Abstract

This study investigates the interactive influence of two dimensions of perceived organizational prestige (POP) on ethical decision-making (EDM). The study also examines the moderating effect of the decision-maker’s financial situation on the POP-EDM relationship. A Survey data from 356 tax accountants in two public-interest organizations were analysed using partial least square structural equation modelling. The study found that perceived external prestige (PEP) dimension of POP predicts EDM. Self-perceived prestige (SPP) dimension of prestige does not directly predict EDM but is a significant antecedent of PEP. Furthermore, decision-maker’s financial situation does not moderate PEP-EDM relationship. The paper holds implications for image-building policies for public-interest organizations. Towards improving EDM, the paper recommends for organizations to focus on PEP-enhancing programs. This paper is foremost in establishing POP-EDM relationship. Further, the paper contributes to social identity theory by examining the EDM effect of both social identity motivations and potential ethical pressures on tax accountants.

PUBLIC INTEREST STATEMENT

Ethical standing of employees in many public-interest organizations has been questioned in Ghana.s. In recent time, tax officers at Ghana Revenue Authority (a foremost public-interest organization in Ghana) were ranked among topmost corrupt public officials in Ghana. This worrying report partly drives this study to examine ways of improving ethical behavior among employees in critical public-interest organizations. This study explains how individual’s quest to identify with prestigious public-interest organizations influence their resolve to act ethically. The study draws on data from tax accountants in Ghana. Key findings were that tax accountants evaluation of their organization’s prestige (PEP) predict their ethical intention. Furthermore, the study found that the tax accountants’ motivation to maintain their relation with prestigious organizations would drive them to act ethically, and this drive remains unshaken by their financial situation.

1. Introduction

A wealth of literature draws on social identity theory to explain how motivations of belongingness to prestigious organizations (perceived organizational prestige) predict multiple in-group norms in organizations. The literature linked perceived organizational prestige (POP) to workplace deviant behaviour (Pratiwi et al., Citation2022), turnover intention (Akgunduz & Bardakoglu, Citation2017; Bright, Citation2021), organizational citizen behaviour (Boğan et al., Citation2020) and employee’s commitment (Kang et al., Citation2011). The literature is, however, sparse in linking POP to ethical decision-making (EDM). This linkage is important for public-interest organizations that thrive on POP (Francis et al., Citation2017). More importantly, these public-interest organizations tout ethics and ethical decision-making as a key in-group norm for sustainable practice (Kportorgbi et al., Citation2022; Mintz & Morris, Citation2022). This study draws on perspectives of tax accountants in Ghana to extend POP linkage to an important ethical behavior proxy-ethical decision-making. POP-EDM linkage with data from tax accountants holds global relevance but more essential for developing countries, where low level of fiscal extraction is partly attributed to poor ethical decisions of tax agents (Addo, Citation2021; Kportorgbi et al., Citation2022).

Another reason for this paper is its attempt to capture the concurrent influence of social identity motivations and potential ethical pressures on ethical decision-making. The extant empirical literature (Akgunduz & Bardakoglu, Citation2017; Boğan et al., Citation2020; Bright, Citation2021) falls short in examining how POP relationships fare in the presence of potential individual-level pressures. The effect of this deficiency is that the current literature is deficient in explaining whether social identity motivations to live up to in-group organizational norms stand in the presence of potential pressures to side-step ethical boundaries. To provide a balanced perspective, this study examines how an individual-level pressure (i.e., decision-maker’s financial situation) anchors the POP-EDM relationship. The choice for financial situation as a potential anchor for POP-EDM is apt for studies in developing economies where financial inducements are often cited as potent pressure against ethical living (Boonmanunt et al., Citation2020; Gumusay, Citation2019; Tang & Chiu, Citation2003).

This study uniquely captures interrelationships between two perspectives of POP. An established literature (Carmeli et al., Citation2011; Dutton et al., Citation1994) distinguished between two dimensions of POP (i.e., perceived external prestige and self-perceived prestige) and argued for studies exploring how each explains pro-organizational behaviours. The literature explained that POP valuations could be based on opinion of external stakeholders (i.e., perceived external prestige (PEP)) or POP valuation solely based on personal experience of organizational members (self- perceived prestige (SPP)). Only few empirical studies (Frunzaru & Dumitriu, Citation2015; Fuller et al., Citation2006) sought to understand how the two dimensions of POP, respectively, influence pro-organizational behaviours. The extant literature is thus constrained in explaining which dimension of POP is a better predictor of pro-organizational behaviour. A literature on relative effect of the two dimensions of POP on EDM has implication for POP-enhancing programs of public-interest organizations. This study provides this perspective by understanding interrelationship between the two perspectives of POP and EDM.

To fully understand this new linkage between POP and EDM, the study traced the influence of POP across multiple stages of Rest’s (1986) EDM scale. This effort is essential in justifying focus and impact of POP-enhancing programs of public-interest organizations.

In summary, this paper sought to examine the simultaneous influence of two perspectives of POP on EDM and moderating effect of decision-makers’ financial situation on the relationship. The specific research objectives (RO) are to:

RO1: trace influence of the two dimensions of POP on EDM.

RO2: examine the interrelationship among the two dimensions of POP and EDM.

RO3: Examine moderating influence of decision-makers’ financial situation on the relationship between POP and EDM.

Remaining sections of the paper are structured as follows: a review of theoretical and empirical literature, methodology, empirical findings, and discussion of the results. The last section contains conclusions and direction for future studies.

2. Literature review

2.1. Ethical decision-making

Ethical decision-making is defined as the cognitive ability and willingness of the decision-maker to incorporate ethical perspectives into decisions (Casali & Perano, Citation2021). Rest (1986) conceptualized it as a four-stage process, comprising ethical issue recognition; ethical judgement; ethical intention; and actual ethical behaviour. The first stage (issue recognition) largely requires the cognitive capacity of the decision-maker to construct ethical reality (Lincoln & Holmes, Citation2008). At the second stage, the decision-maker evaluates the rightness or otherwise of the intended decision by comparing with in-group norms and ethical principles (Rest,1986). The third stage involves the willingness and mental fortitude of the decision-maker to take a purported “right” course of decision amid conflicting influences, other convenient alternatives and in the presence of external stress (Rest, 1986). The fourth stage involves unambiguous and absolute enforcement of the actual decision. Rest (1986) conceptualized the four stages as independent of each other, but contributors to the model (Musbah et al., Citation2016) contend that ethical judgement and ethical intention stages are not independent of each other. The authors contend that ethical judgement stage predicts ethical intention stage. It is thus not uncommon for EDM studies to focus on ethical recognition and ethical intention stages of EDM. The fourth stage is often omitted from empirical studies based on practical difficulties of studying actual behaviour.

2.2. Social identity theory

Social identity, defined as the knowledge of belongingness, value attachment and emotional importance that individuals assign to their membership in socio-economic group, has been linked to group behaviours in a wide range of contexts (Abrams & Hogg, Citation1990). The central theme of social identity theory is that an individual’s motivation to identify and be identified with a prestigious organization/group provides a potent drive for the individual to exhibit pro-organisational/group behaviours (Berghaus, Citation2020; Kang et al., Citation2011). The literature holds that the individual identification process has three interrelated components: self-categorization, discovery of an in-group norm, and assignment of the norm to self (Abrams & Hogg, Citation1990). In undergoing these processes, the individual continuously seeks answers to these questions: where do I belong? what is expected of members in this group? and what must I do to legitimize my membership in this group (Tajfel, Citation1982)? The quest to find the answers to these questions makes the individual conscious of social image of the organization/group.

The construction of the social image of the organization’s image (organizational prestige) could be driven by personal experience of that individual in the organisation (self-perceived prestige) or by opinion of external stakeholders in the organisation that the individual works for (perceived external prestige). Although these two perspectives of constructing the organization’s prestige are grounded in literature, empirical literature on their relative effect on pro-organizational behaviour is scanty. The literature has also not examined whether there is a dialectic relationship between the two POP valuations. This study fetches these dimensions.

The social identity theory has been used to explain how individual motivation to identify and be identified with prestigious groups/organizations could drive them to exhibit pro-organizational behaviours. The social identity theory has not sufficiently addressed whether the drive to live up to in-group norms in order to maintain social ties with prestigious organizations remains in the presence of inherent in the socio-economic situation of the individuals. A fusion of character-induced theories (Nguyen & Crossan, Citation2021) and social identity theory could provide some answers. Proponents of character-infused ethics theories argue that situations of the individuals can serve as pressures or motivations for EDM (Nguyen & Crossan, Citation2021). This study contributes to literature in this aspect by examining whether POP-EDM relationship is anchored by the decision-maker’s financial situation.

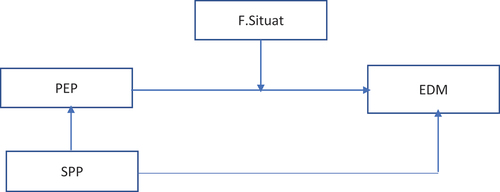

The study postulates that an individual’s valuation of their organisation’s prestige (i.e., PEP and SPP) is related to EDM. This postulation is premised on social identity theory’s holding that an individual’s motivation to identify with prestigious organizations provide a potent drive towards exhibiting a pro-group behaviour, EDM. To study the interrelationship among PEP, SPP, and EDM, the study postulates that PEP mediates the relationship between SPP and EDM. This postulation is premised on social identity theory’s emphasis on social/external valuation of group identities. Finally, the study postulates that the relationship between organizational prestige and EDM is moderated by individual situations. Specifically, the study examined whether the often-touted financial situation of decision-makers alters the prestige-EDM relationship. The study proposes a conceptual framework in Figure .

Figure 1. Conceptual Framework - Organisational prestige-EDM.

Figure suggests a direct link between POP and EDM and suggests that the decision-maker’s financial situation could potentially moderate the POP-EDM relationship.

2.3. Empirical review

2.3.1. Linking PEP and EDM

There is a considerable research effort to understand how employees’ perception of their organization’s prestige influence pro-organizational behaviours. Such attempts resulted in linking PEP to employee deviant behaviour (Emilisa et al., Citation2018; Tuna et al., Citation2016), employees’ attitude (Arthur, Citation2020), commitment (Shrand & Ronnie, Citation2021), ethical intention (D. S. Kang et al., Citation2011) and customer-oriented citizen behaviours (D. S. Kang & Bartlett, Citation2013). The literature also found that PEP is a good predictor of expected values in a work environment (Berghaus, Citation2020).

Extant literature is not exact in linking PEP and ethical behaviour (or its proxies). The works of Emilisa et al. (Citation2018), Tuna et al. (Citation2016) and Kang et al. (Citation2011) provide some perspectives on the link. Emilisa et al. (Citation2018) relied on a sample of 120 automotive workers in Jakarta to establish that high positive PEP is associated with low deviant workplace behaviour. This finding largely confirms the findings of Tuna et al. (Citation2016) who argued that motivations for belonging to prestigious organization produce a positive effect on job satisfaction and reduces workplace deviant behaviour.

It is pertinent to link POP and ethical decision-making, especially using data from public-interest organizations that tout ethics as a key pro-organizational behaviour. The extant literature is faint on this relationship. A proximate literature on this relationship is captured by Kang et al. (Citation2011). Their study draws on a survey data from 477 employees working in leading corporations in South Korea. The study found that perceived external prestige is a predictor of ethical intention. To extend the frontiers of this literature, this current study traced the relationship between the respective POP perspectives (i.e., PEP and SPP) across three EDM stages. Specifically, the study hypotheses as follows:

H1a: PEP predicts the ethical issue recognition, ethical judgement, and ethical intention stages of EDM.

H1b: SPP predicts the ethical issue recognition, ethical judgement, and ethical intention stages of EDM.

2.3.2. Interrelationship among PEP, SPP and EDM

The literature (Frunzaru & Dumitriu, Citation2015) sought to suggest that the two perspectives of POP valuations (i.e., PEP and SPP) are independent of each other. An emerging literature (Bright (Citation2021) provides evidence to the contrary. The study found an interaction between the two POP valuations. The study holds that PEP mediates the relationship between public service motivation (liken SPP), and pro-organizational outcomes (i.e., turnover intention). This finding is critical in providing focus of POP-enhancement activities in organizations. This study is interested in examining whether the interaction between PEP and SPP exists in the context of ethical decision-making. Following the insights provided by Bright (Citation2021), the following hypotheses are proposed:

H2:

PEP mediates the relationship between SPP and EDM.

The mediation effect of PEP is examined at ethical intention stage of EDM, considering that the literature suggests ethical intention is a proximate measure of ethical behaviour (Rest, Citation1984).

2.3.3. Moderation effect of decision-makers’ financial situation on POP-EDM relationship

The pertinent question is whether the presence/absence of situational factors could change PEP-EDM dynamics. The literature has not directly answered this question, but perspectives on the influence of situational factors on pro-organizational behaviours could serve as a starting point for addressing this pertinent question. Shamsudheen and Rosly (Citation2020) used a sample of 262 Islamic banking practitioners in United Arabs Emirate and found that the presence of organizational situational factors (i.e., reward and punishment systems, corporate policies, code of ethics, etc.) change the dynamics of ethical choices in the organization. Lefevor et al. (Citation2017) meta-analysis study with 46,705 participants found that situational factors do not explain spontaneous helping behaviour. The study called for the examination of individual situational factors to explain this pro-organizational behaviour.

Ness and Connelly (Citation2017) relied on a survey of 172 students in a university in USA and reports that decision ethicality is greater when individuals are the recipients of consequences. Elshaer et al. (Citation2022) found a positive association between situations of the individual (i.e., job insecurity, family pressures, and financial pressures) and intention to engaging in unethical organization behaviours.

To advance literature, this study examined whether the relationship between organizational prestige (specifically, PEP) and EDM is moderated by an individual’s financial situation. It is pertinent to test the moderation effect of decision-maker’s financial situation on the POP-EDM relationship at multiple stages because moderation effect could vary across the EDM stages. For convenience, the study tested moderation at the first and third stages, respectively. The hypotheses are that:

H3a: Decision-maker’s financial situation moderates the relationship between PEP and EDM at the ethical issue recognition stage.

H3b: Decision-maker’s financial situation moderates the relationship between PEP and EDM at the ethical intention stage.

3. Methodology

3.1. Research design, sample, and data

The study uses a quantitative survey method, essentially because the study involved establishing relationships among variables. Data for the study was collected from 356 sampled tax accountants in Ghana. The tax accountants work in Ghana Revenue Authority (GRA), private tax practice firms, and tax division of licenced audit firms. A threshold inclusion criterion is professional belongingness to recognized accountancy body (i.e., Institute of Chartered Accountants (Ghana) or ACCA). The target population thus comprises professional accountants who work in the tax workspace in Ghana. The Accountancy profession regulator estimates the population as nine hundred (900). A total of 450 tax accountants (about half of the estimated population) were contacted to participate in the study. The 450 samples was guided by Hair et al.’s (2017) admonition on minimum sample size for PLS-SEM studies. The authors hold that to the sample size should be at least ten times higher than the number of indicators of the construct with the highest indicators. In this study, decision-maker’s financial situation is constructed with the highest number of indicators (4). From this perspective, the minimum sample size is 40. A total of 356 effective responses were received. This sample satisfies the minimum sample size requirement.

The data was collected using self-administered questionnaires (Appendix 1). The questionnaire development process included a technical review of the original instrument by three experienced tax practitioners. The technical review was a step towards ensuring content validity (Taherdoost, Citation2016) of the tax ethics vignette, and the self-constructed constructs (decision-maker’s financial situation). This was followed by a face validity procedure with 63 professional accounting students. The final questionnaire comprises four sections. The first section collected background information of the respondents. The second section collected information on the dependent variable, EDM. The section contained a vignette on a tax-related dilemma, and the respondents were requested to read the vignette, assume the roles of the tax accountants, and respond to specific statements. The third section collected data on the perception of organizational prestige. Two dimensions of perceived organizations (i.e., PEP and SPP) were captured in this section. The fourth section collected data on the financial situation of the respondents.

3.2. Measurement of variables

The variables of interest are ethical decision-making (EDM), perceived organizational prestige (POP), and decision-maker’s financial situation. All the variables of interest are latent variables, with observable variables measured on a 7-point Likert scale.

3.2.1. Ethical decision-making

Following Rest’s (1986) EDM model, the study conceptualized and measured at three stages (i.e., ethical issue recognition, ethical judgement, and ethical intention). To measure EDM, the respondents were exposed to four tax ethical vignettes. The vignette captures interaction of hypothetical tax accountants. Four extracts were taken and for each, the respondents were expected to react to a question to measure ethical issue recognition, ethical judgement, and ethical intention. The vignettes were original but the items for measuring the proxies of ethical decision were adapted from Musbah et al. (Citation2016). The statement for measuring ethical issue recognition is “I consider ethical issue(s) in this scenario as important”. The statement for measuring ethical judgment is “The [decision-maker in the vignette] is right by taking the decision [in the vignette]”. To measure ethical intention, the respondents responded to the statement “I will take same decision if I am the decision-maker [in the vignette]”

The Cronbach’s alpha 0.877, 0.874 and 0.885 for ethical issue identification, ethical judgment, and ethical intention, respectively, is indicative of a good scale reliability.

3.2.2. Perceived organizational prestige

Two dimensions of POP are measured: self-perception of organizational prestige (SPP) and perceived external prestige (PEP). The measurement items were adapted from Arthur (Citation2020).

To measure PEP, the respondents specified their level of agreeableness to two items: “people in my profession think highly of the firm/institution I work for”; and “the firm/institution I work for has prestigious reputation in the business community”. Relatedly, to measure SPP, respondents specified their level of agreeableness to two items: “I recognize the firm/institution I work for as highly prestigious”; and “I consider the firm/institution I work for as ‘one of the best’ in the field”.

Composite reliability for PEP and SPP is 0.961 and 0.973 (higher than benchmark 0.70), respectively, and us indicative of good internal consistency.

3.2.3. Decision-maker’s financial situation

Decision-maker’s financial situation is a latent variable measured with four items. Two items on the scale requested the respondents to react to statements on sufficiency of respondent’s family income to meet regular needs and emergency needs. A third item measured sufficiency of respondent’s savings/investment in case he/she loses his source of employment income. A fourth item requested the respondents to respond directly to the statement that they are not financially pressured. The responses are measured with a 7-point Likert scale with 1 indicative of the lowest level of agreement to the statement and 7 being the highest level of agreement to the statement.

The four indicators have a loading above the 0.70 threshold. The composite reliability for the variable is 0.947 (greater than the threshold of 0.70). The measurement scale is consistent, and the indicators are appropriate for the measurement of the variable.

3.3. Estimation strategy

The study adopted the Structural equation model (SEM) technique for estimating the relationship among the variables of interest. SEM has become a favourite estimation technique, especially when the variables of interest are not readily observable, but manifest through several formative or reflective indicators (Nitzl, Citation2016). Again, SEM comes in handy for studies that involve studying systems of relationships in the same model (Hair et al., Citation2012). The paper adopts the partial least squares structural equation model (PLS-SEM) as opposed to an alternative, covariance-based SEM. PLS-SEM is preferred because it maximizes explained variance of the endogenous latent variables (Hair et al., Citation2012).

4. Empirical Analysis

4.1. Sample description

The sample of tax accountants comprises of 231 (65%) males and 125 (35%) females. This corresponds to male gender dominance demographic characteristic of the accounting profession in Ghana (ICAG, 2021). The majority (71%) of the sample hold professional qualifications in both Accounting and Taxation. The minority (29%) are qualified accountants but not qualified tax accountants. All the respondents claimed tertiary qualifications, with a vast number (47.5%) of the respondents claiming to hold a Master’s degree. Majority of the respondents (62%) have more than 5 years professional experience.

4.2. Descriptive statistics for variables of interest

The independent variables in this study are PEP and SPP. The dependent variable is EDM, proxied by ethical issue recognition, ethical judgement, and ethical intention. The moderating variable is decision-makers’ financial situation. Table provides detailed descriptive characteristics of the variables of interest.

Table 1. Descriptive characteristics of variables of interest

Numerically, respondents score higher for the first stage of EDM (ethical issue recognition) comparative to the second and the third stages. For all three stages of ethical decision-making, the average score falls above median score of 4.0, suggestive that the sampled respondents have a good score for EDM.

Another variable of interest is the financial situation of respondents. Overall, the respondents’ mean score is 3.91, less than the median score of 4. The sampled respondents on average assess their financial situation as financially pressured.

4.3. Diagnostics for PLS-SEM analysis

In preparation for PLS-SEM analysis, it is pertinent to run diagnostic tests to ensure models fitness. In the following sections, tests for indicator reliability (using the indicator loadings), internal consistency (using the composite reliability), and convergent validity (using average variance extracted) are presented. Discriminant validity (using the Forrnell-Larcker criterion) and collinearity (using the variance inflation factor) tests were also conducted.

4.3.1. Indicator reliability, Internal consistency, and convergent validity

Table provides the results for indicator reliability, internal consistency, and convergent validity for all five variables of interest. The results presented are indicator loading, Cronbach alpha (CA), composite reliability (CR), convergent reliability (CR) and average variance extracted (AVE).

Table 2. Indicator reliability, internal consistency, and convergent validity

The indicator reliability is measured using the indicator loadings. As a rule of thumb, a standardised outer loading of 0.70 and above is deemed to be significant and implies that the indicator is reliable (Aryati et al., Citation2018; Hair et al., Citation2014). All the indicators of the various constructs in this survey meet the threshold of 0.70. Based on the indicator loading, it is reasonable to conclude that the indicators for the variables in this study are reliable.

The CA and CR for all the constructs are above the minimum benchmark of 0.70 (Hair et al., Citation2014). It is safe to conclude that internal consistency is achieved. Relatedly, the AVE scores for all variables provide assurance on convergent validity.

4.3.2. Discriminant Validity

Another fitness test is discriminant validity. Using the Fornell-Larcker criterion, the square root of the AVE value of each construct is compared to the construct’s correlation with other constructs. To achieve discriminant validity, the square root of the AVE should be greater than the greatest of the correlations. The result of this test is shown for all three models in this paper in Table .

Table 3. Discriminant validity

The result in Table below shows that the square root of the AVE is higher than all the off-diagonal scores in the corresponding rows and columns. All the constructs of this study pass this test of validity.

4.3.3. Collinearity

The last set of diagnostics was collinearity test and common method bias. Variance inflation factor (VIF) comes in handy for testing for collinearity. As a rule of thumb, VIF below 5 is suggestive that the paired variables in a model are not collinear (Hair et al., Citation2021). Table provides the respective test results for the three models in this study.

Table 4. Collinearity

The VIF for all variables in the three models falls below the ceiling threshold of 5. It is safe to conclude that the models do not suffer from collinearity issues.

In testing for common method bias, the study relies on collinearity assessment approach (Kock, Citation2015). Using this approach, a VIF lower than 3.3 is indicative that the model is free from common method bias (Hair et al., 2017; and Kock, Citation2015). This threshold is satisfied in Table .

4.4. PLS-SEM results

This study has a model for each of the three study objectives. Table and Figure represent the results for the first objective. Table and Figure hold results for the second objective; and Table and Figure presents results for study objective 3.

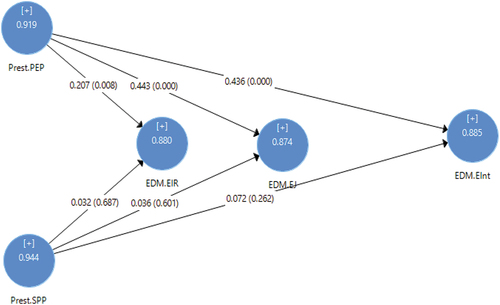

Figure 2. Influence of organizational prestige on EDM.

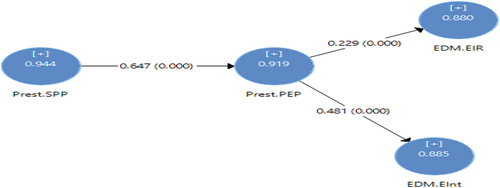

Figure 3. Interrelationship between SPP, PEP and EDM.

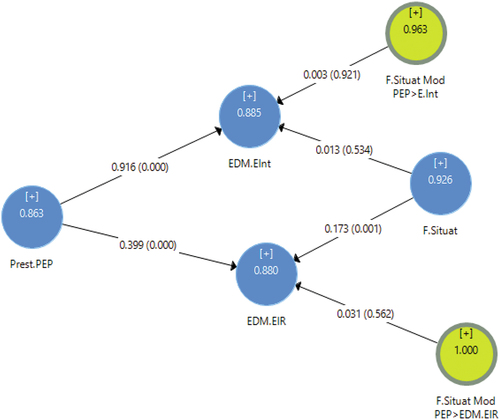

Figure 4. Moderating effect of financial situation (F.Situat) on PEP-EDM relationship.

Table 5. Influence of organizational prestige on EDM

Table 6. Interrelationship between SPP, PEP and EDM

Table 7. Moderating effect of financial situation (F.Situat) on PEP-EDM relationship

To address study objective 3, Table and Figure examined the moderating effect of decision-makers’ financial situation on the PEP-EDM relationship.

4.4.4. Hypotheses

Table provides the results of the underlying hypothesis of the study.

Table 8. Hypothesis results

4.4.5. Summary of results

The first model study traced the influence of SPP and PEP on three stages of EDM. The results show that SPP does not predict EDM; but PEP predicts EDM at all three stages. The second model examined the interrelationship among SPP, PEP and EDM. The results indicate that PEP mediates the relationship between SPP and PEP. The third model examines the moderating effect of decision-makers’ financial situation on the PEP-EDM relationship. The result was that decision-makers’ financial situation does not moderate the PEP-EDM relationship.

4.5. Discussion of the results

4.5.1. Influence of perceived organizational prestige on EDM

The first objective of the study was to trace the influence of perceived organizational prestige on the three stages of EDM. The result shows that PEP predicts all three stages of EDM. On the other hand, SPP does not predict any of the three EDM stages. The results provide justification for separating and studying the respective influence of the two POP valuations on pro-organizational behaviour. The study suggests that the link between POP and pro-organizational behaviour is driven by PEP perspective of POP, and not SPP perspective of POP. Specifically, it is organizational prestige valuation based on opinion of external stakeholders that provides motivation for ethical decision-making of the tax accountants. In the lenses of social identity theory, the study confirms that the tax accountants’ motivation to build and maintain social identity with prestigious tax organizations (publicly perceived as such) leads them to search and live up to a key valued in-group norm (ethical decision-making) of these organizations.

Another explanation for the link between PEP and EDM is that highly ethical employees are attracted to highly prestigious organizations. Whichever the case, the social identity theoretical explanation of the prestige-EDM link remains valid.

The finding of this study supports extant empirical literature that linked PEP to job satisfaction (Emilisa et al., Citation2018), employee commitment and attitudes (Y. H. Kang et al., Citation2020), and detrimental decision-making behaviour (Berghaus, Citation2020). The result of this study fetches at least two additional layers of insight. Firstly, by separating and examining the EDM influence of the two perspectives of POP, the literature is now specific on which dimension of POP counts towards EDM and pro-organizational behaviour in general. The finding has implication for organizations’ POP policy and practice. POP policies and programs should thus focus on building a good public image of the organization. Secondly, by running the EDM effect of PEP across the three EDM stages, this study established the full impact of POP variable on EDM. PEP valuation has been established as a variable that holds pervasive influence on EDM. For public-interest organizations (i.e., tax and accounting organizations) that emphasize ethical behaviour, high PEP valuation is an important variable. A high PEP valuation is a valuable arsenal for attracting and maintaining ethically upright professionals.

4.5.2. Mediating effect of PEP on SPP- EDM relationship

The second objective of the study relates to examining interrelationships among SPP, PEP and EDM. The first model discounts the influence of SPP on EDM (i.e., SPP does not directly influence EDM) but the second model provides a better insight. SPP (i.e., POP valuation based on internal stakeholders’ personal experiences in their organization) is an antecedent for PEP valuation. In other words, PEP mediates the relationship between SPP and EDM. This study discounts the notion that SPP and PEP are independent of each other (Frunzaru & Dumitriu, Citation2015) and lends support to the holding of Bright (Citation2021).

The finding has policy implications. Firstly, SPP is important for improving EDM (by extension pro-organizational behaviours) only to the extent that it translates into improved PEP valuations. POP policies and programs should be conscious in linking internal stakeholders’ experiences in the organization to external public image valuations. For instance, POP programs and policies should encourage internal stakeholders to propagate their memorable experiences with their organization to the public in the bid to improve the organizations’ PEP and ultimately EDM. Secondly, it will be erroneous for organizations to de-emphasize SPP building programs in their POP policies and programs, because SPP is an antecedent of PEP. PEP valuations are optimized when SPP valuations are high.

4.5.3. Moderating effect of decision-makers’ financial situation on PEP- EDM relationship

The third objective of this study was to examine the moderating effect of decision-maker’s financial situation on PEP-EDM relationship. The results indicates that decision-makers’ financial situation does not moderate the PEP-EDM relationship.

In explaining motivations for fraud, the literature (Dorminey et al., Citation2012) underscores that the presence of pressure on individuals could change ethical dynamics. In developing country contexts, unethical practices are often linked to financial situation of the decision-makers (Boonmanunt et al., Citation2020; Gumusay, Citation2019; Tang & Chiu, Citation2003). The result of this study runs contrary to this literature. The decision-maker’s financial situation is not potent enough to alter the dynamic of influence of an organization’s prestige on EDM. In the context of the data, the direction and magnitude of influence of PEP on EDM is unshaken, even in the presence of unsound financial situation of the tax accountants. This study supports the social identity theory’s amplification of the value of social identities and adds that organizational relevance of positive social identity valuations remains potent in the presence of financial pressure/situation of individuals. Future studies should revisit the specific influence of financial inducements on ethical behaviour, especially with data from developing countries.

5. Conclusion, limitations, and recommendations

This paper seeks to establish the dynamics of the relationship among organizational prestige valuations, decision-makers’ financial situation and EDM. The paper draws from the social identity theory. The sample comprises 356 tax accountants in Ghana. Data was analysed using PLS-SEM. The study found that only perceived external prestige valuation (PEP) counts towards EDM. PEP also mediates the relationship between SPP and EDM. Finally, decision-makers’ financial situation does not change the dynamics of the relationship between PEP and EDM.

The study contributes to literature in at least three ways. The study is foremost in linking prestige valuations, financial situation and EDM. By this successful linkage, the study contributes to social identity theory, and provides an additional reason for firms’ prestige-building effort. Secondly, by separating and examining the influence of the two dimensions of organizational prestige valuation, the study provides a precision on the perspective of prestige valuation that organizations should be most interested in. The study also contributes by testing how social identity motivations for ethical decision fare in the presence of an individual-level ethical pressure (decision-maker’s financial situation).

Policy implication of this study is threefold. First, the result of this study provides another justification for genuine organizational prestige-building activities. Policy makers at the firm level will be energized to boost the public image of their organization, as this affects a critical success factor for accounting and tax organisations. The organizations should be keen to associate with activities that project the image of the organization positively and eschew actions that potentially cast the organization’s prestige in a bad light. Secondly, the finding on the interrelationship between SPP, PEP and EDM should guide organizational policymakers to put forward strategies to translate the positive experience of internal stakeholders into positive public organizational prestige. Towards boosting EDM, the organizational members’ goodwill and positive experiences about their firm becomes important only when it translates into positive external prestige valuation of the organization. The study also provides evidence to discount the influence of individual financial situation on ethical behaviour.

The study has two inherent limitations. Firstly, the paper draws on perspectives of only tax practitioners who affiliates with only accountancy profession. The tax workspace has several other professional groups (i.e., lawyers, marketers, IT professionals, etc). The perspectives of tax accountants may thus not represent pervasive view of tax practitioners. Audience should thus be guided in generalizing the findings of the study. Secondly, the study draws on rationalist perspectives on ethical decision-making. The social identity theory and Rest’s EDM framework follows epistemological views of rationalists and assumed that decision-makers can rationally explain their ethical choices. The limitations of rationalists’ argument apply to this study.

Future research should extend the scope of this study by capturing perspectives of multi-professionals in the tax workspace. Relatedly, future studies should explore other potential anchors for the POP-EDM relationship.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Holy Kwabla Kportorgbi

Holy Kwabla Kportorgbi is a lecturer at the department of Accounting and Finance of Ghana Institute of Management and Public Administration (GIMPA). He is also a PhD candidate at University of Ghana Business School. His PhD thesis in on ethical decision-making. His current research interest is in the areas of tax ethics, tax compliance tax policy, and financial reporting.

Francis Aboagye-Otchere is a senior lecturer at the Department of Accounting at the University of Ghana Business School. His research areas are corporate governance, corporate social responsibility, environmental accounting, and ethics. He has extensive experience in university level teaching, executive and adult training, organizational and financial restructuring, design, redesign and improvement of business processes.

Teddy Ossei Kwakye is a senior lecturer at the Department of Accounting at the University of Ghana Business School. Teddy’s research focuses on addressing strategic management accounting, corporate governance, financial and socio-environmental reporting, and ethics.

Notes

1. For all the models, the adjusted R-square is lower than the R-square, indicative that adding additional predictor may add little to the explanatory power of the model.

References

- Abrams, D., & Hogg, M. A. (1990). Social identification, self-categorization and social influence. European Review of Social Psychology, 1(1), 195–22. https://doi.org/10.1080/14792779108401862

- Addo, A. (2021). Controlling petty corruption in public administrations of developing countries through digitalization: An opportunity theory informed study of Ghana customs. The Information Society, 37(2), 99–114. https://doi.org/10.1080/01972243.2020.1870182

- Akgunduz, Y., & Bardakoglu, O. (2017). The impacts of perceived organizational prestige and organization identification on turnover intention: The mediating effect of psychological empowerment. Current Issues in Tourism, 20(14), 1510–1526. https://doi.org/10.1080/13683500.2015.1034094

- Arthur, S. K. (2020). Perceived external prestige and employees’ attitude at the Ghana national fire service, Cape Coast (Doctoral dissertation, University of Cape Coast).

- Aryati, A. S., Sudiro, A., Hadiwidjaja, D., & Noermijati, N. (2018). The influence of ethical leadership to deviant workplace behavior mediated by ethical climate and organizational commitment. International Journal of Law and Management, 60(2), 233–249. https://doi.org/10.1108/IJLMA-03-2017-0053

- Berghaus, B. (2020). Prestige preference and person–organisation fit. In Conspicuous Employment (pp. 141–166). Springer.

- Boğan, E., Dedeoğlu, B. B., Batman, O., & Yıldırgan, R. (2020). Exploring the predictors of prospective employees’ job pursuit intention in Muslim-friendly hotels. Tourism Management Perspectives, 34, 100663. https://doi.org/10.1016/j.tmp.2020.100663

- Boonmanunt, S., Kajackaite, A., & Meier, S. (2020). Does poverty negate the impact of social norms on cheating? Games and Economic Behavior, 124, 569–578. https://doi.org/10.1016/j.geb.2020.09.009

- Bright, L. (2021). Does perceptions of organizational prestige mediate the relationship between public service motivation, job satisfaction, and the turnover intentions of federal employees? Public Personnel Management, 50(3), 408–429. https://doi.org/10.1177/0091026020952818

- Carmeli, A., Gelbard, R., & Goldriech, R. (2011). Linking perceived external prestige and collective identification to collaborative behaviors in R&D teams. Expert Systems with Applications, 38(7), 8199–8207. https://doi.org/10.1016/j.eswa.2010.12.166

- Casali, G. L., & Perano, M. (2021). Forty years of research on factors influencing ethical decision making: Establishing a future research agenda. Journal of Business Research, 132, 614–630. https://doi.org/10.1016/j.jbusres.2020.07.006

- Dorminey, J. W., Fleming, A. S., Kranacher, M. J., & Riley, R. A., Jr. (2012). Financial fraud. The CPA Journal, 82(6), 61.

- Dutton, J. E., Dukerich, J. M., & Harquail, C. V. (1994). Organizational image and member identification. Administrative Science Quarterly, 39(2), 239–263. https://doi.org/10.2307/2393235

- Elshaer, I. A., Ghanem, M., & Azazz, A. (2022). An unethical organizational behavior for the sake of the family: Perceived risk of job insecurity, family motivation and financial pressures. International Journal of Environmental Research and Public Health, 19(11), 6541. https://doi.org/10.3390/ijerph19116541

- Emilisa, N., Putra, D. P., & Yudhaputri, E. A. (2018). Perceived external prestige, deviant workplace behavior dan job satisfaction pada Karyawan Industri Otomotif di Jakarta. Jurnal Manajemen dan Pemasaran Jasa, 11(2), 247–262. https://doi.org/10.25105/jmpj.v11i2.2959

- Francis, J. R., Mehta, M. N., & Zhao, W. (2017). Audit office reputation shocks from gains and losses of major industry clients. Contemporary Accounting Research, 34(4), 1922–1974. https://doi.org/10.1111/1911-3846.12328

- Frunzaru, V., & Dumitriu, D. L. (2015). Self-perceived occupational prestige among Romanian teaching staff: Organisational explicative factors. Management Dynamics in the Knowledge Economy, 3(4), 629–643.

- Fuller, J. B., Hester, K., Barnett, T., Frey, L., Relyea, C., & Beu, D. (2006). Perceived external prestige and internal respect: New insights into the organizational identification process. Human Relations, 59(6), 815–846. https://doi.org/10.1177/0018726706067148

- Gumusay, A. A. (2019). Embracing religions in moral theories of leadership. Academy of Management Perspectives, 33(3), 292–306. https://doi.org/10.5465/amp.2017.0130

- Hair, J. F., Jr., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2021). A primer on partial least squares structural equation modeling (PLS-SEM). Sage publications.

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2012). Partial least squares: The better approach to structural equation modeling? Long Range Planning, 45(5–6), 312–319. https://doi.org/10.1016/j.lrp.2012.09.011

- Hair, J. F., Jr., Sarstedt, M., Hopkins, L., Kuppelwieser, V. G., & Hair, J. F. (2014). Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. Journal of Family Business Strategy, 5 (1), 105–115. European business review. https://doi.org/10.1016/j.jfbs.2014.01.002

- Kang, D. S., & Bartlett, K. R. (2013). The role of perceived external prestige in predicting customer‐oriented citizenship behaviors. Human Resource Development Quarterly, 24(3), 285–312. https://doi.org/10.1002/hrdq.21165

- Kang, Y. H., Lee, E. H., & Kang, K. H. (2020). Effects of organizational socialization, perceived organizational vision and attitude toward organizational change on organizational commitment of general hospital nurses. Journal of Korean Academy of Nursing Administration, 26(5), 468–477. https://doi.org/10.11111/jkana.2020.26.5.468

- Kang, D. S., Stewart, J., & Kim, H. (2011). The effects of perceived external prestige, ethical organizational climate, and leader‐member exchange (LMX) quality on employees’ commitments and their subsequent attitudes. Personnel Review, 40 (6), 761–784. Personnel Review. https://doi.org/10.1108/00483481111169670

- Kock, N. (2015). Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of E-Collaboration, 11(4), 1–10. https://doi.org/10.4018/ijec.2015100101

- Kportorgbi, H. K., Kwakye, T. O., & Aboagye-Otchere, F. (2022). Ethical decision-making of tax accountants: Examining the relative effect of religiosity, re-enforced tax ethics education and professional experience. Cogent Business & Management, 9(1), 2149148. https://doi.org/10.1080/23311975.2022.2149148

- Lefevor, G. T., Fowers, B. J., Ahn, S., Lang, S. F., & Cohen, L. M. (2017). To what degree do situational influences explain spontaneous helping behaviour? A meta-analysis. European Review of Social Psychology, 28(1), 227–256. https://doi.org/10.1080/10463283.2017.1367529

- Lincoln, S. H., & Holmes, E. K. (2008). A Need to Know: An Ethical Decision-Making Model for Research Administrators. The Journal of Research Administration, 39(1), 41–47. http://www.srainternational.org/sra03/template/tntbjour.cfm?id=598

- Mintz, S., & Morris, R. E. (2022). Ethical obligations and decision making in accounting. McGraw-Hill US Higher Ed USE.

- Musbah, A., Cowton, C. J., & Tyfa, D. (2016). The role of individual variables, organizational variables and moral intensity dimensions in Libyan management accountants’ ethical decision making. Journal of Business Ethics, 134, 335–358. https://doi.org/10.1007/s10551-014-2421-3

- Ness, A. M., & Connelly, S. (2017). Situational influences on ethical sensemaking: Performance pressure, interpersonal conflict, and the recipient of consequences. Human Performance, 30(2–3), 57–78. https://doi.org/10.1080/08959285.2017.1301454

- Nguyen, B., & Crossan, M. (2021). Character-infused ethical decision making. Journal of Business Ethics, 178(1), 1–21. https://doi.org/10.1007/s10551-021-04790-8

- Nitzl, C. (2016). The use of partial least squares structural equation modelling (PLS-SEM) in management accounting research: Directions for future theory development. Journal of Accounting Literature, 37, 19–35. https://doi.org/10.1016/j.acclit.2016.09.003

- Pratiwi, I. W., Armanu, A., & Rahayu, M. (2022). Perceived external prestige on deviant workplace behavior with mediation of job satisfaction and organizational commitment. jurnal aplikasi manajemen, 20(3). https://doi.org/10.21776/ub.jam.2022.020.03.16

- Rest, J. R. (1984). Research on moral development: Implications for training counseling psychologists. The Counseling Psychologist, 12(3), 19–29. https://doi.org/10.1177/0011000084123003

- Shamsudheen, S. V., & Rosly, S. A. (2020). The impact of situational factors on ethical choice: A survey of Islamic banking practitioners in UAE. Journal of Islamic Accounting and Business Research, 11(6), 1191–1210. https://doi.org/10.1108/JIABR-03-2018-0048

- Shrand, B., & Ronnie, L. (2021). Commitment and identification in the ivory tower: Academics’ perceptions of organisational support and reputation. Studies in Higher Education, 46(2), 285–299. https://doi.org/10.1080/03075079.2019.1630810

- Taherdoost, H. (2016). Validity and reliability of the research instrument; how to test the validation of a questionnaire/survey in a research. How to Test the Validation of a Questionnaire/Survey in a Research, 10, 2016. https://doi.org/10.2139/ssrn.3205040

- Tajfel, H. (1982). Social psychology of intergroup relations. Annual Review of Psychology, 33(1), 1–39. https://doi.org/10.1146/annurev.ps.33.020182.000245

- Tang, T. L. P., & Chiu, R. K. (2003). Income, money ethic, pay satisfaction, commitment, and unethical behavior: Is the love of money the root of evil for Hong Kong employees? Journal of Business Ethics, 46(1), 13–30. https://doi.org/10.1023/A:1024731611490

- Tuna, M., Ghazzawi, I., Yesiltas, M., Tuna, A. A., & Arslan, S. (2016). The effects of the perceived external prestige of the organization on employee deviant workplace behavior: The mediating role of job satisfaction. International Journal of Contemporary Hospitality Management, 28(2), 366–396. https://doi.org/10.1108/IJCHM-04-2014-0182

Appendix 1:

Questionnaire

SECTION B: TAX DECISION MAKING

The scenarios that you are about to read are hypothetical and are meant for this research only.

Scenario 1:

Nimo and Kaiza have been friends. Their friendship dates to their university days, when they were roommates. Nimo works with Ghana Revenue Authority (GRA) and on one occasion, led a team for tax audit at a company (Freeze Ltd). Kaiza is a senior consultant at a private tax practice firm, and in charge of managing tax affairs of Freeze Ltd. Nimo and Kaiza did not disclose to their long-standing friendship to their respective superiors.

8. Based on the case, rate your reaction to each statement by ticking a number that reflects your opinion, where:

Scenario 2

Nimo suspected that Freeze Ltd operates an undisclosed bank account. Kaiza is aware that Freeze Ltd operates a secret bank account but remained quiet when Freeze’s officials denied the allegation. Nimo’s team did not probe the issue further.

9. Based on the case, rate your reaction to each statement by ticking a number that reflects your opinion, where:

Scenario 3

The GRA team did not carry out any audit procedure on PAYE after realizing that tax filling of Freeze Ltd were handled by Kaiza-a Chartered Tax practitioner.

10. Based on the case, rate your reaction to each statement by ticking a number that reflects your opinion, where:

Scenario 4

Nimo-led team assessed Freeze Ltd.’s tax liability as Ghc450,000. After the field audit, Nimo held a review meeting with his supervisor. At the review meeting, Nimo’s supervisor said, “let the working papers reflect a tax position of GHC80,000; when Freeze Ltd is happy, we are happy as a team” Nimo complied and reviewed the working papers to reflect a tax position of GHC80,000.

11. Based on the case, rate your reaction to each statement by ticking a number that reflects your opinion, where:

SECTION C: FINANCIAL SITUATION

12. Please indicate if you agree or disagree with the following items. Rate your reaction to each statement by ticking a number that to the right of each statement where:

SECTION D: PERCEIVED ORGANIZATIONAL PRESTIGE

13. Please indicate your level of agreement or disagreement with each of the statements, as it relates to the organization you work for. Each reaction represents a feature of an ethical approach, as such, there are no right or wrong answers.