Abstract

The purpose of this study is to examine the effectiveness of clawback to minimize earnings management due to moral disengagement tendencies. To understand the phenomenon of earnings manipulation, as well as the propensity for moral disengagement, we turn to the agency theory and the social cognition theory. In addition, clawback is explained by the supernatural monitoring hypothesis as a tool to lessen earnings manipulation. To test the hypotheses, an experimental study was conducted using a within-subject design. The participants were professional accountants who were pursuing master’s level studies. We found that moral disengagement is preceded by an ethical orientation. More importantly, we found the impact of ethical orientation on intentions for managing earnings is mediated by moral disengagement. Further, we found the clawback scheme reduces the effect of moral disengagement on intentions to manipulate earnings. More specifically, the results show that when adopting a clawback strategy, moral disengagement significantly increases the intention to manipulate accruals but does not significantly affect the intention to manipulate real activity. The results suggest that seriously considering individual characteristics and implementing appropriate incentive programs may lead to a high standard of financial reporting.

1. Introduction

Recently, there has been an increase in the number of ethical scandals in various organizational contexts, including in the accounting field, such as earnings management scandals. According to the 2022 Global Economic Crime and Fraud Survey by PwC, which polled 1,296 business executives across 53 countries, almost half of the firms (46%) report having dealt with fraud and economic crime, suggesting that these ethical scandals have a more significant impact. Further, the survey indicates that nearly one in five businesses said that their most disruptive incident had a financial impact of more than US$50 million, and 52% of businesses with global annual revenues of more than US$10 billion reported experiencing fraud and earnings management over the preceding 24 months.

Earnings management is the subjective selection of reporting and estimating methodologies that fails to adequately capture the fundamental economic circumstances of the company (Healy & Wahlen, Citation1999). Results of earnings management techniques have contributed to the demise of a number of big businesses, including Sunbeam, Worldcom, and Enron. These collapses are the driving force behind the accounting profession and standard-setters putting regulatory changes into practice. Earnings management still continues despite regulatory measures to prevent excessive financial reporting (see Cohen et al., Citation2008; McVay, Citation2006; Sarbanes-Oxley, Citation2004).

A theoretical framework of moral disengagement (Bandura, Citation1986, Citation1999) has been utilized to explain why people act in unethical ways that lead to financial scandals. The idea of moral disengagement, as a set of cognitive mechanisms that allow individuals to violate their internal moral standards and act unethically without feeling pressured and guilty, offers a plausible explanation for the occurrence of several earnings management scandals in recent years. However, the hypothesis of moral disengagement, used to explain accounting crises, has not received much empirical testing (e.g. Beaudoin et al., Citation2015; West & Fleischman, Citation2023). Aside from that, the supernatural monitoring hypothesis (SMH), as a method to reduce the detrimental effects of moral disengagement, is undergoing scant research. Punishment is believed to be beneficial in reducing the harmful effects of moral disengagement, because it makes managers feel watched (Yilmaz & Bahçekapili, Citation2016). The theoretical motivation of this study is to investigate the causes and effects of moral disengagement, as well as methods for mitigating their effects, such as clawback or punishment mechanisms, in accordance with the SMH theory.

Moral disengagement involves various strategies individuals use to rationalize engaging in unethical behaviors so that they can continue to maintain themselves as virtuous people. Moral disengagement is a buffer that allows freedom from guilt and anxiety at the thought that they may have violated accepted moral standards (De Cremer & Vandekerckhove, Citation2017). Moral disengagement explains why individuals engage in unethical actions such as earnings manipulation without feeling moral pressure (Bandura, Citation1990a, Citation1990b, Citation2002).Beaudoin et al. (Citation2015) found that ethical perceptions of earnings manipulation influence their moral disengagement tendencies which, in turn, affect discretionary manipulation of accruals. Some researchers argue that earnings manipulation is an unethical practice with negative consequences (e.g., Johnson et al., Citation2013; Kaplan, Citation2001; Vinciguerra & O’Reilly-Allen, Citation2004).

Past research has examined the effect of moral disengagement on desired and undesired work behavior in individuals and teams, such as unethical decision-making (Baron et al., Citation2015; Ogunfowora et al., Citation2013), unethical behaviors (Keem et al., Citation2018; Welsh et al., Citation2015), social loafing (Alnuaimi et al., Citation2010), unethical pro-organizational behavior (Chen et al., Citation2016; Valle et al., Citation2017),and cheating behavior (Fida et al., Citation2016).However, there are still few studies that examine the effect of moral disengagement on earnings manipulation (Beaudoin et al., Citation2015; West & Fleischman, Citation2023). Furthermore, research that tests effective strategies to reduce the unintended effects of moral disengagement, particularly the manipulation of earnings, remains rare (Newman et al., Citation2020). Therefore, the empirical motivation of this study is to examine the effect of moral disengagement on earnings management, and to examine effective strategies to minimize its dysfunctional impact (SEC, Citation2008) due to moral disengagement tendencies.

In order to investigate this issue, the purpose of this study is to test the effectiveness of a clawback compensation scheme to reduce the effect of moral disengagement on earnings management intentions.We focused on the compensation structure because it is one way to drive managers’ behavior (Anthony & Govindarajan, Citation2007). More specifically,The Sarbanes-Oxley Act of 2002 (SOX)implicitly recommends clawbacks to address accounting fraud and scandals. Clawbacks include a penalty mechanism that allows directors to withhold compensation paid to executives when discrepancies are found in financial reports (Chan et al., Citation2015). The primary purpose of clawback is to align the incentives of management and shareholders to avoid conflicts of interest between these parties and create a culture of ethical management (Mahdy, Citation2019).

In terms of accounting, particularly in terms of earnings management, clawbacks’ usefulness has been examined. Previous studies (Chan et al., Citation2012; DeHaan et al., Citation2013; Natarajan & Zheng, Citation2019; Remesal, Citation2018) have employed secondary data to provide empirical evidence that clawbacks are negatively linked to financial adjustments/misstatements. Additionally, the use of clawback clauses results in less accrual manipulation (Chen et al., Citation2014). Recent research by Sari et al. (Citation2023), using primary data, revealed that, after the implementation of clawback, women’s intention to influence accruals decreased more than men’s. Littleevidence, however, has been offered by other studies assessing the effectiveness of clawbacks onthe tendency for moral deviance or ethical orientation and its effect on managers’behavior to manipulate earnings.

Consequently, the current paper seeks to make the following contribution to the existing literature. First, this research is different from that conducted by Beaudoin et al. (Citation2015), which examined the effect of moral disengagement on earnings manipulation. While Beaudoin et al. (Citation2015) studied a bonus compensation scheme, this study focuses on a clawbacks compensation scheme, and investigates whether clawbacks moderate the relationship between moral disengagement and earnings management. Second, prior studies into the impact of moral disengagement on profit manipulation (Beaudoin et al., Citation2015; West & Fleischman, Citation2023) did not offer suggestions for the approaches necessary to lessen the unintended consequences of moral disengagement (Newman et al., Citation2020). This study, however, suggests ways to reduce the harm that moral disengagement causes. Third, whereas Beaudoin et al. (Citation2015) and West and Fleischman (Citation2023) only looked at the impact of moral disengagement on accrual manipulation, this study looks at both accrual and real activity manipulation of earnings because they have different detection risks (Chan et al., Citation2015). Fourth, in contrast to earlier studies that examined the effectiveness of clawback using secondary data (Chan et al., Citation2015; Iskandar-Datta & Jia, Citation2012), the current study makes use of primary data and an experimental approach.

The rest of the paper is organized as follows. The next section provides the background. The third section is the theoretical literature review. The fourth section is the empirical literature review and hypothesis development. The fifth section is the research design. Then, the sixth section presents the empirical results and discussion. The final section is the conclusion.

2. Background

Various cases of fraud occurred in Indonesia throughout 2021–2022. The losses incurred by the financial services sector from fraud during 2018–2022 reached IDR 123.51 trillion. Throughout 2022 there were 97 cases of fraudulent/illegal investments, 619 cases of illegal online loans, and 62 cases of illegal pawning (Fraudulent Investment Task Force-FSA). Based on a release by the Association of Certified Fraud Examiners (ACFE, Citation2022) entitled Asia-Pacific Occupational Fraud 2022, Indonesia is ranked 4th with 23 cases of fraud in 2022. The biggest frauds in Indonesia are corruption (64%), misuse of state & company assets (28.9%), and financial statement fraud (6.7%). Financial statement fraud is usually done through earnings management. In fact, earnings management is an act of fraud considering that in earnings management, the financial statements are presented according to management’s wishes, not factually (as is) with the support of generally accepted accounting standards.

Financial statement fraud is the intentional misrepresentation of a company’s financial condition through misstatements or omissions of amounts, or disclosures in the financial statements to deceive users of the financial statements. Financial statement fraud is not only detrimental to the company, but can also harm the shareholders, prospective shareholders, creditors, and investors and other users of the financial statements. Financial statement fraud is a serious threat to stakeholders’ confidence in financial information and the capital markets, which will have a negative effect on the stock market financial system. Not all misstatements are fraudulent because ISA (International Standards on Auditing) 240 explains that misstatements in financial statements can be caused by errors or fraud. The difference between the two lies in whether the underlying action was intentional or not (ISA 240). According to the elements of fraud (conversion, concealment, and theft), then earnings management activities fulfill the elements of conversion (engineering, manipulation) and concealment (hiding, covering) even though there is no direct theft (self-benefit).

The following are the results of empirical research in Indonesia related to earnings management practices. Sari and Sholihin (Citation2019) have investigated the impact of religiosity and clawback on corporate disclosure behavior, and found that a clawback policy influenced the opportunistic behavior of one of three models, i.e., accrual manipulation. They imply that accrual manipulation is more easily detected by the authorities, so the change from a conventional bonus scheme to clawback causes a change in the subjects’ behavior. Nurmayanti et al. (Citation2022) find that, in general, the top management team is more likely to choose the strategic choice of real-based earnings management compared to accrual management. Febrianto et al. (Citation2022) investigated the relationship between earnings management and a bank’s intention to choose clawback, pre- and post- the enactment of the Indonesian Financial Services Authority (FSA) regulation number 45/2015, and concluded that banks may have managed their earnings after the implementation of the OJK’s regulation. This result indicates that banks that opt to adopt a clawback provision manage their earnings. By adopting a clawback provision, while reporting an increase in earnings, banks may pay their employees based on their current year’s performance.

The Indonesian government, through the FSA, has made various rules related to governance to prevent fraud and the governance of remuneration. The anti-fraud control strategy has been stated in the Indonesian FSA Regulation No. 39/POJK.03/2019 concerning the Implementation of Anti-Fraud Strategies for Commercial Banks. The Bank Anti Fraud Policy is the main foundation for the implementation of the anti fraud strategy through four pillars of the fraud control system: fraud prevention; fraud detection; investigation, reporting and imposition of fraud sSanctions; fraud monitoring; evaluation and follow-up. The government implemented FSA Regulation No.45/POJK.03/2015 concerning the Implementation of Governance in Providing Remuneration for Commercial Banks. The implementation of governance in the provision of remuneration has considered various aspects, including the financial stability of the bank, risk management, short-term and long-term liquidity needs, as well as the potential for future earnings. The company may defer variable remuneration or clawback variable remuneration that has already been paid to officers classified as material risk takers (MRT). The FSA Regulation No.45/2015 defines the holdback as a policy that permits banks to withhold payment of all or a portion of the variable compensation. It means that, even though the bank has a pay-for-performance compensation policy, the bank can defer this payment until some conditions in the future are met. For example, if the holdback policy correlates with credit default, the bank will defer the payment until the probability of default is low.

The phenomenon of clawbacks does not only occur in executive compensation, but also in initial public offerings (IPOs). Clawback in an IPO is a mechanism for allotting additional ownership of a share, if the demand for shares in the pool has exceeded the number available, then the excess (with a certain percentage) will be determined and the amount of shares taken from the fixed allotment portion. Unlike clawback in the context of executive compensation, clawback in IPOs provides an opportunity for retail investors to obtain additional shares. Clawback in IPOs is regulated by OJK Regulation No.15/SEOJK.4/2020. Several companies that have carried out clawback mechanisms during IPOs include PT Archi Indonesia Tbk, (2021), PT Bukalapak Tbk. Tbk (2021), and PT GoTo Gojek Tokopedia Tbk (2022).

3. Theoretical literature review

Our discussion is based on the agency theory, moral disengagement, and the supernatural monitoring hypothesis, which explain the effect of moral disengagement on earnings management. Also, they explain clawback as a moderator of that relationship as follows:

3.1. Agency theory

In order to explain the relationship between shareholders and managers, the agency theory is applied. According to this theory, the information asymmetry that results from separating a company’s ownership and management can lead to potential conflicts of interest between shareholders and managers (Jensen & Meckling, Citation1976). Compared to shareholders, managers have access to information about the business’s activities, assets, liabilities, and opportunities (Fama & Jensen, Citation1983; Jensen & Meckling, Citation1976). Information asymmetry can lead to situations where managers become opportunistic and act in their own interests, rather than the interests of the shareholders (Jensen, Citation1993). Management has the ability to manipulate information or make decisions that benefit them at the expense of shareholders. Management is concerned with obtaining high salaries, power, or prestige, whereas shareholders are concerned with maximizing returns on their investments.

The practice of managers manipulating earnings can be explained by the agency theory. To meet or exceed the expectations of their shareholders or other stakeholders, managers manipulate the stated earnings. Managers have the motivation to deceive shareholders by misrepresenting the financial data, to further their own interests, which lowers the quality of the financial reporting. According to the agency theory, managers are motivated to manipulate earnings in order to maintain their position and persuade shareholders that they are performing well (Oussii & Klibi, Citation2023). Managers can improve their remuneration, job security, and other perks by artificially inflating profitability, even at the expense of long-term shareholder value.

Earnings management is the indiscriminate use of reports and transaction records to falsify financial statements, mislead certain shareholders about a company’s financial performance, or influence the outcome of contracts that are dependent on reported accounting calculations (Healy & Wahlen, Citation1999). Numerous studies have examined the motivation of managers to influence earnings in line with the agency theory. Healy (Citation1985) found empirical evidence that executives manage earnings reductions when their bonuses reach their limit. DeAngelo (Citation1988) discovered that managers exercise judgment in selecting accounting standards to give shareholders a good picture of firm performance. According to Dechow and Sloan (Citation1991), managers lower R&D expenses in the last year of their employment, in order to boost reported profitability. Recently, several researchers, such as Zalata et al. (Citation2019), have investigated several techniques to lessen earnings manipulation. Findings from a sample of US corporations show that female directors in supervisory positions have a negative impact on managerial opportunism, as shown by discretionary accruals. Elghuweel et al. (Citation2017) discovered that companies with higher governance typically have lower levels of earnings manipulation than companies with poor governance. Female directors with a suitable financial background can lessen earnings management, according to research by Zalata et al. (Citation2022).

Earnings manipulation can be divided into two broad categories: earnings manipulation outside the GAAP corridor (fraud) and inside the GAAP corridor (accounting and real activity manipulation) (Healy & Wahlen, Citation1999). Discretionary accruals are a means of increasing or decreasing a management’s reported earnings through subjective choices in accounting policies (Scott, Citation2009). Manipulation of real activities constitutes a deviation from the normal course of business for an enterprise, yet the management seeks to mislead stakeholders into believing that certain financial reporting objectives have been achieved through the ordinary course of business of the enterprise (Roychowdhury, Citation2006). Increased sales due to longer credit periods, reduced costs due to an increased production volume, and reduced R&D and advertising are all examples of real activity manipulation (Roychowdhury, Citation2006).

Each earnings manipulation method has a different impact. Manipulating accruals has no direct impact on cash flow, so it is less likely to decrease firm value (Badertscher, Citation2011). Meanwhile, manipulating real activities by reducing discretionary spending will impact the cash flow, meaning that in the long run it will negatively impact optimal business operations, possibly damaging the value of the company (Badertscher, Citation2011) and the future cash flows (Cohen et al., Citation2008). Despite the fact that this decreases cash flow and firm value, the danger of real activity manipulation being exposed is actually lower than that with accruals (Badertscher, Citation2011) because the examination of discretionary cost reductions will not be given top priority by auditors or regulators.

The antecedents of accrual manipulation and real activity manipulation, for instance, were examined in prior studies. Al-Begali and Phua (Citation2023) found that the CEO’s non-duality and age reduce real earnings management and improve the quality of financial reporting. However, the CEO’s age increases accrual earnings management and the concentration of family ownership increases the power of older CEOs to engage in accrual earnings management, and also influences the quality of the financial reporting. Alhebri et al. (Citation2020) found that family businesses have lower earnings quality due to manipulation of accruals and real activities. Cheung and Chung (Citation2022) found that Hong Kong companies with audit committee membership tended to have a higher level of real earnings management. A strong audit committee will encourage managers to use their discretion to change earnings management strategies from actual manipulation to real activities.

3.2. Social cognitive theory

According to the social cognitive theory, human functioning is the consequence of a dynamic interaction between a person’s environment and behavioral factors (Bandura et al., Citation1996). The social cognitive theory has several facets, moral disengagement being one of them (Bandura, Citation1986, Citation1991, Citation1999). Moral disengagement is a set of cognitive mechanisms that enable individuals to disconnect from their internal moral standards and behave unethically without feeling guilty (Bandura, Citation1986, Citation1999). Bandura proposed eight cognitive mechanisms that separate a person from the internal moral standards of his or her actions (Moore, Citation2015), and explain why individuals commit unethical actions without self-criticism (Bandura, Citation1986). These eight mechanisms fall into four categories or loci.

The first locus is people ethically disengaging by describing their actions euphemistically, morally justifying their actions, and making favorable comparisons. The second locus is the locus of agency: The way the individual understands the choice of action. The locus of agency includes mechanisms for shifting responsibility. The perpetrator feels no need to take responsibility for his/her immoral behavior and shifts responsibility to external forces or decision-makers higher up in the organizational hierarchy (Bandura, Citation1999).

The third area of moral disengagement is when repercussions are ignored or distorted. This is when someone chooses to downplay the pain their actions have caused, convinces others that the harm is not as severe as it actually is, or believes they haven’t done any harm at all (Bandura, Citation1999). The fourth locus deals with methods of dehumanization and attribution (assigning blame). Dehumanization, as defined by Bandura (Citation1999), occurs when those who do immoral acts see their victims as worthy of harm or as less humane than other people. Attribution refers to a situation where the perpetrator tries to blame someone else, usually the victim, for the immoral act and absolves himself/herself of responsibility.

Moral disengagement is a key mechanism through which motivated reasoning exerts its influence in the area of morality. Moral disengagement helps to facilitate such a process since it allows individuals to stop regulating themselves and feeling guilty for violating ethical standards (Detert et al., Citation2008; Moore et al., Citation2012).

3.3. The supernatural monitoring hypothesis

The supernatural monitoring hypothesis (SMH) makes the assumption that obeying a supernatural agency (God) is equivalent to obeying secular authorities like leaders, judges, and the police (Gervais & Norenzayan, Citation2012). According to the SPH, punishment—whether administered by God or human institutions (police, judges), plays a significant part in encouraging prosocial and cooperative behavior (Yilmaz & Bahçekapili, Citation2016).

In order to increase ethical behavior, businesses have lately established clawback procedures. In the event that false representations are discovered in financial reports, the clawback settlement method enables the board of directors to revoke any remuneration that has been provided to managers (Chan et al., Citation2015). According to Zalata et al. (Citation2019), from 1992 to 2014, misclassification and shifting earnings manipulation by US corporations was widespread prior to the passage of the Sarbanes-Oxley (SOX) Act. Due to the high likelihood of lawsuits, which could result in a 25-year prison sentence and a personal fine of $15 million for company officials if proven guilty, the litigation risk and the cost increase with the passage of SOX, misclassification shifting decreased with the implementation of the SOX Act’s penal provisions, especially among companies with female CEOs. Because clawback has a penalty feature, managers will be more likely to abide by the rules and less likely to manipulate earnings (Chan et al., Citation2015; Dechow et al., Citation2010; Sari & Sholihin, Citation2019; Sari et al., Citation2023).

4. Empirical literature review and hypotheses development

4.1. Ethical orientation as an antecedent to moral disengagement

Moral disengagement refers to a series of cognitive processes that allow people to lose touch with their own moral norms and act unethically (Bandura, Citation1986, Citation1999). Over the past years, there has been a sharp surge in research into the causes of moral disengagement. The researchers examined the antecedents of moral disengagement, such as beliefs about interpersonal justice (Lee et al., Citation2017), beliefs about the ethics of financial management (Beaudoin et al., Citation2015), beliefs about moral identity (Kennedy et al., Citation2017; McFerran et al., Citation2010; Vitell et al., Citation2011), beliefs about moral personality (McFerran et al., Citation2010), and beliefs about religion (Vitell et al., Citation2011). In addition, previous studies have also examined factors that increase moral disengagement, such as resource depletion (Lee et al., Citation2016), psychopathy (Stevens et al., Citation2012), and negative emotions (Fida et al., Citation2015). However, there are only a few studies that examine ethical orientation as an antecedent to moral disengagement.

An individual’s moral orientation can be described as a continuum with relativism at one end and idealism at the other (Forsyth, Citation1980). Idealistic people are more likely to gravitate toward moral decisions that are widely accepted. Relativists, on the other hand, disregard universal moral principles when making decisions and only take into account what is in their own best interests (Chan & Lai, Citation2011; Douglas et al., Citation2001).

Idealistic individuals tend to maintain standards and avoid actions that are harmful to others, while relativist individuals focus more on personal interests than on the interests of society. Idealistic individuals are more likely to activate their own personal moral standards, making it even more difficult for them to adopt strategies for rationalizing unethical behavior; thus the tendency to disengage morally or to deactivate their personal moral standards will be reduced. On the other hand, if someone believes in individual relativism, he/she is less likely to activate his/her own personal moral standards, making it simpler for him/her to adopt justifications for unethical behavior. This will result in a disengagement of their own personal moral standards and any self-sanctions connected to unethical acts of behavior. Therefore, we predict that:

H1:

Relativism (idealism) has a positive (negative) influence on moral disengagement

4.2. The effect of moral disengagement on earnings manipulation

The agency theory states that managers are incentivized to manipulate earnings in order to maintain their positions and persuade shareholders that they are performing well (Oussii & Klibi, Citation2023). Because management has greater access to information than shareholders do, they can take actions that favor them at the expense of shareholders, such as manipulating financial figures to increase their compensation. Earnings manipulation is an immoral behavior with harmful repercussions (e.g., Johnson et al., Citation2013; Kaplan, Citation2001; Vinciguerra & O’Reilly-Allen, Citation2004). There has been an increasing number of ethical scandals in various organizational contexts (e.g. earnings manipulation).

Moral disengagement based on the social cognitive theory explains why individuals knowingly engage in socially inappropriate behavior. The moral disengagement theory posits that acts in which a person deactivates his/her moral regulatory processes are positively associated with unethical behavior (Keem et al., Citation2018; Knoll et al., Citation2016; Tasa & Bell, Citation2015; Welsh et al., Citation2015). Moral disengagement causes people to disregard their own moral values and participate in immoral behavior, such as manipulating earnings without feeling bad. Especially in the context of accounting, Beaudoin et al. (Citation2015) and West and Fleischman (Citation2023) empirically confirmed there is a positive relationship between the measures of moral disengagement and accrual manipulation activity. Thus, we formalize this argument with the following hypothesis:

H2:

Moral disengagement has a positive effect on accrual manipulation

H3:

Moral disengagement has a positive effect on real manipulation

4.3. The mediation effect of moral disengagement on the relationship between ethical orientation and earnings manipulation

According to the social cognitive theory, moral disengagement is a key mechanism that mediates the impact of individual differences on unethical behavior (Ogunfowora et al., Citation2013). For instance, Basaad et al. (Citation2023) found that moral disengagement completely mediated the relationship between exploitative leadership and unethical pro-organizational behavior.

The individual differences that lead to moral disengagement include ethical orientation. An individual’s willingness to compromise his/her own values is inversely related to this/her idealism, making him/her less likely to manipulate earnings. The tendency to disengage morally or deactivate one’s own personal moral standards will be reduced as a result, which will reduce the intention to engage in unethical actions like earnings manipulation. High idealists are more likely to uphold their own personal moral standards, which makes it harder for them to acquire justifications for immoral behavior. Relativists, on the other hand, are more likely to view earnings management as generally beneficial. Because they are less inclined to invoke their own individual moral norms, relativists find it simpler to adopt tactics to excuse unethical actions. This implies that they will be detached from their own moral principles against engaging in immoral activities, including earnings management.

In the accounting context, Beaudoin et al. (Citation2015) and West and Fleischman (Citation2023) found that the nature of moral disengagement mediated the relationship between certain identified key antecedents (such as cynicism and ethical perceptions) and unethical decision-making. Beaudoin et al. (Citation2015) found that the moral traits of disengagement act as a mediating variable between ethical perceptions of earnings manipulation and the discretionary cost manipulation relationship. Meanwhile, West and Fleischman (Citation2023) found that moral disengagement mediates the relationship between cynicism and the opportunistic behavior of earnings manipulation.

We expect idealistic individuals to have a lower tendency to disengage morally. In turn, idealistic individuals with lower moral disengagement tend to lower the intention to manipulate earnings. Conversely, relativistic individuals have a higher moral disengagement tendency, so the intention to manipulate earnings is high. Thus, it is predicted that ethical orientation affects their tendency to disengage morally, which in turn affects the intention to manipulate earnings differently. Therefore, we hypothesize:

H4:

Relativism (idealism) has a positive (negative) impact on manipulating accruals through moral disengagement.

H5:

Relativism (idealism) has a positive (negative) impact on manipulating real activity through moral disengagement.

4.4. The interaction effect of moral disengagement and clawbacks on earnings management

According to the supernatural monitoring hypothesis (SMH), an individual is more likely to act faithfully, cooperatively, and prosocially when he or she is punished by God or a higher authority (Yilmaz & Bahçekapili, Citation2016). The punitive feature of clawbacks allows the board to recover executive compensation paid on the basis of false financial statements provided by the executives (Chan et al., Citation2015). Managers will be encouraged to follow the rules in order to avoid penalties and lower the amount of earnings manipulation because of the punitive nature of clawbacks (Chan et al., Citation2015; Dechow et al., Citation2010; Sari & Sholihin, Citation2019; Sari et al., Citation2023).

This study focuses only on the types of earnings manipulation that still exist in the corridors of accounting standards, namely the manipulation of real activities and accruals. This type of earnings manipulation poses an ethical dilemma, as there are different ethical perceptions of earnings manipulation. Some suggest that it is inherent to the outcome of the financial reporting process, in that it does not diminish the usefulness of accounting earnings (e.g. Graham et al., Citation2005; Lin et al., Citation2012). In general, however, earnings management is unethical because it is designed to prepare financial statements to meet management’s expectations for a company’s financial position and performance, resulting in misrepresentation of the firm’s performance (Diana & Mădălina, Citation2008), leading to negative consequences (Badertscher, Citation2011; Bertrand et al., Citation2002; Cheung et al., Citation2006; Cohen et al., Citation2008; Kaplan, Citation2001).

When faced with an ethical dilemma, a person with a high moral disengagement tendency will adopt a strategy to rationalize earnings manipulation, even though it has a negative impact. There are eight interconnected cognitive mechanisms, which enable people to let go of the self-condemnation that controls their conduct, that lead to moral disengagement (Bandura, Citation1986, Citation1991, Citation2002). People possess moral principles that, when used, serve as a deterrent to their own immoral behavior. However, there is a propensity for people to employ tactics to rationalize, defend, or downplay their unethical decisions, or to abandon their moral standards of behavior (Bandura et al., Citation1996). This reduces cognitive anxiety and permits them to act unethically, which, according to the moral disengagement theory, means that people will consciously engage in socially inappropriate/delinquent behavior, such as managing earnings (e.g. Beaudoin et al., Citation2015).

The characteristics of punishment will further stimulate people’s moral standards because they will be encouraged to follow the rules in order to avoid punishment. This makes it challenging for them to acquire justifications for unethical activity; as a result, their propensity to morally disengage from or shirk their own moral principles will be weakened in the face of clawbacks. However, since modern society has become more materialistic, moral norms have steadily lost their hold on many facets of daily life (Berger, Citation1967; Gorski, Citation2000). Therefore, even with penalties, the intention to manipulate earnings still persists (Chan et al., Citation2015). The regulators initially created the clawback model to enhance the accuracy of financial accounts. In reality, however, the implementation of clawbacks forces managers to select earnings management strategies that are harder for auditors and regulators to spot.

Adopters of the clawback model are transitioning from accrual-based earnings management to real earnings management (Chan et al., Citation2015; Hales et al., Citation2018; Sari et al., Citation2023). Consequently, we predict:

H6:

The clawback scheme moderates the effect of moral disengagement on the intention to manipulate earnings, such that when clawbacks are applied, moral disengagement decreases (increases) the intention to manipulate accruals (manipulation of real activities)

5. Research design

5.1. Experimental design and participants

To test the hypotheses, an experimental study using a within-subject design was conducted. Two 45-minute-long experimental sessions were held. Participants were given the scenario of a corporation in the first section and asked to choose the appropriate policies. The measurement of moral disengagement, their ethical direction, and individual qualities are covered in the second section. Third, they responded to questions in the exit questionnaire regarding the experiment’s understanding and demographic details.

The participants include master’s level accounting students and accounting professionals. Professional accountants were chosen as participants because, according to Geiger and Smith (Citation2010), they all experience the desire to manipulate earnings.

There were 271 participants who took part in the experiment, but 12 participants did not complete the questionnaire, and 9 participants failed the manipulation check. Consequently, 250 participants in all were used Table .

Table 1. Participants

5.2. Dependent variable

The intention to manipulate earnings is the use of subjective reporting and estimating techniques to meet earnings targets. A modified version of the tool used by Clikeman and Henning (Citation2000), Jones (Citation2013), Sari and Sholihin (Citation2019) is used to demonstrate the intention to manipulate accrual and real activity. Participants were asked to select one of the recommended actions from a list of proposals Table .

Table 2. Proposals provided to participants

From Table , the participants could see the scenario and they could choose the appropriate policy. In the first recommendation (Proposal A), the company is considering the postponement of building maintenance recognition. If Proposal A is selected, the earning target is reached by increasing the actual revenue by 20% and an amount equal to 20% of the net profit will be paid out as compensation to the participants. In the second recommendation (Proposal B), the company is considering lowering the building maintenance costs. If Proposal B is selected, actual revenue will increase by 15%, achieving the earnings goal, and participants will receive $15 or 15% of net earnings as compensation. Then, if the participant is in the clawback plan, he/she will have $10 deducted from his/her salary if the auditor detects accrual earnings manipulation. Lastly, if the participant is in the clawback plan, the participant’s compensation will be reduced by $6 when the auditor notices this.

5.3. Moderating variable

The compensation plan—with or without clawbacks—is the manipulated variable. First, the compensation system that was employed did not have a punishment component. In order to achieve the targeted earnings, participants in this scheme must select from various proposals. Compensation will be granted if the participant meets the earnings target. To verify the participant’s responses and look for any earnings manipulation, the experimenter invited an auditor to participate.

Second, a clawback compensation system is employed. Participants in the clawback mechanism are informed that there is a punitive component. The remuneration paid during the session must be returned if a participant is discovered to be manipulating earnings. Proposals comparable to those from session one were given to the participants, and they were tasked to come up with strategies to meet the earnings targets. The auditor examines the participants’ responses to look for evidence of earnings manipulation.

5.4. Mediating variable

Moral disengagement is the propensity for someone to disregard their own moral standards and engage in unethical behavior without feeling guilty about it. A tool developed by Moore et al. (Citation2012) was adapted to measure moral disengagement.

5.5. Independent variable

Relativism and idealism are at opposite ends of the ethical orientation spectrum. Idealistic decision-making is the tendency of a person to follow the recognized norms. Relativism, in contrast, is a decision-making perspective that exclusively takes into account the person’s best interests. A modified version of a test developed by Douglas et al. (Citation2001) was used to test ethical orientation.

5.6. Manipulation checks

The final stage of this experimental study is manipulation checks. To make sure that the participants are aware of the situation they are being given, manipulation checks are carried out. “Will there be punishments if earnings manipulation is found?” is one of the manipulation check items. A summary of the study’s theoretical framework is shown in Figure .

Figure 1. Theoretical model.

We test the theoretical model as depicted in Figure . Ethical orientation, as an antecedent of moral disengagement, with earnings manipulation as a consequence. The punishment aspect of clawback is predicted to moderate the relationship between moral disengagement and the intention to manipulate earnings.

6. Empirical results and discussion

6.1. Empirical results

Table presents the demographic data. There were 144 female participants (57.6%) and 106 males (42.4%). The number of male and female participants was relatively equal. Owusu et al. (Citation2022) found the use of female auditors is an effective mechanism to reduce earnings manipulation. However, in this study there was no significant difference in the number of male and female participants, so it is unlikely to affect the results of the study. Participants were accountants who were currently studying for a Master of Management (42.4%), Master of Accounting (36.8%) or a Master of Science in Accounting (20.8%). Job experience was determined by the participants’ ages. The largest age range was 23–24 (57.6%). There were 59.2% of the participants with a GPA below 3.25, while 40.8% were above 3.25. It is possible that the GPA would cause differences in understanding of the cases given in the experiment. However, the results showed that only nine participants did not pass the manipulation check Table .

Table 3. Frequency distribution of demographic variables

Table 9. Results of multigroup analysis bootstrap of compensation scheme

The PLS path modeling is used to evaluate the validity and reliability of the constructs and evaluate the theoretical model simultaneously. PLS path modeling is used for its ability to evaluate concurrently complex sets of relationships, including latent variables, related constructs, mediations, and pathways analysis. PLS pathway modeling is also suitable for smaller sample sizes (Chin, Citation1998).

The reliability measurement indicators (Table ) show: (1) Cronbach’s alpha exceeds 0.7 and (2) composite reliability exceeds 0.7. So it can be concluded that the items used to represent the construct are reliable.

Table 4. Result of measurement model, reliability and validity

Convergent validity indicates that the indicator has a positive correlation with alternative indicators for the same construct. Reflective construct indicator items must have high convergence, or share the variance. Convergent validity was tested by using average variance extract (AVE). The AVE value must be greater than 0.5 in order to find convergent validity (Hair et al., Citation2017). Table shows AVE values greater than 0.5 for all constructs. Based on these measures, the reliability and convergence values of latent variables are acceptable.

The discriminant value reveals how much the latent variable or component genuinely differs from the other components. The findings in Table demonstrate that the diagonal column’s square root of AVE is bigger than the column’s correlation coefficient of variables. With the components showing as expected, the discriminant validity of the notions can be accepted. The reliability, convergent validity, and discriminant validity criteria are met, according to the results of the measurement model test.

Table 5. Discriminant validity

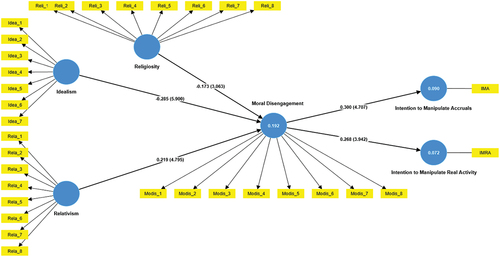

In order to systematically determine whether the structural model’s hypothetical statements are confirmed by the data, structural model validation is performed (Hair et al., Citation2017). Figure displays the PLS-SEM structural model’s test results using SmartPLS, with license keys PRO-S294D9AD2X-AC65E5C1DB284A8E883BF7EF63551DA5158.

Figure 2. Structural model estimates.

Figure shows the outcomes of our evaluation of six hypotheses in accordance with the corresponding coefficient path values from the structural model. According to Hypothesis 1, relativism and idealism have a positive (negative) impact on moral disengagement. There is a positive correlation between relativism and dispositions for moral disengagement, according to our prediction that someone with a relativistic ethical orientation will have a higher tendency for moral disengagement. The results show a positive significant path coefficient (β = 0.219, p < 0.001) on the relationship between relativism and moral disengagement. Conversely, individuals with an ethical idealism orientation will reduce the tendency for moral disengagement. The observed path negative coefficient (β=-0.285) is significant (p < 0.001) in the relationship between idealism and moral disengagement. This confirms Hypothesis 1.

Practically, these results indicate that individuals who tend to be more idealistic when faced with an ethical dilemma will tend to move towards a stronger idealistic position (maintaining moral norms and standards). That is, idealists in this condition will adopt stronger beliefs to avoid these potential problems. Those who are more relativistic also tend to seek personal gain more frequently, which tends to support their relativistic viewpoint. This outcome is largely consistent with the results (Douglas & Wier, Citation2000; Shaub et al., Citation1993) that people tend to improve their ethical orientation when faced with complex business challenges. Growing research on the individual-level causes of moral disengagement is supported by this finding, which also shows that individual differences like moral personality (McFerran et al., Citation2010) and religiosity (Vitell et al., Citation2011) all affect people’s propensity to be morally disengaged. These findings are in line with those of Greenfield et al. (Citation2008)who discovered that people with a relativistic (as opposed to idealistic) ethical perspective were more (as opposed to less) likely to practice earnings management.

Consistent with our arguments leading to H2, the test results show that moral disengagement has a positive effect on the intention to manipulate accruals (β = 0.300, p < 0.001). In turn, individuals with higher (lower) moral disengagement tendencies will have a higher (lower) intention to manage accruals. Likewise, the results of the H3 test showed that moral disengagement has a positive effect on the intention to manipulate real activities (β = 0.268, p < 0.001). This finding is consistent with Beaudoin et al. (Citation2015) who showed that the individual characteristics of morally disengaged thinking will lead to justification for taking unethical actions.

Hypothesis 4 predicts that there will be a positive (negative) relationship between relativism (idealism) and accrual manipulation through moral disengagement. Individuals who tend to be relativistic have a higher intention to manipulate accrual manipulation through moral disengagement. The results show a positive and significant path (β = 0.166, p < 0.01). Likewise, individuals who are idealistic have a lower tendency to manipulate accruals through moral disengagement. The results show a significant negative path coefficient (β = −0.186, p < 0.001) for the mediating effect of moral disengagement on the relationship between idealism and the intention to manipulate accruals, supporting hypothesis 4 Table .These results suggest that moral disengagement is a fundamental mechanism that explains the effect individual differences have on measures of unethical behavior.

Table 6. Structural model and indirect effect results

The results of this study also support hypothesis 5 which posited that individuals who tend to be relativistic have higher intentions to manipulate real activities through moral disengagement (β = 0.159, p < 0.01). Likewise, individuals who are idealistic have a lower tendency to manipulate real activity through moral disengagement (β = −0.176, p < 0.01).

According to hypothesis 6, the clawback program will moderate the impact of moral disengagement on the intention to manipulate earnings. The findings indicate that, when clawback is used, moral disengagement has no discernible impact on the desire to manipulate accruals. The intention to participate in real manipulation was considerably positively impacted by moral disengagement (β = 0.446, p < 0.001). However, if clawbacks are not used, moral disengagement has a significantly negative impact on the desire to manipulate accrual (β = 0.426, p < 0.001), while its impact on the intention to real activity manipulation is not significant Table .

Table 7. Results of multigroup analysis of compensation scheme

A propensity for moral disengagement will, in turn, affect differently the level of earnings management depending on the presence or absence of a clawback scheme. That is, when clawbacks are applied, moral disengagement has no effect on the intention to manipulate accruals. However, in the end, when clawbacks have a punishment feature, the tendency of moral disengagement will have an impact increasing the kind of hard-to-detect earnings manipulation, namely real activity manipulation. This is in line with the findings of Beaudoin et al. (Citation2015) who showed that the bonus compensation scheme moderates moral disengagement and discretionary expense decisions.

6.2. Test of endogeneity and additional analysis

6.2.1. Test of endogeneity

Endogeneity is the determination of a set of control variables that account for part of the variance of the dependent variable (Ebbes et al., Citation2017). Ignoring endogeneity results in imprecise parameter estimates and invalid conclusions. In the initial stage of the regression, we linked ethical orientation with moral disengagement. However, these findings may be imprecise due to the endogenous matching between ethical orientation and the attributes of moral disengagement. Under such circumstances, causality may shift from moral disengagement to ethical orientation, or vice versa. Therefore, the inverse relationship cannot be ignored and endogeneity tests must be carried out.

The variable-free instrumental procedure is one of the statistical methods that have been developed to test for endogeneity (Ebbes et al., Citation2017). The Gaussian copula method is one of the most widely used variable-free instrumental procedures (Becker et al., Citation2022; Park & Gupta, Citation2012). Researchers and practitioners can identify and fix endogeneity in PLS-SEM (i.e., for relationships in structural models) by using the Gaussian copula technique. The test results show that the endogeneity problem has not occurred, as seen in the p values in all models, which are not significant Table .

Table 8. Tests of endogeneity: Gaussian copula

6.2.2. Additional analysis

We further tested whether clawback actually moderates the influence between moral disengagement and earnings management by comparing the two groups (clawback and no clawback).

The test results reveal a significant difference between the groups with and without clawback in the influence of moral disengagement on the intention to manipulate accrual (p < 0.01). In addition, there is a significant difference between the groups with and without clawback in the impact of moral disengagement on the desire to manipulate real activity (p < 0.01).

We also look at how religion affects moral disengagement because, in accordance with the supernatural punishment hypothesis (SPH), believing in a God—who is aware of every action people take and has the power to punish them for their transgressions—motivates people to uphold their moral obligations (Yilmaz & Bahçekapili, Citation2016). Additional test results show that religiosity has a negative effect on moral disengagement (β = −0.173, p < 0.01). The higher a person’s religiosity, the more it will be effective in preventing moral disengagement behavior.

7. Discussion

A theoretical justification for the practice of earnings management is provided by the agency theory. To meet or exceed the expectations of shareholders or other stakeholders, managers manage earnings. This study assesses the behavior of accountants through their “black box” psychological reasoning, which is related to the tendency to disengage morally in certain situations and to justify earnings manipulation by presenting a clawback compensation scheme.

Moral disengagement is a collection of cognitive mechanisms that enable people to disregard their own moral principles and engage in unethical behavior, such as manipulating profits, without feeling bad about it. We found that an ethical orientation is an antecedent of moral disengagement. These findings support the idea that individual differences, such as moral personality (McFerran et al., Citation2010) and religiosity (Vitell et al., Citation2011), all have an effect on the probability that individuals are morally disengaged. Likewise, with the test results, it was found that moral disengagement had a positive effect on the intention to manipulate earnings. This finding is consistent with Beaudoin et al. (Citation2015) and West and Fleischman (Citation2023), who showed that the individual characteristics of thoughts regarding moral disengagement will lead to justification for unethical actions, such as earnings manipulation.

We also found that moral disengagement mediates the influence of ethical orientation on earnings management intentions. Individuals who tend to have a relativist perspective have a higher intention to manipulate accrual activity (and also manipulate real activity) through moral disengagement. Meanwhile, individuals with an idealist perspective have a low tendency to manipulate accruals (or manipulate real activities) through moral disengagement. This finding supports the work of Beaudoin et al. (Citation2015) and West and Fleischman (Citation2023), who showed that moral disengagement mediates the relationship between certain key antecedents (such as cynicism and ethical perception) and earnings management. These studies support Bandura (Citation1986, Citation1991, Citation2002), in that moral disengagement allows an individual to disengage from the self-sanctions that govern his/her behavior. People adopt moral standards (e.g., ideals and values) which, when active, serve as self-reactive deterrents to unethical behavior. However, individuals use strategies to rationalize, justify, or downplay their unethical choices—i.e., to disengage their moral standards from their conduct—thereby protecting their self-image, minimizing cognitive distress and proceeding to act unethically (Bandura et al., Citation1996).

Organizations concentrate on pay contract structures in an effort to reduce earnings management, with the majority of the studies focusing on bonuses (Beaudoin et al., Citation2015; Crocker & Slemrod, Citation2006; Evans & Sridhar, Citation1996; Jensen & Meckling, Citation1976; Watts & Zimmerman, Citation1986). In order to prevent conflicts of interest between managers and shareholders, and to foster an ethical management culture, this study has investigated the effectiveness of clawbacks (Mahdy, Citation2019).

The supernatural monitoring hypothesis contends that when there are indications of punishment from God, or another higher authority, people are more likely to act morally (Yilmaz & Bahçekapili, Citation2016). The clawback compensation scheme’s punitive element incentivizes managers to scale back their use of earnings manipulation (Chan et al., Citation2015; Dechow et al., Citation2010; Sari & Sholihin, Citation2019; Sari et al., Citation2023).

The results of this study found empirical evidence that the clawback compensation scheme moderates the impact of moral disengagement on intentions to manipulate earnings. The findings show that, when clawback is used, moral disengagement has no effect on the desire to manipulate accruals but has a significant positive effect on the intention to manipulate real activities. However, if clawback is not implemented, moral disengagement has a significant negative impact on the desire to manipulate accruals but has no impact on the intention to manipulate real activities. This research supports previous research using secondary data that clawback reduces misstatements in financial reports (Chan et al., Citation2012; DeHaan et al., Citation2013; Natarajan & Zheng, Citation2019; Remesal, Citation2018). However, the adoption of clawback has negative effects, specifically a change in the method used to manipulate earnings from one that is hard to detect (accrual-based earnings management) to one that is easy to detect (real earnings management) (Chan et al., Citation2015; Hales et al., Citation2018; Sari et al., Citation2023).

8. Conclusion

We have extended the previous research regarding moral disengagement in earnings management behavior by examining the antecedents of moral disengagement, and the strategies for reducing earnings management. In conclusion, these data provide credence to the hypothesis that individual variations (such as ethical orientation) influence the likelihood that people are morally disengaged. Additionally, it was discovered that moral disengagement had an encouraging effect on the desire to manage earnings. Additionally, we found that moral disengagement influences the impact of ethical orientation on intentions for managing earnings.

The results of our analysis are in line with prior research that used secondary data to demonstrate, empirically, that clawbacks are adversely associated with financial statements or misstatements (Chan et al., Citation2012; DeHaan et al., Citation2013; Natarajan & Zheng, Citation2019; Remesal, Citation2018). Clawbacks, unfortunately, have an unintended effect that shifts earnings manipulation from an easily detectable type (accrual manipulation) to a harder-to-detect type (manipulation of real activities) (Chan et al., Citation2015; Hales et al., Citation2018; Sari et al., Citation2023).

The results of our research suggest a number of important implications for research and practice. First, our findings indicate that both ethical orientation and moral disengagement play an important role in modeling accountants’ willingness to engage in earnings management. Our research shows that individual differences regarding ethical orientation provide the impetus for moral disengagement, which ultimately improves earnings management. These findings may be useful to those with business interests, professional associations, and educators, as they can improve business ethics and weaken earnings management behavior by reducing moral disengagement through moral intervention, and ethical education and training. For business and professionals, it is necessary to have moral intervention, for example, and this is carried out through the development of policies, culture, and an ethical climate in an organization (Arel et al., Citation2012). Executives need to consider policies and procedures related to ethical codes and acceptable behavior within the company. For academics, ethics training is needed, including more examples and case studies that focus on situations that pose ethical dilemmas and allow for an analysis of the impact on stakeholders of decisions taken. Understanding these impacts on stakeholders is expected to reduce managers’ justification for manipulating earnings, and their tendency to deactivate their moral reasoning to rationalize such unethical behavior. Previous studies have found that the level of moral disengagement can be reduced through external interventions, for example, through ethics training (Paciello et al., Citation2008). Some empirical evidence suggests that ethics training will have an impact by improving moral sensitivities, ethical reasoning, and even ethical behavior (Loe & Weeks, Citation2000; Lowry, Citation2003; Sims, Citation2002; Weber & Glyptis, Citation2000). In this way, corporate culture and ethics training, which can reduce moral disengagement, are expected to contribute to the integrity of the financial reporting process (Treadway-Commission, Citation1987).

Second, the interaction effect of clawback compensation systems, according to our findings, can lessen the impact of moral disengagement on the intention to manipulate earnings. The punishment aspect of clawback systems is a useful behavior control strategy. We specifically discovered a clawback interaction effect that demonstrates how the fear-of-punishment component of clawbacks can reduce the impact of moral disengagement on the intention to manipulate accruals. However, the implementation of clawbacks also has an unintended consequence, which is an increase in real activity manipulation. People are cautious when selecting earnings manipulation techniques to accomplish earnings targets because of the punitive component of clawbacks. For practitioners, these findings have significant ramifications. It is anticipated that clawbacks address some of the practical complaints about the poor quality of financial reporting. The compensation structure must take into account more than just immediate financial results. However, it must be able to increase the incentives for executives to adopt an ethical management style and meet the long-term goals of the business. The implementation of a clawback system will encourage corporate sustainability because clawbacks encourage managers to align with stakeholder goals by improving the quality of company profits and reducing actions that conflict with the company’s long-term goals (e.g. fraud and earnings manipulation). These results may be of interest to organizations that still use incentive contracts to regulate behavior. We suggest that the joint effect of considering individual differences (ethical orientation, moral disengagement) and appropriate compensation schemes can contribute to maintaining a high-quality financial reporting environment. Third, policy implications. After the enactment of the Indonesian Financial Services Authority (FSA) Regulation No.45/POJK.03/2015 on the Implementation of Governance in the Granting of Remuneration, the Indonesian Financial Services Authority should continue to supervise, enforce and monitor the clawback policies taken by companies, as a strategy to prevent fraud through earnings management.

Regardless of the various contributions it makes, this study has a limitation. This is due to its experimental research participants, who do not make decisions in a real business environment. Therefore, there is a possibility that they do not respond to the given case seriously. So, there might be differences in their responses when they are faced with real-life situations. The limitation of this study offers possibilities for future research. The ability to generalize these results can be exercised by testing and examining different groups of accountants, such as accountants in public organizations, or private accountants, to examine possible differences in the degree of ethical orientation, moral disengagement, and the effectiveness of clawbacks.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Acknowledgments

We acknowledge the Deputy for Research and Innovation Facilitation, Indonesian National Research and Innovation Agency (Badan Riset dan Inovasi Nasional) who has provided research funding with decision letters No: 59/IV/KS/05/2023 and No: T/9/UN34.9/PT.01.03/2023.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The data that supports the findings of this study are available from the Directorate of Research and Community Service Yogyakarta State University (DRPM UNY). However, there are limitations on the accessibility of this data, as it was used under a license specifically for this study and is not openly available to the public. Nevertheless, the authors can provide access to the data upon a reasonable request.

Additional information

Funding

Notes on contributors

Ratna Candra Sari

Ratna Candra Sari Drafting the paper; Substantial contributions to the conception and design of the work; analysis and interpretation of data for the work; ensuring that all questions related to the accuracy or integrity of any part of the work are appropriately investigated and resolved.

Mahfud Sholihin

Mahfud Sholihin Reviewed the paper critically for intellectual content; Final approval of version to be published.

Zuhrohtun Zuhrohtun

Zuhrohtun Drafting the design research, background and theories.

Ida Ayu Purnama

Ida Ayu Purnama Drafting literature review and hypothesis development; accountable for all aspects of the work in ensuring that several questions related to the accuracy or integrity of any part of the work are appropriately resolved.

Umi Syafaatul Udhma

Umi Syafaatul Udhma Drafting literature review and hypothesis development

References

- ACFE. (2022). ACFE report to the nations. https://legacy.acfe.com/report-to-the-nations/2022/

- Al-Begali, S. A. A., & Phua, L. K. (2023). Accruals, real earnings management, and CEO demographic attributes in emerging markets: Does concentration of family ownership count? Cogent Business & Management, 10(2). https://doi.org/10.1080/23311975.2023.2239979

- Alhebri, A. A., Al-Duais, S. D., & Ntim, C. G. (2020). Family businesses restrict accrual and real earnings management: Case study in Saudi Arabia. Cogent Business & Management, 7(1), 1806669. https://doi.org/10.1080/23311975.2020.1806669

- Alnuaimi, O. A., Robert, L. P., & Maruping, L. M. (2010). Team size, dispersion, and social loafing in technology-supported teams: A perspective on the theory of moral disengagement. Journal of Management Information Systems, 27(1), 203–24. https://doi.org/10.2753/MIS0742-1222270109

- Anthony, R. N., & Govindarajan, V. (2007). Management control system (20th ed.). McGraw-Hill.

- Arel, B., Beaudoin, C. A., & Cianci, A. M. (2012). The impact of ethical leadership, the internal audit function, and moral intensity on a financial reporting decision. Journal of Business Ethics, 109(3), 351–366. https://doi.org/10.1007/s10551-011-1133-1

- Badertscher, B. (2011). Overvaluation and the choice of alternative earnings management mechanisms. The Accounting Review, 86(5), 1491–1518. https://doi.org/10.2308/accr-10092

- Bandura, A. (1986). Social foundations of thought and action. Upper Saddle River.

- Bandura, A. (1990a). Origins of terrorism: Psychologies ideologies, states of mind. In W. Reic (Eds.), Mechanisms of moral disengagement (pp. 161–191). Cambridge University Press.

- Bandura, A. (1990b). Selective activation and disengagement of moral control. Journal of Social Issues, 46(1), 27–46. https://doi.org/10.1111/j.1540-4560.1990.tb00270.x

- Bandura, A. (1991). Handbook of moral behavior and development. In <. I. I. A. I. C. M. <. Kurtines & <. I. I. A. I. L. <. Gewirtz (Eds.), Social cognitive theory of moral thought and action (pp. 45–103). Lawrence Erlbaum.

- Bandura, A. (1999). Moral disengagement in the perpetration of inhumanities. Personality and Social Psychology Review, 3(3), 193–209. https://doi.org/10.1207/s15327957pspr0303_3

- Bandura, A. (2002). Selective moral disengagement in the exercise of moral agency. Journal of Moral Education, 31(2), 101–119. https://doi.org/10.1080/0305724022014322

- Bandura, A., Barbaranelli, C., Caprara, G. V., & Pastorelli, C. (1996). Mechanisms of moral disengagement in the exercise of moral agency. Journal of Personality and Social Psychology, 71(2), 364–374. https://doi.org/10.1037/0022-3514.71.2.364

- Baron, R. A., Zhao, H., & Miao, Q. (2015). Personal motives, moral disengagement, and unethical decisions by entrepreneurs: Cognitive mechanisms on the “slippery slope”. Journal of Business Ethics, 128(1), 107–118. https://doi.org/10.1007/s10551-014-2078-y

- Basaad, S., Bajaba, S., & Basahal, A. (2023). Uncovering the dark side of leadership: How exploitative leaders fuel unethical pro-organizational behavior through moral disengagement. Cogent Business & Management, 10(2). https://doi.org/10.1080/23311975.2023.2233775

- Beaudoin, C. A., Cianci, A. M., & Tsakumis, G. T. (2015). The impact of CFOs’ incentives and earnings management Ethics on their financial reporting decisions: The mediating role of moral disengagement. Journal of Business Ethics, 128(3), 505–518. https://doi.org/10.1007/s10551-014-2107-x

- Becker, J. M., Proksch, D., & Ringle, C. M. (2022). Revisiting Gaussian copulas to handle endogenous regressors. Journal of the Academy of Marketing Science, 50(1), 46–66. https://doi.org/10.1007/s11747-021-00805-y

- Berger, P. (1967). The sacred canopy: Elements of a sociological theory of religion. Acta stomatologica Belgica, 64(2), 207–231.

- Bertrand, M., Mehta, P., & Mullainathan, S. (2002). Ferreting out tunneling: An application to Indian business groups. The Quarterly Journal of Economics, 117(1), 121–148. https://doi.org/10.1162/003355302753399463

- Chan, L. H., Chen, K. C. W., Chen, T. Y., & Yu, Y. (2012). The effects of firm-initiated clawback provisions on earnings quality and auditor behavior. Journal of Accounting and Economics, 54(2–3), 180–196. https://doi.org/10.1016/j.jacceco.2012.05.001

- Chan, L. H., Chen, K. C. W., Chen, T. Y., & Yu, Y. (2015). Substitution between real and accruals-based earnings management after voluntary adoption of compensation clawback provisions. The Accounting Review, 90(1), 147–174. https://doi.org/10.2308/accr-50862

- Chan, R. Y. K., & Lai, J. W. M. (2011). Does ethical ideology affect software piracy attitude and behaviour an empirical investigation of computer users in China. European Journal of Information Systems, 20(6), 659–673. https://doi.org/10.1057/ejis.2011.31

- Chen, M., Chen, C., & Sheldon, O. J. (2016). Relaxing moral reasoning to win: How organizational identification relates to unethical pro-organizational behavior. Journal of Applied Psychology, 101(8), 1082–1096. https://doi.org/10.1037/apl0000111

- Chen, M. A., Daniel, T. G., & James, E. O. (2014). The costs and benefits of clawback provisions in CEO compensation. Review of Corporate Finance Studies, Forthcoming, 4(1), 108–154. https://doi.org/10.1093/rcfs/cfu012

- Cheung, K. Y., & Chung, C. V. (2022). The impacts of audit committee expertise on real earnings management: Evidence from Hong Kong. Cogent Business & Management, 9(1). https://doi.org/10.1080/23311975.2022.2126124

- Cheung, Y. L., Rau, P. R., & Stouraitis, A. (2006). Tunneling, propping, and expropriation: Evidence from connected party transactions in Hong Kong. Journal of Financial Economics, 82(2), 343–386. https://doi.org/10.1016/j.jfineco.2004.08.012

- Chin, W. W. (1998). The partial least squares approach for structural equation modeling. Modern Methods for Business Research, April, 295–336. https://doi.org/10.4324/9781410604385-10

- Clikeman, P. M., & Henning, S. L. (2000). The socialization of undergraduate Accounting students. Issues in Accounting Education, 15(1), 1–17. https://doi.org/10.2308/iace.2000.15.1.1

- Cohen, D., Dey, A., & Lys, T. (2008). Real and accrual-based earnings management in the pre- and post-Sarbanes-Oxley periods. The Accounting Review, 83(3), 757–787. https://doi.org/10.2308/accr.2008.83.3.757

- Crocker, K. J., & Slemrod, J. (2006). The Economics of Earnings Manipulation and Managerial Compensation. Wiley.

- DeAngelo, L. E. (1988). Managerial competition, information costs, and corporate governance: The use of accounting performance measures in proxy contests. Journal of Accounting and Economics, 10(1), 3–36. https://doi.org/10.1016/0165-4101(88)90021-3

- Dechow, P., Ge, W., & Schrand, C. (2010). Understanding earnings quality: A Review of the proxies, their determinants and their consequences. Journal of Accounting and Economics, 50(2–3), 344–401. https://doi.org/10.1016/j.jacceco.2010.09.001

- Dechow, P. M., & Sloan, R. G. (1991). Executive incentives and the horizon problem: An empirical investigation. Journal of Accounting and Economics, 14(1), 51–89. https://doi.org/10.1016/0167-7187(91)90058-S

- De Cremer, D., & Vandekerckhove, W. (2017). Managing unethical behavior in organizations: The need for a behavioral business ethics approach. Journal of Management & Organization, 23(3), 437–455. https://doi.org/10.1017/jmo.2016.4

- DeHaan, E., Hodge, F., & Shevlin, T. (2013). Does voluntary adoption of a clawback provision improve financial reporting quality? Contemporary Accounting Research, 30(3), 1027–1062. https://doi.org/10.1111/j.1911-3846.2012.01183.x

- Detert, J. R., Treviño, L. K., & Sweitzer, V. L. (2008). Moral disengagement in ethical decision making: A study of antecedents and outcomes. Journal of Applied Psychology, 93(2), 374–391. https://doi.org/10.1037/0021-9010.93.2.374

- Diana, B., & Mădălina, P. C. (2008). Is creative Accounting a form of manipulation? Annals of the University of Oradea, Economic Science Series, 17(3), 935–940.

- Douglas, P., Davidson, R., & Schwartz, B. (2001). The effect of organizational culture and ethical orientation on accountants’ ethical judgments. Journal of Business Ethics, 34(2), 101–121. https://doi.org/10.1023/A:1012261900281

- Douglas, P., & Wier, B. (2000). Integrating ethical dimensions into a model of budgetary slack creation’. Journal of Business Ethics, 28(3), 267–277. https://doi.org/10.1023/A:1006241902011

- Ebbes, P., Papies, D., & Heerde, H. J. V. (2017). Dealing with endogeneity: A nontechnical Guide for Marketing researchers. In C. Homburg, M. Klarmann, & A. Vomberg (Eds.), Handbook of market research (pp. 1–14). Springer International Publish.

- Elghuweel, M. I., Ntim, C. G., Opong, K. K., & Avison, L. (2017). Corporate governance, Islamic governance and earnings management in Oman a new empirical insights from a behavioural theoretical framework. Journal of Accounting in Emerging Economies, 7(2), 190–224. https://doi.org/10.1108/JAEE-09-2015-0064

- Evans, J. H., & Sridhar, S. S. (1996). Multiple contract Systems, accrual Accounting, and earnings management. Journal of Accounting Research, 34(1), 45–65. https://doi.org/10.2307/2491331

- Fama, E. F., & Jensen, M. C. (1983). Agency problems and residual claims. Journal of Law and Economics, XXVI(2), 327–349. https://doi.org/10.1086/467038

- Febrianto, G. N., Ratnawati, T., & Riyadi, S. (2022). The effect of macroeconomic factor, earning management and financial risk on firms’ value: An empirical analysis of Listed Commercial bank. International Journal of Economics & Finance Studies, 14(2), 156–170. https://doi.org/10.34109/ijefs

- Fida, R., Paciello, M., Tramontano, C., Fontaine, R. G., Barbaranelli, C., & Farnese, M. L. (2015). An integrative approach to understanding counterproductive work behavior: The roles of stressors, negative emotions, and moral disengagement. Journal of Business Ethics, 130(1), 131–144. https://doi.org/10.1007/s10551-014-2209-5

- Fida, R., Tramontano, C., Paciello, M., Ghezzi, V., & Barbaranelli, C. (2016). Reframing the moral limits of markets debate: Social Domains, values, allocation methods. Journal of Business Ethics, 153(1), 1-016-3373–6. https://doi.org/10.1007/s1055

- Forsyth, D. (1980). A taxonomy of ethical ideologies. Journal OfPersonality AndSocial Psychology, 39(July), 175–184. https://doi.org/10.1037/0022-3514.39.1.175

- Geiger, M. A., & Smith, J. V. D. V. D. L. (2010). The effect of institutional and cultural factors on the perceptions of earnings management. Journal of International Accounting Research, 9(2), 21–43. https://doi.org/10.2308/jiar.2010.9.2.21

- Gervais, W. M., & Norenzayan, A. (2012). Like a camera in the sky? Thinking about god increases public self-awareness and socially desirable responding. Journal of Experimental Social Psychology, 48(1), 298–302. https://doi.org/10.1016/j.jesp.2011.09.006

- Gorski, P. S. (2000). Historicizing the secularization debate: Church, State, and society in late Medieval and early modern Europe, ca. 1300 to 1700. American Sociological Review, 65(1), 138. https://doi.org/10.1177/000312240006500110

- Graham, J. R., Harvey, C. R., & Rajgopal, S. (2005). The economic implications of corporate financial reporting. Journal of Accounting and Economics, 40(1–3), 3–73. https://doi.org/10.1016/j.jacceco.2005.01.002

- Greenfield, C., Norman, C. S., & Benson, W. (2008). The effect of ethical orientation and professional commitment on earnings management behavior. Journal of Business Ethics, 83(3), 419–434. https://doi.org/10.1007/s10551-007-9629-4

- Hair, J., Hollingsworth, C. L., Randolph, A. B., & Chong, A. Y. L. (2017). An updated and expanded assessment of PLS-SEM in information Systems research. Industrial Management and Data Systems, 117(3), 442–458. https://doi.org/10.1108/IMDS-04-2016-0130