Abstract

Vietnam’s pulp and paper industry has contributed significantly to socio-economic growth but is also one of the industries with a very high risk of environmental pollution. Stems from the goal of economic growth coupled with environmental protection operations in Vietnam, this study examines the factors affecting the implementation of environmental management accounting (EMA) in manufacturing enterprises in Vietnam’s pulp and paper industries. The data used in the study were collected through survey questionnaires in the form of face-to-face interviews or sent by e-mail or post to survey respondents at 290 manufacturing enterprises pulp and paper in provinces and cities of Vietnam. Survey subjects are managers (directors, deputy directors, chief accountants) and accountants who have knowledge of EMA in these enterprises. The survey results were obtained from 250 valid survey questionnaires used in this study. This study uses Cronbach’s alpha analysis, exploratory factor analysis, and linear regression analysis using SPSS 20 statistical software. The results show that coercive pressure, normative pressure, awareness of the benefits of applying EMA, environmental strategy, managers’ perception, and qualifications of accountants have a positive impact on EMA implementation. In which, coercive pressure has the strongest impact, and awareness of the benefits of applying EMA has the weakest impact on EMA implementation in these enterprises.

PUBLIC INTEREST STATEMENT

This paper examines the factors affecting the implementation of environmental management accounting (EMA) in manufacturing enterprises in the pulp and paper industry in Vietnam. This study is necessary because EMA is now considered a relatively new branch of accounting, so the research related to this issue is still quite limited. Furthermore, studies on this topic have been mainly carried out in developed countries, which still lack empirical studies in developing countries. Currently, Vietnam’s economic development activities have created certain pressures and negative impacts on the environment, and environmental pollution continues to be complicated especially environmental pollution caused by manufacturing enterprises. Therefore, this study was conducted to promote the implementation of EMA in manufacturing enterprises in Vietnam to ensure development goals associated with environmental protection. Furthermore, these research findings are valuable reference resources to help agencies, policymakers, professional associations, training institutions, and enterprises develop and promulgate mechanisms and policies to promote EMA implementation in Vietnam’s manufacturing enterprises.

1. Introduction

Environmental pollution and climate change are challenges for countries all over the world. These problems degrade people’s quality of life and pose severe threats to global sustainable development. As a result, environmental protection and green growth are among the top priorities for many countries in attaining long-term socio-economic development. Sustainable development must ensure effective economic growth, a just society, and a protected and preserved environment. The challenge today is to strike a balance between three pillars: economic efficiency, social justice, and environmental protection (Keit, Citation2011). Today, the issue of green economic development has become a business trend in developed countries; while most developing countries temporarily prioritize economic growth, this will lead to the activities of manufacturing enterprises that may cause negative impacts on the environment (O’Neill et al., Citation2005). Similar to other developing countries, economic development activities that contribute to the socio-economic promotion of Vietnam have created certain pressures and negatively impacted the environment; environmental pollution continues to be complicated, in which the leading cause of this situation is manufacturing enterprises, including manufacturing enterprises in the pulp and paper industry. According to the Ministry of Natural Resources and Environment (Citation2021), although the number of enterprises with high technology levels is increasing, the gap is too far compared to some countries in the region. Therefore, to produce goods, it is necessary to consume more raw materials and energy, generate more waste, and put pressure on the environment, especially in industries with the potential to cause environmental pollution in paper processing, textile dyeing, chemicals, etc. Besides, many businesses have not yet focused on investing in environmental protection; environmental protection activities have not been carried out regularly, have not become the awareness and actions of companies, and are still coping (Nguyen & Lai, Citation2021). However, in the context of international economic integration, the change in consumer behavior and awareness, in particular, and the whole society, in general, has created new pressures and motivations for businesses to implement—social responsibility in environmental protection. Therefore, more than ever, managers need to understand that the money spent on controlling and reducing environmental pollution is not an expense, but an investment in the future, to increase the environmental value, image, and brand of the business. Therefore, to serve business decision-making, in addition to information about revenue, costs, and profit, managers also need more information about the environment. Environmental management accounting (EMA) can provide information to meet this requirement (Khalid et al., Citation2012). Many studies around the world have confirmed that environmental accounting (EA) in general, and EMA in particular, are tools that provide businesses with the necessary information to reduce environmental impacts, improve both economic efficiency and environmental performance, and achieve sustainability (IFAC, Citation2005). Along with that, EMA has been confirmed as a valuable tool to overcome the limitations of conventional management accounting (MA); it helps to better understand and quantify related environmental issues for decision-making (Burritt et al., Citation2002), assist organizations in gaining competitive advantage (Godschalk, Citation2008), and improve corporate environmental performance, cost savings, reduce waste costs, operational efficiency, increase in revenue, and improve capital investment decisions (Burritt & Schaltegger, Citation2010).

In Vietnam, the concept of EMA is still relatively new and has not been widely disseminated to many enterprises. As there are currently no specific regulations and guidelines on EA and EMA, enterprises have difficulty collecting, identifying, analyzing, and evaluating effectively environmental data, especially waste management prevention of environmental pollution. Therefore, many enterprises have not yet applied for EMA and are unaware of the benefits of EMA implementation. Enterprises only see the financial benefits (monetary measure) but not the environmental benefits. This leads to the application of EMA in the management of production and business activities of Vietnamese enterprises, including pulp and paper manufacturers, is still at a low level. This can be considered one of the difficulties and challenges for management agencies, policymakers, and businesses themselves in implementing development goals associated with environmental protection. Therefore, the problem for regulators, policymakers, and businesses is how to implement EMA best. In order to solve this problem, Vietnamese regulatory agencies and policymakers need to perfect environmental management institutions, specific regulations, and guidelines on EA as well as EMA to ensure synchronization and create favorable conditions for businesses to apply EMA. At the same time, companies need to be aware of the role and benefits of EMA implementation; that is, using EMA can increase position image, improve reputation, increase access to capital, and be more accessible to expand plans due to increased community trust (USEPA, Citation1995). Furthermore, EMA is a tool for businesses to manage business operations and the environment, effectively control and use natural resources, reduce unwanted environmental impacts, and help improve their image and standardization of enterprise operations (Zutshi & Sohal, Citation2004).

On the other hand, in recent years, there have been many studies that go into depth to examine the factors affecting the implementation of EMA; however, the results of the studies are still different and inconsistent due to the research being done in different countries, fields, professions, time. Furthermore, EMA is a relatively new branch of accounting, so the research related to EMA is still relatively modest (Bouma & van der Veen, Citation2002), especially since not much research has been done in developing countries (Herzig et al., Citation2012). The studies are mainly carried out in developed countries with a synchronous infrastructure and a relatively complete legal system for implementing EMA. Studies on the implementation of EMAs in countries with economies in transition, such as Vietnam, are still relatively modest, especially since there are almost no studies examining the implementation of EMAs in manufacturing enterprises in the pulp and paper industry in Vietnam. Therefore, to help carry out the above efforts, this study examines the influence of factors on the implementation of EMA at pulp and paper manufacturing enterprises in Vietnam. The results show that the factors of coercive pressure, normative pressure, awareness of the benefits of applying EMA, environmental strategy, managers’ perception, and qualifications of accountants have a positive impact on EMA implementation in the pulp and paper manufacturing enterprises in Vietnam. The findings of this study provide evidence on the degree of impact of factors on the implementation of EMA, thereby suggesting several implications to help state management agencies, policymakers, professional associations, training institutions, and enterprises in the process of promulgating mechanisms and policies affecting factors to promote the implementation of EMA in manufacturing enterprises in Vietnam.

2. Environmental and socio-economic impacts of the pulp and paper industry in Vietnam

The pulp and paper industry is one of the significant industries for the socio-economic development strategies of countries. Vietnam’s pulp and paper industry also contribute to the economy’s development (Pham, Citation2022); this is considered one of the key industries contributing to poverty reduction, poverty reduction, economic restructuring, and economic development in remote areas. In recent years, Vietnam’s paper industry has had an average growth rate of about 10–12% per year, the paper industry’s production contributes about 1.5% of GDP value, and export turnover reaches over 1 billion USD (Hoa, Citation2020). However, besides the positive effects on the economy, the pulp and paper industry is characterized by high energy, fuels, and chemicals, emitting toxic emissions, and this is one of the manufacturing industries causing significant environmental pollution. Environmental impacts such as air pollution (e.g., chlorine vapor in the bleaching process, waste from fuel combustion for boilers, H2S gas, etc.), wastewater pollution (e.g., wastewater from the production process, wastewater components containing a mixture of plant extracts such as resins, fatty acids, lignin, etc.), pollution due to solid waste (e.g., packaging, all kinds of paper, sludge from septic tanks, waste paper impurities, coal slag from boilers, incinerators, etc.) of this industry are problems causing heavy consequences for the environment and people’s health; environmental quality continues to deteriorate in many places, many environmental hotspots have been negatively affecting residential areas. Recognizing the impact of the pulp and paper industry on the environment, the Ministry of Industry and Trade (Citation2014) approved the “Plan on development of Vietnam’s paper industry up to 2020 and vision extended to 2025” with the view of developing Vietnam’s paper industry in a sustainable way associated with the task of environmental protection. However, paper and packaging enterprises have not paid much attention to environmental protection. As a result, waste from the paper and packaging production process, such as wastewater, exhaust gases, and solid waste, negatively impacts human life, health, the environment, and the ecosystem. Therefore, this issue is receiving special attention from the authorities (Pham, Citation2022). To produce 1 ton of finished paper, Vietnamese factories must use about 2 tons of wood and 100–350 m3 of water, while the world’s modern paper mills only use 7–15 m3 of water. This situation wastes water resources and causes businesses to increase environmental treatment costs. Therefore, paper manufacturing enterprises need to cut costs, reduce electricity and water consumption, and ensure stable and sustainable development. At the same time, it increases production efficiency, improves technology and management capacity, effectively use natural resources, and reduces undesirable environmental impacts.

3. Theoretical foundations and hypothesis

3.1. Background theory

3.1.1. Isomorphic institutional theory

DiMaggio and Powell (Citation1983) consider isomorphism as the concept that best describes the homogenization process. The authors believe that the organization’s characteristics will be changed to match the features of the environment. The institutional isomorphism theory deals with coercive isomorphism, simulated isomorphism, and normative isomorphism. From the point of view of coercive isomorphism, the legal system is the primary determinant of EMA implementation. Enterprises may face institutional pressure, and they must implement EMA to satisfy the expectations and requirements of stakeholders, especially those with strong influence, such as regulators or owners; even coercive pressures come from customers, investors, competitors, etc. Normative pressure is related to professionalism, i.e., when members jointly manage quality and establish a perceived and legal basis for professional autonomy. The increasingly strong development of professional organizations makes it easier for changes to spread. In Vietnam, domestic and foreign professional associations also play an important role in EMA implementation. Thus, the institutional theory is used to explain the influence of factors such as coercive pressure, normative pressure, education, and occupation on popularizing the application of EMA in enterprises. In addition, simulated pressure is the response that mimics other organizations in the society of enterprises to techniques and methods that have been accepted, adopted, or considered the industry norm (DiMaggio & Powell, Citation1983). However, in the context of Vietnam, it can be seen that Vietnam does not have specific regulations and guidelines on the implementation of EA and EMA, so there are still not many enterprises applying for EMA. That’s why manufacturing enterprises in the pulp and paper industry find techniques and methods of using EMA from other manufacturers that seem very difficult. Therefore, this study does not consider the influence of simulated pressure factors on implementing EMA in manufacturing enterprises in Vietnam’s pulp and paper industry.

3.1.2. Legitimacy theory

The legitimacy theory holds that an organization’s activities must conform to the values or social norms in which it operates. The failure of organizations to adhere to social values or norms can make it difficult for the organization to gain the community’s support to continue working. The sustainable development of enterprises must be considered from three perspectives: economic, environmental, and social (Elkington, Citation1997). Accordingly, an enterprise creates economic values while protecting and developing environmental and social values. However, the reality shows that enterprise activities always have increasingly serious impacts on the environment and social community. Therefore, the pressure of legal authorities, environmental groups, and the social community forces businesses to implement environmental responsibility through environmental management according to standards and to change the accounting system to disclose appropriate environmental information. Likewise, pressure from society will force enterprises to fulfill their responsibility for the environment through standards and change the accounting system to disclose appropriate environmental information. Thus, the theory legitimacy the relationship between enterprises and society. An enterprise’s activities must be consistent with socially accepted values for such actions to be considered legal and for companies to exist and develop in the community. Legitimacy theory explains the reasons and motivations for using EMA as a tool for organizations to carry out social responsibility. Therefore, this theory is used as the basis to form factors such as awareness of the benefits of applying EMA, managers’ perception, and environmental strategies affecting the implementation of EMA in enterprises.

3.2. Implementation of EMA

Implementation of EMA refers to a system of accounting techniques that provide managers with financial and non-financial information about the organization and the environment (Bouma & Correljé, Citation2003). It is a valuable tool to overcome the limitations of conventional MA to better understand and quantify environmental issues for decision-making (Burritt et al., Citation2002). EMA is a technique for identifying, collecting, and analyzing environmental information that uses value and in-kind measures, providing information responsive to an organization’s internal analysis and decision-making (UNDSD, Citation2001). EMA is the management of environmental and economic performance through the development and implementation of appropriate environment-related accounting systems and practices. Environmental management accounting typically involves life-cycle costing, full-cost accounting, benefits assessment, and strategic planning for environmental management (IFAC, Citation2005).

Implementing EMA in an organization includes monetary accounting (financial or monetary information) and non-monetary accounting. In which, EMA on a non-monetary basis, reflects all past, present, and future flow of materials and energy of the organization that impact the ecosystem, presented as a measurement artifact. Non-monetary information, including information related to materials, energy, water, waste, and emissions because of the environmental impacts caused by the organization that are directly related to the use of resource materials and the amount of waste, emissions, and discharge into the environment. EMA is an extension of the traditional application of MA to environmental issues in business operations in monetary terms (e.g., costs of environmental compliance, investment in environmental protection, and pollution prevention). Environment-related costs under EMA include environmental protection expenditures and other important monetary information needed to cost-effectively manage environmental performance (IFAC, Citation2005).

3.3. Research hypothesis

3.3.1. Coercive pressure

Coercive pressure reflects certain institutions’ enforcement and management aspects. According to the institutional theoretical framework, coercive pressure comes from legal regulations of state agencies (pressure from government and regulatory agencies) and threats of losing competitive advantage from the business environment (pressure from customers, suppliers, investors, media, etc.). Therefore, the institutional characteristics of the environment are increasingly being noticed as important determinants of organizational structure and performance (Hussain & Gunasekaran, Citation2002). When the environment is no longer a local or national issue but becomes global, it is necessary and appropriate to protect the environment in the accounting system and carry out environmental responsibility reporting for businesses to achieve legitimacy in their operations. In other words, coercive pressure motivates businesses to apply EMA to achieve legitimacy in their operations. Regulations, legal documents of the government, and environmental management agencies affect the disclosure of environmental information by enterprises (Nguyen et al., Citation2020). However, enterprises tend not to apply EMA when there is no pressure from state management agencies, so increasing coercive pressure, especially from the government, will increase the intention and willingness to apply EMA of enterprises (Chang & Deegan, Citation2007). Mandatory regulations will be a determinant of EMA practice, so the development of EMA will be addressed by the government and other authorities (Jamil et al., Citation2015). Therefore, pressure from the government, environmental protection organizations, inter-agency environmental regulatory agencies, etc., significantly affects the ability to implement EMA practices (Tran et al., Citation2021). In other words, with increasing coercive pressure, manufacturing firms will be more willing to implement EMA (Jamil et al., Citation2015). Based on the above arguments, the first hypothesis of this study is developed as follows:

H1: Coercive pressure positively impacts the implementation of EMA in pulp and paper manufacturing enterprises.

3.3.2. Normative pressures

According to institutional theory, normative pressure derives from the pressure in social norms formed from the background of education and profession to achieve corporate behavior. Therefore, normative pressures are pressures on organizations to comply with professional standards, regulations, principles, and ethics and are accomplished through education and professional associations. The accountants agree that their work is closely related to their education and training. In addition, they react naturally to information provided by other accountants and from professional associations to which they are members (Bennett et al., Citation2004); therefore, it can be expected that the implementation of EMAs by businesses will be affected by pressure from professional bodies or educational institutions, or in other words, normative pressure is a solid premise for applying EMA (Jalaludin et al., Citation2011). Qian et al. (Citation2015) examined normative barriers related to the development of EMA and found that public awareness and education (normative pressure) are important factors affecting the implementation of EMA; however, the effect of normative pressure on the organization may differ from country to country. Chang and Deegan (Citation2010) confirm that in developed countries, professional associations and formal educational institutions play a significant role in influencing the behavior of organizations on environmental issues and EMA implementation, higher than that of developing countries. Based on the above analysis, the second hypothesis of this study is as follows:

H2: Normative pressure positively impacts the implementation of EMA in pulp and paper manufacturing enterprises.

3.3.3. Awareness of the benefits of applying EMA

The understanding and awareness of accountants and other stakeholders towards EMA is an important factor in applying and developing EMA in practice (e.g., Burritt et al., Citation2002; Jalaludin et al., Citation2011). The issue of perception of benefits reflects a basic understanding of EMA, understanding the role and importance of EMA in corporate governance, connecting corporate interests with social benefits, and then being ready to participate in the application of EMA. EMA will help provide more accurate, complete, and comprehensive information to measure performance, thereby improving not only the image of the organization but also increasing relationships with the community and stakeholders, complying with environmental laws, avoiding fines, compensation, and remedying environmental problems (IFAC, Citation2005). Legitimacy theory explains that, through the implementation of environmental protection activities and the disclosure of information on the responsibility to perform social contracts, businesses will gain several benefits in the process of operating, such as: creating more trust in society in the enterprise, improving position, image, gain competitive advantage, etc. This is the reason and motivation that EMA is used as a tool for the organization to implement social responsibility to ensure that its activities meet the requirements of society. However, enterprises with low environmental awareness only implement EMA when they benefit from this. From the above statements, the third hypothesis of this study is as follows:

H3: Awareness of the benefits of EMA adoption has a positive relationship with implementing EMA in pulp and paper manufacturing enterprises.

3.3.4. Environmental strategy

Environmental strategy is understood as a set of initiatives that can reduce the impact of activities on the natural environment through products, processes, and policies such as reducing energy consumption, waste, sustainable green resource use, and implementation of environmental management systems (Bansal & Roth, Citation2000). Accounting information systems such as EMA can be useful in providing information on environmental costs; monitoring financial performance and the environment when implementing environmental strategy (Ferreira et al., Citation2010). However, enterprises agree that using EMA only to meet environmental regulatory requirements (Setthasakko, Citation2010) or pressure and expectations from stakeholders, such as customers, were seen to be the reason for capital investment and other environmental actions (Khalid et al., Citation2012). Notwithstanding, the influence of environmental strategy on EMA implementation is said to be unclear (Chang & Deegan, Citation2007). The recent trend relating to sustainable development has led enterprises, to state their confirmation and declare their responsibility to society in their environmental strategy. Therefore, enterprises should have no choice but improve their image by adopting innovation tools such as EMA (Tran et al., Citation2021). In addition, the concern about environmental protection has encouraged enterprises to organize EMA (Wachira, Citation2014). Indeed, according to the legitimacy theoretical framework, society and the community will evaluate the business’s activities for the environment. Hence, companies need to behave in accordance with environmental responsibility by publishing environmental information and publishing a list of strategies implemented to bring legitimacy or maintain the business’s legitimacy. Enterprises will try to satisfy social requirements to ensure their production and business activities, and the implementation of EMA will be considered for deployment. Based on the above argument, the fourth hypothesis of the study is stated as follows:

H4: Environmental strategy positively impacts the implementation of EMA in pulp and paper manufacturing enterprises.

3.3.5. Managers’ perception

Legitimacy theory is also used to explain the cognitive factor of managers (especially senior managers) affecting the disclosure of environmental information of enterprises. Due to pressure from legal authorities, environmental groups, and the social community, businesses are forced to fulfill their environmental responsibility through standard environmental management and change the accounting system to appropriate environmental information disclosure. Therefore, the reception and response to the change in response to legitimacy, especially for potential social contracts, depends greatly on the perceived needs of business managers. Many previous studies have shown that top management’s interest and support are critical to the success of any environmental management practice (Henriques & Sadorsky, Citation1999; Zhu & Sarkis, Citation2004). The success or failure of the implementation of EMA in enterprises depends on the management ability as well as the support of the administrators. Management’s perception is one of the important factors in EMA practice (Kokubu & Nashioka, Citation2005), as managers influence policy choices; environmental strategy in business activities. When managers are aware of the usefulness of EMA, they will implement a proactive environmental strategy to provide environmental information, reduce operational costs, reduce costly waste, exploit new markets and attract consumers through green products. In contrast, business managers’ lack of environmental responsibility and active support for EMA readiness can hinder EMA implementation (Jamil et al., Citation2015). From the above statements, the fifth hypothesis of the study stated as follows:

H5: Managers’ perception of the usefulness of EMA has a positive relationship with the implementation of EMA in pulp and paper manufacturing enterprises.

3.3.6. Qualifications of accountants

The institutional theory explains the influence of vocational education factors on the process of popularizing the application of EMA in enterprises. The process of enterprises applying a voluntary environmental commitment to relieve pressure from environmental regulations is carried out by promoting the role of accountants in EMA practice. The qualifications of employees are considered an important factor in being able to successfully apply EMA because if the employees do not master the knowledge and skills, it is difficult for EMA to apply to the business. So, in the enterprise, the presence of qualified accountants is a significant factor affecting the implementation of EMA. Usually large enterprises often have specialized accounting/finance departments and tend to employ qualified accountants to provide professional reports and advice. Accountants’ lack of environmental knowledge and experience can restrict the integration of environmental issues into existing accounting practices (Setthasakko, Citation2010). Therefore, accounting staff is an important factor affecting the implementation of green accounting (Nguyen, Citation2020), especially EMA. In fact, the application of EMA differs from traditional accounting, so accountants need knowledge and skills related to the environment and EMA. Applying EMA tools is considered too complex to require highly qualified staff (Tran et al., Citation2021); therefore, accounting staff qualifications influence EMA implementation (Adams, Citation2002; Wilmshurst & Frost, Citation2001). Based on the above arguments, the sixth hypothesis of the study stated as follows:

H6: The qualification of accountants has a positive relationship with the implementation of EMA in pulp and paper manufacturing enterprises.

3.4. Research models

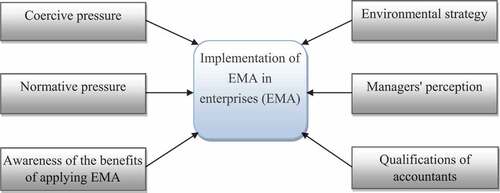

Based on the theoretical background and the above hypotheses, this study’s proposed theoretical research model is described as shown in Figure .

Figure 1. Proposed research model. source: suggested by the author.

Regression model: based on the hypotheses and proposed research models, the expected regression equation reflects the relationship between “factors affecting the implementation of EMA in pulp and paper manufacturing enterprises in Vietnam” as follows:

EMAi = α + β1COERi + β2NORMi + β3BENEi + β4STRAi + β5PERCi + β6QUALi + εi

In which, EMAi is the implementation of EMA in pulp and paper manufacturing enterprises sample i. The variables COER, NORM, BENE, STRA, PERC, and QUAL are the variables of coercive pressure, normative pressure, awareness of the benefits of applying EMA, environmental strategy, managers’ perception, and qualifications of accountants. The variables in this study are described in Table (see Appendix A).

α: Constant term

βi: Coefficients of the explanatory variables

εi: Residual

4. Research methodology

4.1. Data collection methods

This study uses primary and secondary data sources. In which secondary data is obtained from conferences, seminars, published topics, scientific articles, etc.; primary data is obtained through a survey questionnaire with a 5-point Likert scale (from 1: Strongly disagree to 5: Strongly agree) by face-to-face interview or sent by email or post to 290 enterprises. The subject to be surveyed to intelligibility and express their views (Marton-Williams, Citation1986), less confusion, and increased response rates (Babakus & Mangold, Citation1992; Devlin et al., Citation1993); this study selects all structures measured using a 5-point Likert scale. The survey’s subjects are managers (directors, deputy directors, chief accountants) and accountants with knowledge of EMA at pulp and paper manufacturing enterprises in Vietnam’s provinces and cities. This audience consists of individuals who thoroughly understand the enterprise’s internal control system, financial management system, or current condition, so they play a critical and decisive role in its EMA implementation. The survey results yielded 250 valid survey questionnaires (an 86 percent response rate) used in the research. In addition, the author conducted this survey from August to December 2021. Table shows the characteristics of the respondents in this study.

Table 1. Describe the characteristics of the respondents (N = 250)

In addition, the sample size in exploratory factor analysis (EFA) must be 4 or 5 times the number of variables in factor analysis (Hoang & Chu, Citation2008). Furthermore, in practical research applications, the sample size is often larger than 150 (Anderson & Gerbing, Citation1988). Therefore, this study selected a sample size of 250 samples to conduct the study, which is completely appropriate.

4.2. Data analysis methods

The study uses statistical software SPSS 20 for descriptive statistical analysis through a multi-variable linear regression model with criteria such as Cronbach’s Alpha test to assess the reliability of the scale, EFA analysis to regroup observed variables into more meaningful factors, testing the linear regression model to determine the correlation between factors and the implementation of EMA.

5. Results and discussion

5.1. Cronbach’s alpha test

Cronbach’s Alpha coefficients examine the degree of correlation between observed variables in the same factor included in the research model. Table ʹs results show that all variables have Cronbach’s alpha coefficients > 0.6, so the scales can be used well and reliably (Hoang & Chu, Citation2008). Thus, Cronbach’s Alpha test results show that the observed variables belonging to the factor groups remain the same.

Table 2. Cronbach’s alpha test

5.2. Exploratory factor analysis (EFA)

The scales of this study are built based on the scales of previous studies and adjusted to suit the practical conditions in Vietnam. Therefore, this study uses EFA analysis to uncover latent structures among observed variables. EFA analysis is performed to reshape the structure of the groups of scales, consider the convergence and discriminant of the groups of variables, and help remove the observed variables that have no practical significance. Thus, EFA analysis is used to reduce a set of observed variables into a more significant set of factors (Nguyen, Citation2011). The test results in Table show that the coefficient KMO = 0.808 (satisfying 0.5 ≤ KMO ≤ 1) should be satisfactory, and the Barlett test has Sig. = 0.000 < 5%, so these observed variables are closely related to and suitable for EFA analysis. The total variance extracted is 69.387% > 50%, at Eigenvalues = 1.559 > 1, satisfactory (Anderson & Gerbing, Citation1988). The characteristic variables all have factor loading > 0.5, so they are satisfactory (Hair et al., Citation1998). Thus, the results of the EFA analysis are completely consistent, and the extracted factors are reliable and valid.

Table 3. The results of exploratory factor analysis of independent variables

The analysis results of the scale of EMA in Table show that the coefficient KMO = 0.903 (satisfying 0.5 ≤ KMO ≤ 1), the Barlett test has Sig. = 0.000 < 5%, so the model is suitable for the analysis; the variables are correlated overall. Total variance extracted is 62.149% > 50%; at Eigenvalues = 5.593 > 1, so the model is eligible for EFA analysis. The results of Table show that the observed variables of the dependent variable EMA are satisfied (factor loading > 0.5). Thus, after analyzing EFA, the nine observed variables of the EMA variable have no disturbance, so the EMA variable is suitable and included in the study.

Table 4. The results of the exploratory factor analysis of the dependent variable

5.3. Regression analysis

The Pearson correlation test tests a linear relationship between independent and dependent variables. The results in Table show that the independent variables COER, NORM, BENE, STRA, PERC, QUAL, and the dependent variable EMA all have Sig. < 5%, so these independent variables are correlated with the dependent variable and continue to be included in the research model to explain the dependent variable.

Table 5. Correlations

This study uses the linear regression method to test research hypotheses and analyze the relationship between the dependent and independent variables. The test results show that, Adjusted R Square = 41.8% (Table ), which means that the independent variables explain 41.8% of the variation of the dependent variable. Furthermore, the ANOVA test has Sig. = 0.000 < 5% (Table ), so the model is statistically significant and has at least one independent variable affecting the dependent variable.

Table 6. Model summary

Table 7. ANOVA

The results in Table show that the variables COER, NORM, BENE, STRA, PERC, QUAL all have Sig. < 0.05, so the regression model is statistically significant, suitable for the data set, and usable, i.e., the independent variables COER, NORM, BENE, STRA, PERC, and QUAL impact the variable depends on EMA. Furthermore, the independent variables’ variance inflation factors (VIF) are less than 2, so multicollinearity is not violated (Nguyen, Citation2011).

Table 8. Coefficientsa

Thus, after performing hypothesis testing by the linear regression model, hypotheses H1, H2, H3, H4, H5, and H6 are accepted with statistical significance at 1%; the regression coefficients (B, Beta) were found to have statistical significance, and the level of impact of the independent variables on the dependent variable from high to low, respectively: COER, PERC, QUAL, STRA, NORM, BENE.

5.4. Discussion

5.4.1. Coercive pressure

Coercive pressure is an important factor, having the strongest impact on EMA implementation in pulp and paper manufacturing enterprises in Vietnam (B1 = 0.146). This result proves that when the coercive pressure increases by 1 unit, the implementation of EMA in pulp and paper enterprises increases by 0.146 units. In other words, if enterprises face much coercive pressure related to the environment, they will consider implementing EMA in the future. This result is consistent with the study of Chang and Deegan (Citation2007), Jamil et al. (Citation2015), and Tran et al. (Citation2021). In Vietnam, environmental issues and environmental protection are always of particular concern to the government. Many guidelines and policies on environmental protection and climate change have been revised to solve the current environmental situation problems. The legal system on the environment is gradually being perfected to regulate the management and protection of the environment, clearly defining the obligations and responsibilities of enterprises in integrating environmental issues into their business activities. From an accounting perspective, the control of enterprises by the authorities in the field of environment as well as regulations that require enterprises to report and assess impacts related to the environment and society. Therefore, preparing annual reports will pressure enterprises to have financial, environmental, and social management systems. Thus, when enterprises receive pressure from powerful external institutions (government, regulatory agencies, customers, suppliers) will promote and encourage them to implement EMA.

5.4.2. Normative pressure

Normative pressure also is a factor that positively impacts the implementation of EMA in pulp and paper manufacturing enterprises in Vietnam (B2 = 0.090). If normative pressure increases by 1 unit, the probability of EMA implementation in pulp and paper enterprises increases by 0.090 units. This finding is consistent with the research results of Jalaludin et al. (Citation2011), and Qian et al. (Citation2015). This finding is suitable to explain that the current implementation of EMA in Vietnam is nonmandatory; the accounting regulations are focused and directed only to traditional accounting and tax management, while there are no guidelines for EMA application. Therefore, although many enterprises are moving towards production, business processes, and service provision in line with the sustainable development strategy, the accounting staff in the enterprises have a good understanding of the environment is still limited. In contrast, teaching and training programs on the implementation of environmental accounting have not been developed. Therefore, if enterprises are interested in training and practicing to provide employees with a solid foundation in the environment, it will create a premise for them to be able to apply EMA in the future. In addition, professional associations also have a significant influence on the behavior of the accounting team, especially concerning the membership of these associations. Therefore, professional associations’ focus on developing and emphasizing the importance of EMA will spur members to be more interested in and likely to implement EMA. This implies that professional bodies and educational institutions should step up their role in increasing regulatory pressure on pulp and paper businesses to promote EMA implementation.

5.4.3. Awareness of the benefits of applying EMA

Awareness about the benefits of applying EMA positively impacts EMA implementation in pulp and paper manufacturing enterprises in Vietnam (B3 = 0.084). The results show that when the perception of the benefits of applying EMA increases by 1 unit, the implementation of EMA in pulp and paper enterprises increases by 0.084 units. This finding explains that when the accounting department in the enterprise appreciates the benefits of EMA tools and techniques, it will increase the implementation of EMA in enterprises. This result is consistent with the results of Burritt et al. (Citation2002), Jalaludin et al. (Citation2011). Applying EMA helps businesses fulfill their responsibilities and meet the requirements of society, create more trust in the community for businesses, improve their position, image, and gain competitive advantages. However, unfortunately, Vietnam does not have many guiding documents on EA and EMA, so it is difficult for accountants to monitor, record and analyze information about the environment. Along with that, EMA has not been propagated, promoted, and taught in accounting and auditing training programs at professional associations in accounting, training institutions, etc. This leads to limited awareness of the benefits of EMA in the business community in general, accountants and auditors in particular.

5.4.4. Environmental strategy

The environmental strategy is a factor that positively impacts the implementation of EMA in pulp and paper manufacturing enterprises in Vietnam (B4 = 0.110). This result shows that when the environmental strategy increases by 1 unit, the implementation of EMA in pulp and paper enterprises increases by 0.110 units. This finding is consistent with the study of Setthasakko (Citation2010), Ferreira et al. (Citation2010), Chang and Deegan (Citation2007), and Tran et al. (Citation2021). This result implies that, in the context of increasing awareness of the volatility of the business environment, businesses will choose to promote environmental strategies and actively apply the EMA system to manage information environmental news. Thus, to diffuse the implementation of EMA, the enterprise’s environmental strategy should be the first issue that needs to be solved and improved. Currently, Vietnam is in the process of industrialization and modernization of the country; the economic growth rate is relatively high, leading to an improvement in people’s consumption levels, green products, products that meet safety and quality standards and are environmentally friendly have gradually become the practical needs of people. Therefore, “green” quality will become a competitive advantage to help enterprises gain better market share. The brand development associated with the “green” factor—using friendly materials and technologies, offering “clean” products, and ensuring the environment plays a pivotal role in the enterprise’s development strategy. To do this, enterprises themselves need to set common goals and policies on the environment, provide environmentally friendly products, commit to complying with regulations, certify environmental awareness, and provide effective environmental protection and management solutions.

5.4.5. Manager’s perception

Managers’ perception of EMA is also a significant factor, positively impacting the implementation of EMA in pulp and paper manufacturing enterprises in Vietnam (B5 = 0.139). The results show that when managers’ awareness of EMA increases by 1 unit, the implementation of EMA in pulp and paper enterprises increases by 0.139 units. This result is similar to that of Kokubu and Nashioka (Citation2005), Jamil et al. (Citation2015). In fact, managers and business operators stand at the ones who forefront of understanding the role of EMA and are the ones who decide or lead departments in the enterprise to implement EMA. They are the ones who make the right strategies and decisions for enterprises to achieve their sustainable development goals. If the management requires the introduction of EMA as one of the top strategies, the implementation of EMA in these enterprises will accelerate rapidly. Therefore, if managers and business operators are the perception of the benefits and appreciate the usefulness of EMA technical tools, they will be interested in and plan to apply EMA to implement the proactive environment strategy, provide much environmental information, reduce operating costs, exploit new markets and attract consumers through green products. However, many managers and business operators in Vietnam are often interested in financial accounting to provide financial information to management agencies, shareholders, creditors, and other parties, so most businesses have not paid much attention to EMA’s tools and techniques to support the management and administration process. Furthermore, many enterprise managers and executives make operational decisions based on emotional elements or experience rather than principles, skills, management expertise, or other information offered by EMA.

5.4.6. Qualifications of accountants

Qualifications of accountants are also an important factor, positively impacting the implementation of EMA in pulp and paper manufacturing enterprises in Vietnam (B6 = 0.127). Research results confirm that when the qualifications of accountants increase by 1 unit, the implementation of EMA in pulp and paper enterprises increases by 0.127 units. This result is consistent with the study of Wilmshurst and Frost (Citation2001), Setthasakko (Citation2010), Nguyen (Citation2020), and Tran et al. (Citation2021). This finding explains that businesses with well-trained and highly qualified accountants will help implement EMA more smoothly. The accounting staff in enterprises greatly influences the organization of accounting, affecting the process of receiving and processing accounting information to provide managers with decisions to make. Therefore, these accountants need to have the qualifications, knowledge, and experience in accounting to better implement accounting in the enterprise, creating a premise for applying EMA. In Vietnam, accounting and auditing training institutions mainly focus on financial accounting training programs; few MA training programs, especially EMA. This leads to numerous accountants with only knowledge and experience in financial accounting and lacking skills and expertise in MA and EMA. Even the concept of EMA is relatively new to many enterprises in general and accounting practice teams in particular. Therefore, the implementation of EMA in Vietnamese enterprises will face certain difficulties.

6. Conclusion and recommendations

Vietnam has built a strategic orientation to develop a sustainable economy based on harmonizing cultural and social factors, especially balancing the economy with the environment and protecting the environment responsibly. Socio-economic development must permanently attach importance to environmental protection and improvement. However, like other developing countries, Vietnam is being strongly affected by climate change, pollution, and environmental degradation, which has affected the economy as well as the quality of life of the people. In particular, the main object of environmental degradation is businesses. In fact, most enterprises in developing countries often set target profit rather than growth associated with conservation and environmental protection activities. Many studies worldwide have confirmed EMA as a useful tool to quantify environmental-related issues for decision-making. Thereby helping enterprises in gaining competitive advantage, cost savings, reduce waste costs, operational efficiency, increase in revenue, and improve the corporate environment. Stemming from the goal of developing a green economy associated with sustainable development in Vietnam, this study examines the influence of factors on the implementation of EMA in pulp and paper manufacturing enterprises in Vietnam. Empirical research results confirm that coercive pressure, normative pressure, awareness of the benefits of applying EMA, environmental strategy, manager’s perception, and qualifications of accountants has a positive impact on EMA implementation in pulp and paper enterprises in Vietnam. In which, coercive pressure is the factor that has the strongest impact on the ability to implement EMA in pulp and paper enterprises in Vietnam, followed by the manager’s perception of EMA, qualifications of accountants, environmental strategy, normative pressure, and awareness of the benefits of applying EMA have the weakest impact.

Based on the research findings and to promote the possibility of EMA implementation in enterprises, Vietnamese government agencies, policymakers, and other stakeholders, the following issues should be kept in mind:

Firstly, state management agencies should (1) Consider and develop legal documents regulating and guiding enterprises in the process of organizing EA and EMA at enterprises. (2) Perfecting regulations on disclosing or encouraging enterprises to publish some information related to EA, other regulations related to the environment such as taxes, penalties for environmental violations, etc. (3) Propagating and disseminating environmental protection on the media. (4) Coordinate with professional organizations to organize seminars and talks on environmental issues, environmental protection, and accounting activities related to the environment; support and guide enterprises in building long-term business orientations and strategies taking up to impacts of environmental standards and regulations. (5) Regularly check environmental issues at the enterprise.

Secondly, professional associations and training institutions need to (1) Strengthen propaganda and dissemination about the benefits of EMA implementation as well as corporate responsibilities to society. (2) Regularly organize short-term training programs on thematic topics on EA, and EMA or cooperate with international professional organizations to train international certificates in accounting and auditing. (3) Training institutions must gradually research and put into teaching about EA, and EMA, and at the same time, implement the motto of training associated with the practice, through simulation contests about EA, and EMA or organize soft skills festival programs, and practical approaches at enterprises.

Thirdly, enterprises need to (1) Create conditions for accounting staff to participate in courses, seminars related to EA, and EMA, and international certification courses in accounting and auditing such as ACCA, CPA Australia, etc., thereby improving knowledge and also contributing to increasing experience for the accountants. (2) The enterprise managers need to learn from the experience of implementing EMA from domestic and foreign enterprises to improve understanding and usefulness of EMA, thereby changing the view on the role of EMA implementation in the process of building business development strategies associated with “green” factors. (3) Building a strong culture for the enterprise to closely connect departments in the enterprise, through which there will be information sharing or mutual support between managers and employees, between departments together as a premise for the application of EMA in enterprises.

Although this study has achieved specific results and contributed to the reference source for future studies on EMA implementation, however, this study still has some limitations. Firstly, other factors such as simulation pressure, the complexity of tasks, the cost of applying EMA, etc., have not been considered in this study. Secondly, the sample size used in the study may be small, so it does not represent Vietnam’s manufacturing enterprises in general. Therefore, further studies should consider and expand the study in other aspects, such as increasing the number of factors and the sample size to provide meaningful results.

Acknowledgements

The author(s) would like to thank anonymous reviewers for their supportive comments and suggestions.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Thu Hien Nguyen

Thu Hien Nguyen is a main lecturer of accounting in the faculty of accounting at the Academy of Finance (AOF), Vietnam. She obtained her Ph.D (2017) from the Academy of Finance, Vietnam. Her research interests are in accounting, auditing, and finance. She is also the author and co-authors of several textbooks in accounting.

References

- Adams, C. A. (2002). Internal organizational factors influencing corporate social and ethical reporting: Beyond current theorizing. Accounting, Auditing and Accountability Journal, 15(2), 223–22. https://doi.org/10.1108/09513570210418905

- Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modeling in practice: A review and recommended two-step approach. Psychological Bulletin, 103(3), 411–423. https://doi.org/10.1037/0033-2909.103.3.411

- Babakus, E., & Mangold, W. G. (1992). Adapting the SERVQUAL scale to hospital services: An empirical investigation. Health Services Research, 26(6), 767–786.

- Bansal, P., & Roth, K. (2000). Why companies go green: A model of ecological responsiveness. Academy of Management Journal, 43(4), 717–736. https://doi.org/10.2307/1556363

- Bennett, M., Bouma, J. J., & Ciccozzi, E. (2004). An institutional perspective on the transfer of accounting knowledge: A case study. Accounting Education, 13(3), 329–346. https://doi.org/10.1080/0963928042000273807

- Bouma, J. J., & Correljé, A. (2003). Institutional changes and environmental management accounting: Decentralisation and liberalization. Eco-Efficiency in Industry and Science, 257–279. https://doi.org/10.1007/978-94-010-0197-7_12

- Bouma, J. J., & van der Veen, M. (2002). Wanted: A theory for environmental management accounting. Eco-Efficiency in Industry and Science, 78, 279–290. https://doi.org/10.1007/0-306-48022-0_22

- Burritt, R. L., Hahn, T., & Schaltegger, S. (2002). Towards a comprehensive framework for environmental management accounting: Links between business actors and environmental management accounting tools. Australian Accounting Review, 12(28), 39–50. https://doi.org/10.1111/j.1835-2561.2002.tb00202.x

- Burritt, R. L., & Schaltegger, S. (2010). Sustainability accounting and reporting: Fad or trend? Accounting, Auditing and Accountability Journal, 23(7), 829–846. https://doi.org/10.1108/09513571011080144

- Chang, H. C., & Deegan C. (2007). Environmental management accounting within universities: Current state and future potential. In Environmental management accounting for cleaner production S. Schaltegger, M. Bennett, R. L. Burritt, & C. M. Jasch Eds. Springer 301–320. https://doi.org/10.1007/978-1-4020-8913-8_16

- Chang, H., & Deegan, C. (2010). Exploring factors influencing environmental management accounting adoption at RMIT university. In Sixth Asia Pacific interdisciplinary research in accounting (APIRA) Conference(Vol. 26, No. 4, pp. 11-13). http://apira2010.econ.usyd.edu.au/%20conference_proceedings/APIRA-2010-005-Chang-Environmental-management-accounting.pdf

- Devlin, S. J., Dong, H. K., & Brown, M. (1993). Selecting a scale for measuring quality. Marketing Research, 5(3), 12–17.

- DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.2307/2095101

- Elkington, J. (1997). Cannibals with forks: The triple bottom line of 21st century business. Capstone Press.

- Ferreira, A., Moulang, C., Hendro, B., & Burritt, R. L. (2010). Environmental management accounting and innovation: An exploratory analysis. Accounting, Auditing and Accountability Journal, 23(7), 920–948. https://doi.org/10.1108/09513571011080180

- Godschalk, S. (2008). Environmental management accounting for cleaner production. Eco-efficiency in industry and science. In S. Schaltegger, M. Bennett, R. L. Burritt, & C. Jasch (Eds.), Does corporate environmental accounting make business sense? (Vol. 24, pp. 249–265). Springer.

- Hair, J. F., Anderson, R. E., Tatham, R. L., & Black, W. C. (1998). Multivariate data analysis (5th) ed.). Prentice Hall International, Inc.

- Henriques, I., & Sadorsky, P. (1999). The relationship between environmental commitment and managerial perceptions of stakeholder importance. Academy of Management Journal, 42(1), 87–99. https://doi.org/10.2307/256876

- Herzig, C., Viere, T., Schaltegger, S., & Burritt, R. L. (2012). Environmental management accounting: Case studies of South-East Asian companies. Routledge.

- Hoa, T. (2020). Industry—Prospects and challenges. Figures and events review of the GSO (MPI). http://consosukien.vn/cong-nghie-p-gia-y-vie-t-nam-trie-n-vo-ng-va-tha-ch-thu-c.htm

- Hoang, T., & Chu, N. M. N. (2008). Analyzing researched data with SPSS (2nd ed) ed.). Hong Duc Publishing House.

- Hussain, M., & Gunasekaran, A. (2002). An institutional perspective of non‐financial management accounting measures: A review of the financial services industry. Managerial Auditing Journal, 17(9), 518–536. https://doi.org/10.1108/02686900210447524

- IFAC. (2005). Environmental management accounting. International Guidance Document. International Federation of Accountants

- Jalaludin, D., Sulaiman, M., & Nazli Nik Ahmad, N. (2011). Understanding environmental management accounting (EMA) adoption: A new institutional sociology perspective. Social Responsibility Journal, 7(4), 540–557. https://doi.org/10.1108/17471111111175128

- Jamil, C. Z. M., Mohamed, R., Muhammad, F., & Ali, A. (2015). Environmental management accounting practices in small-medium manufacturing firms. Procedia - Social and Behavioral Sciences, 172, 619–626. https://doi.org/10.1016/j.sbspro.2015.01.411

- Keit, T. (2011). The application of Environmental management accounting amongst Kwa-Zulu Natal’s top businesses. Doctoral dissertation, University of KwaZulu-Natal. https://ukzn-dspace.ukzn.ac.za/bitstream/handle/10413/9530/Keit_Timothy_2011.pdf?sequence=1&isAllowed=y

- Khalid, F. M., Lord, B. R., & Dixon, D. K. (2012). Environmental management accounting implementation in environmentally sensitive industries in Malaysia. Proceedings of the 6th NZ management accounting conference, Palmerston North, New Zealand , 22–23 November 2012 (pp. 1–32). University of Canterbury: Department of Accounting and Information Systems. https://ir.canterbury.ac.nz/handle/10092/7376

- Kokubu, K., & Nashioka, E. (2005). Environmental management accounting practices in Japan. Eco-Efficiency in Industry and Science, 54(6), 321–342. https://doi.org/10.1007/1-4020-3373-7_16

- Marton-Williams, J. (1986). Questionnaire design in consumer market research handbook. (R. Worcester & J. Downham, Eds.). McGraw-Hill Book Company.

- Ministry of Industry and Trade. (2014). Decision No. 10508/QD-BCT November 18, 2014, giving approval for the plan on development of Vietnam’s paper industry up to 2020 and vision extended to 2025. https://vanbanphapluat.co/decision-no-10508-qd-bct-plan-development-vietnams-paper-industry-2020-2025.

- Ministry of Natural Resources and Environment. (2021). Report on the state of the national environment for the period 2016-2020. Dantri Publisher. https://moit.gov.vn/upload/2005517/fck/files/20211108_Bao_cao_HTMT_2016-2020_F_a4980.pdf

- Nguyen, D. T. (2011). Methods of scientific research in business. Labor and Social Publishing House.

- Nguyen, T. K. T. (2020). Studying factors affecting environmental accounting implementation in Mining Enterprises in Vietnam. Journal of Asian Finance, Economics, and Business, 7(5), 131–144. https://doi.org/10.13106/jafeb.2020.vol7.no5.131

- Nguyen, T. C., & Lai, V. M. (2021). Enterprises protect the environment with green growth and sustainable development. Natural Resources and Environment Magazine. https://tainguyenvamoitruong.vn/doanh-nghiep-bao-ve-moi-truong-voi-tang-truong-xanh-va-phat-trien-ben-vung-cid1494.html

- Nguyen, T. L. H., Nguyen, T. T. H., Nguyen, T. T. H., Le, T. H. A., & Nguyen, V. C. (2020). The Determinants of environmental information disclosure in Vietnam listed companies. Journal of Asian Finance, Economics, and Business, 7(2), 21–31. https://doi.org/10.13106/jafeb.2020.vol7.no2.21

- O’Neill, J., Wilson, D., Purushothaman, R., & Stupnytska, A. (2005). How Solid are the BRICs? Global Economics Paper No: 134. Goldman Sachs Economic Research Group. https://www.goldmansachs.com/insights/archive/archive-pdfs/how-solid.pdf

- Pham, X. T. (2022). Experience in developing the paper industry in China and some suggestions for Vietnam. Economy and Forecast Review. https://kinhtevadubao.vn/kinh-nghiem-phat-trien-nganh-giay-o-trung-quoc-va-mot-so-de-xuat-cho-viet-nam-21742.html

- Qian, W., Burritt, R., Chen, J., & John Sands,Prof. Ki-Hoon Lee, P. (2015). The potential for environmental management accounting development in China. Journal of Accounting and Organizational Change, 11(3), 406–428. https://doi.org/10.1108/JAOC-11-2013-0092

- Setthasakko, W. (2010). Barriers to the development of environmental management accounting: An exploratory study of pulp and paper companies in Thailand. European Medical Journal of Business, 5(3), 315–331. https://doi.org/10.1108/14502191011080836

- Tran, N. H., Nguyen, T. T. H., & Nguyen, T. P. (2021). Factors affecting an application of environmental management accounting: A case study of the automobile industry in Vietnam. Journal of Asian Finance, Economics, and Business, 8(7), 0509–0516. https://doi.org/10.13106/jafeb.2021.vol8.no7.0509

- UNDSD. (2001). Environmental management accounting: Procedures and principles. United Nations Division for Sustainable Development, United Nations.

- USEPA. (1995). Environmental accounting case studies: Green accounting at AT&T. The United States Environmental Protection Agency.

- Wachira, M. M. (2014). Factors influencing the adoption of environmental management accounting practices among firms in Nairobi, Kenya. Masters Thesis, University of Nairobi. https://su-plus.strathmore.edu/handle/11071/4270

- Wilmshurst, T. D., & Frost, G. R. (2001). The role of accounting and the accountant in the environmental management system. Business Strategy and the Environment, 10(3), 135–147. https://doi.org/10.1002/bse.283

- Zhu, Q., & Sarkis, J. (2004). Relationships between operational practices and performance among early adopters of green supply chain management practices in Chinese manufacturing enterprises. Journal of Operations Management, 22(3), 265–289. https://doi.org/10.1016/j.jom.2004.01.005

- Zutshi, A., & Sohal, A. S. (2004). Adoption and maintenance of environmental management systems: Critical success factors. Management of Environmental Quality, 15(4), 399–419. https://doi.org/10.1108/14777830410540144

APPENDIX A

Table A1. Describe the variables in the study