?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The research on corporate social responsibility (CSR) has taken on particular importance in the current banking literature. This literature focused on the direct effect of CSR on bank performance. However, this study fills this gap by examining the relationship between CSR and Islamic bank stability (IBS). More specifically, it examined, on the one hand, the non-linear relationship between CSR and IBS and, on the other hand, the moderating effect of governance practices (Sharia supervisory board, governance structure, institutional quality) on CSR-IBS nexus. To do this, we selected a group of 43 Islamic banks operated in Gulf Cooperation Council countries over a period from 2012 to 2020. The results obtained using the System GMM method showed that there is a U-shaped relationship between CSR and IBS. Furthermore, they revealed that governance practices have a moderating effect on the relationship between CSR and IBS. Our findings indicate that the combination of corporate social responsibility and governance practices enhances IBS, but a bank risk could occur due to weak governance practices. These findings are likely to be useful for managers, policymakers, and stakeholders. Managers should prioritize CSR aligned with core objectives, enhancing reputation and stability, while a balanced approach is recommended to avoid financial risks. GCC policymakers should encourage CSR in line with national development goals, incorporating responsible practice indicators and appropriate governance standards to ensure stable operations. Stakeholders should consider a moderate level of CSR to enhance trust, returns, industry resilience and employee satisfaction, adapting the implications for sustainable banking stability.

1. Introduction

In recent years, there has been significant interest in corporate social responsibility (CSR) from companies, policymakers, regulators, and stakeholders. CSR refers to a company’s voluntary actions to address social, environmental, and ethical issues in its operations and business practices. It is becoming increasingly important for companies to engage in CSR as customers and investors are increasingly demanding that companies take responsibility for their impact on society and environment (Farah et al., Citation2021). For banks, CSR is especially relevant as they play a critical role in the financial system and have significant economic and social impact. Banks that engage in CSR activities can contribute to sustainable development and promote social and environmental well-being (Mallin et al., Citation2014). This can help banks build a positive reputation and strengthen relationships with their stakeholders.

In academic literature, studies that have been conducted on CSR have mainly focused on how it affects a firm’s performance. Some studies have found a positive relationship between CSR and a firm’s performance (e.g., Cornett et al., Citation2016; Nguyen et al., Citation2017). However, other studies have suggested an inconclusive or negative relationship between CSR and firm performance (e.g., Wright & Ferris, Citation1997). In addition, in recent times, there has been significant focus on the relationship between CSR and risk. Engaging in CSR activities does not necessarily mean that banks are immune to risk. In the extensive literature, some studies suggested that CSR can mitigate risk by counteracting the negative impacts of unfavorable events (e.g., Godfrey et al., Citation2009; Nguyen & Reiter, Citation2015). However, other studies recommended that the CSR increases the risk due to entrenched management (Bouslah et al., Citation2023). In fact, CSR activities can sometimes expose banks to additional risks. For example, if a bank invests in socially responsible projects or companies that are not financially viable, it could result in losses and reputational damage.

Based on this literature, it appears that studies have indicated that the relationship between CSR and risk can be positive or negative depending on the nature of the CSR activities involved. Therefore, the evidence suggests that it is important to think beyond the simple assumption of a direct positive or negative relationship (linear model) between CSR and risk (Farah et al., Citation2021). Therefore, this research intends to contribute to filling this research gap by examining whether such a CSR-Islamic bank stability (IBS) nexus. More precisely, this article presumes that the relationship between CSR and IBS is likely to follow a U-shaped (Curvilinear) trend. Therefore, the U-shaped relationship indicates two types of banks: those whose level of risk (financial stability) increases (decreases) as they should better implement CSR, but only up to a certain point (threshold) where managers start to improve their CSR practices, and those that exceed the optimal level, resulting in enhanced financial stability. This study suggests that CSR does not necessarily lead to an increase in IBS, and that a certain threshold of governance must be reached by Gulf Cooperation Council (GCC) Islamic banks to improve their banking stability.

In addition, the impact of CSR on the IBS should be assessed reflecting the important impacts that other factors have on this relationship. Particularly, governance practices (GP) (Sharia supervisory board (SSB), governance structure (GS) and institutional quality (IQI)) an approach aimed at satisfying shareholder-managers (and/or lender-managers) that has much in common with CSR—plays a significant role in controlling the impacts of CSR on the IBS. Specifically, it is worth noting that improved governance practice can help reduce bank risk (Elgattani & Hussainey, Citation2020; Salim et al., Citation2023). According to agency theory, CSR initiatives have the potential to increase shareholder value and decrease the risk faced by banks, but only if they are implemented in a well-planned and well-governed manner. If governance is lacking, CSR programs may prioritize satisfying stakeholders rather than maximizing shareholder value, which could endanger the bank’s stability (Fama & Jensen, Citation1983; Jensen & Meckling, Citation1976). Although some studies indicate that CSR and GP affect IBS, another gap in the existing study concerns the possible correlation between CSR and GP, as they are two approaches with similar objectives (reducing conflicts of interest and enhance the financial stability (FS)). In other words, the interaction between these two determinants (moderating effect) needs to be investigated.

There are several stylized factors for this study. First, CSR and Islamic banking are aligned in terms of shared values and goals, including justice, fairness, transparency, accountability, and the promotion of social welfare. Thus, CSR can be seen as a coherent extension of the Islamic bank’s mission and vision. Second, implementing CSR can enhance IBS by strengthening their reputation, increasing customer loyalty, improving employee satisfaction, optimizing risk management, and ensuring regulatory compliance. In addition, CSR can serve as a lever for Islamic banks to make progress towards achieving the Sustainable Development Goals (SDGs) set by the United Nations. The 17 SDGs represent a set of global goals aimed at addressing a range of economic, social, and environmental challenges. Third, CSR also creates challenges and constraints for IBS. These include the lack of clear and uniform standards, measures and indicators of CSR performance, the delicate balance between profitability and social commitment, the potential conflict between Sharia principles and certain Sustainable Development Goals, and the need for greater engagement and cooperation with stakeholders (Umar et al., Citation2022; Zafar & Sulaiman, Citation2019).

This study makes a tow important contribution to the literature. First, we examine the non-linear (curvilinear) relationship between CSR disclosure and IBS in GCC countries. Most previous studies have focused on the linear relationship between CSR and bank stability. To our knowledge, this study is the first to address the curvilinear relationship between CSR disclosure and IBS. Second, we investigate the moderating effect of GP on CSR disclosure-IBS nexus. More specifically, we study the moderating effect of each governance characteristic, i.e., SSB, GS, and IQI.

Although several studies on the impact of CSR on financial stability have been conducted in other countries and regions, there are few studies in emerging countries such as GCC countries. There are several relevant motivations for choosing the GCC region. Firstly, this choice depends essentially on the main objective of our research, which is to examine the effect of CSR and governance on the financial stability of Islamic banks. Second, according to Wilson (Citation2009, p. 2), the GCC states are positioned as world leaders in Islamic banking and finance. This pre-eminence is notably reflected in the 31.29% share of total regional banking sector assets held by the GCC Islamic banking sector. In addition, Islamic banks operating in the GCC operate in similar economic contexts, lending further consistency to the analysis. This homogeneity reinforces the relevance of our study in this specific region. Finally, the extent of Islamic governance differs markedly from conventional governance. Based on Sharia principles, Islamic financial institutions emphasize equity, social responsibility, and the rejection of self-interest. This unique orientation influences the decision-making and operational processes within these institutions, resulting in marked differences from conventional governance patterns (Mollah & Zaman, Citation2015; Platonova et al., Citation2018; Raouf & Ahmed, Citation2022). That being said, this research aims to answer the following research questions:

RQ1:

Does CSR have a U-shaped effect on IBS?

RQ2:

Is GP able to exert a moderating effect over the CSR-IBS nexus?

Through a two step system generalized method of moments (GMM), run on a sample of GCC Islamic banks, this paper investigates the non-linear relationship between CSR and IBS, by considering that managers-shareholders may react positively (negatively) to high (low) levels of CSR. The manager-shareholder lens implemented in this study also allows us to provide the first evidence that the involvement of Islamic banks in GP affects the curvilinear effect of CSR on their financial stability. The implementation of these different practices with similar objectives reduces the advantages that CSR has on IBS. More specifically, this paper considers the GP (SSB, GS, and IQI) to assess whether CSR practices are beneficial or not for the IBS.

The organization of the paper is as follows: Section 2 will commence and analyze the relevant literature, Section 3 will describe the methodology and variables used in the study, Section 4 will present and discuss the findings, and Section 5 will offer a conclusion.

2. Literature review and hypotheses

2.1. CSR and financial stability

Based on several theoretical studies, there are two main theories that can be proposed to explain the relationship between CSR and bank stability: agency and stakeholder theories. Under agency theory, CSR can lead to overinvestment, which can negatively affect firm financial stability. Overinvestment occurs when a firm invests too much in social and environmental initiatives at the expense of its core business activities (Barnea & Rubin, Citation2010). This can happen when management seeks to satisfy the demands of stakeholders, including customers, employees, and society at large, without considering the interests of shareholders. In this case, the cost of CSR initiatives can reduce the profits available to shareholders and create a situation where management is not acting in the best interests of shareholders. This can lead to conflicts between shareholders and management and may ultimately threaten the stability of the firms. Therefore, CSR could have a negative impact on its FS (Friedman, Citation1970; Jensen & Meckling, Citation1976). Under stakeholder theory, CSR is a means for firms to balance the interests of all stakeholders, not just shareholders. By considering the interests of customers, employees, and society at large, firms can create long-term value and enhance their reputation, leading to increased stability over time (Carroll, Citation1979; Freeman, Citation1984).

Some empirical studies have highlighted the existence of a positive relationship between CSR and FS in the banking sector, along with their respective theoretical frameworks (e.g., Belasri et al., Citation2020; Chollet & Sandwidi, Citation2018; Gambetta et al., Citation2017; Neitzert & Petras, Citation2022; Ramzan et al., Citation2021; Gaies & Jahmane, Citation2022). However, other studies have found evidence of a negative relationship between CSR and FS, both in developed and developing countries confirming the agency theory predictions (e.g., Salim et al., Citation2023). In addition, the literature suggested that the relationship between CSR and risk could be non-linear. For instance, El Khoury et al. (Citation2022) showed a non-linear (inverted U-shaped) relationship between environmental, social & Governance (ESG) and bank performance in the Middle East and North Africa (MENA) region.

The combination of different types of evidence suggests that it is necessary to consider a more complex relationship between CSR and FS, which goes beyond a simple positive or negative linear relationship. The proposition is that the relationship between CSR and FS can be better represented as a curvilinear rather than a linear relationship. As noted previously, most research on CSR has focused on its effects on the corporate financial performance or on the risk of conventional banking sector. This study aims to fill a gap by examining the CSR-IBS nexus in the Islamic banking sector. Specifically, the study suggests that the link between CSR and IBS is likely to demonstrate a U-shaped relationship. Our theoretical perspective is based on agency and stakeholder theories. Based on the above discussion, we formulate our first hypothesis as follows:

Hypothesis 1.

There is a U-shaped relationship between CSR and IBS.

2.2. Moderating effect of governance practices

The effectiveness of CSR practices should be considered as one of the major investment decisions (Wibisono, Citation2007), requiring the implementation of appropriate policies and programs to meet the needs and expectations of all stakeholders. This decision can help reduce information asymmetry. CSR can play a significant role in avoiding conflicts of interest among all stakeholders, which can ensure the long-term stability of banks. Such influence, however, seems to vary according to economies (developed or developing) and even between different types of banks (conventional or Islamic). CSR practices are more common and advanced in developed economies than in developing economies. However, firms in developing economies often have limited resources and face challenges such as unstable regulatory environments and insufficient infrastructure, which can make it more difficult to establish strong CSR practices (Bagh et al., Citation2017; Wibisono, Citation2007).

Moreover, Islamic banks have a different approach to CSR compared to conventional banks, due to their adherence to Sharia principles and their commitment to participatory financing and community development. However, there is no argument suggesting that CSR in Islamic banks is stronger than that of conventional banks. Nonetheless, theoretical, and empirical evidence highlights the need for the implementation of strong corporate governance mechanisms to ensure transparent, responsible, and ethical management of the firm, which can ensure sustainable financial stability (Ullah et al., Citation2014). The governance structure of Islamic banks enables them to take higher risks and achieve better performance using complex financial products and sophisticated transaction mechanisms (Mollah et al., Citation2017).

The moderating effect of GP on CSR-IBS nexus can be also explained by agency and stakeholder theories. Under agency theory, the role of governance is to align the interests of shareholders and management, and to reduce agency costs. Indeed, good if a bank’s governance structure is strong, CSR initiatives can be implemented in a way that maximizes shareholder value and reduces bank risk and vice versa. In addition, investors maintain their stake through corporate governance practices against any expropriation by the management and other players of the corporation (Fama & Jensen, Citation1983; Jensen & Meckling, Citation1976). Under stakeholder theory, governance has a broader role in ensuring that a firm considers the interests of all stakeholders, not just shareholders. By incorporating stakeholder perspectives into decision-making processes, banks can ensure that their CSR initiatives are aligned with the interests of all stakeholders, which can lead to increased financial stability over the long-term (Freeman, Citation1984).

In practice, most studies of GP investigated its direct or moderating effects on sustainability performance in the banking industry (e.g., Saadaoui & Ben Salah, Citation2022; Tunio et al., Citation2021). Some studies examined the linear relationship between corporate governance mechanism and Islamic and conventional bank performance (e.g., Buallay, Citation2019; Elgattani & Hussainey, Citation2020; Grassa, Citation2016, Jan et al., Citation2019; Wu & Shen, Citation2013), confirming the predictions of agency and stakeholder theories. If we consider the specificities of the governance structure of Islamic banks, most studies in this area have examined the impact of the SSB and other governance mechanisms on financial performance or risk disclosure (e.g., Mukhibad & Nurkhin, Citation2020; Elamer et al., Citation2020).

However, few studies investigated the moderating effect of GP or other factors on CSR -FS nexus in the banking industry (e.g., Salim et al., Citation2023). Most previous studies that examined the moderating effect of CG on the CSR-firm performance nexus have been conducted on non-financial firms (e.g., Galbreath, Citation2013; Pham & Tran, Citation2020; Zahid et al., Citation2022). Consequently, the research has become more specific, and there has been a decrease in attention towards other possible fields of study.

Moreover, IQI has a substantial impact on the bank stability. Indeed, countries that have superior institutional quality generally have banking systems that are more stable (Beck & Feyen, Citation2013). The reason behind this is that robust institutions, like sound regulatory structures and a fair legal system, lessen the possibility of financial catastrophes and increase the ability of banks to withstand sudden shocks. Conversely, weak institutions can lead to a lack of confidence in the banking industry, resulting in bank runs and financial insecurity. In addition, IQI could reduce information asymmetry and transaction costs (Çam & Özer, Citation2021). In this context, Khan et al. (Citation2020) have demonstrated that institutional quality promotes financial development and acts as a positive moderating factor in the relationship between natural resource rents and financial development in the specific context of Pakistan. Athari (Citation2021a) concluded that the profitability of Ukrainian banks is affected both positively and negatively by domestic political stability. The author also found that uncertainty linked to global economic policy is identified as having a significantly negative effect on this profitability. According to Athari (Citation2021b), Nigerian banks tend to reduce dividend payouts and align them with the agency model of dividend substitution due to weak institutional parameters. Additionally, the study revealed that these banks increase dividend payments when presented with growth opportunities, using it as a substitution mechanism to address agency problems and build a positive reputation. In a study of Islamic banks operating in Arab markets, Athari and Bahreini (Citation2023) assessed the effects of external governance mechanisms and regulatory parameters on their profitability. The authors concluded that external governance mechanisms, including political stability, regulatory quality, rule of law and control of corruption, have a positive impact on the profitability of Islamic banks. However, the regulatory framework (particularly the extent of disclosure and the ease of shareholder lawsuits) reduces their profitability. Athari and Irani (Citation2022) found a correlation between better governance at country level and higher capital ratios. He also concluded that Islamic banks improve their capital ratios by taking anti-corruption measures, promoting political stability, increasing government efficiency, and strengthening legal systems. Ali et al. (Citation2022) concluded that the correlation between economic governance, natural resource rents and financial inclusion promotes environmental sustainability by significantly reducing our ecological footprint. Recently, Ali et al. (Citation2023) concluded that good governance could serve to mitigate the adverse impact of economic policy uncertainty on financial stability in both developed and developing countries. However, this influence manifests itself differently from one region to another. In addition, Athari et al. (Citation2023) conducted an econometric study to examine the moderating effect of national governance between corporate responsibility and the exposure of environments to risk factors. The main results highlighted the importance of the moderating role played by national governance. By improving the quality of national governance, it would be possible to mitigate the impact of country-specific financial, economic, and political risks on credit risk. Furthermore, the results suggested that the increase in liquidity, profitability, capital requirements and income diversification lead to a decrease in credit risk. On the other hand, an increase in inefficiency leads to an increase in credit risk. The most important conclusion of this study is that national governance is a key determinant in the management of financial risks.

However, the moderating effect of IQI on the CSR-FS has not yet been examined empirically in Islamic banks. Therefore, we formulate our second hypothesis as follows:

Hypothesis 2.

GP moderates the relationship between CSR and IBS.

H2 (a):

SSB moderates the relationship between CSR and IBS.

H2 (b):

CGS structure moderates the relationship between CSR and IBS.

H2 (c):

IQI moderates the relationship between CSR and IBS.

3. Data and methodology

3.1. Data collection

In this paper, we used a sample of 43 listed IBs from the six GCC countries (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE) from 2012 to 2020. For CSR and GS, we use hand-collected data from yearly reports published on the websites of various banks. The database was used to obtain financial data for banks. The World Development Indicator (WDI) of the World Bank is used to collect macroeconomic indicators. Each country’s sample characteristics are shown in Table .

Table 1. Distribution of firms

3.2. Variables definitions

3.2.1. Dependent variable

In this study, we employed the Z-score to gauge the individual bank stability by assessing the likelihood of insolvency (e.g., Ali et al., Citation2023; Athari & Irani, Citation2022; Fernández et al., Citation2016; Guidi, Citation2021; Iannotta et al., Citation2007; Kasman & Kasman, Citation2015; Laeven & Levine, Citation2009; Schaeck & Cihák, Citation2014). It measures the probability of insolvency at the bank level. The probability of insolvency is higher when the Z-score value is lower, and vice versa (for a more details, see Lepetit & Strobel, Citation2013). In this study, we use the Z-score (IBS) according to the following formula:

Where is return on assets for bank i at time t,

is the ratio of total equity divided by total assets of bank i at a time t, and

is the standard deviation of ROA of bank i at time t. Following, among others, Kasman & Kasman (Citation2015) and Guidi (Citation2021), we calculated the standard deviation of by using a three-year rolling window approach.

3.2.2. Main independent variable

To measure CSR, we follow Mallin et al. (Citation2014) adopting the CSR disclosure index incorporates items (Maali et al., Citation2006; Haniffa & Hudaib, Citation2007). To do so, we used 10 dimensions including 84 items also includes items from AAOFI Standard No.7. In addition, we treated each item as a dummy variable, assigning a value of one if the item appeared in the annual reports/websites and zero otherwise. Thus, the index is equally weighted to prevent any potential scoring and scaling biases as presented in equation (2).

where is CSR index,

is the number of items expected for bank i, and

is a dummy variable which takes the value of 1 if the item is disclosed and 0 otherwise.

3.2.3. Moderator variables

To examine the moderating role of governance practices, we constructed three governance indices. The first index is the SSB score which consists of five dimensions namely, number of SSB (dummy variable that takes 1 if the bank has one or more members of SSB and zero otherwise (SSBN)), educational qualification of SSB members (dummy variable that takes 1 if firms have an SSB member with a PhD and 0 otherwise (SSBEQ)), expertise of SSB (dummy variable that takes 1 if companies have an experienced SSB member and 0 otherwise (SSBEXP)), Reputation of SSB (dummy variable which is equal to 1 if bank have a member of the SSB who has knowledge and expertise in Islamic business law and 0 otherwise (SSBR)), and cross-members of SSB (dummy variable that takes 1 if firms have an SSB member with cross-members and 0 otherwise (SSBCM)). To do this, we then combine these indicators using principal component analysis (PCA) approach. PCA aggregates the variables combined with each factor into a distinct composite score and avoids multicollinearity and reduces measurement error.

The second is CG index which is composed of four dimensions. Depending on data availability, we construct our governance score (GS) based on four internal governance indicators namely board size, board independent, CEO duality, and gender diversification (Koseoglu et al., Citation2021). To do this, we also combine these indicators using PCA approach. Table summarize the definition of this indicators.

The third index is composed of institutional quality (IQI) is a composite measure. According to Kaufmann etCitation2011 al. (2011), there are six dimensions of country governance namely Voice and Accountability (VA), Political Stability (PS), Government Quality (GE), Regulatory Quality (RQ), Rule of Law (ROL), and Control of Corruption (COC). Various sets of values were utilized to measure certain aspects such as the effectiveness of the government from 0 to 4, the quality of regulations and political stability from 0 to 12, and corruption, accountability, and rule of law from 0 to 6. Higher values represented more robust institutions. A higher score means better governance. Also, we employ PCA to combine these indicators. For these three governance indices, we normalize them (using the min-max normalization technique) assigned to each country on a scale of 0 to 1 to facilitate analysis.

3.2.4. Control variables

In investigating the relationship between CSR and IBS, we control for several bank and country level variables. We follow previous studies (e.g., Anginer et al., Citation2014; Ali et al., Citation2023; Athari & Irani, Citation2022; Athari & Bahreini, Citation2023; Athari et al., Citation2023; Fu et al., Citation2014; Khémiri et al., Citation2023; Saliba et al., Citation2023) in the literature to control for asset quality (AQ), bank efficiency (ME), bank age (AGE), bank size (SIZE), and liquidity (LIQ) in our study. For each bank, each year, we use the ratio of loan loss provisions to gross loans to measure asset quality (AQ), the cost to income ratio to measure the bank efficiency (ME), the logarithm of the number of years since bank creation to measure bank age (AGE), the logarithm of the total assets to calculate bank size (SIZE), and the ratio liquid assets to deposits and short term funding to measure liquidity (LIQ). To consider macroeconomic conditions, we introduce in the model to be estimated growth rate of the GDP per capita (GDPG).

3.3. Econometric model

In this study, we investigate the non-linear relationship between CSR and IBS of IBs, as well as the moderating effect of GP on the CSR-IBS nexus. Specifically, we test the two hypotheses as mentioned earlier. The baseline model is developed to test our first hypothesis. Specifically, this model aims to examine the U-shaped relationship between CSR and IBS. To do this, we applied the estimated model can be formulated as follows:

Where is the Islamic bank stability for country c, firm i at time t,

is one year lag of IBS,

is the CSR for country c, firm i at time t,

is the square term of CSR examining the U-shaped relationship,

is the vector of control variables, and

is the error term.

To analysis the area of bank risk, several studies employed system GMM (e.g., Jiménez et al., Citation2013; Maghyereh et al., Citation2022; Maghyereh & Yamani, Citation2022). The use of system GMM has several advantages. First, system GMM can attenuate the problems of omitted variables, measurement errors, dynamic panel heterogeneity, and potential endogeneity due to any independent variables correlated with the error term. Second, it is effective when a panel has a smaller time dimension, such as ours, (T is equal to 9) compared to its cross-sectional dimension (N is equal to 43). However, the test for autocorrelation in the second order of AR (2) model did not show any significant results, indicating the absence of autocorrelation (Arellano & Bond, Citation1991). This implies that the lag structure of the model is appropriate and only one lag for the IBS variable is needed. To ensure the accuracy of the dynamic GMM estimation technique, suitable instruments were used, such as lagged values of t-1 and t-2 for the difference equation and a single lag for the level equation. The reliability of these instruments was evaluated using the Hansen J statistic of over-identifying restrictions, which indicates that the instruments used are reliable for the models.

The baseline model will be modified to investigate the moderating effects of GS on the CSR-IBS nexus testing second hypothesis. Specifically, in model (2) we add the interaction terms as follows:

4. Findings and discussions

4.1. Statistical analyses

The Table presents the descriptive statistics for all variables used in this study, covering both the dependent and independent variables across the 387 observations collected. The Z-score variable has a mean of 2.698, a standard deviation of 1.129, a minimum value of − 1.305, and a maximum value of 5.141. This indicates that the Islamic banks in the GCC countries over the period 2012–2020 is relatively stable. Similarly, CSR variable has a mean of 0.258 and a standard deviation of 0.168, indicating that a relatively low level of CSR disclosure, although Islamic ethics is at the core of Islamic banking (Platonova et al., Citation2018). The GS variable has a mean of 0.603 and a standard deviation of 0. 201, suggesting that a quite level of GS. The SSB variable has a mean of 0.286 and a standard deviation of 0.197, indicating that a relatively low level of SSB. The IQI has a mean 0.467 and a standard deviation of 0.197, suggesting that a relatively low level of IQI. In terms of the control variables, they have a positive sign.

Table 2. Descriptive statistics

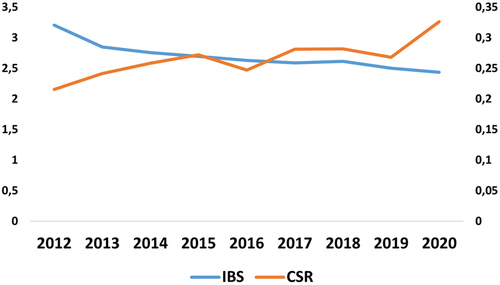

Figure depicts the average IBS measured by the logarithm of Z-score and the average CSR disclosure of GCC countries over the study period from 2012 to 2020. From this figure, it can be observed that Islamic banks are characterized by a certain stability despite the slight decrease between the 2013–2020 period. However, CSR disclosure shows an upward trend over this period. This could be explained by Islamic banks’ awareness of the importance of CSR in improving their competitiveness, reputation, and financial stability.

Figure 1. The IBS and CSR in GCC countries from 2012–2020.

Table indicates that there is probably no issue with multicollinearity in the study’s empirical models because none of the correlation coefficients between the exogenous variables are higher than 0.80. If the correlation coefficients between the regressors are below 0.80, multicollinearity should not significantly affect the multiple regression analysis (Gujarati, 2004).

Table 3. Matrix correlation coefficients

From Table , the result of variance inflation factor VIF is less than 10, suggesting that there is no multicollinearity among variables.

Table 4. Results of variance inflation factor

4.2. Baseline results

The objective of this subsection is to assess the U-shaped between CSR and FS of Islamic banks in the GCC region, using the two-step GMM estimator. The results of the J-Hansen test, presented in Table , indicate that the null hypothesis of instrumental variables is valid, which enhances the reliability of the estimator used. Additionally, the results of the AR (2) test confirm the absence of second-order correlation, further strengthening the validity of the estimator. These results allow us to affirm that the two-step GMM estimator is an appropriate choice for this study. Column 1 reported the results of linear model; and column 2 reported the curvilinear model.

Table 5. CSR and IBS: baseline results

The coefficient of lagged IBS is significantly positive, suggesting that current IBS increases with an increase in IBS of the previous period. For every 10.0% increase in the IBS of the previous period, the current IBS of linear (column 1) and nonlinear (column 2) models increases by 6.0% and 1.8%, respectively. These results indicate that a decrease in previous IBS limits the growth of current IBS.

In addition, the result, reported in column 1 (Table ), showed that the CSR has a significantly positive effect on IBS. Specifically, for 10.0% increase in CSR will lead to a 4.0% increase in IBS. This result can be explained by the fact that CSR can help to improve a bank’s reputation. A good reputation can make it easier for a bank to attract and retain customers, investors, and employees. This can help to reduce a bank’s risk of failure.

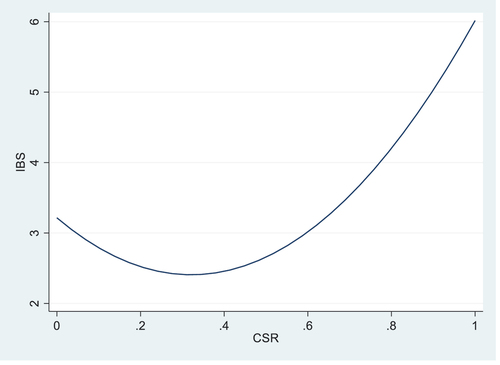

However, this result could be better apprehended by test the U-shaped relationship between CSR and IBS. The result reported in column 2 (Table ) indicates that the coefficient of CSR quadratic term has a positive impact on IBS when the U-shaped curve is verified. However, simply obtaining a result is insufficient to validate the existence of the inverted U-shaped curve. To establish the curve’s validity, it is necessary to examine the lower and upper bounds of the relationship as well as the extreme point. For a U-shaped curve to be valid, the slope of the lower bound must be negative and significant, while the slope of the upper bound must be positive and significant (Lind & Mehlum, Citation2010). The extreme point must be positioned between the extreme values of the curve. According to Lind and Mehlum (Citation2010), we used the test for the presence of a U-shaped (or inverse U-shaped) relationship over an interval. To do this, we used the “utest” command in STATA 17. This test identifies the method used and provides results based on the hypothesis test as to whether the relationship is decreasing at the beginning of the interval and increasing at the end, or vice versa. The result is reported in Table . All these conditions are met proving that the relationship between CSR and IBS is U-shaped and supporting hypothesis 1.

Table 6. Test for the U-shaped curve

Banks on the left side of the curve in Figure experience decreasing IBS as their CSR levels increase, while those on the right side of the curve witness an exponential increase in IBS as their CSR levels rise after the extreme point. Specifically, this correlation changes from negative to positive, indicating that as levels of CSR increase, levels of bank stability of GCC banks increase. Specifically, there is an optimal level of CSR, which is equal to 32.1%, below which the benefits for Islamic banks increase. In other words, if Islamic banks do not invest sufficiently in CSR practices up to a certain level, it may lead to a decrease in their financial stability. This finding supports the acceptance of agency theory. However, above this threshold, improving investment decisions in CSR practices leads to an increase in their stability. Gambetta et al. (Citation2017) found that European banks with higher ESG scores are less risky than those with lower scores. From this result, it appears that levels of CSR in GCC banks are still on the rise. This result is consistent with the predictions of stakeholder theory. It aligns with the findings of Chollet and Sandwidi (Citation2018), Ramzan et al. (Citation2021) and Neitzert and Petras (Citation2022).

Figure 2. The U-shaped relationship between CSR and IBS.

As for the control variables, we observe that all coefficients of control variables are statistically significant, except for AGE. The asset quality, efficiency, size have a negative effect, but LIQ and GDPG have a positive impact.

4.3. Moderating effects

The previous results suggest the existence of a U-shaped relationship between CSR and IBS. However, as mentioned above, the good governance practices can be enhancing the IBS, but they remain weak due to the increasing levels of information asymmetry among the different stakeholders. To mitigate the problems of information asymmetry, it appears that a combination of CSR practices and governance is essential. This combination is likely to reduce risk and ensure financial stability. In this sub-section, we analyze the moderating effect of governance practices (SSB, SG, and IQI) on the CSR-IBS nexus.

The results presented in Table , which display the J-Hansen test outcomes, reveal that the null hypothesis of instrumental variables is valid. Furthermore, the results of the AR (2) test confirm the null hypothesis of a second-order correlation. Therefore, we can conclude that the system GMM estimator is a suitable technique for this study.

Table 7. The moderating effects of GP on CSR-IBS nexus

As for SSB moderating effect, we observe that the coefficient of the SSB variable has a significantly positive effect on IBS (column 1). For 10.0% increase in SSB will lead to a 4.0% increase in IBS. This negative effect indicates that the application of Islamic principles by SSB can generate conflicts of interest and increased agency costs. This may lead to a neglect of other aspects of bank operations, which can harm the interests of other stakeholders and negatively affect their financial stability. This result is in line with the predictions of the agency and stakeholder theories.

Let us now turn to the analysis of the moderating effect of SSB on the CSR-FS nexus. It turns out that the non-linear relationship has been detected again, but its shape has changed from positive () to negative (

), indicating the existence of an inverted U-shape (column 2). This result indicates that the application of Islamic governance prevents managers from taking on more risk and not over-investing in CSR, which can ensure their financial stability. Specifically, there exists an optimal threshold below which SSB positively moderates the relationship between CSR and IBS. In this case, the SSB helps to strengthen the confidence of investors and customers in Islamic banks by ensuring that CSR initiatives comply with Shariah principles. This finding is consistent with stakeholder theory. However, beyond this threshold, SSB negatively moderates the CSR-IBS nexus. This result reflects that over-investment in CSR activities can lead to high financial costs for Islamic banks, which could compromise their financial soundness, hence the validity of agency theory.

The result reported in column 3 indicates that the coefficient of the GS variable has a significantly negative effect on IBS. For 10.0% increase in GS will lead to a 3.1% increase in IBS. In addition, thevariable has a significantly positive effect, while the

variable was significantly negative on IBS (column 4). This finding implies that managers are risk-averse, as evidenced by the continued demonstration of an inverted U-shaped relationship between CSR and IBS. The positive moderating effect of GS on the CSR-IBS nexus is economically explained by the existence of a strong governance structure that enables banks to effectively implement clear CSR policies, which can help reduce costs associated with managing their brand image and improve stakeholder satisfaction. It can help maximize value for all stakeholders by encouraging banks to establish trusted relationships with their customers, investors, and communities, which in turn can help maintain the financial soundness of banks. However, the negative effect can be explained by the fact that even with a strong GS, excessive investment in CSR activities can generate financial risks. This can put pressure on banks’ profit margins and reduce their financial soundness. Therefore, there is a need to balance the benefits and costs of CSR.

As shown in Table , the results are like those found on the moderating effects of SSB and CG on CSR-IBS nexus. After introducing the interaction variables () into our regression model, we found that the coefficients of the

variable became positive and statistically significant at the 1% level, while the coefficient of the

variable was negative and significant at the 1% level. Statistically, this result reflects the existence of a non-linear (U-shaped) relationship between the different factors. From an economic perspective, this finding reveals that the improvement of governance at the country level encourages managers of Islamic banks to adopt and over-invest in CSR activities, which can improve their financial stability.

In this case, the positive moderating effect of IQI on the CSR-IBS nexus indicates that IQI in GCC countries is high. This can help Islamic banks to be more transparent and accountable in their business practices, including in CSR, which can improve their reputation and financial performance. It also helps them to attract more investment opportunities due to their strong reputation and adherence to strict corporate governance standards, which can facilitate access to the financial resources necessary to finance their CSR initiatives. This is likely to reduce risks and ensure more long-term financial stability. However, when a certain level is reached, excessive investment in CSR activities can harm the financial stability of Islamic banks even in the presence of high levels of regulation and supervision because excessive CSR practices can generate high costs for Islamic banks, which could compromise their financial soundness. In addition, the other control variables retained the same results obtained in the previous regressions.

4.4. Robustness check

To ensure the robustness of the empirical findings, five additional tests were carried out. First, we adopted two alternative measures of financial stability: global probability of insolvency (A_Z-score) and insolvency risk (ln (SDROA)). Following Yeyati and Micco (Citation2007) and Fiordelisi & Mare (Citation2014), we measure A_Z-score as: ; where

present the average of the ROA within each individual country c in period t. To further reduce the impact of extreme values in the Z-score distribution, we employ the natural logarithm once again for smoothing purposes. In addition, we employ the natural logarithm of standard deviation of ROA as second proxy of financial stability (i.e., insolvency risk (ln (SDROA)). The results reported in Table are like those obtained from the main findings (Table ).

Table 8. Change in dependent variable

Second, to better explore the impact of CSR and IBS, an alternative measure of CSR (CSRA) was used. To do so, we adopted the PCA method to construct the new index. Similar results to those found in previous regressions were found regarding the U-shaped relationship between CSR and IBS (see, Table ). In addition, the moderating effects of governance (SSB, GS, and IQI) and other control variables on IBS are significant. They also led to similar results as those observed in previous regressions (Table ).

Table 9. Alternative measure of CSR

Third, we analyzed the moderating effect of SSB on the SSB-IBS nexus using each SSB component as a moderating variable. The results reported in Table shows the existence of an inverted U-shaped relationship between all interaction terms of the five components of SSB and CSR and IBS.

Table 10. Decomposition of SSB

Fourth, we employed each GS component as a moderating variable to analysis the moderating effect of GS on the CSR-IBS. The results reported in Table exhibit the same results proven in Table indicating the existence of a U-shaped relationship between four components (GENDER, INDEP, com_audit, and com_risk) on IBS. However, Board size exerts an inverted U-shaped relationship on the IBS, suggesting that managers in Islamic banks are risk-conscious (see column (1)).

Table 11. Decomposition of governance structure

Fifth, we used each IQI component as a moderating variable to analysis the moderating effect of IQI on the CSR-IBS. The results reported in Table are like those obtained from the main findings (Table ).

Table 12. Decomposition of institutional quality

Sixth, we use the Two‐Stage Least Squares (2SLS) method to check the effect of endogeneity. The results reported in Table are like those obtained from the main findings (Table ).

Table 13. 2SLS results

5. Conclusion

This study attempts to examine the nonlinear relationship between CSR and IBS. To do so, we used the system GMM method. The findings show that there is a U-shaped relationship between CSR and IBS. This means that when CSR is low (high), the bank stability is limited (significant) due to the absence (presence) of investment in CSR practices. However, at an optimal level, when CSR increases (decreases), Islamic banks can improve (worsen) investment decisions in CSR practices, which can lead to an enhance (decrease) in their financial stability. These findings approve hypothesis H1, and the agency and stakeholder theories are partially accepted as they predict the existence of an optimal level of CSR. Previous IBS, financial and macroeconomic factors are also considered significant. In addition, the findings also found that there is a moderating effect of GP (SSB, GS, and IQI) on the CSR-IBS nexus, which confirms hypothesis 2.

To the best of our knowledge, our study is the first to provide evidence that GP exerts a moderating effect on CSR-IBS nexus. Our findings complement the recent literature on the issue of IBS determination and have important implications for managers, policymakers, and stakeholders’ perspectives of GCC Islamic banks. Managers of Islamic banks in GCC countries should prioritize CSR activities that are aligned with their core business objectives, such as supporting sustainable and ethical financing. This can help enhance the bank’s reputation and promote customer loyalty, which ultimately contributes to the bank’s stability. In addition, they should establish a balanced approach to CSR activities, avoiding excessive spending on CSR initiatives that may negatively impact their financial stability. The U-shaped relationship suggests that there is an optimal level of CSR spending that maximizes the bank’s stability, and managers should strive to find this balance. Policymakers in GCC countries should encourage Islamic banks to engage in CSR activities that align with national development goals, such as promoting financial inclusion and supporting small and medium-sized enterprises (SMEs). This can help enhance the social and economic impact of Islamic banks, while also promoting their stability. In addition, they should consider incorporating CSR metrics into their supervisory framework, to incentivize Islamic banks to engage in socially responsible practices. This can help promote transparency and accountability, while also improving banking stability. Finally, policymakers should encourage practices and governance standards specific to Islamic banks, to promote best practice and reinforce their stability. This can help ensure that banks operate responsibly and sustainably, ultimately contributing to the banking stability. Finally, the results obtained have implications for the various stakeholders of the Islamic bank. The optimal level of CSR that maximizes the stability of Islamic banks may depend on various factors such as the size, type, location, and culture of the bank, as well as the preferences, values, and expectations of its stakeholders. Therefore, it is important to develop the implications from the stakeholders’ perspective such as customers, investors, regulators, and employees. Customers may prefer to deal with Islamic banks that have a moderate level of CSR, as they may perceive them as more trustworthy, ethical, and socially responsible. Investors may also favor Islamic banks that have a moderate level of CSR, as they can expect higher returns, lower risks, and a better reputation from these banks. Regulators can encourage Islamic banks to adopt a moderate level of CSR, as this can enhance the stability and resilience of the Islamic banking sector. Employees can be motivated and satisfied to work in Islamic banks that have a moderate level of CSR, as they can feel proud, valued, and respected by their employers.

This study has certain limitations that open many possibilities for future research. To ensure the applicability of the results, future studies should be broader in scope and include other Islamic banks operating in other countries. In addition, future research could focus on other econometric methods namely threshold models to determine the optimal threshold. Furthermore, as our sample is limited to Islamic banks, we invite researchers to conduct a comparative study between Islamic and conventional banks. Finally, this research on the financial stability of Islamic banks reflects the context of GCC countries. We encourage researchers to continue their research by examining other regions (e.g., Middle East region) and conducting comparative analyses.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Ali, K., Hongbing, H., Liew, C. Y., & Jianguo, D. (2023). Governance perspective and the effect of economic policy uncertainty on financial stability: Evidence from developed and developing economies. Economic Change and Restructuring, 56(3), 1971–29. https://doi.org/10.1007/s10644-023-09497-6

- Ali, K., Jianguo, D., & Kirikkaleli, D. (2022). Modeling the natural resources and financial inclusion on ecological footprint: The role of economic governance institutions. Evidence from ECOWAS economies. Resources Policy, 79, 103115. https://doi.org/10.1016/j.resourpol.2022.103115

- Anginer, D., Demirguc-Kunt, A., & Zhu, M. (2014). How does competition affect bank systemic risk?. Journal of Financial Intermediation, 23(1), 1–26. https://doi.org/10.1016/j.jfi.2013.11.001

- Arellano, M., & Bond, S. (1991). Some tests of specification for Panel Data: Monte Carlo Evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297. https://doi.org/10.2307/2297968

- Athari, S. A. (2021a). Domestic political risk, global economic policy uncertainty, and banks’ profitability: Evidence from Ukrainian banks. Post-Communist Economies, 33(4), 458–483. https://doi.org/10.1080/14631377.2020.1745563

- Athari, S. A. (2021b). The effects of institutional settings and risks on bank dividend policy in an emerging market: Evidence from Tobit model. International Journal of Finance & Economics, 26(3), 4493–4515. https://doi.org/10.1002/ijfe.2027

- Athari, S. A., & Bahreini, M. (2023). The impact of external governance and regulatory settings on the profitability of Islamic banks: Evidence from Arab markets. International Journal of Finance & Economics, 28(2), 2124–2147. https://doi.org/10.1002/ijfe.2529

- Athari, S. A., & Irani, F. (2022). Does the country’s political and economic risks trigger risk-taking behavior in the banking sector: A new insight from regional study. Journal of Economic Structures, 11(1), 32. https://doi.org/10.1186/s40008-022-00294-4

- Athari, S. A., Saliba, C., Khalife, D., & Salameh-Ayanian, M. (2023). The role of country governance in achieving the banking sector’s sustainability in vulnerable environments: New insight from emerging economies. Sustainability, 15(13), 10538. https://doi.org/10.3390/su151310538

- Bagh, T., Khan, M. A., Azad, T., Saddique, S., & Khan, M. A. (2017). The corporate social responsibility and firms’ financial performance: Evidence from financial sector of Pakistan. International Journal of Economics and Financial Issues, 7(2), 301–308. https://dergipark.org.tr/en/pub/ijefi/issue/32035/354484

- Barnea, A., & Rubin, A. (2010). Corporate social responsibility as a conflict between shareholders. Journal of Business Ethics, 97(1), 71–86. https://doi.org/10.1007/s10551-010-0496-z

- Beck, T., & Feyen, E. (2013). Benchmarking financial systems: Introducing the financial possibility frontier. World Bank Policy Research Working Paper, 6615.

- Belasri, S., Gomes, M., & Pijourlet, G. (2020). Corporate social responsibility and bank efficiency. Journal of Multinational Financial Management, 54, 100612. https://doi.org/10.1016/j.mulfin.2020.100612

- Bouslah, K., Hmaittane, A., Kryzanowski, L., & M’Zali, B. (2023). CSR structures: Evidence, drivers, and firm value implications. Journal of Business Ethics, 185(1), 115–145. https://doi.org/10.1007/s10551-022-05219-6

- Buallay, A. (2019). Corporate governance, Sharia’ah governance and performance: A cross-country comparison in MENA region. International Journal of Islamic & Middle Eastern Finance & Management, 12(2), 216–235. https://doi.org/10.1108/IMEFM-07-2017-0172

- Çam, İ., & Özer, G. (2021). Institutional quality and corporate financing decisions around the world. The North American Journal of Economics & Finance, 57, 101401. https://doi.org/10.1016/j.najef.2021.101401

- Carroll, A. B. (1979). A three-dimensional conceptual model of corporate performance. The Academy of Management Review, 4(4), 497–505. https://doi.org/10.2307/257850

- Chollet, P., & Sandwidi, B. W. (2018). CSR engagement and financial risk: A virtuous circle? International evidence. Global Finance Journal, 38, 65–81. https://doi.org/10.1016/j.gfj.2018.03.004

- Cornett, M. M., Erhemjamts, O., & Tehranian, H. (2016). Greed or good deeds: An examination of the relation between corporate social responsibility and the financial performance of U.S. commercial banks around the financial crisis. Journal of Banking and Finance, 70, 137–159. https://doi.org/10.1016/j.jbankfin.2016.04.024

- Elamer, A. A., Ntim, C. G., Abdou, H. A., & Pyke, C. (2020). Sharia supervisory boards, governance structures and operational risk disclosures: Evidence from Islamic banks in MENA countries. Global Finance Journal, 46, 100488. https://doi.org/10.1016/j.gfj.2019.100488

- Elgattani, T., & Hussainey, K. (2020). The determinants of AAOIFI governance disclosure in Islamic banks. Journal of Financial Reporting and Accounting, 18(1), 1–18. https://doi.org/10.1108/JFRA-03-2019-0040

- El Khoury, R., Nasrallah, N., Harb, E., & Hussainey, K. (2022). Exploring the performance of responsible companies in G20 during the COVID-19 outbreak. Journal of Cleaner Production, 354, 131693. https://doi.org/10.1016/j.jclepro.2022.131693

- Fama, E. F., & Jensen, M. C. (1983). Separation of ownership and control. Journal of Law & Economics, 26(2), 301–325. https://doi.org/10.1086/467037

- Farah, T., Li, J., Li, Z., & Shamsuddin, A. (2021). The non-linear effect of CSR on firms’ systematic risk: International evidence. Journal of International Financial Markets, Institutions and Money, 71, 101288. https://doi.org/10.1016/j.intfin.2021.101288

- Fernández, A. I., González, F., & Suárez, N. (2016). Banking stability, competition, and economic volatility. Journal of Financial Stability, 22, 101–120. https://doi.org/10.1016/j.jfs.2016.01.005

- Fiordelisi, F., & Mare, D. S. (2014). Competition and financial stability in European cooperative banks. Journal of International Money & Finance, 45, 1–16. https://doi.org/10.1016/j.jimonfin.2014.02.008

- Freeman, R. E. (1984). Strategic Management: A stakeholder approach. Cambridge University Press.

- Friedman, M. (1970). A Friedman doctrine: The social responsibility of business is to increase its profits. The New York Times Magazine, 13(1970), 32–33. https://doi.org/10.1007/978-3-540-70818-6_14

- Fu, X.), Lin, Y., and Molyneux, P. (2014). Bank competition and financial stability in Asia Pacific. Journal of Banking and Finance, 38, 64–77. https://doi.org/10.1016/j.jbankfin.2013.09.012

- Gaies, B., & Jahmane, A. (2022). Corporate social responsibility, financial globalization and bank soundness in Europe – novel evidence from a GMM panel VAR approach. Finance Research Letters, 47, 102772. https://doi.org/10.1016/j.frl.2022.102772

- Galbreath, J. (2013). ESG in focus: The Australian evidence. Journal of Business Ethics, 118(3), 529–541. https://doi.org/10.1007/s10551-012-1607-9

- Gambetta, N., García-Benau, M. A., & Zorio-Grima, A. (2017). Corporate social responsibility and bank risk profile: Evidence from Europe. Service Business, 11(3), 517–542. https://doi.org/10.1007/s11628-016-0318-1

- Godfrey, P. C., Merrill, C. B., & Hansen, J. M. (2009). The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strategic Management Journal, 30(4), 425–445. https://doi.org/10.1002/smj.750

- Grassa, R. (2016). Corporate governance and credit rating in Islamic banks: Does shariah governance matters? Journal of Management & Governance, 20(4), 875–906. https://doi.org/10.1007/s10997-015-9322-4

- Guidi, F. (2021). Concentration, competition and financial stability in the South-East Europe banking context. International Review of Economics & Finance, 76, 639–670. https://doi.org/10.1016/j.iref.2021.07.005

- Haniffa, R., & Hudaib, M. (2007). Exploring the ethical identity of Islamic Banks via Communication in annual reports. Journal of Business Ethics, 76(1), 97–116. https://doi.org/10.1007/s10551-006-9272-5

- Iannotta, G., Nocera, G., & Sironi, A. (2007). Ownership structure, risk and performance in the European banking industry. Journal of Banking and Finance, 31(7), 2127–2149. https://doi.org/10.1016/j.jbankfin.2006.07.013

- Jan, A., Marimuthu, M., & Mat Isa, M. P. B. M. (2019). The nexus of sustainability practices and financial performance: From the perspective of islamic banking. Journal of Cleaner Production, 228, 703–717. https://doi.org/10.1016/j.jclepro.2019.04.208

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jiménez, G., Lopez, J. A., & Saurina, J. (2013). How does competition affect bank risk-taking?. Journal of Financial Stability, 9(2), 185–195. https://doi.org/10.1016/j.jfs.2013.02.004

- Kasman, S., & Kasman, A. (2015). Bank competition, concentration and financial stability in the Turkish banking industry. Economic Systems, 39(3), 502–517. https://doi.org/10.1016/j.ecosys.2014.12.003

- Kaufmann, D., Kraay, A., & Mastruzzi, M. (2011). The worldwide governance indicators: Methodology and analytical issues. Hague Journal on the Rule of Law, 3(2), 220–246. https://doi.org/10.1017/S1876404511200046

- Khan, M. A., Khan, M. A., Ali, K., Popp, J., & Oláh, J. (2020). Natural resource rent and finance: The moderation role of institutions. Sustainability, 12(9), 3897. https://doi.org/10.3390/su12093897

- Khémiri, W., Chafai, A., & Alsulami, F. (2023). Financial inclusion and sustainable growth in North African firms: A dynamic-panel-threshold approach. Risks, 11(7), 132. https://doi.org/10.3390/risks11070132

- Koseoglu, M. A., Uyar, A., Kilic, M., Kuzey, C., & Karaman, A. S. (2021). Exploring the connections among CSR performance, reporting, and external assurance: Evidence from the hospitality and tourism industry. International Journal of Hospitality Management, 94, 102819. https://doi.org/10.1016/j.ijhm.2020.102819

- Laeven, L., & Levine, R. (2009). Bank governance, regulation and risk taking. Journal of Financial Economics, 93(2), 259–275. https://doi.org/10.1016/j.jfineco.2008.09.003

- Lepetit, L., & Strobel, F. (2015). Bank insolvency risk and Z-score measures: A refinement. Finance Research Letters, 13, 214–224. https://doi.org/10.1016/j.frl.2015.01.001

- Lind, J. T., & Mehlum, H. (2010). With or without U? The appropriate test for a U-Shaped Relationship. Oxford Bulletin of Economics and Statistics, 72(1), 109–118. https://doi.org/10.1111/j.1468-0084.2009.00569.x

- Maali, B., Casson, P., & Napier, C. (2006). Social reporting by islamic banks. Abacus, 42(2), 266–289. https://doi.org/10.1111/j.1467-6281.2006.00200.x

- Maghyereh, A., Abdoh, H., & Al-Shboul, M. (2022). Oil structural shocks, bank-level characteristics, and systemic risk: Evidence from dual banking systems. Economic Systems, 46(4), 101038. https://doi.org/10.1016/j.ecosys.2022.101038

- Maghyereh, A. I., & Yamani, E. (2022). Does bank income diversification affect systemic risk: New evidence from dual banking systems. Finance Research Letters, 47, 102814. https://doi.org/10.1016/j.frl.2022.102814

- Mallin, C., Farag, H., & Ow-Yong, K. (2014). Corporate social responsibility and financial performance in Islamic banks. Journal of Economic Behavior & Organization, 103, S21–S38. https://doi.org/10.1016/j.jebo.2014.03.001

- Mollah, S., Hassan, M. K., Al Farooque, O., & Mobarek, A. (2017). The governance, risk-taking, and performance of islamic banks. Journal of Financial Services Research, 51(2), 195–219. https://doi.org/10.1007/s10693-016-0245-2

- Mollah, S., & Zaman, M. (2015). Shari’ah supervision, corporate governance and performance: Conventional vs. Islamic banks. Journal of Banking & Finance, 58, 418–435. https://doi.org/10.1016/j.jbankfin.2015.04.030

- Mukhibad, H., & Nurkhin, A. (2020). The mechanism of corporate governance, financial performance, and social performance in Baitul Maal Wat Tamwil (BMT). Journal of Accounting and Strategic Finance, 3(1), 1–17. https://doi.org/10.33005/jasf.v3i1.66

- Neitzert, F., & Petras, M. (2022). Corporate social responsibility and bank risk. Journal of Business Economics, 92(3), 397–428. https://doi.org/10.1007/s11573-021-01069-2

- Nguyen, T. T., Mia, L., Winata, L., & Chong, V. K. (2017). Effect of transformational-leadership style and management control system on managerial performance. Journal of Business Research, 70, 202–213. https://doi.org/10.1016/j.jbusres.2016.08.018

- Nguyen, A.-T., & Reiter, S. (2015). A performance comparison of sensitivity analysis methods for building energy models. Building Simulation, 8(6), 651–664. https://doi.org/10.1007/s12273-015-0245-4

- Pham, H. S. T., & Tran, H. T. (2020). CSR disclosure and firm performance: The mediating role of corporate reputation and moderating role of CEO integrity. Journal of Business Research, 120, 127–136. https://doi.org/10.1016/j.jbusres.2020.08.002

- Platonova, E., Asutay, M., Dixon, R., & Mohammad, S. (2018). The impact of corporate social responsibility disclosure on financial performance: Evidence from the GCC Islamic banking sector. Journal of Business Ethics, 151(2), 451–471. https://doi.org/10.1007/s10551-016-3229-0

- Ramzan, M., Amin, M., & Abbas, M. (2021). How does corporate social responsibility affect financial performance, financial stability, and financial inclusion in the banking sector? Evidence from Pakistan. Research in International Business and Finance, 55, 101314. https://doi.org/10.1016/j.ribaf.2020.101314

- Raouf, H., & Ahmed, H. (2022). Risk governance and financial stability: A comparative study of conventional and Islamic banks in the GCC. Global Finance Journal, 52, 100599. https://doi.org/10.1016/j.gfj.2020.100599

- Saadaoui, A., & Ben Salah, O. (2022). The moderating effect of financial stability on the CSR and bank performance. EuroMed Journal of Business. https://doi.org/10.1108/EMJB-10-2021-0163

- Saliba, C., Farmanesh, P., & Athari, S. A. (2023). Does country risk impact the banking sectors’ non-performing loans? Evidence from BRICS emerging economies. Financial Innovation, 9(1), 1–30. https://doi.org/10.1186/s40854-023-00494-2

- Salim, K., Disli, M., Ng, A., Dewandaru, G., & Nkoba, M. A. (2023). The impact of sustainable banking practices on bank stability. Renewable and Sustainable Energy Reviews, 178, 113249. https://doi.org/10.1016/j.rser.2023.113249

- Schaeck, K., & Cihák, M. (2014). Competition, efficiency, and stability in banking. Financial Management, 43(1), 215–241. https://doi.org/10.1111/fima.12010

- Tunio, R. A., Jamali, R. H., Mirani, A. A., Das, G., Laghari, M. A., & Xiao, J. (2021). The relationship between corporate social responsibility disclosures and financial performance: A mediating role of employee productivity. Environmental Science and Pollution Research, 28(9), 10661–10677. https://doi.org/10.1007/s11356-020-11247-4

- Ullah, S., Jamali, D., & Harwood, I. A. (2014). Socially responsible investment: Insights from Shari’a departments in Islamic financial institutions. Business Ethics: A European Review, 23(2), 218–233. https://doi.org/10.1111/beer.12045

- Umar, U. H., Besar, M. H. A., & Abduh, M. (2022). Compatibility of the CSR practices of Islamic banks with the United Nations SDGs amidst COVID-19: A documentary evidence. International Journal of Ethics and Systems, 39(3), 629–647. https://doi.org/10.1108/IJOES-12-2021-0221

- Wibisono, Y. (2007). Membedah konsep & aplikasi CSR: Corporate social responsibility. Fascho Pub.

- Wilson, R. (2009). The development of Islamic finance in the GCC. Working paper of the Kuwait Programme on development, governance and globalisation in the Gulf States. The Centre for the Study of Global Governance, London School of Economics.

- Wright, P., & Ferris, S. P. (1997). Agency conflict and corporate strategy: The effect of divestment on corporate value. Strategic Management Journal, 18(1), 77–83. https://doi.org/10.1002/(SICI)1097-0266(199701)18:1<77:AID-SMJ810>3.0.CO;2-R

- Wu, M.-W., & Shen, C.-H. (2013). Corporate social responsibility in the banking industry: Motives and financial performance. Journal of Banking & Finance, 37(9), 3529–3547. https://doi.org/10.1016/j.jbankfin.2013.04.023

- Yeyati, E. L., & Micco, A. (2007). Concentration and foreign penetration in Latin American banking sectors: Impact on competition and risk. Journal of Banking and Finance, 31(6), 1633–1647. https://doi.org/10.1016/j.jbankfin.2006.11.003

- Zafar, M. B., & Sulaiman, A. A. (2019). Corporate social responsibility and Islamic banks: A systematic literature review. Management Review Quarterly, 69(2), 159–206. https://doi.org/10.1007/s11301-018-0150-x

- Zahid, R. M. A., Khan, M. K., Anwar, W., & Maqsood, U. S. (2022). The role of audit quality in the ESG-corporate financial performance nexus: Empirical evidence from Western European companies. Borsa Istanbul Review, 22, S200–S212. https://doi.org/10.1016/j.bir.2022.08.011