?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to explain the role of earnings management in mediating the influence of male CEO masculinity on research & development. This study uses a quantitative approach with a population and research sample using companies on the Indonesia Stock Exchange in 2017–2021. This study collects facial images identified as male CEOs from data on the Indonesia Stock Exchange website and company websites and utilizes Google search. The data analysis method in this study uses Structural Equation Modeling which links theory, concepts and data that can be applied to research variables using Stata software. The findings explain that the role of earnings management mediates the influence of the male CEO’s masculinity face on research &development, meaning that the increase and decrease in the part of earnings management has an impact on increasing and decreasing the masculinity face of male CEOs also has an impact on increasing and decreasing research & development. The practical impact of the research results can help the Indonesian Institute of Accountants develop Financial Accounting Standard No. 19 in Indonesia. Theoretical implications of the research results can explain agency theory and behavioral consistency theory. The findings empirically have implications for company management in making policies related to the face of male masculinity which have an impact on earnings management practice policies and policy making on research & development expenditures, so that the empirical findings can be used by company management and the Indonesian government as policy makers in developing countries as a comparison of developed country policies. Throughout the study’s observations to date, it has not found any research on the topic of the role of profit management mediating the influence of the masculinity of male CEOs associated with research & development costs. The distinct role of male CEOs affects research & development policies and cost. The originality of this study can be shown by the differences from previous studies, first (Jia et al., Citation2014) explain that the face of masculinity of male CEOs has a positive effect on profit management practices. The second (Kamiya et al., Citation2018a; Asyik et al., Citation2022) explains that the face of masculinity of male CEOs has a positive impact on leverage. Research & development in the company have an essential position to increase the company’s long-term profitability

PUBLIC INTEREST STATEMENT

Previous research conducted in the United States was carried out by (Jia 2014) with findings explaining that the facial masculinity of male CEOs had a positive effect on earnings management, while (N F Asyik et al.,Citation2022; Kamiya et al., Citation2018a) explained in empirical findings that the CEO’s masculinity face has a positive effect on leverage. This means that the higher the facial masculinity of male CEOs has an impact on increasing leverage, and vice versa, the lower the facial masculinity of male CEOs has an impact on decreasing leverage. While the empirical findings in the study explain that the role of Earnings management mediates the influence of the facial masculinity of male CEOs on research & development. The empirical findings have implications for regulators and corporate governance policy makers regarding male face size as a determinant of leverage, Earnings Management and research & development policies.

1. Introduction

The role of the male CEO in the company is very important to determine the success of the company he leads from the 2017 to 2021 research period. The male CEO has an important role for the company’s success from the performance of its leaders. The CEO in carrying out his leadership in making policies used for the company, the CEO is a company manager who carries out operational activities in the period 2017 to the period 2021. Agency theory explains the contractual relationship between shareholders and the CEO as an agent (DA. Nuswantara et al., Citation2023; IM Hendrati et al., Citation2022; Jensen & Meckling, Citation1976). Shareholders have a male CEO as an agent to perform tasks in the interests of shareholders, including the delegation of decision-making authority from shareholders to a male CEO as an agent (N F Asyik et al., Citation2022; Mahiswari & Nugroho, Citation2014; Prasetyo et al., Citation2022). Companies on the Indonesia Stock Exchange whose capital consists of shares, shareholders act as principals while male CEOs act as agents. Whereas the theory of behavioral consistency (Epstein, Citation1979; Kalbuana et al., Citation2022; Tjaraka et al., Citation2022) Men have a more aggressive nature than women, the aggressive nature of men can affect earnings management and research & development.

A study that was conducted (Jia, Van et al., Citation2014; Sudaryanto et al., Citation2022; Utari, Sudaryanto et al., Citation2021a) explains that there is a relationship between the face size of male CEO masculinity and earnings management policy making, which can improve company performance. The masculine face of male CEOs has an impact on reducing earnings management policies. According to (Aliyyah, Siswomihardjo et al., Citation2021a; Jia, Lent et al., Citation2014; Prasetio et al., Citation2021) also stated that the face size of male CEO masculinity has a positive effect on earnings management, meaning that the higher the masculinity face size of male CEOs has an impact on increasing earnings management, and vice versa the lower the masculinity face size of male CEOs has an impact on decreasing earnings. Management can encourage the performance and desire of employees to realize maximum work performance so as to help achieve the company’s goals.

In contrast to the research conducted (Indrawati et al., Citation2021; Jia, Lent et al., Citation2014; Kamiya et al., Citation2018a) the research conducted (Almor et al., Citation2020; Endarto, Taufiqurrahman, Indriastuty et al., Citation2021; Utari, Iswoyo et al., Citation2021a) found that gender relations have a negative effect on research & development, meaning that higher gender values have an impact on decreasing research & development, the lower the gender value has an impact on increasing research & development. The high level of facial masculinity for male CEOs means that the performance of male CEOs will increase but the increase is not significant. This is precisely in contrast to the results of his research (Almor et al., Citation2020; Endarto, Taufiqurrahman, Setyadji et al., Citation2021; Prasetio et al., Citation2021) which explains that gender values have a negative effect on research & development, meaning that the higher the gender value has an impact on reducing the value of research & development, and vice versa the lower the gender value has an impact on increasing research & development.

The originality of this study can be seen the difference with previous studies (Abadi et al., Citation2021; Almor et al., Citation2020; Prasetyo, Aliyyah, Rusdiyanto, Kalbuana et al., Citation2021) which explained that gender has a negative effect on research & development, whereas (Aliyyah, Prasetyo et al., Citation2021a; Kamiya et al., Citation2018a; Prasetyo, Aliyyah, Rusdiyanto, Kalbuana et al., Citation2021) explains that the facial masculinity of male CEOs has a negative effect on research & development. However, only examining the role of facial masculinity for male CEOs in terms of earnings management and research & development, there is no research that explains the role of earnings management in mediating the influence of facial masculinity for male CEOs on research & development, because high earnings management practices have an impact on increasing research & development by male CEOs. Whereas in agency theory (Aliyyah, Prasetyo et al., Citation2021b; Jensen & Meckling, Citation1976; Rusdiyanto et al., Citation2021a) explains that the role of earnings management mediates the influence of male CEO characteristics on research & development. While the use of earnings management variables, based on opinion (Kalbuana, Suryati et al., Citation2021; Prasetyo et al., Citation2022; Scott, Citation2015) explains that earnings management is a practice in preparing financial reports that does not violate generally accepted accounting principles, so that it can increase or decrease accounting profit as desired by male CEOs as agents. The male CEO as a company agent knows more about company data and the company’s future prospects compared to shareholders. Research & development can be seen in the characteristics of the opportunistic attitude of male CEOs as agents with agency theory (Jensen & Meckling, Citation1976; Kalbuana, Prasetyo et al., Citation2021; Prasetyo, Aliyyah, Rusdiyanto, Suprapti et al., Citation2021). So as to provide empirical evidence of the role of earnings management in mediating the influence of male CEO masculinity on research & development. The empirical findings can complement the literature to provide empirical evidence that the role of earnings management in mediating the influence of male CEO masculinity on research & development has never been done empirically before, thus providing empirical evidence in Indonesia. Previous research (Almor et al., Citation2020; Prasetyo et al., Citation2021b; Prasetyo, Aliyyah, Rusdiyanto, Syahrial et al., Citation2021) explains that gender has a negative effect on research & development, while (Jia, Van et al., Citation2014; Luwihono et al., Citation2021; Prasetyo, Aliyyah, Rusdiyanto, Syahrial et al., Citation2021) explains that the masculine face of male CEOs has a positive effect on earnings management.

Previous research was conducted in the United States (Jia, Van et al., Citation2014; Shabbir et al., Citation2021; Susanto et al., Citation2021) with empirical findings explaining that the facial masculinity of male CEOs has a positive effect on earnings management, while (Kamiya et al., Citation2018a; Prabowo et al., Citation2020; Rusdiyanto et al., Citation2021a) explains the findings in terms of empirically that the CEO’s facial masculinity has a positive effect on leverage. Whereas in Indonesia the research period from 2016 to 2021 (NF Asyik et al., Citation2022; (Juanamasta et al., Citation2019; Rusdiyanto et al., Citation2021b) provides empirical evidence that the masculine face of male CEOs has a negative effect on leverage, the findings are different from the findings (Kamiya et al., Citation2018a; Susilowati et al., Citation2022; Yuhertiana et al., Citation2022). This means that the higher the masculinity of the male CEO’s face has an impact on reducing leverage, and vice versa, the lower the facial masculinity of male CEOs has an impact on increasing leverage. It is hoped that the empirical findings will have implications for regulators and corporate governance policy makers regarding male face size as a determinant of earnings management practice policies and research & development policies.

The face of masculinity is a concept of masculine behaviour that exists in men with implications for aggressiveness; having a complex character tends to be emotional to perform actions (Jewitt, Citation1997; Yuhertiana, Arief et al., Citation2020; Yuhertiana, Izaak et al., Citation2020). The face of male CEO masculinity correlates with testosterone, hostility and social status affects earnings management practices and investment research & development (Tanjaya & Santoso, Citation2020; Yuhertiana, Purwanugraha et al., Citation2019; Yuhertiana, Rochmoeljati et al., Citation2020). The face of masculinity has factors that can affect the performance of a male CEO in managing a company (Kamiya et al., Citation2018a; Yuhertiana, Arief et al., Citation2020; Yuhertiana, Izaak et al., Citation2020). The characteristics of a male CEO with a masculine face affect the company’s financial management process (Kamiya et al., Citation2018b; Yuhertiana, Purwanugraha et al., Citation2019; Yuhertiana, Rochmoeljati et al., Citation2020). The face of masculinity is a personal aspect; the face of a person’s masculinity is carried from birth. The neuroendocrinology literature explains that the face of masculinity in men predicts masculine behaviour habits and aggressive behaviours (Kamiya et al., Citation2018b; Yuhertiana, Bastian et al., Citation2019; Yuhertiana, Purwanugraha et al., Citation2019). The masculinity face of a tall male CEO can be expected to be more aggressive in managing the company (Priono et al., Citation2019; Rahma et al., Citation2016; Tanjaya & Santoso, Citation2020).

The characteristics of a male CEO positively affect the company’s decision-making process (Bertrand & Schoar, Citation2003; Tatiana & Yuhertiana, Citation2014; Yuhertiana, Citation2011a). Characteristics of male CEOs have a confident nature and often practice earnings management. The overconfidence nature of the characteristics of male CEOs often carries out earnings management (Graham et al., Citation2013; Kamiya et al., Citation2018a; Malmendier & Tate, Citation2005), Acquisition (Doukas & Petmezas, Citation2007; Kim, 2013; Kamiya et al., Citation2018a), innovation (Hirshleifer et al., Citation2012; Kamiya et al., Citation2018a). Research in neuroendocrinology explains that a man’s face affects aggressive behaviour. The face of male masculinity affects aggressive behaviour (Carré & McCormick, Citation2008; Christiansen & Winkler, Citation1992; Yuhertiana, Citation2011a). The face of masculinity affects male behaviour (Campbell et al., Citation2011; N F N F Asyik et al., Citation2022; Wahidahwati & Asyik, Citation2022). Characteristics of male CEOs tend to negotiate for personal gain (Dewianawati & Asyik, Citation2021; Wijaya et al., Citation2020; Wong et al., Citation2011). Men who have a high face of masculinity are considered trustworthy (Stirrat & Perrett, 2010; Maulidi et al., Citation2022; D A Nuswantara, Citation2023). The characteristics of male CEOs who have a higher masculinity face have better performance than male CEOs who have a lower masculinity face (Kamiya et al., Citation2018a; Haan et al., Citation2017, & Park, 2017; Wong et al., Citation2011).

The characteristics of male CEOs in the application of accounting methods between capitalising and charging research &development expenditures affect earnings management; companies tend to capitalise on research &development (1) companies have high debts, (2) companies have low-interest guarantee ratios, (3) companies have high dividend ratios or dividend payment limitations (3) high company leverage to shareholders in composition working capital (Daley & Vigeland, Citation1983; Ahmed et al., Citation2022; D A D A Nuswantara & Maulidi, Citation2021). Research &development correlate with earnings management (Lobo & Zhou, Citation2001; IRIANI et al., Citation2021; D A D A Nuswantara et al., Citation2018). Earnings management effect the capitalisation of research & development (Markarian et al., Citation2008; MARIADI et al., Citation2012; Dian Anita DA Nuswantara & Maulidi, Citation2017). The company’s decision to capitalise on research &development relates to earnings levelling (Hendrati et al., Citation2023; MARIADI et al., Citation2012; Markarian et al., Citation2008). This study seeks to provide empirical evidence of the role of profit management in mediating the influence of male CEOs’ masculinity on research & development.

Research provides clear and focused boundaries. This study is an issue on the importance of the masculinity of male CEOs as the root of the problem with research &development. The research was limited to companies listed on the Indonesia Stock Exchange from 2017–2021. Research limits to analysing the facial variables of male CEO masculinity, research &development and earnings management. Male CEO masculinity face variables are measured using ImageJ software.

2. Literature review and hypothesis development

2.1 Agency theory

Agency theory is a consequence of the separation of control agents who have direct access to company information data compared to the principal (Jensen & Meckling, Citation1976; I M; Hendrati & Fitrianto, Citation2020; I M; Hendrati & Taufiqo, Citation2020) explained that the relationship or contract between the agent and the principal is to delegate authority to the agent to manage the company. The goal of the agent and the principal should be the same, to increase the company through the prosperity of the principal, but sometimes the agent has thoughts that are contrary to those of the principal (Mayangsari, Citation2001; I M; Hendrati et al., Citation2019). Agency theory uses three assumptions about human nature, namely: (1) humans are generally self-serving, (2) humans have limited thinking about future perceptions and (3) humans are always risk averse (Eisenhardt, Citation1989; Sabihaini et al., Citation2018, Citation2020). The nature of male CEOs influences policy making, earnings management practices, and research & development. So that the role of agency theory provides an important solution in the decision-making process on the characteristics of male CEOs on earnings management practices and research & development.

2.2 Behavior consistency theory

According to (Epstein, Citation1979; Sabihaini & Prasetio, Citation2018; Sabihaini et al., Citation2018; Saleh et al., Citation2017) explains that the facial masculinity of male CEOs correlates with testosterone, aggressive, and social status affects leverage, seen from the perspective of behavioral consistency theory. He also discusses how behavioral consistency could be used to predict a majority of people within a given time span. The theory of behavioral consistency is assumed to be the opinion of a person’s ability to affect issues that trigger emotions to emerge; consistency of behavior can be shown as a particularly selected subject; consistency of behavior is described in the study with the title: “The Stability of Behaviour: I. Predicting Most of the People Much the Time (Epstein, Citation1979; Sabihaini & Prasetio, Citation2018; Sabihaini et al., Citation2018).

2.3 Face, testosterone and behavior

Previous studies have provided empirical evidence of a link between testosterone and masculine behaviour. The CEO’s face can be the basis for the interconnectedness of the male face to be a topic in this study. A man’s face can predict masculine behaviour (Jia, Van et al., Citation2014; (Saleh et al., Citation2017). Based laboratory evidence (Carré & McCormick, Citation2008; Christiansen & Winkler, Citation1992) explains that men’s faces predict having an aggressive nature. The practice of earnings management with the face of a male CEO has a relationship with masculine behaviour (Adi et al., Citation2022; Jia, Van et al., Citation2014; Sudaryanto et al., Citation2021).

Men’s faces positively affect masculine behavior, while testosterone tends to practice earnings management (Eisenegger et al., Citation2010; Jia, Van et al., Citation2014). The relationship between testosterone and the behaviour of male CEOs affects the brain both before birth and during the growth period (Hanim et al., Citation2019; Jia, Van et al., Citation2014; Sudaryanto et al., Citation2020). A group of nerve cells plays a role in-memory processing and emotional reactions as mediators between testosterone in brain regions to evaluate social interactions (Bos et al., Citation2012; Jia, Van et al., Citation2014).

Testosterone regulates growth acceleration in adolescents (Johnston et al., Citation2001; Putri & Sudaryanto, Citation2018; Sudaryanto et al., Citation2019). Testosterone affects adolescent growth (Jia, Van et al., Citation2014; Verdonck et al., Citation1999). Previous studies have provided evidence empirically that male and female development differs in the bizygomatic (between the left cheekbone to the right cheekbone), but for the height of the upper face, there is no difference in the growth period (Jia, Van et al. (Citation2014). The findings empirically prove that testosterone affects male facial development (Folstad & Karter, Citation1992). A man’s face affects masculine behaviour during infancy (Alrajih & Ward, Citation2014; Jia, Van et al., Citation2014). There is a relationship between testosterone and the ratio of the width of the male face (Lefevre et al., Citation2013). Several studies have proven the existence of a positive relationship between the percentage of male face width to testosterone. Previous research explained that testosterone has a positive relationship with facial development (Lefevre et al., Citation2013). Higher or lower testosterone in men affects the masculine face (Jia, Van et al., Citation2014; Pound et al., Citation2009).

2.4 The face of male CEO masculinity and earnings management

Previous research explained that the face of masculinity of male CEOs has a positive effect on earnings management practices (Jia, Van et al., Citation2014). Development of research that links accounting practices with the characteristics of top management (Fee et al., Citation2013; Bolton & Bruunermeier, 2008; Jia, Van et al., Citation2014). The development of research in accounting, finance, and economics extends to the characteristics of male CEOs in the company’s policy-making process (Fee et al., Citation2013; Bolton & Bruunermeier, 2008; Jia, Van et al., Citation2014).

The characteristic role of male CEOs affects the process of presenting the company’s financial statements (Bertrand & Schoar, Citation2003). The characteristic function of male CEOs positively affects profit management practices (Bamber et al., Citation2010; Brochet et al., Citation2011; Dyreng et al., Citation2010; Feng et al., Citation2011; Ge et al., Citation2011; Jia, Van et al., Citation2014). The characteristics of male CEOs affect the resulting incentive results (Chava & Purnanandam, Citation2010; Jia, Van et al., Citation2014). Characteristics of a particular male CEO having excessive confidence in carrying out profit management practices (Dikolli et al., Citation2012; Jia, Van et al., Citation2014). The face of masculinity of male CEOs positively affects earnings management practices (Jia, Van et al. (Citation2014).

2.5 Research hypothesis

2.5.1 The role of earnings management mediates the influence of facial masculinity of male CEOs on research & development

Agency theory explains the relationship that occurs between the characteristics of male CEOs as agents who function as company managers and shareholders. The male CEO as an agent will be given authority in making corporate decisions. The goal of agency theory is to fulfill the company’s desire to maximize and increase shareholder value (Jensen and Meckling (Citation1976). Motivational characteristics of male CEOs as agents to practice earnings management to increase firm value by increasing earnings (Indriani et al., Citation2014). People are naturally self-centered, limited in their capacity to foresee, and averse to risk, agency theory explains (Eisenhardt, Citation1989) The assumptions about human nature indicate that the nature of male CEOs influences the decision making of earnings management practices as well as research & development.

According to (Epstein, Citation1979) explains that male CEO facial masculinity correlates with testosterone, aggressiveness, and social status can affect earnings management and research & development, seen from the perspective of behavioral consistency theory, also discusses how behavioral consistency can be used to predict the majority of people in the range certain time. The theory of behavioral consistency is assumed as an opinion about a person’s ability to influence issues that trigger emotions; behavioral consistency can be demonstrated as a specially selected subject; Behavioral consistency is explained in a study entitled: “The Stability of Behavior: I. Predicting Most of People Much the Time (Epstein, Citation1979).

Previous research explained that the face of male CEO masculinity has a positive effect on earnings management (Jia, Van et al., Citation2014). The beginning of masculinity of male CEOs positively affects earnings management through masculine behaviour seen from the theory of behavioral consistency’s point of view (Epstein, Citation1979). Earnings management is a safe manipulation of company financial statement data because earnings management activities are legitimate and do not violate generally accepted accounting principles (Scott, Citation2015). The decision of the male CEO characteristic to carry out earnings management is data manipulation in the process of presenting financial statements (Becker, Citation1968). The face of masculinity of male CEOs positively affects earnings management practices through masculine behaviour (Jia, Van et al., Citation2014).

The company capitalises on research & development to achieve profit targets. Capitalisation of research & development is one of the common ways that male CEOs flatten their earnings are (CitationNelson et al., MARIADI et al., Citation2012). His findings explained that the low coefficient of determination indicates the low cost of research &development companies in Indonesia (MARIADI et al., Citation2012). Based on his findings (MARIADI et al., Citation2012) explained that only a small percentage of companies in Indonesia carry out research &development activities and have not become an obligation, so the selection of accounting methods for research & development is only an immaterial policy that does not significantly affect the company’s earnings (MARIADI et al., Citation2012; Suharli & Arisandi, Citation2009)

Based on the description above, earnings management is a behaviour carried out by the characteristics of a male CEO as an agent to manipulate revenue without violating the generally accepted rules of accounting principles (Chandrasegaram et al., Citation2013). The practice of earnings management is expected to be able to mediate the positive influence of the masculinity of male CEOs on Research & Development. The hypothesis proposed is as follows:

H1: Earnings Management Mediates the Positive Influence of a fWHR Male CEO’s On Research & Development.

2.6 Research conceptual framework

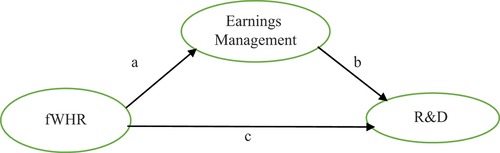

The conceptual framework explains the influence between independent and dependent variables, the mediator variables used in this study. Research places the face of male CEO masculinity as an independent variable, research &development as a dependent variable, and earnings management as a mediator variable. Based on the explanation above, the conceptual framework of the study can be described as follows as shown in :

Figure 1. Conceptual framework of Reseach.

3. Research methods

3.1 Types and approaches to research

This study uses a quantitative approach to provide meaning about the interpretation of statistical figures (Aliyyah, Prasetyo et al., Citation2021a; Prasetio et al., Citation2021). This study aims to provide empirical evidence of the role of earnings management in mediating the effect of male CEO’s facial masculinity on research & development. The research approach uses explanatory research (Endarto, Taufiqurrahman, Indriastuty et al., Citation2021; Indrawati et al., Citation2021). The population and sample in this study used all companies listed on the Indonesia Stock Exchange from 2017 to 2021. This study collected facial measurements identified as male CEOs from the Indonesian Stock Exchange website and company websites from 2017 to 2021 and take advantage of Google search. The data analysis method in this study uses Structural Equation Modeling with Stata Software. Stata software is one of the regression solving procedures that has a high degree of flexibility in research that links theories, concepts and data that can be carried out on research variables.

This study uses a sample of companies listed on the Indonesia Stock Exchange in the 2017–2021 period. The explanation of the sample in this study is as follows:

Samples of male CEO masculinity faces (fWHR). In 2017, there were 353 male CEO masculinity facial samples, while the remaining 32 were female CEO masculinity faces. In 2018, there were 356 male CEO masculinity faces, while the remaining 29 were female CEO masculinity faces. In 2019, there were 358 male CEO masculinity faces, while the remaining 27 were female CEO masculinity faces. In 2020, there were 358 male CEO masculinity faces, while the remaining 27 were female CEO masculinity faces. In 2021, there are 356 male CEO masculinity faces, while the remaining 29 are female CEO masculinity faces. So that the number of samples observed in this study for the facial variable of male CEO masculinity (X) in the 2017–2021 period totaled 1,781 samples.

Sample earnings management (EM). In 2017 the earnings management samples were 385, in 2018 the earnings management samples were 385, in 2019 the earnings management samples were 385, in 2020 the Earnings management samples were 385, in 2021 earnings management samples were 385. So that the number of samples observed in this research is for the earnings variable. management (EM) in the 2017–2021 period totaling 1,925 samples.

Research & Development Samples. In 2017 there were 34 research & development samples, while the remaining 351 companies did not include research & development. In 2018 there were 32 research & development samples, while the remaining 353 companies did not include research & development. In 2019 there were 35 research & development samples, while the remaining 350 companies did not include research & development. In 2020 there were 37 research & development samples, while the remaining 348 companies did not include research & development. In 2021 there are 32 research & development samples, while the remaining 352 companies do not include research & development costs. So that the number of research observation samples for the research & development variable (Y) in the 2017–2021 period totaled 170 samples.

3.2 Operational definitions and measurements

The face of masculinity of male CEOs is an independent variable, variable research & development as a dependent variable, and variable earnings management as a variable mediator.

3.2.1 Independent variables (fWHR)

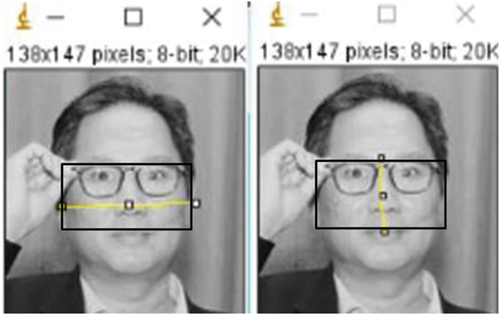

Independent variables can affect other variables. The study used the male CEO’s masculinity face variable as an independent variable. The face of masculinity is a concept of masculine behaviour that exists in men with implications for aggressiveness, has a complex character tends to be emotional in carrying out actions (Jewitt, Citation1997). Measurement of male CEO masculinity face variables using ImageJ software, research converts images of male CEOs’ faces into grayscale images with a height of 8 bits (Kamiya et al., Citation2018a).

The ImageJ software measures the distance between two points on each of the study’s male CEOs’ faces by dragging the mouse across the image; the vertical line size represents the distance between the upper lip to the highest point of the eyelid. While the horizontal line represents the maximum distance between the left cheekbone to the right cheekbone (Kamiya et al., Citation2018a). Accordingly, the study independently assigned a photo quality score between zero and three following criteria: 0: As a result of this poor posture, either one or both ears are obscured, or the photographer captures a picture of the face that causes difficulty in measuring the face’s height. 1: It appears like only half of the ear is visible since the person is leaning slightly to one side. 2: Both ears can be seen on the face, with their roots visible. 3: Proper standing or sitting posture is characterised by a straight back and ears that can be seen all the way up to the crown of the head. The study used quality scores number two and three based on guidelines (Kamiya et al., Citation2018a). The measurement scale of this study using the percentage ratio scale can be seen in the following image ():

Figure 2. Facial Width to Height Ratio (fWHR) male CEO measurement.

3.2.2 Research & Development (R&D)

Dependent variables are variables whose value cannot be influenced by other variables (Kalbuana, Prasetyo et al., Citation2021; Kalbuana, Suryati et al., Citation2021). Dependent variables in this study use Research & Development. Research & development are an investment made by the company on a new science basis to produce more efficient products based on existing resources (Tuna et al., Citation2015). Research & development are measured using the research & development intensity ratio (Arifian & Yuyetta, Citation2012; Padgett & Galan, Citation2010) with the following formula:

3.2.3 Variable mediator (Earnings Management)

Variable mediator is an intermediate variable (Kalbuana, Prasetyo et al., Citation2021; Kalbuana, Suryati et al., Citation2021) which functions to mediate the relationship between independent variables and dependent variables (Baron & Kenny, Citation1986; Mehmetoglu, Citation2018; Zhao et al., Citation2010). Variable mediator in the study using earnings management (Jia, Lent et al., Citation2014). Earnings management is a practice in the process of preparing financial statements, so that it can increase or decrease accounting earnings as desired by management. The characteristics of a male CEO as a company manager know more data about the state of the company and the company’s future prospects than shareholders (Scott, Citation2015).

Earnings management on research using model measurement (Kothari et al., Citation2005) refinement of the model (Jones, Citation1991) by including return on assets, this model adds return on assets in the calculation of discretionary accruals, so as to be able to measure profit management more accurately. The measurement scale of this study uses a percentage ratio scale. Here’s the model equation (Kothari et al., Citation2005) with the following formula:

(1) Calculating TA (total accrual) i.e. net profit for year t less operating cash flow for year t with the following formula:

The following is an estimate of total accrual (TA) using the Ordinary Least Square method:

(2) The NDA (non-discretionary accruals) are calculated using the formula above, which includes the regression coefficient.:

(3) Finally, the formula for determining DA (discretionary accruals) as a metric of profit management is as follows::

3.3 Data analysis techniques

Research data analysis is part of the data testing process after the stage of selecting and collecting research data (Sudaryanto et al., Citation2022; Utari, Citation2021). Data analysis in the study using Stata Software. Use of Stata Software on research for several reasons: The study aims to confirm existing theories and concepts using data. Stata software version 14.2 was used for this study because it can regression Structural Equation Modelling (SEM), The research model is relatively complex, because there is a proxy for profit management to act as a mediator variable to see how the role of earnings management mediates the influence of the male CEO’s masculinity face on research & development, The model that is built there is a tiered causality relationship, which has a distinctive feature, so it is expected that the mediator variable to see the relationship of the independent variable in the dependent variable.

Variable mediator is an intermediate variable, which functions to mediate the relationship between dependent variables and independent variables (Baron & Kenny, Citation1986; Zhao et al., Citation2010). Testing mediators to prove the role of profit management as a mediation variable serves to mediate the relationship between the facial variables of male CEO masculinity to research &development. Criteria for determining the influence of mediation in a relationship (Baron & Kenny, Citation1986; Zhao et al., Citation2010) explains as follows: The first equation, the independent variable must have a significant influence on the mediator variable, The second equation, the mediator variable must have a significant influence on the dependent variable, The third equation, independent variables must have a significant influence on dependent variables.

The following is a picture () that is the process of determining the type of mediator variable (Baron & Kenny, Citation1986; Zhao et al., Citation2010):

Figure 3. Relationship between independent, mediator and dependent variables (Baron & Kenny, Citation1986; Zhao et al., Citation2010).

Zhao et al. (Citation2010) conduct research by developing the types of mediator research that have been carried out previously by (Baron & Kenny, Citation1986) by identifying three patterns consistent with the mediator and two consistent patterns without a mediator as follows: Complementary mediator: the influence of the mediator (axb) and the direct influence (c) they are both genuine and orient themselves in the same broad direction, Competitive mediator: the influence of the mediator (axb) and the direct influence (c) both exist and point in opposite directions, Inderect-only mediator: there is an influence of the mediator (axb), however there is no direct impact, Direct-only nonmediation: there is a direct influence (c), but there is no indirect influence, No-effect nonmediation: no influence either directly or indirectly.

3.3.1. Descriptive statistics

Descriptive statistics are statistics that can describe the picture of the research object through analytical data, without conducting analysis (Prasetio et al., Citation2021; Utari, Iswoyo et al., Citation2021a) from data on the face variables of male CEO masculinity, variable costs of research &development, and variable earnings. Management.

3.3.2. Pearson correlation test

Pearson correlation testing is used to see the relationship between indentent variables and dependent variables by assuming Pearson correlations are normally distributed data (Prasetyo et al., Citation2021a; Rusdiyanto et al., Citation2021a). If there is any correlation between two variables, the results will be either positive (+) or negative (-). Having a positive correlation value indicates that the link is one-way. When the independent variable grows, the dependent variable also grows. This is known as unidirectional growth Correlation values that are negative signify a lack of directionality in the relationship. In other words, if the value of the independent variable is great, then the dependent variable decreases. Between 0 and 1, there is a correlation (Endarto, Taufiqurrahman, Indriastuty et al., Citation2021; Prasetyo, Aliyyah, Rusdiyanto, Kalbuana et al., Citation2021). With Pearson correlation formulations as follows:

3.3.3 Research regression model

Regression analysis to find out how close the relationship that occurs between one variable and another. Regression analysis has the function of predicting or predicting the magnitude of the value of an independent variable (Y) if the dependent variable (X) is changed (Prasetyo, Aliyyah, Rusdiyanto, Syahrial et al., Citation2021; A Rusdiyanto et al., Citation2020). A regression analysis of panel data was used to test the role of earnings management mediating the influence of the male CEO’s masculinity face (fWHR) on research & development (Y). Based on the independent variables and dependent variables that have been described, an equation model is obtained which will be used as follows:

The role of earnings management mediates the influence of the male CEO’s masculinity face on research & development”

To explain from the model of variable face masculinity of male CEOs, variable research &development costs, and variable mediators of earnings management can be explained as follows (Table ):

Table 1. Variable description

4. Results of research and discussion

4.1 Variable descriptive statistics

The results of descriptive statistics can be presented with a minimum, maximum, mean, standard deviation of the studied variable from a sample of enterprises. In addition to presenting based on a sample of companies on the Indonesia Stock Exchange in the period 2017–2021, testing this sample based on companies on the Indonesia Stock Exchange, can be seen in the below:

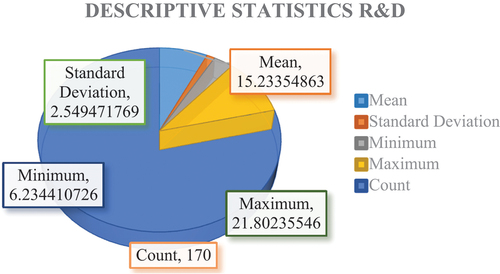

Figure 4. Descriptive statistics R&D.

Based on the above, it shows the number of observations (N) there are 170, out of 170 observations the minimum research & development cost value is 6.234411, and the maximum research & development cost value is 21.80236 the average value of 170 observations or a mean of 15.23355 with a standard deviation of 2.549472.

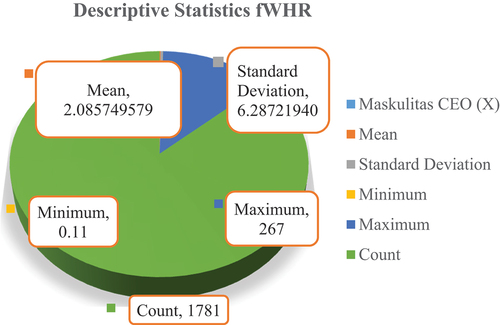

Figure 5. Descriptive statistics fWHR.

Based on the picture above, it shows the number of observations (N) there are 1781, out of 1781 observations the minimum male CEO masculinity face value is 0.11, and the maximum male CEO masculinity face value is 267. The average value of 1781 observations or mean was 2.08575 with a standard deviation of 6.287219 .

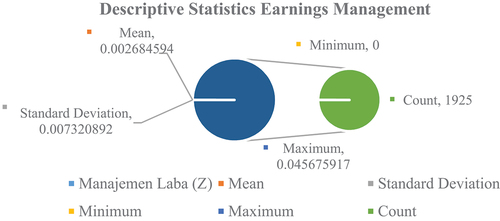

Figure 6. Descriptive statistics earnings management.

Based on the figure above, it shows the number of observations (N) there was 1925, from 1925 this observation the minimum profit management value was .0, and the maximum profit management value was 0.0456759. The average value from 1925 or mean was 0.0026846 with a standard deviation of 0.0073209.

4.2 Pearson correlation test

In the Pearson correlation test to see how strong or how weak the relationship of earnings management roles mediates the influence of the male CEO’s masculinity face on research & development. In this test, if the Pearson correlation value (r) is above 0.05 (5%), then there is a strong relationship the role of management mediating the influence of the male CEO’s masculinity face on research &development costs, if the Pearson correlation value is below 0.05 (5%) then the relationship of Earnings management role mediates the influence of the male CEO’s masculinity face on research &development is declared weak ().

Table 2. Pearson correlation test

Based on the table above, it can be interpreted that the variable of research &development, the face of masculinity of male CEOs and earnings management have a value above 0.05 (5%). Thus, it can be explained that all of these variables are declared valid to be used in model testing. The reliability test results above explain the value above 0.05 (5%). This proves that all variables used are the same reliable if tested.

4.3 Analysis mediator of Research & Development (R&D)

The process for analyzing mediation on an estimation model requires two approaches. The first approach based on (Baron & Kenny, Citation1986) is carried out several stages in analyzing the significance between the specifications of the mediation variables to strengthen the relationship between the independent variables to the dependent variables, so that it can be interpreted that the mediation variable affects in full as a mediator variable

The second approach is based on an approach (Zhao et al., Citation2010) to test mediation with multiple Tests. In the first test, an estimate of indirect impact (indirect effect) was carried out divided by the overall impact (total effect) or called the Ratio Indirect to Total Effect (RIT) which had an independent variable impact on the dependent variable mediated by the mediation variable. In the next test, an estimate of the indirect effect was carried out divided by a direct impact (direct effect) or called the Ratio Indirect Effect to Direct Effect (RID) which indicates the magnitude of the impact of the independent variable on the dependent variable mediated by the mediation variable. The last is the Sobel test, which compares p-value with z-value as the basis for the hypothesis of mediation between variables ().

Table 3. Analysis mediation Research & Development

5. Discussion of research results

Probability research results of Prob>F has a value of 0.03 ≤ 0.05 (5%) this shows that together the regression coefficient has a significant value, meaning that together the face of masculinity of the male CEO affects the cost of research &development. The value of R2 has a value of 0.0887, this shows that the degree of determination of the face of masculinity of male CEOs towards research & development is 0.0887. This means that the 0.0887 variability of research & development can be explained by the masculinity of male CEOs. The discussion of the results of the research analysis is an analysis of the suitability of theories, opinions or previous research that have been put forward by the results of previous studies to overcome phenamines in research. The discussion of the results of the research analysis is an analysis of the suitability of theories, opinions, or previous research that has been stated by the results of previous studies carried out to overcome phenamines in this study. Here are the main parts that can be discussed in the research findings as follows:

5.1. Results of discussion of earning management research mediate the influence of male CEO’s facial masculinity on Research & Development

To empirically evidence the role of earnings management mediating the impact of the male CEO’s masculinity face on research & development, this research approach uses two approaches (Baron & Kenny, Citation1986; Zhao et al., Citation2010) with the procedure of analysis of its processing using (Mehmetoglu, Citation2018):

5.2. Approach (Baron & Kenny, Citation1986) Research & Development

In the First Stage testing the face of masculinity of male CEOs positively affects earnings management practices, obtained p-value significance level values of 0.02 ≤ 0.05 (5%) in the first test were declared passed, the results of the analysis empirically the face of CEO masculinity had a positive effect on profit management practices with a significance level of 0.02, the results of this study are in line with the results of his research (Jia, Van et al., Citation2014) meaning that the increase and decrease in the masculinity of male CEOs has an impact on the increase and decrease in earnings management practices.

In the Second Stage testing earnings management positively affects research & development obtained a p-value significance level value of 0.63 ≥ 0.05 (5%) in the second test stage was declared not to pass the test the effect of earnings management on research & development inconsistent with its findings (Nelson et al.Citation2002, Mariadi et al., Citation2012) The company capitalizes on research & development in order to achieve earnings targets. Research by (Nelson et al., Citation2002, Mariadi et al., Citation2012) Proves that research & development capitalization is one of the ways that male CEOs often do in leveling earnings. The results of the research on the low coefficient of determination indicate the low cost of research & development companies on the Indonesia Stock Exchange (MARIADI et al., Citation2012). Based on the results of research consistent with the results of his research (MARIADI et al., Citation2012) Provide empirical evidence that only a small number of companies on the Indonesia Stock Exchange carry out research & development activities and have not become a liability, so that the choice of accounting method for research & development is only an immaterial policy that does not have a significant effect on company earnings (MARIADI et al., Citation2012; Suharli & Arisandi, Citation2009) So that it can be concluded in the first stage with the results of the singnifikansi p-value of 0.02 ≤ 0.05 (5%) and in the second stage with the results of the Significance Level of p-value 0.63 ≥ 0.05 (5%) is not singnifikan, meaning that the role of earnings management mediates the influence of the masculinity face of the male CEO on research & development, the results of the analysis using an approach (Baron & Kenny, Citation1986). The results of the proposed research hypothesis are supported by the hypothesis put forward by earnings management. Mediating the effect of male CEO masculinity on research & development. The results of this empirical study are included in the category Indirect mediator.

5.3. Approach (Zhao et al., Citation2010) Research & Development

5.3.1. In Testing the Ratio Indirect to Total Effect (RIT)

(Indirect effect/Total effect)/ (0.009/0.086) = 0.103, Meaning about 10% effect of the influence of the male CEO’s masculinity face on research & development mediated earnings management role.

5.3.2. In testing the Ratio Indirect Effect to Direct effect (RID)

(Indirect effect/Direct effect)/ (0.009/0.095) = 0.094, That is, the earnings management mediation effect is 0.1 times the influence of the male CEO’s masculinity face on research &development. Based on the description above, it can be concluded that the hypothesis proposed is accepted, meaning that earnings management mediates the positive influence of the male CEO’s masculinity face on research & development with a Significance Level rate of 10% using climbing (Zhao et al., Citation2010). These results support the hypothesis proposed earnings management mediates a positive influence on the face of male CEO masculinity towards research & development. Findings Empirically this is included in the Indirect Mediator category.

Empirical research results are supported by the theory of behavioral consistency which reveals that the face of male CEO masculinity correlates with testosterone, aggressiveness and social status has a positive influence on earnings management as well as research & development from the point of view of behavioral consistency theory (Epstein, Citation1979). Research & development expenditure results in a level of uncertainty in the output produced by the company. This uncertainty is the cause of the large amount of funds issued by the company which has an impact on the agency problem between the characteristics of male CEOs as agents and shareholders (Aoun & Hwang, Citation2008). Jensen and Meckling (Citation1976) provides empirical evidence that agency relationships arise when shareholders hire male CEOs as agents to provide services and then delegate decision-making authority. So that agency theory provides an important solution in making decisions on the characteristics of male CEOs on earnings management practice policies and research & development.

The company capitalizes on research & development costs in order to achieve earnings targets. Research by (Nelson et al., Citation2002, MARIADI et al., Citation2012) found that the capitalization of research & development is one of the common ways that male CEOs as agents do earnings flattening. The results of the low coefficient of determination show the low cost of research &development of the company on the Indonesia Stock Exchange (MARIADI et al., Citation2012). Based on his findings (MARIADI et al., Citation2012) explained that only a small number of companies on the Indonesia Stock Exchange carry out research &development activities and have not become an obligation, so the selection of accounting methods for research & development is only an immaterial policy that cannot significantly affect the company’s earnings (MARIADI et al., Citation2012; Suharli & Arisandi, Citation2009). Jia, Van et al. (Citation2014) provides empirical evidence that a man’s face can predict masculine behavior. While (Carré & McCormick, Citation2008) provides evidence empirically that a man’s face predicts the nature of a person’s aggressiveness. The face of the male CEO is connected with the process of presenting the company’s financial statements. Jia, Van et al. (Citation2014) provides empirical evidence of a relationship between earnings management practices and the masculinity face of male CEOs who have masculine behavior.

6. Conclusion

The practice of earnings management mediates the influence of the male CEO’s face of masculinity on research & development. The findings provide empirical evidence that earnings management practices have an impact on increasing and decreasing the masculinity of male CEOs as well as having an impact on increasing and decreasing research &development. The findings are supported by agency theory and behavioral consistency theory which explains that the face of CEO masculinity has an influence on earnings management practices and research &development.. Meanwhile, agency theory explains the characteristic role of male CEOs in making earnings management practice policies and research & development policies. The findings are empirically supported by ImageJ software that the masculinity face of male CEOs has an influence on earnings management practices and research &development.

5.1 Research implication

This research can provide some implications for theory, practice in policy making. This research provides both theoretical and practical implications:

5.1.1 Theoretical implications

The findings are empirically supported by agency theory and behavioral consistency theory explaining that the face of CEO masculinity has an influence on earnings management. While agency theory explain the role of male CEO characteristics in earnings management and research & development policy making. Empirical findings that ImageJ software supports this empirical finding that the masculinity of male CEOs has an influence on earnings management and research & development. The empirical findings provide evidence that the presence of male CEOs has an influence on earnings management and research & development decision making, supported by agency theory and behavioral consistency theory. The face describes the distinctive style of male CEOs in making earnings management policies and research & development, supported by agency theory, and behavioral consistency theory. Male CEO style can influence masculine behavior and testosterone is supported by behavioral consistency theory. The face of masculinity in the fields of Biology and Psychology explains a person’s masculine behavior supporting the theory of behavioral consistency. The face of masculinity in accounting explains that the masculinity of male CEOs has an influence on earnings management and research & development.

5.2.1 Practical implications

These empirical findings provide input for the development and improvement of corporate financial governance practices in Indonesia, particularly the practical implications: decision making on research & development spending, so that empirical findings can be used by company management and the Indonesian government as policy making in developing countries as a comparison to policies in developed countries. These empirical findings provide evidence in the field of behavioral accounting by looking at the face of masculinity as a determinant of earnings management practices as well as a determinant of research & development spending. In addition, it enriches empirical findings in the field of behavioral accounting, especially financial accounting standard number 19 and becomes a reference for future research.

5.2 Research limitations

It is impossible to escape the limitations of this investigation. In order to make this research understandable with a non-misleading interpretation, limitations are disclosed. The goal of the limits disclosure is to allow future research to fill up the gaps left by the constraints of this study: The element of conducting content analysis in determining the measurement of the face value of masculinity of male CEOs using imageJ software cannot distinguish images of male CEOs that have been modified or edited, taking pictures of male CEOs is obtained from the company’s annual report for the 2017–2021 period and the use of search image of male CEO on Google. Because the sample for this study was restricted to using images of male CEOs from firm annual reports published between 2016 and 2021 and from Google image searches of male CEOs, researchers were unable to tell apart images of male CEOs that had undergone changes.

Author’s contribution

R, S, JEP, S, HR, AN, AFS, AMRA carried out the research, wrote and revised the article R, S, JEP, R, S, HR, AN conceptualised the central research idea and provided the theoretical framework. R, S,JEP, HR, AN, AFS, AMRA designed the research, supervised research progress; R, S, S, HR, AN, AFS, AMRA anchored the review, revisions and approved the article submission.

Disclosure statement

The authors agree that this research was conducted in the absence of any self-benefits, commercial or financial conflicts and declare absence of conflicting interests with the funders.

Data availability statement

The study did not involve any data sets and the articles collected were sourced from https://www.scopus.com/ home.uri, accessed on 2022 and https://scholar.google.com/, accessed on 2022.

Additional information

Funding

Notes on contributors

Januar Eko Prasetio

Januar Eko Prasetio M.Si., Ak., CA. He earned a Bachelor of Economics degree from STIE Malangkucecwara Malang with a Bachelor of Accounting (S.E) degree, Master of Accounting Postgraduate Program from Universitas Gadjah Mada Yogyakarta Indonesia with a Bachelor Degree (M.Si), Doctor of Accounting Science Program (PDIA) from the Faculty of Economics and Business, Universitas Brawijaya Malang with the title (Dr.). His research interests include financial accounting and syariah accounting, environmental and social responsibility as well as social science and information technology research.

Sabihaini,SE., M.Si., CIIQA., CRP., CPM are AMI Auditors and Higher Education BKD Internal Assessors. She earned a Bachelor of Economics degree from Universitas Krisnadwipayana Jakarta Indonesia with a Bachelor of Management (S.E) degree, Master of Management Postgraduate Program from Universitas Gadjah Mada Yogyakarta Indonesia with a Bachelor Degree (M.Sc), Doctor of Management Science Program (PDIM) from the Faculty of Economics and Business, Universitas Brawijaya with the title (Dr.). His research interests include corporate and competitive strategy, strategic management, organizational design, supply chain management, marketing, environmental and social responsibility as well as social science and information technology research.

References

- Abadi, S., Endarto, B., Taufiqurrahman, A. R., Kurniawan, B., Daim, W., Ismono, N. A., Alam, J., Purwati, A. S., Wijaya, A., Rusdiyanto, A. U., & Kalbuana, N. (2021). Indonesian desirious finality of the community in regard. Journal of Legal, Ethical and Regulatory Issues, 24(SpecialIs), 1–26.

- Adams, R. B., & Ragunathan, V. (2017). Lehman Sisters. Working Paper, 1–57. https://doi.org/10.2139/ssrn.3046451

- Adi, S., Irawan, B., Suroso, I., & Sudaryanto, S. (2022). Loyalty-Based sustainable competitive advantage and intention to choose back at one bank. Quality - Access to Success, 23(189), 306–315. https://doi.org/10.47750/QAS/23.189.35

- Ahmed, A. A. A., Komariah, A., Chupradit, S., Rohimah, B., Nuswantara, D. A., Nuphanudin, N., Mahmudiono, T., Suksatan, W., & Ilham, D. (2022). Investigating the relationship between religious lifestyle and social health among Muslim teachers. HTS Teologiese Studies/Theological Studies, 78, 4. https://doi.org/10.4102/hts.v78i4.7335

- Aliyyah, N., Prasetyo, I., Rusdiyanto, R., Endarti, E. W., Mardiana, F., Winarko, R., Chamariyah, C., Mulyani, S., Grahani, F. O., Rochman, A. S., Hidayat, W., & Tjaraka, H. (2021a). What affects employee performance through work motivation? Journal of Management Information and Decision Sciences, 24, 1–14.

- Aliyyah, N., Prasetyo, I., Rusdiyanto, R., Endarti, E. W., Mardiana, F., Winarko, R., Chamariyah, C., Mulyani, S., Grahani, F. O., Rochman, A. S., Kalbuana, N., Hidayat, W., & Tjaraka, H. (2021b). What affects employee performance through work motivation? Journal of Management Information and Decision Sciences, 24, 1–14. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85110461420&partnerID=40&md5=4b5e50800f8866ccdd52682c4b5a73f4

- Aliyyah, N., Siswomihardjo, S. W., Prasetyo, I., Rusdiyanto, P., Rochman, A. S., & Kalbuana, N. (2021a). THE effect of types of family support on startup activities in Indonesia with family cohesiveness as moderation. Journal of Management Information and Decision Sciences, 24(1), 1–15. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85114711888&partnerID=40&md5=f222b70426b090855de34065cbb416a2

- Aliyyah, N., Siswomihardjo, S. W., Prasetyo, I., Rusdiyanto, P., Rochman, A. S., & Kalbuana, N. (2021b). The effect of types of family support on startup activities in Indonesia with family cohesiveness as moderation. Journal of Management Information and Decision Sciences, 24(SpecialIs), 1–15.

- Almor, T., Bazel-Shoham, O., & Lee, S. M. (2020). The dual effect of board gender diversity on R&D investments. Long Range Planning, 101884. https://doi.org/10.1016/j.lrp.2019.05.004

- Alrajih, S., & Ward, J. (2014). Increased facial width-to-height ratio and perceived dominance in the faces of the UK’s leading business leaders. British Journal of Psychology, 105(2), 153–161. https://doi.org/10.1111/bjop.12035

- Aoun, D., & Hwang, J. (2008). The effects of cash flow and size on the investment decisions of ICT firms: A dynamic approach. Information Economics and Policy, 20(2), 120–134. https://doi.org/10.1016/j.infoecopol.2007.12.001

- Arifian, D., & Yuyetta, E. N. A. (2012). Terhadap Tanggung Jawab Sosial Perusahaan (Corporate Social Responsibility) (Studi Empiris: Perusahaan terdaftar di BEI). Accounting, 1–30.

- Asyik, N. F., Muchlis, M., Riharjo, I. B., & Rusdiyanto, R. (2022). The impact of a male CEO ’ S facial masculinity on leverage The impact of a male CEO ’ S facial masculinity on leverage. Cogent Business & Management, 9(1), 1–19. https://doi.org/10.1080/23311975.2022.2119540

- Asyik, N. F., Wahidahwati, H., & Laily, N. (2022). The Role of Intellectual Capital in Intervening Financial Behavior and Financial Literacy on Financial Inclusion. WSEAS Transactions on Business and Economics, 19, 805–814. https://doi.org/10.37394/23207.2022.19.70

- Bamber, L. S., Jiang, J., & Wang, I. Y. (2010). What’s my style? The influence of top managers on voluntary corporate financial disclosure. Accounting Review, 85(4), 1131–1162.

- Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173. https://doi.org/10.1037/0022-3514.51.6.1173

- Becker, G. S. (1968). Crime and Punishment: An Economic Approach. Journal of Political Economy, 76(2), 255–265. https://doi.org/10.1002/9780470752135.ch25

- Benmelech, E., & Frydman, C. (2013). Military CEOs. Journal of Financial Economics, 117(1), 43–59.

- Bertrand, M., & Schoar, A. (2003). Managing with style: the effect of managers on firm policies. The Quarterly Journal of Economics, CXVIII, 118(4), 1169–1208. https://doi.org/10.1162/003355303322552775

- Bolton, P., Bruunermeier, K., & Markus, K. (2008). Economists ’ Perspectives on Leadership. Working Paper, 1–33.

- Bos, P. A., Hermans, E. J., Ramsey, N. F., & Van Honk, J. (2012). The neural mechanisms by which testosterone acts on interpersonal trust. NeuroImage, 61(3), 730–737. https://doi.org/10.1016/j.neuroimage.2012.04.002

- Brochet, F., Faurel, L., & McVay, S. (2011). Manager-specific effects on earnings guidance: An analysis of top executive turnovers. Journal of Accounting Research, 49(5), 1123–1162. https://doi.org/10.1111/j.1475-679X.2011.00420.x

- Campbell, T. C., Gallmeyer, M., Johnson, S. A., Rutherford, J., & Stanley, B. W. (2011). CEO optimism and forced turnover. Journal of Financial Economics, 101(3), 695–712. https://doi.org/10.1016/j.jfineco.2011.03.004

- Carré, J. M., & McCormick, C. M. (2008). In your face: Facial metrics predict aggressive behaviour in the laboratory and in varsity and professional hockey players. Proceedings of the Royal Society B: Biological Sciences, 275(1651), 2651–2656. https://doi.org/10.1098/rspb.2008.0873

- Chandrasegaram, R., Rahimansa, M. R., Rahman, S. K. A., Abdullah, S., & Mat, N. N. (2013). Impact of audit committee characteristics on earnings management in Malaysian public listed companies. International Journal of Finance and Accounting, 2(2), 114–119.

- Chava, S., & Purnanandam, A. (2010). CEOs versus CFOs: Incentives and corporate policies. Journal of Financial Economics, 97(2), 263–278. https://doi.org/10.1016/j.jfineco.2010.03.018

- Christiansen, K., & Winkler, E. ‐. M. (1992). Hormonal, anthropometrical, and behavioral correlates of physical aggression in !Kung San men of Namibia. Aggressive Behavior, 18(4), 271–280.

- Daley, L. A., & Vigeland, R. L. (1983). The effects of debt covenants and political costs on the choice of accounting methods: The case of accounting for R&D costs. Journal of Accounting and Economics, 5, 195–211. https://doi.org/10.1016/0165-4101(83)90012-5

- Davidson, R., Dey, A., & Smith, A. (2015). Executives’ “off-the-job” behavior, corporate culture, and financial reporting risk. Journal of Financial Economics, 117(1), 5–28. https://doi.org/10.1016/j.jfineco.2013.07.004

- Dechow, P. M., Ge, W., Larson, C. R., & Sloan, R. G. (2011). Predicting material accounting misstatements. Contemporary Accounting Research, 28(1), 17–82. https://doi.org/10.1111/j.1911-3846.2010.01041.x

- Dechow, P., Ge, W., & Schrand, C. (2010). Understanding earnings quality: A review of the proxies, their determinants and their consequences. Journal of Accounting and Economics, 50(2–3), 344–401. https://doi.org/10.1016/j.jacceco.2010.09.001

- Dewianawati, D., & Asyik, N. F. (2021). The impact of climate on price fluctuations to the income of leek farmers in Sajen village, Pacet, Mojokerto. International Journal of Business Continuity and Risk Management, 11(2–3), 247–262.

- Dikolli, S. S., Mayew, W. J., & Steffen, T. D. (2012). Honoring One’s Word: CEO integrity and accruals quality. Working Paper, 1–41. https://doi.org/10.2139/ssrn.2131476

- Doukas, J. A., & Petmezas, D. (2007). Acquisitions, overconfident managers and self-attribution bias. European Financial Management, 13(3), 531–577. https://doi.org/10.1111/j.1468-036X.2007.00371.x

- Dyreng, S. D., Hanlon, M., & Maydew, E. L. (2010). The effects of executives on corporate tax avoidance. Accounting Review, 85(4), 1163–1189.

- Eisenegger, C., Naef, M., Snozzi, R., Heinrichs, M., & Fehr, E. (2010). Prejudice and truth about the effect of testosterone on human bargaining behaviour. Nature, 463(21), 356–359. https://doi.org/10.1038/nature08711

- Eisenhardt, K. M. (1989). Agency theory: An assessment and review. Academy of Management Review, 14(1), 57–74. https://doi.org/10.2307/258191

- Endarto, B., Taufiqurrahman, K., Indriastuty, W., Prasetyo, D. E., Aliyyah, I., Endarti, N., Abadi, E. W., Daim, S., Ismono, N. A., Aji, J., Rusdiyanto, R. B., & Kalbuana, N. (2021). Global perspective on capital market law development in indonesia. Journal of Management Information and Decision Sciences, 24(1), 1–8. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85113411656&partnerID=40&md5=1074bd3526601cda4a86fbdd7b52d1bd

- Endarto, B., Taufiqurrahman, K., Indriastuty, W., Prasetyo, D. E., Aliyyah, I., Endarti, N., Abadi, E. W., Daim, S., Ismono, N. A., Rusdiyanto, J., & Kalbuana, N. (2021). Global perspective on capital market law development in Indonesia. Journal of Management Information and Decision Sciences, 24(SpecialIs), 1–8.

- Endarto, B., Taufiqurrahman, S., Setyadji, S., Abadi, S., Aji, S., Kurniawan, R. B., Daim, W., Ismono, N. A., Alam, J., Rusdiyanto, A. S., & Kalbuana, N. (2021). The obligations of legal consultants in the independent legal diligence of the capital market supporting proportion of legal prepparement. Journal of Legal, Ethical and Regulatory Issues, 24(SpecialIs), 1–8.

- Epstein, S. (1979). The stability of behavior: I. On predicting most of the people much of the time. Journal of Personality and Social Psychology, 37(7), 1097–1126. https://doi.org/10.1037/0022-3514.37.7.1097

- Fee, C. E., Hadlock, C. J., & Pierce, J. R. (2013). Managers with and without style: Evidence using exogenous variation. Review of Financial Studies, 26(3), 567–601. https://doi.org/10.1093/rfs/hhs131

- Feng, M., Ge, W., Luo, S., & Shevlin, T. (2011). Why do CFOs become involved in material accounting manipulations? Journal of Accounting and Economics, 51(1–2), 21–36. https://doi.org/10.1016/j.jacceco.2010.09.005

- Folstad, I., & Karter, A. J. (1992). Parasites, bright males, and the immunocompetence handicap. American Naturalist, 139(3), 603–622.

- Ge, W., Matsumoto, D., & Zhang, J. L. (2011). Do CFOs have style? An empirical investigation of the effect of individual CFOs on accounting practices. Contemporary Accounting Research, 28(4), 1141–1179. https://doi.org/10.1111/j.1911-3846.2011.01097.x

- Graham, J. R., Harvey, C. R., & Puri, M. (2013). Managerial attitudes and corporate actions. Journal of Financial Economics, 109(1), 103–121. https://doi.org/10.1016/j.jfineco.2013.01.010

- Haan, K. Y., Kamiya, S., & Park, S. (2017). The face of risk: CEO facial masculinity and firm risk. Working Paper, 11(4), 1–82. https://doi.org/10.1111/eufm.12175

- Han, K. Y. (2013). Self attribution bias of the CEO: Evidence from CEO interviews on CNBC. Journal of Banking and Finance, 37(7), 2472–2489. https://doi.org/10.1016/j.jbankfin.2013.02.008

- Hanim, A., Zainuri, A., & Sudaryanto, S. (2019). Rationality of gender equality of Indonesian women migrant worker. International Journal of Scientific and Technology Research, 8(9), 1238–1242. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85073422762&partnerID=40&md5=4ea7c8f29260175800e799cf7bce0936

- Hendrati, I. M., & Fitrianto, A. R. (2020). Environmental development and empowerment from industrial impact. IOP Conference Series: Earth and Environmental Science, 519(1). https://doi.org/10.1088/1755-1315/519/1/012025

- Hendrati, I. M., Heriqbaldi, U., Esquivias, M. A., Setyorani, B., & Jayanti, A. D. (2023). Propagation of economic shocks from the United States, China, the European Union, and Japan to selected Asian Economies: Does the global value chain matters? International Journal of Energy Economics and Policy, 13(1), 91–102. https://doi.org/10.32479/ijeep.13789

- Hendrati, I. M., Muljaningsih, S., Sishadiyati, S., Nadia Sasri, W., & Ekawijaya, S. (2019). Surabaya city export expansion policy analysis. Humanities and Social Sciences Reviews, 7(1), 137–146.

- Hendrati, I. M., Soyunov, B., Prameswari, R. D., Suyanto, R., & Nuswantara, D. A. (2022). The role of moderation activities the influence of the audit committee and the board of directors on the planning of the sustainability report the audit committee and the board of directors. Cogent Business & Management, 9(1), 1–20. https://doi.org/10.1080/23311975.2022.2156140

- Hendrati, I. M., & Taufiqo, F. U. K. (2020). Creative industry development model as an economic support in Surabaya. Opcion, 35(22), 1121–1134. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85083102044&partnerID=40&md5=38a28c0cb84b42a496b25bbdbbc1e172

- Hirshleifer, D., Low, A., & Teoh, S. H. (2012). Are overconfident CEOs better innovators? Journal of Finance, 67(4), 1457–1498. https://doi.org/10.1111/j.1540-6261.2012.01753.x

- Indrawati, M., Utari, W., Prasetyo, I., Rusdiyanto, I., & Kalbuana, N. (2021). Household business strategy during the COVID 19 pandemic. Journal of Management Information and Decision Sciences, 24(SpecialIs), 1–12.

- Indriani, P., Darmawan, J., & Nurhawa, S. (2014). Analisis manajemen laba terhadap nilai perusahaan yang Terdaftar di Bursa Efek Indonesia (Studi Khusus: Perusahaan Dagang Otomotif). Jurnal Akuntansi Dan Keuangan, 5(1). https://doi.org/10.36448/jak.v5i1.445

- IRIANI, S. S., NUSWANTARA, D. A., KARTIKA, A. D., & Purwohandoko, P. (2021). The impact of government regulations on consumers behaviour during the COVID-19 pandemic: A case study in Indonesia. Journal of Asian Finance, Economics and Business, 8(4), 939–948. https://doi.org/10.13106/jafeb.2021.vol8.no4.0939

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3, 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jewitt, C. (1997). Images of men: Male sexuality in sexual health leaflets and posters for young people. Sociological Research Online, 2(2), 23–34. https://doi.org/10.5153/sro.64

- Jia, Y., Lent, L., & Zeng, Y. (2014). Masculinity, testosterone, and financial misreporting. Journal-of-Accounting- Research, 3, 1–63. https://doi.org/10.1111/1475-679X.12065.This

- Jia, Y., Van, L. L., & Zeng, Y. (2014). Masculinity, testosterone, and financial misreporting. Journal of Accounting Research, 1–63. https://doi.org/10.1111/1475-679X.12065.This

- Johnston, V. S., Hagel, R., Franklin, M., Fink, B., & Grammer, K. (2001). Male facial attractiveness: Evidence for hormone-mediated adaptive design. Evolution and Human Behavior, 22(4), 251–267. https://doi.org/10.1016/S1090-5138(01)00066-6

- Jones, J. J. (1991). Earnings management during import relief investigations. Journal of Accounting Reserch, 29(2), 193–228.

- Juanamasta, I. G., Wati, N. M. N., Hendrawati, E., Wahyuni, W., Pramudianti, M., Wisnujati, N. S., Setiawati, A. P., Susetyorini, S., Elan, U., Rusdiyanto, R., Muharlisiani, L. T., & Umanailo, M. C. B. (2019). The role of customer service through customer relationship management (CRM) to increase customer loyalty and good image. International Journal of Scientific and Technology Research, 8(10), 2004–2007.

- Kalbuana, N., Kusiyah, K., Supriatiningsih, S., Budiharjo, R., Budyastuti, T., & Rusdiyanto, R. (2022). Effect of profitability, audit committee, company size, activity, and board of directors on sustainability. Cogent Business and Management, 9(1). https://doi.org/10.1080/23311975.2022.2129354

- Kalbuana, N., Prasetyo, B., Asih, P., Arnas, Y., Simbolon, S. L., Abdusshomad, A., Kurnianto, B., Rudy, R., Kardi, K., Saputro, R., Yohana, Y., Sari, M. P., Zandra, R. A. P., Pramitasari, D. A., Rusdiyanto, R., Gazali, G., Putri, I. A. J., Nazaruddin, M., Naim, M. R., & Mahdi, F. M. (2021). Earnings management is affected by firm size, leverage and roa: Evidence from Indonesia. Academy of Strategic Management Journal, 20(2), 1–12. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85107756548&partnerID=40&md5=f648ed22972be531e4986f7c43a47ad4

- Kalbuana, N., Suryati, A., Rusdiyanto, R., Azwar, A., Rudy, R., Yohana, Y., Pramono, N. H., Nurwati, N., Siswanto, E. H., Sari, M. P., Zandra, R. A., Abdusshomad, A., Kardi, K., Solihin, S., Prasetyo, B., Kurniawati, Z., Saputro, R., Taryana, T., Suprihartini, Y., & Hidayat, W. (2021). Interpretation of Sharia accounting practices in Indonesia. Journal of Legal, Ethical and Regulatory Issues, 24, 1–12. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85109955046&partnerID=40&md5=8f66a30f83e1efd68729c64f4c4bd33a

- Kamiya, S., Kim, Y. H., & Park, S. (2018a). The face of risk: CEO facial masculinity and firm risk. European Financial Management, 25(2), 239–270.

- Kamiya, S., Kim, Y. H., & Park, S. (2018b). The face of risk: CEO facial masculinity and firm riske. European Financial Management, 25(2), 1–32. https://doi.org/10.1111/eufm.12175

- Kothari, S. P., Leone, A., & Wasley, C. (2005). Performance matched accruals measures. Journal of Accounting and Economics, 39(1), 163–197. https://doi.org/10.1016/j.jacceco.2004.11.002

- Lefevre, C. E., Lewis, G. J., Perrett, D. I., & Penke, L. (2013). Telling facial metrics: Facial width is associated with testosterone levels in men. Evolution and Human Behavior, 34(4), 273–279. https://doi.org/10.1016/j.evolhumbehav.2013.03.005

- Lobo, G. J., & Zhou, J. (2001). Disclosure quality and earnings management. Asia-Pacific Journal of Accounting & Economics, 8(1), 1–20. https://doi.org/10.1080/16081625.2001.10510584

- Luwihono, A., Suherman, B., Sembiring, D., Rasyid, S., Kalbuana, N., Saputro, R., Prasetyo, B., Taryana, S., Asih, Y., Mahfud, P., Rusdiyanto, Z., & Rusdiyanto, R. (2021). Macroeconomic effect on stock price: Evidence from Indonesia. Accounting, 7(5), 1189–1202. https://doi.org/10.5267/j.ac.2021.2.019

- Mahiswari, R., & Nugroho, P. I. (2014). Pengaruh mekanisme corporate governance, ukuran perusahaan dan leverage terhadap manajemen laba dan kinerja Keuangan. Jurnal Ekonomi Dan Bisnis, 17(1), 1–20. https://doi.org/10.24914/jeb.v17i1.237

- Malmendier, U., & Tate, G. (2005). CEO overconfidence and corporate investment. Journal of Finance, 60(6), 2661–2700.

- MARIADI, Y., Sutrisno, S., & Rosidi, R. (2012). Motivasi Manajemen Laba Dalam Kapitalisasi Biaya Riset Dan Pengembangan. EL MUHASABA: Jurnal Akuntansi (e-Journal), 3(2).

- Markarian, G., Pozza, L., & Prencipe, A. (2008). Capitalization of R&D costs and earnings management: Evidence from Italian listed companies. The International Journal of Accounting, 43(3), 246–267. https://doi.org/10.1016/j.intacc.2008.06.002

- Maulidi, A., Shonhadji, N., Fachruzzaman, S. R., Nuswantara, P., Widuri, R., & Widuri, R. (2022). Are female CFOs more ethical to the occurrences of financial reporting fraud? Theoretical and empirical evidence from cross-listed firms in the US. Journal of Financial Crime. https://doi.org/10.1108/JFC-07-2022-0170

- Mayangsari, V. (2001). Kualitas Hubungan Perempuan Dengan Pasangan Ditinjau Dari Intensitas Hubungan Dengan Ayah. Prodi Psikologi Unika Soegijapranata.

- Mehmetoglu, M. (2018). Medsem: A Stata package for statistical mediation analysis. International Journal of Computational Economics and Econometrics, 8(1), 63–78. https://doi.org/10.1504/IJCEE.2018.088321

- Nelson, M. W., Elliott, J. A., & Tarpley, R. L. (2002). How are earnings managed? Examples from auditors. Examples from Auditors (November 2002).

- Nuswantara, D. A. (2023). Reframing whistleblowing intention: an analysis of individual and situational factors. Journal of Financial Crime, 30(1), 266–284. https://doi.org/10.1108/JFC-11-2021-0255

- Nuswantara, D. A., Fachruzzaman, M., Prameswari, R. D., Suyanto, T., Rusdiyanto, R., & Hendrati, I. M. (2023). The role of political connection to moderate board size, woman on boards on financial distress. Cogent Business & Management, 10(1), 2156704. https://doi.org/10.1080/23311975.2022.2156704