?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Although environmental orientation (EO) has gained surging recent scholarly attention, why, how, and when EO influences green purchasing adoption among firms is inchoate, lacking adequate theorisation and empirical analysis. This study draws on resource orchestration theory (ROT) to test the arguments that the influence of EO on green purchasing is a function of the transformative mechanism of green purchasing capability at differing levels of financial resource. The proposed model is tested on a sample of 165 small and medium-sized enterprises from a sub-Saharan African economy using structural equation modelling (Mplus v7.4) and Hayes’ PROCESS for IBM-SPSS. Findings from the study indicate that green purchasing capability mediates the effect of EO on green purchasing. The study further finds that the effect of EO on green purchasing, via green purchasing capability, is strengthened under the condition of greater financial resource. The findings contribute to the advancement of green purchasing research and the ROT by addressing the green purchasing attitude-behaviour gap from the supply chain perspective. Overall, the study informs supply chain practitioners that bundling EO with green purchasing capability and financial resource is critical for achieving environmental goals.

1. Introduction

Increasing environmental challenges such as resource exhaustion, global warming, decrease in biodiversity, etc., confer an important responsibility on organisations (Khan, Yu, Umar, et al., Citation2022; Yang et al., Citation2022; Yee et al., Citation2021) to support the sustainable development agenda (Van Zanten & Van Tulder, Citation2018). Additionally, corporate green investment is said to foster economic performance (Song et al., Citation2017) and generate competitive advantage (Yook et al., Citation2017). For example, Accor Hotels saved 72 million kWh of electricity in a year after buying energy-efficient light bulbs, while Wal-Mart and Nokia saved US$3.4 billion and €100 million, respectively, through reduced packaging materials (Lefevre et al., Citation2010). Over the years, the dominant logic for green management in the supply chain context has been that organisational outputs crucially depend on the nature of input materials. Thus, purchasing being an input phase function can act as a gatekeeper to effectively engender environmental management (Liu et al., Citation2020; Yang et al., Citation2022). To this end, green purchasing—the degree to which firms achieve environmentally-friendly purchasing objectives (Yasir et al., Citation2020)—has become an important concern to both industry and academia (Keszey, Citation2020; Khan et al., Citation2021; Khan, Yu, Umar, et al., Citation2022). However, the determinants and mechanisms explaining green purchasing behaviour remain a grey area in literature.

The green purchasing literature is brimming with studies on consumers’ attitudes towards green products and their actual green purchasing behaviour (e.g., Palmero & Montemayor, Citation2020; Sharma et al., Citation2020, Citation2022). On the other hand, current research on the determinants of green purchasing behaviour among firms and their supply chain is relatively underdeveloped (Khan, Yu, Umar, et al., Citation2022; Yang et al., Citation2022). Prior authors have examined antecedents of green purchasing mainly from the perspective of institutional pressures (e.g., Ramakrishnan et al., Citation2015; Yang et al., Citation2022), and dynamic capability view (e.g., Khan, Yu, & Farooq, Citation2022; Khan, Yu, Umar, et al., Citation2022). While there are contrasting views on the cost-benefit analysis of adopting green purchasing in firms’ supply chains (Schaper, Citation2002; Yang et al., Citation2022), there is little, if any, on the theorisation and empirical analysis of the green attitude-behaviour gap at the firm level. Ignoring this paucity in this stream of literature (from the fabrication side) will make it practically impossible to completely bridge the green attitude-behaviour gap.

While the resource-based literature suggests that environmental orientation (EO) is a valuable intangible resource that could inspire firms to enhance environmental performance (Chan et al., Citation2012; Yasir et al., Citation2020), EO has not received paralleled attention in the green purchasing literature. EO is a belief and value-based, or attitudinal construct (Gabler et al., Citation2015; Yasir et al., Citation2020) in that it captures the degree of firms’ recognition of the importance of and their proclivity towards environmental protection (Chan et al., Citation2012). However, prior empirical evidence suggests that environmental consciousness may not necessary guarantee green purchasing behaviour (Barbarossa & Pastore, Citation2015; Chaihanchanchai & Anantachart, Citation2022).

Firms normally face challenges in addressing environmental issues, particularly under conditions of low green capability (Liu et al., Citation2020; Liu et al., Citation2017) and financial resource (Boso et al., Citation2017; Zhang et al., Citation2018). The lack or insufficiency of resources and the necessary capabilities implies that EO may remain a mere cognitive capacity that may never materialise into behaviour. Accordingly, this study draws inferences from the resource orchestration theory (ROT) to argue that green purchasing capability and financial resource (as one of many mechanisms and conditions, respectively) underpin the EO-green purchasing relationship. Green purchasing capability refers to the extent to which a firm has a stock of green purchasing-specific knowledge-base and skills (Khan, Yu, & Farooq, Citation2022; Yook et al., Citation2017). On other hand, financial resource is the extent to which a firm has access to adequate funds to support its activities (Essuman et al., Citation2022; Story et al., Citation2015). Following resource-based literature (Lado et al., Citation1992), we specify EO and financial resource as input-based resources while green purchasing capability is modelled as a transformational resource. From the ROT standpoint (Sirmon et al., Citation2011), we contend that, while EO is essential, it could become dormant when firms fail to or lack what it takes to deploy or act on it, thereby limiting green purchasing. We specifically propose that the influence of EO on green purchasing behaviour will be more pronounced when channelled through green purchasing capability, particularly under conditions of high financial resource. Thus, firms’ efficacy and success in pursuing green purchasing is a function of EO through the transformative mechanism of green purchasing capability, at varying levels of financial resource (He et al., Citation2021). Along with this proposition, the study aims to address two critical questions:

Q1. Does green purchasing mediate the link between EO and green purchasing?

Q2. Does financial resource condition the indirect effect of EO on green purchasing, via green purchasing capability?

In addressing these questions, the study advances knowledge in the green purchasing literature and practice as follows. First, prior studies have identified disparately EO (e.g., Chan et al., Citation2012), green purchasing capability (e.g., J. Liu et al., Citation2020), and financial resource (e.g., Zhang et al., Citation2018) as important enablers of environmental sustainability behaviours and outcomes. This study contributes to research on the determinants of green purchasing by integrating these factors to show how, after controlling for their individual effects, they interface to enhance green purchasing. Second, we contribute to research on EO by responding to calls on scholars to detail the mechanisms and conditions that underlie the environmental outcomes of EO (Keszey, Citation2020). More specifically, in extending the resource-based perspective of the implications of EO (Chan & Ma, Citation2020; Chan et al., Citation2012; Gabler et al., Citation2015), we use ROT to open the “black box” characterising the relationship between EO and green purchasing. We achieve this by identifying and demonstrating an important transformational resource—green purchasing capability—via which EO may foster green purchasing. Additionally, our analysis of the indirect effect of EO as a function of changing financial resource circumstances sheds new light on when the deployment of EO might more or less benefit green purchasing. Ultimately, insights from this article contribute to resolving the green purchasing attitude-behaviour gap (He et al., 2020). We achieve this by bringing the green purchasing attitude-behaviour analysis to the fabrication level, that is, firms and their supply chains. Therefore, we extend this literature stream by departing from the consumer-level analyses that dominate the existing literature. For managers, this article offers practical guidelines on how EO can be orchestrated alongside other organisational resources to boost environmental outcomes.

The remaining sections of the article are organised as follows: the theoretical background and hypotheses development on environmental orientation, financial resource, and green purchasing from the perspective of the ROT are discussed in Section 2. Next, we present the study context and research methodology employed in obtaining the study’s data and validating measurement model analysis in Section 3. The structural model’s results are presented in Section 4, and, lastly, a discussion of research findings and implications is presented as well as the conclusion and limitations in Section 5.

2. Theoretical background and hypothesis development

According to the resource-based literature, firm resources facilitate the conception and implementation of strategies that underpin competitive advantage and superior performance (Barney, Citation1991; Lado et al., Citation1992). The resource orchestration perspective (ROT) extends the resource-based literature by arguing that possessing and controlling some stock of resources is a necessary but insufficient condition for competitive advantage (Sirmon et al., Citation2011). Instead, a sufficient condition of resources for generating competitive advantage and superior performance is captured by the notion of how well the firm organises and deploys such stock of resources (Sirmon et al., Citation2011). The resource orchestration framework describes resource management as encompassing structuring the portfolio of resources (i.e., acquiring, accumulating, and divesting), bundling resources to build capabilities (i.e., stabilising, enriching, and pioneering), and leveraging capabilities in the marketplace (i.e., mobilising, coordinating, and deploying) to create value (Sirmon et al., Citation2011). Resources here refer to all the tangible and intangible valuable assets, skills, knowledge, information, processes, etc., which enable a firm to create and deliver value (Barney, Citation1991). The asset orchestration aspect is composed of searching the operating environment for cues that will inform the selection and configuration of resources and capabilities that fit in the dynamic competitive context (Teece et al., Citation1997). Firms’ resources are also said to engender the development and acquisition of capabilities—that is, the set of competencies that determine the efficiency and effectiveness of transforming input resources into valuable outputs (Grawe et al., Citation2009).

Adopting environmental management practices is usually a difficult task, especially in developing economies where firms face greater levels of financial resource and environmental management-specific capability constraints (Boso et al., Citation2017; Zhang et al., Citation2018). To overcome this, firms need to build diverse but complementary resources and capabilities in their quest to go green (Y. Liu et al., Citation2017). From the ROT perspective of resource-based theory, we reason that, beyond their unique roles, it is possible to structure EO with green purchasing capability and financial resource to drive green purchasing (Sirmon et al., Citation2011). Therefore, as specified in Figure , we suggest that EO, when deployed through or matched with complementary resources including green purchasing capability and financial resource, helps firms increase their success in pursuing green purchasing practices. The current study recognises EO (Chan et al., Citation2012) as an intangible resource, green purchasing capability (J. Liu et al., Citation2020; Yook et al., Citation2017) as a transformative resource/mechanism, and financial resource (Boso et al., Citation2017; Zhang et al., Citation2018) as a boundary conditioning resource, which individually and collectively foster green purchasing practices.

Figure 1. Conceptual model.

2.1. Environmental orientation, green purchasing capability, and green purchasing

EO depicts a corporate firm’s beliefs in environmental responsibilities and the willingness to integrate environmental concerns into its strategic planning (Chan et al., Citation2012; Shou et al., Citation2019). A firm’s EO typically reflects its attitudes towards environmental stewardship and commitment to developing its capacity to actualise environmental goals (Miles & Munilla, Citation1993). Although the performance outcome of EO has received significant attention in environmental research, the empirical evidence is mixed (Yang et al., Citation2022). For example, while most empirical studies have established positive relationships (e.g., Chavez et al., Citation2021; Liboni et al., Citation2022; Zameer et al., Citation2022), others established indirect (e.g., Bu et al., Citation2020; Keszey, Citation2020; Moussa et al., Citation2020), non-significant (Hörisch, Citation2015), or negative (Linder et al., Citation2014) relationships (see Table ). Thus, such inconsistency calls for a theoretical specification and empirical examination of relevant mechanisms that explain the EO-performance outcome.

Table 1. Empirical studies

Scholars argue that green-specific capabilities, consisting of skills, expertise, knowledge, and organisational routines (Khan, Yu, & Farooq, Citation2022; Yee et al., Citation2021), could exist within the purchasing function. Firms are likely to possess and control varying levels of such capabilities, which explains why they perform differently in attaining environmental management goals (Large & Thomsen, Citation2011; Yook et al., Citation2017). Green purchasing practices might be new to firms, particularly in developing markets. Such practices may further be dynamic with respect to changing market and non-market forces (Ramakrishnan et al., Citation2015; Yang et al., Citation2022). Thus, green purchasing capability should be built, protected, and extended through investment in the training and acquisition of new environmental technologies (Khan, Yu, & Farooq, Citation2022; Yook et al., Citation2017). However, not every firm may have relevant input resources (e.g., EO) for developing green purchasing capability, thus, accounting for differences in green purchasing capability among firms (Andersén et al., Citation2020). This suggests that green purchasing capability is a valuable, rare, and difficult-to-acquire resource in a given industry; therefore, it constitutes an important source of competitive advantage in the pursuit of environmental management (Barney, Citation1991). By implication, firms that fall short of green purchasing capability may lack the motivation and confidence to initiate green purchasing.

Drawing on the lens of ROT, we propose that the influence of EO on green purchasing may be explained by green purchasing capability. While EO stimulates managers’ consciousness of their environmental responsibility (Liboni et al., Citation2022; Chavez et al., Citation2021), successful implementation of environmental practices such as green purchasing requires green technical skills and expertise (Andersén et al., Citation2020; Khan, Yu, & Farooq, Citation2022). Since green purchasing capability increases firms’ capacity to achieve green purchasing goals (J. Liu et al., Citation2020; Khan, Yu, & Farooq, Citation2022), firms with strong EO are more likely to recognise and seize opportunities to build their green purchasing capability threshold (Chan & Ma, Citation2020; Chan et al., Citation2012; Large & Thomsen, Citation2011). Thus, deploying EO through green purchasing capability can boost and sustains a firm’s perceived behavioural control (Sharma et al., Citation2022) and success in green purchasing activities. Importantly, green purchasing practices involve not only identifying green and eco-friendly products but also developing green specifications, green supplier selection criteria, and monitoring green activities of suppliers (Yang et al., Citation2022). Such practices require technical skills and expertise in green acquisition. Green purchasing capability thus becomes instrumental as it allows environmentally oriented firms to leverage the embedded resources (i.e., internally and externally) to actualise green purchasing (Bu et al., Citation2020). Accordingly, we argue that firms with strong EO are expected to develop their green purchasing capability, which in turn drives green purchasing practices. This proposition is consistent with Liu et al. (Citation2020) assertion that green training mediates the link between top management support for environmental issues and green procurement. Prior research has also established the link between EO and other green capabilities (Bu et al., Citation2020; Liboni et al., Citation2022; Zameer et al., Citation2022) as well as green-related capabilities to environmental practices (Andersén et al., Citation2020; Khan, Yu, Umar, et al., Citation2022; Yook et al., Citation2017). We therefore test the following hypothesis:

H1.

Green purchasing capability mediates the EO-green purchasing relationship.

2.2. The boundary conditioning effect of financial resource

Recent studies suggest that the benefits of EO might be context-dependent (Chan & Ma, Citation2020; Yasir et al., Citation2020). Thus, notwithstanding H1, we draw on ROT tenets to suggest further that firm motivation to, and efficacy in, leveraging EO through green purchasing capability to achieve green purchasing would be strengthened when EO is bundled simultaneously with a strong financial resource base. Liquid assets are vital input resources in conceiving and implementing resource-intensive activities such as environmental management (Singh et al., Citation2019; Zhang et al., Citation2018). Limited financial resources can be prohibitive to strategic options open to firms. Thus, firms’ strategies and action plans are either dependent on or constrained by financial resources (Story et al., Citation2015; Zhang et al., Citation2018).

Additionally, firms with access to financial resources can better nurture EO (Zhang et al., Citation2018). In particular, high levels of financial resource make it possible for firms to translate EO (a cognitive capacity) into green purchasing capability through building and upgrading infrastructure, skills, and knowledge assets appropriate for supporting green practices (Zhang et al., Citation2018). Therefore, under conditions of a high-level financial resource, the influence of EO on green purchasing capability is more likely to be strengthened. Thus, financial resource availability increases firms’ willingness and readiness to act on EO to facilitate green purchasing capability and consequently achieve green purchasing. In support of these arguments, previous empirical research reveals that not only does financial slack boost top management support for energy saving but also reinforces the positive effect of top management support on energy-saving behaviour (Zhang et al., Citation2018). Furthermore, firms with sufficient financial resource are more likely to be concerned about their reputation (Wang et al., Citation2018). As Wang et al. (Citation2018) indicate, a bad environmental reputation can undermine firms’ relationships with stakeholders, which can further impair their ability to access resources for sustainability practices. Therefore, high levels of financial resource might intensify firms’ motivation to lever on EO to develop green purchasing capability to improve green purchasing.

Conversely, firms with scarce financial resource may be limited in their deployment of EO, reducing its relevance and benefits. Such firms might find the costs of putting EO into action prohibitively high with doubtful payback in a reasonable timeframe (Yang et al., Citation2022). To these firms, survival and profitability are paramount; therefore, they tend to focus on utilising their scarce financial resources to meet immediate needs and maximise profits (Wang et al., Citation2018). This may further obscure or divert their orientation towards green initiatives. Thus, firms with limited financial resource are more inclined to respond to environmental protection needs in a ceremonial way (Wang et al., Citation2018). Accordingly, we expect that firms’ potency to use EO to increase green purchasing capability and consequently enhance green purchasing may be weakened under conditions of low financial resource. Taken together, we hypothesise that:

H2.

The interaction between EO and financial resource has a positive indirect effect, via green purchasing capability, on green purchasing, such that, under high conditions of financial resource, the positive effect of EO, through green purchasing capability, on green purchasing is amplified.

3. Methods

3.1. Data and sample

We tested our conceptual model on questionnaire-based survey data (Danso et al., Citation2019; Y. Liu et al., Citation2017; Yasir et al., Citation2020) from firms in Ghana for the following reasons. Ghana remains a major economic force in the sub-Saharan African region and is recognised as one of the top 10 fastest-growing economies in the world, owing, in part, to increases in production and consumption activities (Africa Development Bank Group, Citation2020). Recognising the implication of the growing economic activities on the environment, the government of Ghana has recently initiated market and industrial reforms aimed at encouraging firms to adopt environmentally friendly initiatives in their supply chains (Amankwah‐Amoah et al., Citation2019). Nonetheless, financial resource is a rare and difficult-to-acquire organisational resource in Ghana as the financial and capital markets in the country are underdeveloped (African Development Bank Group, 2018). Again, as in most developing economies (Chan & Ma, Citation2020), most firms in Ghana are small and medium enterprises, which struggle to develop relevant internal capabilities. By implication, financial resource and green purchasing capability are critical sources of competitive advantage for firms in Ghana to pursue environmental management practices.

We relied on Ghana Yellow and Ghana Business Directory databases to construct a sample of firms that meet the following inclusion criteria: that the firm (1) operates in key industrialised/commercialised cities in Ghana (i.e., Accra and Kumasi), (2) is an autonomous business entity, owned and controlled by private individuals; (3) has been operating for at least two years; (4) employs a minimum of five full-time staff; (5) has a senior manager (e.g., CEO, purchasing/supply chain manager) who agreed to participate in the study (Amankwah-Amoah et al., 2019). We started the fieldwork in 2020 after the COVID-19 pandemic restrictions in Ghana were lifted. While in the face of the COVID-19 pandemic, mail and online surveys are ideal, such survey approaches, compared to a face-to-face approach, are less suitable in Ghana. Using a professional data collection agency, which worked closely with and under the direct supervision of the authors, 503 questionnaires were hand-delivered to senior managers (e.g., CEOs, purchasing managers) from firms that meet the inclusion criteria indicated above (Amankwah-Amoah et al., 2019; Zhang et al., Citation2018).

In all, a total of 181 complete responses were received after three follow-ups. Out of this, 165 (corresponding to a 32.8% effective response rate) which had complete responses or met the study’s sample inclusion criteria were retained for analysis. Overall, 72.7%, 15.8%, and 11.5% of the sample operate in the service sector, manufacturing sector, mining/extraction sector, and agribusiness sector respectively. An average firm had operated for 13.67 years (standard deviation = 8.97). Also, an average firm had 26.13 full-time employees (standard deviation = 42.41), suggesting that most of them are small and medium-sized enterprises. Respondents holding top management positions (CEOs/owner-managers) comprised 30.9% of the sample. The remaining percentage were senior managers in purchasing/supply chain management/operations units. A total of 67.8% of the respondents had either a bachelor’s or post-graduate degree while the remaining had either diploma or college qualifications. On average, the respondents had 8.53 years of managerial experience.

3.2. Measurement items

Existing items were used to measure the study’s constructs. Pre-testing was conducted to help revise (where necessary) and retain items that are deemed applicable in the research setting. A full description of the items is shown in Table . Five items were adapted from Chan et al. (Citation2012) to measure EO using a seven-point scale (1 = strongly disagree; 7 = strongly agree). Green purchasing capability was measured with five items, which were adapted from Yook et al. (Citation2017). Each item was anchored on a seven-point ranging from “not at all” ( = 1) to “to a great extent” ( = 7). Five items were adapted from Carter and Jennings (Citation2004) and Chan et al. (Citation2012) to measure green purchasing using a seven-point scale ranging from “not at all” ( = 1) to “to an extreme extent” ( = 7). Four items were adopted from Story et al. (Citation2015) to measure financial resource. Each item was rated on a seven-point scale ranging from “strongly disagree” ( = 1) to “strongly agree” ( = 7). Consistent with prior research, we included firm size, firm age, and industry type as control variables in our analysis (Adomako et al., Citation2019; Y. Liu et al., Citation2017). Firm size and firm age were operationalised as the natural logarithm of full-time employees and the number of years a firm has been in operation, respectively. A dummy variable was created for industry type: service firms = 1, other firms = 0.

Table 2. Measures and validity and reliability results

3.3. Measurement validity and reliability

We examined unidimensionality, reliability, convergent validity, and discriminant validity using covariance-based confirmatory factor analysis in Mplus 7.4. As shown in Table , to ensure a simultaneous evaluation of these aspects of reliability and validity, we conducted CFA on all the measures for the four latent variables in the study. Our four-factor CFA model fits the data satisfactorily: χ2 = 242.71, df = 183, χ2/df = 1.33, RMSEA =.05, NNFI =.97, CFI =.97, SRMR =.04 (Bagozzi & Yi, Citation2012; Hair et al., Citation2014). Additionally, the factor loadings were all positive and greater than .50 and significant at 1.00%. The results further show that composite reliability and average variance extracted values for each measurement set are larger than the recommended minimum thresholds of .60 and .50 respectively (Bagozzi & Yi, Citation2012; Hair et al., Citation2014). Together, these results demonstrate that the measures are reliable and exhibit unidimensionality and convergent validity. Following Hair et al. (Citation2014) recommendation, we assessed discriminant validity by comparing the average variance extracted values with the shared variances between each pair of the measures (see Table ). The highest shared variance in the study is .24, which is far below the lowest average variance extracted value of .61, indicating that the measures exhibit discriminant validity (Hair et al., Citation2014).

Table 3. Descriptive statistics, correlations, and average variance extracted values

3.4. Respondent competence and survey bias assessment

As indicated earlier, to minimise measurement error, we collected the data from CEOs/owner-managers and purchasing/supply chain managers who are educated and have adequate managerial experience. Following prior research, we specifically examined their competence level further using a four-item measure anchored on a seven-point scale (1 = strongly disagree; 7 = strongly agree) (Boso et al., Citation2013). Results indicate that the respondents are generally competent, given that an average respondent’s score for each item was above the median point of the scale (Boso et al., Citation2013): “I have adequate knowledge on the issues I provided responses on” (mean = 5.53, standard deviation =.91); “I clearly understood all the items I provided responses on” (mean = 5.52, standard deviation = 1.05); “I am very confident in the responses I provided” (mean = 5.58, standard deviation = 1.05); “I am sure that the responses I provided represent the situation in my company” (mean = 5.59, standard deviation =.92).

To assess the likelihood of nonresponse bias in the study, we performed t-test to compare the data provided by early respondents (n = 107) and late respondents (n = 58): green purchasing capability (mean difference =.07, t = .28), green purchasing (mean difference = −.27, t = −1.35), EO (mean difference = −.37, t = −1.81), firm size log (mean difference =.04, t = .27), firm age log (mean difference = −.19, t = −1.88). The results reveal no significant difference between the two groups, suggesting that nonresponse bias does not characterise the data (Armstrong & Overton Citation1977).

Although we followed key recommended procedural measures to minimise common method bias (CMB), it became necessary to statistically examine the extent to which it might characterise the data (Podsakoff et al., Citation2012). Specifically, we used Lindell and Whitney’s marker variable (MV) approach (Williams et al., Citation2010). We used our four-item scale respondent competence scale described above as an MV as it meets the conditions of a marker variable: it is theoretically and empirically (see Table ) unrelated to the substantive variables of interest and has good internal consistency (α = .78). We used the lowest positive correlation between the MV and the substantive variables (r = .03) to compute the MV adjusted correlations (Podsakoff et al., Citation2012). The results (Table ) show that the zero-order correlations and the MV-adjusted correlations are largely similar in terms of direction, magnitude, and statistical significance, further suggesting that CMB is unlikely to be a concern in the study (Podsakoff et al., Citation2012). Indeed, research evidence suggests that theoretically specified conditional effect models, as in the case of our conceptual model, are less likely to be biased by common method variance (Podsakoff et al., Citation2012). Moreover, the variance inflation factor (VIF) values reported in Table are all less than 2, suggesting that the variables in the study are not excessively intercorrelated to warrant that multicollinearity is a problem (Hair et al., Citation2014). This is further corroborated by the moderate pairwise correlation among the substantive variables of the study.

4. Results

4.1. Hypothesis testing

Table shows the descriptive statistics for, and correlations between, the study variables. We estimated our conceptual model (Figure ) using a covariance-based structural equation modelling (SEM) in Mplus 7.4, given its capacity to control for measurement errors and analysing mediation and moderation models (Bagozzi & Yi, Citation2012). We specifically used bootstrapping procedures in Mplus 7.4 to test our indirect (H1) and conditional indirect (H2) hypotheses (Aguinis et al., Citation2017). We included firm size, firm age, firm industry, and financial resource as controls in models of green purchasing capability and green purchasing. Table shows the results for the direct and indirect effects model (Model 1) and conditional direct and indirect effects model (Model 2) from the analyses. Results show that Model 2 is superior to Model 1: Δ χ2 = 7.94, Δdf = 1, p < .01.Accordingly, we evaluated all estimated effects based on Model 2 results (Aguinis et al., Citation2017).

Table 4. Structural equation modelling results

Results indicate that EO has significant positive effects on green purchasing capability (β = .37, t = 2.94) and green purchasing (β = .54, t = 4.69), and that green purchasing capability has a significant positive effect on green purchasing (β = .22, t = 2.96). Additional results reveal that, over the main effects of EO and financial resource, the interaction between these variables has a significant positive effect on green purchasing (β = .15, t = 2.80). Of particular interest, the results support H1: EO has a significant positive indirect effect, via green purchasing capability, on green purchasing, given an indirect effect =.08 and associated 95% bootstrapping confidence interval ranging from .03 to .15. Further results are in support of H2: the interaction between EO and financial resource has a positive indirect effect, via green purchasing capability, on green purchasing, given an indirect effect =.03 and associated 95% bootstrapping confidence interval ranging from .01 to .07.

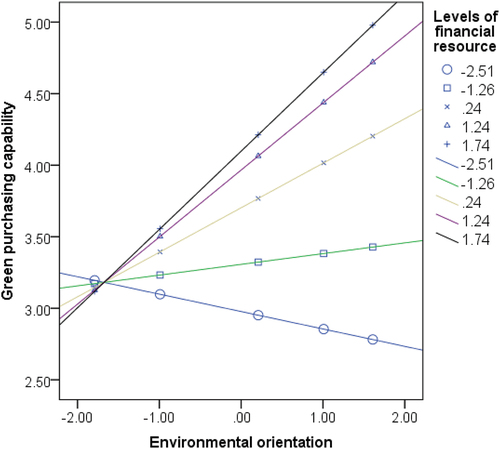

To assess the robustness of these results and generate further insights, we relied on PROCESS for SPSS. PROCESS provides researchers with one-stop resources (e.g., bootstrapping procedures) for directly testing the statistical significance and visualising mediation and moderated-mediation effects models (Hayes, Citation2018), which is relatively easier compared to the SEM platforms. The PROCESS analysis yielded results that are consistent with the SEM results. As shown in Figure , it additionally revealed that the effect of EO on green purchasing capability strengthens at increasing levels of financial resource. In contrast, at lower levels of financial resource, the link between EO and green purchasing capability tends to be negative. Further analysis shows that a significant conditional indirect effect of EO via green purchasing capability on green purchasing occurs for the 50th and above percentile values of financial resource. Specifically, as plotted in Figure , the indirect effect of EO, through green purchasing capability, on green purchasing amplifies when EO is deployed under high conditions of financial resource, supporting H2.

Figure 2. Surface of the effect of EO on green purchasing capability at changing conditions of financial resource.

Figure 3. Surface of the indirect effect of EO, via green purchasing capability, on green purchasing at changing conditions of financial resource.

5. Discussions

5.1. Theoretical implications

Green purchasing is central to the environmental management agenda. There is a growing belief that increased EO will improve a firm’s strategic responses towards green purchasing (Chan et al., Citation2012; Shou et al., Citation2019). However, not only is this belief yet to be fully validated but also the nuances regarding the EO-environmental outcomes such as green purchasing relationships are underexplored (Keszey, Citation2020). In this research, we used ROT to develop a model that suggests that considering just the direct associations between EO and environmental management behaviours provides an incomplete account. Instead, we suggest that the green attitude-behaviour link is quite complex (He et al., 2020); therefore, improper theoretical and empirical specifications of EO and environment management behaviours may lead to wrong nomological conclusions and recommendations. Accordingly, and following calls for researchers to clarify how and when EO is beneficial (Keszey, Citation2020), we theorise and empirically assess the intervening role of green purchasing capability—a rarely studied capability (Khan, Yu, & Farooq, Citation2022)—in the EO-green purchasing relationship. Also, while environmental initiatives may be cost-intensive (Yang et al., Citation2022), prior environmental research on the antecedents of green purchasing seems to assume that the availability and access to funding are homogeneous across firms. We extend the green purchasing-attitude behaviour literature by examining how financial resource combines simultaneously with EO to determine green purchasing via green purchasing capability. Our empirical results are consistent with our theoretical predictions.

First, our empirical analysis reveals that the relationship between EO and green purchasing is mediated by green purchasing capability. This confirms our thesis that green purchasing capability is one of several transformative capabilities that bridge the EO-green purchasing link (He et al., 2020), and thus the ROT’s input-transformation-output resources framework (Sirmon et al., Citation2011). This finding provides credence to prior empirical studies that found a positive association between EO and environmental innovations and capabilities (Liboni et al., Citation2022; Yasir et al., Citation2020), between EO and environmental performance (Liboni et al., Citation2022; Moussa et al., Citation2020; Zameer et al., Citation2022; Zhang et al., Citation2018), and between green purchasing capability and green purchasing practice (Khan, Yu, & Farooq, Citation2022; Khan, Yu, Umar, et al., Citation2022). This finding further reinforces the literature that purchasing capability is a critical factor in explaining environmental management behaviours and a significant intervening force in explicating how EO may be beneficial (J. Liu et al., Citation2020; Singh et al., Citation2019). Further, our study integrates the existing literature to provide a single snapshot of why and how EO influences green purchasing at the firm and supply chain level. By so doing, we contribute to addressing the green purchasing attitude-behaviour gap by bringing the discussion to the firm level and reconciling inconsistencies in prior studies on the EO-performance link.

Second, our findings show that financial resource interacts with EO to drive green purchasing via green purchasing capability. This finding reinforces our ROT argument that EO, as an organisational resource, could be configured with other resources such as green purchasing capability and financial resource to improve green purchasing (Sirmon et al., Citation2011). This finding is consistent with the assertion that firms’ strategies and action plans are either dependent on or constrained by financial resource (Story et al., Citation2015; Zhang et al., Citation2018). For instance, Zhang et al. (Citation2018) find that financial slack not only drives top management support for energy-saving measures but also amplifies the potency of this variable in enhancing energy saving. Especially, given the study’s context as a developing economy where firms usually face difficulty in accessing funding and, if they can, it is at a high cost (Boso et al., Citation2017), greater levels of financial resource could boost firms’ efficacy regarding environmental management. Such conditions have the potential to amplify and sustain firms’ motivation and commitment to act on EO to achieve greater levels of green purchasing via green purchasing capability. A major theoretical implication from this finding is that the resources do not operate in isolation to drive performance, but ought to be carefully bundled, and then orchestrated to achieve a specific performance outcome (Sirmon et al., Citation2011). Again, this finding challenges the popular adage that necessity is the mother of inventions, to add that it (in this case, green purchasing) depends on the availability and level of the necessary support resources and capabilities. Broadly, this finding suggests that conditional process models could play useful roles in helping resolve attitude-behaviour gaps in environmental management. More specifically, the study extends the green purchasing literature by providing a nuanced picture of the link between EO and green purchasing.

5.2. Managerial implications

Our study has some practical implications. First, the study reminds managers of the importance of nurturing a corporate environmental culture and improving their sensitivity to the global environmental demands for greener business practices. In particular, the findings inform industrial practice and senior executives about the essential role of EO in promoting green purchasing. To this end, and as Chan et al. (Citation2012) suggest, senior executives are encouraged to leverage their influence to facilitate the infusion of environmental consciousness, which entails changing habits and making pro-environmental choices as a matter of daily routine within their organisations.

The findings also provide insight for logistics and supply chain executives in their quest to demonstrate environmental responsibilities. The research shows that the green purchasing consequence of EO may be salient when firms develop green purchasing capability. Therefore, allocating significant effort to build, extend, and safeguard a firm’s green purchasing capability is critical for transforming EO into green purchasing. Thus, logistics operations managers need to organise frequent workshops, seminars and green training to build green culture and mentality among employees to actualise their environmental stewardship mindset. Also, the development of logistics capabilities building programmes should incorporate an environmental mindset to groom a cadre of logistics professionals whose capabilities will be congruent with environmental goals.

Moreover, supply chain practitioners should note that green purchasing capability may require substantial financial resource commitment. Thus, when the financial resource is low, top executives would have little motivation to act on EO to drive green purchasing capability. Following this, top executives should not assume that increasing EO alone without a corresponding increment in financial resource and green purchasing capability will result in high levels of green purchasing. Instead, in their quest to adopt green purchasing, practitioners should endeavour to build and allocate the necessary financial resource for support. This will ensure that firms amplify their efficacy in the operationalisation of EO to achieve green purchasing objectives.

5.3. Conclusion

The green purchasing perspective holds significant promises for advancing sustainable development goals; therefore, understanding its critical determinants is imperative. This research builds on the EO literature and ROT logic to develop a framework to describe how EO combines with green purchasing capability and financial resource to enhance green purchasing in a developing economy. A novel insight from this research is that, over and above the individual environmental value of EO, green purchasing capability, and financial resource, leveraging EO under high financial resource conditions through green purchasing capability amplifies green purchasing. A key contribution of the study lies in its ability to account for a mechanism and a condition under which firms’ EO impacts green purchasing. Thus, the study extends the environmental management research domain by integrating resource orchestration theory with environmental sustainability literature to empirically examine how EO drives green purchasing practices, via green purchasing capability under varying levels of financial resource. Significantly, while firms are encouraged to develop EO (responsible attitude and mindset towards the environment), it may not be enough to result in sustainable green behaviour. Rather, firms need to bundle their EO with financial resource to help build green purchasing (technical expertise) capability to better translate their environmental attitude into actual behaviour.

5.4. Limitations and future research directions

Despite the theoretical and practical insight, the study’s findings, as with any study, should be evaluated in light of certain theoretical and methodological limitations that can stimulate further theorisation and empirical analyses. First, while cross validating the present model in different contexts (e.g., countries, industry, and firm size) and or using different methods (e.g., longitudinal survey, multiple sources of data) is necessary, future research may test the model in relation to other environmental outcomes such as green manufacturing and green marketing to generate additional insights (see Yasir et al., Citation2020). Second, consistent with resource-based literature, many scholars may agree that financial resource and green capabilities are important organisational resources for facilitating strategy implementation (Khan, Yu, & Farooq, Citation2022). However, among other things, the capacity of financial resource or green capabilities to create competitive advantage is a function of the extent to which these resources are scarce in a given industry, or how difficult it is for firms to raise and control such resources, relative to competitors. Therefore, it can be expected that the predictive power and accuracy of our model would vary across developing, emerging, and advanced markets as access to finance and training on green issues could vary significantly across these markets. In effect, datasets from developing markets limits the generalisation of the model developed in this study. Therefore, future research should consider emerging and developed markets. Finally, it is shown in this research that conditional process models of EO could generate more insightful findings. Further research should explore additional relevant conditional processes that link EO to green purchasing or other environmental outcomes.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Emmanuel Kwabena Anin

Dr. Emmanuel Kwabena Anin is a Senior Lecturer at the Department of Procurement and Supply Chain Management, Kumasi Technical University, Ghana. Dr. Anin’s current research interests revolve around the interface between institutional environment, governance of inter-firm relationship, procurement management, and supply chain performance. His research has been published in reputable journals, including the Journal of Purchasing and Supply Management, Africa Journal of Management, International Journal of Public Administration, Journal of Inter-Organizational Relationships, and International Journal of Quality and Service Sciences.

Henry Ataburo

Dr. Henry Ataburo holds a PhD in Logistics and Supply Chain from the School of Business, Kwame Nkrumah University of Science and Technology. He is currently researching into Sustainability and Resilience in Transport Logistics firms for his PhD. His research interests include logistics and supply chain operations with a focus on technology and strategic orientation for sustainability and resilience. He works as a research fellow at the ORTaRChI (Oliver and Reginald Tambo Research Chair Institute) at the KNUST School of Business.

Getrude Effah Ampong

Ms. Getrude Effah Ampong is a final year MPhil candidate, Center for Applied Research and Innovation in Supply Chain-Africa (CARISCA), Kwame Nkrumah University of Science and Technology. She is currently researching supply chain responsiveness and the performance of logistics service providers. She holds a BTech. in Procurement and Supply Chain Management.

Nana Dwomoh Osei Bempah

Ms. Nana Dwomoh Osei Bempah is a PhD candidate at the University of Southampton, UK.

References

- Aboelmaged, M. (2018). Direct and indirect effects of eco-innovation, environmental orientation and supplier collaboration on hotel performance: An empirical study. Journal of Cleaner Production, 184, 537–23. https://doi.org/10.1016/j.jclepro.2018.02.192

- Adomako, S., Amankwah‐amoah, J., Danso, A., Konadu, R., & Owusu‐agyei, S. (2019). Environmental sustainability orientation and performance of family and nonfamily firms. Business Strategy and the Environment, 28(6), 1250–1259.

- African Development Bank Group (2020)2020. African Economic Outlook: Developing Africa’s Workforce for the Future. https://www.afdb.org/en/knowledge/publicati ons/african-economic-outlook. Agusti,

- Aguinis, H., Edwards, J. R., & Bradley, K. J. (2017). Improving Our Understanding of Moderation and Mediation in Strategic Management Research. Organizational Research Methods, 20(4), 665–685. https://doi.org/10.1177/1094428115627498

- Amankwah‐amoah, J., Danso, A., & Adomako, S. (2019). Entrepreneurial orientation, environmental sustainability and new venture performance: Does stakeholder integration matter?. Business Strategy and the Environment, 28(1), 79–87.

- Andersén, J., Jansson, C., & Ljungkvist, T. (2020). Can environmentally oriented CEOs and environmentally friendly suppliers boost the growth of small firms? Business Strategy and the Environment, 29(2), 325–334. https://doi.org/10.1002/bse.2366

- Ardito, L., Raby, S., Albino, V., & Bertoldi, B. (2021). The duality of digital and environmental orientations in the context of SMEs: Implications for innovation performance. Journal of Business Research, 123(February 2020), 44–56. https://doi.org/10.1016/j.jbusres.2020.09.022

- Armstrong, J. S., & Overton, T. S. (1977). Estimating Nonresponse Bias in Mail Surveys. Journal of Marketing Research, 14(3), 396. https://doi.org/10.2307/3150783

- Bagozzi, R. P., & Yi, Y. (2012). Specification, evaluation, and interpretation of structural equation models. Journal of the Academy of Marketing Science, 40(1), 8–34. https://doi.org/10.1007/s11747-011-0278-x

- Barbarossa, C., & Pastore, A. (2015). Why environmentally conscious consumers do not purchase green products: A cognitive mapping approach. Qualitative Market Research, 18(2), 188–209. https://doi.org/10.1108/QMR-06-2012-0030

- Barney, J. (1991). Firm Resources and Sustained Competitive Advantage. Journal of Management, 17(1), 99–120. https://doi.org/10.1177/014920639101700108

- Boso, N., Donbesuur, F., Bendega, T., Annan, J., & Adeola, O. (2017). Does organizational creativity always drive market performance? Psychology & Marketing, 34(11), 1004–1015. https://doi.org/10.1002/mar.21039

- Boso, N., Story, V. M., Cadogan, J. W., Micevski, M., & Kadi, S. (2013). Firm Innovativeness and Export Performance: Environmental, Networking, and Structural. Jounal of International Marketing, 21(4), 62–87. https://doi.org/10.1509/jim.13.0052

- Bu, X., Dang, W. V. T., Wang, J., & Liu, Q. (2020). Environmental orientation, green supply chain management, and firm performance: Empirical evidence from Chinese small and medium-sized enterprises. International Journal of Environmental Research and Public Health, 17(4), 1–17. https://doi.org/10.3390/ijerph17041199

- Carter, C. R., & Jennings, M. M. (2004). The role of purchasing in corporate social responsibility: A structural equation analysis. Journal of Business Logistics, 25(1), 145–186.

- Chaihanchanchai, P., & Anantachart, S. (2022, August). Encouraging green product purchase: Green value and environmental knowledge as moderators of attitude and behavior relationship. Business Strategy and the Environment, 2021(1), 1–15. https://doi.org/10.1002/bse.3130

- Chan, R. Y. K., He, H., Chan, H. K., & Wang, W. Y. C. (2012). Environmental orientation and corporate performance: The mediation mechanism of green supply chain management and moderating effect of competitive intensity. Industrial Marketing Management, 41(4), 621–630. https://doi.org/10.1016/j.indmarman.2012.04.009

- Chan, R. Y. K., & Ma, K. H. Y. (2016). Environmental Orientation of Exporting SMEs from an Emerging Economy: Its Antecedents and Consequences. Management International Review, 56(5), 597–632. https://doi.org/10.1007/s11575-016-0280-0

- Chan, R. Y. K., & Ma, K. H. Y. (2020). How and when environmental orientation drives corporate sustainable development in a cross-national buyer–supplier dyad. Business Strategy and the Environment, 30(1), 109–121. https://doi.org/10.1002/bse.2612

- Chavez, R., Malik, M., Ghaderi, H., & Yu, W. (2021). Environmental orientation, external environmental information exchange and environmental performance: Examining mediation and moderation effects. International Journal of Production Economics, 240, 108222. https://doi.org/10.1016/j.ijpe.2021.108222

- Coşkun, A., Vocino, A., & Polonsky, M. (2017). Mediating effect of environmental orientation on pro-environmental purchase intentions in a low-involvement product situation. Australasian Marketing Journal, 25(2), 115–125. https://doi.org/10.1016/j.ausmj.2017.04.008

- Danso, A., Adomako, S., Amankwah-Amoah, J., Owusu-Agyei, S., & Konadu, R. (2019). Environmental sustainability orientation, competitive strategy and financial performance. Business Strategy and the Environment, 28(5), 885–895. https://doi.org/10.1002/bse.2291

- Dickel, P., Hörisch, J., & Ritter, T. (2018). Networking for the environment: The impact of environmental orientation on start-ups’ networking frequency and network size. Journal of Cleaner Production, 179, 308–316. https://doi.org/10.1016/j.jclepro.2018.01.058

- ElTayeb, T. K., Zailani, S., & Jayaraman, K. (2010). The examination on the drivers for green purchasing adoption among EMS 14001 certified companies in Malaysia. Journal of Manufacturing Technology Management, 21(2), 206–225. https://doi.org/10.1108/17410381011014378

- Essuman, D., Bruce, P. A., Ataburo, H., Asiedu-Appiah, F., & Boso, N. (2022). Linking resource slack to operational resilience: Integration of resource-based and attention-based perspectives. International Journal of Production Economics, 254(October 2021), 108652. https://doi.org/10.1016/j.ijpe.2022.108652

- Gabler, C. B., Richey, R. G., & Rapp, A. (2015). Developing an eco-capability through environmental orientation and organizational innovativeness. Industrial Marketing Management, 45(1), 151–161. https://doi.org/10.1016/j.indmarman.2015.02.014

- Grawe, S. J., Chen, H., & Daugherty, P. J. (2009). The relationship between strategic orientation, service innovation, and performance. International Journal of Physical Distribution & Logistics Management, 39(4), 282–300. https://doi.org/10.1108/09600030910962249

- Hair, J. F. J., Black, W. C., Babin, B. J., & Anderson, R. E. (2014). Multivariate Data Analysis (7TH ed.). Pearson Education Limited.

- Hayes, A. F. (2018). Introduction to mediation, moderation, and conditional process analysis: A regression-based approach. The Guilford Press. https://doi.org/10.1016/j.jclepro.2019.118524

- He, Z., Zhou, Y., Wang, J., Li, C., Wang, M., & Li, W. (2021). The impact of motivation, intention, and contextual factors on green purchasing behavior: New energy vehicles as an example. Business Strategy and the Environment, 30(2), 1249–1269. https://doi.org/10.1002/bse.2682

- Hörisch, J. (2015). Crowdfunding for environmental ventures: An empirical analysis of the influence of environmental orientation on the success of crowdfunding initiatives. Journal of Cleaner Production, 107, 636–645. https://doi.org/10.1016/j.jclepro.2015.05.046

- Hsu, P. F., Hu, P. J. H., Wei, C. P., & Huang, J. W. (2014). Green Purchasing by MNC Subsidiaries: The Role of Local Tailoring in the Presence of Institutional Duality. Decision Sciences, 45(4), 647–682. https://doi.org/10.1111/deci.12088

- Keszey, T. (2020). Environmental orientation, sustainable behaviour at the firm-market interface and performance. Journal of Cleaner Production, 243, 118524.

- Khan, S. A. R., Yu, Z., & Farooq, K. (2022). Green capabilities, green purchasing, and triple bottom line performance: Leading toward environmental sustainability. Business Strategy and the Environment, 1–13. https://doi.org/10.1002/bse.3234

- Khan, S. A. R., Yu, Z., & Sharif, A. (2021). No Silver Bullet for De-carbonization: Preparing for Tomorrow, Today. Resources Policy, 71(November 2020), 101942. https://doi.org/10.1016/j.resourpol.2020.101942

- Khan, S. A. R., Yu, Z., Umar, M., & Tanveer, M. (2022). Green capabilities and green purchasing practices: A strategy striving towards sustainable operations. Business Strategy and the Environment, 31(4), 1719–1729. https://doi.org/10.1002/bse.2979

- Lado, A. A., Boyd, N. G., & Wright, P. (1992). A competency-based model of sustainable competitive advantage: Toward a conceptual integration. Journal of Management, 18(1), 77–91. https://doi.org/10.1177/014920639201800106

- Large, R. O., & Thomsen, C. G. (2011). Drivers of green supply management performance: Evidence from Germany. Journal of Purchasing & Supply Management, 17(3), 176–184. https://doi.org/10.1016/j.pursup.2011.04.006

- Lefevre, C., Pellé, D., Abedi, S., Martinez, R., & Thaler, P. F. (2010). Value of sustainable procurement practices: A quantitative analysis of value drivers associated with sustainable procurement practices. PwC and EcoVadis in collaboration with the INSEAD Social Innovation Centre. Available at: (accessed 3 October 2021).http://saulnierconseil.com/wp-content/uploads/2011/01/Value-of-Sustainable-Suppliers-INSEAD-Dec-2010.pdf

- Liboni, L. B., Cezarino, L. O., Alves, M. F. R., Chiappetta Jabbour, C. J., & Venkatesh, V. G. (2022). Translating the environmental orientation of firms into sustainable outcomes: The role of sustainable dynamic capability. Review of Managerial Science, 17(4), 1–22. https://doi.org/10.1007/s11846-022-00549-1

- Linder, M., Björkdahl, J., & Ljungberg, D. (2014). Environmental orientation and economic performance: A Quasi-experimental study of small Swedish firms. Business Strategy and the Environment, 23(5), 333–348. https://doi.org/10.1002/bse.1788

- Liu, J., Liu, Y., & Yang, L. (2020). Uncovering the influence mechanism between top management support and green procurement: The effect of green training. Journal of Cleaner Production, 251, 119674. https://doi.org/10.1016/j.jclepro.2019.119674

- Liu, Y., Zhu, Q., & Seuring, S. (2017). Linking capabilities to green operations strategies: The moderating role of corporate environmental proactivity. International Journal of Production Economics, 187, 182–195. https://doi.org/10.1016/j.ijpe.2017.03.007

- Menguc, B., & Ozanne, L. K. (2005). Challenges of the “green imperative”: A natural resource-based approach to the environmental orientation–business performance relationship. Journal of Business Research, 58(4), 430–438. https://doi.org/10.1016/j.jbusres.2003.09.002

- Miles, M. P., & Munilla, L. S. (1993). The eco-orientation: An emerging business philosophy? Journal of Marketing Theory & Practice, 43–51. https://www.jstor.org/stable/40469669

- Moussa, T., Allam, A., Elbanna, S., & Bani-Mustafa, A. (2020). Can board environmental orientation improve U.S. firms’ carbon performance? The mediating role of carbon strategy. Business Strategy and the Environment, 29(1), 72–86. https://doi.org/10.1002/bse.2351

- Palmero, K. L., & Montemayor, C. T. (2020). An analysis on the factors influencing green purchase intention among young consumers in the Philippine BPO industry. Polish Journal of Management Studies, 22(1), 371–384. https://doi.org/10.17512/pjms.2020.22.1.24

- Podsakoff, P. M., MacKenzie, S. B., & Podsakoff, N. P. (2012). Sources of method bias in social science research and recommendations on how to control it. Annual Review of Psychology, 63(1), 539–569. https://doi.org/10.1146/annurev-psych-120710-100452

- Polonsky, M. J., Vocino, A., Grimmer, M., & Miles, M. P. (2014). The interrelationship between temporal and environmental orientation and pro-environmental consumer behaviour. International Journal of Consumer Studies, 38(6), 612–619. https://doi.org/10.1111/ijcs.12131

- Ramakrishnan, P., Haron, H., & Goh, Y. N. (2015). Factors influencing green purchasing adoption for small and medium enterprises (SMEs) in malaysia. International Journal of Business and Society, 16(1), 39–56. https://doi.org/10.33736/ijbs.552.2015

- Saleem, F., Qureshi, S. S., & Malik, M. I. (2021). Impact of environmental orientation on proactive and reactive environmental strategies: Mediating role of business environmental commitment. Sustainability (Switzerland), 13(15), 8361. https://doi.org/10.3390/su13158361

- Salvador, R. O., & Burciaga, A. (2020). Organizational environmental orientation and employee environmental in-role behaviors: A cross-level study. Business Ethics, 29(1), 98–113. https://doi.org/10.1111/beer.12241

- Schaper, M. (2002). Small firms and environmental management. International Small Business Journal, 20(3), 235–251. https://doi.org/10.1177/0266242602203001

- Sharma, N., Lal, M., Goel, P., Sharma, A., & Rana, N. P. (2022). Being socially responsible: How green self-identity and locus of control impact green purchasing intentions? Journal of Cleaner Production, 357(September 2021), 131895. https://doi.org/10.1016/j.jclepro.2022.131895

- Sharma, N., Saha, R., Sreedharan, V. R., & Paul, J. (2020). Relating the role of green self-concepts and identity on green purchasing behaviour: An empirical analysis. Business Strategy and the Environment, 29(8), 3203–3219. https://doi.org/10.1002/bse.2567

- Shevchenko, A., Pan, X., & Calic, G. (2020). Exploring the effect of environmental orientation on financial decisions of businesses at the bottom of the pyramid: Evidence from the microlending context. Business Strategy and the Environment, 29(5), 1876–1886. https://doi.org/10.1002/bse.2476

- Shou, Y., Shao, J., Lai, K. H., Kang, M., & Park, Y. (2019). The impact of sustainability and operations orientations on sustainable supply management and the triple bottom line. Journal of Cleaner Production, 240, 118280. https://doi.org/10.1016/j.jclepro.2019.118280

- Singh, S. K., Chen, J., Del Giudice, M., & El-Kassar, A. N. (2019). Environmental ethics, environmental performance, and competitive advantage: Role of environmental training. Technological Forecasting & Social Change, 146, 203–211. https://doi.org/10.1016/j.techfore.2019.05.032

- Sirmon, D. G., Hitt, M. A., Ireland, R. D., Gilbert, B. A., Barney, J. B., Ketchen, D. J., & Wright, M. (2011). Resource orchestration to create competitive advantage: Breadth, depth, and life cycle effects. Journal of Management, 37(5), 1390–1412. https://doi.org/10.1177/0149206310385695

- Song, H., Yu, K., & Zhang, S. (2017). Green procurement, stakeholder satisfaction and operational performance. The International Journal of Logistics Management, 28(4), 1054–1077. https://doi.org/10.1108/IJLM-12-2015-0234

- Story, V. M., Boso, N., & Cadogan, J. W. (2015). The form of relationship between firm‐level product innovativeness and new product performance in developed and emerging markets. Journal of Product Innovation Management, 32(1), 45–64. https://doi.org/10.1111/jpim.12180

- Teece, D. J., Pisano, G., & Shuen, A. (1997). Dynamic Capabilities. Strategic Management, 18(7), 509–533.

- Van Zanten, J. A., & Van Tulder, R. (2018). Multinational enterprises and the Sustainable Development Goals: An institutional approach to corporate engagement. Journal of International Business Policy, 1(3–4), 208–233. https://doi.org/10.1057/s42214-018-0008-x

- Wang, S., Li, J., & Zhao, D. (2018). Institutional pressures and environmental management practices: The moderating effects of environmental commitment and resource availability. Business Strategy and the Environment, 27(1), 52–69. https://doi.org/10.1002/bse.1983

- Williams, L. J., Hartman, N., & Cavazotte, F. (2010). Method variance and marker variables: A review and comprehensive CFA marker technique. Organizational Research Methods, 13(3), 477–514. https://doi.org/10.1177/1094428110366036

- Yang, J., Wang, Y., Gu, Q., & Xie, H. (2022). The antecedents and consequences of green purchasing: An empirical investigation. Benchmarking, 29(1), 1–21. https://doi.org/10.1108/BIJ-11-2020-0564

- Yasir, M., Majid, A., Yasir, M., & Qudratullah, H. (2020). Promoting environmental performance in manufacturing industry of developing countries through environmental orientation and green business strategies. Journal of Cleaner Production, 275, 123003. https://doi.org/10.1016/j.jclepro.2020.123003

- Yee, F. M., Shaharudin, M. R., Ma, G., Mohamad Zailani, S. H., & Kanapathy, K. (2021). Green purchasing capabilities and practices towards Firm’s triple bottom line in Malaysia. Journal of Cleaner Production, 307, 127268. https://doi.org/10.1016/j.jclepro.2021.127268

- Yen, Y. X., & Yen, S. Y. (2012). Top-management’s role in adopting green purchasing standards in high-tech industrial firms. Journal of Business Research, 65(7), 951–959. https://doi.org/10.1016/j.jbusres.2011.05.002

- Yook, K. H., Choi, J. H., & Suresh, N. C. (2017). Linking green purchasing capabilities to environmental and economic performance: The moderating role of firm size. Journal of Purchasing & Supply Management, 24(4), 326–337. https://doi.org/10.1016/j.pursup.2017.09.001

- Yu, Y., & Huo, B. (2019). The impact of environmental orientation on supplier green management and financial performance: The moderating role of relational capital. Journal of Cleaner Production, 211, 628–639. https://doi.org/10.1016/j.jclepro.2018.11.198

- Zameer, H., Wang, Y., Yasmeen, H., & Mubarak, S. (2022). Green innovation as a mediator in the impact of business analytics and environmental orientation on green competitive advantage. Management Decision, 60(2), 488–507. https://doi.org/10.1108/MD-01-2020-0065

- Zhang, Y., Wei, Y., & Zhou, G. (2018). Promoting firms’ energy-saving behavior: The role of institutional pressures, top management support and financial slack. Energy Policy, 115, 230–238. https://doi.org/10.1016/j.enpol.2018.01.003