?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We investigate the factors impacting dysfunctional audit behaviour (DAB) in audit companies in Indonesia during COVID-19. We additionally examine at how organisational commitment (OC), employee performance (EP), and turnover intention (TI) play a role as mediators in the relationship between locus of control (LOC) and DAB, how OC and TI play a role as mediators between EP and DAB, and how OC plays a role as a mediator between TI, auditor position (AP), and DAB. This study made use of the structural equation model (SEM) and the SmartPLS methodology. The processed data includes 118 external auditor replies received between May and October 2022. DAB was positively impacted by LOC, TI, time budget pressure (TBP), and AP, according to our findings. DAB is negatively affected by EP and OC. The relationship between LOC and DAB is mediated via OC and EP. EP and DAB interactions are mediated via OC and TI. The relationship between TI, AP, and DAB is mediated by OC. Indonesia’s first comprehensive causal model examined COVID-19 DAB hazards. DAB assessed COVID-19 auditors. This study addresses audit firm and external auditors. Auditing, reviews, auditor monitoring, and peer-reviewing audit organisations prevent DAB. DAB can lower audit quality and fail audits.

PUBLIC INTEREST STATEMENT

This study examines COVID-19-related dysfunctional audit behaviour (DAB) in Indonesian audit firms for evaluating external auditor performance. Our study analyses how OC, EP, and TI mediate in the relationship between LOC and DAB. Our research also analyses the involvement of OC and TI as mediators in the relationship between EP and DAB, and the role of OC as mediators in the relationship between TI, AP and DAB. Studies show LOC, TI, TBP, and AP boost DAB. EP and OC diminish DAB. Internal LOC and EP urge auditors to prevent DAB in COVID-19 audit companies. High EP advises auditors to shun TI to prevent DAB during COVID-19. Due to COVID-19 challenges, low TI and senior auditor roles reduce DAB. This research evaluates auditor performance during COVID-19 and urges audit companies and auditors to apply audit standards, audit processes, review, oversee, and peer-review to minimise DAB, which lowers audit quality.

1. Introduction

This study is the first to empirically aim to investigate the determinants of dysfunctional audit behaviour (DAB) in Indonesian audit firms during COVID-19. These determinants are such as employee performance (EP), locus of control (LOC), turnover intention (TI), organisational commitment (OC), auditor position (AP), and time budget pressure (TBP). Secondly, this study aims to investigate the role of mediators, including (1) the involvement of OC, EP, and TI as mediators in the relationship between LOC and DAB. (2) OC and TI are an intermediary in the relationship between EP and DAB. (3) The role of OC as a mediator in the interaction of TI, AP and DAB. DAB affects audit quality with biased opinions, potentially causing audit failure because external auditors are under pressure to conduct DAB. This study focuses on the deployment of general audits that provide views to customers, as well as the DAB behavior displayed by auditors during general audits. During COVID-19, DAB occurs in distant work contexts (Albitar et al., Citation2020; Amy et al., Citation2022; Dormishi et al., Citation2021; Herrbach, Citation2001; Nehme et al., Citation2019; Qushtom et al., Citation2022; Sweeney & Pierce, Citation2004); This raises concerns about how typical this behaviour is and whether auditors in accounting firms ethically practice it (Hegazy et al., Citation2017). Remote audit work makes it difficult for auditors to obtain audit documents because they must be adequately explained (Amy et al., Citation2022; Rose et al., Citation2020). As a result, external auditors override audit steps, sign off prematurely without completing audit procedures, and report on DAB performance in these circumstances (Gundry & Liyanarachchi, Citation2007, Hyatt & Taylor, Citation2010; McNair, Citation1991; Nguyen Van et al., Citation2023; Otley & Pierce, Citation1995; Shapeero et al., Citation2003). Improper sample reduction, biased sample selection, and initial audits without completion of audit assignments are examples of DABs performed under these conditions (Amy et al., Citation2022; Coram et al., Citation2003; Lord & DeZoort, Citation2001; Smith & Hutton, Citation1995). Others include insufficient client confirmations, extensive client record reviews, failure to track accounting principles, and reducing audit steps below reasonable levels (Gundry & Liyanarachchi, Citation2007, McNamara & Liyanarachchi, Citation2008; Paino et al., Citation2010; Otley & Pierce, Citation1996a, Citation1996b). In practice, the purpose of this study is to indirectly evaluate the performance of auditors in implementing general audits during COVID-19, which is evaluated from individual characteristic performance factors, including EP, LOC, TI, OC, AP, and TBP. Concerning these factors, did they conduct DAB during the general audit during COVID-19?

This study builds on previous research conducted by Donnelly et al. (Citation2003a), Paino et al. (Citation2011), Paino et al. (Citation2012); Yuen et al. (Citation2013); Ghorbanpour et al. (Citation2014); Balasingam et al. (Citation2019); Paino et al. (Citation2019); Amy et al. (Citation2022); Nguyen Van Hau et al. (Citation2023); and Annelin (Citation2023). Apart from that, this study expands on previous research on the factors that influence DAB in audit firms in Indonesia which have been conducted by Alkautsar (Citation2014); Kusumastuti and Nirmala Arum Janie (Citation2014); Anugerah et al. (Citation2016); Umar et al. (Citation2017); Amiruddin (Citation2019); Sunyoto and Sulistiyo (Citation2019); Tjan (Citation2019); Astuty et al. (Citation2022); and Audria and Lubis (Citation2022). Previous research concentrated on the relationship between external audit and DAB dimensions in accounting companies before to COVID-19 and rarely on the factors that influenced DAB during COVID-19, particularly in Indonesia. Because no previous research has explored this topic during COVID-19, researchers are interested in researching the elements that influence DAB in audit firms in Indonesia. Aside from that, Indonesia is a country that takes pandemics seriously, with the government frequently imposing social restrictions and lockdowns. As a result, it has an impact on all professional activities, one of which is how the external auditor feels. During COVID-19, the implementation of the DAB general audit was in the spotlight for research and evaluation of auditor performance because external auditors were under work pressure and pressure in dealing with COVID-19 conditions, which influenced them to carry out DAB (Amy et al., Citation2022). As a result, COVID-19 influenced external auditors to perform DAB (Amy et al., Citation2022). The impact of DAB performed by external auditors during COVID-19 on the implementation of the general audit decreased audit quality, resulting in lower-quality audit reports (Albitar et al., Citation2020; Dormishi et al., Citation2021; Qushtom et al., Citation2022).

Furthermore, this study differs from past research in that it uses OC, EP, and TI as moderators of DAB. This study is intriguing since multiple exogenous variables also serve as mediators in the formation of a causal association. Previous study on mediating effects in a complicated research model involving the DAB that establishes the causal relationship has never been explored. Previous studies (Donnelly et al., Citation2003b; Sunyoto & Sulistiyo, Citation2019) looked into how OC mediated the relationship between LOC and DAB. Donnelly et al. (Citation2003b) and Ghorbanpour et al. (Citation2014) investigated the mediating role of EP, TI, and OC on the relationship between LOC and Acceptance of Dysfunctional Behaviour in a separate study. Furthermore, Anugerah et al. (Citation2016) investigated the role of turnover intention in mediating the association between LOC, OC, and Reduced audit Quality Behaviour. Anugerah et al. (Citation2016) investigated the mediating influence of auditor performance and OC on the association between external LOC and Reduced Audit Quality Behaviour in a separate study. Paino et al. (Citation2011) investigated the LOC-DAB link as mediated by turnover intention. Paino et al. (Citation2012) separated organisation as an endogenous variable not connected to DAB but related to EP and TI as mediated in a different study. The researcher is interested in investigating OC, EP, and TI as mediators based on past research. Because they are under the conditions encountered by the external auditor during the general audit implementation in the face of COVID-19, the consideration of these three variables is necessary. The first aspect is an OC as a mediator that the auditor must have a commitment to love and progress the audit firm so that the COVID-19 requirements remain strong and the auditor does not do DAB in preserving client connections. The second factor to evaluate is TI as a mediator, which indicates that the auditor does not intend to quit from his or her position as an auditor because it is difficult to find a quality job and subsist. To survive, the auditor must remain loyal to the audit firm and not hunt for a new job or relocate to another firm owing to pandemic conditions. Auditors’ high loyalty causes them to refrain from performing DAB. The third factor to examine is staff performance as a mediator, and auditors must perform well at audit companies during the pandemic to protect the company’s reputation and deliver high-quality audit reports. As a result, the auditor is expected to perform tasks other than DAB. Prior to COVID-19, auditor experience in conducting DAB in earlier investigations (Anugerah et al., Citation2016; Donnelly et al., Citation2003a; Ghorbanpour et al., Citation2014; Paino et al., Citation2011, Citation2012; Sunyoto & Sulistiyo, Citation2019) was under normal settings. Meanwhile, this study evaluates auditor performance in pandemic settings so that researchers are inspired to pursue this research.

The following are the author’s motivations for exploring this topic: First, external auditors in Indonesia confront the COVID-19 circumstance, which forces them to operate remotely with various limits in obtaining audit evidence, and it is difficult to carry out audit procedures, so they may be encouraged to conduct out DAB. Second, according to Albitar et al. (Citation2020) and Amy et al. (Citation2022), COVID-19 influences external auditors’ ability to conduct DAB because auditors face job pressure while adhering to social distancing constraints. Third, DAB in practise is auditor behaviour that is commonly observed in the field, making it an intriguing topic for researchers to investigate; according to Shapeero et al. (Citation2003), auditors tend to determine and carry out patterns of DAB, with the majority of auditors engaging in DAB. This issue is felt by auditors when they audit, which is influenced by several circumstances; fourth, auditors in all career positions in accounting companies recognise that DAB is performed to a degree, but audit quality is maintained (Nehme, Citation2017). As a result, the author is interested in exploring DAB in the implementation of general audits. Fifth, the author is motivated to research this topic because it expands the evidence regarding DAB, specifically premature sign-off and under-reporting of time (Soobaroyen & Chengabroyan, Citation2006), which are influenced by external and internal attribution theory and theory of planned behaviour factors such as AP, EP, LOC, OC, TBP, and TI. Sixth, according to a study of literature research and empirical evidence, EP, OC, and TI might operate as moderating variables that connect the external audit component to DAB.

This study is based on the attribution theory developed by Heider (Citation1958) and the notion of planned behaviour developed by Ajzen and Fishbein (Citation1969). These theories serve as the foundation for linking individual characteristics to DAB. Furthermore, because they are behavioural in nature, the two theories used aim to evaluate the auditor’s performance in conducting general audits during COVID-19. First, attribution theory establishes the framework for this research, which demonstrates that auditors undertake DAB as a result of internal control elements such as motivation, personal qualities, ability, and self-perception. Auditors are encouraged to commit to the advancement of accounting firms that avoid DAB, because auditors who have yet to commit to their organisation have the potential to undertake DAB. Auditors with an internal LOC are less likely to engage in DAB, whereas auditors with an external LOC are more likely to engage in DAB. Auditors with high-level abilities, such as a position as an auditor in an accounting firm, have the option to perform DAB. Auditors believe their performance at the audit firm might be improved and aim to leave for another audit firm or other work; auditors who believe this have the possibility to do DAB. According to the attribution theory, extrinsic factors such as ambient conditions can impact the auditor’s decision to do DAB. The COVID-19 condition, which requires auditors to work remotely, allows them to undertake DAB. Second, the theory of planned behaviour expands on the context of this research by claiming that auditors perform DAB because they have already intended to do so. The auditor intends to transfer to another audit company and work elsewhere; the auditor does DAB on purpose because he has a short TBP.

Our research contributes several contributions to the literature on the dimensions of external audit, DAB, TI and OC in the context of COVID-19. First, we add to the auditing literature on external auditing dimensions by demonstrating how external auditors should handle remote work during COVID-19. We discovered a link between external LOC and OC. Furthermore, we discovered a link between LOC and EP. Then we discovered a negative association between EP and TI. Furthermore, we discovered a link between TI and OC. As a result, while dealing with COVID-19, external auditors must have strict internal safeguards in place to avoid being influenced by bad behaviour. External auditors pledge to advancement and to the audit firm. External auditors work hard to perform well, and their audit company keeps them as auditors. They must remain loyal as external auditors under COVID-19 conditions because obtaining big incomes and decent positions is extremely tough. Second, by examining how external auditors performed on audits during COVID-19, we contribute to the literature and external auditors at accounting firms on DAB. We discovered a link between TBP and DAB. External auditors perform DAB because they are under time constraints to undertake distant audits in pandemic conditions. Third, we contribute to the research on TI by examining how it affects the relationship between external audit parameters and DAB. We discovered that turnover intention acts as a mediator between LOC and DAB. So that our research adds to external auditors and audit firms, we found that external auditors’ self-control during COVID-19 is critical in managing themselves so they don’t flip over to audit firms and are mindful not to do DAB, which can affect audit quality. Fourth, we study how OC influences the external audit-DAB relationship. Our findings benefit external auditors and audit firms because OC mediates TI and DAB. To avoid leaving other audit firms or switching employment during COVID-19, external auditors must be loyal. High-loyalty auditors avoid DAB, lowering audit quality. This study may influence accounting company dynamics externally. This study should contribute to auditing and behavioural accounting literature and future research.

First, the novelty of this research evaluates the performance of external auditors in Indonesia during the COVID-19 period, evaluating performance from the individual characteristics factor, namely the relationship between EP, LOC, OC, TI, AP, and TBP with DAB, which previous studies have not done. Second, previous research has not examined the role of OC as a mediator in the link between EP and DAB. Third, TI’s role as a go-between in the relationship between EP and DAB. Fourth, consider OC’s role in the interaction between TI and DAB. Fifth, one of the research models examined in this work features a one-of-a-kind causal link. This study is conceptually advantageous and adds to the auditing and behavioural accounting literature by measuring auditor performance based on internal DAB distinctive characteristics. This study experimentally provides guidance to accounting firms and external auditors on how to systematically implement established audit standards and processes in order to avoid DAB. Furthermore, this study emphasises the significance of audit firm working reviews, auditor supervision, and peer reviews between accounting firms in order to avoid DAB. Furthermore, the execution of this research is directed at auditors as public accounting professionals in the audit office to implement the code of ethics and audit standards in order to avoid DAB, which can degrade audit quality and lead to the failure of a public accounting business.

2. Background

Auditors must follow audit guidelines established by the public accounting profession and audit firms in general audit work, such as following auditing standards, one of which is audit planning. Auditors must comply with auditing standards, which include general standards, fieldwork standards, and reporting requirements, as well as an auditor’s code of conduct (International Auditing and Assurance Standards Board, Citation2023). In reality, the auditor violates the code of ethics and auditing standards, which are influenced by the auditor’s personality type as well as situational and conditional environmental circumstances. Auditors’ deviant behaviour in implementing audits is classified as dysfunctional audit behaviour (DAB). This behaviour has a detrimental influence on audit quality in terms of reliability and accuracy. Various settings and conditions, such as COVID-19, that auditors confront when performing remote audits necessitate clarity in assessing attitudes in order for auditors to carry out DAB. The more pressed the auditor feels by working in certain scenarios and conditions, such as COVID-19, the more ready the auditor is to do DAB. Beginner auditors face pressure from superiors to make decisions that will allow them to conduct DAB, which is influenced by time constraints, financial constraints, and the auditor’s position. Auditors who use DAB to make audit decisions are more unethical than auditors who do not use DAB.

Another criterion that the auditor must follow in a general audit is to identify risks and analyse the initial and final materiality levels of the audited account balances. The auditor performs highly extensive audit procedures in order to provide audit opinions based on various documentary evidence collected and audit findings (International Auditing and Assurance Standards Board, Citation2023). One of the initial audit techniques is that the auditor understands the client’s business, determines business continuity, and suggests potential misstatements. The auditor evaluates it to assess the fairness of the financial statement presentation, which is required for choosing whether to form an opinion on attestation at the final stage of the audit process. Personal variables such as abilities and personality influence decision-making in determining the attestation’s opinion. The most essential aspect of the audit process that influences audit quality is decision making. As a result, the quality of the auditor’s assessment influences the auditor’s and stakeholders’ professional reputations. The assessment includes, among other things, (1) a risk assessment of material misstatement of financial statements; (2) a risk assessment of performance and audit procedures to address the risk of audit failure; and (3) an evaluation of audit evidence to determine audit quality (International Auditing and Assurance Standards Board, Citation2021a). Despite the fact that the auditor employed the same facts and evidence in conducting the audit, the findings of the auditor’s assessments varied. Many factors, including the auditors’ behaviour, are likely to influence the disparities in these judgements. The auditor manipulates the situation for the sake of convenience and to establish a secure environment for the audit. Individual auditors’ decisions to do or choose something in various scenarios are influenced by their opinions. The auditor’s personal view determines his or her decision to approve DAB. Each auditor is capable of carrying out audit programmes in accordance with audit procedures and acting functionally. However, auditors who are unable to perform audits within the audit programme will be motivated to perform DAB inspired by EP, LOC, OC, TI, AP, and TBP.

The audit firm’s policy for overcoming DAB is to strengthen the competence and experience of a good auditor during the audit. The auditor’s expertise in carrying out the audit demonstrates the auditor’s level of knowledge and expertise in carrying out the audit. The stronger the auditor’s audit experience, the more thoroughly the auditor understands numerous audit difficulties, and the auditor is more likely to terminate established audit procedures prematurely. Auditor experience is the intensity with which an auditor has conducted audits over a long period of time. Experienced auditors pay close attention to audit procedures with a high degree of accuracy. Another policy targeted to the auditor by the audit business is professional behaviour in avoiding DAB. A professional auditor must be objective when doing audit activities, which displays honesty by not performing premature sign-off, replacing any audit methods, or underreporting time.

Auditors must uphold the code of ethics by refraining from engaging in deviant audit behaviour. Audit firms must conduct quality control in the auditor profession and the accounting firm itself by conducting periodic audit work reviews and peer reviews of audit firms conducted by fellow accounting firms under the Centre for Financial Profession Development at the Ministry of Finance of the Republic of Indonesia (Indonesian Institute of Certified Public Accountants, Citation2021). Audit programmes and procedures are reviewed to avoid disobedience and errors in accordance with auditing and professional standards. Audit businesses use review and peer review as quality control tools to avoid DAB from affecting audit quality. The audit company’s quality control system can evaluate the auditor’s and audit firm’s performance in preventing DAB, one of which is a conflict of interest in the audit assignment between the audit firm, the auditor, and the client. Auditors who are not independent fall under DAB since the client wants the auditor to provide the best opinion. The auditor, on the other hand, must maintain independence in accordance with the accountant’s code of ethics and auditing standards (International Auditing and Assurance Standards Board, Citation2021b). The DAB phenomenon raises concerns about audit quality by providing biassed conclusions and can result in audit failures of customers evaluated by accounting firms’ auditors. To avoid DAB, which can reduce the quality of audits performed by auditors at audit firms in Indonesia, the Ministry of Finance of the Republic of Indonesia issued a policy aimed at audit firms that violate standard auditing regulations (SA)—professional standards for Indonesian public accountants (Indonesian Institute of Certified Public Accountants, Citation2021). Policy to freeze Audit Company permits that breach regulations, which is issued almost every year. To address DAB issues, audit firms must create rules to assess the performance of external auditors during COVID-19, which is based on EP, LOC, OC, TI, AP, and TBP.

3. Theoretical literature review

3.1. Attribution theory

This is the first study to apply Heider’s (Citation1958) basic research theory of attribution, which states that individuals can judge the behaviour of others as being influenced by internal factors or social perceptions, better known as dispositional attributions, and external factors, better known as situational attributions. Through a three-stage procedure, each of these persons may grasp and understand what other people’s behaviour they are doing (Kelley & Michela, Citation1980; Gunawan et al., Citation2020; Handoko et al., Citation2021; Hendijani et al., Citation2020; Tran et al., Citation2022; Wahidahwati & Asyik, Citation2022). These stages are as follows: (1) the individual must witness another individual’s behaviour. (2) Individuals must comprehend that the behaviour they are engaging in is done on purpose. (3) Individuals must decide whether or not to use force to carry out the behaviour. Internal elements stem from a person’s personality and personal control, and include motivation for behaviour, personal qualities, and perceptions. Internal factors that induce auditors to undertake DAB are influenced by behaviour in this study, specifically turnover intention (TI) and auditor position (AP). Internal auditors undertaking DAB are influenced by characteristics, specifically locus of control (LOC) and organisational commitment (OC), and perceptions, specifically auditor performance and time budget pressure (TBP). External factors, on the other hand, are associated with outside forces. That which cannot be controlled comes from humans, namely contextual forces that determine how people behave. Societal environment, societal ideals, and community perspectives are examples of external variables. In this study, the external factors that drove auditors to perform DAB were the conditions of COVID-19, where the auditor had to perform remote audit tasks, as well as when they were presented with a short TBP, thus they decided to undertake DAB.

Auditors utilise the attribution theory to conduct DAB because three internal and external causal factors influence them: Specificity is a situation in which the auditor behaves in carrying out DAB given the circumstances, especially a limited audit time budget. Consensus is a situation in which auditors conducting DAB face the same situation and respond in the same way to conducting DAB, namely the condition of COVID-19 in which auditors conduct remote audits, which have many limitations in collecting documentary evidence, sampling, and performing other audit procedures. When it came to COVID-19, the auditor performed a premature sign-off audit. When the auditor acts consistently to conduct DAB in all situations, this is referred to as consistency. These criteria include auditors with a low commitment to audit firms, auditors with a high turnover intention, auditors with poor performance, and auditors with a higher status. By analysing auditor behaviour from internal and external sources, this attribution theory can be utilised as a foundation for audit companies to evaluate auditor performance during COVID-19. This performance evaluation pertains to the auditor’s behaviour when performing audit assignments, including whether they perform DAB, which is influenced by internal factors such as EP, internal LOC, TI, OC, AP, TBP, and external LOC, as well as the condition of COVID-19 as an external factor.

3.2. The theory of planned behaviour

This study also employs the second core theory, Ajzen and Fishbein’s (Citation1969) theory of planned behaviour. According to this idea, three elements determine individual behaviour (Aziz et al., Citation2018; Bernardus et al., Citation2020). The first factor is belief and behaviour evaluation. The second aspect, normative belief, refers to the expectations of others to execute the behaviour as well as the drive to preserve those expectations of the behaviour that is performed. Perceptual power and individual control for behaviour are the third factors (Phuong Dung et al., Citation2023; Velástegui et al., Citation2021). Individual confidence in carrying out planned behaviours that generate negative and positive attitudes (Nguyen et al., Citation2022). Individual perceptions of what to do as a result of social pressure are formed as a result of normative beliefs (Shodipe & Ohanu, Citation2023). Individuals’ perceptions of control are also influenced by their belief in control (Purwanto et al., Citation2022). Control over perceptions derives from the combination of individual attitudes towards subjective norms (Nguyen et al., Citation2020; Zaman et al., Citation2021).

This theory is particularly relevant as a fundamental theory used to explain the auditor’s behaviour in accepting DAB since this behaviour is the auditor’s planned aim. Auditors believe that their performance at the audit firm is subpar. They also believe that the work they undertake is a burden on their lives that they cannot complete well, which is an example of external LOC. They have a high turnover rate and intend to move to another audit firm or work in a different profession. Auditors recognise that they have a low level of commitment to the accounting business where they work. Auditors recognise that they hold a very high position or level as auditors due to their extensive knowledge and expertise as auditors who can instruct junior auditors. Auditors encounter a lot of audit work with a short audit time, hence they receive TBP. The auditor’s numerous aspects provide assurance, evaluation, perception, and control, and the auditor ultimately plans whether they will obtain DAB. And this is in addition to the issue of environmental conditions, specifically COVID-19, which impacts auditors regardless of whether they approve DAB.

Before accepting the DAB, the auditor must be certain in the results received from the behaviour. The auditors will next decide whether or not to accept the DAB. The auditor faces normative expectations in audit tasks, as well as motivation and confidence from other parties. The greater the requirement for fairness guarantees from users of audited financial statements, the more motivated auditors are to act functionally by avoiding DAB. As a result, the auditor is more confidence in conducting an audit without DAB. Furthermore, the auditor considers the punishments obtained if they do DAB, which is within the auditor’s power to avoid DAB acceptance. The more severe the auditor’s consequence for accepting DAB, the more motivated the auditor is not to undertake DAB. This theory is also critical for audit firms. Because this condition is carefully intended for auditors to carry out DAB from belief, perception, and motivation elements such as EP, LOC, OC, TI, AP, and TBP, it may be utilised to evaluate auditor performance during COVID-19.

4. Empirical literature and hypotheses development

The premise for strengthening the relationship between internal locus of control and organisational commitment is attribution theory. Someone with excellent self-control, which is impacted by internal forces. These auditors are strongly dedicated to their organisation because of their exemplary behaviour, personal attributes, and self-perceptions. A person’s success is determined by their own actions or by external forces influenced by certain circumstances (Frucot & Shearon, Citation1991). Individuals’ achievement of goals and success is influenced by internal and external controls in specific settings and events (Ngoc et al., Citation2022). Patten (Citation2005) defines locus of control as a person’s self-control over an event that occurs to him. A person’s self-control consists of both internal and external loci of control. A person’s behaviour is heavily influenced by their attributes, which are influenced by an internal and external locus of control (Hyatt & Prawitt, Citation2001). They, like auditors, can carry out work to attain desired goals by adopting an internal locus of control and viewing life through an external locus of control (Hyatt & Prawitt, Citation2001). By having a high level of commitment, the locus of control promotes good performance (Donnelly et al., Citation2003b; Hyatt & Prawitt, Citation2001). Halil et al. (Citation2012) define organisational commitment as a willingness to advance organisational goals through good behaviours such as presence, discipline, and work performance. Auditors stay with accounting firms because they care about and believe in the goals and values of their organisation and profession (Donnelly et al., Citation2003a).

Paino et al. (Citation2012), Donnelly et al. (Citation2003a), Ghorbanpour et al. (Citation2014), and Anugerah et al. (Citation2016) conducted empirical study on the relationship between internal locus of control and organisational commitment. Paino et al. (Citation2012) discovered that the internal auditor’s locus of control positively influences organisational commitment. Meanwhile, empirical research by Donnelly et al. (Citation2003a), Ghorbanpour et al. (Citation2014), and Anugerah et al. (Citation2016) shows that internal locus of control affects organisational commitment. Auditor participation and loyalty have a significant impact on auditor performance, therefore an auditor’s high internal locus of control can have an impact on organisational commitment. The more the auditor’s internal locus of control, the greater the auditor’s commitment to the organisation. As a result, the first proposed hypothesis is:

H1:

There is a positive association between internal locus of control and organisational commitment.

Furthermore, attribution theory strengthens the association between internal locus of control (LOC) and employee performance (EP). Someone who has good self-control because of good behaviour, qualities, and perceptions that establish internal LOC. Someone with good internal LOC who is related with EP is motivated and responsible for their task with maximum results. So that a good internal locus of control is directly proportional to one’s performance, resulting in good output, some people believe that events are controlled by luck, fate, and other people, whereas others believe that events can be controlled by themselves, which is the internal locus of control (Frucot & Shearon, Citation1991; Serang & Wiwik, Citation2020).

Chen and Silverthorne (Citation2008) investigated the effect of locus of control on auditor performance, as did Paino et al. (Citation2012), Ghorbanpour et al. (Citation2014), Rahmisyari and Rizal (Citation2020), and Ngoc et al. (Citation2022). Chen and Silverthorne (Citation2008) found that internal LOC is positively connected to auditor performance in their empirical research. A study conducted by Ghorbanpour et al. (Citation2014), on the other hand, found that internal LOC is inversely connected to auditor performance. External auditors who believe their efforts do not result in good goals or performance are too indolent to work more efficiently because they have a relatively low or high external locus of control (Patten, Citation2005). They see their work as a burden that they cannot complete well (Ratnawati, Citation2020). Auditors with a high internal locus of control, on the other hand, are ambitious to perform a good job so that their goals can be met appropriately. Auditors in this category have a high level of responsibility, ability, planning, and goal achievement (Hyatt & Prawitt, Citation2001). Thus, the internal locus of control influences auditor performance; the more the external auditor’s internal locus of control, the better the auditor’s performance. As a result, the second hypothesis suggested is:

H2:

Internal locus of control and employee performance have a positive association.

The association between external LOC and turnover intention (IT) is strengthened by the attribution hypothesis. Individuals with external LOC view fate and luck to be external variables impacting their achievement, according to the hypothesis. Individuals with internal LOC outperform externals in terms of business, job happiness, and work drive (Chen & Silverthorne, Citation2008). Auditors with an internal locus of control are more resilient in general because they have a high level of personal control in coping with a variety of scenarios (Frucot & Shearon, Citation1991).

Previous research on the link between LOC and TI was undertaken by (Anugerah et al., Citation2016; Paino et al., Citation2012). Anugerah et al. (Citation2016) research findings give empirical evidence that external LOC has a favourable link with TI (Anugerah et al., Citation2016). Internal LOC, on the other hand, has a strained relationship with TI (Paino et al., Citation2012). Auditors with an external locus of control may prefer to leave a larger accounting company, but auditors with an internal locus of control have a low intention to leave (Donnelly et al., Citation2003b). Furthermore, auditors with an external locus of control show low organisational commitment, which increases their desire to leave the organisation (Donnelly et al., Citation2003b). According to Donnelly et al. (Citation2003b), auditors with a turnover goal are more prone to engage in dysfunctional behaviour in order to advance in their careers. Auditors with a high internal locus of control are more committed to their organisations because they are less likely to face punishments and can complete all tasks and targets to the best of their abilities. Auditors with a strong external locus of control, on the other hand, have a high intention to leave. Auditors with this locus of control are more likely to want to relocate to another audit firm or corporation. Auditors like these are afraid of getting fired if their work does not satisfy the criteria and objectives specified. As a result, the third hypothesis, which is as follows, follows.

H3:

External locus of control and turnover intention have a favourable association.

Attribution theory first strengthens the association between external LOC and dysfunctional audit behaviour (DAB). External LOC is influenced by external elements such as fate and luck, who want their job to meet aims, according to this viewpoint. A Locus of Control (LOC), according to Patten (Citation2005), is a hope in life that is controlled by one’s actions (internality) or outside influences (externalities). Individuals with internal LOC rely on themselves more to act ethically by regulating diverse situations and taking responsibility for their actions (Bryan et al., Citation2005). Individuals with external LOC, on the other hand, are governed by forces beyond their control and, as a result, are less personally responsible (Ngoc et al., Citation2022). Second, if external LOC is connected with dysfunctional audit behaviour (DAB), the theory of planned behaviour is the right framework for this interaction. The auditor carefully develops and executes DAB, which is influenced by social-environmental elements, specifically COVID-19. Those working remotely had difficulties gathering audit evidence, following systematic audit procedures, and managing a large amount of time and audit work, thus auditors received DAB to help them overcome these restrictions in COVID-19.

Donnelly et al. (Citation2003b); Paino et al. (Citation2011) (Paino et al., Citation2012); Alkautsar (Citation2014); Ghorbanpour et al. (Citation2014); Anugerah et al. (Citation2016); and Sunyoto and Sulistiyo (Citation2019) conducted previous studies evaluating the association between LOC and DAB. External locus of control has a positive link with DAB, according to empirical study (Alkautsar, Citation2014; Anugerah et al., Citation2016; Donnelly et al., Citation2003b; Ghorbanpour et al., Citation2014; Paino et al., Citation2011, Citation2012). Internal LOC, on the other hand, has a negative association with DAB (Sunyoto & Sulistiyo, Citation2019). Thus, an auditor with an internal LOC is expected to have a negative association with the desire to sign off prematurely (change/replace audit methods) and to report the time charged (signing ahead of time). Auditors with an internal LOC are more confident in their ability to control their lives than those with greater control (Bryan et al., Citation2005), whereas externals believe that external factors, such as luck, fate, or the influence of other people, control their lives (Malone & Roberts, Citation1996). External auditors are more prone to engage in dysfunctional acts that degrade audit quality (Donnelly et al., Citation2003b; Shapeero et al., Citation2003). As a result, the researchers proposed a fourth hypothesis:

H4:

There is a link between an external locus of control and dysfunctional audit behaviour.

According to the attribution theory, auditors with an external locus of control believe that the outcomes obtained are due to situational elements such as miracles, luck, and the environment rather than their own efforts. As a result, auditors like these must be pushed harder to accomplish audit targets by performing well. Meanwhile, auditors with an internal locus of control do their best and are really devoted to achieving something when given specific targets. Donnelly et al. (Citation2003a), Ghorbanpour et al. (Citation2014), Anugerah et al. (Citation2016), and Sunyoto and Sulistiyo (Citation2019) conducted empirical research on the role of organisational commitment in mediating the relationship between external locus of control and dysfunctional audit behaviour. According to the findings of Donnelly et al. (Citation2003a) and Anugerah et al. (Citation2016), OC modulates the link between external LOC and DAB. Nonetheless, empirical study by Ghorbanpour et al. (Citation2014) and Sunyoto and Sulistiyo (Citation2019) shows that OC does not regulate the relationship between external LOC and DAB. Auditors with an external locus of control are more prone to engage in dysfunctional audit behaviour (DAB) when their organisational commitment to the audit business is very low, especially when combined with situational and environmental elements such as the COVID-19 condition. As a result, the researcher suggests hypothesis 4a as follows:

H4a:

The association between external locus of control and dysfunctional audit behaviour is mediated by organisational commitment.

According to the attribution theory, auditors have a high internal LOC driven by views of wanting to advance and obtain good results, which determine what performance they expect. Auditors that have excellent performance and wish to improve their performance at the audit business do not receive DAB. The auditor can plan performance and DAB using the theory of planned behaviour. They can plan the desired performance, but they must have a plan and a drive to move forward. Furthermore, auditors receive DAB under specific conditions and situations, such as COVID-19, which forces them to operate remotely in order to complete audit assignments on time.

Previous research (Anugerah et al., Citation2016; Donnelly et al., Citation2003b) looked at employee performance (EP) as a moderator between external LOC and Acceptance of Dysfunctional Behaviour. According to the findings of Donnelly et al. (Citation2003b), EP did not influence the link between external LOC and DAB. Meanwhile, Anugerah et al. (Citation2016) found that EP mediates the link between external LOC and DAB in their empirical investigation. They are inspired to carry out planned and premeditated DAB under these settings. As a result, the auditor’s performance as an intermediary connecting LOC and DAB. A good internal LOC has a positive impact on the auditor’s performance, so they are less likely to accept DAB. External LOC, on the other hand, has a direct association with DAB, and external LOC has a negative impact on auditor performance, thus they incline to accept DAB. As a result, hypothesis 4b is:

H4b:

The association between external locus of control and dysfunctional audit behaviour is mediated by employee performance.

According to attribution theory and the theory of planned behaviour, TI plays a mediating role in the link between external LOC and DAB. Auditors with a high external LOC believe that luck and fate bring about life changes that lead to a desire to leave audit firms and other professions. Auditors are motivated to take DAB because they intend to leave the audit firm to work in their new audit firm or profession. Auditors have the possibility to obtain DAB based on the notion of planned behaviour that auditors have a high turnover intention. According to attribute theory and the theory of planned behaviour, auditors with high external LOC have a higher turnover intention because they quit the audit firm to work for a new audit firm or profession to get DAB. As a result, TI mediates the link between the external LOC and the DAB. Previous research, such as Donnelly et al. (Citation2003b), Paino et al. (Citation2012), Ghorbanpour et al. (Citation2014), and Anugerah et al. (Citation2016), has examined how TI mediates the link between external LOC and DAB. Empirical evidence suggests that TI mediates the link between external LOC and DAB (Anugerah et al., Citation2016; Donnelly et al., Citation2003a; Ghorbanpour et al., Citation2014; Paino et al., Citation2012). As a result, the proposed 4c hypothesis is:

H4c:

The association between external locus of control and dysfunctional audit behaviour is mediated by turnover intention.

According to the attribution theory, an individual is motivated to enhance their performance, which is impacted by internal causes, namely intrinsic motivation, in order to become more devoted to their organisation and profession. Thus, the paradigm of attribution theory strengthens the association between auditor performance and organisational commitment in this study. Auditors excel because they are passionate about the accounting company where they work (Setianingrum et al., Citation2016). The same is true for good auditor performance since auditors are extremely dedicated to their profession and career. Junior auditors’ performance differs from that of senior auditors, managers, and partners, and is determined by the amount of commitment (Martini et al., Citation2020). The performance of the junior auditor effects the effort to mobilise the organisation, which is influenced by willingness, but the performance of the senior auditor influences the effort to sustain organisational membership, which is influenced by a strong desire (Paino et al., Citation2012). Previous study has linked auditor performance to organisational commitment, such as empirical research (Ghorbanpour et al., Citation2014). Ghorbanpour et al. (Citation2014) discovered that auditor performance is positively related to organisational commitment. In general, auditors who do well have a strong organisational commitment to the profession.

H5:

There is a favourable association between employee performance and organisational commitment.

According to the attribution theory, elements such as motivation, beliefs, and perceptions influence someone who performs well internally. They believe their performance is good, thus they are loyal to their employer and are hesitant to leave. In other words, they have no intention of relocating to another company or organisation. Auditors with the lowest performance intend to leave the most (Paino et al., Citation2012). Thus, the inclination to change occupations is low among auditors who do well (Luna‐Arocas & Camps, Citation2007). Previous study has looked at the association between Employee Performance (EP) and Turnover Intention (TI) (Balouch & Hassan, Citation2014; Biron & Boon, Citation2013; Ghorbanpour et al., Citation2014; Nawaz & Pangil, Citation2016; Paino et al., Citation2012; Saeed et al., Citation2014; Shofiatul et al., Citation2016; Yücel, Citation2021). According to the findings of Paino et al. (Citation2012) and Ghorbanpour et al. (Citation2014) empirical research, auditor performance is inversely associated to TI. However, empirical research (Shofiatul et al., Citation2016) shows that auditor performance is inversely associated to TI, but the relationship is not substantial. Empirical evidence suggests that EP is negatively connected to TI (Biron & Boon, Citation2013; Nawaz & Pangil, Citation2016; Saeed et al., Citation2014; Yücel, Citation2021). Nonetheless, empirical study (Balouch & Hassan, Citation2014) shows that EP is inversely connected to TI, but the relationship is not substantial. Individual performance suffers when turnover intention is high (Raza & Raja, Citation2014). The smaller the intention to turnover, the better the auditor’s performance. Auditors who perform well are promoted and more loyal to their organisations (Wong et al., Citation2015), whereas auditors who fail to meet predetermined minimum standards or meet work targets face sanctions and may even be expelled from the audit firm where they work (Paino et al., Citation2012). The sixth hypothesis is as follows:

H6:

Employee performance and turnover intentions have a negative association.

Attribution theory strengthens the initial relationship between EP and DAB; auditors have views and opinions about their performance. If their performance is poor, they will behave poorly when performing audit tasks, and vice versa. The auditor’s bad performance persuades him to accept the DAB. The acceptance of DAB reflects the auditor’s purpose to plan this behaviour, implying that the notion of planned behaviour reinforces it. Employees who perform well will have less dysfunctional behaviour since they can prevent it and work at full capacity (Johansen & Christoffersen, Citation2017). Donnelly et al. (Citation2003b); Anugerah et al. (Citation2016); Paino et al. (Citation2012); Ghorbanpour et al. (Citation2014); Nehme et al. (Citation2019) are examples of previous studies evaluating the link between EP and DAB. According to empirical research, auditor performance is negatively related to dysfunctional audit behaviour (Anugerah et al., Citation2016; Donnelly et al., Citation2003a; Nehme et al., Citation2019), but employee performance is positively related to DAB (Ghorbanpour et al., Citation2014; Paino et al., Citation2012) because the auditor’s goal is to get a promotion and does not consider it unethical behaviour. When conducting audits, high-performing auditors have very low DAB (Nehme et al., Citation2021). Low auditor performance, on the other hand, influences auditors to engage in highly dysfunctional behaviour (Al-Qatamin et al., Citation2021; Nehme, Citation2017); this is because auditors with substandard performance levels lack the expertise and ability to survive in the audit firm (Khalil & Nehme, Citation2021; Nehme et al., Citation2021). According to attribution theory, auditors like this would frequently go to great lengths to improve performance so that it looks good, such as committing fraud during the audit process and falsifying audit reports. As a result, the seventh hypothesis suggested is:

H7:

There is a link between poor employee performance and dysfunctional audit behaviour.

Previous research had not studied the mediating function of organisational commitment (OC) in the link between EP and DAB, hence this study was innovative. Attribution theory and the theory of planned behaviour both support the function of OC as a mediator in the interaction between EP and DAB. According to attribution theory, auditors believe their performance is good, hence they are committed to the audit firm and should not take DAB. In contrast, auditors who are confident in their performance in the audit firm have minimal commitment to the audit firm, which is the framework of the theory of planned behaviour. Because the COVID-19 condition supports DAB in this reverse connection, the auditor is likely to accept it. The hypothesis of planned behaviour, on the other hand, strengthens this attitude because the auditor intends or consciously accepts DAB. As a result, the proposed hypothesis 7a is:

H7a:

The association between employee performance and dysfunctional audit behaviour is mediated by organisational commitment.

Because there has been no previous research evaluating the function of TI mediation in the link between EP and DAB, this study is unique. Attribution theory and the theory of planned behaviour both support TI’s position as a mediator in the interaction between EP and DAB. According to the Attribution theory, auditors who believe their performance at the audit firm is poor intend to leave the firm. Those who intend to leave their jobs at audit firms are encouraged to plan to do DAB as well. This behaviour is related to the planned behaviour idea. EP deals directly with DAB, whereas TI serves as an intermediate, forming an indirect interaction between EP and DAB. External LOC persuades auditors to perform TI in audit firms or other professions so that they can receive DAB in carrying out their audit obligations after leaving the audit firm. So the proposed H7b theory is:

H7b:

The desire to turnover influences the association between employee performance and dysfunctional audit behaviour.

According to the theory of planned behaviour, auditors with high turnover intention (TI) have a very low organisational commitment (OC) to the audit business because they want to leave or pursue another career. High TI indicates that they have a strong desire to leave the audit firm, which is impacted by internal elements like as attitudes, views, and motivation, as well as external factors such as the environment. Attribution theory reinforces this state. Kumar et al. (Citation2012); Jehanzeb et al. (Citation2013); Ghorbanpour et al. (Citation2014) investigate the association between turnover intention and organisational commitment. The empirical findings of the study (Ghorbanpour et al., Citation2014) reveal that TI is inversely connected to OC. The desire to retain organisational membership; in this situation, the auditor is loyal to his profession (Al Balushi et al., Citation2022). According to the study’s findings (Donnelly et al., Citation2003b), auditors who are willing to leave a high organisation have a low organisational commitment. Auditors who are extremely loyal to the accounting firm where they work are less likely to leave or go on to another audit firm. The more the auditor’s intention to leave, the lower the organization’s commitment to the profession. As a result, the eighth hypothesis suggested is:

H8:

Turnover intention and organisational commitment have a negative association.

The notion of planned behaviour provides a framework for thinking about the interaction between TI and DAB. Auditors engage in planned behaviour when it comes to TI and DAB. Tjan (Citation2019) defines turnover intention as an auditor’s desire to depart an accounting business. Auditors have confidence, motivation, and views about doing TI since it is influenced by internal and external factors. Attribution theory supports auditors who do TI in audit organisations. Auditors who perform DAB can also be viewed through the lens of attribution theory because they perform DAB while being influenced by internal factors such as perceptions, motivations, and beliefs.

Donnelly et al. (Citation2003b); Paino et al. (Citation2011); Paino et al. (Citation2012); Ghorbanpour et al. (Citation2014); Anugerah et al. (Citation2016) have previously investigated the link between TI and DAB. TI has a favourable link with DAB, according to empirical study (Anugerah et al., Citation2016; Donnelly et al., Citation2003b; Ghorbanpour et al., Citation2014). While TI has a negative connection with DAB, as demonstrated by Paino et al. (Citation2011) and Paino et al. (Citation2012) studies. According to Malone and Roberts (Citation1996), auditors who intend to move to an accounting firm or other profession are more likely to perform DAB during an audit. This is due to a decrease in the auditor’s fear of being fired from the organisation where they work, which causes the auditor to perform DAB. Meanwhile, auditors who intend to leave quickly avoid DAB (Anugerah et al., Citation2016). The more the auditor’s turnover intention, the better the DAB, or auditors, perform during the audit. Furthermore, auditors with a high turnover intention are more likely to perform DAB in order to obtain a more suited position in a new organisation (Anugerah et al., Citation2016; Donnelly et al., Citation2003b; Paino et al., Citation2011). Dysfunctional behaviour leads to lower job satisfaction and higher levels of turnover intention, resulting in lower organisational performance (Paino et al., Citation2011). Auditors that engage in high DAB have a high turnover intention because they are afraid of being caught (Balasingam et al., Citation2019). Furthermore, according to attribution theory, auditors engage in dysfunctional audit behaviour and are unconcerned about it since they have a strong intention to leave their work (Tjan, Citation2019). As a result, the ninth hypothesis is as follows:

H9:

There is a link between turnover intent and dysfunctional audit behaviour.

Previous research has not studied the function of mediating organisational commitment (OC) in the relationship between TI and DAB, hence this study is innovative. Attribution theory and the theory of planned behaviour both support the function of OC as a mediator in the interaction between TI and DAB. According to attribution theory, auditors have the view and conviction that using TI would result in the desired changes in their lives. They do TI because they believe it will improve their job. New employment and locations ensure a better life. TI and DAB are both behaviours carried out with the goal of what is planned with a specific purpose, according to the notion of planned behaviour. Auditors feel confident in changing jobs or moving to a different audit firm with higher expectations. Auditors with this level of devotion to the audit firm where they work are more likely to receive DAB in carrying out audit assignments since auditors depart the audit firm where they work. As a result, hypothesis 9a is as follows:

H9a:

The association between turnover intention and dysfunctional audit behaviour is mediated by organisational commitment.

Attribution theory and the idea of planned behaviour help to deepen the link between OC and DAB. It explains, in conjunction with attribution theory, why auditors are confident in their commitment to the audit firm and loyalty to their organisation. Auditors are responsible for the advancement of their organisations because they care about them. A committed auditor is also accountable for the audit assignment given if DAB is not scheduled; this relationship is the attitude of the theory of planned behaviour. Organisational commitment is defined as acceptance of the organization’s principles and aims (Lord & DeZoort, Citation2001). Organisational commitment, according to Halil et al. (Citation2012), demonstrates motivation variations between persons with high and low commitment. Individuals who are committed to making the greatest sacrifice contribute to and advance their careers as auditors in the organisation (Donnelly et al., Citation2003a). Individuals with a high level of organisational commitment desire the organisation to progress and develop in a positive manner (Halil et al., Citation2012). Individuals with low commitment, on the other hand, are more concerned with themselves than with the interests of others or the organisation (Donnelly et al., Citation2003a).

As a result, auditors who are less dedicated to the organisation are more likely to perform DAB as a means of promoting themselves (Donnelly et al., Citation2003a). Auditors with strong organisational commitment, according to Halil et al. (Citation2012), restrict DAB, whereas auditors with insufficient organisational commitment have the ability to engage in extremely dysfunctional audit behaviour (Donnelly et al., Citation2003a; Malone & Roberts, Citation1996). Empirical evidence suggests that OC is inversely connected to DAB (Anugerah et al., Citation2016; Donnelly et al., Citation2003a; Paino et al., Citation2012; Sunyoto & Sulistiyo, Citation2019). While empirical research results (Ghorbanpour et al., Citation2014; Kusumastuti & Nirmala Arum Janie, Citation2014; Svanberg & Öhman, Citation2016) show that OC has a favourable connection with DAB. High commitment to the organisation and the profession to refrain from doing DAB since they are accountable for performing well (Donnelly et al., Citation2003a). Most auditors who are disciplined in their work and work hard to achieve organisational goals have a high organisational commitment, do not lower audit quality to reach personal goals, and are more ethical not to perform DAB (Donnelly et al., Citation2003a). As a result, the tenth hypothesis suggested is:

H10:

Organisational commitment and dysfunctional audit behaviour have a negative association.

The association between time budget pressure (TBP) and DAB is strengthened by the theory of planned behaviour and attribution theory. According to the theory of planned behaviour, the auditor is under pressure to meet the audit time budget specified in the plan. The capacity of the auditor to accomplish the task set within the predetermined time budget is related to the auditor’s performance rating at the accounting company (Robertson et al., Citation2011). The time budget is used in accounting companies to plan and manage audit tasks, as well as to control the efficacy of audit fees (Lord & DeZoort, Citation2001). The audit time budget is highly necessary for the auditor to finish the audit until the audit report is completed, while some scholars believe the time budget is not important for the auditor (Mansor et al., Citation2022; Sweeney & Pierce, Citation2004). According to attribution theory, the auditor’s perspective has various reasons why it is critical to meet the time limit in order to evaluate auditor performance (Nor et al., Citation2017). Auditors confront time budget pressures such as failure to trace accounting principles, reduction of audit procedures, and reduction of audit evidence so that audit evidence is weak, according to Soobaroyen and Chengabroyan (Citation2006). Time budget pressure expresses concern about not having enough time to perform audit work as a result of excessive stress on audit work (Amiruddin, Citation2019; Lord & DeZoort, Citation2001). Due to a lack of reporting and personal presence in completing audits, duties may not be completed on time due to unrealistic time budgets (Umar et al., Citation2017; Wetmiller, Citation2022). This pressure is strongly associated with dysfunctional audit behaviour, which can result in poor audit quality (Astuty et al., Citation2022; Svanström, Citation2016). Failure to explore problematic problems and early audit sign-off are examples of dysfunctional audit behaviours (Cook & Kelley, Citation1988). Furthermore, other issues that put pressure on time budgets include the impact of audit programmes, the effect of client expectations on audit fees, and the previous year’s budget (Nehme et al., Citation2022; Otley & Pierce, Citation1996a; Pierce & Sweeney, Citation2004).

DAB has a linear relationship with time budget pressure (Amy et al., Citation2022; DeZoort & Lord, Citation1997; Otley & Pierce, Citation1996a). Pierce and Sweeney (Citation2004), Balasingam et al. (Citation2019), San Ong et al. (Citation2022), and Nguyen Van Hau et al. (Citation2023) did empirical study on the association between TBP and DAB. Time budget pressure is positively and strongly connected with DAB, according to empirical study (Pierce & Sweeney, Citation2004; Balasingam et al., Citation2019; San Ong et al., Citation2022; Nguyen Van Hau et al., Citation2023. High audit time budget pressure will also influence the auditor’s behaviour because the auditor is under pressure to complete the audit promptly following the predetermined audit deadline (Amiruddin, Citation2019; Coram et al., Citation2003; Svanberg & Öhman, Citation2016). Auditors with limited time invite dysfunctional audit behaviour (Kelley & Seller, Citation1982; Paino et al., Citation2019). When time budget demands are deemed unaffordable and tighter, DAB will increase (McNamara & Liyanarachchi, Citation2008; Otley & Pierce, Citation1996a; Soobaroyen & Chengabroyan, Citation2006). As a result, the eleventh hypothesis given is:

H11:

Time budget pressure and dysfunctional audit behaviour have a good link.

Attribution theory strengthens the association between auditor position (AP) and OC. According to the hypothesis, the auditor is motivated to advance in the audit firm. And the auditor is confident that those with advanced AP and extensive experience demonstrate the auditor’s dedication to the audit business. The position or position of the auditor can be seen in the audit firm’s hierarchical organisational structure. Auditor positions are organised in the audit firm’s organisational structure as follows: junior auditor, senior auditor, manager, and partner (Donnelly et al., Citation2003a). The position of the auditor in the firm audit differs depending on the auditor’s duties, authorities, interests, and responsibilities in the organisation (Lambert & Agoglia, Citation2011). Organisational commitment is related to tenure in the organisation (Quarles, Citation1994); individuals are committed because of their position and sense of duty. Meyer and Allen (Citation1984) found that organisational tenure corresponds positively with organisational commitment.

Previous study on the link between AP and OC, such as empirical work by Chen and Francesco (Citation2000), Donnelly et al. (Citation2003a), and Sweeney et al. (Citation2003). Empirical evidence shows that AP correlates positively with OC (Chen & Francesco, Citation2000; Sweeney et al., Citation2003). In contrast, empirical studies undertaken by Donnelly et al. (Citation2003a) demonstrated that AP harms OC. Sweeney et al. (Citation2003) found that the higher the auditor’s status in the audit business, the greater their commitment to the organisation. Their position and function in the audit company have an impact on auditor performance. In this scenario, an employee is an auditor with a position, significant autonomy, and a high level of dedication to the audit firm (Bassett, Citation1994). As a result, the twelfth hypothesis given is:

H12:

The auditor role and organisational commitment have a good association.

The relationship between AP and DAB can be explained by attribution theory and the theory of planned behaviour. According to attribution theory, auditors are driven to accomplish audit activities in accordance with the audit company’s projected targets because they have the motivation and confidence to achieve good AP in the audit firm. According to the theory of planned behaviour, auditors might plan and intend to advance to a higher level in the audit business. A senior AP, on the other hand, can order and influence lower-level auditors to meet audit targets. According to the principle of planned behaviour, AP at a high degree should be given DAB because it is a planned behaviour.

Raghunathan (Citation1991), Donnelly et al. (Citation2003a), Morris (Citation2014), Nor et al. (Citation2015), and Herda and Martin (Citation2016) conducted previous studies on the link between AP and DAB. According to the findings of Donnelly’s et al. (Citation2003a) empirical investigation, AP has a negative relationship with DAB. According to Raghunathan (Citation1991) empirical research, the auditor’s position influences dysfunctional audit behaviour produced by time budget constraint. Morris (Citation2014); Nor et al. (Citation2015); Herda and Martin (Citation2016) assert that upper-level auditors are more professional when they audit by following proper audit processes (Herda & Martin, Citation2016; Morris, Citation2014; Nor et al., Citation2015). In this study, auditor positions were divided into two categories: lower-level auditor positions, known as junior auditors, and upper-level auditor positions, known as senior management and partner auditors (Ponemon, Citation1992a). Accounting businesses delegate audit time to junior auditors who can make appropriate decisions based on the risk-based audit time budget (Lee, Citation2002). Senior auditors must have expertise and skills in recognising any attempt by junior auditors to prematurely sign off (Hyatt & Taylor, Citation2013), whereas superior auditors evaluate and supervise the work of other auditors (Gimbar et al., Citation2018). Experienced auditors train and manage inexperienced junior auditors (McManus & Subramaniam, Citation2009). Auditors exhibit dysfunctional behaviour during audits due to time and money constraints (McNamara & Liyanarachchi, Citation2008; Ponemon, Citation1992b; Wetmiller, Citation2022). To function well, lower-level auditor jobs, such as junior auditors, require the attention, guidance, and supervision of supervisors, managers, and partners (Sweeney et al., Citation2010). Upper-level auditors must provide lower-level auditors with performance ratings. This review is performed to ensure that lower-level auditors accomplish audit activities correctly and on time in order to minimise DAB (Morris, Citation2014; Sweeney & Pierce, Citation2004). As a result, the thirteenth hypothesis is as follows:

H13:

The auditor role has a negative link with dysfunctional audit behaviour.

Previous research has not studied the mediating function of organisational commitment (OC) in the link between AP and DAB, hence this study is innovative. Attribution theory and the theory of planned behaviour both support the function of OC as a mediator in the interaction between AP and DAB. According to attribution theory, auditors in audit firms have the perception, incentive, and confidence to achieve a higher AP. At a high level, AP demonstrates that they have a high OC as well because most auditors who work in audit firms are aware of the success of their audit businesses. And it differs from auditors who achieve AP at a high level due to the nature and experience of other audit firms, when the auditor has recently joined a new audit firm. DAB is discouraged for higher level APs with high OC because their experience has shown them that it is not a good practise. Auditors have goals and plans to raise their level to a higher position so that they do not face pressure from auditors with a higher level, according to the Figure : the conceptual framework of the study. Auditors who desire and aspire to attain high AP have a high OC in the audit firm, therefore they limit DAB when conducting audits. As a result, OC serves as a middleman between AP and DAB. As a result, hypothesis 13a is as follows:

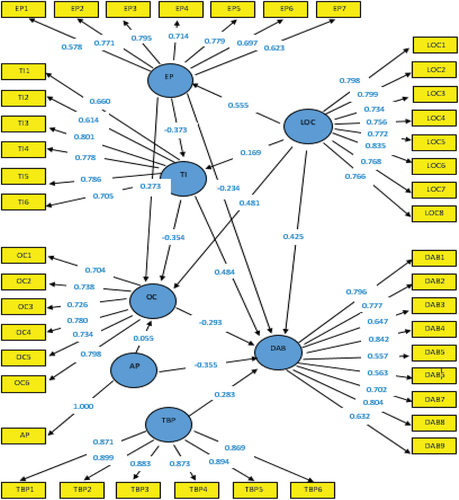

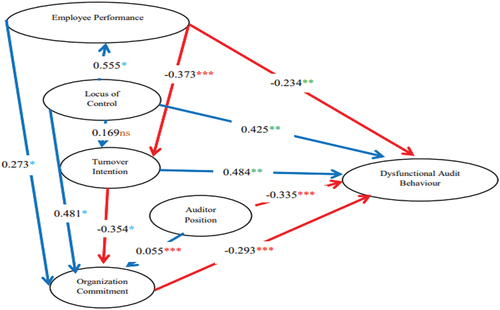

Figure 1. Depicts the conceptual framework of the factors impacting dysfunctional audit behaviour (DAB).

H13a: The association between auditor position and dysfunctional audit behaviour is mediated by organisational commitment.

Figure depicts the conceptual framework of the study, which was developed after a thorough review of mainstream literature.

5. Research design

5.1. Sample and procedure

The participants in this study are external auditors from Indonesian accounting companies. There are 635 accounting firms in Indonesia, according to the Indonesian Institute of Certified Public Accountants (Citation2022). Based on these , there are 4,722 external auditors in Indonesia, including 1,442 partners and 3,280 auditors who have Certified Public Accountants (CPA) registered with the Indonesian Institute of Certified Public Accountants (Citation2022). However, because the total number of external auditors in Indonesia, including senior and junior auditors, is not known with certainty, the sampling technique in this study used a random sampling technique because the total number of external auditors working in accounting firms in Indonesia is not known with certainty. The external auditors are also dispersed across Indonesia’s large area and between islands. Another explanation is the COVID-19 pandemic factor, which is a factor of uncertainty regarding uncertain economic conditions, which enables for the external auditor turnover rate to arise in accounting businesses. The COVID-19 circumstances resulted in the distribution of questionnaires in this study, which was conducted from May to October 2022 utilising a Google form.

Figure 2. Path analysis research model.

In this study, data is processed using structural equation modelling of partial least squares (SEM-PLS) to test causal and theoretical models with SmartPLS. This is due to Cohen’s (Citation1992) suggestion that the minimum sample size required for PLS-SEM analysis be 103. The study can estimate the dispersed questionnaires based on these criteria, as shown in Table .

Table 1. Sample questionnaire count recapitulation

According to Cohen (Citation1992), the researchers assessed the expected sample size by distributing 220 questionnaires to complete the expected number of study samples based on the minimal sample size criteria for PLS-SEM analysis of at least 103 samples. There were 135 returned questionnaires, with 17 damaged questionnaires because the respondents’ answers were untrustworthy; where respondents with the same number filled in the answers and did not vary, the researcher judged the questionnaire unacceptable for use. As a result, 118 samples were collected, with a response rate of 135 (61.36%) and a usable response rate of 118 (53.64%). As a result, this study lends itself well to structural equation modelling of partial least squares.

5.2. Data collection

As primary data, a questionnaire was constructed based on prior research conducted by external auditors at audit companies and modified to the requirements of COVID-19 in Indonesia. 7 Likert scales were used to create surveys for employee performance, locus of control, turnover intention, organisational commitment, time budget pressure, and dysfunctional audit behaviour. The auditor position variable, on the other hand, employed a dummy variable pertaining to positions in accounting firms. Each study variable or construct is made up of multiple indicators that were created based on past research and include several questions and answer choices on the current Likert scale.

In this study, all variables were examined using a Likert scale with the same seven alternative answers, namely “strongly disagree” (1) to “strongly agree” (7). The survey questionnaire in this study is written in Indonesian. In this study, the opening section of the questionnaire briefly outlined the reasons for the research, as well as the instructions for filling out the survey questionnaire and demographic profile. Respondents completed a demographic profile that included their gender, age, amount of education, job experience, and auditor position. The second section includes questions about each of the variables studied. Table shows the classification of variables, constructs, indicators, and the Likert scale, which are operational variable measurements.

Table 2. Measurement of the constructs

6. Empirical results and discussion

6.1. Empirical results

The findings of this empirical study interpret the respondents’ identities, descriptive statistics of the research variables, and PLS test results. The three research findings clarify what was seen, making it simpler for researchers to share their findings in discussion.

6.1.1. Respondent identification

Table shows the gender distribution of the 118 external auditors in this study, revealing that 77 (65%) were male and 41 (35%) were female. The majority of external auditors are between the ages of 31 and 35, with 54 (46%); under 30, with 19 (16%); 36–40, with 32 (27%); and over 41, with 13 (11%). External auditors in Indonesia have an average education level of 71 (60%), master’s degree 38 (32%), and doctorate 9 (8%). The majority of external auditor job experience ranges from 5 to 10 (74 or 63%), less than 5 (29 or 25%), and greater than 10 (15 or 12%). 51 senior auditors (43%), 32 junior auditors (27%), 27 managers (23%), and 8 partners (7%) held the most external auditor positions. The identities of the respondents are displayed in Table :

Table 3. Demographic profile of the sample

6.1.2. Descriptive statistics

This descriptive statistics provides mean, minimum, maximum, and standard deviation values for the research variables. The significance of these descriptive statistics explains that external auditors’ EP is good, their self-control is excellent, their TI during COVID-19 is very high, their position is mostly senior and junior auditors, their OC is high, their time budget pressure is high, and their DAB is high. Table shows the results of the descriptive statistics for the research variables.

Table 4. Displays descriptive statistics for exogenous and endogenous variables

6.1.3. Partial least squares results

This study uses PLS-SEM to investigate causal and theoretical models. The test was evaluated using a two-step procedure: (1) evaluating the measurement model and (2) evaluating the structural model (Hult et al., Citation2018; Wold, Citation1980).

6.1.3.1. Measurement models

This measurement model examines the relationship between exogenous and endogenous variables to evaluate research variable indicators. These indicators clarify the concept and improve results. This model evaluates Cronbach’s alpha composite dependability (Dijkstra & Henseler, Citation2015; Hult et al., Citation2018; Nunnally & Bernstein, Citation1994). Hair et al. (Citation2017) say composite reliability makes data reliable (greater than 0.7). Individual item reliability has an outer loading of 0.40–0.70 (Hult et al., Citation2018). Validity is another measurement model. Henseler et al. (Citation2015), Hult et al. (Citation2018) describe data quality as an average variance extracted (AVE greater than 0.5). Table shows this study’s findings. All indicators are trustworthy and valid over standard values. This study’s construct threshold was 0.557–0.899 (See Table ).

Table 5. Convergent validity and reliability of constructs: LOC, OC, EP, TI, TBP, AP, and DAB