Abstract

Previous research separately investigated the relationship between competence of the village official, organizational commitment, leadership, internal control, external pressure, and accountability with village official research objects and only looked at how village officials carried out their functions as members of the organization, namely the village, so they had not fully described how attitudes and tendencies individual social behavior of village officials on the imp Thus, this study tries to fill a gap in research by looking at the link between village officials’ accountability and competence, organizational commitment, leadership, internal control, external pressure, and prosocial behavior in a comprehensive research model with prosocial behavior as a moderator. This study was undertaken in all Indonesian communities to assess local finance management accountability. Random sampling was used to acquire survey data. 689 Indonesian village officials were studied. PLS-SEM analyzed data. This study found that village officials’ competency, leadership, internal control, and external pressure affect village fund management accountability. Organizational commitment and internal control do not promote local fund management accountability in Indonesia. Village finance management accountability and prosocial conduct regulate and improve leadership. Official leadership, internal control, and prosocial behavior promote village money management accountability. This work advances agency theory, stewardship theory, role theory, quality theory and financial accounting and public sector accounting, particularly in village governance.

PUBLIC INTEREST STATEMENT

Law no. 6 of 2014 on communities (Village Law) has allowed communities to flourish, strengthen, and establish regional programs fostering autonomy and independence. The law also gives the Village more power to run government, grow, empower, and develop community. The Village Law changed the village’s status from an administrative region under the district to an entity with the right to regulate and administer its own governmental affairs, including village-owned finances and assets. This makes accountability a significant problem because managing village finances requires accountability to work smoothly and benefit the community. Village officials are both individuals and social creatures, therefore their prosocial behavior is essential to accountability. Researchers study responsibility elements that affect prosocial behavior from this perspective. Prosocial conduct moderates accountability aspects, according to the findings.

1. Introduction

Diverse and multicultural, Indonesia’s islands. The economy and villages need a lot of infrastructure improvement. The regional budget must be well-managed. A land border with territorial bounds and a group responsible for managing its affairs, community interests, and aims, including customary rights recognized by the Unitary State of the Republic of Indonesia based on Law No.6 of 2014. A village’s operations, communal interests, and goals are managed by staff. Residents govern a village. Article 2 paragraph 1 of Home Affairs Regulation No.20 of 2018 mandates village financial management transparency, accountability, and budgetary discipline. Village leaders know this to maximize resource management. Accountability and openness are fixed.

According to the Directorate General of Fiscal Balance, the Village Government Work Plan says that the most important way to use village funds is to pay for community development and empowerment projects that aim to improve the welfare of village communities, improve the quality of human life, and reduce poverty. Large amounts of village funds increase the chances of fraud in their management due to limited understanding of human resources in managing village funds which are quite large (Arthana, Citation2019). Identification of several risks in the village financial management business process can be categorized as business risk and financial risk (fraud). Several village financial risks can occur in village financial management, including programs and activities that do not meet the needs of the community, failure to implement a healthy village financial management cycle, failure or delay in preparing reports, and management of village assets that are not effective and efficient (Jasasila, Citation2020).

According to Indonesia Corruption Watch (ICW) asked the government to oversee the management and use of village funds because there were findings about rampant corruption cases involving officials from village officials. Based on data from ICW, from 2015 to 2020, there were 676 defendants in corruption cases from village officials, and resulted in losses for the state reaching IDR 111 billion. ICW data for 2021 shows that there are 154 cases of corruption in village funds, the number of cases is the highest compared to other sectors and types.

The number of cases that occur related to corruption has become one of the most popular social issues in society. To overcome this problem, accountability for managing village funds is needed. Accountability is when the community’s right to get approved Village Government Budgets information is met, as well as when procedures are followed in the planning stage and the community’s right to get ratified budget estimate plan information at the planning stage (Asmawati & Basuki, Citation2019).

Indonesians are receiving prominence due to fiscal decentralization. Regional autonomy altered budget spending. Good governance requires transparent financial management. It includes financial statements and management details (Adiputra et al., Citation2018). Regional financial management improves government performance (Nirwana & Haliah, Citation2018).

Indonesians often show altruism. Some use situations for personal or group gain (Fetchenhauer et al., Citation2006). Most village fund managers are nonsocial, affecting economic and community growth. It’s a government official’s behavior to help people without expecting anything in return, which affects financial resource management. Prosocial village officials improve human resources, local budget management, and accountability (Mahayani, Citation2017). Each village official must be qualified to manage revenues and other tasks (Zulkifli et al., Citation2021). Employee performance is connected to organizational commitment. Each government employee must reduce fund-management problems to attain responsibility (Abouraia & Othman, Citation2017). Program implementation takes organization-wide buy-in (Serhani, Citation2022; Suryani & Suprasto, Citation2021). They can take sides and stay in village government. Leadership, internal controls, and external variables provide transparency. Leaders determine a company’s success (Sonmez Cakir & Adiguzel, Citation2020). Akparep et al. (Citation2019) say they direct and motivate subordinates. Leadership organizes and directs managerial work. et al. Coordination of government activities using internal control mechanisms. These help achieve stated goals by executing duties successfully and efficiently, reporting financial. Internal controls can detect discrepancies in village funds. External variables affect the public’s openness to information, putting pressure on financial manager (Lubis et al., Citation2019).

The purpose of this research is to investigate the possible relationship that exist between village officials’ accountability and competence, organizational commitment, leadership, internal control, external pressure, and prosocial behavior in a comprehensive research model with prosocial behavior as a moderator. Many studies examine accountability, but the authors try to research with prosocial behavior as a moderation variable.

The novelty of this study is a theoretical model. The study uses the role theory and quality theory. This study also uses perspective of agency theory and stewardship theory, This theory underpins the majority of public-sector organizations. The difference in research results is a research gap argument that encourages researchers to include moderating variables. Finding additional variables that act as moderators or mediates in research models requires the use of a contingency strategy (MacKinnon, Citation2011; Murray, Citation1990). Studies have shown that confounding variables can alter the link between the independent and dependent variables. These conditional factors can be divided into four categories: cultural, organizational, interpersonal, and individual (Brownell, Citation1982) Role theory (role theory) provides an analysis of social behavior in society. A person’s social behavior in a group is the result of the actualization of a particular role (Myers, Citation2010). The role of government village officials is to seize social position in society and be trusted by the community in managing village finances. Crosby’s theory of quality suggests conformity with standardized, a product or service must be done by people who have high skills (competent) and good attitude or behavior (Crosby, Citation1979). Role theory and quality theory are used to include prosocial behavior as a contingency factor. The prosocial behavior factor acts as a moderator of the relationship between human resource competence, organizational commitment, leadership, internal control and external pressure on village fund management accountability in Indonesia. This research is a development of Mahayani (Citation2017) and Wibawa and Dwirandra (Citation2022) research.

2. Literature review & hypotheses development

2.1. Agency theory

Agency theory is the principal-agent relationship (Hendriksen & Van Breda, Citation1992). Several factors prevent a standard analysis of the agency’s government connection. First, existing entities in the public sector (Government) have different ideologies about assessing the services they provide. Most public-sector organisations follow this philosophy. (Bergman and Lane (Citation1990) said public groups can use it. Modern democracies rely on principal-agent relationships.

2.2. Teori stewardship

Stewardship is an attitude and set of behaviours that prioritises the communal over individual goals (Hernandez, Citation2012). This theory covers situations in which managers aren’t motivated by personal interests, but by the organization’s profit (Donaldson & Davis, Citation1991). The stewardship theory assumes collaborative conduct is better than individualistic. Management tends to strengthen HR’s proficiency in streamlining internal control, which creates a solid corporate culture with strong governance (Hernandez, Citation2012).

2.3. Quality theory

According to quality theory, for a product or service to meet standards, it must be produced by individuals with high abilities (competent) and moral character. Research by Ramasoyan et al., (Citation2021) states that human resource competence influences the performance accountability of government agencies. In contrast to Saputra (Citation2022) proves that Human Resource accountability for the financial performance of the government is unaffected by competence. Prosocial activity is one way that people can do their part to preserve the harmony of the universe (Cowan et al., Citation2022). When people are close to one another, prosocial conduct takes place. Generosity toward fellow group members is influenced by a person’s official position within an organization or community. Competence has no effect on government financial performance accountability. Humans have an obligation to maintain the balance of the universe, among others, in the form of prosocial behavior (Cowan et al., Citation2022). When people are close to one another, prosocial conduct takes place. Generosity toward fellow group members is influenced by a person’s official position within an organization or community (Baldassarri et al., Citation2013)

2.4. Role theory

The benefits of volunteering and assisting others to health and well-being are frequently explained by the role theory. Robert Merton, an American sociologist, is the author of the original role theory (Merton, Citation1957). Role refers to the social roles that people play, such as those of teachers, mothers, and consumers, as well as the behaviors that go along with those roles. The hazards and rewards of roles are likely to differ according on the individual, the historical period, and the cultural setting. Roles can give people a sense of belonging and access to resources, which in turn can boost confidence, prestige, and ego satisfaction.

According to Hogg and Vaughan (Citation2014), roles also give behavioural guidance in ambiguous situations, which can help to lower stress and improve wellbeing. Humans frequently play multiple roles at once (such as mother, director, and child), and these successions may alter over life ((Riley & Riley and Riley, Citation1994; Rotolo, Citation2000).

2.5. Village fund management accountability

Convenient accounting is accountability. Environmental, societal, and government regulations (Patton, Citation1992). Responsible accounting considers finance, environment, and society. Economic, political, and social cultures combine. Recordkeeping ensures financial accountability. Government values client-professional, social-community interactions (Siriwardhane & Taylor, Citation2017). Accountability demands openness, transparency, and action reports (Sian, Citation2021). Good municipal administration and finance require accountability. Money well-managed. PERMENDAGRI No. 113 of 2014 requires budgeted, transparent, participatory village finance management. This policy is represented by the village head.

2.6. Research design and hypothesis development

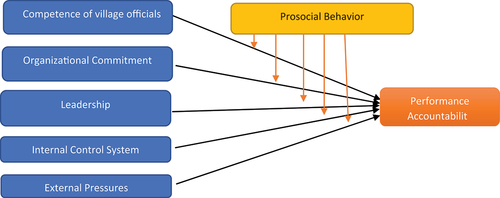

Figure 1. Conceptual model.

2.6.1. The competence of village official related to the accountability of village fund management

Competence is the mental and physical competence to do work-related duties (Stephen and Robbins, Citation2013). Accountability increases when local officials manage finances well. Yet, if it lacks sufficient resources to do its job, this attribute may not be optimally realized (Umaira & Adnan, Citation2019). To maximize funding, village officials require qualified staff. This can be earned by taking financial bidnags training or studying accounting. Experience helps village officials improve accountability (Rosari & Manabulu, Citation2020; Yulianto et al., Citation2020) and (Afifi et al., Citation2021) found that competent village officials and fund management effect accountability, whereas Claudia et al. (Citation2022) found that village fund management village official competency partially does not affect accountability. Previously discussed research hypotheses are reported as follows:

H1:

Competence of village official has a significant effect on the accountability of village fund management.

2.6.2. Commitment of the organization related to the accountability of village fund management

Organisational commitment involves loyalty and goal-setting. Matani and Hutajulu (Citation2021) say it enhances accountability. Strongly dedicated employees perform well, while those that are less committed perform poorly Princy and Rebeka (Citation2019). Indriasih and Sulistyowati (Citation2022) found no impact on village fund management accountability. Apriana et al. (Citation2020) found that village fund management accountability increases with local government organization commitment. This description led to the proposed hypotheses:

H2: commitment of the organization have a significant effect on the accountability of village fund management.

2.6.3. Leadership related to accountability of village fund management

Great leaders motivate others to control the entire process by taking accountability for all factors and measurements or surrogates of quality under their control (Cerfolio, Citation2020). Leaders encourage teammates to improve and assume accountability. They plan, organize, and set an organization’s goals as local government officials, motivating village workers (Lestari et al., Citation2020). Leadership affects village fund management accountability (Savitri et al., Citation2020). Based on the earlier mentioned analysis, the following hypothesis was proposed:

H3: leadership has a significant effect on the accountability of village fund management.

2.6.4. Internal control related to the accountability of village fund management

To be more accommodating and efficient, control system policies must be linked to accountability procedures (Atan et al., Citation2017). According to Government Regulation No. 60 of 2008 on the Government Internal Control System (SPIP), internal controls, also known as internal auditing systems, are integral actions and activities carried out continuously by leadership and all employees to efficiently and effectively achieve organizational goals (Nuha, Citation2021; Hastuti et al., Citation2020). The village government uses all its resources to implement efficient internal control to create quality financial reports in accordance with PSAP No.1 and manage village funds as a community service. Leadership and staff regularly use an internal control system to meet company goals (Savitri et al., Citation2020). It ensures local government financial transparency (Hafit et al., Citation2018). Afifi et al. (Citation2021) and Priantono and Vidiyastutik (Citation2022) found that the internal control system influences village fund management, whereas Y. A. Dewi et al. (Citation2021) found no significant effect. This led to the following hypothesis:

H4:

Internal Control has a significant effect on the accountability of village fund management.

2.6.5. External pressure related to the accountability of village fund management

External pressures are caused by government rules or other entities to adopt certain structures or systems. A regulation causes a company to focus on the positive to appear good to outsiders. Reporting is just a formality to get credibility due to financial statement transparency pressures, hiding beneficial features. Greater transparency and accountability. External influences affect transparent financial reporting in Jatmiko and Setiawan (Citation2020) and Yudin and Utami (Citation2020). External forces impacted financial reporting transparency., and this led to the following hypothesis:

H5:

External Pressure has a significant effect on the accountability of village fund management.

2.6.6. Prosocial behavior has a moderating effect on the relationship between the competence of the village official and accountability of village fund management

Quality theory requires competent and well-behaved people to supply a standard, product, or service.Saputra (Citation2022) discovered competent workers affect government agency performance. It does not affect government financial performance accountability like Rofika and Ardianto (Citation2014). Prosocial behavior helps people balance the universe (Shaw Marvin and Costanzo, Citation1982). It’s closeness. Compassion towards group members is affected by one’s formal status (Baldassarri et al., Citation2013). Social behavior theory defines prosocial activity as selfless help. Realistic social responsibility norms (Sears et al., Citation1991). Administrators frequently come from various villages. Outsiders are aided less than insiders (Brewer & Brown, Citation1998). Local government officials’ selflessness allocates funds. Their generosity boosts village fund management’s human resource skills and accountability (Mahayani, Citation2017). Savitri et al., (Citation2019) claim local administrators’ competence affects money accountability. Luthfiani et al., (Citation2020) found that village fund accountability is unaffected by administrator skill. These findings demonstrate organizational commitment is not the only factor determining village fund management official competency. Researchers believe village government officials’ behavior affects financial management. Prosocial village authorities will improve village official competency and village fund management accountability. Village officials prosocial behaviour enhances village official competence on village fund management accountability, according to theoretical foundation, pertinent concepts, and empirical study. Wibawa and Dwirandra (Citation2022) discovered that organizational commitment increased the impact of official competence on village fund accountability. Based on this description, the following hypothesis was proposed:

H6:

Prosocial behavior has a moderating effect on the relationship between the village official ‘s competence and village fund management’s accountability.

2.6.7. Prosocial behavior has a moderating effect on the relationship between organizational commitment and accountability of village fund management

Accountability and organizational commitment are closely related. Some authorities believe that organizational commitment is essential to accountability (Cavoukian et al., Citation2010). Organizational commitment contributes to accountability. Asserts that the organization’s public commitment may be shown to help the public accountability system (Brown & Moore, Citation2001). Working hard rather than focusing on constituents might increase an organization’s accountability. Organizational commitment measures how much a member supports a firm and how well it can perform its duties. Village officials with strong prosocial conduct are likely to help others with a genuine feeling of duty, enhancing their commitment to the organization.Based on this description, the following hypothesis was proposed:

H7: prosocial behavior has a moderating effect on the relationship between organizational commitment and accountability of village fund management.

2.6.8. Prosocial behavior has a moderating effect on the relationship between leadership and accountability of village fund management

Leader person allowed to lead an organization to achieve aspirations village fund management accountability. According to Ernawati (Citation2022), leadership quality affects accountability report performance. The village head must manage the community’s finances to achieve the spending plan’s goals. Good village leaders focus on collective goals rather than individual ones. The village head’s ability to collaborate with the community and other village officials to achieve village fund goals will affect accountability for village fund administration. In local governance, it involves encouraging, organizing, and directing village devices to manage funds (Adji et al., Citation2019). It guides members toward common goals. Village heads manage local government funds, demonstrating leadership. Social roles explain behavior. In this situation, prosocial activities strengthened village fund management leadership responsibility. Wirakusuma and Kawisana (Citation2022) argue that village government employees operate prosocially, which strengthens the leadership-authority relationship and boosts accountability in village finance administration.Therefore, this led to the following hypothesis :

H8: prosocial behavior has a moderating effect on the relationship between leadership and accountability of village fund management

2.6.9. Prosocial behavior has a moderating effect on the relationship between internal control and accountability of village fund management

Internal control monitors government activities to achieve goals. To provide proper assurance, it directs and supervises leaders and staff. Hence, improved government internal control means more effective and efficient objective achievement. 2019. Previous research showed its impact on local government financial statement accountability and transparency (Adiputra et al., Citation2018). Financial transparency and accountability require better internal control. Better regional financial reporting are more accountable and transparent, according to Adiputra et al. (Citation2018). Kindness boosts internal control and accountability., and this led to the following hypothesis:

H9:

Prosocial behavior has a moderating effect on the relationship between internal control and accountability of village fund management.

2.6.10. Prosocial behavior has a moderating effect on the relationship between the external pressures and accountability of village fund management

External pressures include rules, CEOs, and communities. Frumkin and Galaskiewicz (Citation2004) say it reduces government capabilities, notably policy or procedural execution. SKPD is a formality for legitimacy caused by external forces. Baron and Byrne (Citation1997) defined prosocial conduct as helping others without directly benefiting and even risking the helper. External pressure increases the urge to support each other, making the village official stronger and more likely to break procedures. Because they feel pressured and friends, asking for transaction proof is uncomfortable. The village official’s altruism boosts external pressure and accountability. This description led to the following hypothesis:

H10:

Prosocial behavior has a moderating effect on the relationship between the external pressures and accountability of village fund management

3. Method

This study was undertaken in all Indonesian communities to assess local finance management accountability. Random sampling was used to acquire survey data. 689 Indonesian village officials were studied. PLS-SEM analyzed data. This study measures village officials’ competency, organizational commitment, leadership, internal control, and external factors affecting fund management performance. Determine how prosocial behaviour moderates competence, organizational commitment, leadership, internal control, and external pressure. These queries uncovered village financial management issues.

Modeling PLS paths empirically. Initial analysis and data. It provides descriptive statistics and multivariate data assumptions. This chapter justifies and examines PLS in the current inquiry, dividing findings into two areas. Model outputs include item assessments, internal consistency, convergent and discriminant validity. Start here. The second essay portion gives examples. Include path coefficient, R-squared, effect size, and model relevance. PLS-SEM is explained. Modeling:

The scale for measuring this variable uses a Likert scale from 1 to 5 with an answer score of 1 strongly disagree, 2 disagree, 3 neutral, 4 agree and 5 strongly agree (Preedy, Citation2010).

4. Result

4.1. Data description

The survey was addressed to Indonesian village governments that manage local money. Google forms and direct questionnaires are used. Table shows survey responses. This study uses quantitative questionnaire data. 792 questionnaires and 73 google form data were collected. This Study have seven variables. Table show the measurement of variable.

Table 1. Variable measurement

Table 2. Distribution of the questionnaire

Table reveals that all Village Governments in Indonesia received 792 surveys, 73 via google form. Each village government was given 8 questions on PERMENDAGRI No. 20 for 2018. From the table above, we can see that Questionnaire Returns 723, Questionnaire can be processed 689 as 91.29 %, the reason for not returning is because it is not in place, on external assignment, on leave, has given birth, is on permission, or cannot be answered because there are several empty questions. Unanswered questions halted questionnaire processing.

4.2. Assessment of the PLS SEM measurement model (path model analysis)

4.2.1. Measurement model (outer model)

After the PLS-SEM algorithm has been carried out, there are 52 indicators from 7 constructs that are used for further analysis as shown below:

4.2.2. Internal consistency reliability

show the construct of variable and Table shows that internal consistency reliability ranged from 0.806 to 0.967 for all study constructs. This exceeds the suggested level of 0.70 (Bagozzi et al., Citation1991), hence it is assumed that the measurement model has appropriate internal dependability.

Table 3. Construct

Table 4. Latent construction results

4.2.3. Convergent validity

This study assessed the measurement model’s convergent validity using average variance extract (AVE). AVE > 0.5 indicates convergent validity (Albers, Citation2010).

Cronbach’s Alpha is used to test the unidimensionality of latent variable statement items (competency of village officials, organisational commitment, leadership, internal control, external pressure, prosocial behavior, and village fund management accountability). Reliable Cronbach’s Alpha > 0.60 (Hair et al., Citation2021).

4.2.4. Discriminant validity

Using Chin (Citation1998) and Fornell and Larcker’s (Citation1981) standards, discriminant validity was determined (1981). Check the cross loading table to see how the loading indicator compares to other reflective indicators. AVE values of 0.50 or higher are used to measure discriminant validity (Fornell & Larcker, Citation1981). Second condition: AVE square root > latent construct correlation (Fornell & Larcker, Citation1981). Mean variance was 0.698 to 0.965, which is acceptable. Table and Table lists them. Table compares latent constructs. The extracted mean variance square root is bolded. Table demonstrates that extracted mean variances are bigger than latent variable correlations, demonstrating discriminant validity (Fornell & Larcker, Citation1981).

Table 5. Average Variance Extracted (AVE)

Table 6. Discriminant validity

Chin (Citation1998) and Hair et al., (Citation2011) compare outer and crossloadings to show how discriminant validity can be tested. To achieve this

4.2.5. Summary of measurement model results

PLS-SEM analysis is affected by the measurement model. Figure and Table evaluate the model (Henseler et al., Citation2009). Next, summarize Tables . These tables show that the model’s criteria were met and demonstrate the study’s reliability and validity. Table shows model conditions met.

Table 7. Structural model results (direct effects)

4.2.5.1. Structural model significance assessment (direct effect)

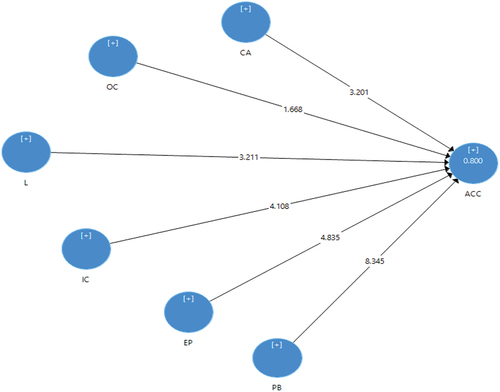

All construct measures are valid, according to the prior section’s model results. This part runs the model utilizing all the research variables to find direct (exogenous and endogenous) correlations from the study’s research aims. This section discusses variable linkages. Figure displays path coefficients from bootstrapping 1,000 times the study’s sample size. Hair et al. (Citation2014) accept path coefficients. Figure illustrates the model’s results.

Figure 2. Structural model or internal model (direct effect).

4.2.5.2. Determining the path coefficient in structural models (direct effects)

The model’s construct and coefficients are evaluated. The t-value verifies the earlier premise. Using t-statistics and probability, this work estimates path coefficients. t-value significance was determined using one-way distribution (Chin et al., Citation2000), (Churchill, Citation1979), (Sharma, Citation2000). Churchill (Citation1979) and Sharma (Citation2000) discovered t-value significant levels of 2,326, 1,645, and 1,282 at 1%, 5%, and 10%. Two-tailed tests showed this. Low t is deemed unimportant. What makes a research project remarkable is debated (Verma & Goodale, Citation1995). Dallal (Citation1986) claims a 0.90 probability demands a large sample size, whereas this study needs a small one. In social and behavioral sciences, 10% probability is usual (Cohen, Citation1988; Hinkle & Oliver, Citation1983).

4.2.5.3. Assessing the structural model’s coefficient of determination (R2 value)

Albers (Citation2010) and Chin (Citation2010) say that R squared values of.2550, and.75 should be used in PLS-SEM to describe findings that are weak, moderate, or strong. Three levels of importance. The R-squared values before and after moderator interactions are shown in Tables 4.11 and 4.12.

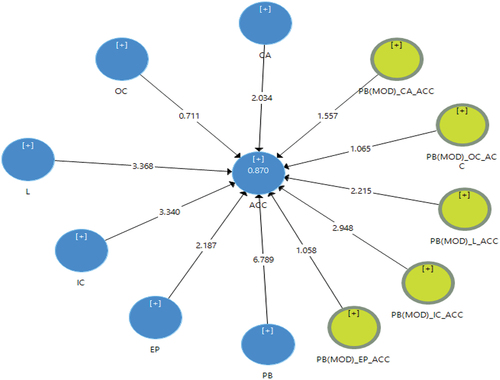

The research model accounts for 80% of the variance in responsibility (Table ). 80% of the endogenous variance is explained by organizational commitment, leadership, organizational competence, internal control, and external pressure. When Fig. 9‘s interaction effects of prosocial behavior are added, the model is complete. 87% of accountability variation is explained. Exogenous latent construct and Prosocial Behavior moderate 87% of endogenous latent construct variation. According to Albers (Citation2010) and Chin (Citation2010), endogenous latent variables have enough R-squared

Table 8. Variances in endogenous latent variables are explained prior to the interaction of prosocial behavior’s effects

4.2.5.4. Testing the moderation effect

A moderating impact exists when a predictor variable’s future effect on a criterion variable depends on another variable. This is especially true when the variable modifies the predictor-criterion relationship (Hair et al., Citation2014). route model illustrates the prosocial behaviour interaction

Figure 3. Path model results: prosocial behavior interaction.

Prosocial behavior’s moderating influence was examined. Tables and figures showing the moderating effect of prosocial behaviour on competency of village officials, organizational commitment, leadership, internal control, external pressure, and accountability.

Table show the variances explained in endogenous latent variables before interacting of prosocial behaviour and Table displays the results of interacting effect:

Table 9. Variances Explained in Endogenous Latent Variables before Interacting Effects of Prosocial Behavior

Table 10. Results of the moderating effect

Competency of village officials and accountability are moderated by prosocial behavior (H6). Competency of village officials x prosocial behavior interaction is not significant ( = 0.104, t = 1.557, p > 0.10).

Prosocial conduct moderates organizational commitment and accountability, says Hypothesis (H7). The interaction variables expressing organizational commitment x prosocial behavior are not significant ( = 0.141, t = 1.065, p > 0.10).

Prosocial behavior moderates leadership and accountability, says Hypothesis (H8). The interaction variables reflecting leadership x prosocial behavior are supported (= −0.370, t = 2.215, p 0.05).

Prosocial behavior moderates internal control and accountability, says Hypothesis (H9). The data (Tables ) reveal that internal control x prosocial conduct interacts significantly, supporting the theory.

(β = 0.259, t = 2.948, p < 0.05).

Prosocial behavior moderates external pressure and accountability, External stress x prosocial behavior association was not statistically significant ( = 0.064, t = 1.058, p > 0.10).

Two hypotheses (H8 and H9) are supported by the moderating data, but the other three (H6, H7, H10) are not.

4.3. Discussion

After testing quantitatively, it is described in more depth with the following results: the results of hypothesis testing are presented in the following description:

4.3.1. Competency of village officials related to village fund management accountability

Using a 0.122 correlation coefficient, we examine how village officials’ competence affects their accountability for managing village funds. The competency of village authorities influences the accountability of village money management since the t-statistical value is 2.034 (> t-critical 1.96). Hence, hypothesis 1 (H1), that the competency of village authorities influences the accountability of village money management, is accepted. The PLS analysis demonstrates that the competency of village administrators influences the accountability of village budget management (H1 is accepted). The more competent Indonesian village administrators are, the more accountable local fund management will be. These results show that Indonesian village administrators understand their major responsibilities. Comprehend the village financial planning and budgeting process, work well with colleagues, manage workplace difficulties, understand and prepare village financial reports appropriately, and attend training on village financial report administration. This is consistent with stewardship theory, which has implications for describing village government as a dependable public sector organisation, accommodating community aspirations, providing excellent service, and being able to account for what has been entrusted to them. So that organisational objectives for the good of society can be optimally achieved. Whether or not there is good governance can be determined by performance accountability (Khotami, Citation2017). The stewardship theory explains the existence of the Village Government as an institution that can be relied upon to act in the public interest by carrying out its duties and responsibilities effectively. In order to fulfil these responsibilities, the stewards (management and internal auditors) direct all capabilities towards the production of accurate and dependable financial information reports. To produce quality and accountable financial reports, competent human resources must have a sufficient educational background, frequently participate in education and training, and have experience in finance. If human resources are competent, they will generate reliable and accurate financial reports. However, if the company’s human resources are incompetent, the credibility of its financial reports can be questioned. Human resource competence positively affects village finance management accountability, according to (Taufik et al., Citation2022). Sofyani (Citation2022) note that village officials competence affect accountability. These results agree with those of (Aziiz & Prastiti, Citation2019; Mada et al., Citation2017; Mahayani, Citation2017), and (Mus et al., Citation2022), who found that village officials’ competence affected village fund management accountability. Princy and Rebeka (Citation2019) discovered that village officials’ competence did not affect village fund management accountability.

4.3.2. Organizational commitment related to village fund management accountability

The correlation coefficient between organizational commitment and village fund management accountability in the Original Sample was 0.112. The organizational commitment to village financial management accountability has a t-statistical value of 0.711 (t-critical 1.96). Hence, the hypothesis that organizational commitment influences the accountability of village fund management is refuted. PLS analysis shows organizational commitment has no effect on village fund management accountability (H2 is rejected). Indriasih, (Citation2022) research shows that village government’s organizational commitment is a financial management success, but it doesn’t effect the smallest element of government. Organizational commitment makes individuals responsible and side with the organization, with concern for organizations that haven’t shown accountability in handling village funds without action to achieve organizational goals (Stephen and Robbins, Citation2013). Village finances require trust and responsibility. Safelia et al., (Citation2022) found that village government organizational commitment does not affect village fund management accountability. This study contradicts the research Marlina et al., (Citation2021) and Mualifu Guspul and Hermawan (Citation2019). Organizational commitment improved village fund management accountability (Cavoukian et al., Citation2010).

4.3.3. Leadership related to village fund management accountability

The original sample correlation coefficient was 0.434, testing the influence of leadership on village fund management accountability. The t-statistic is 3.368 (> t-critical 1.96), showing leadership influences village money management accountability. Leadership affects village fund management accountability, hence H3 is acceptable.Leadership positively affects Village Fund Management Accountability, according to PLS study (H3 is accepted). The better a leader is at handling village funds, the more responsibility will be seen. Leadership According to (William, Citation1962), leadership impacts group actions to attain specific goals. Leadership includes encouraging others to comprehend what has to be done and how to do it, as well as facilitating collective individual efforts to attain common goals (Yukl, Citation2008). The financial accounts prepared in line with the regulations and the Village government budget Report demonstrate this. This study supports N. K. A. J. P. Dewi and Gayatri (Citation2019) research. In compliance theory, if the leader complies with the minister of home affairs’ village rules, the management of village funds must be accountable and transparent, which will increase village funds and prevent late disbursements (Marlina et al., Citation2021). Leadership influences village fund management accountability (Yulianto et al., Citation2020). The village chief is the status bearer in this study. The better the leader or the more involved, the better the responsibility of village fund administrators.

4.3.4. Internal control is related to the accountability of village fund management

Internal Control’s influence on village fund management accountability was tested with a −0.338 correlation coefficient (Original Sample). The t-statistical value is 3.340 (> t-critical 1.96), hence Internal Control affects village fund management accountability. Thus, H4 is acknowledged, which states that Internal Control affects village fund management accountability. This study’s major influence is negative (negative and significant). Less Internal Control System discoveries equal higher Financial Statement Accountability. Based on processed data, the Regency/City Government met Law 60 of 2008. According to Purbasari and Bawono (Citation2017) research the Internal Control System hurts Financial Report Accountability. Cecilia says internal control affects local government financial accountability in Indonesia (Lelly Kewo, Citation2017). Better internal control improves local government’s financial responsibility. Eton et al. explain that control environment and monitoring controls affect financial accountability more than control actions (Eton et al., Citation2022).

4.3.5. External pressurerelated to accountability of village fund management

External Pressure on Village Fund Management with a Correlation Coefficient of −0.209 (Original Sample). External Pressure has a considerable effect on village fund management accountability if the t-statistic is 2.187 (t-critical 1.96). External Pressure affects village fund management accountability, hence H5 is approved. External pressure negatively affects accountability, according to this study. External pressures include government rules and outside pressure. Government regulation enhances environmental performance directly, changes company processes and structures (Graafland, 2020). External pressure makes all members of the organization carry out operational activities well and more publicly, so financial reports are more transparent. This shows that outside pressure on Indonesian village governments affects accountability. External pressure improves financial reporting openness, Government rules requiring the use of Government Accounting Standards influence the transparency of financial statement makers (Yudin & Utami, Citation2020). External influences affect financial reporting transparency (Jatmiko & Setiawan, Citation2020). First, accountability is tied to transparency. Transparency is vital for public accountability because it makes it easier for citizens to know government acts, their logic, and how they correspond to existing values. No public accountability without transparency. In society, suppressing human nature does not increase performance or accountability, but instead generates a sense of apathy and diminishes accountability.

4.3.6. Prosocial behavior has a moderate effect on the relationship between competency of village officials and village fund management accountability

A correlation coefficient of 0.91 and a T-statistics value of 6.78 (> t-critical 1.96) indicate a positive and statistically significant influence of prosocial behavior on village fund management accountability. Positive but insignificant effect of the interaction variable competency of village officials with prosocial behavior (X.Z1) on village fund management accountability. PLS analysis reveals that prosocial behavior is advantageous, and that the interaction variable competency of village officials with prosocial behavior (X.Z1) favorably influences village fund management accountability. Prosocial conduct can’t improve village leaders’ money management skills (H6 is rejected). The more competent and prosocial village administrators are, the less accountable they are with village funds. To meet standards, a product or service must be performed by talented, good individuals. People are a company’s greatest asset. Village official improve company productivity or growth. The findings of this study are consistent with the Quality Theory, which holds that in order for a product or service to comply to what is standardised, it must be produced by individuals with high skills (competence) and excellent behaviour. Human resources are the most crucial aspect of a business. The importance of village authorities as human resources in enhancing productivity or organisational development cannot be overstated. This study confirms Mahayani’s (Citation2017) finding that competency of village official expertise improves local finance management. Aziiz and Prastiti (Citation2019) states compentence of village officials affects the village fund management accountability, hence their behavior affects financial management success. In this study, prosocial behavior by village leaders did not affect competency and responsibility in managing village funds. Cooperation is prosocial. Cooperation is a relationship between two or more people who depend on each other for their goals, therefore one person’s action tends to boost others’. Cooperation can have negative consequences, like reasoning activities that weaken accountability, like understanding if a financial reporting error is material.

4.3.7. Prosocial behavior has a moderate effect on the relationship between organizational commitment and village fund management accountability

Testing the hypothesis that prosocial conduct affects village fund management accountability yielded a correlation coefficient (Original Sample) of 0.918 and a T-Statistics value of 6.789 (> t-critical 1.96), indicating that the effect is both positive and significant. The effect of the interaction variable of organizational commitment with prosocial behavior (X2.Z) on village fund management accountability yielded a correlation coefficient value (Original Sample) of 0.141, with a t-statistic value obtained of 1.065 (t-critical 1.96), then The effect of the interaction variable of village officials’ competence with prosocial behavior (X2.Z) on village fund management accountability is positive and not significant.

The analysis’s findings indicate that the prosocial behavior variable is positive and that the organizational commitment and prosocial behavior interaction variable (X2.Z) have no discernible influence on the accountability of village fund administration. Hence, prosocial behavior is unable to strengthen and reduce the impact of organizational commitment on the accountability of village fund administration (H7 is rejected). According to the findings of the village government’s organizational commitment is one of the achievements of financial management, but it has no bearing on the tiniest aspect of governance. Individuals become accountable to and in favor of the organization when they commit to it. The organizational commitment of village officials, which would promote responsibility in the handling of village money, cannot be increased by the prosocial behavior of village government officials.

4.3.8. Prosocial behavior has a moderating effect on the relationship between leadership and village fund management accountability

Prosocial behavior and village fund management accountability correlate −0.370 (original sample). Prosocial behavior affects village fund management accountability (t = 2.215 > 1.96). Leadership and prosocial behaviour interaction (X3.Z) impacted village fund accountability by −0.370 (> t-critical 1.96)

Leadership (X3,Z) and village financial management are linked to prosocial behavior. Prosocial behavior moderates and improves community finances (H8 is accepted). More accountable village money management means more leadership from the village head and more prosocial local officials. The village head is responsible for budgeted activities (Silva, Citation2016). Permendagri No. 20 of 2018 says the village head manages money. Village head oversees APBDesa via camat. Village head tells agents and principals about agency concerns. Interview results suggest village fund management followed regulations and protocols, including planning, budgeting, implementation, administration, reporting, and accountability. Online questionnaires helped him evaluate North Denpasar Regency’s village chiefs. Leaders effect organizational goals (Dwika et al., Citation2021). Leadership boosts accountability report performance, according Ernawati (Citation2022). The village head’s cash management is crucial for goals. Good village leadership avoids self-interest. The village head’s capacity to embrace the community and village authorities affects local money management accountability. Social position indicating role in village governance is the role of a head villages in the management of village funds. role theory explain social behavior in the context of functions and social position in society.

4.3.9. Prosocial behavior has a moderate effect on the relationship between internal control and village fund management accountability

The influence of prosocial behavior on the accountability of village fund management is large and in a positive direction, as evidenced by a correlation coefficient of 0.91 and a T-statistics value of 6.78 (which is greater than the t-critical value of 1.96). There is a correlation that can be considered positive and significant between the altruistic actions of village leaders and the responsible administration of local funds (X1.Z4).

Prosocial behavior is linked to Internal Control (X4.Z) and village fund management accountability. Prosocial behavior moderates and promotes village fund management accountability (H9 is accepted). Village fund management is more accountable with higher internal control and prosocial behavior. The internal control system is a continual series of actions and activities by the leadership and all staff, per Government Regulation 60 of 2008. Effective and efficient activities, reliable financial reporting, and protecting state assets inspire trust in achieving organizational goals. Internal control influences decision-making, accountability, and openness (Indriasih & Sulistyowati, Citation2022). Integrating leader and staff actions and activities creates transparency and accountability (Alam et al., Citation2019). Village finances and public trust. Human resources and technical systems influence an organization’s internal control system (Akhmetshin et al., Citation2018). Effective village internal controls increase village fund management accountability. Internal control affects village finances (Afifi et al., Citation2021).

4.3.10. Prosocial behavior has a moderate effect on the relationship between external pressure and accountability of village fund management

Prosocial behavior is correlated with village fund management accountability (Original Sample). Prosocial behavior improves village fund management accountability (t-statistic 1.058, t-critical 1.96). The effect of external pressure to prosocial conduct (X.Z5) on village fund management accountability was 0.064 with a t-statistic of 1.058 (t-critical 1.96). The influence of village officials’ skill with prosocial behavior (X1.Z5) is positive but not significant. External pressure and prosocial conduct interact negatively and insignificantly on village fund management accountability, according to the investigation. Prosocial behavior can’t reduce village fund management accountability (H10 is rejected). This means that village leaders’ prosocial behaviors, which preclude high accountability, don’t harm financial statement openness. According to prior research Nurcahyono et al., (Citation2021) external pressure does not affect financial statement openness. External pressure won’t alter financial statement openness. Financial transparency. Nadia proves external pressure doesn’t effect financial statement transparency (Davici). Outside pressure on Indonesian village governance doesn’t affect accountability and openness. This shows that outside pressure hasn’t enhanced organizational understanding of new requirements, harming village fund management accountability in Indonesia.

5. Conclusion

Village Fund Management The ability of village officials, the quality of their leadership, the level of internal control, and the amount of pressure applied from the outside all have a significant impact on accountability. This indicates that the amount of competency, leadership, and pressure from outside the village all have a role in increasing the level of responsibility associated with the administration of village funds in Indonesia. On the other hand, organizational commitment and internal control do not have a favorable impact on an individual’s level of accountability. It is not inappropriate to engage in prosocial activity, to be in a position to moderate and increase the authority of leadership, or to have an internal check on how the village’s money are managed. This indicates that the management of local funds will be held accountable to a greater degree the more effective the leadership and internal control of the village officials are, as well as the more helpful the village officials are.

6. Implication

6.1. Theoretical implications

The research conducted can provide empirical support for agency theory, where agency theory in the public sector explains that the public as actors in agency relations have the right to obtain accountability from the management of public funds carried out by agents. In compliance theory, there are two compliance perspectives, namely the instrumental perspective and the normative perspective. The normative perspective gives rise to the perception that a person tends to obey the law in accordance with internal norms. This theory is in accordance with the topic of this research where to achieve accountability in village financial management, village officials are required to have high competence, good prosocial behavior and high organizational commitment. This result is also in accordance with stewardship theory and quality theory. Stewardship theory which states that the party entrusted with the responsibility for managing village funds is the village official. Village officials who have a high organizational commitment will be responsible for all activities carried out within the organization to realize good services to the community and can achieve effective budget management. So with high organizational commitment, village officials can always act carefully and have a positive impact on the village. Furthermore, quality theory states that in order to comply with what is standardized, a product or service must be carried out by people (human resources) who have high skills (competent) and a good prosocial behaviour. Human resources are the most important factor in an organization. Village official as human resources is an important factor to increase productivity or organizational progress, so it is important to have a good prosocial attitude.

The results of hypothesis testing in this study found that prosocial behavior was statistically able to moderate the effect of organizational commitment, leadership, internal control on village fund management accountability, so that this variable could be maintained as a moderating variable. This means that prosocial behavior has the effect of being able to weaken and strengthen other variables in influencing accountability.

6.2. Methodological and analytical implications

The application of quantitative analysis is one of the most important contributions made by this thesis. With the help of multivariate analysis of the second generation known as PLS, this study makes an attempt to moderate the factors that influence the accountability of basic fund management by using a variable that prioritizes a psychological approach. This variable is prosocial behavior, and it is measured using PLS. The results of PLS provide further evidence in favor of the assertion that PLS is an acceptable method for the analysis of studies that involve a causal relationship between variables. The results of this study demonstrate that the variable measuring prosocial behavior can successfully be utilized in research as a moderating variable.

6.3. Practical implications

Human resource development at its most basic level can be used to help the village government. When it comes to the central government, it is possible to make a good structure and set of rules. The results give government auditors information about the things that affect how accountable village budget management is. Possibilities provide educational resources for improving the scientific accountability of village leaders, and universities can use these possibilities.

6.4. Limitation & suggestion for the future

Most respondents don’t answer the accountability question because they feel the researcher is connected to their impending evaluations. This study used simple random sampling and examined limited criteria. Time and money constraints unevenly distributed respondents. Future research could use more in-depth purposive sampling to establish respondent characteristics and ensure proportional data dissemination across Indonesia.

Author contributions

RAD : Conceptualization, Methodology, Analysis, writing of original drafts, Revisions.

AAM : Methodology, Supervision

JZ: Methodology, Oversight

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Rani Eka Diansari

Rani Eka Diansari is studying for a doctoral degree in accounting at Management and Science University, where she is a doctoral candidate. currently serving as a member of the faculty at Universitas PGRI Yogyakarta, where I have been employed for the past eight years. The author spent seven years working in the banking industry for CIMB Group and continues to this day to work as a trainer in banking and finance (microfinance). Throughout the course of his academic career, the author has had a keen interest in issues concerning public sector accounting. As a result of this interest, he has written a number of scholarly works that are connected to accounting and accountability procedures in businesses that are part of the public sector.

References

- Abouraia, M. K., & Othman, S. M. (2017). Transformational leadership, job satisfaction, organizational commitment, and turnover intentions: The direct effects among bank representatives. American Journal of Industrial and Business Management, 07(4), 404–25. https://doi.org/10.4236/ajibm.2017.74029

- Adebanjo, D., Teh, P. L., & Ahmed, P. K. (2016). The impact of external pressure and sustainable management practices on manufacturing performance and environmental outcomes. International Journal of Operations & Production Management, 36(9), 995–1013. https://doi.org/10.1108/IJOPM-11-2014-0543

- Adiputra, I. M. P., Utama, S., & Rossieta, H. (2018). Transparency of local government in Indonesia. Asian Journal of Accounting Research, 3(1), 123–138. https://doi.org/10.1108/AJAR-07-2018-0019

- Adji, A., Asmanto, P., & Tuhiman, H. (2019). Reform on Village Fund Formulation. June. Office of the Vice President's Secretariat. http://www.tnp2k.go.id/download/1986840WPVillagefundEngFinal.pdf

- Afifi, Z., Mulyanto, M., & Nugroho, D. H. (2021). The effect of internal control system and village fund management accountability. International Journal of Economics, Business and Accounting Research (IJEBAR), 5(3), 2425–2429. https://doi.org/10.31629/jmap.v1i2.3738

- Akhmetshin, E. M., Vasilev, V. L., Mironov, D. S., Zatsarinnaya, Е. I., Romanova, M. V., & Yumashev, A. V. (2018). Internal control system in enterprise management: Analysis and interaction matrices. European Research Studies Journal, 21(2), 728–740. https://doi.org/10.35808/ersj/1036

- Akparep, J. Y., Jengre, E., & Mogre, A. A. (2019). The influence of leadership style on organizational performance at tumakavi development association, tamale, northern region of Ghana. Open Journal of Leadership, 08(1), 1–22. https://doi.org/10.4236/ojl.2019.81001

- Alam, M. M., Said, J., & Azizal, M. B. A. A. (2019). Role of Integrity System, internal control system, and leadership practices on the accountability practices in the public sectors of Malaysia. Social Responsibilty Journal, 15(7), 955–976. https://doi.org/10.1108/SRJ-03-2017-0051

- Albers, S. (2010). PLS and Success Factor Studies in Marketing BT - Handbook of Partial Least Squares: Concepts, Methods and Applications (V. Esposito Vinzi, W. W. Chin, J. Henseler, & H. Wang, Eds.). Springer. https://doi.org/10.1007/978-3-540-32827-8_19

- Apriana, S., Said, D., & Nurleni, N. (2020). The influence of organizational commitment, competence of village fund management offficers, and utilization of information technology on accountability of village. AFEBI Accounting Review, 4(2), 94. https://doi.org/10.47312/aar.v4i02.291

- Arthana, I. K. (2019). Analisis faktor-faktor terjadinya kecurangan (fraud) dalam pengelolaan dana desa pada Kecamatan Amabi Oefeto Timur. Jurnal Akuntansi : Transparansi Dan Akuntabilitas, 7(1), 35–43. https://doi.org/10.35508/jak.v7i1.1302

- Asmawati, I., & Basuki, P. (2019). Akuntabilitas pengelolaan dana desa. Jurnal Studi Akuntansi Dan Keuangan, 2(1), 63–76. https://doi.org/10.29303/akurasi.v2i1.15

- Atan, R., Alam, M. M., & Said, J. (2017). Practices of corporate integrity and accountability of non-profit organizations in Malaysia. International Journal of Social Economics, 44(12), 2271–2286. https://doi.org/10.1108/IJSE-09-2016-0260

- Aziiz, M. N., & Prastiti, S. D. (2019). Faktor-faktor yang mempengaruhi akuntabilitas dana desa. Jurnal Akuntansi Aktual, 6(2), 334–344. https://doi.org/10.17977/um004v6i22019p334

- Bagozzi, R. P., Yi, Y., & Phillips, L. W. (1991). Assessing construct validity in organizational research. Administrative Science Quarterly, 36(3), 421–458. https://doi.org/10.2307/2393203

- Baldassarri, D., Grossman, G., Sánchez, A., & The Effect of Group Attachment and Social Position on Prosocial Behavior. (2013). Evidence from Lab-in-the-Field Experiments. PLos One, 8(3), e58750. https://doi.org/10.1371/journal.pone.0058750

- Baron, R. A., & Byrne, D. E. (1997). Social psychology. Allyn and Bacon.

- Bergman, M., & Lane, J.-E. (1990). Public policy in a principal-agent framework. Journal of Theoretical Politics, 2(3), 339–352. https://doi.org/10.1177/0951692890002003005

- Brewer, M. B., & Brown, R. (1998). The Handbook of Social Psychology. McGraw-Hill.

- Brownell, P. (1982). The role of accounting data in performance evaluation, budgetary participation, and organizational effectiveness. Journal of Accounting Research, 20(1), 12–27. https://doi.org/10.2307/2490760

- Brown, L. D., & Moore, M. H. (2001). New roles and challenges for NGOs. Accountability, strategy, and international nongovernmental organizations. Nonprofit and Voluntary Sector Quarterly, 30(3), 569–587. https://doi.org/10.1177/0899764001303012

- Cavoukian, A., Taylor, S., & Abrams, M. E. (2010). Privacy by Design: Essential for organizational accountability and strong business practices. Identity in the Information Society, 3(2), 405–413. https://doi.org/10.1007/s12394-010-0053-z

- Cerfolio, R. J. (2020). Reply from the authors: Accountability and leadership changes culture—yes, even for lymph nodes. The Journal of Thoracic and Cardiovascular Surgery, 159(2), e146. https://doi.org/10.1016/j.jtcvs.2019.09.005

- Chin, W. W. (1998). The partial least squares approach for structural equation modeling. In Marcoulides, G. A. (Ed.) Modern methods for business research (pp. 295–336). Lawrence Erlbaum Associates Publishers.

- Chin, W. W. (2010). Handbook of partial least squares. Handbook of Partial Least Squares, 655–656. https://doi.org/10.1007/978-3-540-32827-8

- Chin, W. W., Marcelin, B. L., & Newsted, P. R. (2000). A partial least squares latent variable modeling approach for measuring interaction effects: Results from a Monte Carlo simulation study and an electronic-mail emotion/adoption study. Information Systems Research, 14(2), 189–217. https://doi.org/10.1287/isre.14.2.189.16018

- Churchill, G. A. (1979). A paradigm for developing better measures of marketing constructs. Journal of Marketing Research, 16(1), 64–73. https://doi.org/10.1177/002224377901600110

- Claudia, P., Pongantung, J., Elim, I., & Mawikere, L. M. (2022). The influence of the role of village apparatus, competence of village fund management apparatus and government internal control system on village fund management accountability (study on villages in Kumelembuai District). AFEBI Accounting Review (AAR), 7(1), 50–64. https://doi.org/10.47312/aar.v7i1.568

- Cohen, J. (1988). Statistical power analysis for the behavioral sciences. The SAGE Encyclopedia of Research Design. https://doi.org/10.4135/9781071812082.n600

- Cowan, S. K., Bruce, T. C., Perry, B. L., Ritz, B., Perrett, S., & Anderson, E. M. (2022). Discordant benevolence: How and why people help others in the face of conflicting values. Science Advances, 8(7), eabj5851. https://doi.org/10.1126/sciadv.abj5851

- Crosby, P. B. (1979). Quality is Free: the art of making quality certain. New American Library, New York. McGraw-Hill.

- Dallal, G. E. (1986). PC-SIZE: A program for sample size determinations. American Statistician, 40(1), 52. https://doi.org/10.2307/2683121

- Dewi, N. K. A. J. P., & Gayatri, G. (2019). Faktor-Faktor Yang Berpengaruh Pada Akuntabilitas Pengelolaan Dana Desa. E-Jurnal Akuntansi, 26, 1269. https://doi.org/10.24843/eja.2019.v26.i02.p16

- Dewi, Y. A., Nasfi, N., & Yuliza, M. (2021). Internal control system, utilization of accounting information technology, on village fund management accountability. International Journal of Economics, Business and Accounting Research (IJEBAR), 5(1), 190–203. https://doi.org/10.29040/ijebar.v5i1.2040

- Donaldson, L., & Davis, J. H. (1991). Stewardship theory or agency theory: CEO governance and shareholder returns. Australian Journal of Management, 16(1), 49–64. https://doi.org/10.1177/031289629101600103

- Dwika, R. K. D., Gayatri, & Gayatri, G. (2021). Factors affecting accountability of village fund management in north Denpasar district. E Jurnal Akuntansi, 31(12), 3273–3287. https://doi.org/10.24843/EJA.2021.v31.i12.p18

- Ernawati, D. P. (2022). Examining factors affecting the accountability of the performance of regional apparatus organizations. ATESTASI : Jurnal Ilmiah Akuntansi, 5(1), 77–93. https://doi.org/10.57178/atestasi.v5i1.24

- Eton, M., Mwosi, F., & Ogwel, B. P. (2022). Are internal controls important in financial accountability? (Evidence from Lira district local government, Uganda). International Journal of Financial, Accounting, and Management, 3(4), 359–372. https://doi.org/10.35912/ijfam.v3i4.810

- Fetchenhauer, D., Flache, A., Buunk, A. P., & Lindenberg, S. (Eds.). (2006). Solidarity and prosocial behavior: An integration of sociological and psychological perspectives. Springer Science & Business Media. https://doi.org/10.1007/0-387-28032-4

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Frumkin, P., & Galaskiewicz, J. (2004). Institutional isomorphism and public sector organizations. Journal of Public Administration Research and Theory, 14(3), 283–307. https://doi.org/10.1093/jopart/muh028

- Hafit, M., Irianto, G., & Purwanti, L. (2018). Analysis of government internal control system on budget implementation in accordance with government regulation no 60 of 2008. Journal of Accounting and Business Education, 2(2), 253–272. https://doi.org/10.26675/jabe.v2i2.11227

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2014). A primer on partial least squares structural equation modeling (PLS-SEM). Sage Publications.

- Hair, J. F., Jr., Hult, G. T. M., Ringle, C. M., Sarstedt, M., Danks, N. P., & Ray, S. (2021). Partial least squares structural equation modeling (PLS-SEM) using R: A workbook. Springer Nature Switzerland AG. https://doi.org/10.1007/978-3-030-80519-7

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory & Practice, 19(2), 139–152.e. https://doi.org/10.2753/MTP1069-6679190202

- Hastuti, M. R., Rufaedah, Y., Barnas, B., & Mulyana, D. (2020). Role of the Government Internal Control System (SPIP) towards Good University Governance: Evidence from Vocational Higher Education in Indonesia. Researchgate Net, 3(4), 495–504. https://www.researchgate.net/profile/Hastuti_Hastuti4/publication/344896692_Role_of_the_Government_Internal_Control_System_SPIP_towards_Good_University_Governance_Evidence_from_Vocational_Higher_Education_in_Indonesia/links/5f97b98a458515b7cfa17eb6/Role-o

- Hendriksen, E. S., & Van Breda, M. F. (1992). Accounting Theory. Irwin. https://books.google.co.id/books?id=kJ5ZAAAAYAAJ

- Henseler, J., Ringle, C. M., & Sinkovics, R. R. (2009). The use of partial least squares path modeling in international marketing. Advances in International Marketing, 20(May 2014), 277–319. https://doi.org/10.1108/S1474-7979(2009)0000020014

- Hernandez, M. (2012). Toward An Understanding Of The Psychology Of Stewardship. Academy of Management Review, 37(2), 172–193. https://doi.org/10.5465/amr.2010.0363

- Hinkle, D. E., & Oliver, J. D. D. (1983). How large should the sample be? A question with no simple answer?. In Educational and Psychological Measurement (Vol. 43, pp. 1051–1060). Sage Publications. https://doi.org/10.1177/001316448304300414

- Hogg, M. A., & Vaughan, G. M. (2014). Social Psychology (7rd ed.). Prentice Hall.

- Indriasih, D., & Sulistyowati, W. A. (2022). The Role of Commitment, Competence, Internal Control system, Transparency and Accessibility in Predicting the Accountability of Village Fund Management. The Indonesian Accounting Review, 12(1), 73. https://doi.org/10.14414/tiar.v12i1.2650

- Jasasila, & Jasasila, J. (2020 1). Perkembangan dan efektivitas pelaksanaan pengawasan pengelolaan dana desa pada Inspektorat Daerah Kabupaten Batang Hari. Ekonomis: Journal of Economics and Business, 4(1), 172. https://doi.org/10.33087/ekonomis.v4i1.134

- Jatmiko, B., & Setiawan, M. B. (2020). The Effect of External Pressure, Management Commitment and Accessibility towards Transparency of Financial Reporting. Journal of Accounting and Investment, 21(1). https://doi.org/10.18196/jai.2101140

- Khotami, M. (2017). The Concept Of Accountability In Good Governance Proceedings of the International Conference on Democracy, Accountability and Governance (ICODAG), 163, (30–33). Atlantis Press. https://doi.org/10.2991/icodag-17.2017.6

- Lelly Kewo, C. (2017). The Influence of Internal Control Iplementation and Managerial Performance on Financial Accountability Local Government in Indonesia. International Journal of Economics and Financial Issues, 7(1), 1–5.https://0Awww.econjournals.com

- Lestari, T. S., Adiwisastra, J., Hubeis, M., & Ambiar, H. (2020). the Impact on Leadership of the Village Government, the Government Official’S Competence, Motivation and Participation of the People Toward Effectiveness of the Empowerment of Bum Desa in Klaten Regency. Scientific Research Journal, 08(2), 82–88. https://doi.org/10.31364/scirj/v8.i2.2020.p0220746

- Lubis, N. K., Hartono, A., & Mustoffa, A. F. (2019). Pengaruh Tekanan Eksternal, Ketidakpastian Lingkungan, Dan Komitmen Manajemen Terhadap Penerapan Transparansi Pelaporan Keuangan. ISOQUANT : Jurnal Ekonomi, Manajemen Dan Akuntansi, 3(2), 87. https://doi.org/10.24269/iso.v3i2.291

- Luthfiani, B. M., Asmony, T., & Herwanti, R. T. (2020). Analisis faktor – faktor yang mempengaruhi akuntabilitas pengelolaan dana desa di Kabupaten Lombok Tengah. E-Jurnal Akuntansi, 30(7), 1886. https://doi.org/10.24843/eja.2020.v30.i07.p20

- MacKinnon, D. P. (2011). Integrating Mediators and Moderators in Research Design. Research on Social Work Practice, 21(6), 675–681. https://doi.org/10.1177/1049731511414148

- Mada, S., Kalangi, L., & Gamaliel, H. (2017). Pengaruh Kompetensi Aparat Pengelola Dana Desa, Komitmen Organisasi Pemerintah Desa, dan Partisipasi Masyarakat Terhadap Akuntabilitas Pengelolaan Dana Desa Di Kabupaten Gorontalo. Jurnal Riset Akuntansi Dan Auditing “Goodwill, 8(2), 106–115. https://doi.org/10.35800/jjs.v8i2.17199

- Mahayani, N. L. A. (2017). Prosocial Behavior dan Persepsi Akuntabilitas Pengelolaan Dana Desa Dalam Konteks Budaya Tri Hita Karana. Jurnal Ilmiah Akuntansi Dan Bisnis, 129. https://doi.org/10.24843/jiab.2017.v12.i02.p07

- Marlina, E., Rahmayanti, S., & Futri, A. D. R. A. (2021). Pengaruh Kepemimpinan, Kompetensi, Teknologi Informasi Terhadap Akuntabilitas Pengelola Dana Desa di Kecamatan Rakit Kulim, Riau. Jurnal Akuntansi Dan Ekonomika, 11(1), 89–100. https://doi.org/10.37859/jae.v11i1.2517

- Matani, C. D., & Hutajulu, L. (2021). Pengaruh Kompetensi, Komitmen Organisasi, Partisipasi Masyarakat, dan Sistem Pengendalian Internal Terhadap Akuntabilitas Pengelolaan Dana Kampung Dikota Jayapura. KEUDA (Jurnal Kajian Ekonomi Dan Keuangan Daerah), 5(3), 21–45. https://doi.org/10.52062/keuda.v5i3.1532

- Merton, R. K. (1957). Social Theory and Social Structure (Revised Edition ed.). Free Press.

- Mualifu, M., Guspul, A., & Hermawan, H. (2019). Pengaruh Transparansi, Kompetensi, Sistem Pengendalian Internal, Dan Komitmen Organisasi Terhadap Akuntabilitas Pemernitah Desa Dalam Mengelola Alokasi Dana Desa (Studi Empiris Pada Seluruh Desa Di Kecamatan Mrebet Kabupaten Purbalingga). Journal of Economic, Business and Engineering (JEBE), 1(1), 49–59.

- Murray, D. (1990). The Performance Effects of Participative Budgeting: An Integration of Interventing and Moderating Variables. Behavior Research In Accounting, 2(2), 104–123.

- Mus, A. R., Malongi, S., & Alam, N. (2022). Effect of Internal Control System, Apparatus Competence, Internal Supervision on Accountability and Performance of Financial Managers of Makassar City Government. IOSR Journal of Business and Management, 24(7), 22–29. https://doi.org/10.9790/487X-2407052229

- Myers, D. G. (2010). Social Psychology (10 ed.). McGraw-Hill.

- Nalukenge, I., Kaawaase, T. K., Bananuka, J., & Ogwal, P. F. (2021). Internal audit quality, punitive measures and accountability in Ugandan statutory corporations. Journal of Economic and Administrative Sciences, 38(3), 417–443. https://doi.org/10.1108/jeas-05-2020-0084

- Nirwana, Haliah, Nirwana, N., & Haliah, H. (2018). Determinant factor of the quality of financial statements and performance of the government by adding contextual factors: Personal factor, system/administrative factor. Asian Journal of Accounting Research, 3(1), 28–40. https://doi.org/10.1108/AJAR-06-2018-0014

- Nuha, S. U., Miqdad, M., & Sulistiyo, A. B. (2021). The Implementation Internal Control System Government with Government Regulation Release of No. 60/2008 in KPU Jember Regency: A Phenomenology Approach. Jurnal Riset Akuntansi Dan Bisnis Airlangga, 6(2), 1091–1107. https://doi.org/10.20473/Jraba.V6i2.132

- Nurcahyono, N., Sukesti, F., & Alwiyah, A. (2021). Covid 19 Outbreak and Financial Statement Quality: Evidence from Central Java. AKRUAL: Jurnal Akuntansi, 12(2), 193. https://doi.org/10.26740/jaj.v12n2.p193-203

- Patton, J. M. (1992). Accountability and Governmental Financial Reporting. Financial Accountability & Management, 8(3), 165–180. https://doi.org/10.1111/j.1468-0408.1992.tb00211.x

- Preedy, V. R., & Watson, R. R. (Eds.). (2010). 5-Point Likert Scale BT - Handbook of Disease Burdens and Quality of Life Measures (pp. 4288). Springer New York. https://doi.org/10.1007/978-0-387-78665-0_6363

- Priantono, S., & Vidiyastutik, E. D. (2022). The Influence of Internal Control System and Accountability of Village Fund Allocation Management on Village Financial Performance. International Journal of Social Science and Business, 6(1), 18–26. https://doi.org/10.23887/ijssb.v6i1.40068

- Princy, K., & Rebeka, E. (2019). Employee commitment on organizational performance. International Journal of Recent Technology and Engineering, 8(3), 891–895. https://doi.org/10.35940/ijrte.C4078.098319

- Purbasari, H., & Bawono, A. D. B. (2017). Pengaruh Desentralisasi Fiskal, Sistem Pengendalian Internal Dan Kinerja Pemerintah Daerah Terhadap Akuntabilitas Laporan Keuangan. Riset Akuntansi Dan Keuangan Indonesia, 2(2), 102–108. https://doi.org/10.23917/reaksi.v2i2.4884

- Ramasoyan, R., Van Sweet Sesa, P., Patma, K., & Larasati, R. (2021). Analysis Of Human Resource Competency, Internal Control System, Quality Of Financial Statements and Application Of Government Accounting Standards To Accountability Of Performance Of Government Agencies In Pegunungan Bintang Regency. Journal of Social Science, 2(4), 429–443. https://doi.org/10.46799/jss.v2i4.188

- Riley, M. W., & Riley, J. W., Jr. (1994). Age Integration and the Lives of Older People1. The Gerontologist, 34(1), 110–115. https://doi.org/10.1093/geront/34.1.110

- Rofika, & Ardianto. (2014). Pengaruh Penerapan Akuntabilitas Keuangan, Pemanfaatan Teknologi Informasi, Kompetensi Aparatur Pemerintah Daerah dan Ketaatan terhadap Peraturan Perundagan terhadap Akuntabilitas Kinerja Instansi Pemerintah. Jurnal Akuntansi, 2(2), 197–209.

- Rosari, R., & Manabulu, H. A. (2020). Increasing An Accountability Of Village Financial Managament With Apparatus Competence And Government ’ S Internal. Jurnal Riset Akuntansi Dan Bisnis Airlangga, 5(2), 902–919. https://doi.org/10.31093/jraba.v5i2.209