Abstract

This study explores the accountants’ (academic, auditor, and attorney) perspective on tax amnesty to enhance tax compliance dimensions in a slippery slope framework in Indonesia. Data were extracted by interviewing accountants, and the manuscripts analyzed from three perspectives, namely values, governance, and prosperity, to ground the values of the Pancasila Ideology in fundamental tax strategy. The behavior of taxpayers participating in Tax Amnesty (TA) and the Voluntary Disclosure Program (VDP) is a rational choice from the perspective of values in terms of the value of economic benefits. Accountants’ views from values, governance, and prosperity perspectives are that TA and VDP have not been able to improve long-term compliance; therefore, a derivative policy is required after TA and VDP. It is highly recommended to develop a policy for tracking assets reported in the TA and VDP as potential future taxes, not by developing a similar policy in the form of tax amnesty. The novelty of this study lies in the formulation of fundamental sincerity values, balancing governance, and a sustainable prosperity viewpoint within the extended slippery slope framework.

1. Introduction

The two dimensions that shape tax compliance in the slippery slope framework tax compliance model introduced by Kirchler et al. (Citation2008) are trust and power. Ritsatos (Citation2014) states that the slippery slope framework tax compliance model is currently the most comprehensive. Various studies have tested the slippery slope framework tax compliance model using different approaches (Agusti & Rahman, Citation2023; Darmayasa & Hardika, Citation2024; Gangl et al., Citation2015; Kastlunger et al., Citation2013; Kogler, Batrancea et al., Citation2013; Lozza et al., Citation2013; Nurkholis et al., Citation2020; Prinz et al., Citation2014). In addition to testing the two dimensions of trust and power, the characteristics of taxpayers in the trust dimension are of concern to researchers (Darmayasa et al., Citation2022; Haning et al., Citation2019; Janas & Oljemark, Citation2021; Sudarma & Darmayasa, Citation2017). The two dimensions that form tax compliance can be translated into a tax amnesty policy, which is manifested in the authority of the tax authority to grant tax amnesty, while trust is realized through taxpayer participation in the tax amnesty policy.

Tax amnesty is a strategic policy adopted by a country when it experiences a decline in revenue from the tax sector and tax compliance is still low (Keen & Slemrod, Citation2017; Slemrod, Citation2019). However, not all tax amnesty policies can achieve these goals. The short-term goal of increasing tax revenue is more realistic (Alm et al., Citation2009; Sayidah & Assagaf, Citation2019). Interestingly, the goal of increasing tax compliance has not been optimally achieved through the 2018 tax amnesty policy (Darmayasa et al., Citation2016, Citation2017; Nuryanah & Gunawan, Citation2022). In fact, the tax amnesty policy in Zimbabwe between 2014 and 2018 has not been able to achieve the goal of increasing tax revenue and compliance (Marire & Sunde, Citation2012; Wadesango et al., Citation2020).

Indonesia’s tax amnesty policy is divided into three: the sunset policy in 2008, the tax amnesty (TA) from 2016 to 2017, and the voluntary disclosure program (VDP) in 2022. Based on the tax authority’s publication, additional state revenue from TA in 2016-2017 amounted to 146 trillion Rupiah. However, there are differences in taxpayers’ asset reports between the 2018 Annual Tax Return and Automatic Exchange of Information data, indicating that post-TA tax compliance is not optimal. From the perspective of the tax authority, the 2016-2017 tax amnesty is claimed to have been able to increase tax revenues (Ibrahim et al., Citation2017; Sayidah & Assagaf, Citation2019), whereas the dimension of increasing compliance can only increase individual taxpayer compliance (Nuryanah & Gunawan, Citation2022). From the perspective of taxpayers, individual taxpayers who participate in a tax amnesty program are more likely to maximize the utility of the policy (Darmayasa, Citation2017, Citation2019; Darmayasa et al., Citation2018; Hamilton-Hart & Schulze, Citation2016; Wadesango et al., Citation2020). On the other hand, the perception of trust cannot encourage taxpayers to comply (Inasius, Citation2019). Looking at the various research results, there is a state of the art regarding the behavior of taxpayers who participate in tax amnesty policy, starting from deterrence economics, the theory of planned behavior, attribution theory, and the long-run effect. However, this study has not been able to describe the behavior of taxpayers who participate in the tax amnesty policy within the framework of the slippery slope compliance model, which is supported by various theories of taxpayer behavior. There is a tendency for taxpayers to avoid tax authorities and choose to utilize the services of tax practitioners who are more comfortable discussing such matters (Frecknall-Hughes et al., Citation2023). Therefore, accountants who have played a role in helping taxpayers from the perspective of a compliance model that includes values, governance, and prosperity need to be studied further.

Philosophically, tax amnesty in Indonesia is based on the Pancasila ideology as stated in academic texts, which seeks to ground the philosophical value of tax amnesty through the values contained in Pancasila, namely values, government, and prosperity (Darmayasa et al., Citation2017). Values are defined as the fundamental meaning of tax amnesty, government is defined as the management of tax amnesty implementation, while prosperity is the goal of tax amnesty (Latif, Citation2018). In practice, the involvement of accountants with the slippery slope framework model approach can encourage compliance, through the perspective of the extended slippery slope framework and from the perspective of providing forgiveness to taxpayers.

This study seeks to close this research gap by presenting the roles of academics, auditors, and attorneys from a tax compliance model perspective. Separately, accountants contribute to preparing financial reports (El Aboudi & Khanchaoui, Citation2020), auditors play a strategic role through professional audit services for financial reports (Ahmar, Citation2018), and attorneys contribute to providing professional tax services (Frecknall-Hughes et al., Citation2023; Hermawan et al., Citation2020; Mangoting et al., Citation2019; Mashiri et al., Citation2021). Previous research looked more at the effectiveness of policies from TA and VDP results and subsequent compliance conditions but did not examine the role of accountants in each TA and VDP program process. The novelty of this study is based on a new perspective, which is a relevant contribution. Three points of view – values, governance, and prosperity –used to ground the values of the Pancasila ideology in fundamental tax strategy is a new approach that is suitable in the Indonesian context. The presence of a fundamental basis from the perspective of value, governance, and prosperity in balancing the dimensions of the power and trust in the extended slippery slope framework is important and urgent for enhancing tax compliance.

2. Literature review

2.1. Tax amnesty

Tax amnesty is widely used by countries to overcome a decline in tax compliance (Alm et al., Citation2009; Keen & Slemrod, Citation2017) and the program has recently been used to increase short-term tax revenues in situations such as the Covid-19 pandemic (Darmayasa & Hardika, Citation2024; Darmayasa & Partika, Citation2024; Pogorletskiy & Söllner, Citation2020). Ideally, the tax amnesty policy should not be implemented routinely and over short periods of time because, if not, it can lead to good compliance behavior decreasing again (Sudarma & Darmayasa, Citation2018; Torgler & Schaltegger, Citation2005). Tax abundance in Indonesia can be classified into soft amnesty in 2008 and hard amnesty in 2016 (Phase 1) and 2022 (Phase 2) (Darmayasa, Citation2019; Hasanah et al., Citation2021).

2.2. Tax compliance model

Tax compliance created from policy evaluation was determined by adopting the compliance model. The SSF tax compliance model is the most widely applied, considering that the balanced dimensions of power and trust can form long-term compliance (Kirchler et al., Citation2008; Kogler et al., Citation2023). TA and VDP strategic policies require a different perspective regarding the conditions of taxpayers who prioritize rationality when participating in TA and VDP programs (Darmayasa et al., Citation2022; Darmayasa & Hardika, Citation2024). Academic accountants, auditors, and attorney accountants who contribute to the implementation of TA and VDP need to be considered in encouraging tax compliance in the existing SSF model.

2.3. Extended slippery slope framework

The SSF model has become a reference for various countries in developing policies to increase taxpayer compliance (Kogler et al., Citation2023; Ritsatos, Citation2014). The SSF model consists of two dimensions, namely power and trust (Kirchler et al., Citation2008; Kogler, Muehlbacher et al., Citation2013). The power dimension that dominates, namely government centered, tends to create forced obedience and, if trust dominates, it will form obedience that lasts in the long term (Darmayasa, Citation2017; Darmayasa et al., Citation2022). However, in the tax amnesty policy, it can be seen that the role of power is more dominant through its authority to provide forgiveness to taxpayers. The extended SSF model seeks to balance the power of the tax authority through fair policies so that the trust of taxpayers continues to grow, leading to honest tax payments that do not necessarily wait for the tax amnesty policy.

3. Methods

3.1. Research paradigm

This research is of a qualitative nature with an interpretive approach from an accountant’s perspective through the perspective of values, governance, and prosperity. The values, governance, and prosperity perspectives are the values contained in Pancasila as a source of rules and regulations, not limited to tax provisions. As strategic tax policies, TA and VDP must comply with the values of Pancasila. Internalizing Pancasila values using the values, governance, and prosperity perspectives in a policy in keeping with the approach taken by Latif (Citation2018). This study also uses the methodological guidance of Cresswell and Poth (Citation2018) and Miles et al. (Citation2019), the former greatly influencing the type of data needed, while the latter’s ideas are applied to the interaction model of data collection, presentation, and conclusions to recollect data if needed.

3.2. Research informants

The objective of this study is to examine TA policy and VDP from the perspective of strategic tax policy as a translation of the strength or power of the tax authority, which is responded to by taxpayer trust as forming tax compliance in the extended slippery slope framework model. Research informants’ perspectives on TA policy and the VDP program regarding tax compliance are the main objectives of the policy. The research informants began with Mr. Yudi Latif, who initiated the ideas of values, governance, and prosperity. From an accountant academic perspective, this study involved three accountants who actively researched and conducted outreach in the form of tax webinars. This research involves three accountants’ attorneys (tax practitioners), who provide professional services on a daily basis, especially to clients who participate in TA and VDP. This research also involved three auditors who audited auditees who participated in TA and VDP.

Exploring the views of research informants uses an interview guide that can develop as the interview progresses and that remains in a natural setting. The interview guide is divided into three outlines according to three points of view, – values, governance, and prosperity– to ground the values of the Pancasila ideology in a fundamental tax strategy. The first guide to taxpayer behavior responds to TA and VDP strategic policies while the second involves governance for implementing TA and VDP strategic policies based on the dimensions of power and trust. In the third guide, the objective of TA and VDP is to enhance tax compliance in the extended slippery slope framework.

The researcher is the key instrument of this research, and all of the researcher’s knowledge and experience are expressed in understanding the views of all informants in the form of contemplation of the researcher’s intuition. Researchers have closeness (report cards) with all informants, so they can obtain primary data through interviews in natural settings. Considering that this study only captures the implementation of TA and VDP from the perspective of accounts that help technically and educate taxpayers, it does not include tax authorities as research informants. A list of informants with their names, roles and views is presented in .

Table 1. List of research informants.

3.3. Data analysis

The interpretive analysis technique in this research was developed from Cresswell’s guidelines, in which interpreters view dynamic social reality full of subjective meaning as a synthesis of social construction with the assumption that society has an intentional human being (Cresswell & Poth, Citation2018). Considering that the social reality in this research is taxpayer compliance after TA and VDP as seen from the SSF tax compliance model, the interpretive analysis uses the values, governance, and prosperity of Pancasila values. The stages of data analysis techniques are: 1) data collection (in-depth interviews and observations), complete with data triangulation; 2) data reduction, which forms the themes of accountants’ views; 3) presenting new meaning through values, governance, and prosperity; and 4) compiling research conclusions that answer the research questions.

4. Results and discussion

Related searches on the tax compliance model led to research results by Kirchler et al. (Citation2008), who first introduced the slippery slope framework. The slippery slope framework integrates the theory of psychological contracts, tax morals, trust in organizations, motivation crowding, and social effects into a tax compliance model framework (Ritsatos, Citation2014). Broadly speaking, the slippery slope framework combines the economic and psychological perspectives. The slippery slope framework is formed into two dimensions: power and trust. In the model, taxpayers are assumed to understand and respond to the regulations. The compliance realized in the model is divided into enforced compliance (prioritizing power) and voluntary compliance (prioritizing trust). The power dimension is perceived as the tax authority’s capacity to detect and punish tax-evaders. The trust dimension includes social psychology through the clarity and ease of following the tax provisions.

In the Discussion section, the accountants’ point of view is described, starting from values, governance, and prosperity. The value perspective explores informants’ views from the perspective of the values contained in TA and VDP strategic policies. The perspective is not limited to policy values that can be developed from the perspective of taxpayers who participate in TA and VDP. The governance perspective explores the views of accountant informants at the level of implementation of tax authority power and taxpayer trust in TA and VDP strategic policies within the extended slippery slope framework.

The prosperity perspective explores accountants’ views at the level of usefulness of TA and VDP strategic policies. At the end of the discussion, the essence of the research results is presented from three perspectives: values, governance, and prosperity as a fundamental strategic TA and VDP.

4.1. The values point of view

The point of view of values was used to examine the sharpness of informants’ views from a value perspective, which explores the views of accountant academics who are taxation researchers. The following is Mrs. Damayanti’s view of TA fairness as a professor of taxation:

… Prior to the implementation of the TA in 2016, in 2015 the Taxpayer Development Year (TPWP) was implemented so that taxpayers who had participated in TPWP felt disappointed because they had corrected their tax returns with the consequence of paying more tax than the TA. In addition, taxpayers who have participated do not receive special treatment when participating in the TA. Therefore, fairness in the implementation of TA is less considered.

To deepen the analysis of the values point of view, the researcher turned to the views of other accounting academics. Researchers had the opportunity to interview directly several times to improve the data quality through time triangulation. The following are Mr. Pratama’s views regarding implementation of the Indonesian Accountants Association Financial Accounting Standards (accounting standard taskforce) and accountant academics:

…So, the point is how to get the funds that are outside to come back to us again. Yes, if we at that time gave a high tax rate or ransom rate, they would not want it. So, at that time, we forced the ransom rate to be low. If they must use fair value, they will have to use appraisal services to measure the fair assets, there is another cost. Maybe they think it’s complicated, ‘I don’t want to do that’. So, at that time, when they were in the TA, finally, please use the taxpayer’s version of value. Well, when the VDP is not anymore, because of what, when the VDP is, I think the political motive has been somewhat reduced. So, if the VDP can be said that there is no political motive. In 2016, the political motive was very high.

…Because the TA has its own law and its own mechanism, and the government at that time also learnt from the mistakes of the second sunset policy, the revaluation of assets. The failure of the asset revaluation at that time was that the revaluation had to be carried out in accordance with accounting guidelines, using accounting standards. It turns out that the accounting provisions are complicated, so what? Many did not want to participate, because ‘it’s very complicated, I want to revalue my assets’.

Other views were explored by accountant academics, who are very active in various tax provision socialization activities, both as resource persons and moderators. It is important for researchers to explore the views of other accountant academics in addition to accounting academic professors in taxation and accounting standard taskforce accountant academics by interviewing other academic sources who are active in the socialization of tax policies. Due to distance constraints, the researcher decided to interview Mrs. Tjen through Zoom media, which was further confirmed when Mrs. Tjen moderated an international tax conference that took place in Bali:

…If we talk about fairness, maybe it doesn’t fulfil fairness, because for example, if you look at it like that, people who have paid their taxes, what is open, they are already compliant, they are not compliant. But this is not compliant given a lower rate, right compared to those who are compliant, compliant has paid, for example, he paid 22% or 20% first, for example, well that’s 25% first, for example. But at the time of our TA, he will only pay a low ransom so maybe from the point of view of ‘Is it fair, maybe someone will protest, it’s not fair’. But he fulfils simplicity maybe yes, ‘let’s just pay this much if we want to be honest’. It’s simple but not fair in my view like that because it’s a bit difficult for clients.

The values point of view from the accountant academic perspective focused on the main influence of the government center, negating fair value, and prioritizing simplicity over fulfilling a sense of fairness. Further exploration of the views was conducted with attorneys to strengthen data quality through source triangulation. Exploring the views of the accountant attorney began with Mr. Ysa’s views on the TA and the VDP’s fairness aspects:

…If we talk about authority oh this is fair, why? because there is a rate that you have to pay when you are forgiven the amount of information you have to pay. It should be noted for my friends in this case are taxpayers who say ‘I have complied, I have fulfilled all my obligations’ will be very, very biased for me when I say this is fair for everyone, it will be biased like that. Because there are those who feel compliant who have fulfilled their obligations in accordance with what they have to pay, but on the other hand the government opens a gap for those of you who have not complied, come to me, our government will forgive you but with certain conditions.

Mr. Ysa also provided another view regarding the interesting aspects of fairness in VDP behind the views obtained by the previous researcher, as follows:

…Why? Yes, because when the complaints are put aside, once again I try to stand in the middle, not talking to the taxpayer, not seeing from the authority side. Now that this VDP exists, the interesting thing is that as I said earlier, the tariff goes up, scheme 2 or scheme 1, and the interesting thing is that when we don’t participate in TA, the assets are now traced from 1985 to 2016 and then 2017-2020.

In the prospect theory framework, Kahneman and Tversky (Citation1979) describe taxpayers’ rational choices for behavior, referring to judgments (beliefs) and choices (Pan, Citation2019; Ritsatos, Citation2014). This neoclassical economic model illustrates that, in an economic activity, there is a role for individual participation in the form of behavior that contains beliefs, norms, cultures, and social interactions. In social interaction, there is a discipline of sociology on individual behavior, whereas psychology is more related to individual sentiments and beliefs. Sociology and social psychology are described by their preferences for rational behavior.

Auditors’ views complement the values of various academics and attorneys. The auditors’ view is that taxpayers who participated in TA and VDP previously received enlightenment from accountant academics and assistance from an accountant attorney when it was time for an accountant auditor to audit. Starting with the accountant auditors’ view on value point of view, researchers obtained information from Mr. Budi, an accountant auditor, who has a career track as the founder of an accounting firm. Mr. Budi’s view of the fairness aspect of the VDP is as follows:

…So, from the implementation of the policy, it does focus on tax evaders, sir. Whether it is in the country or abroad, the realm of fairness arises, that’s why the neutrality applies to those who have not reported their assets and income, whether overseas assets or domestic assets. That’s why there are two schemes, scheme one has two sub-schemes, overseas assets, domestic assets. Policy scheme two also has sub-schemes, overseas assets, domestic assets, well this. But when we compare those who have complied and those who have not complied here unfairness arises.

…Yes, every long policy must be based on a principle. It’s just a matter of which principle you want to priorities under different conditions or revenue productivity. Because what is highlighted is revenue productivity, not fairness. Yes, that’s right because when there is a policy, it is often not often possible that sometimes one principle and another principle contradict each other. Yes, the principle of revenue productivity and fairness. In the end, rational choice theory emerged, a theory that exists in politics used in decision-making theory, which is the most rational.

Moving on from the accountant auditors’ perspective after taxpayers have received enlightenment and assistance in carrying out tax obligations, the researcher obtained another view from the same perspective on the VDP strategic policy, which focuses more on taxpayers who are indicated to have committed tax evasion. Taxpayers who commit tax evasion automatically become non-compliant taxpayers. Researchers try to describe the behavior of non-compliant taxpayers with the theory of tax morale (Alm et al., Citation1992; Alm & Beck, Citation1993; Khozen & Setyowati, Citation2023; Sutrisno & Dularif, Citation2020; Torgler, Citation2003); rational taxpayers become non-compliant since they are not detected and are not subject to sanctions, which has been happening for a long time and can be explained by the theory of economic deterrence. Ritsatos (Citation2014) states that Allingham and Sandmo’s research results were the first to describe taxpayers’ decisions to evade from an economic perspective.

Alm et al. (Citation1992) predicted that most rational taxpayers will be non-compliant because they are not detected and there are no sanctions. Alm et al. (Citation1990) examined social norms and social psychology to explain taxpayers’ economic behavior. Torgler (Citation2003) constructed two combinations of economic and social theories to provide a comparative definition of tax morality. Alm and Torgler (Citation2006) found that direct democracy and religiosity positively influence the level of tax morale. Similar research findings confirm that tax morale is influenced by factors such as voice accountability, political stability, government efficiency, regulatory quality, the rule of law, and control of corruption.

The behavior of taxpayers who prioritize rationality can also be explained by various taxpayer theories ranging from economic deterrence, and tax morale combined into a strategic policy referring to the slippery slope framework (Darmayasa et al., Citation2022; Kirchler et al., Citation2008;Ritsatos, Citation2014). Developing a strategic tax policy needs to consider taxpayers with good morals, whose level of tax compliance is not influenced by economic conditions (Cahyonowati et al., Citation2023; Hartmann et al., Citation2022). Reflecting on the two dimensions of the slippery slope framework, it seems that the TA and VDP policies emphasize more on power authority in the form of formulating strategic revenue productivity policies rather than fairness; as such, the TA and VDP strategic policies do not fully comply with this tax collection principle advanced by Adam Smith (Glaze, Citation2015; Inasius, Citation2019; Smith, Citation2014).

The perspective of accountant auditor Mr. Budi is the first step for researchers to explore new views from other accountant auditors to enrich the accountant auditors’ perspective on TA and VDP values. The researcher conducted an interview directly with Mr. Nugraha, a taxpayer auditor who participated in TA and VDP, both individual and corporate, as follows.

…The fairer one is in VDP, but the tariff is expensive. If it’s Tax Amnesty, the taxpayer will deliberately redeem it at a low price, so he won’t be audited. The TA benefits the taxpayer. In VDP, it is the tax office that benefits. Even then, they can refuse to participate in the VDP, if it turns out that the data is wrong, they can just correct the tax return.

Continuing the values point of view from the perspectives of accountant academics, accountant attorneys, and accountant auditors, the VDP principle of fairness is realized by setting a higher tax rate when compared to TA. The strategic policy of TA is utilized by taxpayers to avoid audits and preferring to pay ransom. The taxpayers’ decision to pay ransom is the behavior of taxpayers who prioritize rationality as a speculative action. The behavior of choosing a lower risk when a taxpayer’s strategic policy is available can also be explained by a combination of economic and psychological perspectives. In every taxpayer’s action to respond to strategic policies, the TA and VDP policies contain economic aspects in the sense of paying income tax rates to obtain amnesty, influenced by taxpayer psychology in making decisions.

Like putting together, a puzzle, the values point of view of a strategic tax policy for TA and VDP involves accountants (academic, auditor, and attorney), which leads to taxpayer behavior in responding to the tax authority’s strategic policy. Accountant academics, auditors, and attorneys have the same view of the quality of the values point of view, which is the main view of the Pancasila ideology, in this case that divinity is not fully translated into policy, considering that strategic policies are loaded with values, namely, the materiality of revenue from the tax sector. The value of fairness as one of the precepts in the Pancasila ideology is not the main factor considering the characteristics of taxpayers, which can be explained by the theories of economic deterrence, neoclassical economics, tax morale, slippery slope framework, and Adam Smith’s tax collection principles, which favor the simplicity of implementing strategic policies.

Economic deterrence states that taxpayers prefer to postpone their tax obligations by considering the probability of imposing the next sanctions. This is in accordance with the response of taxpayers who take economic action to pay ransoms to reduce the probability of imposing subsequent sanctions. However, this behavior is influenced by the moral conditions of each taxpayer. Comprehensively, various taxpayers can be described in two dimensions within a slippery slope framework. However, only the power enforcement dimension appears to dominate TA and VDP policy implementation. The point of view of values is not sufficient to provide insight into TA and VDP strategy policies; further analysis is needed from a governance point of view.

4.2. The governance point of view

The governance perspective is the second point of view previously used to ground the philosophical foundation of strategic taxation policies. According to Latif (Citation2018), the results of a discussion in a direct interview are appropriate for criticizing the governance of strategic taxation policies toward policies that provide prosperity to all taxpayers.

Exploring views from the governance perspective begins with the role of accounting academics in the economy. The Institute of Indonesia Chartered Accountants Congress affirmed that accountant academics are catalysts of the economy, as compilers of financial statements. Mrs. Damayanti’s view of accountant academics is well-recognized by researchers on the role of accountant academics as catalysts of economic growth.

…Of course, with various academic inputs that are meaningful to decision makers, it will be able to accelerate economic growth. Of course, the assistance provided can accelerate economic growth. Economic growth is not only produced by one or two parties but by several parties including accountant educators and professional consultants. Therefore, synergy is needed to create economic growth.

Complementing Mrs. Damayanti’s view, Mr. Pratama expressed another view regarding accountant academics as catalysts:

…Yes, in principle, the accounting function is not a guardian of governance in the long term or maybe indirectly we must have contributed to economic growth, right. But, if we say that we are a catalyst in a direct sense, this seems impossible too, right? Why? Because yes, we are micro, right, we are the accountant profession, yes, it’s okay that we have a contribution, but yes, if we pay attention to the Financial Services Authority (OJK), they see us as a supporting profession in the capital market, not the main profession, yes, so we are supporting activities in the capital market but yes, we are supporting, supporting. So, it’s not direct.

Mrs. Damayanti’s view of accountant academics is slightly different from that of Mr. Pratama, who emphasizes the importance of synergy from stakeholders in creating economic growth. However, Mr. Pratama sees the role of accountant academics not directly but only as a supporting profession. Referring to the results of research by El Aboudi and Khanchaoui (Citation2020) accountants play a role in preparing financial reports. Thus, it is logical that the roles and synergies of other professionals are needed.

Mr. Pratama also provided another view of catalyzing economic growth through the participation of professional consultants, as follows:

…Yes, the point is that tax must still be the main source of revenue, we don’t have other main sources, except for tax, which is sustained only by tax. Now in my opinion, the problem is that our tax ratio is still low. Yes, now it’s even going downright, because yes, we’ve spoiled it too much with TA, VDP program, which if researched are proven not to increase the tax ratio in the long run, right. In fact, to increase the long-term tax ratio, it is indeed law enforcement and on the one hand reform of the tax structure.

…If for example it helps, yes, it will help, depending on what the role is, for example, if I am an educator accountant, the role is to provide education, provide education to the public to students through webinars, if for example there are thousands of people participating, it means that it helps the government also to educate the public.

Continuing the governance point of view that the role of accountant academics is not directly related to economic growth, Mr. Pratama argued that tax revenue is a more tangible contributor to economic growth. Mr. Pratama believes that the most sustainable source of state revenue is the taxation sector. His recent criticism is that the tax ratio has decreased because of TA and VDP policies that spoil taxpayers. Mrs. Tjen, who is active in various seminars as both a moderator and resource person, always invites participants (taxpayers) to participate in TA and VDP policies. Her role as an accountant academic from an educational perspective is her concern for increasing the tax ratio.

Complementing the views of previous informants, the researchers obtained the views of Mr. Partika as another accountant attorney regarding the role of professional accountants as catalysts for economic growth:

…As a tax consultant, I still behave properly to be safe. Tax consultants are educating too. That’s why if there are more tax consultants, the better the country will be, the more helpful it will be. Yes, it’s not allowed to be political either, what is it called providing misleading solutions that violate the law.

As in the first stage of the point-of-view analysis, to ground the ideology of Pancasila in the strategic policies of TA and VDP also provides views from various accountant academic informants and accountant attorneys from a governance perspective. From a governance perspective, accountants are catalysts or economic drivers; however, they also indirectly affect economic growth. More precisely, both accountant academics and accountant attorneys become agents of change or accountants who provide professional and educational services indirectly, which will change the taxpayer’s perspective on the strategic policies of TA and VDP, so that compliance is expected to increase. The governance point of view should be an input for various parties, be it the association in this case the Institute of Indonesia Chartered Accountants or the tax authority to provide space for accountant academics and accountant attorneys to make a real contribution to increasing taxpayer awareness of strategic policies that ultimately increase tax compliance. This section also reinforces that additional professional tax consultants are needed to provide education and space for accountant academics in making strategic policies to criticize the policies that are managed so as to achieve increased compliance that does not necessarily increase tax revenue in the short term. To complete this perspective, a prosperity perspective is presented in the next review.

4.2.1. The prosperity point of view

The prosperity point of view is the final stage of grounding the values of the Pancasila ideology in the strategic policies of TA and VDP. From a prosperity perspective, TA and VDP strategic policies should provide benefits to improve the prosperity of the community in accordance with the fifth principle of Pancasila. The TA and VDP strategic taxation policies contain philosophical, juridical, and sociological principles. The prosperity perspective relates to the sociological aspects of TA and VDP policies. Exploring views from the perspective of prosperity involves the views of academic and auditors. The exploration of these views began with Mrs. Damayanti and continued with Mr. Pratama’s views.

Mrs. Damayanti views:

…Both TA and VDP are normatively able to create tax compliance. However, TA that is repeated in various studies will create tax non-compliance. Therefore, we must be careful in developing government program related to TA or VDP.

…Personally, I think the TA should be done in a non-frequent manner. We can see in local taxes, why motor vehicle tax or land and building tax never have high compliance, because the local government always gives bleaching, and the bleaching is predictable. Every three years, there will be a change of government or when there is an election, there will be bleaching. That’s why, if I say so, it will fail. Yes, people will hold back, why? Because ‘there will be bleaching anyway’ plus the law enforcement in local taxes is not good. Well, I don’t know, but I also see that after the tax amnesty is completed, what should be improved next is law enforcement.

…If I look at it again, it is because this VDP is not meant to be an image tool. So, this VDP is to create natural, long-term compliance. So, if it is reported, it will be misleading, people will think that this is the same as TA. The achievement will not be as good as TA, I’m sure, if you compare TA, it was only nine months, but it was successful, like that. We are said to be the most successful country in the world of tax amnesty, now VDP with a longer time may not have achieved what TA achieved in nine months. People will make that comparison. So, if I say so, politically, the government will not dare to show off this VDP, plus next year is a political year. They will definitely withhold information that can allegedly bring down the current government, if my guess is yes.

…Yes, VDP is more optimal, they won’t play games. If the TA is playing around, it could also be that only 50% of them report during the TA. If it’s VDP, they can join those who didn’t join the TA before, they can join again. If there is another TA or VDP, it shows that the state is weak. From TA to VDP, it seems to be stricter, because the tariff is not bad, and they also have data. But if there are repeated promotions like that, the country needs funds to be weak.

Utilizing the opportunity for the accountant auditor’s presence in continuing professional development, the researcher conducted an in-depth interview, and the interview script was reconfirmed the next day. Mr. Sihotang, as an accountant auditor, gave his views on the auditees who participated in TA and VDP, as follows:

…On average, during the TA, my clients participated in the TA program, because they knew their sins would be erased, but during the VDP policy, they did not want to. They don’t want to reveal all their information. The TA policy is good, and many people participate, but the VDP policy is not interesting. I advise all clients to participate in TA, because it will not be audited by the tax authority and I emphasis that if the client does not report correctly, it is at their own risk, he he he.

…We give advice to comply with the rules, that means helping clients to maintain the sustainability of client companies. Companies that enter the Fortune 500 if studied comply with regulations, taxation, employment, and care for the environment. I emphasize that if you want the company to be long lasting and a going concern, maybe now you are profitable but, in the future, there will be an inspection and get caught and there will be even heavier fines, finally the client asks for the correct calculation, and this is the role of education as an auditor.

The prosperity perspective in the context of TA and VDP strategic policies is a manifestation of increased long-term compliance. Likewise, the entity’s going concern is maintained by complying with various provisions, not limited to taxes, to realize sustainability. In relation to tax compliance, long-term compliance is the main objective of TA and VDP, which are expected to increase revenue from the tax sector in the long term and is used for the prosperity of society. However, Mrs. Damayanti and Mr. Pratama are of the view that repeated TA and VDP policies in the short term cannot improve long-term compliance. This view is in line with the results of several studies on countries that have implemented TA and have only succeeded in collecting revenue from the tax sector in the short term without being able to improve compliance (Alm et al., Citation1990, Citation2009; Darmayasa et al., Citation2016; Nuryanah & Gunawan, Citation2022). This indicates that taxpayer trust, which forms compliance, has not been fully realized in accordance with the SSF tax compliance model.

4.2.2. Three perspectives: Values, governance, prosperity as a fundamental strategic TA and VDP

After analyzing the TA and VDP strategic policies from the point of view of values, governance, and prosperity, the researcher focused on the views of the accountant auditor, Mr. Nugraha, as related to the existence of repeated policy patterns waiting for the momentum of the situation surrounding it. To increase confidence, the researchers explored the views of the accountant auditor, Mr. Sihotang, who shared the same belief in repeatable policies. As a program to match population identification numbers with tax registration numbers is underway, this could become a strategic policy momentum, such as TA or VDP, after the tax authorities have data that need to be confirmed by taxpayers. The following is taken from an interview with Mr. Nugraha:

…There can be a third shock after the first shock of TA, the second shock of VDP, the third shock after Population Identification Number (NIK) is paired with Taxpayer Identification Number (NPWP). So, people who have never filed tax returns, they don’t have an NPWP, are finally hit. So, the market is people who don’t have an NPWP. There are many in Indonesia who don’t have an NPWP but have a lot of assets.

Some interesting experiences of Mrs. Masari from clients questioned the sense of unfairness of taxation on clients who received an appeal letter and were eventually forced to participate in the VDP. Taxpayers complain about the unfairness of tax collection to other taxpayers, including those who do not have NPWP. Responding to complaints from taxpayers, there are those who feel that injustice is presented to them by educating them that the NIK, paired with the NPWP in a core tax system container, will be a medium to bring justice to people who do not fulfil their tax obligations properly, or people who do not have an NPWP.

Observing Mrs. Masari’s views when educating taxpayers about participating in the VDP strengthens the researcher’s belief that the tax authority uses power to implement the VDP. Certainly, the power of tax authorities triggers coercive compliance. Mrs. Masari believes that there will be a follow-up TA or VDP when there is a fundamental difference between the core tax system and the fulfilment of tax obligations for taxpayers or even for people who do not have an NPWP. The implication of this follow-up policy is a recurring policy that leads to the emergence of speculative behavior to delay the fulfilment of their tax obligations in the hope of waiting for future TA or VDP strategic policies guaranteeing no tax audits. Tax audits normally ignore taxpayers; thus, efforts to improve compliance are not enough to conduct audits but should make efforts to reward compliant taxpayers (Fatas et al., Citation2021).

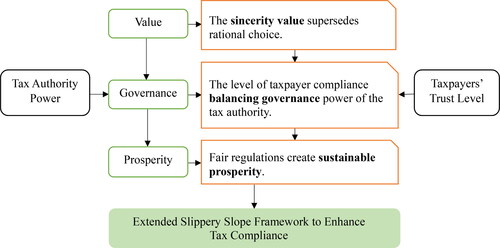

From the point of view of values, the governance point of view and the prosperity point of view regarding TA and VDP policies are the entry points for proposing values, governance, and prosperity that can balance the power of the tax authority with the trust level of taxpayers so that policies can be realized, with fairness in terms of increasing compliance. From a value perspective, we have not been able to demonstrate that fulfilling tax obligations is a form of gratitude for the income bestowed by the creator. From a governance perspective, remembering that the value of gratitude has not yet grown, the impact of sincere obedience has not yet been established because of the waning of gratitude. Finally, from a prosperity perspective, sustainability increases in all aspects, particularly compliance. The following is a proposal for integrating values, governance, and prosperity as a fundamental viewpoint for TA and VDP policies within the extended slippery slope framework shown in .

Figure 1. Fundamental Values, Governance, and Prosperity Viewpoint Within The Extended Slippery Slope Framework.

5. Conclusion

The main objective of TA and VDP policies is to increase tax compliance, but this objective still does not seem to be optimally realized. From three points of view, namely values, governance, and prosperity, to ground the values of the Pancasila ideology in fundamental tax strategy, the views of accountants (accountant academics, accountant auditors, and accountant attorneys) are obtained. The point of view of taxpayers who decide to follow the TA and VDP is a rational choice to benefit from low tax redemption rates. The governance perspective of the tax authority prioritizes the power dimension through TA and VDP policies to increase revenue from the tax sector in the short term. The prosperity point of view of TA and VDP policies prioritizes simplicity over the fulfilment of a sense of fairness, which is carried out in the short term. From the points of view of values, governance, and prosperity, TA and VDP policies have not been able to increase long-term compliance. Considering this, a derivative policy is required after TA and VDP. It is highly recommended to develop a policy for tracking assets reported in the TA and VDP as potential future taxes, not by developing a similar policy in the form of tax amnesty.

6. Theoretical and practical implications

This study has theoretical and practical implications. The theoretical implications of this research form the basis for developing better TA and VDP policies in the future. The two dimensions that should be balanced are more at the implementation level from three points of view of values, governance, and prosperity, emphasizing the power of the tax authority. This study contributes to the fundamental basis for TA and VDP strategic policies within the extended slippery slope framework to enhance tax compliance. Future TA and VDP strategic policies should be based on sincere values, balanced governance, and a sustainable prosperity viewpoint within the extended slippery slope framework. The practical implications of TA and VDP strategic policies in the future focus on the rational actions of taxpayers who participate in TA and VDP and are not limited to obtaining benefits from TA and VDP policies, but rather to the self-improvement of taxpayers toward compliant taxpayers.

7. Limitations and directions for future study

This study uses three points of view – values, governance, and prosperity – to analyze the effectiveness of TA and VDP strategic policies. In this study, we did not quantitatively calculate the increases in post-TA and VDP adherence. It is hoped that further research will present a new paradigm complemented by quantification of policy effectiveness and quantification of increased tax compliance.

Author contributions

All authors contributed equally to the conception and design of the study.

I Nyoman Darmayasa and I Made Marsa Arsana were involved in the conception and design. Nyoman Sentosa Hardika was involved in the analysis and interpretation of the data. I Made Agus Putrayasa was involved in the drafting of the paper. All authors agree to be accountable for all aspects of the work.

The authors confirm that the data supporting the findings of this study are available within the article [and/or its supplementary materials].

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

I Nyoman Darmayasa

I Nyoman Darmayasa is a lecturer (Associate Professor) and researcher in the Accounting Department, Bali State Polytechnic, Indonesia. He holds a doctoral degree in accounting, specializing in taxation, from Brawijaya University. His research expertise is related to taxation, accounting, and auditing. He is a partner of a Public Accounting Firm.

Nyoman Sentosa Hardika

Nyoman Sentosa Hardika is a lecturer (Associate Professor) and researcher in the Accounting Department, Bali State Polytechnic, Indonesia. He holds a doctoral degree in economics, specializing in taxation, from Airlangga University. His research expertise is related to taxation, finance, and accounting. He also held a registered tax consultant.

I Made Marsa Arsana

I Made Marsa Arsana is a lecturer and researcher in the Accounting Department, Bali State Polytechnic, Indonesia. He holds a Master’s degree in management from Udayana University. His research expertise is related to auditing, accounting, management, and taxation. He also held a registered tax consultant.

I Made Agus Putrayasa

I Made Agus Putrayasa is a lecturer and researcher in the Accounting Department, Bali State Polytechnic, Indonesia. He holds a Master’s degree in accounting from Brawijaya University. His research expertise is related to auditing, accounting, and taxation. He is a partner of a Public Accounting Firm.

References

- Agusti, R. R., & Rahman, A. F. (2023). Determinants of tax attitude in small and medium enterprises: Evidence from Indonesia. Cogent Business & Management, 10(1), 1. https://doi.org/10.1080/23311975.2022.2160585

- Ahmar, N. (2018). Role of Public accountants to the success of tax amnesty in financial institutions and Bangking in Indonesia. Proceeding International Seminar on Accounting for Society Bachelor, 1(1), 181–16. https://openjournal.unpam.ac.id/index.php/Proceedings/article/view/1829/0

- Alm, J., & Beck, W. (1993). Tax amnesties and compliance in a long run: A time series analysis. National Tax Journal, 46(1), 53–60. http://www.jstor.org/stable/41788996 https://doi.org/10.1086/NTJ41788996

- Alm, J., Martinez-Vazquez, J., & Wallace, S. (2009). Do tax amnesties work? the revenue effects of tax amnesties during the transition in the russian federation. Economic Analysis and Policy, 39(2), 235–253. https://doi.org/10.1016/S0313-5926(09)50019-7

- Alm, J., McClelland, G. H., & Schulze, W. D. (1992). Why do people pay taxes? Journal of Public Economics, 48(1), 21–38. https://doi.org/10.1016/0047-2727(92)90040-M

- Alm, J., Mckee, M., & Beck, W. (1990). Amazing grace: Tax Amnesties and compliance. National Tax Journal, 43(1), 23–37. https://doi.org/10.1086/NTJ41788822

- Alm, J., & Torgler, B. (2006). Culture differences and tax morale in the United States and in Europe. Journal of Economic Psychology, 27(2), 224–246. https://doi.org/10.1016/j.joep.2005.09.002

- Cahyonowati, N., Ratmono, D., & Juliarto, A. (2023). The role of social norms and trust in authority in tax compliance dilemmas. Cogent Business & Management, 10(1), 2174084. https://doi.org/10.1080/23311975.2023.2174084

- Cresswell, J. W., & Poth, C. N. (2018). Qualitative Inquiry and Research Design: Choosing Among Five Approaches (4th ed.). Sage Publications Inc. USA. https://us.sagepub.com/en-us/nam/qualitative-inquiry-and-research-design/book246896

- Darmayasa, I. N, Politeknik Negeri Bali. (2017). Yadnya Sebagai Pemaknaan Lain Atas Nilai Wajar Harta Amnesti Pajak. Jurnal Akuntansi Multiparadigma, 8(1), 166–182. https://doi.org/10.18202/jamal.2017.04.7046

- Darmayasa, I. N, Politeknik Negeri Bali. (2019). Preskriptif Ketentuan Umum Perpajakan Pada Perspektif Akuntansi Pancasila. Jurnal Akuntansi Multiparadigma, 10(1), 22–41. https://doi.org/10.18202/jamal.2019.04.10002

- Darmayasa, I. N., Arsana, I. M. M., & Putrayasa, I. M. A. (2022). Reconstruction of the slippery slope framework tax compliance model. ACRN Journal of Finance and Risk Perspectives, 11(1), 19–32. https://doi.org/10.35944/jofrp.2022.11.1.002

- Darmayasa, I. N., & Hardika, N. S. (2024). Core tax administration system : the power and trust dimensions of slippery slope framework tax compliance model. Cogent Business & Management, 11(1) https://doi.org/10.1080/23311975.2024.2337358

- Darmayasa, I. N., & Partika, I. D. M, Politeknik Negeri Bali, Badung, Indonesia. (2024). Reconstruction concept of the meaning of permanent establishment physical presence for tax purposes. Journal of Tax Reform, 10(1), 38–50. https://doi.org/10.15826/jtr.2024.10.1.155

- Darmayasa, I. N., Sudarma, I. M., Achsin, M., & Mulawarman, A. D. (2016). Deconstruction of equitable tax amnesty. International Journal of Applied Business and Economic Research, 14(11), 8167–8179. https://serialsjournals.com/abstract/25007_51.pdf

- Darmayasa, I. N., Sudarma, I. M., Achsin, M., & Mulawarman, A. D, I Made Sudarma. (2017). Deconstruction of tax amnesty in based on pancasila values: The case of Indonesia. The International Journal of Accounting and Business Society, 25(1), 15–25. https://doi.org/10.21776/ub.ijabs.2017.25.1.2

- Darmayasa, I. N., Sudarma, I. M., Achsin, M., & Mulawarman, A. D. (2018). Constructed interpretation of tax compliance through the historicity, rationality, and actuality of Pancasila (cases in Indonesia). International Journal of Trade and Global Markets, 11(1/2), 67–76. https://doi.org/10.1504/IJTGM.2018.092481

- Diakomihalis, M, University of Ioannina, Ioannina, Epirus, Greece. (2020). Factors of tax evasion in Greece: Taxpayers’ perspective. Journal of Tax Reform, 6(2), 180–195. https://doi.org/10.15826/jtr.2020.6.2.081

- El Aboudi, S., & Khanchaoui, I. (2020). The nexus between attitude, social norms, intention to comply, financial performance, mental accounting and tax compliance behavior. Asian Economic and Financial Review, 11(12), 894–907. https://doi.org/10.18488/JOURNAL.AEFR.2021.1112.938.949

- Fatas, E., Nosenzo, D., Sefton, M., & Zizzo, D. J. (2021). A self-funding reward mechanism for tax compliance. Journal of Economic Psychology, 86(October), 102421. https://doi.org/10.1016/j.joep.2021.102421

- Feld, L. P., & Frey, B. S. (2007). Tax compliance as the result of a psychological tax contract: The role of incentives and responsive regulation. Law & Policy, 29(1), 102–120. https://doi.org/10.1111/j.1467-9930.2007.00248.x

- Fochmann, M., Müller, N., & Overesch, M. (2021). Less cheating? The effects of prefilled forms on compliance behavior. Journal of Economic Psychology, 83(March), 102365. https://doi.org/10.1016/j.joep.2021.102365

- Frecknall-Hughes, J., Gangl, K., Hofmann, E., Hartl, B., & Kirchler, E. (2023). The influence of tax authorities on the employment of tax practitioners: Empirical evidence from a survey and interview study. Journal of Economic Psychology, 97(August), 102629. https://doi.org/10.1016/j.joep.2023.102629

- Gangl, K., Hofmann, E., & Kirchler, E. (2015). Tax authorities’ interaction with taxpayers: A conception of compliance in social dilemmas by power and trust. New Ideas in Psychology, 37, 13–23. https://doi.org/10.1016/j.newideapsych.2014.12.001

- Glaze, S. (2015). Schools out: Adam Smith and pre-disciplinary international political economy. New Political Economy, 20(5), 679–701. https://doi.org/10.1080/13563467.2014.999757

- Hallsworth, M. (2014). The use of field experiments to increase tax compliance. Oxford Review of Economic Policy, 30(4), 658–679. https://doi.org/10.1093/oxrep/gru034

- Hamilton-Hart, N., & Schulze, G. G. (2016). Taxing Times in Indonesia: The challenge of restoring competitiveness and the search for fiscal space. Bulletin of Indonesian Economic Studies, 52(3), 265–295. https://doi.org/10.1080/00074918.2016.1249263

- Haning, M. T. H. T., Hamzah, H., & Tahili, M. H. (2019). Investigating the Effect of public trust on tax compliance. Bisnis & Birokrasi Journal, 26(2), 100–109. https://doi.org/10.20476/jbb.v26i2.10279

- Hartmann, A. J., Gangl, K., Kasper, M., Kirchler, E., Kocher, M. G., Mueller, M., & Sonntag, A. (2022). The economic crisis during the COVID-19 pandemic has a negative effect on tax compliance: Results from a scenario study in Austria. Journal of Economic Psychology, 93(October), 102572. https://doi.org/10.1016/j.joep.2022.102572

- Hasanah, U., Na’im, K., Elyani, E., & Waruwu, K. (2021). Analisis Perbandingan tax amnesty Jilid I dan Jilid II (Program Pengungkapan Sukarela) Serta Peluang Keberhasilannya. Owner, 5(2), 706–716. https://doi.org/10.33395/owner.v5i2.565

- Hermawan, M. S., Abigail, P., Martowidodjo, Y. H., & Tohang, V. (2020). Understanding tax amnesty and tax compliance in indonesia: an institutional approach. Journal of Economics, Business, & Accountancy Ventura, 22(3), 424–434. https://doi.org/10.14414/jebav.v22i3.1810

- Ibrahim, M. A., Myrna, R., Irawati, I., & Kristiadi, J. B. (2017). International Journal of Economics and Financial Issues A Systematic Literature Review on Tax Amnesty in 9 Asian Countries. International Journal of Economics and Financial Issues, 7(3), 220–225. http:www.econjournals.com

- Inasius, F. (2019). Factors Influencing SME Tax Compliance: Evidence from Indonesia. International Journal of Public Administration, 42(5), 367–379. https://doi.org/10.1080/01900692.2018.1464578

- Janas, M., & Oljemark, E. (2021). Trust and reputation under asymmetric information. Journal of Economic Behavior & Organization, 185, 97–124. https://doi.org/10.1016/j.jebo.2021.02.023

- Kahneman, D., & Tversky, A. (1979). ‘Prospect theory: An analysis of decision under risk’. Econometrica, 47(2), 263–292. https://doi.org/10.2307/1914185

- Kastlunger, B., Lozza, E., Kirchler, E., & Schabmann, A. (2013). Powerful authorities and trusting citizens: The slippery slope framework and tax compliance in Italy. Journal of Economic Psychology, 34, 36–45. https://doi.org/10.1016/j.joep.2012.11.007

- Keen, M., & Slemrod, J. (2017). Optimal tax administration. Journal of Public Economics, 152, 133–142. https://doi.org/10.1016/j.jpubeco.2017.04.006

- Khozen, I., & Setyowati, M. S. (2023). Managing taxpayer compliance: Reflections on the drivers of willingness to pay taxes in times of crisis. Cogent Business & Management, 10(2), 2218176. https://doi.org/10.1080/23311975.2023.2218176

- Kirchler, E., Hoelzl, E., & Wahl, I. (2008). Enforced versus voluntary tax compliance: The “Slippery Slope” framework. Journal of Economic Psychology, 29(2), 210–225. https://doi.org/10.1016/j.joep.2007.05.004

- Kogler, C., Batrancea, L., Nichita, A., Pantya, J., Belianin, A., & Kirchler, E. (2013). Trust and power as determinants of tax compliance: Testing the assumptions of the slippery slope framework in Austria, Hungary, Romania and Russia. Journal of Economic Psychology, 34, 169–180. https://doi.org/10.1016/j.joep.2012.09.010

- Kogler, C., Muehlbacher, S., & Kirchler, E. (2013). Trust, power, and tax compliance: Testing the “slippery slope framework” among self-employed taxpayers. WU International Taxation Reserach Paper Series, 05, 2–18.

- Kogler, C., Olsen, J., Kirchler, E., Batrancea, L. M., & Nichita, A. (2023). Perceptions of trust and power are associated with tax compliance: A cross-cultural study. Economic and Political Studies, 11(3), 365–381. https://doi.org/10.1080/20954816.2022.2130501

- Latif, Y. (2018). The religiosity, nationality, and sociality of pancasila: Toward Pancasila through Soekarno’s way. Studia Islamika, 25(2), 207–245. https://doi.org/10.15408/sdi.v25i2.7502

- Lozza, E., Kastlunger, B., Tagliabue, S., & Kirchler, E. (2013). The relationship between political ideology and attitudes toward tax compliance: The case of Italian taxpayers. Journal of Social and Political Psychology, 1(1), 51–73. https://doi.org/10.5964/jspp.v1i1.108

- Mangoting, Y., Widuri, R., & Eoh, T. S. (2019). The dualism of tax consultants’ roles in the taxation system. Jurnal Akuntansi Dan Keuangan, 21(1), 30–37. https://doi.org/10.9744/jak.21.1.30-37

- Marire, J., & Sunde, T. (2012). Economic growth and tax structure in Zimbabwe: 1984-2009. International Journal of Economic Policy in Emerging Economies, 5(2), 105–121. https://doi.org/10.1504/IJEPEE.2012.048495

- Mashiri, E., Dzomira, S., & Canicio, D. (2021). Transfer pricing auditing and tax forestalling by Multinational Corporations: A game theoretic approach. Cogent Business & Management, 8(1) https://doi.org/10.1080/23311975.2021.1907012

- Miles, M. B., Huberman, A. M., & Saldana, J. (2019). Qualitative data analysis: A methods sourcebook. Sage Publications Inc. USA. https://us.sagepub.com/en-us/nam/qualitative-data-analysis/book246128

- Musimenta, D. (2020). Knowledge requirements, tax complexity, compliance costs and tax compliance in Uganda. Cogent Business & Management, 7(1), 1812220. https://doi.org/10.1080/23311975.2020.1812220

- Nurkholis, N., Dularif, M., & Rustiarini, N. W. (2020). Tax evasion and service-trust paradigm: A meta-analysis. Cogent Business & Management, 7(1), 1827699. https://doi.org/10.1080/23311975.2020.1827699

- Nuryanah, S., & Gunawan, G. (2022). Tax amnesty and taxpayers’ noncompliant behaviour: evidence from Indonesia. Cogent Business & Management, 9(1), 1–17. https://doi.org/10.1080/23311975.2022.2111844

- Pan, Z. (2019). A Review of Prospect Theory. Journal of Human Resource and Sustainability Studies, 07(01), 98–107. https://doi.org/10.4236/jhrss.2019.71007

- Pogorletskiy, A. I., & Söllner, F, St. Petersburg State University, St. Petersburg, Russian Federation. (2020). Pandemics and Tax Innovations: What can we Learn from History? Journal of Tax Reform, 6(3), 270–297. https://doi.org/10.15826/jtr.2020.6.3.086

- Prinz, A., Muehlbacher, S., & Kirchler, E. (2014). The slippery slope framework on tax compliance: An attempt to formalization. Journal of Economic Psychology, 40, 20–34. https://doi.org/10.1016/j.joep.2013.04.004

- Ritsatos, T. (2014). Tax evasion and compliance; from the neo classical paradigm to behavioural economics, a review. Journal of Accounting & Organizational Change, 10(2), 244–262. https://doi.org/10.1108/JAOC-07-2012-0059

- Sayidah, N., & Assagaf, A. (2019). Tax amnesty from the perspective of tax official. Cogent Business & Management, 6(1), 1659909. https://doi.org/10.1080/23311975.2019.1659909

- Slemrod, J. (2019). Tax compliance and enforcement. Journal of Economic Literature, 57(4), 904–954. https://doi.org/10.1257/jel.20181437

- Smith, A. (2014). An inquiry into the nature and causes of the wealth of nations. The University of Adelaide.

- Sudarma, I. M., & Darmayasa, I. N. (2017). Does voluntary tax compliance increase after granting tax amnesty? Accounting and Finance Review, 2(3), 11–17. https://ssrn.com/abstract=3008397

- Sudarma, I. M., & Darmayasa, I. N, Bali State Politechnic. (2018). The philosophy of tat twam asi: The foundation of consciousness regarding post-tax amnesty (Cases In Indonesia). Journal of Business & Finance in Emerging Markets, 1(1), 153–160. https://doi.org/10.32770/jbfem.vol1153-160

- Sutrisno, T., & Dularif, M. (2020). National culture as a moderator between social norms, religiosity, and tax evasion: Meta-analysis study. Cogent Business & Management, 7(1), 1772618. https://doi.org/10.1080/23311975.2020.1772618

- Torgler, B. (2003). Tax morale : Theory and empirical analysis of tax compliance. University Basel.

- Torgler, B., & Schaltegger, C. A. (2005). Tax amnesties and political participation. Public Finance Review, 33(3), 403–431. https://doi.org/10.1177/1091142105275438

- Trawule, A. Y., Gadzo, S. G., Kportorgbi, H. K., & Sam-Quarm, R. (2022). Tax education and fear-appealing messages: A grease or sand in the wheels of tax compliance? Cogent Business & Management, 9(1), 2049436. https://doi.org/10.1080/23311975.2022.2049436

- Wadesango, N., Bizah, S., & Nyamwanza, L. (2020). The impact of tax amnesty on tax compliance and tax evasion behavior among SMEs. Academy of Entrepreneurship Journal, 26(3), 1–10. https://www.abacademies.org/journals/month-september-year-2020-vol-26-issue-3-journal-aej-past-issue.html