?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to examine the effect of the environmental accounting strategy on sustainability performance and explore waste management as a mediation between environmental accounting strategy and the sustainability performance of Micro, Small and Medium Enterprises (MSMEs). Research data was collected from 194 MSMEs in East Java Indonesia through online and offline questionnaires. The data analysis is performed with PLS-SEM. The results of the study found that the MSME’s environmental accounting strategy had an effect on sustainability performance, and it was proven that MSME’s waste management mediated the effect of environmental accounting strategy on MSME sustainability performance. The originality of this research is the development of research instruments, which combine from various sources from previous researchers, GRI standards and Indonesian Government Regulations so that they can contribute Environmental Management Accounting literature and practical contributions to MSMEs and related institutions in determining sustainability performance strategies. This research implication supports the goals of the Indonesian Government’s Sustainability Development Goals (SDGs) regarding SDGs Goal number 12 Responsible consumption and production. The government needs to establish a waste management policy to improve environmental problems. The implications of future research can collect larger data and can compare the MSMEs between emerging countries. Also, MSMEs need to establish strategic Environmental Accounting so that it has an impact on sustainability performance

1. Introduction

Companies produce goods or services using raw materials and other materials in the production process. As a result, it impacts material waste, product, and packaging waste. The impact on economic sustainability can reduce sales and operating profits because consumers prefer environmentally friendly products. The impact on environmental sustainability not only can reduce environmental damage such as soil and water pollution and increased global warming but also decrease in employee welfare along with a decrease in operating profit.

Moreover, management’s understanding and knowledge of environmental accounting strategies and waste management are essential in achieving business sustainability in companies, including Micro, Small, and Medium Enterprises (MSMEs). The negative impacts of MSMEs include environmental pollution from production waste. As many as five industries are the biggest producers of B3 (Toxic Hazardous Materials) waste in Indonesia, namely: the metal, chemical, electricity, sugar, and paper industries. As stated by the Deputy Chairperson of Investment in East Java, Turino Junaidi, said that the amount of MSME waste is large, but the level of investment for the waste treatment industry is still small (www.kompasiana.com). For example, from 71 SMEs making tofu in Jombang, almost all of the soybean waste is disposed of together on village roads before finally being dumped into the river. As a result, it polluted the environment in three villages and even polluted surface water and well water. (www.jatim.kompas.tv/article/126221). Therefore, the environmental problems are mostly caused by the impact of economic and social activities of companies, including Micro, Small Medium Enterprises (MSMEs). Polluted water sources, polluted air, deforested forests, and global warming have damaged the environment. People’s awareness demands the importance of protecting environmentally friendly production processes and being concerned with business continuity than the short-term goal of profit.

Accounting management is one of the management strategies in achieving the company’s sustainability performance Research on Environmental Management Accounting (EMA) conducted in Indonesia needs consistent findings. Abdullah et al. (Citation2020) found that firm size, leverage, profitability, environmental performance as measured by PROPER certificates affect the disclosure of corporate carbon emissions in Indonesia. Sari et al. (Citation2020) found that the application of environmental management accounting has a positive effect on organizational performance. MSMEs can implement EMA by identifying their production processes so that they can plan and control non-value added activities (Xiong et al., Citation2022). By minimizing non-value-added activities, it means that there is no need to incur internal environmental failure costs that arise in activities due to the production of waste and waste, and external environmental failure costs that arise as a result of releasing waste or garbage into the environment (Miehe et al., Citation2022) . The scope of EMA in this study relates to the implementation of environmental costs which consist of environmental prevention costs, environmental detection costs, environmental internal failure costs and external environmental failure costs. MSMEs that apply EMA can ultimately achieve sustainability performance goals, related to environmental, social, economic and institutional aspects.

Likewise Raharjo (Citation2019) found that stakeholder demand, resources, knowledge, and product uniqueness have a significant effect on the implementation of green management, and green management has a significant effect on sustainability performance. The performance of MSMEs was also carried out by Le and Behl (Citation2022) which proved to have found the Mediating Role of Social Responsibility Engagement and Environmental Responsibility Engagement in the relationship between Corporate Governance and Firm Performance in MSMEs. Likewise Sroufe and Gopalakrishna-Remani Citation(2019) found that sustainability management has a positive direct relationship with social sustainability performance.

In addition, the investment in waste management is pricely (Da Silva et al., Citation2019), it requires planning, implementation, control and management knowledge about environmental accounting (Syarif & Novita, Citation2019). EMA is an important part of what companies do because it can encourage better operational procedures and improve corporate environmental management practices (Schaltegger (2018) in Syarif and Novita (Citation2019) . Furthermore, Luthfiani and Atmanti (Citation2021) regarding waste management in Indonesia. found that the waste management efficiency of the Waste Management System in Indonesia is still not good with an average efficiency of 0.39. Economic and social factors have a significant effect, but the educational factor has the biggest influence on efficiency negatively.

However, MSMEs have limited human resources, experience, and even a record of their financial success, making it challenging to evaluate their performance (Maheshwari et al., Citation2020) . Furthermore, Hanaysha et al. (Citation2022) researched on the sustainability performance of MSMEs conducted research on the sustainability performance of MSMEs Measuring the performance of MSMEs is difficult because MSMEs have limited human resources and knowledge and do not even have a record of their business performance. Research on the sustainability performance of MSMEs has been carried out by (Hanaysha et al., Citation2022) Business sustainability is measured based on various items developed by Khan dan Quaddus (Citation2015) in Hanaysha et al. (Citation2022) found that product innovation and service innovation have a significant positive effect on business continuity.

Measurement of the performance of MSMEs in Indonesia has been researched by Madyaratry et al. (Citation2020). The results shows there are four measures of MSME performance that have high (good) scores, namely: ecological, social, economic and institutional dimensions. Furthermore, Maziriri(Citation2020) found that MSME business performance should be seen not only as monetary execution but also as non-financial execution such as consumer loyalty, client maintenance, social recognition, corporate image and employee fulfillment.

Research on the sustainability of MSMEs with external pressure factors has been carried out by previous researchers. Kurniawati et al. (Citation2022) that Innovation is proven to have a positive relationship with sustainability performance. Moreover, Ramos et al. (Citation2016) found that environmental impact evaluation can benefit SMEs in the food industry. Unlike Mady et al. (Citation2022), found that environmental regulations proved to have no effect on eco-innovation in Small and Medium Enterprises in Egypt.Ulupui et al. (Citation2020) regarding green accounting at cement companies listed on the Indonesia Stock Exchange (IDX) found that green accounting as measured by the GRI G-4 index has an effect on environmental performance as measured by PROPER.

In terms of waste management, the responsibility of MSMEs to achieve responsible and environmentally friendly products, and sustainability performance is a unity of economic, social and environmental aspects, called triple bottom line (Hernández et al., Citation2020). The reason for choosing MSMEs is because they have different characteristics from large companies, have a positive contribution to the country regarding employment but also have a negative impact related to the environment (Maiti, Citation2018; Sultan & Sultan, Citation2020).

The novelty of this research was conducted on SMEs which have different characteristics compared to large companies so that they may have different findings. The research instrument is the development of various sources, namely based on the GRI Standards, Madyaratry et al. (Citation2020), Hansen/Mowen (Citation2009) and from government regulation Permen PU/PR No. 3/PRT/M/2013 which has never been made by researchers before. Also, the research is exploring waste management as a mediation between strategy environmental accounting and the sustainability performance of MSMEs. Besides that, the novelty of the research instrument is developing from previous research by adding government regulations regarding waste in Indonesia.

This research contributes to both scientific and practical contributions. Scientific contributions can add references, especially in the field of Management Accounting, especially Environmental Accounting, by proposing waste management as an environmental accounting mediation for the sustainable performance of MSMEs. As for the practical contribution, the results of this study can be used as information in making MSME management decisions in managing production waste and environmental costs. regarding the sustainability of SMEs.

The content of this paper is organized as follows; the next section is a brief summary of the literature on environmental accounting strategy, waste management and the sustainability performance of MSMEs. Next is the development of hypotheses from related literature and conceptual framework. Then we explain the research methods, research results as well as discussion and research conclusions including limitations and future research.

2. Theoretical background and hypotheses development

2.1 Stakeholders theory

Freeman (Citation1999) defines a stakeholder as any group or individual that can affect or be affected by the achievement of corporate goals. Also, Freeman et al. (Citation2010) stated that stakeholders are focused on value and improving company operations. Stakeholders theory put forward by Freeman in 1984, previously also stated that stakeholders depend on the company in satisfying their own interests. The main focus in several literacies of stakeholder theory is also the discussion that stakeholders manage well with things for their own interests. (Freeman et al., Citation2010).

According to stakeholder theory, Jensen and Meckling (Citation1979) view the company as a contact link between different stakeholders. Thus, this theory views the organization as a system that considers not only the interests of the owners, but also the interests of other groups in the environment in which the business operates. MSMEs should also carry out their operations by paying attention to all stakeholders, especially to providing products that are environmentally friendly and environmentally responsible, including in managing their production waste (Kutz, Citation2007).

2.2 Legitimacy theory

Legitimacy theory states that companies have contracts with the community to carry out their activities based on the values of justice, and how companies respond to various interest groups to legitimize company actions. Legitimacy theory states that organizations must continuously try to ensure that they carry out activities in accordance with the boundaries and norms of society (Brown & Deegan, Citation1998). Furthermore, the MSMEs should convince stakeholders that they run a business in accordance with government regulations and community norms related to waste management.

2.3 Polluters Pays Principle (PPP) theory

Based on the Polluters Pays Principle (PPP) Theory as stated by Charles and Ilelaboye (Citation2014), companies are responsible for environmental costs and bear the costs of environmental pollution. This is based on the framework put forward by Abdullah, et al. (Citation2019) PPP first appeared in the recommendations of the Organization for Economic Co-operation and Development (OECD) in 1972 and was reaffirmed in 1992. The PPP theory is set forth in Principle 16, which regulates the internalization of environmental costs by taking into account that polluters must bear the costs of pollution, taking into account public interest and without distorting international trade and investment. The company not only covers pollution prevention and control measures, but also covers liabilities in terms of cleaning costs. The PPP theory believes that if companies take into account and disclose their environmental costs, it will increase the trust and good image of the company, which will ultimately improve performance.

2.4 Institutional theory

Institutional theory is a prominent perspective in contemporary organizational research. It includes a large, diverse body of theoretical and empirical work linked by a common emphasis on cultural understanding and shared expectations. Institutional theory is often used to explain the adoption and spread of formal organizational structures, including written policies, standard practices, and new organizational forms (Peters, Citation2022). Institutional theory states that companies in a certain environment tend to be structured and similar to established companies. That is, most companies that are in the same environment tend to have similar characteristics (Powell & DiMaggio, Citation1983). Deegan (Citation2006) further mentions that companies that deviate from institutionalized norms may have problems achieving and maintaining legitimacy.

2.5. Environmental accounting strategy

The term Environmental Accounting is also called environmental management accounting (Environmental Management Accounting). The definition shares the same objectives, namely: identifying, collecting, calculating and analyzing material and energy related costs; internal reporting and use of information on environmental costs; provide other costs related, information in the decision—making process, with a view to adopting decisions that are efficient and contribute to environmental protection (Ikhsan, Citation2008).

Environmental Management Accounting Strategy is one of the existing systems in environmental accounting that is useful for assisting internal decision making according to The United Nations Division for Sustainable Development (2001). It can be said that environmental management accounting as a process of identifying, collecting, and analyzing information about costs and performance to assist organizational decision making. According to Chang (Citation2007), environmental costs presented in EMA usually refer to the types of costs to control or prevent environmental damage. Based on IFAC (2005), environmental costs under the EMA consist of other monetary information necessary to manage an organization’s environmental performance effectively Tsui (Citation2014) about the benefits associated with the application of EMA, including: reduced costs, increased product prices, attractive human resources, and increased corporate reputation. Apart from Tsui (Citation2014) found that management accounting practices are facilitators for the continuous improvement of environmental performance, compliance with environmental legislation, communication with interested parties, and employee engagement.

Furthermore, the MSMEs that carry out an environmental quality cost accounting strategy can plan, implement and control environmental quality costs by identifying, collecting, analyzing information about the materials used and the waste produced and related costs (Liu et al., Citation2021). Management can run the production process and minimize waste and prevent environmental damage by an environmental quality cost strategy (Chen et al., Citation2022). Also, environmental management Accounting is a process of identifying, measuring and allocating environmental costs and integrating environmental costs carried out by MSMEs entities into making business decisions.

This study uses the concept of environmental accounting strategy from Hansen/Mowen (Citation2009, p. 413), is an environmental cost measured by its application to the following indicators: Environmental prevention costs, namely costs arising from activities to prevent the production of waste that can damage the environment; Environmental detection costs, namely costs incurred as a result of activities carried out to identify that products, processes and other activities within the company have met applicable environmental standards, both from the government, voluntary (ISO 14001) and management policies; environmental internal failure costs are costs incurred in activities carried out due to the production of waste and garbage, but not disposed of to the outside environment and external environmental failure costs incurred as a result of activities carried out after releasing waste or garbage into the environment.

Environmental accounting which describes the actions taken by companies to incorporate environmental benefits and costs as important information into corporate decision-making processes or as business financial results. Based on the three basic pillars of Elkington, green accounting has three basic pillars, namely: environmental accounting, social accounting and financial accounting. Environmental accounting is the process of recognizing, measuring, recording, summarizing and reporting environmental transactions, events or objects to produce environmental accounting information. (Lako, Citation2018). Environmental accounting is more appropriate to use because it is more fundamental and has an ecological nuance (Thornton, 1992 & 2013; Gallhofer and Haslam, 1997; Greenham, 2010 in Lako (Citation2018). Environmental accounting means accounting that cares and loves, and takes into account values and is accountable for environmental, social and economic information of corporate entities in an integrated manner in the process of accounting and reporting information. (Nguyen et al., Citation2020).

2.6. Waste management

Big cities and provincial capitals contribute a large part of the amount of waste in Indonesia. Currently, Indonesians living in cities produce 105,000 tonnes per day and it is predicted that this will increase to 150,000 tonnes per day by 2025 (World Bank, 2019). The increase in population, economic activity and urbanization causes the amount of waste in this area to tend to be greater than in other cities or regencies in the vicinity. The Government of Indonesia through Presidential Regulation No. 97/2017 has targeted 100% of waste to be managed by 2025. This can be achieved by reducing 30% of waste and 70% of waste handling or service (Luthfiani & Atmanti, Citation2021).

The government through Permen PU/PR No. 3/PRTM/2013 states that the method of waste management carried out by the government is sorting, collecting, transporting, processing and final processing. Final waste processing, generally in big cities in Indonesia, is carried out using a sanitary landfill system. Accumulated waste is buried in soil in landfills known as Final Disposal Sites (TPA). MSMEs are one of the entities that must comply with Ministerial Regulation PU/PR No. 3/PRTM/2013 because their waste is a type of small waste. MSMEs can use their waste management strategy in accordance with the stages regulated by the Ministerial Regulation.

2.7. MSME’s sustainability performance

Sustainability is also known as sustainability development and experts define sustainability differently. Referring to the notion of sustainability according to Brutland (1987) in Sukoharsono,Eko et al. (Citation2021) that sustainable development is development that can meet the needs of the present without compromising the ability of future generations to meet their needs. The ideal business referring to sustainability is a business in which there is a balance between planet, people and profit in making decisions or what is known as the Triple Bottom Line which was introduced by Elkington in 1972.(Sukoharsono,Eko et al., Citation2021). Likewise according (Hanaysha et al., Citation2022)Hanaysha et al. (Citation2022) that business continuity focuses on achieving three different objectives; economic, environmental and social performance with the aim that the concept of sustainability emphasizes the fulfillment of business goals and human welfare.

The performance of MSME’s business sustainability is the result of business processes that pay attention to the balance of the planet, people and profit. Various studies have found a measure that can be used to measure the sustainability of MSME’s. Setiawan et al. (Citation2021) found that performance measurement and management model for sustainability proven not only based on financial performance but also based on non-financial performance which is referred to as the 5S introduced by Takashi Osada in the early 1980s consisting of: shitsuke (sustain/discipline), seiri (sort), seiton (set in order), seiso (clean/shine), seiketsu (standardize). As well Hale et al. (Citation2019) found that the sustainability of the agricultural industry can be measured by the financial interests of farmers and environmental practices through changes in behavior, reducing the use of fertilizers and recruiting members. The sustainability performance of MSME’s can be measured by social sustainability efforts in the SME supply chain and supply chain performance (Mani et al., Citation2020). It is strengthened Yang and Jang (Citation2020) that sustainability in the fashion industry refers to compatible systems that do not adversely affect happiness or the environment. Schönborn et al. (Citation2019) based on empirical results there are four dimensions of social sustainability related to corporate culture which are specific predictors of companies classified as financially successful consisting of: sustainability strategy and leadership; Mission, communication and learning; Social concerns and work life; and Loyalty and identification.

Referring to the findings of previous research, the measurement of MSME’s sustainability in this study consists of financial and non-financial indicators according to the triple bottom line concept, namely: planet, people and profit and pressure from external parties.

2.8. Environmental accounting strategy has an effect on MSME’s sustainability performance

Several studies on environmental accounting have proven to have an effect on environmental performance. Abdullah et al. (Citation2020) found that firm size, leverage, profitability, environmental performance as measured by PROPER certificates have an effect on the disclosure of carbon emissions of companies in Indonesia that are listed on the Jakarta Islamic Index from 2012 to 2016. Sari et al. (Citation2020) found that the application of environmental management accounting has a positive effect on organizational performance. Raharjo (Citation2019) conducting a research at Batik SMEs in Surakarta, found that stakeholder demand, resources, knowledge, and product uniquenes affects the implementation of green management, and green management has a significant effect on sustainability performance.

In term of stakeholders theory, the organization as a system that considers not only the interests of the owner, but also the interests of other groups in the environment in which the business operates. MSME’s must also carry out their operations by paying attention to all their stakeholders, especially with regard to providing products that are environmentally friendly and environmentally responsible, including in managing their production waste. Parmar et al. (Citation2010) states that stakeholders are focused on the value and operational improvement of the company. Stakeholders theory put forward by Freeman in 1984, previously also stated that stakeholders depend on the company in satisfying their own interests. The main focus in several literacies of stakeholder theory is also the discussion that stakeholders manage well with things for their own interests. Parmar et al. (Citation2010) defines stakeholders as “any group or individual who can affect or be affected by the achievement of company goals. Based on the description above, the first hypothesis is:

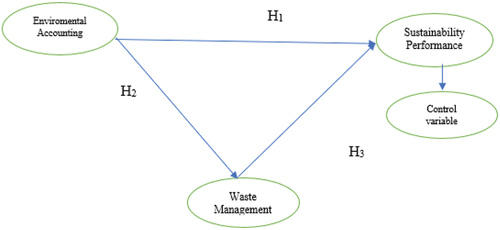

H1: Environmental accounting Strategy has an effect on the sustainability performance of MSME’s

2.9. Environmental accounting strategy has an effect on MSME’s waste management

The environmental accounting strategy is carried out by identifying activities related to the production process and environmental costs and then planning, implementing and controlling environmental activities and costs. The resulting information is useful for preparing waste management as a result of inefficient production processes. Waste management is adjusted to the type of waste, the need for waste collection and transportation facilities. In term of the research on MSME’s environmental accounting related to how MSME’s management manages waste have been carried out by (Maulidah and Wahib Muhaimin (Citation2021) on Sustainable Business Models. The results of this study indicate that the Potato agro-industry MSME’s achieves sustainable performance. Strengthened by Y. Huang et al. (Citation2022) that analysis of the global context of sustainability to reduce and design waste as a new way to change the traditional linear economic model.

In term of legitimacy theory, it can be directly linked to the concept of “social contract”. In particular, it is considered that the survival of the organization will be threatened if society perceives that the organization is operating in an acceptable or lawful manner, then society will effectively revoke the organization’s “contract” to continue its operations (Deegan, Citation2002). In the context of MSMEs managing waste, it is a special contract with the community, especially with regard to environmental sustainability and producing responsible and environmentally friendly products. Based on this description, the second hypothesis is:

H2: The environmental accounting strategy has an effect on MSME’s waste management

2.10. Waste management has an effect on the sustainability performance of MSME’s

Based on the Polluters Pays Principle (PPP) Theory (Charles & Ilelaboye, Citation2014), the company is responsible for environmental costs and bears the cost of environmental pollution. PPP first appeared in the recommendations of the Organization for Economic Co-operation and Development (OECD) in 1972 and was reaffirmed in 1992. The PPP theory is set forth in Principle 16, which regulates the internalization of environmental costs by taking into account that polluters must bear the costs of pollution, public interest and without distorting international trade and investment. The company not only covers pollution prevention and control measures, but also covers liabilities in terms of cleaning costs. The PPP theory believes that if companies take into account and disclose their environmental costs, it will increase the trust and good image of the company, which will ultimately improve performance.

According to empirical evidence based on Schmidt and Nakajima (Citation2013) which states that MFCA can improve environmental performance. MFCA (Material Flow Cost Accounting) is the adoption of Flow Cost Accounting (FCA) originating from Augsburg in Germany which was later promoted and adopted by Japan (Loen, Citation2018; Loen, Citation2019). The main concept of MFCA is that every input(material) and all and output including waste, is determined in a quantity center, and the calculation of material, energy, and costs incurred for products as well as material losses. Material Flow Cost Accounting provides information on the driving costs of materials and energy use as well as provides new and precise information on costs associated with inefficiencies. Companies that implement MFCA can identify and control the costs that will be incurred to manage waste due to inefficient production processes, so that sustainability performance is related with environmental aspects can be achieved (S. Y. Huang et al., Citation2019). Likewise, Cuc and Tripa (Citation2018) conducted research Design recycling Clothing industry in Romania. It was found that by encouraging the creativity of fashion designers to make new models with different fabric combinations so that there is no more leftover cloth to become waste because it is processed into environmentally friendly products. In addition, the company can reduce the cost of waste treatment and can make a profit. Then, the third hypothesis is:

H3: Waste management has an effect on the sustainable performance of MSME’s

2.11. Environmental accounting strategy affects the sustainability performance of MSME’s through waste management

According to the stakeholder theory, which views the organization as a system that considers not only the interests of the owners, but also the interests of other groups in the environment in which the business operates. MSMEs must also carry out their operations by paying attention to all stakeholders, especially with regard to providing products that are environmentally friendly and environmentally responsible, including in managing their production waste. Charles and Ilelaboye (Citation2014). Findings Moneva and Ortas (Citation2010) that companies that obtain better environmental performance can improve internal efficiency and can improve environmental performance in the next period. Malesios et al. (Citation2021) who conducted a literature review of published journal articles in 2018 found that the sustainability performance of MSMEs was most focused on the economy and environment

In term of the institutional theory, which states that organizations are not only subject to economic pressures, but also social and cultural pressures that arise from interactions between organizations in their institutional environment.(Suddaby, Citation2010). The theory views that the holder of an important role in management and organizational theory is the pressure and dynamics in an environment that can form an organization. Based on this description, the fourth hypothesis:

H4: Environmental accounting Strategy influences the sustainability performance of MSME’s through waste management

The theoretical framework in this research is seen as bellow:

3. Research methods

3.1. Sample data

This research was conducted with a quantitative approach, namely testing the proposed research hypothesis. The data was obtained by distributing questionnaires to MSME’s owners in East Java Indonesia who are members of the Cooperative and MSME’s Development Office. The research sample was conducted randomly with the one approach is to use another data set to predict the likely effect size and a second approach is to use clinical judgment to specify the smallest effect size that consider to be relevant (Anvari & Lakens, Citation2021; Pogrow, Citation2019). Researchers sent questionnaires to MSME’s groups under the auspices of the Cooperative Service by sending a Googleform link. In addition, researchers also conducted direct surveys of MSME’s in East Java. The survey was conducted starting in early May 2022 and ending in June 2022. There were 185 questionnaires filled out via Googleform and 32 questionnaires filled in directly by MSME’s. The total quessionnaires is 217. However, 23 questionnaires could not be processed further because many answers were not filled in. In the end, the number of questionnaires processed was 194 respondents (Bougie & Sekaran, Citation2019).

3.2. Research and measurement variables

The research variables consist of the dependent variable is the sustainable performance of MSME’s, the independent variable is environmental accounting strategy, the waste management mediation variable and the control variable are turnover and the number of MSME employees. Researchers developed research instruments based on GRI Standards and Madyaratry et al. (Citation2020) by adding government regulations Permen PU/PR No. 3/PRT/M/2013 and Hansen/Mowen (Citation2009). Prior to sending the questionnaires to the respondents, the face validity was carried out by MSME experts and Sustainability experts. A trial of the instrument then carried out on SMEs and students who have businesses as many as 20 respondents. The results of the pilot test found that a total of 21 questions were invalid, so the questions were eliminated. The data has been cleaned and run based on the component analysis loading factor above 0.60 which is still acceptable because this research is still at the development stage referring to Ghozali and Nasehudin (Citation2012) and . Then the internal consistency run shows the Composite Reliability value above 0.7 based on Hair, Risher et al. (Citation2019) . The results of the construct validity test showed that the environmental accounting variable was valid (0.842) and reliable with an Average Variance Extracted value of 0.619. However, the results of the construct validity test of the waste management and sustainability performance variables showed valid but not reliable with the conbranch alpha values of 0.830 and 0.852 respectively and the Average Variance Extracted of 0.281 and 0.351, respectively. After tracing questions about Sustainability performance, numbers 4,5,7,8,9,10,11 were invalid and dropped. Questions about waste management number 1,3,4,8,9.10,11,12.13,14,15,16,17 and 18 are also eliminated.

Based on the pilot test, there are 15 indicators with loading factor values above 0.5, with details of 5 environmental accounting strategy variable indicators, 6 sustainability performance variable indicators, and 4 waste management variable indicators. This research is in the development stage, so the loading scale of 0.50 to 0.60 is still acceptable based on Ghozali & Nasehudin (2012b). The indicator relevance with loading 0.50 which is statistically significant is considered relevant (Hair, Risher et al., Citation2019). Following are the results of the validity test with the outer model analysis:

In term of the data analysis, a Common Bias Test was carried out to prove the correlation value between constructs and between indicators should not be high, ideally VIF < 3. All variables show VIF values below 3. Then, the data analysis technique was carried out using Partial Least Square assisted by SmartPLS version 3.0 software. PLS analysis consists of two models, namely the measurement model and the structural model (I. Ghozali, Citation2021). The data analysis includes: Descriptive Statistical analysis, with the aim of describing research data in general by measuring the mean, median, mode, minimum, maximal values; Evaluation of the Measurement Model (Outer Model-Measurement Model). To describe the relationship between indicator blocks and their latent variables, it can be described through outer analysis. The criteria for viewing the outer model consist of: convergent validity, discriminant validity and composite reliability (Imam Ghozali, Citation2014). Convergent validity of the measurement model with reflexive indicators can be seen from the correlation between the item score/indicator and the construct score. Individual reflective measure is high if more than 0.70 with the construct you want to measure. According to Hair, Risher et al. (Citation2019), the indicator relevance with loading 0.50 which is statistically significant is relevant. Next, the composite reliability test is used to measure the reliability of constructs or latent variables. The reliability test is reliable if the composite reliability value is at least 0.7 for all constructs. Then, R2(R-square) indicates the size of the endogenous variables that can be explained by exogenous variables. R2 values of 0.75, 0.50 and 0.25 are considered substantial, moderate and weak.

To assess whether the measurement of exogenous latent variables on endogenous variables has a substantive effect, it can be seen from the change in the R2 value through the effect size. Effect size can be done by Chi Square test and fit test. By looking at Chi2 predictive relevance if the Chi2 value is greater than 0 it indicates the model has predictive relevance, while less than 0 indicates the model has no predictive relevance value.

The following is the model equation according to Baron and Kenny (Citation1986):

With, SP is sustainability performance MSME’s, EAS is environmental accounting strategy, WM is waste management and K is control variable and e is residual.

Hypothesis testing is carried out based on the results of testing the inner model. The decision to accept the hypothesis provided that the t-table value of the two tailed test is 1.96 for a maximum siginifiancy of 0.1. To see if a hypothesis is accepted or rejected can look through the value of the calculation of the probability value. So that the hypothesis test criteria are said to be accepted if the t-statistical value is above the t-table value of 1.96 and the p-value < 0.1

4. The data analysis and results

4.1. Descriptive statistics

Based on the pilot test, there are 15 indicators with loading factor values above 0.5, with details of 5 environmental accounting strategy variable indicators, 6 sustainability performance variable indicators, and 4 waste management variable indicators shown in Table below. This research is in the development stage, so the loading scale of 0.50 to 0.60 is still acceptable based on (Ghozali & Nasehudin, Citation2012). The indicator relevance with loading 0.50 which is statistically significant is considered relevant (Hair et al., Citation2019).

Table 1. Pilot test validity test results

The sample of this research is SMEs in East Java, Indonesia with various types of businesses. The largest sample is MSME with the type of food and beverage business (58,25%) and the least is the Batik business (1.55%). When viewed from the age of the company, the most are MSMEs with age less than 5 years (48,45%). Most of the samples in this study were from the micro category because they were dominated by MSMEs with a workforce of less than 10 people (80,41%) and a total turnover of less than IDR 300 million (77,84%) as shown in Table below:

Table 2. The results of respondent demographic statistics

The following is the demographic data of the respondents in this study. It appears that most of the fillers in this questionnaire are female (51,03%) with the most education being Degree (50,51%) and positions in the company are owners (92,27%) as shown in Table below:

Table 3. The data of the respondents

Table shows that the average MSME’s in East Java Indonesia has implemented an environmental accounting strategy with an average value of more than 3,000, which means they tend to agree. MSME’s have achieved sustainability performance with an average value of 3.494. MSMEs have also carried out waste management with an average value of 3.601, which means that they quite agree tend to agree.

Table 4. Variable descriptive statistical results

Based on Table , MSME’s have not been optimally responsible for product waste. (Z2, Z3, Z4) proves that they have not labeled the type of waste, have not distinguished the color of the waste container and all the waste containers have not been closed. Based on Table , it shows that the mean value is below the median value, indicating that waste management has not been carried out optimally. Waste management carried out by MSME’s after being collected is then only transported with simple means or then sold directly to waste collectors.

Table 5. The MSME’s Responsibilities for Product Waste

Table 6. MSME sustainability performance

The result of the less than optimal waste management has an impact on low sustainability performance. The following is evidence of the low sustainability performance of MSME’s in Table below:

Based on Table , sustainability is based on environmental performance aspects with a minimum indicator of using 50% recyclable material and checking heating temperatures during the production process, has not been fully carried out by MSME’s, it appears that the mean value is below the median value. Sustainability performance on the social aspect shows that MSME’s have provided benefits to employees with a mean value equal to the median value. Sustainability performance in the economic aspect shows that MSME’s have participated in infrastructure and services for the public interest, although it is still low. Likewise, when viewed from the institutional aspect, MSME’s have low sustainability performance, it is evident that employee training on the environment is still low and the acquisition of environmental certificates is also still low, with a mean value below the median value.

The result of the less than optimal waste management has an impact on low sustainability performance. This is also because MSME’s understanding of Environmental Accounting is still low as shown in Table below:

Table 7. MSME’s environmental accounting strategy

The Table shows that the MSMEs management’s understanding of Environmental Accounting is quite understandable. Based on Table above, it shows that MSMEs have carried out employee training on waste reduction and waste recycling as a form of environmental prevention costs, although it is not optimal with a mean value below the median value. The cost of environmental detection for inspection of environmentally friendly products has been carried out optimally by MSMEs, it is proven that the mean value is close to the median value (Singh, Citation2019). Also, the costs of internal failure for waste treatment and external failure for environmental cleaning have been carried out by SMEs but are still not optimal, it is proven that the mean value is below the median value.

Table 8. Outer Loading Factor Estimation Results for the third stage

The need for a strategy on Environmental Accounting and Waste Management in supporting the Sustainability Performance of MSMEs. Based on the evidence of sub-optimal waste management, the understanding of MSME regarding Environmental Accounting is relatively low which has an impact on the achievement of MSME Sustainability performance which is less than optimal. Then a management strategy is needed related to waste management and Environmental Accounting to achieve Sustainability performance (Dhar et al., Citation2022) . The following is an alternative model of an exploration of waste management which can mediate an understanding of Environmental Accounting to achieve Sustainability performance for MSMEs.

4.2. The evaluation of measurement model (outer model)

The stages of hypothesis testing are carried out by evaluating the outer model and then the inner model. The convergent validity testing with the aim of testing related units in a variable, does not compare with other variables by looking at the loading factor value. This research is only at the development stage, so a loading scale of 0.50 to 0.60 is still acceptable (Ghozali & Dan, Citation2014). Also, based on Hair, Risher et al. (Citation2019) the indicator relevance with loading 0.50 which is statistically significant is considered relevant Evaluation of the outer loading value is said to be valid if the outer loading value is > 0.5 and ideal if the outer loading value is > 0.7. Based on this, there are 3 indicators of MSME sustainability performance variables that are invalid (Y2, Y3 and Y5), and 2 indicators of waste management (Z5 and Z6) and 1 indicator of the control variable (K2) which are invalid so they are eliminated. Then a second stage outer test was carried out with the result that the Z1 indicator was invalid so it was eliminated for the next test. The following are the results of the outer model test after Z1 is dropped. Discriminant Validity majorly uses Fornell Larcker. Hair, Risher et al. (Citation2019) is determined the value < 0.85. The results show that all variables have a value of < 0.85 so they can be said to be valid.

The evaluation of the model is then carried out by measuring the reliability of constructs or latent variables as measured by their composite reliability. Following are the results of the reliability test:

Based on Table , all constructs have a composite reliability value of more than 0.7, so it can be concluded that all indicators of reflective constructs are reliable.

Table 9. Composite reliability values

4.3. Hypothesis testing

Hypothesis testing is carried out based on internal model testing which includes: fit test and parameter coefficients and t statistics. According to the research design that has been determined, the level of confidence maximum used is 90% and the p value is less than 0.1, so the research hypothesis successfully supported.

The evaluation of the model is then carried out by measuring the reliability of constructs or latent variables as measured by their composite reliability. Following are the results of the reliability test It can be seen in table below.

While the results of path statistics for hypothesis testing shows bellow:

It is based on Table that the resulting path coefficient values all show a statistical t value above 1.96 with a p value of less than 0.1. This means that all of the research’s hypotheses are supported. Based on the predicted results of the effect of the environmental accounting strategy variable on the sustainability performance of MSMEs is positive at 0.558 and statistically significant with a p value of 0.000. The coefficient shows a strong and significant influence, meaning that if the environmental accounting strategy variable increases by 1%, the sustainability performance will increase by 0.558%(H1 is supported). The prediction results for the effect of environmental accounting strategy on waste management are positive at 0.711 and statistically significant with a p value of 0.000(H2 is supported). The coefficient shows a strong and significant influence, meaning that if the environmental accounting strategy variable increases by 1%, waste management will increase by 0.711% and the P-value of 0.000.

Table 10. Path coefficients

The predicted results of the effect of waste management on the sustainability performance of MSMEs are positive by 0.290 and statistically significant with a p value of 0.004. The coefficient shows a weak and significant influence, meaning that if variable waste management increases by 1%, sustainability performance will increase by 0.290% (H3 is supported).

The predicted result of the indirect effect of environmental accounting strategy through waste management on the sustainability performance of MSMEs is positive at 0.206 with a p value of 0.004. The coefficient shows a weak and significant effect, meaning that if the environmental accounting strategy variable increases by 1% then through an increase in waste management by 1% there will be an increase in sustainability performance of 0.206% (H4 is supported).

Furthermore, the fit model evaluates the structural model predictions using R2, Chi square and f2

The adjusted R2 sustainability performance value of 0.580 indicates that the sustainability performance of SMEs can be explained by environmental accounting and waste management of 58% and the rest is explained by other variables not examined in this study. Hair, Risher et al. (Citation2019) stated that the Adjusted R2 Waste management value of 0.379 indicates that waste management can be explained by environmental accounting variables of 37,9% and the rest is explained by other variables not examined in this study and included in the moderate category. The result is shown on Table .

Table 11. R square, Chi square and f square values

The Chi square value of 294,620 > 0, the prediction model has predictive relevance that the theoretical model is in accordance with the empirical model. The value of f2 shows the change in the value of R2 when the exogenous construct is removed from the model. The substantive impact of exogenous constructs on endogenous constructs can be evaluated in this way. The value of f2 = 0.02, 0.15, and 0.35 respectively represents the level of small, medium, and large influence, from the exogenous construct (Hair et al., Citation2021). The exogenous construct that has a large influence is the environmental accounting strategy and the one that has a moderate effect is waste management.

5. Discussion

5.1. Environmental accounting strategy has an effect on the sustainability performance of MSMEs

The result shows that there is a positive and statistically significant influence of the environmental accounting strategy on the sustainability performance of MSMEs. The environmental accounting strategy includes: Environmental prevention costs, environmental detection costs are costs incurred as a result of activities carried out to identify that products, processes and other activities within the company have been comply with applicable environmental standards, both from government and management policies, internal environmental failure costs are costs incurred in activities carried out due to the production of waste and garbage, but are not disposed of to the outside environment and external environmental failure costs, namely costs incurred as a result of activities that carried out after releasing waste or garbage into the environment.

The results are in-line with Charles and Ilelaboye (Citation2014) and according to stakeholder theory which views the company as a contact link between different stakeholders. The findings of this study also supporting the findings Ali et al. (Citation2021) that social value orientation has a positive relationship with green advertising effectiveness. Green advertising is part of environmental accounting related to environmental detection costs. It is also empirically proven that awards have an influence on the innovation performance of SMEs (Kankisingi & Dhliwayo, Citation2022) and in-line with Sari et al. (Citation2020) regarding the application of environmental management accounting has a positive effect on organizational performance. Raharjo (Citation2019) found that the application of green management has a significant effect on the sustainability performance of MSMEs. Moreover, Kantabutra and Punnakitikashem (Citation2020) shows that MSMEs in Thailand adopt the Sufficiency Economy philosophy achieve corporate sustainability performance both from cultural, social, environmental and economic results. Wentzel et al. (Citation2022) shows that surveyed SMEs in the South African Construction Industry (SACI) found a positive relationship between the integration of CSR in their business and sustainable business performance from an internal and external perspective.

5.2. Environmental accounting strategy has an effect on waste management

The results of this study found that the MSME environmental accounting strategy is related to how MSME management manages waste. This research supports research on environmental accounting for SMEs in developing countries such as Indonesia, that this is influenced by the awareness of the MSME managers. As done Nyahuna and Doorasamy (Citation2021)) found that the practice of EMA in SMEs related to the use of monetary indicators is not yet popular. The study concluded that EMA applications have not been popular with SMEs in developing countries such as South Africa, according to findings in Nyahuna and Doorasamy (Citation2021) regarding the adoption of EMA in Malaysian SMEs is still low due to lack of awareness by managers. Chinomona (Citation2013) that the skills training of small business employees is positively related to the performance of small businesses. It is proven in this study that the cost of employee training includes an element of environmental prevention costs Hansen/Mowen (Citation2009) which can affect how MSMEs manage their waste. Likewise, it strengthens the research results Maulidah and Wahib Muhaimin (Citation2021), also strenghtens by Y. Huang et al. (Citation2022)

This is appropriate Legitimacy theory (Deegan, Citation2002). For this reason, the company continuously ensures that they carry out activities in accordance with the limits and norms of society, for example, by reducing the demand for raw materials or actions that are not in accordance with norms or regulations. This research proves that MSMEs in Indonesia have carried out activities that are based on applicable norms and regulations to convince the local community to manage their production waste.

5.3. The waste management has an effect on the sustainability performance of MSMEs

Based on the Polluters Pays Principle (PPP) Theory, put forward Charles and Ilelaboye (Citation2014) that the company is responsible for environmental costs and bears the cost of environmental pollution. The PPP theory believes that if companies take into account and disclose their environmental costs, it will increase the trust and good image of the company, which will ultimately improve performance. Schmidt and Nakajima (Citation2013) states that MFCA can improve environmental performance. The results of this study support the findings Henriques and Catarino (Citation2015) who researched SMEs in Portugal.

The results of this study also prove that institutional pressure can influence MSMEs to carry out waste management activities in achieving sustainability goals because MSMEs manage their waste in accordance with the regulations of the Ministry of PUPR in Indonesia. This was also discovered by Ernst et al. (Citation2022). D’Adamo et al. (Citation2019) found that the recovery of waste embedded in “waste electrical and electronic equipment” can achieve economic sustainability performance. Cuc and Tripa (Citation2018) conducted research Design recycling Clothing industry in Romania. In addition, the company can reduce the cost of waste treatment and can make a profit.

This study found that the prediction of the effect of waste management on the sustainability performance of MSME’s is positive with the coefficient showing a weak and significant effect. This could be due to the lack of awareness of managers and environmental training in SMEs. The results are in-line with (Balasubramanian et al., Citation2020) that the cost of environmental training is very expensive for MSME’s. Waste management depends on the knowledge and expertise of its human resources. This is reinforced by the Amrutha and Geetha (Citation2020) which revealed that the requirement of Corporate Social Responsibility is the main reason for Green Human Resources management initiatives in many organizations. Moreover, according to institutional theory (Suddaby, Citation2010), it shows external pressure, namely government regulations have proven to encourage MSMEs to carry out waste management to achieve sustainable performance.

5.4. The strategy environmental accounting influences the sustainability performance of MSMEs through waste management

The waste management is able to mediate the influence of the environmental accounting strategy on the sustainability performance of MSMEs. Thus, if the environmental accounting is improved by adding waste management, it can help achieve sustainable MSME performance. According to stakeholder theory (Ang et al., Citation2007), the company is a contact link between different stakeholders. Thus, this theory views the organization as a system that considers not only the interests of the owners, but also the interests of other groups in the environment in which the business operates. MSMEs must also carry out their operations by paying attention to all stakeholders, especially with regard to providing products that are environmentally friendly and environmentally responsible, including in managing their production waste (Charles & Ilelaboye, Citation2014)

This is reinforced by Crossley et al. (Citation2021) that MSMEs use a complex mix of symbolic and substantive sustainable social and environmental practices (SEP). This research supports the findings Malesios et al. (Citation2021). So are the findings Moneva and Ortas (Citation2010) that companies that obtain better environmental performance can improve internal efficiency and can improve environmental performance in the next period.

The waste management is proven to mediate environmental accounting strategy with sustainability performance. This can be influenced by management orientation, innovation, regulations and internal and external pressures related to the environment so that it has an impact on sustainability performance. The results of this study are consistent with the findings Adomako et al. (Citation2021), Nawi et al. (Citation2020), and Muñoz-Pascual et al. (Citation2021) found that manager creativity has a mediating effect between human resource relations and sustainable product innovation performance. So are the findings Ullah et al. (Citation2021) that innovative performance mediates the relationship between domestic financial access and MSME sustainability performance. Mady et al. (Citation2022) found that the relationship between regulations which are performance indicators of sustainability and eco-innovation is mediated by the environmental orientation of MSMEs. Lutfi et al. (Citation2022) shows that external pressure significantly affects the implementation of the Accounting Information System, which in turn achieves sustainable business performance for MSMEs.

Moreover, this study proves that institutional pressure from within or outside the company can influence MSMEs to carry out waste management activities in achieving sustainability goals because MSMEs manage their waste in accordance with the regulations of the Ministry of public works and human settlement in Indonesia. In accordance with the Institutional theory which states that organizations are not only subject to economic pressures, but also social and cultural pressures that arise from interactions between organizations in their institutional environment.(Suddabv & Greenwood, Citation2009).

6. Conclusion and implication of the research

Indonesia is concerned with Green Accounting because MSMEs waste is quite high and poor waste management. The East Java government has the second largest MSMEs in Indonesia and has a problem with industrial waste. However, it does not take maximum responsibility for product waste and an impact on low sustainability performance. This indicates the need for an Environmental Accounting strategy to support policies to minimize environmental costs related to environmental prevention costs for waste reduction employee training, environmental prevention costs for waste recycling training, environmental detection costs for environmentally friendly product inspection, internal failure costs for waste treatment and failure costs. external for cleaning polluted environment. This research implication supports the goals of the Indonesian Government’s Sustainability Development Goals (SDGs) regarding SDGs Goal number 12 Responsible consumption and production. The government needs to establish a waste management policy to improve environmental problems. Therefore all parties, namely: entrepreneurs including MSMEs, government, private sector, communities including financial institutions have the same responsibility to carry out activities and run a business with due regard to production that is responsible for the environment and society.

7. Limitation and future research

This study achieved its objectives, but the findings still contained several limitations such as the number of respondents and the various types of MSME businesses. Besides that, this research was conducted in Indonesia, which is a developing country, which is certainly different from MSMEs in other developed countries. Developing countries have many obstacles, especially with regard to human resource education and the waste management technology used. It is evident from the results of this study that waste management has a weak mediation in environmental accounting for the sustainability performance of MSMEs.

The larger data on MSMEs in various sectors and can compare developing countries with developed countries is needed in the future research. The implications for the government can provide guidance and human resource training related to waste management so that MSMEs can achieve higher sustainability performance. MSME owners should have waste planning and management in accordance with government regulations and make efforts to obtain environmental certification so that people have more confidence in the products they produce because the production process pays attention to environmental and social responsibility and not solely to achieve profit. MSMEs can formulate waste management strategies according to their characteristics and allocate environmental costs and determine MSME key performance indicators based on environmental, social, economic and institutional aspects.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Sri Wahjuni Latifah

Sri Wahjuni Latifah is a Doctoral candidate in Accounting at Universitas Airlangga Surabaya Indonesia and a Lecturer in the Department of Accounting, Faculty of Economics and Business, University of Muhammadiyah Malang. Her research interests are SMSEs Management Accounting, Sustanaibality and Financial Accounting.

Noorlailie Soewarno

Noorlailie Soewarno is head of Doctoral Programme of Accounting and a Lecturer at the Faculty of Economics and Business, University of Airlangga, Surabaya Indonesia. Her research interests are in strategic management accounting, intellectual capital, strategic management, performance management systems, green accounting, governance and sustainability, management control systems.

References

- Abdullah, M. W., Musriani, R., Syariati, A., & Hanafie, H. (2020). Carbon emission disclosure in indonesian firms: The test of media-exposure moderating effects. International Journal of Energy Economics and Policy, 10(6), 732–24. https://doi.org/10.32479/IJEEP.10142

- Adomako, S., Amankwah-Amoah, J., Danso, A., & Dankwah, G. O. (2021). Chief executive officers’ sustainability orientation and firm environmental performance: Networking and resource contingencies. Business Strategy and the Environment, 30(4), 2184–2193. https://doi.org/10.1002/bse.2742

- Ali, M., Hassan, U., Mustapha, I., & Osman, S. (2021). An empirical analysis of the moderating effect of consumer skepticism between social value orientations and green advertising effectiveness. Nankai Business Review International, 12(3), 458–482. https://doi.org/10.1108/NBRI-01-2021-0004

- Amrutha, V. N., & Geetha, S. N. (2020). A systematic review on green human resource management: Implications for social sustainability. Journal of Cleaner Production, 247, 119131. https://doi.org/10.1016/j.jclepro.2019.119131

- Ang, J. S., Cole, R., & Lin, J. W. (2007). Agency costs and ownership structure. Corporate Governance and Corporate Finance: A European Perspective, 111–131. https://doi.org/10.4324/9780203940136

- Anvari, F., & Lakens, D. (2021). Using anchor-based methods to determine the smallest effect size of interest. Journal of Experimental Social Psychology, 96, 104159. https://doi.org/10.1016/j.jesp.2021.104159

- Balasubramanian, S., Shukla, V., & Chanchaichujit, J. (2020). Firm size implications for environmental sustainability of supply chains: Evidence from the UAE. Management of Environmental Quality: An International Journal, 31(5), 1375–1406. https://doi.org/10.1108/MEQ-01-2020-0004

- Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173. https://doi.org/10.1037/0022-3514.51.6.1173

- Bougie, R., & Sekaran, U. (2019). Research methods for business:. A skill building approach: John Wiley & Sons.

- Brown, N., & Deegan, C. (1998). The public disclosure of environmental performance information—a dual test of media agenda setting theory and legitimacy theory. Accounting and Business Research, 29(1), 21–41. https://doi.org/10.1080/00014788.1998.9729564

- Chang, H.-C. (2007). Environmental management accounting within universities: Current state and future potential. RMIT University.

- Charles, S., & Ilelaboye, M. E. A. (2014). Environmental Accounting and Financial Performance of Listed Family- Owned Companies in Nigeria, 6(1), 71–83. https://digitalcommons.du.edu/cgi/viewcontent.cgi?article=1338&context=irbe

- Chen, M., Liu, Q., Huang, S., & Dang, C. (2022). Environmental cost control system of manufacturing enterprises using artificial intelligence based on value chain of circular economy. Enterprise Information Systems, 16(8–9), 1856422. https://doi.org/10.1080/17517575.2020.1856422

- Chinomona, R. (2013). Business Owner’s Expertise, Employee Skills Training And Business Performance: A Small Business Perspective, 29(6), 1883–1896. https://doi.org/10.19030/jabr.v29i6.8224

- Abdullah, R., Mahmuda, D., Malik, E., Pratiwi, E.T., Rais, M., Dja‘wa, A., Abdullah, L.O.D., Hardin, Lampe, M., & Tjilen, A.P. (2019). The influence of environmental performance, environmental costs, and firm size on financial performance with corporate social responsibility as intervening variables (empirical study on manufacturing companies listed on the Indonesia stock exchange 2014-2018). IOP Conf. Series: Earth and Environmental Science, 343. https://doi.org/10.1088/1755-1315/343/1/012136

- Crossley, R. M., Elmagrhi, M. H., & Ntim, C. G. (2021). Sustainability and legitimacy theory: The case of sustainable social and environmental practices of small and medium-sized enterprises. Business Strategy and the Environment, 30(8), 3740–3762. https://doi.org/10.1002/bse.2837

- Cuc, S., & Tripa, S. (2018). Redesign and upcycling - A solution for the competitiveness of small and medium-sized enterprises in the clothing industry. Industria Textila, 69(1), 31–36. https://doi.org/10.35530/it.069.01.1417

- D’Adamo, I., Ferella, F., Gastaldi, M., Maggiore, F., Rosa, P., & Terzi, S. (2019). Towards sustainable recycling processes: Wasted printed circuit boards as a source of economic opportunities. Resources, Conservation and Recycling, 149(June), 455–467. https://doi.org/10.1016/j.resconrec.2019.06.012

- da Silva, L., Prietto, P. D. M., & Korf, E. P. (2019). Sustainability indicators for urban solid waste management in large and medium-sized worldwide cities. Journal of Cleaner Production, 237, 117802. https://doi.org/10.1016/j.jclepro.2019.117802

- Deegan, C. (2002). Introduction: The legitimising effect of social and environmental disclosures – A theoretical foundation. Accounting, Auditing & Accountability Journal, 15(3), 282–311. https://doi.org/10.1108/09513570210435852

- Deegan, C. (2006). Legitimacy theory Methodological issues in accounting research: theories, methods and issues (pp. 161–181): Spiramus Press Ltd.

- Dhar, B. K., Sarkar, S. M., & Ayittey, F. K. (2022). Impact of social responsibility disclosure between implementation of green accounting and sustainable development: A study on heavily polluting companies in Bangladesh. Corporate Social Responsibility and Environmental Management, 29(1), 71–78. https://doi.org/10.1002/csr.2174

- https://surabaya.bisnis.com/read/20201111/532/1316134/investasi-bidang-pengolahan-limbah-b3-di-jatim-kecil. Di akses 15 april 2022

- Ernst, R. A., Gerken, M., Hack, A., & Hülsbeck, M. (2022). SMES’ reluctance to embrace corporate sustainability: The effect of stakeholder pressure on self-determination and the role of social proximity. Journal of Cleaner Production, 335, 130273. https://doi.org/10.1016/j.jclepro.2021.130273

- Freeman, R. E. (1999). Divergent stakeholder theory. Academy of Management Review, 24(2), 233–236. https://doi.org/10.5465/amr.1999.1893932

- Freeman, R. E., Harrison, J. S., Wicks, A. C., Parmar, B. L., & De Colle, S. (2010). Cambridge University Press.

- Ghozali, I. (2014). Model Persamaan Struktural Konsep dan Aplikasi dengan Program Amos 22.0 (VI). Badan Penerbit Universitas Diponegoro.

- Ghozali, I. (2021). Partial least squares Konsep, Teknik dan Aplikasi Menggunakan program smartPLS 3.2.9 untuk Penelitian Empiris (3rd) ed.). Badan Penerbit Universitas Diponegoro.

- Ghozali, I., & Dan, H. L. (2014). Partial least squares Konsep,Metode dan Aplikasi Menggunakan Program WarpPLS 4. Badan Penerbit Universitas Diponegoro.

- Ghozali, I., & Nasehudin, T. S. (2012). Metode Penelitian Kuantitatif. CV Pustaka Setia.

- Hair, J. F., Hult, G. T. M., Ringle, C., Sarstedt, M., Danks, N., & Ray, S. (2021). Partial least squares structural equation modeling (PLS-SEM) using R: A Workbook. Otto von Guericke University Magdeburg. https://doi.org/10.1007/978-3-030-80519-7

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European business review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

- Hale, J., Legun, K., Campbell, H., & Carolan, M. (2019). Social sustainability indicators as performance. Geoforum, 103(February), 47–55. https://doi.org/10.1016/j.geoforum.2019.03.008

- Hanaysha, J. R., Al-Shaikh, M. E., Joghee, S., & Alzoubi, H. M. (2022). Impact of innovation capabilities on business sustainability in small and medium enterprises. FIIB Business Review, 11(1), 67–78. https://doi.org/10.1177/23197145211042232

- Hansen, D. R. &Mowen, M. M. (2009). Akuntansi Manajerial (Managerial Accounting) (8th ed). Salemba Empat: Jakarta. 978-981-254-673-9.

- Henriques, J., & Catarino, J. (2015). Sustainable value and cleaner production - Research and application in 19 Portuguese SME. Journal of Cleaner Production, 96, 379–386. https://doi.org/10.1016/j.jclepro.2014.02.030

- Hernández, J. P. S.-I., Yañez-Araque, B., & Moreno-García, J. (2020). Moderating effect of firm size on the influence of corporate social responsibility in the economic performance of micro-, small-and medium-sized enterprises. Technological Forecasting and Social Change, 151, 119774. https://doi.org/10.1016/j.techfore.2019.119774

- Huang, S. Y., Chiu, A. A., Chao, P. C., & Wang, N. (2019). The application of material flow cost accounting in waste reduction. Sustainability, 11(5), 1270. https://doi.org/10.3390/su11051270

- Huang, Y., Shafiee, M., Charnley, F., & Encinas-Oropesa, A. (2022). Designing a framework for materials flow by integrating circular economy principles with end-of-life management strategies. Sustainability (Switzerland), 14, 7. https://doi.org/10.3390/su14074244

- https://wjourw.kompasiana.com/syahrijal/5ff91e7e8ede480cc915a3c4/resiko-bisnis-umkm-di-kab-sidoarjo

- https://id.berita.yahoo.com/ketahui-lima-fakta-limbah-fesyen-024507513. html,diakses 9 April 2022

- https://sdgsc.itb.ac.id/id/apa-itu-sdgs/diakses,9 April 2022

- Ikhsan, A. (2008). Pengenalan Akuntansi Lingkungan (pp. 1–10). Graha Ilmu: Yogyakarta.

- Jensen, M. C., & Meckling, W. H. (1979). Rights and production functions: An application to labor-managed firms and codetermination. The Journal of Business, 52(4), 469–506. https://doi.org/10.1086/296060

- Kankisingi, G. M., & Dhliwayo, S. (2022). Rewards and innovation performance in manufacturing Small and Medium Enterprises (SMEs). Sustainability (Switzerland), 14, 3. https://doi.org/10.3390/su14031737

- Kantabutra, S., & Punnakitikashem, P. (2020). Exploring the process toward corporate sustainability at a Thai SME. Sustainability (Switzerland), 12(21), 1–19. https://doi.org/10.3390/su12219204

- Khan, E. A., & Quaddus, M. (2015). Development and Validation of a Scale for Measuring Sustainability Factors of Informal Microenterprises – a Qualitative and Quantitative Approach. Entrepreneurship Research Journal, 5, 347–372.

- Kurniawati, A., Sunaryo, I., Wiratmadja, I. I., & Irianto, D. (2022). Sustainability-oriented open innovation: A small and medium-sized enterprises perspective. Journal of Open Innovation: Technology, Market, and Complexity, 8(2), 2. https://doi.org/10.3390/joitmc8020069

- Kutz, M. (2007). Environmentally conscious manufacturing (Vol. 1). John Wiley & Sons.

- Lako, A. (2018). Akuntansi Hijau Isu,Teori Dan Aplikasi (ke-dua). Penerbit Salemba Empat.

- Le, T. T., & Behl, A. (2022). Role of corporate governance in quick response to Covid-19 to improve SMEs’ performance: Evidence from an emerging market. Operations Management Research, 2020. https://doi.org/10.1007/s12063-021-00238-4

- Liu, Y., Wang, A., & Wu, Y. (2021). Environmental regulation and green innovation: Evidence from China’s new environmental protection law. Journal of Cleaner Production, 297, 126698. https://doi.org/10.1016/j.jclepro.2021.126698

- Loen, M. (2018). Penerapan Green Accounting Dan Material Flow Cost Accounting (mfca)terhadap Sustainable Development. Jurnal Akuntansi dan Bisnis Krisnadwipayana, 5(1). http://dx.doi.org/10.35137/jabk.v5i1.182

- Lutfi, A., Al-Khasawneh, A. L., Almaiah, M. A., Alsyouf, A., & Alrawad, M. (2022). Business sustainability of small and medium enterprises during the COVID-19 pandemic: The role of AIS implementation. Sustainability (Switzerland), 14, 9. https://doi.org/10.3390/su14095362

- Luthfiani, N. L., & Atmanti, H. D. (2021). Waste management service in Indonesia based on stochastic frontier analysis. Trikonomika, 20(2), 54–61. https://doi.org/10.23969/trikonomika.v20i2.3952

- Mady, K., Abdul Halim, M. A. S., Omar, K., Abdelkareem, R. S., & Battour, M. (2022). Institutional pressure and eco-innovation: The mediating role of green absorptive capacity and strategically environmental orientation among manufacturing SMEs in Egypt. Cogent Business and Management, 9(1), 1. https://doi.org/10.1080/23311975.2022.2064259

- Madyaratry, L. H., Hadjomidjojo, H., & Anggraeni, E. (2020). The mapping of sustainability index in small and medium enterprises: A case study in lampung Indonesia. Jurnal Teknik Industri, 21(1), 58. https://doi.org/10.22219/JTIUMM.Vol21.No1.58-69

- Maheshwari, M., Samal, A., & Bhamoriya, V. (2020). Role of employee relations and HRM in driving commitment to sustainability in MSME firms. International Journal of Productivity and Performance Management, 69(8), 1743–1764. https://doi.org/10.1108/IJPPM-12-2019-0599

- Maiti, M. (2018). Scope for alternative avenues to promote financial access to MSMEs in developing nation evidence from India. International Journal of Law and Management, 60(5), 1210–1222. https://doi.org/10.1108/IJLMA-06-2017-0141

- Malesios, C., De, D., Moursellas, A., Dey, P. K., & Evangelinos, K. (2021). Sustainability performance analysis of small and medium sized enterprises: Criteria, methods and framework. Socio-Economic Planning Sciences, 75(June2019), 100993. https://doi.org/10.1016/j.seps.2020.100993

- Mani, V., Jabbour, C. J. C., & Mani, K. T. N. (2020). Supply chain social sustainability in small and medium manufacturing enterprises and firms’ performance: Empirical evidence from an emerging Asian economy. International Journal of Production Economics, 227(January), 107656. https://doi.org/10.1016/j.ijpe.2020.107656

- Maulidah, S., & Wahib Muhaimin, A. (2021). Sustainable business models: Challenges on potato agro-industry SMEs. IOP Conference Series: Earth and Environmental Science, 709(1). https://doi.org/10.1088/1755-1315/709/1/012082

- Maziriri, E. (2020). Green Packaging and Green Advertising as Precursors of Competitive Advantage and Business Performance among Manufacturing Small and Medium Enterprises in South Africa. Cogent Business & Management, 7. https://doi.org/10.1080/23311975.2020.1719586

- Miehe, R., Finkbeiner, M., Sauer, A., & Bauernhansl, T. (2022). A system thinking normative approach towards integrating the environment into value-added accounting—Paving the way from carbon to environmental neutrality. Sustainability, 14(20), 13603. https://doi.org/10.3390/su142013603

- Loen, M. (2019). Pengaruh penerapan green accounting dan Material Flow Cost Accounting (MFCA) terhadap Sustainable Development dengan Resource Efficiency sebagai pemoderasi. Jurnal Akuntansi dan Bisnis Krisnadwipayana, 6(3). https://doi.org/10.35137/jabk.v6i3.327

- Moneva, J. M., & Ortas, E. (2010). Corporate environmental and financial performance: A multivariate approach. Industrial Management and Data Systems, 110(2), 193–210. https://doi.org/10.1108/02635571011020304

- Muñoz-Pascual, L., Galende, J., & Curado, C. (2021). Contributions to sustainability in smes: Human resources, sustainable product innovation performance and the mediating role of employee creativity. Sustainability (Switzerland), 13(4), 1–20. https://doi.org/10.3390/su13042008

- Nawi, N. C., Al, M. A., Daud, R. R. R., & Nasir, N. A. M. (2020). Strategic orientations and absorptive capacity on economic and environmental sustainability: A study among the batik small and medium enterprises in Malaysia. Sustainability (Switzerland), 12(21), 1–16. https://doi.org/10.3390/su12218957