?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper aims to investigate empirically the impact of corporate social responsibility (CSR) on firm performance (FP) with the maritime transportation industry of Vietnam as a case study. To evaluate the research model, this study surveyed 145 shipping companies (SCs) across Vietnam, and adopted a structural equation modeling (SEM) to test the proposed hypotheses. It is found: (1) CSR measures significantly directly affect FP and indirectly influence through customer loyalty (CL), (2) CSR initiatives improve customer satisfaction (SAT), and CL. Based on empirical results, this research suggests some management recommendations for SCs to improve their CSR initiatives and, in turn, boost their performance.

1. Introduction

Under the increasingly competitive business environment, a company’s social and environmental contributions during operations are essential for its performance. In the relevant literature, such contributions are called CSR initiatives, which have received much interest from scholars (Hur et al., Citation2020), industry executives (Barnett et al., Citation2020), and policymakers (Ahmed et al., Citation2020). Furthermore, it is commonly accepted that CSR has numerous dimensions, with most recent studies focusing on the philanthropic component of CSR, also known as social marketing (Shahzad et al., Citation2020). It has a reasonable ground to demonstrate that providing high-quality shipping services results in a cascade of positive outcomes for an organization, including customer satisfaction (Nguyen et al., Citation2022), customer loyalty (W. -K. -K. Hsu et al., Citation2023), and higher profits (Yuen Thai et al., Citation2018). Still, there have been a lot of disputes about whether or not CSR practices improve a company’s operational performance (Chang & Yeh, Citation2017; Famiyeh, Citation2017). The primary goal of this research is to use institutional theory to investigate the interplay between CSR, SAT, and CL and their effects on performance outcomes.

CL is frequently attributed to CSR, either directly or indirectly, via other constructions (Karaman et al., Citation2021) or in combination with CSR (Singh & Misra, Citation2021). Prior research has demonstrated that by improving CSR through establishing a strong company image and brand value, firms have the potential to effectively boost their firm performance (Ahmed et al., Citation2020; Karaman et al., Citation2021). With reference to contemporary business standards, businesses are urged to participate actively in CSR practices since it is demanded by their clients. These CSR activities are necessary for every industry, including maritime transportation. SCs tend to enhance their image by developing effective CSR policies, and implementing self-regulations to demonstrate to consumers, employees, communities that their operations are ethical, safe, and environmentally friendly, and thereby improving their reputation in the long term (Kuzey et al., Citation2022).

Critics of CSR claim that it distracts from a company’s core mission and wastes resources for little return on investment. According to W. -K. -K. Hsu et al. (Citation2022), previous correlational analyses erroneously overestimate positive correlations because they fail to account for opportunity costs. The hundreds of millions of dollars spent on CSR disclosure outweigh or nullify the limited value of CSR. Scholars who support CSR, however, have suggested that it can be financially beneficial if it is administered strategically (Cheema et al., Citation2017). Strategically designed CSR actions help organizations’ competitive advantages and provide mutually beneficial value for their stakeholders (Indriastuti et al., Citation2021). It is argued that maritime businesses’ CSR adoption is typically driven by strategic or economic considerations. According to Akkan (Citation2019), environmental initiatives are often implemented because of the possible cost savings they may provide. However, maritime transportation corporations give less weight to the efficiency of abating environmental impacts than they should. In the meantime, Hirata (Citation2019) pointed out that the economic-centric execution of CSR initiatives results in higher negative social and ecological consequences.

This article aims to investigate the relationship among CSR, SAT, CL, and FP in maritime transportation. The current research selected the maritime transportation sector as an empirical study on account of increasing demand from authorities, clients, and the general public to adopt CSR programs. The maritime sector is often criticized for being slow to adopt progressive social and environmental policies. As a result, our research can shed much-needed light on the strategies employed by maritime companies in their quest to achieve commercial excellence. When deciding to use limited company resources, maritime companies often face difficult trade-offs, such as whether to boost SAT and CL by investing in CSR. Since SAT, CL, and financial performance are so crucial to a company’s success, it will be necessary to know how CSR investments affect these key areas of performance.

The remaining part of the article is structured as follows: Section 2 provides an extensive review of past literature on the theory of institutions, CSR practices, SAT, CL, and FP, and then suggests 06 research hypotheses that need to be tested. Section 3 outlines this article’s methods, including the research sample, survey measures, and the way to analyze data. Section 4 gives the results of the empirical analysis, which includes exploratory factor analysis (EFA), confirmatory factor analysis (CFA), as well as structural equation modeling (SEM). In the end, conclusions, limitations, and recommendations for further studies are presented in the last section.

2. Literature review

2.1. The theory of institutions

Although institutional theory has been widely studied since the 1970s, its application to investigate CSR-related problems in enterprises is inadequate. The theory of institutions focuses on the importance of social, political, and economic frameworks through which firms function and earn legitimacy (Suddaby, Citation2010). In other words, firms face increasing pressure from communities to comply with institutional expectations to reach social legitimacy. This is because violations might endanger firms’ operational performance (Drori, Citation2019), and strategic development in the long term (Lewis et al., Citation2019).

Using the lens of institutional pressure from international organizations (i.e., IMO), professional organizations (i.e., ISO), and rival organizations, this study provides the theoretical basis to explain why SCs are adopting CSR practices. Theoretically, institutional theory distinguishes three forms of pressure: coercive (Flynn & Walker, Citation2020), normative (Depoers & Jérôme, Citation2019), and mimetic pressure (Martínez-Ferrero & García-Sánchez, Citation2017). According to Flynn and Walker (Citation2020), coercive pressure refers to national or international regulations (i.e., the IMDG code, the anti-bribery laws, and the anti-discrimination laws) that organizations have to obey; otherwise, they will face legal action and financial consequences. Such regulatory standards are argued to substantially affect firms’ CSR practices, among them, legal responsibility and environmental responsibility.

Meanwhile, Depoers and Jérôme (Citation2019) indicated that normative pressure relates to compliance with professional organizations’ quasi-legal requirements, for instance, the Code of Ethics and Conduct (CEC), the whistleblower program, etc. Flynn and Walker (Citation2020) also argued that to achieve legitimacy and progress in the long-term, firms prefer to implement new measures and practices compatible with the institutional business creeds and values. In maritime transportation, normative pressure ensures SCs operate in a socially compliant way, thereby stimulating them to adopt CSR practices. By doing so, SCs may influence public opinion by implementing effective communication and management techniques. Tang and Gekara (Citation2020) believed that SCs’ image and reputation might suffer if they do not control public perception and do not improve the relationship with members of labor unions. It is clear that impaired reputations may result in external losses as well as a loss of competitive advantage for SCs. Because of this, firms’ image, reputation, and competitive advantage are all affected by the adoption of CSR activities (Hur et al., Citation2020).

From Martínez-Ferrero and García-Sánchez (Citation2017)’s viewpoint, mimetic pressure refers to the fact that firms in the same sectors imitate the strategic actions of successful rivals to duplicate their success. In this circumstance, the CSR adoption (i.e., charitable activities, donations, etc.) may be costly (Depoers & Jérôme, Citation2019), but beneficial (Lewis et al., Citation2019). While corporations in Europe and North America use mimetic pressure as an effective tool for achieving higher performance, organizations in less developed countries employ it to promote better CSR management. Tang and Gekara (Citation2020) demonstrated that by responding to intense mimetic pressures, SCs may attain financial benefits by becoming more competitive. It can be said that although CSR adoption is costly, it assists SCs in coping with mimetic pressures and, in turn, boosting SCs competitive advantage.

2.2. Corporate social responsibility

Although many interpretations exist regarding CSR among academics, the broad concept of CSR, including 4 dimensions, viz., economic, legal, ethical, and philanthropic, has mainly been acknowledged. Research towards customer-oriented CSR has used many different methods of analysis. Numerous studies have examined the influence of cause-related marketing initiatives, with the findings indicating that consumers favor companies who participate in these activities (Ahmed et al., Citation2020; Wild, Citation2021). A company’s social responsibility has an enormous impact on its product’s total value, according to Shahzad et al. (Citation2020). Ethical issues have been addressed in other literature, for instance, Kuzey et al. (Citation2022), Singh and Misra (Citation2021), and Karaman et al. (Citation2021). There have been a number of studies examining whether or not CSR has an effect on a company’s performance, and the findings have been contradictory. According to Kitada and Tansey (Citation2018), the causal connection between CRS and FP is more nuanced than previously assumed because of the existence of unexplored mediating variables. Relevant research has examined the intervening factors from the point of view of the many parties involved. According to the stakeholder theory, a company cannot maximize its financial outcomes without fulfilling the needs of its stakeholders, including customers, staff members, vendors, and others in the community. Evidence shows that stakeholders need to be contented with a company’s CSR efforts before financial performance is improved (Flynn & Walker, Citation2020; Shurrab et al., Citation2019; Wagner, Citation2018).

Nowadays, we can easily recognize that some major shipping lines, such as APM-Maersk, CMA-CGM, COSCO, and Hyundai Merchant Marine, have incorporated the principles of sustainable development and corporate social responsibility into their operational strategies (UNCTAD, Citation2022). Many prior works of literature have demonstrated a mutually beneficial connection between CSR practices and firm performance. This also illustrates the significance of CSR practices in the marine transportation industry. Yet, just a few articles have looked into CSR in the container shipping sector, for example, Tang and Gekara (Citation2020), Yuen Thai et al. (Citation2018), and Geerts and Dooms (Citation2020). However, notwithstanding contemporary CSR frameworks are divergent and that different organizations’ definitions regarding CSR are not consistent either, past studies have reached a consensus that CSR might be separated into 4 constructs, including economic responsibility, philanthropic responsibility, ethical and legal responsibility, and environmental responsibility (Barnett et al., Citation2020; Depoers & Jérôme, Citation2019; Geerts & Dooms, Citation2020; Karaman et al., Citation2021).

Recent studies have demonstrated that CSR activities and actions can have a positive impact on consumer attitudes (Singh & Misra, Citation2021), purchasing intentions (Shahzad et al., Citation2020), customer satisfaction (Hur et al., Citation2020), and brand loyalty toward a company (Barnett et al., Citation2020). As a result, this article established and evaluated a conceptual framework to posit that CSR activities assist enterprises to satisfy customers. In turn, this will contribute positively to customer loyalty and organizational success. On the basis of the literature, some following hypotheses are suggested as shown in Figure :

Hypothesis 1:

CSR actions will positively affect firm performance in the maritime transportation industry.

Hypothesis 2:

CSR actions will positively affect customer loyalty in the maritime transportation industry.

Hypothesis 3:

CSR actions will positively affect customer satisfaction in the maritime transportation industry.

Figure 1. Conceptual framework.

2.3. Firm performance

Firm performance measures firms’ ability to use human material resources to achieve goals set by firms (Yuen Thai et al., Citation2018). Firm performance also considers efficiency of corporate resources utilized during the production and consumption processes. In principle, lagging and leading criteria can be used to evaluate a company’s success. In particular, criteria reflecting progress toward a goal are called lagging ones, such as profits and revenues, alongside all other measures of economic performance (Singh & Misra, Citation2021). In contrast, leading criteria are a group of measurements used to forecast potential economic outcomes or consequences (Wagner, Citation2018). In this discussion, leading criteria include SAT and CL.

Past research has demonstrated a positive link between CSR and organizational success (Tang & Gekara, Citation2020), as well as a linkage between positive brand assessments and customer satisfaction (Geerts & Dooms, Citation2020). Empirical evidence suggests that CSR practices are becoming increasingly crucial to an enterprise’s competitiveness. Besides, they have a positive impact on other areas of firm operations, viz., sale planning (Ahmed et al., Citation2020), cost reductions (Hur et al., Citation2020), credit and financing (Shahzad et al., Citation2020), and client connections (Tang & Gekara, Citation2020).

Karaman et al. (Citation2021) argued that consumers who demonstrate advocacy behavior and attributes (i.e., the increase in repurchasing, helpful interpersonal communication, and willingness to accept a higher price) can be turned into brand ambassadors for firms. The growing body of theoretical and empirical research postulates that the CSR strategy provides a wide range of tangible and intangible benefits. Notably, improved brand value and reputation (Depoers & Jérôme, Citation2019), cost reductions, incremental income, easier access to financing (Martínez-Ferrero & García-Sánchez, Citation2017), and the acquisition of operating licenses (Lewis et al., Citation2019) are typical examples of these types of accomplishments in the business world.

2.4. Customer satisfaction

Research on customer satisfaction has been considerable, but scholars have not agreed on a single definition. According to Hirata (Citation2019), customer satisfaction is the customer’s psychological reaction to their prior experience when comparing their expectation and perception. Satisfaction is also quantified by a single transaction or through a set of interactions with a product and services over time. Liu (Citation2019) argued that customer satisfaction is precisely a primary antecedent of firms’ long-term profits.

Because CSR initiatives have been highlighted as a goal for a lot of organizations to satisfy their customers, it is broadly accepted that enterprises with satisfied customers tend to have higher customer loyalty (Yuen Thai et al., Citation2018), a better reputation (Tang & Gekara, Citation2020), and improved organizational performance (Martínez-Ferrero & García-Sánchez, Citation2017). Further, customers who are satisfied with a company’s products or services are more likely to repurchase and/or spread word of mouth about the company’s offerings (Wen-Kai Hsu et al., Citation2021). As a result, both of which have a beneficial effect on the company’s future revenue and, by extension, its financial performance. In light of these facts, this article suggests some research hypotheses, as below:

Hypothesis 4:

Customer satisfaction will positively affect customer loyalty in the maritime transportation industry.

Hypothesis 5:

Customer satisfaction will positively affect firm performance in the maritime transportation industry.

2.5. Customer loyalty

According to marketing theories, the long-term success of firms is not determined by the number of one-time buyers but by that of loyal ones who continue purchasing firms’ goods and services (Caliskan & Esmer, Citation2020). Customer loyalty refers to a continuing emotional bond between firms and their customer, demonstrated by a customer’s willingness to engage with and repurchase companies’ products and services in comparison to firms’ competition (Balci, Citation2021; Bergek et al., Citation2021). Loyalty develops as a result of a customer’s pleasant experience with the firms’ brand and contributes to the development of trust. Several relevant studies have examined customer loyalty by employing a combination of attitudinal and behavioral variables to determine satisfaction. In the container shipping industry, there is a significant deal of interest in determining the elements that influence customer loyalty, mainly because it is commonly assumed that satisfied customers contribute to increased profitability. Yuen Wang et al. (Citation2018) posited that customer loyalty is of paramount critical to a company’s survival and growth; establishing a loyal client base has emerged as one of the strategic marketing objectives.

On top of that, CL is a critical variable in the conversion of CSR into organizational success. Chaudhuri et al. (Citation2019) argued that revenues and profits can grow in the first year after introducing loyalty programs, and these gains can be expected to last for at least three more years. Stated differently, it illustrates that the implementation of well-planned loyalty programs might substantially improve a company’s performance. As a result, the following hypothesis is suggested in this study:

Hypothesis 6:

Customer loyalty will positively affect firm performance in container shipping operations.

3. Methodology

3.1. Research framework

This research was carried out via five main steps, as shown in . The first step was to develop a research instrument through extensive literature review and expert interviews. Particularly, this study implemented six rounds of discussion with six experts who had a good experience in the container transportation industry across Vietnam. The experts’ background is shown in Table .

Figure 2. Research process.

Table 1. The background of the experts interviewed

An in-depth interview was conducted as follows. First, the research team sent invitation letters to potential experts to know whether they would join our interview. Secondly, depending on the geographic distance between interviewers and interviewees, experts were interviewed directly (online or in person) to get the necessary information. More specifically, experts read the drafted questionnaire to guarantee it was understandable and coherent. Moreover, they checked whether essential observed items were missed in such a prepared questionnaire. Thirdly, experts’ suggestion in terms of the latent and observed variables was absorbed to revise the original questionnaire. Finally, the revised questionnaire was re-sent to experts to make sure that it was ready to deliver to respondents.

In Step 2, the article collected data from shipping lines throughout Vietnam by designed questionnaires. Next, data was conducted item purification by adopting EFA. Afterwards, CFA was employed to assure that collected data satisfies four requirements, including unidimensionality, reliability, convergent validity, and discriminant validity. Finally, SEM was carried out to test research hypotheses.

3.2. Data collection

According to the 2021 report of the Vietnam Ship Agents and Brokers Association (VSABA), there were roughly 312 enterprises doing business in the container transportation industry across Vietnam. More specifically, nearly 39% of them were headquartered in the North of Vietnam; about 15% were located in the Middle, while over 65% were situated in the South. On the basis of operational revenues during the latest five years, this research selected 100 enterprises with the biggest revenue and their business operations spreading nationwide as the sample survey. Then, thanks to the consultation from VSABA, this study randomly delivered 300 questionnaires to such 100 companies via email and postage-paid return envelopes between October 2021 and January 2022. In addition, two chief ways were made to minimize non-response bias. First, respondents were informed that the information they provided was used solely for research analysis and remained confidential; second, fortnight reminders were sent to respondents. By the cut-off date, the research team received 235 answered questionnaires. After checking and screening some bad and invalid responses, only 145 questionnaires were acceptable for further analysis. Consequently, the valid response rate was 48.3%. Descriptive statistics for the survey sample are shown in Table .

Table 2. The background of the respondents

3.3. Measures

Observed variables for evaluating CSR practices, SAT, CL, and FP were developed primarily from earlier research (see Appendices 1, 2, and 3). All of the measurement scales were established and adjusted with feedback from experienced experts in the maritime transportation industry via in-depth interviews, as presented above. These observed items were assessed on a five-point Likert scale, with 1 indicating strongly disagree and 5 indicating strongly agree with the statement.

3.4. Data analysis

Initially, the EFA approach was conducted to determine the critical constructs of CSR initiatives, SAT, CL, and FP. The research hypotheses were then tested using an SEM technique, which was developed specifically for this purpose. One can recognize that a large number of endogenous and exogenous variables, as well as latent (unobserved) variables described as linear combinations (weighted averages) of the observed variables, can be handled using this technique. On top of that, this study adopted a two-step approach for analyzing data, as advised by Cleff (Citation2019). The first phase was to employ CFA to determine the validity of the measurement model. To complete the second stage, this article estimated SEM from the unobserved variables. All of the analyses were carried out adopting the statistical software SPSS 22 and AMOS 20.

4. Empirical results

4.1. EFA results and reliability test

To purify and reduce a large number of observed variables to a smaller, more controllable collection of principal components, this research adopted the EFA method with principal component (PC) and VARIMAX rotation. Besides, the requirements for selecting the EFA model are KMO >0.5, and eigenvalue >1, subtraction of two items <0.3. As shown in Appendixes 1, 2, and 3, eight dimensions were extracted. More specifically, CSR practices were measured by four other constructs, including economic responsibility (coded as CSR1), philanthropic responsibility (termed as CSR2), ethical and legal responsibility (labeled as CSR3), and environmental responsibility (named CSR4). Whereas customer loyalty was assessed by two constructs, including willingness to pay (called CL.1) and intention to use (coded as CL.2). Meanwhile, other dimensions were evaluated by one construct. Further, factor loadings ranging from 0.528–0.945 reflected the reliability of measurement scales.

4.2. Confirmatory factor analysis

Following the EFA, a CFA method was conducted to test the hypothesis that a relationship between observed variables and their underlying latent constructs exists. In this stage, the normality, outliers, and multicollinearity of the data were also tested, as advised by Cleff (Citation2019). Consequently, 145 surveys were retained for future tests.

When testing a measurement model’s validity, it is essential to establish acceptable levels of goodness of fit while also identifying concrete evidence of its construct validity. To do so, the prior literature has posited that some fit indices must be reported when verifying a measurement model, such as: the χ2/df statistic, the Tucker Lewis index (TLI), the mean square error of approximation (RMSEA), and the comparative fit index (CFI). Additionally, Crede and Harms (Citation2019) suggested the Parsimony-Adjusted Measures Index (PNFI) to compare models’ different complexities. The goodness of fit indices is shown in Table , which offers an excellent fit for the measurement model. Such goodness of fit indices might verify the validity of the measurement model. Furthermore, the PNFI of 0.727 illustrates an acceptable range of complexities.

Table 3. The goodness of fit indices for the measurement model

CFA results were also used to determine the construct validity of the data. According to Ahmed et al. (Citation2020), the convergent, discriminant, and nomological evaluations should be performed in the following order. The convergent validity was assessed by the composite reliability (CR), the average variance extracted. Yuen Wang et al. (Citation2018) suggested testing the convergent validity by utilizing t-values that are statistically significant on the factor loadings. In theory, the t-value is computed by dividing estimated parameters by its standard errors (SE). Singh and Misra (Citation2021) demonstrated that the construct convergent validity will be verified if the standardized factor loadings of indicators are more than 0.50 and t values >1.96.

As exhibited in Table , we can see that all of the factor loadings are more than 0.5 while their t-values are more than 1.96, illustrating the construct convergent validity. CR and AVE values also demonstrate the convergent validity of constructs.

Table 4. CFA results

According to Benson and Tippets (Citation2018), the discriminant validity tests whether concepts or measurements are actually unrelated. In practice, the most common way to test this is to compare the AVE values with the square of the correlations between each pair of constructs. And AVE values must exceed the squared correlations values. As displayed in Table , the square of the correlation value for every construct satisfies the above-mentioned requirement, thereby providing evidence for the construct discriminant validity.

Table 5. The discriminant analysis

4.3. Hypotheses testing

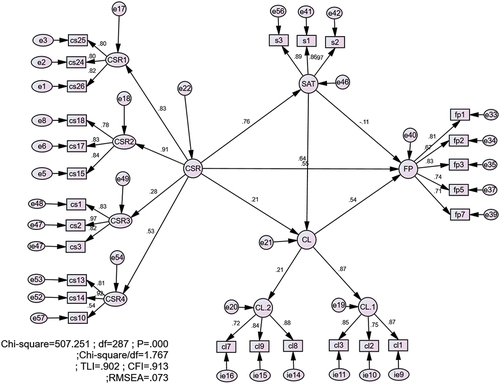

Hypothesis testing was carried out via the SEM approach, as seen in Figure . The structural model’s fit indices also satisfy the acceptable range (χ2/df = 1.767, CFI = 0.913, TLI = 0.902, RMSEA = 0.073). Besides, the SEM model’s individual paths were assessed. The hypothesized relationships were tested by the standardized coefficients and p-values that were associated with them, as shown in Table . Among six hypotheses, the hypothesis H5 was rejected on the basis of the p-value of greater than 0.1. On the contrary, other hypotheses were supported with a significant level ranging from 0.01 to 0.05.

Figure 3. SEM results.

Table 6. Hypothesis testing results

4.4. Discussions

The present research aims to evaluate the causal relationship between CSR initiatives and firm performance in the maritime transportation industry. As seen in Figure , CRS actions directly affect FP with a standardized coefficient of 0.55 (p = 0.004). The finding is consistent with Yuen Thai et al. (Citation2018), who demonstrated that CRS strongly impacts cost savings and profits, which can assist firms in surviving and developing in an economic recession. Furthermore, it has been postulated that CSR implementation can step up firms’ market share, thus expanding their intangible resources, such as reputation (Liu, Citation2019) and positive consumer evaluations (Hsu et al., Citation2022). Besides, CSR is argued to be the driver of SAT, with a relatively high path coefficient of 0.763 (p = 0.000). This finding supports prior research that CSR initiatives influence customer attitudes and quality assessments of enterprises’ products/services in a variety of contexts (Cheema et al., Citation2017; Christodoulou & Cullinane, Citation2021). Accordingly, this finding can help shipping operators establish viable methods for retaining current consumers by leveraging their CSR efforts/practices.

Figure also indicates that CL plays a crucial role in mediating the positive impact of CSR on FP. The finding is in agreement with the pertinent research adopting institutional theories to elucidate the causal relationship between CSR practices and firms’ economic performance (Balci, Citation2021; Chaudhuri et al., Citation2019). Therefore, it is essential that CSR initiatives are analyzed and aligned with customers’ interests and performed in association with the satisfaction of consumers before any changes can be made to the company’s economic performance. Moreover, CL directly affects FP with a standardized coefficient of 0.54 (p = 0.047).

According to the model, SAT has no significant, positive impact on FP. This finding is contrary to the relevant literature, especially the marketing theory, which appreciates customer satisfaction and its role in driving firm performance. One probable explanation can be the maritime transportation sector’s business-to-business character. Nevertheless, it is evident that SAT indirectly influences FP via CL. Accordingly, CL should be deemed the intermediary for efficient CSR practices and FP.

5. Conclusions, Implications, and Limitations

5.1. Conclusions

Along with the increasing significance of CSR, it is imperative to increase our knowledge of CSR, firm performance, and the interrelationships between these factors and consumers. In addition, the extensive literature review argues that CSR-related research should be further developed because CSR practices and actions in the maritime transportation industry are undocumented. To fill the literature gap, this research presents an empirical study of the relationship among CSR, SAT, and CL in the maritime transportation sector, as well as how these factors impact firm performance. Since then, this article hypothesized that companies’ CSR practices and actions have a direct and considerable effect on overall SAT, CL, and FP. Moreover, the impact of perceived SAT on CL and FP, and the effect of CL on FP in maritime transportation were investigated. Some main findings are as follows:

Firstly, the empirical results supported the positive influence of CSR practices on SAT, CL, and especially FP. So, hypotheses H1, H2, and H3 are supported. Past research has discovered that unethical marketing practices harm consumers’ attitudes (Wagner, Citation2018), satisfaction (Christodoulou & Cullinane, Citation2021), and behavioral intentions (Akkan, Citation2019). CSR measures are also considered social norms between firms and their customers (Kitada & Tansey, Citation2018).

Secondly, hypotheses H4 and H6 are accepted, arguing the existence of a positive relationship between SAT and CL, and between CL and FP. Empirical studies from Fasoulis (Citation2021), Yuen Kan and Ko (Citation2020), and Fasoulis and Kurt (Citation2019) also resulted in consistent findings. By contrast, hypothesis H5 is rejected, implying no relationship between SAT and FP exists. This finding is so different from that of the last literature, such as Yuen Thai et al. (Citation2018), and Singh and Misra (Citation2021). Yet, it is argued that SAT indirectly influences FP via CL. Accordingly, CL should be deemed the intermediary for efficient CSR practices and FP.

5.2. Theoretical implications

This paper’s findings provide a significant contribution to theory in several manners. Initially, the empirical findings add to the body of existing knowledge in the maritime transportation industry. The current findings are consistent with earlier research investigating the beneficial link between CSR implementation and organizational performance, indicating CSR actions as an antecedent of FP (Barnett et al., Citation2020; Singh & Misra, Citation2021; Yuen Thai et al., Citation2018). Nonetheless, such a relationship is mediated by CL. Thence, improving firm performance by enhancing CL is necessary. Findings indicate that CSR practices impact CL and service assessment.

Nevertheless, a practical CSR strategy will not suffice to ensure CL if firms’ customers feel unsatisfied with the services provided. Therefore, this research suggests that CSR initiatives can aid in the development of SAT, which can then be followed by the development of FP and CL. It is clear that major international containership companies primarily implement CSR activities in the maritime transportation sector. Nonetheless, as demonstrated by the examples of Yang Ming Line and OOCL, their administration mainly concentrates on the environmental aspects to comply with global environmental regulations, while failing to gain a thorough understanding of the needs of their customers. To address latent CSR requirements, shipping lines should reevaluate their policies to truly comprehend the needs of economic entities throughout the entire supply chain, and they should incorporate this information into the development programs for CSR-related business activities.

5.3. Managerial implications

From the managerial viewpoint, the current research reveals that international organizations (e.g., the United Nations, the European Union, the International Maritime Organization, etc.) play an institutionally crucial role in the promotion of CSR requirements and regulations, as well as the education of maritime practitioners, specially in the field of environmental, philanthropic, social, and economic responsibilities. These organizations also have the authority to define agendas supporting CSR activities and reporting requirements in accordance with the World Bank’s recommendations, including requiring, facilitating, collaborating, approving, and demonstrating their effectiveness.

Second, discussing CSR practices with customers is critical since consumers who have knowledge of CSR practices and who take into consideration a company’s commitments to CSR activities have more favorable views, satisfaction, and loyalty than those who do not. Container shipping firms must become more concerned with the well-being and retention of their customers since devoted consumers consume more, pay more, suggest more, and ultimately increase the organization’s success.

It is argued that customer loyalty is the intermediary between CSR initiatives and firm performance; this study advocates for the active publication of CSR reports to increase SAT and loyalty and, in turn, developing the number of loyal customers and their repurchasing. Hirata (Citation2019) also had a similar suggestion. Some information channels, which can be helpful for the publishing of firms’ CSR performance, include official websites, advertising, social media, etc. Additionally, CSR activities with customers, such as shippers and consignees, might be developed by container shipping executives to promote customer satisfaction, preserve customer loyalty and boost a reputable brand’s public image. Also, maritime transport companies must strive to improve long-term customer relationships to reduce the unfavorable impacts of their shipping operations on society, environment, and culture, as well as to develop the number of customers who are satisfied and loyal to the company.

Third, maritime transport firms might utilize the examined CSR metric as a strategic instrument for differentiation and market segmentation, as well as for market segmentation themselves. Balci (Citation2021) postulated that CSR initiatives can help managers strengthen their corporate strategy because ethical, social, and environmental considerations will help a firm improve its financial success. Yet, to enhance a firm’s CSR operations, the first step is to grasp the idea behind it. Vessels should also be operated in an environmentally responsible manner to minimize their effect on the sea environment. On top of that, workarounds to prevent ships from unpredictable events, such as sea accidents, collisions, etc., should be paid more attention to.

Lastly, the implementation of CSR practices not only creates many opportunities, but also poses significant obstacles for maritime transportation firms. For opportunities, shifting market power from suppliers to customers could lead to fundamental changes in the transportation industry. As a result, big suppliers with the ability to assure a responsible upstream supply chain will have more commercial options. In terms of potential obstacles, companies in the shipping industry will have to face their customers’ new needs and requirements. The new requirements can be authentication, regulation obedience, and business activities regarding CSR initiatives or even the needs outside companies.

5.4. Limitations

This section presents a few research limitations that should be addressed by future studies. First, this paper collected data from the maritime transportation industry in Vietnam to test research hypotheses. Hence, external validity is the limitation of this research. It is suggested that further studies should broaden sample sizes to other industries and countries to generalize empirical results.

Second, the scope of this research was limited to the effects of CSR, SAT, and CL on the performance of firms in the maritime transportation industry. We know that many additional factors influencing organizational success, such as suppliers, workers, and other stakeholders, are ignored. For that reason, future studies are advised to take into account these variables in the research model.

Third, it will be more significant for maritime transportation firms’ marketing strategies if future studies can separate customers of CSR-implementing shipping companies from those of non-implementing ones. Furthermore, the CSR measurement scale needs to be improved from the customers’ viewpoint. During the preliminary stages of this study, we discovered that customers were unaware of the CSR programs of maritime transportation firms. Thus, we will better understand how customers view CSR if we conduct more research into CSR implementation.

And last but not least, the attitudes of CSR practices, SAT, CL, and FP obviously change over time. Still, this paper carried out the cross-sectional survey, which happened at a single point in time and thus was not representative of the whole population. Accordingly, it is highly recommended that future research should conduct a longitudinal survey to evaluate the impacts of CSR policies on FP over time and test the hypothesized pathways again.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Ahmed, M., Zehou, S., Raza, S. A., Qureshi, M. A., & Yousufi, S. Q. (2020). Impact of CSR and environmental triggers on employee green behavior: The mediating effect of employee well‐being. Corporate Social Responsibility & Environmental Management, 27(5), 2225–18. https://doi.org/10.1002/csr.1960

- Akkan, E. (2019). CSR activities in maritime and shipping industries. In Maria, A. (Ed.), Cases on corporate social responsibility and contemporary issues in organizations (pp. 276–298). IGI Global.

- Balci, G. (2021). Digitalization in container shipping: Do perception and satisfaction regarding digital products in a non-technology industry affect overall customer loyalty? Technological Forecasting & Social Change, 172, 121016. https://doi.org/10.1016/j.techfore.2021.121016

- Barnett, M. L., Henriques, I., & Husted, B. W. (2020). Beyond good intentions: Designing CSR initiatives for greater social impact. Journal of Management, 46(6), 937–964. https://doi.org/10.1177/0149206319900539

- Benson, J., & Tippets, E. (2018). Confirmatory factor analysis of the Test Anxiety Inventory. In Charles, D. S. (Ed.), Cross-cultural anxiety (pp. 149–156). Taylor & Francis.

- Bergek, A., Bjørgum, Ø., Hansen, T., Hanson, J., & Steen, M. (2021). Sustainability transitions in coastal shipping: The role of regime segmentation. Transportation Research Interdisciplinary Perspectives, 12, 100497. https://doi.org/10.1016/j.trip.2021.100497

- Caliskan, A., & Esmer, S. (2020). An assessment of port and shipping line relationships: The value of relationship marketing. Maritime Policy & Management, 47(2), 240–257. https://doi.org/10.1080/03088839.2019.1690172

- Chang, Y. -H., & Yeh, C. -H. (2017). Corporate social responsibility and customer loyalty in intercity bus services. Transport Policy, 59, 38–45. https://doi.org/10.1016/j.tranpol.2017.07.001

- Chaudhuri, M., Voorhees, C. M., & Beck, J. M. (2019). The effects of loyalty program introduction and design on short-and long-term sales and gross profits. Journal of the Academy of Marketing Science, 47(4), 640–658. https://doi.org/10.1007/s11747-019-00652-y

- Cheema, S., Javed, F., & Nisar, T. (2017). The effects of corporate social responsibility toward green human resource management: The mediating role of sustainable environment. Cogent Business & Management, 4(1), 1310012. https://doi.org/10.1080/23311975.2017.1310012

- Christodoulou, A., & Cullinane, K. (2021). Potential for, and drivers of, private voluntary initiatives for the decarbonisation of short sea shipping: Evidence from a Swedish ferry line. Maritime Economics & Logistics, 23(4), 632–654. https://doi.org/10.1057/s41278-020-00160-9

- Cleff, T. (2019). Applied statistics and multivariate data analysis for business and economics. Springer.

- Crede, M., & Harms, P. (2019). Questionable research practices when using confirmatory factor analysis. Journal of Managerial Psychology, 34(1), 18–30. https://doi.org/10.1108/JMP-06-2018-0272

- Depoers, F., & Jérôme, T. (2019). Coercive, normative, and mimetic isomorphisms as drivers of corporate tax disclosure: The case of the tax reconciliation. Journal of Applied Accounting Research, 21(1), 90–105. https://doi.org/10.1108/JAAR-04-2018-0048

- Drori, G. S. (2019). Hasn’t institutional theory always been critical?! Organization Theory, 1(1), 2631787719887982. https://doi.org/10.1177/2631787719887982

- Famiyeh, S. (2017). Corporate social responsibility and firm’s performance: Empirical evidence. Social Responsibility Journal, 13(2), 390–406. https://doi.org/10.1108/SRJ-04-2016-0049

- Fasoulis, I. (2021). Understanding CSR and sustainability integration patterns into the corporate governance and organisational processes of a ship management company: A case study. World Review of Intermodal Transportation Research, 10(3), 245–268. https://doi.org/10.1504/WRITR.2021.117678

- Fasoulis, I., & Kurt, R. E. (2019). Determinants to the implementation of corporate social responsibility in the maritime industry: A quantitative study. Journal of International Maritime Safety, Environmental Affairs, and Shipping, 3(1–2), 10–20. https://doi.org/10.1080/25725084.2018.1563320

- Flynn, A., & Walker, H. (2020). Corporate responses to modern slavery risks: An institutional theory perspective. European Business Review, 33(2), 295–315. https://doi.org/10.1108/EBR-05-2019-0092

- Geerts, M., & Dooms, M. (2020). An analysis of the CSR portfolio of cruise shipping lines. Research in Transportation Business & Management, 100615, 100615. https://doi.org/10.1016/j.rtbm.2020.100615

- Hirata, E. (2019). Service characteristics and customer satisfaction in the container liner shipping industry. The Asian Journal of Shipping and Logistics, 35(1), 24–29. https://doi.org/10.1016/j.ajsl.2019.03.004

- Hsu, Wen-Kai, Huang, Show-Hui, & Huynh, Tan Nguyen (2021). An evaluation model for foreign direct investment performance of free trade port zones. Promet-Traffic&transportation, 33(6), 859–870. https://doi.org/10.7307/ptt.v33i6.3844

- Hsu, W. K., Tai, H. -H., Huynh, T. N., & Chen, J. W. C. (2022). Assessing the investment environment in container terminals: A knowledge gap model. Proceedings of the Institution of Mechanical Engineers, Part M: Journal of Engineering for the Maritime Environment, 236(3), 585–599. https://doi.org/10.1177/14750902211070739

- Hur, W. M., Moon, T. W., & Kim, H. (2020). When and how does customer engagement in CSR initiatives lead to greater CSR participation? The role of CSR credibility and customer–company identification. Corporate Social Responsibility & Environmental Management, 27(4), 1878–1891. https://doi.org/10.1002/csr.1933

- Indriastuti, M., Chariri, A., & McMillan, D. (2021). The role of green investment and corporate social responsibility investment on sustainable performance. Cogent Business & Management, 8(1), 1960120. https://doi.org/10.1080/23311975.2021.1960120

- Karaman, A. S., Orazalin, N., Uyar, A., & Shahbaz, M. (2021). CSR achievement, reporting, and assurance in the energy sector: Does economic development matter? Energy Policy, 149, 112007. https://doi.org/10.1016/j.enpol.2020.112007

- Kitada, M., & Tansey, P. (2018). Impacts of CSR on women in the maritime sector. In Lisa, L. F. (Ed.), Corporate social responsibility in the maritime industry (pp. 237–251). Springer.

- Kuzey, C., Fritz, M. M., Uyar, A., & Karaman, A. S. (2022). Board gender diversity, CSR strategy, and eco-friendly initiatives in the transportation and logistics sector. International Journal of Production Economics, 247, 108436. https://doi.org/10.1016/j.ijpe.2022.108436

- Lewis, A. C., Cardy, R. L., & Huang, L. S. (2019). Institutional theory and HRM: A new look. Human Resource Management Review, 29(3), 316–335. https://doi.org/10.1016/j.hrmr.2018.07.006

- Liu, J. (2019). Customer satisfaction and firms’ innovation efforts in marketing: Taking shipping logistics companies as an example. Journal of Coastal Research, 94(SI), 940–944. https://doi.org/10.2112/SI94-185.1

- Martínez-Ferrero, J., & García-Sánchez, I. -M. (2017). Coercive, normative and mimetic isomorphism as determinants of the voluntary assurance of sustainability reports. International Business Review, 26(1), 102–118. https://doi.org/10.1016/j.ibusrev.2016.05.009

- Nguyen, Quyet Thang, Ngo, Thi Tuyet Lan, Huynh, Tan Nguyen, Le, Quoc Thanh, Hoang, Van Long (2022). Assessing port service quality: An application of the extension fuzzy AHP and importance-performance analysis. PLos One, 17(2), e0264590. https://doi.org/10.1371/journal.pone.0264590

- Shahzad, M., Qu, Y., Javed, S. A., Zafar, A. U., & Rehman, S. U. (2020). Relation of environment sustainability to CSR and green innovation: A case of Pakistani manufacturing industry. Journal of Cleaner Production, 253, 119938. https://doi.org/10.1016/j.jclepro.2019.119938

- Shurrab, J., Hussain, M., & Khan, M. (2019). Green and sustainable practices in the construction industry: a confirmatory factor analysis approach. Engineering, construction and architectural management, 26(6), 1063–1086. https://doi.org/10.1108/ECAM-02-2018-0056

- Singh, K., & Misra, M. (2021). Linking corporate social responsibility (CSR) and organizational performance: The moderating effect of corporate reputation. European Research on Management and Business Economics, 27(1), 100139. https://doi.org/10.1016/j.iedeen.2020.100139

- Suddaby, R. (2010). Challenges for institutional theory. Journal of Management Inquiry, 19(1), 14–20. https://doi.org/10.1177/1056492609347564

- Tang, L., & Gekara, V. (2020). The importance of customer expectations: An analysis of CSR in container shipping. Journal of Business Ethics, 165(3), 383–393. https://doi.org/10.1007/s10551-018-4062-4

- UNCTAD. (2022). Review of Maritime Transport 2021 https://unctad.org/webflyer/review-maritime-transport-2021

- Wagner, N. (2018). Ways of implementing corporate social responsibility idea in shipping companies. European Journal of Service Management, 26(2), 315–321. https://doi.org/10.18276/ejsm.2018.26-39

- Wen-Kai, H., Yu-Chen, W., Chung-Hong, L., Van Long, H., & Tan Nguyen, H. (2023). A risk assessment model of work safety in container dry ports. Proceedings of the Institution of Civil Engineers-Maritime Engineering, 176(1), 1–13. https://doi.org/10.1680/jmaen.2022.006

- Wild, P. (2021). Corporate social responsibility, cost structures, and COVID-19: Impact of passenger behavior on business models. Transportation Research Interdisciplinary Perspectives, 12, 100494. https://doi.org/10.1016/j.trip.2021.100494

- Yuen Kan, M. H., & Ko, A. H. (2020). Corporate social responsibility practice in shipping logistics industry: A practitioners perspectives. International Journal of Innovation, Management and Technology, 11(3), 81–87. https://doi.org/10.18178/ijimt.2020.11.3.880

- Yuen Thai, V,V., Wong, Y. D., Wang, X., & Wang, X. (2018). Interaction impacts of corporate social responsibility and service quality on shipping firms’ performance. Transportation Research Part A: Policy & Practice, 113, 397–409. https://doi.org/10.1016/j.tra.2018.04.008

- Yuen Wang, X., Wong, Y., Zhou, Q., & Zhou, Q. (2018). The effect of sustainable shipping practices on shippers’ loyalty: The mediating role of perceived value, trust and transaction cost. Transportation Research Part E: Logistics & Transportation Review, 116, 123–135. https://doi.org/10.1016/j.tre.2018.06.002

Appendix 1:

EFA results for CSR practices

Table

Appendix 2:

EFA results for the customer loyalty

Table

Appendix 3:

EFA results for the customer satisfaction, and firm performance

Table