Abstract

The study focuses on the factors affecting the application of Balanced Scorecard (BSC) in Vietnamese listed companies, through which they can improve the ability to apply BSC in their businesses. The factors included in the study consist of organizational size, organizational culture, manager’s awareness, accountant’s capability, cost of using BSC, and benefits of using BSC. In addition, the study examines the impact of BSC application on the operational efficiency of listed companies in Vietnam. The authors used the mixed research method combined with Structural Equation Modelling (SEM) to conduct the research. Data were collected from June 2021 to December 2021 from 274 listed companies in the Vietnamese stock market. The research results show that all factors positively influence the application of BSC. Also, the study shows that the higher the level of BSC application, the higher the operational efficiency of enterprises. The authors give some management implications to support enterprises in implementing BSC effectively.

1. Introduction

As the economy is entering a period of rapid growth due to global economic integration, the competition between businesses in the Vietnamese market, particularly, and the world in general, is becoming fiercer. Studies about evaluating business performance are getting necessary for companies in Vietnam (Kim et al., Citation2021). Lee et al. (Citation2007) argued that the methods of evaluating business performance using traditional financial indicators had become outdated, only meeting short-term goals and incapable of measuring them in the long term. When profitable activities increasingly shift from being dependent on tangible assets to intangibles, they cannot fully reflect the enterprise’s operational efficiency. To evaluate operational efficiency, the enterprise needs a system of indicators associated with its development strategy and accessible to both financial and non-financial aspects. BSC was built with four perspectives of finance, customer, internal process, and learning & growth, all of which, along with the business development strategy, are related causally to measure and evaluate all aspects of the organization comprehensively (Kaplan & Norton, Citation1992). Following this, Martinsons et al. (Citation1999) stated that BSC is a foundation for the strategic management of information systems.

Furthermore, the success of an organization depends on its ability to turn resources into products and services customer’s desire. Thanks to these advantages, BSC has evolved as a decision-making support tool at strategic management levels. Thereby, managers evaluate the operational efficiency of the business by supplementing financial accounting data with other objectives-related measures to the following factors: customers, internal process, learning, and growth. Since then, many businesses around the world have used BSC as a tool to evaluate their operational efficiency. According to Hofer (Citation1983, cited by Bagodi et al. Citation2021), operational efficiency is an economical category understood from many angles. From the organization’s financial perspective, operational efficiency is understood as financial efficiency because most of the studies on operational efficiency focus on financial results. However, to accurately evaluate operational efficiency, it is necessary to consider non-financial factors. Cameron (Citation1986) argued that there needs to be a comprehensive concept of operational efficiency, which should be considered case-by-case. Therefore, evaluating operating efficiency must depend on the characteristics of each industry and must be aligned with the goals and strategies of the business in both financial and non-financial aspects. D. Otley (Citation1999) states that operational efficiency is shown in different parts, including targets, strategies, performance indicators, reward systems, and information technology systems. Operational efficiency also helps managers maintain and improve the standards in the organization. According to Kaplan and Norton (Citation1992), operational efficiency could also be measured using financial and non-financial indicators, including total profit, market share, customer satisfaction, quality of products, service, development, training, etc. Similarly, Hoque and James (Citation2000) argued that operational efficiency was measured by appraising five performance dimensions: return on investment, the margin on sales, capacity utilization, customer satisfaction, and product quality. These indicators are assessed on both financial and non-financial aspects, which helps businesses comprehensively evaluate their operational efficiency. Since there is no common standard to assess performance, companies can flexibly use indicators following their business characteristics. Many businesses have begun using performance measurement tools such as BSC to accurately link indicators to evaluate operational efficiency.

Since BSC is mentioned, there are many studies on BSC, which usually focus on the application of the BSC. Some previous studies have shown that the application of BSC in enterprises of different organizational sizes differs. Silk (Citation1998) presented that 60% of large companies in the US have applied for BSC. They considered BSC as an effective management tool. Various studies in Europe and Asia showed that in large-scale corporations and listed companies, BSC is viewed as a valuable strategic management tool and fully implemented with four perspectives. Non-financial measures also helped businesses benefit and increase financial indicators, such as Blundell et al. (Citation2003), Evans (Citation2005), Jusoh et al. (Citation2008), Anand et al. (Citation2005), and Khan and Halabi (Citation2009). In recent years, the research on BSC has been expanded to more and more aspects.

Rafiq et al. (Citation2020) investigated the practical effect of a strategic management system on sustainable development by using a BSC as a theoretical lens and organizational performance as an intervening variable. The findings suggest that non-financial measures have better consequences for employees’ performance because these measures make them more responsible regarding environmental sustainability. The results are aligned with the findings of Kaplan and Norton (Citation2004), who suggested non-financial measures. The empirical findings also stress learning and growth that should be taken as a part of routine matters compared with somewhat seasonal activity. Research conducted by Benková et al. (Citation2020) presented the results from the research on the factors influencing the use of the BSC methodology in measuring company performance in the engineering sector. The study’s main result is that there is a statistically significant relationship between the enterprises considering the non-financial indicators and the use of the BSC tools as necessary. The research also found that a lack of human resources and financial sources define the barriers to implementing the BSC methodology into corporate practice. The research contributed to the extension of the knowledge of the BSC concept that we considered to be a modern managerial future-oriented tool and supported its implementation in companies so that they could operate within the framework of sustainable development. In addition, BSC is not only applied in large-scale enterprises but is also significant in implementing development strategies for small and medium-sized enterprises. However, the application of BSC in small and medium-sized enterprises is incomplete because their financial resources are not strong enough (Lonbani et al., Citation2015) or because their awareness and understanding of BSC are still low (Giannopoulos et al., Citation2013). Besides, the use of the BSC tool in small and medium enterprises is often suboptimal because the enterprise size is not large enough to represent the four aspects of the BSC. At the same time, these enterprises pay more attention to financial factors than non-financial factors to evaluate performance, reducing the significance of applying BSC (Chimwani et al., Citation2013); (Giannopoulos et al., Citation2013); Lonbani et al., Citation2015). Therefore, through research around the world, it can be seen that large-scale enterprises or listed companies will have more favourable conditions to successfully apply the BSC model (Benková et al., Citation2020).

In Vietnam, BSC was initially introduced and mentioned in the early 2000s through seminars on implementing and applying BSC in business management and several related articles on this issue. Large enterprises such as FPT, Phu Thai, and Kinh Do … have pioneered this model into practice; however, the implementation has yet to be successful as expected. Regarding research direction, the authors found that there are two main research directions. Firstly, the research focused on the application of BSC to measure and evaluate the performance of an organization (Giao & Trí, Citation2021; Huyen, Citation2018; Trinh, Citation2020) or an industry (Huong, Citation2010; Tuan, Citation2020). These studies are mainly qualitative research, and the research scale is relatively small; however, these studies have also shown the positives and limitations of applying BSC in Vietnamese enterprises. Secondly, the research concentrated on determining the factors that impact the application of BSC in enterprises. Many factors are considered to have a significant impact on the application of BSC. Still, not all enterprises have those factors, so they should be determined based on the specific conditions of the business. Ha (Citation2019) studies the factors affecting the application of BSC in small and medium enterprises in Ho Chi Minh City. Accordingly, the author has pointed out six factors that positively influence the application of BSC, including ease of use, organization size, awareness of managers, cost of using BSC, strategy business, and benefits of using BSC. The research results are consistent with previous studies in this direction, such as Giang (Citation2017), Nhi and Toan (Citation2018), and Pham and Pham (Citation2019) has a different point of view when saying that factors from managers have a significant and direct influence on the use of BSC in enterprises. The research results show that there are 4/5 factors affecting the application of BSC, including the control system that hotel managers have used, the hotel manager’s ability to receive new knowledge, the perception of hotel managers about the usefulness of BSC, the perception of hotel managers about the ease of use of BSC. Therefore, the role of managers in applying BSC in enterprises is crucial. If managers accept BSC, the application of this tool will be more straightforward and effective. Following this, Truong et al. (Citation2020) studied the factors affecting the application of BSC in tourism enterprises. The authors grouped factors into internal and external factors to see the impact of these two groups of factors on the application of BSC. The results show that both internal and external factors positively impact the application of BSC, but there is a difference in the degree of impact. In terms of financial, customer, and learning & growth aspects, internal factors are said to have a more significant impact. Conversely, external factors in the internal process aspect are more influential than internal factors.

From practice, the authors found that businesses in Vietnam are increasingly interested in applying management accounting in general and BSC to improve management efficiency. The authors understood that applying BSC for businesses in Vietnam is essential, contributing to the success of enterprises in Vietnam. However, for large-scale enterprises with many departments (especially listed companies), it will be more challenging to implement BSC to these companies as it requires higher accuracy due to the large scale and complexity of management accounting. Therefore, they realized that it is necessary to do more in-depth research on the factors affecting the application of BSC in listed companies in Vietnam to serve as a basis to support these enterprises in effectively applying BSC. In addition, the authors’ use of analytical methods through structural equation modeling (SEM) is also a new approach. In contrast, studies in Vietnam on this issue still use traditional analytical methods to perform the analysis.

2. Theoretical framework and literature review

2.1. Theoretical framework

2.1.1. Contingency theory

The contingency theory explains that it is impossible to determine an optimal structure because the structure of manufacturing firms is constantly fluctuating. The contingency theory has refuted some of the previous views that the optimal structure of manufacturing firms can be determined (Weber, Citation1946). In addition, there are several other views on contingency theory. D. T. Otley (Citation1980) suggested that contingent factors affect the design of enterprise structure and tools and techniques in management accounting, including BSC. The view of Chenhall and Harrison (Citation1981) argues that the operating processes and decision-making of the business depend on the business environment and the business’s random factors such as technology, size, strategy, structure, etc. According to contingency theory, relating to the application of BSC, the theory shows that no standard BSC model is suitable for all businesses and organizations. The effective BSC model also depends on the enterprise’s external and internal environmental factors.

2.1.2. Agency theory

Agency theory was also first developed in the research of Ross (Citation1973). Agency theory explains the economic relationship between two parties whose goals are different. Based on the core assumption that human beings are inherently private and risk-averse, this theory aims to determine the optimal conditions in economic relations between two parties to minimize losses. These relationships have different goals, and each party will try to achieve individual goals. The essence is that the lack of information or incorrect information about the other party increases the risks in the economic relationship due to asymmetric information. Since then, agency theory suggests that the contract should be built between the parties based on behavior (working time) and results and productivity. In addition, to minimize the lack of information in the behavior-based contract, the employer can use a monitoring mechanism to monitor and evaluate the work. For the application of BSC, economic relationships also exist, thus creating certain risks.

2.2. Literature review

The BSC is a comprehensive tool that guides each organizational unit to align its activities to achieve its goals and business strategy in general (Zazueta Salido et al., Citation2019). The BSC approach is organized around four distinct perspectives, including the customer perspective, the perspective of internal processes, the perspective of innovation and education, and the financial perspective that balance short- and long-term performance, external and internal performance, financial and non-financial performance, and different stakeholder perspectives (Benková et al., Citation2020). Therefore, many research directions on BSC are expanded and diversified so that enterprises can identify this tool in many aspects, thereby promoting the application of BSC. Lenhard (2007, cited in Ahmed et al. Citation2011) mentioned the success of the BSC model in enterprises. This study has introduced BSC as an effective management tool that can identify and quantify the progress toward achieving business goals. The author points out three stages of building BSC for businesses: the early stage (determining the basic measures), the current stage (measuring from the beginning compared to the present), and the ending stage. (Measurement at the early and current stage against the set goal). At the same time, the author also believes that BSC helps to quantify the decisions of leaders, employees, and external information users to access information easier to understand. Eric Tanyi (Citation2011) has a new direction in the study of BSC application. He presents that with different purposes of use, the factors affecting the application of BSC will be different. To use BSC for decision-making, the ability to receive new knowledge and perceive the ease of use of the BSC by managers will significantly affect the ability to use BSC. As for the monitoring of work performance, the ability of managers to receive new knowledge is the only factor affecting the application. Based on the research results, businesses will identify the factors affecting the application of BSC based on the purpose of using it. In addition, many other studies also study factors, including organization size, organization structures, and cost of applying BSC, … affecting BSC implementation in enterprises (Ahmad & Zabri, Citation2016; Koske & Muturi, Citation2015; Rababah & Bataineh, Citation2016). Benková et al. (Citation2020) point out that three factors, including the importance of non-financial indicators, the lack of human resources, and the lack of financial resources, influence the use of the BSC methodology in engineering enterprises. The research results show that the larger the non-financial indicators, the more likely they will use the BSC. Besides, the two factors, including the lack of human resources and financial resources, also have a positive relationship in implementing BSC in practical enterprises. Thus, from the research results, the authors have successfully considered all three factors affecting the use of BSC in measuring performance for companies.

Although BSC has not been widely applied in Vietnam, there have been some studies on BSC application. Huong (Citation2010) is one of the great studies on this issue in Vietnam. The study mentions five advantages of implementing BSC in Vietnamese service enterprises: Proactivity in innovation, access to modern management tools, awareness of the role of strategy and strategy implementation, implementation management based on their objectives, a hard-working workforce, and the development of science and information technology. On the other hand, the author also pointed out five difficulties in implementing BSC, including Lack of awareness and commitment from the leadership; difficulties in applying the implementation process according to the BSC model; the educational level and limited competence of the leaders; Corporate culture; Financial difficulties. Giang (Citation2017) presents six factors: (1) company size, (2) manager’s perception of BSC, (3) business strategy, (4) company culture, (5) cost of applying for BSC, (6) qualification of the accountant influences the application of BSC. Nhi and Toan (Citation2018) conducted a study to identify and measure the factors affecting the application of BSC in 147 listed companies on the Ho Chi Minh City Stock Exchange. Six factors in the research model affect the application of BSC, including Company size, manager’s perception, business strategy, company culture, the cost of using BSC, and the capacity of accountants. All have a positive impact on the application of BSC.

Thus, although there have been several studies on the application of BSC, the research results have yet to be consistent. Moreover, only a few studies have been conducted in Vietnam (an emerging economy). Therefore, we intend to conduct this research study with the research model including the most comprehensively synthesized variables from studies worldwide and in Vietnam. The research model uses six factors, including Organizational size; Organizational culture; Manager’s awareness, Accountant’s capabilities; Cost of using BSC, and Benefits of using BSC, which influences the application of BSC and the relationship of applying the BSC to performance.

3. Hypothesis development

BSC plays a crucial role in formulating and designing strategies and performance measurement in the business; additionally, it supports information exchange in the enterprise while supporting the vision, mission, and strategy. For enterprises, measurement is crucial, and they can only manage and process what can be measured. If enterprises want to maintain and grow in an increasingly competitive environment, they must apply the BSC system to support effective business management (Kaplan & Norton, Citation1996). In another aspect, BSC is a strategic management system that helps convert an enterprise’s strategy into specific goals and actions. In addition, BSC also supports enterprises in monitoring, setting strategies, and optimizing work according to expected goals (Kaplan & Norton, Citation1996). Moreover, BSC makes it easier to exchange information within the enterprise; strategies and actions are decentralized to each department so that all employees can understand. At the same time, information is also transmitted to the management board to help them identify possible risks and make timely adjustments (Kaplan & Norton, Citation1996).

Currently, listed companies increasingly assert their importance, contributing to Vietnam’s economic development. However, listed companies face difficulties and barriers from both inside and outside. Due to the nature of many transactions and financial disclosure, enterprises need a performance measurement system to provide information and evaluate strategy implementation. Furthermore, relying only on financial indicators to evaluate the implementation of the enterprise’s strategy will not reflect the information comprehensively.

Based on previous studies, the authors have identified the factors affecting the application of BSC to conduct research, including Organizational size; Organizational culture; Manager’s awareness, Accountant’s capabilities; Cost of using BSC, and Benefits of using BSC. In addition, the authors also consider the relationship between BSC application and business performance to see more clearly the benefits that BSC brings.

3.1. Organizational size (QM)

According to the contingency theory of Burns and Stalker (Citation1961), the scale of the enterprise is closely related to the decentralization and structure of activities because when the size increases, it will place constraints on information processing for senior managers. Moreover, the need to create effective communication methods is emphasized in large firms. Therefore, many problems with information and measurement will arise in large enterprises, so it is necessary to have a solution to cover information sources and strengthen management. One of the best solutions is the application of complex management systems such as BSC. Koske and Muturi (Citation2015) also investigates the impact of firm size on BSC adoption in non-governmental organizations. The need for a strategic management tool like BSC is increasing in larger enterprises, so they are more willing to apply BSC than small businesses. Ahmad and Zabri (Citation2016) points out that the business size, as measured by annual sales and number of employees, has a significant impact and increases the use of non-financial performance. The adoption of non-financial performance measures tends to increase in line with the increasing complexity of the company and the need for more standardized control procedures. Therefore, the authors believe that firm size positively relates to BSC adoption. Giang (Citation2017) shows that company size positively impacts the application of BSC. A large-scale company such as a listed company usually has solid economic potential and very high and complex management needs, so these companies will need measures to enhance efficiency activity results. Applying BSC will meet the needs of management and performance evaluation of these companies. Based on these studies, the paper proposes the following hypothesis:

H1: Organizational size has a positive impact on BSC application

3.2. Organizational culture (VH)

Erserim (Citation2012) has shown that corporate culture factors positively impact the ability to apply management accounting, including BSC. The two main elements of corporate culture mentioned by the author include supporting culture and management culture by the target. The culture of support is reflected in the mutual support between departments and divisions in the business, from superiors to subordinates or between colleagues at work. Management culture by the target is often expressed through a high consensus on the common goal, the consensus on the common goal of the whole enterprise, or the agreement of individuals on the common goal of each department. Huu et al. (Citation2021) present that management improves to better advocate resources of the organization or focus on exploiting more dominant aspects of organizational relationships to achieve the goals. These two factors are closely related to the application of management accounting in general and BSC in particular. Research conducted by Rababah and Bataineh (Citation2016) was based on the organizational culture profile model (OCP) of O’Reilly et al. (Citation1991) to examine the influence of 5 factors of organizational culture on the application of BSC at businesses in Jordan. However, the research results published by the author showed that only 3 out of 5 factors positively impact the application of BSC, which are team orientation, innovation, and mission. Outcome orientation and attention to detail have little or no effect on the application of BSC. This study has pointed out the significant influence of organizational culture factors on the application of BSC in companies that are rarely mentioned in written research. In Vietnam, Nhi and Toan (Citation2018) also included the cultural factor in their research. According to the authors, a good corporate culture will help businesses attract talent and retain employees’ loyalty and enthusiasm. The research results showed that organizational culture positively affects the application of BSC in enterprises. At the same time, when applying new tools such as BSC, it is necessary to have consensus and cooperation for employees to be motivated to overcome obstacles. Based on that, the authors propose the second hypothesis as follows:

H2: Organizational culture has a positive impact on BSC application

3.3. Manager’s awareness (NT)

Tanyi (Citation2011) has shown that if managers know the benefits of BSC compared to traditional financial accounting data, they will likely need to apply BSC, helping them manage the company and measure performance more effectively. At this time, the application of BSC in enterprises will be easier to succeed because of the benefits that BSC brings. In contrast, Northcott and Taulapapa (Citation2012) studied the use of BSC to manage the operations of local state organizations in New Zealand. Research showed that managers’ understanding of BSC is very high (91.67%), but only eight units use BSC tools. Through survey and consultation, the authors showed that the application of BSC is more suitable for businesses with strategic orientation and competition in the market. At the same time, public entities operate without competitors, and long-term strategies are often specified by law and regulations rather than by managers. Therefore, managers believed that applying BSC in general units brings few benefits. Nhi and Toan (Citation2018) explained that a manager’s awareness is understanding the potential, benefits and how to use and implement BSC. Since Vietnam’s economy is transitioning to a market economy and is still learning a lot from abroad, as well as the new and still researched BSC method, the application of BSC in enterprises is trivial. Therefore, the application of BSC is challenging to succeed if managers do not clearly understand this method and its benefits. From this, the third hypothesis is proposed as follows:

H3: Manager’s awareness has a positive impact on BSC application

3.4. Accountant’s capabilities (TD)

According to Hung (Citation2016), accountants are essential human resources in implementing and applying managerial accounting, including BSC. If the accountant’s professional capabilities do not meet the requirements, the application of BSC in the enterprise is impossible or can be applied but is not fully efficient. Research by Giang (Citation2017) on listed companies in Ho Chi Minh City considered accounting’s capabilities as a factor affecting the application of BSC. Research results showed that the capability of accounting staff has the most substantial and most positive impact on the application of BSC. The results showed that accountants have an essential role in successfully using BSC because they are directly involved in building and operating it. Nhi and Toan (Citation2018) believed that the BSC method is relatively new in Vietnam, and not all accountants know how to operate BSC. However, staff with suitable qualifications and an understanding of managerial accounting, including BSC, will increase the possibility of applying for BSC in enterprises. The research results also showed that accountants’ capabilities positively influence the application of BSC to enterprises. Based on that, the paper proposes the fourth hypothesis as follows:

H4: Accountant’s capabilities have a positive impact on BSC application

3.5. Cost of using BSC (CP)

BSC is a tool that is too expensive for enterprises. This significantly hinders businesses wishing to apply for BSC (Benková et al., Citation2020; Hristov et al., Citation2019). Perkins et al. (Citation2014) present that evaluating the BSC application’s effectiveness is necessary to consider the relationship between benefits with time and costs for applying BSC. All companies face financial difficulties with BSC applications. In addition, it is also important to consider based on the empirical evidence behind the implementation of BSC in both the private and public sectors leading to improved financial performance after completion. According to Koske and Muturi (Citation2015), the cost of implementing BSC is an essential factor. Investment costs for the application of BSC in the company from the highest to the lowest level will be costly because it includes many cost items such as cost of installation, cost of training, cost of purchasing equipment, machinery, etc. Therefore, it is necessary to analyze the benefits—costs, and risk assessment when implementing the application of BSC. Giang (Citation2017) examined the influence of the cost of implementing BSC on the application of BSC to listed companies. Through survey and regression analysis, the cost of applying BSC positively influences the application of this tool, but this factor has a low impact. Enterprises should consider the cost of using BSC, but it is not the deciding factor. The author believed that listed companies should invest at reasonable prices to build and operate the BSC system for businesses, in which it is necessary to apply information technology to the enterprise accounting system. Thereby, the fifth hypothesis is proposed by the author as follows:

H5: Cost of using BSC has a positive impact on BSC application

3.6. Benefits of using BSC (LI)

Islam et al. (Citation2014) studied the impact of four behavioral factors on the application of BSC, including the benefit of BSC. Research showed that this factor positively impacts the application of BSC, and there is a correlation between the factors. According to the authors, awareness of the potential of BSC is a crucial factor affecting other factors, including the benefits of BSC. Employees’ understanding of the benefits makes them more willing to use the tool, thereby improving the enterprise’s applicability to use BSC. The study of Koske and Muturi (Citation2015) also considered the BSC benefits in non-governmental organizations. The authors have made three statements about the benefits of using BSC, including BSC is useful for internal communication and decision-making in the enterprise; BSC increases the business’s competition; and BSC supports service delivery through the customer perspective. The authors recommended that managers consider BSC’s benefits before applying this tool. Ha (Citation2019) also examined the effect of the benefits of using BSC on the application of BSC in small and medium enterprises in Ho Chi Minh City. The benefits of using BSC are significant enough; businesses will tend to use BSC more. Enterprises often evaluate the benefits of using BSC from the results of using this tool in other enterprises. Based on these studies, the authors propose the following hypothesis:

H6: Benefits of using BSC have a positive impact on BSC application

3.7. BSC application (VD)

Hoque and James (Citation2000) provided 20 scales to measure the use of BSC, which are developed based on four aspects: finance, customers, internal process, and learning & growth. Research results showed a significant influence of BSC application on operational efficiency. Koske and Muturi (Citation2015) pointed out that when businesses are knowledgeable enough and realize the value that BSC brings, it will improve the performance of enterprises in four aspects of BSC. Thus, to evaluate whether the BSC application increases operational efficiency, it is necessary to rely on its four aspects. Thereby, the paper proposes the seventh hypothesis as follows:

H7: BSC application has a positive impact on Operational efficiency

4. Research methodology

4.1. Research model

Based on the literature review and expert opinions on the research topic, the authors developed the research model with the following six elements affecting the application of BSC. At the same time, the authors also examined the impact of the BSC application on the operational efficiency of listed companies in Vietnam. The specific research model is presented in as following:

Figure 1. Proposed research model.

The authors measured dependent variables, intermediate variables and independent variables in Table as follows:

Table 1. Summary table of observed variables of research factors

4.2. Research process

The authors built a research process consisting of 4 main stages as follows:

Stage 1: The authors determined this study’s research problems and objectives. This is the basis for defining research questions. The primary purpose of this research is to answer these questions. By inheriting the literature reviews of previous studies, the authors identified the factors that significantly affect the application of BSC. The authors also gave an overview of BSC, its performance, and the background theories used in the research.

Stage 2: The authors conducted qualitative research by collecting experts’ opinions on BSC. The paper interviewed ten experts with over ten years of experience in management accounting and strategic management in general and experience in applying BSC in enterprises. From experts’ opinions and combined with inheriting items from previous studies, the authors synthesize and build a questionnaire to select appropriate items for variables in the Vietnamese context.

Stage 3: At this stage, the authors conducted quantitative research. Based on the research model, the survey was built using the Google Forms tool, including eight variables and 34 items. Accordingly, a questionnaire was designed with three parts. Part 1 is the demographic information of the interviewees; part 2 presents questions related to BSC to test interviewees’ knowledge about BSC; part 3 reveals questions to investigate the impact of six independent variables on the application of BSC through which they can improve the operational efficiency of listed companies in Vietnam, using a 5-level Likert scale (1: Absolutely disagree; 2: Disagree; 3: Neutral; 4: Agree; 5: Absolutely agree). The questionnaires were sent from June 2021 to December 2021 from 385 listed Vietnamese companies. After collecting the questionnaires, the authors removed the invalid questionnaires in which interviewees answered incorrectly on more than 50% of the questions to test the interviewees’ knowledge of BSC. In addition, if the survey form does not fill in 3/4 of the number of questions or the answer of the questionnaires only select a single scale, the questionnaires are not considered valid and are removed. After collecting valid questionnaires, the authors conducted the analysis using AMOS & SPSS tools.

Stage 4: From the results of data analysis, the authors concluded the research problem and provided solutions to increase the level of application of BSC to enhance the operational efficiency of listed companies in Vietnam.

4.3. Sampling method

Due to the impact of the Covid-19 pandemic in this study, the research team used the non-probability sampling method, namely the convenient sampling method. Accordingly, convenience sampling is based on the convenience and accessibility of the survey object of the interviewer. The survey is conducted online using google Forms and sent via email.

The total number of Vietnamese listed companies is 753 enterprises, including 397 companies in the Ho Chi Minh Stock Exchange (HOSE) and 356 enterprises Hanoi Stock Exchange (HNX; State Securities Commission of Vietnam, Citation2021). The paper selects the sample size from the population based on the following requirement. The sample size needs to be larger than the minimum sample requirement. Some of the minimum sample requirements in the article are as follows:

Determine sample size according to population estimate: According to the formula for determining the sample size of Yamane (Citation1967), the minimum sample size for the study was 261.

Determine sample size for EFA analysis: According to Hair, Sarstedt, et al. (Citation2014), the minimum sample size to use EFA was 50, preferably 100 or more. The ratio of observations to a variable should be 5:1 or 10:1. For this study, the number of analyzed variables is 34; with a ratio of 5:1, the minimum number of samples to be determined is 170.

Determining sample size for SEM model analysis: According to Bollen (Citation1989), the sample size must have at least five observations per estimated parameter for practical SEM model analysis. Accordingly, the minimum sample of the study was 170.

However, the research has a limitation in the sampling scope. The listed companies with less than one fiscal year are not interviewed (as of 31 March 2021). Because these companies have just been listed for a short time, the company’s operating procedures still need to adapt to the nature of listed companies. Therefore, when selecting these companies in the sample, they are not generally representative of listed companies. According to statistics of HNX and HOSE, as of 31 March 2021, there were 38 newly listed companies under one fiscal year. Therefore, the research team excluded these 38 companies from the sample and surveyed them from June 2021 to December 2021. Therefore, from June 2021 to December 2021, the authors collected data by sending questionnaires to 385 companies listed on two stock exchanges, including HNX and HOSE. The total number of questionnaires collected was 325 (84.4%), of which 51 (13.25%) were invalid. The remaining 274 (71.17%) valid questionnaires were included in the analysis.

5. Analysis of results

5.1. Demographic information of respondents

Table presents the demographic information of respondents, including Age, Education, Position, Working Experience, Business Industry, and Stock Exchange where their company is listed. This information provides an overview of the characteristics of the sample to draw accurate conclusions.

Table 2. Demographic information of respondents

Regarding age, most respondents are between the ages of 26 and 35 (44.5%). Because BSC has just been brought to Vietnam recently, this age group has a lot of knowledge and experience to use BSC effectively. Regarding education, the authors reported that up to 197 respondents (71.9%) had a university degree, and only 18 (6.6%) had a college degree. It shows that respondents must have a sufficient level of education to understand and apply BSC in business. Staff (103 people) and head of department (98 people) were the most asked regarding the position. There were also 46 respondents (16.8%) who were consultants and 27 respondents (9.9%) who were on the board of managers. The interviewees are entirely suitable for the research because the staff and the head of the department are the ones who directly apply BSC to activities in the companies. For working experience, 42.7% of the interviewees have 5 to 10 years of experience, 25.9% with 10 to 20 years of experience, 20.8% with less than 5 years of experience, and 10.6% with more than 20 years of experience. Interview information about work experience is relevant to the job position of the interviewers in the business industry. The paper focuses on non-financial listed companies in 3 primary industries, including manufacturing enterprises (59.2%), Services (22.6%), and Commerce (18.2%). Regarding the stock exchange, there are 160 companies listed on HNX (58.4%) and 114 companies listed on HOSE (41.6%). These two stock exchanges allow the company to be officially listed in Vietnam.

5.2. Reliability test using Cronbach’s Alpha

The variables used in the study are latent variables that have no expression with a specific criterion. In this study, these latent variables are measured by items; each item measures one aspect of the latent variable, and the set of items is called the latent variable measurement scale. Therefore, before performing further analysis, it is necessary to evaluate the reliability of the scales of the latent variables.

Hair, Sarstedt et al. (Citation2014) suggested that a scale that ensures unidirectionality and reliability should reach Cronbach’s Alpha threshold of 0.7 or higher. However, as a preliminary exploratory study, Cronbach’s Alpha is 0.6, which is acceptable. The higher the Cronbach’s Alpha coefficient, the higher the scale’s reliability.

Another important indicator is the Corrected Item—Total Correlation. This value represents the correlation between each observed variable with the remaining variables in the scale. If the observed variable has a stronger positive correlation with other variables in the scale, the higher the value of the Corrected Item—Total Correlation, the better the observed variable. Cristobal et al. (Citation2007) said that a good scale is when the observed variables have the Corrected Item—Total Correlation value of 0.3 or more. Therefore, when performing the Cronbach’s Alpha reliability test, the observed variable has the Corrected Item—Total Correlation coefficient of less than 0.3. It is necessary to consider removing that observed variable. The higher the Corrected Item—Total Correlation coefficient, the better the quality of the observed variable.

Table shows the results of reliability testing by Cronbach’s Alpha coefficient and Corrected Item—Total Correlation for observed variables. The research team evaluated Cronbach’s Alpha coefficient and Corrected Item—Total Correlation based on collected research data to test the reliability of each scale and eliminate inappropriate observed variables in the research model. All 34/34 observed variables of 8 factors in the research model meet the standard. All factors have a variable correlation with a total variable greater than 0.3. Additionally, the coefficients of Cronbach’s alpha of all factors are greater than 0.6, so it can be concluded that the reliability of the scales used in the model ensures the allowed reliability.

Table 3. Results of Cronbach’s Alpha test

For each factor with Cronbach’s Alpha coefficient greater than 0.6, If any observed variables in this factor are removed, the Alpha coefficient will decrease, and the total correlation coefficient is greater than 0.3, so all observed variables in the study are kept.

5.3. Exploratory factor analysis (EFA)

The research team used the EFA method to analyze each variable separately to check the multidimensionality of the factor and evaluate the scale for the factors.

When analyzing EFA for the scales in the research model, the research team used the Principal Component Analysis method with Promax rotation and the breakpoint to extract factors with Eigenvalue > 1. Table shows Kaiser-Meyer-Olkin (KMO) coefficient = 0.890 > 0.5 and the Bartlett test with Sig. = 0.000 (< 0.05) indicates that EFA analysis is appropriate. Factor loading coefficients of all observed variables are greater than 0.5 and only uploaded for 1 factor.

Table 4. Rotated component matrix

Also, at Eigenvalue = 1.195 > 1, 8 factors were extracted from 34 observed variables with a total extracted variance of 63.555% (> 50%). It was concluded that no new factors were formed compared to the initially proposed research model. Thus, after analyzing EFA, these 34 observed variables met EFA analysis criteria; no variables were excluded at this stage.

5.4. Confirmatory factor analysis (CFA)

Confirmatory Factor Analysis (CFA) is the test used in this study to accomplish the following purposes:

Firstly, CFA evaluates the overall fit of the data based on the modes fit indexes. According to Hair, Black et al., Citation2014), Multivariate Data Analysis, 7th edition of the indicators considered to evaluate Model Fit include CMIN/df ≤ 2 is good, CMIN/df ≤ 5 is acceptable, CFI ≥ 0.9 is good, CFI ≥ 0.95 is perfect, CFI ≥ 0.8 is acceptable (CFA ranges from 0 to 1). GFI ≥ 0.9 is good, GFI ≥ 0.95 is very good, RMSEA ≤ 0.08 is good, and RMSEA ≤ 0.03 is very good (Hair, Black et al., Citation2014).

Secondly, CFA evaluates the quality of observed variables and confirms the factor structures. If the EFA is tasked with discovering the factor structure from a set of observed variables and assuming that it is unknown which variables are in the same scale (with the same factor), the CFA is different. The observed variables included in the CFA analysis are assumed to have already determined which observed variables belong to these scales. The function of the CFA is to assess whether the observed variables within that scale are appropriate and standard. In addition, CFA evaluates the convergence and discriminant of variable structures.

The model fit indexes illustrated in Table are as follows: CMIN/df = 1.159 (between 1 and 3), RMSEA = 0.024 (<0.06), PCLOSE = 1 (>0.05), CFI = 0.985 (>0.95) met the standard and are very good. This result indicated that the measurement model fits the data well. The combined reliability of CR and extracted variance AVE are greater than 0.5, and the scale is considered reliable. The normalized weights of the scales are all high and greater than 0.5, and the sig value of each pair of concepts is less than 0.05. On the other hand, the correlation coefficients with standard deviation showed that they are all different from 1. Therefore, the adjusted research model achieved convergent and discriminant values. The model did not correlate the measurement errors of the groups of factors together, so the model achieved one-dimensionality.

Table 5. Composite reliability and average variance extracted

5.5. Structural equation modelling (SEM)

Structural Equation Modeling (SEM) is a technique for analyzing multidimensional relationships among many variables in a model (Hair, Black et al., Citation2014). The relationships between variables can be represented in a variety of single regression equations and multiple regression equations. The linear structural modeling method (SEM) combines quantitative data and correlated (cause-effect) assumptions into the same model. With SEM, researchers can directly examine the relationships that exist between variables. The fact that latent variables that are difficult to measure can be used in SEM makes it ideal for solving research problems. In this study, the paper uses the SEM model to study the influence of factors on BSC application (VD) and the influence of BSC application (VD) on enhancing Operational Efficiency (HQ). The research team tested the proposed research hypotheses based on the results of running SEM.

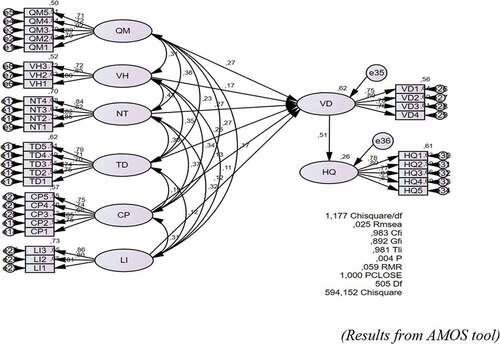

The results in Table and Figure showed that the model has suitable suitability with the data, and the indexes are at an excellent level: CMIN/df = 1.177 (between 1 and 3), CFI = 0.983 (>0.95); RMSEA = 0.025 (<0.06) and PCLOSE = 1.000 (>0.05). All regression coefficients have a sig. values less than 0.05, the coefficients are statistically significant. In conclusion, the theoretical model is consistent with the survey data.

Figure 2. Structural equation modeling (SEM).

Table 6. Results from SEM model

The results of the standardized regression coefficient of the model showed that all factors positively impact the BSC method’s application in listed companies in Vietnam, in the order of Organizational size, Manager’s awareness, Accountant’s capabilities, Organizational culture, and Cost of using BSC, Benefits of using BSC. At the same time, the statistics also showed that with other factors remaining constant, the successful application of BSC would positively impact operational efficiency.

6. Discussion and conclusion

The authors summarize the results in Table :

Table 7. Summary of research results

The study’s findings indicated that the variables all had positive effects on the application of BSC, but their magnitude of influence varied. More precisely, as follows:

Organizational size has the most substantial influence on the application of BSC in listed companies in Vietnam. The larger the enterprise, the higher the level of BSC usage. Previous studies have also shared this meaning, such as Koske and Muturi (Citation2015), Ahmad and Zabri (Citation2016), and Giang (Citation2017).

Managers’ awareness has the second level of impact on the application of BSC. Thus, it can be seen that the application of BSC is challenging to succeed if managers do not clearly understand this method and what it brings. This is also consistent with some previous studies by Tanyi (Citation2011), Northcott and Taulapapa (Citation2012), and Nhi and Toan (Citation2018).

The accountant’s capabilities have the third level of impact on the application of BSC. However, the level of influence is still relatively large because accountants are the essential human resources in implementing and applying management accounting, specifically BSC. Therefore, if the professional qualifications of accountants do not meet the requirements, the application of BSC in the enterprise is impossible, or it can be applied but not efficiently. This result is consistent with the expectation of the research team as well as other studies, including Hung (Citation2016), Giang (Citation2017), and Nhi and Toan (Citation2018).

Organizational culture has the fourth level of impact on the application of BSC. When applying a new tool like BSC, it is necessary to have consensus and cooperation for employees to be motivated to overcome obstacles. Previous studies also have the same result, such as Erserim (Citation2012), Rababah and Bataineh (Citation2016), and Nhi and Toan (Citation2018).

The cost of using BSC has a relatively low level of impact and ranks fifth among the factors affecting the application of BSC in this study. However, it can be seen that the cost factor significantly affects the application of anything in the business. The majority believed that if enterprises realize that the cost of building and operating the BSC system is higher than the benefits achieved, they will choose to apply other tools. This is also consistent with previous studies such as Perkins et al. (Citation2014), Koske and Muturi (Citation2015), and Giang (Citation2017).

The benefits of using BSC have the lowest impact on BSC usage in this study. However, it still has a significant effect, so this factor cannot be ignored. It can be seen that the awareness of the benefits and ease of use of BSC will make businesses more willing to use the tool, thereby helping to improve their applicability to use BSC. This result is also consistent with previous studies such as Islam et al. (Citation2014), Koske and Muturi (Citation2015), and Ha (Citation2019).

Furthermore, the impact of BSC Application on Operational efficiency is also determined to have a positive effect and is consistent with previous studies such as Hoque and James (Citation2000) and Koske and Muturi (Citation2015).

From the above results, in order to strengthen the application of BSC, Vietnamese-listed companies need to prepare essential factors, including organizational size, manager’s awareness, accountants’ capabilities, organizational culture, costs, and benefits to apply BSC. However, with the current context in Vietnam, the implementation of BSC faces many challenges when considering these factors. First, the organizational size of Vietnamese-listed companies is not too large compared to internationally listed companies. However, organizational size significantly impacts the successful implementation of BSC, which has many challenges for listed companies that want to apply for BSC. The next factor is managers’ awareness which creates difficulties in implementing BSC in enterprises because many managers in Vietnam are still not fully aware of the role of management accounting, especially the role of application of BSC in improving operational efficiency. They mainly focus on developing tax accounting and financial accounting systems. Similarly, accountants’ capabilities are also a problem when implementing BSC because the accounting training programs mainly focus on financial accounting. Implementing BSC is not widespread, so most accountants do not know the BSC. For organizational culture factors, Vietnam has many distinct cultural features which can change corporate culture. This is a difficult factor to evaluate when implementing BSC in Vietnamese-listed companies. Regarding the benefits and costs of using BSC, there are not many changes in the context of Vietnam. Although these factors have the lowest influence on the application of BSC, the listed companies still necessary to control these factors to achieve operational efficiency. Recommendations

Furthermore, the authors deduced that improving the influencing factors will increase the level of BSC application, thereby improving operational efficiency. Therefore, the authors suggested that business managers should pay attention to the following issues:

Firstly, the implementation process of BSC should be started with an overall analysis and assessment of the current situation and size of the business. Through that, businesses can develop detailed strategies that are more suitable to the size of the business.

Secondly, under intense competitive pressure, companies must improve their understanding and grasp the new knowledge of the times. This needs to be implemented synchronously from administrators to employees. Thereby, every company member can understand and implement the company’s strategy effectively.

Thirdly, to successfully apply the BSC, managers need to determine the value it can create for their business. This value needs to be assessed in both financial and non-financial factors. Many businesses only care about financial factors, so they think applying BSC brings little benefit. Therefore, misjudging the benefits of BSC will reduce the ability to apply it in the enterprise. Enterprises need more training programs for managers and accountants to increase awareness about the role of BSC in operational efficiency.

Finally, they also need to accept investment in technology and related costs to deploy the application of BSC. Managers need to plan specific costs and compare them with the benefits that can be achieved. This is still a challenge for Vietnamese businesses due to the high cost of applying, but businesses cannot maximize the benefits of this tool.

In addition, the authors believe that the state’s participation is required to increase the ability to apply BSC in Vietnamese enterprises. First, the government must enforce specific policy actions to encourage pursuing knowledge and understanding of managerial accounting in general and the BSC model. Next, the government must develop appropriate policies to support, and help listed companies deploy BSC. And then, the government should promote and develop plans to introduce the BSC model into state organizations and agencies to serve as a premise to increase the application of BSC in Vietnamese enterprises, especially listed companies.

From the research results, the authors have answered the research questions and met the research objectives initially set. Hence, this contributed to the theoretical basis of studies on this issue to support enterprises successfully applying BSC. However, the study still has several limitations due to limited resources and research time. Specifically, the number of surveyed enterprises is not large enough, so the representativeness is not high. Furthermore, the convenient sampling method also does not guarantee representativeness due to the impact of the Covid pandemic. In addition, the study using the previous studies’ scale may not be suitable for the characteristics of Vietnamese enterprises. Thereby, the authors suggested further studies can build more on the sample size factor and number of non-financial and financial listed companies from different business industries, and at the same time, use the probabilistic sampling method to increase the representativeness and reliability of the study. In addition, in the future, researchers can also adjust and build new scales and factors plausible to the characteristics of Vietnamese enterprises.

Correction

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Ahmad, K., & Zabri, S. M. (2016). The application of non-financial performance measurement in Malaysian manufacturing firms. Procedia Economics and Finance, 35, 476–24. https://doi.org/10.1016/S2212-5671(16)00059-9

- Ahmed, Z., Ahmed, Z., Nawaz, M. M., Dost, K. B., Khan, M. A. 2011 Comparative significance of the four perspectives of balanced scorecard.Interdisciplinary Journal of Contemporary Research in Business,3(1), 981–993. Accessed 10 9 2022 https://d1wqtxts1xzle7.cloudfront.net/30512194/may11-with-cover-page-v2.pdf?Expires=1669217461&Signature=eXYGXclJUGigcpCt1KGQbZFRMQ4DqQ-zKFPVmmSHkaX2YQN4AhPu3gpUWXkZdW4hzt~jvjCf778d7GASR~IcvdSoRi7lsI8nOAOIQZTt0ND0doal7pGwQ6M~ofROFjWi~yONzqhz9E24z9npML2TRWdZBOzWI33eERIz-P7RjyiPkodEBj4c~ynwUqwncfJaej5XB60YqT7plQhaRmdevfQlW9Ry671WdEsGSXLh3h2x0dahb8iZopRbS~5eC07wV8i53km1Gz9yFDNv1hUs4bYnvRaHIGrxsanymSoijBqR8f3c050JcKzni43rbXuEmAOWFOc6lV6W8M~ino6vNg__&Key-Pair-Id=APKAJLOHF5GGSLRBV4ZA#page=981

- Anand, M., Sahay, B. S., & Saha, S. (2005). Balanced scorecard in Indian companies. Vikalpa, 30(2), 11–26. https://doi.org/10.1177/0256090920050202

- Bagodi, V., Venkatesh, S. T., Sinha, D. 2021 A study of performance measures and quality management system in small and medium enterprises in India Benchmarking: An International Journal, 28(4), 1356–1389. https://doi.org/10.1108/BIJ-08-2020-0444

- Benková, E., Gallo, P., Balogová, B., & Nemec, J. (2020). Factors affecting the use of balanced scorecard in measuring company performance. Sustainability, 12(3), 1178. https://doi.org/10.3390/su12031178

- Blundell, B., Sayers, H., & Shanahan, Y. (2003). The adoption and use of the balanced scorecard in New Zealand: A survey of the top 40 companies. Pacific Accounting Review, 15(1), 49–74. https://doi.org/10.1108/eb037971

- Bollen, K. A. (1989). A new incremental fit index for general structural equation models. Sociological Methods & Research, 17(3), 303–316. https://doi.org/10.1177/0049124189017003004

- Burns, T. S., & Stalker, G. M. (1961). GM (1961) The management of innovation. London. Tavistock.

- Cameron, K. S. (1986). Effectiveness as paradox: Consensus and conflict in conceptions of organizational effectiveness. Management Science, 32(5), 539–553. https://doi.org/10.1287/mnsc.32.5.539

- Chenhall, R. H., & Harrison, G. L. (1981). The organizational context of management accounting. Pitman Publishing.

- Chimwani, P., Nyamwange, O., & Otuyo, R. (2013). Application of strategic performance measures in small and medium-sized manufacturing enterprises in Kenya: The use of the balanced scorecard perspectives. International Journal of Management Sciences and Business Research, 2(6). https://ssrn.com/abstract=2712116

- Cristobal, E., Flavián, C., & Guinalíu, M. (2007). Perceived e-service quality (PeSQ): Measurement validation and effects on consumer satisfaction and web site loyalty. Managing Service Quality, 17(3), 317–340. https://doi.org/10.1108/09604520710744326

- Erserim, A. (2012). The impacts of organizational culture, firm’s characteristics and external environment of firms on management accounting practices: An empirical research on industrial firms in Turkey. Procedia-Social and Behavioral Sciences, 62, 372–376. https://doi.org/10.1016/j.sbspro.2012.09.059

- Evans, N. (2005). Assessing the balanced scorecard as a management tool for hotels. International Journal of Contemporary Hospitality Management, 17. https://doi.org/10.1108/09596110510604805

- Giang, N. T. P. (2017). Các nhân tố ảnh hưởng đến việc vận dụng bảng điểm cân bằng (BSC - Balanced ScoreCard) trong các công ty niêm yết tại thành phố Hồ Chí Minh. (Master’s thesis, University of Economics Ho Chi Minh City). https://digital.lib.ueh.edu.vn/handle/UEH/56697

- Giannopoulos, G., Holt, A., Khansalar, E., & Cleanthous, S. (2013). The use of the balanced scorecard in small companies. International Journal of Business and Management, 8(14), 1–22. http://dx.doi.org/10.5539/ijbm.v8n14p1

- Giao, H. N. K., & Trí, N. H. (2021). Vận dụng thẻ điểm cân bằng tại Công ty cổ phần Khu Công Nghiệp Nam Tân Uyên. T?P CHÍ KHOA H?C Ð?I H?C M? THÀNH PH? H? CHÍ MINH-KINH T? VÀ QU?N TR? KINH DOANH, 17(3), 68–83. http://dx.doi.org/10.2139/ssrn.3979472

- Ha, T. L. N. (2019). Các nhân tố ảnh hưởng đến việc vận dụng bảng điểm cân bằng (BSC - Balanced ScoreCard) đối với các doanh nghiệp nhỏ và vừa tại thành phố Hồ Chí Minh. (Master’s thesis, University of Economics Ho Chi Minh City). https://digital.lib.ueh.edu.vn/handle/UEH/59316

- Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2014). Multivariate data analysis (7th ed.). Pearson Education Limited.

- Hair, J. F., Jr, Sarstedt, M., Hopkins, L., & Kuppelwieser, V. G. (2014). Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. European Business Review. https://doi.org/10.1108/EBR-10-2013-0128

- Hendricks, K., Menor, L., & Wiedman, C. (2004). Adoption of the balanced scorecard: A contingency variables analysis. Ontario: Richard Ivey Business School. University of Western Ontario. https://citeseerx.ist.psu.edu/viewdoc/download?doi=10 .1.1.503.806&rep=rep1&type=pdf

- Hofer, C. W. (1983). ROVA: A new measure for assessing organizational performance. Advances in Strategic Management, 2, 43–55.

- Hoque, Z., & James, W. (2000). Linking balanced scorecard measures to size and market factors: Impact on organizational performance. Journal of Management Accounting Research, 12(1), 1–17. https://doi.org/10.2308/jmar.2000.12.1.1

- Hristov, I., Chirico, A., & Appolloni, A. (2019). Sustainability value creation, survival, and growth of the company: A critical perspective in the sustainability balanced scorecard (SBSC). Sustainability, 11(7), 2119. https://doi.org/10.3390/su11072119

- Hung, T. N. (2016). Các nhân tố tác động đến việc vận dụng kế toán quản trị trong các doanh nghiệp nhỏ và vừa tại Việt Nam. (Doctoral dissertation). University of Economics Ho Chi Minh City). https://digital.lib.ueh.edu.vn/handle/UEH/55618

- Huong, D. T. (2010). Áp dụng thẻ điểm cân bằng tại các doanh nghiệp dịch vụ Việt Nam. VNU Journal of Science: Economics and Business, 26(2). https://repository.vnu.edu.vn/handle/11126/837

- Huu, H. D., Manh, Q. N., & Van, T. T. (2021). Why the policy could not absorb by SMES? A view through reciprocity lens in a case in Vietnam. Journal of Legal, Ethical and Regulatory Issues, 24(S4), 1–12. https://www.proquest.com/docview/2573888619?pq-origsite=gscholar&fromopenview=true

- Huyen, P. T. H. (2018). Vận dụng bảng điểm cân bằng (Balanced Scorecard) để đo lường thành quả tại Ngân hàng TMCP Công thương Việt Nam. ( Master’s thesis, University of Economics Ho Chi Minh City). https://digital.lib.ueh.edu.vn/handle/UEH/57704

- Islam, M., Yang, Y. F., Hu, Y. J., & Hsu, C. S. (2014). Factors affecting balanced scorecard usage. International Journal of Business Information Systems, 17(1), 112–128. https://doi.org/10.1504/IJBIS.2014.064125

- Jusoh, R., Ibrahim, D. N., & Zainuddin, Y. (2008). The performance consequence of multiple performance measures usage: Evidence from the Malaysian manufacturers. International Journal of Productivity and Performance Management, 57. https://doi.org/10.1108/17410400810847393

- Kaplan, R. S., & Norton, D. P. (1992). The balanced scorecard: Measures that drive performance. Harvard Business Review, 70(7/8), 172–180. https://www.academia.edu/39249393/Using_the_Balanced_Scorecard_as_a_Strategic_Management_System?from=cover_page

- Kaplan, R. S., & Norton, D. P. (1996). The balanced scorecard: Translating strategy into action. Harvard Business School Press. http://jackson.com.np/home/documents/MBA4/Management_accounting/BSCHarvardBusinessReview.pdf

- Kaplan, R. S., & Norton, D. P. (2004). The strategy map: Guide to aligning intangible assets. Strategy & Leadership, 32(5), 10–17. https://doi.org/10.1108/10878570410699825

- Khan, M. H. U. Z., & Halabi, A. K. (2009). Perceptions of firms learning and growth under knowledge management approach with linkage to balanced scorecard (BSC): Evidence from a multinational corporation of Bangladesh. International Journal of Business and Management, 4(9). https://doi.org/10.5539/ijbm.v4n9p257

- Kim, N. L. T., Duvernay, D., & Le Thanh, H. (2021). Determinants of financial performance of listed firms manufacturing food products in Vietnam: Regression analysis and Blinder–Oaxaca decomposition analysis. Journal of Economics and Development. https://doi.org/10.1108/JED-09-2020-0130

- Koske, C. C., & Muturi, W. (2015). Factors affecting application of BSC: A case study of nongovernmental organizations in Eldoret, Kenya. Journal of Management, 2(2), 1868–1898. https://strategicjournals.com/index.php/journal/article/view/193/208

- Lee, M. C., Wang, H. W., & Wang, H. Y. (2007). A method of performance evaluation by using the analytic network process and balanced score car. In 2007 International conference on convergence information technology (ICCIT 2007) (pp. 235–240). IEEE. https://doi.org/10.1109/ICCIT.2007.216

- Lonbani, M., Sofian, S., & Baroto, M. B. (2015). Linking balanced scorecard measures to SMEs’ business strategy: Addressing the moderating role of financial resources. International Journal of Research Granthaalayau, 3(12), 92–99. https://doi.org/10.29121/granthaalayah.v3.i12.2015.2893

- Martinsons, M., Davison, R., & Tse, D. (1999). The balanced scorecard: A foundation for the strategic management of information systems. Decision Support Systems, 25(1), 71–88. https://doi.org/10.1016/S0167-9236(98)00086-4

- Nhi, V. V., & Toan, P. N. (2018). Factors influencing to the application of balanced scorecard among listed companies in Ho Chi Minh city. The 5th IBSM International Conference on Business, Management and Accounting, pp. 19–21 April. Hanoi University of Industry, Vietnam. http://www.caal-inteduorg.com/proceedings/ibsm5/AACT8-52.pdf

- Northcott, D., & Taulapapa, T. M. A. (2012). Using the balanced scorecard to manage performance in public sector organizations: Issues and challenges. International Journal of Public Sector Management, 25(3), 166–191. https://doi.org/10.1108/09513551211224234

- O’Reilly, C. A., III, Chatman, J., & Caldwell, D. F. (1991). People and organizational culture: A profile comparison approach to assessing person-organization fit. Academy of Management Journal, 34(3), 487–516. https://journals.aom.org/doi/abs/10 .5465/256404

- Otley, D. T. (1980). The contingency theory of management accounting: Achievement and prognosis. In Clive, Emmanuel, David, Otley, Kenneth, Merchant (Eds.) Readings in accounting for management control (pp. 83–106). Springer. https://link.springer.com/chapter/10 .1007/978-1-4899-7138-8_5

- Otley, D. (1999). Performance management: A framework for management control systems research. Management Accounting Research, 10(4), 363–382. https://doi.org/10.1006/mare.1999.0115

- Perkins, M., Grey, A., & Remmers, H. (2014). What do we really mean by “Balanced Scorecard”? International Journal of Productivity and Performance Management, 63(2), 148–169. https://doi.org/10.1108/IJPPM-11-2012-0127

- Pham, T., & Pham, D. (2019). Factors affecting to the application of balanced scorecard in Vietnamese hospitality firms. Management Science Letters, 9(13), 2383–2390. https://doi.org/10.5267/j.msl.2019.7.017

- Rababah, A., & Bataineh, A. (2016). Factors influencing balanced scorecard implementation. Research Journal of Finance and Accounting, 7(2), 204–212. https://portal.arid.my/Publications/ff52ee2e-12f2-40.pdf

- Rafiq, M., Zhang, X., Yuan, J., Naz, S., & Maqbool, S. (2020). Impact of a balanced scorecard as a strategic management system tool to improve sustainable development: Measuring the mediation of organizational performance through PLS-smart. Sustainability, 12(4), 1365. https://doi.org/10.3390/su12041365

- Ross, S. A. (1973). The economic theory of agency: The principal’s problem. The American Economic Review, 63(2), 134–139. https://www.jstor.org/stable/1817064

- Silk, S. (1998). Automating the balanced scorecard. Strategic Finance, 79(11), 38. https://www.proquest.com/openview/7e12dd71a2486f45ee40384b6e6aa500/1?pq-origsite=gscholar&cbl=48426

- State Securities Commission of Vietnam. (2021, June 4). https://www.ssc.gov.vn/ubck/faces/vi/vimenu/vipages_vithongtinthitruong/thongkettck/quymothitruong?_adf.ctrl-state=2rfpbtrvr_154&_afrLoop=51698186868000&_afrWindowMode=0&_afrWindowId=null#%40%3F_afrWindowId%3Dnull%26_afrLoop%3D51698186868000%26_afrWindowMode%3D0%26_adf.ctrl-state%3Da4kxr9wfp_4

- Tanyi, E. (2011). Factors influencing the use of Balanced Scorecard. ( Unpublished MAS Thesis, Hanken School of Economics). https://helda.helsinki.fi/bitstream/handle/10138/26702/tanyi.pdf

- Trinh, L. T. T. (2020). Vận dụng thẻ điểm cân bằng (Balanced scorecard - BSC) tại Công ty Cổ phần May Xuất khẩu Phan Thiết. ( Master’s thesis, Industrial University of Ho Chi Minh City). https://tapchicongthuong.vn/bai-viet/van-dung-the-diem-can-bang-balanced-scorecard-bsc-tai-cong-ty-co-phan-may-xuat-khau-phan-thiet-75075.htm

- Truong, D. D., Nguyen, H., & Duong, T. Q. L. (2020). Factors influencing balanced scorecard application in evaluating the performance of tourist firms. The Journal of Asian Finance, Economics and Business, 7(5), 217–224. https://doi.org/10.13106/jafeb.2020.vol7.no5.217

- Tuan, T. T. (2020). The impact of balanced scorecard on performance: The case of Vietnamese commercial banks. The Journal of Asian Finance, Economics and Business, 7(1), 71–79. https://doi.org/10.13106/jafeb.2020.vol7.no1.71

- Weber, M. (1946). Science as a Vocation. In Alfred, I. Tauber (Eds.) Science and the quest for reality. Palgrave Macmillan. https://link.springer.com/chapter/10 .1007/978-1-349-25249-7_17

- Yamane, T. (1967). Statistics: An introductory analysis. No. HA29 Y2 1967.

- Zazueta Salido, R. A., Lagarda‐Leyva, E. A., & Lozoya Díaz, D. G. (2019). Strategic plan for a regional innovation center and business accelerator of southern sonora using megaplanning and balanced scorecard. Performance Improvement Quarterly, 32(3), 287–323. https://doi.org/10.1002/piq.21299