?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Countries have greatly depended on taxes and corporate finance to support government expenditures and business activities, respectively. However, contrasting arguments on their effects on environmental quality prevail in literature. While Ghana’s carbon dioxide emissions have seen an upward trend with taxes and corporate finance, their role in the level of carbon emissions is uncertain. This paper assesses the effect of tax and corporate finance on Ghana’s carbon dioxide emissions. Time-series data from 1971 to 2021 from the World Bank were used for analysis. The Autoregressive Distributed Lag (ARDL) estimation technique shows that in the short run, tax positively affects carbon dioxide emission, while trade openness and government expenditure reduce it. In the long run, tax and corporate finance increase carbon emissions. However, urbanization, trade openness and government expenditure reduce carbon emissions. Policy wise, financial institutions should be motivated to set aside special funds to support green activities. In addition, restructuring Ghana’s tax system to have an explicit environmental tax meant to reduce carbon emissions is needed. Committing significant portions of tax revenues to support research and development towards energy efficiency is necessary to attain low carbon economy.

1. Introduction

The role of taxation and corporate finance remains significant variables in every economy. This is because taxation is a major source of government revenue, through which the government embarks on its expenses to provide citizens with essential services. Corporate finance also provides firms and investors with financial resources for business activities. Thus, without taxation some aspects of socioeconomic development may be hampered and without corporate finance, businesses and investors may struggle to expand. That notwithstanding, it is commonly argued that tax imposition may pose as a hindrance to business growth and reduce wellbeing of individuals. This situation prevails when indirect taxes increase the cost of doing business, thereby crippling business and/or making the prices of goods and services expensive for citizens (Tanzi, Citation1982). Direct taxes also reduce consumers’ disposable income.

Aside that, taxation and corporate finance may have environmental quality implications. For example, through taxes, the government can raise funds needed for the development and successful implementation of appropriate policies to protect the environment (Zhang et al., Citation2023). Moreover, environmental tax has been suggested as a solution to the negative externalities from polluting firms (Smith, Citation1992). On the other hand, when a tax imposition leads to a higher cost of living (Gale & Samwick, Citation2017) households may resort to an environmentally unfriendly way of life. Taxes may also increase the prices of imported energy-efficient machines, which may retard the efforts of firms and households to switch to energy-friendly machines leading to environmental degradation.

Regarding corporate finance, on the one hand, by providing firms with cheap credit, they can acquire energy-efficient machines that reduce environmental pollution. In addition, corporate finance that supports research and development as well as renewable energy development will promote cleaner environments (Kwakwa et al., Citation2023). On the other hand, the low interest rate of firms in accessing corporate finance may lead to the acquisition of energy-intensive gadgets such as vehicles and air conditions, which may increase carbon emissions (Amuakwa-Mensah et al., Citation2018; Musah et al., Citation2023). In addition, when firms expand through access to credit, their dependence on energy of which majority is sourced from fossil fuel for production activities can lead to an increase in carbon emission.

Empirical assessment of the environmental effect of taxation and corporate finance has become eminent in recent times where global leaders have sought to tame the pace of carbon emissions. This move is to address the issue of climate change and its harmful effects. Despite the growing interest among researchers on the drivers of environmental quality in line with sustainable development goals (SDGs), empirical studies have yielded conflicting results (Chekouri et al., Citation2020; Li et al., Citation2023; Lv et al., Citation2023; Opuala et al., Citation2023). This situation calls for further studies to offer more insights into shaping policy formulations. In the case of Africa and Ghana, in particular, a relative dearth of analysis on the effect of corporate finance and taxation exists in an era where the government of Ghana is eager to have a low-carbon economy. The little to no evidence from African countries have developmental implications since the differences in economic conditions and systems in Africa and other part of the world may not be helpful to rely on the results from these countries to shape policy issues in Africa.

Moreover, several of the studies have focused on the long run effect without presenting the short run outcome (Domon et al., Citation2022; Hussain et al., Citation2024; Ling et al., Citation2022; Telatar & Birinci, Citation2022). This neglect may not reveal to policymakers the possible differences in short and long run effects that could be associated with policies that affect the level of taxation and corporate finance. More so, not much is known empirically about the evolving contributions of tax and corporate funding to carbon emissions behavior. Such analysis brings to bear the share of these variables to changes in carbon emissions as the years go by.

Given that although African countries’ contribution to the levels of global carbon dioxide emissions (the major driver of climate change) is less than 4% (Friedlingstein et al., Citation2022), the increasing trend in recent times have cast doubt on whether many of the SDGs can be realized in Africa. This again presents a serious situation since the African continent is the region that is severely affected by climate change. The numerous studies on the drivers of environmental degradation especially in Africa are yet to give much attention to the effect of corporate finance and taxation (Abokyi et al., Citation2021; Chekouri et al., Citation2020; Degirmenci & Aydin, Citation2023; Opuala et al., Citation2023). Many African countries including Ghana have over the years witnessed an increased levels of tax revenue and corporate finance alongside carbon emissions (World Bank, Citation2023). Discussions in many quarters have largely been on economic growth impact of taxation and corporate funding (Takumah & Iyke, Citation2017; Egbunike et al., Citation2018; Bekele & Degu, Citation2023; Adefolake & Omodero, Citation2022; Ho et al., Citation2023). As significant as such analysis is, there is equally a pressing need to pay attention to the effect of taxation and corporate finance on environmental quality (Mesagan et al., Citation2022) in the country.

From the above, the present study assesses the role of taxation and corporate finance in Ghana’s environmental quality. The specific objectives are:

To assess the short and long run effect of taxation and corporate finance on carbon dioxide emissions in Ghana; and

To ascertain the share of taxation and corporate finance in the changes of the levels of carbon dioxide emissions in Ghana.

The study offers five contributions to the literature. Various tax related issues in developing countries have gained attention in recent times (Wahab et al., Citation2018; Wahab et al., Citation2022; Egbunike et al., Citation2018; Ojo & Shittu, Citation2023; Agusti & Rahman, Citation2023). However, the environmental effect of tax in Africa is relatively under investigated. Thus, first, this work contributes to the literature by focusing on a country from Africa where studies on the subject matter are under researched. Second, while a number of studies have focused on the environmental tax effect (He et al., Citation2019; Li et al., Citation2023; Soku et al., Citation2023; Wolde-Rufael & Mulat-Weldemeskel, Citation2022) this study focuses on the tax on products. The tax effect on environmental sustainability analysis is crucial for developing countries who are compelled to increase taxes to meet the growing expenses of the government. Third, the outcome of the study offers further insight on how cautious policymakers should be when they are eager to raise taxes for revenue mobilization. Fourth, the paper shifts attention from assessing the economic growth effect of corporate finance and tax revenue to the environmental impact in an African country. Fifth, cointegration estimation methods to reveal the short and long run effects of taxation and corporate funding are explored alongside a variance decomposition assessment to unravel the share of taxation and corporate funding on the changes in carbon emissions over sometime period.

The rest of the paper is structured as follows: in Section 2, the background of the paper is presented; Section 3 is on theoretical framework; Section 4 presents a review of related literature and hypotheses development; in Section 5, issues related to methodology are presented; in Section 6, the results are presented and discussed; and in Section 7, the study is concluded with implications, limitations and recommendations for future works.

2. Background

Comparatively, the tax system in developing countries like Ghana leaves much to be desired, and corporate finance has not yet advanced as well in these countries. Like many African countries, Ghana’s tax revenue is insufficient to support government expenses. This has partly contributed to rising government debt (Kamasa et al., Citation2022; Ricky-Okine et al., Citation2023). Efforts to increase tax revenue by widening the tax net have not been successful (Hammond et al., Citation2023) and as a result, tax deepening has been resorted to by the government.

More so, funding or credit remains a major challenge for corporate firms in Ghana (Amankwaah & Baidoo, Citation2023). Aside from the high interest rate and collateral requirements (Attrams & Tshehla, Citation2022), financial institutions committed to providing financial support to corporate entities have a low capital base (Sandow et al., Citation2021). The low savings rate in the country (World Bank, Citation2023) could be another reason financial institutions in the country are unable to offer the expected support to firms. However, the World Bank (Citation2023) shows that there has been an increasing trend in the amount of support for private sector development (corporate funding) from 4.94% of GDP in 1990 to 18.07% of GDP in 2013, and it has since dropped to 13% of GDP in 2021.

Ghana is obliged to take actions that enhance the quality of the environment as a signatory to several international treaties meant to protect the environment and achieve sustainable development. Despite the fact that policies on energy and climate change, including the Renewable Energy Master Plan, the National Energy Policy, and the National Climate Change Policy, have been developed, the country is still battling various environmental challenges. These include forest degradation, water pollution, indiscriminate waste disposal, and rising carbon dioxide emissions (Alhassan et al., Citation2020; World Bank, Citation2023). In Ghana, carbon dioxide emission, a major contributor to climate change, has more than tripled between 1994 and 2021 (World Bank, Citation2023) which is an issue of concern for researchers and policymakers. To offer guidelines to shape policy formulation and implementation towards the attainment of a low-carbon economy, as outlined in Ghana’s National Energy Policy, empirical analysis of the drivers of carbon dioxide emission in Ghana is becoming popular (Abokyi et al., Citation2019; Adams & Klobodu, Citation2017; Kwakwa et al., Citation2023).

Some analyses in Ghana have examined the effect of business-related activities on carbon emissions. Twerefou et al. (Citation2016) and Abokyi et al. (Citation2021) found that trade affects carbon emissions in Ghana. Owusu and Asumadu-Sarkodie (Citation2016) reported a positive effect of agricultural production on carbon emissions, Kwakwa et al. (Citation2023) obtained a mixed effect of financial indicators of financial institutions, and Appiah et al. (Citation2021) found that industrialization and economic growth influence carbon emissions in Ghana.

However, the effects of corporate finance and taxation in Ghana are yet to be subjected to empirical scrutiny. It is very important to analyse this issue now, especially when the number of taxes has increased over the past years (BBC, Citation2023; PWC, Citation2023) and the country’s financial sector has seen some shake up in recent times (Hammond et al., Citation2023). A look at the data shows that there is an upward trend in Ghana’s carbon dioxide emissions with tax revenue and corporate finance (World Bank, Citation2023). This suggests a possibility of causation from the latter two. An empirical analysis to unearth the effect tax revenue and corporate finance on carbon emissions will confirm this suspicion or otherwise.

3. Theoretical framework

Econometric analysis related to the assessment of the drivers of environmental degradation, including carbon emissions, has relied on strong theories or models. One of the most common and reliable models employed by researchers is the Stochastic Impacts by Regression on Population, Affluence, & Technology (STIRPAT) model (Karaka et al., 2023; Lv et al., Citation2023; Ma et al., Citation2022; Yu et al., Citation2023). This model developed in the 1990s by Dietz and Rosa (Citation1997) argues that in a stochastic manner the level of environmental quality is determined by population, affluence and technology.

It stresses that pressure from the population lowers environmental quality, resulting from the need to extract more resources from the environment to meet human needs (Adams et al., Citation2016). Affluence, on the other hand, affects the environment through the consumption and production associated with economic growth (Kwakwa, Citation2023). Technology refers to the methods employed by economies to produce goods. It also indicates the socioeconomic characteristics of an economy (Dietz & Rosa, Citation1997). For the sake of empirical assessment, it is important to note that while income has predominantly and in some case trade openness (Marfo et al., Citation2023) been used to represent affluence, population growth or urbanization has been used for population, whereas energy usage, finance development and industrialization have often been used for technological progress (Karaka et al., 2023; Lv et al., Citation2023; Yu et al., Citation2023). Also, most studies on the forces behind environmental degradation for countries have used carbon dioxide emissions. The main reason cited has been that it contributes to a greater share of greenhouse gasses (Chekouri et al., Citation2020; Li et al., Citation2023; Lv et al., Citation2023; Opuala et al., Citation2023; Yan et al. (Citation2023).

A strength of the STIRPAT model is its ability to allow for the inclusion of other relevant variables, especially when technology is extended to include other social, cultural, and institutional dynamics of the economy that can affect the environment (Dietz & Rosa, Citation1997; York et al., Citation2003). Consequently, it can be argued that corporate finance and taxation could be added to the STIRPAT model. The level of tax revenue and corporate finance reflects some economic characteristics of an economy and as a result the two are strong enough to measure technology.

The STIRPAT model is appropriate for this investigation because the variables of interest argued in the introduction can be justified by the model. Thus, given that Ghana’s carbon emission is rising over the years it is appropriate to adopt this model to unravel the influence of the pace of urban growth, economic activities, taxes and some features of the financial sector especially increasing corporate finance.

4. Literature review and hypotheses development

4.1. Taxation and carbon dioxide emissions

Although taxation has traditionally been seen as a major avenue for mobilizing revenue for government operations, it has emerged as having some environmental quality implications. This is because the government can generate the revenue required to implement clean environmental programs (He et al., Citation2019). However, economic theory suggests that a tax imposition can reduce the disposable income of individuals and increase the selling prices (Tanzi, Citation1982) of environmentally friendly goods. While the former can improve environmental quality, the latter can reduce environmental quality.

There could be cases where environmental taxes are imposed to address environmental challenges. These include the Pigouvian taxes (taxes on per certain unit of measured pollution output), ‘approximations’ to Pigouvian taxes (indirect taxes on goods and services that may be environmentally unfriendly) and cost-sharing or mutualization (taxes to raise revenue for government expenses on environmental protection) (Smith, Citation1992). Through such taxes, polluting firms’ cost of production increases, and the government raises revenue to implement appropriate environmental policies, eventually reducing environmental pollution, including carbon emissions (He et al., Citation2019).

Some empirical studies have assessed the direction of the effect of tax revenue on environmental quality. Halkos and Paizanos (Citation2016) reported that tax revenue helps reduce the carbon emissions of G7 economies. Also, Katircioglu and Katircioglu (Citation2018) as well as Yuelan et al. (Citation2022) found revenues from taxes improve environmental quality in Turkey; and for the Belt and Road initiative (BRI) regions. Zhang et al. (Citation2022) using data from 48 developing countries found that taxes improve environmental quality.

Other researchers have focused on the effects of environmental tax on the quality of the environment. Degirmenci and Aydin (Citation2023) investigated the effects of environmental taxes on environmental pollution in selected African countries. Regression results indicate that environmental taxes worsen environmental degradation for Cameroon, Ivory Coast, and Mali, but they improve the quality of the environment in the case of South Africa. Guo et al. (Citation2022) assessed the effect of environmental tax on urban pollution in China and revealed that air quality has improved as a result of the environmental tax imposition.

Xu et al. (Citation2023) found that environmental taxes controlled waste pollution in China. Rotimi et al. (Citation2021) found that an environmental tax is helpful in reducing air pollution in the Nigerian economy. Chien et al. (Citation2021) found that, in addition to green energy and eco-innovation, environmental taxes improve the environmental quality of Asian economies. Wolde-Rufael and Mulat-Weldemeskel (Citation2021) also established that environmental taxes reduce carbon emissions in emerging economies. Zhang et al. (Citation2023) found that environmental taxes reduce the industrial water pollution of firms in China. Sanderson et al. (Citation2023) noted that carbon taxes reduce carbon emissions in the South African economy. However, Pretis (Citation2022) found that carbon tax reduces emissions from the transport sector, but not the total carbon emissions of British Columbia.

Although the empirical evidences are mixed, given that tax imposition in Ghana has been associated with high cost of doing business and in most cases, consumers bearing the incidence of tax it is hypothesized that:

H1: Taxation increases carbon dioxide emissions.

4.2. Corporate finance and carbon dioxide emissions

The financial curse theory explains that financial development promotes environmental degradation rather than environmental enhancement. This situation occurs when as a result of financial development there is cheap financial support for firms to engage in activities that are detrimental to the environment (Musah et al., Citation2023). Based on this corporate finance may increase carbon dioxide emissions.

Some authors argue that the effect of financial development is dependent on the sector in which the funds are pushed. Mesagan et al. (Citation2022) argued that financial support for industrial expansion would imply more energy consumption, leading to increased carbon emissions. However, support for green projects would reduce carbon emissions (Kwakwa et al., Citation2023). Moreover, financial support for corporate companies can reduce carbon emissions when they are financially empowered to purchase energy-efficient technology or implement environmentally friendly means of production, distribution, and consumption (Musah et al., Citation2022). On the other hand, receiving financial support for corporate bodies can whet their appetite for energy-intensive products, which will trigger carbon emissions (Kwakwa, Citation2020).

Divergent reports regarding the environmental effect of corporate finance have been found in the empirical literature. Peng et al. (Citation2022) found that green credit is helpful in promoting lower emissions from Chinese firms. However, Lyu et al. (Citation2022) found that firms that are highly indebted to financial institutions pollute more than those with lower debt to service. Mesagan et al. (Citation2022) reported that in African countries, corporate finance increases carbon emissions but moderates the emission effect of the industrial sector. Zhang et al. (Citation2021) established that green credit reduces carbon emissions in the Chinese provinces. Sun and Zeng (Citation2023) found that a green credit policy reduces the carbon emission rate of heavily polluting firms. Nwani and Omoke (Citation2020) found that credit to the private sector helps reduce the rate of carbon emissions in Brazil, but Tsaurai (Citation2019) reported a positive effect of credit to the private sector on carbon emissions.

The prevailing situation in Ghana is that most of the corporate firms are not into renewable energy related sector and financial institutions also are quick to support energy intensive business due to their profit motive. From this angle, it is hypothesized that:

H2: Corporate finance increases carbon dioxide emissions.

5. Methodology

5.1. Research design and empirical modelling

The study adopts explanatory research design. This is premised on the fact that the study’s objective is to analyse the effect of corporate finance and taxation on carbon dioxide emissions. Largely, quantitative research approach using time series mechanism is adopted for analysis.

This study adopts the Stochastic Impacts by Regression on Population, Affluence, & Technology (STIRPAT) model by Dietz and Rosa (Citation1997) as the foundation for analysis. The import of the model is that environmental impact (I) is a function of the level of population (P), affluence, economic (A), and technology (T). Mathematically, the argument of the model is specified as follows:

(1)

(1)

The variables I,P,A, and T remain as explained earlier, while a, β, λ, σ, δ and e are parameters to be estimated. However, given that the environmental issue of concern is the level of carbon dioxide (CO2) emissions (CO2E), it is used to replace I. Urbanization (UR) replaces P and by following Marfo et al. (Citation2023) trade openness (TR) replaces A. Dietz and Rosa (Citation1997) argue that technology is the way resources are transformed into output, as well as the socio-economic characteristics of an economy. Thus, based on the objective of this study, taxation (TX) and corporate finance (CF) are used to capture technology while controlling for government expenditure (GE). This leads to:

(2)

(2)

Taking the natural logarithm of EquationEquation (2)(2)

(2) to linearize it for a time-series model gives:

(3)

(3)

The t denotes the time (years) under consideration.

5.2. Data and estimation techniques

The data used in this study were obtained from the World Bank (Citation2018) and (Citation2023). While carbon dioxide emissions used data from World Bank (Citation2018) and World Bank (Citation2023) the rest of the data came from World Bank (Citation2023). Annual time series data for 1971–2021 period is utilized for the assessment. This period was chosen because of data availability. shows the measurement of each of the variables used.

Table 1. Measurement of variables.

The proxies for these variables were used in similar studies mentioned in the literature review section. The descriptive statistics and correlations of the variables are shown in .

Time-series data are usually not stationary because they may contain a unit root. An analysis using such data may yield inaccurate results. To avoid this problem, econometric analysis requires a unit root test to ascertain the stationarity of the variables. When the variables are not stationary at levels, the difference term is taken until stationarity is achieved. This study uses three tests to ascertain stationarity. These are the Augmented Dickey Fuller (ADF), Philips-Perron (PP), Zivot-Andrew (ZA), and unit root tests. The first two tests were among the earlier tests for this analysis. However, their inability to produce robust results in the presence of structural breaks led to the emergence of the ZA test.

Also, time-series variables tend to be cointegrated (long-run relationships among the series). An Autoregressive Distributed Lag (ARDL) cointegration test was employed for this analysis. The strength of the ARDL method is its ability to provide better results, even if there is a mixture of integrated variables of order zero I (0) or one I (1). Confirmation of long-run relationships among the variables allows regression analysis to be performed with cointegration regression techniques. The study uses the ARDL method to analyse the short and long run effects of corporate finance and tax on carbon dioxide emissions.

The ARDL framework is given as below:

(4)

(4)

where δ1 is the intercept and µ1t is error term; the short-run effects are denoted by the terms with the summation sign; the terms with σ are the long-run outcomes; ECTt-1 is the error correction term with coefficient ʋi representing the speed of adjustment to long-run equilibrium and Δ is a difference operator.

To ensure the robustness of results diagnostic analysis from the ARDL approach will be performed. In addition to that, other cointegration regression techniques namely the Fully Modified Ordinary Least Squares (FMOLS) and Canonical Cointegrating Regressions (CCR) will be used to assess the long run effects. The details of the mechanisms under which these methods work can be inferred from Park Joon, Phillips and Hansen (Citation1990), and Pesaran and Shin (Citation1995).

After assessing the effect of each variable on carbon emissions, the variance decomposition analysis will be employed to ascertain the contribution of each of the explanatory variables to the levels of carbon emission over the study period ().

Table 2. Variables descriptive statistics and correlation.

6. Results and discussion

6.1. Results on unit root and cointegration analysis

The stationarity analysis of the variables, as shown in , suggest that the variables are stationary at different orders. For instance, ZA, ADF, and PP show that government spending is stationary at levels, ZA indicates that urbanization is stationary at levels, and the remaining variables are stationary at first difference. Thus, the variables are a mixture of I(0) and I(1), which is necessary for the regression analysis. In , the cointegration analysis confirms that the variables have a long-term relationship. Thus, cointegration is confirmed between carbon dioxide emission and the regressors, suggesting that in the long run, carbon dioxide emissions in Ghana can be influenced by tax revenue, corporate finance, government expenditure, urbanization, and trade openness.

Table 3. Unit root results.

Table 4. Cointegration results.

6.2. Results on regression and variance decomposition analysis

6.2.1. Long and short run effects

The ARDL results in reveal that, in the short run, corporate finance, urban growth, tax revenue, and trade openness influence carbon emissions in Ghana. Specifically, while urbanization and tax increase carbon emissions, trade openness and corporate finance decrease emissions. A one percent increase corporate finance and trade openness leads to about 0.32 and 0.36% reduction in carbon dioxide emission respectively. On the other hand, when tax revenue and urbanization increase by one percent, carbon dioxide emission increases by 0.10 and 31.2% respectively. The effect of government expenditure is observed to be insignificant although it has a positive coefficient. The error correction term ECT(−1) captures the speed of adjustment from disequilibrium to equilibrium. The coefficient of −0.27 indicates that there is approximately 27% speed of adjustment to equilibrium. The negative value further confirms the long-run relationship between carbon emissions and explanatory variables.

Table 5. ARDL short run results (dependent variable = LCO2E).

In the long run, evidence from ARDL in shows that urbanization, government expenditure, trade openness, corporate finance, and tax have significant effect on carbon dioxide emissions. A positive effect is seen from corporate finance and tax whereas government expenditure, urbanization and trade openness reduce emissions. For corporate finance, any one percent increase leads to 0.71% of carbon dioxide emission in the long run. With tax a one percent increase causes carbon dioxide emissions to increase by 0.38%. For government expenditure, trade openness and urbanization, whenever it witnesses a one percent increase, carbon dioxide emissions reduce by about 1.1, 0.49 and 2.41%, respectively. It is observed that the effect of the variables is more inelastic in the short run than the long run period.

Table 6. ARDL long run results (dependent variable = L CO2E).

6.2.2. Diagnostic and robust analysis

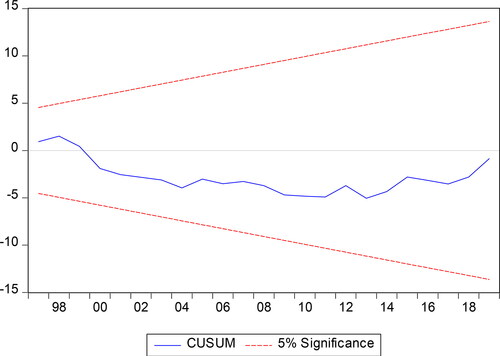

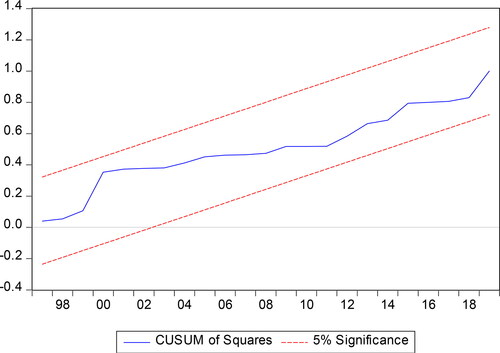

The results from the ARDL regression analysis are subjected to scrutiny to ensure robustness. The negative coefficient of the error correction term ECT(−1) shown in confirms the long-run relationship between carbon emissions and explanatory variables. The diagnostic tests in show that the carbon dioxide emission model is free from the problems of non-normality, non-stability, heteroscedasticity, and autocorrelation because the Jarque-Bera, Ramsey RESET, ARCH, and Breusch-Godfrey tests reject the null hypothesis of non-normality, non-stability, heteroscedasticity, and autocorrelation. and further demonstrate that the model is stable and robust. Consequently, the model is reliable for guiding policy formulation.

Figure 1. CUSUM results of model stability. Source: Author’s estimation.

Figure 2. CUSUM of squares results of stability. Source: Author’s estimation.

Table 7. Post regression diagnostic results.

Results from the FMOLS and CCR methods () also show all the explanatory variables except urbanization have significant effect on carbon emission. A positive effect is witnessed from corporate finance and tax confirming the ARDL outcome. Also, government expenditure and trade openness exert negative effect on carbon emission while urbanization has a positive although it is not significant statistically. The above results to a large extent support the evidence from the ARDL.

Table 8. FMOLS and CCR long run results (dependent variable = LCO2E).

6.2.3. Variance decomposition analysis

The results of the variance decomposition analysis to assess the extent to which each variable in the model affects carbon dioxide emission within the study period are reported in . The observation from the results is that over the period, the impact of each variable has been moderate, although many seem to witness an increasing trend regarding their contribution. For instance, in period five, the share of corporate finance increased from 6.67 to 13.1% in the twentieth period and 14.9% in the thirty fifth period. By the fiftieth period its share to carbon emission has reached 16.36%. Within the same period, the share of tax moved from 4.71% to 9.55%, 9.81% and finally to 13.03%. For urbanization its effect increased from 0.003% to 1.57% to 3.44%. The variable with the highest impact is urbanization, followed by corporate finance, tax revenue, trade openness and government expenditure have the least impact.

Table 9. Results of variance decomposition analysis.

6.3. Discussion on the role of taxation and corporate finance

The short run and long run positive effect of tax on carbon dioxide emissions in Ghana indicates that increasing taxes may be environmentally unfriendly in the country. Thus, high taxes may harm the quality of the environment instead of protecting it. A comparison of the coefficients shows that the short run effects are more inelastic than the long run effects. The relatively larger coefficient in the long run supports economic theory of elasticity. Thus, in the long run economic agents have ample time to respond to changes in tax yielding a greater effect that in the short run. In all, researchers have expressed that a tax imposition meant specifically for environmental protection can reduce environmental pollution, as reported in the empirical works of Alper (Citation2017) for European countries, Zhang et al. (Citation2023) for China and Sanderson et al. (Citation2023) for South Africa but Pretis (Citation2022) found some contradictory results for British Columbia. However, the results of this study suggest that tax imposition meant for raising revenue for the government may trigger environmental degradation through carbon dioxide emissions.

The observed outcome could be that high tax rates in the country place burdens on firms and individuals. As such, they are unable to access environmentally friendly goods for production or consumption activities. In addition, the positive effect of taxes on carbon emissions in Ghana could be linked to the fact that taxes in the country are largely not meant to address environmental challenges. Thus, while individuals and firms may be complaining about the economic cost of taxes in the country, the results reveal that taxes in the country have detrimental environmental effects as well. This finding is consistent with that reported by Ren et al. (Citation2021) and Pretis (Citation2022) and it confirms hypothesis 1.

The results revealed that corporate finance has a positive effect on carbon dioxide emissions in the long run but a negative effect in the short run. However, like the effect of taxation, the short run effect of corporate finance is more inelastic than the long run effect suggesting that the long run period allows corporate bodies ample time to use funds from financial institutions in ways that increase carbon emissions while in the short run the reverse occurs. This means that as more funds are given to corporate bodies for their activities, it helps to initially reduce carbon emissions when perhaps corporate bodies are able to access energy efficient tools for production (Alhassan et al., Citation2022). However, in the long corporate finance increasing environmental degradation through carbon emissions may be attributed to several reasons, including the fact that firms may have cheaper access to credit for expansion, which causes them to use more energy. In addition, easy accessibility to credit might have caused corporate entities in the country to purchase extra energy-intensive technology (Amuakwa-Mensah et al., Citation2018; Musah et al., Citation2023).

Furthermore, although financial institutions in the country might have increased corporate loans, the loans have not been directed towards firms that support clean energy production. This supports the financial curse proposition. As espoused by Kwakwa et al. (Citation2023), because financial institutions are profit-oriented, they would prefer to support dirty industries that have a short-term capacity to pay back rather than firms that are in renewable energy and clean technologies that are associated with long-term returns. This could explain why green finance is low in the country (Owusu-Manu et al., Citation2021). The findings are in line with those of Tsaurai (Citation2019) and Mesagan et al. (Citation2022). In the long run the results supports hypothesis 2.

6.4. Discussion on the role of trade, urbanization and government expenditure

Trade openness reduces carbon dioxide emissions in both the short run and long run periods. Trade openness promotes competitiveness and transfer of technologies that can lower the rate of carbon emissions (Chhabra et al., Citation2022). The positive effect of trade openness sends a signal that Ghana’s engagement with the international community in terms of trade to be more affluent as a nation helps promote environmental quality.

Urbanization is found to exert a negative effect on carbon emissions in both short- and long-run periods, indicating that it is helpful in promoting environmental quality in Ghana. Ghana’s urban population and towns continues to increase (Adams & Klobodu, Citation2017; World Bank, Citation2023). Although one would have thought this could lead to higher carbon dioxide emissions, the observed finding can be attributed to the compact city theory or the economies of conglomeration. Studies by Adebayo and Ullah (Citation2024) and Yan et al. (Citation2023) have found similar outcomes.

Government expenditure reduces carbon emissions in both the short and the long run. Recently, Ghana’s expenditure trend has raised eyebrows among Ghanaians, especially when it has partly led to higher public debt. Media discussions have centered on the economic effect of such high expenses, with little attention given to environmental costs (Kwakwa, Citation2022). However, the results indicate that the government of Ghana’s expenditure has some environmental quality-enhancing effect, as found in other studies such as Xi et al. (Citation2023), Wu and Song (Citation2023), and Azam et al. (Citation2023).

7. Conclusion and policy implications

7.1. Conclusion

Achieving a low-carbon economy is a global agenda to address climate change. Both developing and developed countries have played a role in the realization of this dream. Therefore, researchers have sought to identify the driving forces behind carbon dioxide emissions. Various factors have been considered in previous studies. However, despite the possible carbon emission effects of taxation and corporate finance mentioned in the literature, empirical analysis of the same is limited in African, especially for Ghana. Given that the government of Ghana has increased taxes and the pace of corporate finance from financial institutions is increasing, this study analyzed how the two can influence the low-carbon economic agenda in the country. Based on the STIRPAT model and relying on data from 1971 to 2021, carbon emissions were modelled as a function urbanization, government expenditure, trade openness, corporate finance, and taxation. Regression from ARDL, FMOLS, and CCR provides evidence of a long-term positive influence of taxation and corporate finance. However, trade openness, urbanization and government expenditures have carbon emission-reducing effects in the long term. In the short run, trade and corporate finding reduce carbon emissions while tax has the opposite effect. Also, the effect of the short run is more inelastic than the long run effects. A variance decomposition analysis shows that over the period urbanization, corporate finance, tax revenue are the top three factors influencing changes in the level of carbon emissions. Overall, it is deduced that efforts to address carbon dioxide emission needs to pay attention to taxation, government spending, trade openness and corporate finance.

7.2. Implications

The implications of the results are as follows.

Theoretically, this study contributes to the robustness of the STIRPAT model as a predictor of the environmental quality. This emerges from the significant effects of the variables in the regression results as well as the outcome of the post-regression diagnostic analysis. Therefore, it is important for researchers to pay attention to taxation and corporate finance in their analysis of the drivers of carbon dioxide emissions. Towards the attainment of SDGs the results imply that taxes and corporate financing have a crucial role to play.

The industrial or practical implication is that the more financial firms provide credit support to corporate firms, the lower the environmental quality. Therefore, it is necessary for financial institutions to be circumspective when providing financial support. It would be appropriate if they reconsidered environmental sustainability along with their profit motives. In such cases, they will balance giving credit to environmentally polluting firms yet very profitable to service their loans in a short period of time with environmentally clean firms that require longer time to service their loans. Financial institutions should also be motivated to set aside special funds to support green activities.

Tax revenue noted to increase carbon emissions means that the more tax is imposed to raise revenue, the more environmental quality is reduced via carbon emissions. Owing to its importance in the growth and development process, it may be difficult to abandon taxes completely in the country. Rather, there should be reforms or restructuring of the tax system. Therefore, it is important to ensure that the tax imposition that triggers environmentally unfriendly behavior is reduced. Since Ghana does not have an explicit tax on carbon emissions, it is about time that the option is pursued to reduce carbon emissions. Portions of tax revenues may be channeled to areas such as research and development as well as technological innovation that would reduce energy intensity and improve environmental quality.

Government expenditure reported to reduce carbon emissions in the long run signals that expenditure by the government has been environmentally friendly and needs to be continued although initially it may not yield significant effect. It is important for the government to have robust checks and balances to ensure that its spending pattern does not negatively influence the environment. In the case of urbanization, although it currently helps to reduce carbon emissions, there should be innovative ways of reducing traffic congestion in urban towns. Carpooling is not a common feature in urban Ghana. Authorities should encourage this practice to ensure that urban growth continues to reduce carbon emission. Trade policies in the country must be aligned with environmental quality. This will contribute to ensuring that trade openness helps reduce carbon emissions in the country.

7.3. Limitation and suggestions for future studies

This study has some limitations that future studies should consider. The analysis carried out in this study uses the credit given to the private sector. In the future, when data become available, a disaggregated analysis should be conducted to ascertain how corporate finance in specific sectors affects carbon emissions.

The availability of data in the future should also warrant studies that examine how various taxes in the country affect other forms of environmental degradation, including water pollution, deforestation, and indiscriminate waste disposal. Other analyses can focus on how various taxes in a country affect carbon emissions. Further studies can address the effect of taxes on carbon emissions emanating from various sectors, such as the residential, industrial, and transport sectors. In addition, since the study focused on aspects of fiscal policy in Ghana, future studies could consider the carbon emission effects of monetary policy.

Ethical approval

I declare no human participant was used for the study

Table_and_figure.docx

Download MS Word (46.9 KB)clean copy of manuscript QABM-2023-0640.R1.doc

Download MS Word (150 KB)Acknowledgment

No funding was received for this research.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

Data was obtained from World Bank (Citation2023) World Development Indicators. https://databank.worldbank.org/source/world-development-indicators#

Additional information

Notes on contributors

Paul Adjei Kwakwa

Paul Adjei Kwakwa is a senior lecturer with the University of energy and natural Resources. He teaches economics-related subjects. his interests focus on economic sustainable development, and environmental and resource economics. His recent articles have appeared in the Journal of environmental Management, cogent Business and Management, and Research in globalization.

References

- Abokyi, E., Appiah-Konadu, P., Abokyi, F., & Oteng-Abayie, E. F. (2019). Industrial growth and emissions of CO2 in Ghana: The role of financial development and fossil fuel consumption. Energy Reports, 5, 1–18. https://doi.org/10.1016/j.egyr.2019.09.002

- Abokyi, E., Appiah-Konadu, P., Tangato, K. F., Abokyi, F., & Electricity Consumption, E. (2021). (2017). Analysis of carbon tax on selected European countries: Does carbon tax reduce emissions. Applied Economics and Finance, 5(1), 29–36.

- Adams, S., Adom, P. K., & Klobodu, E. K. M. (2016). Urbanization, regime type and durability, and environmental degradation in Ghana. Environmental Science and Pollution Research International, 23(23), 23825–23839. https://doi.org/10.1007/s11356-016-7513-4

- Adams, S., & Klobodu, E. K. M. (2017). Urbanization, democracy, bureaucratic quality, and environmental degradation. Journal of Policy Modeling, 39(6), 1035–1051. https://doi.org/10.1016/j.jpolmod.2017.04.006

- Adebayo, T. S., & Ullah, S. (2024). Towards a sustainable future: the role of energy efficiency, renewable energy, and urbanization in limiting CO2 emissions in Sweden. Sustainable Development, 32(1), 244-259. https://doi.org/10.1002/sd.2658

- Adefolake, A. O., & Omodero, C. O. (2022). Tax revenue and economic growth in Nigeria. Cogent Business & Management, 9(1), 2115282. https://doi.org/10.1080/23311975.2022.2115282

- Agusti, R. R., & Rahman, A. F. (2023). Determinants of tax attitude in small and medium enterprises: Evidence from Indonesia. Cogent Business & Management, 10(1), 2160585. https://doi.org/10.1080/23311975.2022.2160585

- Alhassan, H., Kwakwa, P. A., & Donkoh, S. A. (2022). The interrelationships among financial development, economic growth and environmental sustainability: Evidence from Ghana. Environmental Science and Pollution Research International, 29(24), 37057–37070. https://doi.org/10.1007/s11356-021-17963-9

- Alhassan, H., Kwakwa, P. A., & Owusu-Sekyere, E. (2020). Households’ source separation behaviour and solid waste disposal options in Ghana’s Millennium City. Journal of Environmental Management, 259, 110055. https://doi.org/10.1016/j.jenvman.2019.110055

- Alper, A. E. (2017). Analysis of carbon tax on selected European countries: Does carbon tax reduce emissions. Applied Economics and Finance, 5(1), 29–36.

- Amankwaah, E., & Baidoo, N. O. (2023). Effect of firm size and corruption on financial challenges of savings and loans companies: Evidence from Ghana. Social Sciences & Humanities Open, 8(1), 100552. https://doi.org/10.1016/j.ssaho.2023.100552

- Amuakwa-Mensah, F., Klege, R. A., Adom, P. K., Amoah, A., & Hagan, E. (2018). Unveiling the energy saving role of banking performance in Sub-Sahara Africa. Energy Economics, 74, 828–842. https://doi.org/10.1016/j.eneco.2018.07.031

- Appiah, K., Appah, R., Mintah, O. K., & Yeboah, B. (2021). Economic growth, industrialization, trade, electricity production and carbon dioxide emissions: Evidence from Ghana. Journal of Economic Science Research, 4(1), 31–43. https://doi.org/10.30564/jesr.v4i1.2716

- Attrams, A. S., & Tshehla, M. (2022). Collateral ability of small and medium-sized enterprises financing in a developing country. Journal of the International Council for Small Business, 3(3), 237–245. https://doi.org/10.1080/26437015.2021.1982370

- Azam, W., Khan, I., & Ali, S. A. (2023). Alternative energy and natural resources in determining environmental sustainability: A look at the role of government final consumption expenditures in France. Environmental Science and Pollution Research International, 30(1), 1949–1965. https://doi.org/10.1007/s11356-022-22334-z

- BBC. (2023). Wetin be di three new taxes Ghana. Parliament pass and how e go affect citizens. https://www.bbc.com/pidgin/articles/c6pq9m709zdo.

- Bekele, T. D., & Degu, A. A. (2023). The effect of financial sector development on economic growth of selected sub-Saharan Africa countries. International Journal of Finance & Economics, 28(3), 2834–2842.

- Chekouri, S. M., Chibi, A., & Benbouziane, M. (2020). Examining the driving factors of CO2 emissions using the STIRPAT model: the case of Algeria. International Journal of Sustainable Energy, 39(10), 927–940. https://doi.org/10.1080/14786451.2020.1770758

- Chhabra, M., Giri, A. K., & Kumar, A. (2022). Do technological innovations and trade openness reduce CO2 emissions? Evidence from selected middle-income countries. Environmental Science and Pollution Research International, 29(43), 65723–65738. https://doi.org/10.1007/s11356-022-20434-4

- Chien, F., Sadiq, M., Nawaz, M. A., Hussain, M. S., Tran, T. D., & Le Thanh, T. (2021). A step toward reducing air pollution in top Asian economies: The role of green energy, eco-innovation, and environmental taxes. Journal of Environmental Management, 297, 113420. https://doi.org/10.1016/j.jenvman.2021.113420

- Degirmenci, T., & Aydin, M. (2023). The effects of environmental taxes on environmental pollution and unemployment: A panel co-integration analysis on the validity of double dividend hypothesis for selected African countries. International Journal of Finance & Economics, 28(3), 2231–2238. https://doi.org/10.1002/ijfe.2505

- Dietz, T., & Rosa, E. A. (1997). Effects of population and affluence on CO2 emissions. Proceedings of the National Academy of Sciences of the United States of America, 94(1), 175–179. https://doi.org/10.1073/pnas.94.1.175

- Domon, S., Hirota, M., Kono, T., Managi, S., & Matsuki, Y. (2022). The long-run effects of congestion tolls, carbon tax, and land use regulations on urban CO2 emissions. Regional Science and Urban Economics, 92, 103750. https://doi.org/10.1016/j.regsciurbeco.2021.103750

- Egbunike, F. C., Emudainohwo, O. B., & Gunardi, A. (2018). Tax revenue and economic growth: A study of Nigeria and Ghana. Signifikan: Jurnal Ilmu Ekonomi, 7(2), 213–220. https://doi.org/10.15408/sjie.v7i2.7341

- Friedlingstein, P., O’Sullivan, M., Jones, M. W., Andrew, R. M., Gregor, L., Hauck, J., Le Quere, C., Luijkx, I. T., Olsen, A., Peters, G. P., Peters, W., Pongratz, J., Schwingshackl, C., Sitch, S., Canadell, J. G., Ciais, P., Jackson, R. B., Alin, S. R., Alkama, R., … Zheng, B. (2022). “Global carbon Budget 2022”. Earth System Science Data, 14(11), 4811–4900.

- Gale, W. G., & Samwick, A. A. (2017). Effects of income tax changes on economic growth. In: Auerbach, A. J. and Smetters, K. (Eds.), The Economics of Tax Policy. New York: Oxford University Press.

- Guo, B., Wang, Y., Feng, Y., Liang, C., Tang, L., Yao, X., & Hu, F. (2022). The effects of environmental tax reform on urban air pollution: A quasi-natural experiment based on the Environmental Protection Tax Law. Frontiers in Public Health, 10, 967524. https://doi.org/10.3389/fpubh.2022.967524

- Halkos, G. E., & Paizanos, E. Α. (2016). The effects of fiscal policy on CO2 emissions: evidence from the USA. Energy Policy, 88, 317–328. https://doi.org/10.1016/j.enpol.2015.10.035

- Hammond, P., Kwakwa, P. A., Berko, D., & Amissah, E. (2023). Taxing informal sector through modified taxation: Implementation challenges and overcoming strategies. Cogent Business & Management, 10(3), 2274172. https://doi.org/10.1080/23311975.2023.2274172

- He, P., Ning, J., Yu, Z., Xiong, H., Shen, H., & Jin, H. (2019). Can environmental tax policy really help to reduce pollutant emissions? An empirical study of a panel ARDL model based on OECD countries and China. Sustainability, 11(16), 4384. https://doi.org/10.3390/su11164384

- Ho, T. T., Tran, X. H., & Nguyen, Q. K. (2023). Tax revenue-economic growth relationship and the role of trade openness in developing countries. Cogent Business & Management, 10(2), 2213959. https://doi.org/10.1080/23311975.2023.2213959

- Hussain, S., Ahmad, T., Ullah, S., Rehman, A. U., & Shahzad, S. J. H. (2024). Financial inclusion and carbon emissions in Asia: Implications for environmental sustainability. Economic and Political Studies, 12(1), 88–104. https://doi.org/10.1080/20954816.2023.2273003

- Kamasa, K., Nortey, D. N., Boateng, F., & Bonuedi, I. (2022). Impact of tax reforms on revenue mobilisation in developing economies: Empirical evidence from Ghana. Journal of Economic and Administrative Sciences. https://doi.org/10.1108/JEAS-01-2022-0011

- Katircioglu, S., & Katircioglu, S. (2018). Testing the role of fiscal policy in the environmental degradation: The case of Turkey. Environmental Science and Pollution Research International, 25(6), 5616–5630. https://doi.org/10.1007/s11356-017-0906-1

- Kwakwa, P. A. (2020). The long-run effects of energy use, urbanization and financial development on carbon dioxide emissions. International Journal of Energy Sector Management, 14(6), 1405–1424. https://doi.org/10.1108/IJESM-01-2020-0013

- Kwakwa, P. A. (2022). The effect of industrialization, militarization, and government expenditure on carbon dioxide emissions in Ghana. Environmental Science and Pollution Research International, 29(56), 85229–85242. https://doi.org/10.1007/s11356-022-21187-w

- Kwakwa, P. A. (2023). Climate change mitigation role of renewable energy consumption: Does institutional quality matter in the case of reducing Africa’s carbon dioxide emissions? Journal of Environmental Management, 342, 118234. https://doi.org/10.1016/j.jenvman.2023.118234

- Kwakwa, P. A., Adzawla, W., Alhassan, H., & Oteng-Abayie, E. F. (2023). The effects of urbanization, ICT, fertilizer usage, and foreign direct investment on carbon dioxide emissions in Ghana. Environmental Science and Pollution Research International, 30(9), 23982–23996. https://doi.org/10.1007/s11356-022-23765-4

- Li, Z., Murshed, M., & Yan, P. (2023). Driving force analysis and prediction of ecological footprint in urban agglomeration based on extended STIRPAT model and shared socioeconomic pathways (SSPs). Journal of Cleaner Production, 383, 135424. https://doi.org/10.1016/j.jclepro.2022.135424

- Ling, G., Razzaq, A., Guo, Y., Fatima, T., & Shahzad, F. (2022). Asymmetric and time-varying linkages between carbon emissions, globalization, natural resources and financial development in China. Environment, Development and Sustainability, 24(5), 6702–6730. https://doi.org/10.1007/s10668-021-01724-2

- Li, S., Samour, A., Irfan, M., & Ali, M. (2023). Role of renewable energy and fiscal policy on trade adjusted carbon emissions: Evaluating the role of environmental policy stringency. Renewable Energy, 205, 156–165. https://doi.org/10.1016/j.renene.2023.01.047

- Lv, T., Hu, H., Xie, H., Zhang, X., Wang, L., & Shen, X. (2023). An empirical relationship between urbanization and carbon emissions in an ecological civilization demonstration area of China based on the STIRPAT model. Environment, Development and Sustainability, 25(3), 2465–2486. https://doi.org/10.1007/s10668-022-02144-6

- Lyu, X., Shan, C., & Tang, D. Y. (2022). Corporate finance and firm pollution. Available at SSRN: https://ssrn.com/abstract=3805629 or http://dx.doi.org/10.2139/ssrn.3805629

- Ma, H., Liu, Y., Li, Z., & Wang, Q. (2022). Influencing factors and multi-scenario prediction of China’s ecological footprint based on the STIRPAT model. Ecological Informatics, 69, 101664. https://doi.org/10.1016/j.ecoinf.2022.101664

- Marfo, E. O., Kwakwa, P. A., Aboagye, S., & Ansu-Mensah, P. (2023). The role of female population, urbanization and trade openness in sustainable environment: The case of carbon dioxide emissions in Ghana. Cogent Economics & Finance, 11(2), 2246318. https://doi.org/10.1080/23322039.2023.2246318

- Mesagan, E. P., Adewuyi, T. C., & Olaoye, O. (2022). Corporate finance, industrial performance and environment in Africa: Lessons for policy. Scientific African, 16, e01207. https://doi.org/10.1016/j.sciaf.2022.e01207

- Musah, M., Owusu-Akomeah, M., Nyeadi, J. D., Alfred, M., & Mensah, I. A. (2022). RETRACTED ARTICLE: Financial development and environmental sustainability in West Africa: evidence from heterogeneous and cross-sectionally correlated models. Environmental Science and Pollution Research, 29(8), 12313–12335.

- Musah, M., Gyamfi, B. A., Kwakwa, P. A., & Agozie, D. Q. (2023). Realizing the 2050 Paris climate agreement in West Africa: The role of financial inclusion and green investments. Journal of Environmental Management, 340, 117911. https://doi.org/10.1016/j.jenvman.2023.117911

- Nwani, C., & Omoke, P. C. (2020). Does bank credit to the private sector promote low-carbon development in Brazil? An extended STIRPAT analysis using dynamic ARDL simulations. Environmental Science and Pollution Research International, 27(25), 31408–31426. https://doi.org/10.1007/s11356-020-09415-7

- Ojo, A. O., & Shittu, S. A. (2023). Value added tax compliance, and small and medium enterprises (SMEs): Analysis of influential factors in Nigeria. Cogent Business & Management, 10(2), 2228553. https://doi.org/10.1080/23311975.2023.2228553

- Opuala, C. S., Omoke, P. C., & Uche, E. (2023). Sustainable environment in West Africa: the roles of financial development, energy consumption, trade openness, urbanization and natural resource depletion. International Journal of Environmental Science and Technology, 20(1), 423–436. https://doi.org/10.1007/s13762-022-04019-9

- Owusu, P. A., & Asumadu-Sarkodie, S. (2016). Is there a causal effect between agricultural production and carbon dioxide emissions in Ghana? Environmental Engineering Research, 22(1), 40–54. https://doi.org/10.4491/eer.2016.092

- Owusu-Manu, D. G., Mankata, L. M., Debrah, C., Edwards, D. J., & Martek, I. (2021). Mechanisms and challenges in financing renewable energy projects in sub-Saharan Africa: A Ghanaian perspective. Journal of Financial Management of Property and Construction, 26(3), 319–336. https://doi.org/10.1108/JFMPC-03-2020-0014

- Peng, B., Yan, W., Elahi, E., & Wan, A. (2022). Does the green credit policy affect the scale of corporate debt financing? Evidence from listed companies in heavy pollution industries in China. Environmental Science and Pollution Research International, 29(1), 755–767. https://doi.org/10.1007/s11356-021-15587-7

- Pesaran, M. H., & Shin, Y. (1995). An autoregressive distributed lag modelling approach to cointegration analysis. (Vol. 9514). Department of Applied Economics, University of Cambridge.

- Phillips, P. C. B., & Hansen, B. E. (1990). (1990). Statistical inference in instrumental variables regression with I(1) processes. The Review of Economic Studies, 57(1), 99–125. https://doi.org/10.2307/2297545

- Pretis, F. (2022). Does a carbon tax reduce CO2 emissions? Evidence from British Columbia. Environmental and Resource Economics, 83(1), 115–144. https://doi.org/10.1007/s10640-022-00679-w

- PWC. (2023). Ghana Corporate - Significant developments. Available at https://taxsummaries.pwc.com/ghana/corporate/significant-developments.

- Ren, Y., Jiang, Y., Ma, C., Liu, J., & Chen, J. (2021). Will tax burden be a stumbling block to carbon-emission reduction? Evidence from OECD countries. Journal of Systems Science and Information, 9(4), 335–355. https://doi.org/10.21078/JSSI-2021-335-21s

- Ricky-Okine, R. O., Tetteh, F. K., & Twum, A. (2023). Is fiscal policy responsible for the high debt levels in Ghana? ADRRI Journal of Arts and Social Sciences, 20(2), 39–57.

- Rotimi, O, Federal University, Oye-Ekiti, Nigeria. (2021). Environmental tax and pollution control in Nigeria. Kampala International University Interdisciplinary Journal of Humanities and Social Sciences, 2(1), 280–301. https://doi.org/10.59568/KIJHUS-2021-2-1-17

- Sanderson, A., Mukarati, J., Jeke, L., & Le Roux, P. (2023). Carbon tax and environmental quality in South Africa. International Journal of Energy Economics and Policy, 13(2), 484–488. https://doi.org/10.32479/ijeep.13474

- Sandow, J. N., Duodu, E., & Oteng-Abayie, E. F. (2021). Regulatory capital requirements and bank performance in Ghana: Evidence from panel corrected standard error. Cogent Economics & Finance, 9(1), 2003503. https://doi.org/10.1080/23322039.2021.2003503

- Smith, S. (1992). Taxation and the environment: A survey. Fiscal Studies, 13(4), 21–57. https://doi.org/10.1111/j.1475-5890.1992.tb00505.x

- Soku, M. G., Amidu, M., & William, C. (2023). Environmental tax, carbon emission and female economic inclusion. Cogent Business & Management, 10(2), 2210355. https://doi.org/10.1080/23311975.2023.2210355

- Sun, C., & Zeng, Y. (2023). Does the green credit policy affect the carbon emissions of heavily polluting enterprises? Energy Policy, 180, 113679. https://doi.org/10.1016/j.enpol.2023.113679

- Takumah, W., & Iyke, B. N. (2017). The links between economic growth and tax revenue in Ghana: an empirical investigation. International Journal of Sustainable Economy, 9(1), 34–55. https://doi.org/10.1504/IJSE.2017.080856

- Tanzi, V. (1982). Tax increases and the price level. Finance and Development, 19(3), 27–30.

- Telatar, O. M., & Birinci, N. (2022). The effects of environmental tax on ecological footprint and carbon dioxide emissions: A nonlinear cointegration analysis on Turkey. Environmental Science and Pollution Research International, 29(29), 44335–44347. https://doi.org/10.1007/s11356-022-18740-y

- Tsaurai, K. (2019). The impact of financial development on carbon emissions in Africa. International Journal of Energy Economics and Policy, 9(3), 144–153. https://doi.org/10.32479/ijeep.7073

- Twerefou, D. K., Adusah-Poku, F., & Bekoe, W. (2016). An empirical examination of the Environmental Kuznets Curve hypothesis for carbon dioxide emissions in Ghana: an ARDL approach. Environmental & Socio-Economic Studies, 4(4), 1–12. https://doi.org/10.1515/environ-2016-0019

- Wahab, N. S. A., Ntim, C. G., Adnan, M. M. M., & Tye, W. L. (2018). Top management team heterogeneity, governance changes and book-tax differences. Journal of International Accounting, Auditing and Taxation, 32, 30–46. https://doi.org/10.1016/j.intaccaudtax.2018.07.002

- Wahab, N. S. A., Ntim, C. G., Tye, W. L., & Shakil, M. H. (2022). Book-tax differences and risk: Does shareholder activism matter? Journal of International Accounting, Auditing and Taxation, 48, 100484. https://doi.org/10.1016/j.intaccaudtax.2022.100484

- Wolde-Rufael, Y., & Mulat-Weldemeskel, E. (2022). The moderating role of environmental tax and renewable energy in CO2 emissions in Latin America and Caribbean countries: Evidence from method of moments quantile regression. Environmental Challenges, 6, 100412. https://doi.org/10.1016/j.envc.2021.100412

- Wolde-Rufael, Y., & Mulat-Weldemeskel, E. (2021). Do environmental taxes and environmental stringency policies reduce CO2 emissions? Evidence from 7 emerging economies. Environmental Science and Pollution Research International, 28(18), 22392–22408. https://doi.org/10.1007/s11356-020-11475-8

- World Bank. (2018). “World development indicators”. Available at: https://databank.worldbank.org/source/world-development-indicators# Accessed on June 5, 2018

- World Bank. (2023). World development indicators. https://databank.worldbank.org/source/world-development-indicators#

- Wu, D., & Song, W. (2023). Does green finance and ICT matter for sustainable development: role of government expenditure and renewable energy investment. Environmental Science and Pollution Research International, 30(13), 36422–36438. https://doi.org/10.1007/s11356-022-24649-3

- Xi, M., Wang, D., & Xiang, Y. (2023). Fiscal expenditure on sports and regional carbon emissions: Evidence from China. Sustainability, 15(9), 7595. https://doi.org/10.3390/su15097595

- Xu, Y., Wen, S., & Tao, C. Q. (2023). Impact of environmental tax on pollution control: A sustainable development perspective. Economic Analysis and Policy, 79, 89–106. https://doi.org/10.1016/j.eap.2023.06.006

- Yan, J., Dong, Q., Wu, Y., Yang, H., & Liu, X. (2023). The impact of urbanization on carbon emissions from perspective of residential consumption. Polish Journal of Environmental Studies, 32(3), 2393–2403. https://doi.org/10.15244/pjoes/160193

- York, R., Rosa, E. A., & Dietz, T. (2003). A rift in modernity? Assessing the anthropogenic sources of global climate change with the STIRPAT model. International Journal of Sociology and Social Policy, 23(10), 31–51. https://doi.org/10.1108/01443330310790291

- Yu, S., Zhang, Q., Hao, J. L., Ma, W., Sun, Y., Wang, X., & Song, Y. (2023). Development of an extended STIRPAT model to assess the driving factors of household carbon dioxide emissions in China. Journal of Environmental Management, 325(Pt A), 116502. https://doi.org/10.1016/j.jenvman.2022.116502

- Yuelan, P., Akbar, M. W., Zia, Z., & Arshad, M. I. (2022). Exploring the nexus between tax revenues, government expenditures, and climate change: Empirical evidence from belt and road initiative countries. Economic Change and Restructuring, 55(3), 1365–1395. https://doi.org/10.1007/s10644-021-09349-1

- Zhang, W., Hong, M., Li, J., & Li, F. (2021). An examination of green credit promoting carbon dioxide emissions reduction: A provincial panel analysis of China. Sustainability, 13(13), 7148. https://doi.org/10.3390/su13137148

- Zhang, Y., Khan, I., & Zafar, M. W. (2022). Assessing environmental quality through natural resources, energy resources, and tax revenues. Environmental Science and Pollution Research International, 29(59), 89029–89044. https://doi.org/10.1007/s11356-022-22005-z

- Zhang, Y., Xia, F., & Zhang, B. (2023). Can raising environmental tax reduce industrial water pollution? Firm-level evidence from China. Environmental Impact Assessment Review, 101, 107155. https://doi.org/10.1016/j.eiar.2023.107155