Abstract

Drawing on Lazarus and Folkman’s transactional stress theory, this study aims to explore a broader range of what constitutes work stress among life insurance agents and their needs for organisational work stress prevention. Face-to-face interviews were conducted with life insurance agents (n = 45) that focused on their stress experiences and needs regarding the prevention of work stress. Performing thematic analysis, topics, and themes were extracted from the verbatim transcribed interviews using Atlas.ti. Respondents located the stress factors that affected their mental health which should be targeted for prevention. Various themes were extracted, falling under job responsibilities, handling customers and maintaining long-term relationships, work pressure, mental health indicators, and measures to handle stress. The findings of this research specified that life insurance agents have multifaceted work stress prevention needs where mapping this could facilitate intervention implementation. The agents were explicit about the causes of stress emerging due to relationship between the individual and the challenging environment, leading to Litigation Stress Syndrome. This study sets a platform for the insurance sector to take necessary steps in helping the agents to mitigate stress and cultivating an innovative habit of mindful selling in them by implementing mindfulness interventions.

1. Introduction

With the rapid urbanisation, economic growth, and popular education, insurance industry expanded considerably in the nineteenth century (Clemente & Cornaro, Citation2022), resulting in acute competitiveness and rivalry between companies (Agyapong et al., Citation2016). The impact of this competitiveness is felt among employees and full-time agents in life insurance industry by engendering general feelings of distrust, tension, strain in interpersonal relations, jealousy from colleagues, interpersonal conflicts, and coping with sustained pressure to produce and perform (Selvan & Abraham, Citation2022). The challenging work conditions that life insurance agents face are alarmingly high due to high job responsibilities, difficulties in pitching a sale with clients, gaining customer trust, and facing hurdles in maintaining long-term relationships that lead to stress (Malik & Shahabuddin, Citation2015).

Insurance sector requires salespeople to allocate their efforts to activities aimed at uncovering each customer’s specific needs. Despite this, research suggests that salespeople often engage in activities which are unproductive and involve themselves in dumping the policies to their clients to fulfil their annual targets (Schwepker & Dimitriou, Citation2022). Survey findings show that salespeople dedicate only 15% of their time to serve the customer while 35% of their time is spent on administrative tasks (Robinson et al., Citation2005). Life insurance agents spend a large portion of their productive time and energy in convincing the customers for the purpose of pursuing sales opportunities that can help them meet their performance goals (Yong-Cheng, Citation2021). The resulting frustration and stress impact both physical health and emotional well-being as stress at workplace is associated with physical and mental health risks that poses a burden to individual employees, organisations, and society at large (Shifrin & Michel, Citation2021). Among service sector employees, life insurance agents are prone to stress factors in their insurance selling business (Chaturvedi & Joshi, Citation2017). If, however, work stress could be mitigated, its detrimental consequences could eventually be curtailed (Ganster & Rosen, Citation2013).

Although life insurance agents in India are at risk of significant work-related stress due to target pressures, deadlines, and stringent IRDA (Insurance Development Regulation of India) norms, very little effort has been made to bridge these literatures, and few studies have examined the impact of stress from the perspective of life insurance agents (Bun, Citation2002). Oversighting the needs of life insurance agents can drastically hinder the success rate of the companies (Lamontagne et al., Citation2007). Intervention development and mindfulness trainings drawn from past research on work stress determinants include psychosocial work factors, as experienced by these life insurance agents (Tsuzuki et al., Citation2012).

Empirical investigation of the emerging reasons for findings regarding work stress among life insurance agents is meagre (Dinesh et al., Citation2022). A better understanding of stress factors that influence employee well-being and views of their jobs is required to allow consideration of how work stress and poor mental health might be prevented or ameliorated among life insurance agents (Fu et al., Citation2020). While both practitioners and academics have recognized that a substantial portion of insurance salespersons undergo different phases in their policy selling journey, no published studies have examined the effect of salespeople’s perceptions on their job responsibilities, maintaining long-term relationship with clients, identifying target customers to pitch a sale, and thereby facing the different challenges in the Insurance selling business.

Few investigators have paid attention to the work experiences and stress factors of life insurance agents and to the best of the researcher’s knowledge, there is no qualitative study published on work stress of life insurance agents. Most studies examining work stress among them are quantitative in nature specially conducted in Western and European countries (Goel & Verma, Citation2020). Hence, conducting a qualitative study in this regard can help to clarify and extend a complete understanding of work stress by considering the effects of work stress on their physical and mental health of the agents in the insurance sector (Sahni, Citation2020). Being retrieved that there is a lack of related studies and attention to individual perceptions, and experiences of Life insurance agents in this area, this qualitative study explores the stress factors, their experiences, and perceptions at workplace.

Taking a step back, need arises on exploring the stress factors of life insurance agents from a long-term vision. Hence, the aim of the current paper is to understand this new phenomenon of exploring the factors leading to stress and the measures to mitigate stress. Our study provides a clear overview of how agents react to their job roles and responsibilities, and how their responsibilities shape their strategies to overcome the challenges by meeting the customers’ expectations.

This paper is structured as follows. First, we provide the literature review on contributing factors of stress at workplace and theoretical context of transactional stress theory including a conceptual framework for this study. Second, we show the methodology adopted to investigate the relationship between the challenges faced and its impact on stress, thus gauging the measures for mitigating stress. Third, the results are presented and followed by analysis in consecutive chapters. Finally, in conclusion, we summarize our findings with limitations and outline directions for further research.

2. Theoretical underpinnings

The transactional stress theory developed by Lazarus and Folkman (Citation1984) was used as the theoretical framework for this study. The interaction between individual and environment, in which working conditions create a feeling of being stressed, is the foundation of Lazarus’ cognitive theory of stress (Goh et al., Citation2010). An individual, according to this theory, has a cognitive assessment of threats that come from the environment known as appraisal. The degree to which an individual appraises stress as a serious threat reveals the degree of stress experienced (Laugeri, Citation2020). However, “stress is not a property of the person, or of the environment, but arises as a conjunction between a particular kind of environment and a particular kind of person that leads to a threat appraisal” (Sivam & Chang, Citation2016). The term transaction indicates that neither the individual nor the environment is carrying stress. What carries either objective or subjective stress emerges from the relationship between the individual and the environment. For instance, work environment encompasses events called stimuli that are encountered in different ways by employees (Woods et al., Citation2019). The responses of individuals to such environmental stimuli are under the influence of their appraisal.

The transactional model of stress (Lazarus & Folkman, Citation1984) proposes that “challenges and threats, arise from cognitive judgments of the meaning of a situation and one’s ability to respond to the situation”. It, however, considers primary appraisal that refers to “to the judgment of a situation as being benign or stressful” (Vos & van Rijn, Citation2021). Benign situations are judged as requiring no instrumental action on the part of the individual to facilitate a positive outcome, whereas stressful situations are judged to require specific actions. Stressful situations themselves fall into two categories: they can be challenging or threatening. In the context of life insurance selling business, challenging situations are those perceived to offer the potential for growth, mastery, and gain (e.g., performing well in the career by making more policies and maintaining long term relationships). Threatening situations are those perceived to potentially result in harm or loss (e.g., difficulties in pitching a sale or failure to fulfil job responsibilities).

The perception of challenge or threat is determined in a secondary appraisal of one’s ability to cope with, and respond to, the stressful situation. Challenge results from the judgment that one has the necessary resources to cope (e.g., I know that pitching a sale of a life insurance policy with clients is not easy, but I have belief in my ability), and threat from the judgment that one does not (e.g., I know that pitching a sale of a life insurance policy with clients is difficult and I may not be able to do it). Even though the implication of secondary appraisals would determine the initial relevance of a situation, primary appraisal highlights that judgments of relevance of a situation precede judgments of coping (Jamieson et al., Citation2022).

Therefore, in this theory, the experience of stress in life insurance agents depends not only on the quality of one’s individual resources and the level of environmental threats but also on the quality of the interactions between individual and environment. Accordingly, by drawing on Lazarus and Folkman’s (Citation1984) theoretical framework, it was possible to conduct a study that described stress factors in life insurance agents and across their professional lives whereby a clear and a fuller picture of work stress could be described from a life insurance perspective.

Life insurance agents have come under fire to gain the trust of the customers where against this backdrop, the rewards and incentives they are procuring have become obscured due to different challenges (Fu et al., Citation2020). Alarming rates of life insurance agents stress come as no surprise where large proportions of them experience psychological distress and mental fatigue when compared with other professions (Muchlish, Citation2020).

In a study done by W.J. Coetzer and S. Rothmann, 1,100 employees in an insurance company were targeted where performance pressure was the contributing sources of work stress among employees in the insurance industry. Other sources of stress within the insurance industry were entwined with possibilities of dealing with difficult and demanding clients, working continually to achieve targets, ability of the agents to survive in the insurance business and to accomplish their career goals, time pressures and meeting deadlines, and also mental strain of work overload (Fu et al., Citation2020). The overall perception of work stress by employees within the insurance industry was associated with work demands, lack of job security, and the need to maintain a professional self.

Mental stress at workplace adversely is widely recognized as a major contributor to poor morale, absenteeism, high staff turnover, and reduced productivity at work. Also, in large-scale studies, service sector employees with high stress have significantly higher annualized medical expenditures (odds ratio = 1.528) compared with those with lower stress, and their medical expenses are estimated at 45–46% above those for lower stress employees (Wolever et al., Citation2012).

The recognition of major sources of workplace stress attempts to offer a twofold benefit for both employees and management where, first, it results in work environment changes ultimately which reduce stress and simultaneously increase productivity. On the other hand, it also facilitates the development of effective interventions and trainings that could reduce the debilitating effects of occupational stress in the agents (Wolever et al., Citation2012). The link streamlined between unmanaged stress and its negative impact on well-being is demonstrated in stress research which showcases severe consequences, some of which may be fatal (Hyun Yoon, Citation2016).

The above literature review allowed us to get an overview of the emerging stress factors, detailing the information concerning the impact of the challenges faced and the measures to mitigate stress along with a theoretical context of impact of stress on life insurance agents. However, this is quite a new phenomenon in the mainstream human resource and psychology, and there are not a lot of literature existing on this topic. Indeed, during the literature review, we noticed that there were no data on life insurance perspective to study their reaction facing challenges and there are also no studies on stress mitigation strategies for life insurance agents who are especially undergoing litigation stress syndrome (LSS). Hence, to address these gaps, this research intends to answer the following questions: (a) To what extent do life insurance agents feel stressed in their policy selling business? (b) What are the experiences contributing to work‐related stressors among life insurance agents?

3. Methods and procedure

3.1. Study design

This research tries to build on previous studies that employed Lazarus and Folkman’s (Citation1984) transactional stress theory to examine job stress, coping, and work performance in service sector comprising hospitality and finance industries (Althaus et al., Citation2013). It also strengthens the studies in which employees experienced a considerable amount of job strain, having negative impact on their coping skills and work performance also (Wang et al., Citation2020).

A qualitative approach was chosen for this study because there would be more possibilities to generate rich and finest descriptions of phenomena that would help to investigate previously unexplored complex issues on work stress prevailing in life insurance agents (Bhui et al., Citation2016). Qualitative approach provides an opportunity to explore and is beneficial when the important variables to examine are difficult to find (Huyler & McGill, Citation2019). According to N. Denzin and Y. Lincoln, a qualitative approach is “concerned in capturing the individual’s point of view and in the need for securing rich descriptions” (DeVault et al., Citation1995). A better understanding of the work stress prevention needs of life insurance agents can promote the development, selection, and implementation of stress prevention programmes, and mindfulness interventions was attempted with the help of qualitative approach.

3.2. Study procedure

A total of 45 structured face-to-face interviews were conducted with life insurance agents between April and June 2022 from six private life insurance companies. Methodological studies in the area of qualitative research foster to offer guidance on saturation and attempt to develop a practical application by operationalising evidence saturation (Guest et al., Citation2006). It is posited that sample size ranging from 20 to 40 interviews are required to achieve data saturation that can cut across various research sites (Hagaman & Wutich, Citation2017).

The interview predominantly focused on the experiences of the respondents in their insurance policy selling business to gauge the stress factors and within the context of their organisation, and on their needs for the prevention of work stress within that organisational context. Respondents were at work at the time of the interviews. These life insurance agents were requested to occupy themselves in a discussion room of the insurance company during the interview, where they could speak freely.

Study participants were primarily recruited through the network of insurance development officers and the branch managers of the respective insurance companies. Recruitment of the study participants was done face to-face, by telephone, and/or by email. Purposive sampling was used to select respondents that aimed at selecting a diverse sample with a criteria of gender, age, educational level, salary, and years of experience. To be eligible for participation, respondents had to be 18 years of age or older and had to perform as full-time life insurance agents paid work on commission basis. To maximize diversity in the present study sample, the researchers made sure to select respondents in six different insurance companies. Few potential respondents were directly contacted, while others were recruited by their branch manager. Some reasons disagreed to participate with reasons like complexity of the subject, fear to express, and lack of interest in the subject. Three agents who were scheduled to participate in the interview dropped out (n = 2) or were excluded (n = 1). The reason for exclusion was that the interviewer knew the possible respondent personally. First, the study was introduced to the respondents through an information folder and also explained in person by the researcher. Before commencement of the interview, respondents were asked to fill out an informed consent form. If the study participants had no further questions, the interview was commenced.

But, however, it was noted that the main limitation of this research with in-depth interview method would lie in the findings that may not be possible to be extended to wider populations with the same degree of certainty that quantitative analyses can as these findings were not tested to discover whether they are statistically significant or due to chance.

3.3. Interview protocol

The interview protocol comprised a short introduction, and 10 questions (see Appendix), and were developed using existing qualitative research literature, (Salmons, Citation2014) as well as organisational stress with life insurance sector context (Bun, Citation2002; Ludick et al., Citation2007) and COREQ guidelines (Dossett et al., Citation2021).

The protocol was reviewed by all authors to serve the purpose of assessment of face validity. Member checking was utilized in order to avoid researcher and respondent bias and unclear responses were dealt with by asking the respondents whether the transcribed data has no difference to the answer. A pilot test of two interviews was conducted which led to a further clarification of items in the interview protocols. The interviews were recorded and simultaneously the researcher made notes during the interview.

On average, interview duration was 45 minutes. Saturation of the data was considered by the coders which focused on between interview occurrence of variation in answers to the questions (Bowen, Citation2008). The interviews were conducted in two rounds to facilitate iteration, a reflexive process, in which collected data can be used to guide further data collection, or data analysis (Srivastava & Hopwood, Citation2009).

Follow-up questions and probes were formulated, to help the study participants in understanding the subject. The probes were used only when required. The protocols were centred around the main themes. (Table ). There existed no prior relationship between the interviewer and the study participants.

Table 1. Socio‐demographic characteristics of participants

3.4. Data analysis

The interview recordings were transcribed verbatim which were cross-checked for better accuracy. The objective of this study called for an approach of inductive interpretation. Thematic analysis was an ideal research methodology (Braun & Clarke, Citation2006) in which the researcher works systematically through the texts to identify the respective topics, later clustered in themes having relevance to the research question (Calcraft, Citation2005). The coders used a bottom-up, inductive coding style where coding scheme was adapted after every round, so that new themes could be added, and code names could be consolidated. Reappearing themes were isolated, which facilitated increasing, but gradual abstraction and summation of the data. The COREQ-checklist was used in reporting this study (Tong et al., Citation2007). We conducted data management, followed by coding and analysis using ATLAS.ti, version 7.5.11.

4. Results

4.1. Participants

The study sample consisted of life insurance agents of six private life insurance companies (n = 45). Their age ranged from 21 to 62 years (female n = 20 and male n = 25). Respondents worked as full-time life insurance agents. Few respondents were freshers and had below 5 years of experience (n = 18), few had an experience of 5 to 10 years in the field of insurance selling business (n = 20), and remaining had an experience of more than 10 years (n = 7). Their education background was diploma (n = 16), undergraduates (n = 19), and post graduates (n = 10). The average mean and standard deviation is presented in Table , depicting the socio‐demographic characteristics of participants.

5. Themes

The themes extracted from the qualitative data were divided into job responsibilities, handling customers and long-term relationships, work pressure, and mental health indicators which were the factors leading to stress. These stress factor led to measures which could help in handling and mitigating stress (Figure ).

Figure 1. Conceptual framework.

5.1. Theme 1

Job responsibilities: Life insurance agents expressed that their main job responsibility lies in providing service to the changing insurance needs of clients and compiling a list of prospects. Respondents indicated that their job responsibility is to enhance the reputation of the insurance agency by venturing new and different requests and exploring opportunities to add value to job accomplishments. Some participants explained that work of a life insurance agent is rewarding, but the job roles in the policy selling business were difficult.

Selling right policy to the right customer: Agents find it difficult to automatically generate the right policies to the customers based on their lifestyle and previous policies, although it is the most fundamental responsibility of every insurance agent. One participant stated that “ … … . then of course searching for the right customer in the crowd is not easy but we have to sell the right product to them, that responsibility turns out a good challenge … ”. Another respondent indicated that “ … .Whatever policies I have sold to the clients I have managed them diligently. When it comes to selling new policies or finding new clients let me see, if I can do it I will definitely do it, but sell the right policies to the right people however restless it makes me … ”.

Reaching sale targets: A life insurance agent will always try to boost insurance business with existing accounts (cross-selling) by increasing retention and renewals. Winning against difficult competitors by optimizing the sales process will improve sales opportunity planning laying a foundation to reach sales target. The agents highlighted that they are paid salary on commission basis where the fear of fulfilling the sales target will always be escalating. One agent who was a fresher responded that “ … .as a fresher, my responsibilities are to make more and more policies actually, and reach my sales target. I have to search for clients, and as told by my senior colleagues it is better to set target first rather keeping it at the time of deadline … ”. Hence, the job responsibilities of life insurance agents are quite challenging. There are instances when one will appreciate being in this field as it is a rewarding profession, but few instances may obstruct their growth and turn challenging when they approach their clients or when they are not able to meet the targets. According to one more agent “ … . clients and they would just turn me down so my job would be to turn criticism into opportunity to utilize.That would be great because today the clients would most certainly want me to be practical and want things to be in a comprehensive manner … ”. Considering the clients as their job responsibility has no other alternative. Another participant commented “ … … . Like if we just leave them then they may escape or rather just start ignoring us. If we give some sort of closeness and care we can avail their connects and build more connects with different clients which may help in reaching sales targets … …”.

Accountability towards the business in bringing new leads: Accountability in customer service from a life insurance agent perspective is the ability to account for policy selling business actions and decisions. It entwines the willingness to showcase the care and trust to be developed in the customers by carrying an unspoken pledge to respond to a customer’s request for information or help. One participant reported “ … … We have to search the customers and make them known about the need of the policy, build trust and also we have to check whether they are really interested in the policy by responding to their queries”. Another participant reported that “ … If we simply approach them then success rate will be definitely less and we are accountable to the business for this … ”. A good convincing skill will, however, try to enhance the productivity of the agents. One of the strategies to enhance productivity is by always appearing excited and eager. A dreary or worn-down disposition will rub off on clients and discourage them from buying the policies. One of the respondents remarked that “ … … … A good convincing skill is important and when people understand the benefit of insurance and try to approach and respond to our convincing notes it really helps in our productivity enhancement by finding new leads though its been very difficult to fulfil this task … …”.

Keeping up with technology (AI): Agents highlighted their role transitions to process facilitators and product educators. The agent of the future can sell nearly all types of coverages which adds value to their productivity by helping clients manage their portfolios of coverage across experiences and their lives. Agents use smart personal assistants to optimize their tasks as well as AI-enabled bots to find potential deals for clients. These tools help agents to support a substantially larger client base while making customer interactions (a mix of in-person, virtual, and digital) shorter and more meaningful, given that each interaction will be tailored to the exact current and future needs of each individual client. The task of upgrading oneself through a granular and sophisticated way based on technology will create a new wave of challenge for the agents in the life insurance sector. One agent reported that “ … … . I am not a young agent. I am aging … but when my young colleagues talk about all this technology, they are asked to learn about really makes me anxious. I agree its our responsibility to be technologically upgraded but I also know it is not possible so easily that too for an employee who is above 50 like me … ”. One more agent stated that “ … . yes, keeping up with the technology is really a good habit but implementing this with people like us working as life insurance agents is not easy as said. We focus on convincing the customers and getting our policies done, so again technology is like an extra burden to learn about though we all know its our responsibility to be technologically strong …”. Another agent entailed that “ … .we are used to handling clients personally, even though phone we find it convenient. But we are always being reminded to keep ourselves upgraded in technology and AI. Thinking about this creates a feeling of fear and we get stressed out … ”.

Goal achievements: Life insurance again agreed that the sales efforts of the insurance agents’ (rewards based on the sales volume generated) is successfully contributing towards performance of their job responsibilities. The reason being that insurance agents believe that the compensation (commission, bonuses, benefits, and awards) earned is a true reflection of what they deserve. One agent underscored that “ … . we all know that commission is like an incentive for us but being a life insurance agent earning commission is for our daily bread. Doing something beyond this like achieving more and more policies and taking a recognition for that through awards and felicitations is a different feeling and challenging too … ”. Another agent said that “ … . having goals to reach the targets and making more policies and thereby uplifting the goodwill of the company is my job responsibility. This will not only give recognition to the company but also to me as an agent. Getting recognition, bonus and winning awards needs a lot of hard work and dedication which is just like a challenge in this profession …”.

5.2. Theme 2

Handling customers and maintaining long-term relationships: Client engagement results in a happy customer who will return to the agent again and again. Not only will the client be loyal to the agent and the company, he may also refer the products and services to many of his colleagues, friends, and family members which in turn improves the reputation of insurance business, as satisfied clients tend to respond with positive reviews and rate it online.

Knowledge about the complexity and diversity of products: Complexity and diversity of life insurance products is rising on multiple fronts. Left unchecked, this complexity could land up the career of agents hobbled at a time when organisational agility is more significant, as consumers continue to question the value of life insurance products. Some agents proclaimed that there is a widening array of products where aligning and integrating distribution is a complex job. One agent stated that “ … . Insurance companies must take pains to distinguish between good complexity, which creates operational efficiencies and variety valued by customers, and bad complexity, which creates variety that customers don’t care about and reduces organizational agility and efficiency in exchange for no benefit. We find these situations difficult to handle … ”. One more agents reported that “ … .Controlling complexity will make life insurance agents more efficient today and position them to grow tomorrow. We will be able to understand whether new offerings are worth the complexity and finally we can focus relentlessly on offering the ‘right’ level of complexity and diversity of products to meet customer requirements … ”.

Information asymmetry: Asymmetric information in insurance refers to a market situation in which one party in a transaction has insufficient information about the other party which leads to market failure. Some agents reported that when they meet new clients, they find themselves unable to answer few questions and the clients know better than them. The problem of asymmetric information is common in life insurance markets. One agent said that “ … . it’s really difficult to gauge a customer as at-risk customers and low risk customers. They know better about themselves, so it becomes a tangle for us to explain the policy they actually need from us … ”. One more agent reported that “ … . I have come across few clients who know better than me, they have a correct picture in which category of clients they fall in … .that shows they are less interested in listening to us when we explain them the need to buy our policies”.

Handling annoying customers: In the scenario of selling insurance policies, an agent comes across diverse types of clients. Some customers may be friendly, some may be amiable, and few may be annoying. Managing annoying customers is the greatest challenge an agent faces. Listening to customers instead of trying to explain over and again when they are on rant would be a wise decision. Finding a chance to steer the acceptance may take more time and energy. One client claimed that “ … . sometimes we get so much tensed when a customer is not at all ready to listen because he thinks we are dumping policies just to finish our targets. Nothing works actually, they are so arrogant that somewhere we feel convincing customers is a dreadful task in this profession” (client 10). One more agent stated that “ … .Even if we have done everything correct here people may still be upset. In our business there are a lot of negative situations that can arise and there is a negative connotation to the industry. When clients get irritated and annoyed I get distracted by their anger and lose focus”. One respondent addressed that “ … . Targeting on the customer that I am communicating with and understanding my target client as in which category of people what is their age? Of course, I have received criticisms from the clients, and they would just turn me down so my job. These target pressures actually force us to pitch a sale and clients get annoyed as they think we are forcing them to buy … ”.

Managing changes in customer expectations: A few agents addressed that they need to come to meetings and conferences armed with specific sales opportunities, including data to showcase where and how opportunities exist and come up with new actionable ideas for meeting the customer expectations that creates work stress. One agent mentioned “ … What work life Synergy has been difficult customers, also to understand their needs, their needs are in variety and the need of youth and senior citizens is changing. There has been a frequent updating upgradation so probably understanding the needs of the customers is also become very tricky and customers would not like to disclose certain items. … ”.

Keeping close contacts with customers and being persistent: Asking questions and giving suggestions and creating a bonding by asking what you can do for him/her is the best way to build connects and maintain long-term relationships. Although this is a “self-help” strategy, these suggestions may provoke the clients to come back to the agents, which is a good sign of strengthening the relationship. Respondents reported that taking in a personal tone, voluntarily meeting them, and having conversations would, however, help in maintaining strong relationships. One respondent reported that “ … . Like, regular meetings would help, personal meetings I feel. Also, when we accidently meet them in any function, or any crowd, greeting them talking to them and asking them about their life. This helps to create a bonding”. Life insurance agents also mentioned that when such meetings and greetings are delivered to the clients, a sense of belongingness and feeling of trust is originated. One more agent indicated that “ … . When I ask them about them apart from insurance and policies. they feel secured that yes someone is asking about them. Someone is worried for them … ”. Agents agreed that keeping records of their clients and however wishing them and acknowledging them with personal greetings on phone through social media platforms do help in maintaining long-term relationships. One respondent stated that “ … . It is important to document things and keep them handy I keep a track of my customer’s birthday or anniversary and send him/her a card or a note. It pays to remember his/her kids’ names too. It is important to do a little extra if you want to thrive in the business of insurance and also good morning and good night messages work a lot … ”. The kind of competition that exists in the insurance sector has made it tough to survive for insurance agents. The only remedy for their survival is the long-term relationship with their clients. Another agent responded that “ … … . we need to set realistic expectations, When you under-promise there is a possibility to over-deliver and this can improve your image in the eyes of your customer and the customer starts feeling that he is important to you and takes a step forward to build a relationship with you … ”.

5.3. Theme 3

Work Pressure: When an agent tries to locate a good prospect, difficulties become intense as the product itself is hard to sell. Clients loath to discuss or even acknowledge their own mortality. Agents said that life insurance provides none of the instant gratifications that lead people to make impulse purchases. Constant reminders of the deadlines and targets also add to the work pressure say few agents in the insurance sector.

Supervisory pressure on targets and deadlines: Agents always get reminders about the number of policies they must cover in the stipulated time. Supervisors and trainers in the insurance agency ask the agents for the progress they have done and keep a track of this. One agent reported that, “ … I still remember my previous supervisor just called me one day and told me that I have very less time left to complete my sales target as the deadline was approaching. He was a bit rude, and I felt a bit humiliated on his conversation … ”. One more agent addressed that “ … . One fine day I was just told straight in front of another agent that I need to put in a lot of efforts to match other agents and they are making policies enormously, but I am lagging. This pressure he put on me led me down and made me feel insulted. I was totally stressed”. Agents underscored that getting more referrals is a challenging task. Finding new leads organically is difficult though. One agent pointed out that “ … .We have to find new leads, at the same time we cannot neglect the existing customers, this thought actually turns to be a challenge”. Another client shared his opinion that “.we have monthly commitment and we have to do so many policies within a time limit. that pressurises and also these deadlines ruin mental peace. We sometimes feel anxious if we cannot reach the targets and in finding new leads … ”.

Balancing between administrative work and policy selling business: A few agents reported that they often have to handle all the administrative and operational work ranging from handling client paperwork to managing agency bookkeeping and it is not only to drum up sales. One agent indicated that “ … We have a lot of admin work. But we cannot just keep on doing that, we have to balance this operational work and the policy selling business which is somewhere a stressful challenge … ”. Another agent mentioned that “We get a bit agitated when these deadlines are nearing us and we get emotionally affected, we find ourselves difficult to cope. Managing admin work, clients and home also is a great challenge”.

Maintaining work-life balance: Agents stated that they always miscalculate the time they invest in life or in work and behind either or both. One agent addressed that “ … At work, I need to make sure I am around people who understand and respect my life outside the office, so that I can depend on them if I need to take time off to be with my family or deal with an emergency. But we cannot expect the same thing always … ”. One more agent stated that “ … Sometimes I get stressed when I feel these challenging questions have no answers like what’s my idea of success and happiness in this profession? Am I serious about taking care of a family? Or am I so passionate about my work that I don’t mind working long hours practically every day?”

Following rules and regulations: Agents have witnessed an increasing number of rules and regulations in recent times intended for the welfare of the general public and the insurance sector, and keeping up with the changes can seem to be a daunting and pressurising task. Agents mentioned that understanding the new regulations and its impact on the customers’ policies is difficult and implementing these rules is like a pressure to them. One agent claimed that “ … we are therefore advised to stay on top of updates affecting our respective areas of insurance … ”. One more agent stated that “ … .Now, learning the laws is not only the challenge faced by agents like us we need to help clients understand how some of the regulations might affect them. So must ensure that we are well-versed with the laws before attempting to answer the questions that prospects”.

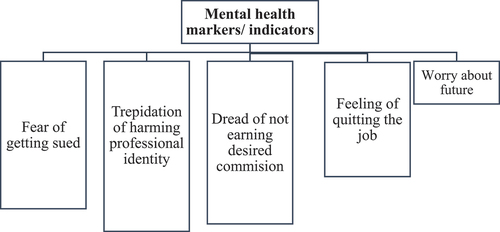

5.4. Theme 4

Mental health markers/indicators: Life insurance agents are exposed to mental health markers such as fear of getting sued and harming professional identity, inability of earning desired commission, future worries, etc. These job-related stressors can result in the arousal of certain emotions which are unpleasant such as tension, anxiety, anger, frustration, burnout, and depression. Life insurance agents have an emotional engagement which is unavoidable in the line of work on selling policies to the customers. Stress related to work is the ultimate response which hinders and threatens the ability to cope. This is characterized by the lingering effect where the work affects the personal lives of life insurance agents.

Fear of getting sued: A client may sue an agent after an investment goes sour, even if the risks were well known and within the guidelines established by the client. All insurance agents, regardless of their business practices, have liability exposure, whether they do anything wrong or not. Insurance agents face the threat of E&O (errors and omissions insurance) litigation where most of the agents do not take it seriously because they believe their “by-the-book” business practices will nip litigation in the bud. This is a misconception. And when they get sued, frustration and anger can flood them with stress. Psychologists have coined a term for this phenomenon: “Litigation Stress Syndrome (LSS)”. One agent claimed that” … I always have that fear in my profession of getting sued though I am very careful while addressing the customers. One instance where I failed to notify my client that his policy is about to be cancelled that is prematurely cancelled by the insurer, I was held liable for this and that fear is still emotionally affecting me … ”. One more agent addressed that “ … I have that fear as some of my colleagues have gone through situations where they were sued for misrepresenting their policies. I always get few dreadful thoughts in mind like whether I will able to continue adding new clients to your business and whether my long-term financial security will take a hit if I try running behind clients and sometimes they think we are putting pressure on them”.

Trepidation of harming professional identity: Agents stated that not only the fear of getting sued but also the trepidation of harming professional identity when you cannot fulfil your targets or when you are known as a poor performer with least number of policies in hand harms one emotional and mental state. One agent mentioned that “. I remember in my second year of career I had a lot of difficulty in making policies. I just started pressuring people whoever I met. One client just complained to the insurance development officer with allegations on me saying I pester her to buy policies. Of course, this harmed my professional identity and I was in stress for nearly months and still difficult to come out of it”. Also, one agent addressed that “ … Its difficult to let go a client. When he promises to buy and changes his decision its like we have lost a big deal. we as agents walk through the insurance application and complete the application accurately and truthfully. Still they threaten us of putting allegations that we have misrepresented the application”.

Dread of not earning desired commission: Insurance industries give greater recognition to individual pay and performance not only to encourage increased productivity and efficiency but also to retain highly valued to achieve the firm’s objectives. When remuneration is linked to effort, both individual and organisational performance is enhanced. Firms are beginning to give greater recognition to individual pay and performance not only to encourage increased productivity and efficiency but also to retain highly valued workforce to achieve the firm’s objectives. Tying remuneration to performance improves employee motivation, as workers become more results oriented. Employees will make more effort to achieve results when they are aware that their remuneration package is determined by their contribution to the firm’s performance. However, the concept of variable compensation can be an issue on the other side. How much an agent makes depends on how much effort he puts in and how many sales he can close. Being an agent is like always getting up with a fear of earning the desired commission. One agent mentioned that “ … . when your financial obligations are fixed, but your compensation is variable, it’s natural to worry about bringing in enough money to pay my bills … ”. Another agent stated that “ … . Not jealousy but sometimes you get that emotional feeling and stress when your friend earns more commission, and you are still struggling to get 10%of it. That self-doubt of why I cannot get my policies sold …we get emotionally affected I feel … ”.

Feeling of quitting the job: As an insurance agent, they have daily opportunities to change their lives for the better. These agents are sometimes afraid to use the incentives as incentives sometimes pressurize them to make more policies which cannot be easily done. Lack of training for finding customers is also a biggest challenge. Target pressures and deadlines, commission-based salary, and boss culture give them a feeling of quitting their job. An agent stated that “ … during my deadline period I sometimes feel I should just quit my job, so much pressure I get from the supervisors that I have not completed my target. I feel exhausted and emotions run out of myself leaving me helpless … ”. Another agent claimed that “ … there are instances when I just entered this profession and had high goals however they were unachievable, I set myself up for failure … which drove me to decide to quit … ”.

Worry about the future: Role of an agent focuses on repetitive work and manual processes will cease to exist in their present form, while technology and digitally savvy workers will increase in value. Agents say that emotional, interpersonal, and social skills will become more critical, especially for customer-facing agents who can help consumers address their changing financial and coverage needs. However, these workforce shifts will not eliminate jobs. Our research indicates net new jobs will be created due to advances in automation but instead change the nature of the work. One agent affirmed that “ … . The COVID-19 pandemic has only accelerated trends of digital native, automation and omnichannel. That fear of replacing us with technology bothers me everyday as I am the only bread winner in my house … ”. One more agent addressed that “ … . People ask me how do you survive on a commission basis job, how do you manage your targets, how do u balance worklife? Actually these questions have only two options either fulfil them or quit the job. But after quitting what next makes me feel very tensed and anxious … ”.

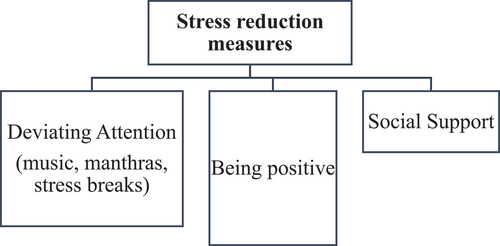

5.5. Theme 5

Stress reduction measures: Mitigating stress is equally vital when an agent tries diving deeper into client relationships and leveraging data. Agents reported that by being positive and acknowledging the challenges, they can start on the path toward solving them. This theme contains the requisite that the agents expressed for circumstances that would be supportive to work stress measures. These circumstances could be interpreted as prerequisites for active work stress prevention like mindfulness intervention and different situations that participants indicated they needed to prevent them from experiencing stress at work.

Diverting attention: Agents mentioned that diverting attention by a short conversation with peer team, glancing on a pop-up message on social media, or talking to someone on phone would mitigate stress. This was supported by two agents “ … . taking stress breaks to divert attention. I have also learned to get help from not just my colleagues. I have learned to share my thoughts and feelings with my family. I’ve also learned to take professional help because the job has been stressful, especially during my mid 50s where I used to go through a health issue … ”. One more agent reported that “ … Actually to relieve myself from stress I listen to some soft music or enchant mantras which really helps and give me a soothing feeling to my body and mind… … ”. Secondly, agents indicated that to prevent work stress, they should be “ready for change”. This individual readiness for change was described as the awareness and acknowledgement of work stress being a problem and their willingness to participate in intervention process.

Being positive: Agents embarked that having a positive outlook even when hardships arise is the best measure to handle stress. One respondent reported that “ … … We need to explore practical strategies for increasing positivity and dealing with difficult situations techniques for stopping negative thought patterns and cultivating positive environments, relationships, and habits at work … ”.Another respondent said that “ … I believe in today. Past and future are important but we cannot keep worrying about the future, that may spoil our present. So staying positive in the present would help us to reduce stress and uncertainties”.

Social support: A family member or a friend or peer who could aid recommendations to these stressed individuals will magnify and boost their psychological well-being through happiness, safety, comfort, and positive mindset. Social support can buffer stress including preventing the individual from negatively reacting to a stressor by redefining it as not stressful, increasing an individual’s ability to proactively and reactively cope with the stressor, and by providing supportive solutions for stress.One respondent mentioned that “ … when I am too much stressed I just see my mobile for some time, sometimes I talk to my kid on phone …and then I just ask my family member whether I will succeed in my career or no?. This support give me a relaxed mind for working”.One more agent addresses that “Yes there are times when I feel nothing works, so when I am in stress I divert my attention by just checking my phone or just giving a call to my friend. Her support in giving me some positivity in the challenges I face at work makes me feel lighter … ”.

6. Discussions

The qualitative interviews explored and provided a richer understanding of work‐related stressors among life insurance agents of six private life insurance companies. As stated in transactional stress theory developed by Lazarus and Folkman (Citation1984), “what carries as either subjective or objective stress resides in the relationship between the environment and the individual that leads to a threat appraisal”. The interaction between life insurance agents and job responsibilities along with the challenges in the work environment plays a major role in the respondent’s experiences of stress.

Target pressures, difficulty in pitching sales, maintaining long term relationships, lack of knowledge and technical know-how, difficulties in approaching the customers and convincing the clients to buy policies which affects them emotionally and hinders their mental peace were identified as sources of work stress that support the theory (stressors resulted from interactions between individuals and their environment, workplace).According to this theory “A stressor was viewed as any event, situation, or person that an individual may encounter in the environment that requires change or adaptation”. The study provided a framework of stressors and a structure to facilitate analysis of the study findings.

The respondents, irrespective of gender, experienced high levels of work stress. This finding is consistent with the previous study of Sharma and Kaur (Citation2013) where lack of advancement opportunities, lack of positivity and disturbed mind were found to associate with stressors of life insurance agents.

It was identified that accountability towards the business in bringing in new customers and fulfilling the sales target was the highest source of work stress in the insurance sector and has been linked to disruption of mental health thus leading to attrition. This finding was consistent with the study by Amuthan and Ramachandran (Citation2010), the results of which showcased that certain job roles or job responsibilities are one of the major work‐related stressors for life insurance agents. Jain and Hyde (Citation2021) also found that insurance industry targets are unrealistic and sometimes unachievable where consequently they must spend a lot of time and energy leading to stress at work thereby further compounding the problem.

In another study by Coetzer and Rothmann (Citation2006), it was opined that job characteristics and roles best predicted psychological or mental health due to stress at workplace.

Researchers claim that life insurance agents find it difficult to discover the right customer for the right policy which they are selling. They become vulnerable to negative outcomes including higher levels of depression, anxiety, and burnout (Torkelson & Muhonen, Citation2004).

The second important sources creating stress which were mentioned by the participants of the present study have been referred to having a good strand over technical know-how (Yan & Xie, Citation2009). The study conducted by Cappiello (Citation2018) substantiate that implementing the digital technologies with the insurance use cases requires an integrated strategic perspective and agents find it difficult to build themselves with technological knowhow contributing to work stressors. Apart from this, letting the customer decide for themselves, without pushing or convincing towards any of the choices, the agents indirectly send a signal to the client to accept the offer (Aoba, Citation2022). This study affirms that a sales call more often does not always end up as a success and impacts on their mental health due to stress. If a customer feels that they can make a choice and notice that their opinion is important only then they will be convinced and will take a step ahead to buy the policies. Avoiding the agent’s conversation and a straight away no from the clients will discourage the agents thus leading to job stressors. Customer long-term relationship is the main pillar in life insurance business. Harmonious relationship with customers can help the agents reach any level of success but maintaining it is undoubtedly difficult (Aburumman et al., Citation2020).

A finding from the present study shows that maintaining long term relationship was a difficult task and a major work‐related stressor. A qualitative study underscored those interpersonal skills of keeping close contacts with customers will enhance long term relationship (Nguyen et al., Citation2019). None of the previous studies paid attention directly to work stress associated with maintaining long term relations through close contacts and being persistent thus contrasting the findings. From this study’s findings it would appear that interacting with clients is equally as difficult and demanding as Life insurance agents of private sector. Also, lack of persistency may break the trust of the clients and the agent may lose his customer which is supported by Lee (Citation2018).

Life insurance agents admitted that they find a lot of bottlenecks when they meet annoying customers. The study showcases the difficulty of these agents to select the customer to be targeted (Shetty & Basri, Citation2018). There was a similar finding conducted among selling agents who proclaimed that pitching a sale with clients who are difficult to get convinced may lead to stressful work environments as the agents may not be able to make policies as anticipated by them (Matthews & Edmondson, Citation2022).

Roy and Roy (Citation2020) indicated that common challenges faced by life insurance are related failure to achieve the targets, rampant mis-selling to customers, pressure from subordinates, minimum business guarantee, bombardment from managers and lucrative benefits offered by competitive companies, among others. This study tried to explore the experiences of these agents in balancing administrative work with policy selling business which is the toughest challenge. Also, finding new leads and managing changes in customer expectations add on to the challenges (Nagaraju & Vijaya, Citation2022). A novel concept being gauged in this study is agents need to have a mind map to face these challenges of being flexible to the customer expectations. Customer expectations keep on changing with the changing environment and keeping pace with such circumstances leads to job stress (Chang & Chang, Citation2007). Agents in the insurance sector fall in different age categories and work experience slabs. Depending on this every agent cannot cope with the technology and automation invented in this field. Information asymmetry also adds to one of the challenges faced by the agents in this sector (Chen & Peng, Citation2022). The greatest challenge is to cope with this technological advancement which was supported by Revathi (Citation2020). Mental health markers like fear of getting sued and getting professional identity harmed indicated stress at work in service sector employees (Metzner & Gendel, Citation2022). However, insurance companies should take these work‐related stressors into consideration to reduce levels of work stress and mitigate the worries related to future.

For the purpose of mitigating stress, agents indicated that having a positive mindset would help them to reduce their stress levels. Diverting their attention in a short conversation or scrolling through social media would enhance them to curtail from stress for a short while. One study reported that being mindful in having improved the quality of attention with mindfulness would help oneself to relieve from stress (Malinowski & Lim, Citation2015). Another study reports that launching certain initiatives and programmes that are directed towards training managers to be servant leaders in their teams can help in enhancing the well-being, thus creating a positive climate that will help in building new networks. Hence organisations should see through it that employees have a personality trait (mindfulness) through which they are more likely to reach higher levels of empathy and positive emotions and psychological flexibility (Ruiz-Palomino et al., Citation2023).

7. Future implications

Numerous opportunities can be attained for stress in life insurance agents research stemming from this initial qualitative study. However, a refined replication of this study with a large sample of life insurance agents in different regions in remote provinces in public and private insurance sectors is needed to compare and contrast findings. A study likewise may assist in identifying the overall levels of work stress and its related sources in each sector that may differ from this study’s findings and address knowledge gaps. Furthermore, the effects of work stress and its sources on agents’ mental health in Indian context have not been, and needs to be, studied. Moreover, the study findings may serve as a resource for developing policies, guidelines, and practices to improve work environments by adopting stress reduction programmes or interventions to develop a positive mindset at work.

With stress-relieving programmes and mindfulness training, future research could evaluate how servant leadership can also help to reduce stress by increasing the network of relationships within the organisation and outside the organisation (Zoghbi-Manrique de Lara & Ruiz-Palomino, Citation2019).

8. Conclusion

In conclusion, life insurance agents revealed their job roles, their difficulties in making policies, coping with technology, hurdles in pitching a sale and maintaining long-term relationship as factors leading to work stress. They initiated conversation for stress prevention measures may be because they are experiencing the challenges first-hand. This will give the agents a better insight into which measures will combat work stress. The sub-themes reported by employees indicated that though they are under stress, they try to manage it themselves and organisations do not take any lead to suggest stress reduction programmes or trainings.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

Data availability statement will be made available on request (transcribed data).

References

- Aburumman, O., Salleh, A., Omar, K., & Abadi, M. (2020). The impact of human resource management practices and career satisfaction on employee’s turnover intention. Management Science Letters, 10(3), 641–21. https://doi.org/10.5267/j.msl.2019.9.015

- Agyapong, K., Muhammed, M. A., & Acheampong, A. (2016). Personal selling stress and coping strategies among sales executives: A case of selected insurance companies in Ghana. International Journal of Scientific Research and Management. https://doi.org/10.18535/ijsrm/v4i2.07

- Althaus, V., Kop, J.-L., & Grosjean, V. (2013). Critical review of theoretical models linking work environment, stress and health: Towards a meta-model. Le Travail Humain, 76(2), 81. https://doi.org/10.3917/th.762.0081

- Amuthan, R., & Ramachandran, A. (2010). Financial potential of Life Insurance Companies in India : A comparative study among Private and Public Sector Insurance Companies. I-Manager’s Journal on Management, 4(4), 63–69. https://doi.org/10.26634/jmgt.4.4.1163

- Aoba, N. (2022). The Sales Channel of Life Insurance and Relationship Marketing. New Frontiers in Regional Science: Asian Perspectives, 391–414. https://doi.org/10.1007/978-981-16-6695-7_21

- Bhui, K., Dinos, S., Galant-Miecznikowska, M., de Jongh, B., & Stansfeld, S. (2016). Perceptions of work stress causes and effective interventions in employees working in public, private and non-governmental organisations: A qualitative study. BJPsych Bulletin, 40(6), 318–325. https://doi.org/10.1192/pb.bp.115.050823

- Bowen, G. A. (2008). Naturalistic inquiry and the saturation concept: A research note. Qualitative Research, 8(1), 137–152. https://doi.org/10.1177/1468794107085301

- Braun, V., & Clarke, V. (2006). Using thematic analysis in Psychology. Qualitative Research in Psychology, 3(2), 77–101. https://doi.org/10.1191/1478088706qp063oa

- Bun, C. K. (2002). Coping with work stress, work satisfaction, and social support: An interpretive study of Life Insurance Agents. Asian Journal of Social Science, 30(3), 657–685. https://doi.org/10.1163/156853102320945439

- Calcraft, R. (2005). Book Review: Qualitative Research Practice: A Guide for Social Science Students and Researchers. Qualitative Research, 5(4), 549–551. https://doi.org/10.1177/146879410500500410

- Cappiello, A. (2018). Technology and insurance. Technology and the Insurance Industry, 7–28. https://doi.org/10.1007/978-3-319-74712-5_2

- Chang, T.-Y., & Chang, Y.-L. (2007). Relationship between role stress and job performance in sales people employed by travel agents in Taiwan. International Journal of Stress Management, 14(2), 211–223. https://doi.org/10.1037/1072-5245.14.2.211

- Chaturvedi, A., & Joshi, M. (2017). Work stress and employee performance in Public and Private Sector Life Insurance Companies. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3011147

- Chen, Y.-T., & Peng, S.-C. (2022). Information asymmetry in medical insurance: an empirical study of one life insurance company in Taiwan. Applied Economics, 54(46), 5351–5356. https://doi.org/10.1080/00036846.2022.2044994

- Clemente, G. P., & Cornaro, A. (2022). A multilayer approach for systemic risk in the insurance sector. Chaos, Solitons & Fractals, 162, 112398. https://doi.org/10.1016/j.chaos.2022.112398

- Coetzer, W. J., & Rothmann, S. (2006). Occupational stress of employees in an insurance company. South African Journal of Business Management, 37(3), 29–39. https://doi.org/10.4102/sajbm.v37i3.605

- DeVault, M. L., Denzin, N., & Lincoln, Y. (1995). Handbook of Qualitative research. Contemporary Sociology, 24(3), 418. https://doi.org/10.2307/2076551

- Dinesh, T. K., Shetty, A., Dhyani, V. S., TS, S., & Dsouza, K. J. (2022). Effectiveness of mindfulness-based interventions on well-being and work-related stress in the financial sector: A systematic review and meta-analysis protocol. Systematic Reviews, 11(1). https://doi.org/10.1186/s13643-022-01956-x

- Dossett, L. A., Kaji, A. H., & Cochran, A. (2021). SRQR and COREQ reporting guidelines for qualitative studies. JAMA Surgery, 156(9). https://doi.org/10.1001/jamasurg.2021.0525

- Fu, W., He, F., & Zhang, N. (2020). Antecedents of organizational commitment of insurance agents: Job satisfaction, ethical behavior, and ethical climate. Journal of Global Business Insights, 5(2), 134–149. https://doi.org/10.5038/2640-6489.5.2.1135

- Ganster, D. C., & Rosen, C. C. (2013). Work stress and Employee Health. Journal of Management, 39(5), 1085–1122. https://doi.org/10.1177/0149206313475815

- Goel, M., & Verma, J. P. (2020). Workplace stress and coping mechanism in a cohort of Indian service industry. Asia Pacific Management Review, 26(3), 113–119. https://doi.org/10.1016/j.apmrv.2020.10.001

- Goh, Y. W., Sawang, S., & Oei, T. P. S. (2010). The Revised Transactional Model (RTM) of occupational stress and coping: An improved process approach. The Australian and New Zealand Journal of Organisational Psychology, 3, 13–20. https://doi.org/10.1375/ajop.3.1.13

- Guest, G., Bunce, A., & Johnson, L. (2006). How many interviews are enough? An Experiment with data saturation and variability. Field Methods, 18(1), 59–82. https://doi.org/10.1177/1525822x05279903

- Hagaman, A. K., & Wutich, A. (2017). How many interviews are enough to identify metathemes in multisited and cross-cultural research? Another perspective on guest, Bunce, and Johnson’s (2006) landmark study. Field Methods, 29(1), 23–41. https://doi.org/10.1177/1525822X16640447

- Huyler, D., & McGill, C. M. (2019). Research design: Qualitative, quantitative, and mixed methods approaches. In John Creswell & J. David Creswell, Eds., New Horizons in Adult Education and Human Resource Development (p. 275). Sage Publication, Inc. $67.00 (Paperback)31(3), 75–77. https://doi.org/10.1002/nha3.20258

- Hyun Yoon, H. (2016). Do Customers want Employees’ Authentic Service or Just Service? The Effects of Employees’ Authenticity and Justice on Customers’ Commitment and Behavior. Culinary Science & Hospitality Research, 22(6), 120–131. https://doi.org/10.20878/cshr.2016.22.6.013

- Jain, R., & Hyde, A. (2021). Effectiveness of stress management interventions in Indian insurance sector. International Journal of Happiness and Development, 6(4), 390. https://doi.org/10.1504/ijhd.2021.117794

- Jamieson, S. D., Tuckey, M. R., Li, Y., & Hutchinson, A. D. (2022). Is primary appraisal a mechanism of daily mindfulness at work? Journal of Occupational Health Psychology, 27(4), 377–391. https://doi.org/10.1037/ocp0000324

- Lamontagne, A. D., Keegel, T., Louie, A. M., Ostry, A., & Landsbergis, P. A. (2007). A systematic review of the job-stress intervention evaluation literature, 1990–2005. International Journal of Occupational and Environmental Health, 13(3), 268–280. https://doi.org/10.1179/oeh.2007.13.3.268

- Laugeri, M. (2020). Emerging change: A New transactional analysis frame for effective dialogue at work. Transactional Analysis Journal, 50(2), 143–159. https://doi.org/10.1080/03621537.2020.1726660

- Lazarus, R. S., & Folkman, S. (1984). Stress, appraisal, and coping. Springer.

- Lee, C.-Y. (2018). Does corporate social responsibility influence customer Loyalty in the Taiwan insurance sector? The role of Corporate image and customer satisfaction. Journal of Promotion Management, 25(1), 43–64. https://doi.org/10.1080/10496491.2018.1427651

- Ludick, M., Alexander, D., & Carmichael, T. (2007). Vicarious traumatisation: Secondary traumatic stress levels in claims workers in the short-term Insurance Industry in South Africa. Problems and Perspectives in Management, 5. http://www.irbis-nbuv.gov.ua/cgi-bin/irbis_nbuv/cgiirbis_64.exe?C21COM=2&I21DBN=UJRN&P21DBN=UJRN&IMAGE_FILE_DOWNLOAD=1&Image_file_name=PDF/prperman_2007_5_3_11.pdf

- Malik, F., & Shahabuddin, S. (2015). Occupational health stress in the service sector. The Qualitative Report. https://doi.org/10.46743/2160-3715/2015.2272

- Malinowski, P., & Lim, H. J. (2015). Mindfulness at work: Positive affect, hope, and optimism mediate the relationship between dispositional mindfulness, work engagement, and well-being. Mindfulness, 6(6), 1250–1262. https://doi.org/10.1007/s12671-015-0388-5

- Matthews, L. M., & Edmondson, D. R. (2022). Influencing students into sales careers through a speed selling event. Journal of Global Scholars of Marketing Science, 33(2), 231–247. https://doi.org/10.1080/21639159.2022.2052340

- Metzner, J. L., & Gendel, M. H. (2022). The stress of being sued. Malpractice and Liability in Psychiatry, 79–84. https://doi.org/10.1007/978-3-030-91975-7_11

- Muchlish, M. (2020). Antecedents of perceived organizational support to improve organizational commitment in the public sector institutions. Journal of Accounting Research, Organization and Economics, 3(2), 163–171. https://doi.org/10.24815/jaroe.v3i2.17244

- Nagaraju, J., & Vijaya, J. (2022). Boost customer churn prediction in the insurance industry using meta-heuristic models. International Journal of Information Technology, 14(5), 2619–2631. https://doi.org/10.1007/s41870-022-01017-5

- Nguyen, X. N., Thaichon, P., & Nguyen Thanh, P. V. (2019). Customer-Perceived value in long-term buyer–supplier relationships: The general B2B insurance sector. Services Marketing Quarterly, 40(1), 48–65. https://doi.org/10.1080/15332969.2019.1587866

- Revathi, P. (2020). Technology and innovation in insurance – present and future technology in Indian Insurance Industry. Papers.ssrn.com. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3559980

- Robinson, L., Marshall, G. W., & Stamps, M. B. (2005). An empirical investigation of technology acceptance in a field sales force setting. Industrial Marketing Management, 34(4), 407–415. https://doi.org/10.1016/j.indmarman.2004.09.019

- Roy, N. C., & Roy, N. G. (2020). Life insurance industry agent’s attrition: A game changer for insurance business. Global Business Review, 23(2), 426–439. https://doi.org/10.1177/0972150919861452

- Ruiz-Palomino, P., Zoghbi-Manrique de Lara, P., & Silva, G. M. (2023). How Temporary/Permanent employment status and mindfulness redraw employee organizational citizenship responses to person-organization fit. Journal of Work and Organizational Psychology, 39(1), 23–36. ( online). https://doi.org/10.5093/jwop2023a3

- Sahni, J. (2020). Impact of COVID-19 on employee behavior: Stress and coping mechanism during WFH (Work From Home) among service industry employees. International Journal of Operations Management, 1(1), 35–48. https://doi.org/10.18775//ijom.2757-0509.2020.11.4004

- Salmons, J. (2014). Qualitative online interviews: StrategIes, design, and skills. In Google Books. SAGE Publications. https://books.google.com/books?hl=en&lr=&id=ghxzAwAAQBAJ&oi=fnd&pg=PP1&dq=qualitative+study+design+interviews&ots=g3lT-xKInE&sig=rB_y3z85TEZnRyZYPIrdz1lX1Cs

- Schwepker, C. H., & Dimitriou, C. K. (2022). Reducing service sabotage: The influence of supervisor social undermining, job stress, turnover intention and ethical conflict. Journal of Marketing Theory & Practice, 31(4), 450–469. https://doi.org/10.1080/10696679.2022.2080713

- Selvan, T. A. K. S., & Abraham, D. P. (2022). Employee stress and its impact on the performance of LIC employees in Tirunelveli District. Journal of Positive School Psychology, 6(2), 4753–4758. https://www.journalppw.com/index.php/jpsp/article/view/2931

- Sharma, S. & Kaur, R.(2013). The effect of demographic factors on occupational stress: A study of insurance sector. OPUS: HR Journal, 4(1), 60. https://search.proquest.com/openview/98b67f1071b07805743888c25c3f7340/1?pq-origsite=gscholar&cbl=4581244

- Shetty, A., & Basri, S. (2018). Assessing the technical efficiency of traditional and corporate agents in Indian Life Insurance Industry: slack-based data envelopment analysis approach. Global Business Review. https://doi.org/10.1177/0972150917749722

- Shifrin, N. V., & Michel, J. S. (2021). Flexible work arrangements and employee health: A meta-analytic review. Work & Stress, 36(1), 60–85. https://doi.org/10.1080/02678373.2021.1936287

- Sivam, R.-W., & Chang, W. C. (2016). Occupational stress: The role of psychological resilience in the ecological transactional model. European Scientific Journal, ESJ, 12(14), 63. https://doi.org/10.19044/esj.2016.v12n14p63

- Srivastava, P., & Hopwood, N. (2009). A practical iterative framework for Qualitative data analysis. International Journal of Qualitative Methods, 8(1), 76–84. https://doi.org/10.1177/160940690900800107

- Tong, A., Sainsbury, P., & Craig, J. (2007). Consolidated criteria for reporting qualitative research (COREQ): A 32-item checklist for interviews and focus groups. International Journal for Quality in Health Care, 19(6), 349–357. https://doi.org/10.1093/intqhc/mzm042

- Torkelson, E., & Muhonen, T. (2004). The role of gender and job level in coping with occupational stress. Work & Stress, 18(3), 267–274. https://doi.org/10.1080/02678370412331323915

- Tsuzuki, Y., Matsui, T., & Kakuyama, T. (2012). Relations between positive and negative attributional styles and sales performance as moderated by length of insurance sales experience among Japanese Life Insurance Sales Agents. Psychology, 03(12), 1254–1258. https://doi.org/10.4236/psych.2012.312a186

- Vos, J., & van Rijn, B. (2021). The evidence-based conceptual model of transactional analysis: A focused review of the research literature. Transactional Analysis Journal, 51(2), 160–201. https://doi.org/10.1080/03621537.2021.1904364

- Wang, J. (., Fu, X., & Wang, Y. (2020). Can “bad” stressors spark “good” behaviors in frontline employees? Incorporating motivation and emotion. International Journal of Contemporary Hospitality Management, 33(1), 101–124. https://doi.org/10.1108/ijchm-06-2020-0519

- Wolever, R. Q., Bobinet, K. J., McCabe, K., Mackenzie, E. R., Fekete, E., Kusnick, C. A., & Baime, M. (2012). Effective and viable mind-body stress reduction in the workplace: A randomized controlled trial. Journal of Occupational Health Psychology, 17(2), 246–258. https://doi.org/10.1037/a0027278

- Woods, S. A., Wille, B., Wu, C., Lievens, F., & De Fruyt, F. (2019). The influence of work on personality trait development: The demands-affordances TrAnsactional (DATA) model, an integrative review, and research agenda. Journal of Vocational Behavior, 110, 258–271. https://doi.org/10.1016/j.jvb.2018.11.010

- Yan, Y., & Xie, H. (2009, August 1). Research on the application of data mining technology in insurance informatization. IEEE Xplore. https://doi.org/10.1109/HIS.2009.255

- Yong-Cheng, C. (2021). An empirical analysis of the influencing factors on the degree of life insurance individual agent loyalty: Based on the survey data of Jiangxi Life Insurance Company. Journal of Jiangxi University of Finance and Economics, (6), 611. http://cfejxufe.magtech.com.cn/xb/EN/abstract/abstract13746.shtml

- Zoghbi-Manrique de Lara, P., & Ruiz-Palomino, P. (2019). How servant leadership creates and accumulates social capital personally owned in hotel firms. International Journal of Contemporary Hospitality Management, 31(8), 3192–3211. https://doi.org/10.1108/ijchm-09-2018-0748