?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study addresses the problem of value relevance and accounting for goodwill positions, as the measures used in previous studies are only suitable to a limited extent for measuring the growth potentials through M&A. For this purpose, the measure of future potential (FP) is defined as a company’s expected growth from a capital market perspective, which is already priced in but has not yet been realized and separates it from the growth already realized in the income statement. The study includes 2660 acquisitions from US companies between 1998 – 2018. Goodwill (premiums) are identified as carriers of FP, and we seek to determine whether they affect long-term operating performance. Our results show that changes in FP, like goodwill, significantly negatively affect future operating performance, demonstrating the realization of growth potentials through M&A. Second, using moderation analysis, we show that the interaction between goodwill and FP predicts changes in operating performance, and the negative relationships decreased significantly when firms were able to generate more potential through the transaction. Our model is particularly suitable for acquirers who have purchased only a few FP. The controversy surrounding goodwill’s value relevance and the impairment-only approach’s discretionary nature is scrutinized.

1. Introduction

In today’s environment, companies are pressured to make increased investments that often fail to pay off (Gu & Lev, Citation2011; Harford, Citation2005; Harford & Li, Citation2007). The challenge is to find new investment opportunities that drive growth constantly. Due to M&A, the share of intangible assets in balance sheets has continued to rise. In 1975, the percentage of intangible assets in the market value made up 17% in the S&P 500; this exploded to 90% by 2020, and M&A strongly influenced the development, because goodwill often represents the largest single item on companies’ balance sheets (Brown, Citation2023; Ocean Tomo, Citation2020). Goodwill reflects the present value of expected future benefits from intangible assets that cannot be identified individually and are not recognized separately. However, goodwill in the origination and subsequent measurement of these items is highly controversial in the literature and difficult to define (Bloom, Citation2009; Giuliani & Brännström, Citation2011; Johnson & Petrone, Citation1998).Footnote1

The increasing criticism of the current accounting principles for goodwill has led both the United States’ (US) Financial Accounting Standards Board (FASB) and its European counterpart, the International Accounting Standards Board (IASB), to revise the accounting principles on Identifiable intangible assets and subsequent accounting for goodwill (Financial Accounting Standards Board, Citation2023; IAS Plus, Citation2022). In recent years the literature reviews on accounting for goodwill by Wen and Moehrle (Citation2016) focus on the US’s Generally Accepted Accounting Principles (GAAP) accounting requirements and d’Arcy and Tarca (Citation2018) on International Financial Reporting Standards (IFRS) requirements, while overarching review by Amel-Zadeh et al. (Citation2023) reviews the determinants and decision usefulness of goodwill reporting. In subsequent valuations, goodwill impairments convey a negative signal about the acquisitions’ quality, as value-destroying M&As lead to more frequent and larger future goodwill impairments (Ahn et al., Citation2020). Also, Filip et al. (Citation2015) showed that managers delay goodwill impairments by manipulating cash flows and the resulting consequences for future performance. They study the effect of real earnings management on future performance and confirm that the actual manipulation of activities adversely affects future performance. This underlines that the company has not been able to create value from past acquisitions (Caplan et al., Citation2018). Therefore, managers have significant discretion in recognizing goodwill impairment, as impairment losses must be disclosed to the extent that the carrying amount of goodwill on the balance sheet exceeds its fair value. The fair value of goodwill can be inflated by opportunistic valuation assumptions or by inflating the current level of cash flow to assume as the basis for forecasting future cash flow used to estimate the fair value of goodwill (Banker et al., Citation2017; Penman, Citation2013). Therefore, there are doubts about the impairment of the goodwill position because the acquirer originally pays a price above the company’s market value in the hope of realizing the synergies of the merged organization (Krishnan et al., Citation2007; Sirower, Citation1997). However, according to agency theory, compensation and reputational concerns, as well as concerns about breaching debt obligations, incentivize managers to delay the recognition of goodwill impairment (Li & Sloan, Citation2017). In addition, Chung and Hribar (Citation2021), Hayn and Hughes (Citation2006), and Jarva (Citation2009) observed that the recognition of goodwill impairment is usually delayed for several years due to the deterioration of economic performance.

In accounting research, some papers have investigated whether accounting goodwill is relevant to the equity valuation of capital market participants. The studies have consistently found a positive relationship between firm value and goodwill (Jennings et al., Citation1996). Goodwill may be strongly associated with expected future benefits when the acquisition is recognized but is likely to decline rapidly. No differential effect was found between recently acquired goodwill and older goodwill, but annual amortization rather than the impairment-only approach (IPO) was also examined. Bugeja and Gallery (Citation2006) investigated the value relevance after the change to the IPO. They found a positive relationship between goodwill and firm value in the observation year, but not with goodwill acquired more than two years previously. However, some research criticizes that market prices and accounting measures are not correlated and are, therefore, not very informative (King et al., Citation2004, Citation2021; Papadakis & Thanos, Citation2010). The increasing goodwill positions due to the introduction of the IPO in the balance sheet have since been criticized, as the actual economic value of the goodwill is doubted due to the absence of impairments. Wang and Huang (Citation2019) show that excess goodwill has no positive effect on firms’ market performance, but a significant adverse effect on firms’ financial performance.

Therefore, this work is motivated by the fact that most frameworks on the value relevance of goodwill measure market performance while at the same time not considering the realization of synergy potential that has already taken place and, in addition to this, the achievement of value-oriented targets. However, the share of synergies already realized can only be found in accounting and is always accompanied by the assessments of capital market participants on the other side. But accounting information is past-oriented and is not a good indicator of future corporate performance. To address the complexity of goodwill accounting, a mediating measure that can calculate value-based goodwill is needed to provide information to preparers of annual reports as to whether the reported value of goodwill is justified. The work is significantly motivated by Yehuda et al. (Citation2019), which examined whether goodwill determined for accounting purposes by US acquirers corresponds to the underlying economic reality of the transaction according to the Financial Accounting Standard Board (FASB) and demonstrates the discrepancy between the perspectives.

Research question:

Can a value-based measure control the value relevance and information content of goodwill and premium regarding long-term performance?

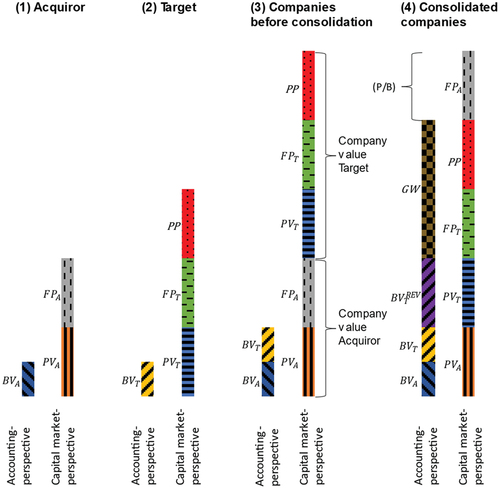

To overcome the existing misalignment of goodwill recognition and its subsequent measurement, a holistic value component, which includes the economic significance of goodwill from a combined metric composed of the accounting capital market and value-oriented perspective, is used to classify the previous results. In order to isolate the effect of goodwill on M&A success, the market value (MV) of a company is divided into the components’ present value (PV) and FP (Honold et al., Citation2016). The PV is developed based on a perpetual annuity from the adjusted net income and the company’s cost of capital. The PV represents the operating performance of the company, a key figure that indicates the performance a company can achieve based on the assets shown in the balance sheet and the income statement. Compared to other valuation mechanisms, such as cash flow, growth rates are deliberately omitted in this case, as they are not associated with current performance. The difference between the calculated PV and the company’s MV gives the company’s periodized FP. FP implies the expectations placed on the company by the shareholders regarding future business development, which the company could not yet realize at the operational level. FP is the goodwill created from a market perspective that the company has to realize in the future. Figure shows an illustrative example of the FP approach to the goodwill problem.

Figure 1. Value gaps in M&A from an accounting- and capital market- perspective.

In the first two columns, three different dimensions are compared. Simplified, it is assumed that the PV exceeds the book value of the acquiring company, but further FP are also included in the market value.Footnote2 The target differs from the acquirer only in the acquisition premium paid. The takeover premium includes the maximum purchase price based on the fundamental analysis of the acquiring company, which is higher than the current market value due to synergies and cost savings (Damodaran, Citation2005). Aktas et al. (Citation2016) point out that takeover premiums are seen in connection with management’s overestimation of their skills, implying values for target companies that are not realizable. But premiums are necessary to induce the target company’s shareholders to sell their shares to gain control over the company (Ciobanu, Citation2015). A further value gap results from the difference between the acquisition premium paid and the market value if the . While column three contains the aggregate balance before consolidation, column four shows the consolidation’s influences on the value gaps, with a remaining difference between the accounting and capital market perspective solely explained by the original FP of the acquirer. The values in the first two columns can be easily transferred to column four without structural changes. The differences from column three to the accounting perspective in column four result from the consolidation measures of the target company on the balance sheet side. No further adjustments are required from a capital market perspective. The disclosure of hidden reserves leads to a revaluation of the equity of the target by the acquirer, expressed by

. Revaluating the BV closes the gap between PV and BV, as the identified assets are recognized at their respective fair value following the fair value balance sheet. The accounting for the FP of the target company and the acquisition premium were not recognized in the balance sheet prior to the transaction, but are now recognized as goodwill in the balance sheet and contribute to an increase in the carrying amount. The amount of the premium paid and the target’s FP share in its market value determine the amount of goodwill recognized. The effects on the P/B are unaffected by this and thus irrelevant to assessing the company’s growth prospects. The figure suggests a decline in the ratio, meaning lower growth intentions than before the transaction. The ratio is highly controversial and must be interpreted differently depending on the industry.

The study analyzes a sample of 2660 business combinations completed by US acquirers between 1998 – 2018. The results show that goodwill negatively impacts the industry-adjusted operating performance two years after the transaction’s closing, which also renews the criticism of IOA. In contrast, value-based FP, which includes the transaction’s synergies, shows an opposite relationship with performance. Companies that realize the synergies quickly manage to show better performance. In contrast, for other companies, the capital market confirms the value of the synergies, and the companies are expected to perform better in the long run. Using a moderation analysis, the interaction effect between goodwill and FP also shows strong support for mitigating the negative impact of goodwill on performance and, therefore, for goodwill being classified as significantly more value-relevant by the capital market. In addition, the results show that the model is particularly relevant for acquirers who can realize their potential quickly. The positive effect between goodwill and performance for low-FP acquirers can be attributed to the fast synergy realization. At the same time, however, a decline in operating performance can be expected if the company cannot create new FP.

We contribute to several existing research streams. The research on empirical goodwill is controversial due to the introduction of the IPO, and the second is the general criticism of M&A performance measurement.

First, our study provides new insights into the value relevance approach, investigating whether stock prices behave as if investors perceive goodwill as an asset. We extend the results of Aharony et al. (Citation2010) and Amel-Zadeh et al. (Citation2020), who provide isolated evidence that the value relevance of goodwill increased after introducing the IPO. They neglect the already partial realization of the acquired goodwill from a balance sheet perspective in the form of better performance and possible distortions in stock prices.

Second, we contribute to the purchase price allocation studies demonstrating managers’ opportunistic use of goodwill discretion, leading to a higher purchase price allocation to goodwill (Amel-Zadeh et al., Citation2023). In this regard, Paugam et al. (Citation2015) find that the portion of the purchase price specifically allocated to goodwill leads to negative abnormal returns. Their study also reports that “abnormal goodwill” is negatively associated with future firm performance. However, the results suggest that the goodwill position cannot be measured by changes in performance alone, as this disregards investors’ expectations of the goodwill position.

Third, our research explains the results of Li et al. (Citation2011) on the information content of goodwill impairment charges. Li et al. (Citation2011) examine the market reaction to goodwill impairment announcements and find that the negative reaction is lower in the SFAS 142 period. While goodwill impairments are informative for investors, verifiability must be tested as a moderating factor (Amel-Zadeh et al., Citation2023). The FP has a significantly higher information content because it includes different valuation perspectives.

This paper also contributes to the heated debate of how to reform FASB and IFRS goodwill. Most recently, literature reviews by Amel-Zadeh et al. (Citation2023), d’Arcy and Tarca (Citation2018), and Wen and Moehrle (Citation2016) have pointed out that empirical research does not allow us to conclude whether the current goodwill accounting rules provide an optimal level of discretion and it is therefore strongly influenced by management incentives and the institutional context. Zhang and Zhang (Citation2017) also noted that under SFAS 142, the allocation of the purchase price to goodwill is influenced not only by economic determinants but also by management’s incentives. This is also due to the non-verifiable fair value measurements, which are related to the underlying economic circumstances, but also deviate from the true values when management reporting incentives are present. The FP is therefore likely to scrutinize fair value measurements by giving balance sheet preparers less incentive to use discretion. Similarly, external appraisers alone cannot completely eliminate management discretion in the valuation of intangible assets.

Within a third research stream, the paper contributes to the general concerns about the criticisms of purely accounting measures (Papadakis & Thanos, Citation2010). They argue that, on the one hand, accounting profit is the closest measure of performance (Venkatraman & Ramanujam, Citation1986), as it measures the pure economic performance of a firm (Lubatkin & Shrieves, Citation1986). The data from financial statements are considered credible and usable due to the strict regulations and compliance with international standards (Eriksson & Lausten, Citation2000).

Second, accounting ratios are problematic in that they only reflect past firm performance and, therefore, cannot predict future results (Chenhall & Langfield-Smith, Citation2007; Wernerfelt & Montgomery, Citation1988).

Third, accounting data provide only aggregated data derived from the entire firm’s performance; therefore, these data are not suitable for determining the success of transactions (Chenhall & Langfield-Smith, Citation2007; Lubatkin, Citation1983; Panigrahi et al., Citation2014).

Fourth, the lack of correlation with stock returns is critique-worthy. The returns do not reflect the change in the economic value of a company and do not allow reliable statements about the change in market value (Rappaport, Citation1998).

These criticisms are directed at the studies on future performance presented earlier, which refer to pure changes in key figures from accounting. We address this mismatch by introducing FP as a measure that can better explain future performance. Therefore, it is investigated whether the introduction of the FP can reduce the problems of accounting studies (Honold et al., Citation2016) and whether the new dimension can provide more explanatory power for scholars and practitioners.

The structure of the paper is as follows. First, Chapter 2 discusses the current reforms. This is followed by a theoretical literature review in Chapter 3 and an empirical literature review and hypothesis formulation in Chapter 4. Chapter 5 contains the research design, while Chapter 6 describes and discusses the results. In the final Chapter, a summary of the research is drawn, and limitations and an outlook are provided.

2. Background

Goodwill accounting, or the introduction of IOA by the US FASB in 2001 and by the IASB in 2003,Footnote3 is a highly controversial topic in accounting policy and has not been finalized to date (Ramanna, Citation2008; Watts, Citation2003). There appears to be increasing criticism of the current accounting principles for goodwill, so the accounting principles are being reviewed by both the IASB and the FASB. Most recently, the literature reviews on goodwill accounting by Wen and Moehrle (Citation2016) focus on US GAAP accounting requirements for goodwill and US studies, while d’Arcy and Tarca (Citation2018) focus on IFRS requirements, and the overarching research by Amel-Zadeh et al. (Citation2023) addresses goodwill accounting principles.

The impairment of goodwill has been controversial from the beginning. On the one hand, there is widespread agreement that the IPO provides more decision-useful information, as an appropriate impairment charge more accurately reflects the decline in value of an asset with an indefinite useful life than if it were amortized on a blanket basis over an arbitrary useful life. In contrast, it is argued that the IOA provides a large degree of discretion that impairment managers can use opportunistically; for example, to delay or avoid necessary impairment charges (Ramanna & Watts, Citation2012; Watts, Citation2003). Purchase price allocation (PPA) is a method of accounting for acquisitions that assigns a fair value to all assets acquired and liabilities assumed by the target company (e.g., Paugam et al., Citation2015; Zhang & Zhang, Citation2017). During the PPA, managers are given the opportunity to identify and revalue intangible assets, which may affect the contribution of allocated goodwill. The number and amount of previously unrecognized assets determine the difference between the revalued net assets and the purchase price (Shalev, Citation2009). This opportunistic opportunity may result in the purchase price premium differing from the recognized goodwill. Managers can use their knowledge when allocating goodwill to units to specifically allocate goodwill to those units where there is a lot of internally generated goodwill (which may not be recognized). Thus, there is a great opportunity to avoid having to impair goodwill in the future. In case of doubt, the calculations of the recoverable amount may be based on purely subjective and non-verifiable company-specific forecasts (European Financial Reporting Advisory Group, Citation2017). On the other hand, preparers of financial statements criticize that goodwill impairment tests are complex and unreasonably costly (International Accounting Standards Board, Citation2020, paragraph 4.5).

With continued criticism of the standards for accounting for business combinations and goodwill, the IASB and FASB broke away from their harmonization, but both reconsidered their standards (Financial Accounting Standards Board, Citation2019; IASB, Citation2020). While the FASB made a preliminary Board decision to reinstate amortization in late 2020 (FASB, Citation2023), the IASB opposed reinstating amortization because it “has no compelling evidence that amortizing goodwill would significantly improve the information provided to investors.” (IASB, Citation2020, para IN35(c)). However, as this decision was extremely close, the IASB decided to issue a discussion paper inviting stakeholders to provide further evidence to help the IASB further develop the standards (International Accounting Standards Board, Citation2019). In addition, the IASB plans to deviate from the annual review if there are no indications of impairment and the introduction of additional disclosure requirements about the acquisition targets of the entities and the subsequent achievement of these targets by the acquired entities (Amel-Zadeh et al., Citation2023). On 15 June 2022, the FASB made a surprise decision to abandon the project on identifiable intangible assets and subsequent accounting for goodwill, stating that the change they were seeking to make to subsequent accounting for goodwill would not improve the current rules because investors believed the information would provide only marginal benefits (Financial Accounting Standards Board, Citation2022). Previously, a statement from the International Organization of Securities Commissions (IOSCO) noted that: “When the requirements under US GAAP are as aligned as possible with those under IFRS on accounting for goodwill, there is greater comparability in financial statements prepared under IFRS and US GAAP… the likelihood of achieving a converged outcome is greatly enhanced when the two Boards work collaboratively” (IAS Plus, Citation2022).

3. Theoretical literature review

In the research, several theories addressed the economic consequences of goodwill and how to deal with goodwill impairment. In M&A, potential acquirers have to pay a premium to give the owners of the target company an incentive to sell their shares (La Bruslerie, Citation2013). However, the premiums often do not reflect the firm’s economic performance. However, the impact of purchase price premiums on success after M&A shows that acquisitions bought at too high a price do not pay off (Krishnan et al., Citation2007; Sirower & Sahni, Citation2006). In theory, firms hope to achieve synergies by leveraging the complementary assets of acquiring and acquired firms to produce valuable and unique products or services (Ravenscraft & Scherer, Citation1987). Synergy can also be achieved by consolidating assets to achieve economies of scale and scope, eliminating inefficiencies and redundancies in firms’ value chains by combining sales forces and production facilities, sharing trademarks, brand names, or distribution channels (Capron, Citation1999; Haspeslagh & Jemison, Citation1991; Rabier, Citation2017). The synergy motive is rooted in the resource-based approach to the firm, in which the complementary resource profiles of the two firms, such as physical resources, intangible resources, financial resources, and human resources, are integrated in a way that uniquely positions the firm relative to its competitors, creating competitive advantages (Capron, Citation1999). While creating synergies is the stated motive for paying high premiums (Hitt et al., Citation2008), agency theory and managerial hubris also explain the inflated goodwill balances (Michael A. Hitt et al., Citation2012).

Second, Roll’s (Citation1986) hubris hypothesis postulates that managers systematically overestimate their capabilities in relation to the assessments of the target companies, resulting in negative performance. Further studies confirm these results (Aktas et al., Citation2016; El-Khatib et al., Citation2015; Qiu et al., Citation2014). As a result of hubris, companies pay too much for their targets (Hayward & Hambrick, Citation1997). Overconfidence may cause the CEO to perform inferior due diligence and to ignore negative information from this process (Hitt et al., Citation2001).

Third, agency theory postulates that acquiring companies often overpay for acquisitions when top managers engage in opportunistic behavior that provides them with personal benefits and creates wealth transfers from acquirer shareholders to acquirer management (Geiger & Schiereck, Citation2014; Trautwein, Citation1990). With the acquisitions, the size of the company also continues to grow, which in turn has a positive effect on the remuneration of the Executive Board and expands its power. In M&A, the agency problem arises from the separation of ownership and control. The conflict of interest and information asymmetry between shareholders and management cause management to take some opportunistic actions that promote management’s self-interest but destroy firm and shareholder value (Jensen & Meckling, Citation1976).

4. Empirical literature review and hypotheses development

The research stream on the value relevance of goodwill shows that goodwill accounting is found to be positively associated with stock prices (Aharony et al., Citation2010; Cascino et al., Citation2021; Chauvin & Hirschey, Citation1994; Elnahass & Doukakis, Citation2019; Horton & Serafeim, Citation2010; Jennings et al., Citation2001). On the other hand, Zheng et al. (Citation2014) show that goodwill on the balance sheet can significantly reduce the company’s future performance due to an excessive focus on short-term performance while neglecting the company’s long-term goals, which leads to expensive acquisitions and high goodwill positions.

Secondly, goodwill contains a certain predictive power about the future cash flow that can be generated and generally about the economic performance after transactions (Bostwick et al., Citation2016; Chalmers et al., Citation2011; Jarva, Citation2009; Li & Sloan, Citation2017).

Thirdly, other studies have examined the value relevance of goodwill impairments (Bens et al., Citation2011; Guler, Citation2018; Hamberg et al., Citation2011; Knauer & Woehrmann, Citation2016; Li & Sloan, Citation2017; Li et al., Citation2011). Although the FASB and IASB, following the agency theory, explicitly require entities to perform the impairment test once a year, the subsequent recognition of the impairment loss could be delayed (Chung & Hribar, Citation2021; Hayn & Hughes, Citation2006). Managers are allowed to manipulate and improve the company’s profits to convince others that the goodwill is not impaired, even if the economic value of the goodwill has decreased, and to protect their private interests from feeling adverse effects due to impairment (Filip et al., Citation2015, Citation2021; Glaum et al., Citation2018; Li & Sloan, Citation2017; Li et al., Citation2011; Nguyen & Thi Duong, Citation2022).Footnote4 Therefore, a company’s management can use discretionary power and strategically place write-offs in opportunistic periods to avoid losses (Filip et al., Citation2015; Li & Sloan, Citation2017). Han and Tang (Citation2020) assumed that impaired goodwill is less likely to generate future profits when using the is allowed to be changed in ROA and ROE to measure future performance. Suppose an impairment loss is omitted in the short term. In that case, the likelihood increases that a high impairment loss will be recognized in the long term, negatively affecting a firm’s performance growth and increasing the risk of a stock price decline. Companies increase short-term accounting performance and market prices by not impairing goodwill (Li & Sloan, Citation2017). This is also because goodwill is only impaired if the carrying amount in the balance sheet exceeds its recoverable amount. However, based on management’s subjective assumptions, fair value is derived from an alternative financial model and is not driven by an active market, so companies may make optimistic assumptions about these variables to increase fair value (Filip et al., Citation2015, Citation2021). Yehuda et al. (Citation2019) examined whether goodwill reflects the underlying economic reality for US acquirers. Although 41% of the transactions have a negative net present value, the acquirer did not impair the goodwill at the acquisition date as required. Acquirers with economic losses allocate significantly more proportion of the total purchase price to goodwill instead of impairing it. Using an additional test, it was possible to demonstrate that, in the case of acquisitions with an economic gain, the estimated economic gain and the goodwill recognized are highly significantly related to future performance, justifying the synergies promised by the acquisition. In the case of acquisitions with economic losses, it has been demonstrated that higher losses lead to the recognition of higher goodwill.

Since the calculation of the fair value of money can be arbitrarily adjusted by using the manager’s discretion, and accounting standards have not yet been able to eliminate this problem (Ayres et al., Citation2019; Bens et al., Citation2011), the question arises as to the actual economic value of the goodwill recognized. Li and Sloan (Citation2017) have already demonstrated that avoiding impairments leads to higher goodwill amounts when using one-dimensional measures, which either increase accounting earnings and share prices in the short term. The FP fills this gap by having the measure identify and evaluate the synergies created from the transaction. In doing so, the measure considers not only the acquirer’s long-term performance increases but also the market’s dynamic assessment of the value of the synergies. Consequently, the FP can influence the effect of the value of goodwill. A strengthening of the effect occurs when the position of goodwill is very valuable and is associated with the performance, while a deterioration of the effect represents the use of managerial discretion, and the goodwill recognized does not match the economic goodwill.

Hypothesis 1a:

Future potential moderates the effect of transactional goodwill on firm performance.

The accounting guidance for goodwill decides that the purchase price of a business is allocated to the various components of the acquired company based on the fair value of the underlying assets and liabilities (Zhang & Zhang, Citation2017). If the purchase price is higher than the fair value of the identifiable net assets of the acquired company, the difference is recognized as goodwill (Gore & Zimmerman, Citation2010). Opportunistic behavior on the part of the manager may result in the use of their discretion in the revaluation of intangible assets to influence the contribution of allocated goodwill, such that the purchase price premium differs from the recognized goodwill.

The synergy hypothesis implies that the greater the expected synergies to be realized through the takeover, the higher the premium the bidder is willing to pay. The relationship between premiums and bidders’ long-term performance has been the subject of numerous studies, but the linear relationship found between the variables does not indicate whether the relationship is positive or negative (Antoniou et al., Citation2008; Bradley et al., Citation1983; Diaz Diaz et al., Citation2013; Sirower, Citation1997). Rani et al. (Citation2020) find that synergy-motivated M&A leads to significantly higher long-term performance after M&As than agency-motivated M&As. Antoniou et al. (Citation2008) found that the synergy hypothesis demonstrated that the merger premium better indicates the synergies between the acquirer and its target company. Wang et al. (Citation2021) also argue that high premiums from non-state firms are negatively correlated with the current financial performance of firms, but not with future annual financial performance. A harmful M&A motivation can exacerbate the risk of M&A integration and block the realization of M&A synergies. If there is disharmony and exclusion in various parts of the company in the integrated management stage after transactions, it will affect the performance of M&As. If an anticipated higher performance is not achieved in the long term, this leads to a deterioration in financial performance, which is reflected in the position of goodwill.

The overpayment hypothesis on the other hand is motivated by agency problems and hubris (Roll, Citation1986; Shleifer & Vishny, Citation1997). Acquirers pay a premium that exceeds expected synergies, so the negative relationship between the premium and the acquirer’s performance expresses value destruction (Aktas et al., Citation2016; El-Khatib et al., Citation2015; Hayward & Hambrick, Citation1997; Qiu et al., Citation2014; Sirower, Citation1997). Gupta and Misra (Citation2007) viewed the differences in empirical studies on synergies and overpayment as an opportunity to examine whether the relationship between premiums and returns is asymmetric and depends on whether the acquisition is value-enhancing or value-decreasing. They only showed that premiums have a negative impact on acquiring firms when the acquisition is classified as value-enhancing.

From the two underlying theories examining the impact of the premium on performance, contradictory empirical results emerge. The research suggests that synergies expressed in terms of premiums alone provide little information. Using FP as a moderator, the information content of the premium is tested, and the interaction effect can be used to test the value of the premium and how well the premium is actually suited to predict future company performance. Since proponents of the synergy hypothesis measure the realization of synergies purely in terms of financial performance, they ignore the fact that shareholders’ expectations change significantly a few years after the transaction, which is expressed in the FP. Therefore, FP is expected to influence the impact of premiums on performance.

Hypothesis 1b:

Future potential moderates the effect of purchase price premiums paid on firm performance.

So far, research has completely ignored how the synergies achieved with the transaction can be measured from a value-oriented perspective. The synergy value should be consistent with the value of goodwill. But the well-known studies show that recognizing goodwill impairment usually lags several years behind deteriorating economic performance (Chung & Hribar, Citation2021; Hayn & Hughes, Citation2006; Jarva, Citation2009). Adjacent to the criticism of excessively high goodwill balances by Han and Tang (Citation2020), it can be assumed these are related to highly disclosed FP under rational capital market participants. Wang and Huang (Citation2019) showed in a study the negative impact of excess goodwill on operative performance (ROE & ROA). This is related to the manipulation of profits by managers to prevent goodwill impairment losses, even if the economic value of the goodwill has decreased (Filip et al., Citation2015, Citation2021; Glaum et al., Citation2018). Since goodwill is expressed as a proxy by capital market expectations and balance sheet-realized synergies in FP, FP behaves asymmetrically to goodwill. Despite realizing synergies (decrease in FP), managers use discretion to prevent impairment.

Hypothesis 2a:

The impact of the goodwill on operating performance is positive and stronger if few future potentials are attributed to the acquirer after the transaction.

Hypothesis 2b:

The impact of the purchase price premium paid for the transaction on operating performance is stronger if few future potentials are attributed to the acquirer after the transaction.

5. Research design

5.1. Sample construction and selection

The sample compilation is based on the Refinitiv database Eikon and Datastream. In addition, capital market data was obtained from the investing.com financial platform. The M&A deals had to meet the criteria as described in Appendix A to remain in the sample. Initially, the total sample size was 4360 companies. Further limitations in the sample result from the choice of the longitudinal study in order to be able to measure the post-merger performance. Thus, all transactions were eliminated for which a value could not be determined at all measurement points. Other cases were also eliminated if no value or financial information could be determined for any of the variables required for the multiple regression model. For acquiring companies that do not have their reporting date on December 31, adjustments were made to allocate the transaction to the associated accounting period if a transaction occurred after the reporting date. Furthermore, all transactions were removed from the sample for which no accounting data was available. This resulted in a final sample size of 2660 transactions.

5.2. Measures

5.2.1. Dependent variable

The operating performance of the acquiring companies is measured as the difference between the return on assets (ROA) 2 years (1 year) after the transaction and ROA 1 year before the transaction. The anticipation of real economic gains cannot be distinguished from false market prices if only short-term stock prices are considered (Healy et al., Citation1992). ROA is an appropriate measure of M&A performance because all value creation occurs after the acquisition, and therefore of critical importance is the quality of the post-merger integration process (Fu et al., Citation2013; Haspeslagh & Jemison, Citation1991). Most of the M&A literature attributes the failure of M&A to a misjudgment of potential synergies (Bauer & Friesl, Citation2022; Roll, Citation1986), but especially in successful acquisitions, up to 75% of the synergy effects are already achieved in the first year after the takeover (Ficery et al., Citation2007).

For some target companies, data specifically before the transaction announcement is absent due to missing identifiers. Similarly, the degree and intensity of integration of the target company after the transaction also complicates the measurement of post-acquisition performance. In addition, Renneboog and Vansteenkiste (Citation2019) criticize that in many empirical studies there is little clarity on the construction of post-merger operational metrics, which limits the observation of how post-merger performance is affected by the choice of earnings-based versus cash flow-based metrics. In addition to the existing measurement problems, this study will focus on the acquisition of companies, as the development of FP relates to the target companies and is relevant for this study. The regression models will account for other deal- and company-specific characteristics via control variables. To attribute the changes in operating performance solely to the transactions, the ROA of the acquiring companies was adjusted for the performance of the applicable peer of the acquirer. Choosing the right benchmark is just as important for calculating the long-term operating performance as for the long-term performance of shares (Renneboog & Vansteenkiste, Citation2019). The peer controls for industry effects was implemented similarly to Rao-Nicholson et al. (Citation2016) and Healy et al. (Citation1992). In contrast, Martynova et al. (Citation2006) used pre-acquisition size and performance in addition to adjustments for industry effects, but the results did not change significantly. A separate industry portfolio was created for each acquirer, including all public companies with their headquarters in the US and the same two-digit North American industry classification (NAIC) code. In order to take into account both industry and time effects, a new industry portfolio was calculated for every year. As with Rao-Nicholson et al. (Citation2016), the benchmark values are derived from the median values of the ROA so that distortions due to outliers can be reduced.

The approach for measuring operational performance can then be expressed as follows by Zollo and Singh (Citation2004):

and

represent the post-merger performance and

the pre-merger performance of each acquirer.

,

and

represent the median return on assets of the same industry as the acquiring company in the respective period.

5.2.2. Independent and moderator variable

5.2.2.1. Future potential

Consistent with Honold et al. (Citation2016), a measure of FP is used to capture the impact of the transaction on the acquirer. The measure is the change of FP for the acquiring company from the previous year of the announcement to year 2 (1) after the acquisition (Formula (5) and (6)). Year 0 is defined as the year in which the transaction took place. FP is measured as the difference between the market value of equity and the present value and is expressed as a percentage (Formula (4)). The market value of equity is the share price multiplied by the number of ordinary shares in issue measured at the end of the calendar year. The present value is calculated as the perpetual annuity resulting from the net income for the year and the cost of equity from the capital asset pricing model (CAPM) (Formula (3)). Calculating the cost of equity (CoE) using the CAPM formula requires making various assumptions for capital market data. In order to ensure comparability between market and accounting data, the data was collected at the end of the calendar year, as the reporting of the companies then corresponds to the capital market data. The S&P 500 was chosen as the reference market for the average market return over 30 years, as it almost wholly represents the market capitalization of listed stock corporations in the US. The yield of a 30-year federal bond as of December 31 of the calendar year was included as the risk-free interest rate. In addition, 5-year beta factors were used for the model. Net income before extraordinary items measures the companies’ operating profit and eliminates distortions due to one-off effects.

5.2.2.2. Goodwill

Studies of goodwill find that it is a good predictor of future business performance because accounting data are used to make predictions of future economic results accurate. Lee (Citation2011) found that goodwill under SFAS 142 significantly predicted future cash flows. Discretionary reporting is also used less opportunistically and supports the elimination of systematic depreciation. In contrast, Hamberg et al. (Citation2011) argue that unimpaired goodwill is a sign of strength. A lack of impairment indicates a company’s success, as it contains information about good historical investments. The earnings statement is higher if the company does not recognize any impairment and the share price increases. In even greater detail, Bugeja and Gallery (Citation2006) examined the value relevance of acquired goodwill with increasing maturity. The results show that currently acquired goodwill has information content, whereas older goodwill does not.

5.2.2.3. Premium

The debate about the appropriateness of the takeover premium is highly controversial in the literature. Purchase price premiums are mandatory in many transactions to incentivize shareholders to sell their shares. However, transactions that are procured too expensively lead to a failure of post-merger integration and the destruction of value (Krishnan et al., Citation2007; Sirower & Sahni, Citation2006). Companies willing to pay high takeover premiums expect to achieve synergies through the transaction, which can then justify the price paid for gaining control (Antoniou et al., Citation2008; Bradley et al., Citation1983). Zhu and Jog (Citation2009) found a negative effect in their study on the relationship between ROA and takeover premium, but only for domestic transactions. The primary function of the takeover market should be to replace inefficient management because it is easier to increase the value of the target company, especially for companies with poor performance, which also explains the negative relationship between the premium and ROA for target companies.

5.2.3. Control variables

Studies of the long-term operational performance of M&A control for various deal and firm-specific characteristics. Previous literature addresses method of payment (Haleblian et al., Citation2009), industry relatedness (Bryson et al., Citation2006; Healy et al., Citation1992), crossborder status (Aguiar & Gopinath, Citation2007; Chen, Citation2011; Moeller & Schlingemann, Citation2005), Tobin’s Q (Alhenawi & Krishnaswami, Citation2015; McLaughlin et al., Citation1998), deal size (Asquith et al., Citation1983; Fuller et al., Citation2002), M&A experience (Haleblian & Finkelstein, Citation1999; Zollo & Leshchinkskii, Citation2000; Mohite, Citation2017), leverage (Masulis et al., Citation2007), and goodwill impairment (AbuGhazaleh et al., Citation2011; Carlin & Finch, Citation2009; Chalmers et al., Citation2011; Petersen, Citation2006; Watts, Citation2003) as key factors impacting M&A. Han and Tang’s (Citation2020) study of future company performance also use numerous control variables, such as size, financial leverage, market-to-book ratio, sales growth, and the share of intangible assets. Following the studies presented, similar control variables were chosen. The collection and calculation of all variables is detailed in Appendix B.

5.3. Model

Using multivariate analysis, the effects of the independent and moderating variables on changes in operational performance are measured.

Table contains the correlation matrix to all variables used in the following studies. These include the moderator, independent, and control variables in addition to the dependent variables. The results show very low correlation coefficients between the variables. Larger values are obtained only for the correlation between the dependent variables used in this study, which therefore need not be considered further. Collinearity bias between the variables can be ruled out for the sample. Similarly, the data set was checked for multicollinearity using a variance inflation factor (VIF) test. For all models, the variables receive a VIF factor, which is slightly above 1, well within the limit of the critical value of 10 (Kutner et al., Citation2005). Even in the models with interactions, the VIF never reaches the value of 2. Unexplained multicollinearity can be excluded. In addition, the standard model was tested to see if it was homoscedastic. A uniform distribution of the individual points over the horizontal axis could be determined through a scatter plot. The Durbin-Watson test was also applied to check the model for autocorrelation. Both the scatter plot and the Durbin-Watson statistic of 1.848 indicate that there is no autocorrelation.

Table 1. Correlation table

Table reports the descriptive statistics for the data used in this study. Different effects between the ∆ROA and ∆ROE were found for both measurement time points. Studies using ROA report, on average, negative outcomes, while the contrary is found for cash flow (Thanos & Papadakis, Citation2012,p. 116). The mean values of the ROA are slightly negative and are −.052% and −.388%, thus matching the research of Zollo and Singh (Citation2004). On the other hand, ROE was positive at 1.433% and 2.898%. The variable ROE has to be assessed critically, as some high outliers (see standard deviation) may distort the mean value. The outliers are due in part to very low equity ratios. The moderating variable ∆FP and the independent variable PREMIUM also show a high standard deviation, which is also reflected in the extreme values of the variables. These variables are winsorized in the regression models to limit the problem with outliers.

Table 2. Descriptive statistics

Table shows the distribution of the sample by NAIC codes. Financial and insurance companies remain in the sample, as in other M&A performance measures that use ROA as the dependent variable.

Table 3. Sample compilation

Table shows the change in raw and industry-adjusted operating performance. For ROE, there are no significant differences in any of the three event windows, neither for raw performance nor for industry-adjusted performance. All measurement points show that the industry-adjusted performance is significantly higher than the raw performance. ROE increased by up to 2.898% after the transaction. The non-significant results can be attributed to the already large scatter in the data set. In contrast, ROA shows highly significant results for both raw performance and industry-adjusted performance for the different measurement time points. With −1.326% and −0.772%, the results look very similar to those in the studies of Rao-Nicholson et al. (Citation2016) and Dickerson et al. (Citation1997), respectively. Based on the t-test, further analyses focus exclusively on ROA as the dependent variable, as already indicated in the model description.

Table 4. Changes in operating performance

6. Empirical results and discussion

6.1. Cross-sectional analysis (H1a & H1b)

The results of the multiple regression analysis of the model are presented in Table (including fixed year and industry effects). Different models were constructed for both ∆ROA2 and ∆ROA1 to consider the respective influence of the independent variables separately. Models 4 and 8 include all variables and moderating effects. In all models, all control variables are included. All models show that the included variables have good coherence, as the F-statistics for all models (p < 0.001) are strongly significant, and the R2 increases from the initial model to the entire model. For ∆ROA2, the R2 increases from 15.1% to 32.7%, and for ∆ROA1 from 12.2% to 28.7%. Models 1 and 5 first show the pure influence of the control variables on ROA changes. In Models 2 and 3, as well as 5 and 6, the respective independent variables are set in interaction with the change in FP. Independent of the previous studies on the relationship between goodwill and premium, the influence of FP on terms can thus be analyzed. The final Models 4 and 8 include all variables.

Table 5. Cross-sectional analysis of post-M&A operating performance

First, the controls’ findings show highly significant negative relationships with operating performance for the variables SIZE, EARNED, and CROSSBORDER. In contrast, the variables LEVERAGE and EXPERIENCE significantly positively affect operating performance. The effects are very constant in all models.

Second, the strong, significant negative relationship between ∆LNGOODWILL and operational performance in Models 2 and 4 is consistent with the previous findings of Li and Sloan (Citation2017), which criticize failure to amortize goodwill and postulate that, in the long run, operating performance suffers as a result. While in the short term, goodwill may well reflect the economic benefits of transactions, in the long term, goodwill is an asset unsuitable for reflecting future operating performance due to, among other things, intense intermingling between derivative and original goodwill. Immediately after the transaction, managers can attribute strong potential to goodwill, which, however, has to be realized quickly using a successful post-merger integration (PMI).

Third, interestingly, none of the models can be identified as having a significant influence of the PREMIUM on performance. The results do not support the synergy hypothesis, so the payment of high premiums is not associated with more synergies (Hitt et al., Citation2008), and they also do not support the overpayment hypothesis, so the opportunistic behavior of managers is not associated with takeover premiums (Geiger & Schiereck, Citation2014).

Fourth, in addition to the previous findings on accounting-based performance measurements of M&A, the ∆FP introduced a value-based metric that can measure the extent to which the transaction created new potential for the company that the acquirer was able to develop during the transaction. For all six models, highly significant effects can be observed between the operating performance and ∆FP. The negative relationship between the variables show that acquiring companies with a positive development of the operating performance are more likely to realize the company’s potential. In contrast, acquirers who fail to increase performance still retain the potential in the company.

Fifth, the models first separately measured the interaction relationships between the main effects and the interaction coefficient ∆FP. In Models 2 and 3, the interaction coefficients have a positive sign for the main effects, which are all significant. Thus, the negative impact of the ∆LNGOODWILL is less significant if the company can show more FP in return. Therefore, in Model 2, 0.010 must be added to the main effect of the ∆LNGOODWILL for each unit of ∆FP. The increase in R2 up to 27.1% also indicates that the ∆FP offers additional explanatory potential for the development of operating performance that has not been considered in previous research. The research expands the understanding of the fair value of goodwill, which in the literature is attributed exclusively to subjective assessments by management (Filip et al., Citation2015, Citation2021). The results also support the synergy hypothesis (Hitt et al., Citation2008), showing that companies have problems realizing all synergies even in the long run after the acquisition. Contrary to the IOA proponents, goodwill has more intrinsic value than previously known. Thus, the empirical analysis finds much support for Hypotheses 1a and 1b. In contrast, for the models with the variable ∆ROA1 measuring the impact on post-transaction performance, no significant effects of the ∆LNGOODWILL, PREMIUM, and interactions are found, which is due to the fact that reporting seems to be correct in the short run after M&A but deviates from value orientation in the long run.

With the final interaction between ∆LNGOODWILL, PREMIUM, and ∆FP, the market and accounting perspectives were combined, and further explanatory potential by combining the different perspectives could be found, shown in Model 4 with an R2 of 32.7%.

6.2. Additional tests (H2a & H2b)

The results show that the ∆FP contains a lot of information relevant to post-transaction performance. However, the partly highly significant results allow only a partial interpretation of the figures, since only the overall effect of the ∆FP has been investigated so far. In a further step, the acquirer companies were divided into three subcategories. Companies that were able to realize a substantial amount of potential through the transactions (the top 25% quantile) are shown as high FP acquirers. In contrast, there is a category for low FP acquirers that have the least FP after the transaction, since they were either unable to generate any FP or were able to convert them quickly into returns. In each model, all variables, including all control variables, were included as in the full model (Table ). An adjusted R2 of 63.2% is particularly striking for low FP and indicates that the model can explain low FP acquisition well. None of the independent variables or the interactions can predict acquirers’ performance with average FP. For the variable ∆LNGOODWILL, a negative and significant effect (p < 0.05) on operating performance was found for high FP acquirers. At the same time, it is positive and strongly significant (p < 0.01) for low FP acquirers. Therefore, high FP acquirers with increasing firm performance have less goodwill accounted for in the transaction, as goodwill impairment could be more likely to occur. M&A in the High FP category also shows that less goodwill is recognized when the company’s long-term performance is performing well. The results are also consistent with Yehuda et al. (Citation2019), which have already demonstrated that acquirers with economic losses allocate a significantly higher proportion of the total purchase price to goodwill. Nevertheless, it should be noted that the negative relationship between ∆LNGOODWILL and ∆ROA2 should be put into perspective by the FP, since the capital market nevertheless attributes many previously unrealized synergies to the acquirer.

Table 6. Influence of high and low future potential on operating performance

For companies that have not succeeded in gaining potential through the transaction, the relationship between performance and goodwill is in the same direction. In companies that were able to realize FP quickly, there is a positive relationship between goodwill and performance. This shows the mismatch between the perspectives particularly clearly. Although the market recognizes that companies have already realized their FP, the goodwill on the balance sheet still seems to justify the actual performance, which satisfies the auditors of the accounting data. Thus, we confirm the findings of Chung and Hribar (Citation2021), Hayn and Hughes (Citation2006) and Jarva (Citation2009), that the recognition of goodwill impairment usually lags several years behind deteriorating economic performance. Also, the results complement the research of Gonçalves et al. (Citation2023) showing that auditors for highly profitable companies are less likely to report goodwill impairment as a key audit matter.

Consistent with the results of the ∆LNGOODWILL, the PREMIUM behaves in all models, so a lower premium has a positive effect on performance, especially for high FP companies. These directions of effect are consistent with the previous studies that analyzed overpriced transactions.

In each case, the interaction relationships are highly significant at low FP. For goodwill, the interaction ∆LNGOODWILL x ∆FP runs in the same direction and shows that FP amplifies the effect between the variables. Again, an identical impact for the PREMIUM was found. For high FP acquirers, there is only a highly significant effect for the interaction PREMIUM x ∆FP, which is the opposite and confirms that as long as the capital market awards the company high FP, high premiums are also associated with weaker on-balance sheet performance. The assumptions made in Hypotheses 2a and 2b that there is a positive and strong effect of goodwill and PREMIUM on the operating performance of companies with little FP could not be directly confirmed. Based on the results, it can be clearly demonstrated that FP’s interaction variable significantly affects both variables and amplifies the effects. Thus, it is also proved that the relationships between the market view and the accounting view in M&A are more strongly linked than could be assumed. With the variable FP, it is possible to incorporate significantly more explanatory potential into the model than the usual studies that choose the market value/book value ratio at this point. However, this cannot represent the actual value creation of M&A. This effect is even stronger if the future share of intangible assets increases.

6.3. Robustness checks

Some adjustments were made to test the models for robustness. First, all firms from the finance and insurance industry were removed, reducing the size of the sample to 1830 transactions. The results for ∆LNGOODWILL and the PREMIUM remained constant. Changes occurred only for the control variables. Second, changing the measurement of PREMIUM from a metric variable to a categorical variable resulted in no changes in the significance levels for the interaction effects. Third, the elimination of the insignificant control variables also substantially increased the significance levels without changing the overall conclusions of the model. Fourth, the dependent variable was changed by no longer measuring M&A performance as Change in ROA, but as Tobin’s Q. The variable was defined as Market value of equity plus Total assets minus Total equity divided by Total assets). Tobin’s Q represents an interesting measure in the context of FP, as it incorporates replacement costs and is thus much more forward-looking than a purely operative measure. Only after ∆ROE was used as the dependent variable instead of ∆ROA did the model change, and no significant effects were detected, which is consistent with the univariate analysis.

7. Summary and conclusion

In recent years, goodwill volumes on balance sheets worldwide have risen steadily due to the introduction of the IPO. Numerous studies have investigated whether managers use discretion to delay or avoid goodwill impairment even if the economic value of the goodwill has decreased and to protect their private interests from feeling adverse effects due to impairment (Filip et al., Citation2015, Citation2021; Glaum et al., Citation2018). In addition, buyers are criticized for paying prices for companies significantly higher than the expected synergies. As a result, the amount of goodwill recognized on balance sheets has continued to increase, and both the FASB and the IASB seem unable to find a solution.

Therefore, this paper aims to determine the economic value of synergies and test whether the goodwill position following the transaction is justified or whether managers should have recognized impairment losses. Based on a holistic view, the FP is derived by combining elements of the value-based view, book values, and market values to analyze the value relevance and information content of goodwill and the resulting future earnings. By distinguishing between actual realized accounting performance and the FP to be initially realized in the future, which is already reflected in the market price, the approach can better measure isolated M&A effects. FP implicates the expectations placed on the company by the shareholders regarding future business development, which the company could not yet realize at the operational level.

Although there is support in the models that goodwill has a negative long-term impact on performance, which also renews the criticism of IOA. But equally, the effect of value-based FP that incorporates the transaction’s synergies is also negative. Companies that realize the synergies quickly manage to show better performance. In contrast, for other companies, the capital market confirms the value of the synergies, and the companies are expected to perform better in the long run. Using a moderation analysis, the interaction effect between goodwill and FP also shows strong support for mitigating the negative impact of goodwill on performance and, therefore, for goodwill being classified as significantly more value-relevant by the capital market. In addition, the results show that the model is particularly relevant for acquirers who can realize their potential quickly. The positive effect between goodwill and performance for low-FP acquirers can be attributed to the fast synergy realization. At the same time, however, a decline in operating performance can be expected if the company cannot create new FP.

This paper delivers practical implications for managers, capital market participants, and standard setters for assessing the impairment of goodwill, the information content of goodwill, and the predictive power of future earnings. The current discussions of the FASB and IASB on “Identifiable Intangible Assets and Subsequent Accounting for Goodwill” show that for more than 20 years, there has still been no agreement on how goodwill should be treated. The scientific approaches discussed have little explanatory potential if they generalize goodwill. The interplay between accounting, capital market perspective, and value-based view provides essential information about the value of goodwill and helps forecast company performance development.

Further research must verify whether the results also apply to capital market performance. Some limitations result from the country error, as only US-based acquirers are considered. In addition, further studies need to consider more than just the operating performance of the acquirer. For example, the FP of the target company before the transaction should also be integrated into the analysis, as this is where the real potential is embedded. M&A motivations should also be better scrutinized from a theoretical perspective. If one transaction is motivated by synergies and others by agency theory, then the capital market should also price the companies at different levels of FP.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The data will be made available on request.

Notes

1. The International Financial Reporting Standards (IFRS) 3 Appendix A describes goodwill as “an asset representing the future economic benefits arising from other assets acquired in a business combination that are not individually identified and separately recognized.”.

2. Formally, and consequently

for the acquiring company and

and consequently

for the target company.

3. Detailed explanations can be found in the Standards. See Statement of Accounting Standards (SFAS) No. 141 (Financial Accounting Standards Board, Citation2001a), and SFAS No. 142 (Financial Accounting Standards Board, Citation2001b), as well as the European counterparts IFRS 3 and IAS 36 (IASB, Citation2015).

4. In contrast, there is empirical evidence that the value relevance of acquired goodwill increased after the amendment of IFRS in 2008, suggesting that management discretion actually improved the quality of financial information (Tunyi et al., Citation2020).

References

- AbuGhazaleh, N. M., Al-Hares, O. M., & Roberts, C. (2011). Accounting discretion in goodwill impairments: UK evidence. Journal of International Financial Management & Accounting, 22(3), 165–28. https://doi.org/10.1111/j.1467-646X.2011.01049.x

- Aguiar, M., & Gopinath, G. (2007). Emerging market Business cycles: The cycle is the trend. Journal of Political Economy, 115(1), 69–102. https://doi.org/10.1086/511283

- Aharony, J., Barniv, R., & Falk, H. (2010). The impact of mandatory IFRS adoption on equity valuation of Accounting numbers for security investors in the EU. European Accounting Review, 19(3), 535–578. https://doi.org/10.1080/09638180.2010.506285

- Ahn, S., Cheon, Y. S., & Kim, M. (2020). Determinants of initial goodwill overstatement in affiliated and non‐affiliated mergers. Journal of Business Finance & Accounting, 47(5–6), 587–614. https://doi.org/10.1111/jbfa.12442

- Aktas, N., Bodt, E. D., Bollaert, H., & Roll, R. (2016). CEO narcissism and the takeover process: From private initiation to deal completion. Journal of Financial and Quantitative Analysis, 51(1), 113–137. https://doi.org/10.1017/S0022109016000065

- Alhenawi, Y., & Krishnaswami, S. (2015). Long-term impact of merger synergies on performance and value. The Quarterly Review of Economics & Finance, 58, 93–118. https://doi.org/10.1016/j.qref.2015.01.006

- Amel-Zadeh, A., Faasse, J., Li, K., & Meeks, G. (2020). Has Accounting regulation secured more valuable goodwill disclosures? SSRN Electronic Journal. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2306584

- Amel-Zadeh, A., Glaum, M., & Sellhorn, T. (2023). Empirical goodwill research: Insights, issues, and implications for standard setting and future research. European Accounting Review, 32(2), 415–446. https://doi.org/10.1080/09638180.2021.1983854

- Antoniou, A., Arbour, P., & Zhao, H. (2008). How much is too much: Are merger premiums too high? European Financial Management, 14(2), 268–287. https://doi.org/10.1111/j.1468-036X.2007.00404.x

- Asquith, P., Bruner, R. F., & Mullins, D. (1983). The gains to bidding firms from merger. Journal of Financial Economics, 11(1–4), 121–139. https://doi.org/10.1016/0304-405X(83)90007-7

- Ayres, D. R., Campbell, J. L., Chyz, J. A., & Shipman, J. E. (2019). Do financial analysts compel firms to make accounting decisions? Evidence from goodwill impairments. Review of Accounting Studies, 24(4), 1214–1251. https://doi.org/10.1007/s11142-019-09512-0

- Banker, R. D., Basu, S., & Byzalov, D. (2017). Implications of impairment decisions and assets’ cash-flow horizons for conservatism research. The Accounting Review, 92(2), 41–67. https://doi.org/10.2308/accr-51524

- Bauer, F., & Friesl, M. (2022). Synergy evaluation in mergers and acquisitions: An Attention‐based view. Journal of Management Studies. https://doi.org/10.1111/joms.12804

- Bens, D. A., Heltzer, W., & Segal, B. (2011). The information content of goodwill impairments and SFAS 142. Journal of Accounting, Auditing & Finance, 26(3), 527–555. https://doi.org/10.1177/0148558X11401551

- Bloom, M. (2009). Accounting for goodwill. Abacus, 45(3), 379–389. https://doi.org/10.1111/j.1467-6281.2009.00295.x

- Bostwick, E. D., Krieger, K., & Lambert, S. L. (2016). Relevance of goodwill impairments to cash flow prediction and forecasting. Journal of Accounting, Auditing & Finance, 31(3), 339–364. https://doi.org/10.1177/0148558X15596201

- Bradley, M., Desai, A., & Kim, E. (1983). The rationale behind interfirm tender offers. Journal of Financial Economics, 11(1–4), 183–206. https://doi.org/10.1016/0304-405X(83)90010-7

- Brown, M. (2023, April 19). Boom of intangible assets felt across industries and economy, UCLA Anderson Review. https://anderson-review.ucla.edu/boom-of-intangible-assets-felt-across-industries-and-economy/

- Bryson, J. M., Crosby, B. C., & Stone, M. M. (2006). The design and implementation of cross-sector collaborations: Propositions from the literature. Public Administration Review, 66(s1), 44–55. https://doi.org/10.1111/j.1540-6210.2006.00665.x

- Bugeja, M., & Gallery, N. (2006). Is older goodwill value relevant? Accounting and Finance, 46(4), 519–535. https://doi.org/10.1111/j.1467-629X.2006.00181.x

- Caplan, D., Dutta, S. K., & Liu, A. Z. (2018). Are material weaknesses in Internal Controls associated with poor M&A decisions? Evidence from goodwill impairment. AUDITING: A Journal of Practice & Theory, 37(4), 49–74. https://doi.org/10.2308/ajpt-51740

- Capron, L. (1999). The long-term performance of horizontal acquisitions. Strategic Management Journal, 20(11), 987–1018. https://doi.org/10.1002/(SICI)1097-0266(199911)20:11<987:AID-SMJ61>3.0.CO;2-B

- Carlin, T. M., & Finch, N. (2009). Discount rates in disarray: Evidence on flawed goodwill impairment testing. Australian Accounting Review, 19(4), 326–336. https://doi.org/10.1111/j.1835-2561.2009.00069.x

- Cascino, S., Clatworthy, M. A., García Osma, B., Gassen, J., & Imam, S. (2021). The usefulness of Financial Accounting information: Evidence from the field. The Accounting Review, 96(6), 73–102. https://doi.org/10.2308/TAR-2019-1030

- Chalmers, K. G., Godfrey, J. M., & Webster, J. C. (2011). Does a goodwill impairment regime better reflect the underlying economic attributes of goodwill? Accounting and Finance, 51(3), 634–660. https://doi.org/10.1111/j.1467-629X.2010.00364.x

- Chauvin, K. W., & Hirschey, M. (1994). Goodwill, profitability, and the market value of the firm. Journal of Accounting and Public Policy, 13(2), 159–180. https://doi.org/10.1016/0278-4254(94)90018-3

- Chen, W. (2011). The effect of investor origin on firm performance: Domestic and foreign direct investment in the United States. Journal of International Economics, 83(2), 219–228. https://doi.org/10.1016/j.jinteco.2010.11.005

- Chenhall, R. H., & Langfield-Smith, K. (2007). Multiple perspectives of performance measures. European Management Journal, 25(4), 266–282. https://doi.org/10.1016/j.emj.2007.06.001

- Chung, B. H., & Hribar, P. (2021). CEO overconfidence and the Timeliness of goodwill impairments. The Accounting Review, 96(3), 221–259. https://doi.org/10.2308/TAR-2016-0555

- Ciobanu, R. (2015). Mergers and acquisitions: Does the legal origin matter? Procedia Economics and Finance, 32, 1236–1247. https://doi.org/10.1016/S2212-5671(15)01501-4

- Damodaran, A. (2005). The value of synergy. https://doi.org/10.2139/ssrn.841486

- d’Arcy, A., & Tarca, A. (2018). Reviewing IFRS goodwill Accounting research: Implementation effects and cross-country differences. The International Journal of Accounting, 53(3), 203–226. https://doi.org/10.1016/j.intacc.2018.07.004

- Diaz Diaz, B., Sanfilippo Azofra, S., & López Gutiérrez, C. (2013). ichange1 synergies or overpayment in European corporate M&A. Journal of Contemporary Issues in Business Research, 2(5), 135–153.

- Dickerson, A. P., Gibson, H. D., & Tsakalotos, E. (1997). The impact of acquisitions on company performance: Evidence from a large panel of UK firms. Oxford Economic Papers, 49(3), 344–361. https://doi.org/10.1093/oxfordjournals.oep.a028613

- El-Khatib, R., Fogel, K., & Jandik, T. (2015). CEO network centrality and merger performance. Journal of Financial Economics, 116(2), 349–382. https://doi.org/10.1016/j.jfineco.2015.01.001

- Elnahass, M., & Doukakis, L. (2019). Market valuations of bargain purchase gains: Are these true gains under IFRS? Accounting and Business Research, 49(7), 753–784. https://doi.org/10.1080/00014788.2019.1609345

- Eriksson, T., & Lausten, M. (2000). Managerial pay and firm performance – Danish evidence. Scandinavian Journal of Management, 16(3), 269–286. https://doi.org/10.1016/S0956-5221(99)00026-3

- European Financial Reporting Advisory Group. (2017 June). Goodwill test - can it be improved? (discussion Paper).

- Ficery, K. L., Herd, T. J., & Pursche, B. (2007). Where has all the synergy gone? The M&A puzzle. Journal of Business Strategy, 28(5), 29–35. https://doi.org/10.1108/02756660710820802

- Filip, A., Jeanjean, T., & Paugam, L. (2015). Using real activities to avoid goodwill impairment losses: Evidence and effect on future performance. Journal of Business Finance & Accounting, 42(3–4), 515–554. https://doi.org/10.1111/jbfa.12107

- Filip, A., Lobo, G. J., & Paugam, L. (2021). Managerial discretion to delay the recognition of goodwill impairment: The role of enforcement. Journal of Business Finance & Accounting, 48(1–2), 36–69. https://doi.org/10.1111/jbfa.12501

- Financial Accounting Standards Board. (2001a). Summary of statement no. 141 business combinations. 01.09.2023. http://www.fasb.org/summary/stsum141.shtml*.

- Financial Accounting Standards Board. (2001b). Summary of statement no. 142 goodwill and other intangible assets. 01.09.2023. https://www.fasb.org/summary/stsum142.shtml*.

- Financial Accounting Standards Board. (2019 July). Identifiable intangible assets and subsequent accounting for goodwill (discussion paper).

- Financial Accounting Standards Board. (2022 June). Identifiable intangible assets and subsequent accounting for goodwill (discussion paper).

- Financial Accounting Standards Board. (2023). Project update: Identifiable intangible assets and subsequent Accounting for goodwill. https://www.fasb.org/Page/ProjectPage?metadata=fasb-IdentifiableIntangibleAssetsandSubsequentAccountingforGoodwill-022820221200&isPrintView=true

- Fu, F., Lin, L., & Officer, M. S. (2013). Acquisitions driven by stock overvaluation: Are they good deals? Journal of Financial Economics, 109(1), 24–39. https://doi.org/10.1016/j.jfineco.2013.02.013

- Fuller, K., Netter, J., & Stegemoller, M. (2002). What do returns to acquiring firms tell us? Evidence from firms that make many acquisitions. The Journal of Finance, 57(4), 1763–1793. https://doi.org/10.1111/1540-6261.00477

- Geiger, F., & Schiereck, D. (2014). The influence of industry concentration on merger motives—empirical evidence from machinery industry mergers. Journal of Economics & Finance, 38(1), 27–52. https://doi.org/10.1007/s12197-011-9202-y

- Giuliani, M., & Brännström, D. (2011). Defining goodwill: A practice perspective. Journal of Financial Reporting and Accounting, 9(2), 161–175. https://doi.org/10.1108/19852511111173112

- Glaum, M., Landsman, W. R., & Wyrwa, S. (2018). Goodwill impairment: The effects of Public enforcement and monitoring by institutional investors. The Accounting Review, 93(6), 149–180. https://doi.org/10.2308/accr-52006

- Gonçalves, I., Morais, A. I., & Pinto, I. (2023). Goodwill impairment and key audit matters. Cogent Business & Management, 10(2). Article 2207877, 2207877. https://doi.org/10.1080/23311975.2023.2207877

- Gore, R., & Zimmerman, D. (2010). Is goodwill an asset? The CPA Journal, 80(6), 46–48.

- Guler, L. (2018). Has SFAS 142 improved the usefulness of goodwill impairment loss and goodwill balances for investors? Review of Managerial Science, 12(3), 559–592. https://doi.org/10.1007/s11846-016-0223-y

- Gu, F., & Lev, B. (2011). Overpriced shares, ill-advised acquisitions, and goodwill impairment. The Accounting Review, 86(6), 1995–2022. https://doi.org/10.2308/accr-10131

- Gupta, A., & Misra, L. (2007). Deal size, bid premium, and gains in Bank mergers: The impact of Managerial motivations. Financial Review, 42(3), 373–400. https://doi.org/10.1111/j.1540-6288.2007.00176.x

- Haleblian, J., Devers, C. E., McNamara, G., Carpenter, M. A., & Davison, R. B. (2009). Taking stock of What we know about mergers and acquisitions: A Review and research agenda. Journal of Management, 35(3), 469–502. https://doi.org/10.1177/0149206308330554