?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper examines the impact of earnings quality (EQ) on the Vietnam companies’ cost of debt (COD). We use data from companies listed on the Vietnam stock market from 2010 to 2019. In this paper, we develop a model to investigate the influence of audit quality and foreign ownership on COD. We find that EQ had a negative relationship with COD. However, when firm is in financial distressed, EQ has a positive relationship with COD. As an intermediate variable, EQ also has a negative relationship with COD.

PUBLIC INTEREST STATEMENT

Using the OLS estimation method and the data of 3800 observations of listed companies in 2010–2019, we find empirical evidence that firms of high EQ would reduce their own COD. Simultaneously, the study also identifies evidence for the relationship between COD and factors of audit quality and foreign ownership. Besides, the study also considers that upon the impact of EQ when interacting with financial distress, earnings quality has a positive relationship with COD.

1. Introduction

Businesses’ earnings quality (EQ) is an essential factor in minimizing information asymmetry and thus promoting the development of financial markets. EQ is the possibility of potential earnings growth of the business or the probability that the business will achieve the expected earnings growth in the future. Lenders often rely mainly on figures presented in financial statements in the relationship between businesses and creditors and in setting terms in credit contracts. Therefore, information asymmetry due to the low quality of information presented in financial statements will affect funding decisions. Firms with a high level of information asymmetry will find it more difficult to access external funding sources or encounter strict loan terms and shortened loan tenor as well as high COD, which is the protection by the price set by the creditor to limit credit risk.

According to Richardson et al. (Citation2001), EQ was assessed based on the stability of future sales (Beneish & Vargus, Citation2002) and also assumed that the stability of the firm’s revenue would be evidence for the EQ of the business. Penman and Zhang (Citation2002) defined EQ as the predictability of future earnings of a firm. Investors or other stakeholders in the capital market often rely on the information presented on financial statements to assess future cash flows of a business and thereby estimate expected returns (Francis et al., Citation2004). As such, in order to be capable of predicting future cash flows better, earnings published in the financial statements should be of good quality.

Several empirical studies produced quite similar results in terms of the negative relationship between EQ and the cost of debt, such as Francis et al. (Citation2005), Gao (Citation2010), Lambert et al. (Citation2007), Carmo et al. (Citation2016), and Beltrame et al. (Citation2017), and Orazalin and Akhmetzhanov (Citation2019), and Houcine and Houcine (Citation2020). However, the EQ measure followed various earnings management measurement models in different contexts and markets.

In Vietnam, a recent study by Le et al. (Citation2021) examined the impact of accrual quality on the cost of debt with a sample of 889 observations from 2012 to 2017, which showed that EQ had a negative relationship with COD. We continue to develop in the research direction of Le et al. (Citation2021), with larger sample size and, at the same time, add other independent factors such as independent audit quality and the impact of foreign ownership on the cost of debt. Also, we keep developing our model upon considering the impact of earnings quality when interacting with financial distress on COD and the research findings are pretty and attractive when considering this interaction variable. Simultaneously, we also considered whether or not there was an influence of EQ as an intermediate variable on COD. According to this study, providing high-quality information on financial statements will reduce the cost of borrowing, open up opportunities for businesses to gain access to loans, survive and develop in today’s volatile market economy.

2. Theories

2.1. Earnings qualit

Dechow et al. (Citation2010) and Francis et al. (Citation2004) summarized previous studies and provided criteria for EQ evaluation and divided these criteria into two groups based on which basis researchers adopted to assess whether accounting profit honestly reflected the business performance of the entity if it was worthwhile. The EQ classification can be based on the following criteria:

Firstly, the accounting-based measures, including earnings management, accrual quality, earnings persistence, predictability, and smoothness, are built based on the assumption that accounting profit results from efficient cash flow allocation into the reporting periods through accrual accounting. As reported earnings reflect the actual performance of the reporting entity, a relationship will exist among earnings, cash flow, and other accounting information.

Secondly, market–based attributes are determined based on the view that earnings reflect economic profits, and that stock return reflects economic profits. This group consists of two criteria: (1) value relevance, or the extent to which reported earnings can account for the fluctuations in a company’s stock price and the return that investors receive from the company’s stocks, and (2) Timeliness, which focuses on evaluating whether losses are recognized on time and in the same period as they are incurred.

Vander Bauwhede et al. (Citation2015) used accrual accounting to measure EQ, which showed that this method measured EQ and allowed direct testing of the impact of EQ on COD. Research by Vander Bauwhede et al. (Citation2015) revealed that higher information quality would reduce information asymmetry, and banks will reward firms with higher EQ by offering lower interest rates. The results indicated that high EQs receive economic benefits, while high EQ also minimizes financial COD. Choi and Pae (Citation2011), in a study on the relationship between business ethics and financial statement quality in Korea, measured EQ in three ways: earnings management (using accrual accounting variables), prudential accounting, and the verity of accruals about future operating cash flows. The results indicated that businesses with higher commitment had higher EQ. Such firms also showed less interfered earnings management meant more consistency in financial statements and more accurate cash flow forecasts than other firms. In addition, these businesses also influenced the maintenance of EQ in the future. Schipper and Vincent (Citation2003) believed that EQ played an essential role for those individuals who used earnings data to contract and make investment decisions. In other words, EQ was a critical decision-making factor for private and institutional investors and partners in setting up contracts. Furthermore, previous research literature suggested that higher EQ helped reduce adverse selection (Lambert et al., Citation2007) and lower COD (Vander Bauwhede et al., Citation2015).

2.2. The cost of debt

The cost of debt is the portion of capital expenditure payable to external funds. This cost includes both short-term and long-term loans. In the case of a company issuing shares, this issuance cost should also be added. One of the methods adopted by professionals in the financial management industry is to calculate the capital expenditure based on a weighted average of the costs using various capital sources. In financial sponsorship, the interest rate or the cost of debt is the main economic benefit the lender can derive from the borrowing business. Lenders lend money to businesses in exchange for principal and interest, but the control of the business and the combination of shareholders and managers under the contract terms are preserved, such as covenants (Kothari et al., Citation2010). As such, lenders look for information on the earnings power of a firm, for example, its periodic business performance, as an indicator of loan repayment capacity and avoiding defaults. Debt contract theories will consider the debt interest rate as an essential mechanism in establishing a debt contract, and previous studies have shown a significant impact and trade-off between COD and debt contract terms used.

3. Literature reviews

3.1. Studying earnings quality and the cost of deb

Recently, researchers have focused on EQ concerning COD. Anderson et al. (Citation2004) collected a sample of 252 industrial companies in the period 1993 to 1998. The findings revealed that the BOD size and the complete independence of the auditors would have a positive relationship with the reliability of EQ and therefore, significantly reduce the COD. Lambert et al. (Citation2007) developed a model based on the CAPM model and showed that EQ directly impacted COD—investors’ perception of future cash flow allocation, and indirectly—decisions made by businesses on future cash flows. Given the direct influence of EQ, it is not a separate information risk factor. In other words, this influence is not diversified in large economies. The quality of accounting information, directly and indirectly, impacts the cost of debt. Results by Yee (Citation2006) noted that given uncertainty about future dividend payouts, EQ would increase the risk premium. The author also deemed that as long as there was uncertainty about portfolio diversification (future dividend payouts are uncertain) and investors were not wholly calm, limited EQ would increase equity risk premium. In a study by Kim and Qi (Citation2010) on for businesses in the US, samples were collected from January 1970 to December 2006. After examining low-priced securities, the authors concluded about EQ (using the accrual accounting model) and found a significant price impact of accrual quality on stock profit. Furthermore, the authors also revealed that the accrual quality risk insurance premium was associated with fundamental risks related to the macroeconomic conditions and business activities of enterprises.

Gao (Citation2010) found that the negative correlation between EQ and COD existed only under certain conditions. In an economy where investor competition was perfect, the author provided conditions under which the negative correlation between EQ and COD was unlikely. The quality of financial statement disclosure improved investor benefits by reducing COD. The research result by Choi and Pae (Citation2011) revealed that businesses with higher commitment would have higher EQ. Such firms also showed fewer earnings management, more consistent financial statements, and more accurate cash flow forecasts than other firms. In addition, such enterprises also impacted future financial statements’ quality. More recently, Van Caneghem and Van Campenhout (Citation2012) provided evidence revealing that financial leverage had a positive relationship with the EQ of firms. The authors used a series of EQ variables based on the auditor’s verification to test EQ’s influence on enterprises’ financial leverage.

Furthermore, studies using auditors’ confirmations—based on these samples assumed that verification from auditors would increase the information quality in the financial statements and considered issues (1) Auditor’s verification improved EQ, and (2) EQ affected debt availability and usability. The findings showed that EQ impacted enterprises’ credit access capacity, affecting the cost of debt. Vander Bauwhede et al. (Citation2015) used the accrual quality to represent the EQ of firms from 1997 to 2010 and found evidence showing that the EQ of the firm had a negative impact on the interest costs of the firms.

3.2. Studying the audit quality and the cost of debt

Previous studies have examined various aspects of the relationship between audit quality and the cost of debt (Dhaliwal et al., Citation2008; Kim et al., Citation2013; Li, Xie & Zhou, Citation2010; Pittman & Fortin, Citation2004). DeAngelo (Citation1981) defined audit quality as the probability that the auditor would detect serious material misstatement in a client’s financial statements. According to this definition, audit quality was determined by the auditor’s professional competence, independence, and other resources designed for the audit (such as the time and the audit team). DeAngelo (Citation1981) suggested that audit quality was positively related to audit firm size. Auditors of large audit firms were expected to be motivated by a more excellent reputation to maintain independence from clients. Francis and Wilson (Citation1988) argued that the audit firm’s brand is a proxy variable for audit quality. As such, previous studies on audit quality focused on examining the impacts of audit quality by comparing audits conducted by the largest audit firms (currently Big4) and those by smaller ones. These studies are usually based on a sample of listed companies, which showed that the audit performed by Big4 was indeed associated with higher audit quality. In particular, integrated studies on audit quality revealed that those audits performed by Big4 had lower litigation rates (Palmrose, Citation1988), higher audit fees (DeFond et al., Citation2000), and reduced level of earnings management through accrual accounting (Becker et al., Citation1998). Besides, they raised the likelihood of putting forth opinions of total disapproval (Francis & Krishnan, Citation1999) and provided passages that emphasized financial distress signals.

Regarding the cost of debt, Blackwell et al. (Citation1998) showed that auditing impacted the US firms’ cost of bank loans. Other related empirical studies applied indirect measurement to the cost of debt. Using data on firms in Korea, Kim et al. () extended the findings of Blackwell et al. (Citation1998) to show that audit quality through firm audit reputation had an impact on reducing the cost of borrowing. Empirical evidence from Spain indicated that the audit performed by Big4 impacted the debt valuation for firms, while the audit opinion did not have such a correlation (Cano Rodríguez et al., Citation2008). Furthermore, Illueca Muñoz and Gill-de-Albornoz (Citation2006) suggested a negative relationship existed between accrual quality and the cost of debt based on a sample of Spanish firms audited by an audit firm Big4, the findings of which indicated the audits of listed companies. Clients of Big4 auditors had larger stock trading volumes offered in the initial public offerings (IPOs; Jang & Lin, Citation1993) and higher earnings ratios (Teoh & Wong, Citation1993).

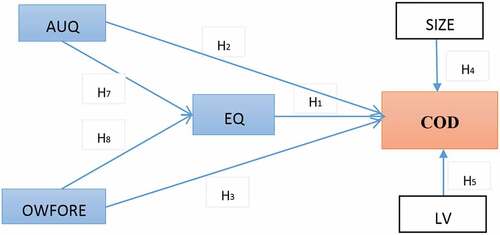

4. The model

4.1. Earnings quality

To measure earnings quality, we follow the approach of McNichols (Citation2002) which was developed based on the model of Dechow and Dichev (Citation2002). This measure takes into account the change of revenue (∆REV), property, plant, and equipment (PPE).

where is the accrued working capital of enterprise i in year t, calculated by the change in current assets (∆CA) minus the change in cash and cash equivalents (∆Cash), minus the change in short-term debt (∆CL) and plus the change in short-term bank debt (∆Debt).

WCA = ∆CA—∆CL—∆Cash + ∆Debt

are the operating cash flows in year t-1, year t and year t + 1, respectively. All variables are divided by total assets (Ait −Total assets); ΔREVit is the change in receivables of the company i in year t; PPEit is the fixed asset cost of the company i in year t. All variables in Equation (1) are summarized in Table A1 (Appendix).

To estimate the quality of accruals, we used a model developed by McNichols (Citation2002), which represented the quality of accruals as working capital accruals regressed on operating cash flows for the previous year, current year, and the immediately following year, the difference between receivables and fixed assets, all divided by total assets at the beginning of the period. To measure EQ, an AQ variable was generated as the negative standard deviation of residual εi,t of Equationequation (1)(1)

(1) after performing the regression.

A higher accrual quality (AQ) value indicates poorer accumulation quality as cash flow performance accounts for minor variation in current accruals. Since earnings are the sum of accruals and cash flows, and the cash flow component is generally considered objective and unmanipulated, EQ depends on the quality of the accruals. Therefore, poorer accrual quality implies lower EQ. Variable EQ is measured by accrual quality EQ = AQ*(−1).

4.2. Earnings quality and the cost of debt

Based on the study overview, we have established the model as follows:

Model 1:

4.2.1. The cost of debt (COD)

When examining the cost of debt, each study had a different way of measuring it. Borisova and Megginson (Citation2011) and Borisova et al. (Citation2015) determined the cost of debt based on the yield variance between corporate and government bonds with respective maturities. The above measurement suits developed countries with long-standing corporate bond markets and strong business capital mobilization channels. However, this measurement becomes difficult to implement in emerging markets, where loans are mainly through banks (Shailer & Wang, Citation2015). In order to standardize the distribution of interest expenses and fit the characteristics of bank financing in emerging markets, Shailer and Wang (Citation2015), Bliss and Gul (Citation2012), Francis et al. (Citation2005), and Gray et al. (Citation2009) calculated the cost of debt as the logarithm of the ratio between interest expense and total current liability plus long-term liability. Stanišić et al. (Citation2016), and Francis et al. (Citation2005) measured the cost of debt differently. Previously, the capital expenditure was determined based on the pre-tax interest expense via the formula of total interest expense divided by the average of interest-bearing liabilities for the year. In this study, we measure the cost of debt according to Stanišić et al. (Citation2016), Francis et al. (Citation2005), Persakis and Iatridis (Citation2015), and Pittman and Fortin (Citation2004) to fit the debt characteristics of Vietnamese enterprises (COD = Interest expense/ (Interest-bearing long-term liability + Interest-bearing current liability).

4.2.2. Earnings quality (EQ)

Based on the studies by Anderson et al. (Citation2004), Yee (Citation2006), Lambert et al. (Citation2007), Kim and Qi (Citation2010), Gao (Citation2010), Choi and Pae (Citation2011), and Vander Bauwhede et al. (Citation2015), and Hung and Van (Citation2020), and Dang and Tran (Citation2020), and Dang et al. (Citation2020), Dang et al. (Citation2021), high-quality information facilitated transparency, which would help reduce the problem of information asymmetry and satisfy the requirements set by investors and shareholders. A series of advantages of providing high-quality information were mentioned by researchers; improving EQ would reduce information and liquidity risks, restrict managers from using their rights for the purposes of their own interests, enable them to make more effective investment decisions. The enhancement of EQ required firms to provide more information with improved information quality, in order to ensure that market participants have adequate information to make investment and credit decisions. The authors also concluded that the higher EQ means more likelihood to ease the problem of information asymmetry between firms and creditors.

Therefore, we form the following hypothesis:

H1: Earnings quality has a negative relationship with the cost of debt.

In Model 1, we add the control variables which are firm size (SIZE) and financial leverage (LEV). Firm size (SIZE) is measured by the logarithm of total assets and financial leverage (LV) equals to liabilities to equity. We also use dummies to represent industry-specific characteristics.

4.2.2.1. Size

Size can allow lenders to calculate the value of a company’s market power, indirectly estimating its bankruptcy risk. The more significant assets, earnings, revenue, or number of employees means the greater financial autonomy of the company; therefore, such companies tend to diversify their business activities more, and the result obtained is lower risk and less likely bankruptcy. Large firms tend to use long-term debt, while small ones choose to access short-term loans. Large firms often have economies of scale (Berger & Udell, Citation2006) in accessing long-term debts and even have the capacity to negotiate with banks and creditors about loan terms, preferential interest rates and credit limits. Moreover, large firms tend to diversify their businesses and own more stable cash flows; therefore, the risk of bankruptcy for large firms is relatively lower than that of smaller ones. This suggests that size has a negative relationship with COD. Information asymmetry theory also explains the negative relationship between size and COD. Thus, this implies that the relationship between size and COD is negative. We hypothesize:

H2: Size has a negative relationship with the cost of debt.

4.2.2.2. LV

The positive relationship between financial leverage and COD was found in previous studies (Berger & Udell, Citation2006; Pittman & Fortin, Citation2004), and this reflects the fact that the higher financial leverage of the company means more risk that the company is facing. Therefore, a positive relationship between leverage and COD is expected. Moreover, the trade-off theory also suggests a positive relationship between COD and financial leverage. This theory argues that firms with higher levels of financial leverage will face higher costs of financial distress, which leads to bankruptcy. If the company is aware of the existing risk, for whatever reason, the lender will have to ask for a higher interest rate on the loan to offset the risks that the company is facing. Previous studies suggest that financial leverage is measured by the debt ratio to the company’s total assets. We suggest the following hypothesis:

H3: Leverage has a positive relationship with the cost of debt.

4.3. Audit quality, foreign ownership and cost of debt

Model 2:

4.3.1. Audit quality (AUQ)

Recent studies showed that Big4 audit firm was related to reducing the cost of borrowing in US-listed companies (Kim et al., ; Pittman & Fortin, Citation2004). Using an indirect measure of the cost of debt, Pittman and Fortin (Citation2004) found a lower cost of debt for newly listed US firms audited by Big4. Similarly, Kim et al. () indicated that those companies audited by Big4 had lower interest rates on bank loans than those audited by nonBig4 firms. Mansi et al. (Citation2004) argued that the audit performed by Big4 was related to falling bond yields and high risks. However, Piot and Missonier-Piera (Citation2007) adopted an indirect measure of the cost of debt yet found no empirical evidence for the influence of Big4 audits in the context of French listed companies. In this study, we measured audit quality (AUQ) through audited financial statements as a Big4 company. For those enterprises audited by Big4 company, the audit quality (AUQ) is equal to 1; the rest will be 0.

Audit quality impacts debt performance by increasing the reliability of financial information, thereby reducing information asymmetry and past debt monitoring costs for lenders (Jensen & Meckling, Citation1976; Kim et al., ; Watts & Zimmerman, Citation1986). In other words, financial information’s reliability reduced banks’ need to rely on alternative information in debt contracts. We built up the following hypothesis:

H4: Audit quality has a negative relationship with the cost of debt

4.3.2. Foreign ownership (OWFORE)

When studying medium-sized manufacturing enterprises in the US, Rahaman and Al Zaman (Citation2013) found that foreign-owned enterprises often had better operational management and more transparent disclosure of information than other types of business ownership; therefore, the cost of debt of foreign-owned enterprises is lower. In addition, foreign-owned firms were more reputable in borrowing, so they often attracted sources of capital with a low cost of debt (Boubakri et al., Citation2013). The findings of Stanišić et al. (Citation2016) for 4710 Serbian enterprises from 2008 to 2013 also showed that increased foreign ownership in enterprises would help reduce the cost of debt. In Vietnam, the wave of foreign investment in domestic enterprises has increased since the introduction of the stock market. Vietnamese enterprises attracted foreign investment to improve management practices to reduce operating costs, including the cost of debt. So, do foreign-owned enterprises reduce the cost of debt for firms? We built up the following hypothesis:

H5: Foreign ownership has a negative relationship with the cost of debt

4.4. Financial distress, earnings quality, and cost of debt

Model 3:

Financial distress refers to a company’s difficulty paying in its debts or meeting other financial obligations (Ghazali et al., Citation2015). In the event of severe financial distress, the company might go bankrupt. Binti and Ameer (Citation2010) defined financial distress as a term used to designate a situation when contractual arrangements with creditors could not be fulfilled due to a company’s financial difficulties. Recently, many studies have demonstrated that managers of those companies in a period of financial distress tend to adjust the recognition of revenue, expenses, liabilities, and receivables. In other words, they have a motive for earnings management and reduce their earnings quality. The purpose of earnings management here may be to cover up the financial distress to mobilize additional sources of funding, thereby reducing the likelihood of bankruptcy (Rosner, Citation2003). Rogers and Stocken (Citation2005) argued that managers were generally worried about losing their jobs if the company went into financial distress; therefore, they managed earnings to provide optimistic forecasts, thereby promising to restore financial status to ensure their job, salary and reputation. In addition, via earnings management, companies could also avoid breaches of contractual terms with related parties when the company falls into financial distress (Dechow & Dichev, Citation2002). As such, we continue to develop a model that considered the impact of EQ when combined with financial distress on COD. We built up the following hypothesis:

H6: Earnings quality interacting with financial distress has a positive relationship with the cost of debt.

Currently, there are many ways to measure financial distress; however, each measure has its advantages and disadvantages. Ghazali et al. (Citation2015) stated that Altman Z-Score could be considered the most popular method to measure the financial status of a company and was used to determine financial distress in various studies. Thus, in this study, we define financial distress based on the Z-index (Altman, Citation1968). Altman’s Z-Index provided a calculation of the Z-index based on the following formula:

Where X1 is current assets minus current liabilities divided by total assets; X2 is retained profit divided by total assets; X3 is profit before tax and interest divided by total assets; X4 is book value of equity divided by total liability and X5 is revenue divided by total assets. All variables in Equation (5) are summarized in (Appendix).

If the Z index < 1.81, the company is in financial distress, and the financial distress variable will have a value of 1; otherwise, it will have a value of 0.

4.5. Earnings quality as an intermediary and the cost of debt

Persakis and Iatridis (Citation2015) examined the impact of earnings quality and audit quality on the cost of equity and debt under the influence of the 2008 financial crisis. Leuz (Citation2010) used linear regression analysis, in which 137,091 observations of businesses from 18 countries worldwide were classified into three study groups according to the level of investor protection based on country classification.Footnote1 The findings showed that the 2008 global financial crisis positively impacted the cost of debt for groups 1 and 2. Those firms audited by Big4 auditors in group 1 had a negative relationship with the cost of debt.

In Vietnam, the financial statements of listed companies are all audited. Therefore, audited financial information can be a reliable source of information in a contract. As such, banks may need less reliance on alternative information sources when assessing the credit risk of borrowers and monitoring old debt contracts, leading to more effectiveness in monitoring debt contracts based on accounting information and establishing the monitoring mechanism. Consistent with this view, Niskanen and Niskanen (Citation2004) argued that corporate debt covenants in Finland aimed at protecting interests against the discretion of the bank managers. Therefore, the information quality of financial statements can be of great importance in valuing debt for listed companies in Vietnam. In this study, we investigate how the EQ factor as an intermediate variable of audit quality and foreign ownership will affect costs in Vietnam. Model 4:

The quality of audit activities has a positive impact on the transparency and reliability of financial statements. Although there are various criteria for quantifying the audit quality, the fact that Big4 audits financial statements is considered a commitment to its conformity with accounting practices. Previous studies (Becker et al., Citation1998; Francis & Yu, Citation2009; Krishnan, Citation2003) proved that financial statements audited by auditors under the Big 4 group had lower earnings management than those audited by non-Big4. Thus, it is hypothesized that the company audited by the auditor of higher quality (Big4) has higher earnings quality than the one audited by the auditor in the other company (non-Big4). Based on the above arguments and studies, we develop the following hypothesis:

H7: Audit quality has a positive relationship with earnings quality, and earnings quality has a negative relationship with the cost of debt.

The foreign ownership ratio represents the ownership structure of the organization. According to Widigdo (Citation2013), the foreign ownership ratio, the percentage of shares held by foreign investors, was considered to have a positive meaning in creating an excellent governance mechanism. Foreign investors had various skills in detecting fraud in the company and were not easily deceived by the company’s management board, thereby limiting earnings management practices. Sharma (Citation2004) found that as the percentage of independent foreign ownership increased, there would be a decrease in the likelihood of fraudulent financial information. These findings suggested that foreign institutional investors could actively monitor and control financial statements, reduce management board fraud, and promote more honest managerial disclosure of financial information. Therefore, the hypothesis related to the foreign ownership ratio is given as follows:

H8: Foreign ownership has a positive relationship with earnings quality, and earnings quality has a negative relationship with the cost of debt.

All of our models and hypotheses are summarized in .

Figure 1. Influence of GC, EQ on FV.

4.6. Research data and samples

This study uses data collected from the Vietnamese stock exchange from 2010 to 2019. These data are collected from audited financial statements of listed companies after excluding those in the banking, securities, and insurance sector. The final dataset consists of 3,800 observations presented in Table by year and industry. We first test for autocorrelation and variable variance. The model test results show that the received P-values are equal to 0.000 < α (5%). This implies that the null hypothesis in the models is rejected at the 5% significance level. Therefore, we proceed to overcome the defects of the regression model by the Robust testing and industry fixed effects regression method.

Table 1. Statistics of research samples

5. Results and discussion

Statistical data in Table shows that the average COD was 7.9%, the highest is 38.6%, and the standard deviation is 5.6%. EQ has a mean value of −0.017, a minimum of 0.102, and the highest of 0.000, a standard deviation of 0.017. The rate of foreign ownership (OWFORE) accounts for 9.4% on average, and the standard deviation of 13.4%. The size is measured as the logarithm of the total assets of the average 27,388; financial leverage (LV) accounts for 53.6%. Out of 3800 observations in our sample, the number of Big Four audit firms was 1078, accounting for 28.37%.

Table 2. Descriptive statistics Std

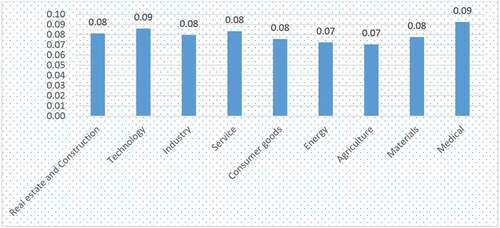

Figure reveals that COD is at a high level in 2011–2012 and tends to decrease, while in 2015–2017, it remains at around 6%. The lowest cost of debt is in 2016, at 6.2%, and increases slightly to 6.8% in the period 2018–2019. Further examining the cost of debt across the industry (Figure ), we find that firms in the agricultural sector has the lowest cost of debt at 7.1%, while the highest is from the healthcare businesses, with the average cost of debt at 9.3%.

Figure 2. Variable cost of debt over the years.

Figure 3. Variable cost of debt across industries.

Table shows descriptive statistics of the difference between the cost of debt at various quantiles. At the lowest quantile (Q1), the cost of debt is 2%, whereas at the Q5 quantile (the highest), this is 17%. The result of test on the difference in the cost of debt at the lowest and highest quantile is different and statistically significant.

Table 3. Descriptive statistics

Table provides the correlation coefficient results among variables. Testing the correlation between independent and dependent variables is to eliminate factors that could lead to multicollinearity before running the regression model. The correlation coefficient among the independent variables in the model has been no greater than 0.8; therefore, multicollinearity does not exist. After performing descriptive statistics and correlation matrix analysis, we estimate the model using least squares regression. The cost of debt has a negative relationship with the independent variables in the model and is statistically significant.

Table 4. Correlation matrix

The results in Table indicate that EQ shows a negative relationship with COD with 1% statistical significance. This result suggests that higher EQ meant a lower COD. This finding is consistent with the hypothesis H1 we built initially. This study also agrees with the findings of Carmo et al. (Citation2016), Beltrame et al. (Citation2017), Orazalin and Akhmetzhanov (Citation2019), and Houcine and Houcine (Citation2020), and Le et al. (Citation2021).

Table 5. Results of multivariate regression of model 1

Similar to the impact of EQ on COD, size also has a negative impact on COD at 1% significance. These finding reveals that the larger the size the lower COD. This finding is consistent with the empirical evidence found in previous studies (Berger & Udell, Citation2006) and the hypothesis H2 we established initially. The reason is that large firms will encounter lower information asymmetry than small ones, and concurrently, such firms have a pretty low degree of cash flow volatility and tend to diversify their businesses; therefore, they can negotiate lower lending rates. In other words, the COD of large companies will be relatively lower than that of small ones. When the firm uses high financial leverage, the cost of debt will also decrease with a statistical significance of 1%, which is contrary to hypothesis H3, and the previous empirical evidence by Berger and Udell (Citation2006) and Pittman and Fortin (Citation2004). However, our finding is consistent with the finding of Yen et al. (Citation2018) in the context of Vietnam where the most businesses used limited loans.

The results from Table indicates that audit quality (AQ) impacted the cost of debt at a 1% statistical significance. According to the findings, audit quality has a positive relationship with the cost of debt; that is, audit quality impacts debt valuation. The audit quality’s impact on the cost of debt is not consistent with the developed hypothesis H4 and is in contrast to previous empirical evidence from Spain and Korea (Illueca Muñoz & Gill-de-Albornoz, Citation2006; Kim et al.,). However, our findings agree with empirical evidence from the US (Fortin & Pittman, Citation2007).

Table 6. Results of multivariate regression of model 2

According to Common Law, legal systems in developed countries prioritize investor protection at a higher level, the results of which imply that the role of management or signals from audits by those audits companies under Big4 is even more important in civil law environments with lower investor protection (Porta et al., Citation1998). Empirical evidence from the United States is limited to the specific context of bond prices (Fortin & Pittman, Citation2007) as investors can rely on supervisory practice; therefore, the supervisory role of the audit firm may be less important in this context and possibly suitable for Vietnam. In Vietnam, the audit firm’s reputation has not been rated reliable. Based on the above arguments, the findings of this study indicate that the audit quality expressed through the audit firm’s reputation has not contributed to the financial information of the listed companies evaluated by lending institutions.

To better understand why we obtained different results than hypothesis H4, we compare and test the difference between the cost of debt of two groups, i.e., the group of Big Four audit firms and the other group. Table reveals a difference between earnings quality and the cost of debt, and that the Big Four audit firms have lower debt expenditure than non-Big Four audit firms. Therefore, the cost of debt of Non—Big Four audit firms is higher, leading to a higher financial risk. Besides, the earnings quality of Big Four audit firms is lower and of statistical significance; therefore, the financial statement quality of this group is of more excellent reliability.

Table 7. Testing results

Also, according to Table , the finding shows that the foreign ownership ratio (OWFORE) has a negative relationship with the cost of debt. In terms of corporate governance, increasing foreign ownership will reduce the cost of debt for businesses. These findings are of 1% statistical significance. The higher foreign ownership means more openness and transparency about their governance structure, production and business activities. Thereby, the risk of information asymmetry for creditors is minimized. As such, these firms also receive a lower cost of debt.

Table indicates the research findings of model 3, which examined the impact of earnings quality on financially distressed firms. The variable of financial distress is measured through the Z-index and had a value of 1 if Z < 1.81; otherwise, it would have a value of 0. The results reveal that earnings quality under financial distress (EQ*FD) positively correlates with the cost of debt. As such, under financial distress, the earnings quality positively relates to the cost of debt, whereas considering the entire research sample, earnings quality negatively relates to the cost of debt. Dutzi and Rausch (Citation2016) and Xu and Ji (Citation2016) argued that financially distressed firms tended to conduct earnings management in response to poor financial performance. Under financial distress, managers tended to conduct earnings management to express that the company was still meeting its creditor obligations, to avoid increasing the cost of debt, and thus, maximize its benefits (Moreira & Pope, Citation2007). Ghazali et al. (Citation2015) argued that the pressure from financial distress could be detrimental to the company, whereby investors and creditors could suffer significant losses. If the company went into financial distress, managers could expect their bonuses to be cut down and the possibility of replacement and damages to their careers and reputations. As such, conservative managers would take advantage of the opportunity to cover up financial distress by choosing various accounting methods that increase earnings and mask losses (Habib et al., Citation2013), with a view to reducing the cost of debt.

Table 8. Results of multivariate regression of model 3

For a comprehensive view of control variables of firm size and financial leverage, we divide the research samples into two groups. Based on the median value of the firm size variable, the sample is divided into small and large firms together with financial leverage into low and high-leverage groups. The research findings in Table show that earnings quality has a negative impact on the cost of debt at 1% statistical significance, whether the firm is under the small or large group, with high or low financial leverage. Large-scale enterprises have a more significant influence coefficient than small-scale ones, and low leverage firms had a higher regression coefficient than high-leverage ones. Besides, audit quality only positively influences the small group and the low financial leverage ones and vice versa.

Table 9. Regression results

Based on the regression results according to the SEM structural model in Table (SEM structural model is illustrated in and Table ), the finding suggests that the audit quality factor (AUQ) poses a direct effect on the cost of debt, and concurrently, the audit quality also had a negative impact on the intermediate variable, earnings quality. This finding is consistent with the established hypothesis H7 and agrees with the research findings of (Becker et al., Citation1998), (J. R. Francis & Yu, Citation2009), (Krishnan, Citation2003). Meanwhile, the foreign ownership variable (OWFORE) only directly affects the cost of debt but does not impact the intermediate variable, earnings quality. This is inconsistent with the developed hypothesis H8 and does not agree with the research findings of Sharma (Citation2004). As an intermediate variable of audit quality and foreign ownership ratio, earnings quality (EQ) negatively impacts the cost of debt at a 1% significance level.

Table 10. Results of multivariate regression according to SEM model

All of the testing results of the model’s indexes (Table ) satisfies the criteria of the estimation model as qualified with the explanatory level of earnings quality factors as an intermediate variable affecting the cost of debt as well as the interpretation of factors affecting the cost of debt at the level of as low as 8%.

Table 11. Testing according to SEM model fit indexes standard model testing

6. Conclusion and recommendations

Using the OLS estimation method and the data of 3800 observations of listed companies in 2010–2019, we find empirical evidence that firms of high EQ would reduce their own COD. Simultaneously, the study also identifies evidence for the relationship between COD and factors of audit quality and foreign ownership ratio. Besides, the study also states that upon the impact of EQ when interacting with financial distress, earnings quality has a positive relationship with COD.

Besides the obtained results, the study also shows some limitations: Firstly, the impact of earnings quality on the cost of debt is possibly influenced by endogenous variables; however, this has not been addressed in the research. Second, the study analyzes listed companies from a developing country like Vietnam; since the audit environment varies from country to country, these findings may not be generalizable to other countries in the region. Finally, the explanatory level in the model is low. For future studies, it will be necessary to extend other measures of earnings quality on the cost of debt and compare with countries in the ASEAN region and worldwide.

Along with the above research findings, financial statement information plays an important role, and financial statement information audited by large audit firms always provides the basis for investors and bank analyses. However, financial statement information will be of no meaning without the trust of investors and banks. It lays the foundation and driving force for the development of the stock market, especially in young markets like Vietnam’s stock market. From the obtained results, we put forth some recommendations as follows:

Firstly, the managers of enterprises should consider improving their units’ EQ so they can reduce their COD and indirectly facilitate their businesses to improve their performance. To do this, managers and shareholders (who own capital) must be more prudent in choosing independent audit firms to audit their financial statements. Enterprises need to pay attention to several issues about financial statement disclosure, such as timing, the quality of financial statement information, and the selection of an audit firm.

Secondly, the research findings suggested that Vietnamese firms with high foreign ownership or large scale often had a low cost of debt. Therefore, listed companies should maintain foreign ownership ratio and attract foreign investors strategically and at a high concentration level, enabling companies to mobilize debt financing at a low cost. In addition, the capacity to pay interest well and use high financial leverage also facilitates firms to save on the cost of debt. However, firms also need to be aware that increasing lending interest rates will pressure the additional cost of debt. Therefore, firms need to be cautious before deciding to increase the debt ratio in the capital structure and closely monitor the fluctuation of lending interest rates in the market to maintain a reasonable debt cost.

Thirdly, firms can also choose a strategy to negotiate their COD with creditors in favor of the business. Firms may consider issuing bonds instead of borrowing from banks. Finally, the most practical thing is that firms should consider reducing their leverage ratio to the possible extent to minimize the COD they are approaching.

Fourthly, the common goal of regulators is to stabilize and develop the stock market. This is reflected in the management to increase investment efficiency; attract investors and increase market liquidity; manage transparency issues such as audit quality, time to publish audit reports, controlling negative behaviors to increase market efficiency.

Acknowledgements

The article came into being within the project no. CBQT2.2020.29/QD-DHKTQD, financed by National Economics University, 2020.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Van Vu Thi Thuy

Van Vu Thi Thuy is a lecturer at the School of Banking and Finance, National Economics University, Vietnam. Her works focus on corporate finance and the stock market.

Hung Dang Ngoc

Hung Dang Ngoc is an associate professor at Hanoi University of Industry and a Ph.D. since 2011. He teaches and researches accounting and finance.

Tram Nguyen Ngoc

Tram Nguyen Ngoc is a lecturer and research student at the National Economics University. She teaches and researches corporate finance and the stock market.

Hoang Anh Le

Hoang Anh Le is a lecturer and research student at the National Economics University. He teaches and researches corporate finance and the stock market

Notes

1. Three groups include: Group 1—developed countries, with a priority legal system to protect investors and shareholders (Australia, Ireland, UK); Group 2- countries with moderate investor protection (Austria, Belgium, Denmark, Finland, France, Germany, Netherlands, Norway, Spain, Sweden, Switzerland); and Group 3—countries with low levels of investor protection legislation (Greece, Italy, Portugal).

References

- Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. The Journal of Finance, 23(4), 589–22. https://doi.org/10.2307/2978933

- Anderson, R. C., Mansi, S. A., & Reeb, D. M. (2004). Board characteristics, accounting report integrity, and the cost of debt. Journal of Accounting and Economics, 37(3), 315–342. https://doi.org/10.1016/j.jacceco.2004.01.004

- Becker, C. L., DeFond, M. L., Jiambalvo, J., & Subramanyam, K. (1998). The effect of audit quality on earnings management. Contemporary Accounting Research, 15(1), 1–24. https://doi.org/10.1111/j.1911-3846.1998.tb00547.x

- Beltrame, F., Floreani, J., & Sclip, A. 2017. Earnings quality and the cost of debt of SMEs. In Financial Markets, SME Financing and Emerging Economies. Palgrave Macmillan Studies in Banking and Financial Institutions. G. Chesini, E. Giaretta, & A. Paltrinieri, Eds. Palgrave Macmillan, Cham 21–39. https://doi.org/10.1007/978-3-319-54891-3_3

- Beneish, M. D., & Vargus, M. E. (2002). Insider trading, earnings quality, and accrual mispricing. The Accounting Review, 77(4), 755–791. https://doi.org/10.2308/accr.2002.77.4.755

- Berger, A. N., & Udell, G. F. (2006). A more complete conceptual framework for SME finance. Journal of Banking & Finance, 30(11), 2945–2966. https://doi.org/10.1016/j.jbankfin.2006.05.008

- Binti, S., & Ameer, R. (2010). Turnaround prediction of distressed companies: Evidence from Malaysia. Journal of Financial Reporting and Accounting, 8(2), 143–149. https://doi.org/10.1108/19852511011088398

- Blackwell, D. W., Noland, T. R., & Winters, D. B. (1998). The value of auditor assurance: Evidence from loan pricing. Journal of Accounting Research, 36(1), 57–70. https://doi.org/10.2307/2491320

- Bliss, M. A., & Gul, F. A. (2012). Political connection and cost of debt: Some Malaysian evidence. Journal of Banking & Finance, 36(5), 1520–1527. https://doi.org/10.1016/j.jbankfin.2011.12.011

- Borisova, G., Fotak, V., Holland, K., & Megginson, W. L. (2015). Government ownership and the cost of debt: Evidence from government investments in publicly traded firms. Journal of Financial Economics, 118(1), 168–191. https://doi.org/10.1016/j.jfineco.2015.06.011

- Borisova, G., & Megginson, W. L. (2011). Does government ownership affect the cost of debt? Evidence from privatization. The Review of Financial Studies, 24(8), 2693–2737. https://doi.org/10.1093/rfs/hhq154

- Boubakri, N., Cosset, J.-C., & Saffar, W. (2013). The role of state and foreign owners in corporate risk-taking: Evidence from privatization. Journal of Financial Economics, 108(3), 641–658. https://doi.org/10.1016/j.jfineco.2012.12.007

- Cano Rodríguez, M., Sánchez Alegría, S., & Torres, P. A. (2008). Do banks value audit reports or auditor reputation? Evidence from private Spanish firms. Working paper, University of Jaén and Public University of Navarra.

- Carmo, C. R., Moreira, J. A. C., & Miranda, M. C. S. (2016). Earnings quality and cost of debt: Evidence from Portuguese private companies. Journal of Financial Reporting and Accounting, 14(2), 178–197. https://doi.org/10.1108/JFRA-08-2014-0065

- Choi, T. H., & Pae, J. (2011). Business ethics and financial reporting quality: Evidence from Korea. Journal of Business Ethics, 103(3), 403–427. https://doi.org/10.1007/s10551-0110871-4

- Dang, H. N., Hoang, K., Vu, V. T. T., & Van Nguyen, L. (2021). Do socially responsible firms always disclose high-quality earnings? Evidence from an emerging socialist economy. Asian Review of Accounting, 29(3), 291–306. https://doi.org/10.1108/ARA-11-2020-0174

- Dang, N. H., & Tran, M. D. (2020). Impact of financial leverage on accounting conservatism application: The case of Vietnam. Custos E Agronegocio Online, 16(3), 137–158. http://www.custoseagronegocioonline.com.br/numero3v16/OK%207%20leverage.pdf

- Dang, H. N., Vu, V. T. T., Ngo, X. T., & Hoang, H. T. V. (2020). Impact of dividend policy on corporate value: Experiment in Vietnam. International Journal of Finance & Economics, 26(4), 5815–5825. https://doi.org/10.1002/ijfe.2095

- DeAngelo, L. E. (1981). Auditor size and audit quality. Journal of Accounting and Economics, 3(3), 183–199. https://doi.org/10.1016/0165-4101(81)90002-1

- Dechow, P. M., & Dichev, I. D. (2002). The quality of accruals and earnings: The role of accrual estimation errors. The Accounting Review, 77(s–1), 35–59. https://doi.org/10.2308/accr.2002.77.s-1.35

- Dechow, P., Ge, W., & Schrand, C. (2010). Understanding earnings quality: A review of the proxies, their determinants and their consequences. Journal of Accounting and Economics, 50(2–3), 344–401. https://doi.org/10.1016/j.jacceco.2010.09.001

- DeFond, M. L., Francis, J. R., & Wong, T. J. (2000). Auditor industry specialization and market segmentation: Evidence from Hong Kong. Auditing: A Journal of Practice & Theory, 19(1), 49–66. https://doi.org/10.2308/aud.2000.19.1.49

- Dhaliwal, D. S., Gleason, C. A., Heitzman, S., & Melendrez, K. D. (2008). Auditor fees and cost of debt. Journal of Accounting, Auditing & Finance, 23(1), 1–22. https://doi.org/10.1177/0148558X0802300103

- Dutzi, A., & Rausch, B. (2016). Earnings management before bankruptcy: A review of the literature. Journal of Accounting and Auditing: Research & Practice, 2016(2016), 1–21. https://doi.org/10.5171/2016.245891

- Fortin, S., & Pittman, J. A. (2007). The role of auditor choice in debt pricing in private firms. Contemporary Accounting Research, 24(3), 859–896. https://doi.org/10.1506/car.24.3.8

- Francis, J. R., & Krishnan, J. (1999). Accounting accruals and auditor reporting conservatism. Contemporary Accounting Research, 16(1), 135–165. https://doi.org/10.1111/j.1911-3846.1999.tb00577.x

- Francis, J., LaFond, R., Olsson, P. M., & Schipper, K. (2004). Costs of equity and earnings attributes. The Accounting Review, 79(4), 967–1010. https://doi.org/10.2308/accr.2004.79.4.967

- Francis, J., LaFond, R., Olsson, P., & Schipper, K. (2005). The market pricing of accruals quality. Journal of Accounting and Economics, 39(2), 295–327. https://doi.org/10.1016/j.jacceco.2004.06.003

- Francis, J. R., & Wilson, E. R. (1988). Auditor changes: A joint test of theories relating to agency costs and auditor differentiation. Accounting Review, 663–682. https://www.jstor.org/stable/247906

- Francis, J. R., & Yu, M. D. (2009). Big 4 office size and audit quality. The Accounting Review, 84(5), 1521–1552. https://doi.org/10.2308/accr.2009.84.5.1521

- Gao, P. (2010). Disclosure quality, cost of capital, and investor welfare. The Accounting Review, 85(1), 1–29. https://doi.org/10.2308/accr.2010.85.1.1

- Ghazali, A. W., Shafie, N. A., & Sanusi, Z. M. (2015). Earnings management: An analysis of opportunistic behaviour, monitoring mechanism and financial distress. Procedia Economics and Finance, 28, 190–201. https://doi.org/10.1016/S2212-5671(15)01100-4

- Gray, P., Koh, P. S., & Tong, Y. H. (2009). Accruals quality, information risk and cost of capital: Evidence from Australia. Journal of Business Finance & Accounting, 36(1 2), 51–72. https://doi.org/10.1111/j.1468-5957.2008.02118.x

- Habib, A., Bhuiyan, B. U., & Islam, A. (2013). Financial distress, earnings management and market pricing of accruals during the global financial crisis. Managerial Finance, 39(2), 155–180. https://doi.org/10.1108/03074351311294007

- Houcine, A., & Houcine, W. (2020). Does earnings quality affect the cost of debt in a banking system? Evidence from French listed companies. Journal of General Management, 45(4), 183–191. https://doi.org/10.1177/0306307020916296

- Hung, D. N., & Van, V. T. T. (2020). Researching the firm characteristics affecting the earnings quality: The case of Vietnam. Calitatea, 21(179), 106–112. https://www.proquest.com/openview/1b126abfb6f417d27b6f8dacc2749801/1?pqorigsite=gscholar&cbl=1046413

- Illueca Muñoz, M., & Gill-de-Albornoz, B. (2006). The effect of auditor reputation on the pricing of accruals: Evidence from privately held companies. http://dx.doi.org/10.2139/ssrn.908813

- Jang, H.-Y. J., & Lin, C.-J. (1993). Audit quality and trading volume reaction: A study of initial public offering of stocks. Journal of Accounting and Public Policy, 12(3), 263–287. https://doi.org/10.1016/0278-4254(93)90030-F

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Kim, D., & Qi, Y. (2010). Accruals quality, stock returns, and macroeconomic conditions. The Accounting Review, 85(3), 937–978. https://doi.org/10.2308/accr.2010.85.3.937

- Kim, J.-B., song, B. Y., & Tsui, J. S. (2013). Auditor size, tenure, and bank loan pricing. Review of Quantitative Finance and Accounting, 40(1), 75–99. https://doi.org/10.1007/s11156-011-0270-z

- Kothari, S., Ramanna, K., & Skinner, D. J. (2010). Implications for GAAP from an analysis of positive research in accounting. Journal of Accounting and Economics, 50(2–3), 246286. https://doi.org/10.1016/j.jacceco.2010.09.003

- Krishnan, G. V. (2003). Audit quality and the pricing of discretionary accruals. Auditing: A Journal of Practice & Theory, 22(1), 109–126. https://doi.org/10.2308/aud.2003.22.1.109

- Lambert, R., Leuz, C., & Verrecchia, R. E. (2007). Accounting information, disclosure, and the cost of capital. Journal of Accounting Research, 45(2), 385–420. https://doi.org/10.1111/j.1475-679X.2007.00238.x

- Leuz, C. (2010). Different approaches to corporate reporting regulation: How jurisdictions differ and why. Accounting and Business Research, 40(3), 229–256. https://doi.org/10.1080/00014788.2010.9663398

- Le, H. T. T., Vo, X. V., & Vo, T. T. (2021). Accruals quality and the cost of debt: Evidence from Vietnam. International Review of Financial Analysis, 76, 101726. https://doi.org/10.1016/j.irfa.2021.101726

- Li, C., Xie, Y., & Zhou, J. (2010). National level, city level auditor industry specialization and cost of debt. Accounting Horizons, 24(3), 395–417. https://doi.org/10.2308/acch.2010.24.3.395

- Mansi, S. A., Maxwell, W. F., & Miller, D. P. (2004). Does auditor quality and tenure matter to investors? Evidence from the bond market. Journal of Accounting Research, 42(4), 755–793. https://doi.org/10.1111/j.1475-679X.2004.00156.x

- McNichols, M. F. (2002). Discussion of the quality of accruals and earnings: The role of accruals estimation errors. The Accounting Review, 77(1), 61–69. https://doi.org/10.2308/accr.2002.77.s-1.61

- Moreira, J., & Pope, P. F. (2007). Earnings management to avoid losses: A cost of debt explanation. Research Center on Industrial, Labour and Managerial Economics, Papers 0704. https://core.ac.uk/download/pdf/6379127.pdf

- Niskanen, J., & Niskanen, M. (2004). Covenants and small business lending: The Finnish case. Small Business Economics, 23(2), 137–149. https://doi.org/10.1023/B:SBEJ.0000027666.84118.a7

- Orazalin, N., & Akhmetzhanov, R. (2019). Earnings management, audit quality, and cost of debt: evidence from a central Asian economy. Managerial Auditing Journal, 34(6), 696–721. https://doi.org/10.1108/MAJ-12-2017-1730

- Palmrose, Z.-V. (1988). 1987 competitive manuscript co-winner: An analysis of auditor litigation and audit service quality. Accounting Review, 36(1), 55–73. https://www.jstor.org/stable/247679

- Penman, S. H., & Zhang, X.-J. (2002). Accounting conservatism, the quality of earnings, and stock returns. The Accounting Review, 77(2), 237–264. https://doi.org/10.2308/accr.2002.77.2.237

- Persakis, A., & Iatridis, G. E. (2015). Cost of capital, audit and earnings quality under financial crisis: A global empirical investigation. Journal of International Financial Markets, Institutions and Money, 38(1), 3–24. https://doi.org/10.1016/j.intfin.2015.05.011

- Piot, C., & Missonier-Piera, F. (2007). Corporate governance, audit quality and the cost of debt financing of French listed companies. Communication Présentée Au 28ème Congrès del’Association Francophone de Comptabilité, Poitiers, 1–22. http://dx.doi.org/10.2139/ssrn.960681

- Pittman, J. A., & Fortin, S. (2004). Auditor choice and the cost of debt capital for newly public firms. Journal of Accounting and Economics, 37(1), 113–136. https://doi.org/10.1016/j.jacceco.2003.06.005

- Porta, R. L., Lopez-de-Silanes, F., Shleifer, A., & Vishny, R. W. (1998). Law and finance. Journal of Political Economy, 106(6), 1113–1155. https://doi.org/10.1086/250042

- Rahaman, M. M., & Al Zaman, A. (2013). Management quality and the cost of debt: Does management matter to lenders? Journal of Banking & Finance, 37(3), 854–874. https://doi.org/10.1016/j.jbankfin.2012.10.011

- Richardson, S. A., Sloan, R. G., Soliman, M. T., & Tuna, A. (2001). Information in accruals about the quality of earnings. Working paper, University of Michigan.

- Rogers, J. L., & Stocken, P. C. (2005). Credibility of management forecasts. The Accounting Review, 80(4), 1233–1260. https://doi.org/10.2308/accr.2005.80.4.1233

- Rosner, R. L. (2003). Earnings manipulation in failing firms. Contemporary Accounting Research, 20(2), 361–408. https://doi.org/10.1506/8EVN-9KRB-3AE4-EE81

- Schipper, K., & Vincent, L. (2003). Earnings quality. Accounting Horizons, 17(s–1), 97–110. https://doi.org/10.2308/acch.2003.17.s-1.97

- Shailer, G., & Wang, K. (2015). Government ownership and the cost of debt for Chinese listed corporations. Emerging Markets Review, 22, 1–17. https://doi.org/10.1016/j.ememar.2014.11.002

- Sharma, V. D. (2004). Board of director characteristics, institutional ownership, and fraud: Evidence from Australia. Auditing: A Journal of Practice & Theory, 23(2), 105–117. https://doi.org/10.1016/j.ememar.2014.11.002

- Stanišić, N., Stefanović, N., & Radojević, T. (2016). Determinants of the cost of debt in the Republic of Serbia. Teme, 40(2), 869–882. https://teme2.junis.ni.ac.rs/index.php/TEME/article/view/218/147

- Teoh, S. H., & Wong, T. J. (1993). Perceived auditor quality and the earnings response coefficient. Accounting Review, 68(2), 346–366. https://www.jstor.org/stable/248405

- Van Caneghem, T., & Van Campenhout, G. (2012). Quantity and quality of information and SME financial structure. Small Business Economics, 39(2), 341–358. https://doi.org/10.1007/s11187-010-9306-3

- Vander Bauwhede, H., De Meyere, M., & Van Cauwenberge, P. (2015). Financial reporting quality and the cost of debt of SMEs. Small Business Economics, 45(1), 149–164. https://doi.org/10.1007/s11187-015-9645-1

- Watts, R. L., & Zimmerman, J. L. (1986). Positive accounting theory. Prentice-Hall, NJ. https://ssrn.com/abstract=928677

- Widigdo, I. (2013). Effect of corporate social performance, intellectual capital, ownership structure, and corporate governance on corporate performance and firm value (studies on companies listed in the Sri Kehati index). International Journal of Business, Economics and Law, 2(1), 2289. https://dokumen.tips/documents/effect-ofcorporatesocial-performance-intellectual-capital-ownership-.html?page=1

- Xu, G. L., & Ji, X. (2016). Earnings management by top Chinese listed firms in response to the global financial crisis. International Journal of Accounting and Information Management, 24(3), 226–251. https://doi.org/10.1108/IJAIM-06-2015-0034

- Yee, K. K. (2006). Earnings quality and the equity risk premium: A benchmark model. Contemporary Accounting Research, 23(3), 833–877. https://doi.org/10.1506/8M44W1DGPLG4-8E0M

- Yen, N. H., Thanh, N. P., & Loc, B. N. (2018). Factors affecting cost of debt of companies listed on Ho Chi Minh Stock exchange. Science & Technology Development Journal-Economics-Law and Management, 2(3), 71–79. https://doi.org/10.32508/stdjelm.v2i3.521

Appendix

Table A1. Variable description in equation (1)

Table A2. Variable description in equation (5)

Figure A3. SEM structural model.