?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Regulators and managers in the banking sector prioritize the banking system’s stability and safety to limit risks, shocks, and potential losses. This study reveals why a bank is more or less stable via bank capital, liquidity creation, and asset diversification. We form a structural model in which bank capital affects stability through liquidity creation, and asset diversification moderates the relationship between liquidity and stability of banks. We employ a moderated mediation model and the Partial Least Squares Structural Equation Modeling (PLS-SEM) with panel data on 27 commercial banks publicly listed in Vietnam from 2014 to 2021. Surprisingly, the empirical results show that raising bank capital reduces liquidity creation while lowering liquidity creation increases bank stability. Thus bank capital has a positive impact on stability via the mediating role of liquidity creation. Moreover, the relationship between liquidity creation and bank stability is moderated by “asset diversification”. Higher asset diversification mitigates the detrimental impact of liquidity creation on bank stability and vice versa. Finally, this study recommends using bank capital, liquidity creation, and asset diversification to bolster bank stability.

Public Interest Statement

Bank stability has received significant attention from academic researchers, practitioners, and regulators. The banking sector in emerging economies such as Vietnam is improving steadily, but stability is required. Bank stability may help the economy or an organization absorb unfavorable shocks primarily through self-adjusting mechanisms. Prior studies focused on understanding the partial links between bank capital and liquidity creation, bank capital and bank stability, liquidity creation and banking stability. However, we suggest that the relationship among these variables is structural. In particular, liquidity creation serves as a mediator in transferring the effect of bank capital on bank stability.

Furthermore, our study suggests that asset diversification may moderate the effect of liquidity creation on bank stability. The study employs moderated mediator model to depict the relationship among the variables. The study makes a contribution to the literature by discovering and explaining the structural relationship between these variables in the Vietnamese banking context.

1. Introduction

Bank stability has received significant attention from academic researchers, practitioners, and regulators. Because of the immediate exogenous shock caused by the COVID-19 pandemic, banks must be prepared for extremely difficult and diverse future challenges (Elnahass et al., Citation2021). As a result, bank stability is becoming highly emphasized, and it is critical to thoroughly investigate the effects of its antecedents. One topic of active debate in economics is why a bank is stable. Some previous studies, such as Coval and Thakor (Citation2005), hold that bank capital is a risk-absorbing buffer. Moreover, bank capital helps banks absorb losses incurred during a recession (Steffen, Citation2014). In addition, by acting as a buffer against financial shocks, it decreases chain defaults (Anginer et al., Citation2018). Hence, it enhances bank stability.

Liquidity creation is also considered an antecedent of stability. We also discover that liquidity creation can mediate the link between bank capital and stability. Bank capital affects not only stability but also liquidity creation. Berger and Bouwman (Citation2009) summarize three theories that explain the connection between the two variables: (1) the fragility of capital structure, (2) the crowding-out hypothesis, and (3) the risk absorption hypothesis. They show a positive relationship between the two variables. However, recent empirical research, such as Casu et al. (Citation2019); Chaabouni et al. (Citation2018); Evans and Haq (Citation2022); Fungáčová et al. (Citation2017); Le (Citation2018); Toh (Citation2019), reveal a heterogeneous influence of bank capital on liquidity creation in different contexts.

Other researchers find a direct relationship between liquidity creation and stability. They reason that, other than transferring risk, creating liquidity is a critical role played by commercial banks. Specifically, banks borrow short-term funds to finance long-term assets, which boosts profit margins but exposes banks to credit and liquidity risk (Berger & Bouwman, Citation2009). Fungacova et al. (Citation2015), based on the high liquidity creation hypothesis, state that when a bank’s liquidity creation exceeds the optimal point, the probability of failure increases. Nevertheless, the findings on the influence of liquidity creation on bank stability vary across empirical research. According to Davydov et al. (Citation2021); Gupta and Kashiramka (Citation2020); Zheng et al. (Citation2019), liquidity creation has a favorable impact on bank stability. However, according to the findings of Fungacova et al. (Citation2021), the higher the liquidity creation, the greater the likelihood of bank failure, or, in other words, the lower the bank stability. Berger et al. (Citation2019); Berger and Bouwman (Citation2017); Fungacova et al. (Citation2015) all reach different results, suggesting that a third variable can moderate the link between the two variables. We discover that asset diversification might be this third variable.

Numerous previous studies have investigated the relationship between bank diversification (which comes in many types: income diversification, loan portfolio diversification, and asset diversification) and bank stability (see Kim et al. (Citation2020); Nisar et al. (Citation2018)). Although asset diversification has received less attention, M. F. Hsieh et al. (Citation2013) indicate that this variable positively affects stability. In this study, we show that liquidity creation harms a bank’s stability if it engages in less diversification. In other words, asset diversification and liquidity creation may have an interactive effect on bank stability. For these reasons, asset diversification is selected as a variable to examine not just its link to bank stability but also its role as a moderating variable in the relationship between liquidity creation and bank stability.

Prior studies focused on understanding the partial links between bank capital and liquidity creation, bank capital and bank stability, and liquidity creation and banking stability. However, we suggest that the relationship among these variables is structural. In particular, liquidity creation serves as a mediator in transferring the effect of bank capital on bank stability. Furthermore, the moderating effect of asset diversification on the relationship between liquidity creation and bank stability has never been investigated. Our study suggests that the variable should be incorporated into the structural model. Hence, we use a moderated mediator model to depict the relationship among the variables. Specifically, the structural influence of bank capital on bank stability is examined via the mediating effects of liquidity creation and moderating effect of asset diversification. The Partial Least Squares Structural Equation Modeling (PLS-SEM) is deemed an appropriate method for estimating the moderated mediator model.

The banking sector in emerging economies such as Vietnam is improving steadily, but stability is required. As a result, research on the influence of bank capital, liquidity creation, and asset diversification on bank stability assists bank managers in making decisions about whether to enhance equity, liquidity creation, and asset diversification to preserve bank stability. We make a contribution to the literature by discovering and explaining the empirical relationship between these variables in the banking context of Vietnam.

2. Literature review

2.1. Bank capital

Bank capital is a risk-absorbing resource (Berger & Bouwman, Citation2009). This means that, throughout the course of their operations, banks frequently develop risky assets, and in order to ensure operational safety, bank capital offsets these risky assets after they become unrecoverable. The more capital a bank has, the more risk it can absorb and the more stable it is. In addition to being one of many significant aspects that determine a bank’s profitability, bank capital also plays a significant role in boosting public trust and confidence in the stability of the bank (Abbas et al., Citation2019). Regulations on bank capital are crucial for guaranteeing sound bank governance and promoting risk-taking in bank business operations (Santos, Citation2001). The State Bank of Vietnam now bases its laws on Basel II and Basel III of the Basel Committee on Banking Supervision, which is applicable to all commercial banks and foreign bank branches operating in Vietnam.

This study explores bank capital based on the views of Berger and Bouwman (Citation2009). Tier 1 capital is considered to be reflective of bank capital because it is core capital, highest quality capital and has a better risk absorption capability than Tier 2 capital (Evans & Haq, Citation2022). Basel requirements are followed in calculating Tier 1 capital.

2.2. Liquidity Creation

Liquidity creation is a well-known essential function of banks (Dang, Citation2020), the primary rationale for the existence of banks (Berger & Sedunov, Citation2017), one of the primary tasks of banks in any economy (Allen et al., Citation2014), a crucial intermediary role that banks perform for the economy (Evans & Haq, Citation2022). Classically, banks create liquidity by converting relatively liquid liabilities, such as deposits, into relatively illiquid assets, such as loans (M. -F. Hsieh et al., Citation2022). Bank liquidity creation is crucial for the financial system and the economy (Acharya & Naqvi, Citation2012; Berger & Sedunov, Citation2017). Liquidity creation increases tangible investment, but not intangible investment, across countries and particularly for industries with greater debt financing needs (Beck et al., Citation2022). The ability of a bank to convert maturities is reflected in its liquidity creation (Gupta & Kashiramka, Citation2020).

In the first approach, the act of creating liquidity for deposits and liquidity for credits is defined as liquidity creation (Diamond, Citation2007), as shown by Diamond and Dybvig (Citation1983); Diamond and Rajan (Citation2000); Holmstrom and Tirole (Citation1997); Kashyap et al. (Citation2002). In the second approach, represented by Berger and Bouwman (Citation2009); Deep and Schaefer (Citation2004); Ramakrishnan and Thakor (Citation1984), liquidity creation or liquidity transformation refers to instances in which liquid capital is used to finance illiquid assets (Ramakrishnan & Thakor, Citation1984). The liquidity transformation gap is the difference between liquid liabilities and liquid assets, as described by Deep and Schaefer (Citation2004). If this difference is positive, the bank invests liquid liabilities in illiquid assets. Alternatively, the bank is creating liquidity creation. However, when a bank invests illiquid funds in highly liquid assets, liquidity is destroyed. Intuitively, liquidity is created when the liquid liabilities of a bank exceed its liquid assets.

Berger and Bouwman (Citation2009) split the bank’s assets and capital into liquid, semiliquid, and illiquid. Each of these groups is given a distinct weight. This calculation, as well as the second strategy for liquidity creation, is used in this research.

2.3. Bank Stability

Financial stability refers to the smooth operation of the major components of the financial system (Duisenberg, Citation2001). Schinasi (Citation2004) defines the financial stability of a financial institution at a lower level (individual institution level) as the ability to perform economic operations, regulate risks, and absorb risks. According to the Bank (Citation2016), financial stability helps the economy or an organization absorb unfavorable shocks primarily through self-adjusting mechanisms, which help avoid negative consequences.

According to Ozili (Citation2018), many people describe the financial stability of banks as the absence of banking crises. According to Brunnermeier et al. (Citation2009), banking stability is the lack of banking crises, which is accomplished through the stability of all banks in the system. Segoviano and Goodhart (Citation2009) define financial stability as the stability of banks linked in one of two ways: (1) directly through the interbank deposit market and participation in syndicated loans or (2) indirectly through lending to general sectors and proprietary trades. In developed countries, bank stability is based mostly on capital adequacy, but in developing countries, structural weaknesses of banks are viewed as the primary factor in whether a bank is stable or not (Caprio & Honohan, Citation1999).

2.4. The mediating role of liquidity creation on the relationship between bank capital and bank stability

2.4.1. Bank capital and bank stability

Much attention has been paid to the role that bank capital plays in minimizing the negative effects of risk on bank operations. Bank capital plays a positive role in extending asset possibilities for investment and enhancing the bank’s control over borrowers (Thakor, Citation2014), helping to maintain bank stability. The regulation of bank capital has long promoted the stability of financial systems (Evans & Haq, Citation2022).

Berger and Bouwman (Citation2009) believe bank capital is a risk-absorbing buffer. Bank capital assists banks in absorbing losses that arise during a recession (Steffen, Citation2014). Bank capital reduces chain defaults by acting as a cushion against financial shocks (Anginer et al., Citation2018). Unlike the other capital sources in a bank’s capital structure, equity serves as a buffer, liquidity, and agency cost (Allen et al., Citation2015; Diamond & Rajan, Citation2000). That is, banks frequently create risky assets in the course of their operations to profit. Bank capital is used to cover losses sustained when these risky assets become unrecoverable in the event of uncertainty. When banks have more capital, their level of risk absorption is greater, and so is the bank’s risk tolerance (Coval & Thakor, Citation2005). As a consequence, the bank’s stability is further enhanced.

The equity of a bank signifies its right to acquire assets. The value of the bank’s equity might rise if it chooses to invest in riskier assets. Banks with less capital are more likely to take risks to boost their capital’s value. Bank stability will suffer. As a result, many bank executives believe that expanding the bank’s capital will reduce the risk appetite of low-capital institutions. A well-capitalized banking system has longer-term financial stability advantages (Rubio & Yao, Citation2020). In the belief that more capital helps banks achieve better stability, Holmstrom and Tirole (Citation1997) argue that having higher capital generates more incentives for banks to regulate borrowers, increasing the quality of the borrower’s credit and lowering related risk. According to Coval and Thakor (Citation2005), increased capital translates into decreased risk exposure for banks. Sufficient bank capital encourages banks to screen borrowers more thoroughly, and shareholders may be certain that only respectable borrowers will be approved for loans (Thakor, Citation2014). As a result, having more capital makes the bank more disciplined and stable.

Kiemo et al. (Citation2022) argue in their empirical research that bank capital enhances bank stability through its influence on credit risk and lending operations. Bank capital acts as a buffer, allowing banks to absorb economic shocks and preventing them from spreading across the financial system (Anginer et al., Citation2018). Anginer and Demirgüç-Kunt (Citation2014) find similar results in their empirical study on the positive influence of bank capital on bank stability.

Based on our review of both theoretical and empirical aspects of the relationship between bank capital and bank stability, recognizing in particular the role of bank capital in absorbing risks and limiting the negative impact of risk on the bank’s existence, this study proposes the following research hypothesis on the impact of bank capital on bank stability:

Hypothesis 1: Bank capital has a positive impact on bank stability.

2.4.2. Bank capital and liquidity creation

Since the Basel Capital Accord of 1988 and the global financial crisis of 2008, the relationship between capital and liquidity creation has been the subject of debate and growing interest (M. -F. Hsieh et al., Citation2022). Berger and Bouwman (Citation2009) summarize three theories used to predict the direction of the influence of equity on liquidity creation: (1) fragility of capital structure, (2) the crowding-out hypothesis, and (3) risk absorption. The majority of subsequent empirical investigations are based on Berger and Bouwman’s conclusion that these three theories explain the correlation between bank capital and liquidity and use these theories to explain the effect of bank capital on liquidity creation.

The fragility of capital structure theory cannot be employed to explain the influence of bank capital on liquidity creation in this study because Diamond and Rajan (Citation2000) use it to describe the first approach to liquidity creation. Meanwhile, Berger and Bouwman (Citation2009) use this theory to explain the second method of liquidity creation (the influence of bank capital on the transition from highly liquid liabilities to assets with low liquidity).

Berger and Bouwman (Citation2009) use the crowding-out hypothesis based on the working paper of Gorton and Winton in 2001, which was published in 2017 (see Gorton and Winton (Citation2017)). In addition, Gorton and Winton note the predominance of bank capital over deposits within the context of this theory. The research indicates that depositing money in banks to earn interest is a risk-hedging strategy that does not generate large returns. Consequently, they have an incentive to convert from deposits to investments (from depositor to investor). The increased quantity of money invested (increased bank capital) has made banks less appealing to depositors, hence, reducing the amount of liquidity created. That is the impact of bank capital crowding out deposits. Thus, Gorton and Winton relate to the negative impact of bank capital on deposit-side liquidity creation only indirectly (according to the first approach).

This study concentrates on the third theory to explain the positive effect of bank capital on liquidity creation based on the analysis above. According to the theory of risk absorption, two variables should be positively correlated. This theory is intimately connected to the function of banks in risk transformation. When a bank accepts deposits (from individuals who are less risk-averse) and makes loans (to those who are more risk-averse), it becomes a risk-absorbing institution and is rewarded for the gap between lending rates (high interest rates) and deposit rates (low interest rates). The riskier a bank is, the more likely it is that it will convert from highly liquid deposits (e.g., short-term deposits) with extremely low risk to very liquid assets (e.g., long-term loans) with high risk. When a risk occurs, the bank must spend its own money (equity) to manage it. If the capital is tiny, the bank does not dare to increase the liquidity or risk gap because a small amount of capital cannot help the bank cope with the consequences of high risk. When more capital is raised (raising bank capital), the capacity to manage risks also increases. In other words, the bank’s risk absorption capacity increases as its equity increases (Bhattacharya & Thakor, Citation1993; Coval & Thakor, Citation2005; Repullo, Citation2004; Von Thadden, Citation2004). And the higher the amount of risk absorption, the more liquidity banks create for the economy (Berger & Bouwman, Citation2009).

Prior empirical research by Casu et al. (Citation2019); Chaabouni et al. (Citation2018); Evans and Haq (Citation2022); Le (Citation2018); T. T. H. Nguyen et al. (Citation2022); Toh (Citation2019) on the effect of bank capital on liquidity creation yield conflicting results. Nonetheless, this study supports Berger and Bouwman (Citation2009)’s argument and hypothesizes as follows:

Hypothesis 2: Bank capital has a positive impact on liquidity creation.

2.4.3. Liquidity creation and bank stability

Banks that boost liquidity creation are wealthier (Berger & Bouwman, Citation2009; Duan & Niu, Citation2020) because illiquid assets yield higher returns than liquid assets. However, the influence of liquidity creation on bank stability varies depending on the context.

The high liquidity creation hypothesis states that when a bank’s liquidity creation level surpasses the optimal level, the likelihood of collapse increases (Fungacova et al., Citation2015). If the bank creates too much liquidity, its solvency will be very low, and it will be unable to meet the withdrawal demands of depositors. In other words, the bank’s financial fragility will grow. Banks are compelled to sell illiquid assets at low prices to avoid failure. As a result, when liquidity levels are excessively high, the bank’s stability and profitability suffer. The greater a bank’s liquidity creation, the greater its likelihood of failing (Fungacova et al., Citation2021). In the opposite case, the level of liquidity creation is low, which also has a negative impact on the bank’s stability. Banks that are heavily dependent on long-term finance (e.g., syndicated loans, bonds), rather than short-term deposits, may have poor liquidity creation. As a result, the danger of a bank run is reduced, but the risk of limiting the bank’s access to these funds is increased by the flexibility of these long-term grants. The probability of bank failure increases (Fungacova et al., Citation2015). Furthermore, banks’ ability to extend loans to borrowers is limited by a shortage of liquidity creation. As the bank’s income declines, so does its stability. Liquidity creation, according to Gupta and Kashiramka (Citation2020), is a double-edged sword for bank stability.

From an empirical perspective, the findings on the influence of liquidity creation on bank stability vary. Davydov et al. (Citation2021); Gupta and Kashiramka (Citation2020); Zheng et al. (Citation2019) reveal that liquidity creation has a positive influence on bank stability. Berger et al. (Citation2019); Berger and Bouwman (Citation2017); Fungacova et al. (Citation2015) obtain contradictory results.

Banks can create liquidity in two ways. The first way involves banks converting short-term liquid liabilities into long-term illiquid assets (Diamond & Dybvig, Citation1983). The main business capital of a bank is formed and used to offer credit to borrowers as a result of the acceptance of deposits from individuals and organizations in the economy. At the same time, the bank allows depositors to use payment services with convenient early withdrawal. Banks can also create liquidity by increasing off-balance-sheet lending obligations and guarantees (Kashyap et al., Citation2002). In this approach, the bank’s off-balance-sheet liquidity creation allows clients to manage their investment and reduce their exposure to financial risk (Berger et al., Citation2019). Liquidity creation is the primary function of a bank on both portions of the balance sheet, raising the bank’s market risks and operational risks. As a result, the bank’s stability may suffer. The following research hypothesis is proposed in the study:

Hypothesis 3: Liquidity creation has a negative impact on bank stability

2.4.4. The mediating role of Liquidity creation

In this section, we reason that Bank capital directly affects Bank stability. Besides, Bank capital also affects Liquidity creation. Finally, Liquidity creation has a direct impact on Bank stability. Thus, Liquidity creation can be considered one of the mediators explaining the relationship between Bank capital and Bank stability. For more details, Liquidity creation may transfer the negative effect of Bank capital to Bank stability.

2.5. The moderating role of asset diversification

Various aspects of bank diversification are investigated, including revenue, loan portfolio, and asset diversification. Many previous papers have been written on the relationship between bank diversification and bank stability, of which the most concern revenue diversification. Amidu and Wolfe (Citation2013); Kim et al. (Citation2020); M. Nguyen et al. (Citation2012); Nisar et al. (Citation2018) reveal empirical evidence of a positive effect of revenue diversification on stability. Shim (Citation2019) also argues that increasing the amount of loan diversification enhances bank stability. Although asset diversification has received less attention, the empirical investigation by M. F. Hsieh et al. (Citation2013) shows that this variable has a positive influence on stability.

For the following reasons, we study asset diversification in this paper.

First, revenue diversification, the most extensively studied type of diversification, derives in part from asset diversification. Revenue diversification is difficult to increase if banks cannot diversify their assets. If a bank does not diversify into certain asset classes, such as trading or investment securities, its income from them declines, leading to less revenue diversification.

Second, diversification of bank assets can be viewed as diversification of financial assets, and Markowitz (Citation1952)’s portfolio theory can be used directly to explain the positive correlation between this variable and stability. In general, when a bank diversifies into multiple assets, the volatility in the overall portfolio’s revenue decreases, and, as a result, bank stability increases. Because income is derived from assets, this argument should not apply to revenue diversification.

Third, loan portfolio diversification means that the bank diversifies its lending activities in various entities or industries. As a result, this type of diversification only analyzes loans to customers (a key asset of the firm) but does not include other types of assets.

For the reasons presented above, the study assumes that a bank’s asset diversification has a positive impact on stability, so we propose the following hypothesis:

Hypothesis 4: Bank stability improves when asset diversification is enhanced.

The empirical relationship between liquidity creation and bank stability varies, depending on the circumstances. In other words, a variable that moderates the relationship between liquidity creation and stability might exist, such as asset diversification. In particular, increasing bank diversification reduces the negative impact of liquidity creation on stability. In contrast, if banks diversify less (or focus more on lending), the magnitude of the negative impact of liquidity creation on stability rises. As a result, asset diversification and liquidity creation are likely to have an interaction effect on stability. The following hypothesis describes the interaction effect:

Hypothesis 5:

Bank asset diversification acts as a moderating variable in the relationship between liquidity creation and stability. The negative correlation between the two variables becomes stronger as asset diversification declines. Conversely, as asset diversification rises, the negative effect decreases.

2.6. Conceptual model

Based on the hypotheses proposed, Figure depicts the research model illustrating the relationship between the concepts:

Figure 1. Research model.

The model describes that Liquidity creation plays a mediating role while Asset diversification act as moderating role.

3. Methods and data

3.1. Measurements

3.1.1. Scale of liquidity creation

Liquidity creation (LC) is calculated using the procedure of Berger and Bouwman (Citation2009) in three steps: identifying the liquidity characteristics of assets and liabilities, assigning weights, and determining the level of liquidity creation (Table ). Beck et al. (Citation2022) argue that this liquidity creation measurement covers not just all bank activities on both sides of the balance sheet (asset side and liability side), but also off-balance sheet bank activities; therefore, this scale’s comprehensiveness is greater. Chen et al. (Citation2021); Fungacova et al. (Citation2021) also use this three-step procedure to measure the bank liquidity creation.

Table 1. Liquidity classification and weight

The bank’s liquidity creation is determined using the following formula:

in which

IlA = Illiquid assets

SemiA = Semiliquid assets

LiA = Liquid assets

LiL = Liquid liabilities

SemiL = Semiliquid liabilities

IlL = Illiquid liabilities.

3.1.2. Scale of bank capital

Based on studies of Berger and Bouwman (Citation2009); Horváth et al. (Citation2014); Isnurhadi et al. (Citation2021), bank capital (Cap) is calculated as follows:

3.1.3. Scale of bank stability

Bank stability (Stab) is evaluated using the Z-score and the components of the CAMEL index, an official measure of bank stability. The Z-score index is used to assess the convergence of the measurement model for Stab.

Following the experimental studies by Berger et al. (Citation2019); Gupta and Kashiramka (Citation2020); Vo et al. (Citation2021); Zheng et al. (Citation2019), bank stability is determined by:

in which ROA is return on assets; CAR is the capital adequacy ratio, and σ (ROA) is the standard deviation of ROA.

The CAMEL index (created by the Federal Deposit Insurance Corporation (FDIC) in 1979) comprises five key categories: capital adequacy, asset quality, management quality, earnings risk, and liquidity risk. These five variables are used in this study to assess five aspects of bank stability (Table ).

Table 2. Selected variables for assessing bank stability

In the past, multiple-criteria decision analysis (MCDA) or stochastic multicriteria acceptability analysis (SMAA-2) was often employed to evaluate stability based on the CAMEL index. This study employs a novel method for determining stability using the five factors described above. The result is that the synthesized measurement model of stability exists as a formative measurement model. The confirmatory tetrad analysis (CTA-PLS) proposed by Bollen and Ting (Citation2000) is used to statistically check whether this measurement model is reflective or formative. If the results indicate that a formative measurement model is appropriate, additional evaluations of the measurement model will be conducted, including those for convergent validity, the degree of multicollinearity between the variables, and the level of statistical significance of each regression weight, following Hair et al. (Citation2021).

3.1.4. Scale of asset diversification

The measurement of diversification is an important part of the theory of diversification and plays a crucial role in empirical research. The majority of empirical research on diversification uses measurement approaches such as the number of business sectors or of investment asset classes, the Herfindahl index, the concentric diversification index by Caves et al. (Citation1980), and measure in entropy. In this study, entropy is used to assess asset diversification.

A bank’s asset diversification is calculated as follows:

in which Div is the level of asset diversification, t is a bank’s assets, and pt is the ratio of t assets to total assets.

3.2. Estimation method

3.2.1. Structural equation modelling

We employ structural equation modeling (SEM) for two main reasons: Firstly, there exists a mediator (liquidity creation) in the research model. The relationship among BankCap (bank capital), LiqCreation (liquidity creation), Stability (bank stability), and Div (asset diversification) forms a structural model. Secondly, the stability of a bank is measured by a set of indicators. For more details, LiqCreation is a construct that represents stability. This latent variable is assessed by a set of five indicators (Table ). The connection between Stability and its indicators forms a measurement model. Hence, our model consists of a structural model and a measurement model.

In an SEM model, there are primarily two methods for estimating the relationships (Rigdon et al., Citation2017). One is called CB-SEM, while the other is called PLS-SEM. Each is appropriate for a different research context, and researchers need to understand the differences to apply the correct method. Each is ideal for a unique study situation, and researchers must be aware of the distinctions between them to choose the proper technique (Rigdon et al., Citation2017). Following the instruction of Hair et al. (Citation2021), PLS—SEM is appropriate for our research for several reasons: (i) there exists a moderator (Div) in the model, (ii) the measurement model of Stab may be formative, (iii) we have to handle constructs with single-item measures, and (iv) distributional assumptions are not the concern of PLS—SEM.

3.2.2. Structural model and statistical model

Figure represents the structural model (a) and statistical model (b). The earlier model describes the relationship between latent variables. While the latter, based on the earlier, is employed for estimation. In the statistical model, we create an interaction term called Div×LC. This variable represents the moderation effect of Div on the relationship between LC and Stab. We apply a two-stage calculation method, suggested by Wynne W Chin et al. (Citation2003), to create an interaction term (Div×LC).

Figure 2. Structural model (a) and statistical model (b).

3.2.3. The equations of the structural model

Based on the statistical model, the relationship between latent variables is described by the following equations:

The set of equations above explains a path model with two endogenous variables in the estimated model: LiqCreation and Stability. As a result, there are two equations. The influence of BankCap on LiqCreation is described in Equation (1), whereas the effect of BankCap, LiqCreation, and Div on Stability is expressed in Equation (2). In addition, Div×LC represents the impact of the interaction between Div and LiqCreation on Stability in Equation (2).

The set of given equations also describes the indirect influence of LiqCreation on the relationship between BankCap and Stability. In addition, the moderating influence of Div on the relationship between LiqCreation and Stability is presented, including both the main effect (Div effect on Stability) and the interactive effect (Div × LC effect on Stability).

3.2.4. Path model

PLS—SEM, often known as the path model, is a method for estimating and assessing complex interrelationships between constructs and indicators. In this study, we apply SmartPLS software as a tool to analyze the path model.

The path model includes the structural (inner) and measurement (outer) model. Two types of models are visualized in a path diagram. In our research, the path diagram is illustrated in Figure .

Figure 3. Structural model and measurement model.

The inner model describes the structural relationship among five latent variables: BankCap, LiqCreation, Stability, Div, and Div&LC. The outer model consists of five measurement models. Four of the five are single-item measurement models, including BankCap, LiqCreation, Div, and Div&LC. The Stability measurement model may be a formative measurement model formed by five indicators (A, CAR, E, L, M).

3.2.5. Panel data in an SEM model

According to Wooldridge (Citation2015), unobserved effects, including time and individual-fixed effects, are one characteristic of panel data and should be controlled. Equation (3) describes a panel data regression model in matrix form.

where:

: the inputs matrix (

In order to control individual fixed effects in an SEM model, Vu and Ha (Citation2021) propose the demeaning method to transform the data before applying SEM. When applying the demeaning method, Equation (3) is modified in scalar form as follows:

where

• Y*kit = (Yi1 + (Yi2 + . . .+ (Yit)/t

• X*kit = (Xki1 + (Xki2 + . . .+ (Ykit)/t

• Δvit = (ui + (eit) – (u*i + e*it) = eit - e*it

By using the demeaning method to transform data, ui is eliminated from Δvit. In other words, ui is removed from the model (Equation (5)). As a result, the unobserved individual-fixed effect does not affect independent variables.

3.3. Data

First, we compile the data on 27 commercial banks listed on the Vietnam stock exchange from 2014 to 2021. Concern that the banking sector was still affected by the global financial crisis in 2008 and Vietnam’s financial troubles in 2012 prevented the collection of bank data prior to 2014. In addition, the CAR index of Vietnamese commercial banks are comprehensively available only since 2014. As a result, there are 189 observations in the sample. The resulting data form an unbalanced panel data sample. Before employing PLS—SEM, this study applies the demeaning method to transform data. This transformation helps the research to remove unobserved individual-fixed effects from the model.

4. Results and discussion

4.1. Descriptive statistics

The descriptive statistics of all indicators that formed the measurement model are described in Table .

Table 3. Descriptive statistics of all periods

Table 4. Descriptive statistics over time

4.1.1. Bank stability

Capital adequacy (CAR), Asset quality (A), Management quality (M), Earnings risk (E), and Liquidity risk (L) are the components of the CAMEL index, which measure to Stab (Bank Stability) latent variable.

For most components of the CAMEL index, each indicator’s average value shows the bank’s stable performance in each aspect. For example, CAR is equal to 12.2%, greater than 8%. Currently, according to Basel II standards, which are widely applied by Vietnam banking systems, the CAR is 8%. Additionally, asset quality (A = Allowance for loans/Loans to customers) is relatively low (equal to 1.3%). However, the return on assets (E) in the period was meager, only 0.8% on average.

Table displays the improvement of some indicators of CAMEL over time. Since 2018, M, E, and L seem to improve more than before. For instance, the E appears to have improved from 2018 and reached its highest value (1.3%) in 2021.

4.1.2. Bank capital

Throughout the entire time, the average ratio of equity to total assets (Bank capital) is approximately 8.5% (Table ). Table demonstrates that this indicator gradually increases from 2017 and peaks in 2021 at 9.12%. This sign depicts the efforts of banks to increase the buffer capital over time. Hence, banks may enhance safety as well as expand credit growth.

4.1.3. Liquidity creation

Over the eight years of observation, on average, a bank has a liquidity creation (LC) ratio of −10.6% (Table ). This result illustrates that banks generate negative economic liquidity, also known as liquidity de-creation. The mean value of the liquidity creation from 2014 to 2021 is displayed in Table . Prior to 2019, this figure varies between 7.9% and 10.5%. This value reaches a higher level after 2019 and fluctuates by about 13%.

4.1.4. Asset diversification

Table and 4 depict that bank asset diversification, on average, equals 1.73, which can be separated into two evaluation periods. The bank’s level of asset diversification was higher before 2018 than from 2018 to the present (Table ). This disparity is because banks’ investment allocation in major asset classes, such as loans to customers, investment securities, and balances with and loans to other credit institutions, has grown since 2018.

4.2. Confirmatory tetrad analysis and measurement model assessment

4.2.1. Confirmatory tetrad analysis

As previously stated, the bank stability construct is measured by multi-item scales, CAMEL index (CAR, A, M, E, and L). The suggested formative measurement model is used to measure the latent variable Stab. However, to confirm the measurement model of bank stability from a statistical perspective, the study employs CTA-PLS by Bollen and Ting (Citation2000). The findings in Table demonstrate that all p-values are less than 0.05; hence, the suggested measurement model is appropriate. Since the theoretical substance of the study and the statistical evidence are consistent, we employ a formative measurement model to measure bank stability.

Table 5. Results of confirmatory tetrad analysis

4.2.2. Measurement model assessment

Before starting with the assessment of the structural model, the measurement model is evaluated to ensure it meets the quality criteria. There are two types of measurement models in this study: single-item and formative models.

Single-item measurement model, which captures the essence of the construct under consideration, is generally sufficient. Houston (Citation2004) suggests that a single-item measuring a similar concept would be used if a research model relies on secondary data. In this study, LiqCreation, Div, Div&LC, and BankCap are measured by a single-item measurement model, so the validity and reliability assessment are unnecessary (Hair Jr, Hult, Ringle, & Sarstedt, Citation2021).

The formative model forms stability latent variable; hence, the convergent validity, the degree of multicollinearity between the indicators, and the significance level of each regression weight are all considered (Hair et al., Citation2021).

4.2.2.1. Convergent validity

We employ the “redundant analysis” approach recommended by Wynne W Chin (Citation1998). This approach requires a path model in which stability construct is an input and a single-item measurement model act as an output. The Z-score index, the output, is used to assess the convergence of the measurement model for Stability.

Figure depicts the R2 = 0.54 > 0.5, which exceeds the necessary threshold, indicating that the indicators for stability satisfy the requirement for convergence accuracy.

Figure 4. Convergent validity.

where:

Stability_F: Formative model (measured by CAMEL indicators)

Stability_S: Single item model (measured by Z-Score)

4.2.2.2. Multicollinearity

According to Table , the VIF coefficients of A, CAR, E, L, and M are 1,106, 1,077, 1.561, 1,021, and 1,732, respectively, enabling us to conclude that no multicollinearity is found between them.

Table 6. VIF coefficients

4.2.2.3. Outer weights significance

Finally, the p-values of outer weights are all less than 0.05 (details in Table ), showing that all five indicators play a significant role in forming the Stab latent variable. As a result, all the measures are retained in the measurement model and used for future analysis.

Table 7. The significance of outer weights

4.3. Structural model assessment

We perform a structural analysis on latent variables such as BankCap, Div, LiqCreation, Div&LC, and Stability. Before analyzing the mediating role of LiqCreation and moderating role of Div, the study performs some common PLS-SEM structural model evaluations such as multicollinear (VIF), determinant coefficient (R2), effect size (f2), and the significance of coefficients.

4.3.1. Structural model evaluation

First, the VIF coefficients for BankCap (VIF = 1.136), Div (VIF = 1.059), LiqCreation (VIF = 1.081), and Div&LC (VIF = 1.077) are all less than 5, indicating that the four variables are not multicollinear. Furthermore, R2 = 0.535 demonstrates that these four factors explain 53.5% of the variation in Stability. Their f2 illustrates the influence of each of these factors on stability. BankCap (f2 = 0.056) and Div&LC (f2 = 0.034) have a more substantial explanatory effect than Div (f2 = 0.399) and LiqCreation (f2 = 0.298). Based on the criteria of Cohen (Citation2013), the effective level of LiqCreation is moderate, and the effective level of Div is high.

Next, we perform a bootstrapping test to access the significance of coefficients. Table shows the result of the bootstrapping test. The impact coefficients are statistically significant based on the 95% confidence interval values.

Table 8. Results of direct effects, indirect effects, and total effects after a bootstrapping test

BankCap has a regression coefficient of −0.197 and a statistically significant negative influence on LiqCreation. As a result, H2 about the positive relationship between BankCap and LiqCreation is rejected. That is, increasing a bank’s capital reduces the bank’s liquidity creation. In recent years, Vietnamese commercial banks have expanded their charter capital to achieve a variety of critical goals, including increasing the capital adequacy ratio, the number of deposits, and the size of the credit. As owner’s equity grows, so do total assets (from short-term deposits, long-term deposits, equity increases, and debt instruments). However, the rise in overall assets does not imply that most of these funds are being used to invest in long-term assets. This is because the State Bank of Vietnam has already enacted laws to reduce the ratio of short-term deposits to long-term loans. In particular, from October 2010 to January 2015, the State Bank relaxed limits on this percentage. Subsequently, it reinstated a 60% ceiling before lowering it to 45% and 40% as of 1 January 2019. According to the current regulations, this 40% rate was in effect only from January 1 to 30 September 2020, and will continue to fall soon. As a result, equity rose to increase short- and long-term deposits. However, because of these bank restrictions, when growth in short-term capital is higher, the liquidity creation ratio is lower (the ratio of short-term capital to long-term loans). The percentage of short-term deposits to long-term loans is declining; although short-term capital grows, the ability to convert liquidity shrinks. This also means that, in Vietnam, the State Bank has implemented policies to restrict the ratio of short-term deposits to long-term loans. Over time, this ratio tends to tighten, reducing liquidity creation while the bank’s capital rises. Thus H2 is rejected.

BankCap has a statistically significant positive influence on Stability, with a regression coefficient of 0.172. Hence, H1 is supported. As a result, the rise in bank capital has contributed to bank stability. The empirical results in Vietnam are consistent with the theory and with most other empirical studies conducted worldwide.

4.3.2. Mediating effect of liquidity creation

In this study, LiqCreation is viewed as a mediating variable in the relationship between BankCap and Stability. First, LiqCreation has a regression coefficient of −0.387 and a statistically significant direct negative influence on stability. As a result, H3 is supported. Regarding the mediating variable, LiqCreation is expected to cause a shift in the negative indirect impact of BankCap on Stability. That is, BankCap positively influences LiqCreation, and LiqCreation adversely affects stability. However, because H2 is rejected and H3 is supported, LiqCreation’s mediating role is not as predicted. More specifically, the indirect impact of BankCap on Stability becomes positive because the effects of BankCap on LiqCreation and LiqCreation on Stability are negative. This indirect impact has a magnitude of 0.076. Thus, when the bank’s capital rises, liquidity creation falls (perhaps as a result of the influence of the State Bank’s restrictions on short-term mobilization for long-term loans). Then the risk is minimized, and the stability is improved.

4.3.3. Moderating effect of asset diversification

Table shows Div has a statistically significant direct influence on Stability, with a regression coefficient of 0.443. The interaction term Div&LC has a statistically significant direct positive influence on Stability, with a regression value of 0.115. As a result, H4 and H5 are both confirmed. However, to understand Div’s moderating role, we perform further analysis.

Based on the path model results in Figure , the following regression equation describes the relationship between LiqCreation and Stability, modified by Div:

Figure 5. Estimated results of the structural model.

A determination of the role of Div requires an investigation of it at three distinct levels: high, medium, and low. Because the PLS-SEM algorithm uses standardized data (the mean is always 0, and the standard deviation is always 1), a high level of Div is defined as the mean plus one standard deviation and equals 1. In contrast, a low level of Div is defined as the mean minus one standard deviation and equals −1. Meanwhile, at the medium level, Div is zero. Equation (6) is rewritten in each scenario as follows:

(i) If Div has low-level status (Div = −1):

(ii) If Div has medium-level status (Div = 0):

(iii) If Div has high-level status (Div = 1):

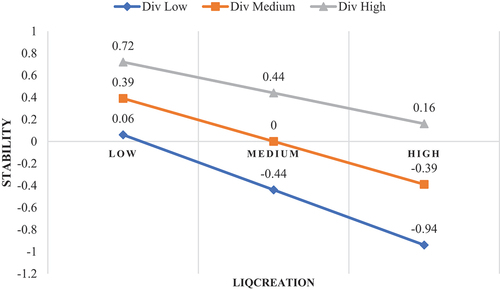

According to Equations (7), (8), and (9), as Div grows (from low to high), so does the slope of the regression line illustrating the relationship between LiqCreation and Stability (from − 0.50, fell to −0.39, and fell to −0.28). This variation is due to the contribution of the interaction variable Div&LC, whose regression coefficient is positive and statistically significant (−0.11). This also suggests that greater asset diversification has lessened the negative impact of liquidity creation on the bank’s stability. As a result, hypothesis H5 is supported.

The study graphed three Equations (7), (8), and (9) to acquire a better understanding of how the role of the moderator Div influenced the relationship between LiqCreation and Stability. Stability is computed by adding the values of LiqCreation and Div at high, medium, and low levels as follows:

Based on the matrix in Table , the graphs for Equations (7), (8), and (9) are depicted in Figure as follows:

Figure 6. Graphs depicting Equations (7), (8), and (Equation9(9)

(9) ).

Table 9. The value calculation matrix for stability

The chart illustrates the relationship between LiqCreation and Stability following three levels of Div scores: low, medium, and high. The slopes of the three lines remain negative. However, the slope is more negative if the DIV is at a low level of scores and vice versa. As a result, the moderating role of Div is confirmed.

The regression coefficient of the interaction variable Div&LC in Equation (6) is 0.11, which is statistically significant according to the bootstrapping test. Although the role of the interaction variable is confirmed, the bootstrapping test for this regression coefficient does not determine the difference between the three regression coefficients in Equations (7), (8), and (9). As a result, we next examine the difference in these regression coefficients for “low,” “medium,” and “high” Div, with the results in Table .

Table 10. The gap between the regression coefficients

Table demonstrates that the gaps between the regressions in Equations (7), (8), and (9) are all statistically significant based on a bootstrapping test with 50,000 subsamples for the deviations β(High—Medium), β (Low—Medium), and β (High—Low). This means that the moderating effect of Div is more effective if it is outside the range (−1, 1).

As a result, increased asset diversification has reduced the negative impact of liquidity creation on bank stability and vice versa. Banks with a “high” degree of diversification would experience a less negative impact from liquidity creation on their stability than banks with a “low” level of diversification. This also implies that if a bank tries to increase the degree of liquidity creation in order to prioritize profit, its stability will decline. Banks, however, can minimize this negative impact by diversifying their portfolio of financial assets. But suppose a bank wants to increase liquidity creation in order to prioritize profits while limiting investment diversification. In that case, the degree of stability will decline more quickly because of the interaction impact of Div and LiqCreation.

4.4. Robustness check in PLS-SEM framework

Lu and White (Citation2014) describe robustness checks as “how certain ‘core’ regression coefficient estimates behave when the regression specification is modified in some way, typically by adding or removing regressors.” However, Sarstedt et al. (Citation2020), based on Lu and White (Citation2014), conclude that PLS—SEM researchers rarely employ the approach above. In order to test the robustness of structural model parameters, researchers should handle endogeneity in a PLS-SEM framework (Sarstedt et al., Citation2020).

Considering endogeneity is a key issue when applying regression-based methods such as PLS-SEM (Hult et al., Citation2018). When a predictor construct is connected with the dependent construct’s error term, PLS-SEM exhibits endogeneity (Bascle, Citation2008). We follow the systematic procedure of Hult et al. (Citation2018) to check the endogeneity in PLS—SEM, using the latent variable scores of the original model estimation as the inputs. Three steps to assess the endogeneity need to be performed as follows:

Step 1: Test the normal distribution of input latent variables. Gaussian Copula Approach is only applicable if the distribution of latent variables is nonnormal.

Step 2: Compute the Gaussian copula of the latent variables’ scores.

Step 3: Calculate the model that includes the Gaussian copula.

This study applies Kolmogorov—Smirnov test on the latent variable scores of BankCap, LiqCreation, Div, and Div&LC, which play as input variables in the structural model. The results depict that all inputs have not normally distributed. Hence, we perform the next two steps. After calculating Gaussian copula terms (CBankCap, CLiqCreation, CDiv, CDiv&LC), we estimate 14 models which Stability serves as the only output in all the models.

Table summarizes the significant level of all the Gaussian copulas, but none of them is statistically significant. The result implies that the endogeneity is not considered in our structural model.

Table 11. Assessment of endogeneity: Gaussian Copula Approach

5. Conclusions and recommendations

Bank stability receives a great deal of attention. This paper aims to clarify the influence of bank capital, the mediating role of liquidity creation, and the moderating role of asset diversification on the relationship between liquidity creation and bank stability.

In terms of measurement, Cap (a measure of bank capital) is proxied by the ratio of equity to total assets. LiqCreation (a measure of liquidity creation) is calculated based on Berger and Bouwman (Citation2009). The entropy calculation suggested by Jacquemin and Berry (Citation1979) is used to determine Div (asset diversification). Finally, Stability is assessed using the Z-score and components of the CAMEL index. These components are used to construct a formative measurement model for Stability. The research employs the Z-score in the assessment of stability’s measurement model.

The study creates a path model using models with single variables, such as BankCap, LiqCreation, and Div. The remaining variable, Stability, is measured using the formative model. This is a kind of structural model with “moderated mediation,” in which Div moderates the relationship between LiqCreation (mediating variable) and Stability (output variable). The PLS-SEM approach is then used to assess the relationship between these concepts.

According to our findings, bank capital has a statistically significant negative impact on liquidity creation but a statistically significant positive effect on bank stability. Furthermore, liquidity creation has a statistically significant negative influence on bank stability. Liquidity creation acts as a mediating variable between bank capital and bank stability. Additionally, asset diversification enhances bank stability and moderates the relationship between liquidity creation and bank stability. As a consequence, H1, H3, H4, and H5 are supported, but not H2.

The governance activities of Vietnamese commercial banks today are compliant not only with Basel 2 or Basel 3 regulations, but also with Vietnamese law. These distinct regulations are tailored to the context and development objectives of Vietnam, an emerging economy. Therefore, based on our findings, the following recommendations are made to policymakers and bank managers in Vietnam regarding government management and banking management in relation to bank stability. This can also serve as a reference for interested parties in other countries.

First, bank capital contributes to bank stability in both direct and indirect ways. As a result, the role of bank capital should be acknowledged as a key contributor to the stability of each bank and the entire banking system. As a result, the State Bank of Vietnam (SBV) must continue to find efficient strategies for progressively increasing the ratio of each bank’s equity to total assets. Increasing equity is difficult for banks because it requires large-scale stock issuance (issuance of bonus shares and additional issuance). Within its scope, the study suggests only that the SBV continues to pay attention to the development of the scale of bank capital and collaborate with banks to eliminate obstacles to capital expansion.

Furthermore, the study’s empirical findings suggest that an increase in bank capital may lead to a decrease in liquidity creation. So that it minimizes the negative impact of liquidity creation on stability. This implies that, in addition to increasing the size of capital at all banks in the system, the SBV must also focus on regulating short-term deposits for long-term loans. The study does not definitively determine how much tightening is required because more research is needed. Still, proper control of this tightening must be accompanied by evaluating the system’s profitability. Specifically, proper management of the ratio of short-term deposits to long-term loans will boost bank capital in the context of enhanced stability. However, the degree of this control should be evaluated from the perspective of profitability because when control is tighter, the entire banking system is less profitable.

In addition, the SBV must periodically assess the level of diversification of the entire system. A lower level of diversification leads to a larger negative influence of liquidity creation on stability. However, as the level of diversification into financial assets grows, the negative impact of liquidity creation on the bank system’s stability declines.

Bank executives must carefully assess the significance of equity expansion in enhancing bank stability. If increasing owners’ equity in the future is viable, the manager should have a plan to do so. In addition, managers must adhere to restrictions on the ratio of short-term deposits to long-term loans and plan for future tightening. Although this tightening might reduce profits to some degree, the benefit is that it will increase bank stability.

In addition, bank managers should use our findings to solve two crucial issues simultaneously: preservation of bank stability and expansion in business profits. Diversification of assets is the best solution. Diversifying the portfolio of financial assets helps banks become more stable as it raises its level of liquidity creation in pursuit of greater profits. In addition, the interaction effect between asset diversification and liquidity creation causes a larger reduction in bank stability if liquidity creation increases and asset diversification declines.

5.1. Limitations and future search

This paper creates a structural model to show the connection between bank capital, liquidity creation, and bank stability. The model integrates asset diversification as a moderating variable and should be examined with various circumstances (various countries, different times, etc.) to determine its effectiveness. Furthermore, the findings on the influence of bank capital on liquidity creation in Vietnam vary from those in many other empirical studies.

The findings indicate that the direct influence of bank capital on stability remains statistically significant. This means that one or more additional mediating variables explain bank capital’s impact on stability. As a result, more research should be conducted to incorporate other mediating variables into the suggested model. Furthermore, this model focuses on only one independent variable, bank capital; future research should include additional independent variables to create a more comprehensive picture of bank stability. Further research on the stability measurement is one option. Measuring stability with the Z-score or CAMEL indicators might not be the best method. This model can be used in future studies to enhance the model for measuring stability. Finally, subsequent research could employ this model in various situations to analyze the role of the mediating variable in liquidity creation and the progressive variable in asset diversification.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Thanh Huu Vu

Thanh Huu Vu is a teacher at the Faculty of Finance and Banking at the Ho Chi Minh City Open University (HCMCOU). He earned a doctorate from HCMCOU in 2018. His research concerns broadly fall under the field of quantitative finance.

Trung Thanh Ngo

Trung Thanh Ngo is a Doctor of Business Administration. He holds a Doctor of Philosophy in Business Administration from HCMCOU, Vietnam. He is currently a lecturer in the Faculty of Finance and Banking and a member of FEMR, HCMCOU.

References

- Abbas, F., Iqbal, S., Aziz, B., & Yang, Z. (2019). The impact of bank capital, bank liquidity and credit risk on profitability in postcrisis period: a comparative study of US and Asia. Cogent Economics & Finance, 7(1), 1605683. https://doi.org/10.1080/23322039.2019.1605683

- Acharya, V., & Naqvi, H. (2012). The seeds of a crisis: A theory of bank liquidity and risk taking over the business cycle. Journal of Financial Economics, 106(2), 349–25. https://doi.org/10.1016/j.jfineco.2012.05.014

- Allen, F., Carletti, E., & Gu, X. (2014). The roles of banks in financial systems. In A. N. Berger, P. Molyneux, & J. O. S. Wilson (Eds.), The oxford handbook of banking (p. 27). Oxford University Press.

- Allen, F., Carletti, E., & Marquez, R. (2015). Deposits and bank capital structure. Journal of Financial Economics, 118(3), 601–619. https://doi.org/10.1016/j.jfineco.2014.11.003

- Amidu, M., & Wolfe, S. (2013). Does bank competition and diversification lead to greater stability? Evidence from emerging markets. Review of Development Finance, 3(3), 152–166. https://doi.org/10.1016/j.rdf.2013.08.002

- Anginer, D., & Demirgüç-Kunt, A. (2014). Bank capital and systemic stability. Retrieved from https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2459698

- Anginer, D., Demirgüç-Kunt, A., & Mare, D. S. (2018). Bank capital, institutional environment and systemic stability. Journal of Financial Stability, 37, 97–106. https://doi.org/10.1016/j.jfs.2018.06.001

- Bascle, G. (2008). Controlling for endogeneity with instrumental variables in strategic management research. Strategic Organization, 6(3), 285–327.

- Beck, T., Döttling, R., Lambert, T., & van Dijk, M. (2022). Liquidity creation, investment, and growth. Journal of Economic Growth, 1–40. https://doi.org/10.1007/s10887-022-09217-1

- Berger, A. N., Boubakri, N., Guedhami, O., & Li, X. (2019). Liquidity creation performance and financial stability consequences of Islamic banking: Evidence from a multinational study. Journal of Financial Stability, 44, 100692. https://doi.org/10.1016/j.jfs.2019.100692

- Berger, A. N., & Bouwman, C. H. (2009). Bank liquidity creation. The Review of Financial Studies, 22(9), 3779–3837. https://doi.org/10.1093/rfs/hhn104

- Berger, A. N., & Bouwman, C. H. (2017). Bank liquidity creation, monetary policy, and financial crises. Journal of Financial Stability, 30, 139–155. https://doi.org/10.1016/j.jfs.2017.05.001

- Berger, A. N., & Sedunov, J. (2017). Bank liquidity creation and real economic output. Journal of Banking & Finance, 81, 1–19. https://doi.org/10.1016/j.jbankfin.2017.04.005

- Bhattacharya, S., & Thakor, A. V. (1993). Contemporary banking theory. Journal of Financial Intermediation, 3(1), 2–50. https://doi.org/10.1006/jfin.1993.1001

- Bollen, K. A., & Ting, K. -F. (2000). A tetrad test for causal indicators. Psychological Methods, 5(1), 3. https://doi.org/10.1037/1082-989X.5.1.3

- Brunnermeier, M., Crockett, A., Goodhart, C. A., Persaud, A., & Shin, H. S. (2009). The fundamental principles of financial regulation (Vol. 11). Center for Monetary and Banking Studies Geneva.

- Caprio, G., & Honohan, P. (1999). Restoring banking stability: Beyond supervised capital requirements. Journal of Economic Perspectives, 13(4), 43–64. https://doi.org/10.1257/jep.13.4.43

- Casu, B., DiPietro, F., & Trujillo-Ponce, A. (2019). Liquidity creation and bank capital. Journal of Financial Services Research, 56(3), 307–340. https://doi.org/10.1007/s10693-018-0304-y

- Caves, R. E., Porter, M. E., Spence, M., & Scott, J. T. (1980). Competition in the open economy: A model applied to Canada. Harvard University Press.

- Chaabouni, M. M., Zouaoui, H., & Ellouz, N. Z. (2018). Bank capital and liquidity creation: New evidence from a quantile regression approach. Managerial Finance, 44(12), 1382–1400. https://doi.org/10.1108/MF-11-2017-0478

- Chen, R., Li, B., Zhang, Y., Zhang, C., Yang, P., & Zhang, J. (2021). Impact of interest rate liberalization: Analysis on bank liquidity creation. International Journal of Higher Education Teaching Theory, 2(4), 70.

- Chin, W. W. (1998). The partial least squares approach to structural equation modeling. Modern Methods for Business Research, 295(2), 295–336.

- Chin, W. W., Marcolin, B. L., & Newsted, P. R. (2003). A partial least squares latent variable modeling approach for measuring interaction effects: Results from a Monte Carlo simulation study and an electronic-mail emotion/adoption study. Information Systems Research, 14(2), 189–217. https://doi.org/10.1287/isre.14.2.189.16018

- Cohen, J. (2013). Statistical power analysis for the behavioral sciences. Routledge.

- Coval, J. D., & Thakor, A. V. (2005). Financial intermediation as a beliefs-bridge between optimists and pessimists. Journal of Financial Economics, 75(3), 535–569. https://doi.org/10.1016/j.jfineco.2004.02.005

- Dang, V. D. (2020). Do non-traditional banking activities reduce bank liquidity creation? Evidence from Vietnam. Research in International Business and Finance, 54, 101257. https://doi.org/10.1016/j.ribaf.2020.101257

- Davydov, D., Vähämaa, S., & Yasar, S. (2021). Bank liquidity creation and systemic risk. Journal of Banking & Finance, 123, 106031. https://doi.org/10.1016/j.jbankfin.2020.106031

- Deep, A., & Schaefer, G. K. (2004). Are banks liquidity transformers? KSG Working Paper No. RWP04-022. https://doi.org/10.2139/ssrn.556289

- Diamond, D. W. (2007). Banks and liquidity creation: A simple exposition of the Diamond-Dybvig model. FRB Richmond Economic Quarterly, 93(2), 189–200.

- Diamond, D. W., & Dybvig, P. H. (1983). Bank runs, deposit insurance, and liquidity. The Journal of Political Economy, 91(3), 401–419. https://doi.org/10.1086/261155

- Diamond, D. W., & Rajan, R. G. (2000). A theory of bank capital. The Journal of Finance, 55(6), 2431–2465. https://doi.org/10.1111/0022-1082.00296

- Duan, Y., & Niu, J. (2020). Liquidity creation and bank profitability. The North American Journal of Economics and Finance, 54, 101250. https://doi.org/10.1016/j.najef.2020.101250

- Duisenberg, W. F. (2001). The contribution of the euro to financial stability. In C. Randzio-Plath (Ed.), Globalization of financial markets and financial stability—Challenges for Europe (pp. 37–51). Nomos Verlagsgesellschaft.

- Elnahass, M., Trinh, V. Q., & Li, T. (2021). Global banking stability in the shadow of Covid-19 outbreak. Journal of International Financial Markets, Institutions and Money, 72, 101322. https://doi.org/10.1016/j.intfin.2021.101322

- Evans, J. J., & Haq, M. (2022). Does bank capital reduce liquidity creation? Global Finance Journal, 54, 100640. https://doi.org/10.1016/j.gfj.2021.100640

- Fungacova, Z., Turk, R., & Weill, L. (2015). High liquidity creation and bank failures: Do they behave differently? IMF Working Papers. Retrieved from https://www.elibrary.imf.org/view/journals/001/2015/103/001.2015.issue-103-en.xml

- Fungacova, Z., Turk, R., & Weill, L. (2021). High liquidity creation and bank failures. Journal of Financial Stability, 57, 100937. https://doi.org/10.1016/j.jfs.2021.100937

- Fungáčová, Z., Weill, L., & Zhou, M. (2017). Bank capital, liquidity creation and deposit insurance. Journal of Financial Services Research, 51(1), 97–123. https://doi.org/10.1007/s10693-016-0240-7

- Gorton, G., & Winton, A. (2017). Liquidity provision, bank capital, and the macroeconomy. Journal of Money, Credit, and Banking, 49(1), 5–37. https://doi.org/10.1111/jmcb.12367

- Gupta, J., & Kashiramka, S. (2020). Financial stability of banks in India: Does liquidity creation matter? Pacific-Basin Finance Journal, 64, 101439. https://doi.org/10.1016/j.pacfin.2020.101439

- Hair, J. F., Jr., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2021). A primer on partial least squares structural equation modeling. Sage publications.

- Holmstrom, B., & Tirole, J. (1997). Financial intermediation, loanable funds, and the real sector. The Quarterly Journal of Economics, 112(3), 663–691. https://doi.org/10.1162/003355397555316

- Horváth, R., Seidler, J., & Weill, L. (2014). Bank capital and liquidity creation: Granger-causality evidence. Journal of Financial Services Research, 45(3), 341–361. https://doi.org/10.1007/s10693-013-0164-4

- Houston, M. B. (2004). Assessing the validity of secondary data proxies for marketing constructs. Journal of Business Research, 57(2), 154–161. https://doi.org/10.1016/S0148-2963(01)00299-5

- Hsieh, M. F., Chen, P. F., Lee, C. C., & Yang, S. J. (2013). How does diversification impact bank stability? The role of globalization, regulations, and governance environments. Asia‐pacific Journal of Financial Studies, 42(5), 813–844. https://doi.org/10.1111/ajfs.12032

- Hsieh, M. -F., Lee, C. -C., & Lin, Y. -C. (2022). New evidence on liquidity creation and bank capital: The roles of liquidity and political risk. Economic Analysis and Policy, 73, 778–794. https://doi.org/10.1016/j.eap.2022.01.002

- Hult, G. T. M., Hair, J. F., Jr., Proksch, D., Sarstedt, M., Pinkwart, A., & Ringle, C. M. (2018). Addressing endogeneity in international marketing applications of partial least squares structural equation modeling. Journal of International Marketing, 26(3), 1–21. https://doi.org/10.1509/jim.17.0151

- Isnurhadi, I., Adam, M., Sulastri, S., Andriana, I., & Muizzuddin, M. (2021). Bank capital, efficiency and risk: Evidence from Islamic banks. The Journal of Asian Finance, Economics and Business, 8(1), 841–850. https://doi.org/10.13106/jafeb.2021.vol8.no1.841

- Jacquemin, A. P., & Berry, C. H. (1979). Entropy measure of diversification and corporate growth. The Journal of Industrial Economics, 27(4), 359–369. https://doi.org/10.2307/2097958

- Kashyap, A. K., Rajan, R., & Stein, J. C. (2002). Banks as liquidity providers: An explanation for the coexistence of lending and deposit‐taking. The Journal of Finance, 57(1), 33–73. https://doi.org/10.1111/1540-6261.00415

- Kiemo, S., Talam, C., & Rugiri, I. W. (2022). Bank capital, credit risk and financial stability in Kenya. Retrieved from http://hdl.handle.net/10419/249557

- Kim, H., Batten, J. A., & Ryu, D. (2020). Financial crisis, bank diversification, and financial stability: OECD countries. International Review of Economics & Finance, 65, 94–104. https://doi.org/10.1016/j.iref.2019.08.009

- Le, T. (2018). The interrelationship between liquidity creation and bank capital in Vietnamese banking. Managerial Finance, 45(2), 331–347. https://doi.org/10.1108/MF-09-2017-0337

- Lu, X., & White, H. (2014). Robustness checks and robustness tests in applied economics. Journal of Econometrics, 178, 194–206. https://doi.org/10.1016/j.jeconom.2013.08.016

- Markowitz, H. (1952). The utility of wealth. The Journal of Political Economy, 60(2), 151–158. https://doi.org/10.1086/257177

- Nguyen, T. T. H., Phan, G. Q., Wong, W. -K., & Moslehpour, M. (2022). The influence of market power on liquidity creation of commercial banks in Vietnam. Journal of Asian Business and Economic Studies. https://doi.org/10.1108/JABES-06-2021-0076

- Nguyen, M., Skully, M., & Perera, S. (2012). Market power, revenue diversification and bank stability: Evidence from selected South Asian countries. Journal of International Financial Markets, Institutions and Money, 22(4), 897–912. https://doi.org/10.1016/j.intfin.2012.05.008

- Nisar, S., Peng, K., Wang, S., & Ashraf, B. N. (2018). The impact of revenue diversification on bank profitability and stability: Empirical evidence from South Asian countries. International Journal of Financial Studies, 6(2), 40. https://doi.org/10.3390/ijfs6020040

- Ozili, P. K. (2018). Banking stability determinants in Africa. International Journal of Managerial Finance, 14(4), 462–483. https://doi.org/10.1108/IJMF-01-2018-0007

- Ramakrishnan, R. T., & Thakor, A. V. (1984). Information reliability and a theory of financial intermediation. The Review of Economic Studies, 51(3), 415–432. https://doi.org/10.2307/2297431

- Repullo, R. (2004). Capital requirements, market power, and risk-taking in banking. Journal of Financial Intermediation, 13(2), 156–182. https://doi.org/10.1016/j.jfi.2003.08.005

- Rigdon, E. E., Sarstedt, M., & Ringle, C. M. (2017). On comparing results from CB-SEM and PLS-SEM: Five perspectives and five recommendations. Marketing: ZFP–Journal of Research and Management, 39(3), 4–16.

- Rubio, M., & Yao, F. (2020). Bank capital, financial stability and Basel regulation in a low interest-rate environment. International Review of Economics & Finance, 67, 378–392. https://doi.org/10.1016/j.iref.2020.02.008

- Santos, J. A. 2001 Bank capital regulation in contemporary banking theory: A review of the literature Financial Markets, Institutions Instruments 10 2 41–84 https://doi.org/10.1111/1468-0416.00042

- Sarstedt, M., Ringle, C. M., Cheah, J. -H., Ting, H., Moisescu, O. I., & Radomir, L. (2020). Structural model robustness checks in PLS-SEM. Tourism Economics, 26(4), 531–554. https://doi.org/10.1177/1354816618823921

- Schinasi, G. J. (2004). Defining financial stability. IMF Working Paper. Retrieved from https://www.imf.org/external/pubs/ft/wp/2004/wp04187.pdf

- Segoviano, M. A., & Goodhart, C. (2009). Banking stability measures. IMF Working Paper. Retrieved from https://www.imf.org/external/pubs/ft/wp/2009/wp0904.pdf

- Shim, J. (2019). Loan portfolio diversification, market structure and bank stability. Journal of Banking & Finance, 104, 103–115. https://doi.org/10.1016/j.jbankfin.2019.04.006

- Steffen, S. (2014). Robustness, validity and significance of the ECB’s asset quality review and stress test exercise. Retrieved from

- Thakor, A. V. (2014). Bank capital and financial stability: An economic trade-off or a Faustian bargain? Annual Review of Financial Economics, 6(1), 185–223. https://doi.org/10.1146/annurev-financial-110613-034531

- Toh, M. Y. (2019). Effects of bank capital on liquidity creation and business diversification: Evidence from Malaysia. Journal of Asian Economics, 61(April 2019), 1–19. https://doi.org/10.1016/j.asieco.2018.12.001

- Vo, D. H., Nguyen, N. T., & Van, L.T. -H. (2021). Financial inclusion and stability in the Asian region using bank-level data. Borsa Istanbul Review, 21(1), 36–43. https://doi.org/10.1016/j.bir.2020.06.003

- Von Thadden, E. -L. (2004). Asymmetric information, bank lending and implicit contracts: The winner’s curse. Finance Research Letters, 1(1), 11–23. https://doi.org/10.1016/S1544-6123(03)00006-0

- Vu, H. T., & Ha, N. M. (2021). A study on the relationship between diversification and firm performance using the GSEM method. Emerging Markets Finance and Trade, 57(1), 85–107. https://doi.org/10.1080/1540496X.2019.1582413

- Wooldridge, J. (2015). Introductory econometrics: A modern approach. Nelson Education.

- World-Bank. (2016). Global financial development report 2015/16. Retrieved from https://www.worldbank.org/en/publication/gfdr/gfdr-2016/background/financial-stability

- Zheng, C., Cheung, A., & Cronje, T. (2019). The moderating role of capital on the relationship between bank liquidity creation and failure risk. Journal of Banking & Finance, 108, 105651. https://doi.org/10.1016/j.jbankfin.2019.105651