?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This is the first study to explore the impact of Indonesia’s adoption of International Financial Reporting Standards (IFRS) on information flow and stock price informativeness throughout the pre-IFRS (2007–2011), transition (2012–2014), and post-IFRS (2015–2019) adoption periods, as determined by stock price synchronicity (SYNCH). This study examines if IFRS has reduced Indonesia’s SYNCH. The empirical data show that the mean value of SYNCH was negative for each of the 13 years investigated in this study, with the post-IFRS period having the lowest value. After that, SYNCH values steadily recovered. This study used panel data regression to objectively examine the relationship between a variety of independent variables and SYNCH. This research found that requiring the adoption of IFRS will first boost the flow of private information (firm-specific information) into stock price formation and eventually reduce the surprise impact of future disclosed information. This study also contributes new knowledge by offering proof of the effects of IFRS adoption and helping standard-setters in weighing the pros and disadvantages of their choices to keep implementing IFRS in Indonesia.

1. Introduction

Significant changes occurred on the Indonesian capital market between 2016 and 2020. On the Indonesia Stock Exchange (IDX), there will be 713, or 33%, more listed businesses by the end of 2020 than there were in 2016. Despite a little decline in value due to the COVID-19 epidemic in 2020 to Rp. 6.970 trillion, the market capitalization has grown significantly since 2016, reaching Rp. 7.265 trillion at the end of 2019. (IDX, Annual Statistics 2016–2020). Additionally, between 2016 and 2020, the IDX’s Composite Stock Price Index (JCI Index) rose by 13% to 20% (IDX, Citation2020).

Several empirical studies on stock market return volatility have been undertaken to uncover factors that could cause major market index movements. Previous research has found that the major causes of the JCI’s exceptional changes include macroeconomic variables such as inflation, GDP, currency rate, economic growth, international oil prices and interest rates (Ningsih & Waspada, Citation2018; Pradhypta et al., Citation2018). The second query is: Why does it seem that firm-specific information used to determine a firm’s fundamental value is ignored by the stock market?

The literature on stock price synchronicity (SYNCH) explains the stock market’s behaviour in relation to the firm-specific information disclosed in financial reports. Roll (1998) is the first to propose the idea that investors may use firm-specific and market-wide information in their investment decisions. Additionally, if a company’s stock price returns are more properly explained by market information, stock price returns will show higher synchronicity with market returns.

Contrarily, less synchronicity will be evident with market-related information if fluctuations in the company’s stock prices are more adequately explained by firm-specific information (Morck et al., Citation2000). Accordingly, the literature relating to SYNCH uses the terms higher firm-specific information or lower SYNCH interchangeably.

On the other hand, if firm-specific information is more effective at explaining changes in the company’s stock prices, there will be less synchronicity evident with market-related information (Morck et al., Citation2000). As a result, the terms higher firm-specific information or lower SYNCH are used interchangeably in the literature on SYNCH.

Financial statements and additional information, known as disclosures, are included in published financial reports and explain relevant activities that significantly impact the firm’s financial performance. As a result of an accounting process, financial reports must include high-quality firm-specific data to provide meaningful information to potential investors. According to the literature associated with SYNCH, greater firm-specific information or adequate firm-specific information disclosures become critical in determining the quality of the information in financial reports. Therefore, it is reasonable to claim that the accuracy of the information in financial reports will depend on the quality of the accounting standards used (Barth et al., Citation2008).

International Financial Reporting Standards (IFRS)-generated financial statements are of higher quality than those prepared in accordance with national accounting standards or GAAP, according to several studies that examined the effects of implementing IFRS (Patro & Gupta, Citation2016).Footnote1 It will be interesting to know if implementing the IFRS Standards in Indonesia improves the stock prices’ ability to provide useful information, as measured by SYNCH during the pre-IFRS, transitional, and post-IFRS adoption periods. The objective of this study is to ascertain whether the SYNCH of Indonesia after the adoption of IFRS is significantly lower than it was before the standards’ implementation. Thus, this study examines whether there is a significant decrease in SYNCH of post-IFRS adoption in Indonesia compared with that in the pre-IFRS adoption period. This study offers new evidence about the effects of IFRS adoption on increasing the quality of financial report information, which resulted in a rise in stock price informativeness, as assessed by SYNCH for Indonesian firms across a wide timeframe from 2007 to 2019.

The next section includes a review of the literature and the development of hypotheses. In the following part, the steps for collecting data and using a regression model to analyse it are explained. The following section discusses the empirical results. The important findings, conclusions, limitations, and suggestions for further research are presented in the final section.

2. Literature review

2.1. Stock price synchronicity (SYNCH)

The efficient market hypothesis (EMH) states that no one can generate abnormal returns using readily available information since stock prices quickly capture all information on which investment decisions to make. EMH also makes the supposition that investors have easy access to reliable information so they can evaluate the firm’s capacity to generate cash flow and the actual status of the economy, and that they will only react to unexpected news when it comes to investing. As the information environment surrounding a firm improves and more data about the firm’s fundamentals becomes publicly available, investors can more accurately predict the occurrence of future events that should be reflected in the firm’s stock prices.

In a similar vein, the signalling theory proposes that management of listed entities can base specific decisions on their expectations regarding the information conditions of their companies. This results in endogeneity between the informativeness of stock prices and specific information announcements.

Roll (Citation1988) proposed the idea of SYNCH in his study on the capitalisation of firm-specific information into changes in stock prices. His research is based on the conventional capital asset pricing model, which contends that a low level of R-square shows that market returns have a limited capacity to explain fluctuations in an individual firm’s stock returns (R2). According to Roll (Citation1988), the co-movements of stock prices are determined by the amount of firm- and market-level information that is absorbed into stock prices. Investors who believe firm-specific information is accurate and valuable will use it in their trading, causing stock prices to change. When the accuracy of firm-specific information is questioned, investors will seek for alternate sources of information, and market-wide information will have a higher increasing impact on stock price movements. R2 has been extensively used in a huge body of literature since the publication of Roll’s work, either as a direct measure for SYNCH or an indirect measure for firm-specific information capitalized into the stock price.

Previous research has been done to identify the factors that influence SYNCH. Morck et al. (Citation2000) found that stock returns in emerging markets are more synchronized than in developed markets, implying a higher SYNCH level. Similarly, Daouk et al. (Citation2006), Patro and Gupta (Citation2016) and A. H. Nguyen et al. (Citation2020) argued that a rise in the index of capital market governance was negatively related to SYNCH.

Piotroski and Roulstone (Citation2004), Chan and Hameed (Citation2004), and Gao et al. (Citation2020) provided evidence that analyst coverage has beneficial impact on SYNCH. According to Gul et al. (Citation2010), foreign ownership and auditor quality have a negative relationship with SYNCH. The impact of additional variables on SYNCH has also been studied, including corporate transparency, earnings informativeness, voluntary disclosures, ownership structures, earnings management, and adoption of IFRS (Boubaker et al., Citation2014; Durnev et al., Citation2003; Kim & Shi, Citation2012; Phan Trong et al., Citation2021; Song, Citation2015; Suk, Citation2008)

Previous recent studies on the SYNCH in Indonesia using samples of post-IFRS adoption data suggest various results. Butar Butar (Citation2019) examined the association between board governance and SYNCH. Using firms listed in IDX in 2013–2015, the regression analysis results shows that board independence and board size are adversely related to SYNCH. Pratiwi et al. (Citation2021) employed a selection of listed manufacturing firms in IDX in 2014–2018 to examine the quality of sustainability reports and ownership by institutional investors on SYNCH. According to the empirical findings, firms that produced sustainability reports of greater quality had lower SYNCH, and institutional investors had no moderating influence on this relationship.

According to Li et al. (Citation2004) and Ntow-Gyamfi et al. (Citation2015), transparency has an impact on how managers (or insiders) and investors (or outsiders) share risk. For instance, insiders experience less firm-specific risk in more transparent firms, whereas outsiders experience less market risk. As a result of more firm-specific disclosure, a company’s stock price will consequently represent more firm-specific information and less SYNCH. However, Dasgupta et al. (Citation2010) shown in a time series scenario that SYNCH may gradually rise when transparency improves. According to Li et al., Citation2004) and Cahan et al. (Citation2021), when the information environment surrounding a firm improves as more firm-specific information is made available, SYNCH initially declines. The SYNCH then rises when market players may enhance their forecasts of the occurrence of upcoming firm-specific events by giving firm-specific information.

2.2. IFRS adoption

Published financial reports consist of financial statements and additional information, known as disclosures, that explain significant activities that substantially impact the firm’s financial performance. Financial reports, which carry out its firm-specific information reflecting the financial condition of a firm, are the final output of an accounting process. Financial reports must include accurate firm-specific data in order to give valuable information to potential investors. The amount of firm-specific information revealed affects how well financial reports are produced. As a result, the quality of the accounting standards used might affect how accurate the information in financial reports is.

Numerous studies that have looked into the effects of implementing IFRS have found that IFRS-compliant financial reporting is of higher quality than financial statements based on GAAP (Patro & Gupta, Citation2016). Furthermore, the empirical research on how IFRS implementation affects the capital markets generally shows benefits, which leads to more comparable and transparent financial reports. The initial group of research concentrated on aspects of the capital markets that are closely related to firm valuation, such as cost of equity capital (Daske et al., Citation2008b), stock market liquidity (Daske et al., Citation2008b), the efficiency of firm-level capital investment (Schleicher et al., Citation2010), and cross-border equity investments (DeFond et al., Citation2011). The second group of studies examined the informational value of earnings announcements to determine how the capital markets view accounting quality (Landsman et al. (Citation2012), Chen et al. (Citation2017)), SYNCH (Beuselinck et al. (Citation2009), J. Gassen et al. (Citation2020)) and the level of information quality available to analysts (Byard et al., Citation2011).

The International Accounting Standards Board (IASB) has received widespread support and acceptance from national accounting standard-setters and recognition from international organisations (e.g., IFAC, IOSCO, World Bank and IMF) to converge with a set of IFRS Standards. Currently, 166 nations have adopted IFRS Standards, implying that the objective of a global accounting language is progressively becoming a reality (IFRS, Citation2020).

The Institute of Indonesia Chartered Accountants (IAI) announced the adoption of IFRS in Indonesia in December 2008, and it would go into effect in 2012. Many Indonesian Financial Accounting Standards (“Standar Akuntansi Keuangan” or “SAK”) that were converged with IFRS standards have been released since 2009 by the Indonesian Financial Accounting Standards Board (“Dewan Standar Akuntansi Keuangan” or [DSAK]), a standard-setting board financed by IAI.

Most of the accounting standards which are in line with the IFRS standards that the IASB issued in 2009 and that will go into effect on January 1st, 2012 were released by DSAK. In Indonesia, the first phase of the IFRS adoption period, which is distinguished by a three-year gap between local standards and IFRS, ran from 2009 to 2012. This gap was reduced to one year starting in 2015 when the DSAK adopted the 2014 edition of IFRS Standards. As a result, the second phase of IFRS implementation began in 2015, and the years in between are referred to as the transition period.

Since 2010, empirical researches on Indonesia’s IFRS adoption have been carried out. Tri Wahyuni et al. (Citation2020) completed the largest study on Indonesia’s IFRS adoption. They assessed the effects of IFRS implementation in Indonesia from 2010 to 2016 using systematic literature research. The study found that value relevance and earnings management are two most popular effects of IFRS. According to the study’s findings, the adoption of IFRS in Indonesia will raise the level of financial reporting quality, as evidenced by the firm’s financial results, increased value relevance, high-quality accounting information, high-quality earnings, and declining earnings management practices.

IFRS adoption has been the subject of numerous studies that have examined the extent to which firm-specific information is capitalised into share prices, as determined by SYNCH. In order to reducing the gap between research and practices, several studies have been conducted, however, most of those studies used European countries’ settings, adopting IFRS earlier than emerging countries. Kim and Shi (Citation2012) discovered that SYNCH is much lower for IFRS adopters than non-adopters using firm-level data from 34 emerging and developed markets. To the best of our knowledge, only limited study examined the capitalisation of firm-specific data into listed firms’ stock prices in Indonesia in the post-IFRS period, compared to the pre-IFRS era, exhibiting a decrease in SYNCH. By illuminating the connection between IFRS adoption and SYNCH, especially in the context of emerging country, this study makes an important contribution to the accounting literature.

3. Hypothesis development

3.1. SYNCH and IFRS adoption

The research’s hypotheses are built on signalling theory. Information asymmetry is the root cause explaining signalling theory. Information asymmetry exists between managers and shareholders in a firm or public investors (in a listed firm); managers run the firm daily to get to know the firm better, whereas shareholders or investors are not involved in firm operations (Taj, Citation2016). Asymmetric information always occurs whenever the managers do not convey all relevant information influencing investors’ judgment in their investment decision-making. Therefore, the signal from managers to investors become important because the signal is expected to provide information about the firm’s financial potential and is influenced by accounting standards implemented in a country. Previous literature shows that the accounting standard, such as IFRS, which promotes the adoption of accounting conformity would limit managers’ ability to inform investors (Scott, Citation2009). Previous literature has also indicated that by implementing IFRS, the financial statements are now more comparable, giving investors a signal that reflects the value and importance of accounting figures. (e.g., Dimitropoulos et al., 2013; Iatridis, 2010).

Additionally, earlier studies discovered that a decrease in SYNCH is linked to additional firm-specific information (Beuselinck et al., Citation2009; Kim & Shi, Citation2012; Patro & Gupta, Citation2016; Shin, Citation2019). Shin and Choi (Citation2013) found that SYNCH decreased after IFRS implementation using Korean data, with the decrease greater for firms with low synchronicity before the adoption. The adoption of IFRS is said to be more advantageous in markets with more established capital markets as opposed to developing markets, according to prior research on the effects of IFRS. However, Patro and Gupta (Citation2016) discovered that SYNCH decreased in four Asian markets (the Philippines, China, Israel, and Hong Kong) where IFRS became mandated in 2009.

Increased disclosure and improved comparability have been linked to the mandated implementation of IFRS in Europe, according to certain arguments. Beuselinck et al. (Citation2009) investigated the implications of IFRS adoption becoming required in the EU in 2005 on stock price informativeness and flow of information (EC Regulation 1606/2002), also the years following the adoption of IFRS (2006–2007), when compared to the years before IFRS adoption (2003–2004). Using a carefully selected sample of firms from fourteen EU countries, they discovered that SYNCH declined in the year of required IFRS adoption but then increased in the post-implementation era to levels greater than the pre-adoption period. This finding confirms the theoretical hypothesis that initially the flow of private information into process of stock price movements will be improved by mandatory adoption of IFRS, reduce the impact of future information surprises, and eventually lead to an increase in SYNCH.

Dasgupta et al. (Citation2010) found in a time-series scenario that SYNCH can gradually increase when transparency improves, which is in line with Jin and Myers (Citation2004)’s study. The disclosures of firm-specific information will, however, increase SYNCH to the degree that participants in the market can improve their forecasts of forthcoming firm-specific events. Accordingly, we hypothesised the following:

H1: The adoption of IFRS in Indonesia led to a significant decrease in SYNCH.

H2: Following the adoption of IFRS, SYNCH initially declines then rises in later post-IFRS periods.

4. Data and methodology

4.1. Sample

We used firms listed as of 31st of December 2007 and still listed until 2019 in the IDX. The selection period is from 2007 to 2019 and is meant to encompass all phases of Indonesia’s IFRS adoption. Pre-IFRS adoption (2007–2011), transitional (2012–2014), and post-IFRS adoption (2014–2017) are the three time periods covered by this 13-year study (2015 to 2019).

The sample, which consisted of 240 selected firms, did not include firms with insufficient data as well as firms listed in the banking and financial services industries. Over a 13-year span, balanced panel data sets with 3,120 firm-year observations were gathered. The sample selection process is displayed in Table . Daily stock prices for the firm and the JCI daily market index level were included in the sample, was collected from the Bloomberg database. Accounting information was manually collected from annual reports and the IDX website, www.idx.co.id.

Table 1. Sample selection procedure

4.2. SYNCH computation

SYNCH, as a proxy for firm-specific information that is reflected in stock prices, was first introduced by Roll (Citation1988), and it was further refined by Morck et al. (Citation2000). The R2 value of the regression of individual stock returns on market indexes and industry indexes was used in the literature to calculate SYNCH. However, Chan and Hameed (Citation2004) asserted that it is typically troublesome to include industrial returns in the calculation because distinguishing between industry and market effects in a market with the domination of several industries is challenging as in the context of emerging markets. The JCI, which was divided into nine industry or sector indices, featured about 700 firms. It can be problematic when some major businesses, like manufacturing, had 63% weighting, whereas other industries had only fewer than five firms. As a result, industry returns were not taken into account when calculating SYNCH in this study. In order to define SYNCH, this study refers to Morck et al. (Citation2000) and Gul et al. (Citation2010).

where RET stands for the daily return on firm stock traded on IDX for firm i and day t, where MRKTRET stands for the value-weighted market return (JCI index) and ɛ stands for unknown random factors.

SYNCH was defined as the percentage of common return variation to total return variation, which equals the market model’s R2. SYNCH is frequently calculated through the regression of individual stock returns on market returns using R2 value. The more closely a company’s stock prices synchronise with market returns, the higher its R2. The useful interpretation of this proxy is supported by a growing body of empirical data (Boubaker et al., Citation2014). Within the unit interval [0,1], the R2 result of regression is bounded. The SYNCH is then determined using the following R2 logistic transformation:

where SYNCHi,t is the empirical measure of firm i’s SYNCH on year t.

In this study, the publication date of financial reports—whichever is earlier than the submission date to the IDX of audited financial statements or the publication date in newspapers—is used. This study also used a window of a few days before and after the publication date in order to have ample time to gather market responses to the information published. If the market reaction is large before and after the financial statements are issued, the published financial statements can contain incremental information (Firth et al., Citation2007).

Previous empirical research has shown a different result of the reaction to stock prices in the IDX that occurs within a window period before and after the date of publication. In a window period of [−20, +20] days following the publication of the audit opinion, Leo (Citation2007) discovered that stock price changes to audit opinions took place. However, using a window period of [−7, + 7] days, Prasetyo and Rini (Citation2014) found no changes in market reaction before and after the disclosure of the audit opinion, indicating that the window duration may have been too short. Therefore, daily stock and market return data were employed in this analysis with a 15-day window period [−15,+15].

4.3. Model specification

The following regression model was estimated to examine the hypotheses:

where

4.4. Panel data regression

Using panel data regression, this study objectively investigated the relationship between a number of independent variables and the dependent variable SYNCH. The panel data included the same cross-section unit that was measured at different periods. The three methods—Ordinary Least Square (Pooled Least Square), Fixed Effect Model (FEM), and Random Effect Model (REM)—are used to estimate panel data regression models (Gujarati, Citation2004). Then, using the Chow, Hausman, and Lagrange multiplier tests, the best model was chosen.

5. Empirical results and discussion

5.1. Descriptive statistics

Table includes the values for the minimum, mean, median, maximum, standard deviation, and range of all dependent and independent variables, as well as the descriptive statistics for the sample from 2007 to 2019. The distribution of SYNCH measurements is slightly skewed since the mean value is a little bit higher than the median. The average (median) market-to-book ratio (MBV) for the sample firms is 5.16. (1.04). 95% of the observations show that financial leverage, which is calculated as total liabilities divided by total assets (LEV), is lower than 87%. Throughout the course of our study (2007–2019), the mean natural logarithm of foreign sales or export (LNFORSALE) and net income (LNNETINC) was 4.73 and 8.72 billion rupiah, respectively.

Table 2. Descriptive statistics

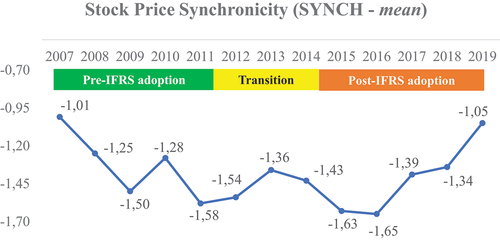

Figure displays the mean values of the dependent variable, SYNCH, for the pre-IFRS, transition, and post-IFRS adoption periods for the whole study period (2007 to 2019). In the pre-IFRS period for the Indonesian market (2007–2011), SYNCH first displays a declining pattern, with a 56% decrease from −1.01 in 2007 to −1.58 in 2011. The lowest SYNCH was reached in post-IFRS in 2016 (down another 4% from 1.58 in 2011 to 1.65 in 2016), then it increased in 2017–2019 (up 36% from −1.65 in 2016 to −1.05 in 2019).

Figure 1. The mean values of SYNCH.

Meanwhile, earlier SYNCH research in Indonesia employed different computations that produced a range of outcomes. In contrast to this study which used daily returns with a 15-day window period [−15,+15], Butar Butar (Citation2019) used weekly firm’s stock and market returns (a total of 52 weeks of returns data for each year). SYNCH’s mean and median, according to Butar Butar (Citation2019), were 0.61 and 0.62, respectively. Meanwhile, for their measurement, Pratiwi et al. (Citation2021) used weekly firm’s stock, market, and industry returns using the formula ri,t = δ0+ δ1rmkti,t+ δ2rmkti,t-1 + δ3rindi,t+ δ4rindi,t-1 + ɛ; where ri,t = company return, rmkti,t = market returns and rind1,t = industry return (manufacture). SYNCH had mean and median values of −0.0217 and 1.2749, respectively, according to Pratiwi et al. (Citation2021).

According to Gul et al. (Citation2010), considering the China market, the mean and median SYNCH statistics in earlier research carried out outside of Indonesia were 0.433 and 0.439, respectively. According to Piotroski and Roulstone (Citation2004), the mean and median stock price synchronicity measures for US firms are −1.742 and −1.754, respectively. Meanwhile, the mean and median SYNCH values in Indian enterprises are, according to Das et al. (Citation2013), −1.01 and −0.80, respectively. According to empirical data from the Vietnam stock market, SYNCH is, respectively, −1.426 and −0.9385 on the mean and median (Nguyen et al., Citation2020).

This study, which spans a longer period (from 2007 to 2019), shows intriguing results. SYNCH’s statistics show mean, median, minimum, and maximum of—1.3857, 1.0931,—8.0957 and 0.6070, respectively, consisting of positive and negative values of SYNCH. However, all mean statistics from 2007 to 2019 (all periods covered) show negative figures for SYNCH (see, Figure ), with the lowest values of—1.6280 and—1.6500 taking place after the adoption of IFRS.

Thus, the first hypothesis (H1) is supported by this research, which also adds to earlier studies that have found a decline in SYNCH following the adoption of IFRS (Beuselinck et al., Citation2009; Kim & Shi, Citation2012; Patro & Gupta, Citation2016; Shin, Citation2019), many earlier studies, notably in the Asian region, claim that the adoption of IFRS is more advantageous in countries with more developed capital markets than in emerging markets.

In addition, the results suggest that signalling theory applies to the application of high-quality standards. Most Indonesian investors captured signals offered by listed entities and capitalized extensive disclosures of firm-specific information as required by IFRS Standards, hence lowering SYNCH.

This study offered new evidence regarding the effects of IFRS adoption. This study was conducted in response to earlier research’s suggestions that the effects of IFRS adoption must be examined over a longer time period and be concentrated in one country (Brüggemann et al., Citation2012). This research followed that recommendation by computing SYNCH for the Indonesian listed firms with the most comprehensive period from 2007 to 2019. Meanwhile, previous research in Indonesia has shown different empirical results, as described in the previous paragraph, covering relatively shorter periods and only including post-IFRS adoption [e.g., Butar Butar (Citation2019) used the period of 2013–2015, and Pratiwi et al. (Citation2021) covered the period of 2014–2018].

The present study indicated similar evidence to the previous study by Beuselinck et al. (Citation2009) and Dasgupta et al. (Citation2010), examining stock price informativeness before and after IFRS becomes mandatory. According to this study, the SYNCH formed a V-shaped pattern which is declined in the year of mandatory IFRS adoption before rising to a level higher than the pre-IFRS adoption period in the years following IFRS adoption.

Beuselinck et al. (Citation2009) used a sample of 1,904 required IFRS adopters in 14 EU countries for the years 2003–2007 and found a V-shaped pattern in synchronicity surrounding IFRS adoption. This tendency is consistent with the adoption of IFRS disclosing additional firm-specific information (i.e., a reduction of SYNCH) and subsequently lowering the surprise of subsequent disclosures (i.e., an increase in SYNCH). Only Ireland and Denmark, out of 14 EU counties, displayed a concave form (inverted from V-shaped). The mean of SYNCH’s data for Austria, Finland, and Greece, for instance, has the following V-shape. For pre-IFRS, IFRS and post-IFRS, Austria showed −2.256, −2.345 and −1.429, respectively; Finland showed −1.969, −1.976 and −1.411, respectively; and Greece showed −0.906, −1.268 and −0.917, respectively.

In the context of Indonesia, as depicted in Figure , the SYNCH level gradually increased after reaching its lowest level; therefore, H2 is supported. This research shows that mandating the adoption of IFRS will first increase the flow of private information (or firm-specific information) into the process of forming stock prices and will eventually diminish the surprise impact of future published information.

5.2. Correlation

For each of the 14 independent variables, the correlation of coefficients is first calculated, as shown in Table . None of the independent variables are found to be substantially connected, as evidenced by any independent variables’ correlation coefficients with r2 values less than 0.75 (Gujarati, Citation2004).

Table 3. Correlation matrix

When compared to variables AVGTRADVOL, LNASSET, LEV, STD5YROA, DPS, LNSALES, LNNETINC, dBIG4 and LNMCAP, the SYNCH shows a positive correlation with those variables, whereas it has a negative correlation with dTRANS, dPOSTIFRS, LARGEST, MBV and LNFORSALE. The negative correlations imply that the SYNCH is decreased as the variables dTRANS, dPOSTIFRS, LARGEST, MBV, and LNFORSALE increase.

5.3. Fixed effect panel data regression

The link between SYNCH and each independent variable was examined using panel data. The STATA statistical analysis program was used to apply the three approaches for estimating panel data regression models: Pooled Least Square (PLS), FEM, and REM. The classical hypothesis was then evaluated to confirm that fundamental assumptions were met and the model was devoid of multicollinearity, heteroskedasticity, and autocorrelation. The robust FEM model was utilized to solve the heteroskedasticity issue after the Chow and Hausman tests revealed that the FEM was the model that best fit the results of the statistical test. Using panel-corrected standard errors in STATA, the autocorrelation issue was fixed. Multicollinearity occurs when the multiple linear regression analysis includes several independent variables with a strong correlation between the dependent variable one another and is tested using the variance inflating factor (VIF) with a VIF limit of 10. If the VIF value is greater than 10, then multicollinearity occurs (Gujarati, Citation2004). After removing LNASSET, LNSALES, LNMCAP and LARGEST, all variables which had VIF values greater than 10, as shown in Table , only ten independent variables with VIF values under 10 were used in the model.

Table 4. The variance inflating factor (VIF)

5.4. IFRS adoption

Table shows that, with the exception of the panel corrected standard error model, all regression models (PLS, FEM, REM, and Robust FEM) reveal negative and statistically significant coefficients (p < 0.01) for variables related to all phases of IFRS adoption (dTRANS and dPOSTIFRS variables). Those models generated negative coefficients for dTRANS variables (transition period of IFRS adoption) of −0.1902, −0.1292, −0.1132 and −0.1292 and dPOSTIFRS variables (post-IFRS adoption period) of −0.1665, −0.0803, −0.0750 and −0.0803. By dividing the coefficient of −3.1925 on the intercept provided in the first row by the coefficient of −0.1890 on the dTRANS variable, it can be determined that the change from pre-IFRS to the transition era decreased SYNCH by almost 5.9% in terms of economic magnitude.

Table 5. Model panel regression results

This study, which covered a long complete period of adoption of IFRS in Indonesia (2007 to 2019), also showed all negative figures of SYNCH (see, Figure ) with the lowest values of SYNCH (strongest effects) in post-IFRS adoption. The regression results therefore support our hypothesis that Indonesia’s adoption of IFRS led to a significant decline in SYNCH and lessen scepticism regarding the idea that countries with more developed capital markets benefit more from IFRS adoption than those with emerging markets (Beuselinck et al., Citation2009; Ho et al., Citation2013; JB Kim & Shi, Citation2012; Patro & Gupta, Citation2016; Shin, Citation2019).

5.5. Independent variables (firm-specific variables)

This study used a set of independent variables, which represent firm-specific variables, which in previous research studies have been shown to affect SYNCH. Panel data regression was performed by including eight firm-specific variables. Leverage and growth potential are likely to have an impact on SYNCH if these traits put a company in financial distress. Market-to-book (MBV) and the percentage of total debt to total assets (LEV) were included as firm-specific variables. Firms with higher growth potential and more financial leverage probably possess lower SYNCH due to their higher underlying risk. Therefore, we anticipate that SYNCH, MBV, and LEV will have a negative relationship (Dasgupta et al., Citation2010; Hutton et al., Citation2009). The percentage of foreign sales (LNFORSALES) is negatively related to SYNCH. Patro and Gupta (Citation2016), Kim and Shi (Citation2012), and Gul et al. (Citation2010), argue that foreign business counterparts demand transparency of firm-specific information, so that less SYNCH results from an increase in sales abroad.

Furthermore, the firm-specific variables related to earnings and their volatility, such as net income (LNNETINC), dividends (DPS) and volatility of return on assets (STD5YROA), are also included. Because greater earning uncertainty results in more variation within firms, the connection between earning volatility and SYNCH is anticipated to be negative (Gul et al., Citation2010; Kim & Shi, Citation2012; Skaife et al., Citation2005).

Table presents the outcomes for the regression models. In general, only two variables—firm foreign sales (LNFORSALE) and firm earnings volatility (STD5YROA) showed meaningful results.

Generally speaking, only two variables—firm foreign sales (LNFORSALE) and firm earnings volatility (STD5YROA)—produced findings that were significant.

6. Conclusion

It can be argued that changes in share prices are influenced by market data and firm-specific information. SYNCH is projected to be lower when firm-specific information influences stock price fluctuations more than market-wide information also the opposite.

Financial reports must offer high-quality firm-specific data to influence investment decisions. Accounting data improves with accounting rules. Many studies found that financial reporting under IFRS is better than GAAP in many jurisdictions. This study demonstrates that signalling theory also apply to full disclosure as mandated by IFRS Standards.

This study examined stock price informativeness and information flow before (2007–2011), during (2012–2014), and after (2015–2019) IFRS adoption in Indonesia. This study is the first to examine Indonesia’s full adoption of IFRS. Since 2016, IDX has grown in market capitalization (20%) and listed firms (33%), making the implementation of IFRS, a set of high-quality accounting standards, vital for investors. The post-IFRS period had the lowest SYNCH value. According to SYNCH, IFRS adoption has made Indonesian stock prices more informational and reduced Asian mistrust, contradicting prior arguments that IFRS benefits developed capital markets more than emerging economies. SYNCH was negative before IFRS and significantly lower later.

This analysis used 3,120 firm observations from 2007 to 2019. SYNCH values eventually rise after IFRS implementation. IFRS adoption is expected to increase firm-specific information flow entering the stock price creation process and lessen the surprise impact of subsequent firm information releases.

This study uses a set of independent variables representing firm-specific variables that affect SYNCH, as shown in previous research. STATA panel data regression examined fourteen independent variables, which were decreased to ten to fulfil the free multicollinearity effect. Only firm foreign sales (LNFORSALE) and firm earnings volatility (STD5YROA) were significant in the regression analysis. These support the idea that overseas business partners require firm-specific transparency to continue sales outside the home country, which reduces SYNCH. Earning volatility increases firm-specific information, which lowers SYNCH value.

The results of this study are important for all parties involved in financial reporting so that concerns pertaining to the results of IFRS adoption and SYNCH can be better understood. First off, this work adds to the body of SYNCH literature by presenting new evidence that back up the instructive explanations for a low SYNCH value. Second, this study focused on IFRS adoption, which provided an appropriate setting to analyse the impact of IFRS on SYNCH to reduce cross-country disparities. This study used a sample from one country to look at the impact of IFRS adoption. Thirdly, by offering new facts on the effects of IFRS adoption, this study will assist standard-setters in weighing the pros and disadvantages of their choice to keep IFRS in use in Indonesia. Fourthly, by better understanding the factors that influence stock prices, managers will be able to make better management decisions and investors will be able to allocate resources for investment decisions in an effective manner.

This study has several limitations. Therefore, it is important to interpret the data with caution. Several formulas can be used to calculate SYNCH, but this study only employs one to quantify SYNCH after a thorough analysis of the literature on stock price informativeness. As a result, future researchers may employ other measures of stock price informativeness.

Author contributions

Concept and data: Dwi Astuti Rosmianingrum

Analysis and methodology: Dwi Astuti Rosmianingrum, Nor Farizal Mohammed, Imbarine Bujang

Writing – original draft: Dwi Astuti Rosmianingrum

Writing – editing: Nor Farizal Mohammed

Writing – review: Nor Farizal Mohammed, Imbarine Bujang, Lianny Leo

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Acknowledgements

We acknowledge the Accounting Research Institute (ARI), Universiti Teknologi MARA, Ministry of Higher Education Malaysia for HICoE Research Funding, Universitas Indonesia, for all support and resources providers.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1. Because IFRS are not yet mandated in other Asian markets at that time, Patro and Gupta (Citation2016) only examined the impacts of mandatory IFRS adoption and stock price synchronicity in China, Hong Kong, Israel, and the Philippines.

References

- Barth, M. E., Landsman, W. R., & Lang, M. H. (2008). International accounting standards and accounting quality. Journal of Accounting Research, 46(3), 467–17. https://doi.org/10.1111/j.1475-679X.2008.00287.x

- Beuselinck, C., Joos, P., Khurana, I. K., & Van der Meulen, S. (2009). Mandatory IFRS reporting and stock price informativeness. (pp. 0924–7815). https://doi.org/10.2139/ssrn.1381242

- Boubaker, S., Mansali, H., & Rjiba, H. (2014). Large controlling shareholders and stock price synchronicity. Journal of Banking and Finance, 40(1), 80–96. https://doi.org/10.1016/j.jbankfin.2013.11.022

- Brüggemann, U., Hitz, J.-M., & Sellhorn, T. (2012). Intended and unintended consequences of mandatory IFRS adoption: A review of extant evidence and suggestions for future research. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.1684036

- Butar Butar, S. (2019). Board of commisioners composition, governance committee, and stock price synchronicity. Jurnal Akuntansi Dan Keuangan, 21(1), 1–11. https://doi.org/10.9744/jak.21.1.1-11

- Byard, D., Li, Y., & Yu, Y. (2011). The effect of mandatory IFRS adoption on financial analysts’ information environment. Journal of Accounting Research.

- Cahan, S., Lam, B. M., Li, L. Z., & Rahman, M. J. (2021). Information environment and stock price synchronicity: Evidence from auditor characteristics. International Journal of Auditing, 25(2), 332–350. https://doi.org/10.1111/ijau.12221

- Chan, K., & Hameed, A. (2004). Stock price synchronicity and analyst coverage in emerging markets*.

- Chan, K., & Hameed, A. (2006). Stock price synchronicity and analyst coverage in emerging markets. Journal of Financial Economics, 80(1), 115–147. https://doi.org/10.1016/j.jfineco.2005.03.010

- Chen, J. Z., Lobo, G. J., & Zhang, J. H. (2017). Accounting quality, liquidity risk, and post-earnings-announcement drift. Contemporary Accounting Research, 34(3), 1649–1680. https://doi.org/10.1111/1911-3846.12310

- Daouk, H., Lee, C. M. C., & Ng, D. T. (2006). Capital market governance: How do security capital market governance: How do. Journal of Corporate Finance, 12(3), 560–593. https://doi.org/10.1016/j.jcorpfin.2005.03.003

- Dasgupta, S., Gan, J., & Gao, N. (2010). Stock return synchronicity and the informativeness of stock prices: Theory and evidence. Journal of Financial and Quantitative Analysis, 45(5), 1189–1220. https://doi.org/10.1017/S0022109010000505

- Daske, H., Hail, L., Leuz, C., & Verdi, R. (2008b). Mandatory IFRS reporting around the world: Early evidence on the economic consequences. Journal of Accounting Research, 46(5), 1085–1142. https://doi.org/10.1111/j.1475-679X.2008.00306.x

- Das, R. C., Mishra, C. S., & Rajib, P. (2013). Firm specific information? A study in the Indian context. South Asian Journal of Management, 23(4), 124–149.

- DeFond, M. L., Hu, X., Hung, M., & Li, S. (2011). The impact of mandatory IFRS adoption on foreign mutual fund ownership: The role of comparability. SSRN Electronic Journal, April 2020.

- Durnev, A., Morck, R., Yeung, B., & Zarowin, P. (2003). Does greater firm-specific return variation mean more or less informed stock pricing. Journal of Accounting Research, 41(5), 797–836. https://doi.org/10.1046/j.1475-679X.2003.00124.x

- Firth, M., Fung, P. M. Y., & Rui, O. M. (2007). Ownership, two-tier board structure, and the informativeness of earnings – Evidence from China. Journal of Accounting and Public Policy, 26(4), 463–496. https://doi.org/10.1016/j.jaccpubpol.2007.05.004

- Gao, K., Lin, W., Yang, L., & Chan, K. C. (2020). The impact of analyst coverage and stock price synchronicity: Evidence from brokerage mergers and closures. Finance Research Letters, 33(January), 1–6. https://doi.org/10.1016/j.frl.2019.05.008

- Gassen, J., Skaife, H. A., & Veenman, D. (2020). Illiquidity and the Measurement of Stock Price Synchronicity. Contemporary Accounting Research, 37(1), 419–456. https://doi.org/10.1111/1911-3846.12519

- Gujarati, D. N. (2004). Basic Econometrics 4ed. Prentice Hall.

- Gul, F. A., Kim, J. B., & Qiu, A. A. (2010). Ownership concentration, foreign shareholding, audit quality, and stock price synchronicity: Evidence from China. Journal of Financial Economics, 95(3), 425–442. https://doi.org/10.1016/j.jfineco.2009.11.005

- Ho, S. S. M., Shun Wong, K., Uyar, A., Kilic, M., Bayyurt, N., Herroelen, W., & Leus, R. (2013). Financial crisis and real earnings management in family firms: A comparison between China and the United States. SSRN Electronic Journal, 5(1), 1–11. https://doi.org/10.1590/1808-057x201704450

- Hutton, A. P., Marcus, A. J., & Tehranian, H. (2009). Opaque financial reports, R2, and crash risk. Journal of Financial Economics, 94(1), 67–86. https://doi.org/10.1016/j.jfineco.2008.10.003

- IFRS. (2020 April). Who uses IFRS Standards? Use of IFRS Standards by Jurisdictions. Retrieved from the IFRS website, https://www.ifrs.org/use-around-the-world/use-of-ifrs-standards-by-jurisdiction

- Indonesia Stock Exchange. (2020). IDX Statistics 2020.

- Jin, L., & Myers, S. (2004). R-squared around the world-new theory and new tests.

- Kim, J. B., & Shi, H. (2012). IFRS reporting, firm-specific information flows, and institutional environments: International evidence. Review of Accounting Studies, 17(3), 474–517. https://doi.org/10.1007/s11142-012-9190-y

- Landsman, W. R., Maydew, E. L., & Thornock, J. R. (2012). The information content of annual earnings announcements and mandatory adoption of IFRS. Journal of Accounting and Economics.

- Leo, L. (2007). Incremental information content dalam opini audit unqualified dengan paragraf penjelasan. Jurnal Akuntansi Dan Keuangan Indonesia, 4(2), 155–168. https://doi.org/10.21002/jaki.2007.08

- Li, K., Morck, R., Yang, F., & Yeung, B. (2004). Firm-specific variation and openness in emerging markets. Review of Economics and Statistics, 86(3), 658–669. https://doi.org/10.1162/0034653041811789

- Morck, R., Yu, W., & Yeung, B. Y. (2000). The information content of stock markets. Why Do Emerging Markets Have Synchronous Stock Price Movements? Journal of Financial Economics, 58, 215–260. https://doi.org/10.2139/ssrn.194530

- Nguyen, A. H., Vu, T. M. T., & Doan, Q. T. T. (2020). Corporate governance and stock price synchronicity: Empirical evidence from Vietnam. International Journal of Financial Studies, 8(2), 1–13. https://doi.org/10.3390/ijfs8020022

- Ningsih, M. M., & Waspada, I. (2018). PENGARUH BI RATE DAN INFLASI TERHADAP INDEKS HARGA SAHAM GABUNGAN (studi pada indeks properti, real estate, dan building construction, di BEI periode 2013-2017). Jurnal MANAJERIAL, 17(2), 247. https://doi.org/10.17509/manajerial.v17i2.11664

- Ntow-Gyamfi, M., Bokpin, G. A., & Gemegah, A. (2015). Corporate governance and transparency: Evidence from stock return synchronicity. Journal of Financial Economic Policy, 7(2), 157–179. https://doi.org/10.1108/JFEP-10-2013-0055

- Patro, P. A., & Gupta, K. (2016). Impact of international financial reporting standards on stock price synchronicity for asian markets. Contemporary Management Research, 12(1), 1–29. https://doi.org/10.7903/cmr.14160

- Phan Trong, N., Vu Thi, T. V., & McMillan, D. (2021). Impacts of ownership structure on stock price synchronicity of listed companies on Vietnam stock market. Cogent Business and Management, 8(1), 1. https://doi.org/10.1080/23311975.2021.1963178

- Piotroski, J. D., & Roulstone, D. T. (2004). The influence of analysts, institutional investors, and insiders on the incorporation of market, industry, and firm-specific information into stock prices. The Accounting Review, 79(4), 1119–1151. https://doi.org/10.2308/accr.2004.79.4.1119

- Pradhypta, I. C., Iskandar, D., & Tarumingkeng, R. C. (2018). Analisis faktor faktor yang mempengaruhi indeks harga saham gabungan di bursa efek Indonesia. Jurnal Manajemen Bisnis, 13(1), 43–56.

- Prasetyo, A. W., & Rini. (2014). Perbandingan reaksi pasar sebelum dan sesudah pengumuman opini audit unqualified. Jurnal MIX, IV, (3), 410–418.

- Pratiwi, U. D., Saraswati, E., & Prastiwi, A. (2021). Stock price synchronicity, sustainability reports, and earnings quality. Research in Business & Social Science, 10(1), 139–148.

- Roll, R., 1988. ”R².” Journal of Finance, 43, 541–566.

- Schleicher, T., Tahoun, A., & Walker, M. (2010). IFRS adoption in Europe and investment-cash flow sensitivity: Outsider versus insider economies. International Journal of Accounting.

- Scott William, R (2009). Financial Accounting Theory. 5nd Prentice Hall Canada Inc.

- Shin, H. (2019). The effects of industry characteristics on stock price synchronicity around IFRS adoption. Investment Management and Financial Innovations, 16(1), 89–99. https://doi.org/10.21511/imfi.16(1).2019.07

- Shin, S., & Choi, K. (2013). The Effect of K-IFRS Adoption on Information Asymmetry and Stock Price Synchronicity (Working Paper). Sungkyunkwan University.

- Skaife, H. A., Gassen, J., & LaFond, R. (2005). Does stock price synchronicity represent firm-specific information? The international evidence. SSRN, october 2005. (Vol. 4551-05). MIT Sloan Research Paper.

- song, L. (2015). Accounting disclosure, stock price synchronicity and stock crash risk. International Journal of Accounting & Information Management, 23(4), 349–363. https://doi.org/10.1108/IJAIM-02-2015-0007

- Suk, K. S. (2008). Simultaneous relationship between ownership structures, CG, and firm value in Indonesia-Suk. The South East Asian Journal of Management, 2(1), 1–25.

- Taj, S. A. (2016). Application of signaling theory in management research: Addressing major gaps in theory. European Management Journal, 34(4), 338–348. https://doi.org/10.1016/j.emj.2016.02.001

- Tri Wahyuni, E., Puspitasari, G., & Puspitasari, E. (2020). Has IFRS improved accounting quality in Indonesia? A systematic literature review of 2010-2016. Journal of Accounting and Investment, 21(1), 1. https://doi.org/10.18196/jai.2101135