?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Management accounting is very important in the field of accounting. It is a subject which implementation can bring about firm development. There are a lot of studies about management accounting. Past research have analysed various aspects of management accounting. However, the effect of management accounting services on the financial performance of SMEs have not been deeply researched into. This study aims to fill this gap by analysing the effect of management accounting service on the financial performance of SMEs in Ghana’s commerce, service, and manufacturing industries. The study’s population comprises registered SMEs from the Registrar General’s Department. The sample size was calculated using a population of 4,000 registered small and medium businesses to arrive at 365 SMfomular. Managers of SMEs were chosen and contacted using a systematic sample process and given questionnaires to complete. This study used the agency theory and Technology Acceptance Model (TAM). The PLSSEM Software was used to analyze the data collected from the respondents. The study found a relationship between SMEs’ performance and management accounting methods.

1. Introduction

In our world, Small and Medium Enterprises (SMEs) play a significant role in most economies, particularly in developing countries (Gherghina et al., Citation2020). SMEs account for most businesses worldwide and are essential contributors to job creation and global economic development. Small and medium enterprises are the backbone of the Ghanaian economy. They represent about 85% of businesses, mainly within the private sector, and contribute about 70% of Ghana’s gross domestic product (GDP; KorankyeSakyi & Yin, Citation2022).

However, there are no studies on the effects of management accounting on the financial performance of SMEs. Prior research on SME performance has typically focused on topics other than management accounting services and the financial performance of SMEs. For instance, Motta and Sharma (Citation2020) investigate the effects of lending technologies on the financial performance of SMEs, including fixed asset lending and financial statement lending. Through entrepreneurial oriented financing, Rita and Huruta (Citation2020) investigated the relationship between access to capital and performance in batik SMEs but were unable to detect any positive correlation. In addition to the aforementioned, researchers concentrated on specific industries run by SMEs. For instance, Motta and Sharma (Citation2020) investigate the relationship between the financial performance of SMEs and lending technologies such as fixed asset lending and financial statement lending in the services sector. Through entrepreneurial oriented financing, Rita and Huruta (Citation2020) investigated the relationship between access to capital and performance in batik SMEs but were unable to detect any positive correlation.

Literature has discussed various aspect of SMEs. For example, Lopez and Hiebl (2015) studied how management accounting knowledge could help SMEs to improve their managerial functions.

Another area studied by Mayr et al. (Citation2021) was to look at how management accounting could be used to prevent the poor performance of SMEs. Khalid and Kot (Citation2021) also found that management accounting is associated with the business’s success and vice versa and can influence organisational performance. Davilla and Foster (Davila & Foster, Citation2005) added that management accounting services are a subset of management accounting and refer to tools and techniques specifically designed to support management functions in improving operational efficiency and achieving optimal performance. Dahal et al. (Citation2020) studied information technology and management accounting effect on SMEs and found that management accounting services such as budgeting, performance analysis, cost volume-profit analysis, stock control, and standard costing analysis can be effective and have an impact on performance when SMEs employ the service of information technology. (Lesjak, Citation2001b) proved that information technology helps SMEs develop and implement business strategies. However, information technology on its own cannot provide essential information. Instead, it collects data and information from these management accounting services that have been implemented.

Hence, there is a need to investigate how management accounting services affect SMEs’ financial performance in Ghana and the moderating effect of information technology.

1.1. Literature review

1.1.1. Theoretical review

1.1.1.1. Agency theory

Agency problems have existed since the dawn of human civilization, when people first engaged in commerce and sought to further their own interests. One of the enduring issues that has existed since the development of joint stock firms is the agency problem (Panda & Leepsa, Citation2017).

Agency theory was proponded by Jensen and Meckling (Citation1976), an agency relationship is a legal arrangement in which one person, known as the principal, hires another, known as the agent, to carry out a task on their behalf. As part of this, the principal will grant the agent some discretion over decision-making. According to the agency theory, a principal must hire an agent to carry out tasks on his or her behalf (Jensen & Meckling, Citation1976). Agency theory explores and focuses on the issues that arise in businesses as a result of the separation of owners and management. The application of various governance techniques to regulate agent behavior in jointly owned firms is made easier by this approach (Panda & Leepsa, Citation2017).

The agency theory has been one of the fundamental theoretical paradigms in managerial accounting for the past 25 years. This theory provides a theoretical framework for understanding organisational processes from the principal-agent perspective (Vitolla et al., Citation2020).

The agency problem was possibly first suspected by Adam Smith in 1976, and since then, economists have been encouraged to develop the elements of agency theory. Smith predicted in his book The Wealth of Nations that there is a potential that an organization’s managers may not act in the owners’ best interests if they are not the actual owners (Panda & Leepsa, Citation2017).

This study focuses on the relationship between management accounting services and its effect on the financial performance of SMEs. The assumption that the researcher holds to guide the study in the use of the agency theory is that, the agency theory comes from a concept that can predict how management accounting services respond to financial information to ensure financial performance. There is, therefore, a principal-agent relationship between management accounting and financial performance. According to agency theory, there is an agreement between owners (principals) and outside auditors to oversee the performance of other agents (management). Owners (principals) assign management (agents) responsibilities to complete. The objective of agency theory is that the agent must develop good principles to ensure the smooth running of the business in other to bring about performance (Turnbull, Citation2019). This assumption of the agency theory is specifically used in this study in the sense that, if the operators of SMEs delegate their activities or perform on their own, and those in charge can apply management accounting principles to the business, It will bring about financial performance. Merendino and Melville (Citation2019), used agency theory in their studies about analysing the effect of board characteristics on integrated reporting quality Therefore, applying the theory helps deepen the understanding of agency theory. Agency theory was used by Teece (Citation2019) in his study of the capability theory of the firm. Audretsch and Link (Citation2019), based on agency theory, analyze the relationship between a Research joint venture’s governance structure and its propensity to adopt components of its research-based ecosystem. Sotarauta and Grillitsch (Citation2020) analyzed the three agents of change regional development paths and opportunity spaces using the agency theory. Shi et al. (Citation2017) used agency theory in their studies and made the point that according to agency theory, managers may be discouraged from acting opportunistically by external governance mechanisms such as activist owners, the market for corporate control, and securities analysts. There are criticism of the agency theory. Perrow (Citation1986), argued that the “principal and agent problem” could arise from the principal side and criticized positivist agency scholars for focusing solely on the agent side of the issue. He pointed out that the principals, who lie, avoid, and take advantage of the agents, are not taken into account by this theory. According to Zogning (Citation2017), the agency theory is a concept that is occasionally inappropriate for social interaction. It makes the supposition that all actors are self-interested, indivisible, and that social interactions have no bearing on the market. Additionally, it makes the assumption that actions are primarily driven by individual financial interests and that collaboration is evidence of an agreement between the parties. One sort of internal expense imposed by or payable to an agent acting on behalf of a principal is an agency cost. Agency expenses were primarily caused by the division of ownership and control, the divergence of ownership and control, and the diversity of objectives. The agency theory has a lot of advantages. The agent is supposed to develop good principles which can help the business to grow. One of the principles include management accounting services. The agency cost associated with agency theory can be compensated by the good principles employed by the agent to ensure the growth and development of the firm. The agency theory is therefore suited for this studies because of the advantages mentioned above.

1.2. Management accounting and SME

A variety of different authors and researchers across the world concerning the effects of management accounting on financial performance have conducted several studies. Some have also researched the moderating effect of information technology. Some research found a strong positive relationship others found a weak positive relationship. These researchers established several relationships. Some were positive, others were negative, and some established no relationship. Adu-Gyamfi, Kong and Wayne (Adu-Gyamfi et al., Citation2020) determined the Impact of management accounting practices on the performance of manufacturing companies in Ghana. Their findings suggested a positive relationship between management accounting practices and financial performance. Ahmad (Citation2012) examines the management accounting practices of SMEs in Malaysia and finds that Management accounting plays a significant role in the management of SMEs in Malaysia. Chege et al. (Citation2020) examine the association between technology innovation and firm performance in Kenya by considering the Impact of entrepreneur innovativeness on this association. Their findings indicate that technology innovation influences firm performance positively. Astuti et al. (Citation2020), examines digital technology for innovation adoption in mediating the relationship between the attributes of innovation adoption towards the performance of SMEs and found that technology significantly influences SMEs’ performance. Pedroso et al. (Citation2020) researched the Impact of management accounting systems (MAS) features and roles on today’s corporate organisations’ management, systems, processes, people, performance, and competitive settings. The results of their study demonstrated that MAS has a direct impact on managerial and organisational performance. Le et al. (Citation2020), investigated the relationship between organisational culture, management accounting, innovation capabilities, and firm performance in Vietnamese small and medium-sized firms (SMEs). Their findings show that combining management’s cultural orientation with management accounting information significantly impacts business performance. Osim et al. (Citation2020), investigate the Impact of Management Accounting Practices (MAPs) on the performance of small and medium-sized businesses (SMEs). According to their findings, the dependent variable (firm performance) and independent variables (Costing System, Budgeting System, Performance Evaluation System, Decision Support System, and Strategy Management Accounting System) had a substantial positive relationship.

Management accounting services are an essential routine that aims at supporting an organisation or managers of an organisation in decision-making and organisational performance, and accountability (Gomez-Conde et al., Citation2019). Management accounting enables managers in their planning and operational decision-making process (Ghasemi et al., Citation2019). Management accounting establishes a fundamental structure where the economic events of an organisation are measured and presented to organisational members responsible for making various organisational decision-making processes (Alsharari, Citation2019).

Alvarez et al. (Citation2021) employed a non-parametric approach to investigate the impact of Management Accounting Practices (MAP) systems on the performance of the user and non-user organisations. Their findings show that most management accounting systems have positive and statistically significant associations with hotel business performance.

According to Ruiz and Collazzo (Citation2020), despite their importance, micro and small businesses are arguably understudied because it is considered that they do not adopt Management Accounting (MA) techniques or that if they do, it is in a very rudimentary manner. On the other hand, micro and small businesses are essential to examine for various reasons. Among them are its economic importance and the ability to track the progress of these practices in businesses from their earliest stages. However, to their knowledge, no investigation has been conducted into how the MA tools are used in these businesses. To fill this vacuum in the research, an exploratory investigation of how micro and small businesses apply MA methods was conducted using a qualitative approach (Ruiz & Collazzo, Citation2020).

Adu-Gyamfi and Chipwere () looked at the Impact of management accounting methods on the performance of manufacturing companies in Ghana. They acquired data using a quantitative research strategy from 200 manufacturing firm managers who were chosen using the probability simple random sampling technique. The findings of their study show that costing systems, budgetary systems, performance evaluation systems, strategic management, and information for decision-making are the most common management accounting practices used by manufacturing firms in Ghana, and that these management accounting practices have a positive impact on their performance. The gap in literature is that there is no specific study on management accounting services and financial performance of SMEs.

HI: There is a significant relationship between management accounting services and the financial performance of SME

1.3. Information technology and SME financial performance

Information Technology adoption leads to more jobs, financial benefits, increased efficiency, productivity, and growth, confirming the conclusions of other research on the socio-benefits of ICT adoption, particularly in developing countries. Poverty reduction, employment development, money generation, and economic progress are some goals (Okundaye et al., Citation2019). Information Technology incorporation has already positively impacted the economic performance of enterprises in emerging countries (World Bank, Citation2015). Information Technology has a significant role in the growth and development of businesses. SMEs can utilise ICT to improve or replace existing information systems and networks, thereby expanding their market (Chege et al., Citation2020). Tarutė and Gatautis (Citation2014), examine the ICT impact on SME’s performance. The findings of their study show that ICT has an impact on improving SME performance and that aligning ICT investments with internal skills and organisational processes is critical for the best results. Paul (Citation2018) concluded that adopting ICT services for SMEs greatly has improved their performance. Okundaye et al. (Citation2019), examine how small and medium-sized enterprise (SME) leaders in Nigeria use information and communication technology (ICT) as a business strategy to increase profitability and compete globally. Their findings indicate that ICT has a positive and significant effect on the financial performance of SMEs. Appiahene et al. (Citation2019) found out that information technology had significant impact on banks’ performance. Mbilla et al. (Citation2020). Assessed the impact of information technology on banks performance in Ghana. Their results indicated that Information technology have a weak significant effect on financial performance and that there was no significant effect between Monitoring and financial performance.

H2: There is a significant relationship between information technology and SME financial performance

H3: information technology can significantly moderate management accounting and the financial performance of SMEs.

1.5. Financial performance

Financial performance can be defined as a general measure of a firm’s overall financial health over a given period. Stakeholders are interested in tracking companies’ financial performance (small-medium enterprises). Financial performance identifies how well a company (SME) generates revenues and manages its assets, liabilities, and the financial interests of its stake-and stockholders. Murphy et al. (Citation1996) believe that performance measures are defined by their finances or organisation. Sandberg and Hoffer (Sandberg & Hofer, Citation1987) also added that popular measures used to gauge financial performance include maximising profits, increasing profits derived from assets, and maximising the benefits of shareholders, which act as the key measures in ensuring the effectiveness of a firm ().

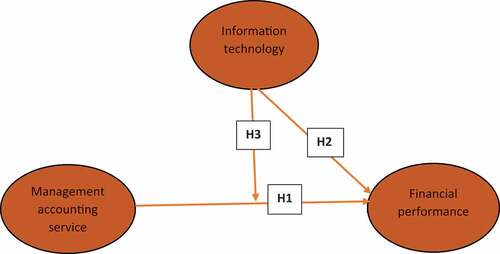

Figure 1. Conceptual framework

conceptual framework

Source: Author’s construction (2022)

1.6. Conceptual framework

Management accounting services are a significant concept, and their proper implementation could enhance financial performance. The reason is that management accounting has developed many principles which bring about effective planning, control and decision-making. Management should use management accounting principles to plan, control and take decisions that will drive the entity to achieve financial performance. SMEs can use management accounting concepts to develop plans and take decisions in the firm’s best interest. The conceptual framework above asserts that implementing management accounting services enhances financial performance. Information technology has become the economic driver of every business. The conceptual framework asserts that if SMEs use information technology in their use of management accounting services, it will enhance financial performance.

H1 states that the implementation of management accounting services will lead to financial performance SME

H2 states that implementing information technology will enhance the financial performance of SMEs.

H3 states that the use of information technology in the delivery of management accounting services will lead to the financial performance of SME

1.7. Methodology

A quantitative study using cross sectional data supported by a questionnaire was used to solicit management accounting and SMEs performance information from the respondents

Managers of SMEs were given questionnaires to evaluate if they employed management accounting methods and how their financial performance was influenced. A questionnaire was used since it may help gather more detailed information from respondents. The questionnaire consists of four (4) sections: demographics, management accounting procedures, information technology, and a financial performance questionnaire using a Likert scale of 1 to 5, with 1 representing strong disagreement and five denoting strong agreement.

The study’s population comprises registered SMEs from the Registrar General’s Department. The sample size was calculated using a list of 4,000 registered small and medium businesses. The SMEs were chosen using a systematic sample process and given questionnaires to complete. To obtain a sample size that has an adequate size relative to the goals of the study, the researcher adopted Yamane’s formula as follows:

Population = 4,000Error term = 0.05Square root of 0.05 is 0.00254,000 × 0.0025 = 1010 + 1 = 114,000/11 = 365Sample size is therefore = 365Creswell (2016)

Where n is the sample size, N is the population size and e is the margin of error (Yamane, Citation1967). Categories of sample are Food & Beverages, Agro processing, Agro industrial, Services, Fabrication, Wood processing, textile.

1.8. Data analysis methods

The data were analysed using a variety of data analysis techniques. First, a preliminary examination of the data was done. Here, the data were checked for normality to see whether the PLS-SEM method utilised in the further analysis was appropriate. The hypotheses in the suggested research model were then tested using the Partial Least Square structural equation modelling method. The two-step procedure Chin (Citation1998) suggested is beneficial for conducting PLS-SEM analysis. Finally, the measurement model was tested to evaluate the variables’ validity and reliability in the suggested research model. Below is a thorough explanation of structural equation modelling and why PLS-SEM methodology should be used (J. F. Hair et al., Citation2019).

1.9. Structural equation modelling (SEM)

PLS-SEM, or partial least squares structural equation modelling, is one of the most used approaches for analysing multivariate data (Memon et al., Citation2021). The combination of latent variables and structural links is known as structural equation modelling (SEM). The most prominent research methodologies utilised across various areas include the partial least squares SEM (PLS-SEM), which is used to estimate complex cause-effect relationship models using latent variables (Cepeda-Carrion et al., Citation2018). SmartPLS is a scientifically based software whose concept is to implement algorithms and model statistics that have been tested and published in scholarly journals with peer-reviewed quality assurance. This research uses SmartPLS for its analysis (Memon et al., Citation2021). A series of second-generation statistical approaches known as structural equation modelling is used to evaluate and estimate causal links between many variables using statistical data and qualitative causal hypotheses (Vinodh & Joy, Citation2012). SEM has grown in recent years, along with the advancement of computer technology and software. SEM is a member of the multivariate-analysis family, which analyses several variables (Cepeda-Carrion et al., Citation2018). Among business and social science experts, partial least squares structural equation modelling (PLS-SEM), commonly referred to as PLS Path Modeling, is one of the most used techniques for multivariate data analysis. Since the early 2000s, due to its rapid development, PLS-SEM has gained popularity among academics and students and is primarily used to analyse models with latent variables (Memon et al., Citation2021).

1.10. PLS-SEM model assessment

Chin (Citation1998) recommended a two-step approach in undertaking PLS-SEM analysis. These two steps were adopted in this study. The first point is to test for reliability and validity. After that, there is the need to test further the structural relationships between the latent and the observed variables in the research model. If, after the test, the acceptable threshold is met, then one can go ahead. If, after testing the measurement model, it is ascertained that the measurement items do not measure the latent variables reliably, then the suggested relationships between these variables cannot be verified (Hair et al., Citation2021b)

1.11. Measurement model assessment

Internal consistency reliability is looked at in the second stage of the reflective measurement model assessment. The degree to which indicators measuring the same construct are related is known as internal consistency reliability (Hair et al., Citation2021b).

When evaluating the measurement model, the researcher must distinguish between reflecting and formative modes; in the case of this study, all latent variables are modelled as reflective latent variables. Reliability, discriminant, and convergent validity are used to evaluate reflective latent variables (J. F. Hair et al., Citation2019).

1.12. Reliability

The evaluation of the internal consistency of the constructs is called reliability. If a measurement consistently yields the same results under the same circumstances, it is considered high dependability. Utilising Composite Reliability and Cronbach’s Alpha, SMART-PLS reliability is evaluated (Stefanic & Randles, Citation2015). The measurement model’s internal consistency reliability should be examined as the first criterion using Cronbach’s alpha (Cronbach, Citation1951). According to J. F. Hair et al. (Citation2019), another internal consistency reliability test that uses similar assumptions and yields lower results than composite reliability is Cronbach’s alpha. Since the items are not weighted, Cronbach’s alpha is a less accurate reliability indicator. Contrarily, with composite reliability, the items are loaded according to the various construct indicators, and the dependability is more excellent than Cronbach’s alpha. The composite reliability rhoc developed by Jöreskog in 1971 is one of the primary metrics used in PLS-SEM. Better values correspond to higher reliability levels. In exploratory research, reliability levels between 0.60 and 0.70, for instance, are deemed “acceptable,” and reliability values between 0.70 and 0.90 are categorised as “satisfying to good.” Values greater than 0.90 (and unquestionably greater than 0.95) provide a challenge since they suggest that the indicators are redundant, which lowers construct validity (Hair et al., Citation2021).

Another internal consistency reliability test that uses similar assumptions and yields lower results than composite reliability is Cronbach’s alpha which assumes the same thresholds as the composite reliability (rhoc). (Kalkbrenner, Citation2021) The genuine dependability of the construct is commonly thought to fall between these two extreme values, even if Cronbach’s alpha is generally considered relatively conservative and the composite reliability rhoc may be overly liberal (Hair et al., Citation2021).

1.13. Discriminant validity

The degree to which a construct is empirically different from other items in the structural model is measured by its discriminant validity (J. F. Hair et al., Citation2019). It assesses how different a construct is from other constructs in the structural model experimentally and reflects how unique it is from other constructs (Gim & Cheah, Citation2020). Three methods have been proposed for assessing discriminant validity (J. F. Hair et al., Citation2019). The latent construct indicators load more heavily in the model using the first approach. The second method involves applying the Fornell-Larcker criterion, which stipulates that a latent construct’s AVE must be more significant than the square correlations between the construct and any other construct. (Hair et al., Citation2021). Henseler, Ringle, and Sarstedt (Henseler, Citation2015) pointed out certain flaws in the Fornell-Larcker and suggested the Heterotrait-Monotrait ratio (HTMT) for judging discriminant validity. The HTMT is described as the geometric mean of the average correlations for the indicators measuring the same construct (i.e., the monotrait-heteromethod correlations) compared to the mean value of the indicator correlations across constructs (i.e., the heterotrait-heteromethod correlations; J. F. Hair et al., Citation2019). According to Henseler (Citation2015), the HTMT should discriminate between two factors of 0.85 or less.

1.14. Convergent validity

The degree to which a construct converges to account for its elements’ variance is known as convergent validity. The average variance extracted (AVE) for all items on each construct is the statistic used to assess a concept’s convergent validity (Hair et al., Citation2021). The average variance extracted (AVE) values are the foundation for determining convergent validity (J. F. Hair et al., Citation2019). The loading of each indicator on a construct must be squared to get the mean value, which is then used to calculate the AVE. In addition, the construct must explain at least 50% of the variation of the items that make up the construct for the AVE to be considered acceptable, which must be at least 0.50 (Hair et al., Citation2021). Checking the degree to which the variation of the indicators of a specific construct is shared might be another way to evaluate the quality of a measurement model. By proving convergent validity, the degree of shared variance is determined. Convergent validity is shown by high factor loadings (>0.7) and average variance extracted (AVE) (>0.5). The AVE is the average of the commonalities of the indicators related to any given construct (i.e., factor loadings squared, which should be at least 0.50). A construct is said to explain at least half of the variation of its observable variables when the AVE is 0.50 (Sarstedt et al., Citation2021).

1.15. Structural model assessment

When the structural model assessment of the measurement model is satisfactory, the PLS-SEM results are evaluated. The coefficient of determination (R2), the blindfolding-based cross-validated redundancy measure Q2, and the statistical significance and relevance of the path coefficients are standard evaluation criteria that should be considered. Additionally, if the sample size is large enough, researchers should use the PLSpredict process to evaluate their model’s out-of-sample predicting power (J. F. Hair et al., Citation2019). The collinearity, path coefficients, coefficient of determination, effect size, and predictive relevance are all evaluated as part of the structural model assessment (Gim & Cheah, Citation2020). The route coefficient, the coefficient of determination R2, predictive relevance Q2, and f2 effect sizes must be considered when evaluating the structural model. Path coefficients are rated according to their power, importance, and significance. The explanatory strength of the model is indicated by the R2, which measures the variance explained by each of the endogenous constructs (Purwanto & Sudargini, Citation2021). Greater explanatory power is shown by higher values of the R2, which range from 0 to 1. For example, R2 values of 0.75, 0.50, and 0.25 might be regarded as significant, moderate, and weak, respectively (J. F. Hair et al., Citation2019). However, acceptable R2 levels depend on the research setting, and in some fields, such as stock return prediction, an R2 value as low as 0.10 is regarded as suitable (Sarstedt et al., Citation2021). Calculating the Q2 value is another way to evaluate the PLS path model’s predictive precision (Geisser, Citation1974). As a general rule, Q2 values greater than 0, 0.25, and 0.5 represent the PLS-path model’s minor, medium, and substantial predictive importance, respectively (J. F. Hair et al., Citation2019).

1.16. Statistical software

SPSS version 23 was used for descriptive analysis in the study because it is user-friendly. The structural equation modelling was tested using SmartPLS version 3 by the researcher. The researcher obtained training on using SmartPLS, which made it very easy to use. Additionally, SmartPLS software incorporates the Cronbach alpha and composite reliability measure for reliability and the HTMT ratio for assessing discriminant validity.

1.17. Ethical considerations

It is crucial to guarantee secrecy and anonymity to acquire access to individuals and groups. Once access has been given, the researcher must adhere to the research goals. Any action that deviates from what was agreed upon could anger people and lead to an early end to the data collection process (Endrikat et al., Citation2017). The researcher informed the SMEs in the letter, which prefixed the questionnaire, that the research was being conducted for academic purposes and outlined its inspiration. The SMEs’ operators were assured that the requested data would be handled with care and utmost confidentiality. The researcher requested the respondents to submit demographic data about their gender, age, industry type and educational background. The researcher did not request personal information like their names. Therefore, this data could not be used to identify any particular respondent. The subjects of the data collection cannot be coerced into providing any information. Respondents in this study were assured that they were not required to complete the questionnaire and could stop at any time after beginning if they so desired. The researcher needed to be objective in his analysis because he used a positivist perspective. Data were analysed objectively, with no modifications made to the findings.

1.18. Non-response and standard method bias

Cronbach’s alpha was calculated for each construct to prevent common method bias. Every value above the critical threshold of 0.7 shows the items’ reliability (Cooper et al., Citation2020). PLS-SEM was used to estimate the structural model with complex relationships, such as those in this case that included several independent and dependent variables and many independent-dependent interactions (J. F. Hair et al., Citation2019). Testing for moderation was required because the study’s model included a moderating element. SMART PLS-SEM is better suited in this situation since it can evaluate models that include moderators. Finally, PLS-SEM was utilised since the study’s main objective was to forecast the primary target construct, in this case, financial accounting services, and how this construct may affect financial performance.

1.19. Calculation of sample size

Our sample size is computed using the (Yamane, Citation1967) formula with a 95% confidence level plus or minus 5% confidence intervals using n = N/1 + N(e)2, where n is the sample size. The population is N, and the error margin is e. Although a sample size of 375 was calculated based on a population estimate of 6000 people. Of the 375 questionnaires sent out, 370 were returned, with 50 being discarded since they were either small businesses or did not use management accounting. As a result, the sample size for the analysis was determined by the number of respondents who practised management accounting and owned medium-sized businesses (320). A large sample size yields more reliable results than smaller samples. A sample size of fewer than 50 respondents is a weaker sample, a sample size of 100 respondents is weak, a sample size of 200 respondents is adequate, 300 is good, 500 is very good, and 1000 is extraordinary, according to inferential statistics by Comrey and Lee (Citation1992). As a result, a sample size of three hundred and twenty (320) is sufficient.

1.20. Variables of the study

The primary dependent variable for this study is a financial performance which Return will measure on Asset (ROA), Gross Profit Margin, and Net Profit Margin, which is a vital activity in any organisation. It is an ideal practice for controlling an organisation’s financial activities, such as procurement, utilisation of funds, accounting, payments, risk assessment, and every other thing related to money. The independent variable in the research is management accounting practices measured by: Budgetary control, Decision support system, cost control, labour costing, and inventory management system. The moderating variable in this study is Information Technology. Information Technology is a moderator between Management Accounting and Financial Performance, thus influencing the Impact that Management accounting has on the Financial Performance of SMEs. Information technology is measured as perceived ease of use and perceived usefulness. Questions were asked to ascertain the effect of individual management accounting variables on financial performance. The effect of Budgetary control on the financial performance of SMEs was analysed after collecting the data using the questionnaire. The use of decision support systems to enable operators of SMEs to take a decision and how this system has helped to improve financial performance was also analysed. The effect of cost control and its effects on financial performance was also analysed, and finally, the effect of labour costing and the inventory management system’s effect on financial performance was also analysed.

1.21. Data analysis and results

The PLS-SEM was employed to analyse this study (Henseler et al., Citation2009). PLS-SEM provides numerous advantages. When employing PLS for complicated models, one of the advantages of PLS-SEM is that the sample size requirements are likely to be substantially reduced (Chin & Newsted, Citation1999). The researchers selected 320 valid responses for the study, with 48.4 per cent representing males and 51.6 per cent representing females (see, Table ).

Table 1. Demographics of Respondents

Table 2. Loading, Reliability, and Validity

According to Fornell and Bookstein (Citation1982), PLS frequently gives component-based loadings and structural routes without the need for distributional assumptions. Therefore, PLS-SEM provides high statistical power, benefiting researchers (J. F. Hair et al., Citation2019). In addition, PLS-SEM has more statistical power, implying that it is more likely to uncover significant connections in the population (Sarstedt et al., Citation2021). The current studies’ analysis is based on a two-step method for reporting PLS-SEM results (Henseler et al., Citation2009). We first looked at the measurement model to assess the instrument’s reliability and validity. Following that, the structural model based on the hypotheses proposed in this study was investigated.

1.22. Descriptive statistics

Table below demonstrates the descriptive statistics of the study. As previously mentioned, a total of 365 paper surveys were given, and 345 received responses.

However, 320 valid replies were used for analysis due to missing values. Out of these 320 responses, 155 (or about 48%) were provided by men, while women provided 165 (42%). There were 281 responses between 30–49 (87.81%) as the modal age range for respondents. 22 respondents were between the ages of 20 and 29 (6.88%), whiles 17 respondents were 50 and above (5.32%)

1.23. Measurement model

Reliability refers to the similarity of results obtained by independent but comparable measures of the same item or construct or a measure of consistency (Churchill & Iacobucci, Citation2010). The essential reliability indicators in this study were composite reliability (CR) and Cronbach’s alpha values. Validity tests were divided into two categories: convergent and discriminant. Convergent validity was determined using an item or factor loadings larger than 0.5 on their respective constructs (Chinomona, Citation2013). Validity was determined using the Average Variance Extracted (AVE) values and the Fornell-Lacker Criterion. These confirm that no significant factors were related to one another and that the variables were thus independent and valid in predicting the outcome variable (Chin, Citation2010).

As previously indicated, composite reliability and Cronbach’s alpha values were used to examine the reliability of the three research constructions assessments. Cronbach’s alpha (CA) values ranged between 0.631 to 0.790, while the Composite Reliability (CR) values ranged from 0.666 to 0.852 (see, Table ). The reliability measures of Composite Reliability (CR) and Cronbach’s alpha (CA) for management Accounting practices, Financial Performance, and Information Technology were all higher than the recommended threshold value of 0.6 to 0.7, indicating that these three research construct measures are reliable (Nunnally & Bernstein, Citation1994).

As previously indicated, convergent validity was measured using the Average Variance Extracted (AVE), whereas discriminant validity was measured using the Fornell-Lacker Criterion. Because all AVEs were more than 0.5, convergent validity was acceptable (J. F. Hair et al., Citation2019). Individual factor loadings for each relevant study construct that was more than the proposed value of 0.5 were used to examine the reliability and validity of the results and the factor loadings (Anderson & Gerbing Citation1988). All three constructs’ factor loadings were over the recommended threshold of 0.5, as shown in Table . All the factor loadings for management accounting practices (MAN), financial performance (FP), and information technology (IT) were above the permissible value of 0.5. Given the preceding, it can be inferred that most of the items used to assess the three research variables in this study accurately measured more than half of the variables of management accounting services, information technology, and financial performance. Therefore, AVE is acceptable because, in this research, AVE ranged from 0.500 to 0.538, as shown in Table (Hair et al., Citation2011).

The Fornell-Lacker Criterion was used to measure discriminant validity. The square root of AVE was more significant than the inter-construct correlation, as seen in Table . The Heterotrait-Monotrait Ratio (HTMT) was also used to assess discriminant validity, as shown in Table (Henseler, Citation2015).

Table 3. Heterotrait-Monotrait Ratio(HTMT)

Table 4. Discriminant validity using Fornell–Larcker Criterion

1.24. Structure model

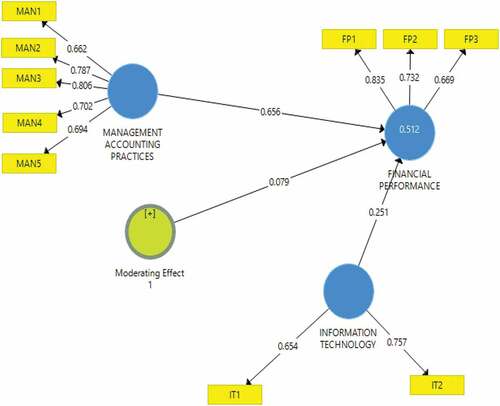

This section goes through the structural model. The study framework’s theorised paths are depicted in the structural model. A structural model is evaluated using R2 and Q2. (Dijkstra & Henseler, Citation2015). The coefficient of determination for the Endogenous variable is the strength of each structural path as evaluated by the R2 value. The R2 must be greater than or equal to 0.1 (Falk & Miller, Citation1992). Table demonstrates that the R2 value is more than 0.1. That means the present model’s R2 is 0.512. As a result, the model’s predictive capacity is established.

Table 5. Path coefficients and their significance

Q2 also establishes the predictive relevance of the endogenous concept. The study’s Q2 value is 0.258, which is higher than zero (0), indicating that the model is predictive. The findings imply that the constructions’ prediction is relevant (see, Table ; Falk & Miller, Citation1992). The importance of the relationship was determined by further testing of the idea. H1: determines if MAN (Management Accounting Practices) significantly impacts FP (Financial Performance). The findings showed that MAN had a major effect on FP. (β = 0.049, t = 5.147, p < 0.000). Hence H1 was supported.

H2: evaluates whether IT (Information Technology) significantly affects FP (Financial Performance). The findings revealed that IT and FP positively and significantly affect financial performance. (β = 0.033; t = 2.274, p < 0.000). As a result, H2 was supported.

1.25. Moderation analysis

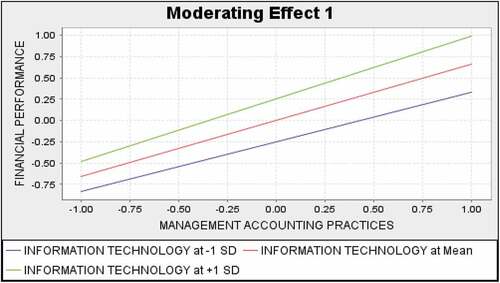

H3: Information technology has the potential to significantly moderate the relationship between management accounting practice and financial performance, so an increase in IT (information technology) should increase financial performance. Moderation analysis was performed to evaluate the moderating role of IT. The results revealed a significant moderating role of IT in the relationship between MAN and FP. (β = 0.035, t = 2.274, p < 0.023).

The results of the hypothesis confirm with the graph that when IT increases, as shown by the green line in the graph (see, Figures ), the effect on FP also increases.

Figure 2. Structural Model Results from PLS

Figure 3. Structural model results from PLS.

2. Implications of the Study

This study aimed to consider the effect of management accounting services on the financial performance of SMEs in Ghana. H1 indicated a positive impact of management accounting on the financial performance of SMEs. These positions were supported by the findings of: (Adu-Gyamfi & Chipwere, ; Alsharari, Citation2019; Alvarez et al., Citation2021); that is, if a firm accesses management accounting services, it will lead to an increase in financial performance. As a result, SMEs must include management accounting services in their operations to expand. However, due to financial constraints and a lack of technological skills, some SMEs may be unable to use management accounting services. The government can assist SMEs by employing accounting companies to provide management accounting services through the Ministry of Trade and Industry. H2 also shows a positive and robust relationship between SMEs’ financial performance and information technology. These positions were supported by the findings of (Chege et al., Citation2020). The relationship suggests that SMEs can apply information technology in various processes, including management accounting, which can improve their financial performance. H3 assessed whether Information Technology could significantly moderate the use of management accounting services and financial performance. The results indicated a positive significant moderating effect between management accounting services and financial performance. SMEs that use management accounting services can also utilise information technology. However, some SMEs who use management accounting services may be doing it manually and thus not reaping the full benefits. Therefore, using information technology to improve management accounting services will be more appropriate.

2.1. Conclusion

SMEs (small and medium-sized enterprises) are the backbone of any economy, including Ghana’s. Many of these SMEs, however, collapse within a few years after their inception. Several factors could cause these problems. One of the possible causes of SMEs’ extinction is a lack of access to management accounting services. According to the current study, management accounting services have a positive and significant impact on the financial performance of SMEs. As a result, the government must intervene to ensure that management accounting services are available. Information technology has been a driving force in every aspect of advancement. According to the current study’s findings, when the relationship between financial accounting and financial performance is moderated, it has a positive and significant effect on the financial performance of SMEs. As a result, SMEs are encouraged to incorporate technology into their operations.

2.2. Theoretical implications

The research broadens our understanding of how management accounting services and SMEs’ financial performance are related. The agency theory is strengthened by establishing this relationship. Because we will recognize the connections and benefit from a better understanding of SMEs and management accounting services, we will be better able to package management accounting courses and have more effective programs that will directly impact business processes. Additional services that will be highlighted include accounting, audit, and management accounting services, which will necessitate more study.

2.3. Practical implications

There are two ways to examine the study’s relevance to practice. First, accounting practitioners will benefit from the study’s results by better understanding the effects or influences of various accounting services on SMEs. Additionally, it will instruct them on how to offer targeted services that will affect the performance of SMEs. Second, the SMEs will start to understand the importance of using accounting services and their worth to their business.

2.4. Limitations and areas for future research

One of the main limitations of this study is that the data were mainly collected from SMEs in Accra (Ghana) which hinders the findings from being generalized, even though most of the SME are in Accra and very few in the other regions. In addition, the SMEs in Accra are a replica of those in the other regions. Inspite of this, the current study recommends that future research collect data from the other regions to find out if different results will come out. Furthermore, the current study did not find out the reason why some of the SMEs are not using management accounting services. We suggest that future studies sample views of managers of SME as to the reasons for the use or non-use of management accounting services. It will allow a deeper understanding of SME systems in Ghana. More importantly, this study used the quantitative method and it is recommended that future studies could make use of qualitative method in other to allow the operators or managers of SMEs to be interviewed so they could express themselves well as to the use of management accounting services.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Henseler, J. (2015). Is the whole more than the sum of its parts? On the interplay of marketing and design research. Inaugural lecture held, University of Twente.

- Adu-Gyamfi, J., Yusheng, K., & Chipwere, W. (2020). The Impact of Management Accounting Practices on the Performance of Manufacturing Firms; An Empirical Evidence from Ghana. Research Journal of Finance and Accounting, 11(20), 10.7176/RJFA/11-17–13.

- Ahmad, K. (2012). The use of management accounting practices in Malaysian SMEs. University of Exeter.

- Alsharari, N. M. (2019). Management accounting and organisational change: Alternative perspectives. International Journal of Organizational Analysis, 27(4), 1124–19. https://doi.org/10.1108/IJOA-03-2018-1394

- Alvarez, T., Sensini, L., Bello, C., & Vazquez, M. (2021). Management Accounting Practices and Performance of SMEs in the Hotel Industry: Evidence from an emerging economy. International Journal of Business and Social Science, 12(2), 24–35. https://doi.org/10.30845/ijbss.v12n2p3

- Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modeling in practice: A review and recommended two-step approach. Psychological bulletin, 103(3), 411.

- Appiahene, P., Missah, Y. M., & Najim, U. (2019). Evaluation of information technology impact on bank’s performance: The Ghanaian experience. International Journal of Engineering Business Management, 11, 1847979019835337. https://doi.org/10.1177/1847979019835337

- Astuti, E. S., Sanawiri, B., & Iqbal, M. (2020). Attributes Of Innovation, Digital Technology and their Impact on SME Performance In Indonesia. International Journal of Entrepreneurship, 24(1), 1–14. https://doi.org/10.3946/75-24-1-371

- Audretsch, D. B., & Link, A. N. (2019). Embracing an entrepreneurial ecosystem: An analysis of the governance of research joint ventures. Small Business Economics, 52(2), 429–436. https://doi.org/10.1007/s11187-017-9953-8

- Cepeda-Carrion, G., Cegarra-Navarro, J. G., & Cillo, V. (2018). Tips to use partial least squares structural equation modelling (PLS-SEM) in knowledge management. Journal of Knowledge Management. https://www.researchgate.net/publication/328743256

- Chege, S. M., Wang, D., & Suntu, S. L. (2020). Impact of information technology innovation on firm performance in Kenya. Information Technology for Development, 26(2), 316–345. https://doi.org/10.1080/02681102.2019.1573717

- Chin, W. W. (1998). The partial least squares approach to structural equation modeling. In G. A. Marcoulides (Ed.), Modern methods for business research (pp. 295–358). Erlbaum.

- Chin, W. W. (2010). “Bootstrap cross-validation indices for PLS path model assessment”, in Esposito Vinzi, V., Chin, W.W., Henseler, J. and Wang, H. (Eds). In Handbook of Partial Least. Springer-Verlag Berlin Heidelberg. https://doi.org/10.1007/978-3-540-32827-84

- Chin, W. W., & Newsted, P. R. (1999). Structural Equation Modelling: Analysis with Small Samples Using. In S. R. Partial Least & H. Hoyle (Eds.), Statistical Strategies for Small Sample Research (pp. 307–341). Sage.

- Chinomona, R. (2013). The influence of brand experience on brand satisfaction, trust and attachment in South Africa. International Business & Economics Research Journal (IBER), 12(10), 1303–1316.

- Churchill, D. A., & Iacobucci, D. (2010). Market research: Methodological foundations. In South-Western Cengage Learning. Earlie Lite Books, Inc.

- Comrey, A. L., & Lee, H. B. (1992). Interpretation and Application of Factor Analytic Results. A First Course in Factor Analysis (pp. 2). Hillsdale, NJ: Lawrence Eribaum Associates.

- Cooper, B., Eva, N., Fazlelahi, F. Z., Newman, A., Lee, A., & Obschonka, M. (2020). Addressing common method variance and endogeneity in vocational behavior research: A review of the literature and suggestions for future research. Journal of Vocational Behavior, 121, 103472. https://doi.org/10.1016/j.jvb.2020.103472

- Cronbach, L. J. (1951). Coefficient alpha and the internal structure of tests. psychometrika, 16(3), 297–334. https://doi.org/10.1007/BF02310555

- Dahal, R. K., Bhattarai, G., & Karki, D. (2020). Management accounting techniques on rationalise decisions in the Nepalese listed manufacturing companies. Researcher: A Research Journal of Culture and Society, 4(1), 112–128. https://doi.org/10.3126/researcher.v4i1.33816

- Davila, A., & Foster, G. (2005). Management accounting systems adoption decisions: Evidence and performance implications from early‐stage/startup companies. The Accounting Review, 80(4), 1039–1068. https://doi.org/10.2308/accr.2005.80.4.1039

- Endrikat, J., Hartmann, F., & Schreck, P. (2017). Social and ethical issues in management accounting and control: An editorial. Journal of Management Control, 28(3), 245–249. https://doi.org/10.1007/s00187-017-0253-x

- Falk, R. F., & Miller, N. B. (1992). A primer for soft modeling. University of Akron Press

- Fornell, C., & Bookstein, F. L. (1982). Two structural equation models: LISREL and PLS applied to consumer exit-voice theory. Journal of Marketing research, 19(4), 440–452.

- Geisser, S. (1974). A predictive approach to the random effect model. Biometrika, 61(1), 101–107. https://doi.org/10.1093/biomet/61.1.101

- Ghasemi, R., Habibi, H. R., Ghasemlo, M., & Karami, M. (2019). The effectiveness of management accounting systems: Evidence from financial organisations in Iran. Journal of Accounting in Emerging Economies, 9(2), 182–207. https://doi.org/10.1108/JAEE-02-2017-0013

- Gherghina, Ș. C., Botezatu, M. A., Hosszu, A., & Simionescu, L. N. (2020). Small and medium-sized enterprises (SMEs): The engine of economic growth through investments and innovation. Sustainability, 12(1), 347. https://doi.org/10.3390/su12010347

- Gim, G. C., & Cheah, W. S. (2020). Pay Satisfaction and Organizational Trust: An Importance Performance Map Analysis. Journal of Applied Structural Equation Modeling, 4(1), 1–16. https://doi.org/10.47263/JASEM.4(1)01

- Gomez-Conde, J., Lunkes, R. J., & Rosa, F. S. (2019). Environmental innovation practices and operational performance: The joint effects of management accounting and control systems and environmental training. Accounting, Auditing & Accountability Journal, 32(5), 1325–1357. https://doi.org/10.1108/AAAJ-01-2018-3327

- Hair, J. F., Hult, G. T. M., Ringle, C. M., Sarstedt, M., Danks, N. P., & Ray, S. (2021). Evaluation of reflective measurement models. In Partial Least Squares Structural Equation Modeling (PLS-SEM) Using R (pp. 75-90). Springer.

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bulle. Journal of Marketing Theory and Practice, 18((2)), 139–152. https://doi.org/10.2753/MTP1069-6679190202

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

- Henseler, J., Ringle, C. M., & Sinkovics, R. R. (2009). The use of partial least squares path modeling in international marketing. In New challenges to international marketing. Emerald Group Publishing Limited. 1474–7979. https://www.researchgate.net/publication/229892421

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the Firm: Managerial Behaviour, Agency Costs and Ownership Structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Kalkbrenner, M. T. (2021). Alpha, omega, and H internal consistency reliability estimates: Reviewing these options and when to use them. In Counseling Outcome Research and Evaluation (pp. 1–12). Taylor & Francis.

- Khalid, B., & Kot, M. (2021). The Impact of accounting information systems on performance management in the banking sector. In IBIMA Business Review. IBIMA Business Review. https://doi.org/10.5171/2021.578902

- Korankye-Sakyi, F. K., & Yin, E. T. (2022). Analysis of Ghana’s SMES industrial policy approach: Call for a new beginning. UCC Law Journal, 2(1), 133–156. https://doi.org/10.47963/ucclj.v2i1.902

- Le, H. M., Nguyen, T. T., & Hoang, T. C. (2020). Organisational culture, management accounting information, innovation capability, and firm performance. Cogent Business & Management, 7(1), 1857594. https://doi.org/10.1080/23311975.2020.1857594

- Lesjak, D. (2001b). Are Slovene Small Firms Using Information Technology Strategically? Journal of Computer Information Systems, 41(3), 74–81. https://www.researchgate.net/publication/291841077

- Mayr, S., Mitter, C., Kücher, A., & Duller, C. (2021). Entrepreneur characteristics and differences in reasons for business failure: Evidence from bankrupt Austrian SMEs. Journal of Small Business & Entrepreneurship, 33(5), 539–558. https://doi.org/10.1080/08276331.2020.1786647

- Mbilla, S., Nyeadi, J. D., Gbegble, M. K., & Ayimpoya, R. N. (2020). Assessing the impact of monitoring, information and communication on banks performance in Ghana. Asian Journal of Economics, Business and Accounting, 14(3), 58–71. https://doi.org/10.9734/ajeba/2020/v14i330197

- Memon, M. A., Ramayah, T., Cheah, J. H., Ting, H., Chuah, F., & Cham, T. H. (2021). PLS-SEM statistical programs: A review. Journal of Applied Structural Equation Modeling, 5(1), 1–14. https://doi.org/10.47263/JASEM.5(1)06

- Merendino, A., & Melville, R. (2019). The board of directors and firm performance: Empirical evidence from listed companies. Corporate Governance: The International Journal of Business in Society, 19(3), 508–551. https://doi.org/10.1108/CG-06-2018-0211

- Motta, V., & Sharma, A. (2020). Lending technologies and access to finance for SMEs in the hospitality industry. International Journal of Hospitality Management, 86, 102371. https://doi.org/10.1016/j.ijhm.2019.102371

- Murphy, G. B., Trailer, J. W., & Hill, R. C. (1996). Measuring performance in entrepreneurship research. Journal of Business Research, 36(1), 15–23. https://doi.org/10.1016/0148-2963(95)00159-X

- Nunnally, J. C., & Bernstein, I. H. (1994). Psychometric Theory. In McGraw-Hill. McGraw-Hill.

- Okundaye, K., Fan, S. K., & Dwyer, R. J. (2019). Impact of information and communication technology in Nigerian small-to-medium-sized enterprises. Journal of Economics, Finance and Administrative Science, 24(47), 29–46. https://doi.org/10.1108/JEFAS-08-2018-0086

- Osim, E., Umoffong, N. J., & Goddymkpa, C. P. (2020). Management accounting practices and the performance of small and medium-sized enterprises in Akwa Ibom State, Nigeria. Business Perspective Review, 2(2), 57–74. https://doi.org/10.38157/business-perspective-review.v2i2.153

- Panda, B., & Leepsa, N. M. (2017). Agency theory: Review of theory and evidence on problems and perspectives. Indian Journal of Corporate Governance, 10(1), 74–95. https://doi.org/10.1177/0974686217701467

- Paul, L. Y. (2018). Information And Communication Technology Usage And financial Performance Of Small And Medium-Sized Enterprises In (Doctoral Dissertation, Department Of Accounting And Finance In Partial Fulfillment Of The Requirement For The Award Of The Degree Of Masters Of Business Administration (Management Information System Option), Kenyatta University).

- Pedroso, E., Gomes, C. F., & Yasin, M. M. (2020). Management accounting systems: An organisational competitive performance perspective. Benchmarking: An International Journal, 27(6), 1843–1874. https://doi.org/10.1108/BIJ-12-2019-0547

- Perrow, C. (1986). Complex organizations. Random House.

- Purwanto, A., & Sudargini, Y. (2021). Partial least squares structural squation modeling (PLS-SEM) analysis for social and management research: A literature review. Journal of Industrial Engineering & Management Research, 2(4), 114–123. https://doi.org/10.7777/jiemar.v2i4.168

- Rita, M. R., & Huruta, A. D. (2020). Financing access and SME performance: A case study from batik SME in Indonesia. International Journal of Innovation, Creativity and Change, 12(12), 203–224. https://www.researchgate.net/publication/341232526

- Ruiz, T. N., & Collazzo, P. (2020). Management accounting use in micro and small enterprises. In Qualitative Research in Accounting & Management. https://www.emerald.com/insight/1176-6093.htm

- Sandberg, W. R., & Hofer, C. W. (1987). Improving new venture performance: The role of strategy, industry structure, and the entrepreneur. Journal of Business Venturing, 2(1), 5–28. https://doi.org/10.1016/0883-9026(87)90016-4

- Sarstedt, M., Ringle, C. M., & Hair, J. F. (2021). Partial least squares structural equation modeling. In Handbook of market research (pp. 587–632). Springer International Publishing. https://doi.org/10.1007/978-3-319-57413-4_15

- Shi, W., Connelly, B. L., & Hoskisson, R. E. (2017). External corporate governance and financial fraud: Cognitive evaluation theory insights on agency theory prescriptions. Strategic Management Journal, 38(6), 1268–1286. https://doi.org/10.1002/smj.2560

- Sotarauta, M., & Grillitsch, M. (2020). Trinity of change agency, regional development paths and opportunity spaces. Progress in Human Geography, 44(4), 704–723. https://doi.org/10.1177/0309132519853870

- Stefanic, N., & Randles, C. (2015). Examining the reliability of scores from the consensual assessment technique in the measurement of individual and small group creativity. Music Education Research, 17(3), 278–295. https://doi.org/10.1080/14613808.2014.909398

- Tarutė, A., & Gatautis, R. (2014). ICT impact on SMEs performance. Procedia - Social and Behavioral Sciences, 110, 1218–1225. https://doi.org/10.1016/j.sbspro.2013.12.968

- Teece, D. J. (2019). A capability theory of the firm: An economics and (strategic) management perspective. New Zealand Economic Papers, 53(1), 1–43. https://doi.org/10.1080/00779954.2017.1371208

- Turnbull, S. (2019). Corporate governance. Taylor and Francis. 9781315191157.

- Vinodh, S., & Joy, D. (2012). Structural Equation Modelling of Lean Manufacturing Practices. International Journal of Production Research, 50(6), 1598–1607. https://doi.org/10.1080/00207543.2011.560203

- Vitolla, F., Raimo, N., & Rubino, M. (2020). Board characteristics and integrated reporting quality: An agency theory perspective. Corporate Social Responsibility and Environmental Management, 27(2), 1152–1163. https://doi.org/10.1002/csr.1879

- World Bank. (2015). Small and medium enterprises (SMEs) finance resource document.

- Yamane, T. (1967). Elementary Sampling Theory. Prentice-Hall, Inc.

- Zogning, F. (2017). Agency theory: A critical review. European Journal of Business and Management, 9(2), 1–8. .