Abstract

The purpose of this study is to examine the role of budgetary participation of employees in boosting their performance and through mental model and individual creativity. To address this research question, the study conducts a survey among 78 municipal officers from Lampung regional province using smartPLS method. The study shows that budgetary participation could improve individual performance through mental model building and individual creativity. The direct correlation between budgetary participation and individual performance could be proved statistically. The study reveals that budgetary participation could improve mental model building which in turn will boost individual creativity and performance. This research is the first to empirically examine the positive effect of mental model and creativity for the positive correlation between participation in decision making and individual performance in municipal government.

1. Introduction

In the management and accounting literature, the importance of the role of budgeting participation in the improvement of individual performance has been widely discussed (Uyar & Kuzey, Citation2016; Winata & Mia, Citation2005; Wong-On-Wing et al., Citation2010; Yuliansyah & Khan, Citation2017; Yuliansyah et al., Citation2019). Additionally, Wong-On-Wing et al. (Citation2010), for example, confirm that budgeting participation supports managers to improve individual learning through their intrinsic and extrinsic motivations. Furthermore, Winata and Mia (Citation2005, p. 24) point out that ‘from an individual employee’s point of view, budgetary participation is the process of developing an individual’s mental and emotional feelings that provide them with ownership of their decisions’. In addition, generating learning process through mental confirmation and mental building stimulate individual creativity that can impact on individual performance. However, study that seeks the development of mental model is relatively new and it still provides wide room for discussion in the management study. Thus, this study attempts to investigate how participate in budgeting can improve learning through mental model that can impact on individual creativity which in turn the higher performance.

Confirming and updating their mental models of how the organization runs is a crucial part of the learning process for managers (Hall, Citation2011). Participation in decision making has the potential to encourage learning process in individuals by sharing experience and ideas that can confirm and build mental model. In addition, some forms of data from the results of participation in budgeting would be very beneficial in supporting and building managers’ mental models of business operations (Hall, Citation2011). Further, mental model confirmation and building can facilitate individual to be creative. Previous studies confirms that mental model could accelerate learning process by which will boost capabilities to generate new ideas of product and service in the organization (Easterby-Smith, Citation1997; Hult et al., Citation2001). Lastly, it can also enhance job performance.

This study has several contributions. First, we provide a contribution how participation, mental model, and creativity improve job performance. Though previous studies have extensively identified the impact of participation in budgeting on managerial performance, however, research on the combination of the effect of participation in budgeting on job performance which is mediated by mental model and creativity is sparse.

Second contribution is related to public sector. Previous author contented to investigate the relationship between budgetary participation and individual performance by focusing on manufacturing sector (Kihn, Citation2010; Shields, Citation1997; Winata & Mia, Citation2005; Zawawi & Hoque, Citation2010) and less in public sector (Kihn, Citation2010) while this study contributes to management accounting literature in the public sector. The presence of this research gap has been voiced out by Kihn (Citation2010, p. 484) that “A number of gaps and under-researched yet important areas in the literature were also identified in existing management accounting research. They include: ‘[…] analysis of specific important, but under-researched samples (such as […], not-for-profit organizations, […]”.

This paper is organized as follows: Section 1 gives a brief introduction to the paper and subject matter. Section 2 provides a description of review of literature and hypotheses development. Section 3 explains the research method. Section 4 illustrates the result of the study. Finally Section 5 concludes the article.

2. Literature review

Many theorists argue that Budgeting is a prominent tool for the controlling, planning and coordinating of the firm’s operation (Lau & Lim, Citation2002; Lau et al., Citation2018; Uyar & Kuzey, Citation2016). From management perspective, participation in budgeting can help organisation’s efficiency and effectiveness to develop a sustainable and competitive company by controlling costs, monitoring and evaluating units of organisation, accomplishing targets and improving market share (Uyar & Kuzey, Citation2016). In addition, based on individual perspective, participation in budgeting has a prominent advantage for employees. It can improve behaviour outcomes for employees including organisational commitment, trust, self-efficacy, reduced stress, boosting sense of belonging, which in turn improving performance (Selvina & Yuliansyah, Citation2016; Yuliansyah & Khan, Citation2017). However, study between budgeting and performance does not propose direct effect between these factors. (Derfuss, Citation2016). Derfuss (Citation2016, p. 22) suggest that “the relation is described as being contingent on and mediated by other variables”. Hence, in this study, we could claim that participation in budgeting can improve individual mental model by generating learning and exchanging information that lead to the improvement of individual creativity to raise job performance.

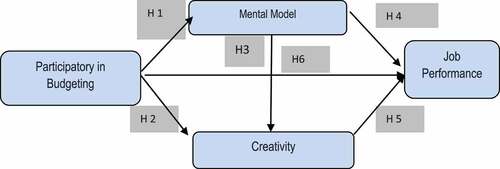

Previous studies note that participation in budgeting process and performance in decision making may transfer of knowledge between senior management and sub-ordinate. This way promotes experiential learning about reflection of previous business activities and transform a mutual understanding for better future activities (See Figure ).

Figure 1. Conceptual Framework.

Based on above explanation, we draw a research framework as follows:

2.1. Participation in budgeting and mental model

Participation in budgeting could improve learning process through dialogue forum and communication to acquire and store information in producing the expected goal (Yuliansyah & Khan, Citation2017; Yuliansyah et al., Citation2019). Sitepu et al. (Citation2020) stated that among the benefits of budgeting participation is boosting individual capabilities in expressing ideas and suggestion for generating useful output of the company.

Based on this conducive process, budgeting participation becomes an important mechanism in developing mental model for individuals to perceive how the budgeting process took place. (Hall, Citation2011). Furthermore, Hall (Citation2011) stated that a dynamic process in budgeting participation in decision making creates mental model of managers how they transform their understanding over the time.

From psychology-based budgeting, point of view Covaleski et al. (Citation2003) argued that budgeting participation could affect mental model particularly on individual attitudes and behaviour in running the business. This in turn will promote a more conduce organization environment by inter-individual interactive dialogue (Chong & Mahama, Citation2014). Budgeting participation could also contribute positively to mental model development by direct learning process of individual in budgeting itself. Based on this explanation, we propose the following hypothesis:

H1: There is a positive effect between Participation in budgeting and mental model

2.2. Participation in budgeting and creativity

Budgeting participation is a process where staff voice out their previous activities for future program. Previous authors note that employees that don’t not provided “space” to voice their argument, it may reduce their creativity (Guo et al., Citation2018). By budgeting participation managers and staff will share knowledge and experiment to project new agenda or business activities in future. Sharing knowledge including debate and dialog between upper and subordinate may generate new information and learning for organization (Jansen, Citation2015).

Jansen (Citation2015) also notes individuals’ voice in decision-making process could help to achieve their organisation goals and objectives. Another aspect when senior managers allow employees to participate in budgeting, it creates a “sense of belonging” among individuals in organisation. By which budgeting participation could stimulate individual creativity by offering new insight and suggestion to the organization. Thus, we hypothesise as follows

H2: There is a positive effect between Participation in budgeting and Creativity

2.3. Mental model and creativity

Mental model is expected to increase individual creativity. This can be understood by following logic (1) managements developed mental model in the organization based on their previous experiments and existing information in business process (Hall, Citation2011) then these experiences and information developed as learning mechanism to produce new ideas (Chenhall, Citation2005; Yuliansyah & Jermias, Citation2018). Hall (Citation2011) also stated that among the benefits of mental model is to facilitate learning process that could promote fresh ideas in business operation and strategy that may occurs over periods and situations. By this we confirm that mental model could promote creativity. Based on these arguments we can safely conclude that mental model has a positive correlation with creativity. Hence we propose a hypothesis that.

H3: There is a positive effect between mental model and Creativity

2.4. Mental model and job performance

Lim and Klein (Citation2006) argued that individual mental model influences individual performance. Hall (Citation2011) says that organization that have better learning can raise better performance compared to organization with less learning mechanism. Similar to Yuliansyah and Jermias (Citation2018), also identified that ability of learning can change individual behavior to learn to solve operational problems from prior experience of their peer individuals or seniors. This interaction could develop individual mental model to generate new insights of knowledge (Yuliansyah & Khan, Citation2015).

Briefly, previous studies show that there is a positive effect of mental model on job performance. Study conducted by Hall (Citation2011) found that mental model can help the improvement of individual performance. Lim and Klein (Citation2006)’s study identified that mental model in team can improve team performance. Capelo and Dias (Citation2009) found that there is a positive effect between mental model and performance. Based on above argument, we propose the following hypothesis.

H4: There is a positive effect between mental model and Job performance

2.5. Creativity and job performance

Amabile (Citation1988, p. 126) said that creativity is the production of novel and useful ideas by an individual or small groups of individuals working together. We assume that the main purpose of creativity is to find ideas to the working improvement. Furthermore, creativity is a way to improve job performance (Choi et al., Citation2019; Sue‐Chan & Hempel, Citation2016). In this assumption, creativity and performance are linked to one to another.

Empirical study found that creativity can enhance performance. For example, study undertaken by Shahzad et al. (Citation2016) found that creativity can improve performance. Alzghoul et al. (Citation2018)’s study in two Jordanian telecommunication firms found that creativity can improve job performance. Based on these two examples, we propose:

H5: There is a positive effect between creativity and Job performance

2.6. Participation in budgeting and job performance

It is argued that allowing subordinate to participate in decision-making process will enable them to increase their job performance (Chong et al., Citation2005; Yuliansyah et al., Citation2018b, Citation2019). There are several reasons how participation in budgeting can improve job performance. One example for that is job-relevant information. When individual involve in budgeting preparation, they automatically generate and share information about budgeting process (Chong et al., Citation2005; Groen et al., Citation2017; Kren, Citation1992; Shields & Shields, Citation1998). Study from Kren (Citation1992), Chong et al. (Citation2005) found that when management allows subordinates to participate in decision making they have more information about their jobs which in turn could improve their job performances.

Another reason for positive impact of budgeting involvement in job performance improvement is because participation in budgeting can improve individual job satisfaction, fairness self-efficacy, role clarity, organisational commitment, and trust by which could lead to the improvement of performance (Chong et al., Citation2005; Lau & Buckland, Citation2001; Lau & Tan, Citation2003, Citation2012, Citation2006; Yuliansyah et al., Citation2018b; Yuliansyah & Khan, Citation2017). Giving an example from study undertaken by Lau and Tan (Citation2012) the budgetary participation can improve job performance and job fairness. Based on this argument, we propose the following hypothesis:

H6: There is a positive effect between Participation in budgeting and Job performance

3. Research method

3.1. Sample selection

This research is a quantitate study. We do a survey study in 8 municipals in the province of Lampung—Indonesia. A survey research is extensively used in academia and is crucial for gathering data. There are two reasons or the extensive use of survey study. First, there is the significantly reduced cost involved in completing them; second, the procedures for surveys are frequently seen to be straightforward enough that people and organizations (Dillman, Citation1991). In order to increase the validity of sample study, we select samples with experience of involvement in budgeting process in their respected offices. Samples that have no experience in budgeting process are excluded from the study. To do our survey, we follow the best survey practice from previous study (Yuliansyah, Citation2016; Yuliansyah et al., Citation2018a).

Firstly, we do pre-test study to ensure validity and reliability of the study. Van der Stede et al.’s (Citation2005, p. 670) suggestion that “pre-testing is especially important in mail surveys because there are no interviewers to report problems in the questions and the survey instrument to the researcher”. In addition, following Van der Stede et al. (Citation2005, p. 670), we eliminate poor quality of survey study and use a common language. Secondly, we follow Henri (Citation2006)’s four steps of survey: pre-notification, initial mailing, first follow up, and second follow up. Based on 200 distributed questionaries; we obtained usable data from 78 out of 79 respondents (39%). Table illustrates the respondents’ demographics

Table 1. Respondents’ demographics

3.2. Variable measurements

3.2.1. Budgetary participation

Budgetary participation applies a six-item questionnaire which was developed by Milani (Citation1975). Its variable has been used by previous studies (e.g., Chong et al., Citation2006; Yuliansyah & Khan, Citation2017; Yuliansyah et al., Citation2019). In this study, respondents were asked to indicate their perception using a 5-point likert scale anchored 1 (very disagree) to 5 (very agree)

3.2.2. Mental model

We apply a seven-item questionnaire of mental model Hall (Citation2011). This variable consists of two dimensions: a three-item question of mental model confirmation and a four-item question of mental model building. In this study respondent is asked to rate their agreement of each item using a 5 Likert-scale anchored from 1 (very disagree) to 5 (very agree).

3.2.3. Creativity

Employee creativity uses instrument which was developed by Moulang (Citation2013) based on previous studies such as Spreitzer (Citation1995), Wang and Netemeyer (Citation2004), and Denison et al. (Citation1995). This study uses only six questions to ask respondent opinion using a five-point likert scale with anchors 1 = almost never to 5 almost always.

3.2.4. Job performance

Job performance questionnaire in this study is generated from Burney et al. (Citation2009) which was initially developed by Williams and Anderson (Citation1991). Based on a seven-item question, we ask respondent to answer how far their individual performance in this period compared to the last period using a 5 likert-scale anchored from 1 (far below average) to 5 (far above average).

4. Partial least square

In order to reach the goals of the study, we test data using SmartPLS. Advantages of SmartPLS is that appropriate for 1) small sample, 2) non-normal data, and 3) theory development (Faizan et al., Citation2018; Hair et al., Citation2012; Henseler et al., Citation2009). Some scholars such as Smith and Langfield-Smith (Citation2004), Hulland (Citation1999), and Sarstedt and Cheah (Citation2019) and others note that testing using SmartPLS follows a two-sequential step: measurement model and structural model.

4.1. Measurement model

The aim of measurement model in Partial Least Square is to ensure whether reliability and validity are good. Measurement reliability can be generated by evaluating composite reliability and Cronbach’ alpha. Both indicators have good score when the value of construct is higher than 0.7. Table shows that the scores of composite reliability and Cronbach’ alpha of each construct are more than 0.7. This indicates reliability is adequate.

Table 2. Factor loadings, Composite Reliability, Cronbach’s Alpha and AVE

Measurement model of validity is conducted by testing convergent and discriminant validity. Measurement model of convergent validity can be seen by the score of Average Variance Extracted (AVE) which is more than 0.5. A way of compensating for small sample size in SEM is to use bootstrapping. Bootstrapping is a resampling procedure in which the researcher’s data set is treated as population(Smith & Langfield-Smith, Citation2004, p. 66)

4.2. The assesment of structural model

A discriminant validity test is another validity evaluation. It is possible to achieve discriminant validity using the Fornell-Larcker Criteria. If the diagonal line of AVE2 is higher than the AVE2's vertical and horizontal lines, this indicates good discriminant validity. According to Table , all AVE2 values for each item (in bold) appear to be higher than the sum of all vertical and horizontal scores for the row and column items. Fornell-Larcker discriminant validity is adequate.

Table 3. Fornel Larcker criterion

The assesment of the structural model was conducted by evaluating the R-squared(R2) of each dependent variable and its path coefficient. Camisón and López (Citation2010) suggest that an R2 higher than 0.1 is considered acceptable. As shown in Table , all the R2 are higher than 0.1 indicating that the structural model used in this study is acceptable.

Table 4. The result of PLS structural model: path coefficient, and t-statistics

4.3. Test of hypothesis

4.3.1. Participation in budgeting and mental model

Hypothesis 1 states that there is a positive relation between participation in decision making and mental model. Our study found that participation in decision making has a positive and significant relation with all components of mental model confirmation (β = 0. 0.569; t = 6.046; p < 0.01), and mental model building (β = 0.675; t = 9.672; p < 0.01). These results are consistent with H1.

4.3.2. Participation in budgeting and creativity

Hypothesis 2 states that there is a positive relation between participation in decision making and employee’s creativity. As seen in Table that participation in decision making has a no positive effect on individual creativity (β = 0.140; t = 1.534; p < 0.10). Thus, hypothesis 2 is rejected

4.3.3. Mental model and creativity

Hypothesis 3 states that there is a positive relation between mental model and individual creativity. Table indicates that mental model confirmation has no positive effect on individual creativity (β = 0.177; t = 1.513; p < 0.10), but mental model building has a positive effect on individual creativity (β = 0.557; t = 4.656; p < 0.01). Thus, hypothesis 3 is partly supported.

4.3.4. Mental model and job performance

Hypothesis 4 states that there is a positive relation between mental model and job performance. The results reported in Table indicate that mental model confirmation has no positive effect on job performance (β = 0.040; t = 0.343; p < 0.10), this is also similar to mental model building and job performance (β = 0.242; t = 1.491; p < 0.10). Thus, H4 is rejected.

4.3.5. Creativity and job performance

Hypothesis 5 states that there is a positive relation between individual creativity and job performance. The result of the study finds that there is a positive effect between them (β = 0.547; t = 3.511; p < 0.01). Thus, hypothesis 5 is accepted.

4.3.6. Participation in budgeting and job performance

Hypothesis 6 states that there is a positive relation between participation in decision making and job performance. The results reported in Table shows that participation in budgeting has no a positive effect on job performance (β = 0.063; t = 0.718; p < 0.10), Thus, Hypothesis 6 is rejected.

4.3.7. Path analysis

In order to analyze the path, we follow Baron and Kenny (Citation1986)’s suggestion. They note that path analysis can be conducted if all direct and indirect path is supported. Based on the study we found that direct effect between budgetary participation and job performance is rejected and indirect path is supported. Thus, we do need to do further analysis of path test. Hence, in this study, there are full mediation of the study.

5. Discussion and conclusion

Participation in budgeting is a prominent way to improve learning among employees. Much organization facilitates this way to generate information from internal experience and knowledge to pursue organization goal. Hall (Citation2011) notes that this learning can build and confirm mental model. Previous study found that improving learning can stimulate creativity among employees that can impact on the improvement of employees. This study aims to investigate the extent to which participation in budgeting can improve individual performance through mental model and creativity.

In order to pursue the purpose of the study, authors do study of public sector employees in the eight municipals in the Province of Lampung—Indonesia. Distributing 200 questionnaires to them, we collected a 78 usable data from 79 received respondents. Then, those data were analyzed using smartPLS using a two-step process: measurement model and structural model then followed by testing hypotheses. The study found that participation in budgeting can help mental model of employees that lead to the improvement of individual creativity, which in turn on the improvement of job performance. However, a direct effect between participation in budgeting and job performance in this study doesn’t not exist. Even, engagement in budgeting stimulates creativity, but only through the development of mental models.

This study concludes that participation in budgeting helps management in public sector to increase individual learning process that forms mental model. Mental model is a primary source to organisation in stimulating individual creativity. Psychological effect on individual participation in decision making will stimulate greater morale to learn that effect on an increase in individual self-efficacy to be creative that lead to the improvement of job performance. Our study differs from other studies from the perspectives of behavioural management and psychological research in terms of both the theoretical framework and the nature of the variables included in the model. This study confirms a previous study that mental model enable to increase managerial performance in Australian manufacturing industries (Hall, Citation2011). In addition Hall (Citation2011) notes that given the significant impact of mental model creation and confirmation on individual performance, the study suggests there is much to be learned from examining the ways in which these two types of managers’ learning capacities may be enhanced through participation in budgeting.

Like other empirical research studies, this study has some limitations. Firstly, this study is conducted in municipal institution where it has different in private sector. Thus, this study needs careful attention to be generalised in the private sector. Further, using the same model can be a good idea to be conducted to confirm an external validity of the study in different angle sectors. Second limitation is about research method. Although some scholars note that survey study has a strong generalisation of the results, it has some limitation in terms of deep results about factors that can build mental model and creativity that lead to the improvement of job performance. Hence, for future study, it suggests to do another method such as qualitative study to generate deep result of those factors.

This study implies that organization in public sector may allow a member of organisation to participate in decision making that not only can improve an individual performance but it also can help improve their mental model and creativity.

Disclosure statement

No potential conflict of interest was reported by the author(s)

Additional information

Funding

References

- Alzghoul, A., Elrehail, H., Emeagwali Okechukwu, L., & AlShboul Mohammad, K. (2018). Knowledge management, workplace climate, creativity and performance: The role of authentic leadership. Journal of Workplace Learning, 30(8), 592–12. https://doi.org/10.1108/JWL-12-2017-0111

- Amabile, T. M. (1988). A model of creativity and innovation in organizations. Research in Organizational Behavior, 10(1), 123–167.

- Baron, R., & Kenny, D. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037/0022-3514.51.6.1173

- Burney, L. L., Henle, C. A., & Widener, S. K. (2009). A path model examining the relations among strategic performance measurement system characteristics. Organizational Justice, and Extra- and in-role Performance. Accounting, Organizations and Society, 34(3–4), 305–321. https://doi.org/10.1016/j.aos.2008.11.002

- Camisón, C., & López, A. V. (2010). An examination of the relationship between manufacturing flexibility and firm performance: The mediating role of innovation. International Journal of Operations & Production Management, 30(8), 853–878. https://doi.org/10.1108/01443571011068199

- Capelo, C., & Dias, J. F. (2009). A system dynamics‐based simulation experiment for testing mental model and performance effects of using the balanced scorecard. System Dynamics Review: The Journal of the System Dynamics Society, 25(1), 1–34. https://doi.org/10.1002/sdr.413

- Chenhall, R. H. (2005). Integrative strategic performance measurement systems, strategic alignment of manufacturing, learning and strategic outcomes: An exploratory study. Accounting, Organizations and Society, 30(5), 395–422. https://doi.org/10.1016/j.aos.2004.08.001

- Choi, J., Rhee, M., & Kim, Y.-C. (2019). Performance feedback and problemistic search: The moderating effects of managerial and board outsiderness. Journal of Business Research, 102, 21–33. https://doi.org/10.1016/j.jbusres.2019.04.039

- Chong, V. K., Eggleton, I. R., & Leong, M. K. (2005). The effects of value attainment and cognitive roles of budgetary participation on job performance. Advances in Accounting Behavioral Research, 213–233. https://doi.org/10.1016/S1475-1488(04)08009-3

- Chong, V. K., Eggleton, I. R., & Leong, M. K. (2006). The multiple roles of participative budgeting on job performance. Advances in Accounting, 22, 67–95. https://doi.org/10.1016/S0882-6110(06)22004-2

- Chong, K. M., & Mahama, H. (2014). The impact of interactive and diagnostic uses of budgets on team effectiveness. Management Accounting Research, 25(3), 206–222. https://doi.org/10.1016/j.mar.2013.10.008

- Covaleski, M. A., Evans, J. H., Luft, J. L., & Shields, M. D. (2003). Budgeting research: Three theoretical perspectives and criteria for selective integration. Journal of Management Accounting Research, 15(1), 3–49. https://doi.org/10.2308/jmar.2003.15.1.3

- Denison, D. R., Hooijberg, R., & Quinn, R. E. (1995). Paradox and performance: Toward a theory of behavioral complexity in managerial leadership. Organization Science, 6(5), 524–540. https://doi.org/10.1287/orsc.6.5.524

- Derfuss, K. (2016). Reconsidering the participative budgeting-performance relation: A meta-analysis regarding the impact of level of analysis, sample selection, measurement, and industry influences. The British Accounting Review, 48(1), 17–37. https://doi.org/10.1016/j.bar.2015.07.001

- Dillman, D. A. (1991). The design and administration of mail surveys. Annual Review of Sociology, 17(1), 225–249. https://doi.org/10.1146/annurev.so.17.080191.001301

- Easterby-Smith, M. (1997). Disciplines of organizational learning: contributions and critiques. Human Relations, 50(9), 1085–1113. https://doi.org/10.1177/001872679705000903

- Faizan, A., Mostafa, R. S., Marko, S., Kisang, R., & Ryu, K. (2018). An assessment of the use of partial least squares structural equation modeling (PLS-SEM) in hospitality research. International Journal of Contemporary Hospitality Management, 30(1), 514–538. https://doi.org/10.1108/IJCHM-10-2016-0568

- Groen, B. A., Wouters, M. J., & Wilderom, C. P. (2017). Employee participation, performance metrics, and job performance: A survey study based on self-determination theory. Management Accounting Research, 36, 51–66. https://doi.org/10.1016/j.mar.2016.10.001

- Guo, L., Decoster, S., Babalola, M. T., Schutter, L. D., Garba, O. A., & Riisla, K. (2018). Authoritarian leadership and employee creativity: The moderating role of psychological capital and the mediating role of fear and defensive silence. Journal of Business Research, 92, 219–230. https://doi.org/10.1016/j.jbusres.2018.07.034

- Hair, J. F., Sarstedt, M., Ringle, C. M., & Mena, J. A. (2012). An assessment of the use of partial least squares structural equation modeling in marketing research. Journal of the Academic Marketing. Sciece, 40(3), 414–433. https://doi.org/10.1007/s11747-011-0261-6

- Hall, M. (2011). Do comprehensive performance measurement systems help or hinder managers’ mental model development? Management Accounting Research, 22(2), 68–83. https://doi.org/10.1016/j.mar.2010.10.002

- Henri, J.-F. (2006). Management control systems and strategy: A resource-based perspective. Accounting. Organizations and Society, 31(6), 529–558. https://doi.org/10.1016/j.aos.2005.07.001

- Henseler, J., Ringle, C., & Sinkovics, R. (2009). The use of partial least squares path modeling in international marketing. Advances in Intenational Marketing, 20, 277–319. https://doi.org/10.1108/S1474-7979(2009)0000020014

- Hulland, J. (1999). Use of partial least squares (PLS) in strategic management research: A review of four recent studies. Strategic Management Journal, 20(2), 195–204. https://doi.org/10.1002/(SICI)1097-0266(199902)20:2<195::AID-SMJ13>3.0.CO;2-7

- Hult, G., Ketchen, J., & David, J. (2001). Does Market orientation matter?: A test of the relationship between positional advantage and performance. Strategic Management Journal, 22(9), 899–906. https://doi.org/10.1002/smj.197

- Jansen, E. P. (2015). Participation, accounting and learning how to implement a new vision. Management Accounting Research, 29, 45–60. https://doi.org/10.1016/j.mar.2015.07.003

- Kihn, L. A. (2010). Performance outcomes in empirical management accounting research: Recent developments and implications for future research. International Journal of Productivity and Performance Management, 59(5), 468–492. https://doi.org/10.1108/17410401011052896

- Kren, L. (1992). Budgetary participation and managerial performance: The impact of information and environmental volatility. The Accounting Review, 67(3), 511–526.

- Lau, C. M., & Buckland, C. (2001). Budgeting-the role of trust and participation: A research note. Abacus, 37(3), 369–388. https://doi.org/10.1111/1467-6281.00092

- Lau, C. M., & Lim, E. W. (2002). The effects of procedural justice and evaluative styles on the relationship between budgetary participation and performance. Advances in Accounting, 19, 139–160. https://doi.org/10.1016/S0882-6110(02)19008-0

- Lau, C. M., Scully, G., & Lee, A. (2018). The effects of organizational politics on employee motivations to participate in target setting and employee budgetary participation. Journal of Business Research, 90, 247–259. https://doi.org/10.1016/j.jbusres.2018.05.002

- Lau, C. M., & Tan, S. L. (2003). The effects of participation and job-relevant information on the relationship between evaluative style and job satisfaction. Review of Quantitative Finance and Accounting, 21(1), 17–34. https://doi.org/10.1023/A:1024803621137

- Lau, C. M., & Tan, S. L. C. (2006). The effects of procedural fairness and interpersonal trust on job tension in budgeting. Management Accounting Research, 17(2), 171–186. https://doi.org/10.1016/j.mar.2005.10.001

- Lau, C. M., & Tan, S. L. (2012). Budget targets as performance measures: The mediating role of participation and procedural fairness. Advances in Management Accounting, 151–185. https://doi.org/10.1108/S1474-7871(2012)0000020013

- Lim, B.-C., & Klein, K. J. (2006). Team mental models and team performance: A field study of the effects of team mental model similarity and accuracy. Journal of Organizational Behavior, 27(4), 403–418. https://doi.org/10.1002/job.387

- Milani, K. (1975). The relationship of participation in budget-setting to industrial supervisor performance and attitudes: A field study. The Accounting Review, 50(2), 274–284. https://doi.org/10.1111/acfi.12059

- Moulang, C. (2013). Performance measurement system use in generating psychological empowerment and individual creativity. Accounting & Finance.

- Sarstedt, M., & Cheah, J.-H. (2019). Partial least squares structural equation modeling using SmartPLS: A software review. Journal of Marketing Analytics, 7(3), 196–202. https://doi.org/10.1057/s41270-019-00058-3

- Selvina, M., & Yuliansyah, Y. (2016). Relationships between budgetary participation and organizational commitment: Mediated by reinforcement contingency evidence from the service sector industries. International Research Journal of Business Studies, 8(2), 69–80. https://doi.org/10.21632/irjbs.8.2.69-80

- Shahzad, K., Bajwa, S. U., Siddiqi, A. F. I., Ahmid, F., & Sultani, A. R. (2016). Integrating knowledge management (KM) strategies and processes to enhance organizational creativity and performance. Journal of Modelling in Management, 11(1), 154–179. https://doi.org/10.1108/JM2-07-2014-0061

- Shields, M. D. (1997). Research in management accounting by North Americans in the 1990s. Journal of Management Accounting Research, 9, 3–61.

- Shields, J. F., & Shields, M. D. (1998). Antecedents of participative budgeting. Accounting. Organizations and Society, 23(1), 49–76. https://doi.org/10.1016/S0361-3682(97)00014-7

- Sitepu, E. M. P., Appuhami, R., & Su, S. (2020). How does interactive use of budgets affect creativity? Pacific Accounting Review, 32(2), 197–215. https://doi.org/10.1108/PAR-05-2019-0054

- Smith, D., & Langfield-Smith, K. (2004). Structural equation modeling in management accounting research: Critical analysis and opportunity. Journal of Accounting Literature, 23, 49–89.

- Spreitzer, G. M. (1995). Psychological empowerment in the workplace: Dimensions, measurement, and validation. Academy of Management Journal, 38(5), 1442–1465. https://doi.org/10.2307/256865

- Sue‐Chan, C., & Hempel, P. S. (2016). The creativity‐performance relationship: How rewarding creativity moderates the expression of creativity. Human Resource Management, 55(4), 637–653. https://doi.org/10.1002/hrm.21682

- Uyar, A., & Kuzey, C. (2016). Contingent factors, extent of budget use and performance: A structural equation approach. Australian Accounting Review, 26(1), 91–106. https://doi.org/10.1111/auar.12090

- Van der Stede, W. A., Young, S. M., & Chen, C. X. (2005). Assessing the quality of evidence in empirical management accounting research: The case of survey studies. Accounting. Organizations and Society, 30(7–8), 655–684. https://doi.org/10.1016/j.aos.2005.01.003

- Wang, G., & Netemeyer, R. G. (2004). Salesperson creative performance: Conceptualization, measurement, and nomological validity. Journal of Business Research, 57(8), 805–812. https://doi.org/10.1016/S0148-2963(02)00483-6

- Williams, L. J., & Anderson, S. E. (1991). Job satisfaction and organizational commitment as predictors of organizational citizenship and in-role behaviors. Journal of Management, 17(3), 601–617. https://doi.org/10.1177/014920639101700305

- Winata, L., & Mia, L. (2005). Information technology and the performance effect of managers’ participation in budgeting: Evidence from the hotel industry. International Journal of Hospitality Management, 24(1), 21–39. https://doi.org/10.1016/j.ijhm.2004.04.006

- Wong-On-Wing, B., Lan, G., & Lui, G. (2010). Intrinsic and extrinsic motivation and participation in budgeting: Antecedents and consequences. Behavioral Research in Accounting, 22(2), 133–153. https://doi.org/10.2308/bria.2010.22.2.133

- Yuliansyah, A. (2016). Meningkatkan response rate dalam penelitian survey: Suatu study literature. Smart Publisher.

- Yuliansyah, Y., Hariri, H., & Razimi, M. S. (2018a). Comprehensive strategy to conduct a mail survey: Techniques to improve response rates. International Journal of Management and Business Research, 8(4), 89–96.

- Yuliansyah, Y., Inapty, B. I., Dahlan, M., & Agtia, I. O. (2018b). Budgetary participation and its impact on individual performance. Tourism and Hospitality Management, 24(2), 325–340. https://doi.org/10.20867/thm.24.2.10

- Yuliansyah, Y., & Jermias, J. (2018). Strategic performance measurement system, organizational learning and service strategic alignment: Impact on performance. International Journal of Ethics and Systems, 34(4), 564–592. https://doi.org/10.1108/IJOES-07-2018-0102

- Yuliansyah, Y., & Khan, A. (2015). Interactive use of performance measurement systems and the organization’s customers-focused strategy: The mediating role of organizational learning. Problems and Perspectives in Management, 13(2), 219–229.

- Yuliansyah, Y., & Khan, A. (2017). A re-visit of the participative budgeting and employees’ self-efficacy interrelationship –Empirical evidence from Indonesia’s public sector. International Review of Public Administration, 22(3), 213–230. https://doi.org/10.1080/12294659.2017.1325584

- Yuliansyah, Y., Triwacananingrum, W., Mohd-Sanusi, Z., & Said, J. (2019). Enhancing task performance of bank employees: The relevance of trust, self-efficacy and budget participation. International Journal of Business Excellence, 17(4), 397–413. https://doi.org/10.1504/IJBEX.2019.099122

- Zawawi, N. H. M., & Hoque, Z. (2010). Research in management accounting innovations: An overview of its recent development. Qualitative Research in Accounting & Management, 7(4), 505–568. https://doi.org/10.1108/11766091011094554