Abstract

This study aims to examine the effect of economic factors and psychological factors on dilemmas in tax reporting. This study considers psychological factors caused by the inconsistency of the traditional tax compliance model. The economic factors tested are fines and tax audits while the psychological factors tested are trust and social norms. This study applied an experimental method with a 2x2x2 factorial design to investigate tax compliance. The final participants comprise 196 students. The results provide empirical evidence that trust and social norms can be explanatory factors in tax reporting dilemmas. However, this study does not provide empirical evidence regarding the effect of economic factors on tax compliance. The research results imply that the tax authorities need to consider the psychological factors behind taxpayers achieving honesty in tax reporting. This research also has implications in terms of the importance of a comprehensive approach in investigating compliance behavior. Overall, this study contributes to the literature that emphasizes the importance of psychological factors to investigate tax compliance. This study suggests the importance of social norms and trusts to guide behavior in tax compliance dilemmas.

1. Introduction

Improving tax compliance is a fundamental goal in countries around the world (Alm et al., Citation2019). According to the traditional approach, tax evasion can be suppressed with inspection instruments and fines (Allingham & Sandmo, Citation1972). The existence of audit and fines is a necessity in a country’s tax system (Kirchler et al., Citation2008). Both are mechanisms built using a constructivist rationality approach, namely a top-down mechanism based on formally determined instruments that create incentives (Górecki & Letki, Citation2020; Smith, Citation2003). However, empirical research examining the effectiveness of audits and fines in mitigating tax evasion continues to yield inconclusive results (Alm, Citation2018; Górecki & Letki, Citation2020; Nurkholis et al., Citation2020) There are many empirical studies that deviate from the assumption of rationality in the traditional model of tax compliance and psychological factors or non-economic factors cannot be ignored in tax compliance research (Alm, Citation2018; Alm et al., Citation2020; Kirchler, Citation2007; Yaser et al., Citation2019). Psychological variables are able to provide alternative explanations when investigating decisions about tax compliance (Alm et al., Citation2019). Therefore, this study will investigate the role of both economic factors and psychological factors in tax compliance decisions, especially in dilemma situations. Psychological has been widely examined in tax compliance, however, to the best of the authors’ knowledge, empirical research has not extensively investigated the role of psychological factors in tax compliance as a social dilemma.

Tax compliance decisions indicate a social dilemma (Gangl et al., Citation2015), that taxpayers must choose between minimizing taxes so that individuals’ utility increases in the short term or choosing to pay taxes so that they contribute to the provision of public facilities for the long-term collective interest (Balliet & Van Lange, Citation2013). Fundamentally, there is a conflict of interest between the taxpayer and the tax authority. In addition, the taxpayer’s decision is also influenced by other taxpayers and also the taxpayer’s perception of the government, tax authorities, tax accountants, and other taxpayers (Alm et al., Citation2020).

Social norms can become informal institutions in society that can be understood to realize tax compliance (Di Gioacchino & Fichera, Citation2020; Górecki & Letki, Citation2020; Kirchler & Hoelzl, Citation2017; Shafer & Wang, Citation2017). The social norms grow spontaneously from society as a combination of deeply rooted principles of behavior, norms, traditions, and morality (Górecki & Letki, Citation2020; Smith, Citation2003). Empirical research shows that social norms can encourage tax compliance (Alm et al., Citation2019; Górecki & Letki, Citation2020; Shafer & Wang, Citation2017; Wenzel, Citation2004).

In addition, the behavior of taxpayers cannot be separated from the behavior of other taxpayers (Alm, Citation2018). In tax reporting, the behavior of others contributes to decision of taxpayer. Social norms represent the behavior accepted by most taxpayers. If compliance (or reporting tax honestly) become the accepted behavior then taxpayer will follow others to report tax honestly. Alm et al. (Citation2019) suggested that individuals are more likely to feel discomfort when they perceived their behaviors or attitudes deviate from the norms of most people. Furthermore, Górecki and Letki (Citation2020) stated that social norms become ecological rationality, describing what others behave and believe in tax reporting. The believe and perception of honesty in most taxpayers then become the rationale for taxpayer to follow the others. Therefore, the authors argue that social norms become guidelines on how individuals behave when facing dilemmas in tax reporting.

This study also investigates the relationship between taxpayers and tax authorities which is built on trust. In a social dilemma situation, trust is relevant for realizing cooperative attitudes (Balliet & Van Lange, Citation2013; Gangl et al., Citation2015). Trust shows the hope that other parties have good motives in social interactions that involve conflicts of personal interests with shared interests. This study argues that conflicts of interest when there is a social dilemma in paying taxes can be overcome if there is trust (Lange, Rockenbach, and Yamagishi Citation2017). In general, taxpayers will be willing to pay taxes only if there is fairness and trust; that is to say, if taxpayers believe that other taxpayers also pay taxes, that the taxes paid are not misused through corruption or used to pay incompetent government employees, and the tax burden is distributed fairly (Lange et al., Citation2017). Consistent with this, the literature on the slippery slope theory also states that synergy in the relationship between taxpayers and the government that is based on trust will manifest itself in a willingness on the part of taxpayers to pay taxes honestly (Kirchler et al., Citation2008).

This study contributes in several ways. First, tax compliance is a complex issue that cannot be answered only with deterrence approach. The importance of psychological variables in investigating tax compliance has been suggested in the literature (Alm, Citation2018; Alm et al., Citation2019). This study suggests that psychological variables strongly explain tax compliance. This research contributes to a growing body of literature that shows that an instrumental approach alone is insufficient to explain the complexities of tax compliance.

Second, this study investigates tax compliance as a social dilemma behavior. Alm et al. (Citation2020) state that in a dilemma situation, it is assumed that individuals still think rationally and maximize utility. In addition to testing the effectiveness of compliance instruments in social dilemma situations, this study also examines social norms as guidelines for compliance decisions. This is consistent with Deglaire et al. (Citation2021) and Alm et al. (Citation2019) who states that a person’s tax compliance behavior is also influenced by perceptions of the compliance behavior of other taxpayers. To the best of the authors’ knowledge, no studies have investigated the role of social norms in tax compliance dilemma situations. This research contributes by providing empirical evidence that the behavior of taxpayers in a dilemma condition can be influenced by social behavior that is approved by most people.

Third, Alm et al. (Citation2020) state that research on social dilemmas in taxation that examines interactions between taxpayers through certain groups has been carried out, but other types of interactions and also the behavior of other actors (namely the government) have not been sufficiently investigated. This study fills this gap by examining the type of climate in the relationship between taxpayers and tax authorities. The interaction between authorities and the taxpayers should be based on trust. Trust in this interaction is believed to be able to provide guidelines for taxpayers in determining their reaction to the dilemma behind tax reporting decisions.

2. Literature review and hypothesis development

2.1. Tax compliance as a social dilemma

One of the paradigms in tax compliance research is tax compliance as a social contribution dilemma (Alm et al., Citation2020). Dawes (Citation1980) defines social dilemma as a situation that involves conflict between individual and society or collective interest. Selfish behavior can only benefit oneself. However, when other people decide to behave in the same way, then everyone will be disadvantaged because public facilities will not be available. This tragedy can be overcome if the authorities are able to regulate and actively monitor individual contributions to public goods (Gangl et al., Citation2015). This has implications for the importance of the presence of authority in overcoming social dilemmas in taxation. Under tax system legitimacy, tax authority organize audit and penalties for evasion (Górecki & Letki, Citation2020).

In addition to the presence of authority, abundant empirical evidences have identified psychological or non-monetary factors as determinants of compliance (Argentiero et al., Citation2021; Dularif & Rustiarini, Citation2022). In short, individuals are motivated not only by self-interest but also by group notions (Alm et al., Citation2019). Social norms can act as guidelines for individual behavior in various situations (Jimenez & Iyer, Citation2016), including tax compliance dilemmas. Trust is also needed to overcome situation when there is conflict between individual and collective interest (Lange et al., Citation2017).

2.2. Tax compliance: the traditional approach

The traditional model of tax compliance states that individual compliance with tax regulations is determined by penalties, the probability of detection, level of income, and tax rate (Alm, Citation2018). This model states that individuals pay taxes because of fear of punishment, fear of paying penalties or fines. The tax authorities also assume that taxpayers do not report the actual amount of income unless a tax audit is carried out. Thus, tax compliance is obtained only by coercive mechanisms in the term of fines and audits (Alm & Malézieux, Citation2021).

This traditional model emphasizes that punishment makes individuals obedient because individuals consider economic benefits when doing negative things. Therefore, tax compliance can only be achieved by enforcement, so reported income is directly proportional to the level of tax penalties and the probability of receiving a penalty from the tax authorities. From an economic point of view, the taxpayer is assumed to be a rational decision-maker seeking to maximize personal utility (Allingham & Sandmo, Citation1972).

Fines and tax audits are two instruments that necessarily exist in a country’s tax system (Kirchler et al., Citation2008). The presence of these two instruments is consistent with constructivist rationality, a top-down mechanism in which formal institutions establish instruments to encourage tax compliance (Górecki & Letki, Citation2020; Smith, Citation2003) Individuals decide whether to comply or not comply with taxes based on considerations of benefits and costs (Allingham & Sandmo, Citation1972). The higher the tax penalties and tax audits, the more compliant the individual will be.

H1: The level of tax compliance is higher in conditions of high audit probability than in conditions of low audit probability.

H2: The level of tax compliance is higher in conditions of high penalties than in conditions of low penalties.

2.3. Social norms and tax compliance

Social norms are a psychological variable that has been widely studied in research on taxpayer behavior (Kirchler & Hoelzl, Citation2017; Shafer & Wang, Citation2017). Social norms are rules and standards understood by group members that serve as guidelines or boundaries for social behavior (Cialdini & Trost, Citation1998). As ecological rationality, social norms serve as individual guidelines to identify behavior that may, or may not, be accepted by the society where the individual is part of that society (Górecki & Letki, Citation2020; Smith, Citation2003). Social norms have been recognized as important motivations for individual to pay taxes. Decision to comply related to social reputation (Di Gioacchino & Fichera, Citation2022).

The perception about what most people do regarding tax reporting has become the rationale for individuals to behave. Individual who act contrary to the norm will suffer from negative psychological effect such as feeling discomfort, guilt or shame for not complying (Alm et al., Citation2019). Accepting social norms, motivated by avoiding negative psychological aspect or maintaining social reputation, tends to realize behavioral conformity (Di Gioacchino & Fichera, Citation2022).

The existence of free riders among taxpayers, and also the choice of spending on taxpayer needs, indicate a social dilemma in tax compliance. Taxpayers have to choose whether to act as free rider or to contribute for collective interest. As informal institutions in society, social norms provide approval for individual behavior in tax reporting (Górecki & Letki, Citation2020). The perception that most people comply will determine taxpayers’ behavior consistent with the social norms that they believed in. In the norms of compliance, individual will tend to behave for long-term-oriented shared interest by reporting tax honestly. Previous research had recognized the role of social norms in achieving tax compliance (Abraham et al., Citation2018; Alm et al., Citation2019; Di Gioacchino & Fichera, Citation2022; Górecki & Letki, Citation2020; Shafer & Wang, Citation2017; Wenzel, Citation2004).

H3: Social norms have a positive effect on tax compliance.

2.4. Trust in authorities and tax compliance

The literature shows that trust plays an important role in social dilemmas (Balliet & Van Lange, Citation2013; Gangl et al., Citation2015; Lange et al., Citation2017). In their review, trust has strong connection with tax evasion (Yong et al., Citation2019). Trust is needed to overcome conflict between individual and collective interest (Gangl et al., Citation2015; Lange et al., Citation2017). This study investigates the behavior of authorities in building trust-based relationship with taxpayers. The authorities’ action creates certain climate in this relationship. Taxpayers’ perception to authorities will determine their behavior in tax reporting.

Kirchler et al. (Citation2008) define trust in authorities as a public opinion at the level of individuals and community groups that sees the tax authorities working properly and actually carrying out their functions as one of the actors in the provision of public goods. Trust is a special relationship, namely the interaction between parties, each of which emphasizes positive aspects and intrinsic motivation to maintain good relations. In the context of taxation, the taxpayer wants to pay taxes because he believes that tax money will be used for the public good, and that the tax authorities, together with the government as recipients of funds, allocate the funds honestly to provide public facilities. Thus, individual trust in the tax authorities can reduce the intention to embezzle taxes.

Trust in authorities also indicates that the authorities treat other taxpayers in the same manner. Fair treatment leads to each taxpayer fulfils their tax obligation fairly. This implies that there is no free rider among taxpayers. Therefore, we argue that trust in authorities will determine behavior in tax paying dilemma. In high trust in authorities, taxpayer will tend to emphasize collective interest. In contrast, when the authorities are perceived as untrustful parties, then taxpayer tend to prioritize individual interest by reporting dishonestly. Previous empirical research supported the role of trust in authorities to increase tax compliance (Batrancea et al., Citation2019; Güzel et al., Citation2019; Yaser et al., Citation2019).

H4: The level of tax compliance is higher when trust in authorities is high than when trust in authorities is low.

3. Research method

Students had been widely used to surrogate taxpayers in experimental research (Alm & Kasper, Citation2020). The subjects of this study were students of the Bachelor of Accounting program at Diponegoro University, Indonesia. They were asked to participate voluntarily. To be included in the final analysis, the subjects must fulfil the following criteria. They have to had signed the consent form, answered manipulation questionnaires correctly, and fulfilled the whole questionnaires completely. Subjects fail to fulfil these requirements will be dropped.

The dependent variable of this study is tax compliance decisions. Tax compliance is defined as reporting all the number of incomes in accordance with tax law, therefore, the higher the reported income indicated the higher level of tax compliance. Each subject was given a scenario that provided information that he or she was acting as a permanent employee of a company in a hypothetical country called Varosia. Subjects received additional income from work as freelance consultants. This additional income was taxable income that should be reported honestly in tax return. The scenario also provided information that the subject needed a car to support his or her work and so would buy one. If the additional income was fully reported on the tax return, subject would pay more taxes and have significantly less money to buy the car. Subjects were then asked to make a decision regarding the amount of additional income to report. The scenario was adapted from Brizi et al. (Citation2015).

This study used an experimental approach with a 2 (audit: 0% and 25% probability) x 2 (tax fine: 2% and 200%) x 2 (trust: high trust and low trust) between subject factorial design. The trust scenario is adapted from Wahl, Kastlunger, and Kirchler (Citation2010). This study included social norms as one of the factors that influence tax compliance decisions. Social norms are non-random assignments and are measured using four questions developed by Wenzel (Citation2004). The demographic variables measured in this study were age and gender (1 = male, 0 = female).

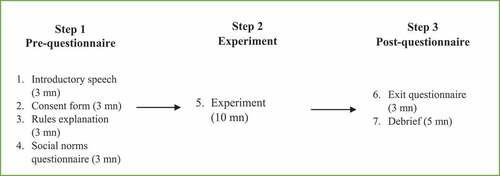

Figure depicted the experiment procedures. The subjects were asked to fill out an informed consent form before the experiment began. The questionnaires were arranged randomly and distributed to the subjects. They were asked not to open the questionnaire before being instructed to do so.

Figure 1. Experiment procedures.

The experimenter read the rules aloud before the subjects fill out the questionnaires. The subjects were not allowed to leave the classroom during the experiment. They were also not allowed to communicate and have discussion with other subjects during the experiment.

The subjects then filled out the questionnaires about social norms. After completing step 1, the subject received information about the manipulation scenario and the tax decision scenario. Subjects were asked to decide on the amount of additional income reported on a scale of 0 to 10,000 Kron (a hypothetical currency in fictious country, Varosia). As an exit questionnaire, the subject filled out questions about the manipulation check and demographics. The manipulation check consisted of three questions. First, subjects were asked to respond about their agreement with the statement “Varosia citizens do not trust the government” on a 5 Likert scale (1 = strongly disagree, 5 = strongly agree). Second, the subjects were asked to choose the probability that the subjects would be audited by the tax office (0% vs 25%). Third, the subjects were asked to choose information regarding tax fine that they would incur if the fact that the income report was incorrectly reported was not detected (2% vs 200%). The experimental session ended with a debriefing. Altogether, the experiment took about 30 minutes.

4. Results

There were 248 undergraduate students participated in this study. These students have taken courses in taxation and have had practical experience filling out tax return, therefore, they understand that the amount of additional income other than salary is taxable income and should be reported.

Of the 248 subjects, 52 (20.97%) subjects did not answer the questions regarding audit probabilities and fine levels correctly, so the final participants were 196 (79.03%). The final participants consisted of 152 (77.6%) female students and 44 (22.4%) male students. The average age of the subjects was 19 years; the youngest subject was 18 years old while the oldest subject was 23 years old (Table ).

Table 1. Descriptive statistics

The manipulation check questionnaire of trust in authorities was measured with a Likert scale of 5 (1 = strongly disagree, 5 = strongly agree). The average scores of subjects’ answers in low trust and high trust conditions were 4.44 and 1.62. The mean answers in the two groups were significantly different (F = 1603.675; p = 0.000). This shows that the subject has understood the given scenario.

Table shows that the subjects who received information about fines of 2% reported an average income of 7,783. Subjects who received information on fines of 200% reported an average income of 7,949. Subjects who received information about 0% audit probability reported an average income of 8,043. Subjects who received information about 25% audit probability reported an average income of 7,714. Subjects in high level of trust in authorities reported a greater amount of additional income (mean = 8,670) than subjects in low level of trust in authorities (mean = 7,081).

Table 2. Mean (standard deviation) of reported income in each cell

Table shows that the traditional instruments in tax compliance have no significant effect on tax compliance. The different level of audit probability does not have significant effect on the reported income (F = 0.000, p = 0.998). In similar, the reported income is not affected by different level of tax fines (F = 0.022, p = 0.882). Therefore, these two instruments do not provide guidelines for taxpayer behavior in dilemma situations. These results do not empirically support H1 and H2.

Table 3. Testing hypotheses

The results show that the level of tax compliance in the high trust condition is significantly higher than the level of tax compliance in the low trust condition (F = 12.899; p = 0.000). Trust can reduce individual economic motivation to evade taxes and create a synergistic climate in the relationship between authorities and taxpayers (Kirchler et al., Citation2008). In the high trust condition, taxpayers entrust their money to the government and then the authorities will use the taxpayer’s money to finance projects that are beneficial to the public. This finding supports H4 empirically.

Social norms that are believed in can be a guideline for taxpayer behavior when experiencing a dilemma in reporting the amount of income. These social norms also provide an understanding that tax compliance is the right behavior so that there are no free riders when it comes to fulfilling tax obligations. This study shows that beliefs about social norms play a significant role in tax compliance (F = 4.524, p = 0.035). Social norms have a positive and significant correlation with tax compliance (correlation coefficient = 8.187, p = 0.004). These results indicate that the higher the taxpayer’s belief in social norms, the higher the taxpayer’s compliance. This finding supports H3 empirically. Finally, this study also shows that the gender (F = 7.122, p = 0.008) and age of the respondents (F = 3.075, p = 0.081) also influence tax compliance decisions.

5. Discussion

Based on constructivist rationality, audits and fines are legally constructed instruments to achieve tax compliance (Górecki & Letki, Citation2020; Smith, Citation2003). However, this study suggested that, in tax reporting dilemma, subjects did not consider audit probability and tax fines as their behavioral guidance. The total average of reported additional income was 7,867. Compared to this number, in the absence of audit, subjects report relatively higher additional income (mean = 8,043), and in the low level of tax fines, subjects also report higher additional income (mean = 7,783).

This study indicates that instrumental enforcement was not able to promote compliance in dilemma situation. Even, in the low level of enforcement, subjects behave for long-term collective interest by reporting above average additional income. These findings confirm the literature showing that taxpayers are not fully rational and not economically motivated in fulfilling tax obligations (Alm, Citation2018). The results of this study also indicate that the traditional tax compliance model overpredicts non-compliance (Dularif & Rustiarini, Citation2022), since subjects report above average additional income in low level of enforcement. However, this study does not imply that instrumental enforcement through audit and fines are needless. Audit and fines can only partly investigate the complex behavior in tax compliance (Kirchler & Hoelzl, Citation2017). The comprehensive investigation of tax compliance should consider other factors than deterrence factors.

Tax compliance behavior, as a social dilemma, still assume individual as rationale actor and maximize utility (Alm et al., Citation2020). The individual will not behave cooperatively if he can hide in the anonymity of the masses (Alm et al., Citation2012). When tax payments occur in social dilemma situations, the optimal strategy for rational taxpayers is to commit tax evasion (Kirchler, Citation2007). However, this study provides empirical evidence that a dilemma situation does not encourage individuals to choose a tax evasion strategy. There are social norms and trust in authority that become the constraints of taxpayers’ behavior.

This study measures social norms that are believed in before the subject gets manipulated. The results show that social norms play a significant role in overcoming the tax compliance dilemma. The results of this study are consistent with Górecki and Letki (Citation2020) who show that tax compliance is not only achieved by building formal institutions that carry out enforcement functions; however, there is also the need to develop informal institutions that interact with formal institutions to achieve tax compliance. Informal institutions can be social norms that are born and rooted in society. The believed social norms prevent individuals from becoming free riders in the collective interest so that they behave cooperatively. Moreover, this study confirms Gürdal et al. (Citation2020), that in the absence of free rider, because of adherence to the norms of compliance, individual tend to contribute.

Wenzel (Citation2004) measures social norms using the definitions of injunctive norms (Onu & Oats, Citation2015). Injunctive norms focus on how individuals are affected by behavior that society disapproves of. These norms indicate the individual’s perception of the moral code of the group. Social norms that can influence taxpayer behavior indicate that individual taxpayer behavior is influenced by other taxpayers. The perception that society disagrees with tax evasion can prevent individuals from behaving rationally in a tax compliance dilemma. This research shows that the behavior of taxpayers is influenced by the perception of behavior or moral rules that most people agree with. These results confirm Alm et al. (Citation2019) who implies that taxpayer decisions are influenced by the behavior of other taxpayers. Furthermore, the results of this study are also consistent with Alm (Citation2018) who states that taxpayer behavior is influenced by group considerations, including, in this case, social norms.

This study shows that trust in authority plays a significant role in the tax compliance dilemma. The synergistic climate that is built in the relationship between the taxpayer and the government shows that both parties act in good faith with respect to their respective rights and obligations. The existence of a clean and reliable government in managing tax funds and ensuring that other taxpayers have paid taxes can reduce short-term-oriented individual egos. A synergistic climate is able to encourage individuals to behave in accordance with long-term-oriented collective interests. The results of this study confirm the findings of Balliet and Van Lange (Citation2013), Lange et al. (Citation2017), Gangl et al. (Citation2015).

The results of this study are consistent with the “trust paradigm” which emphasizes the importance of ethics, morality, and social norms in tax compliance decisions (Alm & Torgler, Citation2011). The trust paradigm emphasizes that the government needs to make changes in the culture of paying taxes. For example, clarifying the relationship between tax payments and public services provided by the government. This research also has implications for regulators who need to communicate tax norms through tax compliance campaigns in the mass media. Taxpayers need to be convinced that all taxpayers fulfil their tax obligations proportionally and that there are no free riders in the provision of public facilities. Regulators also need to develop scenarios to build a synergistic relationship with taxpayers, for example, by minimizing leakage in the use of tax funds, transparency in the use of tax funds, and equity in the use of tax funds.

6. Conclusion

This study provides empirical evidence that psychological factors can play an important role in investigating tax compliance in social dilemma situations. Investigation of psychological factors is important because economic factors alone are not enough to investigate the complexity of tax compliance issues. Furthermore, the empirical findings of traditional compliance did not provide significant support regarding the effect of compliance instruments on tax compliance. This study provides empirical evidence that psychological factors have an important role when taxpayers face dilemmas in reporting their income. Social norms act as ecological rationality that provides a guideline to taxpayers that they should contribute to the collective interest because other taxpayers are also doing the same thing. The relationship between the taxpayer and the tax authority is also a significant factor in tax compliance decisions. The synergistic climate between the two will help taxpayers overcome the tax compliance dilemma. A synergistic climate is indicated by situations where tax funds are used properly and the authorities trust taxpayers to fulfil their tax obligations honestly. This causes taxpayers to tend to suppress personal interests for the benefit of the public who are generally obedient with regard to tax rules. In conclusion, this study confirms the deviation from the assumptions of the traditional tax compliance model (Alm, Citation2018). This study shows that psychological factors can be significant in encouraging individuals to fulfil collective interest. This research is limited in several respects. First, the use of college students in tax compliance experiments continues to be a matter of debate. This study uses students as its experimental subjects. However, this is a common practice in tax compliance experiments. In addition, this research places more emphasis on the subject’s cognition process in understanding scenarios, and not on emphasizing the subject’s experience in reporting income. Second, the subjects of this research were predominantly female respondents. This is a natural characteristic of accounting departments, which are generally dominated by female students. However, this dominance does not affect the results of the analysis in this study which remain robust after including gender in the empirical model. Third, although this study provides significant empirical evidence regarding the role of social norms in the tax compliance dilemma, the individuals’ process of building their social environment is ignored. Social norms in this study are limited to injunctive norms. Wenzel (Citation2004) and Jimenez and Iyer (Citation2016) show that social norms become personal norms through an independent identification process, so individuals determine relevant social norms and then reject irrelevant social norms. Future research could investigate how this process occurs and examine the impact of this process on tax compliance dilemmas.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Abraham, M., Lorek, K., Richter, F., & Wrede, M. (2018). Breaking the norms: When is evading inheritance taxes socially acceptable? European Journal of Political Economy, 52(May2017), 85–11. https://doi.org/10.1016/j.ejpoleco.2017.05.003

- Allingham, M. G., & Sandmo, A. (1972). Income tax evasion: A theoretical analysis. Journal of Public Economics, 1(3–4), 323–338. https://doi.org/10.1016/0047-2727(72)90010-2

- Alm, J. (2018). What Motivates Tax Compliance? Journal of Economic Surveys, 1–36. https://doi.org/10.1111/joes.12272

- Alm, J., Gerbrands, P., & Kirchler, E. (2020, September). Using “responsive regulation” to reduce tax base erosion. Regulation and Governance, https://doi.org/10.1111/rego.12359

- Alm, J., & Kasper, M. (2020). Laboratory experiments. In Tulane economics working paper series laboratory (pp. 1-34). https://doi.org/10.4135/9781483381411.n287

- Alm, J., Kirchler, E., Muehlbacher, S., Gangl, K., Hofmann, E., Kogler, C., & Pollai, M. (2012). Rethinking the research paradigms for analysing tax compliance behavior. CESifo Forum, 2, 33–41. https://www.cesifo.org/DocDL/forum2-12-focus5.pdf

- Alm, J., & Malézieux, A. (2021). 40 years of tax evasion games: A meta-analysis. Experimental Economics, 24(3), Springer US. https://doi.org/10.1007/s10683-020-09679-3

- Alm, J., Schulze, W. D., von Bose, C., & Yan, J. (2019). Appeals to social norms and taxpayer compliance. Southern Economic Journal, 86(2), 638–666. https://doi.org/10.1002/soej.12374

- Alm, J., & Torgler, B. (2011). Do ethics matter? Tax compliance and morality. Journal of Business Ethics, 101(4), 635–651. https://doi.org/10.1007/s10551-011-0761-9

- Argentiero, A., Casal, S., Mittone, L., & Morreale, A. (2021). Tax evasion and inequality: Some theoretical and empirical A. (2021). Tax evasion and inequality: Some theoretical and empirical insights. Economics of Governance, 22(4), 309–320. https://doi.org/10.1007/s10101-021-00261-y

- Balliet, D., & Van Lange, P. A. M. (2013). Trust, conflict, and cooperation: A meta-analysis. Psychological Bulletin, 139(5), 1090–1112. https://doi.org/10.1037/a0030939

- Batrancea, L., Nichita, A., Olsen, J., Kogler, C., Kirchler, E., Hoelzl, E., Weiss, A., Torgler, B., Fooken, J., Fuller, J., Schaffner, M., Banuri, S., Hassanein, M., Alarcón-García, G., Aldemir, C., Apostol, O., Bank Weinberg, D., Batrancea, I., Belianin, A., … Zukauskas, S. (2019). Trust and power as determinants of tax compliance across 44 nations. Journal of Economic Psychology, 74(July), 102191. https://doi.org/10.1016/j.joep.2019.102191

- Brizi, A., Giacomantonio, M., Schumpe, B. M., & Mannetti, L. (2015). Intention to pay taxes or to avoid them: The impact of social value orientation. Journal of Economic Psychology, 50, 22–31. https://doi.org/10.1016/j.joep.2015.06.005

- Cialdini, R., & Trost, M. (1998). Social influence: Social norms, conformity, and compliance. D. Gilbert, S. Fiske, & G. Lindzey, Eds. (4th) The handbook of social psychology, (Vol. 27, pp. 607). Issue 6 Oxford University Press. https://doi.org/10.2307/2654253

- Dawes, R. M. (1980). Social Dilemmas. International Journal of Psychology, 31, 2. https://doi.org/10.1080/002075900399402

- Deglaire, E., Daly, P., & Le Lec, F. (2021). Exposure to tax dilemmas deteriorate individuals’ self-declared tax morale. Economics of Governance, 22, 363–397. https://doi.org/10.1007/s10101-021-00262-x

- Di Gioacchino, D., & Fichera, D. (2020). Tax evasion and tax morale: A social network analysis. European Journal of Political Economy, 65(June), 101922. https://doi.org/10.1016/j.ejpoleco.2020.101922

- Di Gioacchino, D., & Fichera, D. (2022). Tax evasion and social reputation: The role of influencers in a social network. Metroeconomica, 73(4), 1048–1069. https://doi.org/10.1111/meca.12391

- Dularif, M., & Rustiarini, N. W. (2022). Tax compliance and non-deterrence approach: A systematic review. International Journal of Sociology and Social Policy, 42(11–12), 1080–1108. https://doi.org/10.1108/IJSSP-04-2021-0108

- Gangl, K., Hofmann, E., & Kirchler, E. (2015). Tax authorities’ interaction with taxpayers: A conception of compliance in social dilemmas by power and trust. New Ideas in Psychology, 37, 13–23. https://doi.org/10.1016/j.newideapsych.2014.12.001

- Górecki, M. A., & Letki, N. (2020) Social norms moderate the effect of tax system on tax evasion: Evidence from a large-scale survey experiment. Journal of Business Ethics. 2003. https://doi.org/10.1007/s10551-020-04502-8.

- Gürdal, M. Y., Torul, O., & Vostroknutov, A. (2020). Norm compliance, enforcement, and the survival of redistributive institutions. Journal of Economic Behavior and Organization, 178, 313–326. https://doi.org/10.1016/j.jebo.2020.07.031

- Güzel, S. A., Özer, G., & Özcan, M. (2019). The effect of the variables of tax justice perception and trust in government on tax compliance: The case of Turkey. Journal of Behavioral and Experimental Economics, 78, 80–86. https://doi.org/10.1016/j.socec.2018.12.006

- Jimenez, P., & Iyer, G. S. (2016). Tax compliance in a social setting: The influence of social norms, trust in government, and perceived fairness on taxpayer compliance. Advances in Accounting, 34, 17–26. https://doi.org/10.1016/j.adiac.2016.07.001

- Kirchler, E. (2007). The Economic Psychology of Tax Behaviour. Cambridge University Press.

- Kirchler, E., & Hoelzl, E. (2017). Tax behaviour. In Rob R. (Ed.), Economic psychology (pp. 255–271). John Wiley & Sons Ltd. https://doi.org/10.1002/9781118926352.ch16

- Kirchler, E., Hoelzl, E., & Wahl, I. (2008). Enforced versus voluntary tax compliance: The “slippery slope” framework. Journal of Economic Psychology, 29(2), 210–225. https://doi.org/10.1016/j.joep.2007.05.004

- Lange, P. A. M., Van, Rockenbach, B., & Yamagishi, T. (2017). Trust in social dilemmas. Oxford University Press.

- Nurkholis, N., Dularif, M., Rustiarini, N. W., & Ntim, C. G. (2020). Tax evasion and service-trust paradigm: A meta-analysis. Cogent Business and Management, 7(1), 1. https://doi.org/10.1080/23311975.2020.1827699

- Onu, D., & Oats, L. (2015). The role of social norms in tax compliance: Theoretical overview and practical implications. Journal of Tax Administration, 1(1), 113–137. http://jota.website/article/view/11/64

- Shafer, W. E., & Wang, Z. (2017). Machiavellianism, social norms, and taxpayer compliance. Business Ethics: A European Review, July, 1–14. https://doi.org/10.1111/beer.12166

- Smith, V. L. (2003). Constructivist and ecological rationality in economics. The American Economic Review, 93(3(Jun., 2003)), 465–508. https://doi.org/10.1257/000282803322156954

- Wahl, I., Kastlunger, B., & Kirchler, E. (2010). Trust in authorities and power to enforce tax compliance: An empirical analysis of the ‘‘slippery slope framework’’. Law & policy, 32(4), 383–406. https://doi.org/10.1111/j.1467-9930.2010.00327.x

- Wenzel, M. (2004). The social side of sanctions: Personal and social norms as moderators of deterrence. Law and Human Behavior, 28(5), 547–567. https://doi.org/10.1023/B:LAHU.0000046433.57588.71

- Yaser, S., Jolodar, E., Ahmadi, M., & Imankhan, N. (2019). Presenting the model of tax compliance: The role of social-psychological factors. Asia-Pacific Management Accounting Journal, 14, 2. https://apmaj.uitm.edu.my/images/Vol-14-2/07.pdf

- Yong, S., Lo, K., Freudenberg, B., & Sawyer, A. (2019). Tax compliance in the new millennium: Understanding the variables. Australian Tax Forum, 34(4), 766–809. https://search.informit.org/doi/10.3316/ielapa.971007102558243