Abstract

The current study investigated the adoption of IFRS for SMEs among 800 SMEs in the northern sector of Ghana. The study specifically determined the awareness level and extent of adoption of the standard. It also assessed how coercive, memetic, normative and environmental factors influenced the adoption of standards among the SMEs. It utilized an explanatory research design that adopted a quantitative approach to analyzing data and making inferences. Adapting a close-ended questionnaire, the PLS-SEM was used in analyzing the data. The study revealed that the majority of SMEs were aware of IFRS for SMEs in financial reporting to a high extent. The study further found that most SMEs did not fully comply to the IFRS for SMEs in preparing and presenting financial statements. Again, Coercive isomorphism and Environmental factors positively influenced the adoption of IFRS for SMEs among SMEs in the northern sector of Ghana. In contrast, mimetic and normative isomorphism played no significant role in the adoption process. The study further found that level of compliance positively moderates the effect of the level of Awareness on IFRS for SME adoption. Challenges associated with IFRS for SMEs (COF) positively influenced its adoption.

PUBLIC INTEREST STATEMENT

SMEs are expected to prepare financial reports to their users just like other “big” entities do. The criteria for preparing the financial reports of these SMEs are straightforward and simple as they use the IFRS for SMEs as a guide. The accounting body known as IFAC set up this IFRS for SMEs so SMEs will find it easy to report their financial statements in the appropriate manner. This aim was not achieved as SMEs did not fully adopt the standard although they were aware of the standard and its requirements. Again, some environmental factors and some regulatory forces (coercive) had a positive influence on the adoption of the standard. On the other hand, SMEs do not mimic other firms who adopted the standard in the preparation of their financial reports. Again, the existence of professional bodies had little to do with the adoption of the standard among SMEs.

1. Introduction

Small and Medium Enterprises (SMEs) have proven over the years to be very crucial to the development of every economy. Globally, they have contributed significantly to emerging economies’ production capacity and provided employment and a source of income to individuals and households (Cobbinah et al., Citation2020; Olango, Citation2014). Their activities have contributed significantly to the gross domestic product of nations through their manufacturing activities, import, export, and other economic activities (Dhliwayo, Citation2017). A summary of their economic activities and contributions is mainly seen in their periodic financial reports prepared for their stakeholders. These financial reports are expected to follow a specific standardized format.

Considering the crucial role SMEs play and the necessity of their reporting to stakeholders, the International Accounting Standard Board (IASB) developed a unique International Financial Reporting Standard (IFRS), IFRS for SMEs to enhance the reporting of their economic activities. This standard was aimed at helping to coordinate and standardize their reporting style and presentation of SMEs financial activities and reduce the complexity of adopting the full IFRS that IFAC member countries were required to comply with.

Over the years, small companies have expressed concerns that complete IFRS are beyond their needs and capabilities, giving the IASB the legitimacy to develop a “less complicated” standard that will meet the needs and capacity of the smaller firms (IASB, 2016). The standard-setting process for SMEs began in 2001 and became an official document published in October 2009 (IASB, Citation2009), with the most recent update in 2015 (IASB, Citation2016). The IASB, ever since then, has been working on making the standard easy to adopt for most jurisdictions.

In a document issued by the Institute of Chartered Accountants, Ghana (ICAG), being the body legally mandated to coordinate the practice of accounting in Ghana, the institute stated the road map for adopting the standard. The institute required SMEs to commence the adoption process for financial periods ending on or after 31 December 2013. The institute further gave a two-year moratorium which extended the compliance date to financial periods ending on or after 31 December 2015. It can be inferred that; SMEs in Ghana would have gotten enough time to study the detailed requirement of the standard and are fully complying with it.

Before the introduction of this standard, many local SMEs complained about the rigidity of the full IFRS and their inability to comply with it and even the Ghana National Accounting Standard (GNAS), which appeared to be less sophisticated (Bunea-Bontas et al., Citation2011; Onalo et al., Citation2014). It was based on some of these complaints that led the IASB to come out with the IFRS for SMEs, expecting full compliance from them. Surprisingly, the case in the Ghanaian setting appears to be different from the expectations of many.

Empirical evidence within Ghana suggests that most SMEs have challenges adopting the standard, leading to a non-adoption. The few that adopted, only did that partially (Arhin et al., Citation2017; Mawutor et al., Citation2019). According to Mawutor et al. (Citation2019), many of these SMEs indicated that they need to learn this standard and its demands, making it impossible to adopt. On the other hand, some studies (Abakah, Citation2017; Rudzani & Charles, Citation2016) suggested that SMEs within certain parts of the country complied with the standard’s requirements to some extent. This current study is aimed at resolving the controversy in the literature. Again, these studies were conducted in regions distant from the northern sector of the country. Close to a decade after the full adoption of the standard, there appears to be little information about the SMEs in the northern sector (the five northern regions) of Ghana regarding the adoption of this standard. Meanwhile, the Northern sector has experienced tremendous growth in the past decade with the emergence of several SMEs.

It is worth noting that the Northern sector has the highest percentage share of employment by micro, small and medium enterprises in Ghana, exceeding the national average rate (Amoah & Amoah, Citation2018). Despite being regarded as one of the poorest regions in the country, Tamale, the business hub for the northern sector, is said to be one of the fastest-growing cities in West Africa in recent years (World Kentucky, Citation2020). To the best of the researchers’ knowledge, this is the only study assessing the adoption of IFRS for SMEs within the Northern sector of Ghana. Also, this study provides insights on the adoption of IFRS for SMEs in the Northern sector of Ghana. Again, it highlights the importance of IFRS adoption for SMEs in improving their financial reporting and facilitating access to capital, investment and other financial resources. Finally, it helps regulators and policy makers to develop effective strategies to support the adoption of IFRS by SMEs in the region.

It, therefore, becomes imperative to assess the level of adoption of the standard by SMEs within the Northern sector of Ghana. The study specifically aimed to determine the awareness level of the IFRS for SMEs among SMEs; the extent to which IFRS for SMEs is applied among SMEs and how the determinants of IFRS for SMEs influence the level of adoption in the Northern sector of Ghana. The study further assessed whether the challenges associated with IFRS for SMEs significantly influence its adoption and whether the challenges associated with IFRS for SMEs positively influenced the level of awareness in the Northern sector of Ghana.

2. Literature review

2.1. Theoretical review: institutional theory

The institutional theory was judged suitable for this investigation. Several research attempting to explain the institutional theory have focused on the adoption of international accounting standards and international financial reporting standards (Aboagye-Otchere & Agbeibor, Citation2012; Judge et al., Citation2010; Mbawuni, Citation2018). The institutional theory aims to provide a more comprehensive, inter-organizational framework for understanding organizational behavior’s mechanisms, causes, and effects (Carroll, Citation2016). In the research conducted by Judge et al. (Citation2010), the institutional theory was used to demonstrate that companies must comply with society’s standards of an acceptable practice to get the continual support they need for existence from their essential stakeholders. This is a widely acknowledged theory that emphasizes coherent isomorphism and legality. Also, it is the dominant approach to understanding organizations. According to the institutional theory of organizations, the analysis of the structure and behavior of organizations revolves around institutions.

The institutional theory examines how institutions, techniques, norms, and practices establish effective procedures for social behavior by delving into the sturdy and profound aspects of social structure. The various elements of institutional theory explain how these fundamental ideas are accepted and modified over time. Scholars in the field of accounting have emphasized that the theory is an excellent tool for discussing issues regarding adopting accounting standards. In this case, it becomes a conducive theory in the current study as it deals with adopting IFRS for SMEs among SMEs. Although John Meyer and Brain Rowan introduced the theory in the late 1970s, an article by Paul DiMaggio and Walter Powell in 1983 introduced the idea of institutionalized fields and identified three isomorphic pressures; coercive isomorphism, mimetic isomorphism, and normative isomorphism (Carroll, Citation2016).

The root of coercive isomorphism is strong external organizations that coerce one organization or institution to embrace a particular practice. It manifests as severe or lenient pressure exerted on an institution by other, more powerful institutions that govern it or by the social milieu in which it functions. Certain institutions that provide supervisory roles in the accounting field may compel SMEs to adopt accounting standards and practices. In Ghana, the registrar of companies and the Ghana Enterprise Agency requires SMEs to submit periodic financial reports. Some of these reports are mandatory for the registration processes, while some are needed for tax purposes. These reports must be prepared in a particular standardized manner which demands the adoption of the IFRS for SMEs standard.

For mimetic isomorphic pressure, it deals with instances where organizations imitate others that appear to be successful and legitimate within their environment (DiMaggio & Powell, Citation1983). Most firms are quite similar in operation. Hence, it becomes easy for upcoming ones to copy from the already-established ones. According to El-Gazzar et al. (Citation1999), firms overseeing who happen to be pioneers of the adoption of the accounting standards are sometimes imitated by the local players, especially those hoping to toe the same success line of these foreign institutions. Along the same line, Foreign Direct Investments (FDI) have been a significant factor in influencing the international standards that are qualified within a country. The study area (northern sector of Ghana) is receiving a significant influx of several multinational organizations due to the high prospect of growth within the sector, which has led to eruption of several firms. These firms are likely to be influenced to operate in a particular manner, especially in the context of collaboration which will compel the local SMEs to adopt some of these accounting standards to match up with their collaborators.

The last isomorphic pressure relates to communal ideals that produce uniformity of thinking and action in institutional settings. This is called normative isomorphic pressure. It results from the professionalization of members of a profession, which takes the form of formal schooling and cross-organizational professional networks. Professionalism insists that practitioners conform to specified rules of ethics and professional practice recommendations. This is often accomplished via the development of social groups in which workers discuss professional-related ideas. In the case of the Ghanaian economy, the ICAG occasionally arranges continuing professional development for chartered accountants in the nation, which entails exchanging ideas about contemporary accounting trends. In the opinion of Guler et al. (Citation2002), the degree of a nation’s professional technical expertise correlates positively with its adaptability to accounting standards. Unfortunately, most SMEs cannot boast of these top accounting professionals working with them, as a chunk of them are with more prominent institutions. However, account personnel within these SMEs have an appreciable knowledge of accounting and hence can appreciate the need for the standard.

2.2. Conceptual review

2.2.1. The concept of SMEs

The meaning of SME has been conceptualized from different perspectives by different scholars. Ward, Citation2018) stated that individuals are permitted to perceive their definition and understanding of SME as the term appears to be broad and abstract. Several scholars believe that the concept of SME varies from country to country and industry to industry (World Bank, Citation2017). Some authors indicated that defining a firm as an SME largely depended on some criteria, such as the number of employees, financial strength, size, capital, and sales value, among others. The European Commission based its criteria on the number of employees. They stated that firms with 0 to 9 employees are micro firms, 10 to 99 are small firms, and 100 to 499 are medium firms (Amoah & Amoah, Citation2018). Using the number of employees as a criterion, the United Nations Industrial Development Organization defined an SME in developing countries as a firm having between 5 and 19 employees as small firms and between 20 to 99 employees as medium firms (Ackah & Vuvor, Citation2011).

In Ghana, the definition of SMEs varied from time to time and according to institutions (Oppong et al., Citation2014). The National Board for Small Scale Industries (NBSSI) gave its criteria for defining SMEs. They used the number of workers and the value of the firm’s assets as the basis for the classification. According to them, a micro firm has between 1 to 5 employees and an asset value of less or up to US$ 10,000. For small firms, an employee range of 6 to 29 and an asset value of up to US$ 10,000. A firm with employees ranging from 30 to 99 and an asset base of US$ 10,000 was classified as a medium firm, while a large firm had to deal with employees of 100 and more with an asset base of US$ 10,000. Zaato et al. (Citation2020) also confirmed and conceptualized the definition according to the NBSSI.

Additionally, the Ghana Statistical Service (GSS) classified an SME based on the company’s number of workers. GSS defined SME as any company or commercial entity employing between one and five people as micro, between six and thirty as small, thirty-one and one hundred as a medium, and more than one hundred as a big enterprise. Other definitions that painted a different image came from the Registrar General’s Department, the Statistical Service of Ghana, and the Venture Capital Fund Act of 2004 (Act 680).

This research followed the IASB’s definition of SMEs. According to the IASB (Citation2009), small and medium-sized enterprises are non-accountable organizations that publish financial statements for external consumers. These external users include proprietors who are not actively engaged in the firm’s day-to-day operations, present and potential creditors, and credit rating organizations. IASB (Citation2009) states that a business has public responsibility if its debt or equity instruments are publicly traded or if it is in the process of issuing such instruments additionally, if it handles assets in a fiduciary position for a large group of outsiders as one of its core operations, such as banks and insurance organizations.

2.2.2. IFRS for SMEs

Considering the complex nature of the full IFRS, several SMEs realized it was challenging and costly to comply fully. The IASB began the standard-setting procedure in 2001. A working group of specialists was formed to offer input on the difficulties, alternatives, and possible solutions. The IFRS foundation’s trustees indicated their support for the IASB’s work to study difficulties unique to emerging economies and small and medium-sized businesses in 2002. The IASB established preliminary and tentative opinions regarding the general approach it would take in drafting accounting rules for SMEs between 2003 and 2004. In June 2004, the IASB released a discussion paper outlining the Board’s strategy and asking for feedback. After that, the IASB evaluated the problems highlighted by the discussion paper’s responders and decided to publish an exposure draft (International Accounting Standard Board, Citation2016).

The IASB realized in 2005 that it needed more information on future changes to the recognition and measurement principles for use in an IFRS for SMEs. As a tool for identifying possible simplifications and omissions, a questionnaire was produced. The standard advisory council, SME working group, world standard-setters, and public roundtables discussed the questionnaire responses. To keep constituents informed, the IASB’s debates and deliberations on the exposure draft were released in 2006. In 2007, an exposure draft was produced, suggesting five categories of comprehensive IFRS simplifications and recommended implementation recommendations and conclusions. The exposure draft and a field test questionnaire were provided in five languages. Based on the replies to the exposure draft and the outcomes of the field test, the IASB re-deliberated the ideas in the exposure draft between March 2008 and April 2009. Individual jurisdictions can implement the final IFRS for SMEs whenever possible once it was released in July 2009 (International Accounting Standard Board, Citation2016).

To continually meet stakeholders’ changing demands and sustain its quality, the IASB commenced the first comprehensive review in 2012. The whole review process was fully completed in 2015. The IASB issued the amendments, and SMEs were required to operationalize it effectively on 1 January 2017. In 2019, the second comprehensive review also commenced. The review process is currently ongoing at various stages.

SMEs were recommended to use IFRS for SMEs to simplify financial statements and generate long-term economic and other advantages (Essa, Citation2018). Comparing financial reports enhances global trade and investment, and adopting international standards increases financial statement credibility for all stakeholders and makes it easier for most SMEs to get funds and loans for development and expansion (Sava et al., Citation2013). IFRS for SMEs addresses small business demands (Lubbe et al., Citation2014). These goals include simplified reporting requirements due to decreased complexity, more cost-effective and time-efficient resources to produce financial accounting records, and providing relevant, valuable information to stakeholders to improve decision-making and understanding (Sanders et al., Citation2013).

2.2.3. Adoption of IFRS in Ghana

The 1963 Chartered Accountants Act founded the Institute of Chartered Accountants (Ghana) (Act 170). It regulated Ghana’s accounting profession and set standards (IFRS Foundation, 2021). Firms have to follow ICAG’s Ghana National Accounting Standards (GNAS). The GNAS followed IAS and UKAS. Firms used this standard until 2004 when World Bank research on accounting and auditing procedures in the nation found that the GNAS was obsolete and diverged from the IAS (Abedana et al., Citation2016). Again, weaknesses were identified with the law and regulations authorizing financial reporting. It was also observed that most publicly listed firms needed to fully comply with the existing GNAS because of the incapacity to run the affairs of ICAG (Arhin et al., Citation2017).

The ICAG moved to fully adopt the IFRS due to the challenges observed and the perceived benefits associated with the use of IFRS. It was a general belief that adopting IFRS would propel high confidence among global investors in the financial reports of firms in the Ghanaian jurisdiction and promote uniformity and comparability of firms’ financial statements among various jurisdictions (Mensah, Citation2020). The ICAG agreed to adopt the International Financial Reporting Standards (IFRS) as Ghana’s national accounting standards on 1 January 2007. The ICAG Council officially declared its support for a single set of high-quality global accounting standards, reinforced in 2010 when the Institute endorsed the IFRS for SMEs Standard. All listed firms were obliged by the Ghana Stock Exchange listing regulations to submit financial statements following the GNAS published by the ICAG, which is the IFRS (IFRS Foundation, 2021).

Firms, over the period, had attempted to comply with the requirements of the IFRS. Available evidence suggested that the full impact of the standard still needed to be achieved as firms complained about the complexity. Other studies also revealed that adopting IFRS has allowed for manipulating accounting standards, thereby encouraging creative accounting and misleading reports to users. With this, the real intent of the migration from the GNAS to IFRS still needs to be fully achieved (Mensah, Citation2020).

2.3. Empirical evidence

2.3.1. Awareness and level of adoption

Modibbo et al. (Citation2015) revealed that most SMEs in Nigeria were unaware of the standard, which automatically resulted in no adoption of the standard. A similar study by Arhin et al. (Citation2017) revealed that the level of adoption of IFRS for SMEs was very low, as only 12 percent adopted the standard. Of this, only 22% have done full adoption, while 78% have partially adopted the standard. They, however, indicated that SMEs within the study area adopted other standards, such as the Ghana National Accounting Standard and the Generally Accepted Accounting Principles. Abakah (Citation2017), in a similar study, revealed a different picture of the level of adoption. Medium-scale enterprises’ level of compliance was preferably high, about 77.9%. This revelation is encouraging as it depicted that the aim of the standard is gradually being met.

On the other hand, Dhliwayo (Citation2017) revealed that most SMEs had little awareness of the standard. In affirmation of this, in their report, Mawutor et al. (Citation2019) revealed that most SMEs in the nation were unaware of IFRS SMEs. With this, they need to provide an objective view of the awareness level and the level of adoption. In a relatively recent study in Nigeria, Abraham and Adeiza (Citation2020) indicated that the costs involved in adopting the standard outweighed the expected benefits the organizations enjoy from adopting the standard. This, therefore, implied that the level of adoption was very low as most SMEs revealed that it was cost ineffective to adopt the standard.

The studies reviewed made it clear that the literature on the subject needs to be more detailed. There is yet to be a study on the subject within the entire northern sector of Ghana, although there has been an enormous contribution from SMEs within these regions of the country. Those that presented the awareness level and level of adoption needed to provide an objective view for quantification and comparison.

2.3.2. Factors influencing IFRS adoption

Institutions implement accounting standards for several reasons. Mir and Rahaman (Citation2005) believe institutional legitimization drives standard accounting adoption in institutions. Their investigation found this. The institutional theory of legitimization states that three isomorphic pressures—coercive, mimetic, and normative—influence adoption.

Coercive isomorphism involves regulatory bodies pressuring other organizations to adopt the IFRS (DiMaggio & Powell, Citation1983). According to Al-Akra et al. (Citation2009), the IASB, IMF, and World Bank have pressured Jordan to adopt the accounting standard. Judge et al. (Citation2010) reported that the IMF helped nations implement the IFRS. These international organizations have helped many nations embrace IFRS. Affirming what previous scholars have revealed, Ritsumeikan (Citation2011) stated that the IMF and others have helped implement IFRS in some jurisdictions. Also, Damak-Ayadi et al. (Citation2020) and Kossentini and Othman (Citation2014) found that enforced isomorphism promotes IFRS adoption in developing economies. Contradicting the previous scholars, Kaya and Koch (Citation2015) found that coercive isomorphism does not affect SMEs’ decision to adopt the FIRS for SMEs. This needs to be clarified about the role coercive isomorphism plays in adopting the standard. Therefore, this hypothesis was formulated;

H1a: Coercive isomorphism significantly influences SMEs’ adoption of IFRS for SMEs.

Mimetic isomorphism deals with situations where organizations imitate other organizations, they deem legitimate and successful in their operations. Scholars like Albu et al. (Citation2011) and Judge et al. (Citation2010) revealed that many multinational corporations form mimetic pressures that influence countries to adopt IFRS. Ritsumeikan (Citation2011) and Kossentini and Othman (Citation2014) concluded that mimetic isomorphic pressures influence the adoption of IFRS as it happens to be a powerful force driving the adoption rate among organizations. Sellami and Gafsi (Citation2018) also supported the claims of previous scholars by stating that more mimetic pressure encourages the rate of adoption among SMEs. Contradicting previous findings, Damak-Ayadi et al. (Citation2020) revealed that mimetic isomorphism has no influence on the adoption of IFRS for SMEs standard among SMEs. This study proposes that;

H1b: Mimetic isomorphism significantly influences SMEs’ adoption of IFRS for SMEs.

The term normative isomorphism refers to steps taken collectively by members of a profession to determine how their job should be performed. IFAC regulates the accounting profession via numerous national accounting organizations. These organizations have an impact on the adoption of international standards. In confirmation to this, Hassan (Citation2008) and Muniandy and Ali (Citation2012) found that the accounting profession helps adopt and implement accounting standards. Also, Albu et al. (Citation2011) believe that The Big Four impacts adopting accounting standards. Judge et al. (Citation2010) identified education level as another kind of normative pressure. According to them, education plays a significant role in adopting accounting standards. Kossentini and Othman (Citation2014) disputed past claims by demonstrating that professional pressure has a detrimental impact on developing nations’ adoption of IFRS. Additionally, Sellami and Gafsi (Citation2018); and Damak-Ayadi et al. (Citation2020) supported Kossentini and Othman’s assertion. Their research revealed that normative pressures had a negative but insignificant influence on SMEs’ adoption of IFRS. From the above, we anticipate that;

H1c: Normative isomorphism significantly influences SMEs’ adoption of IFRS for SMEs.

Some environmental factors influenced the decision to adopt accounting standards among SMEs. Law enforcement quality, culture, economic conditions, political system, and tax systems were revealed to be these factors (Cooke & Wallace, Citation1990; Iqbal, Citation2002; Nobes et al., Citation2008). Again, Aboagye-Otchere and Agbeibor (Citation2012) revealed that size, legal form, and the number of owners influenced the adoption of the IFRS for SMEs. Enterprise attributes such as types, profitability, and audit type can influence an enterprise’s compliance with IFRSs disclosure requirements (Abakah, Citation2017). Hence, this study assumes that;

H1d: Environmental factors significantly influence SMEs’ adoption of IFRS for SMEs.

H1e: The level of Awareness of SMEs significantly influences SMEs’ decision on IFRS adoption: Moderating the role of the level of compliance in the Northern sector of Ghana

2.3.3. Effect of Challenges of IFRS adoption on its awareness and adoption

The adoption and implementation of the IFRS for SMEs by SMEs have encountered several challenges. These challenges, in many instances, tend to impair the potential advantage of the standard. These challenges have often deterred many SMEs from adopting and implementing the standard. The few ones that adopted the standard could not achieve full compliance. Tesfu (Citation2012) revealed that the high cost of adoption, the complex nature, the lack of proper instructions from regulatory bodies for implementing IFRS, and the emphasis on fair value accounting were the challenges hampering perfect adoption and compliance. Similarly, Phan et al. (Citation2014) revealed that the cost of educating financial and managerial personnel was the challenge affecting the adoption and implementation of the standard. They also added that insufficient guidance, lack of timely translation, and limited coverage in the university curriculum affected the adoption level.

In South Africa, Rudzani and Charles (Citation2016) also made a discovery in their bid to identify the challenges of adopting IFRS for SMEs. According to them, lack of skills to implement the standard, implementation cost, and lack of knowledge about it were the main challenges associated with implementing it. A study by Arhin et al. (Citation2017) in Kumasi sought to investigate the challenges of adopting and implementing IFRS for SMEs. It was revealed that inadequate requisite skills, inadequate support from regulators and professional bodies, the complexity of the standard, and high implementation cost were barriers to smooth adoption. A similar study was conducted by Dhliwayo (Citation2017) in Zimbabwe, focusing on the significant challenges faced by SMEs in adopting the standard; IFRS for SMEs. The study revealed that little awareness of the standards, the cost of implementation, and the complexity of the standard made it difficult for adoption and implementation.

Similarly, Mbawuni (Citation2018) revealed that the most significant perceived challenge is the constant revision of IFRS and the resulting influence on the ongoing adjustment of existing accounting procedures of corporate organizations to adhere to IFRS. In the opinion of Le Thia et al. (Citation2019), the challenges facing SMEs in their quest to adopt the IFRS for SMEs are the high cost, the complexity of information disclosure, and the subjectivity of some information. Surprisingly, Abraham and Adeiza (Citation2020) in Nigeria, who investigated the same subject, revealed that continuous professional development programs (CPDP) tended to affect the adoption of the standard.

H2: The challenges associated with IFRS for SMEs significantly influence its Adoption in the Northern sector of Ghana

H3: The challenges associated with IFRS for SMEs positively affect its level of Awareness in the Northern sector of Ghana

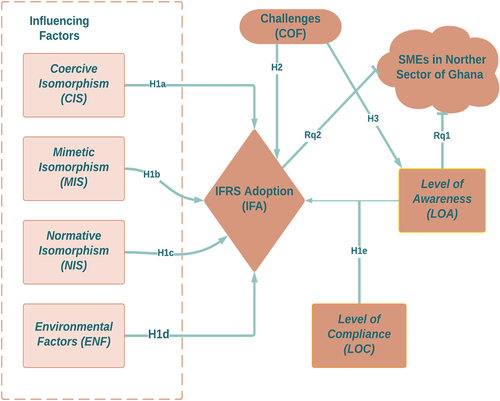

A conceptual framework was designed for the study based on the extensive literature review and the formulation of research hypotheses as shown in .

Figure 1. Conceptual framework of the study.

3. Methodology

3.1. Research design

The study adopted the explanatory research approach to investigate the level of adoption of IFRS standards by SMEs within the Northern sector of Ghana. This is an approach of utilizing quantitative methods to investigate a phenomenon that had yet to be well explained previously in a proper way (Osei-Mireku et al., Citation2020; Rahi, Citation2017; Sarpong & Sarpong, Citation2020, Sarpong, Sarpong & Asor, Citation2020). Quantitative data were collected using a questionnaire and analyzed using descriptive and inferential statistics as they were deemed suitable for the study (Kwarteng et al., Citation2021; Makwetta et al., Citation2021; T. Sarpong et al., Citation2020). The awareness level, compliance level, and the influencing factors of the accounting staff’s background on the awareness and compliance level were analyzed quantitatively.

3.2. Sampling procedure

The targeted population of the study was 2300 SMEs within the Northern sector of Ghana. These SMEs were those who have been in operation for at least five years and have been preparing financial statements for at least three consecutive years. Those responsible for handling the financial reports of these SMEs were responsible for responding to the requirement of the questionnaire. The accessible population was 1500 SMEs since most SMEs were unwilling to respond to the mail sent by the researchers to seek their prior consent. The questionnaire was sent to these SMEs, and responses were obtained from 550 within three months. A follow-up email was sent to the rest of the SMEs. Within a space of two months, 250 of them responded to the questionnaire making a total of 800 responses. This number is suitable for conducting SEM as recommendations from studies such as (Kir et al., Citation2021; Owusu et al., Citation2022) stated that a sample size between (100–150) is considered the minimum sample size for conducting SEM. Essentially, the data collection procedure took a period of 6-months (May to October 2022) to be completed.

3.3. Data collection instrument

The questionnaire was structured under six main sections; the first section gathered data related to the respondents’ background, while the other sections dealt with data relevant to addressing the research objectives in the manner they were formulated.

Five-point Likert scale questionnaire items were employed to collect data from respondents to measure the constructs under investigation. The following paragraphs explain the measurement scales in detail.

Level of Awareness (LOA): To measure the awareness of IFRS adoption, ten items were adapted for the study. The scale was adapted from Dewi’s and Dewi’s (Citation2019) studies on the awareness level of the use of IFRS by accountants and accounting students.

IFRS Adoption (IFA): The study ascertained SMEs’ level of adoption of IFRS in the northern sector of Ghana. The study adopted a 7-items on a five-point Likert scale (Cai et al., Citation2014; Tsalavoutas, Citation2009)

Level of Compliance (LOC): The study measured the Adoption of IFRS using seven items on a four-point Likert scale. This was adapted from Mnif and Znazen (Citation2020) studies and Alfaraih’s (Citation2009) studies. Respondents were asked whether they agreed to questions such as “I do not prepare accounts using the standards because they are complex to understand.”

Challenges of IFRS adoption (COF): To measure the challenges accountants face in IFRS adoption in the firms, the study adopted a 7-items on a five-point Likert scale from two central studies (Owolabi & Iyoha, Citation2012; Zakari, Citation2014).

Coercive isomorphism (CIS): Using five questionnaire items on a five-point Likert scale from Perera and Baydoun (Citation2007), the study measured Coercive isomorphism.

Mimetic isomorphism (MIS): The study further adopted five questionnaire items from Al-Omari (Citation2010) and Gelb et al. (Citation2008) to measure mimetic isomorphism.

Normative isomorphism (NIS): Regarding the measurement of normative isomorphism, five questionnaire items on a five-point Likert scale adapted from Rodrigues and Craig (Citation2007) were used.

Environmental Factors (ENF): The study assessed SMEs’ environmental factors using four questionnaire items on a five-point Likert scale adapted from the study of Aboagye-Otchere and Agbeibor (Citation2012).

3.4. Data analysis: structural modeling approach (SEM)

The study adopted Structural Equation Modeling (SEM) to analyze the three-research hypothesis formulated for the study. SEM is a popular multivariate statistical method for examining direct and indirect correlations between one or more independent latent variables and one or more dependent latent variables (Ganiyu et al., Citation2020; Gefen et al., Citation2000; Owusu et al., Citation2022). SEM can do regression analysis, route analysis, factor analysis, canonical correlation analysis, and growth curve modeling (Gefen et al., Citation2000; Urbach & Ahlemann, Citation2010). SEM helps researchers evaluate model fit and structural test models (Chin, Citation1998a; Gefen et al., Citation2000). SEM also estimates postulated structural links between constructs and measurements, making it significant. It also outperforms first-generation analytic methods (i.e., principal component analysis, factor analysis, or multiple regression). Researchers may also evaluate theory-data interactions (Chin, Citation1998b). SEM can model connections between numerous predictors and criterion variables, generate unobservable latent variables, and model measurement errors for observed variables.

SEM enables researchers to express complicated interactions between theoretical, sometimes latent, elements in a structural or theoretical model and quantify its fit with empirical data using a measurement model (Allard et al., Citation2021). PLS-SEM is more robust and can evaluate non-normal data. PLS standardization procedures convert non-normal data into central limit theorem-compliant data. Therefore, data normality is unnecessary (Beebe et al., Citation1998). Thus, the PLS-primary SEM’s goal is to evaluate and forecast the literature-based theoretical model, not to determine which alternative model fits the data better (Sosik et al., Citation2009).

4. Results and discussions

The study found that male respondents constituted 65% (n= 520), while female respondents comprised only 35% (n=280) of the study. The study further collected data on the working position of the respondents; it was found that the majority of the respondents were accounting staff, 78%(n=624), and the remaining 22%(n=176) consisted of administrators who were also familiar with the accounting records of the firm. The results revealed that the respondents were deemed fit to possess relevant information on IFRS adoption, awareness, compliance, and its use in their firms. Concerning the educational background of respondents, the majority had completed their first-degree n=408, 64 of the respondents had postgraduate degrees, while 328 had Diplomas and HND certificates. Regarding their professional background, a few respondents (n=144) were affiliated with professional bodies such as ICAG, CIMA, ACCA, and CFA. Most (n=656) of the respondents were not affiliated with any professional body. In addition, data regarding the age of the organization, we found out that (n= 608) of the respondents were graduates with 1 to 4 years, while (n=192) were between 5 or more years of work experience. The empirical results in line with the research objectives were explained in tables and figures.

4.1. Main results

4.1.1. The awareness level of IFRS for SMEs among SMEs in the Northern sector

The essence of this research question was to unravel how popular the standard was among the preparers of financial statements for the SMEs engaged in this study. The results from this section gave a clearer picture of whether or not there will be successful adoption of the standard, as the level of awareness is directly related to the level of adoption as shown in Table . The specific questions asked transcended beyond the awareness level as the respondents’ knowledge of the standard’s requirements in some instances was quizzed.

Table 1. Level of awareness of IFRS for SMEs

From the responses obtained, respondents were aware of the existence standard (M = 4.01, SD = 0.82). Respondents expressly indicated that they know the IFRS and that Ghana has adopted it. They also revealed that they appreciated the difference between the full IFRS and IFRS for SMEs (M = 4.10, SD = 0.92). This revelation was not surprising as the respondents possessed an appreciable level of knowledge in accounting. Knowledge of IFRS serves as a focal point in the curriculum of accountants at the entry-level and even at the advanced stage. Although respondents were aware of the standard, their comprehension of it could have been better though it was appreciable. Most of them were indifferent about some specific requirements of the IFRS for SMEs (M = 3.10, SD = 0.62). This revelation tends to impair the standard’s level of adoption. Research Question 2 described the extent of adoption by the preparers of the financial statement of the various SMEs within the Northern sector of Ghana.

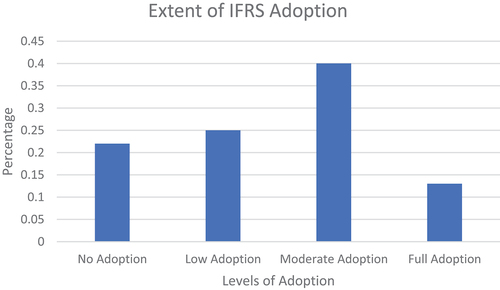

4.1.2. The extent of adoption of IFRS for SMEs in northern sector

Research Question 2 assessed the extent of adoption of the IFRS for SMEs among SMEs within the Northern sector of Ghana. Respondents were given the option to select among the options “full adoption, moderate adoption, low adoption, and no adoption.” From the data gathered, most (40 percent) of the respondents moderately adopted the standard. Twenty-five percent of the respondents adopted the standard on a low level, while 22 percent did not, with 13 percent fully adopting the standard. Although respondents possessed a high level of awareness of the standard, the extent of adoption was not at the whole level, as shown in Figure . The subsequent research objectives investigated what might have accounted for the challenge.

Figure 2. Extent of IFRS adoption.

The researchers used the information summarized in Figure to re-classify adoption into two main categories; non-adopters and adopters. Although some SMEs indicated partial adoption (low adoption and moderate adoption), it amounts to no adoption as the formulators of the standard expects SMEs not to settle for anything below “full adoption” (Mukokoma & Tushabwomwe, Citation2019). Based on this, 13 percent fully adopted the standard while majority (87%) did not.

4.2. Empirical results from hypotheses testing

The three main hypotheses were analyzed using PLS-SEM. A diagnostic test was done to assess the normality, multi-collinearity, autocorrelation, and validity and reliability of the model.

4.2.1. Test of Pre-SEM fundamental assumptions

Normality testing is one of the pre-SEM fundamental assumptions. Using skewness and kurtosis, the dataset’s normality was evaluated. Hair et al. (Citation2014) state that Z-Skewness is a crucial parameter. The PLS test was applied to identify data abnormalities after the initial data analysis. Table demonstrated that the fundamental premise of normalcy was satisfied. The excess kurtosis and skewness requirements (± 2.58 and 1.96, respectively) satisfy the normalization assumption.

Table 2. Descriptive statistics of empirical data

The study diagnosed multicollinearity. The presence of multicollinearity implies that many constructs share variances, such as high construct correlations and shared attributes (Andreev et al., Citation2009; Bagozzi & Yi, Citation2012). The study utilized VIF measures to assess multicollinearity. The VIF demonstrates how one building component affects others (Urbach & Ahlemann, Citation2010). VIFs above 10 imply high collinearity (Henseler et al., Citation2009). According to Hair et al. (Citation2014), a VIF score above 5.00 indicates significant multicollinearity, below 5.00 is moderate, and below 0.20 shows no multicollinearity. Table displays all VIF values below the 5.00 cut-off. (Hair et al., Citation2014). PLS enhanced business research for 30 years. Companies utilized PLS often between 1985 and 2010 (Hair et al., Citation2014). The correlation matrix analyzed dependent, independent, and control variable multicollinearity. Table shows discriminant validity for each valid research construct.

Table 3. Correlation matrix of the constructs

4.2.2. Measurement of the model’s validity and reliability

The research assessed model validity and consistency. The analysis measured item construct validity and reliability using factor loadings, Cronbach’s alpha, composite reliability, and Average Variance Extracted (Table ). The items scored 0.6, 0.7, 0.7, and 0.5 respectively; hence the data was deemed valid and reliable. Our theoretical model constructs were considered valid. The data constructs have good internal consistency and reliability, as shown by D.G’s Rho value (0.818–0.981 > 0.7) and Cronbach’s Alpha (0.728–0.915 > 0.7). The model’s composite reliability (CR) is 0.813–0.890 > 0.8. AVE values are (0.643 to 0.7463 > 0.5). Thus, the items were valid and trustworthy for measuring IFRS adoption drivers in Northern Ghana.

Table 4. Results of validity and reliability of items constructs

4.2.3. Discriminant validity using fornell-larcker criterial and Heterotrait-Monotrait Ratio (HTMT)

The study concluded that these prior studies demonstrated convergent validity. The discriminant validity of the model was evaluated. Table summarizes outcomes. Acceptable values are those that are less than 0.90. Fornell-Larcker Criteria-based and HTMT techniques validate the structural model. The discriminant assists the researcher in linking the dependent and independent variables of the investigation. Researchers discovered a correlation between the two concepts. In addition, discriminant validity was evaluated to determine if unrelated measures are indeed unrelated. Table displays findings for discriminant validity. According to the Fornell-Larcker criterion, the square root of the average variance recovered for each construct must be more significant than its strongest correlation with any other construct. Table demonstrates robust discriminant validity.

Table 5. Discriminant validity (fornell-larcker criterial)

The heterotrait-monotrait (HTMT) correlation ratio is becoming more common for PLS-SEM discriminant validity measurement than the Fornell-Larcker criterion and cross-loadings. The correlations’ heterotrait-monotrait ratio is a measure of discriminant validity. The HTMT matrix uses correlation absolute values (Longo et al., Citation2017). Two reflective conceptions are discriminatory if the HTMT score is less than 0.90.

4.2.4. Measurement of the model

A structural model is constructed using the path’s R2, Q2, and F2 significance. The quality of the model is defined by the strength of each structural route as measured by the R2 values for the dependent variable (Hair et al., Citation2020). The R2 should be greater than or equal to 0.1 (Falk & Miller, Citation1992). Table indicates that the R2 value is more than 0.1. Thus, predictive significance is demonstrated. Additionally, Q2 confirms the endogenous construct’s predictive significance. A Q2 value greater than 0 indicates the model’s predictive usefulness. The findings indicate that the construct’s predictions are significant (see, Table ). The purpose of model fit assessment is to validate the theoretical model using the technique of parameter fitting (Benah & Li, Citation2020; Owusu et al., Citation2022). Furthermore, the model fitness was assessed using SSMR. The value of SSMR was 0.06, thus the value is above the require value of 0.10 indicating the acceptable model fit (Hair et al., Citation2013) as shown in Table and Figure .

Figure 3. Outcome of structural model.

Table 6. Heterotrait-monotrait ratio (HTMT)

4.2.5. Significance of the model

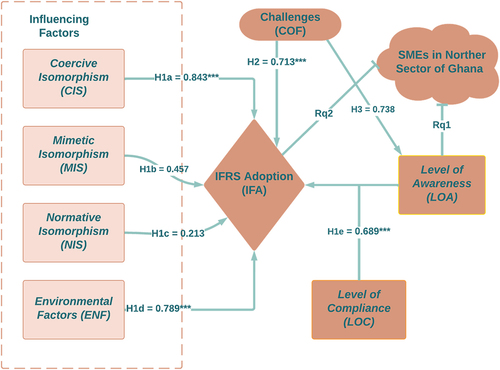

The Bootstrapping technique permits the study of the importance of the link between model components through the interpretation of t-statistics and the correlation between these constructs by comprehensively analyzing the path coefficient values. The t-statistics must be greater than 1.96 to be deemed significant (Chin, Citation1998a). Table summarizes these data. The significance of the model was first using R2, F2, and Q2. The use of R2 was to measure how the independent variables (Coercive isomorphism, Mimetic isomorphism, Normative isomorphism, and Environmental Factors) explain the variations in the dependent variable (IFRS for SMEs Adoption). In line with the findings of (Falk & Miller, Citation1992; Hair et al., Citation2020), the R2 explains the strength of each structural route as measured by the R2 values for the dependent variable. The R2 should be greater than or equal to 0.1. The R2 should be greater than or equal to 0.1. (Falk & Miller, Citation1992). Table indicates that the R2 value is more than 0.1. The study found that CIS and ENF to IFA indicates an R2 value of 0.843 and 0.789 respectively, while MIS and NIS did not have a significant impact on IFA revealed a respective R2 value of 0.457 and 0.213. This study revealed that the variables (CIS and ENF) account for more than 70% of IFRS adoption variations for SMEs in the Northern sector of Ghana. The model was further tested for its predictive accuracy using the statistical value of Q2. Additionally, Q2 confirms the endogenous construct’s predictive significance. A Q2 value greater than 0 indicates the model’s predictive usefulness (Cai et al., Citation2022). The findings indicate that the construct’s predictions are significant. The study further adopted the F2 to measure the effect size of the strength interplay path among the latent variables in the structural model (Hair et al., Citation2014). Per the findings of (Cohen, Citation1988; Hair et al., Citation2014), the effect size of >0.12 (small), >0.15 (moderate), and >0.35 (large) demonstrate as to whether an exogenous construct has a significant impact on the endogenous construct. The model revealed that F2 > 0.35, indicating a significant effect of (CIS and ENF) on IFA. The remaining sections explain the results of the hypothesis formulated for the study.

Table 7. Hypothesis testing results

4.3. Hypothesis testing

The following hypotheses were formulated and tested;

Proposition 1:

H1a: Coercive isomorphism significantly influences SMEs’ adoption of IFRS for SMEs.

The study analyzed whether the pressure mounted by a regulatory organization such as the Ghana Enterprise Agency or the registrar of companies mount of SMEs in Ghana, specifically in the Northern sector, significantly influenced their level of adoption of IFRS for SMEs. The study revealed a positive effect of Coercive Isomorphism (CIS) on IFRS Adoption (IFA) in Northern Ghana, based on the first research hypothesis. The research discovered that CIS has a statistically significant positive relationship with IFA (β1a = 0.843, t = 11.812, p < .05). The hypothesis is thus supported, as seen in Table .

H1b: Mimetic isomorphism significantly influences SMEs’ adoption of IFRS for SMEs.

In addition to the above, the study further analyzed how the mimetic behavior of SMEs in the Northern sector influenced their level of Adoption of IFRS for SMEs. Based upon the analysis of the response from the accounting staff and administrators of the SMEs involved in the study. It was revealed that Mimetic isomorphism (MIS) had no significant influence on SME’s decision to adopt IFRS for SMEs in the Northern sector of Ghana (β1b = 0.457, t = 20.126, p > .05). Other similar organizations did not influence the decision of SMEs to adopt IFRS for SMEs in the field. Successful organizations similar to SMEs do not influence how the SMEs prepare their financial reports.

H1c: Normative isomorphism significantly influences SMEs’ adoption of IFRS for SMEs.

The following section analyzed how the collective decision by SMEs belonging to IFAC influenced their choices in adopting IFRS for SMEs in reporting their financial and corporate documents. The study tested the hypothesis that NIS influenced the IFA of SMEs in the Northern sector. It was found that Normative isomorphism had no significant effect on SME’s decision to adopt IFRS for SMEs in the Northern sector of Ghana (β1c = 0.213, t = 18.130, p > .05). This revealed that professional organizations in the field of accounting do not influence the decisions of SMEs to adopt IFRS for SMEs.

H1d: Environmental factors significantly influence SMEs’ adoption of IFRS for SMEs.

The model further tested whether environmental factors such as enforcement quality, culture, economic conditions, political system, and tax systems significantly influenced SMEs adoption of IFRS of SMEs in the Northern sector. From the results, it was found that Environmental Factors (ENF) positively influenced IFRS for SMEs adoption (IFA) of SMEs (β1d = 0.789, t = 12.869, p < .05). This implies that the presence of environmental factors provides a higher chance of SMEs adoption of IFRS for SMEs in the preparation and presentation of financial reports.

H1e: The level of Awareness of SMEs significantly influences SMEs’ decision on IFRS for SMEs adoption: Moderating the role of the level of compliance in the Northern sector of Ghana

The model tested the significant mediating role played by the Level of Compliance (LOC) on the relationship that exists between an SME’s level of awareness (LOA) and IFRS for SMEs adoption (IFA). The study first conducted a mediation analysis assessing LOC’s direct and indirect effect on IFA. The results revealed a significant total effect of LOC on IFA through LOA. Details of the model revealed a significant direct effect of LOC on the IFA of SMEs in the northern sector of Ghana. The results revealed that the Level of Awareness (LOA) significantly moderates the relationship between the Level of Compliance (LOC) and IFRS adoption (IFA) ((β1e = 0.689 t = 18.612, p < .05). Therefore, supporting the hypothesis that LOC significantly moderates the effect of LOA on IFA in the northern sector of Ghana.

Proposition 2:

H2: The challenges associated with IFRS for SMEs significantly influence its Adoption in the Northern sector of Ghana

The adoption of IFRS for SMEs has faced several internal and external challenges. Most SMEs did not prepare their financial reports using the standard due to the cost associated with it. Others also failed to do so due to its complex nature and difficulty in understanding. Some were also of the view that, regulatory bodies do not provide any support. These challenges can impair the essence of adopting the standard in preparing and presenting SMEs’ financial reports. Therefore, the researchers hypothesized that the challenges SMEs faced during the implementation of IFRS influenced their decision to adopt IFRS for SMEs in their financial reports. The study found that there exists a positive effect of challenges of IFRS (COF) on IFA among SMEs in the northern sector of Ghana as shown in the model (β2 = 0.713 t = 10.939, p < .05).

Proposition 3:

H3:The challenges associated with IFRS for SMEs standard positively affect the level of Awareness of IFRS of SMEs in the Northern sector of Ghana

The last research hypothesis investigated whether the challenges of IFRS for SMEs (COF) positively influenced the LOA of IFRS among the SMEs involved in the study in the Northern sector of Ghana, as shown in Table . The study found that challenges of IFRS for SMEs (COF), such as the high cost of adopting, the complex nature, lack of proper instructions, had no significant influence on the level of awareness of IFRS for SMEs (β3 = 0.738 t = 12.639, p > .05).

4.4. Discussions

4.4.1. Awareness level of the IFRS for SMEs standard among the SMEs

From the study findings, preparers of financial statements of SMEs were aware of the existence of IFRS for SMEs on a whole. This implied that the standard was popular among SMEs within the northern sector although their level of awareness in areas such as deferred tax exemption and valuation of asset was moderate. Therefore, there is a possibility of a higher chance of adoption and compliance with the standard’s requirements as awareness of the standard is the initial step for adoption and compliance. Pais and Bonito (Citation2018) held that one key route to the effective adoption and implementation of any IFRSs is demonstrating acceptance of the standard by the complying body and familiarity with the standard.

The high level of awareness of respondents towards IFRS for SMEs, although not surprising, deviated from the propositions of other scholars investigating the matter. Aside the revelation of Modibbo et al. (Citation2015), which was confirmed by the current study, Dhliwayo (Citation2017), Mawutor et al. (Citation2019) stated that most preparers of financial statements for SMEs were not aware of the existence of the standard. Although the findings of this study deviate from them, it is not surprising because the content of the curriculum for accounting professionals expounds extensively on the standard. Due to this, the majority of account personnel are aware of the standard.

4.4.2. The extent of adoption of IFRS for SMEs

Although the respondents were aware of the existence of the standard, compliance with the standard’s requirements was not automatic. From the study, it was evident that SMEs have low compliance levels with the use of IFRS for SMEs in preparing and presenting their financial statements as majority of them are not fully adopting the standard. With this revelation, it is clear that the cause of the low compliance may be a decision by the SMEs not to fully comply with the standard for specific reasons. The majority of the respondents, who are diploma and degree holders and not ICAG members, lacked the required qualification to appreciate the need to fully comply with the standard regulating a firm’s financial reporting.

To instill public confidence, SMEs must migrate from merely keeping financial records and preparing some financial statements to preparing financial statements per the requirement of the approved standard (Amoah & Amoah, Citation2018; Musah et al., Citation2018; Nketsiah, Citation2018). This aims to ensure harmony in preparing financial statements to enable comparison to all IFAC member countries.

The results gathered on the level of compliance with the IFRS for SMEs shares the findings with other scholars who investigated a similar phenomenon. For instance, Arhin et al. (Citation2017)’s study revealed that the adoption level of IFRS for SMEs was very low, as only 12 percent adopted the standard. Their reason for the inability to adopt differed from the current study as they indicated that respondents did not possess the requisite skills to implement the standard. This study also corroborates the findings of Dhliwayo (Citation2017) and Mawutor et al. (Citation2019), who revealed low standard adoption. The low adoption was due to the low level of awareness, confirming the reason given by Arhin et al. (Citation2017).

Furthermore, the findings of this study related more to Abraham and Adeiza (Citation2020), who revealed that SMEs’ level of adoption was relatively low and attributed that to the cost of adoption. According to Abraham and Adeiza, the costs involved in adopting the standard outweighed the expected benefits the organizations enjoy from adopting the standard. This was translated into a low level of adoption and compliance with the requirement of the standard. However, this study contradicts the findings of Abakah (Citation2017), who revealed a different picture of adoption and compliance. According to them, Medium-scale enterprises’ level of compliance was preferably high, about 77.9%.

4.4.3. Factors influencing the adoption of IFRS for SMEs in the Northern Sector of Ghana

From the study, the respondents revealed that coercive isomorphism has the highest impact on adopting the standard IFRS for SMEs. This implies that the existence of specific systems and institutions coerces SMEs to implement the standard. Institutional bodies like the Ghana Enterprise Agency and the companies’ registrar regulate SMEs’ procedures in Ghana. These institutions require SMEs to present their financial statements standardized as approved by IFAC, the regulatory body for the practice of accounting. For tax, the Ghana Revenue Authority periodically conducts tax audits to ensure whether registered businesses of which SMEs are part prepared financial statements appropriately to depict their actual profit or loss.

This study confirmed the findings of other scholars who revealed that coercive isomorphism significantly influenced the adoption and compliance with accounting standards. For instance, Al-Akra et al. (Citation2009), Judge et al. (Citation2010), and Ritsumeikan (Citation2011) revealed that international bodies like the IASB, IMF, and World Bank had put pressure on Jordan to adopt the accounting standard. This was subsequently passed on to firms within the jurisdiction of the affected countries. In the case of SMEs within the northern sector of Ghana, the influence to adopt came from organizations responsible for regulating these SMEs’ operations. The current study, however, contradicted the findings of Kaya and Koch (Citation2015). According to Keya and Koch, coercive isomorphism does not affect the adoption of IFRS for SMEs.

Again, the study revealed that mimetic isomorphism does not significantly influence the adoption and implementation of IFRS for SMEs. This indicates that SMEs within the study area do not see the need to imitate other successful organizations regarding preparing financial statements in accordance with IFRS for SMEs. The probable reason may be that the study area is regarded as the most remote region within Ghana. Due to this, the presence of pioneering firms who are influential in reporting financial information in the required manner may be few there compared to the southern sector of the country. With this, their impact on SMEs’ financial statement preparation is very low.

This study’s revelation did not align with the findings of other scholars (Albu et al., Citation2011; Judge et al., Citation2010; Kossentini & Othman, Citation2014; Ritsumeikan, Citation2011; Sellami & Gafsi, Citation2018) who researched a similar concept. According to them, many multinational corporations form mimetic pressures influencing countries to adopt IFRS. They concluded that mimetic isomorphic pressures influence the adoption of IFRS as it happens to be a powerful force driving the adoption rate among organizations.

Furthermore, from the study, it was clear that normative isomorphism does not influence the adoption of IFRS for SMEs among SMEs within the northern sector of Ghana. This implies that the professional body of accountants in Ghana does not influence SMEs regarding the adoption and compliance with the requirement of IFRS for SMEs. This revelation is not surprising as most SMEs cannot boast of top accounting professionals who are members of the ICAG, ACCA, CIMA, etc, being the preparers of their financial statements. At best, most of the preparers of the financial statements for these SMEs are students of the institute who are yet to be admitted into membership. Owing to this, they need to be more keenly regulated by the professional body to stick to the standard’s requirements. Until these accountants become members of the professional accounting body, the impact of normative isomorphism will continue to be low.

This finding was in line with the revelation made by Kossentini and Othman (Citation2014) and Sellami and Gafsi (Citation2018) who investigated the impact of normative isomorphism on adopting IFRS among SMEs. According to them, professional pressure has an insignificant impact on adopting IFRS for SMEs. They revealed that professional bodies do not influence SMEs to comply with the requirement of IFRS for SMEs. This finding, however, contradicts what Hassan (Citation2008) and Muniandy and Ali (Citation2012) revealed about mimetic isomorphism in adopting IFRS for SMEs. They indicated that regulatory bodies of accounting play a very significant role in adopting accounting standards.

Finally, the study revealed that environmental factors significantly influence the adoption of FRS for SMEs. Specifically, enterprise attributes such as profitability and audit type positively influence the adoption of IFRS for SMEs. Enterprises with high-profit margins were found to conform to the accounting standard requirement. This may be because enterprises with colossal profit margins can afford the services of a chartered accountant who appreciates the need for conformance to the accounting standard. Again, these enterprises are regularly monitored by the Ghana Revenue Authority for the payment of taxes; hence they mostly prepare their financial statements in a standardized manner conformable to the requirement of IFRS for SMEs.

Also, SMEs who subject their financial statements to regular audits ensure that their financial statements are compatible with the requirements of the international auditing standard, which is similar to IFRS. This finding is in line with what Aboagye-Otchere and Agbeibor (Citation2012) revealed on the influence of environmental factors on adopting accounting standards among SMEs.

4.4.4. Challenges of IFRS on level of awareness

It was evident from the study that challenges confronting SMEs had a significant positive impact on the adoption and compliance with IFRS for SMEs. This implies that the more the challenges persist, the higher the chance for SMEs not being able to implement the standard fully. Some challenges include the high cost of implementation, the standard’s complex nature, and the standard’s time-consuming nature. These claims are in line with Tesfu (Citation2012), who revealed that the high cost of adopting, the complex nature of accounting standards, the lack of proper instructions from regulatory bodies for implementing IFRS, and the emphasis on fair value accounting were the challenges hampering perfect adoption and compliance. In the opinion of Le Thia et al. (Citation2019), the challenges facing SMEs in their quest to adopt the IFRS for SMEs are the high cost, the complexity of information disclosure, and the subjectivity of some information.

5. Conclusion and recommendation

Those responsible for preparing financial statements for SMEs have the primary requirement to fully comply with the IFRS requirement due to their awareness of the standard. This is because awareness of the standard is a precursor to adoption and compliance. Although this requirement is appropriate, it is not sufficient to warrant full adoption and implementation of the standard. Coercive and environmental factors highly influence adoption and implementation. The challenges SMEs face also influences the adoption and implementation of the standard. These forces have impaired the full adoption and compliance with the requirement of IFRS for SMEs.

Evidence from this suggests that SMEs within the Northern sector of the country do not prepare financial statements in line with the regulatory requirements. Therefore, it implies that the quality of financial statements prepared by these SMEs could be better since they must fully comply with the accounting standard regulating their operations. This also begs the question of whether SMEs are meeting the requirements of their establishment, are flouting the rules for their institutions, or whether standard enforcers are ensuring the right things are done. To achieve full adoption, regulatory bodies must regularly inspect the books of SMEs to ensure they are implementing the standard requirement. Again, they should provide support and incentives such as tax incentives, training, and technical assistance to SMEs to encourage their adoption. Financial institutions and investors should encourage SMEs to adopt the standard in order to increase their trust in the financial reports of these companies and reduce the risk of investments

The study was premised on the institutional theory, which outlines three central isomorphic pressures influencing the adoption of the standard. From this study, coercive isomorphic pressure and some environmental factors positively influence the adoption and implementation of the standard. The understanding of this is that, for SMEs to fully comply with the standard’s requirements, regulatory authorities must regularly inspect the financial records of these SMEs to ensure they stick to the IFRS for SMEs standard. Also, SMEs must be encouraged to employ the services of associates and members of ICAG to assist in preparing financial statements to attain maximum quality.

6. Limitation and area of further study

The study cannot be generalized to other parts of the country since it was based on the activities of SMEs within the Northern sector. With this, a further study could be conducted engaging all other sectors within the country to obtain a holistic picture of the status of SME’s adoption of IFRS for SMEs, nationwide. Again, using only a closed-ended questionnaire meant that the inherent limitation present within the instrument could be addressed. A further study can employ the mixed method approach to manage these limitations.

Authors contribution

Peter Sappor: Concept development, literature review and methodology. Francis Sarpong: Conceptualization, methodology, and formal analysis. Rezikatu Ahmed Seidu Seini: Proof-reading, discussion, and conclusion

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Peter Sappor

Peter Sappor is an assistant lecturer at the Department of Accounting of the University for Development Studies, Ghana. He is a researcher with peculiar interest in financial reporting, accounting education, accounting ethics, sustainability reporting, management and cost accounting.

Francis Atta Sarpong

Francis Atta Sarpongis a PhD candidate at the School of Finance, Zhongnan University of Economics and Law, Wuhan, China. His main research interests lie in sustainable accounting and finance, green financing, energy financial, green investment and financial risk.

Rezikatu Ahmed Seidu Seini

Rezikatu Ahmed Seidu Seini is an assistant lecturer at the Department of Accounting of the University for Development Studies, Ghana. She has strong research interest in audit quality, financial reporting and sustainability reporting. The researchers have a wider interest in understanding how SMEs report their financial information. This will inform how they train accounting professionals to pick up future accounting roles with these SMEs in the area of preparation of financial reports.

References

- Abakah, E. Y. (2017). Corporate compliance with international financial reporting standards (IFRS): A case study of selected small and medium-sized enterprises (SMEs) in the Cape Coast Metropolis (Doctoral dissertation, University of Cape Coast).

- Abedana, V., Omane-Antwi, K., & Oppong, M. (2016). Adoption of IFRS/IAS in Ghana: Impact on the quality of corporate financial reporting and related corporate tax burden. Abedana, VN, Omane-Antwi, KB and Oppong M. (2016), Adoption of IFRS/IAS in Ghana: Impact on the Quality of Corporate Financial Reporting and Related Corporate Tax Burden, Research Journal of Finance and Accounting, 7(8), 10–32. https://ssrn.com/abstract=2803423

- Aboagye-Otchere, F., & Agbeibor, J. (2012). The international financial reporting standard for small and medium-sized entities (IFRS for SMES). Journal of Financial Reporting and Accounting, 10(2), 190–214. https://doi.org/10.1108/19852511211273723

- Abraham, V. O., & Adeiza, M. O. (2020). Adoption of IFRSs by SMEs in Sokoto State, Nigeria: Issues, Challenges and Prospects. International Journal of Research and Scientific Innovation, 7(6), 174–180.

- Ackah, J., & Vuvor, S. (2011). The challenges faced by small & medium enterprises (SMEs) in obtaining credit in Ghana (master’s thesis in business administration, MBA programme). Digitala Vetenskapliga Arkivet(DIVA). Accessed on20 11 2022 http://urn.kb.se/resolve?urn=urn:nbn:se:bth-2408

- Al-Akra, M., Ali, M. J., & Marashdeh, O. (2009). Development of accounting regulation in Jordan. The International Journal of Accounting, 44(2), 163–186. https://doi.org/10.1016/j.intacc.2009.03.003

- Albu, N., Albu, C. N., Bunea, Ş., Calu, D. A., & Girbina, M. M. (2011). A story about IAS/IFRS implementation in Romania. Journal of Accounting in Emerging Economies, 1(1), 76–100. https://doi.org/10.1108/20421161111107868

- Alfaraih, M. (2009). Compliance with international financial reporting standards (IFRS) and the value relevance of accounting information in emerging stock markets: evidence from Kuwait (Doctoral dissertation, Queensland University of Technology).

- Allard, K., Hasselgren, C., & Dellve, L. (2021). Gender equality and managers’ work in elderly and social care: A structural equation modelling approach. Journal of Nursing Management, 29(8), 2689–2696. https://doi.org/10.1111/jonm.13396

- Al-Omari, A. M. (2010). The institutional framework of financial reporting in Jordan. European Journal of Economics, Finance and Administrative Sciences, 22(1), 32–50.

- Amoah, S. K., & Amoah, A. K. (2018). The role of small and medium enterprises (SMEs) to employment in Ghana. International Journal of Business and Economics Research, 7(5), 151–157. https://doi.org/10.11648/j.ijber.20180705.14

- Andreev, P., Heart, T., Maoz, H., & Pliskin, N. (2009). Validating formative partial least squares (PLS) models: Methodological review and empirical illustration. International conference on information systems, November 2015 (pp. 1–17), Phoenix, Arizona.

- Arhin, T., Perprem, A., & Hulede, A. (2017). The challenges of adoption and implementing IFRS for SMEs in Ghana. a case of SMEs in the Kumasi metropolis. Research Journal of Accounting, 5(4), 1–13.

- Bagozzi, R. P., & Yi, Y. (2012). Specification, evaluation, and interpretation of structural equation models. Journal of the Academy of Marketing Science, 40(1), 8–34. https://doi.org/10.1007/s11747-011-0278-x

- Bank, W. (2017). World Bank SME Statistics.

- Beebe, K. R., Pell, R. J., & Seasholtz, M. B. (1998). Chemometrics: A practical guide (Vol. 4). Wiley.

- Benah, S., & Li, Y. (2020). Examining the relationship between lean supplier relationship management (LSRM) and Firm Performance: A study on manufacturing companies in Ghana. Open Journal of Business and Management, 8(6), 2423. https://doi.org/10.4236/ojbm.2020.86150

- Bunea-Bontas, C., Petre, M. C., & Petroianu, O. G. (2011). Consensual and Controversial Issues on IFRS for SMEs, Annals. Economic Science Series (Anale. Seria Stiinte Economice), 17(1), 495–501.

- Cai, L., Kwasi Sampene, A., Khan, A., Oteng-Agyeman, F., Tu, W., & Robert, B. (2022). Does entrepreneur moral reflectiveness matter? Pursing low-carbon emission behavior among SMEs through the relationship between environmental factors, entrepreneur personal concept, and outcome expectations. Sustainability, 14(2), 808. https://doi.org/10.3390/su14020808

- Cai, L., Rahman, A., & Courtenay, S. (2014). The effect of IFRS adoption conditional upon the level of pre-adoption divergence. The International Journal of Accounting, 49(2), 147–178. https://doi.org/10.1016/j.intacc.2014.04.004

- Carroll, C. E. (Ed.). (2016). The SAGE encyclopedia of corporate reputation. Sage Publications.

- Chin, W. W. (1998a). Commentary: Issues and opinion on structural equation modeling (pp. vii–xvi). MIS quarterly.

- Chin, W. W. (1998b). The partial least squares approach to structural equation modeling. In G. A. Marcoulides (Ed.), Modern methods for business research (pp. 295–358). Mahwah: Erlbaum.

- Cobbinah, B. B., Cheng, Y., Milly, N., & Sarpong, F. A. (2020). Relationship between determinants of financial assistance and credit accessibility of small and medium-enterprises (SME’s): A case study of sme’s in Takoradi metropolis in the western region of Ghana. Open Journal of Business and Management, 9(1), 430–447. https://doi.org/10.4236/ojbm.2021.91023

- Cohen, J. (1988). Statistical power analysis for the behavioral sciences–second edition. 12 Lawrence Erlbaum associates inc. Hillsdale, New Jersey, 13.

- Cooke, T. E., & Wallace, R. O. (1990). Financial disclosure regulation and its environment: A review and further analysis. Journal of Accounting and Public Policy, 9(2), 79–110. https://doi.org/10.1016/0278-4254(90)90013-P

- Damak-Ayadi, S., Sassi, N., & Bahri, M. (2020). Cross-country determinants of IFRS for SMEs adoption. Journal of Financial Reporting and Accounting, 18(1), 147–168. https://doi.org/10.1108/JFRA-12-2018-0118

- Dewi, A. A., & Dewi, L. G. K. (2019). International Financial Reporting Standard (IFRS): The awareness level in accounting student. AKRUAL: Jurnal Akuntansi, 10(2), 157–176. https://doi.org/10.26740/jaj.v10n2.p157-176

- Dhliwayo, R. M. (2017). An assessment of the challenges faced by SMEs in adopting and effectively implementing IFRS for SMEs: Survey of SMEs in Norton (Doctoral dissertation, BUSE).

- DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2), 147–160. https://doi.org/10.2307/2095101

- El-Gazzar, S. M., Finn, P. M., & Jacob, R. (1999). An empirical investigation of multinational firms’ compliance with international accounting standards. The International Journal of Accounting, 34(2), 239–248. https://doi.org/10.1016/S0020-7063(99)00005-9

- Essa, S. (2018). IFRS for SMEs: An emperical study of the KwaZulu-Natal SME sector (Doctoral dissertation). University of Kwazulu-Natal.

- Falk, R. F., & Miller, N. B. (1992). A primer for soft modeling. University of Akron Press.

- Ganiyu, S. A., Yu, D., Xu, C., & Providence, A. M. (2020). The Impact of supply chain risks and supply chain risk management strategies on enterprise performance in Ghana. Open Journal of Business and Management, 8(4), 1491–1507. https://doi.org/10.4236/ojbm.2020.84095

- Gefen, D., Straub, D., & Boudreau, M. C. (2000). Structural equation modeling and regression: Guidelines for research practice. Communications of the Association for Information Systems, 4(1), 7. https://doi.org/10.17705/1CAIS.00407

- Gelb, D., Holtzman, M. P., & Mest, D. (2008). International operations and voluntary disclosures by US-based multinational corporations. Advances in Accounting, 24(2), 243–249. https://doi.org/10.1016/j.adiac.2008.09.002

- Guler, I., Guillén, M. F., & Macpherson, J. M. (2002). Global competition, institutions, and the diffusion of organizational practices: The international spread of ISO 9000 quality certificates. Administrative Science Quarterly, 47(2), 207–232. https://doi.org/10.2307/3094804