?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the shariah governance reporting (SGR) of Islamic banks (IBs) through a reporting index comprised of six dimensions, namely shariah committee, shariah review, shariah audit, shariah risk, overall transparency, and investment account holders. The data between 2014–2018 werecollected from the annual reports of 16 licensed IBs in Malaysia and was analyzed using the content analysis technique to gain insight into SGR practices. The empirical results indicate that sampled IBs have reported above average (60%) information of shariah governance (SG) and overall dominance of shariah reporting across the index. The segmental overview of SGR represents that all six dimensions were reported in a scattered pattern, while thematic reporting was less scattered. Broad spectrum results indicate that Malaysian IBs have reported above average (62.22%) information about shariah review and shariah risk (71.11%), whereas other dimensions’ reporting was below average. The findings have also confirmed that the SGR of IBs is statistically different. This research offers matrices for IB managers to determine the accuracy, validity, and authenticity of their annual reports and customize according to shariah reporting requirements. The regulators may use this study to assess IBs’ compliance with SG and improve their regulations as per globally accepted governance standards.

1. Introduction

Besides conventional governance structure, Islamic banks (IBs) have an additional governance layer known as the shariah governance (SG), which is a key tool used by IBs to mitigate the risks associated with shariah noncompliance (Zuhroh, Citation2022). The term SG was first coined by M.A Qatan in 2003 and defined it as “the governance process essentially relies on the fundamentals of Islamic financial architecture” (Ginena & Hamid, Citation2015). The standard setting bodies, Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) and the Islamic Financial Services Board (IFSB) started using this concept to develop and assess the SG of Islamic financial institutions (IFIs) (Tabash et al., Citation2022). [IFSB] (Citation2009) defined it as ‘the organizational and institutional arrangements to authenticate effective and independent supervision of shariah compliance of the relevant Shariah pronouncements/resolution and its dissemination as well as an internal and annual Shariah compliance review/audit.

The extant literature on shariah governance reporting (SGR) outlines that developing effective SG mechanisms and practicing transparency in reporting allows IFIs to rebuild public confidence, achieve business objectives, and ensure growth consistency (Ab Ghani et al., Citation2023; Elamer et al., Citation2020a). Additionally, SGR streamlines IFIs’ business, affairs, and activities to fulfill regulatory requirements as well as ensure the prevalence of shariah standards in internal policies and procedures (Ferriswara et al., Citation2022; Laldin & Furqani, Citation2018). Several emerging studies have identified multiple reasons for the need for SGR in IFIs (Elghuweel et al., Citation2017). First, reporting of products, services, operations, and governance information through annual reports allows stakeholders to assess institutional compliance with shariah principles, the level of internal control, SG practices, and credibility of financial information (Alam et al., Citation2022; Kasim et al., Citation2013). Second, transparency in SGR boosts shareholders, board of directors (BODs), management, and stakeholders’ confidence by preserving IFIs’ integrity and reputation (Mukhibad et al., Citation2022). Third, SGR represents IFIs’ capability to understand and interpret shariah rules and principles to ensure the implementation of shariah principles in every business activity allows them to conform to religious requirements (Garas & Pierce, Citation2010; Muhammad et al., Citation2021).

Several studies in the past have examined the SG practices, issues, and challenges faced by IFIs across jurisdictions (Abdullah Saif Alnasser & Muhammed, Citation2012; Fatmawati et al., Citation2022; Hasan, Citation2011). Ironically, a large proportion of these studies have used descriptive techniques to examine the SG, while a small number of studies have focused on empirical techniques to address SG issues (Garas, Citation2010, Citation2012). From the SGR perspective, six seminal studies (Darmadi, Citation2011; Hameed & Pramono, Citation2005; Hassan & Christopher, Citation2005; Majid et al., Citation2011; Pramono, Citation2005; Sulaiman et al., Citation2011) were conducted which have laid the foundation of modern empirical studies. A few novel studies (see, Albassam & Ntim, Citation2017; Elamer et al., Citation2020a, Citation2020b; Elghuweel et al., Citation2017) employed statistical analytical techniques to link SGR to several macro- and social-level factors, religious orientations, appointment of shariah supervisory board (SSB), and ownership structure with improved governance and risk management.

The plethora of literature focuses on SG and social reporting of IFIs have largely used content analysis techniques to develop a range of indices (Amalina Wan Abdullah et al., Citation2013; Belal et al., Citation2015; Haniffa & Hudaib, Citation2007; Kamla & Rammal, Citation2013; Maali et al., Citation2006; Mallin et al., Citation2014). However, the findings of these studies offer little insight into the actual mechanism of SGR, especially using graphic properties. Whereas, the importance of graphic properties in content analysis of annual reports is well documented in conventional as well as Islamic finance literature (Abdul Latif et al., Citation2023; Beattie & Jones, Citation2002; Kamla & Roberts, Citation2010; Preston et al., Citation1996; Yin, Citation2005). A few studies on social reporting of IBs have emphasized the significance of graphics in content analysis (Haniffa & Hudaib, Citation2007; Hussain et al., Citation2021; Maali et al., Citation2006). However, these studies were also unable to offer any logical explanation of the outcome of graphics, especially related to SGR of IBs. This issue was addressed by a recent study of Amin et al. (Citation2021) investigating the SGR of IBs in Malaysia through content analysis of annual reports. However, the findings of the study do not offer an insight into the periodic developments in SGR pattern of Malaysian, as the results were based on the analysis of a single year (2016) annual report. Hence, it is difficult for the investors, stakeholders, and IB customers to track the periodic changes in SGR patterns and conclude how different aspects of SG have responded to the introduction of latest SG standards of AAOIFI and IFSB. Consequently, this study aims to bridge this gap by expanding the data coverage and analyzing the SGR of each aspect involved in SG of IBs. Precisely, this study aims to investigate the following research questions;

What is SGR pattern of IBs in Malaysia?

What are the essential dimensions and themes of SGR covered by IBs in Malaysia?

What are the differences in SGR of different IBs in Malaysia?

Malaysian IBs are selected to determine the SGR patterns, essential themes, and dimensions, and to explore the difference among different IBs. Malaysia is championing the global Islamic finance industry with a net worth of more than RM2.3 trillion, rendering it as one of the key contributors to the global Islamic banking assets and an Islamic finance hub in the region (Malaysia, Citation2022). The provision of Islamic banking services is achieved through 16 (11 locally owned and 5 foreign-owned) licensed IBs coupled with Islamic banking windows in conventional banks to cater to the rising demand of the local community (Bank Negara Malaysia [BNM], Citation2023). An empirical analysis of SGR of Malaysian IBs will determine the shariah compliance level of IFIs, which often face criticism due to their governance mechanism. Hence, this study anticipates to offer a comprehensive insight into SGR practiced by highly regulated IFIs, which will improve the overall image and reputation of IFIs.

This study has three distinct contributions to the literature on SGR of IBs. First, this research will assess SGR patterns of IBs which will determine the authenticity, validity, and accuracy of IFIs’ annual reports related to SG. Second, the empirical evidence of this study is constructed using a content analysis technique that is supported by logical and scientific reasoning. This will serve as a robust methodology for the future researchers considering to investigate the SGR of IFIs in a regulated environment. Third, the detailed analysis of SGR patterns, dimensions, themes, and differences will offer matrices for benchmarking by other IFIs to assess and restructure their SG frameworks according to globally accepted governance reporting standards. Fourth, an insight to SGR of IBs will allow regulators to reinstate the reputation of IFIs by overcoming transparency and governance issues which contributes to perpetual regulatory reforms.

The proceeding sections present a literature review in section two followed by the research methodology in section three. Section four discusses the major findings, and finally, this study is concluded in section five.

2. Literature review

2.1. SGR of IBs in Malaysia

The definitions of both SG and traditional corporate governance (CG) conforms to the globally accepted governance standards as outlined in Cadbury’s (Citation1992), which defined CG as “a system created to direct and control a company and the BODs are responsible for companies’ governance.” The shareholders appoint the directors and auditors to ensure an effective governance structure (Cadbury, Citation1992). In Malaysia, the rudiments of CG can be traced in the Malaysian Code of Corporate Governance (MCCG) issued in 2017 by the Securities Commission of Malaysia, which defined CG as, “the procedures and structure implemented for monitoring and managing a company’s business affairs in a way that it advances towards success and corporate accountability whose ultimate goals are to create sustainable value for shareholders and also safeguard the interest of stakeholders” (Securitties Commission [SC], Citation2017). CG of financial institutions in Malaysia is covered in the Guidelines on Corporate Governance for Licensed Institutions-2013 issued by Bank Negara Malaysia (BNM) (BNM, Citation2013).

Presently, there is no standardized definition of SG of IFIs in Malaysia due to disagreement among scholars on a single definition. IFSB’s guidelines on the SG system for institutions offering Islamic financial services defined it as the coordination between strategic roles and functioning of each governance organ and processes to balance the institutions offering Islamic financial services by holding them accountable to stakeholders (IFSB, Citation2009). SG of IFIs in Malaysia is supervised by BNM’s shariah advisory committee (SAC) that empowered SAC to overseas IFI’s compliance with shariah governance framework 2010 (SGF-10) (Haqqi, Citation2014; Uyob et al., Citation2022). A few common issues in the governance of IFIs in Malaysia were related to shariah non-compliance, funds disbursement without proper aqad, errors in profit calculation generated from customers exceeding banks sale price, rollover allowance, financing extensions without proper aqad, and inaccurate use of transaction documents for different shariah contracts (Ab Ghani et al., Citation2023; Ali & Hassan, Citation2020; Ginena, Citation2014; Syed Alwi et al., Citation2022).

2.2. Previous studies on SGR in Malaysia

The literature on SGR of IFIs in Malaysia can be divided into SGR and social reporting. A recent study (Shahar et al., Citation2020) investigated the difference between SGR of locally owned and foreign-owned IFIs and concluded that SGR is not influenced by institutional ownership. Sulaiman et al. (Citation2015) confirmed that the majority of IFIs concentrate on reporting traditional CG instead of SG due to the prevalence of low awareness of the benefits of SG reporting among the management. Another study consolidated that more than 50% IFIs in Malaysia lack the motivation to report SG information to the stakeholders (Amalina Wan Abdullah et al., Citation2013). The transparency level of IFIs’ SGR is significantly low and requires a proper disclosure mechanism (Besar et al., Citation2009; Hasan, Citation2010). A few studies have also examined other underlying features of SGR in IFIs (Abdul Rahman et al., Citation2010; Abu Kassim, Citation2012; Haniffa & Hudaib, Citation2007; Khan, Citation2013; Othman & Thani, Citation2010; Raman & Bukair, Citation2013).

The social and shariah disclosure of approved companies listed on Bursa Malaysia revealed that these companies disclose minimal information in their annual reports, which represent that despite an established narrative of accountability, these companies are less transparent in their SGR to the public (Othman & Thani, Citation2010). Another study on Bank Islamic Malaysia Berhad’s corporate social responsibility reporting found that the disclosure pattern of the bank had omitted several important themes such as information about impermissible transactions and abnormal supervisory restriction required by AAOIFI (Abdul Rahman et al., Citation2010). The analysis of shariah committee’s report on SG practices of IFIs found that these reports fail to offer a deeper insight of shariah compliance mechanism, substantially lack assurance, and were merely created to endorse shariah compliance instead of actually safeguarding the interest of stakeholders (Besar et al., Citation2009). The findings of SGR of Takaful companies in Malaysia concluded that generally, Takaful operators prioritize regulatory compliance over shariah compliance (Abu Kassim, Citation2012). However, progressive Takaful operators these days have started to focus on voluntary adoption of AAOIFI’s disclosure due to rising concerns of SG in IFIs (Mohd Zain et al., Citation2021). A few studies have also analyzed the impact of shariah committee composition, gender, and religious beliefs on SGR of IFIs and linked these to better SGR (Alazzani et al., Citation2019; Kamaruddin et al., Citation2023; Noordin & Kassim, Citation2019).

2.3. Studies related to SGR index

The past studies on SGR have used various themes and dimensions to develop the SGR index. The first disclosure index was developed in 2006 using social disclosure themes for IBs (Maali et al., Citation2006). Later, several robust and comprehensive SGR indices for IBs were developed by the researchers (Belal et al., Citation2015; Haniffa & Hudaib, Citation2007; Haqeem, Citation2019; Shahar et al., Citation2020, Srairi, Citation2015; Sulaiman et al., Citation2015).

The overview of these indices indicates that the first two indices were used as a benchmark by several studies in developing different disclosure indices (Albassam & Ntim, Citation2017; Amalina Wan Abdullah et al., Citation2013; Hassan & Syafri Harahap, Citation2010; Mallin et al., Citation2014). This research adopted the earlier developed indices as a benchmark and modified it to develop a relevant checklist for SGR of Malaysian IBs through an index. The dimensions and themes considered in this research also contain items of SGR promulgated by the notable standard setting bodies from conventional and Islamic backgrounds such as Global Reporting Initiative (GRI), BNM, Organization for Economic co-operation and Development (OECD), IFSB, AAOIFI. Additionally, several developing countries are yet to implement international standards such as GRI; hence, this study addresses this issue by incorporating these standards (Ahmad et al., Citation2021).

Despite ongoing discussion on the growth of IFIs through good governance, the actual indicators required for exceptional governance are lacking (Majid et al., Citation2011). Moreover, the existing SGR indices have used different guidelines, and the fact is IFIs prefer to use their local or their own distinct Islamic governance framework (Elamer et al., Citation2020; Shaharuddin & Rahim, Citation2020). Accordingly, from the Malaysian IFIs perspective, this study has selected six major dimensions to engage with annual reports through content analysis.

3. Research design

3.1. Data collection

Based on the objectives of this study, the philosophical foundation and organization of this study was designed through an explanatory and qualitative research approach. The primary data related to SGR were collected from the annual reports between 2014–2018. The use of yearly annual report will allow researchers to respond to the desired investigation pertaining to the SGR pattern, reported aspects of SG in the form of themes and dimensions, and track the periodic difference in SGR pattern among Malaysian IBs. Altogether, 80 annual reports (5 for each bank) were retrieved from the web portals of 16 IBs in Malaysia (see appendix A for sampled IBs). Traditionally, financial institutions use annual reports as a key reporting tool to disclose information related to socially responsible behavior (Ha, Citation2022). The studies on SGR of IFIs have used a similar content analysis technique to investigate SG practices and procedures through annual reports (Belal et al., Citation2015; Mallin et al., Citation2014). The underlying features of annual reports such as formal presentation of reporting process and diversity of content coverage such as social, environmental, and crucial organizational issues within the same document (Gray et al., Citation1995) had motivated the researchers to use this technique to examine SGR in IBs. Also, annual reports are largely used as a major analytical technique to prepare the external reports by the external accountants and auditors (Tilt, Citation1994); therefore, the ease of access and opportunity to obtain a consistent measure of SGR explains engaging annual reports as a source of primary data collection. Malaysian IBs are selected for the purpose of this study as the region has emerged as the hub for Islamic finance and numerous standard setting bodies and supportive organizations such as IFSB, International Shariah Research Academy for Islamic Finance (ISRA), and Islamic Banking and Finance Institute Malaysia (IBFIM) exist in this region. These standard setting bodies facilitate IBs’ operations through structured and procedural processes, which makes Malaysia an ideal geographical location to analyze the research in the Islamic financial sector.

3.2. Data analysis

The collected data are analyzed using the content analysis technique in NVivo software to generate SGR patterns of different IBs in Malaysia. Content analysis is considered reliable in generating elicit and meaningful outcomes of collected data (Bengtsson, Citation2016). However, it is essential for the researchers to identify external and internal sources to use for content analysis, and the researchers need to fully understand the concept under investigation so that personal bias does not influence the outcome (Bengtsson, Citation2016). The past studies have broadly exploited content analysis techniques to evaluate social and environmental disclosures of both conventional and IBs (Haniffa & Hudaib, Citation2007; Maali et al., Citation2006). Accordingly, this study advances and complements the data collection techniques of past studies by following the data analysis criteria of previous studies. Generally, content analysis refers to data collection techniques that involve coding qualitative information in anecdotal and literary form and classifying them into different quantitative scales of various levels of complexity (Abbott & Monsen, Citation1979). From an operational perspective, it represents the methods to code data into different categories based on earlier selected principles (Krippendorff, Citation1980; Weber, Citation1988). Hence, content analysis predominantly uses categories based on the previously established scales for classifying the content of units.

3.3. Validation of content analysis approach

The reliability and consistency of the data analysis technique (content analysis) were assured following Krippendorff’s (Citation2012) criteria. It is crucial to establish consistency and reliability in content analysis so that the coding approach is replicable for the use of other researchers. The reliability and consistency in the content analysis were achieved using four different measures. First, the researcher coded the same annual report twice at different time frames using a checklist (Microsoft excel) and the three-level structure sheet (Microsoft word) to confirm that the researchers fully understand the coding process. Second, testing and verifying the reliability of inter-code through experts with similar academic backgrounds and expertise in content analysis of the same annual report which is then compared with the researchers’ results. Additionally, the reliability of the intercoder is enhanced by giving a similar checklist of content analysis and three-level structure to another coder with no academic background and prior expertise in content analysis to test the clarity and feasibility of instructions. The second coder was provided one day of training prior to the analysis. The replicability assessment results of the content analysis method are reported below in Table .

Table 1. Coders’ information

The results in Table represent that the coder with prior experience and knowledge of coding procedure (coder 1) has 100% similarity with the researchers’ coding. Whereas, the second coder rating declined due to the lack of concentration, instead of misunderstanding the structure and instructions provided in the checklist. The variance in results was discussed with the second coder, and it was revealed that the coder fully understood the structure and the checklist after concentrating on the instructions. Third, determining the reliability and consistency through a pilot test which was conducted on 32 annual reports from the year 2014–2015 (16 banks x 2 years). These 16 banks were coded again on alternative dates, and a slight difference was adjusted to ensure the replicability of the method. Fourth, revaluation of the missing scores of the initially computed scores through the scoring sheet (Microsoft Excel and Word), which helped in adjusting inaccuracy of scores. Since this method involves a revaluation of the scores, therefore, efficiency and effectiveness are the major limitations. Despite these limitations, it is a robust method to generate relevant and reliable findings from content analysis.

3.4. Operational definitions of variables

The variables of this study are operationalized as multiple dimensions and sub-themes. The selection of dimensions and themes is a key to the content analysis process as it classifies and groups the content analysis information to interpret meaningful results. This study has selected six major dimensions (shariah committee with 14 themes, shariah review with 5 themes, shariah audit with 6 themes, shariah risk with 5 themes, overall transparency level with 11 themes, and investment account holders with 4 themes) and 45 sub-themes to develop a robust SGR index and analyze the reporting pattern of IBs for these dimensions and themes. These dimensions and themes were adopted and modified using earlier indices in the literature and considering SG reporting guidelines (governance of shariah committee for IFIs known as GPS1 and IFSB-10) promulgated by BNM and IFSB. Appendix B outlines the dimensions and themes selected to develop the SGR index for IBs in Malaysia. Selected dimensions and themes were coded using a dichotomous scale (0 and 1) following the criteria developed by previous studies on shariah and social reporting in IFIs (Belal et al., Citation2015; Haqeem, Citation2019). If the item is reported in sampled IBs’ annual report, it is coded as “1”, and the absence of the item was given a “0” score. The developed SGR index may obtain a maximum score of 45, and the index may range from 0 to 100%.

The index constructed through this process is considered unweighted as it signifies the equal role of each item. These unweighted scores are useful to examine the content of annual reports for all the users, which implies that the results of unweighted scores are not influenced by the perception of a certain group (Hossain & Hammami, Citation2009). The critics of unweighted indices highlighted that these measures only estimate the quality of the index, whereas the disclosure quantity is essential to represent the level of disclosure (Beretta & Bozzolan, Citation2008). Hence, the estimation of different levels of the disclosure can be measured by weighted indices as used in this study. Ironically, weighted scores have also received criticism due to their objective nature and predetermined method of assigning weights based on the users’ perception and understanding of the items (Beretta & Bozzolan, Citation2008). The findings of studies that adopted weighted and unweighted scores show that there were no significant differences in estimating disclosure indices, even though some studies found similar results using both methods (Hossain & Hammami, Citation2009). The index is estimated through a ratio of score awarded over the total number of selected dimensions, which is represented as follows;

Where;

SGR represents shariah governance reporting;

jt = SGR for dimension/theme j and period t;

Xijt = Variable X from 1 up to n for dimension j and time t;

N = Number of variables/statements.

4. Empirical findings and discussion

4.1. Descriptive statistics

The descriptive statistics of the SGR index are presented in Table . These results indicate that pooled IBs obtained a minimum score of 12 and a maximum score of 29 confirming that the lowest SGR score was approximately 26% (Items reported in annual reports of IBs/Total items used for creating index × 100) (12/45 × 100 = 26) and the highest score was 64% (29/45 × 100 = 64). While the mean score was 27, establishing that on average, IBs reported more than 60% (27/45 × 100 = 60) information related to SG, which is an indicator of “good reporting” (Sulaiman et al., Citation2015).

Table 2. Descriptive statistics of SGR index

4.2. Overview of SGR index

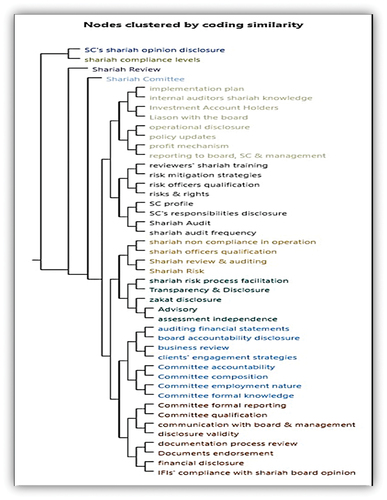

Before presenting the overview of the SGR index, it is essential to analyze the reliability of data sets to explore whether the dimensional and thematic layers are strongly interrelated with each other. This is measured by estimating the Jaccard coefficient whose values range from 0% to 100% (Agresti, Citation1990). The higher percentage determines the stronger inter correlation between the dimensions and themes. Figure presents the results of the Jaccard coefficient are presented in Figure .

Figure 1. Clustered overview of dimensions and themes.

The findings in Figure indicate that the dimensions and themes of SGD are strongly correlated with each other as the Jaccard coefficient varies from 0.56 to 1 (56% to 100%). This also confirms that all the layers of dimensions and themes are a reliable measure of SGR for IBs in Malaysia.

The distribution of SGR dimensions is analyzed by estimating the mind maps which generate the overview of content coverage for the dimensions of SGR. The overview of these dimensions is presented in Figure .

Figure 2. Dimensions segmental overview.

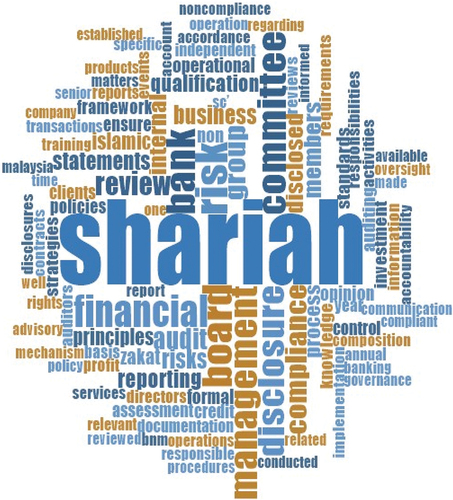

Figure presents an overview of the reporting coverage for all six dimensions (shariah committee, shariah review, shariah audit, shariah risk, overall transparency, and investment account holders) of SGR. It is notable that the majority of IBs have disclosed all the dimensions of SGR used in this study. However, Affin bank, Alliance bank, Alrajhi bank, and HSBC Amanah Malaysia Berhad have not reported all the dimensions of SGR. This finding is consistent with the findings of past studies (Belal et al., Citation2015; Haqeem, Citation2019; Shahar et al., Citation2020) establishing that regardless of ownership (foreign and local), IBs practice a consistent SGR mechanism. However, the findings contradict the study of Sulaiman et al. (Citation2015) reinforcing that IBs prioritize disclosure of specific CG. The results of this study confirm that SGR is the first priority and the majority of dimensions are disclosed by most of the IBs. The dominance of SG reporting was further verified by analyzing the word frequency of the sampled data. The results of word frequency are reported in Figure .

Figure 3. Estimating SGR trends of IBs in Malaysia.

The findings in Figure delineate that shariah reporting dominates the overall SGR trends of Malaysian IBs. Similarly, other dominant dimensions and themes dominated in reporting were related to “shariah committee,” “shariah compliance,” “board responsibility,” “financial reporting,” and “Shariah disclosure”. Also, the majority of the dimensions and themes used in this study are loaded in the SGR of sampled IBs.

4.3. Thematic overview of SGR

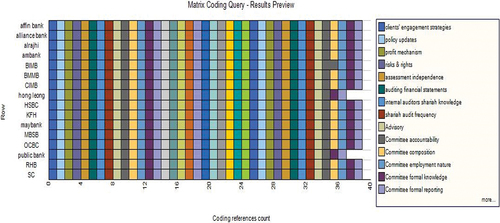

The thematic overview analyses the reporting coverage for the themes selected in this study. Comparatively, themes provide a deeper overview of the SGR by IBs which complement the dimensional maps. The overview of thematic reporting is presented in Figure .

Figure 4. Thematic reporting maps of IBs.

The thematic maps represent that majority of IBs have reported all the themes of SGR except Hong Leong Islamic Bank Berhad and Public Islamic Bank Berhad. The proposed themes in the segmental map reveal interesting trends and information related to SGR. The segmental map highlights that IBs have fairly reported the required SG information; however, the reporting pattern is uniform and follows a similar disclosure sequence, and it is less scattered as compared to the dimensional maps. This indicates that Malaysian IBs follow a similar reporting mechanism for the themes identified under each dimension of SGD. This finding is consistent with the past study of Amalina Wan Abdullah et al. (Citation2013) indicating that based on the SG reporting index, Malaysian IBs’ SGR was above average. Hence, it is crucial that all IBs follow similar reporting trends for the success of the Islamic banking industry and validate the position of Malaysia as an Islamic finance hub. This result contradicts the findings of previous studies (Besar et al., Citation2009; Hasan, Citation2010) revealed that the level of SGR in Malaysia is substantially low. This difference can be explained by the argument that with the passage of time, the development of regulatory frameworks guided by the fears of possible recession has forced IBs to implement stringent governance measures and practice total disclosure.

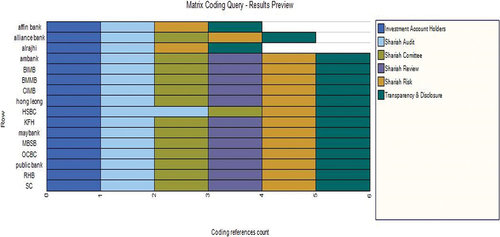

4.4. Broad-spectrum results of dimensions’ reporting

The distribution of different dimensions across SGR is analyzed by estimating the matrices coding for each dimension which will provide a better overview of disclosure by IBs. The results of matrices coding for each dimension are presented in Table .

Table 3. Coding matrix results of SGR index dimensions

The findings in Table indicate the coding matrix results for the dimensions of the SGR index. The minimum score for “shariah committee” was 13 (29%), the maximum was 17 (38%), and the mean score was 19 (42%). This represents that Malaysian IBs reported below average information about functions and operations of shariah committee in IBs which may escalate compliance issues and have a negative impact on investors’ interest (Hasan, Citation2010; Syed Alwi et al., Citation2022). Alternatively, the lack of Shariah committee reporting will further worsen the controversies associated with IBs’ shariah compliance (Aziz et al., Citation2019). Even though the lack of shariah committee reporting has no direct influence on consumers such as on the selection of Islamic mode of financing (Shafii et al., Citation2013), the elements of justice in partnership financing contracts may further become agile due to fears of contamination of interest elements (Anwar, Citation2003; Usmani, Citation2004).

The findings of “shariah review” indicate that the minimum score obtained from the coding matrix of “shariah review” reporting was 7 (16%), the maximum was 28 (62%), and the mean score was 14 (31%), indicating that “shariah review” reporting was above average. This result was expected as Malaysian IBs have significantly improved their governance structure by implementing regulatory frameworks such as Islamic Financial Services Act (IFSA) 2013, which provides a new legal pathway for IBs to ensure Shariah compliance in business operation and demand IBs to fulfill these legal requirements (Aziz et al., Citation2019). Similarly, coding matrices for “shariah audit” reporting had a minimum score of 6 (13%), maximum of 12 (28%), and mean was 14 (31%), representing that shariah audit dimension’s reporting was also below average. This finding is consistent with several past studies which concluded that Malaysian IBs face shariah compliance issues due to a lack of competency and independence. Therefore, there is an urgent need to train auditors to conduct a holistic shariah audit (Ali et al., Citation2015; Salleh et al., Citation2019; Shafii et al., Citation2014).

The findings pertaining to “shariah risk” reporting had a minimum score was 10 (22%), maximum of 32 (71%), and mean was 15 (33%), establishing that “shariah risk” reporting of IBs in Malaysia was above average. This finding advance that IBs these days have established several governance layers to lower the shariah non-compliance risks guided by the effective functions of the Shariah committee, which prohibit IBs to involve in gharar, gambling, and excessive risk-taking (Mollah & Zaman, Citation2015; Nomran & Haron, Citation2019). Furthermore, this finding indicates that IBs with lower Shariah risk disclosure levels may fail to establish legitimacy and strengthen their organizational culture, which is a key indicator of risk mitigation strategies (Khan et al., Citation2017).

Moving on to the results of “overall transparency” reporting, it is notable that the minimum score of coding matrices was 4 (9%), maximum 13 (29%), and mean was 15 (4%), indicating that the “overall transparency” reporting was below average. Iits a proven fact that IBs need to establish transparent SGD frameworks to achieve social, economic, governance, and legal objectives (Hidayat & Al-Khalifa, Citation2018). This finding indicates that IBs in Malaysia are yet to grab the low-hanging fruits of SGR by implementing transparency & disclosure in its practices. These results would draw policymakers’ attention to impose further regulations and encourage Malaysian IBs to adopt sophisticated jurisdictions to ensure the growth of a rapidly evolving industry (Hasan, Citation2011). Additionally, past studies of Masruki et al. (Citation2020), and Hassan and Christopher (Citation2005) have also confirmed that Malaysian IBs are less likely to report complete information about overall transparency practices. These low levels of transparency in reporting coupled with customers’ low level of trust in certain aspects of Islamic banking could be a recipe for a disaster in the Malaysian Islamic banking industry (Ab Ghani et al., Citation2023; Satkunasingam & Shanmugam, Citation2004). Indeed, IBs are required to practice transparency in reporting so that their religious reputations, institutional purpose, and customers’ trust is restored (Elamer et al., Citation2020).

Finally, the results of “investment account holders” dimension minimum score were 6 (13%), maximum 20 (44%), and mean score was 25 (56%), confirming that “investment account holders” reporting was below average. This finding indicates that lower reporting of investment account holders and risks of shariah non-compliance arise due to IBs’ management of these accounts, and continuation of such practices are likely to further undermine the business and financial dealings transparency (Rosman et al., Citation2017).

4.5. SGR comparison between IBs

Prior to examining the SGR difference between IBs, it is mandatory to test the data normality so that appropriate statistical technique, such as parametric and/or non-parametric, is applied. The distribution of data among different banks are estimated by drawing a histogram, indicating an abnormal distribution of data on both sides of the histogram, which was further verified through Skewness-kurtosis and Shapiro-Wilk W tests. Skewness-Kurtosis test was performed to estimate the sum of prob>chi2, and the values for all the dimensions were below 0.05, confirming data abnormality. The results of the Shapiro-Wilk test also indicated an abnormal distribution of data, establishing that non-parametric technique [(Wilcoxon rank-sum (Mann-Whitney)] is relevant to explore the SGR difference between IBs. The results of the Wilcoxon rank sum (Mann-Whitney) are presented in Table .

Table 4. Results of Mann-Whitney and two sample t test

Table indicate that all the prob>|z| values are less than 0.05 criteria, which confirms that SGR differs between IBs in Malaysia for all the dimensions. This finding provides empirical evidence that the majority of IBs in Malaysia have different reporting levels for each dimension of SGR. However, it is essential to analyze the actual reporting levels of SGR for each bank to rank IBs with high performance in terms of reporting.

The actual difference was computed by performing a percentage coverage test for individual banks in NVivo which offered an insight of statistical difference for ranking the top performers of SGR. Table presents the overview of the top 10 performers of SGR.

Table 5. Ranking top 10 performing IBs in the SGR

Table represents interesting findings as the pioneer IBs such as Bank Islamic Malaysia Berhad (BIMB) and Bank Muamalat Malaysia Berhad are ranked on 10th and 9th position based on SGR. However, other fully fledged IBs such as Kuwait Finance House (Malaysia) Berhad and MBSB Bank Berhad are ranked on 2nd and 3rd position. This finding indicates that the index scoring is systematic and in line with the literature as it replaced the volume and quantified the reporting to represent the performance (Krippendorff, Citation2012). This can be justified from the findings presented in Table as the reporting variance between scores of SGR has a uniform pattern. However, the existing variance in the actual scores confirms that large discrepancies exist and need further explanation to reinforce the findings. Additionally, this finding also authenticates the consistency of IBs in Malaysia towards SGR. However, one might argue on the statistical proportion of reporting (lower levels); yet, this finding is reliable as the developed index considered checklist adopted from the previous studies (Belal et al., Citation2015; Haniffa & Hudaib, Citation2007; Maali et al., Citation2006). The checklist items also incorporated the elements from reputable regulatory bodies such as Bank Negara Malaysia (BNM) and Islamic Financial Services Board (IFSB), which indicates that the index represents the SGR practices in Malaysia and the findings are actual representative of IBs in Malaysia.

5. Summary and conclusion

The debate on SGR of IBs is ongoing and continue fascinating regulators, policymakers, and customers due to difference in SR mechanisms and patterns. Therefore, it is timely to investigate the SGR of Malaysian IBs which are popular due to their highly regulated regimes. Accordingly, this study examined the SGR patterns of these IBs using a reporting index comprised of various dimensions and themes. We used self-designed reporting index to analyze the SGR pattern of each IB as well as explored the underlying differences in reporting among IBs. The results of this study are derived employing various analytical, scientific, and statistical techniques.

The results of this study concluded that sampled IBs have reported more than 60% information related to SG, which is an indicator of good reporting. The shariah reporting dominates in the overall reporting trends of SGR. The mind maps revealed that all six dimensions (shariah committee, shariah review, shariah audit, shariah risk, overall transparency, and investment account holders) of SGR were reported by all IBs; however, the reporting pattern was more scattered as compared to the thematic reporting pattern. The reporting patterns of dimensions further revealed that IBs in Malaysia have reported above average information of shariah review and shariah risk, whereas IBs have reported below average information regarding shariah committee, shariah audit, overall transparency, and investment account holders. The results have also confirmed the statistical differences in SGR among sampled IBs.

5.1. Implications for practice

The findings of this study offer several managerial and policy implications. First, the SGR insight offered in this study may facilitate the managers, board of directors, shariah committee members, shariah reviewers, and auditors to encourage IBs to improve the mechanisms of SGR in their annual reports. Second, the regulators of the Islamic financial industry in Malaysia, such as BNM and IFSB, may develop stringent and robust regulatory frameworks to essentialize SGR which will require IBs to practice full disclosure of different dimensions as proposed in this study. Third, the regulators of the Islamic financial industry may encourage IBs to participate in the global initiatives and comply with the global reporting standards established by other institutions such as AAOIFI. This will improve the SG frameworks of IBs as well as preserve the reputation of the Islamic banking brand. Fourth, the proposed SGR in this study may be used as a benchmark for training IBs concerned with improving SGR. This will bridge the elongated human skill gaps in the Islamic financial industry of Malaysia. Finally, the insight offered in this study may be used as a case study by the managers to conduct inter- and intra-sectional training of the managers such as Shariah officers, audit officers, and risk officers. This will ensure the consistent commitment of IFIs to improve the governance at the institutional level.

5.2. Limitations and future research

Like any other empirical study, the current research also has several limitations and constraints that occurred due to numerous factors which should be resolved by future studies. These limitations were related to the period of study, extension, and harmonization of the SGR checklist, analytical techniques to estimate the SGR of individual a bank, sampling and data collection procedures through annual reports, graphical displays of the findings. Future researchers may consider selecting wider time coverage such as 15 years, or perhaps before the introduction of SG regulating frameworks, which will diversify the findings and represent the actual SGR of IBs. Future studies may consider engaging additional dimensions like the board of directors and CEOs to offer a wider prospect of SGR. The diversification of data collection through interviews and observations should be considered by future studies to develop a more logical explanation of the difference in SGR pattern among IBs. Lastly, future researchers are recommended to use a combination of graphical and statistical techniques to gain a better insight into SGR patterns and differences among IBs.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abbott, W. F., & Monsen, R. J. (1979). On the measurement of corporate social responsibility: Self-reported disclosures as a method of measuring corporate social involvement. Academy of Management Journal, 22(3), 501–20. https://doi.org/10.2307/255740

- Abdullah Saif Alnasser, S., & Muhammed, J. (2012). Introduction to corporate governance from Islamic perspective. Humanomics, 28(3), 220–231. https://doi.org/10.1108/08288661211258110

- Abdul Latif, R., Taufil Mohd, K. N., Kamardin, H., & Mohd Ariff, A. H. (2023). Determinants of sustainability disclosure quality among plantation companies in Malaysia. Sustainability, 15(4), 3799. https://doi.org/10.3390/su15043799

- Abdul Rahman, A., Hashim, M. F. A. M., & Abu Bakar, F. (2010). Corporate social reporting: A preliminary study of Bank Islam Malaysia Berhad (BIMB). Issues in Social and Environmental Accounting, 4(1), 18–39. https://doi.org/10.22164/isea.v4i1.45

- Ab Ghani, N. L., Mohd Ariffin, N., & Abdul Rahman, A. R. (2023). The extent of mandatory and voluntary shariah compliance disclosure: Evidence from Malaysian Islamic financial institutions. Journal of Islamic Accounting and Business Research. https://doi.org/10.1108/JIABR-10-2021-0282

- Abu Kassim, N. A. (2012). Disclosure of shariah compliance by Malaysian takaful companies. Journal of Islamic Accounting and Business Research, 3(1), 20–38. https://doi.org/10.1108/17590811211216041

- Agresti, A. (1990). Categorical data analysis. John Wiley and Sons.

- Ahmad, S., Akbar, S., Halari, A., & Shah, S. Z. (2021). Organizational non-compliance with principles-based governance provisions and corporate risk-taking. International Review of Financial Analysis, 78, 101884. https://doi.org/10.1016/j.irfa.2021.101884

- Alam, M. K., Ahmad, A. U. F., Muneeza, A., Tabash, M. I., & Rahman, M. A. (2022). Proposing an organizational framework for the Sharīʿah Secretariat of Islamic banks in Bangladesh. ISRA International Journal of Islamic Finance, 14(1), 107–118. https://doi.org/10.1108/IJIF-03-2021-0046

- Alazzani, A., Wan-Hussin, W. N., & Jones, M. (2019). Muslim CEO, women on boards and corporate responsibility reporting: Some evidence from Malaysia. Journal of Islamic Accounting and Business Research, 10(2), 274–296. https://doi.org/10.1108/JIABR-01-2017-0002

- Albassam, W. M., & Ntim, C. G. (2017). The effect of Islamic values on voluntary corporate governance disclosure: The case of Saudi-listed firms. Journal of Islamic Accounting and Business Research, 8(2), 182–202. https://doi.org/10.1108/JIABR-09-2015-0046

- Ali, M. M., & Hassan, R. (2020). Survey on sharīʿah non-compliant events in Islamic banks in the practice of tawarruq financing in Malaysia. ISRA International Journal of Islamic Finance, 12(2), 151–169. https://doi.org/10.1108/IJIF-07-2018-0075

- Ali, N. A. M., Mohamed, Z. M., Shahimi, S., & Shafii, Z. (2015). Competency of shariah auditors in Malaysia: Issues and challenges. Journal of Islamic Finance, 4(1), 22–30. https://doi.org/10.12816/0024798

- Amalina Wan Abdullah, W., Percy, M., & Stewart, J. (2013). Shari’ah disclosures in Malaysian and Indonesian Islamic banks: The Shari’ah governance system. Journal of Islamic Accounting and Business Research, 4(2), 100–131. https://doi.org/10.1108/JIABR-10-2012-0063

- Amin, M. N. A., Mohd Ariffin, N., & Fatima, A. H. (2021). Shariah disclosure practices in Malaysian Islamic banks using the shariah disclosure index. International Journal of Islamic Economics and Finance, 4(SI). https://doi.org/10.18196/ijief.v4i0.9953

- Anwar, M. (2003). Islamicity of banking and modes of Islamic banking. Arab Law Quarterly, 18(1), 62–80. https://doi.org/10.1163/026805503773081735

- Aziz, R. A., Abdul-Rahman, A. I. S. Y. A. H., & Markom, R. (2019). Best practices for internal shariah governance framework: Lessons from Malaysian Islamic banks. Asian Journal of Accounting & Governance, 12, 37–49. https://doi.org/10.17576/AJAG-2019-12-15

- Bank Negara Malaysia. (2023). Financial sector participant directory. Retrieved May 23, 2023, from https://www.bnm.gov.my/regulations/fsp-directory?p_p_id=com_liferay_asset_publisher_web_portlet_AssetPublisherPortlet_INSTANCE_jXC730NRlqU0&p_p_lifecycle=0&p_p_state=normal&p_p_mode=view&p_r_p_tag=islamic-bank

- Bank Negara Malaysia, BNM. 2013. Guidelines on corporate governance for licensed institutions. Retrieved October 13, 2021, from http://www.bnm.gov.my/guidelines/01_banking/04_prudential_stds/16_corporate_governance.pdf

- Beattie, V., & Jones, M. J. (2002). The impact of graph slope on rate of change judgments in corporate reports. Abacus, 38(2), 177–199. https://doi.org/10.1111/1467-6281.00104

- Belal, A. R., Abdelsalam, O., & Nizamee, S. S. (2015). Ethical reporting in islami bank Bangladesh limited (1983–2010). Journal of Business Ethics, 129(4), 769–784. https://doi.org/10.1007/s10551-014-2133-8

- Bengtsson, M. (2016). How to plan and perform a qualitative study using content analysis. NursingPlus Open, 2, 8–14. https://doi.org/10.1016/j.npls.2016.01.001

- Beretta, S., & Bozzolan, S. (2008). Quality versus quantity: The case of forward-looking disclosure. Journal of Accounting, Auditing & Finance, 23(3), 333–376. https://doi.org/10.1177/0148558X0802300304

- Besar, M. H. A. H., Sukor, M. E. A., Muthalib, N. A., & Gunawa, A. Y. (2009). The practice of shariah review as undertaken by Islamic banking sector in Malaysia. International Review of Business Research Papers, 5(1), 294–306.

- Cadbury, S. A. (1992). Report of the committee on the financial aspects of corporate governance. Professional Publishing:

- Darmadi, S. (2011). Corporate governance disclosure in the annual report: An exploratory study on Indonesian Islamic banks. Indonesian College of State Accountancy.

- Elamer, A. A., Ntim, C. G., & Abdou, H. A. (2020a). Islamic governance, national governance, and bank risk management and disclosure in MENA countries. Business & Society, 59(5), 914–955. https://doi.org/10.1177/0007650317746108

- Elamer, A. A., Ntim, C. G., Abdou, H. A., & Pyke, C. (2020b). Sharia supervisory boards, governance structures and operational risk disclosures: Evidence from Islamic banks in MENA countries. Global Finance Journal, 46, 100488. https://doi.org/10.1016/j.gfj.2019.100488

- Elghuweel, M. I., Ntim, C. G., Opong, K. K., & Avison, L. (2017). Corporate governance, Islamic governance and earnings management in Oman: A new empirical insights from a behavioural theoretical framework. Journal of Accounting in Emerging Economies, 7(2), 190–224. https://doi.org/10.1108/JAEE-09-2015-0064

- Fatmawati, D., Ariffin, N. M., Abidin, N. H. Z., & Osman, A. Z. (2022). Shariah governance in Islamic banks: Practices, practitioners and praxis. Global Finance Journal, 51, 100555. https://doi.org/10.1016/j.gfj.2020.100555

- Ferriswara, D., Sayidah, N., & Agus Buniarto, E. (2022). Do corporate governance, capital structure predict financial performance and firm value?(empirical study of Jakarta Islamic index). Cogent Business & Management, 9(1), 2147123. https://doi.org/10.1080/23311975.2022.2147123

- Garas, S. N. (2010). The performance of Shari’a supervisory boards within Islamic financial institutions in the Gulf cooperation council countries. Corporate Ownership & Control, 8(1), 247–266. https://doi.org/10.22495/cocv8i1c2p1

- Garas, S. N. (2012). The conflicts of interest inside the shari’a supervisory board. International Journal of Islamic & Middle Eastern Finance & Management, 5(2), 88–105. https://doi.org/10.1108/17538391211233399

- Garas, S. N., & Pierce, C. (2010). Shari’a supervision of Islamic financial institutions. Journal of Financial Regulation & Compliance, 18(4), 386–407. https://doi.org/10.1108/13581981011093695

- Ginena, K. (2014). Sharı‘ah risk and corporate governance of Islamic banks. Corporate Governance the International Journal of Business in Society, 14(1), 86–103. https://doi.org/10.1108/CG-03-2013-0038

- Ginena, K., & Hamid, A. (2015). Foundations of shariah governance of Islamic banks. Wiley. https://doi.org/10.1002/9781119053507

- Gray, R., Kouhy, R., & Lavers, S. (1995). Methodological themes: Constructing a Research database of social and environmental reporting by UK companies. Accounting Auditing & Accountability Journal, 8(2), 78–101. https://doi.org/10.1108/09513579510086812

- Ha, H. H. (2022). Audit committee characteristics and corporate governance disclosure: Evidence from Vietnam listed companies. Cogent Business & Management, 9(1), 2119827. https://doi.org/10.1080/23311975.2022.2119827

- Hameed, S., & Pramono, S. (2005). Analysis of corporate governance disclosure in Islamic commercial banks’ annual reports: a comparative study of Islamic commercial banks in Malaysia and Indonesia. Paper presented at Accounting, Commerce and Finance: The Islamic Perspective Conference, Jakarta, Indonesia, 29-31 March.

- Haniffa, R., & Hudaib, M. (2007). Exploring the ethical identity of Islamic banks via communication in annual reports. Journal of Business Ethics, 76(1), 97–116. https://doi.org/10.1007/s10551-006-9272-5

- Haqeem, A. A. G. (2019). An empirical Examination into the social reporting practices of Islamic banks in Malaysia and Bahrain. Durham University, Retrieved October 4, 2021, from http://etheses.dur.ac.uk/13109/.

- Haqqi, A. R. A. (2014). Shariah governance in Islamic financial institution: An appraisal. US-China Literature Review, 121–124.https://heinonline.org/HOL/LandingPage?handle=hein.journals/uschinalrw11&div=8&id=&page=

- Hasan, Z. (2010). Regulatory framework of shariah governance system in Malaysia, GCC countries and the UK. Kyoto Bulletin of Islamic Area Studies, 3(2), 82–115.

- Hasan, Z. (2011). A survey on Shari’ah governance practices in Malaysia, GCC countries and the UK: Critical appraisal. International Journal of Islamic & Middle Eastern Finance & Management, 4(1), 30–51. https://doi.org/10.1108/17538391111122195

- Hassan, S., & Christopher, T. (2005). Corporate governance statement disclosure of Malaysian banks and the role of Islam. Asian Review of Accounting, 13(2), 36–50. https://doi.org/10.1108/eb060786

- Hassan, A., & Syafri Harahap, S. (2010). Exploring corporate social responsibility disclosure: The case of Islamic banks. International Journal of Islamic & Middle Eastern Finance & Management, 3(3), 203–227. https://doi.org/10.1108/17538391011072417

- Hidayat, S. E., & Al-Khalifa, A. K. (2018). Shariah governance practices at Islamic banks in Bahrain from Islamic bankers’ perspective. Al-Iqtishad: Journal of Islamic Economics, 10(1), 53–74. https://doi.org/10.15408/aiq.v10i1.5991

- Hossain, M., & Hammami, H. (2009). Voluntary disclosure in the annual reports of an emerging country: The case of Qatar. Advances in Accounting, 25(2), 255–265. https://doi.org/10.1016/j.adiac.2009.08.002

- Hussain, A., Khan, M., Rehman, A., Sahib Zada, S., Malik, S., Khattak, A., & Khan, H. (2021). Determinants of Islamic social reporting in Islamic banks of Pakistan. International Journal of Law and Management, 63(1), 1–15. https://doi.org/10.1108/IJLMA-02-2020-0060

- Islamic Financial Services Board, IFSB. (2009). IFSB-10: Guiding principles on shariah governance Systems for institutions offering Islamic financial Services. Islamic Financial Services Board (IFSB). Retrieved September 13, 2021, from http://www.ifsb.org/standard/IFSB10%20Shariah%20Governance.pdf

- Kamaruddin, M. I. H., Shafii, Z., Hanefah, M. M., Salleh, S., & Zakaria, N. (2023). Exploring shariah audit practices in zakat and waqf institutions in Malaysia. Journal of Islamic Accounting and Business Research. https://doi.org/10.1108/JIABR-07-2022-0190

- Kamla, R., & Rammal, H. G. (2013). Social reporting by Islamic banks: Does social justice matter? Accounting Auditing & Accountability Journal, 26(6), 911–945. https://doi.org/10.1108/AAAJ-03-2013-1268

- Kamla, R., & Roberts, C. (2010). The global and the local: Arabian Gulf states and imagery in annual reports. Accounting Auditing & Accountability Journal, 23(4), 449–481. https://doi.org/10.1108/09513571011041589

- Kasim, N., Htay, S. N. N., & Salman, S. A. (2013). Conceptual framework for Shari’ah corporate governance with special focus on Islamic capital market in Malaysia. International Journal of Trade, Economics and Finance, 4(5), 336. https://doi.org/10.7763/IJTEF.2013.V4.312

- Khan, M. M. (2013). Developing a conceptual framework to appraise the corporate social responsibility performance of Islamic banking and finance institutions. Accounting and the Public Interest, 13(1), 191–207. https://doi.org/10.2308/apin-10375

- Khan, I., Khan, M., & Tahir, M. (2017). Performance comparison of Islamic and conventional banks: Empirical evidence from Pakistan. International Journal of Islamic & Middle Eastern Finance & Management, 10(3), 419–433. https://doi.org/10.1108/IMEFM-05-2016-0077

- Krippendorff, K. (1980). Content analysis: An introduction to its methodology. Sage.

- Krippendorff, K. (2012). Content analysis: An introduction to its methodology (4th ed.). SAGE Publications.

- Laldin, M. A., & Furqani, H. (2018). Islamic Financial Services Act (IFSA) 2013 and the Sharīʿah-compliance requirement of the Islamic finance industry in Malaysia. ISRA International Journal of Islamic Finance, 10(1), 94–101. https://doi.org/10.1108/IJIF-12-2017-0052

- Maali, B., Casson, P., & Christopher, N. (2006). Social reporting by Islamic banks. Abacus, 42(2), 266–289. https://doi.org/10.1111/j.1467-6281.2006.00200.x

- Majid, N. A., Sulaiman, M., & Ariffin, N. M. (2011). Developing a corporate governance disclosure index for Islamic financial institutions. In Paper presented at the 8th International Conference on Islamic Economics and Finance. Islamic Research and Training Institute (IRTI).

- Malaysia, B. (2022). Islamic capital market market in Malaysia. Bursa Digital Research. Retrieved June 15, 2023, from https://www.bursamalaysia.com/sites/5bb54be15f36ca0af339077a/content_entry617bfd1939fba20f54a06543/62df4aad5b711a425737fd44/files/July_26_Market_Updates_-_Islamic_Capital_Market_in_Malaysia.pdf?1658808173

- Mallin, C., Farag, H., & Ow-Yong, K. (2014). Corporate social responsibility and financial performance in Islamic banks. Journal of Economic Behavior & Organization, 103, 21–38. https://doi.org/10.1016/j.jebo.2014.03.001

- Masruki, R., Hanefah, M. M., & Dhar, B. K. (2020). Shariah governance practices of Malaysian Islamic banks in the light of shariah compliance. Asian Journal of Accounting & Governance, 13, 91–97. https://doi.org/10.17576/AJAG-2020-13-08

- Mohd Zain, F. A., Wan Abdullah, W. A., & Percy, M. (2021). Voluntary adoption of AAOIFI disclosure standards for takaful operators: The role of governance. Journal of Islamic Accounting and Business Research, 12(4), 593–622. https://doi.org/10.1108/JIABR-08-2018-0119

- Mollah, S., & Zaman, M. (2015). Shari’ah supervision, corporate governance and performance: Conventional vs. Islamic banks. Journal of Banking & Finance, 58, 418–435. https://doi.org/10.1016/j.jbankfin.2015.04.030

- Muhammad, R., Azlan Annuar, H., Taufik, M., Nugraheni, P., & Ntim, C. G. (2021). The influence of the SSB’s characteristics toward sharia compliance of Islamic banks. Cogent Business & Management, 8(1), 1929033. https://doi.org/10.1080/23311975.2021.1929033

- Mukhibad, H., Yudo Jayanto, P., Suryarini, T., & Bagas Hapsoro, B. (2022). Corporate governance and Islamic bank accountability based on disclosure—A study on Islamic banks in Indonesia. Cogent Business & Management, 9(1), 2080151. https://doi.org/10.1080/23311975.2022.2080151

- Nomran, N. M., & Haron, R. (2019). Dual board governance structure and multi-bank performance: A comparative analysis between Islamic banks in Southeast Asia and GCC countries. Corporate Governance the International Journal of Business in Society, 19(6), 1377–1402. https://doi.org/10.1108/CG-10-2018-0329

- Noordin, N. H., & Kassim, S. (2019). Does shariah committee composition influence shariah governance disclosure? Evidence from Malaysian Islamic banks. Journal of Islamic Accounting and Business Research, 10(2), 158–184. https://doi.org/10.1108/JIABR-04-2016-0047

- Othman, R., & Thani, A. (2010). Islamic social reporting of listed companies in Malaysia. International Business & Economics Research Journal, 9(4), 135–144. https://doi.org/10.19030/iber.v9i4.561

- Pramono, S. (2005). Corporate governance disclosure in Islamic commercial banks’ annual reports: A comparative study of Islamic commercial banks in Malaysia and Indonesia [ Unpublished Masters Thesis]. International Islamic University Malaysia.

- Preston, A. M., Wright, C., & Young, J. J. (1996). Magining annual reports. Accounting, Organizations & Society, 21(1), 113–137. https://doi.org/10.1016/0361-3682(95)00032-5

- Raman, A. A., & Bukair, A. A. (2013). The influence of the shariah supervision board on corporate social responsibility disclosure by Islamic banks of Gulf Co-operation council countries. Asian Journal of Business and Accounting, 6(2), 65–106.

- Rosman, R., Azmi, A. C., & Amin, S. N. (2017). Disclosure of Shari’ah non-compliance income by Islamic banks in Malaysia and Bahrain. International Journal of Business and Society, 18(1), 45–58.

- Salleh, S., Hanefah, M., Shafii, Z., & Kamaruddin, M. I. H. (2019). Shariah audit practices in Malaysian Islamic banks: An audit expectation-performance gap analysis. In Mohd Hanefah, M., & Kamaruddin, M.I.H. (Eds.), Shariah governance and assurance in Islamic financial sectors (pp. 113–145). USIM Press.

- Satkunasingam, E., & Shanmugam, B. (2004). Disclosure and governance of Islamic banks: A case study of Malaysia. Journal of International Banking Regulations, 6(1), 69–81. https://doi.org/10.1057/palgrave.jbr.2340182

- Securitties Commission. (2017). Malaysian Code on Corporate Governance 2017 (MCCG 2017). Securities Commission of Malaysia (SC): Kuala Lumpur. Retrieved October 11, 2021, from https://www.sc.com.my/wp-content/uploads/eng/html/cg/mccg2017.pdf

- Shafii, Z., Abidin, A. Z., Salleh, S., Jusoff, K., & Kasim, N. (2013). Post implementation of shariah governance framework: The impact of shariah audit function towards the role of shariah committee. Middle East Journal of Scientific Research, 13, 7–11. https://doi.org/10.5829/idosi.mejsr.2013.13.1874

- Shafii, Z., Ali, N. A. M., & Kasim, N. (2014). Shariah audit in Islamic banks: An insight to the future shariah auditor labour market in Malaysia. Procedia-Social & Behavioral Sciences, 145, 158–172. https://doi.org/10.1016/j.sbspro.2014.06.023

- Shahar, N. A., Nawawi, A., & Salin, A. S. A. P. (2020). Shari’a corporate governance disclosure of Malaysian IFIS. Journal of Islamic Accounting and Business Research, 11(4), 845–868. https://doi.org/10.1108/JIABR-05-2016-0057

- Shaharuddin, N. S., & Rahim, M. A. (2020). Shariah governance disclosure index: An ideal indicator for Islamic financial institutions. Proceedings of the 4th ICSSED International Conference of Social Science and Education. Sciendo.

- Srairi, S. (2015). Corporate governance disclosure practices and performance of Islamic banks in GCC countries. Journal of Islamic Finance, 4(2), 001–017.

- Sulaiman, M., Abd Majid, N., & Ariffin, N. M. (2011). Corporate governance of Islamic financial institutions in Malaysia. In Paper presented at the Proceedings of the 8th International Conference on Islamic Economics and Finance. Islamic Research and Training Institute (IRTI).

- Sulaiman, M., Majid, N., & Ariffin, N. (2015). Corporate governance of Islamic financial institutions in Malaysia. Asian Journal of Business and Accounting, 8(1), 65–93.

- Syed Alwi, S. F., Osman, I., Badri, M. B., Muhamat, A. A., Muda, R., & Ibrahim, U. (2022). Issues of letter of credit in Malaysian Islamic banks. Journal of Risk and Financial Management, 15(9), 373. https://doi.org/10.3390/jrfm15090373

- Tabash, M. I., Alam, M. K., & Rahman, M. M. (2022). Ethical legitimacy of Islamic banks and shariah governance: Evidence from Bangladesh. Journal of Public Affairs, 22(2), 2487. https://doi.org/10.1002/pa.2486

- Tilt, C. A. (1994). The influence of external pressure groups on corporate social disclosure some empirical evidence. Accounting Auditing & Accountability Journal, 7(4), 47–72. https://doi.org/10.1108/09513579410069849

- Usmani, T. (2004). An introduction to Islamic Finance. Arham Shams.

- Uyob, S., Zin, A. S. M., Ramli, J., Othman, J., Ghani, N. A. A., & Salleh, K. (2022). The effect of shariah committee composition on Malaysian Islamic banks’ audit report lag. International Journal of Applied Economics, Finance and Accounting, 14(1), 67–76. https://doi.org/10.33094/ijaefa.v14i1.652

- Weber, R. P. (1988). Basic content analysis. Sage University Paper series on quantitative applications. In Michael S., & Beck, L. (Eds.), Social sciences, series (pp. 07–49). Sage.

- Yin, X. (2005). The effect of graphic disclosures on users’ perceptions: An experiment. Journal of Accounting & Finance Research, 1(1), 39–50.

- Zuhroh, I. (2022). Mapping Islamic Bank governance studies: A systematic literature review. Cogent Business & Management, 9(1), 2072566. https://doi.org/10.1080/23311975.2022.2072566

Appendix A.

List of sampled IBs for data collection

Appenxi B. Dimensions and themes used to develop SGR index.