?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the impact of voluntary disclosure on the cost of capital and information asymmetry, and thereby on firm value in a comprehensively recursive model. We argue that there is unidirectional dependency among the information asymmetry, cost of capital, and such firm value, hence, for any given value of voluntary disclosure, values for information asymmetry, cost of capital, and firm value can be determined sequentially rather than jointly. A sample of 1920 companies-years of non-financial companies listed on the Indonesia Stock Exchange from 2012 to 2019 is employed. The data used are a voluntary disclosure index obtained by using a self-constructed index. To calculate the cost of capital, stock market data in the form of closing prices, bid and ask prices, and some outstanding shares, as well as company financial data, are used. In examining the hypothesis, the recursive path model is utilized. The results show that the negatively direct effect of disclosure on information asymmetry and cost of capital is consistent with the hypothesis. The indirect effect of disclosure on firm value through information asymmetry is also relevant to the hypothesis. The findings suggest that higher disclosure provides great benefits for the companies as well as investors and lenders. Increasing disclosure reduces information asymmetry and the cost of capital, thereby increasing firm value.

PUBLIC INTEREST STATEMENT

This study aims to examine whether more complete and numerous disclosures by a company are beneficial for investors as well as for the company Conveying complete and ample information to the public is expected to reduce the information gap amongst decision makers, lower the cost of capital, and thereby increase increases firm value. This study specifically fills the gap to explore whether the companies benefit greatly as a consequence of the large costs incurred to produce more complete and multiple disclosures in their financial reports, and whether investors obtain the most benefit from disclosure of financial information.

By using data from a sample of 1920 companies-years of non-financial companies listed on the Indonesia Stock Exchange from 2012 to 2019, we employed a comprehensively recursive path model to examine the hypothesis.

The results support our prediction that more complete and numerous disclosures by a company are beneficial for investors, i.e., lower information asymmetry, as well as for the company, i.e., lower cost of capital and higher firm value.

1. Introduction

This study aims to examine whether complete and numerous disclosures by a company are beneficial for investors as well as for the company Conveying complete and ample information to the public is expected to reduce the information gap amongst decision maker (Bertomeu et al., Citation2021), lower the cost of capital (Chen et al., Citation2022; Michaels & Grüning, Citation2017; Botosan & Plumlee, Citation2002), and increase public trust to the company (Sheu et al., Citation2010); thus, it increases firm value (tTemiz, Citation2021; McMullin, Citation2019). Specifically, Wong and Zhang (Citation2022) reveal that the market reacts to information voluntarily disclosed by a firm which reflected in the higher stock price. This study specifically fills the gap to explore whether the companies benefit greatly as a consequence of the large costs incurred to produce complete and multiple disclosures in their financial reports (Coffie and Bedi, Citation2018), and whether investors obtain the most benefit from disclosure of financial information.

Previous research has focused more on the benefits of financial reports only for the investors (Dutta and Nezlobin, Citation2017) and the companies (Michaels & Grüning, Citation2017). Meanwhile, those considering costs and benefits for companies as well as investors in a comprehensive model are still limited. It is argued that large disclosures not only cause large costs for the company (Coffie and Bedi, Citation2018) but also provide great benefits (Bertomeu et al., Citation2021), a reduction in the cost of capital (Chen et al., Citation2022; Cuadrado-Ballesteros et al., Citation2016; J.E. Core et al., Citation2015), and an increase in company value (Cianciaruso & Sridhar, Citation2018; McMullin, 2018). Besides, the generous disclosures reduce information imbalance which benefits investors. Therefore, investors ask for a lower cost of capital (implicitly showing benefits also for the companies; Cheynel, Citation2013; Botosan, Citation2006). To comprehensively investigate the costs and benefits of financial reporting information for companies and investors at the same time in one financial reporting period, this study investigates the correlation between disclosure, information asymmetry, cost of capital, and firm value in one comprehensive recursive model. It is suggested that the correlation between disclosure, information asymmetry, cost of capital, and firm value is unidirectional dependency. Hence, for any given values of voluntary disclosure, values for information asymmetry, cost of capital, and firm value can be determined sequentially rather than jointly.

Therefore, testing the relationship separately between two factors, supposing that, between voluntary disclosure and information asymmetry only or between voluntary disclosure and cost of capital only, without examining the effect of this relationship on firm value, leads to a cost–benefit analysis inequality of voluntary disclosure to companies and investors. The costs and benefits of disclosure need to be viewed equally from both the company and investors. The negative relationship between voluntary disclosure and information asymmetry (Michaels & Grüning, Citation2017) reflects the high costs borne by investors (Cheynel, Citation2013). This relationship also indicates large benefits experienced by the company as a result of low disclosure. For this reason, information asymmetry is higher, or higher costs are experienced by the company. However, the investors perceive that the benefits are high resulting from high disclosure and low information asymmetry. The negative relationship between disclosure and cost of capital (He et al., Citation2019; Alves et al., Citation2015; Mangena et al., Citation2014) also shows the same result. High disclosure and low cost of capital cause the costs to be borne by investors to be greater, while the company enjoys the benefits of a low cost of capital. Conversely, low disclosure and high cost of capital generate large costs for the company as a result of the increased risk perceived by investors. This relationship does not fully describe the costs and benefits felt by the company and investors at the same time. By testing the recursive relationship of these four variables at once, it provides a comprehensive illustration of the costs and the benefits experienced by investors and companies with voluntary disclosure.

2. Background

The issue of the correlation between voluntary disclosure, information asymmetry, cost of equity capital, and firm value is not a contemporary concern that has been partially tested for more than two decades. The seminal papers of Leuz and Verrecchia (Citation2000) and Healy and Palepu (Citation2001) had explained the relationship of these four variables which led to the idea of recursively testing the four variables in one comprehensive model. Leuz and Verrecchia (Citation2000) explained that higher financial information disclosures reduce information asymmetry and the cost of equity capital. Consistently, Healy and Palepu (Citation2001) enlightened that the demand for disclosure increases due to agency conflict and high information asymmetry between managers and fund owners as reflected in higher cost of capital and lower share prices. Based on these two seminal papers, it can be discerned that information asymmetry and cost of capital mediate the relation between disclosure and firm value. Increased disclosure encourages lower information asymmetry and cost of capital, thereby rising firm value.

Previous research has tested empirically and partially the association between voluntary disclosure, information asymmetry, cost of equity capital, and firm value. In the early period, Botosan (Citation1997) showed a negative relationship between disclosure and the cost of capital. The higher the level of disclosure is, the lower the cost of capital will be. Recent empirical research supports the results of previous research in which the relationship between disclosure and information asymmetry and the cost of capital is negative. Michaels and Grüning (Citation2017) examined the relationship between disclosure, information asymmetry, and the cost of capital. Their results showed a negative association between voluntary disclosure and information asymmetry and between voluntary disclosure and the cost of corporate capital in Germany for the 2013/2014 period. He et al. (Citation2019) investigated the relationship between disclosure and cost of capital by using two types of disclosure, namely mandatory and voluntary disclosures. The results indicated that each of these types of disclosures affects the cost of capital. Previously, Mangena et al. (Citation2014) also tested mandatory disclosure and voluntary disclosure together on the cost of equity. The results indicated that the interaction between mandatory disclosure and voluntary disclosure decreases the cost of capital. Alves et al. (Citation2015) also examined the effect of voluntary disclosure on information asymmetry. It is found that increasing voluntary disclosure decreases information asymmetry. Besides, Blanco et al. (Citation2015) examined the effect of mandatory disclosure on the cost of capital. Their finding revealed that the operating segment disclosure has a significant negative effect on the cost of capital.

Supporting Healy and Palepu (Citation2001), Fosu et al. (Citation2016) examined the effect of information asymmetry on firm value. The results showed that low information asymmetry increases firm value during the financial crisis in the UK in the 2007/2009 period. In contrast to normal conditions, during the crisis, the company’s long-term debt has increased since the currency rate was uncertain, the purchasing power of one country’s currency against the currencies of other countries has decreased. Under this condition, information asymmetry is usually increased and firm value is decreased. Aligned with Fosu et al. (Citation2016), Huynh et al. (Citation2020) examined the correlation between information asymmetry and firm value of companies listed on the Vietnam stock exchange. In contrast to Fosu et al. (Citation2016) who took a sample of companies in the UK, Huynh et al. (Citation2020) took a sample of companies listed in Vietnam since they had a high debt ratio. The results showed that information asymmetry is negatively related to firm value. However, lower information asymmetry increases firm value. McMullin (Citation2019) examined the effect of disclosure on firm value and found that increasing mandatory disclosure increases firm value. In line with McMullin (2018), the results of Cianciaruso and Sridhar’s (Citation2018) research reported that an increase in mandatory and voluntary disclosure increases firm value.

Contrary to these studies, some previous studies in the early period did not support a negative relationship between voluntary disclosure and information asymmetry as well as between voluntary disclosure and the cost of equity capital. Botosan (Citation1997) concluded that the correlation between disclosure and the cost of capital is feeble. According to Zhang (Citation2001), differences in the results of previous studies are caused by the amount of disclosure depending on certain conditions and factors, such as disclosure costs, variations in earnings, etc. Botosan and Plumlee (Citation2002) have not identified this negative association either. Several recent studies have shown the same results. Lopes and de Alencar (Citation2010) stated that the frail correlation between disclosure and the cost of capital was influenced by environmental factors such as changes in financial accounting standards. Elena et al. (Citation2012) and Cuadrado-Ballesteros et al. (Citation2016) found that accounting reporting standards do not affect the quality of reports and also the cost of capital. These findings inform that the effects of disclosure, capital costs, and information asymmetry are inconclusive and become an interesting topic for further study.

This study aims to investigate the relationship between voluntary disclosure, cost of capital, information asymmetry, and firm value in a comprehensive recursive model. It contributes to advancing the disclosure accounting research in terms of developing research methodology to support the negative correlation between disclosure and cost of capital and information asymmetry as well as the negative relationship between information asymmetry and cost of capital and firm value. Some previous studies have partially tested the relationship between these variables. We argue that there is unidirectional dependency among the information asymmetry, cost of capital, and such firm value; hence, for any given value of voluntary disclosure, values for information asymmetry, cost of capital, and firm value can be determined sequentially rather than jointly. This study is the first one to test the unidirectional correlation between voluntary disclosure, information asymmetry, cost of capital, and firm value in one comprehensively recursive model. Previous studies have examined the simultaneously direct correlation between variables in an OLS model. This present study recursively examines the relationship between these variables in one comprehensive recursive model. The novelty of this study can be identified through the enhancement of a model framework to show the cost and benefit of disclosure for companies, investors and lenders in a comprehensive recursive model.

3. Theoretical review and hypothesis development

Agency theory broadly describes the connection between the variables tested in this study. First, it explains the relationship between disclosure, principal and agent, in which the principal and agent have the respective interests that need to be fulfilled through financial reporting. Principals expect them to obtain complete information regarding the company since this is related to the costs they have spent to invest. On the other hand, the authority that agents have over company information permits them to use the information for their benefit. Agent authority as the owner of information allows them to manipulate the company’s financial statements by selecting information that meets their interests and keeping the information private (Stocken & Verrecchia, Citation2004). It induces conflict of interest between agent and company’s owner cause of imbalance amount of information shared between investors and agents for decision-making (Hazaea et al., Citation2022). The standards or regulations that govern the financial reporting system are designed to be aware of the authority and interests of these principals and agents (Bertomeu & Magee, Citation2015). Previous research on the relationship between voluntary disclosure, information asymmetry, cost of capital, and firm value has shown different results.

3.1. Disclosure and information asymmetry

The problem of information asymmetry causes the market to be inefficient. When agents have more information than is available to the public, then the agent’s assessments and predictions on the company’s performance become more accurate than the public. This condition has different implications for companies and investors. Companies are encouraged to leave equity capital and choose debt capital (Shen, Citation2014). From the investor’s side, the issuance of new equity is likely to be lower. Hence, the wealth is shifted from existing shareholders to the new ones. Consequently, a lower price is a good reason for existing shareholders to reject a new investment that could generate positive net present value. In this case, the external financial costs become a burden for a company with higher asymmetric information.

Several past research supports those arguments. Leuz and Verrecchia (Citation2000) and Chiyachantana et al. (Citation2013) found that disclosure can reduce information asymmetry. Chang et al. (Citation2008) proved that increased exposure followed by increased analysts results in a lower cost of information asymmetry and has implications for increasing market capitalization. Renhui et al. (Citation2012) pointed out that high disclosure can reduce information asymmetry and the cost of capital. Buskirk (Citation2012) states that the relationship between disclosure and information asymmetry depends on the disclosure attributes being tested so that the results can be different. Agarwal et al. (Citation2015) argue that by examining the investor relationship variable, it is found that effective investor relations can encourage increased levels of disclosure and reduce information asymmetry. Cuadrado-Ballesteros et al. (Citation2016) proved that companies that increase disclosure of financial and social information tend to decrease information asymmetry.

However, Cheynel and Levine (Citation2020) demonstrated a different conclusion regarding the effect of disclosure on information asymmetry by using Mosaic theory. Investors are provided with a lot of public information that makes it easier for them to make decisions. However, what seems to be a concern is that high public disclosure increases information asymmetry if it is not accompanied by private disclosure.

H1: Higher disclosure reduces information asymmetry.

3.2. Disclosure and Cost of Capital (CoC)

We view the cost of capital from two viewpoints, from investor and company views. For investors, the CoC is the rate of return demanded by investor and lenders from their investment and loan they give (Vitolla et al., Citation2019). For the company, the CoC is companies’ expected return on their potential project or business prospect. Hence, the cost of capital reflects a trade-off between risk and return. When investors and lenders feel the risk is high, they will ask for a high CoC. Companies can increase bonding costs by providing as much information as possible about the investment being worked on. High and relevant information disclosure helps companies to reduce the level of risk perceived by investors and lenders so as to reduce the CoC (Lambert et al., Citation2007). Prior studies had supported those statement. Botosan and Plumlee (Citation2002) pointed out that high disclosure causes an increase in the cost of capital. Cheynel (Citation2013) mathematically formulated the effect of voluntary disclosure on cost of capital. Relying on voluntary disclosure, investors intend to avoid risk and increase return, so that, the more information obtained, the higher investor confidence in the company, which is reflected in a lower cost of capital.

Lopes and de Alencar (Citation2010) noted that increasing the number of disclosures by registered companies in Brazil can lower the cost of capital. Li (Citation2010) proved that disclosure under IFRS is able to reduce the cost of capital. A similar point was also confirmed by Apergis et al. (Citation2011) that an increase in the quality of accounting disclosure can increase expected cash flows, which then reduce the cost of capital. Furthermore, Embong et al. (Citation2012) mention that the negative relationship between disclosure and the cost of capital is more significant in large companies. Renhui et al. (Citation2012) also demonstrated a negative relationship between high disclosure of information asymmetry and the cost of capital. Elena et al. (Citation2012) examined the effect of voluntary disclosure on the cost of capital and revealed that increasing voluntary disclosure lowers the cost of capital. Besides, Mangena et al. (Citation2014) documented the effect of financial disclosures on the cost of capital. John E. Core et al. (Citation2014) reported that the cost of capital is decreased with increased disclosure in a sample of 35 countries from 1990 to 2004. Blanco et al. (Citation2015) discovered a negative relationship between segment disclosure and cost of capital. He et al. (Citation2019) confirmed that the cost of capital is affected by both voluntary disclosure, periodic mandatory disclosure, and event-driven disclosure. Setiany and Suhardjanto (Citation2021) show that higher disclosure lowers the cost of capital.

H2: Higher voluntary disclosure reduces the cost of capital.

3.3. Disclosure and firm value

Voluntary disclosure is the provision of information by management beyond the mandatory disclosures regulated by financial accounting standards, where the information is believed to be relevant to reveal the financial and non-financially firm performance. Cianciaruso and Sridhar (Citation2018) showed mathematically the effect of mandatory disclosure on firm value. The results revealed that financial information disclosure increases firm value in the future. Sheu et al. (Citation2010) and Chen and Lee (Citation2017) demonstrated that such disclosure affects firm value in companies in Taiwan.. Jiao (Citation2011) also mentioned the effect of mandatory disclosure on firm value in America. Faisal et al. (Citation2020) specifically observed the impact of disclosure on firm value. The results showed that higher voluntary disclosure increases firm value. Consistent with the previous results, tTemiz (Citation2021) and Assidi (Citation2020) illustrated a positive significant effect of voluntary disclosure on firm value. However, different findings are confirmed by Sumatriani et al. (). Their results indicated that disclosure does not increase the firm value of companies listed on the stock exchange of Indonesia, Malaysia, and Thailand for the period 2012–2015.

H3: Higher voluntary disclosure increases firm value.

3.4. Disclosure, cost of capital, information asymmetry, and firm value

It seems challenging to find literature showing the relationship between these four variables in a comprehensive model. Several research results support the relationship of these four variables separately. Bertomeu et al. (Citation2021) mathematically explained that higher voluntary disclosure provided a higher benefit for investor in the form of lower information asymmetry and for the company, i.e., lower cost of capital. Studies by Fosu et al. (Citation2016) and Alves et al. (Citation2015) had shown that the information asymmetry is expensive for the companies and investors due to adverse selection costs which prevent the companies from increasing company value and harming investors as identified from the high difference in selling and buying prices of shares. In this situation, the adverse selection cost forces companies to make less optimal investment decisions that seem to be unfavorable for firm value (Fosu et al., Citation2016). Therefore, financing with equity becomes more expensive than debt in conditions of high information asymmetry (Fosu et al., Citation2016; Myers, Citation1984).

This theory is relevant to several studies, such as Easley and O’Hara (Citation2004) which found that complete disclosure decreases the cost of equity capital because 1) it reduces the estimation risk for investors or 2) reduces the transaction costs due to the lack of information asymmetry. Complete disclosure increases expected cash flow which leads to lower capital costs (Apergis et al., Citation2011). This explanation is aligned with He et al. (Citation2019). More specifically, voluntary disclosure has a critical role in reducing information asymmetry (Alves et al., Citation2015). Regarding testing the implications for firm value, Agarwal et al. (Citation2015) and Chang et al. (Citation2008) identified a decrease in the cost of capital as a consequence of increased disclosure and ultimately an increase in market capitalization. Increasing the quality and quantity of disclosure is a consequence of the successful implementation of IFRS in lessening the cost of capital (Li, Citation2010).

Some previous studies showed the association of two or three variables only. Setiany and Suhardjanto (Citation2021) investigated the relationship between disclosure, cost of equity capital, and information asymmetry in an emerging market like Indonesia. They confirmed that the cost of equity capital is decreased by reducing information asymmetry through increased disclosure. Cuadrado-Ballesteros et al. (Citation2016) examined the correlation between information asymmetry, disclosure, and cost of equity capital. He stated that companies with low information asymmetry due to increased disclosure of financial and social information make the risk of estimation smaller and reduce the cost of capital with increased market liquidity. Liu and Chen (Citation2015) illustrated the relation between disclosure, information asymmetry, and firm value. They showed that high disclosure of financial information can reduce information asymmetry and increase financial transparency, thereby increasing the value of companies listed on the American Stock Exchange, namely on the NYSE, AMEX, and Nasdaq.

Fosu et al. (Citation2016) examined the effect of information asymmetry on firm value in the UK. Their results supported their proposed hypothesis that high information asymmetry reduces firm value. In particular, Huynh et al. (Citation2020) examined the relationship between information asymmetry and the value of companies listed on the Vietnam Stock Exchange. In line with Fosu et al. (Citation2016), their research findings showed that information asymmetry is negatively related to firm value. It means that the information asymmetry of companies in Vietnam is high and firm value is low. The information asymmetry of companies listed on the Vietnam Stock Exchange is relatively higher than that of companies listed on the stock exchanges of developed countries.

H4: Higher voluntary disclosure decreases the cost of capital, in that way increasing firm value.

H5: Higher voluntary disclosure decreases information asymmetry, in that way increasing firm value.

To summarize previous studies, as Hazaea et al. (Citation2022) way, this paper explains the top 10 leading papers regarding the relationship between voluntary disclosure, cost of capital, information asymmetry, and firm value as stated in Table .

Table 1. The top 10 foremost studies related to issues discussed

4. Research methods and materials

4.1. Sample and data

The samples were 1920 firm-years of non-financial issuers listed on the Indonesia Stock Exchange in the period 2012–2019 for which audited financial statements are presented. The samples were selected by random sampling method using the Slovin formula: n = N/(1 + (N x e2)), where n is the minimum sample size (1920), N is the population (4160), and e is the error margin (0.01675).

The data used were a voluntary disclosure index obtained employing a self-constructed index. Stock market data were in the form of closing prices, bid and ask prices, and a number of shares outstanding, as well as company financial data, to calculate the cost of capital. Bid and ask price, and closing price data were obtained from data provider www.investing.com. We calculated the eight-year average bid–ask spread based on monthly data from 2013 to 2020. The bid price, ask price, and closing price data taken were the average annual data around February to June each year. The average company published an annual report during these months. These ways are consistent with another recent study that used the average bid–ask spread as a proxy for information asymmetry. As in Michaels and Grüning’s (Citation2017) study, we included the natural logarithm of the bid–ask spread measure for information asymmetry.

4.2. Definition and operationalization of variables

Firm Value. Firm value reflects the composition of market value against book value of asset (Diantimala et al., Citation2021). Higher market value of equity pronounces higher firm value. Hence, firm value is calculated by using the Tobin’s Q ratio, the market value of equity to book value of asset ratio as proposed by Agarwal et al. (Citation2015) and used by Assidi (Citation2020) Bakri and McMillan (Citation2021), Diantimala et al. (Citation2021), tTemiz (Citation2021).

Disclosure. Complete and multiple disclosures are defined as the complete disclosure of corporate financial and non-financial information reflected by voluntary disclosure (Bertomeu & Magee, Citation2015). Multiple disclosures are conveyed in longer financial reporting so that the financial reporting pages are longer (Morunga and Bradbury, Citation2012). Voluntary disclosures are disclosures of financial and non-financial information that reflect the condition and performance of the company. Broadly speaking, voluntary disclosure describes (1) general company information; (2) the company’s business prospects; (3) research and development carried out by companies; (4) information about company employees; (5) product and service improvement; (6) corporate governance; (7) corporate social responsibility reporting; and (8) company financial information. Then, the explanation of each point was broken down in detail. We used a self-constructed index method to calculate the voluntary disclosure index. To assess voluntary disclosure, we employed a voluntary disclosure index developed by Botosan (Citation1997) which was adjusted to the Indonesian replacement regulation KEP-38/PM/1996, namely the Capital Market Supervisory Agency Regulation KEP-134/BL/2006. We used 1 if the voluntary disclosure items are disclosed, 0 otherwise to represent the voluntary disclosure items not available in issuers’ financial reporting. The formula used to measure the voluntary disclosure index is the amount of information disclosed/(the amount of information disclosed + the amount of information that should have been disclosed but not disclosed).

Cost of Capital. The cost of capital is the compensation that capital owners and lenders charge for the funds they provide to the company for more productive investment. In this study, COC is proxied by the Price Earnings Growth Ratio (PEG). PEG is used because it is considered more representative to examine the relationship between the level of disclosure and the cost of equity capital (Easton, Citation2004). PEG has been widely used by previous researchers (Botosan & Plumlee, Citation2002; Mangena et al., Citation2014; Cuadrado-Ballesteros et al., Citation2016). The PEG model is a suitable model to be used in calculating the cost of capital, based on several studies (Botosan & Plumlee, Citation2002; Easton, Citation2004; Mangena et al., Citation2014). The formula used to calculate Price Earnings Growth (COCPEG) is presented as follows:

COCPEG = √(EPS2-EPS1)/Po

where COCPEG = Price Earnings Growth Ratio (a proxy for the cost of capital). EPS2 = Earnings per Share in one year after the publication of the annual report. EPS1 = Earnings per Share in the year the annual report was published. P0 = Share price 1 year before the publication of the annual report.

Information Asymmetry. Information asymmetry is measured by the bid–ask spread (Leuz & Verrecchia, Citation2000). The bid–ask spread is a very valid measure for information asymmetry widely used by previous studies (Leuz & Verrecchia, Citation2000; Buskirk, Citation2012; Blanco et al., Citation2015; He, et al., 2013; Michaels & Grüning, Citation2017). The higher the spread between the bid price and the ask price is, the higher the information asymmetry will be. Conversely, the lower the spread between the bid price and the ask price is, the lower the information asymmetry will be among market participants (Michaels & Grüning, Citation2017). Similar to Michaels and Grüning (Citation2017), this study used proportional quoted half-spreads to measure information asymmetry, as follows: Proportional quoted half-spread = (ask price—bid price)/2*closing price. The summary of variables definition and measurement is stated in Table .

Table 2. Summary of variable definition and measurement

4.3. Analysis Method

We suggest that there is a unidirectional dependency among the information asymmetry, cost of capital, and firm value such that, for any given values of voluntary disclosure, values for information asymmetry, cost of capital, and firm value can be determined sequentially rather than jointly. Therefore, to examine all hypotheses, we used a recursive path model which explains the relationship among variables directly and indirectly as explained by Iaousse et al. (Citation2020). According to Iaousse et al. (Citation2020), the recursive path model describes a unidirectional dependency among the endogenous variables; therefore, for given values of exogenous variables, the values for the endogenous variables can be decided successively rather than mutually. In addition, the major advantage of the recursive path model is that it can consistently estimate using the Ordinary Least Square (OLS) method. The OLS estimators are BLUE which reflects the fulfilment of the classical assumption test. It indicates that the relationship among variables is linear, unbiased, and has the least variance among the class of all linear and unbiased estimators. This model avoids a close relationship between the disturbance term of members of a series of observations ordered in time (as in time-series data) or space (as in cross-sectional data). It strictly states no correlated disturbance term.

Based on Figure , we formulate recursive path model as follows: , where

is the function of DS,

or

… … … (1).

is the function of DS,

or

………………. (2), Finally, FV function can be reformulated as a recursive path model as follows:

Figure 1. Recursive path diagram.

… … … … … … … … . … … … (3) or

……………… . … … … . (4)

where FVit is firm value of firm i in the period t, DSit is voluntary disclosure of firm i in the period t, IAit is information asymmetry of firm i in the period t, COCit is cost of capital of firm i in the period t.

5. Results and discussion

This study aimed to examine whether complete and numerous disclosures of information are beneficial for companies as well as investors and lenders. Therefore, this study re-examined the relationship between disclosure, information asymmetry, cost of capital, and firm value in a comprehensive recursive model. We argued that the correlation between disclosure, information asymmetry, cost of capital, and firm value is unidirectional dependency. Hence, for any given values of voluntary disclosure, values for information asymmetry, cost of capital, and firm value can be determined sequentially rather than jointly. The results of hypothesis testing supported this argument. The descriptive statistics of all variables is shown in Table .

Table 3. Descriptive statistics

Statistical descriptions show that the mean of voluntary disclosure of companies in Indonesia is relatively moderate, between 54.1% and 59.4%, and fluctuates from year to year. The increase occurred in 2018 (63.4%) and 2019 (65.9%). The mean of disclosure is 0.579, indicating that companies disclose the information regarding general company information, the company’s business prospects, research and development carried out by companies, information about company employees, product and service improvement, corporate governance, corporate social responsibility reporting, and company financial information, on average, 57.9% with a range of 18.9% to 98.1%. The mean of information asymmetry is relatively low, 0.11, ranging from 0.000 to 0.807. This shows that information asymmetry in Indonesia is low even though there are companies that experience 80.7% and 0.00% of information asymmetry. The average cost of capital is 1.165, fluctuating between 1.128 and 1.184, within a range of a maximum of 2.281 and a minimum of 0.055. The mean of firm value is 1.519, fluctuating from year to year between 1.127 and 1.773 with a maximum range of 36.857 and a minimum of 0.021.

5.1. Main results

To support our argument that the correlation between disclosure, information asymmetry, cost of capital, and firm value is unidirectional dependency, we formulated a comprehensive recursive path model which showed direct effect and indirect effect amongst testing variables. The direct effect examined the effect of exogenous variables on endogenous variables directly, i.e., the effect of voluntary disclosure on information asymmetry, voluntary disclosure on cost of capital, voluntary disclosure on firm value, cost of capital on firm value, and information asymmetry on firm value. The indirect effect investigated the impact of voluntary disclosure on firm value through cost of capital and through information asymmetry. Consequently, for any given values of voluntary disclosure, values for information asymmetry, cost of capital, and firm value can be determined sequentially rather than jointly. Before that, we stated that all the conditions of the OLS form are meet.

5.2. Direct Effect

The results of direct and indirect effect testing are described in Figure (enclosed at the end of this paper) as well as in Table and Table , respectively.

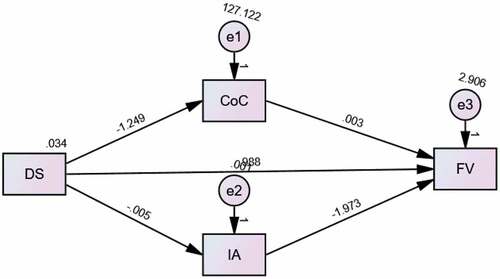

Figure 2. The result of path analysis.

Table 4. Direct effect among variables

Table 5. Indirect Effect between Variables

Pairing 1 shows the direct effect of voluntary disclosure on information asymmetry. Companies disclose financial and non-financial information voluntarily with the aim of avoiding information gaps between companies and their stakeholders. The more complete and numerous information is disclosed, the greater the cost of presenting the information; however, the benefits of the information for stakeholders are also large in reducing the information gap between them (Bertomeu et al., Citation2021). The results of this study support the previous literature regarding negative relation between voluntary disclosure and information asymmetry. The voluntary disclosure has a significantly negative effect on information asymmetry (P.C. −0.280; S.E. 0.052; C.V. −5.359) at 1% level. The results are aligned with previous researches, i.e., Renhui et al. (Citation2012), Buskirk (Citation2012), Agarwal et al. (Citation2015), and Cuadrado-Ballesteros et al. (Citation2016) who found that higher disclosure reduces information asymmetry. The result is also in line with Leuz and Verrecchia (Citation2000) and Chiyachantana et al. (Citation2013) that voluntary disclosure reduces information asymmetry. Companies that increase disclosure of financial and non-financial information tend to decrease information asymmetry. The more information that is conveyed to the public, the information gap between market participants who have superior information and market participants who do not have this information is getting smaller. Therefore, the more information the company conveys, the price speculated by investors who do not have superior information is closer to the price offered by superior market participants. It supports hypothesis 1.

Furthermore, pairing 2 indicates the direct effect of voluntary disclosure on the cost of capital. Investor rely on voluntary disclosure to avoid risk and increase return, so that, the more information obtained, the higher investor confidence in the company, which is reflected in a lower cost of capital (Cheynel, Citation2013). The voluntary disclosure gives a significantly negative effect on the cost of capital (P.C. −0.690; S.E. 0.103; C.V. −6.714) at the alpha level of 1%, meaning that higher voluntary disclosure significantly reduces the cost of capital. It is consistent with previous studies (Embong et al., Citation2012; Renhui et al., Citation2012: Elena et al., Citation2012; Mangena et al., Citation2014; John E. Core et al., Citation2014; Blanco et al., Citation2015; He et al., Citation2018) revealing that increasing disclosure lowers the cost of capital. An increase in the quality of accounting disclosure rises expected cash flows, which then reduces the cost of capital and increase firm value (Cheynel, Citation2013). Thus, the results confirm hypothesis 2.

Pairing 3 reveals the direct effect of voluntary disclosure on firm value. The voluntary disclosure has a significantly positive effect on firm value at the 1% level (P.C. 0.175; S.E. 0.213; C.V. 3.365). This result illustrates that increased voluntary disclosure escalates firm value. It accords with Sheu et al. (Citation2010), Liu and Chen (Citation2015), and Cianciaruso and Sridhar (Citation2018) which reported that disclosure of financial information increases firm value in the future. This result supports hypothesis 3. Further, pairing 4 demonstrates the direct effect of the cost of capital on firm value. The cost of capital has a significant negative effect on firm value (P.C. −0.338; S.E. 0.046; C.V. −7.297) at the alpha level of 1%. An increase in the cost of capital lessens the value of the company. Meanwhile, pairing 5 performs the direct effect of information asymmetry on firm value. The information asymmetry shows a significantly negative effect on firm value (P.C. −0.163; S.E. −0.163; C.V. −1.793). It implies that lower information asymmetry improves firm value. This result is reliable with studies conducted by Fosu et al. (Citation2016) and Huynh et al. (Citation2020), that higher information asymmetry reduces firm value.

5.3. Indirect effect

Indirect effect testing at the same time regarding the impact of voluntary disclosure on firm value through the cost of capital and information asymmetry is presented in Table . The first test investigates whether increased voluntary disclosure is able to reduce information asymmetry, thereby increasing firm value. The second test assesses whether the increase in voluntary disclosure is able to decrease the cost of capital, thereby increasing firm value. The test results are shown in Pairing 6 and Pairing 7. Pairing 6 demonstrates that the sign of the relationship between disclosure and cost of capital is negative. It is consistent with our expectation. However, the sign of the relation between cost of capital and firm value is positive, it is not coherent with our prediction. The result show that higher voluntary disclosure significantly affects firm value indirectly through the cost of capital (Z-Sobel Test = 4,950, p-value = 0.000) at the 1% level. Based on the sign, an increase in voluntary disclosure decreases the cost of capital (coef. = −1.249), and then, lower cost of capital reduces firm value (coef. = 0.003). It is inconsistent with previous research pointing out that a decrease in the cost of capital increases the firm value. These findings suggest that higher disclosure reduces the cost of capital, which unfortunately, decreases the firm value. The results are not aligned with Cuadrado-Ballesteros et al. (Citation2016) which states that companies with higher disclosure of financial and social information lessen the risk of estimation and the cost of capital with increased market liquidity caused by an increase in firm value. Thus, these results are not in accordance with hypothesis 4 (H4) which state that higher voluntary disclosure decreases the cost of capital, in that way increasing firm value.

In addition, pairing 7 reveals that disclosure significantly affects firm value indirectly through information asymmetry (Z-Sobel Test = 1.69, p-value = 0.089) at the 10% level. The sign of the correlation between voluntary disclosure and information asymmetry is negative, as also the correlation between information asymmetry and firm value. These signs are consistent with our expectation. Based on the signs, we conclude that increasing voluntary disclosure decreases information asymmetry (coef. = 0.005), in that way, improves firm value (coef. = —1.973). The result in line with Liu and Chen (Citation2015), higher disclosure of financial information reduces information asymmetry and then increase financial transparency, thereby raising the value of companies. As a result, these findings support hypothesis 5 (H5) that higher voluntary disclosure decreases information asymmetry, in that way increasing firm value.

In general, the results show that complete and numerous disclosures by a company are beneficial for investors in form of lower information asymmetry, as well as for the company in the form of lower cost of capital and higher firm value Conveying complete and plenty information to the public reduces the information gap amongst market players, between management and investors, and between management and lenders (Michaels & Grüning, Citation2017; Helay and Palepu, Citation2001), lower the cost of capital (Michaels & Grüning, Citation2017; Botosan, Citation1997; Francis et al., 2005), and increase public trust to the company (Sheu et al., Citation2010); thus, it increases firm value (McMullin, Citation2018). The results specifically fill the gap that the companies benefit greatly as a consequence of the large costs incurred to produce complete and multiple disclosures in their financial reports (Coffie and Bedi, Citation2019), and investors obtain the most benefit from disclosure of financial information.

6. Conclusion

This study aims to investigate whether more complete and numerous voluntary disclosures by a company are beneficial for investors as well as for the company. Conveying complete and plentiful information to the public is expected to reduce the information gap between market players, management and investors, and management and lenders, lower the cost of capital, and increase public trust in the company, thereby increase firm value. Therefore, this study examines the impact of voluntary disclosure on cost of capital and information asymmetry, and then on firm value in a comprehensively recursive model. We argue that there is unidirectional dependency among the information asymmetry, cost of capital, and such this firm value, for any given values of voluntary disclosure, values for information asymmetry, cost of capital, and firm value can be determined sequentially rather than jointly. The unidirectional dependency amongst exogenous and endogenous variables are the unique characteristic of recursive model. The results show that the negatively direct effect of disclosure on information asymmetry and cost of capital is consistent with the hypothesis. The indirect effect of disclosure on firm value through the information asymmetry and cost of capital is also relevant to the hypothesis. The findings suggest that higher disclosure provides great benefits for the companies as well as investors and lenders. Increasing disclosure reduces information asymmetry and the cost of capital, thereby increasing firm value.

In regard to the direct effect, the results showed that voluntary disclosure has a significantly negative effect on the cost of capital and information asymmetry as well as has a significant positively impact on firm value. Higher voluntary disclosure significantly reduces information asymmetry. Companies that offer more financial and non-financial information voluntarily, tend to experience lower information asymmetry. The more information that is conveyed to the public, the information gap between market participants who have superior information and market participants who do not have superior information is getting smaller. Therefore, the more information the company conveys, the price speculated by investors who do not have superior information is closer to the price offered by superior market participants. It supports hypothesis 1. Furthermore, investor rely on voluntary disclosure to avoid risk and increase return, so that, the more information obtained, the higher investor confidence in the company, which is reflected in a lower cost of capital. The voluntary disclosure gives a significantly negative effect on the cost of capital. This result is consistent with previous literature which state that revealing that increasing disclosure lowers the cost of capital. An increase in the quality of accounting disclosure rises expected cash flows, which then reduces the cost of capital and increase firm value. Thus, the results confirm hypothesis 2. Moreover, the voluntary disclosure has a significantly positive effect on firm value. It is meant that increased voluntary disclosure escalates firm value. The result supports hypothesis 3 (H3).

Concerning the indirect effect, the results revealed that higher disclosure significantly affects firm value indirectly through the cost of capital. The sign of the relationship between disclosure and cost of capital is negative. It is consistent with our expectation. However, the sign of the relation between cost of capital and firm value is positive, which is not coherent with our prediction. An increase in voluntary disclosure decreases the cost of capital, in that way, decreases firm value. This finding is inconsistent with previous research, reporting that a decrease in the cost of capital higher firm value. These results showed that higher disclosure reduces the cost of capital, which unfortunately, decreases the firm value. The results fail to support hypothesis 3. Moreover, the results illustrate that disclosure significantly influences firm value indirectly through information asymmetry. Increasing disclosure decreases information asymmetry while decreasing information asymmetry increases firm value. In line with previous results, higher disclosure of financial information can reduce information asymmetry and improve financial transparency, thereby increasing the value of companies. Companies with higher disclosure of financial and social information lessen the risk of estimation and the cost of capital with increased market liquidity caused by an increase in firm value. Therefore, these results accept hypothesis 4.

In addition, pairing 7 reveals that disclosure significantly affects firm value indirectly through information asymmetry at the 10% level. The sign of the correlation between voluntary disclosure and information asymmetry is negative, as also the correlation between information asymmetry and firm value. These signs are consistent with our expectation. Based on the signs, we conclude that increasing voluntary disclosure decreases information asymmetry, in that way, improves firm value. As a result, these findings support hypothesis 5 (H5).

Acknowledgements

We gratefully acknowledge the financial support of Universitas Syiah Kuala (USK) who provided funding for this research in 2020.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Yossi Diantimala

Yossi Diantimala is an Associate Professor at the Faculty of Economics and Business, Universitas Syiah Kuala, Banda Aceh, Indonesia. She holds a doctorate in Financial Accounting from the University of Gadjah Mada, Yogyakarta, Indonesia. Her research interests are financial accounting standards, disclosure, corporate governance, and accounting education.

Sofyan Syahnur

Sofyan Syahnur is an Associate Professor in Macroeconomics, Universitas Syiah Kuala. He completed his doctoral degree program in Economics at Bonn University. His research focuses on macroeconomics and economic modeling.

Islahuddin Islahuddin

Islahuddin Islahuddin is an associate professor at Accounting Department, Universitas Syiah Kuala. He received his Doctor of Philosophy from School of Management, Universiti Sains Malaysia in 2000. Finance and accounting standards are his research focus.

References

- Abdi, H., & Omri, M. A. B. (2020). Web-based disclosure and the cost of debt: MENA countries evidence. Journal of Financial Reporting and Accounting, 18(3), 533–18. https://doi.org/10.1108/jfra-07-2019-0088

- Agarwal, V., Taffler, R. J., Bellotti, X., & Nash, E. A. (2015). Investor relations, information asymmetry, and market value. Accounting and Business Research. https://doi.org/10.1080/00014788.2015.1025254

- Alves, S. H., Canadas, N., & Rodrigues, M. A. (2015). Voluntary disclosure, information asymmetry, and the perception of governance quality: An analysis using a structural equation model. Tekhne, Review of Applied Management Studies, 13, 66–79. http://dx.doi.org/10.1016/j.tekhne.2015.10.001

- Apergis, N., Artikis, G., Eleftherious, S., & Sorros, J. (2011). Accounting information and cost of capital: A theoretical approach. Modern Economy, 2(4), 589–596. https://doi.org/10.4236/me.2011.24066

- Assidi, S. (2020). The effect of voluntary disclosures and corporate governance on firm value: A study of listed firms in France. International Journal of Disclosure and Governance, 17(2–3), 168–179. https://doi.org/10.1057/s41310-020-00090-1

- Bakri, A. M., & McMillan, D. (2021). Moderating effect of audit quality: The case of dividend and firm value in Malaysian firms. Cogent Business & Management, 8(1), 2004807. https://doi.org/10.1080/23311975.2021.2004807

- Bertomeu, J., & Magee, R. P. (2015). Mandatory disclosure and asymmetry in financial reporting. Journal of Accounting and Economics, 59(2–3), 284–299. https://doi.org/10.1016/j.jacceco.2014.08.007

- Bertomeu, J., Vaysman, I., & Xue, W. (2021). Voluntary versus mandatory disclosure. Review of Accounting Studies, 26(2), 658–692. https://doi.org/10.1007/s11142-020-09579-0

- Blanco, B., Garcia Lara, J. M., & Tribo, J. A. (2015). Segment Disclosure and Cost of Capital. Journal of Business Finance & Accounting, 42(3–4), 367–411. https://doi.org/10.1111/jbfa.12106

- Botosan, C. A. (1997). Disclosure level and the cost of equity capital. The Accounting Review, 72(3), 323–349. https://www.jstor.org/stable/248475

- Botosan, C. A., & Plumlee, M. A. (2002). A re-examination of disclosure level and the cost of equity capital. Journal of Accounting Research, 40(1), 21–40. https://doi.org/10.1111/1475-679X.00037

- Buskirk, A. V. (2012). Disclosure frequency and information asymmetry. Review of Quantitative Finance and Accounting, 38(4), 411–440. https://doi.org/10.1007/s11156-011-0237-0

- Chang, M., D’Anna, G., Watson, I., & Wee, M. (2008). Does disclosure quality via investor relations affect information asymmetry? Australian Journal of Management, 33(2), 375–390. https://doi.org/10.1177/031289620803300208

- Chen, Y. C. R., & Lee, C.-H. (2017). The influence of CSR on firm value: An application of panel smooth transition regression on Taiwan. Applied Economics, 49(34), 3422–3434. https://doi.org/10.1080/00036846.2016.1262516

- Chen, J., Li, N., & Zhou, X. (2022). Equity financing incentive and corporate disclosure: New causal evidence from SEO deregulation. Rev Account Stud. https://doi.org/10.1007/s11142-021-09662-0

- Cheynel, E. (2013). A theory of voluntary disclosure and cost of capital. Review of Accounting Studies, 18(4), 987–1020. https://doi.org/10.1007/s11142-013-9223-1

- Cheynel, E., & Levine, B. C. (2020). Public disclosure and information asymmetry: A theory of the mosaic. The Accounting Review, 95(1), 79–99. https://doi.org/10.2308/accr-52447

- Chiyachantana, N. C., Nuengwang, N., Taechapiroontong, N., & Thanarung, P. (2013). The effect of information disclosure on information asymmetry. Investment Management and Financial Innovations, 10(1), 225–234.

- Cianciaruso, D., & Sridhar, S. S. (2018). Mandatory and Voluntary Disclosure: Dynamic interactions. Journal of Accounting Research, 56(4), 1253–1283. https://doi.org/10.1111/1475-679X.12210

- Coffie, W., Bedi, I., & Amidu, M. (2018). The Effect of Audit Quality on the Cost of Capital of Firms in Ghana. Journal of Financial Reporting and Accounting, 16(4), 639–659. https://doi.org/10.1108/JFRA-03-2017-0018

- Core, J. E., Hail, L., & Verdi, R. S. (2014). Mandatory disclosure quality, inside ownership, and cost of capital. European Accounting Review. https://doi.org/10.1080/09638180.2014.985691

- Core, J. E., Hail, L., & Verdi, R. S. (2015). Mandatory disclosure quality, inside ownership, and cost of capital. European Accounting Review, 24(1), 1–29. https://doi.org/10.1080/09638180.2014.985691

- Cuadrado-Ballesteros, B., Garcia-Sanchez, I.-M., & Martinez Ferrero, J. (2016). How are corporate disclosures related to the cost of capital? The fundamental role of information asymmetry. Management Decision, 54(7), 1669–1701. https://doi.org/10.1108/md-10-2015-0454

- Diantimala, Y., Syahnur, S., Mulyany, R., Faisal, F., & Ntim, C. G. (2021). Firm size sensitivity on the correlation between financing choice and firm value. Cogent Business & Management, 8(1), 1926404. https://doi.org/10.1080/23311975.2021.1926404

- Dutta, S., & Nezlobin, A. (2017). Dynamic Effects of Information Disclosure on Investment Efficiency. Journal of Accounting Research, 55(2), 329–369. https://doi.org/10.1111/1475-679X.12161

- Easley, D., & O’Hara, M. (2004). Information and the cost of capital. Journal of Finance, 59(1), 553–1583. https://doi.org/10.1111/j.1540-6261.2004.00672.x

- Easton, P. (2004). PE ratios, PEG ratios, and estimating the implied expected rate of return on equity capital. The Accounting Review, 79(1), 73–95. https://doi.org/10.2308/accr.2004.79.1.73

- Elena, P., Georgakopoulos, G., Sotiropoulos, I., Konstantinos, Z., & Vasileiou. (2012). Relationship between cost of equity capital and voluntary corporate disclosures. International Journal of Economics and Finance, 4(3), 83–96. https://doi.org/10.5539/ijef.v4n3p83

- Embong, Z., Mohd-Saleh, N., & Hassan, M. S. (2012). Firm size, disclosure, and cost of equity capital. Asian Review of Accounting, 20(2), 119–139. https://doi.org/10.1108/13217341211242178

- Faisal, F., Situmorang, L. S., Achmad, T., & Prastiwi, A. (2020). The Role of Government Regulations in Enhancing Corporate Social Responsibility Disclosure and Firm Value. The Journal of Asian Finance, Economics and Business, 7(8), 509–518. https://doi.org/10.13106/jafeb.2020.vol7.no8.509

- Fosu, S., Danso, A., Ahmad, W., & Coffie, W. (2016). Information asymmetry, leverage, and firm value: Do crisis and growth matter? International Review of Financial Analysis, 46, 140–150. https://doi.org/10.1016/j.irfa.2016.05.00

- Hazaea, A. S., Zhu, J., Khatib, A. F. S., Bazhair, H. A., & Elamer, A. A. (2022). Sustainability assurance practices: A systematic review and future research agenda. Environmental Science and Pollution Research, 29, 4843–4864. https://doi.org/10.1007/s11356-021-17359-9

- Healy, P. M., & Palepu, K. G. (2001). Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics, 31(1–3), 405–440.

- He, J., Plumlee, M. A., & Wen, H. (2019). Voluntary disclosure, mandatory disclosure and the cost of capital. Journal of Business Finance and Accounting, 46(3–4), 307–335. https://doi.org/10.1111/jbfa.12368

- Huynh, D. L. T., Wu, J., & Duong, T. A. (2020). Information asymmetry and firm value: Is Vietnam different?. The Journal of Economic Asymmetries, 21.

- Iaousse, M., El Hadri, Z., Hmimou, A., & El Kettani, Y. (2020). An iterative method for the computation of the correlation matrix implied by a recursive path model. Quality & Quantity, 55(3), 897–915. https://doi.org/10.1007/s11135-020-01034-1

- Jiao, Y. (2011). Corporate disclosure, market performance, and firm performance. Financial Management, 40(3), 647–676. https://doi.org/10.1111/j.1755-053X.2011.01156.x

- Lambert, R., Leuz, C., & Verrecchia, R. E. (2007). Accounting information, disclosure, and the cost of capital. Journal of Accounting Research, 45(2), 385–420. https://doi.org/10.1111/j.1475-679X.2007.00238.x

- Leuz, C., & Verrecchia, R. E. (2000). The economic consequences of increased disclosure. Journal of Accounting Research, 38(3), 91–124. https://doi.org/10.2307/2672910

- Li, S. (2010). Does mandatory adoption of international financial reporting standards in the European Union reduce the cost of equity capital? The Accounting Review, 85(2), 607–636. https://doi.org/10.2308/accr.2010.85.2.607

- Liu, C., & Chen, N. (2015). Earnings surprises and analysts’ forecasts, mandatory disclosure, and share repurchases. Abacus, 51(1), 63–85. https://doi.org/10.1111/abac.12043

- Lopes, A. B., & de Alencar, R. C. (2010). Disclosure and cost of equity capital in emerging markets: The Brazilian case. International Journal of Accounting, 45(4), 443–464. https://doi.org/10.1016/j/intacc.2010.09.003

- Mangena, M., Li, J., & Tauringana, V. (2014). Disentangling the effects of corporate disclosure on the cost of equity capital: A study of the role of intellectual capital disclosure. Journal of Accounting, Auditing & Finance, 1–25. https://doi.org/10.1177/0148558XI4541443

- McMullin, J. L., Miller, B. P., & Twedt, B. J. (2019). Increased mandated disclosure frequency and price formation: Evidence from the 8-K expansion regulation. Review of Accounting Studies, 24(1). https://doi.org/10.1007/s11142-018-9462-2

- Michaels, A., & Grüning, M. (2017). Relationship of corporate social responsibility disclosure on information asymmetry and the cost of capital. J Manag Control, 28(3), 251–274. https://doi.org/10.1007/s00187-017-0251-z

- Morunga, M., & Bradbury, E. M. (2012). The impact of IFRS on annual report length. International Journal of Economics and Accounting, 6(5), 46–62. https://doi.org/10.1504/ijea.2017.10013447

- Myers, S. C. (1984). Capital structure puzzle. Journal of Finance, 39(3), 575–592. https://doi.org/10.2307/2327916

- Renhui, F., Kraft, A., & Zhang, H. (2012). Financial reporting frequency, information asymmetry, and the cost of equity. Journal of Accounting and Economics, 54(2–3), 132–149. https://doi.org/10.1016/j.jacceco.2012.07.003

- Setiany, E., & Suhardjanto, D. (2021). Disclosure, information asymmetry and the cost of equity capital: Evidence from Indonesia. In W. A. Barnett & B. S. Sergi (Eds.), Recent developments in Asian economics international symposia in economic theory and econometrics (international symposia in economic theory and econometrics (Vol. 28, pp. 351–366). Emerald Publishing Limited. https://doi.org/10.1108/S1571-038620210000028020.

- Shen, C. H. H. (2014). Pecking order, access to the public debt market, and information asymmetry. International Review of Economics & Finance, 29, 291–306. https://doi.org/10.1016/j.iref.2013.06.002

- Sheu, J. H., Chung, H., & Liu, L. C. (2010). Comprehensive disclosure of compensation and firm value: The case of policy reforms in an emerging market. Journal of Business Finance and Accounting, 37(9 and 10), 1115–1144. https://doi.org/10.1111/j.1468-5957.2010.02213.x

- Stocken, P., & Verrecchia, R. (2004). Financial reporting system choice and disclosure management. The Accounting Review, 79(4), 1181–1203. https://doi.org/10.2308/accr.2004.79.4.1181

- tTemiz, H. (2021). The effects of corporate disclosure on firm value and firm performance: Evidence from Turkey. International Journal of Islamic and Middle Eastern Finance and Management, 14(5), 1061–1080. https://doi.org/10.1108/IMEFM-06-2020-0269

- Vitolla, F., Salvi, A., Raimo, N., Petruzzella, F., & Rubino, M. (2019). The impact on the cost of equity capital in the effects of integrated reporting quality. Business Strategy and the Environment. https://doi.org/10.1002/bse.2384

- Wong, B. J., & Zhang, Q. (2022). Stock market reaction to adverse ESG disclosure via channels. The British Accounting Review, 54(1), 101045. https://doi.org/10.1016/j.bar.2021.101045

- Zhang, G. (2001). Private information production, public disclosure, and the cost of capital: Theory and implications. Contemporary Accounting Research, 18(2), 363–384. https://doi.org/10.1506/N6G3-RWX7-Y15L-BWPV