?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The Union of European Football Associations (UEFA) has become an industry in recent decades that has attracted many investors. The UEFA issued a Financial Fair Play Regulation (FFPR) policy to control the financial condition of football clubs. This study aims to determine the effect of leverage and financial distress on applying the principle of conservatism to provide a sense of security to investors and creditors. It is quantitative research that uses purposive data from the football companies listed on the London Stock Exchange in 2011–2013. The results indicate that the level of leverage and financial distress positively affect the application of the conservatism principle. In conclusion, the higher level of debt and financial distress will increase the company’s applying the conservatism principle. A suggestion for further research is to test the theory against football leagues in other countries because football leagues in other countries may have different rules.

1. Introduction

Football in Europe has become a multi-million-euro industry in recent decades, attracting many investors, global media, sponsors, and millions of supporters (Dimitropoulos et al., Citation2016). The football industry is considered to be able to generate large amounts of money. This can be seen from the income earned by football clubs from the sale of match tickets, club knick-knacks, sponsored products, television broadcasting rights, and player transfers (Citation2016). The total revenue earned by professional clubs competing in the English Premier League reached $7.3 billion during the 2017/18 season (Reed, Citation2019), based on the revenue generated by football clubs in England, which could encourage investor interest in investing in football clubs. Cave and Miller (Citation2016) reveal that major club acquisitions that occurred in 2015 included the acquisition of West Bromwich Albion by a Chinese investment group, the sale of a 60% stake in Swansea City for £110 million to an American consortium led by investors Kaplan and Levien 49.9% stake in Everton bought by Iranian billionaire Farhad Moshiri, 70% stake in Crystal Palace for £100 million by a group of American investors, even Aston Villa who were relegated that season sold for £70 million to Chinese businessman Tony Xia.

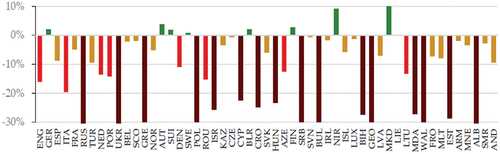

Although the investment value and income that goes into English football clubs are quite high, in reality, there are many clubs that are experiencing financial difficulties. This was caused by an increase in salary payments to players who absorbed 90% of the total turnover value of the top European club divisions recorded by UEFA in 2008 (Zoccali, Citation2011). Franck (Citation2018) states that there are unstable conditions experienced by football clubs in Europe caused by excessive investment that is not proportional to the income earned, resulting in the majority of football clubs in Europe experiencing financial distress. Figure shows the aggregate operating profit of football clubs in Europe which focuses on the operating profit of football clubs originating from the core activities of football which shows an indication of football clubs experiencing financial distress. The red column indicates that the country with the club in the top division spent between €1.10 and €1.20 to earn €1.00 in revenue, while the dark red column shows the country that spent more than €1.20 to earn €1.00 (Franck, Citation2018).

Figure 1. Aggregated net profit/loss for the league in 2011.

Seeing the many phenomena of football clubs experiencing crisis conditions and being threatened with bankruptcy due to the imbalance between the investment value and the income earned by football clubs in England, UEFA 2010 began to introduce the Financial Fair Play Regulation (FFPR), which aims to ensure the club’s financial health condition. Football is registered for competitions organized by UEFA. The regulation ensures that football clubs wishing to enter the competition do not have debts due to other clubs, players, and tax authorities during the season (UEFA, Citation2014). In this regulation, UEFA stipulates that every football club that registers to take part in a professional league competition held by UEFA must comply with the provisions of the FFPR. When the football club does not meet the provisions of FFPR, it will then become the authority of the Club’s Financial Control Body. The club, from now on referred to as the CFCB) to decide on actions and provide sanctions, actions, and sanctions that the CFCB can give in the form of warnings, reprimands, fines, deductions from points, deductions from UEFA competitions, prohibition of registering new players in UEFA competitions, limiting the number of players which can be registered, disqualification from the ongoing competition or exclusion from the next season’s competition, even up to the withdrawal of a title or award (UEFA, Citation2014).

Responsibility and protecting the viability and long-term sustainability of European football clubs (Morrow & Senaux, Citation2013). UEFA enacted FFPR to increase clubs’ economic and financial capacity, increase transparency and credibility of financial reports, improve the protection of creditors, introduce more disciplined and rational financing to football clubs, encourage clubs to conduct revenue-based operations, and encourage more efficient use of budgets. The determination of the FFPR policy by UEFA as a control tool to determine the health of football clubs’ financial conditions is in line with the principle of accounting conservatism. With this goal in mind, the application of FFPR focuses on protecting creditors, whereas the principle of conservatism also has the same goal. The application of the principle of conservatism is used as a counterweight to the attitude of managers who tend to be opportunistic to increase profits with the aim of increasing bonuses that can be received by managers, which can later reduce the value of the company in the future. The implementation of FFPR by UEFA on European football clubs in 2010 was in response to the many cases of financing the club’s operational activities that used the owner’s personal funds and large amounts of debt so that the financial statements presented by football clubs became biased and could interfere with the decision-making process by interested parties.

The use of large amounts of debt to finance the operational activities of football clubs in Europe is caused by a management culture that prioritizes winning on the field and overriding financial reporting performance, which results in football clubs being involved in expensive player transfer markets and giving players salaries that are too high (Dimitropoulos et al., Citation2016). With the high number of debts owed by the company, creditors have the right to oversee the company’s operational activities, so the company will apply the principle of conservatism in reporting earnings (Dewi & Suryanawa, 2014). This also applies to the football industry, which has financial reports and business processes that are not much different from conventional companies, so when a football club has a high debt rate, the club will tend to increase the value of conservatism in its financial reporting process. The increase in the value of conservatism in financial statements is used to meet requests from creditors and investors as a means of controlling the information asymmetry held by management (Watts, Citation2003). With the application of the principle of conservatism in the financial reporting process, it is expected to limit the opportunistic behaviour of managers so that the use of the budget can be used to increase the value of football clubs in the future. UEFA has also set a limit on the total amount of debt that can be obtained by a football club during one season in the FFPR regulations. This is done by UEFA to ensure that football clubs have sound financial statements and can pay any obligations that the club has.

The application of the FFPR policy by UEFA to European football clubs is based on the existence of large-scale spending activities carried out by many European football clubs with the aim of gaining victory in the competition. Massive spending by football clubs is usually used for player spending and infrastructure improvement in the hope that when the club has the best players and adequate facilities, it will be able to give the team victory and increase the popularity of the football club. Uncontrolled spending of football clubs can cause football clubs to experience financial distress, this is caused by investments made by football clubs to players, and infrastructure is not able to encourage an increase in club income during the season, so UEFA needs to implement a licensing policy that involves financial statements (Buraimo et al., Citation2010). With the implementation of FFPR by UEFA, football clubs are required to submit annual financial reports to be able to enter the competition so that UEFA can monitor the financial condition of football clubs that register for the competition. Football clubs can carry out the application of the principle of conservatism in financial statements as a response to the conditions of uncertainty faced by clubs. Restrictions on dividend payments and commissions to managers can help clubs focus on using their budget to increase the club’s value in the future and save more cash to deal with these conditions.

2. Literature review and hypotheses development

2.1. Agency theory

Agency theory, according to (Jensen & Meckling, Citation1976), is a relationship based on a contract between the principal (investor) and the agent (manager) to provide services that involve the process of delegating authority in the decision-making process to the agent. This theory emphasizes the design of performance measurement and the rewards provided with the aim that managers can make positive decisions and can provide benefits to the company as a whole (Raharjo, Citation2007).

Measurement of achievement in the football industry is usually seen from the club’s performance during the current season, so that managers tend to spend large amounts to achieve these goals, while from the principals, it is more important to prioritize how the club can continue to provide benefits so that later it will cause agency costs that result in loss firm value (Dimitropoulos et al., Citation2016). The results obtained from the emergence of agency costs in a club cause an imbalance between club expenses and the achievements or results obtained. This shows that football clubs need regulation or a system that can limit the amount of club spending each season to fulfil the obligations of a club.

2.2. Positive accounting theory

Positive accounting theory focuses on explaining a process that uses accounting skills, understanding, and knowledge to use the most appropriate accounting policies to deal with future conditions (Watts & Zimmerman, Citation1986). Accounting theory seeks to explain several events from an accounting point of view in the form of (1) the number of costs incurred is proportional to the benefits obtained in the selection of alternative accounting methods, (2) the amount of costs incurred is proportional to the benefits obtained in the regulation and accounting standard-setting process, and (3) the impact of published reports on stock prices.

Watts and Zimmerman (Citation1986) in accounting theory argue that there is one hypothesis in accounting theory that can motivate managers to perform earnings management the debt covenant hypothesis. The existence of conditions of uncertainty in the company makes managers required to be able to apply appropriate policies to the conditions faced and be able to ensure the going concern ability of the company so that in the process, there is a possibility that a manager will carry out earnings management to deal with certain conditions. This means that when a company has a high leverage ratio, there is a tendency for managers to transfer future profits to the present in order to avoid the consequences of debt agreements made by the company to creditors so that part of the supervisory function shifts to creditors and creditors have authority to pressure managers to fulfil agreed-upon agreements.

2.3. Leverage on the application of the conservatism principle

Leverage in the company refers to the amount of funding that comes from debt in the company’s capital structure and is an indication of the level of security of the lenders. When the company has been given a loan by the creditor, the creditor automatically has an interest in the security of the loaned funds in the hope of making a profit. In practice, the company wants to show good performance to lenders by presenting optimistic financial statements by increasing the value of assets and profits and reducing the value of liabilities and expenses. This is done with the aim of obtaining long-term loans and providing a sense of security for lenders to provide loan funds to the company. Furthermore, the most important thing in agency theory is that the supervisory function of the owner will be assisted by the creditor.

Thus the function of leverage will help apply the principle of conservatism because a company’s liquidity is considered an important ratio to measure the company’s ability to pay off short obligations so that it will affect the implementation of conservatism in the company’s financial statements (Watts & Zimmerman, Citation1986). This opinion is also reinforced by Iona et al. (Citation2004) and Dang and Tran (Citation2020) showing that financial leverage has a positive effect on accounting conservatism. Therefore, companies with high leverage ratios will make creditors demand to apply conservatism to ensure security and confidence in the return of funds that have been given.

H1: Leverage will increase the application of the principle of conservatism

2.4. Financial distress on the application of the conservatism principle

Financial distress is a condition where a company experiences financial difficulties, which is marked by a decrease in net income for several periods. Positive accounting theory states that managers have a tendency to reduce the level of conservatism when dealing with conditions of high levels of financial difficulty. This can happen because of the possibility of replacing managers with shareholders who are considered unable to manage the company properly.

When faced with a high level of financial distress, managers usually have a tendency to reduce the level of accounting conservatism in financial statements because if the condition of the company’s financial statements looks problematic, the manager is considered to have violated the contract and faces the threat of replacing the manager which will have an impact on the decline in the manager’s market value in the market. Labor. In different conditions, when the company is not facing financial distress, the manager does not face the pressure of breach of contract and will tend to apply more conservative accounting principles to avoid possible conflicts with creditors and shareholders.

The level of financial distress owned by the company has a negative effect on the application of the principle of conservatism caused by a decrease in financial condition due to poor manager performance, which can trigger shareholders to change managers, so managers tend to reduce the level of conservatism. This is in line with when managers are faced with financial difficulties and the threat of changing manager positions, and there is a tendency for managers to reduce the level of conservatism with the aim of making financial statements look good in the eyes of shareholders and creditors.

The opinion that is in line but in different directions is expressed, which states that financial distress conditions positively affect the application of the principle of conservatism. Uncertainty conditions that can occur in companies require accountants to be more careful in recognizing an economic event because the manager’s prudence is considered to be able to provide benefits to all users of financial statements, so the higher the level of financial distress the company has. It will increase the application of the principle of conservatism in its financial statements.

H2: Financial distress will increase the application of the principle of conservatism.

3. Method

This study takes data from European league football clubs registered with UEFA based on the Financial Fair Play Regulations in 2010. Data collection was carried out by purposive sampling on the London stock exchange because the Premier League is the world’s most popular and best league. The sample criteria were made based on the following considerations: (1) Football clubs that have participated in the English Premier League, and (2) operating and publishing financial and annual reports for the period 2011–2013 on London Stock Exchange. Furthermore, to test the impact of leverage and financial distress on conservatism, the following panel data regression model is used:

Where:

CONACC: Degree of accounting conservatism

LEV: Leverage

G-SCORE: Financial Distress

β1: Slope of Leverage Variable

β2: Slope of Financial Distress Variable

λ0: Intercept in 2011

λ1: Intercept in 2012

λ2: Intercept in 2013

ei: Error

3.1. Accounting conservatism

Accounting conservatism is defined as the difference in the level of verification carried out on the recognition of profit and loss in financial statements so that, in practice, managers will need a higher level of verification to recognize good news as gains compared to bad news as losses (Watts, Citation2003). Conservatism as an independent variable is calculated by the accrual model of Givoly and Hayn (Citation2000). The reason for using the accrual model is because the focus of this study is on discussing conservatism in relation to profit and loss, not on market reactions, so the accrual model is more appropriate to use. Total accruals measure accounting conservatism less cash flows from operating activities. This variable is represented by the CONACC symbol, and the formula is as follows:

Where:

CONACC: Degree of accounting conservatism

NI: Net income before extraordinary items, plus depreciation and amortization

CFO: Cash flow operation

The more negative the CONACC value obtained by a company, the more conservative the company is, and vice versa.

3.2. Leverage

Leverage refers to the use of funds originating from debt to finance the company’s operational activities, which causes the emergence of a fixed burden for the company. Companies that do not have leverage use their own capital in full without using debt to finance their operational activities. The leverage variable is measured using the debt-to-asset ratio, which is considered to provide information about the amount of debt used to finance the assets used by the company in carrying out its operational activities. This variable is expressed in the symbol LEV, and the formula is as follows:

Where,

LEV: Leverage

Debt: Total Debt

TA: Total Assets

3.3. Financial distress

The definition of financial distress, in general, is a condition of financial difficulty experienced by a company so that it cannot fulfil its obligations. The condition of a company’s financial difficulties can be measured through financial statements by doing ratio analysis to financial statements. Grover’s G-Score model is a model created by designing and reassessing the Altman Z-Score model. Jeffrey S. Grover used a sample according to the Altman Z-Score model in 1968 by adding 13 new financial ratios. Grover and Lavin (Citation2001) produces the following equation as follows:

Where:

X1: Working capital/Total asset

X3: Earning before interest and taxes/Total asset

ROA: Net income/Total asset

Grover’s model categorizes companies as bankrupt with a score of less than or equal to −0.02 (G − 0.02), while the value of companies categorized as not bankrupt is more or equal to 0.01 (G 0.01). Companies with scores between the upper and lower limits are in the grey area. In this study, the measurement of financial distress is carried out by giving an assessment of one for companies experiencing financial distress and zero for companies not experiencing financial distress.

4. Results

Model testing of multiple linear regression model using a panel data and a confidential level 95%. Furthermore, the multiple linear regression model used in this study has undergone a classical assumption test process, including a normality test, autocorrelation test, multicollinearity test, and heteroscedasticity test. Therefore, the next step is to test the feasibility of the regression panel data that is shown in Table .

Table 1. Summary of panel regression testing results

Testing the model by assuming that the intercept and slope coefficient are constant for three years, the results show that the F test is 6.799 or a p-value of 0.001, which means it is significant with an R square of 0.497. However, the test result for the constant is −1.325 (p-value = 0.196), which means it is not significant, so the intersection point of the regression line on the vertical axis can be interpreted through the original point. However, what is more important is the results of the t-test variable leverage and the G-Score showing the numbers 2.310 (p-value = 0.043) and 3.285 (p-value = 0.003) which means that H1 and H2 are accepted.

To ensure that the results of the panel regression test are robust, the test is carried out using the assumption that the slope is constant but the intercept varies every year. The result of the F-test is 13.318 or a p-value of 0.000 which means it is significant with an increase in R square to 0.521. Furthermore, the results of the t-test for the leverage variable and the G-Score show the numbers 2.332 (p-value = 0.0027) and 3.614 (p-value = 0.001) which means that H1 and H2 are accepted. However, the results of constant slope and intercept testing varied were not proven. This is shown by the constant t-test of −0.279 (p-value = 0.782) and the 2012 dummy of −0.270 (p-value = 0.789) and 2013 of −1.072 (p-value = 0.294) which are also not significant.

4.1. The effect of leverage on the application of the principles of accounting conservatism

The results showed that leverage (LEV) had a positive effect on the coefficient of accounting conservatism. This is indicated by the value of the calculated significance level (0.027) atau (0,043) pada confidence level (0.05). The higher the leverage value of the company, it will encourage managers to increase the value of accounting conservatism in the company. This is because when the leverage value increases, it will make creditors demand that managers apply conservatism by holding back profits in the interest of the security of creditor funds because if the manager remains opportunistic by distributing dividends to shareholders and taking commissions in conditions of high leverage will threaten the funds from creditors cannot be returned by the company, and the company’s condition will worsen.

4.2. The effect of financial distress on the application of accounting conservatism principles

The results showed that financial distress (Distress) had a positive effect on the coefficient of accounting conservatism. This is indicated by the value of the calculated significance level (0.001 or 0,003) pada confidence level (0.05). The higher the value of the company’s financial distress, the manager is required to be more careful in making decisions in the midst of uncertain conditions in the company. Managers’ prudence in recognizing events in uncertain financial distress conditions in the company is expected to be able to provide long-term benefits to the company, investors, and creditors.

5. Conclusion and recommendations

Based on the results of the multiple linear regression analysis that has been presented in this study, it can be concluded that the variables of leverage and financial distress either partially or simultaneously have a positive influence on the application of accounting conservatism principles to English football clubs. This is in line with positive accounting theory, which requires a manager to be able to have the ability, understanding, and knowledge of accounting in the application of appropriate accounting policies in uncertain conditions and is required to be more careful in making decisions because when a manager remains Opportunistic conditions in uncertain conditions will result in losses that may be experienced by companies, investors, and creditors due to the manager’s inability to make decisions.

The author’s suggestion to the next researcher is expected to be able to increase the number of variables and the sampling period so that the research results can be maximized and in accordance with the latest conditions and regulations, as well as to conduct research on clubs in other state leagues. Football leagues will have different regulations, both team formation and competition regulations, as well as regulations in their financial reporting system so that it can produce different results in each league in various parts of the world with a record that existing football clubs have been listed on the stock exchange.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Buraimo, B., Simmons, R., & Szymanski, S. (2010). English football. Football Economics and Policy, 7(1), 162–10. https://doi.org/10.1057/9780230274266_08

- Cave, A., & Miller, A. (2016). Premier League owners: Foreign investment in English football. Retrieved September 26, 2019, from https://www.telegraph.co.uk/investing/business-of-sport/premier-league-investors/

- Dang, N. H., & Tran, M. D.(2020). Impact of financial leverage on accounting conservatism application: The case of Vietnam. Custos e @gronegócio on line - v. 16, n. 3, Jul/Sep. - 2020. 1808–2882. https://www.custoseagronegocioonline.com.br

- Dimitropoulos, P., Leventis, S., & Dedoulis, E. (2016). Managing the European football industry : UEFA’s regulatory intervention and the impact on accounting quality Managing the European football industry : UEFA’s regulatory intervention and the impact on accounting quality (pp. 4742(June). https://doi.org/10.1080/16184742.2016.1164213

- Franck, E. (2018). European Club Football after “Five Treatments” with Financial Fair Play—Time for an Assessment. International Journal of Financial Studies, 6(4), 97. https://doi.org/10.3390/ijfs6040097

- Givoly, D., & Hayn, C. (2000). The changing time-series properties of earnings, cash flows and accruals: Has financial reporting become more conservative? Journal of Accounting and Economics, 29(3), 287–320. https://doi.org/10.1016/S0165-4101(00)00024-0

- Grover, J., & Lavin, A. (2001). Financial Ratios, Discriminant Analysis and The Prediction of Corporate Bankruptcy: A Service Industry Extension of Altman’s Z-Score Model of Bankruptcy Prediction. Working Paper. Southern Finance Association Annual Meeting.

- Iona, A., Leonida, L., & Ozkan, A. 2004. Determinants of financial conservatism: Evidence from low-leverage and cash-rich UK firms. Department of Economics and Related Studies University of York Heslington York, YO10 5DD. Discussion Papers in Economics. January 9, pp. 1–49.

- Jensen, M. C., & Meckling, W. H. (1976). Theory of The Firm Managerial Behaviour, Agency Cost, and Ownership Structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Morrow, S., & Senaux, B. (2013). Football club financial reporting: Time for a new model? Sport, Business and Management: An International Journal, 3(4), 297–311. https://doi.org/10.1108/SBM-06-2013-0014

- Raharjo, E. (2007). Agency Theory Vs. Stewardship Theory in the Accounting Perspective. Fokus Ekonomi, 2(1), 37–46. https://doi.org/10.1016/S0076-6879(07)33002-4

- Reed, A. (2019). European soccer posts record revenues as EPL dominates: Deloitte. Retrieved September 23, 2019. https://www.cnbc.com/2019/05/30/european-soccer-posts-record-revenues-as-epl-dominates-deloitte.html

- Salama, F. M., & Putnam, K. (2015). Accounting Conservatism, Capital Structure, and Global Diversification Pacific Accounting Review. 27(1), 2015., pp. 119-138,© Emerald Group Publishing Limited, 0114–0582, DOI 10.1108/PAR-07-2013-0067.

- Sendy, S., Soepriyanto, G., & Sari, N. (2016). Analysis of the implementation of UEFA financial fair play: a case study on arsenal and machester United football club. Bus Business Review, 5(1), 123. https://doi.org/10.21512/bbr.v5i1.1202

- UEFA. (2014). Financial fair play: all you need to know. UEFA.Com. https://www.uefa.com/community/news/newsid=2064391.html

- Watts, R. L. (2003). Conservatism in Accounting Part I : Explanations and implications. Accounting Horizons: September, 17(3), 207–221. 2003. https://doi.org/10.2308/acch.2003.17.3.207.

- Watts, R. L., & Zimmerman, J. L. (1986). Positive Accounting Theory by Ross L. https://papers.ssrn.com/sol3/papers.cfm?Abstract_id=928677

- Zoccali, C. (2011). The role of financial indicators in the life of Italian football clubs. Rivista Di Diritto Ed Economia Dello Sport, VII, 167–185.