?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper investigates the empirical relationship between language structures and prevalent tax avoidance practices, specifically focusing on the influence of linguistic future time reference (FTR) on conforming tax avoidance. It also explores how corruption and public governance modulate this relationship. This study uses a cross-country analysis of 33 sample countries. The empirical evidence obtained shows that conforming tax avoidance is mostly practiced by companies in countries whose grammar requires speakers to give signs related to future events (Strong Future Time References/Strong FTR) than companies in countries that do not require speakers to give related signs future (Weak Future Time References/Weak FTR). This study also found that low levels of corruption and strong public governance played a role in suppressing high conforming tax avoidance behavior in countries with strong FTR speakers. These insights underscore the significance of national anti-corruption efforts and governance structures. Policymakers should consider these socio-cultural and institutional factors when addressing corporate tax avoidance. This research augments accounting, economics, and finance discourses by integrating linguistics—a perspective often overlooked.

1. Introduction

Taxes are one of the biggest sources of expenditure incurred by companies, where these funds can actually be diverted to increase company value. This encourages companies to avoid paying taxes. Basically, there are two common methods of reducing taxes, namely nonconforming and conforming. Nonconforming tax avoidance is done by lowering taxable profits while keeping accounting profits the same while conforming tax avoidance is done by lowering taxable profit and accounting profit. This type of tax avoidance is known as conforming tax avoidance (Badertscher et al., Citation2019).

The effect of language on corporate tax avoidance has not been fully explored, particularly in relation to conforming tax avoidance which is considered a relatively new topic to study. Previous research conducted by Na and Yan (Citation2021) and Cheng et al. (Citation2022) examined the relationship between language and nonconforming tax avoidance, but has not further explored the relationship between language and conforming tax avoidance. Nonconforming tax avoidance is different from conforming tax avoidance. In nonconforming tax avoidance, there is a difference between accounting profit and taxable profit, and this is done through several methods, such as tax credits, income that is considered non-taxable, differences in recognition of income/expenses (differences in depreciation methods), and so on, while on conforming tax avoidance, book-tax differences tend to be low which makes companies avoid income tax (Badertscher et al., Citation2019). Conforming tax avoidance often results in a decrease in accounting profit, which in turn reduces the amount of taxable profit. For example accelerating the recognition of certain costs, such as research & development, expense & advertising expense, and others to an earlier period (Badertscher et al., Citation2019).

Following the linguistic literature, the languages in this study are separated into two types based on how they encode time, such as present versus future. Languages with strong FTR require speakers to give a grammatical sign related to future events, whereas languages with weak FTR make this optional. For example, a German speaker predicting rain would say “Es regnet morgen” (rain tomorrow), while an English speaker would say “It will rain tomorrow”, this is because English needs the future marker “will” which in this context describes future events (Cheng et al., Citation2022).

The principle of linguistic relativity, also known as the Sapir-Whorf hypothesis, states that the way language encodes cultural and cognitive categories influences the way people think, which explains why speakers of different languages behave in different ways (Whorf, Citation1956). In support of this proposition, Chen (Citation2013) suggests that differences in economic behavior may be related to linguistically induced biases in perceptions of time and beliefs about time. In particular, strong FTR speakers perceive events in the future as more distant, which makes them less likely to engage in future-oriented behavior. So that in making a decision, companies in countries with strong FTR are less likely to consider future situations, which means that countries with strong FTR tend to do higher conforming tax avoidance than countries with weak FTR.

In addition, every country in the world has its own characteristics that need to be considered as country-level moderation in tax avoidance done by companies. The moderation at the country level in question is the level of corruption and public governance in a country, both of which can describe the level of supervision and the risk of detecting tax avoidance in a country. Companies that are in countries with strong FTR and at the same time have low levels of corruption and strong public governance, will receive stronger supervision and face a higher risk of detection than companies in countries with high levels of corruption and bad public governance. Thus if the company decides to carry out tax avoidance, then the space for doing it gets smaller and the risk of being detected gets bigger.

FTR, which can influence speakers’ time orientation, has been found to impact managerial decisions related to corporate tax avoidance strategies (Cheng et al., Citation2022; Na & Yan, Citation2021). Concurrently, national characteristics, notably low corruption levels and robust public governance, shape these strategies. Specifically, diminished corruption levels shape managerial attitudes toward tax and broader compliance (Bame-Aldred et al., Citation2013; Cho et al., Citation2016; Liu, Citation2016; Wenzel, Citation2005). Furthermore, potent public governance reinforces corporate tax compliance by upholding governance principles (Alqooti, Citation2020; Everest-Phillips & Sandall, Citation2009; Everest‐Phillips, Citation2010; Sebele-Mpofu & Ntim, Citation2020). This research seeks empirical evidence of these interrelations. Within a cross-country framework, it aims to address the subsequent inquiries: (1) Does a strong FTR correlate with conforming tax avoidance?; (2) Does reduced corruption attenuate the association between strong FTR and conforming tax avoidance?; and (3) Does robust public governance dilute the linkage between strong FTR and conforming tax avoidance?

Language structure significantly influences speakers’ perceptions, attitudes, and behaviors (Chen, Citation2013; Kim et al., Citation2017; Kim et al., Citation2022; Mavisakalyan & Weber, Citation2018). This research delves into the role of FTR within language structure, emphasizing its association with time perception. Concurrently, it addresses the influence of national characteristics, specifically corruption and public governance. The study aims to ascertain whether languages with obligatory temporal markers (strong FTR) predispose users toward conforming tax avoidance strategies. Additionally, it evaluates how country-specific traits, namely corruption and public governance, modulate the relationship between strong FTR languages and tax avoidance tendencies.

This study aims to make distinct contributions to extant literature. First, while prior research (e.g., Cheng et al., Citation2022; Na & Yan, Citation2021) emphasized nonconforming tax avoidance, our inquiry pivots to the realm of conforming tax avoidance. Historical accounting literature posits that under certain conditions, like subdued capital market pressures or impending significant tax rate alterations, firms lean towards conforming tax avoidance strategies (e.g., Badertscher et al., Citation2019; Guenther, Citation1994; Maydew, Citation1997; Penno & Simon, Citation1986). Second, we expand the socio-cultural dimensions within accounting and tax studies. Drawing from the linguistic relativity principle, which proposes that language-embedded cultural categorizations shape cognition, it is posited that speakers’ thought patterns vary based on their linguistic medium.

Third, while prior research (e.g., Cheng et al., Citation2022; Na & Yan, Citation2021) has predominantly addressed the direct influence of language on nonconforming tax avoidance, the moderating role of national characteristics in the nexus between language and conforming tax avoidance remains unexplored. Our work bridges this gap by introducing the moderation effects of country-level variables, specifically corruption and public governance. Fourthly, extant tax avoidance literature has generally been circumscribed to individual countries (e.g., the United States, Indonesia) or regional clusters (e.g., Asia or Europe). By leveraging a diverse cross-country dataset encompassing 33 nations spanning multiple continents, our study aspires to offer a more holistic understanding. Lastly, we employ a novel methodology articulated by Badertscher et al. (Citation2019) to discern patterns in conforming tax avoidance.s

The sections of this paper are organized as follows. Section 2 describes the background of this research. Section 3 explains the justification for using the theory and elaboration of the literature for each of the variables used. Section 4 contains a review of the theoretically and empirically relevant literature for hypothesis development. In Section 5, we outline our research design. Section 6 presents the research findings and engages in a detailed discussion. The paper concludes with a summarization and reflections on the implications of the study.

2. Backgroud

Tax avoidance remains a pressing challenge for virtually every nation. It encompasses all transactions and schemes that culminate in a diminished corporate tax liability (Dyreng et al., Citation2008). The Tax Justice Network’s “State of Tax Justice 2020” report disclosed a staggering diversion of over $656 billion in profits annually to tax havens, notably the UK, Luxembourg, Netherlands, and Switzerland. Such practices result in an estimated global loss of nearly $117 billion in taxes due to corporate subterfuges (Tax Justice Network, Citation2020). These figures are far from negligible. Taxation’s paramount importance extends beyond merely generating revenue for public utilities and infrastructures; it symbolizes the accountability tether binding governments to their citizens.

Tax avoidance can be broadly categorized into two prevalent methods: nonconforming and conforming. Notably, a significant portion of prior research (e.g., Atwood et al., Citation2010, Citation2012; Cheng et al., Citation2022; Desai & Dharmapala, Citation2009a, Citation2009b; Harymawan et al., Citation2023; Kim et al., Citation2017; Ni et al., Citation2021) has predominantly focused on nonconforming tax avoidance. The detection of nonconforming tax avoidance can be achieved by assessing a firm’s BTD (Hanlon & Heitzman, Citation2010). In contrast, established metrics for gauging conforming tax avoidance are lacking (Badertscher et al., Citation2019). Historical attempts to explore conforming tax avoidance have largely relied on survey methodologies (Cloyd, Citation1995), experimental datasets (Cloyd et al., Citation1996), or relatively confined and specialized samples (Erickson et al., Citation2004).

In our investigation, language serves as a key determinant of conforming tax avoidance. This approach is underpinned by Mavisakalyan and Weber (Citation2018) assertion that linguistic structures, specifically those pertaining to time orientation, profoundly influence speakers’ cognitive perceptions, which subsequently shape their behavior. Time orientation in language becomes apparent when individuals articulate their future intentions, aspirations, or forecasts (Dahl, Citation1985). However, linguistic manifestations of the future vary among speakers, rooted in the distinctive grammatical constructs of their respective languages. A comprehensive comparison of tense systems across major European languages can be found in the EUROTYP project (Dahl, Citation2000). For instance, English typically employs the periphrastic “will” for future intentions, as in “It will rain tomorrow.” In contrast, French integrates future tense inflections (e.g., -ai, -as, -a, -ons, -ez, -ont) in formal discourse, while colloquially leveraging the de-andative “aller” structure. Spanish, with its multifaceted expressions of the future, predominantly appends the -a ending to the primary verb, as illustrated by “llovera mañana” (It will rain tomorrow). Furthermore, this study acknowledges the pivotal roles of corruption and public governance within a nation, emphasizing their capacity to determine oversight intensity and the associated risks of uncovering tax avoidance schemes.

3. Theoretical literature review

3.1. Agency theory

Agency theory assumes that individuals will always act in their own interests and that their behavior may conflict with the interests of the company. Agency theory has the idea that a company is a nexus of contracts between agents and principals, with the aim of limiting or controlling conflicts of interest (Wolk et al., Citation2016).

Agency conflicts occur because of the separation between owners and management. Agents who run the company have a tendency to take actions that conflict with the interests of the principal, which results in a loss of shareholder value. Agents can try to maximize the utility they have at the expense of the owner’s welfare such as taking advantage of the flexibility of choosing accounting policies to behave opportunistically in order to maximize their utility (Jensen & Meckling, Citation1976).

Within the tax realm, agency problems may surface due to principals pressuring agents to enhance post-tax welfare, achievable through strategic decisions by these agents (Slemrod, Citation2004). In essence, tax avoidance serves as an avenue for agents to optimize firm value. Being the residual claimants, shareholders are inclined to favor managers engaging in tax avoidance, as it amplifies the post-tax profit share, which can subsequently be disbursed as dividends (Kim et al., Citation2011).

Tax-related agency problems can manifest not only internally within corporations but also externally between firms and tax authorities (Hanlon & Heitzman, Citation2010; Khan & Nuryanah, Citation2023). In this sense, conflicts of interest emerge. Firms, as taxpayers, naturally seek to minimize tax burdens to optimize post-tax wealth. Conversely, tax authorities consistently aim to bolster state revenues, pursuing various strategies to augment tax collections.

Employing agency theory is pertinent to this study, which anticipates a correlation between language and conforming tax avoidance. Such tax avoidance scenarios arise when principals exert demands on agents to enhance welfare (Slemrod, Citation2004). In this dynamic, tax avoidance becomes a strategy through which agents meet these demands. However, the consequences of these demands may vary based on whether agents operate within strong FTR or weak FTR linguistic environments. FTR, a significant linguistic feature, shapes speakers’ cognitive perceptions, influencing their actions (Mavisakalyan & Weber, Citation2018). Additionally, a setting characterized by minimal corruption and robust public governance can elevate accounting quality and disclosure standards. Within the agency theory framework, public governance acts as a watchdog, scrutinizing firms that exploit tax avoidance for rent-seeking.

3.2. Conforming tax avoidance

Badertscher et al. (Citation2019) contend that nonconforming tax avoidance has predominantly been the focal point of tax avoidance research, overshadowing other strategies at firms’ disposal. They assert that conventional non-conforming measures, such as the effective tax rate (ETR) or book-tax differences (BTD), fail to capture conforming tax avoidance activities. Thus, relying solely on these traditional measures offers a narrow view, potentially overlooking the extent to which firms engage in conforming tax avoidance strategies.

Predominantly, earlier literature concentrated on nonconforming tax avoidance methods, notably effective tax rate (ETR) and book-tax differences (BTD) measures. Yet, they largely overlooked conforming tax avoidance activities. Given that tax avoidance computations have been prevalently utilized in past research, such findings are primarily contextualized within nonconforming tax avoidance. Addressing this oversight, Badertscher et al. (Citation2019) introduced a conforming tax avoidance metric suitable for expansive samples. This measure has since gained widespread acceptance in recent studies and is also employed in the present research.

3.3. Future Time References (FTR)

FTR is a linguistic feature that profoundly impacts a speaker’s cognitive perception and, by extension, their actions (Kim et al., Citation2022; Mavisakalyan & Weber, Citation2018). Classified into “strong” and “weak” FTR, it pertains to perceptions of time. In strong FTR languages, future events require explicit markers, either inflectional (as seen in French with endings like -ai, -as) or periphrastic (as in English with “will”) (Kim et al., Citation2022). Speakers of such languages tend to distinctly delineate the future from the present, creating a clear temporal boundary (Pérez & Tavits, Citation2017). Consequently, those with strong FTR often view the future as distant and distinct from the present, sometimes even deeming it of lesser importance.

Conversely, languages with weak FTR, like German, lack distinct grammatical markers to signify future events (Thieroff, Citation2000). In these languages, future occurrences can be described using present tense, blurring the temporal distinction between the present and future for its speakers (Kim et al., Citation2017). As a result, speakers of weak FTR languages perceive the future as more immediate and akin to the present compared to their strong FTR counterparts, elevating the urgency of future considerations for them (Kim et al., Citation2022) .

Differences in the perceived psychological distance and valuation of the future prompt distinct behaviors amongst speakers of strong and weak FTR languages. Given that those speaking strong FTR languages prioritize the present over the future, they typically exhibit behaviors that are present-focused. In contrast, speakers of weak FTR languages, who perceive the future as more imminent and significant, often adopt behaviors that lean towards future-orientation (Cheng et al., Citation2022; Kim et al., Citation2017; Na & Yan, Citation2021).

Table presents an overview of prior studies related to FTR. The distinguishing factor of the present study, compared to those listed in Table , is its comprehensive examination of the relationship between FTR and conforming tax avoidance. While the majority of the studies in Table utilize FTR as a language proxy at the country level, our research adopts a similar methodology.

Table 1. FTR studies

3.4. Corruption

Transparency International (Citation2019) describes corruption as the misuse of power by public officials for personal benefits. Such misuse can manifest in various forms, including bribery, extortion, conflicts of interest, and illicit financing or capital movements. Similarly, the U.S. Attorney’s Office views corruption as a betrayal of public trust by government officials (Department of Justice, Citation2014). Corruption has gained global attention as it is perceived as a challenge to a country’s economic development. Recently, researchers have taken a keen interest in exploring its implications at the national level (Boateng et al., Citation2021).

Corporate behavior regarding regulation, compliance, and risk-taking is often a reflection of the cultural and environmental conditions of the country in which the company operates (Al-Hadi et al., Citation2021). When public officials in a financial ecosystem engage in corrupt practices such as soliciting bribes, participating in conflicts of interest, or misusing information for personal gains, it inevitably impacts the financial climate and tax adherence in that nation. Such conditions can motivate, or even provide opportunities for, corporate managers to sidestep the law, paving the way for tax avoidance (Al-Hadi et al., Citation2021). A prevalence of illicit activities, including bribery, insider trading, and embezzlement by public officials, can shape managerial attitudes towards tax compliance as well as adherence to other regulations (Bame-Aldred et al., Citation2013; Cho et al., Citation2016; Liu, Citation2016; Wenzel, Citation2005).

3.5. Public governance

Public Governance refers to the traditions and mechanisms through which a country’s authority is exercised, encompassing its institutions and practices (Kaufmann et al., Citation2011). Good governance mechanisms are associated with improved monitoring, enhanced disclosure, accountability, and transparency, which limit conflicts of interest (Boateng et al., Citation2021). As Massey and Johnston-Miller (Citation2016) elaborate, it involves a consortium of public actors tasked with crafting, executing, and overseeing specific regulatory policies, ensuring streamlined coordination across various governmental bodies. Its influence extends to the architecture of a nation’s tax system, playing a pivotal role in determining tax compliance (Everest-Phillips & Sandall, Citation2009). The interplay between public governance and taxation is intrinsic, with one reinforcing the other (Everest-Phillips & Sandall, Citation2009; Everest‐Phillips, Citation2010; Sebele-Mpofu & Ntim, Citation2020).

Furthermore, when governments establish both technical and financial mechanisms to meet developmental objectives, public governance emerges as an instrumental tool to actualize these ambitions. The realization of such goals hinges on upholding governance principles like transparency, accountability, responsibility and integrity (Alqooti, Citation2020; Boateng et al., Citation2021). Drawing from diverse scholarly works, it’s evident that public governance operates as a state-level governance mechanism, encapsulating the political, legal, and institutional landscape of a nation.

Among the plethora of public governance metrics, the World Governance Indicator (WGI) devised by Kaufmann et al. (Citation2011) stands out. It has garnered the endorsement of the World Bank, primarily due to its renowned and comprehensive assessment of a country’s institutional environment (Daniel et al., Citation2012). Kaufmann and his team delineated six pivotal governance metrics: voice & accountability, political stability, government effectiveness, regulatory quality, rule of law, and control of corruption. These indicators have undergone rigorous validation and reliability tests by scholars and policymakers alike (Daniel et al., Citation2012). For the purposes of this study, the control of corruption metric is omitted, given that specific tests are employed for corruption variables.

4. Empirical literature review and hypothesis development

In the first ten to twelve years of their life, humans learn how to live and they absorb all the information that comes from their environment through language (Hofstede et al., Citation2005). Language is an element that affects humans earlier than other social elements, such as religion, culture, and formal education (Kim et al., Citation2017). Humans are even capable of absorbing complex grammatical rules without going through formal teaching. Given this, language can have a great influence on human behavior.

The principle of linguistic relativity or the Sapir-Whorf hypothesis states that differences in the way language encodes cultural and cognitive categories affect the way people think, so that speakers of different languages will tend to think and behave differently depending on the language they use (Whorf, Citation1956). Chen (Citation2013) shows that speakers of languages with weak FTR tend to engage in future-oriented behavior and vice versa for speakers of languages with strong FTR. Based on the results of his research, strong FTR speakers tend to save less, exercise less, and smoke more than weak FTR speakers. The results obtained by Chen (Citation2013) were also confirmed by Sutter et al. (Citation2015) in their research that speakers of languages with strong FTR have a smaller possibility of delaying gratification than speakers of languages with weak FTR. Liang et al. (Citation2014) found that companies in countries with speakers of languages with a strong FTR show lower levels of corporate social responsibility than companies in countries with speakers of languages with a weak FTR. Na and Yan (Citation2021) found that companies in countries with strong FTR in their languages have the potential to be more involved in nonconforming tax avoidance than those in countries with weak FTR in their languages.

Given the existing empirical evidence, this study suspects that companies in countries with strong FTR tend to be more involved in conforming tax avoidance than companies in countries with weak FTR. Speakers of a language with a strong FTR will be less concerned about the future consequences of conforming tax avoidance activities, than speakers of a weak FTR. Previous literatures (Dahl, Citation2008; Kim et al., Citation2017; Thieroff, Citation2000) suggested that a strong FTR creates a psychological distance to the future.

Tax avoidance often results in future costs in the form of reputation risk, detection risk, enforcement actions, litigation, or executive dismissal. Graham et al. (Citation2014) found that corporate tax executives pay attention to reputational consequences when planning tax avoidance. Thus, companies that care about their reputation will be less likely to engage in tax avoidance (Austin & Wilson, Citation2017; Chen et al., Citation2010). This tax avoidance can cost managers taking this risk for incentive purposes. Rego and Wilson (Citation2012) show that managers with high equity incentives engage in riskier tax strategies.

Tax avoidance practices can trigger other costs in the form of investigations by the tax authorities. Detection of misconduct will result in penalties for the company and its managers. For example, France which seek back taxes from Google of 1.6 billion euros (Reuters, Citation2016) and Apple was required to pay taxes of up to 14.5-billion-dollars in the EU tax clampdown (Bloomberg, Citation2016). Bozanic et al. (Citation2017) showed that the Internal Revenue Service (IRS) is more strict in monitoring companies with greater tax avoidance and high uncertainty of tax benefits. In addition, another cost arising from tax avoidance is the negative impact obtained from the stock market and debt market later. Hanlon and Slemrod (Citation2009) found that news arising from the involvement of companies in tax shelters causes their stock prices to fall, and also Kim et al. (Citation2011) who found a positive relationship between tax avoidance and stock price crash risk.

Drawing on agency theory, Slemrod (Citation2004) posits that tax avoidance issues arise when the principal places demands on the agent to achieve enhanced welfare. The repercussions of these demands differ for agents situated in countries with strong or weak FTR languages. This distinction is significant since FTR is a linguistic feature that shapes speakers’ cognitive perceptions, subsequently influencing their behavior (Mavisakalyan & Weber, Citation2018). Compared to speakers of languages with weak FTR, speakers of languages with strong FTR tend to see the future cost of tax avoidance as far away, because their language strictly separates the future from the present, therefore they tend to engage in higher tax avoidance. Given that the negative impact of conforming tax avoidance can also impact future periods, and strong FTR speakers are associated with less future-oriented behavior (Chen, Citation2013; Liang et al., Citation2014; Sutter et al., Citation2015), we predict that companies in countries with strong FTR also tend to engage in conforming tax avoidance. Thus it is suspected that there is a positive relationship between strong FTR and conforming tax avoidance. Therefore:

H1:

Companies in countries with strong FTR languages engage in more conforming tax avoidance than companies in countries with weak FTR languages.

According to Beasley et al. (Citation2010), increasing financial, legal and organizational complexity, along with reduced transparency and exchange of information can lead to corruption. High corruption in a country can be reflected in the high number of cases related to bribery, embezzlement, insider trading and other crimes committed by public officials in a country, where this can affect the attitude of company managers towards tax compliance and other forms of compliance (Al-Hadi et al., Citation2021; Bame-Aldred et al., Citation2013; Cho et al., Citation2016; Liu, Citation2016; Wenzel, Citation2005). Corrupt members of boards, managers and employees tend to be attracted to companies in countries with a culture of corruption (Al-Hadi et al., Citation2021). In addition, environmental factors at the country level (in this study the environment of corruption) can influence corporate culture so that it can motivate managers to engage in tax avoidance (Bame-Aldred et al., Citation2013). Thus, crimes committed by public officials are believed to affect oversight by managers, monitoring executors, control systems, governance, and company compliance with taxes.

Huňady and Orviská (Citation2015) and Arif and Rawat (Citation2018) state that a corrupt environment can have a negative impact on tax audits, tax administration, and institutional credibility. However, it is inversely proportional to a low corruption environment, where in a low corruption environment there is an increase in government efficiency so that the performance of tax revenues becomes better. The negative impact of a high corruption environment is also emphasized by Khlif and Amara (Citation2019) which states that a high corruption environment strengthens political connections and tax evasion. Furthermore, El-Helaly et al. (Citation2020) assert that the environmental conditions of a country, such as corruption, play a critical role in the adoption of International Financial Reporting Standards (IFRS) at the national level. Government officials who engage in corrupt practices may be relatively more reluctant to adopt accounting standards that could enhance transparent, accurate, and comparable financial information (El-Helaly et al., Citation2020).

According to agency theory, managers (agents) have more information for decision making. This allows them to make decisions that benefit themselves or their company, but these decisions may conflict with the interests of the tax authorities (principals) (Hanlon & Heitzman, Citation2010; Khan & Nuryanah, Citation2023). When managers from countries with strong FTR languages are motivated by interests that benefit themselves or their companies, they can take advantage of information asymmetry to adopt policies that are detrimental to the country’s tax revenues. A low corruption environment will increase transparency and disclosure of information will be better, so as to strengthen the tax authorities in increasing company compliance as taxpayers and playing a role in reducing conflicts of interest between companies and tax authorities (Alon & Hageman, Citation2013). Thus, a low-corruption environment helps reduce information asymmetry between firms in countries with strong FTRs and tax authorities and further reduces the discretionary power of agents.

In this study, we suspect that there are differences in the relationship between language and the level of conforming tax avoidance in countries with high and low levels of corruption. This is because companies in countries with high levels of corruption can reduce public scrutiny, as well as reduce the ability of fiscal authorities to enforce tax laws and punish managers and companies involved in tax avoidance practices (Khlif & Amara, Citation2019). That is, this causes the opportunity for black economy practices and tax avoidance to become higher. Conversely, a low level of corruption will encourage transparency and companies operate with higher public scrutiny, thereby creating a favorable environment for reducing tax avoidance and black economy practices.

When company managers in countries with strong FTR face a high risk of being detected due to a low corruption environment in a country, managers will tend to reduce their level of tax avoidance. Managers of companies in countries with strong FTR language see that the present and the future are distant, so they tend to think less about the consequences of tax avoidance in the future. However, at the same time this will be reduced because a country’s low level of corruption results in stronger public scrutiny and law enforcement. So the hypothesis proposed in this study is:

H2:

The lower the level of corruption in a country, the less likely companies in countries with strong FTR languages to engage in conforming tax avoidance than companies in countries with weak FTR languages.

González and García-Meca (Citation2014) argue that a weak public governance framework, characterized by distrust in legal systems and feeble enforcement of rules, can amplify earnings management within firms. Contrarily, Ngobo and Fouda (Citation2012) contend that robust public governance enhances corporate performance while curbing corruption. Bonetti et al. (Citation2016) discovered a nuanced relationship between IFRS adoption and financial reporting quality, indicating that the effects are contingent upon governance at both national and organizational levels. Emphasizing the significance of governance, La Porta et al. (Citation1997, Citation1998) highlighted that fortified public governance augments investor rights protection, necessitating companies to adopt greater transparency and more comprehensive information disclosure. Zeng (Citation2019) further postulates that heightened transparency and disclosure demands escalate the costs borne by companies in tax avoidance pursuits.

Within the agency theory framework, managers, acting as agents, possess superior information that facilitates decision-making. While this places them in a position to make choices benefiting themselves or the corporation, such decisions might be at odds with the tax authorities, who act as principals (Hanlon & Heitzman, Citation2010; Khan & Nuryanah, Citation2023). Specifically, managers fluent in strong FTR languages, driven by self-centric or corporate-centric motivations, can exploit this information asymmetry to enact policies that negatively impact a nation’s tax revenues.

Effective public governance becomes crucial here, acting as a monitoring mechanism against companies leveraging tax avoidance strategies for personal gains or actions adverse to national interests. In jurisdictions characterized by robust public governance, there’s an inherent enhancement in the quality of accounting and transparent disclosure of information (La Porta et al., Citation1997; Porta et al., Citation1998; Zeng, Citation2019). Thus, the strength of public governance is instrumental in curtailing agency dilemmas. Additionally, a fortified public governance apparatus amplifies the state’s oversight capabilities over these agents. Supporting this, Desai et al. (Citation2007) present empirical evidence suggesting that in nations with resilient public governance, tax rate augmentations correspond with a rise in tax revenues. In stark contrast, countries with weaker governance frameworks witness diminishing tax revenues upon similar tax rate hikes.

In this study, we suspect that there are differences in the relationship between language and the level of conforming tax avoidance in countries with strong and weak public governance. This is because the implementation of strong public governance will require companies to be more transparent in disclosing their information and provide additional monitoring related to tax avoidance and increase the risk of detecting tax avoidance. If regulations related to public governance are violated, then the risk of tax avoidance being detected and subject to sanctions becomes even higher.

When company managers in countries with strong FTR language face a high risk of being detected due to strong public governance in that country, managers will tend to reduce their level of conforming tax avoidance. Managers of companies in countries with strong FTR see that there is a gap between now and the next period, so they tend not to think too much about the future consequences regarding their current conforming tax avoidance practices. However, simultaneously this will decrease because the implementation of strong public governance requires companies to be more transparent in disclosing their information to the public. So the hypothesis proposed in this study is:

H3:

The better the public governance in a country, the less likely companies in countries with strong FTR languages to engage in conforming tax avoidance than companies in countries with weak FTR languages.

5. Research design

This research is a cross-country study with an observation period from 2010 to 2020. The total country samples for this study is 33 countries. In the following, we present the variable definitions, research models, and data and samples for this research.

5.1. Variable definitions

5.1.1. Dependent variables

The dependent variable used in this study is conforming tax avoidance. This study measures conforming tax avoidance based on Badertscher et al. (Citation2019). Measurement of conforming tax avoidance is the residue of the following regression equation:

Where TAXESPAID_TO_ASSETS is the ratio of cash taxes paid to lagged total assets. BTD is book income minus taxable income scaled by lagged total assets. NEG is a variable indicator equal to one if BTD is negative and zero otherwise. BTD*NEG is the interaction between BTD and NEG. NOL and ΔNOL are carryforward net operating loss and changes from carryforward net operating loss. ℇ is the residual of the regression equation.

In the conforming tax avoidance equation, the independent variable reflects nonconforming tax avoidance. BTD is a measure of nonconforming tax avoidance. The variables NEG and BTD*NEG take into account that there may be different motivations and reasons for companies having positive or negative BTD. Positive BTD is created when book income is greater than tax income, and in general when this occurs the motivation is considered as tax avoidance. Negative BTD occurs when taxable income is higher than book income, this usually excludes tax avoidance because companies will tend to pay higher taxes than shown in book income. The NOL value is generated when the company has losses in the previous year that are carried forward by the company (or the company can choose not to carry forward). This NOL reduces the tax paid, which decreases the quantifier in the TAXESPAID_TO_TAXES variable, but is not a conforming tax avoidance.

5.1.2. Independent variables

The independent variable used in this study is language (FTR). The language criterion (Strong FTR or weak FTR) used in this study follows Chen (Citation2013), a criterion adopted by the European Science Foundation’s Typology of Language in Europe (EUROTYP) project. Referring to the approach used by Chen (Citation2013) and used by recent studies (Bernhofer et al., Citation2023; Cheng et al., Citation2022; Kim et al., Citation2017; Kim et al., Citation2022; Na & Yan, Citation2021), then in this study the proxy for language is given a value of one if the language in the country grammatically distinguishes the present from the future and is given a value of zero otherwise. A language with a weak FTR does not require future timestamps, whereas a language with a strong FTR is one that requires future timestamps in all circumstances and perhaps only a few are excluded.

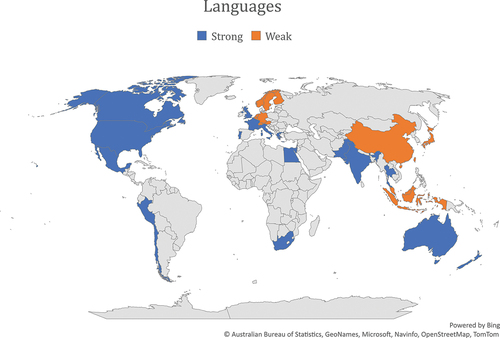

Furthermore, in Table we present the distribution of national languages which are included in the weak and strong FTR groups. In addition, visually, the distribution of countries with strong FTR and weak FTR characteristics can be seen in Figure . In addition, to test the sensitivity of the results of this study, we also examined the relationship between language and conforming tax avoidance using text-based coding developed by Chen (Citation2013).

Figure 1. Distribution of languages (strong and weak FTR).

5.1.3. Moderating variables

This study uses two moderating variables, namely corruption and public governance. First, in identifying the level of corruption in a country, this study uses one of the most widely used indicators, namely the Corruption Perception Index (CPI) by Transparency International. This approach is also widely used by recent studies in measuring corruption, for example Arif and Rawat (Citation2018), Khlif and Amara (Citation2019), El-Helaly et al. (Citation2020), Boateng et al. (Citation2021), Al-Hadi et al. (Citation2021), and Yamen (Citation2021). The CPI index assigns countries a rating on a scale of 0–100 where 0 equals the highest level of perception of corruption and 100 equals the lowest level of perception of corruption. Countries that rank low on the index are due to untrustworthy and underperforming public institutions, such as the police, legislature, and judiciary. Situations of bribery and extortion are often faced by people, because of the poor service system due to the misuse of funds that occur and coupled with the indifference of public officials to the losses from the policies they take. In contrast, countries with higher ratings tend to have higher degrees of press freedom, access to information related to public expenditure, strong standards of integrity for every public official, and an independent judicial system (Transparency International, Citation2020).

Second, in identifying the level of strong or weak public governance in a country, this study uses the WGI issued by the World Bank which reflect the political, legal and institutional environment of a country. The WGI has been used by previous studies (Arif & Rawat, Citation2018; Bonetti et al., Citation2016; Ding et al., Citation2021; González & García-Meca, Citation2014; Harymawan & Nowland, Citation2016; Ogundajo et al., Citation2022; Zeng, Citation2019) in measuring public governance. This research follows Arif and Rawat (Citation2018) who built a public governance index through principal component analysis of governance indicators. Of the six WGI indicators, Arif and Rawat (Citation2018) did not include the control of corruption index in the calculations on the grounds of avoiding multicollinearity. This study adopts the same approach as Arif and Rawat (Citation2018) because this study also uses the corruption variable. Thus, the public governance index built using PCA uses government effectiveness, political stability, regulatory quality, the rule of law, and voice and accountability indicators.

5.1.4. Control variables

We used several control variables in this study, both at the country level and company level. The selection of control variables in this study refers to previous studies (e.g., Atwood et al., Citation2012; Badertscher et al., Citation2019; Cheng et al., Citation2022; Na & Yan, Citation2021). The country-level control variables in this study are CommonLaw: common law countries and non-common law countries; LogGDP: country-level real GDP per capita; GDPGrowth: country-level GDP growth; UncertaintyAvoidance: country-level uncertainty avoidance score; Masculinity: country-level masculinity scores; Individualism: country-level individualism scores; PowerDistance: country-level power distance score; Short/longTermOrientation: country-level short/long term orientation scores; IndulgencevsRestraint: country-level Indulgence vs Restraint score; Inflation: country level inflation rate; TaxRate: the tax rate that applies to a country; WW: countries with a worldwide tax system or territorial tax system; EarnVol: country-level earnings volatility. Furthermore, the company-level control variables in this study are Size: company size; Leverage: level of debt; ROA: company profitability; Loss: a company that has a loss before tax; SalesGrowth: sales growth; PPE: property, plant and equipment.

5.2. Research models

To test the relationship of language to conforming tax avoidance, the estimation of the regression model that we run is as follows:

Where ConformTax is conforming company tax avoidance in a country. StrongFTR is Future Time References in a country. ModVar is a moderation variable that consists of Corrupt and PubGov. Country level controls are country-level control variables used to estimate the model. Firm level controls are company-level controls used to estimate the model. Industry, country and year fixed effects to control for heterogeneity across industries, countries and time.

To test the research hypothesis, we used four estimation models, namely models (2), (4) to investigate the relationship of language (StrongFTR) and conforming tax avoidance (ConformTax); and model (3) and model (5) to investigate the role of moderation (Corrupt and Pubgov) on the relationship between language (StrongFTR) and conforming tax avoidance (ConformTax). In this study we included models (4) and (5) as additional analysis to test the robustness of the main results of this study (model 2 and model 3). We exclude country fixed effects in models (4) and (5).

5.3. Data and sample

This study used secondary data with observation periods from 2010 to 2020. The data and data sources used in this study are (a) language data (FTR) obtained from the European Science Foundation’s Typology of Language in Europe (EUROTYP) project and Chen (Citation2013); (b) the company’s financial report data is obtained from the Revinitiv Eikon database which is then used to measure company-level variables; (c) public governance data obtained from the WGI published by the World Bank; (d) data on corruption was obtained from the Corruption Perception Index published by Transparency International; (e) for data on country-level control variables, this study obtains country-level data representing formal institutions and national culture from Porta et al. (Citation1998), Hofstede (Citation2011), World Bank, Economic Freedom Website, KPMG LLP online summary, PricewaterhouseCoopers LLP’s online information, Coopers & Lybrand LLP’s worldwide tax summary guides, PricewaterhouseCoopers Corporate Taxes: A Worldwide Summary, and financial data obtained from Refinitiv Eikon datastream. Summary and measurement of each variable is described in Table .

Table 2. Variable Measurement

The population of this study is all countries in the world. The selection of sample countries for this study followed the following criteria (a) information regarding the languages spoken in sample countries is available from the European Science Foundation’s Typology in Europe (EUROTYP) and Chen (Citation2013); (b) information related to corruption in each sample country was published by Transparency International during the research period; (c) information related to public governance of each sample country published by the World Bank during the study period; (d) exclude samples for which country-level control variables are not available. Furthermore, the selection of company samples in this study followed the following criteria (d) companies are not included in the financial industry because this industry has special and different regulations. In addition, companies in industries that are subject to special taxes are also excluded from the sample; (e) exclude companies with incomplete data for company-level variables during the study.

This study identified the availability of language-related data from the European Science Foundation’s Typology of Language in Europe (EUROTYP) project and Chen (Citation2013), corruption, public governance, and country-level control variables, so that finally 41 sample countries were selected. Furthermore, researchers used company data from 41 countries as a sample. At the time of data collection, this study excluded companies within the scope of the financial industry and which were subject to special taxes in each country so that a sample of companies was obtained during the 11 year observation period (2010–2020) of 427,790 companies. Furthermore, from the 41 countries whose data were obtained, there were countries where the components of the variables used in the study were incomplete, so they were excluded from the research sample, so that a total of 418,165 companies were observed. Of the 38 countries that met the criteria, an analysis was then carried out to obtain company-years with complete variable data. Thus the number of final observations for observations obtained during the study period was 53,515 companies in 33 countries (Table ). On the other hand, for the corruption moderation model this research only uses 43,785 companies, because there are differences in the methodology in measuring corruption by Transparency International for 2010–2011, so this study uses data from 2012 to 2020.

Table 3. Sample by country

6. Empirical results and discussion

6.1. Descriptive statistics and matrix correlation

Descriptive statistics on the research data are presented in Table . The mean and median of the ConformTax are 0.001 and − 0.002. The mean of StrongFTR is 0.444, meaning that 44.4% of the companies in the sample are located in countries with strongFTR languages. The mean of corruption is 58.432. This indicates that on average the sample has a relatively moderate level of corruption. Furthermore, the average value of public governance is − 0.327 and the median value is 0.763. This indicates that on average the countries in the sample have a relatively low level of public governance. In summary, this research sample has an average LogGDP of 9.763, GDPGrowth of 3.775, Inflation of 2.295, TaxRate of 27.328, EarnVol of 0.164, Size of 20.369, Leverage of 0.484, ROA of 0.044, SalesGrowth of 0.069, and PPE of 0.272. Furthermore, sequentially the average values of the cultural dimensions of UncertaintyAvoidance, Masculinity, Individualism, PowerDistance, ShortlongTermOrientation, IndulgencevsRestraint are 41.755, 57.259, 43.128, 64.629, 60.860, 43.851 respectively. Finally, in this sample there are 51.3% of countries with a Common Law legal system, 73.6% of countries adopt the Worldwide Tax System, and there are 13.7% of companies that experience losses.

Table 4. Statistic Descriptive

Furthermore, the pairwise correlation between variables can be seen in Table . From this test it was found that ConformTax was positively correlated with StrongFTR at a significance level of 1%. This relationship provides initial confirmation for our hypothesis that companies in countries with a language that separates the present from the future engage in more conforming tax avoidance.

Table 5. Pairwise correlation

6.2. Empirical results

Table presents empirical results regarding the relationship between language and conforming tax avoidance (hypothesis 1). Column (1) shows the relationship between StrongFTR and ConformTax with industry, country, and year fixed effects. The coefficient obtained for StrongFTR is 0.0045 (t = 3.96) and is significant at the 1% level. In column (2), this study adds country-level variables and firm-level variables. The coefficient obtained for StrongFTR is 0.0064 (t = 1.73) and is significant at the 10% level. Column (3) shows the relationship between StrongFTR and ConformTax with industry and year fixed effects, excluding country fixed effects. The coefficient obtained for StrongFTR is 0.0069 (t = 6.13) and is significant at the 1% level. In column (4), this study adds country-level and firm-level variables. The coefficient obtained is 0.0035 (t = 4.72) and remains consistent at the 1% level. Thus, consistently the results of this study indicate that companies in countries with strong FTR languages are involved in conforming tax avoidance more than companies in countries with weak FTR languages. Thus, H1 is accepted.

Table 6. The relationship between languages and conforming tax avoidance

Furthermore, in Table , empirical results are presented regarding the role of moderation in the relationship between language and conforming tax avoidance (hypotheses 2 and 3). In column (1), this study examines the role of corruption on the relationship between StrongFTR and ConformTax with industry, country, and year fixed effects. The coefficient obtained for StrongFTRxCorrupt is − 0.0005 (t = −2.70) and is significant at the 1% level. In column (2), this study excludes country fixed effects. The coefficient obtained for StrongFTRxCorrupt is − 0.0001 (t = −4.67) and is significant at the 1% level. Thus, the results of this study indicate that the lower the level of corruption in a country, the smaller the tendency of companies in countries with strong FTR languages to engage in conforming tax avoidance than companies in countries with weak FTR languages. Thus, H2 is accepted.

Table 7. The role of corruption and public governance on the relationship between languages and conforming tax avoidance

In column (3), this study examines the role of public governance on the relationship between StrongFTR and ConformTax with industry, country, and year fixed effects. The coefficient obtained for StrongFTRxPubGov is − 0.0155 (t = −11.37) and is significant at the 1% level. Column (4) shows that this research excludes country fixed effects. The coefficient obtained is − 0.0016 (t = −7.81) and remains consistent at the 1% level. Thus, the results of this study indicate that the better the public governance of a country, the smaller the tendency of companies in countries with strong FTR languages to engage in conforming tax avoidance compared to companies in countries with weak FTR languages. Thus, H3 is accepted.

6.3. Discussion

First, this research shows that companies in countries with strong FTR tend to see the future costs of tax avoidance as far away, because their language clearly separates the future from the present. Therefore they tend to engage in higher conforming tax avoidance. In addition, the negative impact of conforming tax avoidance can also have an impact on the future, and strong FTR speakers are associated with less future-oriented behavior (Chen, Citation2013; Liang et al., Citation2014; Na & Yan, Citation2021; Sutter et al., Citation2015). Therefore, companies in countries with strong FTR languages tend to engage in higher conforming tax avoidance. The evidence we obtained is in line with H1 of the study.

Looking at the agency theory framework, the results of this study confirm that strong FTR speakers tend to be more able to meet principal demands to be able to obtain increased welfare after tax through conforming tax avoidance because strong FTR speakers are relatively higher in conforming tax avoidance. According to Kim et al. (Citation2011), as residual claims, principals tend to want agents to do tax avoidance, so that principals can increase the portion of profit after tax, so they can receive it through dividends.

The evidence obtained in this study confirms the findings of Na and Yan (Citation2021) and Cheng et al. (Citation2022) who find that firms in countries with strong FTR tend to engage more in tax avoidance, Sutter et al. (Citation2015) who showed that individuals with strong FTR were more likely to engage in gratification than individuals with weak FTR, and Liang et al. (Citation2014) who found that companies in countries with strong FTR speakers showed a relatively lower level of social responsibility than companies in countries with weak FTR speakers. The implications of these findings are important for companies to consider in understanding the characteristics of managers through the language they use considering the discretion they have.

Second, this study shows that when company managers in countries with strong FTR face a high risk of being detected due to low corruption in a country, managers will tend to reduce their level of tax avoidance. Managers of companies in countries with strong FTR see that the present and the future have some distance, but at the same time this will be less and less because a country’s low level of corruption results in stronger public oversight and law enforcement. The evidence we obtained is in line with H2 of the study.

Referring to the context of agency theory, the results of this study prove that a low corruption environment plays an important role in reducing information asymmetry between companies in countries with strong FTR and tax authorities and further reduces the discretionary power of agents. A low corruption environment will increase transparency and information disclosure will be better. Thus, a low corruption environment can strengthen tax authorities in increasing company compliance as taxpayers and play a role in reducing conflicts of interest between companies in countries with strong FTR and tax authorities. Therefore, the results of this study confirm that a low role of corruption in a country helps reduce information asymmetry between companies in countries with strong FTR and tax authorities and further reduces the discretionary power of agents.

The evidence obtained in this study is in line with the findings of Huňady and Orviská (Citation2015) and Arif and Rawat (Citation2018) which state that a low corruption environment increases government efficiency so that tax revenue performance becomes better, also with Al-Hadi et al. (Citation2021) who state that members of boards, managers and employees who are corrupt tend to be less attracted to companies in countries with low corruption environments. The evidence obtained is also in line with El-Helaly et al. (Citation2020) which shows that when a country has strong control over corruption, that country will be earlier in adopting IFRS. From the evidence obtained, it is important for a country to have strong and firm controls on corruption to reduce conforming tax avoidance.

Third, This study shows that when company managers in countries with strong FTR face a high risk of being detected due to strong public governance in that country, managers will tend to reduce their level of tax avoidance. Managers of companies in countries with strong FTR see that there is a distance between now and the future, so they tend not to think too much about the consequences going forward regarding the practice of conforming tax avoidance that they are currently doing. However, this will tend to decrease since the implementation of strong public governance requires companies to be more transparent in disclosing their information to the public. The evidence we obtained is in line with H3 of the study.

Within the framework of agency theory, the findings underscore the importance of strong public governance in diminishing information asymmetry between companies in strong FTR countries and tax authorities. Such robust governance ensures stringent oversight over companies that might exploit tax avoidance for rent extraction and other self-serving interests detrimental to the state. Enhanced accounting quality and improved information disclosure are direct byproducts of this governance, making it instrumental in alleviating agency-related issues. Moreover, robust public governance bolsters the government’s ability to monitor agents. In essence, the study corroborates that strong public governance effectively bridges the informational divide between companies in strong FTR nations and tax regulators.

The findings of this study align with González and García-Meca (Citation2014), suggesting that robust public governance curtails earnings management activities. This sentiment is further echoed by Ngobo and Fouda (Citation2012), who argue that sound public governance enhances company performance. Furthermore, Zeng (Citation2019) emphasizes that nations with rigorous public governance impose higher transparency and disclosure requirements, inadvertently raising the costs associated with conforming tax avoidance activities for companies. Thus, for a country to effectively reduce conforming tax avoidance, the establishment and rigorous implementation of robust public governance is imperative.

6.4. Sensitivity test

In this study, we tested the sensitivity of the results using alternative measurements of language, namely sentence ratio and verb ratio. Measurements based on the frequency of sentences and verbs were analyzed from texts taken from weather forecasting websites. Chen (Citation2013) scraped the web of weather forecasts, arguing that the use of weather forecasts has the advantage of comparing relatively controlled sets of texts about future events. An important limitation of this approach is that the languages analyzed are limited to those that are widespread on the internet.

The “sentence ratio” is calculated by dividing the number of sentences that grammatically mark the future by the total number of sentences in the online text from weather forecast sites. Similarly, the “verb ratio” is determined by dividing the number of verbs that grammatically mark the future by the total number of verbs in the same online text (Chen, Citation2013). Both these ratios assess the percentage of sentences and verbs, respectively, that pertain to future weather conditions and contain grammatical future markers. A higher Sentence Ratio or Verb Ratio suggests that the language of that particular country exhibits a strong FTR.

Empirical findings as shown in Table reveal that the verb ratio variable is positively correlated with conforming tax avoidance, significant at the 1% level. This suggests that companies in countries with strong FTR languages engage more in conforming tax avoidance than those in countries with weak FTR languages. These results underscore that speakers of strong FTR languages might not weigh the future consequences of conforming tax avoidance as heavily as speakers of weak FTR languages do. This observation aligns with insights from Kim et al. (Citation2017), Dahl (Citation2008) and Thieroff (Citation2000), which posit that strong FTR languages instill a psychological distance toward the future.

Table 8. The relationship between languages and conforming tax avoidance (verb ratio)

In line with the findings on the verb ratio variable, the empirical results presented in Table generally show that the sentence ratio variable is positively related to conforming tax avoidance at the 1% level. This shows that companies in countries with strong FTR languages are involved in conforming tax avoidance more than companies in countries with weak FTR languages. The results of this study indicate that strong FTR speakers have lower concern regarding the consequences of conforming tax avoidance activities in the future compared to weak FTR speakers, in line with the opinions of Kim et al. (Citation2017), Dahl (Citation2008) and Thieroff (Citation2000) which states that strong FTR speakers create a psychological distance into the future.

Table 9. The relationship between languages and conforming tax avoidance (sentence ratio)

Speakers of strong FTR languages tend to perceive the future repercussions of tax avoidance as distant, given their linguistic propensity to sharply differentiate the future from the present. Consequently, they are more inclined towards tax avoidance. This conclusion aligns with earlier research findings. Specifically, Sutter et al. (Citation2015) found that strong FTR speakers are less prone to delay gratification compared to those of weak FTR. Likewise, Liang et al. (Citation2014) noted a diminished commitment to corporate social responsibility among strong FTR speakers in contrast to their weak FTR counterparts. Moreover, studies by Cheng et al. (Citation2022) and Na and Yan (Citation2021) suggest that strong FTR speakers exhibit a higher inclination towards nonconforming tax avoidance when juxtaposed with weak FTR speakers.

Overall, our results are consistent with the results of the main test, namely companies in countries with strong FTR languages are involved in more conforming tax avoidance than companies in countries with weak FTR languages. It can be concluded that the results obtained in this research are robust.

7. Summary and conclusion

This paper explores the interplay between language and conforming tax avoidance, with an emphasis on the influence of corruption and public governance in this relationship. Using cross-country data to analyze the strategy of conforming tax avoidance, our findings indicate a notable trend: companies in countries with strong FTR languages tend to indulge more in conforming tax avoidance compared to those in nations with weak FTR languages. Nevertheless, the presence of low corruption and robust public governance can significantly curb such tax avoidance behaviors, especially in strong FTR countries.

This research contributes both theoretical and practical implications. First, there’s a noticeable gap in the literature concerning conforming tax avoidance compared to the more expansive discussions on nonconforming tax avoidance (Badertscher et al., Citation2019). Our study not only highlights this discrepancy but also deepens the theoretical understanding by elucidating the connection between language preferences and conforming tax avoidance behaviors.

Second, our findings reveal that language significantly impacts conforming tax avoidance. Specifically, managers who predominantly use strong FTR languages are more inclined to engage in heightened levels of conforming tax avoidance. This knowledge is instrumental for businesses, as recognizing linguistic tendencies of their managers can shed light on potential managerial decision-making inclinations, especially in tax strategies.

Third, this research augments the literature on conforming tax avoidance by underscoring the significance of corruption environments and public governance in influencing tax strategies across strong FTR and weak FTR countries. Our findings echo and extend the insights of Khlif and Amara (Citation2019), Arif and Rawat (Citation2018), Yamen (Citation2021) and Zeng (Citation2019). Specifically, we emphasize the mitigating roles of low corruption levels and robust tax enforcement in curbing conforming tax avoidance. This is of utmost relevance, as effective oversight and stringent sanctions facilitated by these factors foster taxpayer compliance. Given the empirical evidence, countries aiming to reduce conforming tax avoidance must focus on implementing clear rules, enforcing them rigorously, and fostering trust among their stakeholders and taxpayers.

Despite the insights provided by this research, there are notable limitations to consider. First, our study primarily focuses on one social element—language, emphasizing its grammatical features. Future research could broaden the scope by exploring other social elements and delving deeper into various linguistic facets. Second, while our study takes into account institutional factors like corruption and public governance in relation to curbing conforming tax avoidance, it doesn’t encompass the entire spectrum of institutional factors. Subsequent studies could investigate the influence of other pertinent institutional elements, such as the rigor of tax and legal enforcement, on tax avoidance behaviors.

Correaction

This article was originally published with errors, which have now been corrected in the online version. Please see Correction (https://doi.org/10.1080/23311975.2023.2265090).

Acknowledgments

The authors are grateful for the in-depth review and advice to the Senior Editor, Professor Collins Ntim, and two anonymous reviewers. We Also appreciate the helpful comments and suggestions from dissertation committee – Sylvia Veronica NPS (chair), Dwi Martani, Siti Nuryanah, Telisa Aulia Falianty, and Abdul Haris Muhammadi.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Al-Hadi, A., Taylor, G., & Richardson, G. (2021). Are corruption and corporate tax avoidance in the United States related? Review of Accounting Studies, 27(1), 344–30. https://doi.org/10.1007/s11142-021-09587-8

- Alon, A., & Hageman, A. M. (2013). The impact of corruption on firm tax compliance in transition economies: Whom do you trust? Journal of Business Ethics, 116(3), 479–494. https://doi.org/10.1007/s10551-012-1457-5

- Alqooti, A. A. (2020). Public governance in the public sector: Literature review. International Journal of Business Ethics and Governance, 3(3), 14–25. https://doi.org/10.51325/ijbeg.v3i3.47

- Arif, I., & Rawat, A. S. (2018). Corruption, governance, and tax revenue: Evidence from EAGLE countries. Journal of Transnational Management, 23(2–3), 119–133. https://doi.org/10.1080/15475778.2018.1469912

- Atwood, T. J., Drake, M. S., & Myers, L. A. (2010). Book-tax conformity, earnings persistence and the association between earnings and future cash flows. Journal of Accounting and Economics, 50(1), 111–125. https://doi.org/10.1016/j.jacceco.2009.11.001

- Atwood, T. J., Drake, M. S., Myers, J. N., & Myers, L. A. (2012). Home country tax system characteristics and corporate tax avoidance: International evidence. The Accounting Review, 87(6), 1831–1860. https://doi.org/10.2308/accr-50222

- Austin, C. R., & Wilson, R. J. (2017). An examination of reputational costs and tax avoidance: Evidence from firms with valuable consumer brands. The Journal of the American Taxation Association, 39(1), 67–93. https://doi.org/10.2308/atax-51634

- Badertscher, B. A., Katz, S. P., Rego, S. O., & Wilson, R. J. (2019). Conforming tax avoidance and capital market pressure. The Accounting Review, 94(6), 1–30. https://doi.org/10.2308/accr-52359

- Bame-Aldred, C. W., Cullen, J. B., Martin, K. D., & Parboteeah, K. P. (2013). National culture and firm-level tax evasion. Journal of Business Research, 66(3), 390–396. https://doi.org/10.1016/j.jbusres.2011.08.020

- Beasley, M. S., Carcello, J. V., Hermanson, D. R., & Neal, T. L. (2010). Fraudulent financial reporting 1998-2007: An analysis of US public companies. Committee of Sponsoring Organizations of the Treadway Commission. Retrieved from COSO Website: https://www.Coso.Org/Documents/COSO-Fraud-Study-2010-001.Pdf.

- Bernhofer, J., Costantini, F., & Kovacic, M. (2023). Risk attitudes, investment behavior and linguistic variation. Journal of Human Resources, 58(4), 1207–1241. https://doi.org/10.3368/jhr.59.2.0119-9999R2

- Bloomberg. (2016). Apple ordered to pay up to $14.5 billion in an EU tax clampdown. Bloomberg.Com. https://www.bloomberg.com/news/articles/2016-08-30/apple-ordered-to-pay-up-to-14-5-billion-in-eu-tax-crackdown

- Boateng, A., Wang, Y., Ntim, C., & Glaister, K. W. (2021). National culture, corporate governance and corruption: A cross‐country analysis. International Journal of Finance & Economics, 26(3), 3852–3874. https://doi.org/10.1002/ijfe.1991

- Bonetti, P., Magnan, M. L., & Parbonetti, A. (2016). The influence of country‐and firm‐level governance on financial reporting quality: Revisiting the evidence. Journal of Business Finance & Accounting, 43(9–10), 1059–1094. https://doi.org/10.1111/jbfa.12220

- Bozanic, Z., Hoopes, J. L., Thornock, J. R., & Williams, B. M. (2017). IRS attention. Journal of Accounting Research, 55(1), 79–114. https://doi.org/10.1111/1475-679X.12154

- Chen, M. K. (2013). The effect of language on economic behavior: Evidence from savings rates, health behaviors, and retirement assets. American Economic Review, 103(2), 690–731. https://doi.org/10.1257/aer.103.2.690

- Chen, S., Chen, X., Cheng, Q., & Shevlin, T. (2010). Are family firms more tax aggressive than non-family firms? Journal of Financial Economics, 95(1), 41–61. https://doi.org/10.1016/j.jfineco.2009.02.003

- Chen, S., Cronqvist, H., Ni, S., & Zhang, F. (2015). Languages and corporate cash holdings: International evidence. In Technical Report. China Europe International Business School.

- Cheng, C. S. A., Kim, J., Rhee, M., & Zhou, J. (2022). Time orientation in languages and tax avoidance. Journal of Business Ethics, 180(2) , 625–650. https://doi.org/10.1007/s10551-021-04892-3

- Cho, H. J., Choi, S., Lee, W. J., & Yang, S. Y. (2016). Regional Crime Rates and reporting quality: Evidence from private firms in London. Working Paper.

- Cloyd, C. B. (1995). The effects of financial accounting conformity on recommendations of tax preparers. The Journal of the American Taxation Association, 17(2), 50.

- Cloyd, C. B., Pratt, J., & Stock, T. (1996). The use of financial accounting choice to support aggressive tax positions: Public and private firms. Journal of Accounting Research, 34(1), 23–43. https://doi.org/10.2307/2491330

- Dahl, Ö. (1985). Tense and aspect systems.

- Dahl, Ö. (2000). The tense-aspect systems of European languages in a typological perspective. In Tense and Aspect in the Languages of Europe (Vol. 6, pp. 3–26). De Gruyter Mouton. https://doi.org/10.1515/9783110197099.1.3

- Dahl, Ö. (2008). The grammar of future time reference in European languages Ö. Dahl (ed.). De Gruyter Mouton. https://doi.org/10.1515/9783110197099.2.309

- Daniel, S. J., Cieslewicz, J. K., & Pourjalali, H. (2012). The impact of national economic culture and country-level institutional environment on corporate governance practices. Management International Review, 52(3), 365–394. https://doi.org/10.1007/s11575-011-0108-x

- Department of Justice. (2014). Report to congress on the activities and operations of the public integrity section, criminal division. https://www.justice.gov/criminal/file/798261/download

- Desai, M. A., & Dharmapala, D. (2009a). Corporate tax avoidance and firm value. The Review of Economics and Statistics, 91(3), 537–546. https://doi.org/10.1162/rest.91.3.537

- Desai, M. A., & Dharmapala, D. (2009b). Earnings management, corporate tax shelters, and book-tax alignment. National Tax Journal, 62(1), 169–186. https://doi.org/10.17310/ntj.2009.1.08

- Desai, M. A., Dyck, A., & Zingales, L. (2007). Theft and taxes. Journal of Financial Economics, 84(3), 591–623. https://doi.org/10.1016/j.jfineco.2006.05.005

- Ding, R., Liu, M., Wang, T., & Wu, Z. (2021). The impact of climate risk on earnings management: International evidence. Journal of Accounting and Public Policy, 40(2), 106818. https://doi.org/10.1016/j.jaccpubpol.2021.106818

- Dyreng, S. D., Hanlon, M., & Maydew, E. L. (2008). Long‐run corporate tax avoidance. The Accounting Review, 83(1), 61–82. https://doi.org/10.2308/accr.2008.83.1.61

- El-Helaly, M., Ntim, C. G., & Al-Gazzar, M. (2020). Diffusion theory, national corruption and IFRS adoption around the world. Journal of International Accounting, Auditing & Taxation, 38, 100305. https://doi.org/10.1016/j.intaccaudtax.2020.100305

- Erickson, M., Hanlon, M., & Maydew, E. L. (2004). How much will firms pay for earnings that do not exist? Evidence of taxes paid on allegedly fraudulent earnings. The Accounting Review, 79(2), 387–408. https://doi.org/10.2308/accr.2004.79.2.387

- Everest‐Phillips, M. (2010). State‐building taxation for developing countries: Principles for reform. Development Policy Review, 28(1), 75–96. https://doi.org/10.1111/j.1467-7679.2010.00475.x

- Everest-Phillips, M., & Sandall, R. (2009). Linking business tax reform with governance: How to measure success.

- González, J. S., & García-Meca, E. (2014). Does corporate governance influence earnings management in Latin American markets? Journal of Business Ethics, 121(3), 419–440. https://doi.org/10.1007/s10551-013-1700-8

- Graham, J. R., Hanlon, M., Shevlin, T., & Shroff, N. (2014). Incentives for tax planning and avoidance: Evidence from the field. The Accounting Review, 89(3), 991–1023. https://doi.org/10.2308/accr-50678

- Guenther, D. A. (1994). Earnings management in response to corporate tax rate changes: Evidence from the 1986 tax reform act. The Accounting Review, 69(1), 230–243.

- Hanlon, M., & Heitzman, S. (2010). A review of tax research. Journal of Accounting and Economics, 50(2–3), 127–178. https://doi.org/10.1016/j.jacceco.2010.09.002

- Hanlon, M., & Slemrod, J. (2009). What does tax aggressiveness signal? Evidence from stock price reactions to news about tax shelter involvement. Journal of Public Economics, 93(1–2), 126–141. https://doi.org/10.1016/j.jpubeco.2008.09.004

- Harymawan, I., Anridho, N., Minanurohman, A., Ningsih, S., Kamarudin, K. A., & Raharjo, Y. (2023). Do more masculine-faced CEOs reflect more tax avoidance? Evidence from Indonesia. Cogent Business & Management, 10(1), 2171644. https://doi.org/10.1080/23311975.2023.2171644

- Harymawan, I., & Nowland, J. (2016). Political connections and earnings quality: How do connected firms respond to changes in political stability and government effectiveness? International Journal of Accounting & Information Management, 24(4), 339–356. https://doi.org/10.1108/IJAIM-05-2016-0056

- Hofstede, G. (2011). Dimensionalizing cultures: The Hofstede model in context. Online Readings in Psychology & Culture, 2(1), 919–2307. https://doi.org/10.9707/2307-0919.1014

- Hofstede, G., Hofstede, G. J., & Minkov, M. (2005). Cultures and organizations: Software of the mind (Vol. 2). Mcgraw-hill New York.

- Huňady, J., & Orviská, M. (2015). The effect of corruption on tax revenue in OECD and Latin America countries. Theoretical and Practical Aspects of Public Finance, 1(1), 80.

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Kaufmann, D., Kraay, A., & Mastruzzi, M. (2011). The worldwide governance indicators: Methodology and analytical issues1. Hague Journal on the Rule of Law, 3(2), 220–246. https://doi.org/10.1017/S1876404511200046