Abstract

The significant transformations and advances attributed to the Era 5.0 require a comprehensive understanding of the current ramifications of the accounting discipline, along with the prospective difficulties and opportunities. This is pertinent not only in the context of industry, education, and society, but also in terms of labor relations and professions. Thus, the aim of this paper is to understand the current impacts and future expectations of the Era 5.0 on the accounting profession. Based on a recent systematic literature review we note the urgent and pressing need for educational institutions, their audiences, and other entities to interact in the changing process, creating synergies to ensure the success of retraining this valuable strategic resource in organizations and society, and the sustainability of the profession, promoting a sustainable Society 5.0. We contribute to the research on the consequences and challenges of the Era 5.0 in the future of the accounting profession by the originality of the contextualization of the profession in this new Era, filling a gap in the recent state of the art in the research of the accounting profession. We consider that this research will have an impact on academia, industry, and society, bringing these to work together in the development of the accountants’ skills and their future work.

1. Introduction

One of the biggest changes in humanity over the past 50 years has been the remarkable technological progress and growth, especially with the introduction of the internet (Kamal et al., Citation2019). Nowadays almost everyone uses the internet, in own personal devices. Almost every student uses the internet for information as well as a learning resource (Sudibjo et al., Citation2019). In the last decade our lives have been transformed. Digital technology has taken us from an industrial society centered on manufacturing to a society based on information. Both our private and professional lives are saturated with digital data and information technology through which we develop and share ideas, generating new businesses (H-UTokyo Lab., 2020). However, Purnamasari et al. (Citation2019) question whether we are ready to face the new digital era, not only in industry, but also in the revolution of society into Society 5.0.

The global digital revolution has irrevocably transformed industries and societies (Al-Htaybat et al., Citation2018). In the digital era, new changes, developments, and technological transformations are experienced by Artificial Intelligence (AI), robotic technologies, cloud systems, Blockchain, Industry 4.0 and Industry 5.0. The accounting profession is also affected by this change and transformation (Sabunco, Citation2022). The concept of Society 5.0 and Industry 5.0 is not a simple chronological continuation or alternative to the Industry 4.0 paradigm. They reflect the fundamental shift of societies and economies towards a new paradigm to balance economic development with the resolution of social and environmental problems, placing human beings at the center of innovation (Carayannis and Morawska-Jancelewicz, Citation2022). The changes brought about by the development of Industry 4.0 and Society 5.0 will further affect all aspects of human life. The current lifestyle is increasingly promoting practicality and efficiency and, in terms of fulfilling daily needs, Industry 4.0 and Society 5.0 encourage the emergence of various types of new consumer services (Sudibjo et al., Citation2019).

This context of accelerated change is an opportunity for accounting and accounting professionals. Accounting is more influential in our lives than many of us think or can imagine. Accounting, beyond a professional technique, is a social and moral practice that can help move capabilities and influence the creation of a better world (Carnegie, Citation2022), consistent with the principles of sustainability and the Era 5.0.

However accounting education has not kept pace with the technological innovation of multinational accounting firms, despite these firms’ large investment in technological innovation. In the face of changes in the industry, there is a need for existing accounting curricula at universities to prepare and “equip” students with the necessary technological skills for successful careers in accounting and auditing (Damerji & Salimi, Citation2021). With the new needs for information literacy, whether in the field of digitization or Big Data (BD), accounting (and finance) can take on a more strategic role and help to shape the future. It is accounting education that must produce accountants who match the needs of industry and society, with a curriculum that covers these areas of study (Surianti, Citation2020).

Therefore, to face this new era, special skills and strategies are needed to prepare for competition (Ellitan & Anatan, Citation2020) and it is urgent that people adapt to the new reality. The key is updating and developing new skills, in particular soft skills (e.g., communication, teamwork, or conflict management) and professional retraining for those who want to ensure their employability with sustainability. In the study “The Future of Employment and Skills at Work in 2030”, an assessment is made of future challenges and opportunities in the labor market and the implications for jobs and skills in greater demand in 2030, in “disruptive” scenarios. The same work indicates key areas for consideration by employers, individuals, education providers and policy makers (Störmer et al., Citation2014).

Zin et al. (Citation2022) state that the role of accounting education in preparing future accountants with the knowledge and skills needed to deal with BD in the industry is not yet in its infancy, as is its incorporation into accounting programs at higher education institutions. Also, Jackson et al. (Citation2022) highlight the need for broad and relevant collaboration between universities, employer organizations and professional associations to provide accounting education that meets industry requirements regarding technology-related skills.

The evolution of technology in Industry 4.0 has driven the transformation of various sectors in the current digital era. In reaction to these changes, the accounting profession has been forced to adapt, in the social and organizational environment in which accounting operates as the same is true for the tasks, responsibilities, duties, and skills required from accountants (Taib et al., Citation2022).

The emergence of Industry 4.0 as a new era characterized by digitization, information transparency, connectivity, and automatism, followed by the idea of Society 5.0, presents challenges to educational institutions (Sudibjo et al., Citation2019). In this sense, universities are called upon to produce knowledge for new technologies and social innovation and the incorporation of the assumptions of Society 5.0 and Industry 5.0, in their practices and policies, which will allow both universities and societies to fully benefit from the digital transformation (Carayannis & Morawska-Jancelewicz, Citation2022). Accounting education research shows the importance of developing various information and communication technologies (ICT) competences in accounting programs, in particular the ICT skills needed by consultants in professional service firms to help “transform” their clients’ businesses now and in the near future (Yigitbasioglu et al., Citation2022). ICT has become a key element in everyday life, affecting all dimensions that involve people and society (Carayannis & Morawska-Jancelewicz, Citation2022). The introduction of ICT requires a change in the organizational culture of universities and a commitment of the entire community (Benito-Osorio et al., Citation2013). Al-Hattami’s (Citation2021) study confirms that the inclusion of relevant ICT is still neglected in many of the accounting curricula in most universities, failing to meet the demands of the ICT labor market. Only with the inclusion of new technologies in accounting education, Education 5.0 is aligned with Society 5.0, in which the student is the protagonist, mediated by the teacher, who identifies problems, seeks solutions and, at the same time, works on various soft skills, so that the student is capable at the various social and professional challenges. As we have seen, education in the 21st century will face more severe challenges than in the previous century. However, society, in the era of Society 5.0, is a society that can solve various challenges and social problems using various innovations, including new tools, technologies and pedagogical methodologies.

Despite several works and approaches on accounting education over the last 10 to 15 years (Carnegie, Citation2022), there is still a lot to discuss about the future of the profession in the new Era 5.0. Ten years from now the accounting profession will look noticeably different than it does today (Shaffer et al., Citation2020). As accounting is a social science, its professionals will be able to adapt to rapid technological and social changes, also contributing to the improvement of the called Society 5.0. Society is people-centered, in which all citizens are expected to be dynamically involved, introducing digital technologies in a variety of systems, and accelerating their implementation, in favor of quality of life.

Around the years 2015/2016, references to the Era 5.0 began to emerge, whether in industry, society, or education, in addition to other aspects of society. Thus, modern society and industry present challenges to educational institutions, teachers, and students themselves, as future professionals who are required to have new skills, aptitudes, knowledge, and competences. Therefore, it is necessary to analyze the consequences of ICT and AI on the future of the professions and in the accounting profession. Authors such as Leitner-Hanetseder et al. (Citation2021), Yigitbasioglu et al. (Citation2022) and Jackson et al. (Citation2022) report that there are few studies supporting the influence and future consequences of new technologies on the accounting profession, which justifies the present paper. We try to show that all the agents involved in the profession need to reinvent themselves to address the professional needs of the new Era 5.0.

Since the aim of this paper is to understand the current impacts and future expectations of Era 5.0 - Industry 5.0, Education 5.0 and Society, in particular the so-called Society 5.0 - on the accounting profession, we will seek to answer three research questions based on a systematic literature review. The questions are: What is the role of higher education institutions in the technological change process?; What is the contribution of Education 5.0 to the challenges of the accounting profession?; and, How can the accounting professional adapt to the change and transformation of this new era? Thus, we can observe the enormous potential of Universities/Schools in the process of the rapidly changing professional and social competencies of the accounting professional. Accounting Education 5.0, with all partners involved in the process, is crucial in preparing a curriculum that can guide and mold students making them capable and ready to face the new era and the challenges of the accounting profession. We also see that the accounting professional is an apt and capable actor of rapid change and transformation, and a valuable strategic resource in organizations and society, who can, with new skills and roles in organizations and society, promote an innovative, creative, and sustainable Society 5.0.There is currently not much research that can be referred to the Era 5.0 and accounting Professionals’ Education 5.0, as this is among the agendas that are still under discussion. The question arises as to what initiatives can be taken promptly by universities, academic staff, and other bodies (organizations, professional associations, professional bodies, Government, …) in preparing accounting Education 5.0 with a curriculum that can address and shape students and make them capable and ready to face the new era and the challenges of the accounting profession. The era of digital transformation presents many opportunities for future research in the field of accounting.

This paper attempts to fill the gap in the state of the art of the accounting profession by seeking to summarize evidence of how research is addressing the evolution of technology in the profession, as well as to contribute to research on the consequences and challenges of Era 5.0 in the future of the accounting profession. It also seeks, considering the few existing studies, to fill the gap in identifying links between the accounting profession and the concepts of Society 5.0, Industry 5.0, and Education 5.0, for a new era. It also contributes to strengthen the relationship between professional bodies, academia, and the accounting profession itself.Footnote1

In this regard, and in addition to the introduction, we will present the theoretical background of the technological transformation and the paradigm of digitization in the Era 5.0 in the accounting profession. This will be followed by the methodology section, the discussion of the state of the art in the profession regarding the role of higher education institutions, the contributions of Education 5.0 and the future challenges of the profession. Finally, the concluding remarks will be presented.

2. Theoretical framework

2.1. Technological transformation

The well-known Industry 4.0, born in Germany in 2011, focused on collecting information from the network and have it analyzed by humans. In 2016, the Japanese government introduced Society 5.0, a human-centered society that balances economic progress, in which people, things, and systems are all linked together in cyberspace and physical space, to solve social problems (Nakano, Citation2022).

Industry 4.0 has created new values and services, bringing a richer life to everyone, and affecting the way people work and do business (Fitri & Putra, Citation2019; Pereira et al., Citation2020; Sudibjo et al., Citation2019). Although Industry 4.0 is still not well developed, a lot of industry pioneers and technology leaders are looking to the Fifth Industrial Revolution of autonomous manufacturing with human intelligence on and off the loop (Nahavandi, Citation2019). Thus, in contrast to the era 4.0, the Society 5.0 era can be interpreted as a human-centered and technology-based concept of society (Falaq, Citation2020).

The rapid evolution of information technologies makes it possible to combine physical cyber space with real-world information (Nakano, Citation2022; Önday, Citation2020). Having innovative technologies that allow us to accelerate the speed of communication, as well as facilitate information exchanges and business transactions in the space of a second is nothing short of surprising (Kamal et al., Citation2019). And this extraordinary development of technology and information has also had an extraordinary impact on the development of the industry and the structure of people’s lives (Ellitan & Anatan, Citation2020). Also, the rapid evolution of the web has presented universities with the challenge of preparing today’s academic staff for the ICTs of the future. Web 5.0 (sensory and emotive web), conceived to develop computers that interact with human beings, proposes a conceptual and methodological change in the teaching-learning processes in universities (Benito-Osorio et al., Citation2013).

Today, the Fourth Industrial Revolution is built on the digital revolution where technology and people are connected. The trend towards digitization, automation, and broadening the use of ICT in industry contains technologies of cyber-physical systems, Internet of Things (IoT), cloud computing, and cognitive computing (Alaloul et al., Citation2020). The combination and continuity between Industrial Revolution 4.0 and Society 5.0 can form a better pattern of social order, to improve the quality of people’s social life. Industry 4.0 and the Society 5.0 phenomena have brought about a trend of change both at the company and individual level (Ellitan & Anatan, Citation2020).

Industry 4.0 was the emergence of the IoT where automation, machine learning, connectivity and real-time data had been intertwined. Where digitization has opened a new path for manufacturing, with smarter and more sophisticated factories with the help of technologies such as the IoT, automation, robotics, sensors, data science, advanced analytics, and AI. The digitization would not make humans obsolete in the transformation process (Saxena et al., Citation2020). Although many small and medium enterprises show a desire to implement Industry 4.0 technologies, financial and knowledge constraints are the main challenges, despite the benefits it represents in flexibility, cost, efficiency, quality, and competitive advantage (Masood & Sonntag, Citation2020).

In Society 5.0, a lot of information is accumulated in cyberspace from sensors in physical space and this BD is analyzed by AI. The collection and evaluation of AI is beyond human capacity (Nakano, Citation2022; Purnamasari et al., Citation2019; Toprak et al., Citation2020).

AI is a general term for a machine’s ability to mimic the human way of feeling things, making deductions, and communicating (Nakano, Citation2022). Therefore, AI is considered smarter than traditional information systems, as it builds intelligent systems that are capable of learning, reasoning, adapting, and performing human-like tasks. AI provides a bridge for information systems to be transformed into intelligent systems, resulting in more automation and optimization of information systems (Damerji & Salimi, Citation2021). AI is expected to be a machine that truly has general intelligence like humans (Surianti, Citation2020).

Societies are increasingly delegating complex and risk-intensive processes to AI systems, such as probation granting, patient diagnosis, and financial transaction management, to be accountable, fair, and transparent (Cath, Citation2018). AI technologies are being developed, deployed, and used in a growing number of domains to perform complex tasks. However, on one hand, different schools must remain relevant in the AI era by preparing students and the workforce for it. On the other hand, educators must continue to incorporate AI training into higher education curricula and learning environments (Xu & Babaian, Citation2021). The era of Society 5.0 requires society to be able to control and balance the capacity of AI and social intelligence to solve all kinds of national problems (Falaq, Citation2020).

AI has begun to take center stage in the business world and is at the heart of digital transformation and business management. Thus, auditors will soon be able to use an intelligent chatbot to help them navigate the labyrinth of auditing and accounting rules, legislation, practices, and standards, as well as specialized literature (Tiron-Tudor & Deliu, Citation2022). For accounting (and auditing) the rise of robotic process automation systems, through AI, presents critical challenges (Gotthardt et al., Citation2020).

Many professions, such as accounting, are struggling with endless change and disruption as digital technologies challenge the previous professional services offered to clients (Wilkinson et al., Citation2018). Accountants need to be prepared to deal with ICT, from the education stage to the practice of accounting work, so that they understand how technology is changing the area in which they are expected to work, as accounting graduates (Al-Hattami’s, Citation2021). The Revolution 4.0 has also brought about changes in the role of accountants, so higher education must respond quickly and appropriately, either by inserting topics into existing courses or by creating new ones, so that the graduates can meet the qualifications needed for the job market (Surianti, Citation2020).

AI is rapidly growing in accounting practice and companies want to hire those who have adopted this technology. Universities can prepare students to adopt AI by partnering with AI software companies to adopt it in courses that explore the application of AI in accounting, in addition to institutionalizing it in different academic programs (Damerji & Salimi, Citation2021). For the development and implementation of effective web 5.0, pedagogy teachers need to become active and critical users of web 5.0 and develop their own skills and strategies to select or develop high quality web 5.0 and utilize the resources through strategic management of well-prepared activities (Benito-Osorio et al., Citation2013).

2.2. Digitization paradigm in Era 5.0

Digital transformation is not necessarily about a single technology, but a bundle of technologies such as AI, robotic process automation, BD analytics and cloud computing that dramatically affect the way organizations operate to remain competitive (Yigitbasioglu et al., Citation2022). Digital transformation requires the mobilization of ICT resources, including human resources (e.g., skills), ICT technology resources (e.g., hardware and software), and relational resources (e.g., ICT department partnership with other functions), in addition to the criticality of other resources and the flexibility of ICT resources (Yigitbasioglu et al., Citation2022). ICT resource as a range of information technologies, electronics, and telematics, using modern microelectronics, telecommunications, and computing to improve all types of devices, techniques and processes that influence different areas of human life (Berikol & Killi, Citation2021).

Digital transformation is the process of incorporating technological developments into business standards, processes, competencies, and models in a way that accelerates them and provides efficiency. It is the integration of digital technologies in all business processes and businesses, in order to remain in a competitive environment. It is also a transformation and cultural change (Sabunco, Citation2022). To smooth the automation process, it is recommended to determine the level of human involvement in the new digital environment, in general, and in the new digital workplace, in particular. Thus, humans must select the acceptable and develop clarity and confidence in the use of AI solutions, maximizing their benefits, which will increase professional credibility and open new opportunities for the profession (Tiron-Tudor & Deliu, 2021).

Digitization is considered one of the biggest and most lasting changes in society today, which already affects many areas of our lives (Leitner-Hanetseder et al., Citation2021). Digitization refers, by definition, to all areas of social life (Schneider, Citation2018). The digital transformation and the generalization of digital technologies have increased social complexity, with some negative aspects such as security risks and privacy issues (Fukuyama, Citation2018).

Digital connectivity implies data sharing and openness to a competitive market environment, resulting in transparent business ecosystems largely facilitated by online platforms (Müller et al., Citation2018). But, Industry 5.0 has introduced a paradigm shift from digitization to personalization in Society 5.0, where it will highlight the new concept of “Human Touch”, a human-centered society (Saxena et al., Citation2020, p. 360).

The ongoing transformations will cause a social change from the version Society 4.0 to Society 5.0. Society 5.0 will be a super-intelligent society, equipped with problem-solving and value-creation ideology, diverse capabilities, decentralization, resilience, and sustainable development, reinforcing the characteristics of Industry 4.0, making it evolve to a new industrial transformation (Industry 5.0), of autonomous manufacturing with human intelligence which will lead to the emergence of the Super-Smart society (Society 5.0) (Saxena et al., Citation2020).

The concept of Society 5.0 and Industry 5.0 is not a simple chronological continuation or alternative to the Industry 4.0 paradigm. Society 5.0 aims to place human beings at the midpoint of innovation, exploring the impact of technology and Industry 4.0 results from technological integration to improve quality of life, social responsibility, and sustainability. A pioneering perspective that has points in common with the United Nations’ Sustainable Development Goals (SDGs) (2030 Agenda) and with major implications for the transformation of universities (Carayannis & Morawska-Jancelewicz, Citation2022). The concept of Society 5.0 arises as a development of the concept of industrial revolution 4.0, which had the potential to degrade the role of human beings by transferring BD collected through the internet in all fields of life, including in the world of education, improving the quality of teachers (Darmaji et al., Citation2019).

According to Sudibjo et al. (Citation2019), Industry 4.0 and Society 5.0 also bring some changes to the education industry. The future of modern society presents challenges to educational institutions, so the learning characteristics in the era of Industry 4.0 and Society 5.0 are changing rapidly and need to be accommodated in the teaching and learning process, providing quality and appropriate well oriented educational services. Of note, the development and revision of emerging technology-related courses can be very demanding compared to other courses routinely offered, given the rapidly changing nature and lack of applicable materials. Further, ensuring that the course is relevant to business practices can be time consuming due to limited technological resources; faculty members in these courses require extra support and recognition for their efforts; critical collaboration is needed between accounting programs and the business profession and the business world, to bring new practices into the classroom (Wang, Citation2022).

Industry 5.0 is here to stay and put AI, robotics, BD, etc. at the service of men, where everything will be connected, and society will have to adapt. And here education and training—teaching - has an important role in the improvement of new skills in different areas, in particular in accounting.

The important competencies for the future workforce of digital natives extend beyond specific curriculum subjects to a broader skill set demanded by the global citizen. Important skills such as being responsive, innovative, flexible, agile, able to collaborate, dynamic analysis and to apply the “Human Touch” (Al-Htaybat et al., Citation2018).

Industry 5.0 will create more jobs than it takes away. It will create many jobs in the field of human-machine interaction and computational analysis of human factors, the area of intelligent systems, AI and robotics programming, maintenance, training, programming, redirection, and invention of a new generation of manufacturing robots (Nahavandi, Citation2019).

As mentioned by Ellitan and Anatan (Citation2020), technology and innovation need to be used to help and advance society, not to replace the role of human beings. The combination of Industry 5.0 and Society 5.0 can improve the quality of people’s social life, forming a better standard of social order. In Industry 5.0 there will be a fusion of human and technological skills and strengths for the mutual benefit of industry and industry workers, not replacing technology, but complementing human beings. It will enable safer, more satisfying, and more ergonomic work environments, in which humans can use their creativity to solve problems, adopt new roles and improve their skills (European Commission, Citation2020).

Accountants in the digital era must prepare more seriously to anticipate the impact of technology and the need to master non-financial data, such as data analysis, information technology development, and leadership skills (Surianti, Citation2020). Accounting firms and professional associations recommend that BD, technology, and information systems to be integrated into accounting courses to provide students the skills and knowledge needed to adapt to the data center environment. This is an opportunity for accounting educators to integrate these topics into the curriculum (Sledgianowski et al., Citation2017). More than ever, there will be a profound need for teachers to use and promote intra and interpersonal emotional skills. To develop emotional skills and transmit them to their students, to produce graduates who are better adapted to new socio-professional contexts (Benito-Osorio et al., Citation2013). Thus, it is necessary educators’ buy-in for the smooth implementation of a new curriculum reform, Education 5.0 (Muzira & Bondai, Citation2020).

3. Methodology

This study uses a systematic literature review, looking for references from various sources considered relevant to a case or problem that was found and studied. Systematic literature review is a replicable scientific process using criteria-based selection and analysis of published studies, allowing for an evidence-based summary of research (Cook et al., Citation1997). A systematic review of qualitative literature is a form of secondary study, synthesizing the results of multiple primary investigations. It is a means of identifying, evaluating, and interpreting all available research relevant to a particular research question, thematic area, or phenomenon of interest (J. Higgins & Green, Citation2008; Kitchenham, Citation2004).

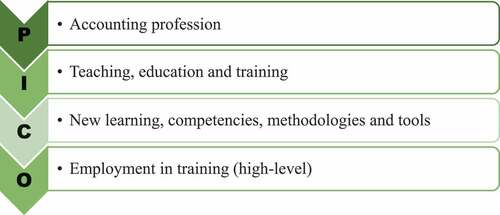

The systematic literature review summarizes existing work in an equitable way and is seen as fair (Kitchenham, Citation2004). The more systematic the review approach, the more transparent and reproducible the associated results are (Tranfield et al., Citation2003). These strategies include a search of all potentially relevant articles and the use of explicit and reproducible criteria in the selection of articles for review, seeking to answer specific questions (Cook et al., Citation1997)., To guide the formulation of our research questions, clearly and objectively, we used the PICO research strategy tools: population, intervention, control, and outcome (Figure ), as this is a qualitative study (Cooke et al., Citation2012).

Figure 1. PICO framework.

As the objective of this research is to assess the impact and challenges of the new technologies of Era 5.0 on the accounting profession and its opportunity for change and contribution for the new era, in industry, society, and education, three interrelated research questions were defined:

Q1: What is the role of higher education institutions in the technological change process?

Q2: What is the contribution of Education 5.0 to the challenges of the accounting profession?

Q3: How can the accounting professional adapt to change and transformation?

Thus, as a research strategy to identify relevant studies for the thematic literature review, we conducted a search using “Scopus” database from Elsevier and the “Google Scholar”. Scopus is widely covered and validated by the academic community (Chadegani et al., Citation2013). The Google Scholar is also an important source of data, despite the lack of quality control of publications (Harzing & Alakangas, Citation2016). For, at a minimum, all search strategies should be reported to ensure transparency and maximum reproducibility, including search strategies “for web search engines, websites, conference proceedings databases, electronic journals, and study registries” (Rethlefsen et al., Citation2021, p. 10).

In “Scopus” database the search was based on the general term “accounting profession”, between 2015 to 2022, including articles, title, abstract and keywords, in the subject area “Business, Management & Accounting”.

As in a first phase of the search strategy no documents were found with the strategy followed - (TITLE-ABS-KEY (accounting AND profession) AND TITLE-ABS-KEY (education 5.0) OR TITLE-ABS-KEY (industry 5.0) OR TITLE-ABS-KEY (society 5.0) AND TITLE-ABS-KEY (digital) OR TITLE-ABS-KEY (artificial AND intelligence))—the authors used another, which sought to be broader, considering that Era 5.0 is a new and recent theme. Thus, the criteria used in the research strategy are described in Table .

Table 1. Scopus search strategy

To complete the study, the authors conducted a new search in “Google Scholar”, searching for the terms “Industry 5.0”, “Education 5.0”, “Society 5.0”, isolated or combined, related to “Accounting Profession” and/or “digital” and/or artificial intelligence, increasing the breadth and depth of the topic under study, in the Era 5.0 (see Table ).

Table 2. Google scholar search strategy

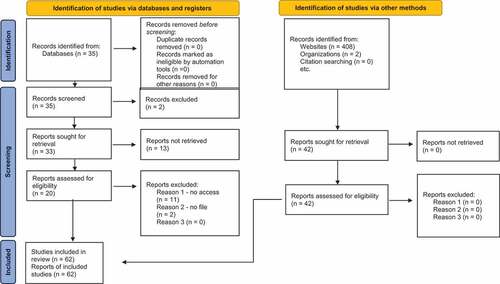

Thus, it was defined how the data would be extracted: select databases; establish the criteria for selection and exclusion of data; elaborate guidelines for data analysis; and determine the qualitative and quantitative analysis procedures to report the results (Rethlefsen et al., Citation2021). To conduct the systematic review of the literature, we followed the recommendations of the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA), which is composed of 27 evaluation items (checklist), that represent a minimum set of information to convey in a systematic review report, covering the rationale for the review, databases used to identify studies, results of meta-analyses performed, and implications of the review results, and a flowchart with the three main strategic blocks: 1. Identification, 2. Selection 3. Inclusion (J. P. Higgins et al., Citation2019; Page, McKenzie, Bossuyt, Boutron, Hoffmann, Mulrow, Shamseer, Tetzlaff, Akl, et al., Citation2021a) (see Figure ).

Figure 2. PRISMA.

The reasons for carrying out a systematic literature review are to seek to summarize the existing evidence regarding the implications, challenges, and opportunities of Era 5.0 in the accounting profession and to identify gaps in research in this area, to help define future research agendas (Cook et al., Citation1997, Tranfield et al., Citation2003; Kitchenham, Citation2004)., The article intends to be an integrative type of publication (Cook et al., Citation1997), so authors looked for various sources of reference that are considered relevant to a case or problem that was found and studied (Darmaji et al., Citation2019). “Complete reporting of systematic reviews is essential for users seeking to determine the trustworthiness and applicability of the review findings” (Page, McKenzie, Bossuyt, Boutron, Hoffmann, Mulrow, Shamseer, Tetzlaff, & Moher, Citation2021b, p. 109).

4. Discussing the state of the art

In this section, the studies that support the analysis to the research questions raised will be presented, as shown in Table .

Table 3. Selected studies related to the research questions

After reading and analyzing the articles presented in Table , we tried to match the articles with the research questions raised, as presented in the last column of that table, that is, Q1 (What is the role of higher education institutions in the technological change process?); Q2 (What is the contribution of Education 5.0 to the challenges of the accounting profession?) and Q3 (How can the accounting professional adapt to change and transformation?).

The systematic literature review is presented below, trying to answer the formulated questions.

4.1. The role of higher education institutions in the technological change process

The learning environment in the digital era is changing very rapidly (Sudibjo et al., Citation2019). Incorporating the assumptions of Society 5.0 and Industry 5.0 into university practices and policies will allow both universities, and societies, to fully benefit from the digital transformation. Thus, digitization opens new perspectives for universities and can become one of the main drivers of their change (Carayannis & Morawska-Jancelewicz, Citation2022).

A digital revolution would involve a disruptive transformation of all industrial and social systems. The university system has been also changing to reflect on digital transformation, as now the main procedure in the university is based on information processing in the engineering domain (H-UTokyo Lab., 2020).

Digitization opens new perspectives for universities and can become one of the main drivers of their change. In this sense, it is up to universities to explore the impact of Industry 4.0 and technologies, which will bring them great implications and transformations (Carayannis & Morawska-Jancelewicz, Citation2022).

In general, industry, society and the nation have looked to universities for solutions for the country’s development needs. Thus, education must help to solve existing social and national problems and universities must be transformed to meet the country’s development needs (Muzira & Bondai, Citation2020). Educational institutions, from elementary school to university, will have a key role to play in helping society acquire information literacy, along with business, government, and local communities. But education will have an essential role to play in training the human resources needed for Society 5.0 (H-UTokyo Lab., 2020). It is very important to ensure that education institutions offer continuously updated and technology related courses, covering a wide range of new and emerging topics, because the formal education system is the first place where future employees are educated (Kharbat & Muqattash, Citation2020).

Educational institutions must pay serious attention to how the education services can respond to new challenges caused by current changes and be able to accommodate technological advances in the era of Industry 4.0 and the new Society 5.0 lifestyle in educational processes (Sudibjo et al., Citation2019).

The main objective of society is to ensure the integration of technological developments, so instead of fearing technology, society must evolve to live with its cooperation. Society 5.0 is starting to reveal the causes of the name Industry 5.0, which is focused on ensuring the integration of technology with social life (Önday, Citation2020).

Toprak et al. (Citation2020, p.173) consider that in the university model required by Industry 4.0 or Society 5.0, “concepts such as joint education, cooperative education, integrated learning, sandwich learning, internship, experience-based learning, and work-integrated learning come to the fore”. Immersive and interactive educational experiences are the future of teaching and learning, combining the best of Education 5.0 and Industry 4.0 learning technologies to engage current generation learners whose learning style is unique even into the digital era (Kamal et al., Citation2019). Educational institutions must not be quickly satisfied and must continue to innovate to create excellence, based on quality in the provision of customer education services and human resource development, to be able to compete with competitors (Darmaji et al., Citation2019).

In this context, education and training institutions play an increasingly important role as providers of lifelong learning and must be aware of the opportunities and challenges inherent to AI (European Commission, Citation2020). Education systems, specifically universities, must change their programs to be more technology-oriented and future-oriented. Companies will also have to invest in technology and in the skillset of their employees, as it will be more expensive to lose business and risk bankruptcy (Kruskopf et al., Citation2020). Universities are called to produce knowledge for new technologies and social innovation (Carayannis & Morawska-Jancelewicz, Citation2022). Thus, universities, in addition to stimulating technological progress, must be responsible for cultivating literacy among information users through general curricula and recurrent education, in order to promote civil society that embodies Society 5.0 (H-UTokyo Lab., Citation2018).

4.1.1. Technology’s impact on accounting students

Incorporating the assumptions of Society 5.0 and Industry 5.0 into university practices and policies will allow both universities and societies to fully benefit from the digital transformation. Making human-oriented innovation the hallmark of universities and developing new cooperative models will also help to achieve sustainable priorities (Carayannis & Morawska-Jancelewicz, Citation2022).

Many universities now incorporate information technology, data analytics, cybersecurity, and database management courses into accounting programs (Shaffer et al., Citation2020). The future of work is a future where the human being and ICT are interconnected (Tsiligiris & Bowyer, Citation2021). However, not everyone has the digital competence to apply ICT to all spheres of life, being able to face challenges and provide solutions, so digital transformation is a current issue that concerns several education stakeholders (Adedoyin & Soykan, Citation2020).

Strong and Portz (Citation2015) surveyed accounting students at three Midwestern universities to determine their specific ICT knowledge levels and the difference between those ICT knowledge levels across universities. They found that accounting students have a low level of self-perceived ICT knowledge and that there are significant differences in ICT knowledge among the three universities in the study.

The study by Lodh and Nandy (Citation2017) reports that the link between higher education and the accounting profession enriches the accounting literature and can help policymakers identify better ways to enhance equality and inclusion of students with disabilities in higher accounting education.

On the other hand, Alvarez-Cedillo et al. (Citation2019) detect an essential deficiency in the current educational models in Mexico and that educational freedom is nil or scarce. This has led to poor student performance and high youth unemployment, which causes serious social and economic problems. It is necessary for the public sector to work closely with the private sector to link education and promote employment and give public schools more autonomy, freedom, and responsibility. This is the only way to achieve Society 5.0.

Kamal et al. (Citation2019) conclude that creating immersive and interactive educational experiences is the future of teaching and learning at Malaysian Universities. It is a real challenge for educators, who need to be one step ahead in learning how to adapt technology to classroom pedagogy, and students in readily utilizing technological learning such as Virtual Reality and Augmented Reality. They also mention the existing obstacles such as inadequate technical infrastructure and the weight of costs for both content creators (teachers) and end users (university students).

Purnamasari et al. (Citation2019) carried out a study collecting opinions from accounting students on preparation in the digital eras, the impact of the eras on the accounting profession, the institution’s support to deal with the digital times, the subjects/courses they have to learn and the difficulties in learning them, the methods/systems of learning in the classroom, the capacity of the lecturers/teachers and some facilities to support their learning process. They present students’ concern in preparing for the digital era, especially in these last eras of the industrial revolution and society and that there are student communities that are not prepared to face the new era.

Muzira and Bondai (Citation2020) reveal in their study exploring the perceptions of educators in relation to the adoption of Education 5.0 that was carried out at a State University in Zimbabwe, that Education 5.0 is a beneficial aid for the education system. However, infrastructure and financial resources for adequate implementation are lacking.

Damerji and Salimi (Citation2021) also examined the individual perceptions of 824 accounting students from two US universities on whether the readiness of AI technology influences its adoption. They found that the relationship between students’ technological readiness and the adoption of AI technology has a significant influence on its adoption.

Banasik and Jubb (Citation2021) visited public websites of Australian universities to analyze what Master’s level accounting programs offered, manually collecting the relevant data, according to the five specific employability skills that universities embody: digital and intellectual technology, communication, teamwork and leadership and management skills. They concluded that the various accreditation requirements are being satisfactorily met.

Silva et al. (Citation2021) in their descriptive research, applied a questionnaire to 361 accounting students from eitght higher education institutions in Rio de Janeiro, using a qualitative paper-and-pencil approach, whose responses were analyzed quantitatively. They concluded that accounting students strongly agree on the need to acquire strategic skills that will enable them to help organizations with information technology/information systems issues but are quite divided about the responsibilities of accountants in the future.

Taib et al. (Citation2022), in a total of 187 questionnaires obtained from trainees of accounting and finance, from public universities in Malaysia, who participated in the online survey, finding a significant link between the future technological readiness of accountants and digitization in the administrative profession. However, there is a weak relationship between technological knowledge and digitization.

Karlsson and Noela (Citation2022) investigated the beliefs of students from five Swedish universities that influence their attitudes and subjective norms, leading them not to choose the accounting profession in Sweden, through electronically sent questionnaires. The results revealed that what influences students’ decision to avoid the accounting profession was: a boring profession, higher salaries in other professions, the influence of teachers and peers. The authors suggest that accounting departments and business school faculties should recruit professional accountants and invite professional accounting bodies to create support activities that would motivate and help students learn more about the profession.

We found the study presented by Gebreiter (Citation2022) very pertinent, which concludes that the academic accounting profession is in danger of disappearing in many English business schools, which started to be colonized by teaching fellows with backgrounds in private sector accountancy tuition who implemented a highly technical accounting curriculum. The author also questions how to ensure that accounting research is sustainable and that it continues to be valued in a corporate higher education environment.

As can be summarized, higher education institutions are the engine and leverage of the process of technological change and transformation in accounting education, regarding the different skills these future professionals must possess, contributing to the progress and advancement of the Era 5.0 and onto the path to a new era. These institutions must be able to train their human resources, in particular accounting teachers and students, for the needs of the industry, the market and society, as well as attract them to the profession. They must stimulate their structures, their teaching staff, and the different professional entities to create synergies for the exchange of knowledge within this professional area, a pillar in the structure of any society and on the path to sustainable development.

4.2. Contribution of education 5.0 to the accounting profession

Education in the 21st century will face severely more challenges than in the previous century. The development of education in the era of industrial revolution 4.0 and Society 5.0 is inevitable and requires us to be ready to face the disruptions of innovation in all lines, including in education in this era of globalization, where the era is full of competition for quality in the world of education. Society in the era of Society 5.0 is a society that can solve various challenges and social problems using various innovations born in the era of industrial revolution 4.0 (Darmaji et al., Citation2019).

In the era of the Fourth Industrial Revolution, learning supports individuals to equip themselves to their best abilities and Education 4.0 is to meet the needs of an innovative society (Ishak & Mansor, Citation2020). Teachers must not be complacent with existing conditions in education; they must continue to improve to become teachers who can produce better quality human resources, as a way of balancing the development of Industry 4.0 (Lase, Citation2019). The Fourth Industrial Revolution presents many opportunities and challenges in a digitized world of work (Tsiligiris & Bowyer, Citation2021).

The accounting profession, like other professional areas, is evolving towards responding adequately to the demands of society, as a result of the profound implementation of information technologies in industries (Stanciu & Bran, Citation2015). The ongoing digital revolution requires the accounting profession to adapt and develop new accounting services that require a broader set of skills than traditionally. Professional accountants will need to possess the business acumen to initiate and manage change in an organization, provide solutions and become more involved in decision making (Banasik & Jubb, Citation2021).

In a changing world, it is necessary to prepare adequate human resources to be prepared to adapt and be able to compete on a global scale (Lase, Citation2019) and education and training have an important role in improving new skills and abilities. This is the only way to improve the so-called Society 5.0, a people-centered society, in which all citizens intend to dynamically engage, introducing digital technologies for the benefit of quality of life (Tavares & Azevedo, Citation2021).

Currently, the teaching-learning process is influenced by enormous technological advances. Industry 4.0 and Society 5.0 also bring some changes to the education industry as students of this era are tech-savvy and almost all of them have access to technology so they can easily get information (Sudibjo et al., Citation2019). They are digital natives and their ability to use intelligent technology and to take advantage of vast amounts of data and content available online is developed from an early age and gives rise to different educational demands and requirements in formal education (Al-Htaybat et al., Citation2018).

Accounting is an exciting and dynamic opportunity. But a comprehensive and integrated approach to international accounting education is needed to equip current and future professional accountants with the skills, capabilities, and ethical behavior required for an evolving business environment. A dual focus on technology and people development will make finance functions richer and more rewarding (IFAC - International Federation of Accountants, Citation2022). According to the work of Taib et al. (Citation2022), accountants need to have high skills and competencies, especially in ICT, professional knowledge and skills, good values ethics, and good attitude. Thus, they would be treated as the information technology manager, the designer, and the evaluator, not diminishing the influence of the accounting profession of accounting graduates.

With borders increasingly converging between humans, machines and other resources, ICTs certainly have an impact on several sectors, one of which is the education system (Lase, Citation2019). Another aspect presented by Karlsson and Noela (Citation2022) is the importance of bringing different bodies to the school, such as accounting professionals, to give lectures, workshops, discussion forums, with real-life examples and success stories, which will provide students with additional and valuable knowledge about the profession. The mentorship figure also allows for a closer connection between the student and the professional, as well as support and guidance.

4.2.1. The skills of the accountant in the Era 5.0

For the development of the visionary society there is a need for Education 5.0 that will be executed and implemented by Educators 5.0. The Educators will be the Cobots (Collaborative Robots), who will be chipped in with machine-centric knowledge, learned in human supremacy, trained in human personalization, and mastered in qualitative delivery based on the learner’s needs and capabilities. For a strong foundation of Industry 5.0, Education 5.0 will only be possible with intelligent, high-definition educators. The challenge for modern educators is to either prepare for this revolutionary change or accept the resignation (Saxena et al., Citation2020).

Digital technologies should play a supporting role in the development of students’ learning process in teaching accounting (Berikol & Killi, Citation2021). Learning models that adapt to the digital era are project-based learning and collaborative learning, which will encourage a variety of learning outcomes from students’ thought processes (Sudibjo et al., Citation2019).

In the knowledge-intensive society, universities and companies will have to help in the paradigm shift of technological development and in the cultivation of new industries that, in turn, will generate new value by pooling and combining knowledge (H-UTokyo Lab., 2018). Technology and innovation need to be used to help and advance society, not to replace the role of human beings (Ellitan & Anatan, Citation2020).

Society 5.0 will emerge with the concept of Industry 5.0 causing an industrial revolution that will be further strengthened by Education 5.0, generating high-definition educators, Educators 5.0 (Saxena et al., Citation2020). With the birth of the era of Society 5.0, new concept of community life, it is hoped that its leading technology in the field of education will not change the role of instructors in teaching moral education, character, and role models to students. The era of Society 5.0 is expected to be more comfortable for humans (Falaq, Citation2020). Thus, educators need to be reactive to changes in the profession and reshape their classrooms to focus on using more active learning models, which include soft skills and technology skills (Aldredge et al., Citation2021). Skills such as pattern recognition and understanding how to evaluate anomalies have not traditionally been the primary focus of accounting education and are often acquired through many years of experience in the field. However, it is necessary to educate students with an expanded skill set to be able to perform data analysis effectively (Earley, Citation2015).

The smart society will be equipped with a new version of education and Educators 5.0, who are likely to lead the world. Human beings will be equipped with collaborative and cooperative intelligent robots to efficiently perform the tasks undertaken. This new super-intelligent society will be enriched with “Human Touch”, with personalized products (Saxena et al., Citation2020).

Education 5.0 will be a personalized education system that will improve the teaching-learning process, producing highly qualified professionals. It will allow an individual to master the skills of how to learn, unlearn and relearn to adapt and embrace the ever-changing environment of the technical world, generating Industry 5.0 educational products. Thus, students would be prepared to withstand and face the uncertainties of the future with an enriched set of skills that will allow them to sustainably create new values and services to benefit and balance a society (Saxena et al., Citation2020). Sustainability is becoming prominent and increasingly seen as something that the professional community of accountants and managers must address in practice in order to enter the business world, leading to increased visibility and awareness of these issues. Thus, and despite the greater openness to teaching sustainability, teachers should be teaching these subjects (Cho et al., Citation2020).

The creativity and innovations that spring from future human generations and the intellect of advanced technologies will regulate and solve this uncertain problem for the future cyber-physical reality to progress adequately and gradually, providing the necessary resources to live and evolve together with the emerging security challenges, in the sense of establishing a new resilient and adaptable digital world (Minchev & Boyanov, Citation2018). Employment, public administration, people’s privacy, and industrial structure are undergoing drastic changes and digital information must respond to current demands (Pereira et al., Citation2020). It is necessary to adjust university curricula and teaching methods to new professional demands, due to the impact of information technology on the accounting profession. Each individual’s computer skills and knowledge become an obligation to ensure social and professional integration (Stanciu & Bran, Citation2015).

Therefore, teachers should not only emphasize their duties in knowledge transfer, but also in character education, morals, and role models. The application of soft skills and hard skills cannot be replaced by any sophisticated tools and technology (Falaq, Citation2020).

Despite the recognition of the high value placed on interpersonal skills by education (e.g., transferable skills, employability skills and soft skills), business, and government stakeholders, this area of skill development is still very nascent in accounting courses (Herbert et al., Citation2022). Accounting education must be changed, with a focus on cognitive abilities, such as critical thinking, teamwork and communication, an educational model centered on three pillars: technology, data, and human interaction. Improving accounting education is crucial to enable students to better understand and experience job opportunities (Shaffer et al., Citation2020).

The learning model that suits the digital era is blended/hybrid learning and e-learning, where the learning environment and atmosphere is the fast-paced IoT and AI. Still collaborative learning, in which students collaborate and work together in the learning process or in creating learning outcomes such as projects. It is the student-centered, teacher-led learning approach that suits the digital era and Industry 4.0 and Society 5.0 (Sudibjo et al., Citation2019).

The emergence of Education 5.0 highlights skills such as communication, leadership and resistance, curiosity, understanding, critical and creative thinking (Saxena et al., Citation2020). Falaq (Citation2020) considers that students are equipped with the necessary skills in the era of Society 5.0, including leadership, digital literacy, communication, emotional intelligence, entrepreneurship, and global citizenship.

Education is always a challenging process and the characteristics of today’s students (digital natives) make it even more demanding (Novak et al., Citation2021). To educate students with the latest skills and raise their standard of thinking, there is a need for high-definition educators, Educators 5.0. These educators will be able to stimulate and apply human intelligence and computer thinking processes, working in a collaborative environment with human beings (Cobots), which will enrich the learning process in Society 5.0 (Saxena et al., Citation2020).

Educational institutions should provide more opportunities for students to acquire skills to bring to the workplace. They should allow the application of their knowledge in field projects, as these are better tested when they work. They should also consider student opinions when designing and updating the curriculum (Ishak & Mansor, Citation2020).

Universities can design course implementation strategies that consider elements to institutionalize AI in academic programs (Damerji & Salimi, Citation2021). Because AI and robot process automation are disruptive and promising emerging technologies that, from the point of view of business management, have the potential to significantly affect the accounting and auditing areas, that is, they will automate accounting and auditing work and will cause labor substitution or supplementation. As society advances, Society 5.0, accountants, and auditors must adapt to these technologies in this new era (Nakano, Citation2022).

4.2.2. The role of the agents for a new accounting curriculum

Higher education is one of the fundamental forms of formal education that enables professional accountants to acquire the necessary knowledge and skills and to develop professional competence. Accounting education should consider market demands related to the skills and knowledge required from professional accountants and adjust the accounting curriculum as well as teaching methods accordingly (Novak et al., Citation2021).

The lack of skills in the accounting profession is not a new issue. The skills and aptitudes needed today for the accounting profession in the broadest sense are not being taught by most universities (Aldredge et al., Citation2021). Existing accounting curricula at universities around the world lack courses in AI technologies that effectively prepare accounting students for changes in the industry. Universities could partner with AI software companies to infuse courses that explore the application of AI in the accounting curricula. This technological readiness would influence the adoption of AI by accounting students and improve accounting students’ experiences in AI (Damerji & Salimi, Citation2021). Universities are a central hub linking accounting students and graduates to professional associations and employers, so they should make efforts to produce qualified graduates of technology skills (Jackson et al., Citation2022).

Various types of new jobs have emerged and their interest in learning is also undergoing changes influenced by evolution and changes in the type of work (Sudibjo et al., Citation2019). In the future people will work in new jobs using the IoT/AI/BD that currently do not exist, as it will require people with expertise in systems engineering, new training programs, new educational curricula, new teaching materials, including education in programming from an early age. These, by allowing to link remote locations, can facilitate active learning and observation of experiences (Aoki et al., Citation2019). There is a new challenge to revitalize education to obtain a competent, creative, and innovative human being who can compete globally (Lase, Citation2019). If universities are to compete and remain relevant both to students and to all industries that utilize accounting professionals, a strategic transformation in accounting curricula is needed (Aldredge et al., Citation2021). All professional accountants need to prepare for the online accounting process for all accounting related transactions and look for new opportunities and investments in their profession as technological developments will offer new opportunities and career areas for accounting professionals (Sabunco, Citation2022). As the use of AI begins to become widespread in accounting practice, students may become ill-equipped with the technological skills necessary to succeed in their careers in accounting and auditing (Damerji & Salimi, Citation2021).

University accounting programs are required to include ICT software tools in accounting courses in order to satisfy this requirement and help students to be ready for future professional life. It is important to integrate courses taught in related sections of digital technologies used in accounting applications into accounting (Berikol & Killi, Citation2021). The study from Al-Hattami’s (Citation2021) suggests including in the current accounting curriculum practical aspects on: professional and business values and ethics; implementing joint programs between universities and economic units in the labor market, which contribute to the development of the accounting curriculum; adequately preparing students regarding the use of computers in accounting; focusing on the use of ICT in accounting.

Accounting students must have specific knowledge, skills, and values, namely information literacy skills, communication skills, interpersonal skills, critical thinking, ethics, accountability, and international and domestic implications (Kharbat & Muqattash, Citation2020). Professional bodies and universities mutually benefit from strong ties and encourage professionals to transfer their knowledge and experiences from the real world to the classroom and lecture theaters. Academics, too, need to create real-world projects that allow students to learn theory while applying relevant professional skills (Wilkinson et al., Citation2017).

Another aspect is presented by Caglio and Cameran (Citation2017), stating that accounting firms and other professional bodies should question whether the importance of professional integrity and ethics and serving the public interest is sufficiently highlighted in continuing education and training programs, through university ethics courses.

Al-Htaybat et al. (Citation2018) focused the study on the expected changes and how the accounting profession, practice and education will be affected and adjusted to new technologies, investigating the perceptions of 16 accounting educators, with semi-structured interviews. The results show that participants’ opinions vary on the need to adjust the accounting curriculum, at the level of classic skills and contemporary skills.

In another line, the study by Soepriyanto et al. (Citation2020) states that it is important to encourage more female involvement in the top position of the audit and accounting industry to advance the profession and its positive impact to society. For female traits related to the monitoring role, greater responsibility, diligence, different points of view, compliance and less opportunistic tolerance are considered central reasons why gender diversity can improve audit quality and thus the quality of audited financial statements.

On the other hand, Kruskopf et al. (Citation2020) analyzed, with current real-life cases, the impact of current and future technologies in the fields of accounting and auditing that are shaping the future of new job descriptions and skills needed in these fields, by force of the digital era, where many predict that within 5–10 years humans will become obsolete in many areas of accounting and auditing. They concluded that their role is changing. Time-consuming and repetitive work will be automated, and the future accountant and auditor will perform more valuable work while transforming into finance and business consultant roles with more specific expertise.

Leitner-Hanetseder et al. (Citation2021) conducted a Delphi study to identify new roles and tasks in future accounting. They concluded that tasks and competencies for existing professional occupations will be subject to major changes over the next 10 years due to digital (AI-based) technologies, although “core” roles and tasks will continue to exist in the future. Some roles will not be played by humans, but by AI-based technology. For other “new” roles, humans will have to make informed use of digital technologies and collaborate with AI-based technology.

Gonçalves et al. (Citation2022) show in their exploratory study, of qualitative nature, which consisted of the analysis of three case studies, using document sources and semi-structured interviews, which aimed to analyze the impact of digital transformation in the accounting sector, that although the digital transformation in the accounting service of Portuguese small and medium-sized companies is just beginning, resistance to change, organizational culture and price seem to be the main barriers to digital transformation in accounting.

Yigitbasioglu et al. (Citation2022) explore, with semi-structured interviews with partners from Australian professional services firms, the role of accountants as consultants and examine the impact of digital transformation on the work, knowledge, and skills of accountants. Their findings show that accountants as consultants play a critical role in these companies and are a valuable strategic resource because of their unique abilities to combine generic human capital with digital human capital and social capital resources. They represent substantial human capital for such companies.

Jackson et al. (Citation2022) investigated whether universities, employers’ organizations and professional associations in Australia are preparing accountants early in their careers well for new technologies and future pathways to build technology-related skills. They found different perceptions between these two groups, accountants beginning their careers and managers/recruiters, but positive.

Sabunco (Citation2022), through a group discussion with accountants with offices in Denizli, sought to assess aspects related to the involvement of accounting practices in the digital transformation process. The results show that a radical change is needed to adapt quickly to this digital transformation in order to survive professionally and economically.

Moore and Felo (Citation2022) reviewed 185 accounting school websites, curricula, course descriptions, programs of study, and learning outcomes to determine how accounting departments incorporate data analytics into their curriculum. They also sent a survey of accounting professionals to seek their views on data analysis and accounting programs. They reveal that there are disruptive technologies that are largely being ignored and that accounting schools seem to be lagging in adopting data analytics in their curricula.

Synthesizing, with the emergence of new functions and jobs in the Era 5.0, higher education institutions should mobilize synergies towards Education 5.0, with their actions, promote change and transformation, and train capable professionals. Thus, accounting education must consider market demands related to the skills and knowledge required from professional accountants and adjust the accounting curriculum and programs as well as the teaching methods. Educators 5.0 are urgently needed. The accountant, as a key human capital in organizations, must possess a set of skills, such as personal skills, but also communication and teamwork, technical (financial and non-financial), business, leadership, and digital skills.

4.3. Challenges for the accounting professional

The 21st century is a century of globalization and learning content is expected to be able to reach 21st century skills: learning and innovation skills (mastery of diverse knowledge and skills, learning and innovation, critical thinking and problem solving, communication and collaboration, and creativity and innovation), digital literacy skills (information literacy, media literacy and ICT literacy) and professional and life skills (flexibility and adaptability, initiative, social and cultural interaction, productivity and accountability and leadership and responsibility) (Lase, Citation2019).

Kruskopf et al. (Citation2020) show the impact of Industry 4.0 on companies and changes in professions and the need to find the right talent and knowledge to know how to adopt the changes. There are professions that will change, performing higher value jobs, with more specific skills that focus their brain power on more rewarding tasks. Xue and Zan (Citation2022) interviewed 21 retired accountants, aged between 60 and 90 years at the time of interview, asking them to share their professional experience in open, unstructured conversations to investigate the career patterns of accountants in China by reconstructing the oral history of individual experiences, which gave insight into the interviewees’ professional lives. In summary, they found that the evolution of accounting took place in the context of a deeply underdeveloped profession within a huge country. But while the demand for accounting knowledge and education increased with the economy, it fell with political movements, along with the status of accounting.

IFAC - International Federation of Accountants (Citation2022) states that it is necessary to prepare the accounting profession for the future in the face of profound changes in the business ecosystem. The profession is not immune to change, and professionals are required to redefine their roles and contributions to society at large. Despite the great challenges for any type of profession, there will be opportunities for those who are prepared to embrace new technologies and automation, which can lead to better jobs. More focus is needed on the issue of qualifications and curriculum within the scope of Industry 4.0 (Berikol & Killi, Citation2021).

Technology and companies are rapidly changing and evolving, as are the expectations of accountants, and there is a growing disparity between what accountants do and what the core accounting curriculum teaches. With these advances in technology and the subsequent changes in business over the last decade, the lack of existing competence and skills is increasingly apparent (Aldredge et al., Citation2021). For this reason, accounting academics have also recently reported increased attention in the accounting profession to the employment of various technologies in the profession (Qasim & Kharbat, Citation2020). The accounting profession is expected to undergo significant change in the future due to technological developments (Al-Htaybat et al., Citation2018; Qasim & Kharbat, Citation2020).

4.3.1. New learning of the accounting professional

Lase (Citation2019) refers that the curricular reorientation, referring to ICT-based learning, IoT, BD and computerization, as well as entrepreneurship and internship, must include a mandatory curriculum to produce qualified graduates in literacy, technological literacy, and aspects of human literacy. For, students with high levels of interpersonal skills are better suited for real industry work and more competitive in their actual interviews or workplace (Herbert et al., Citation2022). Building networks between stakeholder groups, both at university and at work, could better prepare students and early-career accountants for new technologies (Jackson et al., Citation2022). ICT skills are one of the basic technical skills required by accounting graduates (Berikol & Killi, Citation2021).

The accounting profession cannot stand apart from the impact brought about by ICT advances because accounting plays a critical role in the information supply chain, which captures transactional data, integrates the data, and converts the data into usable or meaningful information for data consumers (Wang, Citation2022). Thus, Moore and Felo (Citation2022) consider that the accounting profession is undergoing a sea change that supplants many historical accounting duties, requiring technical skills to be added to the accountant’s toolbox.

There has been a change in the role of accountants, which has caused a shift in the hard skills and soft skills that must be owned by an accountant. The effectiveness and efficiency of accountants’ work can be improved using BD and cloud computing (Surianti, Citation2020).

Accounting education, as well as accounting practice, faces many changes and challenges (Novak et al., Citation2021). New technologies emerging in current accounting education are needed to support student learning development. Therefore, the use of digital technology tools used in accounting education processes should be encouraged (Berikol and Killi (Citation2021). Stakeholders are increasingly adopting disruptive technologies, including data analysis, blockchain, IA, and cloud computing (Moore & Felo, Citation2022). New technologies in accounting are widely regarded as crucial to building organizational success. They have and continue to have an impact on the skills needed for graduation and starting a professional career of accounting (Jackson et al., Citation2022).

As researchers and policymakers continue to work to provide students with the best possible education, a focus on preparing future accounting leaders in the education process area is vital. The job of accountants and auditors is not the same as it was 20–30 years ago and is expected to evolve into the future as new AI technologies emerge. Accounting programs/curricula must be prepared to address changing job requirements and industry practices to satisfy these requirements (Damerji & Salimi, Citation2021). The business environment requires accountants to have a high level of technical and computer skills. But as there is no defined standard curriculum for ICT knowledge in accounting education, faculty can teach ICT as they wish (Strong & Portz, Citation2015). Accounting programs worldwide should incorporate more technology into the curriculum in creative and meaningful ways (Jackson et al., Citation2022).

An unbalanced response between academia and the profession, in the face of technological advances in business operations, will have unfavorable results in the quality of graduates in accounting, as well as in the employability of these graduates. The risk is that if this dilemma persists in the future, the accounting profession may see hiring shifting to ICT graduates, with technical skills in blockchain, data analytics and AI, rather than hiring accounting graduates (Qasim & Kharbat, Citation2020). On the other hand, due to the growing importance of employability in higher education, the workload of teaching staff and students, who work hard to achieve multiple employability-oriented outcomes, increases (Tsiligiris & Bowyer, Citation2021).

The job market for accountants working in consulting service lines is growing, given the need for companies to continually undergo digital transformation, through innovative technologies such as cloud computing, BD analytics and AI. But they need to work more in the field of knowledge and skills, which is increasingly competitive due to digital transformation (Yigitbasioglu et al., Citation2022). The current implementation of new technologies in the industry should be considered by academia when designing and building a successful university accounting curriculum to prepare graduates for the market and to ensure their employability (Qasim & Kharbat, Citation2020).

AI erodes any traditional job as an accountant. But while technology platforms are replacing accounting jobs, there is still a demand for qualified, high-quality accountants, as AI helps professionals learn, think, and perform better. Technology cannot replace a human’s emotional intelligence and critical thinking capabilities soon (Purnamasari et al., Citation2019). Thus, in addition to initial professional training for an accountant career, continuous professional development, lifelong learning and maintaining professional competence are important and ICT should be incorporated into university curricula, professional curricula, and exams (Jackson et al., Citation2022).