Abstract

This research examined the factors that affect customer satisfaction and switching behavior in the post-merger of the state-owned Islamic banks in Indonesia. Data were collected by distributing an online questionnaire to a total of 210 Muslim customers. Furthermore, the collected data were analyzed using SEM-PLS. The findings indicate that product quality can enhance customer satisfaction, and service quality can mitigate customer switching behavior. Interestingly, the Shariah compliance also has a significant effect on customer satisfaction and switching behavior by Indonesian Muslim. This suggested that, in Indonesia, where the majority of the population is Muslim, businesses that prioritize Shariah compliance are more likely to retain customers. Implication of this research provides empirical evidence to Islamic banks regarding the significance of reputation. Based on the findings, bank management tends to consider to integrate the product quality, service quality, and Shariah compliance into the banking business model. It is essential to consistently apply Sharia compliance to enhance customer satisfaction and reduce switching behavior. The Originality of this research is the first in Indonesia to examine customers’ switching behavior in the context of the merger of the State-Owned Islamic Banks. The findings can serve as an evaluation tool for the government and Islamic bank management to strengthen the country’s economy.

1. Introduction

Numerous industries have merged throughout the worldwide economic recession brought on by the global pandemic, which poses a threat to the global economy. Furthermore, in the banking industry, for example, the number of merger and acquisition cases tend to increase over several decades (Srivastava & Sharma, Citation2013). This trend is witnessed all over the world in America, Europe, and Asia, where it is seen as a strategy to create a strong, healthy, and large banking architecture that can withstand economic challenges (Novickytė & Pedroja, Citation2015). In Indonesia, where Muslims make up the majority of the population, there is a push for the growth and innovation of Islamic finance. To that end, on 27 January 2021, the State-Owned Islamic banks merged, as evidenced by letter number SR-3/PB.1/2021. It is believed that the bank management chose this merger as a strategy to improve financial stability and promote the growth of Islamic finance in the country.

The government’s efforts to merge the top three Islamic Commercial Banks including BRI Syariah, Bank Syariah Mandiri (BSM), and BNI Syariah have attracted attention and debates among observers, practitioners, religious figures, as well as the public. This is considered to have a positive effect on strengthening the standing of Islamic banking in relation to the domestic industry and Sharia finance (Novickytė & Pedroja, Citation2015). Therefore, it is expected to make operations more efficient and expand market reach (Das & Kumbhakar, Citation2022). Research believes that the merger only consolidates assets and provides little value while reducing the number of Islamic banks (Leledakis & Pyrgiotakis, Citation2022; Uchino & Uesugi, Citation2022). Although there is still a debate about the merger, the government through the Minister of State-Owned Corporation merged the three banks in early February 2021 under a new brand of Bank Syariah Indonesia (BSI).

As of 2022, the market share of national Islamic banking only reached 7.03% with an increase of 0.44% from the previous year. The assets of this sector increased from IDR676.73 trillion to IDR680.09 trillion in May 2022. These figures come from the entire Islamic banking industry consisting of 12 commercial banks, 21 business units, and rural banks (www.ojk.go.id 2022). Despite the increase in market share and assets, the growth of this sector in Indonesia is still considered low. Following the merger, the Islamic bank aims to achieve a market share of 20% by 2023. This target indicates that the Muslim population in this country is still largely untapped, and Islamic banking remains an untapped potential for the industry.

The merger of BRI Syariah, BSM, and BNI Syariah into Bank Syariah Indonesia (BSI) has implications for the customer relationship. Therefore, BSI needs to pay attention to customer relationship issues and how to maintain and maximize them. The transition period may lead to various behavioral effects among customers, as observed in financial institutions in the UK and Spain (Alvarez-González & Otero-Neira, Citation2020; Biswas et al., Citation2022; Homburg & Bucerius, Citation2005). n this situation, customers will face the halo effect. The halo effect is a general evaluation based on the first impression displayed (Pardo et al., Citation2022; Tri & Anh, Citation2020). Customers who perceive the merger to bring about positive changes (customer satisfaction) are likelier to become loyal to the Islamic bank (Christofi et al., Citation2017). On the other hand, customers who perceive no improvement in performance are more likely to consider switching to alternatives. The behavior of customers leaving the bank is known as switching behavior (Farah, Citation2017a).

Customer turnover serves as a significant issue that needs to be addressed in the financial services sector, as customers are vital assets for the industry. However, switching behavior poses a risk to the profitability of Islamic banks and opens up a potential market for competitors (Lymperopoulos et al., Citation2013)). The merger of the Indonesian Islamic banks is a strategic move to increase the capitalization of the financial market (Liang et al., Citation2013). Thus, to prevent customers from switching to competitors after the merger, this industry should give customer service priority. Therefore, in the highly competitive era of technology and social media, negative word-of-mouth can spread quickly, making it essential for an Islamic bank to ensure customer satisfaction while also preventing switching behavior (Gray et al., Citation2017).

A merger can result in different impacts, both positive and negative (Alvarez-González & Otero-Neira, Citation2020; Andrews & Goldsmith, Citation2015; Farah, Citation2017b, Citation2021). Post-merger, Bank Syariah Indonesia (BSI) faces two customer behaviors: customer satisfaction (Alvarez-González & Otero-Neira, Citation2020; Keisidou et al., Citation2013a, Citation2013b) and Switching Behavior (Farah, Citation2017a, Citation2017b). This research aims to analyze the direct relationships among determinants of post-merger customer behaviors. The study considers independent variables such as product quality, Shariah compliance, service quality, and technological sophistication in determining customer satisfaction and preventing switching behavior. Product quality enhances customer satisfaction and reduces switching behavior (Ahmed et al., Citation2022). Additionally, service quality is a primary determinant of customer satisfaction and switching behavior. Customer-oriented service quality can enhance customer satisfaction (Salleh et al., Citation2019; Zulfitri & Rohman, Citation2019) and reduce switching behavior (Prakash & Srivastava, Citation2019; Srivastava & Sharma, Citation2013). Another determinant is Shariah compliance. The uniqueness and purpose of Islamic banks lie in their alignment with Islamic law (Fatima & Khan, Citation2017; Maali et al., Citation2006; Majeed & Zainab, Citation2018; Mansoor Khan et al., Citation2008; Pollard & Samers, Citation2007). Haniffa and Hudaib (Citation2007) highlight Shariah compliance as a distinguishing feature among conventional banks. Customers choose Islamic banks because their business models firmly adhere to Shariah compliance (Basheer et al., Citation2018; Mbawuni & Nimako, Citation2017; Usman et al., Citation2017). ven without considering the profits obtained, Shariah compliance becomes a determining factor for customers choosing Islamic banks (Ahmed et al., Citation2022). The last determinant of customer satisfaction and switching behavior is technological Sophistication. Post-merger, Islamic banks need to enhance their technology and electronic services to reduce customer switching behavior (Ueno et al., Citation2018). The presence of technology can improve customer satisfaction (Balbin-Romero et al., Citation2022; Harb et al., Citation2022; Tahtamouni, Citation2022; Wiryawan et al., Citation2022) and reduce the incidence of Switching Behavior.

Previous research on post-merger customer behavior could be more extensive. However, the merger situation involving three banks into one with differentiated products, services, and technologies requires time to align with customer expectations. This study differs from previous research by examining two dependent variables and investigating the effects of the merger transition period on customer behavior (Alvarez-González & Otero-Neira, Citation2020; Biswas et al., Citation2022; Homburg & Bucerius, Citation2005). Additionally, there are inconsistencies in the findings of prior studies. While service quality has been found to enhance customer satisfaction Iqbal et al. (Citation2018); Saqib et al. (Citation2016); customers tend to prefer the service quality of conventional banks over Shariah-compliant banks (Moosa & Kashiramka, Citation2022; Ullah & Lee, Citation2012). However, one of the merger’s objectives is to enhance competition. Furthermore, previous research still lacks investigation into the effects of Shariah compliance (Khanna & Sharma, Citation2017; Nikhashemi et al., Citation2017) and its impact on switching behavior. Conversely, Shariah compliance has been studied concerning customer satisfaction, as shown by Ahmed et al. (Citation2022); Baber (Citation2019b, Citation2019a); Bian et al. (Citation2019); Elmontaser and Alhabshi (Citation2016); Firdaus (Citation2021); Jan and Shafiq (Citation2021); Salleh et al. (Citation2019); and Sulaiman et al. (Citation2020). This study aims to address the research gap by investigating how Shariah compliance can be a determinant of increased customer satisfaction and reduced switching behavior.

Therefore, this research examined the factors that affect customer satisfaction and switching behavior in the post-merger of the state-owned Islamic banks in Indonesia. Data were collected by distributing questionnaires to 210 Muslim customers, and data analysis was conducted using Structural Equation Model-Partial Least Square (SEM-PLS). The results showed that both product quality and Shariah compliance significantly affect customer satisfaction, whereas service quality and technological sophistication failed to have a positive effect. Meanwhile, service quality and sharia compliance significantly affect customer switching behavior in Indonesian Islamic banks, whereas product quality, technology sophistication, and customer satisfaction failed to have a positive effect.

In so doing, this research provides empirical evidence on the reputation of Islamic banks and offers factual information about the standing of Islamic banks in the Indonesian context. Thus, it is expected that the empirical evidence on customer satisfaction and switching behavior can help Islamic banking institutions decide which factors are more important in maintaining customer loyalty and preventing the customer from switching to other financial service providers. Product quality and Sharia compliance can serve as benchmarks for customer satisfaction. Attention also needs to be given to service quality and sharia compliance in managing switching behavior at Islamic banks. This research is the first in Indonesia to address customers’ switching behavior while analyzing customer satisfaction in the context of a Merger of State-Owned Islamic Banks. It will certainly draw the attention of the government and Islamic bank management in strengthening the Islamic economic ecosystem to become a world-class center for economics and finance.

2. Literature review Dan hypotheses

2.1. Switching behavior

In the era of open banking, switching behavior has become increasingly prevalent (Szopiński, Citation2021). Exploring the phenomenon of switching behavior in Islamic banking can help identify the reasons why customers switch to other Islamic or conventional banks. Therefore, Islamic banks need to develop a framework that can manage this behavior since switching behavior can affect their profitability and stability (Ben Lahouel et al., Citation2022, Citation2022; Zhao et al., Citation2023). In so doing, the bank management needs to be proactive in managing customer switching behavior (Baruna et al., Citation2023; Makudza, Citation2021; Szopiński, Citation2021; Taoana et al., Citation2022; Zhao et al., Citation2023).

2.2. Customer satisfaction

National and international banking competition makes customer satisfaction the epicenter of all activities for Islamic banks (Mir et al., Citation2023). Customer Satisfaction is a reflection of the bank’s performance in meeting the customer’s expectations, which builds their trust and loyalty (Alharthi et al., Citation2022; Biswas et al., Citation2023; Jawaid et al., Citation2023; Muhammad & Bin Ngah, Citation2023; Senthil, Citation2022; Uppal, Citation2022). Satisfaction will generate trust for customers, because they are treated properly by the company (Alhawamdeh et al., Citation2022). The customer loyalty is derived from customer satisfaction (Alqasa & Afaneh, Citation2022; Biswas et al., Citation2023; Damberg et al., Citation2022). In private sector banks, research has been done on the factors that influence customer satisfaction. According to the study, a bank’s standing and innovation can boost customer satisfaction. Other research has also examined how banks can improve CS, but none have simultaneously examined CSB. However, it is important to note that higher levels of customer satisfaction can help management better manage customer switching behavior.

2.3. Hypotheses

2.3.1. Product quality and customer satisfaction

High-quality products are crucial for satisfying customers as they can fulfill their expectations, particularly in the case of Islamic banking operations. Quality products will increase customer satisfaction (Belás & Gabčová, Citation2016; Hassani & Taati, Citation2020; Kolapo et al., Citation2021; Rod et al., Citation2016; Sipayung et al., Citation2021). The research by Gani and Oroh (Citation2021); Muafa et al. (Citation2020); and Srivastava and Sharma (Citation2013) showed that product quality significantly affects customer satisfaction. Based on these findings, the first hypothesis (H1) could be formulated as follows:

H1:

Product quality significantly affects customer satisfaction in Islamic banks.

2.3.2. Service quality and customer satisfaction

Service quality is another critical factor that greatly affects customer satisfaction in Islamic banks. Service quality affects customer satisfaction Ahmed et al. (Citation2020); Biswas et al. (Citation2023); Chatterjee et al. (Citation2023); Jasin and Firmansyah (Citation2023); Kim et al. (Citation2023); Mir et al. (Citation2023); Ong et al. (Citation2023); Yalcinkaya and Just (Citation2023). After a merger, the Islamic Bank service quality typically results in higher customer satisfaction.

H2: The Post-merger of the Islamic Bank service quality will increase customer satisfaction.

2.3.3. Shariah compliance dan customer satisfaction

Shariah compliance is an important immaterial factor that significantly affects customer satisfaction. Shariah compliance is an important immaterial factor that significantly affects customer satisfaction (Anouze et al., Citation2019, Citation2019; Asnawi et al., Citation2020; Ghamry & Shamma, Citation2022; Hosen et al., Citation2021, Citation2021). Ghamry and Shamma (Citation2022); Usman et al. (Citation2022) have also demonstrated that Sharia compliance affects customer satisfaction. Based on these findings, the third hypothesis could be formulated as follows:

H3: Shariah compliance affects customer satisfaction when it is upheld by Sharia entities.

2.3.4. Technological sophistication dan customer satisfaction

The presence of technology is very important for the quality of Islamic banking services in the digital era because it can simplify and speed up every transaction (Angusamy et al., Citation2022; Ghamry & Shamma, Citation2022; Ighomereho et al., Citation2022; Jaiwani et al., Citation2022; Kou et al., Citation2021; Tahtamouni, Citation2022; Wiryawan et al., Citation2022; Zyberi & Luzo, Citation2022). Lee et al. (Citation2018) and Sindwani (Citation2018) emphasized that technological sophistication significantly affects customer satisfaction. Based on these findings, the fourth hypothesis could be formulated as follows:

H4: Technological sophistication positively affects customer satisfaction in Islamic banks.

2.3.5. Product quality dan customer switching behavior

Customer interest in Islamic banking is dependent on the quality of its products, which can be a determining factor in customer loyalty (Newton et al., Citation2018; Nikhashemi et al., Citation2017). Nikhashemi et al. (Citation2017) explained that product quality significantly affects customer switching behavior. Based on these findings, the fifth hypothesis could be formulated as follows:

H5: The product quality of Islamic banks can reduce customer switching behavior.

2.3.6. Service quality dan customer switching behavior

Service quality is a critical factor that can cause Islamic bank customers to switch. Good service quality tends to increase customer satisfaction (Ahmed et al., Citation2020; Biswas et al., Citation2023; Chatterjee et al., Citation2023; Jasin & Firmansyah, Citation2023; Kim et al., Citation2023; Mir et al., Citation2023; Ong et al., Citation2023; Yalcinkaya & Just, Citation2023), while service failures can lead to switching behavior (Zhao et al., Citation2022, Citation2023). Thus, service quality affects customer switching behavior. Based on these findings, the sixth hypothesis could be formulated as follows:

H6: Good service quality significantly affects customer switching behavior in Islamic banks.

2.3.7. Sharia compliance dan customer switching behavior

Since Muslims make up the majority of Indonesia’s population, Islamic banking must take the religious component into consideration. The Shariah compliance is crucial for increasing customer trust and loyalty (Anouze et al., Citation2019, Citation2019; Asnawi et al., Citation2020; Ghamry & Shamma, Citation2022; Hosen et al., Citation2021, Citation2021). The Sharia compliance significantly affects customer switching behavior. Based on these findings, the seventh hypothesis could be formulated as follows:

H7: Sharia compliance significantly affects customer switching behavior of Indonesian Islamic banks.

2.3.8. Technological sophistication dan customer switching behavior

Ease and speed of access are indicators of technological sophistication that can affect customers’ decisions to stay or leave (Angusamy et al., Citation2022; Ghamry & Shamma, Citation2022; Ighomereho et al., Citation2022; Jaiwani et al., Citation2022; Kou et al., Citation2021; Tahtamouni, Citation2022; Wiryawan et al., Citation2022; Zyberi & Luzo, Citation2022). Ghamry and Shamma (Citation2022) and Gray et al. (Citation2017) emphasized that TS affects CSB. Therefore, an Islamic bank needs to improve its technology or e-services to reduce customer switching behavior after the merger (Martins et al., Citation2013; Sharma & Sharma, Citation2018; Singh et al., Citation2016; Yongho Hyun et al., Citation2014). The eight hypothesis in this research could be formulated as follows:

H8: Technological sophistication affects customer switching behavior of Islamic Bank.

2.3.9. Customer satisfaction dan customer switching behavior

In an Islamic bank, there are both rational and irrational customers. Highly satisfied customers are likely to remain loyal to the bank. Therefore, Islamic banks need to be customer-oriented to maintain customer satisfaction (Baber, Citation2019a, Citation2019b; Bian et al., Citation2019; Elmontaser & Alhabshi, Citation2016; Gopalan et al., Citation2015; Salleh et al., Citation2019; Thaichon et al., Citation2014, Citation2017; Vyas & Raitani, Citation2014; Zulfitri & Rohman, Citation2019). Prakash and Srivastava (Citation2019), Srivastava and Sharma (Citation2013), and Zulfitri and Rohman (Citation2019) indicated that Customer Satisfaction affects Customer Switching Behavior. Based on these findings, the ninth hypothesis could be formulated as follows:

H9: Customer satisfaction significantly affects customer switching behavior of Islamic Bank.

Figure is conceptual framework in this research :

Figure 1. Conceptual Framework.

3. Method

3.1. Sample and procedure

Data were collected by conducting a survey on Indonesian Muslim customers after the merger of the three state-owned Islamic banks. Indonesia has the largest Muslim population in the world, making it a potential market for Islamic banks. The study, which took into account a variety of demographic factors, was carried out online and distributed via social media and WhatsApp groups. WhatsApp is a platform frequently used by the Indonesian community to reach many participants (Fei et al., Citation2022; Kumar & Sharma, Citation2017). An online survey was conducted because it is economical, saves time and energy, and is efficient (Taylor, Citation2000).

This research employed a convenience sampling technique since the size of the population was unknown. Potential respondents were filtered based on their use of the Islamic bank after the merger to obtain accurate answers in line with the research objectives. Furthermore, they were asked to answer questions focusing on the variables such as product quality, service quality, Sharia compliance, technological sophistication, customer satisfaction, and customer switching behavior.

3.2. Measurement variable

The questionnaire consisted of various dimensions and adopted items from previous research. Each item was measured using a 10-point Likert scale, ranging from strongly disagree to strongly agree. This 10-point Likert scale was selected due to the instrument’s efficiency and familiarity with respondents in Indonesia (Awang et al., Citation2016). Table shows the items for each variable. Validity and reliability testing of the questionnaire was conducted before collecting the data (Paramita et al., Citation2021).

Table 1. Variable measurement table

3.3. Data analysis method

Data were analyzed using the Structural Equation Model. SEM-PLS was selected to fulfill the requirements of exploratory research (Hair et al., Citation2011), therefore, it is more feasible to build and test a new model. This research adopted PLS-SEM as it does not require assumptions about the data distribution (Vinzi et al., Citation2009). Additionally, because PLS-SEM is the most effective method for the analysis, it is constrained to a small number of respondents (Wong, Citation2013). This research uses the SmartPLS software. SmartPLS helps researchers fulfill statistical power and data representation requirements (Ahmed et al., Citation2017, Citation2022; Johan et al., Citation2020). Additionally, the unknown population size in this study makes SmartPLS the best option (Ahmed et al., Citation2022; Henseler et al., Citation2016; Rigdon, Citation2016). This research aims to evaluate the structural model, making SmartPLS suitable for theory development and prediction purposes (Ahmed et al., Citation2022; Hulland et al., Citation2017; Joseph F.; Hair et al., Citation2017).

4. Result and discussion

4.1. Result

4.1.1. Respondent profile

Table contains information about the respondents’ profiles. Males dominate the population at 64.29%, while females account for 35.71%. More than half (n = 140, 66.67%) of the respondents are aged 36 years or older. Furthermore, 43.33% and 47.14% of the customers hold a bachelor’s degree and work in academics respectively. Most of the respondents have been customers of Islamic banks for more than 4 years (n = 130, 61.90%).

Table 2. Respondent profile

4.1.2. Measurement model

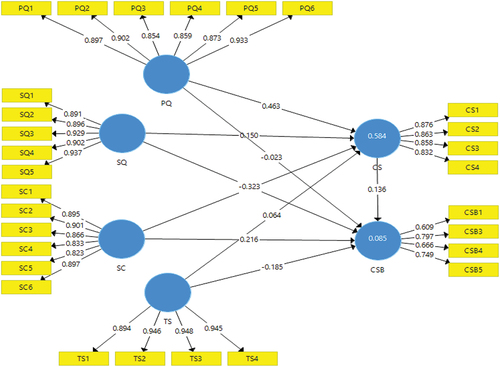

The validity and reliability of the observed variables were evaluated using a measurement model. However, in the customer switching behavior (CSB2) variable, the outer loading value was below 0.50. Therefore, following the guidelines, this item was excluded (Joseph et al., Citation2016). This indicates that the CSB2 item cannot be relied upon in explaining the customer switching behavior. Meanwhile, Table and Figure indicate that all other outer loadings (λ) items are above 0.50 and have met the minimum factor loading criteria. This shows all latent variables can be adequately explained by their observed variables.

Figure 2. Factor loading results.

Table 3. Measurement model results

The Cronbach’s Alpha (α) values of all items ranged from 0.667 to 0.951, which are higher than the recommended thresholds of 0.60 by Joseph et al. (Citation2016). Additionally, all CR values exceeded the recommended level of 0.70 by Hair et al. (Citation2017). Convergent validity was measured using AVE, and the results showed that the AVE value of the latent variables was higher than 0.50. This indicates that the constructs have explained more than half of the variance of their indicators specifically (Hair et al., Citation2017).

The next stage is discriminant validity by comparing the square roots of each AVE construct using Fornell-Larcker. Table shows that each construct has a greater value than the other. Therefore, all constructs have high discriminant validity.

Table 4. Discriminant validity (fornell-larcker criterion)

4.1.3. Structural model

The proposed model was tested using the structural model. As presented in Table , four hypotheses including H1, H3, H6, and H7 were accepted, while H2, H4, H5, H8, and H9 were rejected. Specifically, the P-values for product quality and technological sophistication were above the determined significance level, indicating that they were not correlated with customer satisfaction. PQ, TS, and CS were also reported to have no significant correlation with CSB.

Table 5. Hypothesis testing

According to Hair et al. (Citation2017), the variable of customer satisfaction has an R2 value of 0.584, indicating that product quality, service quality, Sharia compliance, and technological sophistication have a moderate strength of 58.4%. The R2 value for the CSB is 0.085, indicating that PQ, SQ, SC, TS, and CS have a weak strength of 8.5% (Hair et al., Citation2017). It is important to note that other factors not examined in this research may contribute to the remaining predictions.

Table shows a parameter coefficient value and P-Values for each variable. The parameter coefficient value for the product quality is 0.463 and its P-value is smaller than 0.01. This indicates that the variable is significantly correlated with Customer Satisfaction, therefore H1 is accepted. The service quality has a parameter coefficient value of 0.150 but its P-Value is greater than the set level of significance. This indicates that the variable failed to significantly affect customer satisfaction, therefore H2 is rejected. The Sharia compliance has a parameter coefficient value of 0.144 and the P-Value is smaller than 0.1. This indicates that the variable significantly affects customer satisfaction, therefore H3 is accepted. The parameter coefficient value for technological sophistication is 0.064 but its P-Value is greater than the set level of significance. This suggests that the variable failed to significantly affect customer satisfaction, and therefore H4 is rejected.

Product quality does not affect customer switching behavior because it has a parameter coefficient value of −0.023, therefore H5 is rejected. Conversely, service quality has a parameter coefficient value of −0.323 and a P-Value lower than 0.05. This indicates that it does not have a significant effect on customer switching behavior, therefore H6 is accepted. Similarly, Shariah compliance has a parameter coefficient value of 0.216 and a P-Value lower than 0.05, therefore H7 is accepted. Technological sophistication has a parameter coefficient value of −0.185, along with a P-Value greater than the established significance level. This indicates that it does not significantly affects customer switching behavior, therefore H8 is rejected. Furthermore, the P-Value for customer satisfaction is greater than the established significance level, indicating that it does not significantly affect customer switching behavior, therefore H9 is rejected.

5. Discussion

After the merger, customers of the Indonesian Islamic bank placed importance on product quality and Sharia compliance for increasing their satisfaction. The analysis results showed a significant correlation between product quality and customer satisfaction, which aligns with prior research (Srivastava & Sharma, Citation2013) (Gani & Oroh, Citation2021; Muafa et al., Citation2020; Srivastava & Sharma, Citation2013). After the merger, customers of the Indonesian Islamic bank placed importance on product quality and Sharia compliance for increasing their satisfaction. The analysis results showed a significant correlation between product quality and customer satisfaction, which aligns with prior research (Bei & Chiao, Citation2006; Belás & Gabčová, Citation2016; Hassani & Taati, Citation2020; Jun & Cai, Citation2001; Jun et al., Citation2002; Kolapo et al., Citation2021; Nowak, Citation1997; Rod et al., Citation2016; Schuster, Citation1996; Sipayung et al., Citation2021). Therefore, the quality of the Islamic bank’s products plays an important role in increasing customer satisfaction and reducing switching behavior (Khanna & Sharma, Citation2017; Nikhashemi et al., Citation2017; Vyas & Raitani, Citation2014).

Indonesia, with the world’s largest Muslim population, has a strong culture that upholds Islamic teachings. The analysis results showed that Sharia compliance has a significant effect on customer satisfaction in an Islamic bank. This is in line with Ahmed et al. (Citation2017), and Pradeep et al. (Citation2020). Customers view compliance indicators as a key factor in selecting a trustworthy Islamic bank (Ahmed et al., Citation2020 (Anouze et al., Citation2019; Hosen et al., Citation2021)). As noted by (Ghamry & Shamma, Citation2022) Sharia compliance is a crucial determinant of customer satisfaction. It is essential to harmonize banking activities with Islamic law, which is derived from the Quran and Hadith to increase customer trust (Anouze et al., Citation2019; Asnawi et al., Citation2020; Ghamry & Shamma, Citation2022; Hosen et al., Citation2021). Furthermore, this will impact customer satisfaction in an Islamic bank (Usman et al., Citation2022).

Shariah compliance plays an important role in managing customer switching behavior. However, service quality can prevent customers from switching to other financial service providers. This shows it has a negative correlation with customer switching behavior. This is in line with (Liang et al., Citation2013; Srivastava & Sharma, Citation2013). Good service quality can increase customer satisfaction at an Islamic bank (Ahmed et al., Citation2020; Biswas et al., Citation2023; Chatterjee et al., Citation2023; Jasin & Firmansyah, Citation2023; Kim et al., Citation2023; Mir et al., Citation2023; Ong et al., Citation2023; Yalcinkaya & Just, Citation2023). Conversely, service failures may lead to switching behavior (Zhao et al., Citation2022, Citation2023), and effective management of Islamic banks prioritizes the best service for customers.

Interestingly, Sharia compliance is a crucial factor that has a significant correlation with customer switching behavior. The findings are in line with previous findings (Liang et al., Citation2013; Srivastava & Sharma, Citation2013). Furthermore, this variable is the backbone of the Islamic bank, and its operations need to adhere to Sharia principles (Islamic Business Law) (Fatima & Khan, Citation2017; Maali et al., Citation2006; Majeed & Zainab, Citation2018; Mansoor Khan et al., Citation2008; Pollard & Samers, Citation2007). Therefore, Sharia compliance is one of the important factors in preventing switching behavior. After the merger of the Islamic bank, it faces operational consistency in line with Sharia laws. The Bank Syariah Indonesia (BSI) was formed from three top state-owned corporation Islamic banks, each with diverse products and policies. Neglecting Shariah compliance can potentially lead to devout customers switching to other banks. This variable is important for Muslim customers, known for their religiosity, as it offers an alternative and differentiation from conventional systems.

This research found that service quality failed to significantly affect customer satisfaction. Contrary to the previous review (Ahmed et al., Citation2017; Pradeep et al., Citation2020; Rahayu et al., 2019). This result is consistent with findings that customers prefer the service quality of conventional banks over those with Shariah-based services (Moosa & Kashiramka, Citation2022; Ullah & Lee, Citation2012). Customers choose Shariah-compliant banks regardless of the benefits they may obtain (Ahmed et al., Citation2022). Furthermore, in line with this research, product quality and Shariah compliance affect Customer Satisfaction. Product quality and Shariah compliance are two interconnected aspects of Islamic banks. Haniffa and Hudaib (Citation2007) stated that Shariah compliance is one of the distinctive features of Islamic bank products, which are free from riba (interest) and adhere to Shariah principles. Customers choose Islamic banks because their business model firmly upholds Shariah compliance (Basheer et al., Citation2018; Mbawuni & Nimako, Citation2017; Usman et al., Citation2017). Therefore, service quality does not become a significant measure of customer satisfaction during a merger when the Islamic bank already offers products aligned with Islamic principles.

Product quality failed to significantly affect customer switching behavior, contrary to the previous review (Kaur et al., Citation2012). In this research, customers consider that product quality can create satisfaction after the merger. They eagerly await the post-merger product quality, which can improve the bank’s outcome and customer satisfaction (Hassani & Taati, Citation2020; Kolapo et al., Citation2021; Sipayung et al., Citation2021). The quality of the products offered by Islamic banks after the merger will play an important role in enhancing satisfaction, and, in turn, suppressing switching behavior (Khanna & Sharma, Citation2017; Nikhashemi et al., Citation2017). Therefore, product quality may be indirectly related to switching behavior.

Technological sophistication also failed to significantly affect customer satisfaction and switching behavior. This is because Indonesian state-owned banks, on average, already have a high level of technological sophistication (Kesuma et al., Citation2016). In Indonesia, Islamic banks have also adopted high-level technology, with information and managerial sophistication. This technology was already in place before the merger, and BSI has implemented an even more advanced one since it is the embryo of three established conventional banks. Therefore, this variable is not problematic after the merger, contrary to previous research by Ahmed et al. (Citation2017), Gray et al. (Citation2017) and Pradeep et al. (Citation2020). This statistical fact is logical since technological sophistication alone does not appear to cause customers to switch to another bank.

At the same time, customer satisfaction failed to significantly affect switching behavior. The result showed that BSI customers are satisfied with the products offered and do not exhibit switching behavior. This statistical fact is consistent with Kaur et al. (Citation2012) and Keaveney and Parthasarathy (Citation2001). The lack of an effect of customer satisfaction on customer switching behavior indicates that BSI customers remain loyal post-merger, refuting concerns raised by some observers and religious figures about distrust of the merger project. As of 2022, BSI has become the seventh-largest bank in Indonesia based on assets held. The BSI in this same year was awarded The Strongest Islamic Retail Bank among 130 Islamic banks worldwide based on an assessment by the Cambridge Institute of Islamic Finance (CIIF).

6. Conclusion

This research aimed to examine the factors that affect customer satisfaction and customer switching behavior of the Bank Syariah Indonesia (BSI) customers after the merger. The findings of the current study successfully addressed the research questions and achieved the objectives. It was found that product quality, service quality, and Sharia compliance significantly affect customer satisfaction and customer switching behavior. However, technological sophistication did not show any significant correlation between customer satisfaction and customer switching behavior. These findings provide a business model framework that is essential for customer retention. Islamic banks should put their attention on operational aspects that foster customer connection, such as providing high-quality products, services, and adhering to Sharia law. By adopting this business model, Islamic banks can strengthen customer relationships.

Theoretical contribution: The findings of this research provide a conceptual framework for understanding customer satisfaction and switching behavior. Of particular interest is the significant role played by Sharia compliance, which is highly valued by Muslim customers in Indonesia. These customers are extremely concerned about how financial services must adhere to Shariah. These findings generally demonstrated that service quality will perform as expected.

Practical implication: This study offers Islamic banks useful empirical evidence about their standing. To succeed in an increasingly competitive financial market, bank management needs to examine customer satisfaction and customer switching behavior with various variables. Product quality and Sharia compliance can serve as benchmarks for assessing customer satisfaction. Therefore, attention needs to be paid to service quality and Sharia compliance in managing customers’ switching behavior. Integrating product quality and service quality with strict Sharia compliance can increase customer satisfaction as well as reduce customer switching behavior.

Furthermore, this study provides recommendations for future research as follows: Researchers in the future may consider involving various customer variables such as religiosity, trust, and psychological conditions. Loyalty variables should also be considered in the research model. Future studies may also incorporate mediating and moderating variables. Researchers should also develop measurements of variables that align with current developments. Given the competition among Shariah banks, it is essential to identify customer satisfaction, customer switching behavior, and loyalty among Muslim and non-Muslim customers. Moreover, it is important to examine across generations and countries so that the research model remains robust in all countries and conditions.

Author bio.docx

Download MS Word (28.2 KB)Disclosure statement

No potential conflict of interest was reported by the author(s).

Supplemental data

Supplemental data for this article can be accessed online at https://doi.org/10.1080/23311975.2023.2287781

Additional information

Notes on contributors

Mochlasin Mochlasin

Mochlasin Mochlasin is an academic associate professor of Islamic Economics and the Dean of the Faculty of Islamic Economics and Business at the State Islamic University (UIN) Salatiga, Indonesia. His Research Focuses on Islamic Economics, Islamic Banking, Consumer Behavior, and Islamic Business Ethics. Nornajihah Nadia Hasbullah is a Senior Lecturer at Faculty of Business Management, University Teknologi MARA (UiTM) Bandaraya Melaka, 75350, Melaka, Malaysia. Her research interest includes bibliometric analysis, consumer behavior, sustainable marketing, and digital marketing. Ahmad Mifdlol Muthohar is an Associate Professor of Islamic Economics and serves as head of the study program Islamic Economics Postgraduate Program of the State Islamic University (UIN) Salatiga. His Research Focuses on Islamic Finance, including Zakah Waqf, Taxation, and Islamic Public Finance. Saiful Anwar is an Assistant Professor of Islamic Accounting at the Faculty of Islamic Economics and Business at the State Islamic University (UIN) Salatiga, Indonesia. Currently a student in the doctoral program of accounting at Airlangga University, Surabaya, Indonesia. His research interest on Islamic Accounting, Behavioral Accounting, Governance and Sustainability.

References

- Ahmed, S., Islam, R., & Mohiuddin, M. (2017). Service quality, Shariah compliance and customer satisfaction of Islamic banking services in Malaysia. Turkish Journal of Islamic Economics, 4(2), 71–19. https://doi.org/10.26414/tujise.2017.4.2.71-82

- Ahmed, S., Mohiuddin, M., Rahman, M., Tarique, K. M., & Azim, M. (2022). The impact of Islamic Shariah compliance on customer satisfaction in Islamic banking services: Mediating role of service quality. Journal of Islamic Marketing, 13(9), 1829–1842. https://doi.org/10.1108/JIMA-11-2020-0346

- Ahmed, R. R., Romeika, G., Kauliene, R., Streimikis, J., & Dapkus, R. (2020). ES-QUAL model and customer satisfaction in online banking: Evidence from multivariate analysis techniques. Oeconomia Copernicana, 11(1), 59–93. https://doi.org/10.24136/oc.2020.003

- Alharthi, M., Hanif, I., Ur Rehman, H., & Alamoudi, H. (2022). Satisfaction of Pakistan’s Islamic banking system during the COVID-19 pandemic logistic model-based identification of the determinants to improve customer. Journal of Islamic Marketing, 13(11), 2290–2307. https://doi.org/10.1108/JIMA-06-2020-0189

- Alhawamdeh, A. K., Alfukaha, F. A., Padlee, S. F., Salleh, A. M. M., & Saadon, M. S. I. (2022). The impact of customer satisfaction on loyalty in Jordanian banks: The mediating role of corporate reputation. International Journal of Management and Sustainability, 11(2), 70–80. https://doi.org/10.18488/11.v11i2.2998

- Alqasa, K. M. A., & Afaneh, J. A. A. (2022). Exploring the impact of service quality dimensions on customer loyalty with a moderating role of customer trust: An Applied study on the Saudi commercial banks in Eastern Province, Saudi Arabia. International Journal of Operations and Quantitative Management, 28(1), 82–99. https://doi.org/10.46970/2022.28.1.5

- Alvarez-González, P., & Otero-Neira, C. (2020). The effect of mergers and acquisitions on customer–company relationships. International Journal of Bank Marketing, 38(2), 406–424. https://doi.org/10.1108/IJBM-02-2019-0058

- Andrews, M., & Goldsmith, R. (2015). In the wake of a merger: Consumer reactions to service failures. Journal of Applied Marketing Theory, 5(2), 1–25. https://doi.org/10.20429/jamt.2014.050201

- Angusamy, A., Yee, C. J., & Kuppusamy, J. (2022). E-Banking: An empirical study on customer satisfaction. Journal of System and Management Sciences, 12(4), 27–38. https://doi.org/10.33168/JSMS.2022.0402

- Anouze, A. L. M., Alamro, A. S., & Awwad, A. S. (2019). Customer satisfaction and its measurement in Islamic banking sector: A revisit and update. Journal of Islamic Marketing, 10(2), 565–588. https://doi.org/10.1108/JIMA-07-2017-0080

- Asnawi, N., Sukoco, B. M., & Fanani, M. A. (2020). The role of service quality within Indonesian customers satisfaction and loyalty and its impact on Islamic banks. Journal of Islamic Marketing, 11(1), 192–212. https://doi.org/10.1108/JIMA-03-2017-0033

- Awang, Z., Afthanorhan, A., & Mamat, M. (2016). The Likert scale analysis using parametric based structural Equation modeling (SEM). Computational Methods in Social Sciences (CMSS), 4(1), 13–21. https://econpapers.repec.org/RePEc:ntu:ntcmss:vol4-iss1-16-013

- Baber, H. (2019a). E-SERVQUAL and its impact on the performance of Islamic banks in Malaysia from the customer’s perspective. The Journal of Asian Finance, Economics & Business, 6(1), 169–175. https://doi.org/10.13106/jafeb.2019.vol6.no1.169

- Baber, H. (2019b). Relevance of e-SERVQUAL for determining the quality of FinTech services. International Journal of Electronic Finance, 9(4), 257–267. https://doi.org/10.1504/IJEF.2019.104070

- Balbin-Romero, G., Carrera-Mija, E., Serrato-Cherres, A., & Cordova-Buiza, F. (2022). Relationship between e-banking service quality based on the e-SERVQUAL model and customer satisfaction: A study in a Peruvian bank. Banks and Bank Systems, 17(4), 180–188. https://doi.org/10.21511/bbs.17(4).2022.15

- Baruna, S. S. A., Dalimunthe, Z., & Triono, R. A. (2023). Factors affecting investor switching intention to Fintech peer-to-peer lending (Vol. 487). Springer Science and Business Media Deutschland GmbH. https://doi.org/10.1007/978-3-031-08084-5_7

- Basheer, M., Hassan, S., & Ahmad, A. (2018). Patronage factors of Islamic banking system in Pakistan. Academy of Accounting & Financial Studies Journal, (Special Issue), 22.

- Bei, L.-T., & Chiao, Y.-C. (2006). The determinants of customer loyalty: An analysis of intangible factors in three service industries. International Journal of Commerce & Management, 16(3–4), 162–177. https://doi.org/10.1108/10569210680000215

- Belás, J., & Gabčová, L. (2016). The relationship among customer satisfaction, loyalty and financial performance of commercial banks. E A M: Ekonomie a Management, 19(1), 132–147. https://doi.org/10.15240/tul/001/2016-1-010

- Ben Lahouel, B., Taleb, L., Kočišová, K., & Ben Zaied, Y. (2022). The threshold effects of income diversification on bank stability: An efficiency perspective based on a dynamic network slacks-based measure model. Annals of Operations Research, 330(1–2), 267–304. https://doi.org/10.1007/s10479-021-04503-4

- Ben Lahouel, B., Taleb, L., & Kossai, M. (2022). Nonlinearities between bank stability and income diversification: A dynamic network data envelopment analysis approach. Expert Systems with Applications, 207, 207. https://doi.org/10.1016/j.eswa.2022.117776

- Bian, L. K., Haque, A., Wok, S., & Tarofder, A. K. (2019). The effect of customer satisfaction on customer loyalty in the motor industry. Opcion, 35(Special Issue 21), 947–963. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85071367130&partnerID=40&md5=de6a4f80adf5c13a84bf5579db8cb543

- Biswas, A., Jaiswal, D., & Kant, R. (2022). Investigating service innovation, bank reputation and customer trust: Evidence from Indian retail banking. International Journal of Quality & Service Sciences, 14(1), 1–17. https://doi.org/10.1108/IJQSS-03-2021-0042

- Biswas, A., Jaiswal, D., & Kant, R. (2023). Augmenting bank service quality dimensions: Moderation of perceived trust and perceived risk. International Journal of Productivity & Performance Management, 72(2), 469–490. https://doi.org/10.1108/IJPPM-04-2021-0196

- Chatterjee, S., Ghatak, A., Nikte, R., Gupta, S., & Kumar, A. (2023). Measuring SERVQUAL dimensions and their importance for customer-satisfaction using online reviews: A text mining approach. Journal of Enterprise Information Management, 36(1), 22–44. https://doi.org/10.1108/JEIM-06-2021-0252

- Christofi, M., Leonidou, E., & Vrontis, D. (2017). Marketing research on mergers and acquisitions: A systematic review and future directions. International Marketing Review, 34(5), 629–651. https://doi.org/10.1108/IMR-03-2015-0100

- Coker, B. (2013). Antecedents to website satisfaction, loyalty, and word-of-mouth. Journal of Information Systems and Technology Management, 10(2), 209–218. https://doi.org/10.4301/S1807-17752013000200001

- Damberg, S., Schwaiger, M., & Ringle, C. M. (2022). What’s important for relationship management? The mediating roles of relational trust and satisfaction for loyalty of cooperative banks’ customers. Journal of Marketing Analytics, 10(1), 3–18. https://doi.org/10.1057/s41270-021-00147-2

- Das, A., & Kumbhakar, S. C. (2022). Bank merger, credit growth, and the great slowdown in India. Economic and Political Weekly, 57(20), 58–67. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85131055246&partnerID=40&md5=aeb8d38e310335698ffa5311637ae52f

- Elmontaser, M. A., & Alhabshi, S. M. B. S. J. (2016). The impact of service quality on Malaysian Muslim Islamic bank customers: Satisfaction, loyalty and retention. Al-Shajarah, 21(Specialissue), 183–215. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85028665522&partnerID=40&md5=0d298513817a9b5b1affca1d0d79a8cc

- Farah, M. F. (2017a). Application of the theory of planned behavior to customer switching intentions in the context of bank consolidations. International Journal of Bank Marketing, 35(1), 147–172. https://doi.org/10.1108/IJBM-01-2016-0003

- Farah, M. F. (2017b). Consumers’ switching motivations and intention in the case of bank mergers: A cross-cultural study. International Journal of Bank Marketing, 35(2), 254–274. https://doi.org/10.1108/IJBM-05-2016-0067

- Farah, M. F. (2021). Consumer perception of Halal products: An empirical assessment among Sunni versus Shiite Muslim consumers. Journal of Islamic Marketing, 12(2), 280–301. https://doi.org/10.1108/JIMA-09-2019-0191

- Fei, J., Wolff, J., Hotard, M., Ingham, H., Khanna, S., Lawrence, D., Tesfaye, B., Weinstein, J. M., Yasenov, V., & Hainmueller, J. (2022). Automated chat application surveys using whatsapp: Evidence from panel surveys and a mode experiment. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4114839

- Firdaus, A. (2021). Determination of organisational essential needs as the basis for developing a maṣlaḥah-based performance measurement. ISRA International Journal of Islamic Finance, 13(2), 229–250. https://doi.org/10.1108/IJIF-11-2017-0041

- Gani, A., & Oroh, A. (2021). The effect of product quality, service quality and price on customer satisfaction at Loki Store. KnE Social Sciences. https://doi.org/10.18502/kss.v5i5.8803

- Ghamry, S., & Shamma, H. M. (2022). Factors influencing customer switching behavior in Islamic banks: Evidence from Kuwait. Journal of Islamic Marketing, 13(3), 688–716. https://doi.org/10.1108/JIMA-01-2020-0021

- Gopalan, R., Sreekumar, & Satpathy, B. (2015). Evaluation of retail service quality – A fuzzy AHP approach. Benchmarking: An International Journal, 22(6), 1058–1080. https://doi.org/10.1108/BIJ-05-2013-0052

- Gray, D. M., D’Alessandro, S., Johnson, L. W., & Carter, L. (2017). Inertia in services: Causes and consequences for switching. Journal of Services Marketing, 31(6), 485–498. https://doi.org/10.1108/JSM-12-2014-0408

- Hair, J. F., Matthews, L. M., Matthews, R. L., & Sarstedt, M. (2017). PLS-SEM or CB-SEM: Updated guidelines on which method to use. International Journal of Multivariate Data Analysis, 1(2), 107–123. https://doi.org/10.1504/IJMDA.2017.087624

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory & Practice, 19(2), 139–152. https://doi.org/10.2753/MTP1069-6679190202

- Haniffa, R., & Hudaib, M. (2007). Exploring the ethical identity of Islamic banks via communication in annual reports. Journal of Business Ethics, 76(1), 97–116. https://doi.org/10.1007/s10551-006-9272-5

- Harb, A., Thoumy, M., & Yazbeck, M. (2022). Customer satisfaction with digital banking channels in times of uncertainty. Banks and Bank Systems, 17(3), 27–37. https://doi.org/10.21511/bbs.17(3).2022.03

- Hassani, L., & Taati, E. (2020). Studying product quality by exploring credit card customers behaviour via data mining techniques. International Journal for Quality Research, 14(1), 163–182. https://doi.org/10.24874/IJQR14.01-11

- Henseler, J., Hubona, G., & Ray, P. A. (2016). Using PLS path modeling in new technology research: Updated guidelines. Industrial Management & Data Systems, 116(1), 2–20. https://doi.org/10.1108/IMDS-09-2015-0382

- Homburg, C., & Bucerius, M. (2005). A Marketing perspective on mergers and acquisitions: How Marketing integration affects postmerger performance. Journal of Marketing, 69(1), 95–113. https://doi.org/10.1509/jmkg.69.1.95.55510

- Hosen, M. N., Lathifah, F., & Jie, F. (2021). Perception and expectation of customers in Islamic bank perspective. Journal of Islamic Marketing, 12(1), 1–19. https://doi.org/10.1108/JIMA-12-2018-0235

- Hulland, J., Baumgartner, H., & Smith, K. (2017). Marketing survey research best practices: Evidence and recommendations from a review of JAMS articles. Journal of the Academy of Marketing Science, 46(1), 92–108. https://doi.org/10.1007/s11747-017-0532-y

- Ighomereho, O. S., Afolabi, T. S., & Oluwakoya, A. O. (2022). Impact of E-service quality on customer satisfaction: A study of internet banking for general and maritime services in Nigeria. Journal of Financial Services Marketing, 28(3), 488–501. https://doi.org/10.1057/s41264-022-00164-x

- Iqbal, M., Nisha, N., & Rashid, M. (2018). Bank selection criteria and satisfaction of retail customers of Islamic banks in Bangladesh. International Journal of Bank Marketing, 36(5), 931–946. https://doi.org/10.1108/IJBM-01-2017-0007

- Jaiwani, M., Gopalkrishnan, S., Mohanty, S. P., & Murthy, N. (2022). Understanding service quality, customer satisfaction and banking behaviour from an E-Banking perspective: An empirical approach. Institute of Electrical and Electronics Engineers Inc. https://doi.org/10.1109/SIBF56821.2022.9939858

- Jan, M. T., & Shafiq, A. (2021). Islamic banks’ brand personality and customer satisfaction: An empirical investigation through SEM. Journal of Islamic Accounting and Business Research, 12(4), 488–508. https://doi.org/10.1108/JIABR-05-2020-0149

- Jasin, M., & Firmansyah, A. (2023). The role of service quality and marketing mix on customer satisfaction and repurchase intention of SMEs products. Uncertain Supply Chain Management, 11(1), 383–390. https://doi.org/10.5267/j.uscm.2022.9.004

- Jawaid, S. T., Siddiqui, A. H., Kanwal, R., & Fatima, H. (2023). Islamic banking and customer satisfaction in Pakistan: Evidence from internal and external customers. Journal of Islamic Marketing, 14(2), 435–464. https://doi.org/10.1108/JIMA-09-2020-0297

- Johan, Z. J., Hussain, M. Z., Mohd, R., Kamaruddin, B. H., Ahmed, S., Mohiuddin, M., Rahman, M., Tarique, K. M., & Azim, M. (2020). Muslims and non-Muslims intention to hold Shariah-compliant credit cards: A SmartPLS approach. Journal of Islamic Marketing, 12(9), 1829–1842. https://doi.org/10.1108/JIMA-12-2019-0270

- Joseph, F., Hair, J., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2016). A primer on Partial least squares structural Equation modeling (PLS-SEM). SAGE Publications, Inc.

- Jun, M., & Cai, S. (2001). The key determinants of internet banking service quality: A content analysis. International Journal of Bank Marketing, 19(7), 276–291. https://doi.org/10.1108/02652320110409825

- Jun, M., Cai, S., & Kim, D. (2002). The Linkages of Online Banking Service Quality Dimensions to Customer Satisfaction. 2125–2130. https://www.scopus.com/inward/record.uri?eid=2-s2.0-1642482497&partnerID=40&md5=d9c5f8de12a181c2bd610b80faec3b08

- Kaur, G., Sharma, R. D., Mahajan, N., & Roy, S. K. (2012). Exploring customer switching intentions through relationship marketing paradigm. International Journal of Bank Marketing, 30(4), 280–302. https://doi.org/10.1108/02652321211236914

- Keaveney, S. M., & Parthasarathy, M. (2001). Customer switching behavior in online services: An exploratory study of the role of selected attitudinal, behavioral, and demographic factors. Journal of the Academy of Marketing Science, 29(4), 374–390. https://doi.org/10.1177/03079450094225

- Keisidou, E., Sarigiannidis, L., Maditinos, D. I., & Thalassinos, E. I. (2013a). Customer satisfaction, loyalty and financial performance. International Journal of Bank Marketing, 31(4), 259–288. https://doi.org/10.1108/IJBM-11-2012-0114

- Keisidou, E., Sarigiannidis, L., Maditinos, D. I., & Thalassinos, E. I. (2013b). Customer satisfaction, loyalty and financial performance: A holistic approach of the Greek banking sector. International Journal of Bank Marketing, 31(4), 259–288. https://doi.org/10.1108/IJBM-11-2012-0114

- Kesuma, S. A., Saidin, S. Z., & Ahmi, A. (2016). IT sophistication: Implementation on state owned banks in Indonesia. International Review of Management and Marketing, 6(8Special Issue), 234–239. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85008881509&partnerID=40&md5=0a6c678ec30763099e5d10decbc4a893

- Khan, H. F. (2017). Islamic Banking: on Its Way to Globalization. International Journal of Management Research & Review, 7(11), 1006–1014.

- Khanna, V., & Sharma, R. (2017). Consumer switching behavior in banking sector in India. International Journal of Applied Business and Economic Research, 15(9), 427–441. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85019624796&partnerID=40&md5=8fb84631a148f842c6ab36a809cdb5eb

- Kim, J.-H., Ahn, S., & Lee, E. (2023). Effect of power message on employee response and job recruitment in the Hospitality industry. Journal of Hospitality & Tourism Research, 47(2), 303–327. https://doi.org/10.1177/10963480211010992

- Kolapo, F. T., Mokuolu, J. O., Dada, S. O., & Adejayan, A. O. (2021). Strategic marketing innovation and bank performance in Nigeria. Innovative Marketing, 17(1), 120–129. https://doi.org/10.21511/im.17(1).2021.10

- Kotler, P., & Keller, K. L. (2012). Marketing Management. Pearson Education.

- Kou, G., Olgu Akdeniz, Ö., Dinçer, H., & Yüksel, S. (2021). Fintech investments in European banks: A hybrid IT2 fuzzy multidimensional decision-making approach. Financial Innovation, 7(1). https://doi.org/10.1186/s40854-021-00256-y

- Kumar, N., & Sharma, S. K. (2017). Survey analysis on the usage and impact of whatsapp Messenger. Global Journal of Enterprise Information System, 8(3), 52–57. https://doi.org/10.18311/gjeis/2016/15741

- Lee, S. H., Leem, C. S., & Bae, D. J. (2018). The impact of technology capability, human resources, internationalization, market resources, and customer satisfaction on annual sales growth rates of Korean software firms. Information Technology and Management, 19(3), 171–184. https://doi.org/10.1007/s10799-018-0287-2

- Leledakis, G. N., & Pyrgiotakis, E. G. (2022). U.S. bank M&As in the post-Dodd–Frank act era: Do they create value? Journal of Banking and Finance, 135, 135. https://doi.org/10.1016/j.jbankfin.2019.06.008

- Liang, D., Ma, Z., & Qi, L. (2013). Service quality and customer switching behavior in China’s mobile phone service sector. Journal of Business Research, 66(8), 1161–1167. https://doi.org/10.1016/j.jbusres.2012.03.012

- Lymperopoulos, C., Chaniotakis, I. E., & Soureli, M. (2013). The role of price satisfaction in managing customer relationships: The case of financial services. Marketing Intelligence & Planning, 31(3), 216–228. https://doi.org/10.1108/02634501311324582

- Maali, B., Casson, P., & Napier, C. (2006). Social reporting by Islamic banks. Abacus, 42(2), 266–289. https://doi.org/10.1111/j.1467-6281.2006.00200.x

- Majeed, M. T., & Zainab, A. (2018). Sharia’h practice at Islamic banks in Pakistan. Journal of Islamic Accounting and Business Research, 9(3), 274–289. https://doi.org/10.1108/JIABR-03-2015-0011

- Makudza, F. (2021). Augmenting customer loyalty through customer experience management in the banking industry. Journal of Asian Business and Economic Studies, 28(3), 191–203. https://doi.org/10.1108/JABES-01-2020-0007

- Mansoor Khan, M., Ishaq Bhatti, M., & Mansoor Khan, M. (2008). Islamic banking and finance: On its way to globalization. Managerial Finance, 34(10), 708–725. https://doi.org/10.1108/03074350810891029

- Martins, R. C., Hor-Meyll, L. F., & Ferreira, J. B. (2013). Factors affecting mobile users’ switching intentions: A comparative study between the Brazilian and German markets. BAR - Brazilian Administration Review, 10(3), 239–262. https://doi.org/10.1590/S1807-76922013000300002

- Mbawuni, J., & Nimako, S. G. (2017). Determinants of Islamic banking adoption in Ghana. International Journal of Islamic & Middle Eastern Finance & Management, 10(2), 264–288. https://doi.org/10.1108/IMEFM-04-2016-0056

- Mir, R. A., Rameez, R., & Tahir, N. (2023). Measuring internet banking service quality: An empirical evidence. The TQM Journal, 35(2), 492–518. https://doi.org/10.1108/TQM-11-2021-0335

- Moosa, R., & Kashiramka, S. (2022). Objectives of Islamic banking, customer satisfaction and customer loyalty: Empirical evidence from South Africa. Journal of Islamic Marketing, 14(9), 2188–2206. https://doi.org/10.1108/JIMA-01-2022-0007

- Muafa, I. W., Awal, M., Wahyudhi, C. A., Waas, S., Noer, E., & Jusni, J. (2020). The effect of product quality and service quality on customer satisfaction in crocodile skin crafts industry. IOP Conference Series: Earth and Environmental Science, 473(1), 12028. https://doi.org/10.1088/1755-1315/473/1/012028

- Muhammad, T., & Bin Ngah, B. (2023). Mediating role of customer’s satisfaction on Jaiz bank products: A model development. Journal of Islamic Marketing, 14(1), 215–235. https://doi.org/10.1108/JIMA-08-2020-0241

- Newton, S. K., Nowak, L. I., & Kelkar, M. (2018). Defecting wine club members: An exploratory study. International Journal of Wine Business Research, 30(3), 309–330. https://doi.org/10.1108/IJWBR-06-2017-0038

- Nikhashemi, S. R., Valaei, N., & Tarofder, A. K. (2017). Does brand personality and perceived product quality play a Major role in mobile phone consumers’ switching behaviour? Global Business Review, 18(3_suppl), S108–S127. https://doi.org/10.1177/0972150917693155

- Novickytė, L., & Pedroja, G. (2015). Assessment of mergers and acquisitions in banking on small open economy as sustainable domestic financial system development. Economics & Sociology, 8(1), 71–87. https://doi.org/10.14254/2071-789X.2015/8-1/6

- Nowak, L. I. (1997). Partnering relationships between banks and their research firms: The impact on quality. International Journal of Bank Marketing, 15(3), 83–90. https://doi.org/10.1108/02652329710165993

- Ong, A. K. S., Prasetyo, Y. T., Kishimoto, R. T., Mariñas, K. A., Robas, K. P. E., Nadlifatin, R., Persada, S. F., Kusonwattana, P., & Yuduang, N. (2023). Determining factors affecting customer satisfaction of the national electric power company (MERALCO) during the COVID-19 pandemic in the Phillippines. Utilities Policy, 80, 101454. https://doi.org/10.1016/j.jup.2022.101454

- Paramita, W., Zulfa, N., Rostiani, R., Widyaningsih, Y. A., & Sholihin, M. (2021). Ethics support through rapport: Elaborating the impact of service provider rapport on ethical behaviour intention of the tourists. Journal of Retailing and Consumer Services, 63, 102693. https://doi.org/10.1016/j.jretconser.2021.102693

- Parasuraman, A. P., Zeithaml, V., & Berry, L. (1988). SERVQUAL: A multiple- item scale for measuring consumer perceptions of service quality. Journal of Retailing, 64, 12–40.

- Pardo, C., Pagani, M., & Savinien, J. (2022). The strategic role of social media in business-to-business contexts. Industrial Marketing Management, 101, 82–97. https://doi.org/10.1016/j.indmarman.2021.11.010

- Pollard, J., & Samers, M. (2007). Islamic banking and Finance: Postcolonial political economy and the Decentring of Economic Geography. Transactions of the Institute of British Geographers, 32(3), 313–330. https://doi.org/10.1111/j.1475-5661.2007.00255.x

- Pradeep, S., Vadakepat, V., & Rajasenan, D. (2020). The effect of service quality on customer satisfaction in fitness firms. Management Science Letters, 10(9), 2011–2020. https://doi.org/10.5267/j.msl.2020.2.011

- Prakash, G., & Srivastava, S. (2019). Role of internal service quality in enhancing patient centricity and internal customer satisfaction. International Journal of Pharmaceutical and Healthcare Marketing, 13(1), 2–20. https://doi.org/10.1108/IJPHM-02-2018-0004

- Rigdon, E. (2016). Choosing PLS path modeling as analytical method in European management research: A realist perspective. European Management Journal, 34(6), 598–605. https://doi.org/10.1016/j.emj.2016.05.006

- Rod, M., Ashill, N. J., & Gibbs, T. (2016). Customer perceptions of frontline employee service delivery: A study of Russian bank customer satisfaction and behavioural intentions. Journal of Retailing and Consumer Services, 30, 212–221. https://doi.org/10.1016/j.jretconser.2016.02.005

- Salleh, M. Z. M., Abdullah, A., Nawi, N. C., & Muhammad, M. Z. (2019). Assessing the service quality and customer satisfaction on Islamic banking by using SERVQUAL model. Research in World Economy, 10(2), 79–83. https://doi.org/10.5430/rwe.v10n2p79

- Saqib, L., Farooq, M. A., & Zafar, A. M. (2016). Customer perception regarding Sharī‘ah compliance of Islamic banking sector of Pakistan. Journal of Islamic Accounting and Business Research, 7(4), 282–303. https://doi.org/10.1108/JIABR-08-2013-0031

- Schuster, L. (1996). Quality management in banking. Finance a Uver - Czech Journal of Economics and Finance, 1996(8), X4–490. https://www.scopus.com/inward/record.uri?eid=2-s2.0-3743130918&partnerID=40&md5=825dc74f045835d07955ed338e4a21de

- Senthil, B. (2022). Impact of service quality on customers’ satisfaction towards remote banking: A study in Rural Tamil Nadu1. Finance India, 36(4), 1419–1428. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85146754112&partnerID=40&md5=d5dd361b5f0ea732cc0992ca41cff162

- Sharma, A., & Sharma, R. R. K. (2018). Consumer switching behavior in E-services: Organizational and technological antecedents through relational paradigm. Proceedings of the International Conference on Industrial Engineering and Operations Management, 1052–1061. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85051456319&partnerID=40&md5=40fededb38670c42e4be01547690822e

- Sindwani, R. (2018). Technology-based self-service banking quality dimensions, customer satisfaction, and loyalty: Linkages and implications for management. Advances in E-Business Research Series, 139–159. https://doi.org/10.4018/978-1-5225-5026-6.ch007

- Singh, J., Srivastava, S., Sharma, S., Nath, S., & Karmakar, A. (2016). Customer perception of e-service quality in online travel companies in India. International Journal of Applied Business and Economic Research, 14(7), 5245–5254. https://www.scopus.com/inward/record.uri?eid=2-s2.0-84986208324&partnerID=40&md5=7e3efa14e78672841285924e7d904a9a

- Sipayung, M. E. B., Bakhtiar, A., & Handayani, N. U. (2021). Study of the effect of service quality toward customer loyalty with customer satisfaction in financial service industry at pt bank Rakyat Indonesia (Persero) TBK at CEPU branch as an intervening variable. IEOM Society. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85121149560&partnerID=40&md5=e9695b78c6899ad3b4fc1e6e7116894c

- Srivastava, K., & Sharma, N. K. (2013). Service quality, corporate brand image, and switching behavior: The mediating role of customer satisfaction and repurchase intention. Services Marketing Quarterly, 34(4), 274–291. https://doi.org/10.1080/15332969.2013.827020

- Sulaiman, Y., Jamil, N. A. M., Othman, A. R., & Musa, R. (2020). The influence of green marketing, syariah compliance, customer’s environmental awareness and customer’s satisfaction towards Muslim consumer purchasing behaviour in kedah. WSEAS Transactions on Business and Economics, 17, 195–204. https://doi.org/10.37394/23207.2020.17.21

- Szopiński, T. (2021). Impact of consumer awareness on switching behavior in banking. Contemporary Economics, 15(4), 467–478. https://doi.org/10.5709/ce.1897-9254.461

- Tahtamouni, A. (2022). E-banking services and the satisfaction of customers in the Jordanian banks. Journal of Science and Technology Policy Management, 14(6), 1037–1054. https://doi.org/10.1108/JSTPM-06-2021-0082

- Taoana, M. C., Quaye, E. S., & Abratt, R. (2022). Antecedents of brand loyalty in South African retail banking. Journal of Financial Services Marketing, 27(2), 65–80. https://doi.org/10.1057/s41264-021-00111-2

- Taylor, H. (2000). Does internet research work? Comparing online survey results with telephone survey. Journal of the Market Research Society, 42(1), 1–11. https://doi.org/10.1177/147078530004200104

- Thaichon, P., Lobo, A., & Mitsis, A. (2014). An empirical model of home internet services quality in Thailand. Asia Pacific Journal of Marketing & Logistics, 26(2), 190–210. https://doi.org/10.1108/APJML-05-2013-0059

- Thaichon, P., Quach, S., Bavalur, A. S., & Nair, M. (2017). Managing customer switching behavior in the banking industry. Services Marketing Quarterly, 38(3), 142–154. https://doi.org/10.1080/15332969.2017.1325644

- Tri, T. M., & Anh, N. P. (2020). Effect of bank merger on efficiency using stochastic frontier analysis: The case of vietnam. Journal of Critical Reviews, 7(16), 320–329. https://doi.org/10.31838/jcr.07.16.39

- Uchino, T., & Uesugi, I. (2022). The effects of a megabank merger on firm-bank relationships and loan availability*. Journal of the Japanese and International Economies, 63, 101189. https://doi.org/10.1016/j.jjie.2021.101189

- Ueno, A., Sharma, P., & Kingshott, R. P. J. (2018). Exploring the impact of self-service technologies on retail shoppers: An abstract. In Developments in Marketing Science: Proceedings of the Academy of Marketing Science (p. 167). Springer Nature. https://doi.org/10.1007/978-3-319-99181-8_53

- Ullah, S., & Lee, K. (2012). Do customers patronize Islamic banks for Shari’a compliance? Journal of Financial Services Marketing, 17(3), 206–214. https://doi.org/10.1057/fsm.2012.18

- Uppal, R. K. (2022). E-Services in banks customer perception-level of awareness and Consumer protection in E-Age. Finance India, 39(4), 1429–1440. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85146774651&partnerID=40&md5=f147a35256d44f5ae8ba9a9c8470d23e

- Usman, H., Projo, N. W. K., Chairy, C., & Haque, M. G. (2022). The exploration role of Sharia compliance in technology acceptance model for e-banking (case: Islamic bank in Indonesia). Journal of Islamic Marketing, 13(5), 1089–1110. https://doi.org/10.1108/JIMA-08-2020-0230

- Usman, H., Tjiptoherijanto, P., Balqiah, T. E., & Agung, I. G. N. (2017). The role of religious norms, trust, importance of attributes and information sources in the relationship between religiosity and selection of the Islamic bank. Journal of Islamic Marketing, 8(2), 158–186. https://doi.org/10.1108/JIMA-01-2015-0004

- Vinzi, V. E., Trinchera, L., & Amato, S. (2009). Book cover handbook of Partial least squares pp 47–82Cite as PLS path modeling: From foundations to recent Developments and open issues for model assessment and improvement. Springer Handbooks of Computational Statistics.

- Vyas, V., & Raitani, S. (2014). Drivers of customers’ switching behaviour in Indian banking industry. International Journal of Bank Marketing, 32(4), 321–342. https://doi.org/10.1108/IJBM-04-2013-0033

- Wiryawan, D., Suhartono, J., Hiererra, S. E., & Gui, A. (2022). Factors affecting digital banking customer satisfaction in Indonesia using D&M model. Institute of Electrical and Electronics Engineers Inc. https://doi.org/10.1109/CITSM56380.2022.9935928

- Wong, K. (2013). Partial least square structural equation modeling (PLS-SEM) techniques using SmartPLS. Marketing Bulletin, 24(1), 1–32.

- Yalcinkaya, B., & Just, D. R. (2023). Comparison of customer Reviews for Local and Chain Restaurants: Multilevel approach to Google Reviews data. Cornell Hospitality Quarterly, 64(1), 63–73. https://doi.org/10.1177/19389655221102388

- Yongho Hyun, M., Kim, H.-C., & O’Keefe, R. M. (2014). Inter-satisfaction between website and automated call distribution (ACD) Systems. Journal of Travel & Tourism Marketing, 31(8), 1039–1056. https://doi.org/10.1080/10548408.2014.892467

- Zhao, C., Noman, A. H. M., & Asiaei, K. (2022). Exploring the reasons for bank-switching behavior in retail banking. International Journal of Bank Marketing, 40(2), 242–262. https://doi.org/10.1108/IJBM-01-2021-0042

- Zhao, C., Noman, A. H. M., & Hassan, M. K. (2023). Bank’s service failures and bank customers’ switching behavior: Does bank reputation matter? International Journal of Bank Marketing. https://doi.org/10.1108/IJBM-07-2022-0287 41 3 550–571

- Zulfitri, S., & Rohman, F. (2019). The influence of price perception, service quality and variation behavior on electronic banking. International Journal of Economics & Business Administration, 7(1), 183–200. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85062258362&partnerID=40&md5=65badfd938f7e3e3bed43a9cea37f28e

- Zyberi, I., & Luzo, D. (2022). The relationship between satisfaction, trust and loyalty in electronic banking. Finance: Theory and Practice, 26(2), 104–117. https://doi.org/10.26794/2587-5671-2022-26-2-104-117