GOG

- Walczak, D., & Pieńkowska-Kamieniecka, S. (2015), Solidarity on the example of farmers’ pension insurance in Poland, Agrarian Perspectives XXIV, Global Agribusiness and Rural Economy. International Scientific Conference. Prague: Czech University of Life Sciences Prague, pp. 536–540.

- Withanage, S. P., Gunaratne, L. H. P., & Ariyaratne, A. R. (2000). An alternative premium payment method to finance the farmers’ pension and social security benefit scheme. Sri Lankan Journal of Agricultural Economics, 7(10), 51–67. https://doi.org/10.4038/sjae.v7i0.1823

- Wolf, I., & Caridad Yocerin, J. M. (2021). The transition to a multi-pillar pension system: The inherent socio-economic anomaly. Journal of Financial Economic Policy, 13(6), 755–771. https://doi.org/10.1108/JFEP-07-2020-0162

- Wongnaa, C. A., Apike, I. A., Babu, S., Awunyo-Vitor, D., & Kyei, A. B. (2021). The impact of adoption of artificial pollination technology in cocoa production: Evidence from Ghana. Journal of Agriculture and Food Research, 6, 100208. https://doi.org/10.1016/j.jafr.2021.100208

- World Cocoa Foundation. (2014), “World cocoa foundation market update report”, available at: www.worldcocoafoundation.org/wp-content/uploads/Cocoa-Market-Updatepdf

- Yeboah, C. S. (2015), Social Security Pensions in the Informal Sector: The Perspectives of Farmers in the Shai Osu–Doku District, Master’s Thesis, University of Ghana. http://197.255.68.203/handle/123456789/21261

- Zhang, C. (2015). Children, old age support and pension in rural China. China Agricultural Economic Review, 7(3), 405–420. https://doi.org/10.1108/CAER-01-2014-0003