Abstract

Budgets are a compass and guiding light for businesses. Therefore, management and owners of small and medium enterprises (SMEs) must carry out suitable and precise capital budgeting activities and methods to ensure business longevity and progression. There is a high risk of SMEs failing soon after they are found, with one likely cause being poor management skills. Thus, the study aims to assess the management skills of the capital budgeting planning and practices of SMEs. The objective is to ascertain the influence of management skills and owners on current capital budgeting planning and practice. The study adopted the quantitative method by administering questionnaires to 108 owners and managers in the Springfield Industrial Park. The findings of the study indicate that owners and managers were solely responsible for decision-making. Secondly, owners and managers lacked the financial skills, ability to control and lead staff. The study was limited to owners and managers in the SMEs and therefore cannot be inferred to any other area or subject/s. Future studies can be conducted in other regions, of which a comparative study is recommended that owners and managers in SMEs improve their business knowledge, as well as upskilling their financial ability in the capital budgeting process. Thus, the implications of improving owners and manager’s business knowledge will lead to timeous, smarter, and informed decision-making. It is therefore recommended that owners and managers take up short courses to improve computer literacy and financial skills in business processes.

1. Introduction

Small and medium-sized businesses (SMEs) play a crucial role in fostering innovation, creating jobs, and reducing poverty and income inequality (Dzomonda & Fatoki, Citation2019). A contributing factor in many modernised countries’ low unemployment rates and progressive economic growth is the participation of SMEs (Awad-Warrad, Citation2018). Small and medium-sized enterprises in South Africa account for approximately 42% of the country’s Gross Domestic Product (GDP) and 47% of the labour force (Moise et al., Citation2020).

The South African Minister of Small Business Development expressed concerns that SMEs have a 37% probability of surviving in their first four years, with further emphasis that “Business failure is often attributed to the lack of entrepreneurial knowledge, poor business skills, education, training, innovation and risk-taking factors” (Gumede, Citation2019).

Capital budgeting has remained one of the most significant financial decision areas of most business enterprises, including SMEs (Nguyen, Citation2019). Despite this, researchers are still trying to figure out the best strategy for implementing this fundamental idea, and South Africa is no different. As a result, it is necessary to identify the planning and procedures that are currently in place within these organisations, with a focus on capital budgeting planning and procedures. Planning is essential for businesses to be successful and long-lasting in this modern day.

SMEs must discover ways to increase their competitiveness, notably in terms of their capital investment, product cost, and pricing, given the limited resources available for implementing new progressive working methods and the ever evolving market pressure (Khurana et al., Citation2019). Due to poor capital budgeting decisions, many SMEs in South Africa find it difficult to compete with larger businesses (Imran et al., Citation2019).

Few studies have focused on analysing financial decision-making, derived from capital budgeting planning and practices, and its impact on small businesses.

Alles et al. (Citation2021) investigated the usage of capital budgeting strategies in SMEs and the impact of non-financial factors on the approaches that SMEs choose to use. The authors concluded by stating that the type of ownership, age, and experience of the decision-maker are important determinants of the capital budgeting procedures utilised by SMEs.

Siziba and Hall (Citation2021), on the other hand, evaluated the application of capital budgeting techniques over a period of time. Thus, this study aims specifically at the management level who are the key principle in utilising and implementing capital budgeting planning and practices.

As a result, it is necessary to determine what planning and practices exist within these businesses, with a focus primarily on capital budgeting planning and practice. One of the most commonly recognized capital budgeting planning (CBP) practice are owners’ and managers’ influence on capital budgeting planning and practice. Companies today require unique skills and dedication on the part of its personnel in order to thrive in the modern world of tough competition, coupled with the difficulties of globalisation and borderless marketplaces made possible by technology (especially social media). These are typically found in big businesses that have the financial resources to give their staff the appropriate training and education. Unfortunately, SMEs lack these abilities, hence the need to consider the aspects that are disregarded in capital budgeting planning and practices in order to fill this gap in SMEs. Therefore, the aim of the study was to assess the influence of management skills and owners on current capital budgeting planning and practice within the eThekwini Springfield Industrial Park.

2. Literature review

2.1. Capital budgeting theory

This study focuses on the capital budget function. The Capital Budget Theory (CBT) is grounded on the idea “that companies make investment decisions based on wealth maximization and increasing the value of the organization” (Basch, Citation2017). Capital budgeting is the process by which organisations determine which investments will generate long-term returns. Furthermore, maximizing shareholder wealth should not be the sole goal of businesses, as owners should have significant autonomy to pursue multiple objectives (Warren & Jack, Citation2018).

Capital investment decisions in small firms differ from those of large firms in several ways. Firstly, small business owners are concerned not only with wealth maximization but also with maintaining their independence, which may affect their investment selections. Secondly, access to capital may pose an issue for small business owners, which may influence decisions regarding liquidity and maintaining cash reserves. Thirdly, personnel constraints and a lack of investment expertise may limit small business owners’ ability to adequately analyse investment options (Li et al., Citation2020).

To attain greater survival, sustainability, profitability and cost-effectiveness, companies use capital budgeting. This brings critical responsibilities for the managers or owners of the SMEs as their decisions regarding capital budgeting marks the future of their companies in terms of their productivity and growth (Oyelaran-Oyeyinka, Citation2020).

It has been recorded that only 10–20% of SMEs undertake the capital budgeting process, and these are mostly public limited companies, which have sufficient funds to invest in long-term projects. Approximately 20% of the automotive industry’s SMEs have adopted capital budgeting for taking investment decisions and dealing with the tough competition which requires investment in advanced technologies (Burgos et al., Citation2020). The SMEs for electronics also adopt capital budgeting for the same reason (Zainuddin et al., Citation2021).

2.2. Importance of SMEs to eThekwini Municipality and South Africa

Small and medium enterprises (SMEs) are also commonly known in South Africa as small, medium, and micro enterprises (SMMEs). The SMEs within eThekwini include firms with a diverse range of operations or product lines. They include businesses run by the traditional families employing more than one hundred people and categorized under “medium sized enterprises” along with individuals who are self-employed, and mostly come from the lower strata of the society categorized under “micro enterprises which are informal in nature” (Durban Government, Citation2018). These SMEs are heterogeneous and operate in sectors of a diverse nature. They face several challenges in the administration of their business enterprises. The SMEs in eThekwini are operating in both the informal and formal economies. At the current stage, the region encompasses 11769 permit holders who are operating in the informal economy (Kibangou, Citation2019). The informal circle of operation is mostly in the central business district of Durban, encompassing a population of middle-aged black women.

Currently, there are more than 2 600 SMEs operating in the eThekwini Municipality receiving support from the government at various stages, including the establishment of the business, legal matters, and registration of their taxes (Blankespoor et al., Citation2020). However, SMEs still lack guidance in many areas, such as financial management, business management, human resources, and marketing (Ellitan, Citation2021).

2.2.1. The eThekwini Springfield industrial park

The Springfield Industrial Park is located within the city of Durban in the eThekwini Municipality, which is one of the busiest cities in the KwaZulu-Natal province of South Africa. Durban is the third biggest economic hub within South Africa, with around 3.5 million residents (Durban Government, Citation2018) that spread over an area of 2 297 sq. km. It is classified as a Category A municipality. A category “A’ municipality means a municipality that has exclusive municipal executive and legislative authority in its area. This not only makes the Springfield Industrial Park a highly and efficiently managed South African business location, but also a destination for the attraction of all kinds of business activities (eThekwini Municipality, Citation2018). The municipality works with a vision of becoming the most live able, sustainable, and caring city of South Africa where there is harmony and prosperity within the citizenry, thus putting the Industrial Park at the heart for business attraction (Durban Government, Citation2018).

The local economy of the eThekwini Municipality is considered as the province’s economic powerhouse and makes a significant contribution towards the overall economy of the country. The growth within the municipality is being continuously supported by the infrastructure of high quality and world-class industrial activities (eThekwini Municipality, Citation2018). The ensuing development of various industries, including the Springfield Industrial Park, has resulted in the modernization and establishment of infrastructural facilities to achieve the overall aims of government development of South Africa.

The GDP performance of eThekwini Municipality has been a significant contributor towards the GDP of South Africa. The municipality is posed as an economic center of the country ranking second and contributing to the GDP through industrial growth of a significant amount in the region. The GDP of the eThekwini Municipality was R 302.3 billion in 2016 and recorded an annual growth of 1% in comparison to 2015 GDP (Durban Government, Citation2018). Therefore, industries, such as those located within the Springfield Industrial Park, are important role players for the government of the country. There has not been enough research conducted within SMEs in the Springfield area with regard to capital budgeting and sustainability in the longer run which this study aims to serve the locality as a first.

2.3. Skills and influence of managers/owners

The key decision-makers of capital budgeting in the SMEs are the owners of the business and not the managers. It has been observed that either the owners carry out the capital budgeting process or they work in consultation with external experts on capital budgeting (Asgary et al., Citation2020). Most of the SME owners are unskilled and are not highly educated to carry out the process of capital budgeting. The SME owners operating in Springfield Industrial Park are from the local communities and lack both education and funding, which results in not carrying out the capital budgeting processes in more than 50% of the cases (Egbide et al., Citation2019). In their study, Essel et al. (Citation2019), found that a relationship existed between the education level of entrepreneurs and their success in business. The relationship of was that the more qualified the entrepreneur was the greater success there was in business. According to Asgary et al. (Citation2020), reflected results were in their intuition, good marketing strategies, good access to capital and customer needs. These are the essential factors required to answer the second research objective of this study, which is the influence of management skills of the CBP.

The capital budgeting planning process requires a lot of information from managers or owners in SMEs (Awinja & Fatoki, Citation2021). Therefore, one of the positive influences that management or owners can bring into the capital budgeting and planning process is efficient sharing of information (Edvardsson et al., Citation2019). Managers and owners can provide useful information about the net output from the capital budgets and the potential risks (Sacks et al., Citation2018).

A consequence of information-sharing for instance, is that the superior is able to improve the quality of decisions and design of capital budgeting planning (Baah et al., Citation2021). Managers and owners coordinate and propose a more efficient and goal-specific incentive contract, which increases the subordinates’ motivation to achieve the budget. This will, in turn, lead to improved financial performance within an SME (Orobia et al., Citation2020). Are these essential factors play that much of a huge role and contribute to having adequate and sound capital budgeting planning and practices within SMEs?

2.3.1. Decision-making of management

A larger percentage of SMEs have the ownership of the businesses as sole proprietorship and close corporations. Therefore, they are the sole decision makers of budgeting practices. The owners mostly opt for cash flow budgeting rather than capital budgeting in the SMEs (Orobia et al., Citation2020). In most situations, capital budgeting was not even implemented by the owners due to their stand on financial viability; not having capital to invest in new projects; and a lack of knowledge regarding the entire process of capital budgeting (Egbide et al., Citation2019). Bergeron and Gaboury (Citation2020) mention that the rest of the SMEs, which applied the capital budgeting process for their investment in new projects, did so through the assistance of external expert consultants. Does management’s decision-making play a key role in capital budgeting practices and financial viability of SMEs?

2.3.2. Financial considerations

The business environment of South Africa is such that the first obstacle, faced by SMEs, is the non-availability of finances, not only for establishing the company, but also for any future investments (Asah et al., Citation2020). Access to finance is considered to be a hurdle for many start-up businesses including established SMEs (Adegboye & Iweriebor, Citation2018). The second consideration is disturbing, since it is highly likely that limited access to financing opportunities may have a direct influence on the sustainability of South African SMEs (Mbumbo et al., Citation2019).

According to (Pilar et al., Citation2018), a firm’s socio-economic factors, its size, its type ownership, age and their accessibility to finance has an adverse impact. Additionally, any failure to declare assets, deliver accounting records, or ensure creditworthiness and financial performance will adversely influence financial institutions’ promptness to pledge to medium- or long-term investments (Owusu-Anane, Citation2020).

This scarcity to gain credit worthiness is a major limitation for manufacturing SMEs that wish to expand their activities (Horváth & Szabó, Citation2019). It is clear that SMEs present a high risk to the lender. Moreover, many SMEs have inadequate assets that can be used as collateral and will suffer from poor mechanism (Godke Veiga & McCahery, Citation2019). Furthermore, Appiah et al. (Citation2018) asserts that the absence of financial support is also due to the owner’s flaws in drafting a well-prepared and explored credit proposal for the financial institutions.

Different financial institutions, especially private firms, provide loans to SMEs at a very high rate of interest, which deters SMEs from investing in long-term bigger projects or capital budgeting (Page & Okeke, Citation2019). Although the lending rates of government agencies are very low, SMEs are largely not aware of the various policies, rules, and programmes pertaining to lending and are thereby not able to access the benefits.

2.3.3. Government policies

The Department of Trade and Industry (DTI) provides financial support to qualifying companies in various sectors of the economy. Financial support is offered for various economic activities, including manufacturing, business competitiveness, export development and market access, as well as foreign direct investment.

The taxation policies for SMEs by the eThekwini Municipality are very supportive towards the SMEs, especially those operating in the Special Economic Zones which are exempted from taxation for a long period of time, usually for 10–15 years on average (Pilar et al., Citation2018). Since the Springfield Industrial Park comes under SEZ 63 in the eThekwini Municipality, the SMEs operating in this zone have been exempted from taxation for now. Thus, this exemption impacts the capital budgeting of the SMEs positively (Jeganathan, Citation2021).

2.3.4. Lack of networking ability

Although the SMEs are operating in the same park or municipality, they were not connected with each other at any level. This non-connection hampers any type of exchange of business knowledge or experiences between the different entities. Thus, even this internal resource is being under-utilized by the SMEs (Orobia et al., Citation2020).

Mutual production-distribution planning, among the supply network players, is considered a proper mechanism to support enterprises in dealing with the uncertainties and dynamism linked to the current markets (Andres et al., Citation2018). Enterprises, especially SMEs, should be able to overcome the incessant changes of the market by enhancing their agility. Carrying out shared planning allows enterprises to develop their readiness and agility for facing market volatility (Osei et al., Citation2018).

2.3.5. Business knowledge regarding the financial management skills

Most managerial skills, especially financial management skills, are lacking in the owners along with the knowledge that these skills must be acquired. The major cause of this problem was observed to be the background from which these owners hail; their education level and the lack of guidance or training institutes for providing such assistance to them (Orobia et al., Citation2020).

Consequently, most of the owners request the assistance of external consultants in capital budgeting for the lack of internal financial knowledge (Kirton & Greene, Citation2019). Due to the outsourced party not being accountable for the performance of the business, it is not within their contracted scope to do number crunching to provide analytical data and the party is not obligated to highlight concerns and issues (Abdel-Khalik, Citation2018). Do outsourced and third-party funds and borrowings play a significant role in the financial sustainability of SMEs?

2.3.6. Knowledge to identify and resolve business challenges

The knowledge and capabilities of the owner are crucial for business performance and growth because the management structures and independence of small businesses cause owners to have a key role in business operations (Guritno et al., Citation2019). Entrepreneurship education plays a crucial and important role in providing the crucial skills for an owner to operate their daily business requirements, as well as how to face obstacles and challenges that they will face during their business life (Almahry et al., Citation2018).

Several researchers give entrepreneurship a significant focus in their studies (Almahry et al., Citation2018). In addition, Rae and Melton (Citation2017) suggest entrepreneurship education should include skill–building and leadership programmes, new product development, creative thinking and technology innovation.

According to (Nabi et al., Citation2018), individuals, who have work experience and educational background, have a set of various skills. These individuals are more likely to become entrepreneurs and make better business progress than others. This study assesses whether theoretical financial knowhow has an influence on the practical side of the sustainability of SMEs.

2.3.7. Ability to control, lead, manage, direct, and monitor the manpower

All SMEs’ staff are essential to their operations. This includes acquiring new people for the business and ensuring that they are productive additions to the SME (Martínez-Costa et al., Citation2019). Effective human resource management matches and then develops the abilities of job candidates and staff with that of the needs of the firm. An effective personnel system will contribute to the key ingredients for survival, sustainability, and growth (Chams & García-Blandón, Citation2019).

Human resource management is a complementary deed. At one end, one employs qualified people who are well suited to the firm’s needs. At the other end, one trains and develops staff to meet the firm’s needs. Most expanding small businesses fall between the two levels (Bornay-Barrachina et al., Citation2017). In this context, the study also assesses if having advanced and modern technology and accounting software influences positively on capital budgeting planning and practices.

2.3.8. Resource management for capital budgeting and planning

Managers in SMEs can use resource management to ensure the longevity of their financial operations, while others can use it to cultivate a competitive edge in the long- term (Qosasi et al., Citation2019). Resource management is designed to set a firm’s financial course of action, identifying the financial strategies it will use to compete in the marketplace and how it will organise its internal financial activities.

Ramasobana et al. (Citation2017) asserts that managing resources is, in effect, management’s game plan for strengthening the organisation’s financial position, pleasing shareholders, and achieving financial performance targets. Thus, according to Opoku (Citation2016), an SME whose management has poor resource management appears to be directionless and wasteful. There is a great link between resource management and capital budgeting and planning (Al Breiki & Nobanee, Citation2019). Whilst capital budgeting and planning are of such importance to the operation of an SME, Amer et al. (Citation2020) emphasises that in too many cases, the participation of employees in planning and even decision-making is instrumental to improved financial performance.

The researchers sought to determine the nature of resource management required for CBP which ensures longevity of financial operations and can cultivate a competitive edge. The study seeks to determine whether managing resources forms an integral part of management’s key responsibilities in achieving financial performance targets.

2.4. Theoretical review

2.4.1. Contingency theory adopted

The theoretical framework on which this study is based on is the Contingency theory that is extensively used to explain the characteristics of Management Accounting Systems (MAS) as financial and strategic tools in organisations (Macy & Arunachalam, Citation1995).

Bouwens (Citation2017) argues that the adoption and success of the capital budgeting system depends upon specific contingent factors, such as product diversity, cost structure information, firm size, competition, business culture and evaluation tools. Bouwens (Citation2017) also suggests that the effectiveness of a MAS depends on the extent to which the MAS’s distinctiveness meets the requirements of the various contingencies faced by the organisation.

This study seeks to ascertain the influence of management skills on current capital budgeting planning and practice within SMEs. An example is the contingency relationship between the need to invest in a more enhanced financial management system, such as capital budgeting techniques and the organisational factors in increasing survival, sustainability and growth.

In this present study, Macy and Arunachalam’s (Citation1995) Contingency model has been adopted in order to assess the influence of management skills and owners on current capital budgeting planning and practice small business enterprises within the eThekwini Springfield Industrial Park.

3. Research methodology

Given the aim of this study was to assess the influence of management skills and owners on current capital budgeting planning and practice in a specific area, based on the richness of information from a rather large sample of 146, the quantitative method was more suitable. This study used a larger sample size to draw conclusions, hence a quantitative analysis using a questionnaire was used as the research method. The use of quantitative analysis was the finest strategy to guarantee the findings’ measurability, correctness, and reliability.

This study targets a population size of 146 respondents consisting of SMEs in Durban. Data collection from every individual of this population would be both extremely difficult and expensive. Therefore, it would be suitable to gather information from a representative sample of the population, and if the sample results are reasonable, one may draw conclusions and make inferences about the population. A non-random and purposive sample size was chosen for the survey amongst the SMEs in the Springfield Industrial Park in Durban.

To assess the competitiveness and sustainability of SMEs, the researchers made use of a quantitative approach in this study. A descriptive research design was adopted targeting 146 registered SMEs in the Springfield Industrial Park in Durban. A purposive sample of 108 participants was selected using non-probability sampling. The completed sample questionnaires were received representing a 74% response rate. The validity of the study’s questionnaire was established as the validity test of the data met the Cronbach's alpha cut-off point of 0.70. Owners of SMEs or appropriate representatives were given a self-administered, four-point Likert scale-style questionnaire to complete to collect data for the study.

The questionnaires were distributed to respondents to complete. The data, which were converted into numerical values, were analysed using a scientific statistical analysis program. With the aid of a Smart Partial Least Squares (SmartPLS) configuration set up on a computer system, the data acquired for this investigation were analysed.

4. Results and discussion

The following questions and responses were discussed with regard to the influence of management/owners on current capital budgeting planning and practice.

4.1. Skills and influence of managers/owners

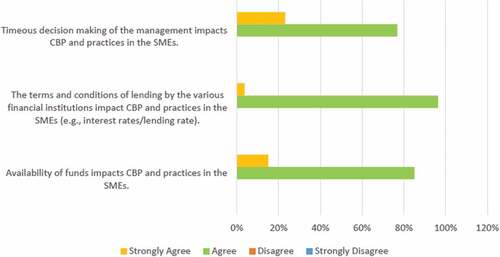

Figure represents the statements related to decision-making of owners and/or managers. The initial question probed whether prompt management decision-making affects CBP and practices in SMEs with results indicating agreement from all respondents (23% agreed, 77% strongly agreed). Close corporations and sole proprietorships account for most of the SMEs’ ownership (De Moura et al., Citation2019). Therefore, they are the only ones that decide on budgeting procedures. In most of the SMEs, the owners typically choose cash flow budgeting over capital budgeting.

Figure 1. Decision-making of Managers/Owners.

The second question, sought to determine whether the CPB, is impacted by the terms and circumstances of loans made by the different financial institutions such as interest rates or lending rates. Ninety-six percent of respondents strongly agreed, and 4% agreed which reflects the difficulty for SMEs in getting finance.

The last inquiry related to the availability of funds impact on CBP and practices in the SMEs. All respondents agreed on the impact, with 85% of the respondents strongly agreed and 15% agreed. This finding is a clear indication of the challenges encountered by SMEs in obtaining credit. As indicated in the literature review, outsourced and third-party funds and borrowings is indeed a critical component of SMEs financial viability.

Various financial institutions provide loans to SMEs at a very high rate of interest, which deters SMEs from investing in long-term bigger projects or capital budgeting. It has also been noted that a failure to ensure creditworthiness and financial performance will adversely influence the financial institutions’ promptness to pledge to medium- or long-term, investments. This scarcity to gain credit worthiness is a major limitation for manufacturing SMEs that wish to expand their activities (Yoshino & Taghizadeh-Hesary, Citation2018).

4.2. Financial consideration

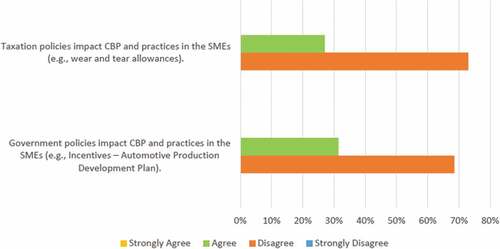

In this section, the first question in Figure investigated if the taxation policies impact CBP and practices in the SMEs (e.g., wear and tear allowances). Most respondents (73%) disagreed with the statement, an indication that respondents were not aware of these incentive schemes. The majority of SMEs are largely not aware of the various policies, rules and programmes (Eniola & Entebang, Citation2017).

Figure 2. Financial considerations.

The second question examined whether government policies impact CBP and practices in the SMEs (e.g., Incentives—Automotive Production Development Plan, Automotive Investment Scheme). Many of the respondents (69%) disagreed and 31% agreed. Yet again, the high level of disagreement indicates that respondents were not aware of these incentive schemes.

The SMEs operating in the Springfield Industrial Park are exempt from tax assessment because this zone is SEZ 63 in the eThekwini Municipality. Consequently, this exemption has a favorable impact on these SMEs’ capital planning. Government financing support for SMEs is still falling short of what is needed for them to expand their operations (Zutshi et al., Citation2021).

4.3. Financial appraisal

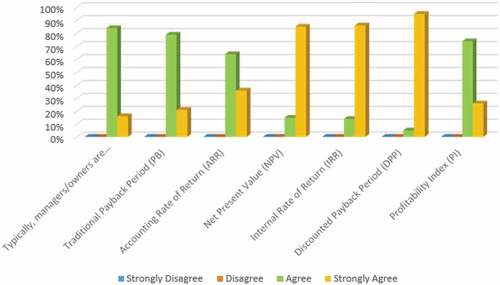

Figure investigates whether managers/owners were in involved in financial appraisal and to the usage of the financial appraisal techniques. Most of the respondents (84%) agreed whilst 16% strongly agreed. This finding is a clear sign that this process is extremely important with a combined agreement of 100%. No responses were recorded for the options strongly disagree and disagree.

Figure 3. Financial appraisal.

The second part of the probe was to ascertain the usage of financial appraisal techniques. As displayed in Figure , the traditional, simpler capital budgeting techniques (payback period and accounting rate of return) had a higher usage than the time-value of money-based techniques (NPV, IRR and discounted payback period).

There were no responses for the disagree options for the usage of financial appraisal techniques. It is noteworthy that respondents were very concerned about the outcome of the financial appraisal.

4.4. Business knowledge

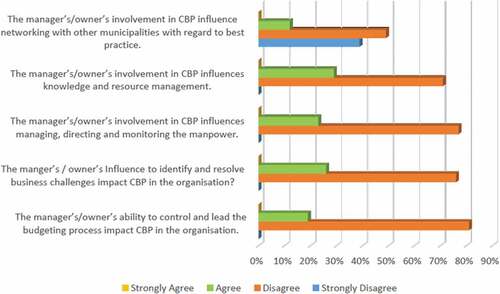

Based on the findings displayed in Figure , manager’s/owner’s involvement in networking with other municipalities regarding best practice, the study found that 12% agreed, 39% strongly disagreed and 49% disagreed. The high level of disagreement indicates that managers/owners lack the ability to network with other municipalities.

Figure 4. Business knowledge.

In relation to the examination of the managers’/owner’s involvement in resource management, the results indicated that 71% of the respondents disagreed with the statement. The high level of disagreement indicates that managers’/owners’ lack the ability to manage resources within the CPB process.

The third question examined the manager’s/owner’s involvement managing, directing, and monitoring the manpower. Most of the respondents (77%) disagreed with the statement. The high level of disagreement indicates that managers/owners lack the ability to manage, direct and monitor the manpower of SMEs in the CBP.

The researchers examined the manger’s/owner’s influence in identifying and resolving business challenges: 76% of the respondents disagreed while 26% agreed. The high level of disagreement points to the fact that managers/owners lack the ability to identify and resolve business challenges within the CBP process.

The last question examined the manager’s/owner’s ability to control and lead the budgeting process. Most respondents (81%) disagreed and 19% agreed. The high level of disagreement indicates that managers/owners lack the ability to control and lead the SMEs in the CBP.

4.5. Financial skills

An investigation on whether the manager’s/owner’s knowledge of financial management skills impacted CBP in the organisation revealed that 90% of the respondents agreed (53% agree and 37% strongly agree). The deduction can be made that managers/owners do not have substantial awareness around Financial Management.

There were overall high levels of agreement that the financial management function was outsourced. The combined 89% (15% agree and 74% strongly agree) of respondents in agreement is confirmation of the lack of financial management skills within the SMEs.

5. Conclusion

In this modern age of competition, coupled with the challenges of globalisation and borderless markets made possible through technology, this study revealed that SMEs need special skills, namely CBP, from its executives in order to sustain.

The results of this study showed that management skills are key determinants of the capital budgeting procedures utilised by SMEs. These findings highlight some significant policy ramifications in the context of Springfield’s developing SME sector. Government and regulatory bodies should adopt legislation and develop regulations that emphasize capital budgeting management as a critical competence for decision-makers. SMEs should implement rules within their management to improve financial literacy and overall organisational effectiveness.

This study’s results demonstrated that the largest percentage of SMEs’ ownership are sole proprietorships and close corporations. The executives are largely not conscious of their creditworthiness, various policies, rules, and programmes offered by government agencies and tax incentives.

Many managers/owners lack the ability to network with other municipalities and also require the assistance of external consultants in capital budgeting due to their shortage of internal financial knowledge. They also require the capability to control, lead, identify and resolve business challenges within the CBP process.

It is recommended that executives of today’s SMEs should depend less on manual processes and venture into technology to enhance the performance of CBP which will definitely lead to efficiency and effectiveness in their service delivery to their respective communities.

Acknowledgements

The authors gratefully acknowledge all the participants that participated in the study.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Abdel-Khalik, A. R. (2018). The un-faithful representation of financial statements: issues in accounting for financial instruments. University of Hawaiʻi at Mānoa.

- Adegboye, A. C., & Iweriebor, S. (2018). Does access to finance enhance SME innovation and productivity in Nigeria? Evidence from the world bank enterprise survey. African Development Review, 30(4), 449–14. https://doi.org/10.1111/1467-8268.12351

- Al Breiki, M., & Nobanee, H. (2019). The role of financial management in promoting sustainable business practices and development. Available at SSRN 3472404. Social Science Research Network.

- Alles, L., Jayathilaka, R., Kumari, N., Malalathunga, T., Obeyesekera, H., & Sharmila, S. (2021). An investigation of the usage of capital budgeting techniques by small and medium enterprises. Quality & Quantity, 55(3), 993–1006. https://doi.org/10.1007/s11135-020-01036-z

- Almahry, F. F., Sarea, A. M., & Hamdan, A. M. (2018). A review paper on entrepreneurship education and entrepreneurs’ skills. Journal of Entrepreneurship Education, 21(1), 1–7. https://www.researchgate.net/profile/Adel-Sarea/publication/338300642_The_Impact_of_Entrepreneurship_Education_on_Entrepreneurs'_Skills/links/5e569d514585152ce8f25e85/The-Impact-of-Entrepreneurship-Education-on-Entrepreneurs-Skills.pdf

- Amer, S. B., Gregg, J. S., Sperling, K., & Drysdale, D. (2020). Too complicated and impractical? An exploratory study on the role of energy system models in municipal decision-making processes in Denmark. Energy Research & Social Science, 70, 101673. https://doi.org/10.1016/j.erss.2020.101673

- Andres, B., Poler, R., Saari, L., Arana, J., Benaches, J.-V., & Salazar, J. (2018). Optimization models to support decision-making in collaborative networks: A review. Closing the Gap between Practice and Research in Industrial Engineering, 249–258. https://doi.org/10.1007/978-3-319-58409-6_28

- Appiah, K., Possumah, B. T., Ahmat, N., & Sanusi, N. A. (2018). Applicability of theory of constraint in predicting Ghanaian SMEs investment decisions. Journal of International Studies, 11(2), 202–221. https://doi.org/10.14254/2071-8330.2018/11-2/14

- Asah, F. T., Louw, L., & Williams, J. (2020). The availability of credit from the formal financial sector to small and medium enterprises in South Africa. Journal of Economic and Financial Sciences, 13(1), 10. https://doi.org/10.4102/jef.v13i1.510

- Asgary, A., Ozdemir, A. I., & Özyürek, H. (2020). Small and medium enterprises and global risks: Evidence from manufacturing SMEs in Turkey. International Journal of Disaster Risk Science, 11(1), 59–73. https://doi.org/10.1007/s13753-020-00247-0

- Awad-Warrad, T. (2018). Trade openness, economic growth and unemployment reduction in Arab Region. International Journal of Economics and Financial Issues, 8(1), 179–183. https://www.econjournals.com/index.php/ijefi/article/download/5573/pdf

- Awinja, N. N., & Fatoki, O. I. (2021). Effect of digital financial services on the growth of SMEs in Kenya. African Journal of Empirical Research, 2(1), 79–94. https://doi.org/10.51867/ajer.v2i1.16

- Baah, C., Opoku-Agyeman, D., Acquah, I. S. K., Agyabeng-Mensah, Y., Afum, E., Faibil, D., & Abdoulaye, F. A. M. (2021). Examining the correlations between stakeholder pressures, green production practices, firm reputation, environmental and financial performance: Evidence from manufacturing SMEs. Sustainable Production and Consumption, 27, 100–114. https://doi.org/10.1016/j.spc.2020.10.015

- Basch, R. J. (2017). Capitalization strategies for small business sustainability. Walden University].

- Bergeron, D. A., & Gaboury, I. (2020). Challenges related to the analytical process in realist evaluation and latest developments on the use of NVivo from a realist perspective. International Journal of Social Research Methodology, 23(3), 355–365. https://doi.org/10.1080/13645579.2019.1697167

- Blankespoor, E., deHaan, E., & Marinovic, I. (2020). Disclosure processing costs, investors’ information choice, and equity market outcomes: A review. Journal of Accounting and Economics, 70(2–3), 101344. https://doi.org/10.1016/j.jacceco.2020.101344

- Bornay-Barrachina, M., López-Cabrales, A., & Valle-Cabrera, R. (2017). How do employment relationships enhance firm innovation? The role of human and social capital. The InTernaTIonal Journal of Human Resource managemenT, 28(9), 1363–1391. https://doi.org/10.1080/09585192.2016.1155166

- Bouwens, J. (2017). Understanding investment decisions: The role of cost accounting. Available at SSRN 2937256. Social Science Research Network.

- Burgos, J. A. M., Kittler, M., & Walsh, M. (2020). Bounded rationality, capital budgeting decisions and small business. Qualitative Research in Accounting & Management. https://doi.org/10.1108/QRAM-01-2019-0020

- Chams, N., & García-Blandón, J. (2019). On the importance of sustainable human resource management for the adoption of sustainable development goals. Resources, Conservation and Recycling, 141, 109–122. https://doi.org/10.1016/j.resconrec.2018.10.006

- de Moura, A. L., Santos, D. F. L., & Conceicao, E. V. (2019). Proposal for a financial management model applied to a small business in the fertilizer segment. Revista de Empreendedorismo e Gestao de Pequenas Empresas, 8(3), 36–69. https://go.gale.com/ps/i.do?id=GALE%7CA608073275&sid=googleScholar&v=2.1&it=r&linkaccess=abs&issn=23162058&p=IFME&sw=w

- Dzomonda, O., & Fatoki, O. (2019). Evaluating the impact of organisational culture on the entrepreneurial orientation of small and medium enterprises in South Africa. Bangladesh e-Journal of Sociology, 16(1), 82–94. https://www.researchgate.net/profile/Alfred_Eboh/publication/331608610_Bangladesh_e-Journal_of_Sociology_Bangladesh_Sociological_Society/links/5c82db40299bf1268d486536/Bangladesh-e-Journal-of-Sociology-Bangladesh-Sociological-Society.pdf#page=82

- Edvardsson, I. R., Durst, S., & Oskarsson, G. K. (2019). Strategic outsourcing in SMEs. Journal of Small Business and Enterprise Development, 27(1), 73–84. https://doi.org/10.1108/JSBED-09-2019-0322

- Egbide, B.-C., Adegbola, O., Rasak, B., Sunday, A., Olufemi, O., & Ruth, E. (2019). Cost reduction strategies and the growth of selected manufacturing companies in Nigeria. International Journal of Mechanical Engineering and Technology, 10(3). https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3451705

- Ellitan, L. (2021). The importance of entrepreneurship and information technology for SMEs strategic planning. International Journal of Trend in Scientific Research and Developmen, 5(4), 1003–1009. https://www.researchgate.net/profile/Lena-Ellitan/publication/352165438_The_Importance_of_Entrepreneurship_and_Information_Technology_for_SMEs_Strategic_Planning/links/60bc40f0458515218f94c7b8/The-Importance-of-Entrepreneurship-and-Information-Technology-for-SMEs-Strategic-Planning.pdf

- Eniola, A. A., & Entebang, H. (2017). SME managers and financial literacy. Global Business Review, 18(3), 559–576. https://doi.org/10.1177/0972150917692063

- Essel, B. K. C., Adams, F., & Amankwah, K. (2019). Effect of entrepreneur, firm, and institutional characteristics on small-scale firm performance in Ghana. Journal of Global Entrepreneurship Research, 9(1), 1–20. https://doi.org/10.1186/s40497-019-0178-y

- Godke Veiga, M., & McCahery, J. A. (2019). The financing of small and medium-sized enterprises: An analysis of the financing gap in Brazil. European Business Organization Law Review, 20(4), 633–664. https://doi.org/10.1007/s40804-019-00167-7

- Government, D. (2018). Medium term revenue and expenditure framework 2018/2019 to 2020/2021. eThekwini Municipality. http://www.durban.gov.za/Resource_Centre/reports/Budget/Documents/MediumTermRevenueAndExpednitureFramework2018_19to2020_2021.pdf

- Gumede, L. (2019). Small businesses and the South African companies act: Does one size really fit all? University of Kwa-Zulu Natal.

- Guritno, P. D., Suyono, H., & Sunarjo, S. (2019). Competency model of social entrepreneurs: Learning from successful Indonesian social entrepreneurs. International Journal of Research in Business and Social Science (2147- 4478), 8(3), 94–110. https://doi.org/10.20525/ijrbs.v8i3.256

- Horváth, D., & Szabó, R. Z. (2019). Driving forces and barriers of Industry 4.0: Do multinational and small and medium-sized companies have equal opportunities? Technological Forecasting and Social Change, 146, 119–132. https://doi.org/10.1016/j.techfore.2019.05.021

- Imran, M., Salisu, I., Aslam, H. D., Iqbal, J., & Hameed, I. (2019). Resource and information access for SME sustainability in the era of IR 4.0: The mediating and moderating roles of innovation capability and management commitment. Processes, 7(4), 211. https://doi.org/10.3390/pr7040211

- Jeganathan, D. (2021). The effect of CEO and director experience on acquisition performance: A pitch. Accounting Research Journal, 34(4), 385–393. https://doi.org/10.1108/ARJ-08-2020-0267

- Khurana, S., Haleem, A., & Mannan, B. (2019). Determinants for integration of sustainability with innovation for Indian manufacturing enterprises: Empirical evidence in MSMEs. Journal of Cleaner Production, 229, 374–386. https://doi.org/10.1016/j.jclepro.2019.04.022

- Kibangou, S. R. (2019). The use of management accounting tools to improve the business performance of small and medium manufacturing enterprises in Cape Town. Cape Peninsula University of Technology].

- Kirton, G., & Greene, A. M. (2019). Telling and selling the value of diversity and inclusion—External consultants’ discursive strategies and practices. Human Resource Management Journal, 29(4), 676–691. https://doi.org/10.1111/1748-8583.12253

- Li, Q., Guan, X., Shi, T., & Jiao, W. (2020). Green product design with competition and fairness concerns in the circular economy era. International Journal of Production Research, 58(1), 165–179. https://doi.org/10.1080/00207543.2019.1657249

- Macy, G., & Arunachalam, V. (1995). Management accounting systems and contingency theory: In search of effective systems. Advances in Management Accounting, 4, 63–86.

- Martínez-Costa, M., Jiménez-Jiménez, D., & Dine Rabeh, H. A. (2019). The effect of organisational learning on interorganisational collaborations in innovation: An empirical study in SMEs. Knowledge Management Research & Practice, 17(2), 137–150. https://doi.org/10.1080/14778238.2018.1538601

- Mbumbo, E., Benedict, H., & Bruwer, J.-P. (2019). The influence of management’s accounting skills on the existence of their South African small, medium and micro enterprises. International Journal of Education Economics and Development, 10(3), 323–334. https://doi.org/10.1504/IJEED.2019.100670

- Moise, L. L., Khoase, R., & Ndayizigamiye, P. (2020). The influence of government support interventions on the growth of African foreign-owned SMMEs in South Africa. In Francisco Jareño Cebrian (Eds.) Analyzing the relationship between innovation, value creation, and entrepreneurship (pp. 104–124). IGI Global.

- Municipality, E. (2018). Draft Process Plan. eThekwini Municipality. http://www.durban.gov.za/City_Government/City_Vision/IDP/Documents/Process%20Plan%20Report_%202018_19.pdf

- Nabi, G., Walmsley, A., Liñán, F., Akhtar, I., & Neame, C. (2018). Does entrepreneurship education in the first year of higher education develop entrepreneurial intentions? The role of learning and inspiration. Studies in Higher Education, 43(3), 452–467. https://doi.org/10.1080/03075079.2016.1177716

- Nguyen, D. (2019). Application of capital budgeting methods in small and medium-sized enterprises: Case studies of SMEs in Vietnam. University of Turku.

- Opoku, M. (2016). The effect of strategic planning on SMEs performance: A case study of selected SMEs in Kumasi. Journal of Business Management, 1(1), 19–25. http://ir.knust.edu.gh/bitstream/123456789/10479/1/Maryann_10102016_COMPLETEs%5B3%5D.pdf

- Orobia, L. A., Nakibuuka, J., Bananuka, J., & Akisimire, R. (2020). Inventory management, managerial competence and financial performance of small businesses. Journal of Accounting in Emerging Economies, 10(3), 379–398. https://doi.org/10.1108/JAEE-07-2019-0147

- Osei, C., Amankwah-Amoah, J., Khan, Z., Omar, M., & Gutu, M. (2018). Developing and deploying marketing agility in an emerging economy: The case of blue skies. International Marketing Review. https://www.emerald.com/insight/content/doi/10 .1108/IMR-12-2017-0261/full/html

- Owusu-Anane, E. K. (2020). The Utilization of Financial Institutions in Ghana: SME’s perspectives (A case study of SMEs in the tema metropolis assembly). University of Ghana].

- Oyelaran-Oyeyinka, B. (2020). Resurgent Africa: structural transformation in sustainable development. Anthem Press.

- Page, M. T., & Okeke, C. (2019). Stolen dreams: how corruption negates government assistance to Nigeriaʹs small businesses. Carnegie Endowment for International Peace.

- Pilar, P.-G., Marta, A.-P., & Antonio, A. (2018). Profit efficiency and its determinants in small and medium-sized enterprises in Spain. BRQ Business Research Quarterly, 21(4), 238–250. https://doi.org/10.1016/j.brq.2018.08.003

- Qosasi, A., Permana, E., Muftiadi, A., Purnomo, M., & Maulina, E. (2019). Building SMEs’ competitive advantage and the organizational agility of apparel retailers in Indonesia: The role of ICT as an initial trigger. Gadjah Mada International Journal of Business, 21(1), 69–90. https://doi.org/10.22146/gamaijb.39001

- Rae, D., & Melton, D. E. (2017). Developing an entrepreneurial mindset in US engineering education: An international view of the KEEN project. The Journal of Engineering Entrepreneurship, 7(3). http://bgro.repository.guildhe.ac.uk/id/eprint/161/

- Ramasobana, M., Fatoki, O., & Oni, O. (2017). Entrepreneurs’ characteristics and marketing communication practices of SMEs in South Africa. Gender and Behaviour, 15(3), 9350–9371. https://journals.co.za/doi/abs/10 .10520/EJC-c382b18b1

- Sacks, R., Eastman, C., Lee, G., & Teicholz, P. (2018). BIM handbook: A guide to building information modeling for owners, designers, engineers, contractors, and facility managers. John Wiley & Sons.

- Siziba, S., & Hall, J. H. (2021). The evolution of the application of capital budgeting techniques in enterprises. Global Finance Journal, 47, 100504. https://doi.org/10.1016/j.gfj.2019.100504

- Warren, L., & Jack, L. (2018). The capital budgeting process and the energy trilemma - A strategic conduct analysis. The British Accounting Review, 50(5), 481–496. https://doi.org/10.1016/j.bar.2018.04.005

- Yoshino, N., & Taghizadeh-Hesary, F. (2018). The role of SMEs in Asia and their difficulties in accessing finance. https://journals.co.za/doi/abs/10 .10520/EJC-c382b18b1

- Zainuddin, N. A., Ismail, M., Ahmad, N. Z. A., Shariff, S., Mazalan, M. I., & Ab Kadir, M. S. (2021). The driven factors on new electronic commerce adoption by Small and Medium Enterprise (SME) in Klang Valley. E-Journal of Islamic Thought & Understanding (E-JITU), 2, 17–28.

- Zutshi, A., Mendy, J., Sharma, G. D., Thomas, A., & Sarker, T. (2021). From challenges to creativity: Enhancing SMEs’ resilience in the context of COVID-19. Sustainability, 13(12), 6542. https://doi.org/10.3390/su13126542