Abstract

The study investigates the effects of financial accounting services on SMEs’ financial performance. The agency theory was used in the research. The study used a quantitative strategy and a survey method to acquire the essential data for the project. The study used a sample of 320 SMEs to carry out the analysis. Partial least square structural equation modelling was used to undertake the statistical analysis. The results indicate that using financial accounting services helps SMEs improve their financial performance. The research also discovered a link between information technology and SMEs’ financial performance. The findings of our research reveal that, small businesses that employ accounting services in their business experience an increase in financial performance. This is because the use of financial accounting has a lot of technical advantages which can be helpful to business users. A lot of SMEs need credit to be able to improve their business, therefore they need a financial statement to serve as evidence of their performance before the loan could be granted to them. This means that financial accounting service is a key component in the scheme of this SME. Information technology has been one of the driving forces of every business. It was found that information technology has a positive effect on the financial performance of SMEs. The study is unique in that it gives a successful approach for small and medium-sized businesses in emerging nations to focus more on the function of financial accounting in improving business performance.

PUBLIC INTEREST STATEMENT

This study examined how access to financial accounting services and information technology can aid in SME financial performance. Specifically, it investigated the idea that firms can benefit from the use of financial accounting services such as the keeping of books of prime entry and preparing a basic financial statement to be able to ascertain the profit that the firm has generated. The implementation of basic accounting functions could help SMEs to know their financial position and to be able to streamline their financial activities. We also investigate how the use of information technology could help increase the financial performance of the SME. The study also looked at how information technology could be employed by the SME in using financial accounting services which will ultimately lead to an increase in the financial performance of the firm. Data were collected from 375 SME owners/managers in Ghana. The findings suggest that the use of financial accounting could lead to an increase in the financial performance of SMEs and also the application of information technology could also lead to an increase in financial performance. The findings also indicate that information technology could moderate financial accounting services and ultimately lead to an increase in financial performance. It was recommended that SMEs should access financial accounting services and should make use of information technology to drive their firm forward and increase their financial performance.

1. Introduction

The idea of a Small and Medium Size Business (SME) has drawn the interest of various researchers over the past few decades, and its significance is increasing. SMEs owe the nation duties above what they owe to themselves to promote national development. SMEs should work to improve, regardless of their size and kind, to fulfil their obligation to the economy (Eniola & Ektebang, Citation2014).

Previous studies on SME performance have usually been limited to issues other than accounting services. For example, Motta and Sharma (Citation2020) examine the impact of lending technologies, such as fixed asset lending and financial statement lending, and the financial performance of SMEs. The weakness in their research is that issues that need to be improved or implemented such as accounting services which can impact financial performance were not looked at. Rita and Huruta (Citation2020), examine the influence between access to financing and performance through the mediation of entrepreneurial-oriented finance in batik SMEs and found no positive effect between financing access and SME performance. In addition to the above, researchers focused on individual sectors operated by SMEs. For example, Motta and Sharma (Citation2020), examine the impact of lending technologies, such as fixed asset lending and financial statement lending, and the financial performance of SMEs. Rita and Huruta (Citation2020), examine the influence between access to financing and performance through the mediation of entrepreneurial-oriented finance in Batik SMEs and found no positive effect between financing access and SME performance. The weakness in their studies is that the focus was on only one sector the Batik industry. These create a research gap that this study attempts to fill. To fill the gap, the current study focuses on four business sectors. Trade sector, Services sector, Manufacturing sector and Agriculture sector

Because of this, the current research has developed research objectives to be achieved by collecting data through questionnaires from SMEs.

The objectives of the study are to analyse the effect of financial accounting services and information technology on the financial performance of SMEs. The research also evaluates the moderating effect of information technology on financial accounting services and SME financial performance. This study seeks answers to the research questions: what are the effects of financial accounting services on the financial performance of SMEs? What are the effects of information technology on the financial performance of SMEs? And what are the moderating effects of information technology on financial accounting services?

To achieve the above objective, the study employed the use of the Agency theory and the Technology acceptance model to aid in answering the research questions. The agency theory has been widely used in the area of research about companies where the principal delegates function to the agent to work on his behalf. Agency theory has not often been used in the area of SME research. This crate a theoretical gap that the current study attempt to fill. According to Gyimah et al. (Citation2022), the accessibility of credit has been a major barrier to SME expansion. However, it is important to note that the banks that grant credit to SMEs demand financial statements before granting credit. This confirms the importance of financial accounting services to SMEs.

The motivation for this study stems from the fact that SMEs are the backbone of various economies and are critical to most economies worldwide, particularly developing and emerging markets such as Ghana. According to the World Bank, formal SMEs account for up to 60% of total employment and 40% of national income (GDP) in emerging nations, and these figures would be much higher if informal SMEs were included (The World Bank, Citation2022). In addition, the World Bank predicts that 600 million people will join the global workforce in the next 15 years, primarily in Asia and Sub-Saharan Africa (The World Bank, Citation2022).

The performance of SMEs is a precondition for overall performance. (SMEs) make up most companies globally (Lim et al., Citation2020). SMEs are a breeding ground for entrepreneurs and propel solutions to problems in human societies, helping to enhance the quality of life. The relevance of SMEs in economic and social development, poverty reduction, increased employment, output, technology development, and social position and improved standards have been established and recognised globally, in both emerging and developed nations. According to Eniola and Ektebang (Citation2014), (SME), development is an issue for many countries. SMEs participate in the economic operations of nations and have evolved into essential tools for economic development and workforces (Razak et al., Citation2018).

SMEs face a lot of challenges in their operations. Obtaining finance or loans is one of the challenges that SMEs encounter (Ivanová, Citation2017). According to Agbemava et al. (Citation2016), most SMEs have incomplete accounting records. Most small businesses have failed to grasp the value of a well-structured accounting system that would have allowed them to maintain accurate financial statements (Aladejebi & Oladimeji, Citation2019). It is submitted here that SMEs can make use of financial accounting services to improve their performance.

Many SMEs do not use accounting services due to a lack of managerial expertise, budgetary constraints, and human resource limits. Most small businesses fail due to a lack of planning, non-deployment of marketing tools, and poor organisational capabilities and competencies. Under Resource-Based Theory, SMEs lack the accounting knowledge needed to perform the accounting function internally (Rankhumise & Letsoalo, Citation2019). Most SMEs do not employ accounting services. The findings of Okwena et al. (Citation2011) show that small and medium-sized businesses’ basic accounting practices are insufficient, and have a detrimental impact on their financial performance.

It has been suggested that some SMEs in Ghana prepare and present financial statements to obtain a tax clearance certificate and bank facilities. It has been an acute challenge for SMEs’ inaccurate and inadequate accounting records and for that matter, access to accounting services.

Accounting services’ primary purpose is to provide reliable information to owners and managers of SMEs in any industry for performance measurement. Despite its importance in the success of enterprises, several SMEs have not paid much attention to accounting record-keeping for their commercial transactions. The challenge that motivates this study is the fact that many small businesses do not have access to accounting services; a fact that has been suggested to have negatively impacted the performance of SMEs.

This study contributes to the literature as follows. First, it addresses the relationship between Financial accounting services and SME financial performance, strengthening prior evidence concerning the positive impact of SMEs on financial performance. Our results support the agency theory, which advocates a positive influence of the agent employing activities on behalf of the principal which will improve the financial performance of the firm financial performance. Second, it contributes significantly to research on the moderating role of information technology between financial accounting services and financial performance. We identify the essential role of information technology and present its significant moderating effects on the relationship between financial accounting services and SME performance. Third, the establishment of the relationship between financial accounting services and SME financial performance strengthens the general operations of the SMEs and such studies are relatively low in the literature. The application of the findings of this research to SMEs in developing nations such as Ghana reinforces the uniqueness of this study and considerably contributes to the literature in terms of policy, theory, and practice. Fourth, this study contributes towards increasing the limited knowledge among SMEs about financial accounting services and the benefit they can derive from it, by confirming the relationship between financial accounting services and financial performance in the circumstance of SMEs. Fifth our findings support the agency theory by eliminating conflicts of interest and coordinating the interests of owners, managers, and employees.

The rest of the paper is as follows. It starts with the background which focuses on the policy, the regulatory regime, the reforms and the developments of SMEs in Ghana. The next one is about theoretical literature review. This point explains the theory supporting the current studies. Furthermore, the next is about the empirical literature review and hypotheses development. This section focuses on the existing literature about the studies and the hypotheses developed. Research design is the next section which explains the kind of design that was adopted for the study. This is followed by the empirical and discussion section which discusses the results of the studies. The final section is the summary and conclusion. This section summarizes the study and concludes.

2. Background of the studies

Years after independence, Ghana’s industrial strategy has favoured large import substitution industries rather than SMEs, although the latter provides a larger share of employment (Adjabeng & Osei, Citation2022). In the early 1960s, after independence, Dr Kwame Nkrumah was concerned with the participation and domination of socialist countries for ideological reasons. The state operates a protectionist trade regime dominated by state-owned enterprises; as a result, the indigenous sector and entrepreneurial class within the country were considered too small and a threat to the political system to be encouraged (Aryeetey et al., Citation1996).

In 1970, the government of Dr Kofi Abrefa Busia promoted the development of small businesses through the enactment of the Ghana Business Promotion Act (Act 334) (Hansen & Ninsin, Citation1989). The political system limited the development of SMEs due to the interference of government officials, bureaucracy, and corruption (Hansen & Ninsin, Citation1989). To correct some of the causes of its prolonged economic downturn, Ghana introduced the Economic Recovery Program (ERP) Aryeetey et al., (1991). Abor and Hinson (Citation2004) confirmed that the main objective of the ERP is to create an enabling business environment that helps SMEs make a fruitful contribution to industrial development. In the past, with the support of other donors, the government has tried, implemented and operated many loan schemes for SMEs. Government and NGOs have contributed to the development of SMEs and significant contributions have been made to the promotion. These agencies include the National Board for Small-Scale Industries (NBSSI), Ghana Appropriate Skilled Industries Service (GRATIS), Business Assistance Fund (BAF), Ghana Investment Fund, Rural Enterprise Project (REP), government agencies, Government Organizations (NGOs), Commercial Banks, Development Finance Institutions (DFIs) and the PAMSCAD Line of Credit for Small Businesses (Baah-Nuakoh et al., Citation2002).

Many nations have identified SMEs as the foundation for sustained economic progress. But a lot of limitations prevent SMEs from reaching their full potential. Among them are outmoded technology, inadequate infrastructure, a lack of scale economies, poor corporate governance, reliance only on financial resources, and restricted access to information and technical skills (Ameyaw & Modzi, Citation2016). As a result, better policy frameworks are required for the development of SMEs. SMEs need professional procedures, financial supplies, and information sharing to help them grow. In Ghana, the regulatory body for SMEs is the Ghana Enterprises Agency (GEA), which is the governmental body responsible for the promotion and development of SMEs. With the passage of Act 1043 by Parliament in 2020, GEA is mandated to coordinate, implement and monitor the activities of the SMEs Sector in Ghana. The government of Ghana channel various policies and programs through the GEA to help develop the SME sector. The Ghana SME and Entrepreneurship Policy are made up of a wide range of meticulously crafted policy recommendations intended to restructure the MSME sector and coordinate government initiatives to provide sustainable growth pillars for the industry (Ministry of Trade and Industry, Citation2023). According to the Ministry, the government of. Ghana has put in place many policies to ensure the growth of SMEs. Among such policies are: Reducing entry barriers, Provision financial supports, Training and education, Involving SMEs in policymaking and the implementation process etc. (Ameyaw & Modzi, Citation2016).

3. Theoretical literature review

3.1. Agency theory

One of the first theories in management and economics literature is the agency model (Mitnick, Citation2019). According to the agency theory, a principal must hire an agent to carry out tasks on his or her behalf (Jensen & Meckling, Citation1976). Eisenhardt (Citation1989) further developed the agency theory under the premise that everyone acts in their own best interests.

The principle will take action to rein in the agent if the agent behaves in a way that serves his or her interests at the expense of the principal. To control the agent, the principal can make a contract with the agent, keep tabs on the agent’s actions, purchase insurance, or engage a second agent to keep watch over the agent (Schillemans & Busuioc, Citation2015). According to the agency theory, managing costs entails monitoring expenditures, reviewing compensation plans, and accounting for residual loss brought on by conflicts of interest between the principal and the agent Ali (Citation2020).

The agreement between shareholders, owners (principals) and management to oversee the performance of the firm is known as agency theory. The core principle of agency theory is that managers should prioritize their interests over those of others. This will permit the pursuit of self-interest, which raises expenses for the company. These costs may include the cost of creating contracts, loss resulting from agent decisions, and the cost of monitoring and overseeing agent behaviour (Payne & Petrenko, Citation2019). Different researchers have used agency theory in their studies to provide a theoretical base (Amin et al., Citation2022; Huu Nguyen et al., Citation2020 Li, Citation2020). This theory aids in investigating a social phenomenon from the standpoint of the principal-agent (manager). Jensen and Meckling (Citation1976) describe the agency theory as a contract that delegates certain decision-making power to the agent under which one or more persons (the principals) hire another person (the agent) to carry out some function on their behalf. Applying the agency theory to the SMEs means that the firms can delegate some key functions to some people (agents) to perform on their behalf which can increase the financial performance of the firm. According to Jensen and Meckling (Citation1976), there are two main tenets of the agency theory. First and foremost, both the principal and the agent aim to maximize their interests. Second, the agent may not act in the principal’s best interests because of potential conflicts between their interests. As a result, there may be a conflict of interest between the principal and agent. This sometimes creates disaffection among SMEs to employ agents who are professionals to management their business on their behalf. However, this fear can be overcome by the SME employing the services of an auditor to audit the work of the agents.

3.2. Limitation of agency theory

Although agency theory is very practical and well-liked, it nevertheless has several drawbacks, which have been noted by numerous authors (Vitolla et al., Citation2020). The theory presupposes an unpredictable future and a contractual agreement between the principal and agent for a finite or infinite future period (Panda & Leepsa, Citation2017). However, the contract between the contracting agreement between the principal and the agent is not permanent. In practice the owner of the SME could hire people to work on his behalf, these people may seek their interest and not the interest of the owner of the firm. In theory, contracting should be able to solve the agency problem, but in practice, it is often constrained by issues like knowledge asymmetry, rationality, fraud, and transaction costs (Bosse & Phillips, Citation2016). Agents employed by the managers of SMEs could engage in fraud and other activities which could affect the firm. Owners of SMEs’ interest is to maximise their return, but their role is sometimes limited in the firm.

3.3. Technology acceptance model (TAM)

While IT innovation has rapidly changed work in some areas of our business life in the past fifty years, some businesses and industries have been slow to adopt new technologies (Ducey & Coovert, Citation2016). Initially, the cost of such technologies enabled only large corporations to benefit from IT-related efficiencies; however, breakthroughs in microprocessors, computers, and industry standards enabled individuals and organizations of all sizes to reap the benefits of IT (Ducey & Coovert, Citation2016).

Information technology makes business and training easier than before. For example, Online trading has become more convenient for many. Online training, for example, makes materials accessible at any time, allowing the content to be reused anytime at little or no cost to the organization. This represents a significant shift from the traditional way of carrying out office functions, which requires much more support personnel at the cost of assigning more jobs to fewer personnel with information technology skills. Also, technology enables training specialists to design high-quality software for SMEs who might be interested in using Information Technology to turn around their business. Collectively, these examples highlight the rapid progression of organizational IT adoption, which has benefited a lot of entities in the late 20th and early 21st centuries.

The Technology Acceptance Model (TAM) is a theory of information technology adoption in organizations (Davis, Citation1987). This theory proposes that individual reactions toward technology influence his/her intentions to use the technology, which ultimately influences actual use. Researchers have identified the relevant factors which influence IT adoption. The most popular IT adoption paradigm is the Technology Acceptance Model (Marangunić & Granić, Citation2015). Davis (Citation1987), conducted a thorough study of the literature on information technology, human factors, and psychometrics concerning technology adoption in companies. He found two prevalent assumptions that affect IT adoption: perceived utility (PU) and perceived ease of use (PEOU). According to Davis (Citation1989), perceived usefulness is “the extent to which a person believes that utilizing a certain system would increase his or her job performance.” It is a cognitive assessment of how using new technology will affect how well one does their job. The term “degree to which a person believes that utilizing a certain system would be devoid of effort” is used to describe perceived ease of use (Granić & Marangunić, Citation2019). It is suggested to change how one feels about using new technology. The relevance of the Technology Acceptance Model to the current study is to identify the extent to which SMEs believe that the use of information technology can increase their performance and whether the use of a system would be free from mistakes.

4. Empirical literature review and hypotheses development

Because SME thoughts and ideas significantly contribute to the economic development of countries all over the world, they are frequently seen as an important phenomenon (Agyapong, Citation2010). It is increasingly difficult to ignore the significance of small and medium-sized firms (SMEs) in the economy in terms of employment, innovation, and standard of life (Larrán Jorge et al., Citation2016). In the western world, institutions, governments and SME owners aid in the implementation of programs and policies which help the firms to grow as compared to Africa. The idea of research and programs is more needed in emerging economies and developing countries such as Ghana to increase the performance of SMEs (Afriyie et al., Citation2019). Despite the widespread belief that SMEs must have an important function in nation development in addition to offering high-quality products and services at competitive prices and making returns for themselves and their families, the absence of strong professional programs like financial accounting services presents significant challenges for businesses that want to grow in developing countries such as Ghana (Amoako, Citation2013). Unfortunately, limited attention has been paid to the potential advantages that SMEs stand to benefit from participating in professional programs. A lot of the discussions about SMEs have centred around issues other than financial accounting services. For example, Ansong (Citation2017) investigated Corporate social responsibility and firm performance of Ghanaian SMEs: The role of stakeholder engagement and found an indirect effect of CSR on SMEs’ financial performance through stakeholder engagement. The agency theory has been used by many scholars and researchers in the context of companies in the past (Donaldson & Davis, Citation1991; Eisenhardt, Citation1989; Hill & Jones, Citation1992). A lot of the current studies also continue to use the agency theory at the corporate level (Kron et al., Citation2021; Vitolla et al., Citation2020). Elmagrhi et al. (Citation2019) used agency theory to explain the impact of female directors and board gender diversity on a company’s environmental performance. However, even though the present study is about SMEs, it is built upon the Agency theory. basic presumptions that agents are self-interested have distinct aims and risk-taking preferences from principals, and that it is problematic for one party (a principle) to use another (an agent) to make decisions and act on their own. Businesses’ responsibilities to society and the need to pursue activities that will contribute to nation-building cannot be overemphasised. According to empirical studies, well-designed and managed technical programs can benefit SMEs in a variety of ways by assisting them in understanding and leveraging such programs to benefit the firm (Raharja et al., Citation2019). Because SMEs mostly specialize in a particular area, their implementation of professional programs such as accounting services will enable them to be efficient and effective in their operations and will stand firm and have the necessary capabilities to perform and also grow to become a bigger company. Scholars have argued that one of the important factors that can drive SMEs forward is access to professional advice or programs (Hu & Kee, Citation2022).

Arguably, one of the programs which SMEs could implement which will have a significant influence on their performance is financial accounting services.

Nakku et al. (Citation2020) researched the interrelationship between SME government support programs (GSP), entrepreneurial orientation, and performance in a developing economy and found that both nonfinancial and financial GSPs on performance. It is important to state that one of the programs the government can offer to support SMEs is to provide them with accounting services.

4.1. The link between financial accounting services and financial performance

Accounting is an essential aspect of an organisation’s management process since it offers crucial information to the company’s planning, analysing, controlling, and decision-making processes (Esch et al., Citation2019). According to Uddin et al. (Citation2017), Accounting is crucial to the success or failure of today’s businesses. Accounting systems are in charge of recording, analysing, monitoring, and evaluating a company’s financial state, preparing tax records and giving information assistance to various other organisational responsibilities. Accounting systems provide owners and managers of SMEs in every industry with information for measuring financial performance.

The four main sub-systems of accounting services are the transaction processing system, general ledger/financial reporting system, fixed asset system, and management reporting system. The transaction processing system simplifies regular company processes by storing many documents and communications for users across the firm (Hall, Citation2010).

SMEs should show the frequency of six basic accounting reports and analyses generated by their firm (Ismail & Mat, Citation2009): the basic report he suggested are: Income statements, Balance sheets, Cash flow statements, Bank reconciliation, Aging schedules and financial ratios.

A few essential variables should be present to indicate that financial accounting is used in the firm. These are some of them: the collection of commercial papers such as invoice receipts, debit and credit notes, and so on daybooks, such as sales day books, purchases daybooks, return inwards and outwards day books, cash books, and so on. Accounting services are the outcome or the output of the activities of the accounting practices of the firm. This comes out when the accounting activities are put together for the benefit of the entity.

Accounting services and functions are essential to SMEs because they can provide them with better management control and assist in decision-making which will eventually lead to an increase in financial performance.

The essential accounting services that SMEs can keep are the daybooks, bank reconciliation, Ledgers and Accounts, Trial Balance, income statements, and statements of financial position. The effect of financial accounting on the performance of SMEs must be researched because there are a lot of benefits that SMEs can derive from accessing financial accounting services. Mwangi et al. (Citation2018) studies evaluated the impact of accounting outsourcing (AO) on SMEs’ financial performance. The relationship between accounting outsourcing (AO) “s influences and their impact on SMEs” financial performance was discovered. Ganesan et al. (Citation2018) evaluated the pattern of SMEs’ non-audit services and examined whether there is a link between non-audit service use and SMEs’ business performance. According to the study’s conclusions, using NAS from an external accountant substantially impacts business performance.

Aladejebi and Oladimeji (Citation2019), investigated the extent to which accounting data is used to assess the financial performance of small businesses. While respondents agreed that knowing the performance of the business is a significant benefit of keeping proper records. And that record-keeping is critical to the company’s success. Most SMEs owners lack basic accounting knowledge and decry the cost of preparing financial statements, so they keep the records manually. The importance of accounting services to firms cannot be overemphasized. Accounting control systems are critical for ensuring long-term and future competitiveness, performance, and success. It strengthens a firm’s adherence to accounting information quality standards and norms, as well as its long-term values, benefits, advantages, and contributions in extremely complicated markets and settings (Phomlaphatrachakom, Citation2020).

If SMEs implement these accounting services in their business, they will benefit from the advantages that come with the use of accounting services and will increase performance.

H1:

There is a positive relationship between Financial accounting services and financial performance.

4.2. The link between information technology and financial performance

ICT integration in companies has already had a positive impact on the economic performance of businesses in developing countries (Akinwale et al., Citation2017), where ICT plays a positive role in the growth and development of business according to the (World Bank Group, Citation2015). Information technology benefits SMEs in various ways, including reduced operational and administrative costs, better productivity, and improved business operations and growth (Chege & Wang, Citation2020). According to Hartoyo and Daryanto (Citation2016), SMEs can use ICT to upgrade or replace existing information systems and networks and thus extend their market. How this is done is that ICT can be used to send information to customers about product availability, and customers can pay through the electronic payment system. Additionally, SMEs can acquire accounting software which can help them to record customer transactions and can enable them to ascertain their profit. Information technology contributes to development by promoting information and knowledge, resulting in social and economic changes (Osborn et al., Citation2015). Information technology, which has become an inextricable part of daily life, is required for society to function (Roztocki & Weistroffer Roland, Citation2011). The above analysis indicates that the adoption of information technology can improve financial performance (Husin & Ibrahim, Citation2014). Performance may be defined as the reflection of how the resources of a company are used in the form which enables, it to achieve its objectives. Financial performance is the employment of economic indicators to measure the extent of objective achievement, contribution to making available financial resources and support of the company with investment opportunities (Gupta & Chopra, Citation2018). Financial performance measures how effectively a company can utilise resources from its main line of business and generate income. It is also used as a broad indicator of a company’s long-term financial stability (Kenton, Citation2022).

Financial performance is typically thought of as being short-term and solely based on the past. It is important to consider them when evaluating performance across four crucial dimensions: effectiveness, liquidity, profitability, and capital structure (Tien et al., Citation2020).

Jepkemboi (Citation2017), observed that organizational financial performance is determined by three specific areas of firms’ outcomes: firm’s financial performance as measured by profits, Return on asset (ROA) and Return on investment (ROI), product market performance and shareholder return, measured by total returns to shareholder and increased residual wealth.

H2:

Information technology has a positive effect on SME performance.

4.3. The link between information technology and financial accounting services

Information technology, or IT, is a key component of modern businesses. To keep their businesses operating continuously and without slowing down, businesses need IT services (Chege et al., Citation2020). Information technology refers to creating, preserving, and using networks, software, and computer systems to process and disseminate data. It alludes to elements of computer technology such as hardware, software, networking, the Internet, and the people who use them (Bouras et al., Citation2020). Information technology helps in various technical services such as accounting services. According to Jalil and Hwang (Citation2019), Information technology is essential to our business because it makes dealing with the unpredictable aspects of business easier. Technology aid in supplying a variety of instruments and software to support the performance of firms.

The entire process of accounting and filing returns has been eased by improvements in accounting and tax software. The majority of accounting software connects with the majority of corporate tax software, allowing for easy segmentation and classification of the data into the proper tax categories (Koong et al., Citation2019). The ability of businesses to create and use computerized systems to track and record financial transactions has had the most impact on accounting. The amount of time that accountants need to prepare and deliver financial information to management has decreased because of IT networks and computer systems. SMEs can easily and quickly produce customized reports using this solution for decision-making (Moll & Yigitbasioglu, Citation2019).

H3:

Information technology can moderate the relationship between Accounting services and Financial performance

4.4. Theoretical/Conceptual framework

According to the agency theory, there are agency conflicts when control and ownership are divided in businesses (Bebchuk & Fried, Citation2003). Prior research has concentrated on the importance of these conflicts in large publicly traded organizations, but very few studies have shown how important agency conflicts are in small and medium-sized businesses (Songini & Gnan, Citation2015). The forms of agency conflicts that frequently occur in SMEs are discussed in this research, along with mitigation strategies.

The agency model is one of the earliest theories in management and economics literature (Mitnick, Citation2019). The agency theory states that a principal must appoint an agent to act on his/her behalf (Jensen & Meckling, Citation1976).

The agency theory is based on a model that forecasts how management accounting services will react to financial information to safeguard financial performance (Gyamera et al., Citation2023).

The issues that the agency theory attempts to address include a lack of trust on the part of both the principal and the agents, opportunism displayed by agents who prioritize their interests over those of the principals, a lack of agent loyalty, the possibility of agents making poor decisions, and agents acting against the interests of the principals. These issues are resolved by the agency theory by improving information flow and coordinating priorities.

The owner(s) should ensure that the managers and staff implement good policies such as financial accounting services and information technology in the business among others. This will bring about an increase in the financial performance of the firm.

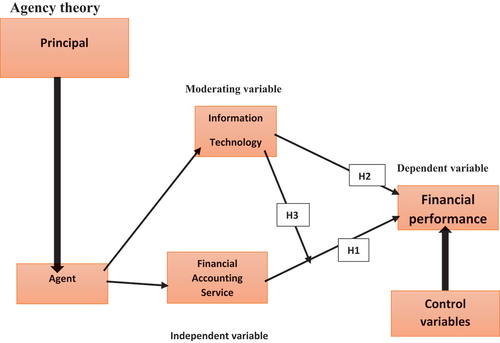

The theoretical/conceptual framework in Figure below asserts that the principal appoints an agent to steer the affairs of the firm. For the company to be able to perform well for the principal to achieve his objectives, the agent must implement financial accounting and information technology which will have a positive impact on the financial performance of the firm. When financial accounting services are moderated by information technology, it will bring about efficiency in financial accounting delivery which will ultimately result in financial performance.

Figure 1. Conceptual Framework.

The dependent variable in the conceptual framework is financial performance. The independent variables are financial accounting services and information technology. The agency theory links these variables. The linkages are that; the agent is supposed to employ good programs and policies on behalf of the principal (owner) to achieve the ultimate objective of the principal. In so doing the agent (manager) can employ accountants to provide the firm with accounting services. The agent can also employ the services of information technology in the firm to boost financial performance. Additionally, the agent can also use information technology in his employment of accounting services to ensure efficiency.

Financial accounting services are an important concept which when implemented will bring about financial performance. The reason is that financial accounting has developed principles which bring about accountability. Transactions are supposed to be recorded in the day books based on documents. These transactions are then recorded in accounts or ledgers and summarized in the trial balance. The financial statements are then prepared to ascertain the profit or loss of the firm. The conceptual framework below asserts that the implementation of financial accounting services enhances financial performance. Information technology has become the economic driver of every business. The conceptual framework asserts that if SMEs make use of information technology in their use of accounting services, it will lead to an increase in financial performance.

We controlled for the effect of years of experience of the owner (s) of the SME and the number of years that the firm has been in operation.

5. Research design

The study used a quantitative research design. Because the study’s goal is to conduct an empirical investigation of the effect of financial accounting services on the performance of SMEs using information technology as a moderating variable. As a result, the study used a quantitative technique and a survey method to gather the necessary data for the project. The population, sample size and data collection procedures are explained below. The questionnaire was administered to the managers of SMEs. In the questionnaire, the question was asked requiring SMEs to state whether or not they use accounting services in their firm. Those who stated that they were not using Accounting services were taken out of the analysis. The reason is that because they are not using the accounting services they will not be able to state the benefit derived from its use because they don’t use it. If they are to be included their answer will be vague and will not help the analysis.

Therefore, the analysis was based on the results of the SMEs who use Financial Accounting services.

5.1. Population, sampling and data Collection

The population of the study is the registered SMEs which was obtained from the Registrar Generals Department. A list received from the Registrar Generals Department contained 6,000 registered SMEs in Accra as of 2020. The 6,000 registered SMEs in Accra were used for calculating the sample size. The sampling technique used is a simple random and convenience sample. It was not everyone was willing to answer the questionnaire so those who were willing to answer were allowed to do so.

The Sample size was calculated based on Yamane’s 1967 formula with 95 per cent confidence level plus or minus 5 per cent confidence intervals using the formula n = N/1+N(e)2 where n= is the sample size N = is the population, and e= is the error margin. The sample size based on the estimated population of 6,000 registered SMEs in Accra was 375. Out of the 375 questionnaires administered, 370 were received; 50 were taken out because some were not employing financial accounting services and others didn’t fill the questionnaire correctly. Therefore, the actual sample size used for the analysis was 320 which was the number of respondents who accessed financial accounting services. simple random technique and the convenience sampling technique were used to select the SMEs, this was appropriate for the studies because it was not everyone was willing to answer the questionnaire and therefore only those who found it convenience to answer were allowed to do so.

A large sample size gives more reliable results than smaller samples in most research. According to inferential statistics by Comrey and Lee (Citation1992), a sample size of fewer than 50 respondents is a weaker sample, a sample size of 100 respondents is weak, a sample size of 200 respondents is suitable, 300 is good, 500 is very good, and 1000 is exceptional. Therefore, a sample size of three hundred and Twenty (320) is good.

Managers and in some cases, owners of the SMEs were given questionnaires to see if they used financial accounting services and how that affected their financial performance. A questionnaire was utilized since it may aid in collecting detailed information from respondents. There are four (4) elements: demographic factor, accounting services questionnaire, information technology questionnaire, and questionnaire on financial performance utilising a Likert scale of 1 to 5, with one denoting severe disagreement and 5 denoting strong agreement. The questionnaire was based on Oluwaremi (Citation2016).

5.2. Variables for the studies

5.2.1. Financial accounting services (independent variable)

Financial accounting services are the normal accounting services presented by accountants. Some of the services include: (1) Use of financial records, such as the sales daybook, purchases daybook, cash receipt book, check payments book, petty cash book, general journal, preparation of nominal ledger, debtors’ ledger and creditors’ ledger and a payroll system; (2) use of double entry bookkeeping; (3) preparation of the statement of financial position, profit and loss and other comprehensive income, statement of cash flow, statement of changes in equity and note to the accounts. (4) preparing projected cash flow statements regularly; (5) preparation of annual budget (6) preparation of bank statements (7) payroll services.

5.3. Financial performance (dependent variable)

The dependent variable for this study is financial performance (FP) which is an acceptable variable used in assessing the performance of the firm/business/SMEs etc. The study used Growth in sales, and return on assets to measure financial performance.

Onyiego (Citation2019) developed a questionnaire around accounting-based ratios to measure financial performance. These questionnaires have been adopted and modified for the current study. According to Earnhart and Lizal (Citation2007), in assessing the financial performance of a firm, one could use either market-based financial indicators or accounting. Hart and Ahuja (Citation1997) used the following accounting ratios: return on assets (ROA) and return on equity (ROE) return on sales (ROS) to measure financial performance. Accounting-based variables were used by Jaggi and Freedman (Citation1992) to measure financial performance. Horváthová (Citation2012) used Accounting based ratios which were: return on equity (ROE) and return on assets (ROA) to measure financial performance.

Russo and Fouts (Citation1997), and Moneva and Ortas (Citation2010) employed Return on assets (ROA) to measure financial performance measure.

5.4. Information technology as a moderating variable

System quality, information quality, and user happiness are how information technology is evaluated, according to Petter et al. (Citation2008), the system outputs are referred to as information quality. Relevance, understandability, accuracy, conciseness, completeness, understandability, timeliness, and usability are all requirements for these outputs. The level of support provided by the information systems division to system users is referred to as service quality. The elements of service quality are responsiveness, accuracy, reliability, technical competence, and empathy of the personnel staff. User satisfaction is measured by the level of satisfaction by the users of the information technology system in terms of the reports generated and the support services received by the staff of the IT department. In the current studies Information technology was measured by Perceived usefulness (IT1) and Perceived ease of use (IT2). These variables were placed on a 5-point Likert scale [(1) strongly disagree, (2) disagree, (3) disagree or disagree, (4) disagree, and (5) perfectly agree.

5.5. Control variable

Years of experience of the owner (s) and the number of years that the firm is a predictor variable and in some cases as a mediator or moderator variable (Dyke et al., Citation1992; Hamori & Koyuncu, Citation2015). In the current study, Years of experience of the owner (s) and the number of years that the firm has been in existence have been used as control variables in the path estimates of the relationship between financial accounting services, information technology and financial performance of SMEs in Ghana. Because the target population is SMEs, the determinant of years of experience was based on the number of years that the owner has operated his firm or similar firms. Additionally, the determinant of the number of years the firm was based on the number of years the firm has been in existence.

5.6. PLS-SEM model assessment

In undertaking PLS-SEM analysis, Chin (Citation1998) recommended a two-step approach which was adopted in this study. Firstly, there is the need to test for reliability and validity. One can move further to test the structural relationships between the latent and the observed variables in the research model. If the result of the tests is acceptable based on the threshold recommended by other researchers, then one can go ahead. If, after testing the measurement model, it is ascertained that the measurement items do not measure the latent variables reliably, then the suggested relationships between these variables cannot be verified (Hair, Citation2020)

5.7. Measurement model assessment

The researcher has to differentiate between reflective and formative modes in assessing the measurement model, and in the case of this research, all latent variables are modelled as reflective latent variables. Reflective latent variables are assessed using reliability, discriminant validity and convergent validity (Sarstedt et al., Citation2014).

5.8. Reliability

Internal consistency reliability is the first criterion to check in assessing the measurement model. Internal consistency reliability has traditionally been assessed with Cronbach’s α (Cronbach, Citation1951). Even though Cronbach’s α is a good measure for assessing reliability, it underestimates it because it assumes that all items in a latent variable load equally on the latent variable (Adamson & Prion, Citation2013). Cronbach’s α underestimates reliability because it is sensitive to the number of items in the latent variable (Kalkbrenner, Citation2021). The alternative to Cronbach’s α is composite reliability with acceptable values between 0.6 and 0.7 in exploratory research, while in advanced stages, values between 0.7 and 0.9 are preferred, and values less than 0.6 demonstrate a lack of reliability (Hair et al., 2014). The factor loadings of each indicator can be used to assess the reliability of each indicator variable with significant indicator loadings above 0.708 (Hair et al., 2014). If an item has an indicator loading of less than 0.4, then it should be deleted. Furthermore, items with indicator loadings between 0.4 and 0.7 should be considered for deletion if deletion will improve the composite reliability (Hair, Citation2020).

5.9. Discriminant validity

Discriminant validity measures how different a construct is from other components in the structural model empirically, which means that the constructs are different from each other and are not represented by other constructs (Henseler et al., Citation2015). Three methods have been proposed for assessing discriminant validity. The first method is where the latent construct indicators load higher in the model. The Second is the use of the Fornell-Larcker criterion, which states that the AVE of a latent construct must be greater than the square correlations between the construct and any other (Hair, Hult, Ringle, Sarstedt, Danks, Ray, Ray, et al., Citation2021). Some deficiencies were identified by Henseler et al. (Citation2015), in the Fornell-Larcker and proposed the Heterotrait-Monotrait ratio (HTMT) for assessing discriminant validity. Henseler et al. (Citation2015), recommended that discrimination between two factors, that is, HTMT, should be 0.85 or less than one.

5.10. Convergent validity

The degree to which a construct converges to explain the variance of its elements is known as convergent validity (Hair, Hult, Ringle, Sarstedt, Danks, Ray, Ray, et al., Citation2021). Convergent validity is the degree to which the construct converges to explain the variance of its indicators. The metric used for assessing a construct’s convergent validity is the average variance extracted (AVE) for all indicators on each construct. The AVE is defined as the total mean value of the squared loadings of the indicators connected to the construct (i.e., the sum of the squared loadings divided by the number of indicators) (Hair, Hult, Ringle, Sarstedt, Danks, Ray, Ray, et al., Citation2021). As a rule, AVE values for each construct must be greater than 0.5 (Hair, Hult, Ringle, Sarstedt, Danks, Ray, Ray, et al., Citation2021).

5.11. Structural model assessment

The structural model has to be assessed by considering the path coefficient, the coefficient of determination R2, predictive relevance Q2 and f2 effect sizes. Path coefficients are assessed based on their strength, significance and sign. In determining the significance of each path coefficient, the bootstrapping procedure was used with 5000 resamples (Matthews et al., Citation2018). A substantial path coefficient means that the path in question is significant or that the two variables it connects have a significant relationship. When the path coefficient is negative, there is an inverse relationship (Shmueli et al., Citation2019). The ability of the structural model to predict endogenous construct is another measure of its efficacy, and this ability was evaluated using the coefficient of determination R2 and Stone-Geisser Q2 (Etemad Sajadi & Ghachem, Citation2015). The squared correlation between the endogenous construct’s actual and expected values is known as R2 for endogenous variables. R2 values of 0.75, 0.5, and 0.25 are regarded as being respectively substantial, moderate, and weak (Henseler et al., Citation2015). The predictive relevance of the model is also tested with the Stone-Geiser Q2 values that are also greater than zero indicating predictive relevance (Trivellas et al., Citation2013).

5.12. Statistical software

IBM SPSS version 23 was used for descriptive analysis because it is user-friendly. In testing the research model, the researcher used SmartPLS version 3 for the structural equation modelling. The researcher obtained training on the use of SmartPLS which made it very easy to use. Additionally, SmartPLS software incorporates the ρA measure for reliability and the HTMT ratio for assessing discriminant validity (Masudin et al., Citation2021).

5.13. Ethical consideration

Before getting access to and collecting data, the respondents’ true consent was solicited, with each respondent indicating a concurring edge to that effect. Furthermore, data was handled in a very secure manner to protect the respondents’ identity, using codes that were only known by the researchers, ensuring that responses could not be traced back to any individual.

5.14. Non-response and common method bias

To avoid common method bias, Cronbach’s alpha was computed for each construct. All the values met the critical threshold of 0.7 indicating items’ reliability (Eisinga et al., Citation2013), ranging from 0.690 to 0.911 (Table presents further information) to ensure the constructs’ internal consistency, as proposed by Peters (Citation2014). PLS-SEM was used to estimate the structural model with complex relationships, such as those with several independent and dependent variables and multiple independent—dependent interactions, as in this example (Hair et al., Citation2019). The model of the study included moderating factors, necessitating moderation testing. In this case, SMART PLS-SEM is more suited because it can examine models incorporating moderators. Because the goal of the study was to predict the key target construct which in this case was financial accounting services, and how this construct could have an effect on financial performance PLS-SEM was used.

Table 1. Demographics of Respondents

6. Empirical results and discussion

The current study used the PLS-SEM to analyse the data (Henseler et al., Citation2009). PLS-SEM has a lot of benefits. One of the PLS-SEM benefits is that the sample size requirements when using PLS for complex models are likely much smaller (Chin & Newsted, Citation1999). The researchers used 320 valid responses in Accra-Ghana to carry out the analysis: 48.4% represented Male whiles 51.6% represented females (see Table ). C. Fornell and Bookstein (Citation1982), have shown that PLS often provides component-based loadings and structural paths without requiring distributional assumptions.

Table 2. Loadings of reliability and validity results

PLS-SEM has statistical power; researchers benefit from the method’s high degree of statistical control (Hair et al., Citation2019). PLS-SEM has better statistical power, which implies it is more likely to find significant correlations when they are present in the population. (Sarstedt et al., Citation2018).

The analysis in the current studies is based on a two-step technique for reporting PLS-SEM results (Henseler et al., Citation2009). We first looked at the measurement model to analyse the instrument’s reliability and validity. The structural model based on the hypotheses suggested in this study was then examined.

6.1. Measurement model

The similarity of results obtained by independent but comparable measures of the same item or construct, or a gauge of consistency, is referred to as reliability (Churchill & Iacobucci, Citation2010).

Composite reliability (CR) and Cronbach’s alpha values were the critical reliability metrics. There were two types of validity tests: convergent and discriminant. Item or factor loadings greater than 0.5 on their respective constructs are used to determine convergent validity (Chinomona, Citation2013). The Average Variance Extracted (AVE) values and the Fornell-Lacker Criterion were used to assess validity. These verify that there were no significant factors related to one another and that the variables were independent and valid in predicting the result variable (Chin, Citation1998).

As stated earlier, the reliability of the three research constructs measurements was principally assessed using composite reliability and Cronbach’s alpha values. The Cronbach’s alpha (CA) values ranged between 0.631 to 0.790, while the Composite Reliability (CR) values ranged from 0.66 to 0.849 (see Table ). The reliability measures of CR and Cronbach’s alpha for Financial Accounting services, Financial performance and information Technology were above the recommended threshold value of 0.6 to 0.7, thereby confirming the reliability of these three research construct measures (Nunnally & Bernstein, Citation1994).

As previously stated, validity was conducted using The Average Variance Extracted (AVE) to measure the convergent validity, whiles the Fornell-Lacker Criterion was used to measure discriminant validity. Concurrent validity is acceptable because some of the AVE was over 0.5. Factor loadings determined the reliability and validity of the results for each construct, a lot of loadings were more than 0.5, as recommended by (Anderson & Gerbing, Citation1988; Hove et al., Citation2014). In Table below, Given the preceding, it can be inferred that the majority of the items used to assess the three research variables in this study accurately measured more than half of the variables of financial accounting services, information technology, and financial performance of SMEs in Ghana. AVE is acceptable because, in this research, AVE ranged from 0.486 to 0.560, as shown in Table . Fornell-Lacker Criterion assessed discriminant validity. Table shows that the square root of AVE was more significant than the inter-construct correlation. The researcher also measured discriminant validity with Heterotrait-Monotrait Ratio (HTMT), as shown in the table below,

Table 3. Heterotrait-monotrait Ratio (Htmt)

Table 4. Discriminant validity using Fornell—Larcker Criterion

6.2. Structure model

The structural model is discussed in this section. The structural model depicts the research framework’s hypothesised routes. R2 and notable routes are used to evaluate a structural model.

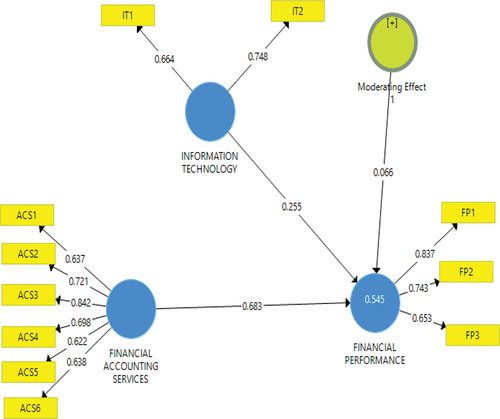

The strength of each structural path, as measured by the R2 value, is the coefficient of determination for the Endogenous variable. The R2 value should be greater than or equal to 0.1 (Falk & Miller, Citation1992). The results in Table show that the R2 is more than 0.1. That is, the R2 for the current model is 0.545. Therefore, the predictive capability of the model is established.

Table 5. Path coefficients and their significance

Furthermore, Q2 establishes the endogenous construct’s predictive relevance. Q2 for the study is 0.275, more significant than zero (0), indicating that the model has predictive relevance. The findings suggest relevance in the constructs’ prediction (see Table ).

Table 6. Control Variables

Further assessment of the hypothesis was tested to ascertain the significance of the relationship. H1 evaluates whether ACS (Financial Accounting Services) has a significant effect on FP (Financial Performance). The result revealed that ACS has a significant impact on FP (See Figure ).

(β = 0.032, t = 21.394, p ˂ 0.000). Hence H1 was supported.

H2 evaluates whether IT (Information Technology) has a significant effect on FP (Financial Performance). The results revealed that IT has a positive significant effect on FP.

(β = 0.044, t = 5.826, p ˂ 0.000). Hence H2 was supported.

6.3. Moderation test results

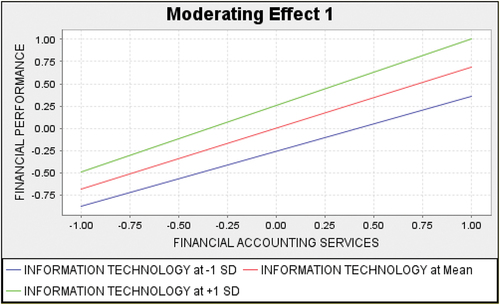

H3: Information technology can significantly moderate the relationship between Accounting services and Financial performance such that an increase in IT (information technology) should lead to an increase in financial performance. Moderation analysis was performed to evaluate the moderating role of IT. The results revealed a significant moderating role of IT in the relationship between ACS and FP. (β = 0.033, t = 2.032, p ˂ 0.043).

The results of the hypothesis confirm with the graph that when IT increases, as shown by the green line in the chart (see Figure ), the effect on FP also increases.

Figure 3. Structural Model Results from PLS.

We controlled for the effect of years of experience of the owner(s) and years of existence of the SME in this study. In the case of years of experience of the owner. We asked the respondents to indicate within a year group to know the number of years of experience they have in the business. The results in Table show that the number of years of experience that the owner of the firm does not affect the dependent variable (Financial performance) (t = 0.76, p = 0.46).

Secondly, the respondents were asked questions about the number of years that their business has been in operation. After carrying out the analysis as shown in Table the results indicate that the number of years that the SME has been in existence did not affect the dependent variable (financial performance) (t = 0.90, p = 0.37).

We considered aquatic effect on the dependent variables. There is a linear relationship between financial accounting service and financial performance. The aquatic results does not dispute this findings. The p value is not significant: (t = 1.749, p = 0.08). The model predict a linear relationship between information technology and financial performance. The aquatic results calculated as demonstrated in Table does not dispute that because the p value is not significant (t = 0.064, p = 0.09).

Table 7. Quadratic effect

7. Summary and conclusion

7.1. Findings of the research

The purpose of this study was to consider the effect of financial accounting services on the financial performance of SMEs in Ghana. H1 indicated a positive impact on the financial performance of SMEs. These positions were supported by the findings of: (Cahyaningtyas & Ningtyas, Citation2020; Karagiorgos et al., Citation2020; Siyanbola et al., Citation2019); that is, an increase in the use of accounting services will lead to a rise in the financial performance of SMEs. This means that SMEs should employ financial accounting services in their operations to improve their financial performance. Through the ministry of Trade and Industry, the government can offer a helping hand by engaging accounting firms to provide accounting services to SMEs. Particularly because the cost is an obstacle to accessing accounting services by SMEs. H2 also indicate a positive and significant relationship between Information Technology and the financial performance of SMEs. These positions were supported by the findings of (Husin & Ibrahim, Citation2014). The relationship indicates that SMEs can use information technology in various operations including the application of financial accounting and this can lead to the financial performance of their firms. H3 assessed whether Information Technology could significantly moderate the use of financial accounting services and financial performance. The results indicated a positive significant moderating effect between financial accounting services and financial performance. In addition, SMEs using financial accounting services may do so through information technology. Some SMEs utilising some form of financial accounting services may be using it manually and therefore may not enjoy the full benefit. It will be more appropriate to strengthen accounting services using information technology.

7.2. Implications of the studies

7.2.1. Theoretical implication

Our appreciation of the relationship between financial Accounting services and SME financial performance is further developed through the use of the Agency theory. Establishing this relationship strengthens the agency theory in the sense that, the theory demand that stakeholders will develop acceptable programs which will help drive the business forward.

Principals delegate decisions-making authority to agents. Because many decisions that affect the principal financially are made by the agent, a conflict of interest can arise. This is called an agency problem. The problems that the agency theory seeks to cure are lack of trust on the part of the principal, lack of trust on the part of agents, demonstration of opportunism by seeking self-interest instead of the principals’ interest, an agent having difficulty being loyal, the risk of the agent making poor decisions, agents taking decisions which are contrary to the principals’s best interest. The agency theory solves these problems by aligning priorities and improving the flow of information.

SMEs are usually owned and controlled by the same person. As the firm grows, it becomes difficult for the owner to manage it alone. So there is the need for him/her to hire managers and other employees to help manage the firm. This situation brings a lot of problems which have been outlined above. SMEs can apply the agency theory to solve these problems which arise among the owner(s) of the business, the managers and other employees.

It has been demonstrated in the study that the TAM model variables of perceived ease of use and perceived usefulness were upheld in the research. It is important to mention that actual use was also achieved in the studies.

To this end, the managers of firms can develop and implement accounting principles using the agency theory to help increase their financial performance. Secondly, the understanding will help academia to better develop an accounting package which will have more impactful programs that will be useful to business processes because the linkages between financial accounting services and SME performance will be more appreciated and will help our understanding. The importance of technology has also been brought to the limelight in this study and SMEs can adapt it to help them increase their financial performance.

7.3. The practical implication

The significance of the study to practice and how it adds to existing knowledge can be looked at in two ways. First, the evidence from the study will be helpful to Accountancy practitioners to help them appreciate the impact or the influence of accounting services on SMEs. Moreover, it will direct them to understand and know how they can provide targeted and relevance services that will increase SME financial performance. Second, financial accounting services have often been used by companies to help them achieve their objectives. This study will help SMEs to understand how relevant it is to access financial accounting services to increase their financial performance.

7.4. The Policy significance

The findings of this study will enable the Ministry responsible for Trade and Industry, in collaboration with the National Board for Small Scale Industry in Ghana, to organize frequent training programs for SMEs to know and appreciate the importance of accessing financial accounting services. The Accountancy Body in Ghana, for example, the Institute of Chartered Accountants (ICAG) in collaboration with the Trade ministry can focus on accountancy programs and offer training for SMEs. Additionally, the Universities will be able to tailor their accounting curricula to focus on the financial accounting services for SMEs and organise programs that will enable their accounting students to gain the accounting knowledge required to assist SMEs to increase their financial performance.

7.5. Limitations and future research

The findings of this research should be understood with some deliberations in light of the following shortcomings. First, this study incorporated the agency theory which can be used to solve many different issues. The study has covered these issues as well as potential solutions. The study examined accounting services that, when used to address agency issues, can be helpful. Many suggestions for resolving principal-agent issues have been presented. The adoption of bonus programs, as well as other social programs like health care, salary increases, and many more ideas, are among the suggested solutions. Future research might examine the impact of these suggested agency problem solutions and how they affect SMEs’ financial performance.

Secondly, some SMEs use software for their operations and that is why they were able to respond to the effect of information technology on financial performance. However, the study didn’t investigate the kind of software being used by the SMEs. The type of software used by the respondents was not captured in this study. It is therefore recommended that future research will consider finding out from the SMEs as to the kind of accounting software they use and how efficiently this software contributes to the efficient running of their business.

Thirdly, even though the study reached out to SMEs in the trading sector, services sector, manufacturing and agriculture sector. These sectorial effects on financial performance were not analysed and it is recommended that future studies will consider a sectorial analysis as mentioned.

7.6. Conclusion

SMEs constitute the backbone of many economies, including Ghana. However, many of these SMEs performed poorly within a few years of their establishment. A variety of reasons could be blamed for these issues. Lack of access to accounting services is one of the possible factors leading to SMEs’ demise. Financial accounting services have a good and considerable impact on the financial performance of SMEs, according to the current study. As a result, the government must step in to gain access to financial accounting services. In every area of progress, information technology has been a driving force. According to the findings of the current study, it has a favourable and significant effect on the financial performance of SMEs when it moderates the relationship between financial accounting and financial performance. As a result, it is advised that SMEs use technology in their operations.

Therefore, the researcher recommends that SMEs should access accounting services to improve their financial performance. In addition to that it is also recommended that the government should get involved to help the SMEs to be able to access accounting services since some of them may not have the financial ability to access accounting services.

References

- Abor, J., & Hinson, R. (2004). Financing Small and Medium Scale Exporters in Ghana’s non-Traditional export Sector. Working paper, University of Ghana Business School,

- Adamson, K. A., & Prion, S. (2013). Reliability: Measuring internal consistency using Cronbach’s α. Clinical Simulation in Nursing, 9(5), 179–26. https://doi.org/10.1016/j.ecns.2012.12.001

- Adjabeng, F. N., & Osei, F. (2022). The development of small medium enterprises and their impact on the Ghanaian Economy. Open Journal of Business and Management, 10(6), 2939–2958. https://doi.org/10.4236/ojbm.2022.106145

- Afriyie, S., Du, J., & Ibn Musah, A. A. (2019). Innovation and marketing performance of SME in an emerging economy: The moderating effect of transformational leadership. Journal of Global Entrepreneurship Research, 9(1), 1–25. https://doi.org/10.1186/s40497-019-0165-3

- Agbemava, E., Godwin Ahiase, G., Sedzro, E., Adade, T. C., Bediako, A. K., Nyarko, I. K., & Kudo, M. B. (2016). Assessing the effects of sound financial statement preparation on the growth of small and medium-scale enterprises. European Journal of Business and Management, 8(7).

- Agyapong, D. (2010). Micro, small and medium enterprises’ activities, income level and poverty reduction in Ghana-A synthesis of related literature. International Journal of Business and Management, 5(12), 196. https://doi.org/10.5539/ijbm.v5n12p196

- Akinwale, Y. O., Adepoju, A. O., & Olomu, M. O. (2017). “The impact of technological innovation on SME’s profitability in Nigeria. International Journal of Research, Innovation and Commercialisation”, 1(1), 74–92. https://doi.org/10.1504/IJRIC.2017.082299

- Aladejebi, O., & Oladimeji, J. A. (2019). The impact of record-keeping on the performance of selected small and medium enterprises in Lagos metropolis. Journal of Small Business and Entrepreneurship Development, 7(1), 28–40. https://doi.org/10.15640/jsbed.v7n1a3

- Ali, C. B. (2020). Agency theory and fraud. In Corporate Fraud Exposed (pp. 149–167). Emerald Publishing Limited.

- Ameyaw, B., & Modzi, S. K. (2016). Government policies, internationalization and ICT usage towards SME’s growth: An empirical review of Ghana. British Journal of Economics, Management & Trade, 12(3), 1–11. https://doi.org/10.9734/BJEMT/2016/23552

- Amin, A., Ur Rehman, R., Ali, R., & Ntim, C. G. (2022). Does gender diversity on the board reduce agency costs? Evidence from Pakistan. Gender in Management: An International Journal, 37(2), 164–181. https://doi.org/10.1108/GM-10-2020-0303

- Amoako, G. K. (2013). Accounting practices of SMEs: A case study of Kumasi Metropolis in Ghana. International Journal of Business and Management, 8(24), 73. https://doi.org/10.5539/ijbm.v8n24p73

- Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modelling in practice: A review and recommended two-step approach. Psychological Bulletin, 103(3), 411–423. https://doi.org/10.1037/0033-2909.103.3.411

- Ansong, A. (2017). Corporate social responsibility and firm performance of Ghanaian SMEs: The role of stakeholder engagement. Cogent Business & Management, 4(1), 1333704. https://doi.org/10.1080/23311975.2017.1333704

- Aryeetey, E., Baah-Nuakoh, A., Duggleby, T., Hettige, H., & Steel, W. F. (1996). The Formal Financial Sector in Ghana after the Reforms. Overseas Development Institute.

- Baah-Nuakoh, A., Turkson, F. E., Baah-Nuakoh, K., & Baah-Boateng, W. (2002). Multi.

- Bebchuk, L. A., & Fried, J. M. (2003). Executive compensation as an agency problem. Journal of Economic Perspectives, 17(3), 71–92. https://doi.org/10.1257/089533003769204362

- Bosse, D. A., & Phillips, R. A. (2016). Agency theory and bounded self-interest. Academy of Management Review, 41(2), 276–297. https://doi.org/10.5465/amr.2013.0420

- Bouras, M. A., Farha, F., & Ning, H. (2020). Convergence of computing, communication, and caching in internet of things. Intelligent and Converged Networks, 1(1), 18–36. https://doi.org/10.23919/ICN.2020.0001

- Cahyaningtyas, F., & Ningtyas, M. N. (2020). The use of outsourced accounting services and its impact on SMEs performance. JABE (Journal of Accounting and Business Education), 4(2), 79–97. https://doi.org/10.26675/jabe.v4i2.8641

- Chege, S. M., & Wang, D. (2020). Information technology innovation and its impact on job creation by SMEs in developing countries: An analysis of the literature review. Technology Analysis & Strategic Management, 32(3), 256–271. https://doi.org/10.1080/09537325.2019.1651263

- Chege, S. M., Wang, D., & Suntu, S. L. (2020). Impact of information technology innovation on firm performance in Kenya. Information Technology for Development, 26(2), 316–345. https://doi.org/10.1080/02681102.2019.1573717

- Chin, W. W. (1998). The partial least squares approach to structural equation modeling. Modern Methods for Business Research, 295(2), 295–336.

- Chin, W. W., & Newsted, p. r. (1999). structural Equation Modelling: Analysis with small samples using partial least squares. In R. H. Hoyle (Ed.), Statistical Strategies for Small Sample Research (pp. 307–341). Sage.

- Chinomona, R. (2013). Business owner’s expertise, employee skills training and business performance: A small business perspective. Journal of Applied Business Research (JABR), 29(6), 1883–1896. https://doi.org/10.19030/jabr.v29i6.8224

- Churchill, D. A., & Iacobucci, D. (2010). “market research: Methodological foundations”. South-Western Cengage Learning.

- Comrey, A. L., & Lee, H. B. (1992). A first course in factor analysis. Lawrence Erlbaum.

- Cronbach, L. J. (1951). Coefficient alpha and the internal structure of tests. psychometrika, 16(3), 297–334. https://doi.org/10.1007/BF02310555

- Davis, F. D. (1987). User acceptance of information systems: The technology acceptance model (TAM).

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319–340. https://doi.org/10.2307/249008

- Donaldson, L., & Davis, J. H. (1991). Stewardship theory or agency theory: CEO governance and shareholder returns. Australian Journal of Management, 16(1), 49–64. https://doi.org/10.1177/031289629101600103

- Ducey, A. J., & Coovert, M. D. (2016). Predicting tablet computer use: An extended Technology acceptance model for physicians. Health Policy and Technology, 5(3), 268–284. https://doi.org/10.1016/j.hlpt.2016.03.010

- Dyke, L. S., Fischer, E. M., & Reuber, A. R. (1992). An inter-industry examination of the impact of owner experience on firm performance. Journal of Small Business Management, 30(4), 72.

- Earnhart, D., & Lizal, L. (2007). The effect of corporate environmental performance on financial outcomes – Profits, revenues, and costs: Evidence from the Czech transition economy. DRUID Working Paper No. 10-15.

- Eisenhardt, K. M. (1989). Agency theory: An assessment and review. Academy of Management Review, 14(1), 57–74. https://doi.org/10.2307/258191

- Eisinga, R., Grotenhuis, M. T., & Pelzer, B. (2013). The reliability of a two-item scale: Pearson, cronbach, or spearman-brown”? International Journal of Public Health, 58(4), 637–642. https://doi.org/10.1007/s00038-012-0416-3

- Elmagrhi, M. H., Ntim, C. G., Elamer, A. A., & Zhang, Q. (2019). A study of environmental policies and regulations, governance structures, and environmental performance: The role of female directors. Business Strategy and the Environment, 28(1), 206–220. https://doi.org/10.1002/bse.2250