?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The primary purpose of this paper is twofold: firstly, to investigate the effect of early compliance with International Financial Reporting Standards 16 on Leases on earnings management and firm performance; secondly, to examine the moderating roles of corruption environment on those relationships. We test our hypotheses by investigating 1071 industrial firms in Southeast Asian countries, including Indonesia, Malaysia, Singapore, Thailand, and Vietnam using multivariate analyses. Our findings suggest that companies with lower governance mechanisms and looser institutional backgrounds are more likely to find that IFRS implementation may provide less room for management to maximize their short-term gain by manipulating earnings. Nevertheless, we do not find a similar pattern among the firms with low corruption culture. We also observe that firms’ performance in high corruption culture imposing early implementation of IFRS 16 is significantly higher than firms in low corruption culture. The results provide valuable input to the standard setters and regulators to consider the importance of a strong institutional framework in ensuring IFRS’s effective implementation.

1. Introduction

Currently, most countries have accepted the International Financial Reporting Standards as part of global accounting harmonization with more than 130 countries have encouraged their organizations to adopt or converge to International Financial Reporting Standards (IFRS). Mazzi et al. (Citation2018) argued that the change from national accounting standards to IFRS should increase firms’ information transparency while reducing economic value transactions.

There are many distinct differences in making the change from national GAAP to IFRS. One of the most notable differences between IFRS and national generally accepted accounting principles (GAAP) is the principles-based approach used in IFRS. In this regard, IFRS may not be detailed in every situation for every specific organizational operation (Kothari et al., Citation2010). Empirical findings, however, have not yet reached final agreements on whether one standard outperforms another (Key & Kim, Citation2020; Bertrand et al., Citation2020; Fuad et al., Citation2019).

For instance, the proponents of IFRS maintained that the standards could increase financial statements’ comparability and minimize reconciliation costs (Brochet et al., Citation2013). M. Barth et al. (Citation2008) and Leuz et al. (Citation2003) found that IFRS increases the transparency and reliability of accounting information and leads to better financial reporting qualities. On the other hand, few others have also suggested that IFRS may be problematic in several ways. First, IFRS is expensive and, hence, it may be difficult for the small and medium enterprises to pay unnecessary expenses during its implementation (Alves & Moreira, Citation2009). Second, IFRS has not yet conclusively proven to produce better accounting qualities (Ahmed et al., Citation2013). Recently, Adhikari et al. (Citation2021) noted that the implementation of IFRS converged standards led to higher discretionary accruals, less accounting conservatism, and lower value relevance of accounting information. Third, IFRS may result in higher earnings management because IFRS facilitates greater flexibility (Callao & Jarne, Citation2010; Capkun et al., Citation2016; Fuad & Wijanarto, Citation2017).

Our research focuses on the IFRS 16 implementation for the following reasons. Firstly, compared to other accounting standards, IFRS 16 has become one of the standards receiving the highest number of comment letters. Durocher and Fortin (Citation2011) argued that stakeholders’ participation positively affects the quality of accounting standards. Second, the change to IFRS 16 greatly affects firms’ financial structure and profitability, which shows the importance of the standard. Third, IFRS 16 allows firms to make early implementation before its effective date (e.g., 1 January 2019). Thus, categorizing firms as “mandatory or voluntary adopters” can be simply done by looking at the firms’ implementation date (before 1 January 2019, voluntary adopters and mandatory adopters are categorized otherwise).

As previously mentioned, before IFRS 16 took place, the lessees had two options in recognizing lease transactions: operation lease and finance lease. However, operating lease is considered an off-balance sheet financing, which could hide the assets and liabilities from being recorded on firms’ balance sheets, making comparability difficult (Beattie et al., Citation2006). International Accounting Standards Board (IASB) noted that more than 85% of the total lease commitments (US $ 3.3 trillion) do not appear on the firm’s balance sheets because of the options in selecting financial and operating leases. Giner and Pardo (Citation2018) further report that IFRS 16 aims to improve the financial transparency and quality of financial reporting. Our study examines whether the new standard provides less flexibility for management to engage in earnings management practices because lessees should recognize all the lease commitments on the balance sheet.

Brown et al. (Citation2014) statement that countries’ legal settings heavily influence financial reporting output is also applicable to our study. In this vein, the success of IFRS adoption goes beyond the implementation per se, but it requires the commitment from the regulators and government to monitor and enforce the IFRS implementation (Preiato et al., Citation2015). El-Halaly et al. (Citation2020) insisted that country-level IFRS adoption depends largely on its environmental settings, including corruption.

Although many researches have been dedicated to linking corruption and business and management settings, N. Houqe and Monem (Citation2016) argued that research is limited when it comes to finding a relationship between corruption and accounting quality. Tsalavoutas et al. (Citation2020) noted that multi-country studies were limited in exploring the cultural and country characteristics that contribute to IFRS compliance. Lewellyn and Bao (Citation2018) proposed that the level of corruption defines how the management and decision-makers rationalize the legitimacy of using accruals to manipulate earnings.

We also argue that firms with more effective and strong institutional environments and lower levels of corruption are more effective in implementing the IFRS (Chua et al., Citation2012; Mazzi et al., Citation2018, Citation2019). Agyei-Mensah (Citation2017), Zaidi and Huerta (Citation2014) on the other hand found that corruption mitigates the accounting quality offered by IFRS among countries with high corruption levels. El-Halaly et al. (Citation2020) also insist that IFRS implementation is likely to be more expensive in low as compared to the strong legal environments.

We study five countries in Southeast Asia: Indonesia, Singapore, Thailand, Vietnam, and Malaysia for their vibrant and dynamic regions. The Organization for Economic Co-operation and Development noted that Southeast Asian countries have become one of the fastest-growing economies in the world (OECD, Citation2019). On the other hand, countries in Southeast Asia shared similar cultures and geography (Noor, Citation2015). Therefore, our study inherently takes into account these differences. Furthermore, those countries allow early adoption of IFRS 16, and thus investigating the impact of voluntary implementation of IFRS 16 to firms’ earnings management and performance is plausible. We leave out other countries in Southeast Asia (the Philippines, Brunei Darussalam, Myanmar, Cambodia, Laos, and Timor-Leste) due to limited data availability and the close similarities with the countries mentioned above.

This study made important contributions in three ways to the literature. First, many relevant studies have explored the relationship between voluntary adoption of IFRS to earnings management. Unlike previous studies, we use IFRS 16 to test the early implementation of a particular accounting on earnings management and accounting performance. Apart from one of the most controversial standards that attracted many comment letters from stakeholders, IFRS 16 introduced huge impact on accounting information because it recognizes most leases on the balance sheet (Rey et al., Citation2020). Second, national corruption has become the main focus of policymakers, standard setters, and regulators worldwide. Thus, how the country’s institutional environment could play an important role in the effectiveness of IFRS implementation is paramount.

We present our study as follows. The second section discusses the institutional and political background and IFRS implementation in the sampled countries. The third section presents relevant literature, theoretical framework, and hypotheses development. Section 4 describes the data and results of our empirical tests. Findings and discussions are discussed in section 5 while section 6 concludes the study, elaborates the limitations, and proposes avenues for further research.

2. Institutional environment and accounting regulatory framework in Southeast Asia

The Association of Southeast Asian Nations is a multinational organization that was created in 1967 to promote intergovernmental cooperation on security, economics, culture, peace and stability, and agriculture. The ASEAN declaration was initially signed by Indonesia, Malaysia, the Philippines, Singapore, and Thailand, but soon other countries followed with the additions of Brunei Darussalam (in 1984), Vietnam (in 1995), Lao PDR (in 1997), Myanmar (in 1997), and Cambodia (in 1999).

As an umbrella organization, ASEAN Federation of Accountants was established in March 1997 to specifically advance accounting profession in the region. It also encourages cooperation ASEAN accountants to make cooperation and assistance through continued professional developments, accounting-related problem solving, information exchange, and assist other ASEAN business groups that are related to ASEAN accountants.

In 2014, all accountant institutions in 10 ASEAN countries signed a mutual recognition agreement to 1) facilitate accountant mobility to provide the accounting services in ASEAN countries, 2) increase the governing rules of accounting professionals among, and 3) information exchange to promote standards’ best practices and qualifications (aseancpa.org, 2020). Within this MRA, a professional accountant that holds the ASEAN CPA can provide accountancy services, except issuing and signing audit report and other accounting services that require domestic licensing. This means, therefore, that ASEAN CPA holder does not have to go through qualification procedures and retraining when they are about to provide the services in any other ASEAN countries.

2.1. Indonesia

Indonesian accounting regulatory started since the inception of its capital market in 1973. Indonesian Accounting Principles was developed by the Indonesian Institute of Accountants that mostly concurred with the US Generally Accepted Accounting Principles. In 1994, the Indonesian Institute of Accountants made a radical change to the accounting standards, and started to compile all the standards into an accessible book for wider users. The commitment of IFRS convergence in Indonesia started on 2 April 2009 among G 20 countries to use a single set of high-quality global accounting standards. In 2012, Indonesia declared that Indonesian financial accounting standards will be based on IFRS, although some exceptions and delays occurred.

On the other hand, Indonesia also issued other standards for different purposes. For instance, the Islamic Financial Accounting Standards Board issued Islamic accounting standards to accommodate the need for robust accounting standards for Islamic-based institutions that were growing rapidly in 2002. On the other hand, accounting standards for governmental institutions were also developed in 2010. According to the Governmental Act No. 71 of 2010, Governmental Accounting Standard should be used as guidelines in preparing transparent and accountable financial accounting reports for the local and central government. Numerous small and medium enterprises also require specific accounting standards to facilitate their needs. The Indonesian Institute of Accounting issued the Indonesian Accounting Standard for Non Publicly Accountable Entities in 2009 (SAK ETAP) which is a simplified form of Indonesian Financial Accounting Standard. Another set of accounting standards for micro, small, and medium enterprises was enacted on 18 May 2016 to facilitate the firms which were not facilitated by SAK ETAP.

2.2. Malaysia

Accounting profession in Malaysia can be traced back to early 1967 through the issuance of the Accountancy Act. The Malaysian Institute of Accountant regulates all accounting professions which is responsible under the Ministry of Finance. All companies registered in Malaysia are required to prepare the financial statements in accordance with the standards set by the Malaysian Accounting Standards Board (MASB). Nevertheless, foreign companies listed in Bursa Malaysia may use the International Financial Reporting Standard. Currently, MASB has issued two main standards, including a) Malaysian Financial Reporting Standards and b) Malaysian Private Entities Reporting Standards (MPERS), which as of 1 January 2016, replaced Private Entity Reporting Standards (PERSs).

2.3. Thailand

In 1997, Thailand began to use IAS standards as a reference for local accounting standards after referring to the US GAAP as the basis for their accounting principles (Saudagaran & Diga, Citation2000). At that time, 17 of 23 local accounting standards were based on IAS, while the rest still referred to US GAAP. The Federation of Accounting Professions (FAP) is responsible for setting Thai Accounting Standards (TAS). By December 2017, Thailand has adopted all IFRS standards with lag of 1 year from IFRS effective date except for some standards such as Financial Instrument (IAS 32 and 39; IFRS 7 and 9) and First Adoption of IFRS (IFRS 1; IFRS Foundation, Citation2017).

As for standards relating to financial instruments, FAP planned to adopt IFRS 7 and 9 in 2019. In addition, FAP also plans to adopt IFRS 15 (Revenue from Contract with Customer) in 2019, IFRS 16 (Leases) in 2020, and IFRS 17 (Insurance Contract) in 2022. Lag of 1 year from IFRS effective date is due to time needed for translation process and preparation. FAP requires the effective date of IFRS-based local accounting standard to be implemented no more than 1 year after IFRS effective date. Currently, Thailand Accounting Standards are substantially converged with IFRS Standards. (IFRS Foundation, Citation2017)

2.4. Singapore

Singapore is among the countries that adapted IAS after the foundation of IASC in 1973. Singapore began to issue IAS-based local accounting standards in 1977 although with the exception of certain standards that must be tailored within the Singapore context (Saudagaran & Diga, Citation2000). The process of adopting IFRS in Singapore took place gradually. Singapore began aligning its local standards, i.e. Singapore Financial Reporting Standards (SFRS) with IFRS in 2002. In 2003, all publicly traded companies were required to use SFRS which is similar to IFRS (IFRS Foundation, Citation2016). Singapore Accounting Standards Council (ASC) announced plans for full convergence of SFRS with IFRS in 2009 (IFRS Foundation, Citation2016).

On 29 May 2014, the Singapore Accounting Standards Council (ASC) announced the full convergence of IFRS for companies listed on the Singapore Stock Exchange (SGX) (ASC Secretariat, Citation2017). The ASC requires these companies to implement SFRS standards that are substantially converged with IFRS, with an effective date starting 1 January 2018 (ASC Secretariat, Citation2017). This also encourages the policy to permit all foreign companies listed on SGX to adopt IFRS.

2.5. Vietnam

Vietnam is one of ASEAN members that has successfully managed its centrally controlled economy to a market economy. This transition however requires better accountability and transparency in firms' financial reporting.

Consequently, Vietnam has become one of few countries that is aggressively in the process of transition from its national generally accepted accounting principles to IFRS. For example, between 2001 and 2005, Vietnam has developed 26 accounting standards which are based on IFRS/IAS (IAS Plus, Citation2009; PWC, Citation2018). Nguyen and Richard (Citation2011) and Nguyen and Tran (Citation2012) stated that this is one important requirement to be accepted as a World Trade Organization (WTO) member. Recently, Vietnam announced a clear, comprehensive roadmap for IFRS as an important milestone to improve its financial reporting quality. Narayan and Godden (Citation2000) stated the development and the settings of accounting standards are not the main responsibility of Vietnamese Accounting Association (VAA). Rather, they were mostly developed by the Ministry of Finance. On 23 March 2019, the Vietnam Ministry of Finance released the draft of IFRS road map for public comments. This road map plans to eliminate VAS and starts adopting the International Financial Reporting Standards (IFRS) by 2025. The road map, however, allows the companies to have different tracks to voluntarily or mandatorily adopt IFRS. As a matter of fact, some firms are allowed to apply Vietnamese Financial Reporting Standards.

3. Literature review and hypothesis development

3.1. The effect of early IFRS 16 adoption on earnings management

According to agency theory, management is in the best position to mislead stakeholders to provide the full story of the organizational performance (Jensen & Meckling, Citation1976) by using their judgment on financial reporting through earnings management. This can be done by choosing an accounting treatment that would maximize the utility of management but sacrificing the best interest of the shareholders.

Accounting literature usually categorizes earnings management into two main streams: real earnings management and accrual earnings management. Real earnings management is conducted by manipulating real operation activities (Dinh et al., Citation2016) and, hence, is less likely to be detected by auditors or regulators (Li et al., Citation2020). Accrual earnings management, on the other hand, is done through applying different accounting methods and techniques that may distort actual firms’ financial position and performance, although some may concur with the accounting standards. However, researchers have concluded that accrual earnings management is subject to under scrutiny by regulators and auditors because earnings management often does not represent the whole story of firm performance and position (Carangelo & Ferrillo, Citation2016).

Research on the positive effects of IFRS has cemented the premise that IFRS is of higher quality and therefore increases earnings informativeness (Gu et al., Citation2019) and results in better accounting quality (M. Barth et al., Citation2008; Landsman et al., Citation2012; M.E. Barth et al., Citation2012). In a study conducted in France, Zeghal et al. (Citation2012) found that earnings management is reduced in post-IFRS era. However, similar studies in Sweden and Germany by Paananen (Citation2008) and Paananen and Lin (Citation2009) concluded that earnings quality decreased after IFRS implementation.

We do not test whether the increase or decrease in accounting quality is due to mandatory IFRS implementation per se. However, we figure out whether firms that voluntarily implement IFRS 16 are less likely to use accruals opportunistically to manage their reported earnings. Capkun et al. (Citation2016) argue that firms engaging in earnings management are more likely to wait for the standards to become mandatory, reducing the spirit of transparency that IFRS carries. Similarly, M. Barth et al. (Citation2008) note that early adopters of IFRS exhibit less earnings management practices. H. B. Christensen et al. (Citation2015) argue that the negative association between early IFRS implementation and earnings management may be explained by the self-selection effect. In this regard, they argue that early adopters are more likely to signal their financial reporting quality by opting for early adoption of IFRS. On the other hand, Van Tendeloo and Vanstraelen (Citation2005) observe that voluntary adoption of IAS/IFRS is not associated with lower earnings management practices.

However, compared to few other standards that also allow early adoption prior to effective implementation date, IFRS 16 eliminates off-balance sheet financing such as structured lease transactions. Krische et al. (Citation2012) argued that theoretically any reduction in structured lease transaction should also reduce the earnings management. Nevertheless, since prior empirical evidence examining the relationship between IFRS adoption and earnings management was mixed; and research examining the accounting quality outcome of IFRS 16 was scarce, we state the following null hypothesis:

H1: Voluntary adoption of IFRS 16 does not affect earnings management.

3.2. Interaction effects of corruption environment and IFRS 16 early implementation to earnings management

Corruption can be defined in many different ways. Shleifer and Vishny (Citation1993) defined corruption as the opportunistic abuse of power or position to gain illegitimate private benefits through unauthorized activities (M.N. Houqe & Monem, Citation2016). The Association of Certified Fraud Examiners defined corruption as “wrongful use of influence to procure a benefit for the actor or another person, contrary to their duty or the rights of others” that can range from bribery, kickbacks, illegal gratuities, economic extortions, conflict of interest, among others. Numerous findings have proven the destructive nature of corruption such as reducing economic growth (Gupta et al., Citation2002), foreign direct investment (Cuervo-Cazurra, Citation2006), government spending on important areas (Wilhelm, Citation2002) and so on.

It has long been accepted that there is a two-way relationship between accounting and corruption. Accounting is essential for information monitoring and barriers to corruptive behaviors (Changwony & Paterson, Citation2020). A good and sound accounting information system may be able to protect shareholders’ funds from misuse and the reports they produce should be transparent and tell the real story of firms’ financial activities (Abdul-Baki et al., Citation2021). On the other hand, the country’s institutional background is responsible for the quality of companies’ accounting information. Corrupt government officials may be slightly reluctant to adopt new accounting standards that could lead to more transparent, accountable, and accurate accounting information (El-Halaly et al., Citation2020).

Malagueno et al. (Citation2010) proved that accounting quality is reduced among firms in highly corrupt countries. On the other hand, Kythreotis (Citation2015) maintained that the extent of countries’ corruption level negatively affects financial statement reliability. Related to IFRS, Zaidi and Huerta (Citation2014) suggested that corruption reduces the positive economic consequences of IFRS adoption it is supposed to bring. The enforcement mechanism is also important to improve the quality of financial information.

Hopper et al. (Citation2017) argued that the quality of accounting information is highly determined by the institutional environment that focuses on better compliance with regulations, strong external audits, more efficient judicial systems, and powerful law and order (Hope, Citation2003). In this regard, Leuz et al. (Citation2003) found that earnings management is less likely to occur in a country that has strong investor protection regulation. Bushman et al. (Citation2004) also insisted that a country’s political economy provides a solid platform for effective governance transparency that ensures the high-quality financial reporting.

Thus, country-level corruption may affect the relationship between IFRS 16 early implementation and accrual earnings management. As previously mentioned, the standard alone cannot decrease accrual earnings management (Jeanjean & Stolowy, Citation2008; Van Tendeloo & Vanstraelen, Citation2005). M.E. Barth et al. (Citation2012) and Landsman et al. (Citation2012) also insisted that IFRS may lead to better accounting quality in a strong enforcement environment, while poor enforcement is likely to cause the inconsistent implementation of regulatory rules (Oz & Yelkenci, Citation2018). On the other hand, earlier researchers such as N. Houqe and Monem (Citation2016) and Lourenco et al. (Citation2017) suggest that developed countries are not more likely to have more benefits from IFRS than their developing counterparts. Therefore, we state the following two-tailed interaction effect:

H2: Corruption levels affect the relationship between early adoption of IFRS 16 on earnings management.

3.3. Interaction effects of corruption environment and IFRS 16 early implementation to financial performance

H.B. Christensen et al. (Citation2009) maintained that the change from old to new accounting standards affects several vital accounts, most importantly profits. Many researchers have also concluded that good-quality accounting information reported under IFRS should contribute to the lower cost of equity (Ball, Citation2006) and increased value relevance to the decision-makers (Ewert & Wagenhofer, Citation2005). The use of the newly implemented IFRS standard has also been found to increase firm disclosure (Alfraih & Almutawa, Citation2014; Iatridis, Citation2011). In a country-level setting, Mhedhbi and Zeghal (Citation2016) found that the performance of emerging capital markets is positively associated with the use of international accounting standards.

Again, this study does not ignore the fact that adopting new accounting systems will depend highly on the country’s legal background and investor protection. Elshandidy and Hassanein (Citation2014) maintained that corporate governance as an enforcement mechanism is paramount to assure the effectiveness of IFRS. Marzuki and Wahab (Citation2018) on the other hand found that corruption weakens the negative relationship between IFRS implementation and accounting conservatism. Thus:

H3: The effect of IFRS 16 early adoption to financial performance is more pronounced among firms in low compared to high corruption environments.

4. Data and sampling procedures

Our study focuses on industrial firms in Southeast Asian Countries, including Indonesia, Singapore, Malaysia, Thailand, and Vietnam, which have the option to implement IFRS 19 earlier than its effective dates or wait for the standard to be mandatory. We further double-check whether the firms have adopted IFRS 16 or not in the firms financial statements. Data on accounting information and early adoption of IFRS 16 were extracted from Bloomberg database. Our initial data contains 1071 industrial firms to be analyzed from Indonesia, Malaysia, Singapore, Thailand, and Vietnam. The extent of corruption at the country level was extracted from the corruption perception index which was measured by transparency.org.

Table shows that Vietnam and Malaysia have the most observations over the sample period, with 466 and 208 companies, respectively (about 66.14%). Singapore, Thailand, and Indonesia followed, with 128, 125, and 92 companies, respectively. However, our data indicate that no company from Vietnam opted for early implementation of IFRS 16, while only one company from Indonesia chose to do so. Most Singaporean and Malaysian companies have already implemented IFRS 16 before its effective implementation date, which comprises 66.40% and 62.02%, respectively.

Table 1. Statistics for IFRS 16 early implementation among firms in Southeast Asia

4.1. Measurements

4.1.1. Earnings management

Although earnings management may be classified into real earnings management and discretionary accruals, we focus on the latter using modified Jones developed by Dechow et al. (Citation1995) for several reasons. First, IFRS imposes considerable judgment and provides managers with substantial discretion; which is captured in discretionary accruals. Since real earnings management is conducted by manipulating real operation activities (Dinh et al., Citation2016), it is difficult to estimate how IFRS affects the professional judgment provided in accounting allowing greater manipulation. Second, the modified Jones model is one of the most famous models to detect earnings management (Chen, Citation2010).

The formula for calculating discretionary expenses started with estimating the following equation to find their estimated parameters:

The parameters found in Equationeq (1)(1)

(1) are used to calculate discretionary accruals, as follows

Where, DISACC is the company’s discretionary accruals. TA/A is total accruals, which is net profit minus net cash from operating activities divided by firms’ total assets; A is total assets; ∆ REV is the change in company’s revenue divided by total assets minus change in company receivables divided by total assets; ∆ REC/A is the change in firms’ receivables divided by total assets; PPE/A is the company’s property plant and equipment divided by total assets. This study uses return on assets to measure firms’ financial performance, which is the net income divided by total assets.

4.1.2. Early implementation of IFRS 16

We use the early implementation of IFRS 16 as a measure for voluntary implementation of IFRS. IFRS 16 is a guideline developed by the International Accounting Standard Board for accounting lease. Most companies use leasing to get access to their assets and therefore are affected by this standard. We use IFRS 16 for the voluntary implementation of accounting standards because it offers early implementation (see Table for the statistics of early implementation in Southeast Asia). Although other standards (for instance, IFRS 15 regarding revenue from contracts with customers, among others) permit early adoption prior to its effective implementation date, IFRS 16 practically eliminates off-balance sheet financing such as structured lease transactions. Theoretically, any reduction on structured lease transactions should also reduce the earnings management (Krische et al., Citation2012)

Table 2. Variables description

This variable is measured using a binary indicator, in which 1 if the firms chose to adopt IFRS 16 before its effective implementation date, and 0 is otherwise. Data for this variable were obtained from the Bloomberg Database.

4.1.3. Corruption

As previously stated, we defined corruption as an opportunistic behavior to wrongfully use the power or influence to get illegitimate benefits through unauthorized activities (Shleifer & Vishny, Citation1993) that can range from bribery, kickbacks, illegal gratuities, economic extortions, conflict of interest, among others. This study used corruption perception index (CPI) from Transparency International that has been widely used in accounting research (Mazzi et al., Citation2019; Liu, Citation2016, among others). CPI scores are based on the perception of groups of experts regarding the severity of corruption in daily business operations. Higher CPI scores indicate lower levels of corruption.

4.2. Earnings management, early implementation of IFRS 16, corruption, and performance

We run three regression models to test the hypotheses. While model 1 tests the first hypothesis, absolute discretionary accruals as a measure of earnings management is regressed on IFRS 16 and other control variables, model 2 tests our second hypothesis by regressing the interaction products of IFRS16 and corruption against discretionary accruals. Model 3 tests the moderating effect of corruption on the relationship between IFRS 16 and financial performance.

Where DISACC is discretionary accruals, calculated from Equationequation 2(2)

(2) , IFRS16 is a dummy variable of 1 where the companies implement IFRS 16 earlier than its effective date and 0 where the companies wait for the standard to be mandatory. SALESGROWTH is the annual percentage change in revenues or sales. CFO is the total cash flow from operations divided by the total assets, and PPE is the total gross of property plant and equipment divided by total assets. SIZE is natural logarithm of total assets, while revenue is the total sales divided by total assets, and receivables are the total receivables deflated by total assets. The first hypothesis is tested from the estimated parameter of β1 from EquationEq. 3

(Model 3)

(Model 3) . For the second hypothesis, we regressed DISACC, on the independent and control variables plus the moderating variable, CORRUPTION and interaction product of CORRUPTION and IFRS 16. The third hypothesis, examining whether corruption affects the relationship between early adoption of IFRS 16 to earnings management, is based on the estimated coefficient of β3 from Eq. 4. The third hypothesis focuses on the moderating effect of CORRUPTION on the relationship between IFRS16 and firm performance (return on assets/ROA). We test the third hypothesis based on the significance of the estimated parameter of β3 from Eq. 5. The control variables used in the EquationEq. 3

(Model 3)

(Model 3) and Eq. 4 are also implemented in Eq. 5.

5. Results and discussion

5.1. Descriptive statistics

In addition, Table provides descriptive statistics for the variables used in the analysis, for total samples, and comparisons across country. The table also presents the univariate mean comparisons to demonstrate any potential differences among the variables and the country. The means of CFO, SALESGROWTH, DISACC, and ROA are not statistically different across country. However, the means of PPE, REVENUE, RECEIVABLE, and SIZE are statistically different across country.

Table 3. Descriptive statistics and univariate differences of variables at country levels

On the other hand, results on Table also display the descriptive statistics on the extent of IFRS 16 implementation for the important variables as well as univariate statistics to test the differences of the variables across the IFRS 16 implementation. Our univariate analyses found that while CFO, PPE, SALESGR, and DISACC are not statistically different across IFRS 16 implementation, REV, RECEIVABLES, and SIZE are. Interestingly, we found that the mean and standard deviation of discretionary accruals are higher among the firms that have not implemented IFRS 16 (mean = .0941; SD = .331) than firms that have implemented IFRS 16 (mean; .0719; SD = .009). These differences urge the need to test the multivariate models to test the impacts of IFRS adoption, corruption, and legal environments on earnings management and financial performance.

Table 4. Descriptive statistics and test of univariate differences of important variables at country levels

Table reports the Pearson correlations and their statistical significance for all the variables used in this study. Our initial findings indicate that there is no harmful multicollinearity issue that may impair the validity of the results. All the correlations among the independent variables are less than 0.8. Further diagnostics in our untabulated results in multivariate regressions also indicate that value inflation factor (VIF) and condition indexes are all below the cutoff threshold of 10 and 30, respectively.

Table 5. Correlation matrix

Table presents the multivariate statistics of three models. Model 1 tests the impacts of IFRS 16 adoption on earnings management in hypothesis 1, while model 2 tests whether the negative effects of IFRS 16 early implementation on earnings management are stronger among firms in the high corruption environment. Model 3 tests the moderating roles of corruption levels on the relationship between IFRS 16 to performance as in the third hypothesis. Our findings indicate that earnings management practices are not influenced by firms that chose to adopt IFRS 16 (coefficient of model 1 = .00248, p > 0.05). This finding confirms our first null hypothesis that the early implementation of IFRS 16 does not affect management likelihood to engage in earnings management. In a recent Monte Carlo simulation regarding the consequences of IFRS 16, Giner et al. (Citation2019) found that reducing the life lease contracts may smooth the key financial ratios. They further found that the transition to IFRS 16 does not necessarily bring improvement on firms’ financial performance. Therefore, management may not be compelled to rationalize this new accounting standard for earnings management purposes.

Table 6. Multiple regression results to test H1−H3

On the other hand, based on the results of model 2, we found that the interaction variable of IFRS 16 and corruption is negative and significant in affecting the earnings management (estimate: .0008601, p < 0.1). This finding supports our second hypothesis that corruption positively affects the relationship between IFRS 16 and earnings management. These results are in line with Leuz et al. (Citation2003) suggestion that earnings management is less likely to occur in a country that has strong investor protection regulations. Similarly, Bushman et al. (Citation2004) also insisted that a country’s political economy provides a solid platform for effective governance transparency that ensures the high-quality financial reporting.

In our third model, we show support for our third hypothesis. Interestingly, the coefficient on CORRUPTION*IFRS, −.0008294, is negative and statistically significant (p < 0.1). This finding shows that the financial performance of firms that implement IFRS 16 earlier than its effective date is higher in a high corruption environment. Our study may hint at the fact that the implementation of IFRS may not be effective if not coupled with a stronger institutional environment. This finding is consistent with Elshandidy and Hassanein (Citation2014), Marzuki and Wahab (Citation2018), and Elshandidy and Hassanein (Citation2014) which suggested that corporate governance as an enforcement mechanism is important to assure the effectiveness of IFRS. On the other hand, Marzuki and Wahab (Citation2018) find that corruption weakens the negative relationship between IFRS implementation and accounting conservatism. Our results are controlled by firms characteristics, including sales growth, operating cash flows, property plant and equipment, firm size, and notes receivable.

5.2. Additional tests

Based on the results presented in Table , we can understand more the mechanism of the relationships among corruption, early implementation of IFRS 16, and earnings management. We run this by manipulating our equation to test the moderating role of corruption in the relationship between IFRS early implementation and earnings management. Our main regression equation (control variables held constant) is:

Since IFRS is measured using a binary variable of 0 for firms that wait for the IFRS 16 to become mandatory, and 1 otherwise (firms that choose earlier adoption of IFRS 16 before its implementation date), the above equation can be restated as follows:

If a firm waits for mandatory IFRS = 0, the above equation (EquationEq. 6)(6)

(6) can be restated as:

(7)

However, if firms choose an earlier adoption of IFRS 16 (IFRS 16 = 1), the regression equation (EquationEq. 6)(6)

(6) would be:

Hence, we can estimate the joint relationships of early IFRS 16 implementation and levels of corruption on earnings management (or performance), as displayed in the following table.

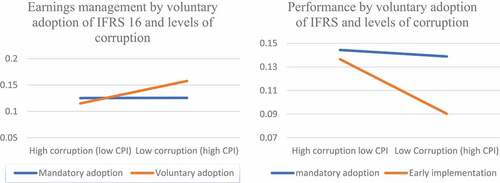

The results depicted in Table indicate that early implementation of IFRS 16 is more likely to engage in earnings management practices among firms with a high perceived corruption index. On the contrary, earnings management practices are more common among firms in low CPI countries implementing IFRS 16 before its effective date. Our studies support the findings stating that countries with high corruption could benefit more from IFRS experience than developed countries. Our findings, however, should not be interpreted in a way that a higher level of corruption (lower CPI) increases accounting quality per se. On the contrary, we are convinced that management in a highly corrupt environment will be more likely “to transfer their belief systems to other forms”, such as misled accounting information (Lewellyn & Bao, Citation2018). However, when put into the context of early implementation of IFRS (or voluntary implementation), companies that have lower governance mechanisms and looser institutional backgrounds are more likely to find that IFRS implementation may provide less room for management to maximize their short-term gain by manipulating earnings. Mongrut and Winkelried (2019) also found that adoption of IFRS guarantees better transparency in emerging markets. Interestingly, we do not find such pattern among the firms with low corruption culture. Callao and Jarne (Citation2010) obtained an increase in earnings management since the adoption of IFRS in 11 EU stock markets. A study conducted by Capkun et al. (Citation2016) in 29 countries prove that flexibility and subjective estimates offered by the IFRS implementation have led to greater earnings management practices.

Table 7. The relationships between IFRS 16 implementation, earnings management (EM), and corruption levels

We offer another explanation for the increase in earnings management among early adopters in low corruption culture. Bertrand et al. (Citation2020), Florou and Kosi (Citation2015), and De Lima et al. (Citation2018) state that the earlier implementation of IFRS 16 provides the companies easier access to debt. Easier debt access may be more intensified among firms in the low corruption culture because formal debt providers may consider that IFRS improves financial reporting quality. However, Mendoza et al. (Citation2020) found that companies with higher leverage carry out more likelihood for the managers to engage in earnings management practices.

We also note that early implementation of IFRS 16 does not bring about higher performance. However, the performance of firms in high corruption culture that impose the early implementation of IFRS 16 is significantly higher than firms in a low corruption culture. Again, our findings suggest that IFRS 16 brings greater positive effects to the firms that have low and loose institutional backgrounds. Barniv et al. (Citation2022) document that the relationship between IFRS experience and forecast accuracy is most pronounced in countries with large differences between domestic generally accepted accounting principles (GAAP) and IFRS. Hsu and Chen (Citation2020) found that a reduction in earnings management and an increase in earnings predictive ability can be observed among firms that use mandatory IFRS adoption. All in all, we find that early IFRS 16 implementation does not necessarily bring about higher performance, either in higher or lower CPI countries. In line with prior research, we argue that the complexity of adopting IFRS may be the reason for the lower performance. Firms may need more time to prepare the resources for effective IFRS 16 implementation by training accounting staffs and financial professionals (Ballas et al., Citation2010; Jones & Finley, Citation2011).

Figure visualizes how corruption culture could change the relationship between IFRS 16 early implementation and earnings management.

Figure 1. Earnings management and performance by voluntary adoption of IFRS and levels of corruption.

5.3. Robustness test

We also perform a set of robustness tests to assure the consistency of our findings. First, we test whether the institutional environment (e.g., law systems and rule of law) moderates the relationship between IFRS and earnings management and performance. Second, as our residual analyses find that our study encounters some multivariate non-normality and heteroscedasticity, we re-estimate models with 1,000 bootstrapped regression and examine whether the results hold.

5.3.1. Institutional environment on early IFRS 16 implementation and earnings management

Numerous literature argue that institutional environments in which the companies operate are multi-dimensional, and they are often measured differently. Ahmed et al. (Citation2013) argued that the positive consequence of IFRS highly depends on the enforcement mechanism the newer standard brings. Akisik (Citation2020) maintained that if the IFRS would have higher quality relative to the national accounting standards if followed with better enforcement. Therefore, rather than use corruption per se, we also use rule of law score as our moderating variable and investigate its impact on the relationship between early adoption of IFRS 16 to earnings management. The score is based on the index developed by the World Bank. The score ranges from −2.5 to 2.5. It measures the extent to which the agents believe in society’s rules and the quality of contract enforcement and other regulations.

We also examine whether the legal system plays a vital role in modifying the effect of IFRS 16 early implementation to earnings management and financial performance. Ball (Citation2006) maintained that IFRS are based on common law systems that put more emphasis on financial disclosure and market activities. However, Oz and Yelkenci (Citation2018) stated that more code law countries are adopting the IFRS despite having different institutional settings. In this regard, Ball et al. (Citation2010) argued that companies in code law countries that adopt IFRS are more likely to carry out opportunistic accounting behavior through discretionary earnings management. We use the legal systems with a dummy equal to 1 if firms’ country is using on common law, and 0 is otherwise.

Our robustness tests are presented in Table . The results indicate that the statistical coefficients of interaction products of rule of law and IFRS confirm our initial analysis. This shows that our findings are quantitatively robust.

Table 8. Robustness test with institutional variables interactions

5.3.2. Residual analyses and bootstrapping regression models

Our results may indicate that the low adjusted r-square could question the validity of our regression models and the goodness of a fitted model. Checking the underlying assumption of residual is important because the regression tests are based on the following assumptions concerning the error term: (1) ε is randomly distributed with an expected value of 0 (multivariate normality), (2) the variance of ε is the same for all values of x (heteroscedasticity), and (3) the values of ε are independent (autocorrelation).

We run several tests to check if the residuals on our models are not randomly and normally distributed. First, we test the skewness and kurtosis for normality. The probability of the skewness and kurtosis test for normality is all significant at 0.05 indicating that the residuals are not normally and asymptotically distributed. We also find the same findings after rechecking our multivariate normality using Mardia’s multivariate skewness and kurtosis tests, Doornik-Hansen omnibus and Henze-Zirkler consistent tests. Heteroscedasticity was checked using the Breusch Pagan test to find out whether there is any systematic change in the variance of residuals over a range of measured values. The results also indicate the presence of mediocre heteroscedasticity. Moran’s I was used to test for the presence of spatial autocorrelation. The Moran’s I test indicates that no spatial autocorrelation is found in our models.

To address the possible issue that our findings are not robust due to violations of classical assumptions, we decided to run several methods. First, all the regression models are estimated by generating robust estimators for standard errors that account for heteroscedasticity in residual distribution. The un-tabulated results remain consistent with our previous findings.

Second, we use bootstrapping regression models, which is a non-statistical approach to statistical inference by resampling the dataset with replacement from the original data. The bootstrapping can be used to generate more accurate inferences when data are not normally distributed or have relatively small sample size. Using 1,000 resampling data, our results are quantitatively identical to our earlier findings.

5.3.3. Alternative measure of earnings management

We also test whether the early implementation of IFRS 16 affects the upward or downward earnings management separately. However, the results do not show any significant effect and, hence, the results are not shown here.

6. Conclusion

This research provides a way out of the debate whether the success of accounting standards should also be followed by strengthening the country’s institutional background. Particularly, this study examines whether the voluntary implementation of IFRS (measured by early implementation of IFRS 16) coupled with strong anti-corruption culture are negatively associated with the earnings management practices while positively associated with firms’ performance.

We used 1071 industrial firms from countries in Southeast Asia, including Indonesia, Singapore, Malaysia, Thailand, the Philippines, and Vietnam to test the propositions. Our univariate tests indicate that larger firms are much more likely to voluntarily implement the IFRS 16 compared to the smaller firm size. When testing univariate differences at the country level, we also find the significant differences among the countries.

Our study supports the findings stating that countries with high corruption could benefit more from IFRS experience than developed countries. In this case, companies that have lower governance mechanisms and looser institutional backgrounds are more likely to find less flexibility by manipulating earnings after IFRS implementation. We also note that early implementation of IFRS 16 does not bring about higher performance. However, the performance of firms in high corruption culture that impose early implementation of IFRS 16 is significantly higher than firms in a low corruption culture.

This research has an important implication for researchers and practitioners. We conjecture that the findings should provide IASB with preliminary information to consider that IFRS implementation’s consequences and efficacy are greatly affected by firms’ institutional background.

Further researchers should also address the limitations of the study. First, due to data difficulty in measuring the transition process from national GAAP to IFRS at the company level, we only use IFRS 16 to measure compliance with standard implementation. Although the use of IFRS 16 implementation as a proxy for mandatory vis-a-vis voluntary adopters regarding the transparency of lease accounting commitment is sufficient, our findings cannot be generalized to the whole international accounting standards. Second, we do not categorize the financial impacts of IFRS 16 on the lessor or lessee. Although this may require sophisticated and time-consuming data collection and analyses, it should be fruitful to better understand the accounting mechanism of this radical transition. We leave this interesting issue to the future researchers.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Fuad Fuad

Fuad Fuad is a lecturer and Head of the Department of Accounting, Faculty of Economics and Business, Diponegoro University. He received his Ph.D. in the area of Accounting from Universiti Sains Malaysia.

References

- Abdul-Baki, Z., Uthman, A., & Kasum, A. (2021). The role of accounting and accountants in the oil subsidy corruption scandals in Nigeria. Critical Perspectives on Accounting, 781, 102128. https://doi.org/10.1016/j.cpa.2019.102128

- Aboody, D., Hughes, J., & Liu, J. (2005). Earnings quality, insider trading, and cost of capital. Journal of Accounting Research, 43(5), 651–23. https://doi.org/10.1111/j.1475-679X.2005.00185.x

- Adhikari, A., Bansal, M., & Kumar, A. (2021). IFRS convergence and accounting quality: India a case study. Journal of International Accounting, Auditing and Taxation, 45, 100430. https://doi.org/10.1016/j.intaccaudtax.2021.100430

- Agyei-Mensah, B. K. (2017). Does the corruption perception level of a country affect listed firms’ IFRS 7 risk disclosure compliance? Corporate GovernanceInternational Journal of Business in Society, 17(4), 727–747. https://doi.org/10.1108/CG-10-2016-0195

- Ahmed, A. S., Neel, M. J., & Wang, D. (2013). Does mandatory adoption of IFRS improve accounting quality? Preliminary evidence. Contemporary Accounting Research, 30(4), 1344–1372. https://doi.org/10.1111/j.1911-3846.2012.01193.x

- Akisik, O. (2020). The impact of financial development, IFRS and rule of LAW on foreign investments: A cross-country analysis. International Review of Economics and Finance, 69, 815–838. https://doi.org/10.1016/j.iref.2020.06.015

- Alfraih, M. M., & Almutawa, A. M. (2014). Firm-specific characteristics and corporate financial disclosure: Evidence from an emerging market. International Journal of Accounting and Taxation, 2(3), 55–78. https://doi.org/10.15640/ijat.v2n3a4

- Alves, P. A. P., & Moreira, J. A. C. (2009). The adoption of the international financial reporting standards in Portugal. Revista Universo Contabil, 5(3), 156–164. http://dx.doi.org/10.4270/ruc.20095

- ASC Secretariat. (2017). Accounting standards council issues new Singapore financial reporting standards (International). https://www.asc.gov.sg/news-events/local-news/accounting-standards- council-issues-new-singapore-financial-reporting-standards-(international) accessed 12 November 2020

- Ball, R. (2006). International Financial Reporting Standards (IFRS): Pros and cons for investors. Accounting and Business Research, 36(sup 1), 5–27. https://doi.org/10.1080/00014788.2006.9730040

- Ballas, A. A., Skoutela, D., & Tzovas, C. A. (2010). The relevance of IFRS to an emerging market: Evidence from Greece. Managerial Finance, 36(11), 931–948. https://doi.org/10.1108/03074351011081259

- Barniv, R. R., Myring, M., & Westfall, T. (2022). Does IFRS experience improve analyst performance?. Journal of International Accounting, Auditing and Taxation, 46, 100443. https://doi.org/10.1016/j.intaccaudtax.2021.100443

- Barth, M., Landsman, W., & Lang, M. (2008). International accounting standards and accounting quality. Journal of Accounting Research, 46(3), 467–498. https://doi.org/10.1111/j.1475-679X.2008.00287.x

- Barth, M. E., Landsman, W. R., Lang, M., & Williams, C. (2012). Are IFRS-based and US GAAP-based accounting amounts comparable?. Journal of Accounting and Economics, 54(1), 68–93. https://doi.org/10.1016/j.jacceco.2012.03.001

- Beattie, V., Goodacre, A., & Thompson, S. J. (2006). International lease-accounting reform and economic consequences: The views of U.K. users and prepares. The International Journal of Accounting, 41(1), 75–103. https://doi.org/10.1016/j.intacc.2005.12.003

- Bertrand, J., Brebisson, H., & Burietz, A. (2020). Why choosing IFRS? Benefits of voluntary adoption by European private companies. International Review of Law and Economics. https://doi.org/10.1016/j.irle.2020.105968

- Brochet, F., Jagolinzer, A. D., & Riedl, E. J. (2013). Mandatory IFRS adoption and financial statement comparability. Contemporary Accounting Research, 30(4), 1373–1400. https://doi.org/10.1111/1911-3846.12002

- Brown, P., Preiato, J., & Tarca, A. (2014). Measuring country differences in enforcement of accounting standards: An audit and enforcement proxy. Journal of Business Finance & Accounting, 41(1–2), 1–52. https://doi.org/10.1111/jbfa.12066

- Bushman, R. M., Piotroski, J. D., & Smith, A. J. (2004). What determines corporate transparency. Journal of Accounting Research, 42(2), 207–252. https://doi.org/10.1111/j.1475-679X.2004.00136.x

- Callao, S., & Jarne, J. I. (2010). Have IFRS affected earnings management in the European Union?. Accounting in Europe, 7(2), 159–189. https://doi.org/10.1080/17449480.2010.511896

- Capkun, V., Collins, D., & Jeanjean, T. (2016). The effect of IAS/IFRS adoption on earnings management (smoothing): A closer look at competing explanations. Journal of Accounting and Public Policy, 35(4), 352–394. https://doi.org/10.1016/j.jaccpubpol.2016.04.002

- Carangelo, R., & Ferrillo, P. (2016). SEC, financial reporting, and financial fraud. Harvard Law School Forum on Corporate Governance. https://corpgov.law.harvard.edu/2016/06/01/sec-financial-reporting-and-financial-fraud/ accessed 8 December 2020

- Changwony, F. K., & Paterson, A. S. (2020). Accounting practice, fiscal decentralization and corruption. The British Accounting Review, 51(5), 100834. https://doi.org/10.1016/j.bar.2019.04.003

- Chen, T. (2010). Analysis on accrual-based models in detecting earnings management. Lingnan Journal of Banking, Finance and Economics, 2, 1–10. http://commons.ln.edu.hk/ljbfe/vol2/iss1/5

- Christensen, H. B., Lee, E., & Walker, M. (2009). Do IFRS/UK-GAAP reconciliations convey new information?. Journal of Accounting Research, 47(5), 1167–1199. https://doi.org/10.1111/j.1475-679X.2009.00345.x

- Christensen, H. B., Lee, E., Walker, M., & Zeng, C. (2015). Incentives or standards: What determines accounting quality changes around IFRS adoption?. European Accounting Review, 24(1), 31–61. https://doi.org/10.1080/09638180.2015.1009144

- Chua, Y. L., Cheong, C. S., & Gould, G. (2012). The impact of mandatory IFRS adoption on accounting quality: Evidence from Australia. Journal ofInternational Accounting Research, 11(1), 119–146. https://doi.org/10.2308/jiar-10212

- Cuervo-Cazurra, A. (2006). Who cares about corruption?. Journal of International Business Studies, 37(6), 807–822. https://doi.org/10.1057/palgrave.jibs.8400223

- Dechow, P. M., Sloan, R. G., & Sweeney, A. P. (1995). Detecting earnings management. The Accounting Review, 70(2), 193–225. https://www.jstor.org/stable/248303

- de Lima, V. S., de Lima, G. A. S. F., & Gotti, G. (2018). Effects of the adoption of IFRS on the credit market: Evidence from Brazil. The International Journal of Accounting, 53(2), 77–101. https://doi.org/10.1016/j.intacc.2018.04.001

- Dinh, T., Kang, H., & Schultze, W. (2016). Capitalizing research & development: Signaling or earnings management?. European Accounting Review, 25(2), 373–401. https://doi.org/10.1080/09638180.2015.1031149

- Durocher, S., & Fortin, A. (2011). Practitioners’ participation in the accounting standard setting process. Accounting and Business Research, 41(1), 29–50. https://doi.org/10.1080/00014788.2011.549635

- El-Halaly, M., Ntim, C. G., & Al-Gazzar, M. (2020). Diffusion theory, national corruption and IFRS adoption around the world. Journal of International Accounting, Auditing and Taxation, 38, 100305. https://doi.org/10.1016/j.intaccaudtax.2020.100305

- Elshandidy, T., & Hassanein, A. (2014). Do IFRS and board of directors’ Independence affect accounting conservatism?. Applied Financial Economics, 24(16), 1091–1102. https://doi.org/10.1080/09603107.2014.924291

- Ewert, R., & Wagenhofer, A. (2005). Economic effects of tightening accounting standards to restrict earnings management. The Accounting Review, 80(4), 1101–1124. https://doi.org/10.2308/accr.2005.80.4.1101

- Florou, A., & Kosi, U. (2015). Does mandatory IFRS adoption facilitate debt financing?. Review of Accounting Studies, 20(4), 1407–1456. https://doi.org/10.1007/s11142-015-9325-z

- Fuad, Juliarto, A., & Harto, P. (2019). Does IFRS convergence really increase accounting qualities? Emerging market evidence. Journal of Economics, Finance and Administrative Science, 24(48), 205–220. https://doi.org/10.1108/JEFAS-10-2018-0099

- Fuad, & Wijanarto, W. T. (2017). How mandatory IFRS adoption changes firms’ opportunistic behavior: Empirical evidences from the earnings management perspective. Academy of Accounting and Financial Studies Journal, 21(2), 1–10. https://www.abacademies.org/articles/how-mandatory-ifrs-adoption-changes-firms-opportunistic-behavior-empirical-evidences-from-the-earnings-management-perspective-6731.html

- Giner, B., Merello, P., & Pardo, F. (2019). Assessing the impact of operating lease capitalization with dynamic Monte Carlo Simulation. Journal of Business Research, 101, 836–845. https://doi.org/10.1016/j.jbusres.2018.11.049

- Giner, B., & Pardo, F. (2018). The value relevance of operating lease liabilities: Economic effects of IFRS 16. Australian Accounting Review, 28(4), 496–511. https://doi.org/10.1111/auar.12233

- Gu, Z., Ng, J., & Tsang, A. (2019). Mandatory IFRS adoption and management forecasts: The impact of enforcement changes. China Journal of Accounting Research, 12(1), 33–61. https://doi.org/10.1016/j.cjar.2018.09.001

- Gupta, S., Davoodi, H., & Alonso-Terme, R. (2002). Does corruption affect income inequality and poverty?. Economics of Governance, 3(1), 23–45. https://doi.org/10.1007/s101010100039

- Hope, O. K. (2003). Disclosure practices, enforcement of accounting standards, and analysts’ forecast accuracy: An international study. Journal of Accounting Research, 41(2), 235–272. https://doi.org/10.1111/1475-679X.00102

- Hopper, T., Lassou, P., & Soobaroyen, T. (2017). Globalisation, accounting and developing countries. Critical Perspectives on Accounting, 43, 125–148. https://doi.org/10.1016/j.cpa.2016.06.003

- Houqe, M. N., & Monem, R. M. (2016). IFRS adoption, extent of disclosure, and perceived corruption: A cross-country study. The International Journal of Accounting, 51(3), 363–378. https://doi.org/10.1016/j.intacc.2016.07.002

- Houqe, N., & Monem, R. (2016). IFRS adoption, extent of disclosure and perceived corruption: A cross- country study. The International Journal of Accounting, 51(2), 363–378. https://doi.org/10.1016/j.intacc.2016.07.002

- Hsu, F. J., & Chen, S. H. (2020). Does corporate social responsibility drive better performance by adopting IFRS? Evidence from emerging market. Journal of Computational and Applied Mathematics, 371, 112631. https://doi.org/10.1016/j.cam.2019.112631

- IAS Plus. (2009). Accounting standards updates by jurisdiction-Vietnam. http://www.iasplus.com/country/vietnam.htm. accessed 12 November 2020

- Iatridis, G. E. (2011). Accounting disclosures, accounting quality and conditional and unconditional conservatism. International Review of Financial Analysis, 20(2), 88–102. https://doi.org/10.1016/j.irfa.2011.02.013

- IFRS Foundation. (2016). IFRS application around the world jurisdictional profile: Singapore. https://www.ifrs.org/use-around-the-world/use-of-ifrs-standards-by-jurisdiction/singapore/ accessed 12 November 2020

- IFRS Foundation. (2017). IFRS application around the world jurisdictional profile: Thailand. https://www.ifrs.org/use-around-the-world/use-of-ifrs-standards-by-jurisdiction/thailand/. accessed 12 November 2020

- Jeanjean, T., & Stolowy, H. (2008). Do accounting standards matter? An exploratory analysis of earnings management before and after IFRS adoption. Journal of Accounting and Public Policy, 27(6), 480–494. https://doi.org/10.1016/j.jaccpubpol.2008.09.008

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economic, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jones, S., & Finley, A. (2011). Have IFRS made a difference to intra-country financial reporting diversity?. British Accounting Review, 43(1), 23–38. https://doi.org/10.1016/j.bar.2010.10.004

- Key, G. K., & Kim, J. Y. (2020). IFRS and accounting quality: Additional evidence from Korea. Journal of International Accounting, Auditing and Taxation, 39, 1–12. https://doi.org/10.1016/j.intaccaudtax.2020.100306

- Kothari, S. P., Ramanna, K., & Skinner, D. J. (2010). Implications for GAAP from an analysis of positive research in accounting. Journal of Accounting and Economics, 50(2–3), 246–286. https://doi.org/10.1016/j.jacceco.2010.09.003

- Krische, S. D., Sanders, P. R., & Smith, S. D. (2012). Lease transaction structuring, earnings management, and management credibility. Research in Accounting Regulation, 24(1), 33–39. https://doi.org/10.1016/j.racreg.2011.12.004

- Kythreotis, A. (2015). The interrelation among faithful representation (reliability), corruption and IFRS adoption: An empirical investigation. International Journal of Business and Economic Sciences Applied Research, 8(1), 25–50. https://ideas.repec.org/a/tei/journl/v8y2015i1p25-50.html

- Landsman, W. R., Maydew, E. L., & Thornock, J. R. (2012). The information content of annual earnings announcements and mandatory adoption of IFRS. Journal of Accounting and Economics, 53(1–2), 34–54. https://doi.org/10.1016/j.jacceco.2011.04.002

- Leuz, C., Nanda, D., & Wysocki, P. D. (2003). Earnings management and investor protection: An international comparison. Journal of Financial Economics, 69(3), 505–527. https://doi.org/10.1016/S0304-405X(03)00121-1

- Lewellyn, K. B., & Bao, S. R. (2018). The role of national culture and corruption on managing earnings around the world. Journal of World Business, 52(6), 798–808. https://doi.org/10.1016/j.jwb.2017.07.002

- Li, Y., Li, X., Xiang, E., & Djajadikerta, H. G. (2020). Financial distress, internal control, and earnings management. Journal of Contemporary Accounting and Economics, 16(3), 1–18. https://doi.org/10.1016/j.jcae.2020.100210

- Liu, X. (2016). Corruption culture and corporate misconduct. Journal of Financial Economics, 122(2), 307–327. https://doi.org/10.1016/j.jfineco.2016.06.005

- Lourenco, I. C., Rathke, A., Santana, V., & Branco, M. C. (2017). Corruption and earnings management in developed and emerging countries. Corporate Governance: The International Journal of Business in Society, 18(1), 35–51. https://doi.org/10.1108/CG-12-2016-0226

- Malagueno, R., Albrecht, C., Ainge, C., & Stephens, N. (2010). Accounting and corruption: A crosscountry analysis. Journal of Money Laundering Control, 13(4), 372–393. https://doi.org/10.1108/13685201011083885

- Marzuki, M. M., & Wahab, E. A. A. (2018). International financial reporting standards and conservatism in the association of Southeast Asian Nations countries: Evidence from Jurisdiction Corruption Index. Asian Review of Accounting, 26(4), 387–510. https://doi.org/10.1108/ARA-06-2017-0098

- Mazzi, F., Slack, R., & Tsalavoutas, I. (2018). The effect of corruption and culture on mandatory disclosure compliance levels: Goodwill reporting in Europe. Journal of International Accounting, Auditing and Taxation, 31, 52–73. https://doi.org/10.1016/j.intaccaudtax.2018.06.001

- Mazzi, F., Slack, R., Tsalavoutas, I., & Tsoligkas, F. (2019). Country-level corruption and accounting choice: Research & development capitalization under IFRS. British Accounting Review, 51(5), 1–25. https://doi.org/10.1016/j.bar.2019.02.003

- Mendoza, J. A. M., Yelpo, S. M. S., Ramos, C. L. V., & Fuentealba, C. L. D. (2020). Effects of capital structure and institutional–financial characteristics on earnings management practices: Evidence from Latin American firms, International Journal of Emerging Markets, ahead-of-print No. ahead-of-print. https://doi.org/10.1108/IJOEM-03-2019-0239

- Mhedhbi, K., & Zeghal, D. (2016). Adoption of international accounting standards and performance of emerging capital markets. Review of Accounting and Finance, 15(2), 252–272. https://doi.org/10.1108/RAF-08-2013-0099

- Narayan, F. B., & Godden, T. (2000). Financial management and governance issues inVietnam. The Asian Development Bank.

- Nguyen, C. P., & Richard, J. (2011). Economic transition and accounting system reform in Vietnam. The European Accounting Review, 20(4), 693–725. https://doi.org/10.1080/09638180.2011.623858

- Nguyen, C. P., & Tran, D. K. N. (2012). International harmonisation and national particularities of accounting: Recent accounting development in Vietnam. Journal of Accounting & Organisational Change, 8(3), 431–451. https://doi.org/10.1108/18325911211258371

- Noor, F. A. (2015). Shared cultures and shared geography: Can there ever be a sense of common ASEAN identity and awareness. Economic Research Institute for ASEAN and East Asia. https://www.eria.org/ERIA-DP-2015-77.pdf accessed 8 December 2020

- OECD. (2019). Auditing and Accounting in Southeast Asia: 2019 OECD-ASIAN Roundtable on Corporate Governance. Kuala Lumpur. https://www.oecd.org/corporate/ca/Auditing-Accounting-Asia-2019.pdf

- Oz, I. O., & Yelkenci, T. (2018). Examination of real and accrual earnings management: A cross-country analysis of legal origin under IFRS. International Review of Financial Analysis, 58, 24–37. https://doi.org/10.1016/j.irfa.2018.04.003

- Paananen, M. (2008). The IFRS adoption’s effect on accounting quality in Sweden. SSRN Electronic Journal, Last accesesed 20 December 2020 https://dx.doi.org/10.2139/ssrn.1097659

- Paananen, M., & Lin, H. (2009). The development of accounting quality of IAS and IFRS over time: The case of Germany. Journal of International Accounting Research, 8(1), 31–55. https://doi.org/10.2308/jiar.2009.8.1.31

- Preiato, J., Brown, P., & Tarca, A. (2015). A comparison of between-country measures of legal setting and enforcement of accounting standards. Journal of Business Finance & Accounting, 42(1–2), 1–50. https://doi.org/10.1111/jbfa.12112

- PWC. (2018). Similarities and differences: A comparison of International Financial Reporting Standards (IFRS) and Vietnamese GAAP. https://www.pwc.com/vn/en/publications/2019/pwc-vietnam-ifrs-vas.pdf accessed 8 October 2020

- Rey, A., Maglio, R., & Rapone, V. (2020). Lobbying during IASB and FASB convergence due process: Evidence from the IFRS 16 project on leases. Journal of International Accounting, Auditing and Taxation, 41, 100348. https://doi.org/10.1016/j.intaccaudtax.2020.100348

- Saudagaran, S. M., & Diga, J. G. (2000). The institutional environment of financial reporting regulation in ASEAN. The International Journal of Accounting, 35(1), 1–26. https://doi.org/10.1016/S0020-7063(99)00046-1

- Shleifer, A., & Vishny, R. (1993). Corruption. The Quarterly Journal of Economics, 108(3), 599–617. https://doi.org/10.2307/2118402

- Tsalavoutas, I., Tsoligkas, F., & Evans, L. (2020). Compliance with IFRS mandatory disclosure requirements: A structured literature review. Journal of International Accounting, Auditing and Taxation, 40, 1–31. https://doi.org/10.1016/j.intaccaudtax.2020.100338

- Van Tendeloo, B., & Vanstraelen, A. (2005). Earnings management under German GAAP versus IFRS. European Accounting Review, 14(1), 155–180. https://doi.org/10.1080/0963818042000338988

- Wilhelm, P. G. (2002). International validation of the corruption perceptions index: Implications for business ethics and entrepreneurship education. Journal of Business Ethics, 35(3), 177–189. https://doi.org/10.1023/A:1013882225402

- Zaidi, S., & Huerta, E. (2014). IFRS adoption and enforcement as antecedents of economic growth. International Journal of Accounting and Financial Reporting, 4(1), 1–27. https://doi.org/10.5296/ijafr.v4i1.5410

- Zeghal, D., Chtourou, S. M., & Fourati, Y. (2012). The effect of mandatory adoption of IFRS on earnings quality: Evidence from the European Union. Journal of International Accounting Research, 11(2), 1–25. https://doi.org/10.2308/jiar-10221