Abstract

Over the last decades, research on the relationship between audit committees (ACs) and audit fees (AFs) has been increasing. Although numerous scholars have studied this topic, to the best of our knowledge, there is no systematic literature review (SLR) that provides a synthesized state of knowledge regarding this research area. To fill this gap this study presents a comprehensive systematic and objective review of existing research on the interaction between ACs and AFs. Using a sample of 78 articles, we find that most studies are empirical and country-specific and focus on developed markets in Europe and America. We also find that the majority of the examined papers use quantitative research methods by employing demand and supply theory either implicitly or explicitly. Further, we develop a categorization scheme, allocating the previous studies to six research themes (i.e. Composition, Diligence, Discrimination, Disclosure, Presence of (strong) AC and Compensation) and ten sub-themes. We then analyze each theme and its sub-themes providing details regarding its importance and impact on AFs and show that Diligence and Discrimination remain underexplored. Finally, we outline some potentially fruitful avenues for future research.

1. Introduction

Over the past three decades, the roles and responsibilities of audit committees (ACs) have been evolving due to environmentally-related economic and regulatory reforms (Kang et al., Citation2015). The impact of AC size, independence, meeting frequency, and the presence of financial expertise promoted by either hard laws (e.g., the Sarbanes-Oxley Act, Citation2002) or soft ones (e.g., various national/supranational codes of good governance) have been of central interest as means of improving the oversight of financial reporting, internal control, and auditor activity (Aguilera & Cuervo‐Cazurra, Citation2009; DeZoort et al., Citation2002, p. 40; Ghafran & O’ Sullivan, Citation2017). That is, the AC has been proven to play a significant role in financial reporting, and it is considered one of the most important board committees (Karim et al., Citation2016).

Among others, an interesting and prominent issue receiving attention in academia, the business world, and among governance activists is empowering ACs with a responsibility to determine external auditors’ compensation (Liu et al., Citation2021). For example, in 301 the SOX (Citation2002) mentions that ACs are directly responsible for auditors’ fees (Beck & Mauldin, Citation2014). In contrast, the United Kingdom has adopted a more laissez-faire approach according to which AC roles and responsibilities should include “conducting the tender process and … approving the remuneration and terms of engagement of the external auditor” (Financial Reporting Council, Citation2018, p. 11). The main objective of these “approaches” is to eliminate the management’s influence over external auditors’ hiring and audit fee (AF) negotiation processes (Liu et al., Citation2021). Under this notion, ACs are not only responsible for overseeing the financial reporting process but also for hiring, compensating, and handling disputes with external auditors (Vafeas & Waegelein, Citation2007). However, the governance role of ACs differs across countries in terms of regulatory responsibilities, and in the determination of external auditors’ compensation (Ghafran & O’ Sullivan, Citation2013). This could be attributed to different specificities, such as in the corporate governance system, the legal system, the cultural background, and the institutional framework (R. La Porta et al., Citation1997; R. L. La Porta et al., Citation1998; Smith et al., Citation2021; Yatim et al., Citation2006).

Considering the second component of our research, audit fees, they are among the most topical audit quality issues and have attracted considerable attention from researchers, audit standard setters, regulators, and stakeholders (Beck & Mauldin, Citation2014; Camfferman & Zeff, Citation2018; D. Hay & Knechel, Citation2010). The increased interest in AFs arises from the assumption that it represents one of the most common measures of audit quality in the literature (DeFond & Zhang, Citation2014; Fredriksson et al., Citation2020; Simnett et al., Citation2016). This suggests that the audit effort is reflected on AFs and is linked to the quality of financial reporting (Caramanis & Lennox, Citation2008; DeFond & Zhang, Citation2014). Thus, a decrease in the allowable detection risk causes an increase in the audit effort and AFs (Duellman et al., Citation2015). Consequently, audit pricing could be interpreted as a way of improving audit quality (DeFond & Zhang, Citation2014).

Collectively, the above discussion illustrates that ACs are the primary entity for audit oversight that can affect a firm’s AFs (Abbott et al., Citation2003a; Karim et al., Citation2016). In practice, ACs affect AFs in two ways: through the selection of auditors, which, in turn, impacts the audit scope and plan (Karim et al., Citation2016). A review of the extant literature that examines the association between AC characteristics and AFs has the potential for making theoretical and practical contributions by clarifying the following: “What have we learned so far, where do we go from here, what do the findings mean for practice, and what are the most fruitful avenues for future research?” (Carcello et al., Citation2011, p. 1). To date, these key questions have not been addressed in the literature.

There are plenty of reasons to undertake a systematic literature review (SLR) of this increasing area of research. First, this corpus of literature is dispersed across a wide range of academic journals from various academic disciplines (e.g., Accounting, Finance, and Ethics-CSR-Management), and it is difficult to construct a general picture of the present state of the specific research domain. This is important for a number of reasons. First, because existing studies use a range of AC characteristics, different theoretical lenses (e.g., demand and supply theory on the demand side, the supply side, or both sides) and supplementary theoretical perspectives (agency theory, institutional theory, political theory, etc.), the contributions of which should be identified. Second, there is a shortage of AF studies in times of economic turbulence (i.e., COVID-19 pandemic), especially, in emerging markets and in smaller entities, which has led to calls for the utilization of archival auditing research (Albitar & Hussainey, Citation2021; Cordery et al., Citation2022; Duppati & Wellalage, Citation2022). Hence, we illustrate the research gaps in terms of empirical investigations, and clarify the challenges and opportunities for future research. Third, our study is motivated by prior studies’ inadequacy in providing a systematic synthesis of studies on the association between AC characteristics and AFs. For instance, Cobbin’s (Citation2002) review study regarding the determinants of AFs fails to mention the impact of ACs, possibly because of the limited research during the examined period. Similarly, the recent study of Widmann et al. (Citation2020) does not consider the potential impact of AC characteristics on AFs. Prior meta-analysesFootnote1 (D. Hay, Citation2013; D. C. Hay et al., Citation2006; Widmann et al., Citation2020) that have focused on determinants of AFs do not provide consistent results regarding the relationship between ACs and AFs, allowing room for further investigation. Specifically, D. C. Hay et al. (Citation2006, p. 175) state that “much more research is needed on this issue,” and D. Hay (Citation2013, p. 174) specifically suggests that “future research may be more usefully directed to individual issues, rather than to meta-analysis of all AF studies.”

Based on the premise that an SLR focused on a specific issue helps organize the literature into a coherent body of findings and generate new knowledge (de Geus et al., Citation2020; Massaro et al., Citation2016), this SLR aims to provide answers regarding the impact of ACs on AFs. Additionally, it aims to develop critical insights and suggest future research paths regarding this corpus of scholarly literature. Finally, and more broadly, this research is relevant not only to scholars but also to policymakers and practitioners (e.g., auditors, directors) who seek to improve firms’ Corporate Governance (CG) quality through AC empowerment.

We contribute to the literature by answering three key research questions (RQ): (RQ1) How is research on the impact of ACs on AFs being developed? (RQ2) What is the literature’s focus and critique on the impact of ACs on AFs? (RQ3) What is the future for research on the impact of ACs on AFs? To address these research questions, first, we focus on studies published between 1996 and 2023, as there is lack of comprehensive literature regarding this issue in these years. Second, we reflect on the existing research published in established and quality journals indexed in the 2021 Academic Journal Guide (2021 AJG)Footnote2 and/or the 2023 Australian Business Deans Council Journal Quality list (2023 ABDC).Footnote3

Our study is the first to cover a comprehensive review of 78 papers from 37 journals. Moreover, for all three RQs it bases its analysis of the relationship between AC characteristics and AFs on numerous key criteria. More specifically, the development of AC impact on AFs (RQ1) is evaluated on the basis of three criteria: the number of studies per journal discipline, the geographic area, and the Morgan Stanley Capital International (MSCI) country classification. This enables us to contribute to a deeper understanding of how this issue has changed over time and across various locations and academic disciplines. Similarly, three criteria are applied to present the focus and criticisms of the literature (RQ2): the number of studies by type of research and data collection approach, theories, and research theme. By identifying these key features, we highlight the challenges and the skepticism that researchers may face. Finally, we answer the third question using the directions suggested by the analysis of RQ1 and RQ2. This enables us to identify unexplored topics which researchers should consider in the future.

The rest of the paper is organized as follows. Section 2 describes the methodology. Section 3 presents the review of the findings by answering the three RQs and presenting avenues for future research. Section 4 concludes the study.

2. Methodology: Systematic literature review

To the best of our knowledge, the only studies that examine the factors affecting AFs are the review study by Cobbin (Citation2002) and the meta-analyses of D. C. Hay et al. (Citation2006), D. Hay (Citation2013), and Widmann et al. (Citation2020). These studies covered a long period of research and concluded that the effects of the characteristics of firms and CG on AFs are inconclusive and that further research is necessary. On that basis, the field lacks a full, critical, and up-to-date SLR examining the impact of ACs and the effect of each of AC characteristics on AFs. This study fills this gap by conducting an SLR as outlined by several scholars adopting this methodology in the accounting and CG disciplines, such as Alhossini et al. (Citation2021), Ibrahim et al. (Citation2022), Lu et al. (Citation2022), Nerantzidis et al (Citation2020, Citation2023). T. H. H. Nguyen et al. (Citation2020) and Schmidthuber et al. (Citation2020).

2.1. Literature review protocol

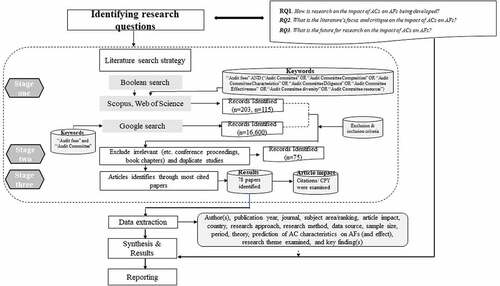

We developed a review protocol to reduce research bias (Stechemesser & Guenther, Citation2012; Xiao & Watson, Citation2019) and guide the SLR. We agreed on the rationale for the survey, research questions, search strategy, and choices regarding data analysis (Busalim & Hussin, Citation2016; Nerantzidis et al., Citation2020; Tsalavoutas et al., Citation2020). This conceptual foundation promotes our review’s reliability (Xiao & Watson, Citation2019) as well as replication by other scholars (Snyder, Citation2019). Figure presents the review protocol used in this study.

Figure 1. Review Protocol.

2.2. Literature search strategy

To search, gather, and analyze studies on AC characteristics and their impact on AFs, we developed a three-step approach based on Alhossini et al. (Citation2021), Street and Hermanson (Citation2019), Nerantzidis et al (Citation2020, Citation2023), and T. H. H. Nguyen et al. (Citation2020), as presented in Figure .

For the first step, we used Google Scholar, Scopus, and the Web of Science as major electronic sources to ensure that we identified all eligible studies based on reputation in terms of size and publication quality (Nerantzidis et al., Citation2020; T. H. H. Nguyen et al., Citation2020). We then performed a Boolean search within the databases of Scopus and Web of Science using “Audit fees” and “Audit committee” (or “Audit committee composition,” “Audit committee characteristics,” “Audit committee diligence,” “Audit committee effectiveness,” “Audit committee diversity,” and “Audit committee resources”) as keywords and phrases. A total of 203 papers were collected from Scopus and 115 from the Web of Science (regarding Boolean searches, see Street & Hermanson, Citation2019). Moreover, Google Scholar was searched using “Audit fees” and “Audit committee” as keywords. This search generated an additional 16,600 potential studies.

For the second step, we reviewed the titles, abstracts, and keywords, and excluded irrelevant studies, conference proceedings, books, and non-English studies (Kubíček & Machek, Citation2019). Moreover, to ensure that our SLR only referenced established and quality journals (similar to Tsalavoutas et al., Citation2020), we retained only articles in journals indexed in the 2021 AJG and/or the 2023 ABDC. This resulted in a set of 217 papers (74 from Scopus, 62 from the Web of Science, and 81 from Google Scholar). We also excluded any duplicate papers, ultimately retaining 75 studies.

For the third step, we used the most-cited studies and gathered all of their cited references. Through this process, we identified three further studies that were relevant and not retrieved during the second step. Thus, our final dataset comprised 78 studies conducted in different contexts from 1996 to 2023. These conditions confirmed that the 78 studies are unbiased and valid and can provide reliable insights from different countries.Footnote4 Indeed, 66 of these were published in journals that AJG ranked 2 or above, while, according to ABDC, 72 were ranked B or above. This study only focused on papers published in established and quality journals, as reflected in previous auditing review studies (e.g., DeFond & Zhang, Citation2014; Simnett et al., Citation2016). However, future researchers could broaden the boundaries to include lower-ranked journals, book chapters, practitioners’ journals, conference proceedings, and working papers (Massaro et al., Citation2016; Rinaldi, Citation2022). This is particularly pertinent in emerging research fields (i.e., where little literature exists), or when unpublished working papers reflect new areas towards which contemporary research is oriented (Lennox & Wu, Citation2018). While grey literature has started to gain popularity in academia in recent years (Mahood et al., Citation2014), the usage of quality peer-reviewed studies as a unit of analysis is the most widely accepted approach in SLRs in the accounting and auditing field for ensuring objectivity and reproducibility (e.g., Lombardi et al., Citation2021; Nerantzidis et al., Citation2020; Schmidthuber et al., Citation2020).

In this third step, we also examined the articles’ impact using the number of citations on Google Scholar (as of 5 July 2023) to indicate whether scholars have a strong interest in this field of research (see, Cricelli et al., Citation2021). We found that the 78 studies we reviewed were cited 8,434 times. To counterbalance the tendency of older articles to accumulate more citations, we also utilized the average number of CPY (Dumay & Dai, Citation2017). Table presents the top 10 reviewed studies by total citations (Panel A) and CPY (Panel B). We found that six articles appeared in both rankings. This confirms that there is contemporary and continuing academic interest in the impact of ACs on AFs.

Table 1. Indicative impact of reviewed studies

Finally, a data extraction form was created in which the following information was recorded: author(s), publication year, journal, subject area/ranking, article impact, country, research approach, research method, data source, sample size, period, theory, AC characteristics’ effect on and ability to predict AFs, research theme examined, and key finding(s) (see appendix 1).

3. Results of the systematic literature review

3.1. Development of research on the impact of ACs on AFs

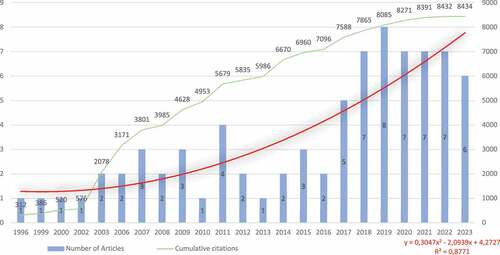

With this research question, we aim to clarify how much research exists on this topic, in what settings, and concerning which periods. This will help scholars and CG practitioners identify the issue’s key components. The answer to this first RQ arises from the description of our data. Figure depicts the details regarding the change in the number of publications of the examined topic and the cumulative citations between 1996 and 2023. It can be observed that there has been a significant increase in the number of studies published from 2017 to 2019. This could be explained by regulatory reforms, and the development and diffusion of new best practices related to AC over the past decade. However, considering the time lag between the periods of investigation and the year of publication, it can be surmised that the intense interest began a few years before 2017 (see, Appendix 1). The general observation is that there is a growing trend that illustrates the constant academic interest in the impact of ACs on AFs. This is also apparent from the citation growth trend, which indicates the increasing significance of this issue, as the total number of citations has grown over the years.

Figure 2. Number of studies and cumulative citations on the impact of AC on AFs by year.

Below, we present the key features of RQ1 based on the three criteria reported in Table .

Table 2. Results of analysis of research question 1 on three criteria

3.1.1. Number of studies per journal discipline

This criterion allows us to identify the number of studies included in our SLR by journal discipline. Following Alhossini et al. (Citation2021), Nerantzidis et al. (Citation2020), and Tsalavoutas et al. (Citation2020), we categorized the studies into four journal disciplines based on the 2021 AJG and 2023 ABDC: i) Accounting, ii) Finance including actuarial studies, iii) Ethics-CSR-Man, and iv) IB & Area/Strategy, Management and Organizational Behavior. The 78 selected studies were found in 37 journals, with the majority in the accounting field; only 11 were published in the other three disciplines (Table ). According to Table , the most prolific journals with at least three relevant published studies were Managerial Auditing Journal (13 articles), International Journal of Auditing (five articles), European Accounting Review (five articles), Accounting & Finance (five articles), Journal of Contemporary Accounting and Economics (four articles), Accounting Research Journal (three articles), and Contemporary Accounting Research (three articles). While AC and audit pricing are published in a wide range of journals, mainly in accounting and auditing, it is evident from the results that top-tier accounting and auditing journals like Auditing: Α Journal of Practice and Theory, The Accounting Review, and Journal of Accounting and Economics are rather under-represented. This may be explained by the papers’ inability to present an incremental contribution due to inadequate theoretical discussion, methodological shortcomings, etc. The review presents the challenges and opportunities involved in tackling these issues.

3.1.2. Geographic area

This criterion was adjusted by Dumay et al. (Citation2016), Guthrie et al. (Citation2012), Nerantzidis et al. (Citation2020), and Tsalavoutas et al. (Citation2020). It depicts the geographical area (i.e., location/regions) where the research was conducted. The results show that the examined topic is an issue with global reach. We categorized our papers into Europe (B1), Asia (B2), Oceania/Australia (B3), Africa (B4), America (B5) and Worldwide (B6). According to the results, the majority of studies were conducted in America (30/78), while Europe (20/78), Oceania (10/78), and Asian countries (14/78) were also remarkable areas. Evidence is scarce from Africa and other world regions as described in the next subsection. This may be explained by limitations in the literature search and the journal selection strategies used.

3.1.3. Number of studies per country classified according to MSCI

This criterion classifies the studies across Developed (C1), Emerging (C2), Frontier (C3) and Standalone (C4) countries and complements the previous criterion. This separation was adopted in the MSCI equity indexes, which are widely used for interregional comparisons (see D’Onza et al., Citation2015; Nerantzidis et al., Citation2020; Sarens & Abdolmohammadi, Citation2011). The impact of ACs on AFs was examined in 29 different countries, with the most recurrent being in Developed markets (61.5 papers). The majority of studies refer to the United States (29/78), while several also refer to the United Kingdom (12/78) and Australia (8/78). However, there are fewer studies in Emerging markets, such as Malaysia (4.25 papers), and almost none in Standalone Markets, with only one paper for Lebanon. Therefore, evidence is lacking on the impact of ACs on AFs for Emerging, Frontier and Standalone markets such as Korea, China, Greece, Nigeria, and Jordan. This limitation may also be attributed to the literature search and journal selection strategies used.

3.2. Literature’s focus and critique on the impact of ACs on AFs

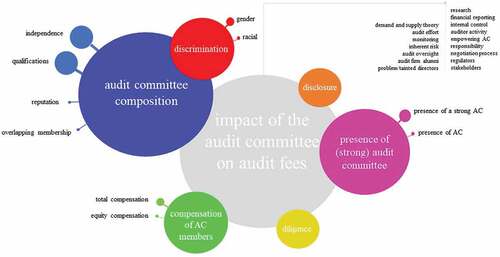

This subsection describes the focus and critique of the literature on the impact of ACs on AFs and discusses key features based on five criteria. The main findings are presented in Table and Figure .

Figure 3. Representation of research themes and sub-themes.

Table 3. Results of analysis of research question 2 on the first two criteria

3.2.1. Number of studies by type of research method, and by data collection

This criterion has been adopted by Zattoni et al. (Citation2020) and presents the methods used in the selection of sample articles and data collection. Table indicates that most previous studies have employed primarily quantitative methodsFootnote5 (D1; 76/78), while qualitative methodsFootnote6 (D2) and experiments (D3) are rarely used (one study each). Consistent with AF literature (D. Hay, Citation2013; D. C. Hay et al., Citation2006), empirical research still outweighs qualitative research. This may be because qualitative researchers face constraints in statistically generalizing their findings; consequently, scholars prefer the nomothetic study focus over the idiographic spectrum (Parker & Northcott, Citation2016).

Regarding data collection, Table provides an overview of the three alternative approaches employed. Most of the sample articles used retrieved data from databases and hand collected data, which is called the mixed approach (E3;30/78). Scholars combine databases, such as AuditAnalytics, Compustat, ExecuComp, RiskMetrics, BoardEx, Datastream (e.g., to collect audit data, financial related data, executive compensation data, and biographies of AC members), and hand collected data from various sources (e.g., annual reports, questionnaires, and corporate governance statements) to create their dataset. Nevertheless, there are some articles that only used either databases (E2;22/78) or hand collected data (E1;25/78).

3.2.2. Theories

This criterion was adapted from Alhossini et al. (Citation2021), Nerantzidis et al. (Citation2020), and T. H. H. Nguyen et al. (Citation2020) and allows us to extract information about each study’s theoretical background and to explicitly show how these theories are linked with the association of AC characteristics with AFs (prediction and effect). This SLR revealed that the majority of the examined papers used demand and supply theory by referring to it either implicitly or explicitly. We classified these studies into four main categories: i) Demand and supply theory (F1), ii) Demand and supply theory on the demand side (F2), iii) Demand and supply theory on the supply side (F3), and iv) Actor-network theory (ANT; F4). Further, we noticed that several studies used demand and supply as their main theoretical perspective and connected it to other theories to address their theoretical underpinnings (e.g., agency theory, institutional theory, organizational behavior theory). Table provides the results for the various theoretical perspectives.

Our review shows that most studies used demand and supply theory, whether from the demand side (26/78), from the supply side (12/78), or from both sides (31/78), as their main theoretical perspective (Panel A). Moreover, one qualitative study used ANT,Footnote7 and eight studies did not list or/and apply any theory (F5). According to the demand and supply theory, the relationship between ACs and external audit is complex. Specifically, from the demand-side perspective, AC presence can cause an increase in AFs, since the committee may need further work to be accomplished by external auditors for greater assurance to mitigate the reporting risk and satisfy its requirements for better reporting quality (Collier & Gregory, Citation1996; Goodwin‐Stewart & Kent, Citation2006; Harjoto et al., Citation2015). Alternatively, from the supply-side perspective, an AC’s involvement in strengthening internal controls may be viewed by the external auditors as improving the overall control environment and therefore reducing the auditor’s control risk, leading to lower AFs (Abbott et al., Citation2003a; Collier & Gregory, Citation1996; Goodwin‐Stewart & Kent, Citation2006). However, as Krishnan and Visvanathan (Citation2009) mention, the demand- and supply-based arguments are not mutually exclusive and may co-exist. This illustrates that strong governance can increase the demand for auditing (increasing AFs) and/or reduce auditors’ risk assessments (reducing AFs; Carcello et al., Citation2002, Citation2011). Primarily, as indicated in Table , regardless of the side from which the authors approach the demand and supply theory, AC characteristics may have a positive (e.g., Kalelkar et al., Citation2018; Lai et al., Citation2017; Stewart & Munro, Citation2007), negative (Chan et al., Citation2013; Habib & Bhuiyan, Citation2018; Nekhili et al., Citation2020), or no effect (O’Sullivan, Citation1999; Rainsbury et al., Citation2009) on AFs. This illustrates that research findings are much more interesting than the adopted theory would predict.

Further, some studies supplement the demand and supply theory with other perspectives, with agency theory being the most commonly used (Panel B). Authors use this framework to explain whether an AC’s characteristics can strengthen or weaken its monitoring role and, thereby, affect financial reporting quality (Liu et al., Citation2021). Surprisingly, the majority of studies focusing on agency theory (either from the demand side or from both sides) have found positive relationships between AC characteristics and AFs (e.g., Fredriksson et al., Citation2020; O’Sullivan & Diacon, Citation2002; Zaman et al., Citation2011). In contrast, only one study found both positive and negative relationships. Schrader and Sun (Citation2019) showed that equity compensation with option grants is negatively related to AFs, while equity compensation with stock awards is positively related.

Only a small percentage of the examined papers (12/78) incorporate more than two theoretical perspectives (e.g., Ariningrum & Diyanty, Citation2017; Bliss et al., Citation2011; Engel et al., Citation2010) to explain how AC characteristics impact AFs. Interestingly, these studies investigate more refined issues, such as gender/racial discrimination (Aldamen et al., Citation2018; Johl et al., Citation2012), compensation of AC members (Engel et al., Citation2010; Liu et al., Citation2021) and AC effectiveness (Ariningrum & Diyanty, Citation2017); this could explain the incorporation of multiple theories. In fact, scholars espoused the advantages of theoretical triangulation/pluralism (i.e., the benefit of using multiple theories) in order to better describe the impact of these “mechanisms” on AFs (Hoque et al., Citation2013).

Overall, the analysis demonstrates that scholars have drawn on different theories to explain the association between AC characteristics and AFs, each theory with its own assumptions and limitations. Some, typically newer publications, indicate an increasing interest in using multiple theories to better explain and test different aspects of this relationship, seeking to construct an optimal theoretical foundation. For instance, a considerable amount of research uses agency theory supplementarily, although the theory is treated differently based on the context examined (see Weimer & Pape, Citation1999), country, industry and regulation. As each theory has its own assumptions and limitations, a combination of theories can complement each other in determining the optimal theoretical foundation.

3.2.3. Research theme examined

To develop the categorization scheme, we considered the framework and the attributes of Alhossini et al. (Citation2021) and DeZoort et al. (Citation2002) relevant to our context. To avoid any problems with allocation in cases wherein more than one research sub-theme is examined, we followed the classification process of Rinaldi (Citation2022). In this process, each study was classified according to its main purpose as highlighted by its authors. This provided the opportunity to intensively investigate the primary themes and provide information on other relevant areas.

To ensure coding reliability, three authors initially coded five papers to determine the appropriateness of the adopted categorization scheme and amend it accordingly (i.e., adding or deleting attributes). Then, the fourth author independently coded four additional papers, and all the authors discussed the coding discrepancies until no further reliability checking was needed (Dumay et al., Citation2016; Tsalavoutas et al., Citation2020). This procedure yielded six main research themes, Composition, Diligence, Disclosure, Discrimination, Presence of (strong) AC, and Compensation and ten sub-themes, Independence, Qualifications, Reputation, Overlapping membership, Gender, Racial, Presence of AC, Presence of strong AC, Total compensation and Equity compensation.

Figure shows the results of our search as allocated to each (sub) theme. Every circle presents the six main themes and 10 sub-themes, while the area of the circles symbolizes the frequency of the papers allocated. Thus, the area of the circle increases proportionally with the number of studies classified in a specific theme. Therefore, the Figure represents the impact of the AC on AFs, organized around the areas that it covers. In particular, of the total 78 studies 34 examined Composition (43.59 percent), six Diligence (7.69 percent), four Disclosure (5.13 percent), 14 Discrimination (17.95 percent), 12 Presence of (strong) AC (15.38 percent), and eight Compensation of AC members (10.26 percent). This shows that a considerable number of studies (approximately 46/78, or 59 percent) emphasize Composition and Presence of (strong) AC, while research sub-themes relating to Racial discrimination, AC members reputation, and Overlapping membership remain underexplored. The key findings for each subject are discussed below.

3.2.3.1. Composition

This topic involves studies that examined the relationship between AC composition and AFs. 34 articles that provide insights into the impact of AC independence, AC member qualification, AC member reputation, and overlapping membership on AFs were thus analyzed. The literature was discussed through a critical analysis, and key challenges and opportunities were identified.

A group of 11 articles within this category explored whether having more independent directors on ACs affects AFs. However, the empirical evidence on the relationship between the two variables was inconclusive and did not clarify whether the direction of the link was positive (Bliss et al., Citation2011; Larasati et al., Citation2019; Naser & Hassan, Citation2016; Nehme & Jizi, Citation2018; Saleh & Ragab, Citation2023; Vafeas & Waegelein, Citation2007), negative (Bliss et al., Citation2007; Boo & Sharma, Citation2008), or neutral (Goddard & Masters, Citation2000; O’Sullivan & Diacon, Citation2002). The discrepancies in the empirical literature may, inter alia, be due to: a) the regulatory and industrial contexts where the relevant study was conducted (Boo & Sharma, Citation2008); b) internal monitoring systems of the firms (Bliss et al., Citation2007); c) CG quality among firms; and d) the methodological approaches employed. Future studies could take these issues and especially the interrelationship between CG variables into account (see, Bliss et al., Citation2007). However, since the majority of CG norms promote AC independence and firms comply with this best practice, future scholarship may face statistical testing restrictions. A potential next stage in the evolution of this body of work could be the broadening of the focus of “independence” by examining other parameters, such as AC members’ tenure (Chan et al., Citation2013). Since true “independence” is unobservable, academic investigations could contribute to understanding the gap between perceived and actual independence (Alderman & Jollineau, Citation2020). Research into this aspect could have important social and institutional implications.

Another stream of research within this subcategory examines the relationship between AC members’ qualifications (i.e., expertise and experience) and AFs. Thus, the 16 articles were separated into two groups: one (14 articles) focusing on “financial/industry/member expertise,” and the other (2 articles) analyzing the results arising from the presence of Audit Firm Alumni (AFA) on ACs. The literature provides different definitions for “financial”, “industry” and “member” expert (Krishnan & Visvanathan, Citation2009). Some scholars use a restrictive definition (i.e., accounting financial expert), while others employ a broader definition (i.e., supervisory financial expert/non-accounting financial expert). For instance, in a U.S. study, Cohen et al. (Citation2014) observed that both financial and industry expertise were associated with higher AFs. Similarly, in a U.S.-based study, Kim et al. (Citation2017) discovered that, on average, firms with accounting experts on ACs pay higher AFs; however, this relationship is weakened when a powerful CEO runs the firm. Further, Ghafran and O’Sullivan N (Citation2017), in a U.K. study, discovered that non-accounting expertise was associated with higher AFs. Additionally, they discovered that accounting and industry expertise did not influence AFs. Further, the study of Alhababsah and Yekini (Citation2021) illustrated that industry expertise was associated with higher AFs. The only studies that suggested a negative relationship between accounting financial expertise and AFs are Krishnan and Visvanathan (Citation2009) in the U.S. context and Nehme et al. (Citation2020) in the U.K. context. Overall, the articles included in this subcategory highlighted that financial expertise had an impact on AFs. However, since “expertise” is at the center of the current reforms suggested by policymakers, further research is needed to meet this challenge and provide evidence on whether broader or narrower financial expertise had a better monitoring role. Furthermore, scholars should also examine other unregulated types of AC members’ expertise/experience, such as technology, cybersecurity, ESG issues, and enterprise risk to facilitate advancement in the field (Deloitte, Citation2022). Moreover, there is much room for research on AC members’ characteristics (e.g., age, tenure, multiple directorships), since firms spend significant amounts of money on such employment (see, Sultana et al., Citation2019; Tremblay & Gendron, Citation2011).

The other group, which includes the two articles, explores an emerging issue, i.e., whether AFA on ACs affects AFs. AFA refers to those “directors that have a CPA and an employment history at the incumbent audit firm” (Ittonen et al., Citation2019, p. 802). Consequently, regulators around the world have started to enact restrictions on the appointment of AFA on ACs as a means of protecting audit quality and the level of AFs (Baumann & Ratzinger‐Sakel, Citation2020). Research into this area has only recently begun (2019–2020), and there is scant empirical evidence. For instance, the U.S. -based study by Ittonen et al. (Citation2019), which examined whether the presence of AFA on AC’s affect AFs, discovered that AFs are lower when the AC chair is AFA; this suggests that a reduced effort is required to audit clients with audit firm alumni. Conversely, Baumann and Ratzinger‐Sakel (Citation2020) in a Germany-based study, demonstrated that the presence of AFA on ACs did not affect AFs. However, they also observed that the appointment of AFA, who have currently left the incumbent audit firm, led to a higher audit quality. This evidence contradicts the expectations of regulators, and raises important concerns, which necessitates more research on this issue. The key insight is that restricting the presence of AFA—to all positions—without sufficient evidence may lead to uncertain consequences for society. Thus, future studies have the opportunity to contribute to a deeper understanding of the role of AFA in practice.

Similarly, other studies (three articles) have explored whether the presence of AC members on compensation committees (known as overlap phenomenon) affects AFs. For instance, Karim et al. (Citation2016) observed a negative relationship between overlapping membership and AFs illustrating that this phenomenon is a signal of poor CG and that it leads to a lower level of monitoring effort. Along the same lines, Kalelkar (Citation2017), in a U.S. study, observed a negative association between overlap and AFs; however, he demonstrated that this reduction in AFs was due to a lowering of audit risk. By contrast, Abdulmalik and Che-Ahmad (Citation2021), in a Nigerian study, observed a positive relationship between overlapping membership and AFs in the post regulatory period. Collectively, the findings indicate that more investigation is needed to improve our understanding of this unexplored issue in countries other than the U.S. and Australia that have different governance conditions for ACs. Future studies could shed light on the consequences of common membership, and provide insights as to whether this attribute diminishes or enhances shareholder value (see Liao & Hsu, Citation2013).

The last subcategory covers a minor topic that does not fall within any of the previous subcategories. It includes three articles that provide insights into the relationship between AFs and the presence of AC directors with “reputation” (i.e., known as “problem”/“taintedFootnote8” directors, “reputableFootnote9”, directors) on the AC and one article that explores multiple AC directorships and AFs. Since AC members are involved in various material aspects related to the auditing process, their “reputation” is highly relevant to AFs. For instance, in a US-based study, examining whether the presence of “problem” directors on AC’s affected AFs, Habib et al. (Citation2019) discovered that this relationship was positive; this suggests that auditors devote more auditing effort towards fulfilling their duties, and charge more than normal. Furthermore, Bhuiyan et al. (Citation2020), in a U.S. study, found that AFs were higher by 11.29% when the AC consisted of a female tainted director, indicating that board diversity benefits are adversely affected by a tainted professional reputation. Finally, Fredriksson et al. (Citation2020) demonstrated in the Finnish context that firms that have “reputable” directors pay higher AFs to protect their capital. Overall, this body of research shows that the “reputation” of directors is related to AFs. Each of these studies represents untapped areas for exploration. A potential next stage in the evolution of this body of work could be the examination of different categories of “problem” directors. This suggests that different proxies/definitions may provide different econometric results, and may therefore, highlight important implications. That is, the directors’ prior background involves many aspects that should be carefully considered. From a methodological perspective, a new avenue for research could be the examination of causality. In these circumstances, innovative methodological approaches and techniques should be used to address endogeneity issues arising from such dynamic causal relationships between directors’ “reputation” and AFs (see, Nerantzidis et al., Citation2022). The last article of this subcategory is the worldwide study of Liu et al. (Citation2022) who found that AC directors with multiple directorships were related to higher AFs. This suggests that AC directors serving on multiple boards have consequences on AC monitoring effectiveness.

3.2.3.2. Diligence

This set of six articles reviewed the contribution of AC diligence in audit pricing (e.g., Abbott et al., Citation2003b; Drogalas et al., Citation2021; Hoitash & Hoitash, Citation2009). From a theoretical perspective, “diligence refers to the willingness of committee members to work together as needed to prepare, ask questions, and pursue answers when dealing with management, external auditors, internal auditors, and other relevant constituents” (DeZoort et al., Citation2002, p. 45). It is worth mentioning that there are multiple components to diligence; however, in practice, it refers to the number of AC meetings (i.e., AC activity), as it is the only available quantitative proxy (Raghunandan & Rama, Citation2007, p. 265; Thiruvadi, Citation2012, p. 370). Under this notion, various issuers of codes of good governance and regulators emphasize the significance of having active and diligent ACs (Aguilera & Cuervo-Cazurra, Citation2004) as a means of preventing opportunistic management behavior and/or enhancing organizational legitimacy (Grenier et al., Citation2012).

Empirical research in this area in the last 20 years was due to the increased attention paid to the efficacy of ACs. For instance, in an Australia-based study, Goodwin‐Stewart and Kent (Citation2006) found that AC meetings have the most positive impact on AFs, suggesting that diligence can influence the demand side for higher quality auditing. Similarly, Stewart and Munro (Citation2007), in the Australian context, examined the impact of AC meetings on AFs. They confirmed the increase in AFs using a hypothetical scenario and varying the number of AC meetings. Furthermore, Adelopo et al. (Citation2012) demonstrated in the U.K. context that firms which have a higher AC activity pay higher AFs to allay the increasing risk of litigation and the potential reputational effects of firm misconduct. These researches indicate that the AFs increase as the frequency of committee meetings increases. However, it is important to highlight that AC frequency is not the best proxy for measuring AC diligence (Raghunandan & Rama, Citation2007, p. 277). Thus, the next stage in developing this body of work would be to consider different variables of diligence, such as the length of AC meetings, voluntary AC disclosures, the interaction among the AC members, the interaction between AC and other participants (such as management and internal and/or external auditors), and the quality of AC meetings (DeZoort et al., Citation2002; Raghunandan & Rama, Citation2007; Thiruvadi, Citation2012). These data can be provided by different sources, such as interviews, questionnaires, and secondary data including access to audit firms’ databases or textual analysis of the content of mandatory/voluntary corporate disclosures (e.g., AC reports or social media posts).

3.2.3.3. Discrimination

Studies in this category focus on how members of demographic minority groups in ACs, including female directors (e.g., Lai et al., Citation2017; Sellami & Cherif, Citation2020) and racial minorities (e.g., Harjoto et al., Citation2015; Johl et al., Citation2012), affect AFs. This aspect was explored through 14 articles, and has garnered increased attention recently, as women and racial minorities have progressively come to occupy boardrooms and sub-committees as a way of improving decision-making and/or ethical and social justice (Kumar & Zattoni, Citation2016; T. H. H. Nguyen et al., Citation2020).

A group of articles (nine articles) within this category explore the effect of gender diversity in ACs on AFs. For instance, a U.S.-based study by Lai et al. (Citation2017), discovered that firms with gender diverse ACs pay 8 percent higher AFs and choose better qualified auditors. Similarly, in an Australia-based study, Aldamen et al. (Citation2018) examined the impact of female representation on AFs, and discovered that this relationship was positive, thereby illustrating that gender diversity in ACs affects the quality of the external audit. Similarly, Sellami and Cherif (Citation2020) demonstrated the same relationship in the Swedish context and Miglani and Ahmed (Citation2019) indicated that Indian companies with female financial experts on ACs have significantly higher AFs. Additionally, Mnif and Cherif (Citation2023) and Fernández-Méndez and Pathan (Citation2023) examined the same issue and found a positive relationship in Swedish and Australian contexts respectively. The studies that suggested a negative relationship between gender diversity and the demand for audit effort (as measured by AFs) were that of Nekhili et al. (Citation2020) for the French context, Alkebsee et al. (Citation2021) in the Chinese context and Hao et al. (Citation2021) in the U.S. context after the post-adoption period of rule 3211.

Contrary to the aforementioned body of research, the results regarding racial minorities and audit pricing (4 articles) were mixed (Firoozi & Magnan, Citation2022; Harjoto et al., Citation2015; Johl et al., Citation2012; Yatim et al., Citation2006). Finally, one article, that of Leung and Sane (Citation2022), explored the effects of both diversity and racial discrimination, in the Asian context, and found a negative relationship of the former with AFs and a positive one of the latter. We conclude that more studies are needed to provide better insight into this issue. Future scholarship could explore whether the discrepancies in the literature can be explained by the differences in the corporate governance systems (e.g., Denis & McConnell, Citation2003) or in the financial reporting environments (e.g., Berger, Citation2011; Beyer et al., Citation2010). Future studies can clarify whether recent political strategies for promoting gender equality and mitigating racial discrimination (e.g., European Gender Equality Strategy 2020–2025 -COM, Citation2020) can play significant roles in AFs and contribute to the quality of financial statements. Furthermore, they could clarify why a large variety of issuers of codes of good governance (e.g., stock markets, investor associations) diffuse these best practices (Aguilera & Cuervo-Cazurra, Citation2004; Aguilera & Cuervo‐Cazurra, Citation2009). Clarifying whether this is done for reasons of efficiency or legitimacy can offer valuable implications for policy makers when implementing future regulatory reforms. Finally, future research could also consider the effect of other types of AC diversity on AFs, such as cultural diversity, religious diversity, and age diversity (see, Alhababsah & Yekini, Citation2021). Broadening the focus of scholars can provide important insights for addressing these challenging societal problems.

3.2.3.4. Disclosure

Studies in this category focus on how AC disclosures affect AFs. This topic was explored through four articles and has recently received scholars’ attention. For instance, in a U.K.-based study, Xue and O’Sullivan (Citation2023) found that higher levels of AC disclosures are related to higher AFs. Similarly, Al Lawati and Hussainey (Citation2022), in the Omani context, examined the impact of Key Audit Matters disclosure on AFs. They confirmed the increase in AFs as a factor that improves audit quality. Furthermore, Bratten et al. (Citation2022) and O’Shaughnessy et al. (Citation2022) demonstrated in the U.S. context that firms with ACs active in overseeing the external audit (as proxied by AC voluntary disclosures) have higher AFs. These results indicate the usefulness of AC reports to stakeholders as well as their effect on financial reporting and AFs. Thus, the next stage in developing this body of work would be to consider different contexts, providing new evidence that could assist regulators to strengthen the oversight role of AC as a means of increasing audit quality.

3.2.3.5. Presence of (strong) AC

This corpus of literature (12 articles) includes research exploring the effect of the presence of (strong) AC on AFs (e.g., Afenya et al., Citation2022; Ali et al., Citation2018; Ariningrum & Diyanty, Citation2017; Duellman et al., Citation2015; Lee, Citation2008; Mitra et al., Citation2019; Redmayne et al., Citation2011; Zaman et al., Citation2011). Scholars have been using the presence of AC as a dummy variable to test its relationship with AFs in the early stages of development of this research (Collier & Gregory, Citation1996; Goddard & Masters, Citation2000; Redmayne et al., Citation2011). However, the next stage of evolution includes eight studies that try to construct AC indices/proxies/metrics as a means of measuring AC strength. In practice, scholars selected a set of key AC variables, known as best practices (see Rainsbury et al., Citation2009), and classified each in terms of its contribution towards creating a strong AC. The variables were then summarized to form an index, which was used as an independent variable to test whether a strong AC affects AFs. Thus, scholars focused on the joint effect of these variables as a proxy of a strong AC.

For instance, in a U.K.-based study, Zaman et al. (Citation2011) used an aggregate construct of the following four characteristics as a proxy of a strong AC: (1) the presence of independent and non-executive directors in the AC; (2) the presence of at least one director with relevant financial expertise; (3) AC meetings at least three times a year; and (4) the attendance of a minimum of three AC members for the effective functioning of the AC. These characteristics demonstrated that a stronger AC is associated with higher AFs for larger clients. Similarly, an Australia-based study by Ali et al. (Citation2018), examining the same hypothesis using an index of five attributes (i.e., AC independence, diligence, size, financial expertise, and chairperson’s accounting expertise), found a positive and significant relationship between a strong AC and AFs. Additionally, Duellman et al. (Citation2015) constructed an index including three characteristics of AC members: (1) independence; (2) level of financial expertise; and (3) stock ownership and discovered that U.S. companies with a strong AC mitigate the negative relationship between AFs and managerial overconfidence. However, the results of the study by Beck and Mauldin (Citation2014), which used three alternative proxies of AC power, tenure; board structure and pay and stock ownership, produced different results from the prior studies. This study focused on the impact of AC and the chief financial officer on AFs during the recent financial crisis in the U.S. The findings demonstrated that more powerful ACs caused smaller reductions in AFs during the recession.

Overall, this line of research indicates that the presence of a strong AC positively affects audit pricing. However, this relationship may be affected by various external factors as illustrated by Beck and Mauldin (Citation2014). There are also endogeneity issues raised by the subjectivity of the index construction—either from omitted variables or reverse causality—that should be addressed (Bruna et al., Citation2021; Duellman et al., Citation2015; Wintoki et al., Citation2012; Zaman et al., Citation2011). The different procedures for the index construction (both on variables as well on the way of weighting them) may produce significantly different conclusions (Nerantzidis, Citation2018). This challenging problem provides a good starting-point for future studies to rethink index construction using strong and innovative methods (for more, see Simnett et al., Citation2016). Additionally, future scholarship could explore the importance of AC power in different regimes using alternative variables not widely examined in the literature (i.e., AC tenure). Additionally, this line of research could be extended to public sector entities. The data shortcomings can be addressed by focusing on appropriate regimes that may provide such data, such as New Zealand (see, Redmayne et al., Citation2011).

3.2.3.6. Compensation of audit committee members

Empowering ACs with the responsibility to determine external auditors’ compensation is a major issue (e.g., Habib & Bhuiyan, Citation2018; Park, Citation2019; Salloum et al., Citation2015). This line of research (eight articles) has been intensively investigated between 2010–2020, mainly in the U.S. The papers in this theme critically discuss the relationship between AC (equity) compensation and AFs.

For instance, a U.S.-based study by Engel et al. (Citation2010) found that total compensation and cash retainers paid to ACs are positively related to AFs. Similarly, Kalelkar et al. (Citation2018) using a sample of 1,287 U.S. listed firms for the period 2004–2012, found that AC excess compensation is positively associated with AFs. This illustrates that AC compensation is considered a monitoring mechanism over the financial reporting process. Furthermore, Lin (Citation2018) using 1,087 U.S. listed firms for the period 2006–2014, found that AC’s incentive-based compensation was positively related to abnormal AFs in cases where firms switched from Big 4 to non-Big 4 auditors, or switched between non-Big 4 auditors. In a Korea-based study, Park (Citation2019) found a positive relationship between AC compensation and AFs. He additionally observed that this relationship was strengthened in cases where the AC complies with all best practices that are mentioned in the AC section of the Korean Commercial Code.

Another stream of this literature (three articles) explores the impact of AC equity compensation on AFs. For example, Liu et al. (Citation2021) observed a negative relationship in the U.S. context. They reported that a one unit increase in AC equity compensation ratio led to a decrease of $297,710 in AFs. Their findings raised important concerns regarding whether equity compensation harms AC independence. Similarly, the study of Schrader and Sun (Citation2019) demonstrated that the type of equity compensation (i.e., option grants and stock awards) affected the interests of ACs members differently. They presented evidence which demonstrated that equity compensation within the stock awards of AC members was positively related to AFs. Nevertheless, the relationship changed in the case of equity compensation with the option grants of AC members. Further, Habib and Bhuiyan (Citation2018), in an Australia-based study, found that AFs are lower for firms with overlapping AC members, who are also owners of company stocks.

Collectively, this line of research indicates that AC compensations are positively associated with AFs, while this relationship is negative in case of equity compensation of AC members with option grants. This illustrates that the type of compensation to AC members may affect their judgment, and consequently the quality of financial statements (Schrader & Sun, Citation2019). It is well possible that AC members with a higher compensation have a higher degree of expertise. The next stage in developing this corpus of literature would be to provide new evidence in research settings which differ from the U.S. Investigating contexts with different characteristics, such as a different legal system, financial reporting environment, or corporate governance system, is expected to provide new and different findings that deepen our understanding regarding the effect of compensation on financial reporting quality (Filip et al., Citation2015; Habib & Jiang, Citation2015). In addition, focus on exogenous shocks, such as COVID-19 May 2001provide deeper understanding regarding this issue. For example, firms need to be flexible and adjust their compensation policy (i.e., to AC members and auditors) to survive during periods of financial distress. Additional research could offer important insights for scholars, practitioners (i.e., auditors, directors), policy makers, and firms.

3.3. Future research direction for the impact of ACs on AFs

Our SLR provides a synthesized state of knowledge regarding the impact of ACs on AFs. In this section, we illustrate the gaps in the literature and propose avenues for future research. First, the review identified that most of the studies were undertaken in a single country, mostly in developed countries (based on the MSCI index) and most frequently in Europe and the United States (64% of the review studies). Specifically, 41 out of the 78 studies were based in the U.S. and the U.K. (29 studies and 12 studies, respectively). However, the system of CGFootnote10 that prevails in these Anglo-Saxon countries is a shareholder or market-based system. Thus, it is reasonable to expect new findings in countries where different systems of CG prevail, as some countries emphasize shareholder value while others focus on stakeholder value (Bushman et al., Citation2004). At a practical level, this implies that there is a lack of generalizability across countries with different specificities (e.g., corporate governance systems, cultural backgrounds, institutional framework). Considering the shortage of studies where “network-oriented” systems prevail (see Weimer & Pape, Citation1999, p. 152), especially in countries that are classified in the emerging, frontier and standalone categories (see, Table ), we believe that further research in different contexts, particularly in countries with weak CG systems, could provide key insights to help scholars gain a clear picture of the impact of ACs on AFs. A multi-country study that examines whether the effect of AC on AFs differs between the different CG systems could also be beneficial. This conceptual research has important implications for policy makers and for future regulatory reforms considering the high interest of academicians, businesspeople, and governance activists in empowering ACs with the responsibility to determine external auditors’ compensation.

Second, despite the importance of providing empirical evidence on the effect of ACs on AFs at a methodological level, this research has serious endogeneity concerns. The literature on international archival auditing illustrates that endogeneity is produced by omitted variables, simultaneous-equation bias, and variable measurement bias (Simnett et al., Citation2016). The extent of this problem indicates the need for scholars to be aware of this issue and produce more quality research. Alternative approaches have been proposed to address this matter. For instance, in the context of ACs, a (quasi) natural experiment could result from a social or political situation. This type of experiment is preferable in cases where the researcher examines legislated corporate governance changes (for more, see Gippel et al., Citation2015). In addition, more sophisticated econometric techniques are proposed to alleviate these concerns. However, prior empirical studies either do not address this problem, or simply mention it without providing further details. Thus, inspired by the general literature we highlight some approaches to tackle this issue, such as: two-stage least squares (Ali et al., Citation2018; Chan et al., Citation2013; Fargher et al., Citation2014; Habib et al., Citation2018), three-stage least squares (Kurauone et al., Citation2021; Q. K. Nguyen, Citation2022), differences-in-differences methodologyFootnote11 (Nekhili et al., Citation2020; Sultana et al., Citation2019), instrumental variables (Chan et al., Citation2013), difference generalized method of moments (GMM) (Rodríguez & Sánchez Alegría, Citation2012), and system GMM (Gull et al., Citation2021; Nekhili et al., Citation2020). Regarding variable measurement bias, it is recommended that scholars construct alternative measures to increase the validity of the results. In other words, future research could alleviate the subjectivity of the index construction (i.e., in cases of measuring the AC strength) by designing robust proxies using the appropriate theory of measurement (Nerantzidis, Citation2018; Simnett et al., Citation2016).

Third, most of the studies used quantitative methods (76 out of 78), highlighting the lack of qualitative methods, such as interviews and questionnaires. New research approaches could provide new perceptions that are difficult to address with empirical/archival studies. For instance, how and to what extent are AC members involved in the determination of AFs? What are the opinions of key actors, such as the head of internal audit, on the discourse about determining AFs? Under this notion, qualitative studies could help policy makers to gain a clear idea of the practitioners’ work reality and improve legislative acts accordingly (Power & Gendron, Citation2015). That is, qualitative methods provide the opportunity to explore different perspectives that generate an incremental increase in the examined issue. It would also be interesting to combine quantitative and qualitative research (mixed methods) to answer more complicated research questions (see, Doyle et al., Citation2009). For instance, AC frequency is criticized in the literature as not the best proxy for capturing AC diligence. Thus, scholars could use the data triangulation technique (i.e., the use of multiple methods of data collection using both qualitative and quantitative approaches) to measure a construct, assess diligence, and provide more innovative and robust results (Hopper & Hoque, Citation2006). From this perspective, they can use qualitative techniques (for example, interviews and open-ended questions) to obtain data, such as the quality of AC meetings, and transform it into quantitative data (for more, see Palinkas et al., Citation2011). Similarly, voluntary AC disclosure could be transformed into quantitative data as an alternative proxy of diligence. Such techniques could be applied in all other proxies where a gap is identified in the literature between perceived and actual AC variables (e.g., AC members’ qualifications/independence/reputation).

Fourth, although the review identifies six research themes and 10 sub-themes, which are presented in Figure , there are issues relating to ACs and AFs that remain un(der)explored. For instance, there is a shortage of studies examining how members of demographic minority groups in ACs, including female directors and racial minorities, can affect AFs. The results regarding racial minorities and audit pricing were inconclusive. Thus, future scholarship should explore whether the discrepancies can be explained by the differences in the CG systems or by the financial reporting environments. Moreover, no study examining the effects of other types of AC diversity on AFs, such as cultural diversity, religious diversity, and age diversity, was found. Additionally, there are opportunities for future researchers to explore the effect of AC members’ reputation/equity compensation/overlapping membership on AFs. Studies that examine how AC disclosures affect AFs are also limited. Thus, future scholarship could explore not only the different levels of AC disclosures and how these affect AFs but also their quality and their usefulness for stakeholders.

Fifth, future studies may consider companies facing financial difficulties or other accounting-related problems, such as financial restatements. For instance, the outbreak of the COVID-19 pandemic caused an economic shock that led to a demand reduction in the global economy and a liquidity crisis in firms (De Vito & Gómez, Citation2020). Thus, it would be interesting to explore the consequences of the COVID-19 crisis on AC characteristics and AFs. The numerous accounting guidelines for COVID-19 were a reflection of the fact that ACs faced accounting and reporting challenges, which enhanced their oversight role in these uncertain times (International Federation of Accountants- IFAC, Citation2020; Loop et al., Citation2020). That means that, in times of financial turbulence, ACs need to be engaged, informed, and effective. Auditing scholars are well suited to address questions, such as: Is the AC more active in the determination of AFs during turbulent economic times? Does working remotely affect the quality of AC meetings and AFs? Do firms facing liquidity risk have different policies on AFs? Is there any significant difference between ACs characteristics and AFs in the pre- versus the post-Covid-19 period? These and other related questions provide a foundation for future research.

Sixth, the review identifies that prior research has emphasized listed firms in general. However, we believe that research that sheds light into listed small and medium enterprises (SMEs) could provide new paths that are important for the auditing process and/or pricing. SMEs represent 99 percent of all global business population and thus constitute a key driver of economic development, innovation, employment, and social integration (Azudin & Mansor, Citation2018; Ribau et al., Citation2018). On that basis, this type of research has many theoretical and practical implications beyond AFs. It would be interesting to explore the level of AC practices among the various firm categories (micro, small, and medium), and its impact on AFs. For instance, this could be applied to European listed SMEs considering the different country groups as illustrated in Kenourgios et al. (Citation2020). In addition, further research is needed regarding public sector firms. To date, the only study that examines the relationship between AC and AFs in the public sector is that of Redmayne et al. (Citation2011). The role of the AC is more significant in these companies as most of these companies do not have tradable equity. However, potential authors must be cognizant of the paucity of data, and focus on appropriate regimes/office that can provide such datasets to address this shortcoming (e.g., the Office of the Auditor-New Zealand).

Finally, scholars could explore new governance mechanisms that could contribute towards the effectiveness of ACs and its impact on AFs. For instance, it would be interesting to explore other unregulated types of AC member experiences, such as technology, cybersecurity, ESG issues, and enterprise risk that have not been previously. Future studies could also investigate the effectiveness of the training of new AC members during the COVID-19 era (namely through AC member onboarding). Since there has been a rapid switch to online learning, understanding the fundamental changes in CG training can be challenging (Oranburg & Kahn, Citation2021; Rinaldi, Citation2022). This can be a very fruitful area for future research as clarification regarding the impact of AC effectiveness on AFs is necessary.

4. Conclusion

The rigorous review presented here is motivated by the need to better understand the impact of ACs on AFs. To shed light on this issue, an SLR was conducted following the methodologies of previous literature. Our paper addresses three interrelated research questions.

The first research question was “How is research on the impact of ACs on AFs being developed?” We addressed this by evaluating three distinct characteristics of review studies: 1) the number of studies per journal discipline, 2) the geographic area, and 3) the MSCI country classification. Our findings illustrate that the examined issue is approached primarily by accounting journals that emphasize the researchers’ interest in shedding light on unique national contexts. More specifically, we observe that there is a gradual increase in the number of studies during the examined period, especially in the more recent years. The majority of studies are empirical, country-specific, and focused on developed markets in Europe and America.

The second research question was “What is the literature’s focus and critique on the impact of ACs on AFs?” Following prior studies, we used three criteria to answer this RQ: 1) the number of studies by type of research method and by data collection, 2) theories and 3) research theme. Our study shows that the majority of the examined papers used quantitative research methods by employing demand and supply theory from the demand or/and the supply side. Some themes, such as Diligence and Discrimination, remain underexplored. These results suggest that researchers face challenges in developing insightful ideas regarding the potential of this specific research field.

The third research question was “What is the future for research on the impact of ACs on AFs?” We answered this question using the directions suggested by the analysis of RQ1 and RQ2. We highlighted several areas in which further research could lead to valuable insights. We identified seven topics, some of which are broad and refer to the constraints of the examined topics and others which stem from the more general literature. For instance, more research on listed SMEs or new governance mechanisms could provide new paths that are important for audit pricing. In addition, we believe that future studies could expand research boundaries by also using data from countries in the emerging, frontier and standalone categories. Additionally, the inclusion of more qualitative methods, such as interviews and questionnaires, may also be valuable.

Our review study has important implications for a range of interested parties. First, the study demonstrates that there are various areas for scholars to expand their research. As has been illustrated, most of the studies are empirical, focusing on a single country and mainly conducted in developed countries using demand and supply theory. Thus, academic researchers could contribute to the expansion of this literature by using theoretical frameworks and methods permitting them to answer more complicated research questions on under-represented issues and contexts. Further research could be undertaken to investigate new governance mechanisms (see Section 3.3) that have not previously been investigated. These new governance mechanisms could contribute towards the effectiveness of ACs and enrich this corpus of literature. Second, policymakers should carefully consider the different characteristics among countries (e.g., corporate governance system, financial reporting environment, and culture background) before designing the introduction of new AC practices, as most prior empirical studies are concentrated on shareholder/market-based systems. While a large variety of issuers of codes of good governance (e.g., stock markets, investor associations) diffuse new AC best practices, the underlying reasons could either be efficiency or legitimacy. Therefore, policy makers should seek out academic evidence that supports the legislation of a new practice that specifically empowers AC’s responsibility to determine AFs. Thus, our analysis draws attention to topics conducive to establishing a better regulatory reform agenda. Third, our review offers interesting implications for practitioners. In particular, the findings could enable board members to better understand the complex environment of audit pricing and build a more effective AC. A more effective AC could better assess and determine the level of AFs. Further, auditors could benefit from this review by evaluating the potential mechanisms that increase the effectiveness of AC to adjust their risk assessment, and improve the precision and predictive ability of the AF model. Finally, the review could help the users of financial statements to increase their awareness of significant issues regarding the impact of ACs on AFs and make better informed decisions.

Finally, as with all literature reviews, the present study is also subject to some limitations. Despite the fact that a SLR differs from narrative reviews (which may be incomplete, see Neely et al., Citation2010), since it eliminates the status quo bias and subjectivity (Caputo, Citation2013), it is affected by the scope of the literature and the interpretation of the findings (Kotb et al., Citation2020). Both our data sample and our methodology were restricted. Specifically, our sample was restricted to established and quality papers indexed in the 2021 AJG and/or in 2023 ABDC and only covered studies that were published between 1996 and 2023. Our analysis was also limited to a Boolean search using certain keywords and phrases within three internationally well-known databases and papers written in English.

Contributions

Conceptualization: Michail Nerantzidis; Methodology: Michail Nerantzidis; Writing—Original Draft preparation: Michail Nerantzidis; Investigation: George Drogalas, Dimitrios Mitskinis, Michail Nerantzidis and Christina Vadasi; Writing—Review & Editing: Michail Nerantzidis, Andreas Koutoupis, George Drogalas, Christina Vadasi.

Supplemental Material

Download MS Word (58.4 KB)Acknowledgments

We are grateful to the senior editor Collins Ntim and two anonymous reviewers for the valuable comments during the review process. We also thank Stergios Leventis, Michail Bekiaris and Diogenis Baboukardos for their constructive and helpful comments on earlier versions of this work.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Supplemental data

Supplemental data for this article can be accessed online at https://doi.org/10.1080/23311975.2023.2238976.

Additional information

Notes on contributors

Michail Nerantzidis

Michail Nerantzidis is an assistant professor of accounting at University of Thessaly and has research interests in audit fees, audit quality, financial reporting and corporate governance.

Andreas Koutoupis

Andreas Koutoupis is an associate professor of financial accounting at University of Thessaly and has research interests in accounting, auditing, corporate governance, enterprise risk management and internal auditing.

George Drogalas

George Drogalas is an associate professor of accounting at University of Macedonia and has research interests in internal audit, audit quality and corporate governance.

Christina Vadasi

Christina Vadasi is visiting lecturer at University of Aegean and has research interests in financial accounting, corporate governance and internal audit.

Dimitrios Mitskinis

Dimitrios Mitskinis is a PhD candidate at University of Macedonia and has research interests in audit fees, audit quality and internal audit.

Notes

1. Our sample only shares few studies with the meta-analyses of Widmann et al. (Citation2020), D. Hay (Citation2013) and D. C. Hay et al. (Citation2006): one with Widmann et al. (Citation2020), one with D. Hay (Citation2013), and five with D. C. Hay et al. (Citation2006).

2. https://charteredabs.org/academic-journal-guide-2021-available-now/, published by the Chartered Association of Business Schools in the UK.

3. https://abdc.edu.au/abdc-journal-quality-list/, published by the Australian Business Deans Council.

4. Tsalavoutas et al. (Citation2020) mentioned that researchers should avoid restricting their analyses to one journal ranking or a certain level of journal ranking (e.g., studies from 3 AJG and above) as the findings would be biased and the review would focus on specific countries. This means that SLRs should engage in the creation of knowledge by avoiding the under-representation of some countries (Boell & Cecez-Kecmanovic, Citation2014).

5. It is worth mentioning that three studies out of 76 used both questionnaires (quantitative data obtained from closed-ended questions) and financial data for quantitative statistical analysis.

6. We classified the research of Tremblay and Gendron (Citation2011), who used semi-structured interviews, as a qualitative study.

7. The ANT concept is used to investigate the motivation and action of groups of heterogenous actors (both human and non-human) who interact with others to form a network of aligned interests (Walsham, Citation1997). Since 1990 this concept has inspired accounting scholars who consider the sociologically based accounting inquiry as a way of undertaking critical accounting research (Baxter & Chua, Citation2020; Justesen et al., Citation2011).

8. A problem or tainted director is the one “who has been personally involved as a director or executive, in one or more corporate bankruptcies, major litigations or corporate infractions, major accounting restatements and other accounting scandals or have served on compensation committees that have approved particularly egregious CEO compensation packages, or other similar circumstances” (Board Analyst, Citation2007 as cited in Habib et al., Citation2019, p. 125).

9. Different proxies have been used to capture reputational capital such as: i) Total number of directorships, ii) Average number of directorships and iii) Board compensation (Fredriksson et al., Citation2020, p. 4).

10. A CG system is defined as “a more-or-less country specific framework of legal, institutional and cultural factors shaping the patterns of influence that stakeholders (e.g., managers, employees, shareholders, creditors, customers, suppliers and the government) exert on managerial decision-making)” (Weimer & Pape, Citation1999, p. 152).

11. To test regulatory changes.

References

- Abbott, L. J., Parker, S., Peters, G. F., & Raghunandan, K. (2003a). The association between audit committee characteristics and audit fees. Auditing: A Journal of Practice & Theory, 22(2), 17–30. https://doi.org/10.2308/aud.2003.22.2.17

- Abbott, L. J., Parker, S., Peters, G. F., & Raghunandan, K. (2003b). An empirical investigation of audit fees, non-audit fees, and audit committees. Contemporary Accounting Research, 20(2), 215–234. https://doi.org/10.1506/8YP9-P27G-5NW5-DJKK