?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The purpose of this study is to find out how the positive influence of corporate sustainable development on corporate financial performance alters during the two recent crises i.e. the global recession (2008–10) and COVID-19 (2019–20). The fixed effect modeling of panel data is applied in the main analysis of Chinese manufacturing companies ranging from 2008 to 2020. The results of the study disclose that there is an overall positive influence of corporate sustainable development on corporate financial performance. However, this influence becomes stronger during both crises i.e. the global recession (2008–10) and COVID-19 (2019–20). Moreover, this positive influence is even stronger during covid −19 recession as compared to this influence during the global recession (2008–10).

1. Introduction

In recent literature, there has been a growing focus on corporate sustainable development (CSD) in response to the escalating environmental problems caused by increased industrial growth around the world (Klára, Citation2011; Rajnoha & Lesníková, Citation2016a; Zdravkovic & Radukic, Citation2012). CSD refers to a business approach that considers the economic, social, and environmental impact of its operations. CSD contains two primary components i.e., corporate social responsibility (CSR), and corporate environmental sustainability (CES).

CSR is a company’s dedication to operating society friendly and contributing to economic progress while developing the life quality of the workers and their dependents, as well as of the local population and society at large (S, Citation2014; Tien & Hung Anh, Citation2018). CES is the practice of integrating environmental considerations into a company’s decision-making processes to minimize negative impacts and promote sustainable business practices (Chang & Kuo, Citation2008; Charlo et al., Citation2015; Lin et al., Citation2009; Martínez-Ferrero & Frías-Aceituno, Citation2015; Tien et al., Citation2020; Zhou et al., Citation2022). Several studies evaluated how the two components i.e., CSR and CES of corporate sustainable development influence corporate financial performance (Ait Sidhoum & Serra, Citation2018; Asif et al., Citation2013; Brogi & Lagasio, Citation2019; Busch & Friede, Citation2018; Choi et al., Citation2010; Herremans et al., Citation1993; Hou, Citation2019; Hussain et al., Citation2018; Klára, Citation2011; Lin et al., Citation2009; Lu et al., Citation2018; Marti et al., Citation2015; Naidoo & Gasparatos, Citation2018; S, Citation2014; Sun et al., Citation2019; Tien et al., Citation2020; Waheed & Yang, Citation2019; Zhu et al., Citation2019). The findings of these studies explain the positive and significant influence of CSD practices on the financial performance of the firms.

Despite the substantial amount of literature on the relationship between CSR and financial performance, there remains a gap in the understanding of how this relationship plays out in exceptional circumstances, whether they occur within or outside an organization. To address this research gap, the present study aims to examine the influence of CSR on financial performance during two global crises, namely the global recession of 2008–10 and the COVID-19 pandemic of 2019–20. The financial stress that companies face during these crises, such as reduced sales, complex supply chains, and limited access to credit, poses significant challenges to their ability to allocate funds toward sustainable activities. Therefore, the primary objective of this study is to assess how the influence of CES on corporate financial performance (CFP) alters in the crises compared to the rest of the period. The result findings indicate that CES has a stronger influence on CFP in macroeconomic crises. Furthermore, as the world continues to evolve with new technologies, innovations, inventions, and lifestyles, this study also compares the two crises to assess how the impact of CSR on financial performance during financial crises changes over time. The study’s results reveal that CSR has a more potent impact on a company’s financial performance during times of global crises. Furthermore, the findings demonstrate that this influence is particularly pronounced during the more recent crisis caused by the COVID-19 pandemic, as compared to the preceding global recession of 2008–10. These findings provide clear guidance to company managers on making decisions about sustainable investments during difficult times.

The current study selects a sample of Chinese companies for the above analysis. In the recent past, the China government has taken steps to improve CSD among Chinese companies, including issuing regulations and guidelines, promoting sustainable development, and encouraging companies to disclose information about their CSR and CES. However, the level of compliance with these regulations and guidelines varies among companies. Some Chinese companies have been found to have a poor record of compliance with environmental and labor regulations and have been involved in controversies related to human rights and environmental issues. Additionally, some multinational companies with Chinese operations have been condemned for their lack of accountability and transparency in their supply chain, particularly regarding labor rights and environmental protection. Overall, there is a growing awareness of the importance of CSR and CES among Chinese companies, but there is still a margin for improvement in terms of compliance and implementation.

The structure of the study is as follows. Section two reviews the existing literature and highlights the literature gap. The third section explains the methodology of the study including data collection, and analytical tools. The fourth section presents and describes the results. The final section concludes the whole study.

2. Literature review

2.1. Sustainable development

CSR is a complex and multifaceted concept, which has various interpretations and perspectives. It is widely acknowledged that firms should not only create worth for shareholders but also contribute positively to society and the well-being of all stakeholders (Zhou et al., Citation2022). The definition of CSR is constantly evolving, and in the background of globalization, particularly in undeveloped countries, policies, and protocols surrounding CSR are subject to change and adaptation. While some argue for a financial model that prioritizes profit above all else, others advocate for a societal model of CSR that considers the well-being of people, the planet, and profitability (Bansal, Citation2005; Zhou et al., Citation2022). Companies are also impacted by government involvement in CSR issues, and there may be inconsistencies between social responsibility and development in some cases. Sustainable Development as defined by the world business council (WBCSD) in 1998 is widely accepted as comprehensive and clear, stating that CSR is a continuous commitment of companies to business ethical values and step forward to economic growth while increasing the life quality of the workforce and their dependents, local communities, and societies.

It is worth noting that CSD is a holistic and integrated approach that goes beyond CSD, it encompasses all aspects of the business operations, and it incorporates sustainable practices in all areas of the organization, such as management, operations, products and services, supply chain, and community engagement. CSD also considers the long-term social, economic, and environmental influence of the enterprise’s actions, and it aims to create shared value for the company, its stakeholders, and the community as a whole (Ait Sidhoum & Serra, Citation2018; Asif et al., Citation2013; Bansal, Citation2002; Chow & Chen, Citation2012; Davis & Searcy, Citation2010).

In summary, the definitions and interpretations of CSD are mainly developed for developed countries, but the scope and priorities of CSD in undeveloped countries may be different. The government policies and regulations, and local socioeconomic, cultural, political, and legal environments in which companies operate in undeveloped countries can alter the situations, context, and circumstances in which enterprises are addressing social and environmental issues. Studies on CSD in undeveloped countries, particularly in China, are limited and there is a lack of research on the association between CSR, CES, and CFP in these countries.

2.2. Corporate financial performance

It is worth noting that these indicators and ratios are not the only ways to measure a company’s performance in terms of sustainable development and CFP. Other methods, such as multi-criteria analysis or sustainability reporting frameworks, may also be used (Griffin & Mahon, Citation2016). Additionally, it is important to keep in mind that there is no universally accepted method for measuring sustainable development and CFP, and different methods may produce different results depending on the company and the industry in which it operates (Zahra & Pearce, Citation2016). Therefore, it is important to consider multiple indicators and methods when evaluating a company’s performance in terms of sustainable development and CFP (Choi et al., Citation2010). Furthermore, it’s also important to consider that the use of financial indicators alone may not be enough to measure a company’s sustainability performance. It is important to take into account non-financial indicators as well, such as environmental and social performance indicators, which provide a complete picture of a firm’s sustainability performance (Soana, Citation2011). In addition, the use of a standardized reporting framework, like GRI (Global Reporting Initiative) or the SASB (Sustainability Accounting Standards Board) can help provide a consistent and comparable way to evaluate a company’s sustainability performance (Smith & Taffler, Citation1992). It is also important to consider stakeholder engagement and participation in the evaluation process to ensure that all relevant perspectives are taken into account (Lu et al., Citation2014). Overall, measuring a company’s sustainability performance is a complex task that requires a combination of different indicators and a holistic approach.

2.3. Corporate sustainable development and corporate financial performance

The theory of stakeholders explains that enterprises have an obligation to their stakeholders, including suppliers, customers, employees, shareholders, and society. This theory suggests that by incorporating the interests of all stakeholders, companies can create value for all parties involved and improve their overall performance. On the other hand, the agency theory argues that there is an inherent conflict of interest between shareholders (principals) and managers (agents) in a company. This theory explains that managers may prioritize their interests instead of shareholders, leading to lower financial progress. Investigation into the association between CSR, sustainability, and CFP has been concluded, with some studies finding a positive relationship and others finding a negative relationship. Factors such as the industry, the specific CSR or sustainability initiatives undertaken, and the time horizon of the study can all affect the relationship. Additionally, CSR and sustainability can have both negative and positive effects on CFP depending on the situation.

The theory of agency suggests that companies must balance the desires of management and stakeholders when prioritizing social and environmental responsibility. CSR efforts are not just benevolent acts, but also a means to enhance future financial success. Businesses engage in CSR initiatives when they expect them to lead to long-term financial stability (Eisenhardt, Citation1989; Hill & Jones, Citation1992a; Lu et al., Citation2014). According to the opinion of business managers from America, Europe, and Japan, the organizations that will thrive in the future are those that can establish flexible and holistic systems which focus not only on achieving specific goals but also on prioritizing social responsibility and environmental sustainability (Mizera, Citationn.d..). The stakeholder theory not only guides the choices of business leaders but also sheds light on a company’s objective of balancing the priorities of various stakeholders. It is closely associated with CSR and the overarching notion of sustainable growth within a corporation (Donaldson & Preston, Citation1995; Hill & Jones, Citation1992b).

CSR is becoming increasingly relevant, especially in developing nations. Research has demonstrated the influence of CSR disclosure on a company’s progress, including its effect on sales and marketing, which ultimately affect the financial performance of a corporation. An investigation (Waheed & Yang, Citation2019) involving 450 medium and small-sized enterprises (SMEs) in Pakistan found that disclosing CSR activities to external stakeholders had a greater positive impact on sales and marketing performance than disclosing CSR activities internally. Brogi and Lagasio (Citation2019) found that the relationship between ESG disclosure and ROA was positive for industrial firms, but not significant for financial intermediaries. This suggests that for industrial firms, better environmental, social, and governance practices may be associated with higher profitability, while for financial intermediaries, such associations may not be as strong. This research highlights the importance of considering industry-specific factors in evaluating the relationship between ESG disclosure and profitability.

The study by Zhu et al. (Citation2019) explored the moderating and mediating effects of technology, management, and marketing innovation on the correlation between CSR practices and business progress in 494 Chinese medium and small-sized businesses. The findings showed that technology and management innovation can enhance a company’s environmental progress, social reputation, and social engagement, while market innovation is vital for achieving financial and economic success. Moreover, Sun et al. (Citation2019) examine the impact of institutional transitions on CSR reporting and the role of financial performance in such reporting. The study uses data from listed firms in China and finds that institutional transitions have a positive impact on CSR reporting and that financial performance plays a mediating role in the relationship between institutional transitions and CSR reporting. The results suggest that in countries undergoing institutional transitions, a firm’s financial performance may influence its level of commitment to CSR.

In a study by Hou (Citation2019), the relationship between CSR and CFP in Taiwan was examined. The findings explained that companies that engage in CSR tend to have better financial results than those that do not. In non-electronic industries, the study found that board ownership has a positive effect on the relationship between CSR and CFP, but for family businesses, it has a negative impact. A study by Hussain et al. (Citation2018), investigates the relationship between a firm’s sustainability performance and its financial performance. The study analyzes data from publicly listed firms in Italy and finds that sustainability performance and financial performance are positively related. Additionally, the study identifies several mediating factors, such as firm size and industry that may explain the relationship between sustainability performance and financial performance. The results suggest that companies that prioritize sustainability may experience better financial performance.

Lu et al. (Citation2018) explore the relationship between CSR and sustainable financial performance in the international construction business. The study finds that there is a paradoxical relationship between CSR and sustainable financial performance, such that companies that are more socially responsible may have lower financial performance and vice versa. The results suggest that the relationship between CSR and financial performance is complex and may depend on the specific characteristics of a company and its industry.

The study conducted by Busch and Friede (Citation2018) investigate the relationship between CSR and financial performance. The study uses meta-analysis to analyze data from previous studies and finds that there is a positive relationship between CSR and financial performance. The results also suggest that this relationship is robust, meaning that it holds across different samples, methodologies, and definitions of CSR and financial performance. The study highlights the importance of considering both CSR and financial performance when evaluating a company’s performance. Furthermore, Marti et al. (Citation2015) investigate the relationship between CSR and financial performance. The study analyzes data from publicly listed firms in Spain and finds that firms that are more socially responsible tend to have better financial performance. The results suggest that companies that prioritize sustainability and social responsibility may experience positive financial outcomes.

Thus, the literature review provides a comprehensive overview of the concepts of CSD, CSR, and their association with financial performance. The review highlights that CSR is evolving, and its definition varies depending on the interpretation and perspectives of the stakeholders. It also discusses the importance of CSD in all areas of the organization, including management, operations, supply chain, and community engagement. The review concludes that there is a lack of research on the relationship between CSR, CSD, and CFP in developing countries, especially China However, the review fails to address the role of corporate sustainability and financial performance during two major crises: the global recession of 2008–10 and the COVID-19 pandemic in 2019–20. Additionally, while the review mentions the importance of using non-financial indicators and reporting frameworks to evaluate a company’s sustainability performance, it does not explore these aspects in detail. Moreover, the review provides a general overview of the stakeholder and agency theories but fails to demonstrate their application in the context of CSR and CSD. Overall, the literature review provides a broad and informative understanding of CSR, CSD, and their association with CFP. However, there are gaps in the literature that need to be addressed, including the role of corporate sustainability during global crises and the importance of non-financial indicators and stakeholder engagement in evaluating a company’s sustainability performance.

3. Methodology

3.1. Theoretical framework and model construction

The argument from a theoretical perspective is that companies that prioritize social and environmental responsibility by regularly publishing their CSR statements and CES reports, tend to perform better financially (Brogi & Lagasio, Citation2019; Griffin & Mahon, Citation2016). This is because consumers and investors are increasingly interested in companies that demonstrate a commitment to social and environmental responsibility. By doing so, companies can increase their reputation, attract new customers, and retain existing ones. Additionally, investors are more likely to invest in companies that prioritize social and environmental responsibility as it indicates the company is well-managed and has long-term sustainability goals. Therefore, companies that prioritize CSR and CES can potentially see financial benefits in the form of increased profits and investment opportunities (Brogi & Lagasio, Citation2019; Griffin & Mahon, Citation2016). CSD initiatives can lead to cost savings for companies, such as through energy efficiency measures or reduced waste.

We hypothesize that the period of the global recession (2008–10) further stronger the relationship between CSD and financial performance because during this recession CSD initiatives may have helped companies build a positive reputation, which made them more resilient during difficult economic times and may be able to attract and retain customers and investors more easily than those that are not. Similarly, we also hypothesize that companies that were already following the CSD guidelines may be in a better financial position during covid-19. During the pandemic, companies that had prioritized efficient supply chains and operations were better equipped to handle the changing consumer demands and supply chain disruptions. These companies had a deeper understanding of their supply chain and operational activities, enabling them to identify areas that could be reduced without affecting the overall performance of the company. By optimizing their operations, these companies were able to maintain or increase their productivity, reduce costs, and remain competitive in a challenging market. As a result, prioritizing efficiency and operational excellence can help companies to adapt to unexpected disruptions and ensure their long-term sustainability (Maher et al., Citation2020).

To test the impact of CSD on the financial performance of companies, following (Mahmood et al., Citation2019) we constructed the following model;

Where ROA stands for the return on assets, CSD represents the companies regularly publishing the CSR and CES statements. Debt to equity shows the ratio of debt to equity, and total assets represent the total assets of the company. Also, i indicates the number of firms ranging from 1 to 5,305 while t represents the years starting from 2001 to 2022. shows the error term due to the time effect while

explains the error term due to industry effects. The

shows the general error term of the regression equation.

This study examines the relationship between CSD and firm performance for the 5,305 Chinese companies during the period ranging from 2000 to 2022. The duration of the data is selected to include both recessions i.e., global recession (2008–10) and Covid-19, and ending data is selected to conduct the updated analysis. ROA is the dependent variable and stands for return on analysis which is the most common proxy in the literature to measure the financial performance of a company. CSD is the independent variable and categorizes the companies into two groups, one which regularly publishes CSD reports and the second one which doesn’t. We allocated the “2” number for the companies that regularly publish their CSD reports and “1” to the rest ones. Debt to equity and total assets are the control variables of the study.

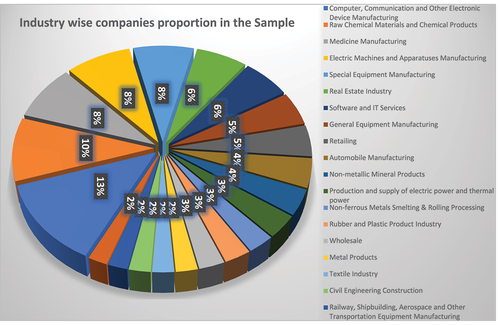

The data for the Chinese companies is collected from the China Securities Market Statistics and Analysis Centre (CSMAR), which is a subsidiary of the China Securities Regulatory Commission (CSRC). The database collects and stores financial data on publicly traded companies in China, including information on their performance, financial statements, and ownership structure. The data is used by various stakeholders, including investors, regulators, and market analysts, to gain insights into the Chinese securities market and make informed investment decisions (CSMAR, Citation2018). The variables measurement is shown in Table . Table and Figure discloses the province-wise distribution of sample observations while Figure explains the industry-wise distribution of the sample.

Figure 1. Province-wide distribution of sample.

Figure 2. Industry-wise sample allocation.

Table 1. Province-wise sample allocation

Table 2. Variables measurement

4. Results and discussion

4.1. Descriptive statistics

We winsorize the data by 5% to remove the outlier values. We also removed the missing values of the dataset. The Descriptive analysis of the remaining dataset is given in Table . According to the table, the data contains the acceptable range of minimum and maximum values of variables and are free from outlier values.

Table 3. Descriptive statistics

The correlation matrix of the variables is given in Table . According to the table, the independent variable has a positive and significant correlation with the dependent variable. The correlation of the control variables is also significant with the dependent variable. However, the correlation among certain variables seems to be stronger which doubts the multicollinearity.

Table 4. Correlation matrix

To ensure the absence of multicollinearity among the independent and control variables, the next test conducted on the selected sample is the variance inflation factor. The results of the VIF analysis are given in Table . In this case, all three variables have relatively low VIF values (all less than 2), which indicates that there is little multicollinearity among the variables. The Mean VIF for all three variables combined is also low at 1.20, reinforcing the conclusion that there is no substantial multicollinearity. Overall, this analysis suggests that the three variables can be safely included in a regression model without concerns about multicollinearity.

Table 5. VIF analysis

4.2. The relationship between CSD and CFP

The F-test is employed to compare the fixed-effect model and the ordinary least squares (OLS) model, to select the more appropriate one. The results of the F-test, presented in Tables VI, VII, and VIII indicate highly significant values, which reject the null hypothesis of zero coefficients of the fixed-effect model. Therefore, it can be concluded that the fixed-effect model is better suited for the given data as compared to the OLS model. Similarly, the Breusch-Pagan test is utilized to compare the random-effect model and the OLS model. The null hypothesis of the Breusch-Pagan test assumes the absence of heteroscedasticity in the errors of a linear regression model. The results of this test reveal high levels of insignificance, indicating that the random-effect model is superior to the OLS model.

To make the final comparison between the fixed-effect model and the random-effect model, the study employs the Hausman test. The null hypothesis of this test assumes that the random-effect model is more efficient than the fixed-effect model. The results of the Hausman test, as presented in Tables VI, VII, and VIII, reveal high levels of insignificance. Therefore, it can be concluded that the fixed-effect model is more appropriate for the given dataset as compared to the random-effect model.

The findings from the fixed effect model for the full sample of the study are presented in Table , which displays the outcomes of three distinct models. The first column exhibits the fixed effect model without incorporating time and industry fixed effects. The second column contains the results of the fixed effect model about time-fixed effects. Finally, the third column includes the industry-fixed effects in the fixed effect model. Overall, the results from all three models indicate a positive and significant relationship between CSD and the financial performance of companies. More specifically, the positive influence of sustainable development is even stronger when time-fixed effects are incorporated into the model. However, the incorporation of industry-fixed effects does not appear to influence sustainable development and firms’ financial performance. It is noteworthy that the control variables remain highly significant in all three models.

Table 6. Effect of sustainable development on financial performance – full sample

There are several reasons why corporate sustainability and financial performance can have a positive relationship. A company that prioritizes sustainability can improve its reputation and brand image, which can increase customer loyalty and trust. This can lead to increased sales and revenue (Naidoo & Gasparatos, Citation2018). Additionally, companies that focus on sustainability often have more engaged and motivated employees, leading to improved retention and reduced turnover. Sustainability initiatives can also improve risk management by reducing environmental and social risks and promoting environmental and social stewardship (Rajnoha & Lesníková, Citation2016b). Companies that prioritize sustainability can also benefit from cost savings through energy and resource efficiency and may have better access to capital and financial resources. Furthermore, sustainability initiatives can lead to increased innovation and market differentiation, improving competitiveness and driving growth (Rajnoha & Lesníková, Citation2016a). Finally, companies that prioritize sustainability can improve relationships with stakeholders and be better positioned to meet regulatory requirements, reducing legal risks (Hussain et al., Citation2018).

Incorporating time-fixed effects in a model helps to control for any time-invariant variables that may affect the relationship between CSD and financial performance. These time-invariant variables can include factors such as industry, size of the firm, location, and historical events, among others, which can have a persistent effect on the financial performance of the firm. By controlling for these variables, the true effect of corporate sustainability on financial performance can be isolated and the positive relationship between the two becomes more robust and statistically significant. This allows for a clearer understanding of the causal relationship between corporate sustainability and financial performance and helps to eliminate any confounding influences that may have distorted the relationship in previous models. The results under the time-fixed effects are revealing a stronger influence of sustainable development on the financial performance of Chinese companies. These results are robust to the above results and reveal a clearer picture of the scenario.

Incorporating industry-fixed effects in a fixed effects model can improve the results by controlling for industry-specific variables that may affect the relationship between the dependent and independent variables. Industry-specific variables can include factors such as industry trends, regulations, competition, and market conditions, among others. These variables can have a persistent effect on the financial performance of firms and can influence the relationship between corporate sustainability and financial performance. The results of Table reveal that sustainable development has a significant and positive influence on corporate financial development, even when the industry-fixed effects are controlled. These results also validate the above results and confirm that the firms following sustainable development earn more profits compared to the other firms. The detailed results are given in Table .

4.3. CSD and CFP during a global recession (2008–10)

The global recession of 2008–2010 was a major economic downturn that affected economies around the world. It was triggered by the collapse of the US housing market and the subprime mortgage crisis, which spread to the banking sector and financial markets globally. The crisis resulted in widespread bank failures, stock market crashes, and a sharp decline in economic activity. Many countries faced high levels of unemployment, reduced consumer spending, and decreased economic growth (Calvo, Citation2010). The recession had a profound impact on the global economy, leading to government intervention in the form of fiscal stimulus, monetary policy, and bank bailouts. The recovery from the recession was slow and uneven, with some countries experiencing a faster and stronger rebound, while others faced a more prolonged period of slow growth. The global recession of 2008–10 had far-reaching consequences, highlighting the interconnectedness of global economies and the importance of financial stability (Calvo, Citation2010).

To evaluate how the influence of CSD changed during the period from 2008 to 2010, we extracted a subsample from the dataset. In Tabel , our findings indicate a positive and significant effect of CSD on financial performance, which is even stronger than observed in the previous results. This can be attributed to the fact that sustainable practices, such as reducing waste, improving energy efficiency, and adopting environmentally friendly processes, can lead to lower costs and improved operational efficiency. During a recession, when companies are facing increased cost pressures and lower consumer demand, such cost savings can provide a competitive edge and contribute to maintaining profitability (Calvo, Citation2010). Moreover, during an economic downturn, consumers and investors may display a growing preference for socially responsible companies, leading to an increased demand for sustainable products and services, and higher profits for firms following sustainable development practices (Sanfey, Citation2011). Although the relationship between sustainable development and financial performance is complex, other factors such as industry and market conditions may also influence the relationship. Nevertheless, the potential for cost savings and increased demand can help to explain why companies following sustainable practices may have performed better during the global recession.

Table 7. Effect of sustainable development on financial performance – global recession (2008–10)

The impact of CSD on corporate financial performance appears to be more pronounced when controlling for time-invariant variables such as firm size, location, and nature of business. This is achieved by applying the fixed effect model with time-fixed effects. Likewise, when accounting for industry fixed effects, such as industry trends, competition, and regulatory policies, and controlling for their influence in the fixed effects model, the results reaffirm the positive and significant effect of CSD on CFP. It is notable here that the influence of CSD on corporate financial performance is stronger in all three models (without effects, with time-fixed effects, and with industry-fixed effects) compared to the whole sample.

4.4. CSD and CFP during COVID-19 (2019–20)

The COVID-19 pandemic has had a profound impact on the global economy, leading to widespread economic disruption and financial hardship. The rapid spread of the virus and measures to contain it, such as lockdowns and travel restrictions, has caused a sharp decline in consumer spending and business activity. Many industries, including hospitality, tourism, and retail, have been particularly hard hit, and millions of workers have lost their jobs (Ciotti et al., Citation2020). Governments around the world have introduced fiscal and monetary measures to support their economies and help mitigate the effects of the pandemic, but the long-term consequences of the crisis are uncertain. The pandemic has exposed vulnerabilities in the global economy and highlights the importance of resilience and preparedness in the face of future shocks. The effects of the crisis will continue to be felt for some time, and the full extent of the economic impact is yet to be determined (Ciotti et al., Citation2020). However, it is clear that the COVID-19 pandemic has had a profound impact on the global economy and will have far-reaching consequences for years to come.

We extracted a subsample of the dataset covering 2019 and 2020 to examine how the association between CSD and CFP evolved during the COVID-19 pandemic. Table present the findings and indicate that there is a positive and significant effect of CSD on CFP in all three models. Specifically, the effect is more pronounced when incorporating time-fixed effects. However, the effect weakens when applying the industry fixed effects model. These results suggest that firms adhering to sustainable practices experienced a more favorable impact on their financial performance compared to their counterparts during the pandemic.

Table 8. Effect of sustainable development on financial performance – Covid-19 (2019–20)

The influence of CSD on CFP was stronger during the COVID-19 pandemic may be for several reasons. Firstly, companies with strong sustainable practices may have been better positioned to weather the economic uncertainty and supply chain disruptions caused by the pandemic (Padhan & Prabheesh, Citation2021). For example, companies with diverse supply chains and resilient operations may have been better able to adapt to changes in consumer demand and maintain profitability. Additionally, consumer preferences for socially responsible companies may have increased during the pandemic, leading to increased demand for sustainable products and services. Furthermore, governments and investors have placed a greater emphasis on sustainability during the pandemic, recognizing the need for long-term, sustainable economic recovery. This has led to increased investment in sustainable companies and a focus on ESG factors in investment decisions (Altig et al., Citation2020).

Finally, companies may have had an opportunity during the pandemic to prioritize sustainable initiatives and implement changes that would improve their long-term sustainability and competitiveness. The pandemic has highlighted the importance of resilience and preparedness, and companies that have integrated sustainability into their operations may have been better equipped to navigate the crisis and emerge stronger (Altig et al., Citation2020). Also, the technology and infrastructure for sustainable practices have improved significantly in recent years, making it easier and more cost-effective for companies to integrate sustainability into their operations. This has made it possible for companies to take a more proactive approach to sustainability, and the crisis may have provided an opportunity for companies to accelerate these efforts and differentiate themselves in the market.

5. Conclusion

As the world becomes more connected, an increasing number of countries are placing a greater emphasis on CSD not only in developed nations but also in emerging economies that are transitioning to a market-based system. These emerging nations can learn from the experiences of more developed countries to improve their CSD practices. Literature reveals abundant material regarding the overall positive linkage between CSD and CFP. However, companies are under extreme financial stress during global recessions and face severe challenges to continue sustainable development. Therefore, the current study evaluates the impacts of CSD on the financial performance of Chinese companies during the recent two recessions i.e., the global recession (2008–10), and caused by Covid-19.

The current study selects companies from several manufacturing sectors of the Chinese economy ranging from 2000 to 2020. The primary results of the study confirm the positive impact of CSD on CFP. When the same study is conducted during the exclusive period of the global recession (2008), the results reveal a stronger positive influence of CSD on CFP than the whole sample. When the exclusive period of COVID-19 is analyzed in terms of the influence of CSD on CFP, again the impact is stronger than the whole sample. Moreover, the positive influence of CSD on CFP is observed to be stronger in the COVID-19 era compared to the global recession (2008–10). The findings of this research may prove useful for state agencies, management scholars, and business practitioners. This article has practical implications for those in management research, business, and government, and suggests that there is a lack of understanding and awareness of CSD among business and political leaders, which is crucial for the success of companies, the economy, and society as a whole. Furthermore, the article examines the relevance of CSD in the context of CSD and proposes that future research should examine the association between CSD and corporate economic performance, considering both financial and socio-economic performance.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Ait Sidhoum, A., & Serra, T. (2018). Corporate sustainable development. Revisiting the relationship between corporate social responsibility dimensions. Sustainable Development, 26(4), 365–16. https://doi.org/10.1002/SD.1711

- Altig, D., Baker, S., Barrero, J. M., Bloom, N., Bunn, P., Chen, S., Davis, S. J., Leather, J., Meyer, B., Mihaylov, E., Mizen, P., Parker, N., Renault, T., Smietanka, P., & Thwaites, G. (2020). Economic uncertainty before and during the COVID-19 pandemic. Journal of Public Economics, 191, 104274. https://doi.org/10.1016/J.JPUBECO.2020.104274

- Asif, M., Searcy, C., Santos, P. D., & Kensah, D. (2013). A review of Dutch corporate sustainable development reports. Corporate Social Responsibility and Environmental Management, 20(6), 321–339. https://doi.org/10.1002/CSR.1284

- Bansal, P. (2002). The corporate challenges of sustainable development. Academy of Management Perspectives, 16(2), 122–131. https://doi.org/10.5465/AME.2002.7173572

- Bansal, P. (2005). Evolving sustainably: A longitudinal study of corporate sustainable development. Strategic Management Journal, 26(3), 197–218. https://doi.org/10.1002/SMJ.441

- Brogi, M., & Lagasio, V. (2019). Environmental, social, and governance and company profitability: Are financial intermediaries different? Corporate Social Responsibility and Environmental Management, 26(3), 576–587. https://doi.org/10.1002/CSR.1704

- Busch, T., & Friede, G. (2018). The robustness of the corporate social and financial performance relation: A second-order meta-analysis. Corporate Social Responsibility and Environmental Management, 25(4), 583–608. https://doi.org/10.1002/CSR.1480

- Calvo, S. G. (2010). The global financial crisis of 2008-10: A view from the social sectors. https://papers.ssrn.com/abstract=2351546

- Chang, D. S., & Kuo, L. C. R. (2008). The effects of sustainable development on firms’ financial performance – an empirical approach. Sustainable Development, 16(6), 365–380. https://doi.org/10.1002/SD.351

- Charlo, M. J., Moya, I., & Muñoz, A. M. (2015). Sustainable development and corporate financial performance: A study based on the FTSE4Good IBEX index. Business Strategy and the Environment, 24(4), 277–288. https://doi.org/10.1002/BSE.1824

- Choi, J. S., Kwak, Y. M., & Choe, C. (2010). Corporate social responsibility and corporate financial performance: Evidence from Korea. Australian Journal of Management, 35(3), 291–311. https://doi.org/10.1177/0312896210384681

- Chow, W. S., & Chen, Y. (2012). Corporate sustainable development: Testing a new scale based on the mainland Chinese Context. Journal of Business Ethics, 105(4), 519–533. https://doi.org/10.1007/s10551-011-0983-x

- Ciotti, M., Ciccozzi, M., Terrinoni, A., Jiang, W. C., Wang, C. B., & Bernardini, S. (2020). The COVID-19 pandemic. Critical Reviews in Clinical Laboratory Sciences, 57(6), 365–388. https://doi.org/10.1080/10408363.2020.1783198

- CSMAR. (2018). The CSMAR Economic and Financial Research Database. http://us.gtadata.com/

- Davis, G., & Searcy, C. (2010). A review of Canadian corporate sustainable development reports. Journal of Global Responsibility, 1(2), 316–329. https://doi.org/10.1108/20412561011079425

- Donaldson, T., & Preston, L. E. (1995). The stakeholder theory of the corporation: Concepts, evidence, and implications. Academy of Management Review, 20(1), 65. https://doi.org/10.2307/258887

- Eisenhardt, K. M. (1989). Agency Theory: An assessment and review. Academy of Management Review, 14(1), 57. https://doi.org/10.2307/258191

- Griffin, J. J., & Mahon, J. F. (2016). The corporate social performance and corporate financial performance debate. Business & Society, 36(1), 5–31. https://doi.org/10.1177/000765039703600102

- Herremans, I. M., Akathaporn, P., & McInnes, M. (1993). An investigation of corporate social responsibility reputation and economic performance. Accounting, Organizations and Society, 18(7–8), 587–604. https://doi.org/10.1016/0361-3682(93)90044-7

- Hill, C. W. L., & Jones, T. M. (1992a). STAKEHOLDER-AGENCY THEORY. Journal of Management Studies, 29(2), 131–154. https://doi.org/10.1111/J.1467-6486.1992.TB00657.X/

- Hill, C. W. L., & Jones, T. M. (1992b). STAKEHOLDER-AGENCY THEORY. Journal of Management Studies, 29(2), 131–154. https://doi.org/10.1111/J.1467-6486.1992.TB00657.X

- Hou, T. C. T. (2019). The relationship between corporate social responsibility and sustainable financial performance: Firm-level evidence from Taiwan. Corporate Social Responsibility and Environmental Management, 26(1), 19–28. https://doi.org/10.1002/CSR.1647

- Hussain, N., Rigoni, U., & Cavezzali, E. (2018). Does it pay to be sustainable? Looking inside the black box of the relationship between sustainability performance and financial performance. Corporate Social Responsibility and Environmental Management, 25(6), 1198–1211. https://doi.org/10.1002/CSR.1631

- Klára, P. (2011). The impact of recession on the implementation of corporate social responsibility in companies. Journal of Competitiveness, 2(3), 83–98.

- Lin, C. H., Yang, H. L., & Liou, D. Y. (2009). The impact of corporate social responsibility on financial performance: Evidence from business in Taiwan. Technology in Society, 31(1), 56–63. https://doi.org/10.1016/J.TECHSOC.2008.10.004

- Lu, W., Chau, K. W., Wang, H., & Pan, W. (2014). A decade’s debate on the nexus between corporate social and corporate financial performance: A critical review of empirical studies 2002–2011. Journal of Cleaner Production, 79, 195–206. https://doi.org/10.1016/J.JCLEPRO.2014.04.072

- Lu, W., Ye, M., Chau, K. W., & Flanagan, R. (2018). The paradoxical nexus between corporate social responsibility and sustainable financial performance: Evidence from the international construction business. Corporate Social Responsibility and Environmental Management, 25(5), 844–852. https://doi.org/10.1002/CSR.1501

- Maher, C. S., Hoang, T., & Hindery, A. (2020). Fiscal responses to COVID-19: evidence from local governments and nonprofits. Public Administration Review, 80(4), 644–650. https://doi.org/10.1111/PUAR.13238

- Mahmood, F., Han, D., Ali, N., Mubeen, R., & Shahzad, U. (2019). Moderating effects of firm size and leverage on the working capital finance-profitability relationship: Evidence from China. Sustainability (Switzerland), 11(7), 19–22. https://doi.org/10.3390/su11072029

- Martínez-Ferrero, J., & Frías-Aceituno, J. V. (2015). Relationship between sustainable development and financial performance: International empirical research. Business Strategy and the Environment, 24(1), 20–39. https://doi.org/10.1002/BSE.1803

- Marti, C. P., Rovira-Val, M. R., & Drescher, L. G. J. (2015). Are firms that contribute to sustainable development better financially? Corporate Social Responsibility and Environmental Management, 22(5), 305–319. https://doi.org/10.1002/CSR.1347

- Mizera, K. (n.d.). Instrumenty społecznej odpowiedzialności biznesu Streszczenie. Retrieved 31 January 2023, from http://www.fi

- Naidoo, M., & Gasparatos, A. (2018). Corporate environmental sustainability in the retail sector: Drivers, strategies and performance measurement. Journal of Cleaner Production, 203, 125–142. https://doi.org/10.1016/J.JCLEPRO.2018.08.253

- Padhan, R., & Prabheesh, K. P. (2021). The economics of COVID-19 pandemic: A survey. Economic Analysis and Policy, 70, 220–237. https://doi.org/10.1016/J.EAP.2021.02.012

- Rajnoha, R., & Lesníková, P. (2016a). Strategic performance management system and corporate sustainability concept - Specific parametres in Slovak enterprises. Journal of Competitiveness, 8(3), 107–124. https://doi.org/10.7441/JOC.2016.03.07/

- Rajnoha, R., & Lesníková, P. (2016b). Strategic performance management system and corporate sustainability concept - Specific parametres in Slovak enterprises. Journal of Competitiveness, 8(3), 107–124. https://doi.org/10.7441/JOC.2016.03.07

- S, K. O. T. (2014). Knowledge and understanding of corporate social responsibility. Journal of Advanced Research in Law and Economics (JARLE), V(10), 109–119.

- Sanfey, P. (2011). South-eastern Europe: Lessons learned from the global economic crisis in 2008–10. Southeast European and Black Sea Studies, 11(2), 97–115. https://doi.org/10.1080/14683857.2011.588017

- Smith, M., & Taffler, R. (1992). THE chairman’s statement and corporate financial performance. Accounting & Finance, 32(2), 75–90. https://doi.org/10.1111/J.1467-629X.1992.TB00187.X

- Soana, M. G. (2011). The relationship between corporate social performance and corporate financial performance in the banking sector. Journal of Business Ethics, 104(1), 133–148. https://doi.org/10.1007/s10551-011-0894-x

- Sun, W., Zhao, C., & Cho, C. H. (2019). Institutional transitions and the role of financial performance in CSR reporting. Corporate Social Responsibility and Environmental Management, 26(2), 367–376. https://doi.org/10.1002/CSR.1688

- Tien, N. H., Anh, D. B. H., & Ngoc, N. M. (2020). Corporate financial performance due to sustainable development in Vietnam. Corporate Social Responsibility and Environmental Management, 27(2), 694–705. https://doi.org/10.1002/CSR.1836

- Tien, N. H., & Hung Anh, D. B. (2018). Gaining competitive advantage from csr policy change –case of foreign corporations in vietnam. Polish Journal of Management Studies, 18(1), 403–417. https://doi.org/10.17512/PJMS.2018.18.1.30

- Waheed, A., & Yang, J. (2019). Effect of corporate social responsibility disclosure on firms’ sales performance: A perspective of stakeholder engagement and theory. Corporate Social Responsibility and Environmental Management, 26(3), 559–566. https://doi.org/10.1002/CSR.1701

- Zahra, S. A., & Pearce, J. A. (2016). Boards of directors and corporate financial performance: A review and integrative model. Journal of Management, 15(2), 291–334. https://doi.org/10.1177/014920638901500208

- Zdravkovic, D., & Radukic, S. (2012). Institutional framework for sustainable development in Serbia. Institutional framework for sustainable development in Serbia. Montenegrin Journal of Economics, 8(3), 27–36. https://citeseerx.ist.psu.edu/document?repid=rep1&type=pdf&doi=45586c2b3ff3a6760e1717b3eb68b3dfd0390607#page=27

- Zhou, G., Liu, L., & Luo, S. (2022). Sustainable development, ESG performance and company market value: Mediating effect of financial performance. Business Strategy and the Environment, 31(7), 3371–3387. https://doi.org/10.1002/BSE.3089

- Zhu, Q., Zou, F., & Zhang, P. (2019). The role of innovation for performance improvement through corporate social responsibility practices among small and medium-sized suppliers in China. Corporate Social Responsibility and Environmental Management, 26(2), 341–350. https://doi.org/10.1002/CSR.1686