?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

There is a lack of consensus on how corporate governance and CSR relationships manifest across different institutional contexts especially within emerging economies, despite the wealth of available studies on the two concepts. The purpose of this study is to examine the relationship between corporate governance and corporate social responsibility as well as their effect on the performance of manufacturing firms via corporate image. The quantitative approach was used to collect data from a sample of 328 top executives of selected manufacturing firms in Ghana using the purposive sampling technique. The data collected was analyzed using AMOS and Process Macro. The study found that corporate governance has a high tendency to catalyze corporate social responsibility performance. The study further revealed that good corporate governance practices enhance both corporate image and performance of firms. Corporate social responsibility was also found to have a significant positive relationship with both corporate image and performance of manufacturing firms. The study further illuminated that corporate governance and corporate social responsibility have an indirect effect on firm performance through corporate image. The study has demonstrated how corporate governance and corporate social responsibility synergistically impact the performance of manufacturing firms. The study helps advance knowledge on the synergy and convergence of CSR and corporate governance interfaces and offers rich insight into the corporate governance and CSR puzzles within the context of the emerging economy.

1. Introduction

High-profile scandals throughout the world have piqued the interest of academic and professional researchers in corporate governance (Ali et al., Citation2022; Ahmed et al., Citation2020; Binh & Hoang, Citation2018; Dartey-Baah & Amoako, Citation2021; Ofoegbu et al., Citation2018; Ali et al., Citation2019; Sarpong Danquah et al., Citation2022; Zaman et al., Citation2021). Thus, corporate governance research has been a significant topic of discussion over the past three decades, as many developed and developing countries have enacted laws requiring companies operating within their jurisdiction to comply with corporate governance principles in order to protect stakeholder interests (Ganda, Citation2022; Ssekiziyivu et al., Citation2018; Antwi et al., Citation2022).

In the wake of previous financial crises and scandals, requests were made for stricter corporate governance policies, leading to the prominence of the issue of corporate governance (Abdullah & Tursoy, Citation2023; Naz et al., Citation2022; Ahmed et al., Citation2020; Dartey-Baah & Amoako, Citation2021; Ali et al., Citation2022; Binh & Hoang, Citation2018; Mertzanisa et al., Citation2019). As such, sound corporate governance has become a critical success factor for firms (Binh & Hoang, Citation2018; Dartey-Baah & Amoako, Citation2021; Ali et al., Citation2019) and a company’s efficient operation (Ahmed et al., Citation2020; Mertzanisa et al., Citation2019). Corporate governance has become critical for strengthening firm performance, protecting investor rights, enhancing the investment climate, and stimulating economic growth (Ahmed et al., Citation2020; Binh & Hoang, Citation2018; Ali et al., Citation2019). Thus, interest in corporate governance has surged, propelling the phrase “corporate governance” from obscurity to the center of much academic and professional research. This piqued curiosity emerged at a time when business executives and auditors are being held to increasingly high standards of accountability and responsibility (Driel, Citation2019; Mardnly et al., 2019). Despite the fact that numerous studies have investigated the relationship between corporate governance and firm performance, the culminating result seems to be spurious and imprecise(Abdullah & Tursoy, Citation2023; Naz et al., Citation2022; Sarpong Danquah et al., Citation2022;; Ali et al., Citation2022; Ahmed et al., Citation2020; Nugroho, Citation2021) and for that matter largely unexhausted.

Similarly, corporate social responsibility (CSR) has grown in importance in contemporary corporate practice and research(Combs et al., Citation2023; Martos‐pedrero et al., Citation2023; Singh & Misra, Citation2021). Globally, there has been a drastic shift in the notion of organizations’ function and duty in society, with corporations being expected to radically contribute to the sustainable development of society (Dartey-Baah & Amoako, Citation2021; Yu & Huo, Citation2021; Jahid et al., Citation2020; Ring, Citation2022). Society expects firms to be actively involved in CSR and give back to the areas in which they operate (Jamali et al., Citation2008; Doshmanli et al., Citation2018; Melissen et al., Citation2018). Firms are therefore under pressure to engage in CSR activities as the relevance of CSR as a criterion for company evaluation grows (Moneva & Hernández-Pajares, Citation2018; Dartey-Baah & Amoako, Citation2021). In line with this, numerous studies have been conducted to assess the direct effect of corporate social responsibility on firm performance; however, the result has equally been largely inconclusive (Doshmanli et al., Citation2018; Melissen et al., Citation2018; Kong et al., Citation2020; Ali et al., Citation2020; Singh & Misra, Citation2021; Ring, Citation2022; Zhang et al., Citation2022; Martos-Pedrero et al., 2023), which is sometimes attributed to the methodological error associated with such studies (Arevalo and Aravind, Citation2017; Kong et al., Citation2020; Zaman et al., Citation2022).

Interestingly, social, environmental, and governance-related scandals have increased dramatically in the new millennium, which has spurred interest in understanding the convergence, synergies, and interdependencies between corporate governance and CSR (Ledi et al., Citation2022; Zaman et al., Citation2022; Zaman et al., Citation2021; Jain & Jamali, Citation2016; Ntim & Soobaroyen, Citation2013). This field of study has theoretically advanced in three directions: the first component employs CSR as an umbrella term that encompasses responsible governance (Young & Thyil, Citation2014; Frynas, Citation2010); the second strand portrays CG as a foundation for CSR (Jamali et al., Citation2008; Ntim & Soobaroyen, Citation2013; Filatotchev & Stahl, Citation2015); and the last piece considers CG and CSR to coexist (Amoako, Citation2017; Ledi et al., Citation2022). Consequently, despite the fact that a few studies have set the pace of research in this field, these existing studies pay scant consideration to the entire spectrum of interactions between CG and CSR (Jain & Jamali, Citation2016), especially when the emergence of interfaces, including classifications of internal and external CG and CSR mechanisms, requires a comprehensive assessment (Zaman et al., Citation2022).

In addition, the underlying relationship between CG and CSR is centered on managerial thoughts, perceptions, and contextual setting; thus, ignoring these characteristics leads to inconclusive results in the literature (Young & Thyil, Citation2014; Jain & Jamali, Citation2016; Tilt, Citation2016; Mansi et al., 2017; Kabir & Thai, 2017; Zaman et al., Citation2021). Thus, there is a growing recognition that different national business systems and their corresponding institutional settings can shape business-society relationships and have varying effects on the CG-CSR nexus (Zaman et al., Citation2022). The majority of CG and CSR research has, however, ignored contextual settings and failed to advance our comprehension of CG and CSR interrelationships in emerging economies (Zaman et al., Citation2022; Jain & Jamali, Citation2016). In emerging economies, for instance, the proliferation of global production chains has, on the one hand, exacerbated social and environmental issues and, on the other, weakened the regulatory capacity of the government. As a result, institutional gaps in these contexts have created opportunities for external monitoring of CG and CSR by transnational entities, international institutions, and corporations in order to develop voluntary codes of conduct for governance and sustainability (Zaman et al., Citation2022; Ofoegbu et al., Citation2018; Ssekiziyivu et al., Citation2018; Eberlein et al., Citation2014) To date, there is little knowledge on CG and CSR linkage within emerging economies and their synergistic effect on firm performance, providing valuable opportunities for progressing knowledge in this area.

In line with this, as previous studies have found conflicting results pertaining to both CSR and CG in relation to performance, a coalesced effect of CSR and CG can better predict firm performance, especially when both CSR and CG emphasize the significance of openness, disclosure, sustainability, and ethical behavior and are concerned with an organization’s interactions with stakeholders. This is particularly the case when there is a growing demand for businesses to address CSR and CG issues in tandem (Ledi et al., Citation2022). However, although the concepts of corporate governance and CSR are well known, their interrelationship has surreptitiously gained negligible attention (Zaman et al., Citation2022; Jahid et al., Citation2020). More specifically, CG and CSR are growing entwined; however, most previous research in developing economies such as Ghana has investigated CG and CSR separately (Sarpong-Danquah et al., Citation2018; Akomea-Frimpong et al., 2022; Musah & Adutwumwaa, Citation2021; Dartey-Baah & Amoako, Citation2021; Nyarku & Ayekple, Citation2019). Thus, the nexus between CG and CSR has garnered insufficient attention in the Ghanaian context.

Consequently, CG and CSR in developing economies require additional critical and exhaustive research. Ghana provides an ideal setting for studying CG-CSR interaction because, in Ghana, most firms are performing better in terms of corporate governance than in terms of CSR. This could be attributed to the fact that the majority of corporate governance rules and practices are mandated by the state, which forces companies to adhere to them, as compared to CSR, which is largely voluntary in nature within the Ghanaian context. This could be attributed to contextual factors such as weak institutions and a lack of a comprehensive legal framework for CSR, making CSR completely voluntary. Therefore, there are clearly developmental issues still to be considered in Ghana within the context of CSR. Firms in Ghana seem to have failed to understand the potential link between CSR engagement and CG systems. As a result, if the CSR-CG nexus is correctly recognized, prioritized, and legitimized in Ghana, corporations may place a greater priority on CSR activities and improve their long-term performance, as postulated by the legitimacy theory. Ghana therefore presents a unique setting for examining the CG-CSR interaction with the level of institutions and legal framework requirements for both corporate governance and corporate social responsibility, especially pertaining to manufacturing companies.

Historically, the manufacturing sector has been regarded as the engine of economic growth and expansion . Therefore, manufacturing contributes significantly to Ghana’s GDP (Sarpong-Danquah et al., Citation2018). Consequently, effective governance of the sector through systems of norms, practices, and processes is becoming increasingly important for practitioners and policymakers. However, limited research has been conducted in Ghana on the relationship between firm performance and corporate governance in the manufacturing sector (Sarpong-Danquah et al., Citation2018). It is against this backdrop that this study attempts to answer the research questions: (1) How can corporate governance anchor CSR? (2) “What differential effect do corporate governance and CSR have on firm performance via corporate image?”

Consequently, this paper aims to contribute the following to the existing literature: Firstly, in a developing economy like Ghana, previous studies significantly ignored corporate social responsibility and corporate governance interaction as the two concepts are investigated separately (Sarpong Danquah et al., Citation2022; Musah & Adutwumwaa, Citation2021; Dartey-Baah & Amoako, Citation2021; Nyarku & Ayekple, Citation2019; Sarpong-Danquah et al., Citation2018). Therefore, there is a lack of consensus on how corporate governance and CSR relationships manifest across different institutional contexts, especially within emerging economies, despite the wealth of available studies on the two concepts. The study helps advance knowledge on the internal antecedents of CSR by revealing that CG sets the fundamental tone for a firm’s CSR performance. Hence, practitioners and policymakers who want to advance CSR should fortify the CG system and practices since the CG system has a massive tendency to curtail or catalyze CSR. Secondly, the study also makes a significant contribution to understanding the antecedents and models influencing firm performance. The study has demonstrated how CG and CSR collectively affect firm performance, both directly and indirectly, by establishing the role of corporate image as a mediator. Third, the study provides a comprehensive understanding of how manufacturing firms in Ghana, which have received negligible attention in the Ghanaian literature, can improve their performance by suitably constituting CG systems and fostering CSR performance to achieve a stellar corporate image, which ultimately leads to improved firm performance. Lastly, this study adds nuances to extant theoretical literature by employing theoretical pluralism to explain the intricacies of the CG and CSR interface and ultimately offering rich insight into the CG and CSR puzzles within the context of emerging economy.

The rest of this study follows this structure: background, theoretical literature review, empirical literature review and hypotheses development, research design, empirical results and discussion, and summary and conclusion.

2. Background

The widespread failure of major firms over many decades has increased interest in the subject in both developed and emerging nations (Antwi et al., Citation2022). Corporate governance as a whole has developed over time in reaction to crises and business failures (Adegbite, Citation2012). This is primarily due to the significant corporate failures that have occurred predominantly in the western world and have been attributed to governance failures. Similarly,) corporate governance failures is regarded as a major cause of the failure of numerous businesses in diverse sectors of the African economy (Banahene, Citation2018; Ofoegbu et al., Citation2018; Ssekiziyivu et al., Citation2018). In many African nations, such as Ghana, the level of corporate governance compliance is low due to a significant enforcement disparity, insufficient board independence, unbalanced power, and inadequate disclosure. In accordance with this, in the early 2000s, a number of companies in Ghana, including Ghana Cooperative Bank Limited, Divine Sea Foods Limited, Bonte Gold Mines Limited, Juapong Textiles Limited, Bank for Housing and Construction Limited, and Ghana Airways Limited, collapsed due to poor governance practices (Banahene, Citation2018; Sarpong-Danquah et al., Citation2018). This prompted the Ghana Security and Exchange Commission (SEC) to establish a corporate governance best practices guideline that adheres to OECD (2004) principles (Adegbite, Citation2012; Agyemang & Castellini, Citation2013; Sarpong Danquah et al., Citation2022).

The largest threat to the Ghanaian system has been recognized as corruption, which has continued and is growing despite calls for full compliance with the codes and their enforcement by the SEC (Adegbite, Citation2012; Agyemang & Castellini, Citation2013). As a result, many Ghanaian institutions collapsed between 2017 and 2019, costing people their jobs and causing investors and the government to pull out their money. The government of Ghana suffered financial losses spending over $1.2 billion trying to restore stability and sustainability (Knott, 2018; Galindo, 2019; Maama, Citation2021). Businesses in Ghana faced extinction as a result of a dramatic drop in public trust. It is possible that this terrible tragedy would have a negative impact on Ghana’s GDP, which relies heavily on the manufacturing and banking industries.

For enterprises in Ghana to attract investors and improve their financial performance, transparency and growth in their reporting methods have been regarded as a significant instrument. As a result, it is recommended that enterprises in Ghana include ESG (environmental, social, and governance) information in their reporting processes. Accounting for environmental, social, and governance (ESG) factors was seen as a management tool that may rebuild trust in Ghanaian businesses (Ackah & Lamptey, 2017; Maama, Citation2021). As a result, the Ghana Stock Exchange proposed ESG criteria in the fourth quarter of 2022, with rollout planned for 2023.

There appears to be little research on corporate governance and accountability in emerging economies, particularly Africa. Zaman et al. (Citation2022) argue that contextual factors, such as institutional requirements or standardization, and the governance structures of these countries have a significant impact on the CSR and CG nexus. As there are substantial differences between developing and developed economies in terms of the practice and theoretical foundations of CG and CSR, it is essential to investigate both concepts from a native perspective, taking into account the historical, cultural, and ethnic factors that influence the practice of CSR and CG. CSR activities, for example, are considerably influenced by general culture and collective orientation in developing economies, which ultimately shape a firm’s societal expectations (Dartey-Baah & Amoako, Citation2021). Ghana is therefore an ideal location to investigate CG-CSR interactions.

3. Theoretical literature review

The study is underpinned by the upper echelon, stakeholder, and legitimacy theories.

The upper echelon theory proposed by Hambrick and Mason (Citation1984) suggests that the qualities, values, and experiences of senior executives are likely to be reflected in the structure, culture, and strategies of the organization. The upper echelon theory posits that organizational behaviors and outcomes reflect the values, qualities, experiences, and cognitive bases of the organization’s top administrators (Hambrick and Mason, Citation1984; Petrenko et al., Citation2016). According to this theory, decision-making power is concentrated in the hands of a few top executives (the “upper echelons”) who shape the strategic direction of the organization. This theory demonstrates how the characteristics and backgrounds of these individuals, such as their education, experience, and social networks, impact organizational decision-making. According to the existing literature, TMT characteristics influence organizational decision-making processes (Hambrick & Quigley, Citation2014; Petrenko et al., Citation2016), and such characteristics would play a role in shaping organizational culture, strategies, and outcomes. Consequently, it is crucial to take into account the executives’ beliefs and values, which significantly influence the actions they are likely to take (Hambrick & Quigley, Citation2014). In accordance with this, a large body of literature asserts that powerful organizational actors play an important role in explaining CSR activities. In line with this, CSR is significantly influenced by CG structure (Jamali et al., Citation2008). CG mechanisms such as board monitoring, top management incentive schemes, and firm ownership structures encourage the incorporation of CSR activities.

Freeman (1984) devised the stakeholder theory, emphasizing the need for managers to be accountable to stakeholders. According to the stakeholder theory, managers have a network of relationships to serve, including employees, shareholders, suppliers, business partners, and contractors. According to Freeman (1984), stakeholders are any group or individual who can influence or is impacted by the accomplishment of a corporation’s mission (Donaldson and Preston, Citation1995; Zhang et al., Citation2022). Stakeholder theory proposes the representation of various interest groups on an organization’s board to assure consensus building, avoid conflicts, and coordinate efforts to achieve organizational objectives. Donaldson and Preston Citation1995 argue that stakeholder theory concentrates on managerial decision-making, that the interests of all stakeholders have intrinsic value, and that no set of interests is assumed to be more important than the others. Therefore, Jensen (2001) suggests that managers should pursue objectives that enhance the firm’s long-term value by safeguarding the interests of all stakeholders. The implication is that managers are expected to consider the interests and influences of individuals affected or potentially affected by the company’s policies and operations. This theory is appropriate for this study as it focuses on manufacturing firms whose activities affect various stakeholders. Corporate governance extends beyond the maximization of shareholder value to encompass the relationships between multiple stakeholders, such as investors, employees, and society, thereby creating responsibility and accountability for the impact of corporate actions on the larger community and environment (Kim, Citation2022).

The last theory considered in this study is legitimacy theory. Suchman (1995) defines legitimacy as the widespread perception or presumption that the actions of an entity are desirable, proper, or appropriate within a socially constructed system of norms, values, beliefs, and definitions. The legitimacy theory is a mechanism that assists organizations in implementing and developing voluntary social and environmental disclosures in order to fulfill their social contract, which enables the recognition of their goals and survival in a volatile and unstable environment. Legitimacy theory is founded on the social contract between an organization and the society in which it operates. Organizations strive to be legitimate by operating within the boundaries and norms of their respective societies (Khan, Muttakin, & Siddiqui, Citation2013); therefore, socially responsible behavior is essential for corporations. To maintain their legitimacy, businesses must adhere to societal values by engaging in corporate social responsibility activities. In this regard, firms’ long-term viability is not jeopardized if their actions are beneficial to society. Moreover, Laan (2009) suggested that a legitimacy disparity will result when the expectations of stakeholders and corporate performance do not align. In order to minimize the impact of these entities, it is crucial that the legitimacy gap be addressed. The legitimacy divide can be addressed in a number of ways, including through legitimacy strategies such as CSR disclosures As firms wish to be perceived as legitimate entities, disclosures serve as an effective communication tool for promoting improved CSR practices. Moreover, corporations engage in CSR reporting because they need society’s approval to be sustainable. By engaging in CSR activities, companies demonstrate that they are sincere about mitigating the negative effects of their business operations while simultaneously portraying their efforts as legitimate to society (Janang, Joseph, and Said, Citation2020).

CG-CSR is a multidisciplinary construct; thus, the use of theoretical pluralism can assist in comprehending how and under what circumstances CG-CSR is influenced and implemented. This is especially significant because unexplored institutional contexts are likely to be significantly different, necessitating the exploration of new, nuanced, and multiple theoretical paradigms to explain and comprehend the complex CG-CSR interfaces (Crane et al., 2016; Zaman et al., Citation2022). The study draws insight from the upper echelon, stakeholder, and legitimacy theories to establish a dynamic relationship between CG, CSR, corporate image, and firm performance, as demonstrated in Figure .

Figure 1. The conceptual framework .

4. Empirical literature review and hypotheses development

4.1. Corporate governance and corporate social responsibility

Corporate governance and corporate social responsibility are inextricably linked (Ntim & Soobaroyen, Citation2013; Zaman et al., Citation2021). On the one hand, corporate governance is viewed as the foundation of CSR (Ntim & Soobaroyen, Citation2013; Jamali et al., Citation2008; Filatotchev & Stahl, Citation2015). In line with this, the configurations of a company’s CG structures have a substantial impact on the company’s CSR intentions and potential (Ntim & Soobaroyen, Citation2013; Jain and Jamali, Citation2016; Gul et al., Citation2017). Companies with robust CG strategies are more likely to engage in CSR initiatives (Zaman et al., Citation2020; Zaid et al., Citation2019; Jahid et al., Citation2020; Zaman et al., Citation2022). Consequently, a robust CG process is the foundation of a successful CSR implementation. This position is supported by the upper echelon theory, which asserts that the characteristics of senior managers have a significant impact on the firm’s strategic decisions and outcomes, including CSR (Hambrick & Mason, Citation1984; Hambrick, Citation2007; Chatterjee & Hambrick, Citation2011). Board characteristics play a significant role in explaining CSR activities. Participation in CSR would be correlated with more efficient CG systems. The adoption of CSR activities is encouraged by CG mechanisms such as firm ownership structures, board monitoring, etc. Consequently, the potential of CG extends beyond maximizing shareholder value and assuring accountability to creating responsibility and establishing relationships with multiple stakeholders, including employees, investors, and society. For example, there is a significant relationship between CEO age and CSR initiatives, tenure and CSR implementation, board gender diversity, board CSR committee, board expertise, and board independence all correlating positively with CSR. The concept of the upper echelon theory may explain how the CG-CSR relationship may be influenced by managerial principles, discretion, power, and ideology in diverse institutional settings (Zaman et al., Citation2022). In effect, executives, particularly in Ghana, adopt CSR as a strategy to satisfy the expectations of stakeholders in order to potentially ensure the business’s long-term success.

Furthermore, CSR is gradually being integrated or fused into corporate governance processes. In line with this, both CSR and CG are concerned with an organization’s ethics and how it interacts with its stakeholders and also emphasize the importance of transparency, disclosure, sustainability, and ethical behavior (Hossain et al., Citation2016; Deev & Khazalia, Citation2017; Jahid et al., Citation2020). Moreover, CSR is founded on the concept of self-governance, which is linked to external legal and regulatory frameworks, whereas corporate governance is the broadest control mechanism through which a corporation makes management decisions (Hossain et al., Citation2016; Zaid et al., Citation2019). Good governance entails accountability and consideration for the wishes of all significant stakeholders, as well as ensuring that corporations are accountable to all stakeholders (Jamali, Citation2008; Jo and Ho, 2011; Ledi et al., Citation2022). As a result, there is considerable overlap between this concept of CG and the stakeholder perspective on CSR, which views businesses as being accountable for a complex web of interconnected stakeholders who support and add value to the business (Jamali, Citation2008; Deev & Khazalia, Citation2017; Zaid et al., Citation2019), leading to the conclusion that CG is considered a critical component of long-term CSR. This viewpoint is supported by stakeholder theory, which states that managers should pursue goals that promote the firm’s long-term value by protecting the interests of all stakeholders by establishing responsibility and accountability for the impact of corporate actions on the larger community and environment (Zhang et al., Citation2022; Donaldson and Preston, Citation1995).

The last piece considers CG and CSR to coexist. In this case, CG and CSR are neither the same nor distinct, but rather connected concepts. According to this line of thinking, CG and CSR should be seen as two ends of the same accountability spectrum (Amoako, Citation2017). Accordingly, a company’s dedication to society and the environment does not take the place of CG standards and policies; rather, they coexist. Coexisting, CG places an emphasis on CSR, which places a greater emphasis on the firm’s self-regulation and its commitment to stakeholders than external compliance (Zaman et al., Citation2020). Thus the study proposed that:

H1:

Corporate Governance has a significant positive relationship with CSR

4.2. Corporate governance and firm performance

One reason for a company’s poor performance is a conflict of interest. According to agency theory, managers in today’s organizations behave in their personal best interests instead of shareholders’ best interests (Khanifah et al., Citation2020). As a result, the CG principle must be applied. Corporate governance balances managers’ and stakeholders’ interests to reduce agency conflict (Ali et al., Citation2022; Naz et al., Citation2022; Ahmed et al., Citation2020). Thus, an institution’s governing bodies represent the interests of various stakeholders (Donaldson and Preston, Citation1995; Freeman, 1984). Stakeholder theory also admonishes board members, for instance, to be enthused or motivated to possibly act in the principals’ best interests and possibly make decisions that benefit the entire organization when different stakeholders have competing goals (Frederick et al., 1992; Freeman, 1984; Binh & Hoang, Citation2018; Khanifah et al., Citation2020; Muntahanah et al., Citation2021). This suggests that corporate governance should strive to strike a balance among its various stakeholders.

With CG, organizations can accomplish stated goals or perform well within the industry while also satisfying the needs of other stakeholders. Several studies have found that outstanding corporate governance (CG) has a substantial impact on firm performance (Amaoko & Goh, 2015; Adams & Mehran, 2016; Mertzanisa et al., Citation2019; Mardnly, Mouselli, and Abdulraouf, 2019; Khanifah et al., Citation2020; Ahmed et al., Citation2020; Muntahanah et al., Citation2021). Specifically, there is a significant positive relationship between non-executive directors and business performance, board independence and business performance (Sarpong-Danquah et al., Citation2018; Boachie, Citation2021), board size and business performance. However, despite the seemingly overreaching positive relationship between CG and firm performance, other research has cast doubt on the positive relationship between corporate governance and firm performance (Al-Ghamdi & Rhodes, Citation2015; Narwal & Jindal, Citation2015;). This shows that the results of these findings are largely inconclusive and in essence unexhaustive, opening windows for further studies. The study postulates that:

H2:

Corporate Governance has a positive and significant effect on firm performance

4.3. The effect of corporate social responsibility and firm performance

Legitimacy theory is based on the concept of a social contract, in which an organization uses legitimization tools, such as CSR reports and disclosures , to communicate to its internal and external stakeholders its conformance within a socially constructed system of norms, values, and beliefs (Khan et al.,Citation2013; Janang et al., Citation2020). Consequently, CSR is driven by both institutional pressures for conformity to national, industry, or professional norms and regulations (institutional theory) and a desire to obtain a social license to operate by engaging with and meeting the expectations of internal and external stakeholders (Zaman et al., Citation2022; Singh & Misra, Citation2021). CSR improves performance by strengthening ties with important stakeholders. Additionally, the willingness to invest in CSR demonstrates that it can be a source of competitive advantage rather than just a cost, a constraint, or the right thing to do (Jamali et al., Citation2008; Lee et al., Citation2017 Kong et al., Citation2020). Businesses that are successful in satisfying their stakeholders gain a competitive edge (Kong et al., Citation2020; Zhang et al., Citation2022; Kim, Citation2022). More so, a growing body of evidence indicates that CSR may enhance innovation, employee satisfaction, save environmental costs, and generally create favorable perceptions of the company (Jamali et al., Citation2008; Alamgir & Uddin, Citation2017). Again, when a business is confronted with a serious crisis, CSR can help them rebuild their reputation (Janney & Gove, Citation2011; Singh & Misra, Citation2021). Businesses are required to generate revenue by creating jobs and providing higher-quality goods and services. A safer workplace and respect for employees’ human rights result in increased production and improved business performance (Jamali et al., Citation2008). Similarly, when a business’s social responsibilities are appropriately communicated and meet the expectations of its stakeholders, the actions result in value creation and a positive impact on the business’s success (Alamgir & Uddin, Citation2017; Kong et al., Citation2020; Kim, Citation2022; Ali et al., Citation2020). Thus the study proposed that:

H3:

Corporate Social Responsibility has a positive and significant effect on firm performance

4.4. The effect of corporate image on firm performance

Every organization places a premium on the company’s image, particularly the perceptions of key stakeholders. The stakeholder theory posits that managers in organizations have a network of relationships to serve, including employees, shareholders, suppliers, business partners, and contractors (FDonaldson and Preston, Citation1995), and that representation of various interest groups on the organization’s board is essential for consensus building, avoiding conflicts, and coordinating efforts to achieve organizational objectives (Zhang et al., Citation2022; Donaldson and Preston, Citation1995). Therefore, it is prudent for firms, especially manufacturing firms, to maintain an inherent and positive image among stakeholders. Therefore, company image and firm performance are significantly associated (Hsu, Citation2018; Lee et al., Citation2017). Corporate image aids in the achievement of organizational goals. A good company image is particularly significant because of its potential for wealth creation and intangible traits that make reproduction or imitation by other organizations more difficult (Caliskan et al., Citation2011; Hossain et al., Citation2016; Kyurova & Yaneva, Citation2017; Jamali et al., Citation2008). A positive corporate image affords businesses distinctive characteristics that enhance brand recognition, consumer and employee loyalty, and corporate reputation (Jamali et al., Citation2008; Platonova et al., Citation2018). Corporate image endows businesses with distinctive characteristics that help increase brand awareness, enhance sales, increase employee loyalty, and increase consumer loyalty, as well as attract new investors (Hossain et al., Citation2016; Mukhibad et al., Citation2017; Hsu, Citation2018).

Corporate image also plays a critical role in increasing firm performance by attracting more customers. More so, corporate image fosters consumer confidence or trust and deters competitors from entering the market. This demonstrates that an organization’s image can significantly enhance organizational performance (Mukhibad et al., Citation2017; Kyurova & Yaneva, Citation2017; Ikon & Chika, Citation2019).

Every organization places a premium on the company’s image, particularly the perceptions of key stakeholders. The stakeholder theory posits that managers in organizations have a network of relationships to serve, including employees, shareholders, suppliers, business partners, and contractors (Donaldson and Preston, Citation1995), and that representation of various interest groups on the organization’s board is essential for consensus building, avoiding conflicts, and coordinating efforts to achieve organizational objectives (Zhang et al., Citation2022; Donaldson and Preston, Citation1995). Therefore, it is prudent for firms, especially manufacturing firms, to maintain an inherent and positive image among stakeholders. Therefore, company image and firm performance are significantly associated (Hsu, Citation2018; Lee et al., Citation2017; Khater, 2019). Corporate image aids in the achievement of organizational goals. A good company image is particularly significant because of its potential for wealth creation and intangible traits that make reproduction or imitation by other organizations more difficult (Caliskan et al., Citation2011; Hossain et al., Citation2016; Kyurova & Yaneva, Citation2017; Jamali et al., Citation2008). A positive corporate image affords businesses distinctive characteristics that enhance brand recognition, consumer and employee loyalty, and corporate reputation. (Jamali et al., Citation2008; Platonova et al., Citation2018). Corporate image endows businesses with distinctive characteristics that help increase brand awareness, enhance sales, increase employee loyalty, and increase consumer loyalty, as well as attract new investors (Hossain et al., Citation2016; Mukhibad et al., Citation2017). Corporate image also plays a critical role in increasing firm performance by attracting more customers. More so, corporate image fosters consumer confidence or trust and deters competitors from entering the market. This demonstrates that an organization’s image can significantly enhance organizational performance (Mukhibad et al., Citation2017; Kyurova & Yaneva, Citation2017; Ikon & Chika, Citation2019).Thus the study postulates that:

H4:

Corporate image has a positive and significant effect on firm performance

4.5. The mediating role of corporate image on the relationship between corporate governance and firm performance

Every organization places a premium on the company’s image, particularly the perceptions of key stakeholders. The stakeholder theory posits that managers in organizations have a network of relationships to serve, including employees, shareholders, suppliers, business partners, and contractors (Donaldson and Preston, Citation1995), and that representation of various interest groups on the organization’s board is essential for consensus building, avoiding conflicts, and coordinating efforts to achieve organizational objectives (Zhang et al., Citation2022; Donaldson and Preston, Citation1995). Therefore, it is prudent for firms, especially manufacturing firms, to maintain an inherent and positive image among stakeholders. This can be achieve with quality corporate governance system.

Company image and firm performance are significantly associated (Hsu, Citation2018; Lee et al., Citation2017). Corporate image aids in the achievement of organizational goals. A good company image is particularly significant because of its potential for wealth creation and intangible traits that make reproduction or imitation by other organizations more difficult (Caliskan et al., Citation2011; Hossain et al., Citation2016; Kyurova & Yaneva, Citation2017; Jamali et al., Citation2008). A positive corporate image affords businesses distinctive characteristics that enhance brand recognition, consumer and employee loyalty, and corporate reputation (Jamali et al., Citation2008; Platonova et al., Citation2018). Corporate image endows businesses with distinctive characteristics that help increase brand awareness, enhance sales, increase employee loyalty, and increase consumer loyalty, as well as attract new investors (Hossain et al., Citation2016; Mukhibad et al., Citation2017). Corporate image also plays a critical role in increasing firm performance by attracting more customers. More so, corporate image fosters consumer confidence or trust and deters competitors from entering the market. This demonstrates that an organization’s image can significantly enhance organizational performance especially when this is situated in the context of solid corporate governance practices (Mukhibad et al., Citation2017; Kyurova & Yaneva, Citation2017; Swati and Archana, 2018; Ikon & Chika, Citation2019; Khanifah et al., Citation2020). Thus, the study postulates that:

H5:

Corporate image mediates corporate governance and firm performance link

4.6. The mediating role of corporate image on the relationship between corporate social responsibility and firm performance

CSR may have a favorable effect on a firm’s image (Maruf, Citation2013; Hakimi et al., Citation2016; Alamgir & Uddin, Citation2017; Hafiz et al., 2019). Thus, it appears that the consequences of CSR implementation have a beneficial impact on corporate image (Esmaeilpour & Barjoei, Citation2016; Hsu, Citation2018; Lee et al., Citation2017). CSR will have external consequences for brand image, resulting in a good impression of a business brand. CSR increased organizational performance and improved business brand image (Alamgir & Uddin,Citation2017). Therefore, CSR positively affects brand performance (Lai et al., Citation2010; Lee et al., Citation2017). Socially responsible activities enhance both the brand image of a company’s products and its overall image (Hakimi et al., Citation2016). CSR initiates the corporate image development process and has an impact on company success (Arendt & Brettel, Citation2010; Hakimi et al., Citation2016; Lee et al., Citation2017). CSR is a great approach for improving a firm’s competitive advantage via the construction of a sound public image, as well as for improving the firm’s competitive advantage through the creation of a sound public image and ultimately influencing a company’s performance. A company’s success is greatly influenced by its image, which is built through corporate social responsibility. CSR thus has a significant indirect effect on firm performance through corporate image (Alamgir & Uddin, Citation2017; Lee et al., Citation2017; Olaroyeke and Nasieku, 2015; Hsu , Citation2018; Hakimi et al., Citation2016; Hossain et al., Citation2016). The study therefore suggest that:

H6:

Corporate image mediates corporate social responsibility and firm performance link

5. Research design

5.1. Sample and data collection

The quantitative approach was utilized to acquire data from study participants. The study’s population was made up of selected manufacturing firms in Ghana. The purposive sampling technique was appropriate for selecting specific respondents who are top executives with relevant knowledge and the power to make strategic decisions for the firms. The estimated population of active manufacturing firms was 5000. Using the Cochran (1977) formula, the estimated ideal sample size was three hundred and fifty-seven (357). However, the study sent four hundred (400) questionnaires to the sampled firms from the Association of Ghana Industries (AGI). The questionnaires were distributed to the respondents via email, with each respondent instructed to fill out the questionnaire and return it. Each company was called as a reminder to encourage a valid total response rate. The process lasted for a span of 5 months and 3 weeks. Three hundred and fifty-seven (357) firms participated in the study, representing an 89 percent effective response rate. However, 328 questionnaires were eventually considered for the study after a preliminary check for completeness. The sampling procedure is presented in the Table .

Table 1. Sampling procedure

5.2. Measure

5.2.1. Independent variables

CG and CSR are well-known concepts with no universally accepted definition in the literature. Corporate governance is considered a set of procedures and rules that direct and control companies. Corporate governance is an institutional, legal, and cultural framework that is more or less country-specific and shapes the patterns of shareholder (or stakeholder) influence on managerial decision-making (Mertzanisa et al., Citation2019). The study adopted eight (8) composite items measuring corporate governance from Jamali et al. (Citation2008). Jamali et al. (Citation2008), for instance, were deemed fit for this study because the eight (8) items cover almost all aspects of corporate governance.

CSR, on the other hand, is a set of business perspectives and ideas that proponents hope to see broadly implemented in the corporate sector (Dartey-Baah & Amoako, Citation2021; Jamali et al., Citation2008). Thus, CSR is businesses’ commitment to add to or contribute to stakeholder interests and ameliorate societal conditions as well as sustainable development. The study thus adopted eight (8) items measuring corporate social responsibility using Carroll’s (Citation1991) conceptualisations.

5.2.2. Dependent variable

Organisational performance refers to indicators that measure how well an organisation accomplishes its objectives. The eight (8) items measuring firm performance were adapted from Yu and Huo (Citation2021).

5.2.3. Mediating variable

Corporate image refers to a state of mind that stakeholders have about a company, or business, or entity. This state is further referred to as the mental picture that the stakeholders have in relation to the way they perceive a company. A corporate image is designed to be appealing to the public so that the company can spark interest among consumers, create share of mind, generate brand equity, and thus facilitate product sales (Obasan, Citation2012). The eight (8) items measuring corporate image were adopted from Lai et al. (Citation2010) and Hsu (Citation2018). All constructs in the study were anchored on a seven-point Likert scale.

5.3. Data processing and analysis

The data was analyzed using AMOS version 23 and SPSS version 25. A Confirmatory factor analysis was conducted to test the suitability of the model. The hypothesis path was tested using Andy Hayes’ Process Macro. Alternatively, Ordinary Least Squares (OLS), Logit regression, or Structural Equation Modelling (SEM) analysis could be used to conduct CG-CSR research.

6. Empirical results and discussion

6.1. Reliability and validity

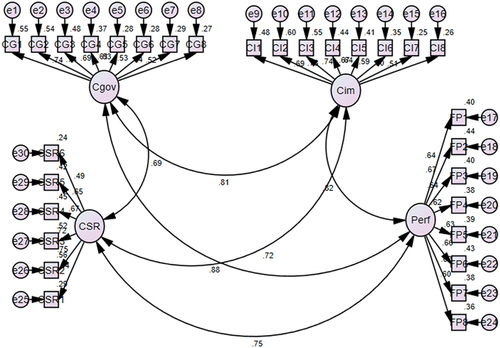

The Confirmatory Factor Analysis (CFA) in Amos was used to determine the fitness model using maximum likelihood, which was conducted on all the constructs of the study. Each construct’s factor loadings against its variables should be greater than or equal to the .50 criterion (Hair et al., 2014). According to this criterion, CFA analysis was omitted for measurement items with a loading of less than 0.5 (2 items were eliminated from CSR). The rest of the items have loaded above the .50 criterion as demonstrated in Table and Figure . Additionally, the study examined the measurement items’ reliability. Internal consistency requires an alpha score of at least 0.7 (Hair et al., 2014). From Table , all four (4) constructs have alpha coefficients above the recommended threshold of .70 (.798 to .846) demonstrating the reliability of the constructs. Additionally, the convergence validity of the constructs was determined by examining the AVE. Convergence validity requires an AVE threshold of 0.5. (Fornell & Larcker, Citation1981). The study thus demonstrated both internal and convergence validity. Items used to measure each construct in Table are provided in Appendix 1.

Figure 2. The CFA model.

Table 2. Reliability and Validity

6.2. Discriminant validity

The Fornell-Larcker criterion was used to test the discriminant validity. By contrasting the square roots of the AVEs with the intercorrelation scores, the study assesses the AVEs’ discriminant validity. Discriminant validity occurs when the square root of the AVE is larger than the coefficient of correlation with any other construct (Fornell & Larcker, Citation1981). From Table , the lowest AVE value of .888 was higher than the highest correlation score of .674, demonstrating discriminant validity.

Table 3. Discriminant validity

CG = corporate governance, CI = Corporate image, CSR = Corporate Social Responsibility, and FP = Firm performance

6.3. Normality and multicollinearity test

The study conducted normality and multicollinearity tests, and the outcomes are presented in Table . The normality test of the study demonstrated that the constructs are normally distributed. The absolute values of booth Skewness and Kurtosis were less than the acceptable thresholds of 2 and 4, respectively (Kline, 2011). The study presents multicollinearity tests in two folds. First, the highest Pearson correlation coefficient among the constructs in Table is .737 which is less than the critical collinearity value of .90. The second approach is done by analysing the correlation between variables using the tolerance value and variance inflation factor (VIF). There is the presence of multicollinearity if the VIF values are above 10 (Kalnins, Citation2018; Tay, Citation2017). From Table , all the VIF are below the acceptable threshold, indicating that there is no presence of multicollinearity issues.

Table 4. Normality and multicollinearity test

6.4. Hypothesis testing

The hypothesis path was tested using Andy Hayes’ Process Macro. The result of the direct path is presented in Table . The study found that there is a significant positive relationship between corporate governance and corporate social responsibility (β = .459; t = 12.319, p 0.05), which is in line with H1. The study further found that there is a positive and significant effect of corporate governance on the performance of manufacturing firms (β = .518; t = 10.373, p

0.05), supporting H2. The study found that there is a positive and significant effect of corporate social responsibility on the performance of manufacturing firms (β = .461; t = 7.618, p

0.05), supporting H3. The study also found that there is a positive and significant effect of corporate image on the performance of manufacturing firms (β = .407; t = 8.415, p

0.05), supporting H4. The study also found that corporate governance (β = .694; t = 16.434, p

0.05) and corporate social responsibility (β = .765; t = 13.713, p

0.05) positively influence corporate image respectively.

Table 5. Direct Path

CG = corporate governance, CI = Corporate image, CSR = Corporate Social Responsibility, and FP = Firm performance

The study further assessed the indirect effect of corporate governance and corporate social responsibility on firm performance via corporate image and the outcome is presented in Table . From Table , the study found that corporate image mediates the relationship between corporate governance and firm performance (β = .283, .1956–.3715), thus supporting H5. The study again found that corporate image mediates the relationship between corporate social responsibility and firm performance (β = .412, .2953–.5176) thus supporting H6.

Table 6. Indirect Path

7. Discussion

Corporate governance and firm performance link, as well as CSR and firm performance link, have developed into research focus areas for both academia and industry practitioners over the years. However, previous research on both links have yielded conflicting results, necessitating further investigation. The study examined the mediating role of corporate image in corporate governance and firm performance nexus as well as CSR and firm performance nexus. Firstly, the study found that there is a significant positive relationship between corporate governance and corporate social responsibility initiatives. This finding is consistent with the findings of other studies (Jamali et al., Citation2008; Ntim & Soobaroyen, Citation2013; Gul et al., Citation2017; Deev & Khazalia, Citation2017; Zaid et al., Citation2019; Jahid et al., Citation2020; Zaman et al., Citation2022; Ledi et al., Citation2022). Thus, a solid CG process serves as the cornerstone of a successful CSR implementation. This position is supported by the upper echelon theory, which echoes that there is a significant impact of top managers’ characteristics on the firm’s strategic choices and outcomes, such as CSR (Hambrick & Mason, Citation1984; Hambrick, Citation2007; Chatterjee & Hambrick, Citation2011). Board characteristics therefore play an important role in explaining the CSR activities of manufacturing firms, as postulated by the upper echelons theory. Secondly, the study found that corporate governance has a significant positive effect on the performance of manufacturing firms. This is quite consistent with existing studies that found similar conclusions (Ali et al., Citation2022; Ahmed et al., Citation2020; Almashhadani & Almashhadani, Citation2022; Ganda, Citation2022; Naz et al., Citation2022). This pinpoints the fact that the CG principle is a kernel ingredient to success in business and must be applied religiously and holistically. Corporate governance balances managers’ and stakeholders’ interests to reduce agency conflict and represent the interests of various stakeholders (Donaldson and Preston, Citation1995). Stakeholder theory also admonishes board members, for instance, to be enthused or motivated to possibly act in the principals’ best interests and possibly make decisions that benefit the entire organization when different stakeholders have competing goals (Ali et al., Citation2022; Nugroho, Citation2021; Muntahanah et al., Citation2021). Corporate governance therefore strikes a balance between its various stakeholders.

Third, the study again found that corporate social responsibility has a positive effect on the performance of manufacturing firms. This finding is consistent with other studies with similar outcomes (Combs et al., Citation2023; Ali et al., Citation2020; Javeed & Lefen, Citation2019; Lu et al., Citation2020; Singh & Misra, Citation2021). Legitimacy theory is based on the concept of a social contract, in which an organization intentionally employs legitimization tools, such as CSR reports and disclosures (Khan et al., Citation2013), to communicate its conformance within a socially constructed system of norms, values, and beliefs to its internal and external stakeholders (Janang et al., Citation2020). Manufacturing companies disclosing information on social responsibility will present a socially responsible image that can be used as a leverage to achieve stellar business performance. this is because, CSR enhances performance by fortifying ties with key stakeholders (Lee et al., Citation2017; Kim Citation2022). Fourth, the study found that corporate image has a positive effect on the performance of manufacturing firms. This finding is equally in line with other studies (Hossain et al., Citation2016; Alamgir & Uddin, Citation2017; Setiawan & Sayuti, Citation2017; Mukhibad et al., Citation2017; Kyurova & Yaneva, Citation2017; Swati and Archana, 2018; Platonova et al., Citation2018; Ikon & Chika, Citation2019; Khanifah et al., Citation2020). All organizations place a high value on the image of the firm, especially the perceptions of key stakeholders, which can lead to improvements in firm performance (Hsu, Citation2018; Lee et al., Citation2017). According to the stakeholder theory, managers in organizations have a network of relationships to serve (Donaldson and Preston, Citation1995), and representation of various interest groups on the organization’s board is essential to ensure consensus building, conflict avoidance, and harmonization of efforts to achieve organizational objectives (Donaldson and Preston, Citation1995; Zhang et al., Citation2022). Therefore, manufacturing firms prudently maintaining an inherent and positive image among stakeholders will lead to significant firm performance.

Lastly, the study found that corporate image mediates corporate governance as well as the CSR and firm performance nexus. The study concludes that CG and CSR synergistically influence firm performance through corporate image. Corporate governance and CSR better enhance improve firm performance (Ntim & Soobaroyen, Citation2013) via corporate image. The findings doubled in confirming stakeholder theory to support the notion that corporate governance and CSR influence performance by building and establishing a firm’s image.

8. Summary and conclusion

Corporate governance has emerged as an issue in emerging economies and has become critical for strengthening firm performance, enhancing the investment climate, and stimulating economic growth. Consequently, sound corporate governance has become a critical success factor for firms. Additionally, CSR has become a prominent element of business interactions, driving numerous worldwide discourses, and has grown increasingly relevant in today’s corporate practices and academic research. Drawing from the theoretical pluralism of upper echelon theory, stakeholder theory, and legitimacy theory, the study confirmed that good corporate governance practices, social engagement, and corporate image collectively enhance the performance of manufacturing firms in Ghana. This finding is consistent with the stakeholder theory, which postulates that rendering social responsibility creates value for the firm. Thus, in the quest to meet the interests of various parties, the firm will maintain a better perception among stakeholders, which will have a ripple effect on its performance.

Furthermore, corporate social responsibility is advantageous to manufacturing firms as it gives a company a competitive edge and ultimately improves corporate image, especially when it is legitimized. In line with this, firms should be more proactive in leading the CSR engagement race since social investment helps in crafting and shaping a sound image and enhances firm performance. Similarly, CSR efforts have a positive relationship with a firm’s governance, as CSR efforts and corporate governance aid firms in improving their performance. As a result, corporate social responsibility (CSR) should not be seen as an optional or voluntary action but as an integral strategy that could contribute substantially to the success of an organization and simultaneously improve society. CG systems facilitates the implementation of CSR projects. Therefore companies with high-quality CG systems and practices are more likely to pursue CSR initiatives that have a beneficial impact on business performance. This is particularly the case when particular attention is paid to the CG structures since they strongly shape CSR initiatives, as suggested by the Upper Echelon Theory that top management team (TMT) influences organizational strategy and outcome. Consequently, constituting a quality CG system influences their ability to engage in social investment, which may enhance the firm’s image, obtain a competitive advantage, and eventually boost organizational performance. Thus, comprehensively and systematically constituting quality CG systems and practices could catalyze and sustain CSR initiatives.

With regards to policymaking, CSR has generally not been well grounded in Ghana. There are no comprehensive and enforceable CSR laws in Ghana, making CSR a completely voluntary service despite the consequences of the operation of these firms on the community and the environment as a whole. It is therefore timely to pursue policy and clear-cut laws pertaining to CSR, looking at the favorable relationship it has with corporate governance, firm image, and performance. The CSR legal framework could constructively boost the commitment of managers to social investment.

Consequently, this paper aims to contribute the following to the existing literature: Firstly, in a developing economy like Ghana, previous studies significantly ignored corporate social responsibility and corporate governance interaction as the two concepts are investigated separately (Sarpong Danquah et al., Citation2022; Musah & Adutwumwaa, Citation2021; Dartey-Baah & Amoako, Citation2021; Nyarku & Ayekple, Citation2019; Sarpong-Danquah et al., Citation2018). Therefore, there is a lack of consensus on how corporate governance and CSR relationships manifest across different institutional contexts, especially within emerging economies, despite the wealth of available studies on the two concepts. The study helps advance knowledge on the internal antecedents of CSR by revealing that CG sets the fundamental tone for a firm’s CSR performance. Hence, practitioners and policymakers who want to advance CSR should fortify the CG system and practices since the CG system has a massive tendency to curtail or catalyze CSR. Secondly, the study also makes a significant contribution to understanding the antecedents and models influencing firm performance. The study has demonstrated how CG and CSR collectively affect firm performance, both directly and indirectly, by establishing the role of corporate image as a mediator. Third, the study provides a comprehensive understanding of how manufacturing firms in Ghana, which have received negligible attention in the Ghanaian literature, can improve their performance by suitably constituting CG systems and fostering CSR performance to achieve a stellar corporate image, which ultimately leads to improved firm performance. Lastly, this study adds nuances to extant theoretical literature by employing theoretical pluralism to explain the intricacies of the CG and CSR interface and ultimately offering richer insight into the CG and CSR puzzles within the context of the emerging economy.

The conceptualisation and measurement of both corporate governance and corporate social responsibility have attracted considerable debate. In line with this, there are several mechanisms for measuring corporate governance (e.g., Jamali et al., Citation2008), as well as several conceptualisations or dimensions for measuring corporate social responsibility (e.g., Carroll, Citation1991), but this study employed composite or integrated variables for both corporate governance and CSR instead of examining the respective influence of various dimensions on firm performance. For this reason, further study could employ the CG rating index or the various mechanisms of CG. Further studies should look at internal CSR in relation to employee performance or organizational performance, as internal CSR has received relatively less attention in the Ghanaian literature. In addition, institutional elements and legal reforms that could strengthen or weaken the connection between CG and CSR were not taken into account in this investigation. Additionally, further studies could examine the moderating role of managerial commitment in CSR and the firm performance nexus, as managerial involvement and commitment to CSR in developing nations such as Ghana are relatively low.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

Conflict of interest: No conflict of interest

Additional information

Funding

References

- Abdullah, H., & Tursoy, T. (2023). The effect of corporate governance on financial performance: Evidence from a shareholder-oriented system. Iranian Journal of Management Studies, 16(1), 79–23.

- Adegbite, G. (2012). Corporate governance developments in Ghana: The past, the present and the future. Public and Municipal Finance, 1(2), 38–49.

- Agyemang, O. S., & Castellini, M. (2013). The guidelines of corporate governance of Ghana: Issues, deficiencies and suggestions. International Business Research, 6(10), 163. https://doi.org/10.5539/ibr.v6n10p163

- Ahmed, E. R. A., Tariq, T. Y. A., Mohammed, M. T., & Eny, M. (2020). Does corporate governance predict firm profitability? An empirical study in Oman. The International Journal of Accounting and Business Society, 28(1), 161–177. https://doi.org/10.21776/ub.ijabs.2020.28.1.7

- Alamgir, M., & Nasir Uddin, M. (2017). The mediating role of corporate image on the relationship between corporate social responsibility and firm performance: An empirical study. International Journal of Business and Development Studies, 9(1), 91–111.

- Al-Ghamdi, M., & Rhodes, M. (2015). Family ownership, corporate governance and performance: Evidence from Saudi Arabia. International Journal of Economics and Finance, 7(2), 78–89. https://doi.org/10.5539/ijef.v7n2p78

- Ali, A., Alim, W., Ahmed, J., & Nisar, S. (2022). Yoke of corporate governance and firm performance: A study of listed firms in Pakistan. Indian Journal of Commerce and Management Studies, 13(1), 8–17. https://doi.org/10.18843/ijcms/v13i1/02

- Ali, H. Y., Danish, R. Q., & Asrar‐ul‐haq, M. (2020). How corporate social responsibility boosts firm financial performance: The mediating role of corporate image and customer satisfaction. Corporate Social Responsibility and Environmental Management, 27(1), 166–177. https://doi.org/10.1002/csr.1781

- Ali, R., Sial, M. S., Brugni, T. V., Hwang, J., Khuong, N. V., & Khanh, T. H. T. (2019). Does CSR moderate the relationship between corporate governance and Chinese firm’s financial performance? Evidence from the Shanghai Stock Exchange (SSE) firms. Sustainability, 12(1), 149. https://doi.org/10.3390/su12010149

- Almashhadani, M., & Almashhadani, A. A. (2022). Corporation performance and corporate governance system: An argument. International Journal of Business and Management Invention, 11(2), 13–18.

- Amoako, G. K. (2017). Relationship between corporate social responsibility (CSR) and corporate governance (CG): The case of some selected companies in Ghana. Responsible Corporate Governance: Towards Sustainable and Effective Governance Structures, 151–174.

- Arendt, S., & Brettel, M. (2010). Understanding the influence of corporate social responsibility on corporate identity, image, and firm performance. Management Decision.

- Arevalo, J. A., & Aravind, D. (2017). Strategic outcomes in voluntary CSR: Reporting economic and reputational benefits in principles-based initiatives. Journal of Business Ethics, 144, 201–217.

- Banahene, K. O. (2018). Ghana banking system failure: The need for restoration of public trust and confidence. International Journal of Business and Social Research, 8(10), 1–5.

- Binh, T. T. D., & Hoang, A. N. (2018). Impact of corporate governance on firm performance and earnings management a study on Vietnamese nonfinancial companies. Asian Economic and Financial Review, 10(5), 480–501. https://doi.org/10.18488/journal.aefr.2020.105.480.501

- Boachie, C., & Tetteh, J. E. (2021). Do creditors value corporate social responsibility disclosure? Evidence from Ghana. International Journal of Ethics and Systems, 37(3), 466–485.

- Caliskan, E., Icke, B., & Ayturk, Y. (2011). Corporate reputation and financial performance: Evidence from Turkey. Research Journal of International Studies, 18(1), 61–72.

- Carroll, A. B. (1991). The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Business Horizons, 34(4), 39–48. https://doi.org/10.1016/0007-6813(91)90005-G

- Chatterjee, A., & Hambrick, D. C. (2011). Executive personality, capability cues, and risk taking: How narcissistic CEOs react to their successes and stumbles. Administrative Science Quarterly, 56(2), 202–237.

- Combs, J. G., Jaskiewicz, P., Ravi, R., & Walls, J. L. (2023). More bang for their buck: Why (and when) family firms better leverage corporate social responsibility. Journal of Management, 49(2), 575–605. https://doi.org/10.1177/01492063211066057

- Dartey-Baah, K., & Amoako, G. K. (2021). A review of empirical research on corporate social responsibility in emerging economies. International Journal of Emerging Markets, 16(7), 1330–1347. https://doi.org/10.1108/IJOEM-12-2019-1062

- Deev, O., & Khazalia, N. (2017). Corporate governance, social responsibility and financial performance of European insurers. Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis, 65(6), 1873–1888. https://doi.org/10.11118/actaun201765061873

- Donaldson, T., & Preston, L. E. (1995). The stakeholder theory of the corporation: Concepts, evidence, and implications. Academy of Management Review, 20(1), 65–91.

- Doshmanli, M., Salamzadeh, Y., & Salamzadeh, A. (2018). Development of SMEs in an emerging economy: Does corporate social responsibility matter?. International Journal of Management and Enterprise Development, 17(2), 168–191.

- Driel, H. (2019). Financial fraud, scandals, and regulation: A conceptual framework and literature review. Journal Business History, 61(8), 1259–1299. https://doi.org/10.1080/00076791.2018.1519026

- Eberlein, B., Abbott, K. W., Black, J., Meidinger, E., & Wood, S. (2014). Transnational business governance interactions: Conceptualization and framework for analysis. Regulation & governance, 8(1), 1–21.

- Esmaeilpour, M., & Barjoei, S. (2016). The impact of corporate social responsibility and image on brand equity. Global Business & Management Research, 8(3), 55.

- Filatotchev, I., & Stahl, G. K. (2015). Towards transnational CSR. Corporate social responsibility approaches and governance solutions for multinational corporations. Organizational Dynamics, 44(2), 121–129.

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Francis Antwi, I., Carvalho, C., & Carmo, C. (2022). Corporate Governance research in Ghana through bibliometric method: Review of existing literature. Cogent Business & Management, 9(1), 2088457. https://doi.org/10.1080/23311975.2022.2088457

- Frynas, J. G. (2010). Corporate social responsibility and societal governance: Lessons from transparency in the oil and gas sector. Journal of Business Ethics, 93, 163–179.

- Ganda, F. (2022). The impact of corporate governance on corporate financial performance: cases from listed firms in Turkey. Journal of Governance & Regulation, 11(2, special issue), 204–217. https://doi.org/10.22495/jgrv11i2siart1

- Gul, S., Muhammad, F., & Rashid, A. (2017). Corporate governance and corporate social responsibility: The case of small, medium, and large firms. Pakistan Journal of Commerce and Social Sciences PJCSS, 11(1), 1–34.

- Hakimi, I., Zeinaddini, M. R., & Soltani Nejad, A. (2016). Studying the role of corporate social responsibility in corporate performance with emphasis on mediator variables of competitive advantage, corporate reputation and customer satisfaction case study: Food industry of Amol Township. International Journal of Humanities and Cultural Studies IJHCS ISSN, 2356-5926(1), 2263–2278.

- Hambrick, D. C. (2007). Upper echelons theory: An update. Academy of Management Review, 32(2), 334–343.

- Hambrick, D. C., & Mason, P. A. (1984). Upper echelons: The organization as a reflection of its top managers. Academy of Management Review, 9(2), 193–206.

- Hambrick, D. C., & Quigley, T. J. (2014). Toward more accurate contextualization of the CEO effect on firm performance. Strategic Management Journal, 35(4), 473–491.

- Hossain, M. M., Alamgir, M., & Alam, M. (2016). The mediating role of corporate governance and corporate image on the CSR-FP link: Evidence from a developing country. Journal of General Management, 41(3), 33–51.

- Hsu, S. L. (2018). The effects of corporate social responsibility on corporate image, customer satisfaction and customer loyalty: An empirical study on the telecommunication industry. International Journal of Social Sciences and Humanities Invention, 5(5), 4693–4703.

- Ikon, M. A., & Chika, C. A. (2019). Organisational identification and employee performance in selected commercial banks in Delta State. European Journal of Business and Innovation Research, 7(4), 1–27.

- Jahid, M. A., Rashid, M. H. U., Hossain, S. Z., Haryono, S., & Jatmiko, B. (2020). Impact of corporate governance mechanisms on corporate social responsibility disclosure of publicly-listed banks in Bangladesh. The Journal of Asian Finance, Economics and Business, 7(6), 61–71.

- Jain, T., & Jamali, D. (2016). Looking inside the black box: The effect of corporate governance on corporate social responsibility. Corporate Governance an International Review, 24(3), 253–273.

- Jamali, D. (2008). A stakeholder approach to corporate social responsibility: A fresh perspective into theory and practice. Journal of Business Ethics, 82(1), 213–231.

- Jamali, D., Safieddine, A. M., & Rabbath, M. (2008). Corporate governance and corporate social responsibility synergies and interrelationships. Corporate Governance an International Review, 16(5), 443–459.

- Janang, J. S., Joseph, C., & Said, R. (2020). Corporate governance and corporate social responsibility society disclosure: The application of legitimacy theory. International Journal of Business and Society, 21(2), 660–678.

- Janney, J. J., & Gove, S. (2011). Reputation and corporate social responsibility aberrations, trends, and hypocrisy: Reactions to firm choices in the stock option backdating scandal. Journal of Management Studies, 48(7), 1562–1585.

- Javeed, S. A., & Lefen, L. (2019). An analysis of corporate social responsibility and firm performance with moderating effects of CEO power and ownership structure: A case study of the manufacturing sector of Pakistan. Sustainability, 11(1), 248.

- Kalnins, A. (2018). Multicollinearity: How common factors cause Type 1 errors in multivariate regression. Strategic Management Journal, 39(8), 2362–2385.

- Khanifah, K., Hardiningsih, P., Darmaryantiko, A., Iryantik, I., & Udin, U. D. I. N. (2020). The effect of corporate governance disclosure on banking performance: Empirical evidence from Iran, Saudi Arabia and Malaysia. The Journal of Asian Finance, Economics and Business, 7(3), 41–51.

- Khan, A., Muttakin, M. B., & Siddiqui, J. (2013). Corporate governance and corporate social responsibility disclosures: Evidence from an emerging economy. Journal of Business Ethics, 114, 207–223.

- Kim, S. (2022). The COVID-19 pandemic and corporate social responsibility of Korean global firms: From the perspective of stakeholder theory. Emerald Open Research, 4(16), 16.

- Kong, Y., Antwi‐adjei, A., & Bawuah, J. (2020). A systematic review of the business case for corporate social responsibility and firm performance. Corporate Social Responsibility and Environmental Management, 27(2), 444–454.

- Kyurova, V., & Yaneva, D. (2017). Research on the impact of the corporate image on the competitiveness of interior design enterprises. In CBU International Conference Proceedings, Prague, Czech Republic (Vol. 5, p. 495). Central Bohemia University.

- Lai, C. S., Chiu, C. J., Yang, C. F., & Pai, D. C. (2010). The effects of corporate social responsibility on brand performance: The mediating effect of industrial brand equity and corporate reputation. Journal of Business Ethics, 95(3), 457–469.

- Ledi, K. K., Ameza-Xemalodzo, E. B., Alhassan, G. A., & Bandoma, S. (2022). Investigating corporate governance and corporate social responsibility nexus in emerging economy: A structural equation approach. Corporate Governance Review, 6(4), 23–32.

- Lee, C. Y., Chang, W. C., & Lee, H. C. (2017). An investigation of the effects of corporate social responsibility on corporate reputation and customer loyalty–evidence from the Taiwan non-life insurance industry. Social Responsibility Journal, 13(2), 355–369.

- Lu, J., Ren, L., Zhang, C., Rong, D., Ahmed, R. R., & Streimikis, J. (2020). Modified Carroll’s pyramid of corporate social responsibility to enhance organizational performance of SMEs industry. Journal of Cleaner Production, 271(4), 122456.

- Maama, H. (2021). Achieving financial sustainability in Ghana’s banking sector: Is environmental, social and governance reporting contributive?. Global Business Review, 1-7. https://doi.org/10.1177/09721509211044300

- Martos‐pedrero, A., Jiménez‐castillo, D., Ferrón‐vílchez, V., & Cortés‐garcía, F. J. (2023). Corporate social responsibility and export performance under stakeholder view: The mediation of innovation and the moderation of the legal form. Corporate Social Responsibility and Environmental Management, 30(1), 248–266.

- Maruf, A. A. (2013). Corporate social responsibility and corporate image. Transnational Journal of Science and Technology, 3(8), 29–49.

- Melissen, F., Mzembe, A. N., Idemudia, U., & Novakovic, Y. (2018). Institutional antecedents of the corporate social responsibility narrative in the developing world context: Implications for sustainable development. Business Strategy and the Environment, 27(6), 657–676.

- Mertzanisa, C., Mohamed, A. K. B., & Ehab, K. A. M. (2019). Social institutions, corporate governance and firm-performance in the MENA region. Research in International Business and Finance, 48(2), 75–96.

- Moneva, J. M., & Hernández-Pajares, J. (2018). Corporate social responsibility performance and sustainability reporting in SMEs: An analysis of owner-managers' perceptions. International Journal of Sustainable Economy, 10(4), 405–420.

- Mukhibad, H., Kiswanto, F., & Jayanto, P. Y. (2017). An analysis on financial and social performance of Islamic banks in Indonesia. International Journal of Monetary Economics and Finance, 10(3–4), 295–308.

- Muntahanah, S., Kusuma, H., Harjito, D. A., & Arifin, Z. (2021). The effect of family ownership and corporate governance on firm performance: A case study in Indonesia. The Journal of Asian Finance, Economics & Business, 8(5), 697–706.

- Musah, A., & Adutwumwaa, M. Y. (2021). The effect of corporate governance on financial performance of rural banks in Ghana. International Journal of Financial, Accounting, and Management, 2(4), 305–319.

- Narwal, K. P., & Jindal, S. (2015). The impact of corporate governance on the profitability: An empirical study of Indian textile industry. International Journal of Research in Management, Science & Technology, 3(2), 81–85.