?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The article analyzes the impact of the establishment of the Indonesia Deposit Insurance Corporation (IDIC) on financial intermediation in Indonesia. The research uses technical analysis and multiple regression data analysis techniques. Results indicated that in the immediacy of IDIC establishment risk aversion increased among savers and banks alike, as reflected by a shift in the composition of bank deposits from time deposits and demand deposits to savings deposits and rising levels of Bank Indonesia certificates held by banks, respectively. However, increase in bank soundness, coupled with confidence in IDIC effectiveness, while mitigates risk-aversion behavior, it seems to have created opportunity for moral hazard in the banking system. Savers’ behavior is no longer driven by consideration of whether or not the potential custodians of their deposits are sound or other, but expected return (interest rate on deposits offered). The same applies to banks, which no longer consider risk-free Bank Indonesia certificates as a good investment. Risk-taking behavior by savers and banks alike seems to be strengthened by expectations of future government intervention for systemically important banks, raising fears of too systemically important to fail problem and continued political intervention in IDIC policymaking. Overall, IDIC establishment by bolstering public confidence in the banking system has reduced the possibility of a repeat of highly destabilizing runs on banks, hence has contributed to better financial intermediation and financial stability. However, rising moral hazard means that future bailouts are still unavoidable.

Public Interest Statement

The establishment of the Indonesian Deposit Insurance Corporation (IDIC) was aimed to prevent a repeat of financial instability that occurred in the aftermath of 1997/1998 economic crisis. The article analyzes the impact of IDIC establishment on the behavior of commercial banks, savers, and borrowers. Results showed an increase in bank deposits and bank credit. In the immediate aftermath of IDIC establishment, while bank deposit level remained unchanged, its composition showed a shift from time and demand deposits to saving deposits with balance that fell within the threshold of IDIC program. Savers also indicated preference for deposit savings in state-owned banks and foreign exchange banks over national private banks and regional development banks. Such behavior seems to wane in the medium term, which attests to restoration of public confidence in the capacity of the banking system to provide safe custodianship for their hard-earned savings. Admittedly, IDIC establishment enhances bank intermediation but also increases the possibility of moral hazard problems from savers, borrowers, commercial banks, and IDIC in the long term. Mitigating such problems is the best way to enhance IDIC program effectiveness in future.

1. Introduction

Financial institutions are crucial for growth and development, which is why the level of advancement and soundness of financial markets, is considered an important determinant of the enterpreneurship growth, innovations and productivity (Schumpeter, Citation1912); fosters industrialization (Hicks, Citation1969); growth and development of financial institutions and markets is inextricably linked to the development process itself (Claus, Jaconsen & Jera, Citation2004), and level of financial development is a “good predictor of economic growth, capital accumulation, technological advancement”(Levine, 1997). The banking sector dominates the financial sector in developing countries in terms of assets, hence they form the core of financial intermediation function. Nonetheless, the commercial banking business model is highly leveraged as it attracts short-term third-party funds at lower cost, transforming them into long-term securities (Gertler, Citation1988), which are subsequently sold to creditors earning the bank higher return. With experience coupled with regulation on prudential banking, banks at any point in time keep just a small percentage of third-party funds they mobilize to meet daily expected cash withdrawals, while investing the remainder in long-term assets that include loans, bonds, and other financial securities. The foregoing encapsulates the working of a fractional reserve banking system (Cochran, Call, & Glahe, Citation1999; O’Leary, undated; Gray, Citation2011). The problem is that the bank faces maturity transformation risk because in the event there is a surge in demand for cash withdrawals that is attributable to depositors fearing losing their money, rush to the bank in droves to withdraw their money (bank runs) not in only one bank but in a wave that affects many banks in the financial system.Footnote1 That creates a serious problem that forces banks to first seek assistance from other banks through interbank market, then lender of last resort, and finally if all that fails to deliver, resorting to selling assets at fire sales, recall loans before maturity, among other efforts, all of which undermine their solvency in the process. Banks dominate the financial sector in developing, and to a large extent transition economies in terms of assets, hence they form the core of financial intermediation services in the financial sector (Scholtens & Wensveen, Citation2003), by providing saving services to surplus spending units (savers), and the backbone of the financial services intermediation by taking deposits (savings) from surplus spending units (savers), and lending it out loans to deficit spending units (investors). Thus, besides the rate of return, guaranteeing the safety of third-party deposits is one of the key factors that influence a saver’s decision to put money in a depository institution other than other financial institutions. This underscores the need for stability, which is one of the reasons underlying deposit protection. Deposit insurance schemes have mainly two goals: (1) reduce the risk to savers of losing their savings in the event of bank failures by precluding the need for depositors to run on banks. This reduces the cost banks, financial system, and economy would incur in meeting sudden surges in demand for cash and reduces potential risk of disruption to financial intermediation. Related to the first, (2) deposit insurance aims at instilling public confidence in the banking system, and financial system, which ensures financial stability, while at the same time minimizing potential cost from moral hazard, principal agency, and adverse selection problems.

By averting the need for owners of demand deposits to make sudden withdrawals of their deposits at higher-than-normal levels, which would cause liquidity problem for banks as they scurry for funds to meet higher-than-normal cash demand, would in turn cause financial problems for non-financial sector. The importance of deposit insurance has become so vital for financial stability that many now consider it to be a "logical step in strengthening the financial sector's infrastructure (Frolov, Citation2004). Incontrovertible evidence succinctly points to the many benefits of a well-designed explicit deposit insurance scheme, including lowering transaction cost, fosters the smooth running of the payments system, enhances efficiency in resource allocation, increases public trust (confidence) in the banking system that is vital for stable financial intermediation, bolsters enterprise growth, innovations, productivity and production of goods and services, fosters industrialization (Hicks, 1989), all of which contribute to higher economic growth (Demirgüç-Kunt & Kane, Citation2002). Stable and predictable financial stability strengthens financial stability that is essential for financial innovation. Financial innovation, in turn creates conducive conditions for financial deepening, which enhances economic development (Shaw, Citation1973; Gross, Citation2001; McKinnon, Citation1973; Fry, Citation1978; Taguch, Citation1993; Demirguc-Kunt & Ross, Citation2001; Kiyotaki & Moore, Citation2005).

The objectives of this research are (1) to determine the influence that the Indonesia Deposit Insurance Corporation (IDIC) establishment has had on the behavior of depositors and commercial banks; and (2) determine whether or not IDIC establishment has contributed to financial stability. Results show that the phased transition from a full blanket guarantee scheme to a limited deposit guarantee scheme initially induced risk aversion of depositors and banks in the short term but returned to normality as the full-fledged insurance scheme became operational and trust in the banking system and IDIC strengthened in the medium term and beyond. Nonetheless, the phased nature of the deposits scheme, while intended to minimize the destabilizing effect on financial intermediation, induced excessive risk aversion initially and moral hazard once all the provisions of the limited deposit insurance scheme were phased in. With restoration of public confidence in the banking system, depositors no longer showed keen interest in differentiating banks by risk profile (moral hazard) as their deposits were guaranteed. Another implication that is ironically linked to the success of IDIC is the impact that heightened risk aversion of banks had on lending in general and to risky sectors in particular. Premiums participating banks pay, besides having to meet the criteria of deposits preset by IDIC, are also dependent on bank risk profiles. Lending, while vital for the economy, is a major source of risk for banks not only with respect to insurance premiums they pay but also risk-weighted capital and liquidity they are required to put in place, all of which lower profitability, and return. One of the principal aims of IDIC was to reduce the cost of troubled banks on state coffers as bailouts are effected from accumulated premiums. Nonetheless, as the case of Bank Century showed, politics continues to play an important role in decisions that IDIC makes with respect to providing capital injections, restoration, and recovery for troubled banks. While the criteria of systemically important banks are theoretically clear, in practice it remains a gray area that lies between IDIC powers and authority and those vested in the macroprudential authority (the central bank) and the Ministry of Finance of the financial system. More clarity is needed on the powers and authority of IDIC and those vested in the central bank and Ministry of Finance with respect to troubled banks. Meanwhile, to mitigate politics influencing IDIC decision on troubled banks in future, the categorization of banks by systemic importance to banking and financial system should be made ex ante as recommended in financial stability authority instead of ex post. Equally important, there is need to strengthen IDIC independence in its decision policymaking, which is unlikely to happen any time soon as long as IDIC management is appointed and approved by the executive and legislative branches of government, respectively. The rest of the paper is presented as follows. Section 2 discusses literature review, followed by Section 3 that describes research methodology. The penultimate section presents result and discussion, while the last section draws the conclusion and policy implications.

2. Literature review

Deposit insurance protection takes various forms including (1) expressly ruling out deposit insurance protection; (2) expressly denying deposit insurance protection but give priority to depositors in the event banks’ insolvency and liquidation; (3) assuming ambiguity on implicit deposit insurance protection, by not issuing laws and regulations to that effect; (4) implicitly depositing insurance protection through bailouts to insolvent banks and depositors; (5) enacting law that guarantees capped explicit deposit insurance protection; and (6) enacting a law that guarantees explicit deposit insurance protection for all deposits (blanket guarantee) (Demirgüç-Kunt & Kane, Citation2002; Garcia, Citation1999).

Nonetheless in practice, deposit insurance schemes take two forms,Footnote2 implicit and explicit. Implicit deposit protection schemes are not based on stated rules but conjectures that are discernible from previous government actions, while explicit deposit protection schemes have stated rules that delineate the terms and conditions, extent of deposit coverage, and guarantee (Mitchel, Citation2007). Deposit insurance also differs by objectives of the scheme in place, with voluntary schemes allowing coverage for deposits in banks that pay premiums and exempting those banks that don’t pay premiums (and some are comprehensive, obliging all banks to participate in the scheme (Indonesia is one such case), while others are broad in nature and cover various types of deposits.

The incentive structure of an effective deposit insurance system must be in line to reflect the three sources of internal governance mechanisms inter alia board of directors, management, and shareholders; actions of depositors, borrowers, and creditors; and regulatory restraint that is imposed by legislature and implemented by supervisory authority (Garcia, Citation1999). Failing to achieve that makes deposit insurance programs susceptible to adverse selection, moral hazard, and agency cost problems, increase risk on depositor money, and exacerbates public trust in the financial system, which in turn reduces monetization of the economy, hence financial development (Cull, Citation1998). Indeed, generous explicit deposit insurance is found to induce bank risk-taking behavior and contributes to bank fragility and eventual crisis. Worth noting as well is that efforts to mitigate such efforts by raising hurdles of entry into the deposit insurance program through applying different premiums for different banks depending on portfolio risk do not always reduce the adverse effect of generous deposit insurance on financial intermediation stability. Thus, deposit insurance (the non-risk-weighted form), unless accompanied by stringent regulatory monitoring and supervision of bank operations, enforcement of the linkage between investment risk and capital level, generates gains for banks at the cost of the insurance agency, taxpayers, and solvent banks. Consequently, economic efficiency suffers as riskier investment practices, according to Hanc (Citation1999), lead to “misallocation of economic resources, costly bank failures, and increased costs to the insurance funds, solvent banks, and tax payers.” Solvent banks are penalized because underpriced deposit insurance premium encourages poorly capitalized banks to attract deposits at lower interest rates (befitting sound strongly capitalized banks) than they would have done in the absence of the scheme. It is also found out that the temptation for insured banks to undertake higher risk investment without increasing capital levels as prudential principles would warrant is higher in a highly competitive banking environment, a tendency that increases banking fragility and potential for a banking crisis.

Nonetheless, explicit deposit insurance encourages moral hazard, adverse selection, and agency problems. Moral hazard, which according to Kambhu, Schuermann, and Stiroh (Citation2007) refers to “changes in behavior in response to redistribution of risk,” which in the case of deposit insurance entails the depository institution making riskier investment decisions because it doesn’t have to “meet all the costs caused by bad outcomes,” while depositors in making their saving decisions no longer differentiate between sound and unsound depository institution (for instance, Ioannidou and de Dreu Citation2005 found that explicit deposit insurance encouraged indiscipline by large depositors). In other words, moral hazard reduces the incentive for bank managers, bank owners, depositors, regulators, and politicians to care much about bank soundness (Garcia, Citation2000). This is attributed to the fact that depositors, upon ensuring that their deposits are insured, no longer have the interest to monitor bank actions as their money is insured; banks engage in riskier investment than would be the case without insurance and that without having to pay higher interest to depositors or demand from investors on loans disbursed since in the event of bank failure depositor claims are met by the insurance agency.

Moreover, riskier bank investment, which is made in the aftermath of insuring bank deposits, generates high profits (because they generate higher returns), which are to the benefit of shareholders (residual owners of the firm) and management (because of performance-related remuneration) but are not factored in the insurance premium risky banks pay to the insurance agencyFootnote3 (Kariastanto, Citation2011) and creditors (Eisdorfer, Citation2010; Jensen & Meckling, Citation1976). Other forms of moral hazard attributable to explicit deposit insurance programs include reluctance of depositors to shift their deposits from unsound banks to healthier ones for the same reason, borrowers deciding to borrow from unhealthy banks on assumption that the existence of deposit insurance creates a level playing field of all banks, regardless of risk profiles, failure of supervisory agencies to obtain and disseminate information on the state of health of banks because market discipline is assumed to be blunted by the existence of deposit insurance protection, and the tendency of depository institutions that participate in the deposit insurance programs to take on riskier investments because some of the ultimate risk on deposits is the responsibility of the deposit insurance agency (DIA) (Demirgüç-Kunt & Kane, Citation2002; Garcia, Citation1999; McCoy, Citation2007). Laeven (Citation2002; Cull et al., Citation2004) finds that explicit deposit insurance and government bailouts (ambiguous policy stance on deposit insurance) increase the opportunity cost of insurance services, an effect that rises with the degree of bank concentration, while Akerlof and Romer (Citation1993) found strong correlation among deposit insurance, low capital ratios, and excessive risk taking, and Demirgüç-Kunt and Detragiache (Citation1997, Citation2002) established a positive correlation between explicit deposit insurance and systematic bank insolvencies, which is in part attributable to moral hazard.

Adverse selection arises from IDA setting premiums that do not reflect risk profiles of participating depository institutions, creating a disincentive for large depository institutions, which leads them to withdraw their participation from the program. With fewer participating depository institutions, deposit insurance premiums are raised, making sound banks even more reluctant to join the program.

Meanwhile, the principal agency problemFootnote4 relates to activities and actions of shareholders of depository institutions, management, regulators, DIA, and politicians that enhance their interest (agents) at the expense of the taxpayers who are the ultimate bearers/payers of risk. This is rooted in differences in the interests and source of incentives between financial institution regulators, who influence the timing of the closure of insolvent banking institutions on one hand, and taxpayers and DIA on the other. DIA officials, who are the agents, may decide to delay the closure of troubled banks in order to conceal past laxity in monitoring and supervision, and wait for improvement in economic conditions on the assumption that should reduce liquidity stress failing depository institutions face, thereby averting the cost of paying insured depositors and even recommend recapitalization to improve liquidity. Such action increases the resolution cost on the agency and by extension taxpayers’ money (Schich, Citation2008; Cull et al., Citation2004). Agency problems may also be attributable to practices of officials of the depository agency or financial institution supervisory agency that are motivated by self-interests (delay taking action to allow the adverse effects of policies adopted by predecessors to come to light), which increases the resolution for the DIA and taxpayer (the principal) than would be the case if bank closure are resolved as soon as they show signs of irrevocable insolvency agency cost arising. Agency costs are also manifested in inaction of DIA staff, which puts interests of depository institutions above those of depositors and taxpayers (Hardy, Citation2006) as well as bowing to pressure from politicians by allowing insolvent depository institutions that should face resolution to continue operating. Consequently, the cost of resolution to DIA, depositors, and taxpayers (government) rises. In final analysis, poorly designed deposit insurance programs lead to the bankruptcy of the DPA, hence unsustainable, and increases financial system instability (Demirgüç-Kunt, Kane, & Laeven, Citation2014; Cull et al., Citation2004).

To that end, the design of a good deposit protection scheme, though influenced by the institutional framework, fiscal capacity, and social-economic settings of a country, should delineate key issues, including the mandate it has in relation to other agencies that play key roles in bank supervision; explicit definition of the deposit insurance system in relevant laws and regulations; given power to take prompt remedial actions; prompt payment of deposits; clear role of the DIA in bank supervision and liquidation of failed banks is in part depends on the insurance; supported by law that succinctly states the coverage, pricing of the coverage, and related terms such power to begin insolvency proceedings of troubled banks, ensures that deposit insurance is mandatory for all banking institutions; must have enforceable coverage limits to encourage large depositors participation; providing small coverage such that depositors and creditors are incentivized to avoid undercapitalized, and high-risk banks; must uphold transparency in implementing claims procedures while maintaining bank confidentiality; ensure that DIA and agency staff are accountable for their actions, while at the same time ensuring legal protection for the agency and staff against criminal and legal liability; sufficient funding to finance operations of the agency and resolution of failed banking institutions; ensuring that DPA is independent in discharging its responsibilities hence free from regulatory capture and forbearance attributable to political intervention and promotes private monitoring and policing of bank risk exposure (through the adoption of complementary private monitoring, and issuing of subordinated debt); conduct of good information organization and prompt dissemination about state of health of depository institutions; and implementing an explicit deposit insurance system on a limited scale, when and if banking system attains soundness. Besides being mandatory for all depository institutions, an effective deposit insurance scheme should instill trust in the banking system from depositors and banking institutions. This is possible if the deposit insurance program has the capacity to limit the contagion effect of unsound banks on sound ones, and ensuring uninterrupted functioning of the interbank market as the lynchpin of the payments, system despite the failure of some banks due to failure to meet liquidity needs (Garcia, Citation1999, p. 9; Kling, Citation2008).

3. Research methodology

The research observes all commercial banks in Indonesia, which comprise state-owned limited liability banks, national private banks, regional development banks, and foreign and joint venture banks. As regards data used, the research was based on secondary data that were obtained from Bank Indonesia. The data included number of all commercial banks in Indonesia, with their respective categories; deposits mobilized by different categories of commercial banks in Indonesia in during the observation period; credit disbursed by commercial banks by type of bank in Indonesia during the March 2000–March 2007 period. While data analysis using multiple regress used data for the 2000–2016 period, data for trend analysis was limited to the March 2000–March 2007 period. This was largely because of the need to observe the trend in the relevant variables prior to IDIC establishment and during the transition phase from full blanket guarantee to fully fledged limited deposit insurance guarantee (September 2005–March 2007). Data on all variables that were used were obtained from Bank Indonesia (central bank) and the financial services supervisory agencies (OJK). Meanwhile, analysis techniques used included technical and analysis of variance. Technical analysis involved establishing the trend (if at all any) of the data during the period of observation (March 2000–March 2007), which was expected to help in identifying patterns, if at all. Trend analysis was conducted on three levels, inter alia: (1) the commercial bank level in general, (2) category of commercial bank level, (3) and rural banks level. Data analysis was based on trend analysis of indicators and multiple regression. Using quarterly data, trend analysis involved mapping the composition and trajectory of source and use of funds; various types of third-party funds (demand deposits, saving deposits, and time deposits) that were mobilized by various categories of commercial and rural banks; bonds issued and loans borrowed by commercial banks in general; credit disbursed by different categories of commercial banks and rural banks; and the trend of various credit types (working credit, investment credit, consumption credit) made by each commercial bank type during the observation period (March 2000–March 2007). To determine whether or not IDIC establishment induced a fundamental change in the bank intermediation equation, structural break test was conducted on various indicators.

The second analysis technique used was an analysis of variance that was aimed at establishing whether or not there were significant differences in sources of funds used by different commercial bank types as well as in uses to which such funds were put. Data on bank assets by type of banks was used to control for bank size in analyzing the variance in sources and uses of funds for commercial banks.

Multiple regression was the third analysis technique used. The multiple regression model used was as follows:

where BC is bank credit, BIC is Bank Indonesia certificates, and ∟ other variables that influence bank credit. Data was transformed into natural logarithms, after which tests for normality and serial correlation were conducted, with results indicating that variables suffered from serial correlation. To that end, data was either differenced or included AR (1 to 2) and time trend terms in the least-squares model to solve that problem. Interpretation of multiple regression coefficients was based on the significance error of 5%. In other words, if the probability value (p-value) of the coefficient estimate was smaller than 5%, the alternative hypothesis was not rejected (null hypothesis rejected), and on the contrary, when the p-value of the coefficient estimate was larger than 5%, the null hypothesis was not rejected, and the alternative hypothesis rejected.

4. Results and discussion

4.1. IDIC and impact on financial stability

While a series of financial deregulation packages (1983, 1988, and 1998) generated many benefits for banking industry and economy, as reflected in increase in bank branches from 62 (1988), 222 (1996), and 138 (2003); increasing importance of banking sector to the economy as reflected in ratio of bank assets to nominal GDP that was 72.8% (1996), 79.8% (1998), and 63.9% (2003); wide choice of banks and financial products for customers, relatively lower interest charged on loans and an increase in interest on deposits, the Indonesian banking industry has been beset by a wave of problems that have ranged highly undercapitalized as reflected in the trend in capital to assets ratio (9.6% (1996), −12.9% (1998Footnote5), and 9.7% (2003)); absence of good corporate governance that has led to fraud abated by complex cross shareholding practices among owners; poor observance of minority shareholder rights; unhealthy competition practices, noncompliance with prudential banking principles, including high indebtedness, poor risk management practice (high gross Non Performing Loans (NPL) of 9.3% 1996, 58.7%Footnote6 in 1998, 8.1% in 2003; and higher-than-threshold affiliated party lending (Brown, Citation1999; Sato, Citation2005)). However, the deep-seated nature of problems besetting Indonesian banking industry came to a head during 1997/1998 economic crisis when economic growth plummeted by −13.7% in 1999, national currency suffered depreciation from US$/IDR2,500 (1996) US$/IDR12,000, spike in inflation from 15.7% (February 1997) to 21.7% (February 1998), unemployment surged from 4.7% (August 1997) to 5.5% (August 1998), and underemployed rose from 35.8% to 39.1% (Basri, Citation2013; Sumarto, Suryhadi, & Widyanti, Citation2002).

Countercyclical policies that Bank Indonesia adopted worsened bank liquidity, while eroding bank assets as default rates surged to (NPLs soared to 27%). Some of the policy measures taken to stem the tide included Bank Indonesia with the collaboration of the Ministry of Finance injected Bank Indonesia liquidity support in the value of IDR145 trillion, closure of some banks, injection of US$47 billion in government bonds to recapitalize almost the entire banking system, and strengthened financial stability by establishing the financial sector stability committee (KSSK), which with the collaboration of Bank Indonesia and Ministry of Finance was charged with macroeconomic surveillance for potential signs of instability in the economy and recommending corrective measures.

Enactment of the new banking law no. 10/1998 and Bank Indonesia law no. 23/1999, as amended by law no. 3/2004 and Bank Indonesia regulation No. 8/8/PBI/2006, laid foundation for a new banking system and independent central bank. Other measures to strengthen bank competitiveness of commercial banks entail raising minimum core capital required to establish a bank (Bank Indonesia regulation no. 7/15/PBI/2005Footnote7); and improving bank management quality by obliging adoption of good governance principles. It is the above policy packages that prevented Indonesian banking sector and financial system to a recurrence of the 1997/1998 crisis during the 2008 global financial crisis. Nonetheless, there is another, often ignored factor that contributed to creating a sound and firm foundation for Indonesia banking industry that prevented a recurrence of the devastating impact of 1997/1998 during the 2008 global financial crisis-establishment of the IDIC that came into effect in 2005.

The establishment of IDIC is based on law no. 24/2004 and presidential decree no. 161/M/2005, and is an integral part of implementing law no.10/1998, article 37B, Sections 1–4,Footnote8 on Banking, enjoins relevant authorities to establish IDIC to support the emergence of a “strong, sustainable financial intermediation function” in the banking sector in Indonesia. The establishment of IDIC was expected to protect customer deposits in commercial banks and rural banks, and monitor potential risk in the Indonesian banking system likely to drain insurance funds.

Moreover, in IDIC regulation no. 5/PIDIC/2006 on handling insolvent banks with potential systemic risk,Footnote9 and the corporation is also responsible for dealing with unsound banks with potential systemic risk (which are recapitalized), and unsound banks without potential systemic risk, as declared by the banking supervisory agency. In other words, IDIC bequeathed the roles played by the defunct Indonesian banking restructuring agency (all commercial banks are obligated to participate in the Indonesia deposit insurance policy). The IDIC, equipped with initial capital of IDR500 billion injected by the state, became operational on 22 September 2005. The deposit insurance program entailed a phased reduction of the maximum level of deposits per account in Indonesian commercial banks covered by the IDIC insurance program.

If during 22 September 2005–21 March 2006 no maximum was set on a single account, the figure dropped to IDR5 billion during 22 March 2006–21 September 2006. Subsequently, during 22 September 2006–21 March 2007, IDIC program covered a maximum of IDR1 billion savings on a single account, a figure that dropped to IDR100 million with effect from 22 March 2007Footnote10 to this day.Footnote11 Guaranteeing savers’ deposits in the Indonesian banking system is vital for reducing the potential risk of recurrence of the debilitating bank runs sparked off by one, two, or so banks, facing liquidity problems, mismanagement, operations that trigger a plummet in public confidence in bank performance, which in turn by either domino or contagion effect or both sets off systemic risk. The IDIC obligates commercial banks to, among other things, pay a premium, twice a year, which is set within 0.1–0.5% range of the average of deposit balances mobilized during the 6-month period (1 January– 31 June, and 1 July–31 December).

By the same token, banks with high investment portfolio risk are obliged to pay higher deposit insurance premium than those with lower investment portfolios risk. It is such premiums that overtime will accumulate into insurance funds that will in future be used to compensate customers of insolvent commercial banks to the extent that such savings fall under the set interest range and maximum insurable deposit amount. The implication of that is that banks with high investment risk portfolios pay higher premiums on their deposits than those with lower investment risk portfolios. This means that deposits are considered safer in banks that fulfill their obligations with respect to premium and are operated on prudential principles with respect to capital/equity, bank asset risk, management, and liquidity (CAMELFootnote12 framework).

Additionally, participating banks are required to pay membership fee, which is 0.1% of bank equity; submission of copies of bank soundness, statements of shareholders, commissioners, and directors; statement of the establishment of the bank; operational permit of the bank; report of savings position; monthly financial report, audited annual financial report or report submitted to the bank supervision agency,Footnote13 report of the composition of shareholders, controlling shareholders for cooperative banks, directors, and commissioners. It is also imperative for participating banks to display evidence of their participation in IDIC program in places that are easily accessible and seen by the general public. The timing of the establishment of the IDIC can be related to the resurgence of public confidence in the banking system attested by rising credit deposit mobilization, bond issuance, and credit disbursement has served as signals for the government to reduce the huge cost it has been incurring since the issuance of the full blanket guarantee policy. Apparently, think tanks in the finance ministry considered the right time to relinquish some of the burden embodied in a full deposit guarantee policy in place since 1998 to the public and commercial banks to bear more responsibility and cost, attendant to the level of risk of their investment decisions. This is the spirit underlying the establishment of the IDIC in September 2005.

The conduct of the deposit insurance program calls for the determination of the applicable interest charged on deposits that qualify for insurance coverage. This is done by the IDIC in consultation with Bank Indonesia. This implies that the establishment of the IDIC in Indonesia in September 2005 brought an end to the full blanket guarantee policy of all third-party funds in the Indonesian banking system that has been in place since 1998. According to sources within the IDIC, interest on deposits covered by the insurance varies by the currency denomination of deposits, and in line with the general interest rate, inflation, exchange rate of Rupiah against hard currencies, in the economy.

However, IDIC fair interest rate, which is set three times a year, largely follows the trajectory of Bank Indonesia rate (the Bank rate). For example, interest rate on Rupiah denominated deposits in commercial banks covered by IDIC insurance policy for 15 September 2007–14 January 2008 period was 8.25% for Rupiah denominated deposits in commercial banks and 11.75% for rural banks, while that on US$ dollar denominated deposits was 4.50%.Footnote14 Interest rate on deposits in commercial banks and rural banks covered by the IDIC program is reviewed on a regular basis, or in case of need, in accordance with Bank Indonesia (Indonesia Central Bank) interest rate policy.

Thus, the establishment of the Indonesian Deposit Insurance Agency is one of the policies enforced to prevent the recurrence of a 1997–1998 drastic plummet in public confidence in the banking system, which spiraled out of control leading to debilitating systemic bank runs, costly government liquidity and recapitalization bailout packages, financial disintermediation, and economic contraction with concomitant falling aggregate demand, and rising unemployment. The measures are aimed at ensuring stable financial intermediation to economic agents even during an impending financial and economic crisis. In that light, deposit insurance policy must be considered as integral to efforts to strengthen financial that emanate from domestic misalignment problems and external factors, beyond the control of a small open economy. Even the best deposit insurance works in a macroeconomic environment that is stable, predictable. Thus, well-designed deposit insurance programs are as effective as supporting macroeconomic environment, manifested in sound financial institutions, responsible monetary and fiscal policies both domestic, regional, and international. This underscores the importance of various initiatives tailored to ensure current and future financial and economic stability at the national, regional, and international levels.

The IDIC, which came into effect in 2005, created a new regulatory regime that in effect transferred the risk that depository institutions had borne, in the event, of a financial crisis that undermined repayment capacity of lenders, from banks to the DIA. What was required was for the ban to pay premium for third-party deposits that was based on interest rate promised, which had to be within the limits of the interest rate on insurable deposits set by the IDIC that in turn was based on Bank Indonesia’s prime interest rate. It is thanks to the establishment of IDIC that perception about the risk borne by deposits declined, reducing the possibility of bank runs whenever a single bank experiences liquidity problems, which in turn increased confidence in the banking system; induces banks to mind about their risk profiles in general and the risks of deposits they take, which is reflected in the interest they pay to depositors, which in turn impacts on interest rate they demand from borrowers; IDIC policy of announcing the fair interest rate on deposits that is considered within the limits of depositor funds covered under its deposit insurance program is another fact that prevents excessive risk taking by banks, depositors, and creditors. However, it can be said that IDIC establishment may lead to moral hazard by banks by taking on more risk since they know that IDIC bears the ultimate risk for third-party funds that fall under its deposit insurance guidelines; and risk aversion from lenders, especially to sectors that are traditionally considered risky (agriculture, especially food crops production, fisheries, and livestock); and micro-, small-, and medium-size enterprises. Thus, there is little doubt that the evolution of the new regulatory regime forces banks to reposition themselves in line with the new high credit risk conditions. Disbursing credit to a sector or enterprise that is feasible but not bankable is now difficult, if not feasible, to do. This is because economic activities funded by the bank significantly impact on the calculation of a bank’s risk-weighted assets, thereby the level capital (adequacy) it must have on its books. Issuing loans to economic activities such as micro-, small-, and middle-size enterprises impacts negatively on a bank’s risk-weighted assets, and in compliance with prudential banking principles induces banks to increase the size of equity on the bank’s books.

4.2. IDIC and bank performance

This research uses chart analysis and analysis of variance to determine the influence, if at all, the establishment of deposit insurance has had on operations of commercial banks in Indonesia. Indicators of bank performance used include bank intermediation indicators: mobilization of third-party funds (deposits: demand, time, and saving; bonds issued and loans received), and loan disbursement (working investment and consumption credit), Bank Indonesia certificates held; and the trend in bank assets and equity.

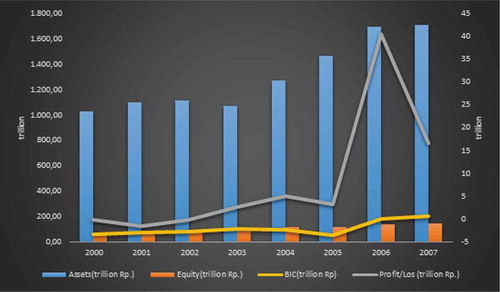

Bank assets, bank equity, and profits and Bank Indonesian certificates held almost flattening out and dropping during 2002–2003 (Figure ). The 2003–2005 periods show another rebound of bank performance but with a difference this time around. While other indicators such as bank assets, bank equity, profit, and loss continue with the momentum that begins several quarters before the establishment of the IDIC, there is a drastic increase in Bank Indonesia certificates held by banks toward the end of 2005, which however stagnates in 2006 and March 2007. One of the best general indicators of the running to safety by Indonesian banks is a drastic increase in their investment in Bank Indonesia certificates, which are risk free, flexible, and more liquid than other investments such as loans. The fact that the increase occurred in the immediate aftermath of IDIC establishment leads one to the conjecture that the sense of charting unfamiliar territory of banking activities under the Indonesia deposit insurance regime, which was new to bank owners and management alike in Indonesia, might have sparked off precautionary measures in bank operations. However, slow growth in 2006 and 2006 in Bank Indonesian certificates points to an interesting signal that the spike in Bank Indonesian certificate holdings was only temporary “adjustment” perhaps to see how things go, and then once it became clear that the rules of the game had changed fundamentally as were the operations, banks then resumed their activities factoring in of new variables in their operations.

Figure 1. Trend in Assets, Equity, BIC, and Profit and Loss, 2000-2007.

Note: *BIC stands for Bank Indonesia certificates.

Source: Bank Indonesia.

What is true with respect to bank assets, equity, and profit and loss is also true for net interest income, nonperforming loans ratio, which continues with the trend that begins some quarters prior to the establishment of the IDIC in September 2005 but slows in 2006 and stagnates in March 2007 (Figure ).

Figure 2. Trend in LDR, NPL, and NIM for Indonesian commercial banks, 2000-2007.

Source: Bank Indonesia.

In June 2007, the NPL ratio declines further (6.40% of all loans disbursed). However, the fear by banks of potential risk is reflected in a decline in the performance of loan to deposit ratio (LDR) in late 2005, but recovers in 2006 and March 2007. Moreover, net interest margin rises to 7.70, which indicates that banks are earning higher interest earnings from their investment activities than they pay for financing them. The problem is that the establishment of the IDIC in September 2005 coincided with government policy that hiked fuel prices by more than 114%, which fueled higher inflation expectations, which in turn induced a reversal of Bank Indonesia interest regime from cutting to hiking, all of which compounded bank risk expectations. The temporary nature of the spurt or hike in Bank Indonesia certificates variable and drop in loan deposit ratio may have more to do with efforts by banks to adjust to tight monetary policy regime at the time than a consequence of heightened perceived bank risk attributed to the establishment of the Deposit Insurance Corporation.

Although at the outset deposits mobilized by commercial banks continue the long-term trend, in the wake of the establishment of IDIC, April 2007 figures show stagnation, which may or may be not related to the coming into effect of the IDIC provision that sets the limit of the maximum amount of Rupiah at IDR100 million per account belonging to an Individual. An examination of the trend of demand deposits mobilized by commercial banks by type reveals some interesting findings. Although the general trend of demand deposits from private enterprises seems to be stable over time, at about 40% of total demand deposits, during the September 2005–March 2007 period, the trend is some notches downward from 40% in September 2005 to 37% in March 2007. Government entities (national, provincial, and regional governments) apparently show an increasing interest in keeping demand deposits in commercial banks over the period of observation as they “control” 30% of demand deposits in March 2007 from about 17.5% in September 2000.

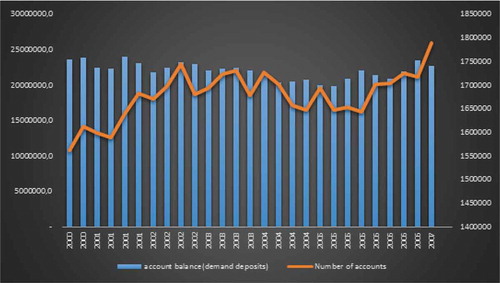

Thus, keeping money in commercial banks in the form of demand deposits by government entities was not significantly affected by the establishment of IDIC. On the contrary, demand deposits from state-owned enterprises register a downward trend during the entire period, as well as during the period of “interest” September 2005 and March 2007. The same applies to demand deposits held in commercial banks that belong to nonresidents. Thus, demand deposits kept by most entities in commercial banks, with the exception of those belonging to government entities, registered a long-term downward trend, which may or may not be attributed to the establishment of the IDIC. Observing the January–June 2007 period shows fluctuation with growth followed by decline January–March 2007 in demand deposits mobilized by commercial banks. However, April, May, and June post strong growth, an indication an upward trend in demand deposits is underway (Figure ).

In general, bank deposits in April, May, and June, 2007 experience growth with June 2007, posting very strong gains, an indication that the dip in March 2007 was at best temporary, rather than a fundamental change in the trajectory of bank deposit mobilization. This implies that the establishment of IDIC has not fundamentally altered the basic parameters influencing bank deposits mobilized by commercial banks in Indonesia (Figure ).

Figure 3. Demand deposit balances September 2000-March 2007 (Billion Rupiah).

Source: Bank Indonesia.

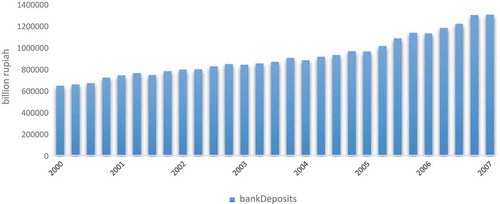

Figure 4. Total Deposits mobilization by Indonesian commercial banks, 2000- 2007 (Billion Rupiah).

Source: Bank Indonesia.

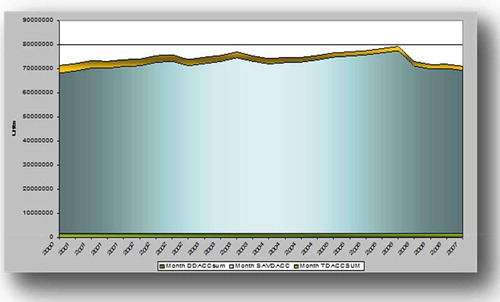

The expectation is that the coming into effect of the IDR100 million insurable maximum per account in March 2007 would induce savers with accounts that have higher values than IDR100 million to draw down such accounts with the aim of reducing potential losses on accounts that have deposits that exceed IDR100 million (Figure ).

Figure 5. Trend of Accounts by type for <=Rp.100 million per account, September 2000-March 2007.

Note: *Month DDACCsum stands for sum of deposit accounts; Month SAVACC stands for total number of savings accounts; Month TDACCSUM stands for total number of time deposit accounts.

Source: Bank Indonesia.

This should be in the form of diversifying account types (time deposit, savings, demand) and opening accounts in various banks (Figure ). However, Bank Indonesia figures show that that is not the case. This is why contrary to expectations the number of banks accounts with nominal value of IDR100 million after experiencing an increase in the September 2005 decreases steadily during 2006 and in March 2007. This is evidence that depositors have not overreacted to the establishment of IDIC by undertaking suboptimal saving methods such as dividing large balance accounts into IDR100 million accounts to ensure that each account met the upper limit of IDIC deposit insurance threshold for each individual account. Such a process, if done, would increase the cost of managing each accounts for the commercial bank and account holder, and in turn increase financial intermediation cost and inefficiency.

Figure 6. The value of Account balances for <=Rp.100 million per account, by type, September 2000-March 2007.

Source: Bank Indonesia.

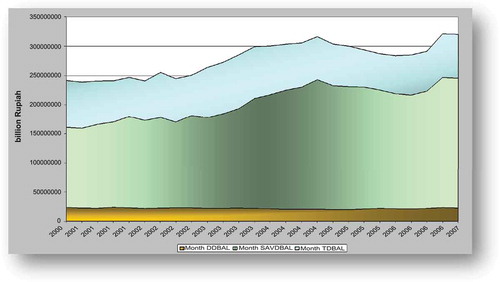

Account balances on savings and time deposit accounts experienced a decrease since March 2005–June 2006, rebounded slightly in September 2006, and recorded strong gains in December 2006 (Figure ). However, March 2007 shows virtual stagnation for time deposit account balances and a decline for savings deposit account balances. Demand deposit account balances, on the other hand, continue the fluctuation that precedes the establishment of IDIC, registering a positive gain in late 2005, mixed results in 2006, and a decrease in March 2007.

Figure 7. Trend in account balances and Number of accounts, all types combined, September 2000-March 2007.

Source: Bank Indonesia.

Thus, the expectation that depositors should reduce the money in time deposit accounts (tied up interests rate, tied up in one bank, which pose higher potential risk) and increase the money in savings accounts and lastly demand deposits does not seem to hold. In any case, a drop in total account balances that occurs in March 2007 is due to lower time deposits balances rather than low demand and savings deposit balances, which should turn the tables on the theory that indeed savers’ behavior had begun to be driven by fear of potential risk inherent in the type of deposit accounts where they put their money. Time deposits account balances continued to be larger than savings accounts, and demand deposit accounts, thus no indication that there was a fundamental shift in saving patterns since IDIC was established. There is a strong indication that account balances on all the three account types (savings, demand, and time deposits) shows a steady increase during the period of observation, while the number of accounts especially savings, registers a steep decline (Figure 7). Such behavior attests to improvement in public trust in the capacity of the banking system to serve as trustworthy custodian of depositors' money rather than a source of risk.

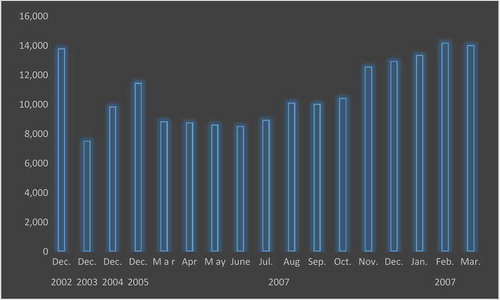

Commercial banks have another important source of funds for their activities: loans. Providers of loans should be cautious in extending credit to borrowers who they consider face higher risk than to those with low risk (Figure ).

Figure 8. Loans received by banks December 2002- March 2007(Billions Rupiah).

Source: Bank Indonesia.

The tumultuous and highly fluctuating decrease in the level of loans received by banks that characterizes March 2000–September 2003 settles to a new, but lower threshold in December 2003.

Pertaining to the observation period, September 2005–March 2007, loans received by banks increase slightly in September and December 2005, but decline slightly in March–September 2006. Recovery gets underway in December 2006, which continues through March and April 2007. One could say that the long span of decline that occurs in March–September 2006 represents a delayed reaction to the coming into force of the IDIC, which is understandable as loan transactions are made in advance carrying long maturities. This means that instant renegotiation or reviewing deals that are already in force is not easy. The problem with that notion is that if indeed the March–September decrease in loans received by banks was caused by the reaction of lenders (albeit delayed one) to the higher risk regime banks face in the wake of the establishment of the IDIC, even deeper cuts should have been made in March and April 2007 since it was then that limits on amount in individual accounts covered by the state sponsored the IDIC came into force. This points to factors other than the establishment of the IDIC and the attendant ripple effects for the March–September 2006 plunge in loans borrowed by banks.

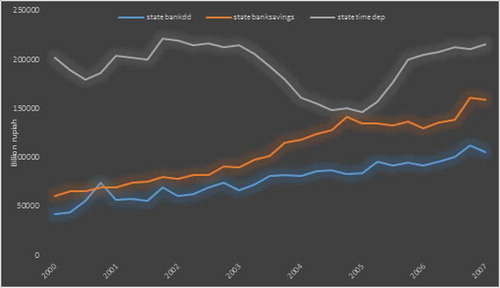

Bank deposits by type of banks experienced steady growth from the third quarter of 2001, with national, private, and regional development banks registering better performance than state-owned and foreign and joint venture banks. Since the last quarter of 2004, there has been a steeper rise in deposits mobilized by foreign and joint venture banks, regional development banks, and private national banks than that in state-owned banks. The only similarity in the pattern of trajectory appears to occur in the first quarter of 2007, when virtually no change is registered as far as deposits growth is concerned (Figure ).

Figure 9. Funds mobilization by state owned banks, 2000- 2007 (Billion Rupiah).

Source: Bank Indonesia.

If one takes the third quarter of 2005 as the time when information about the establishment of the IDIC begun to have an effective impact on the behavior of depositors, there is indeed a steeper rise in deposits in December 2005 than that experienced in September 2005 for state-owned banks, but the same pattern, even at a steeper rise, in other banks during the period. The trend in deposits stagnates and even falls for some banks in the first quarter of 2006, after which it experiences steady growth, until the first quarter of 2007 when it stagnates. If the trend that occurred in the last quarter of 2005 and gains made in the first quarter of 2006 was due to depositors’ wariness about the safety of their deposits, then such a trend would have deepened as time for applying IDR100 million per individual as the maximum insurance by the national the IDIC drew closer 22 March 2007. Apparently, it was not only fear about the security of deposits that influenced depositors’ decisions, but also other factors seem to play an important role (Figure ).

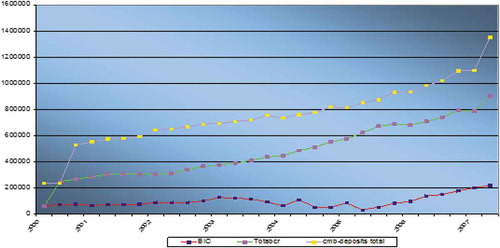

Figure 10. Bank deposits, total bank credit, and bank Indonesia certificates, held by commercial banks, March 2000-June 2007 (Trillion Rupiah)*.

Note: *cmbdepositstotal stands for bank deposits; Totalbcr stands for Total Bank credit; BIC stands for bank Indonesia certificates.

Source: Bank Indonesia.

Borrowed funds through the issuing of securities is yet another means available for commercial banks to finance their investment activities. Borrowed funds through the issuing of securities hit the lowest level in June 2003, after which recovery gains full steam in between March 2003–December 2003. At the start of the “observation period,” recovery in June 2005 from the relatively deep plunge in securities issued, which occurs in March 2005, continues in September and December 2005. However, March 2006 sees another decrease in funds mobilized. However, the trend is reversed in the remaining quarters and April 2007. In the backdrop of the above trend, the inference that can be made relating to the impact of the establishment of the IDIC on the funds mobilized by commercial banks through issuing securities is that there is no indication of a sustained change in the trend discernible, which continues to be upward and appears to be growing at higher rates with time.

However, it must be mentioned that the period after the establishment of the IDIC regime seems to be characterized by relatively lower fluctuations in funds obtained by banks through issuing of bonds than in preceding periods, which might be or not be a result of investor confidence in the banking sector stimulated by improvement in financial stability that is in turn attributable to IDIC establishment. Thus, in the wake of deposit insurance regime, purchasers of bank securities were more eager to acquire them hence a source of investment, an indication that banks’ capacity to mobilize funds by selling securities gained momentum, most likely underpinned more by improvement in bank performance and macroeconomic fundamentals than potential risk in the wake of IDIC establishment.

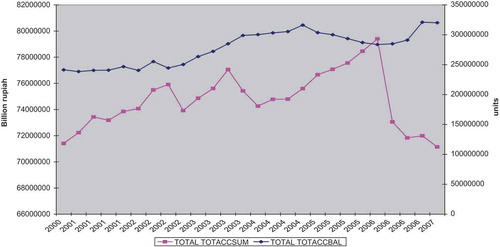

Bank credit disbursed in comparison to Bank Indonesia certificates held by commercial banks shows a steady increase overtime especially the second quarter 2002 (June) until the start of the observation period September 2005 when an apparent threshold is reached with level channeled remaining virtually unchanged for three consecutive quarters September, December 2005 and March 2006. June 2006 sees resurgence of credit growth, which lasts until March 2007, when a significant dip takes effect. The credit disbursement figure for April registers credit growth levels that occurred prior to March 2007, an indication that the decrease in credit expansion in March was of a short term nature rather than the beginning of a new trend.

Nonetheless, loans received by commercial banks, Bank Indonesia figures show a slight improvement (shrugging off) of the effect of the establishment of IDIC but later on nosedives in March 2007 to the lowest level since mid-2003. Robust recovery occurs since then. There is hardly significant difference in total bank deposits (controlled for bank size) in the two periods that is prior to and in the wake of IDIC establishment.

The trend of Bank Indonesia certificates held, on the other hand, shows a steady pattern during March 2000–December 2002, shoots up in March 2003, but experiences fluctuations then after regaining lost momentum in September 2005 (Figure ). The steady growth that starts in September 2005 is sustained throughout the observation period. The rate of growth in Bank Indonesia certificates held by commercial banks in the aftermath of the establishment of the IDIC is the highest and sustained for the longest spell during the March 2000–March 2007 period. April 2007 figures show the sustenance of the growth in Bank Indonesian certificates held by commercial banks even as the credit disbursement rebounds. It is a trend that continues through June 2007.

Although banks do not significantly cut bank credit disbursed, the fact that they increase Bank Indonesia certificates in their investment portfolio at a higher rate provides tentative evidence that wariness about falling into high-risk categories may be preventing banks to extend as much credit as they would like preferring instead to put their funds into flexible, risk-free state-guaranteed securities Bank Indonesia certificates. The significant negative correlation coefficient between Bank Indonesia certificates and bank credit disbursement, and the negative and significant regression coefficient of bank credit on Bank Indonesia certificates confirms the results obtained by technical analysis.

As pertaining to securities issued, Bank Indonesia figures show a slight knock in the immediacy of the establishment of IDIC body in September 2005. However, December 2006 registers a slight mitigation, which dips slightly in March 2007, but shows recovery since then (Figure ).

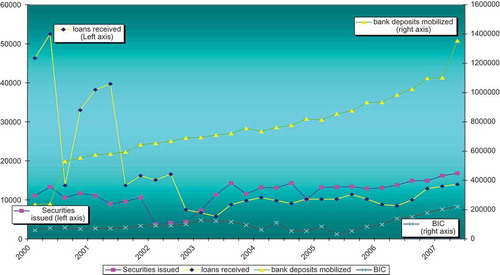

Figure 11. Developments in Bank Indonesia certificates and loans received, by commercial banks, March 2000- June 2007 (Trillion Rupiah).

Source: Bank Indonesia.

4.3. IDIC establishment and bank credit disbursement to risky sectors and subsectors

The trend in total credit in the wake of IDIC establishment indicates that bank credit sustains growth registered in previous quarters, an indication that bank credit disbursement follows the long-term trajectory that dipped slightly in January, but gets on course once again since February 2007. There is significant difference in credit disbursed (weighted by bank assets) for small- and medium-size enterprises dealing in business services, social services during the two periods (before and after) the establishment of IDIC, with higher level of credit channeled to the two Small and Medium size enterprises (SME) subsectors in the aftermath of IDIC establishment than before. It is also evident that there is significant difference in credit disbursement to SMEs by state-owned banks, regional development banks, and private national banks in the wake of IDIC establishment compared to the period before. State banks increase the level of credit to SMEs after IDIC as theorized, but were not followed by regional development banks, contrary to theoretical expectations. Private national banks and joint venture banks reduced the credit level they channeled to SMEs in the aftermath of IDIC establishment compared to the amount disbursed before IDIC (as theorized) (Figure ).

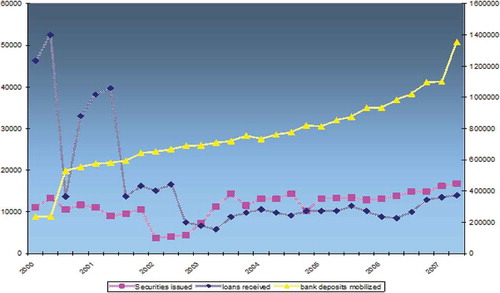

Figure 12. Securities issues, Bank loans received and bank deposits, March 2000-June 2007 (Trillion Rupiah).

Source: Bank Indonesia.

Nonetheless, foreign and joint venture banks do not register significant difference in the level of credit disbursed to SMEs in the wake of IDIC establishment in contrast to the past before. Apparently, the perception that disbursing credit to SMEs posed high risk to banks in the aftermath of IDIC establishment discouraged lenders who were more concerned with the ability to show good quarterly financial statistics than contributing to the survival of more than 40 million SME (representing more than 80% all enterprises) in Indonesia.

By subsector category however based on risk, credit disbursed by Indonesian commercial banks to SMEs dealing in services, trade, and industry, but not as much for agriculture, mining SMEs increased significantly credit to. This is in line with theory that SMEs involved in agriculture and mining sectors pose higher potential risk of default to lenders under conditions of high economic uncertainty than those in industry, services, and trade. Savings deposits, time deposits, credit lent and loans borrowed, and equity show significant positive correlation. Sound rural banks do not find problems in raising funds through borrowing from external sources and providing saving facilities (time and saving deposits).

With respect to Bank Perkreditan Rakyat (BPR) or peoples credit banks credit data, there is an indication that contraction sets in December 2005, one quarter after the establishment of the IDIC. However, March 2006 figures show that credit disbursement returns to growth achieved prior to September 2005 levels, which is testimony to the short-term nature of the decrease registered in December 2005. It is also evident that there is a significant difference between deposits mobilized and credit disbursed by rural banks prior to and after the establishment of IDIC, with levels made in the wake of IDIC establishment higher than those made prior to IDIC. Thus, there is no evidence that the establishment of IDIC in Indonesia has led to the contraction of deposits and credit disbursed by rural banks in Indonesia. What applies to credit disbursed by rural banks in general is also replicated in credit disbursement by sector. There is significant difference in levels of consumer credit, investment credit, and working credit channeled by rural banks prior to and in the wake of the establishment of IDIC.

Meanwhile, credit disbursed by BPR to agriculture, industry, and services also shows significant difference in the two periods, echoing findings unveiled at the general level. There has not been a withdrawal of bank credit facilities from agriculture in the wake of IDIC establishment. In fact, rural banks channel higher levels of credit to agriculture than for industry and services. Nonetheless, rural banks in general disburse more working credit than investment, consumption, and services, which would portend the setting in of conservative lending practices in rural banks credit policy. This generally occurs when lenders’ confidence in borrowers is revised downwards as high risk is factored in credit evaluation leading eventually to credit policy that lends more selectively borrowers by sector, trade, repayment history, type of business, and so on.

This is why private national banks and foreign and joint venture banks reduced the credit they disbursed to the sector. Having to pursue more than profit and value added and quarterly financial figures induced state-owned banks to disburse higher levels of credit to SMES even under conditions of higher risk. Possibly state banks do so because they are agents of development and are the main channels through the high credit initiative of the current government to promote SMEs can be done. Moreover, in accordance with Bank Indonesia regulations, the calculation of capital adequacy ratio takes account of bank credit allocated to SMEs. Nonetheless, regional development banks do not seem to follow state-owned banks in channeled higher credit levels in the aftermath of IDIC establishment.

In general, however, as far as credit to risky sectors is concerned (SMEs and agriculture serves as a proxy here), figures continue to experience even higher fluctuation than before, attesting to the potential high risk that lending to the sector entails. Thus, the inference that can be drawn in reference to the impact of the establishment of the IDIC on SME credit disbursed by commercial banks in Indonesia is at best varied. While SME credit for industry and agriculture-related activities slightly increases at the start of the period (September 2005), stagnation sets in which with minor “spurts” characterizes the December 2005–December 2006 period, before a decline got underway in March 2007. Pertaining to services, credit disbursed to service-related SMEs registers an upward trend punctuated by steep hikes in some quarters that reach the apogee in June 2006. Since then, the downward trend sets in.

There is no indication, however, that the fluctuation of credit going to the sector is attributable to the establishment of IDIC. Nonetheless, given the strong dependence the sector has had on subsidized state credit, mainly channeled through state-owned banks, which has all but been phased out, there is no denying the fact that any policy that increases the credit risk borne by the lender arising from lending to such a risk sector as agriculture is likely to impact on credit channeled to the sector. Thus, IDIC may have an indirect impact on credit disbursed to the sector since it increases the premium banks have to pay for such credit they lend out.

In the backdrop of the above observation, it can be tentatively argued that the advent of the IDIC era has ushered in a regime of higher volumes of working credit disbursed by national private banks, state-owned banks, and foreign and joint venture banks, but has left working credit channeled by regional development banks virtually unchanged. It is worth noting that working credit issued by private national banks and foreign and joint venture banks shows higher fluctuation than is the case in state-owned and regional development banks. This makes state-owned and regional development banks more reliable and predictable providers of working credit than private national and foreign and joint venture banks.

The performance of working credit disbursed by commercial banks, according to Bank Indonesia sources, posted 23% growth in August 2007 to reach IDR461.7 trillion, compared to the previous year’s figure (The Jakarta post, October 16, Citation2007). This is an indication that with respect to working credit disbursement in general banks are doing their job depending on their evaluation of creditworthiness of credit recipients as per normal convention. Improving creditworthiness, indicated by better macroeconomic fundamentals, especially the cost of borrowing, which has been decreasing in line with Bank Indonesia cutting its prime lending rate, coupled with high consumption spending (private and government), rising exports, recovery in investment inflows, and improvement in foreign reserve position, provides positive signals to lender to lend more. And this is exactly what they are doing.

Apparently, the effect of IDIC establishment on working credit disbursement has hardly impacted bank lending for working capital purposes. As pertaining to investment credit to total investment credit disbursed by commercial banks, which being of longer maturity is relatively more sensitive to changes in risk projections than working and consumption credit, shows wide fluctuations in the entire period, with periods of growth often followed by deep dips. This is found to be the case as regards investment credit disbursed by all bank types. There is a significant drop in investment credit that occurs in March 2007, which might be an indication that banks are factoring in potential risk likely to arise from the effecting of IDIC key provision pertaining to deposit insurance. In general, investment credit made by commercial banks to various sectors, with the exception of mining, shows an upward trend with the services sector outperforming other sectors. There is no evidence of an apparent structural change in the trend of investment credit disbursement occurring in the aftermath of the establishment of the IDIC in September 2005. Investment credit to all sectors follows patterns that are set many quarters before the third quarter of 2005 (September 2005), an implication that, at least basing on prevailing data, is the IDIC.

However, if data on investment credit disbursement by commercial banks is included, quite an unwelcome spectacle comes into the picture. Investment credit stagnates for most sectors, and decreases in others, in March 2007. Thus, if the stagnation and decrease in investment that affects trade, all services (including social services), mining, and manufacturing, respectively, are indeed attributed to the coming into effect of the maximum insurable deposit limit per individual account on 22 March 2007, then this represents a dramatic shift from the trend followed since March 2002 and is an eloquent testimony of the potential danger that reaction or overreaction to the ripples sets into motion by the establishment of the IDIC.

Nonetheless, there is significant difference in investment credit (asset-weighted) channeled by the four bank types in the aftermath of the IDIC establishment, with foreign and joint venture banks channeling the highest level, followed by regional development banks, private national banks, and state-owned banks. Apparently, contrary to expectations, state-owned banks shy away from channeling high levels of relatively riskier investment credit than foreign and joint venture banks, private national banks, and regional development banks. In general, investment credit showed significant growth since March 2007 reaching IDR169.83 trillion in July 2007 (Kompas, October 10, 2007). The growth in investment credit in July, which was 25% higher than that in July 2006 (IDR135.7 trillion), was also higher than the growth posted by working credit and consumption credit of 22.13% and 18.64%, respectively.

Such substantial gains in investment credit disbursed by banks is indicative of the fact that the effect on credit disbursement on bank credit, if at all, was short term and was transient rather than a long term, fundamental in nature, as far as bank credit policy is concerned. Investment credit is far riskier than either working or consumption credit due to the long-term nature, which entails complications in making accurate projections of future operations, costs, and returns of ventures to which it is channeled. However, the fact that banks have started channeled investment credit in substantial amounts diminishes the likelihood that the establishment of IDIC in September 2005, and the effecting of the maximum of IDR100 million per individual account covered by the insurance policy under IDIC scheme, has had fundamental impact on bank credit disbursement in Indonesia.

Credit disbursement for consumption use by commercial banks shows an upward trend during the March 2001–March 2007 period, with the four bank categories increasing their respective share of consumption credit market. All in all, the establishment of the IDIC, either directly or otherwise, seems to have contributed to the decrease in the growth rates of consumption credit disbursement in state-owned banks and regional development banks, while private national and foreign and joint venture banks have enjoyed higher growth rates. This could be the preparedness of the private national banks and foreign and joint venture banks to deal with any contingent risk that arise thanks to the existence of good risk management programs and experienced expertise, which may not be the case in either state-owned and regional development banks. Apparently, the September 2005–March 2007 period is characterized by relatively higher fluctuation in consumption credit disbursement made by private national banks, foreign and joint venture banks, and regional development banks, than in state-owned banks. However, in general, bank credit disbursed for consumption purposes shows a steady increase since January 2006 and continues the trajectory through June 2007 by posting substantial growth. The general trend of consumption credit issued by all types of commercial banks is upwards,Footnote15 following apparently similar highs and lows, an indication of being under the influence of similar underlying factors over time. Private national banks show the briskest performance, followed by state-owned banks, regional development banks, and foreign and joint venture banks, in that order.

The behavior of banks shows a shift from risk averseness to risk taking as far as intermediation is concerned (Tables and ). Bank deposit significantly influences bank credit coefficient magnitude (0.793751), T-statistic (6.492055), and p-value (0.0000); while the coefficient on Bank Indonesia certificates has the expected negative sign, it is not significant (−0.000811), T-statistic (−0.038324), and p-value (0.9695). Results for the annual time series showed that coefficient of bank credit disbursement was positive and significant (2.853100), T-statistic (5.505086), and p-value (0.0006); the Bank Indonesian certificate coefficient had the expected negative sign but not significant (−0.023592), T-statistic (−1.423359), and p-value (0.1924) (Table ). In other words, both annual and monthly time series generate results that are similar with respect to signs on coefficients but differ slightly on magnitudes of the coefficients. We tried to run a cointegration regression of the model that produced similar results with the only difference being that the dummy variable was significant and had a positive sign (Table ). The regression findings may reflect the fact that in the medium term in the wake of the establishment of the deposit insurance regime there was perception among banks that bank credit disbursement was no longer as risky as it was prior to IDIC establishment, enabling them to consider expanding credit as a better option, albeit riskier, than investing in low, risk-free Bank Indonesia certificates. Indeed, banks have a wider choice of relatively lower risk safe investments options in the form of government bonds than lending. Nonetheless, from another angle, the decrease in the interest of the banking industry to invest in risk-free Bank Indonesian securities may reflect moral hazard as banks having subscribed to IDIC deposit insurance programs may henceforth consider some of the liability risks covered. In other words, this tendency may reflect increased risk taking of depository institutions after becoming participants in deposit insurance programs (Anginer, Demirguc, & Zhu, Citation2013; Gropp & Vesala, Citation2004; Kariastanto, Citation2011; Laeven & Levine, Citation2009). That would be the case if there is an increasing trend in the LDR. Based on available data, that does not seem to be the case.

Table 1. Multiple regression results of Bank deposits and Bank Indonesia certificates on Bank credit disbursement

Table 2. Robust Tests of Equality of Means

Table 3. Cointegration regression results of source of funds and Bank Indonesia certificates on bank credit disbursement (monthly time series)

Bank assets differ among bank types and show differential impact of the establishment of the IDIC on growth. Assets of state-owned banks experience higher growth in size than before the IDIC; private national banks suffer a slight reduction in size; foreign and joint venture bank assets also experience a tampering of the asset size like private national banks, but the “correction” appears to be sharp; and regional bank assets seem unaffected.

Based on theory, we should expect state-owned banks and regional development banks to perform better as economic agents consider them to be “too important to fail,” while private and quasi private banks should experience a downward correction of their assets for the converse reason that they are not as too important to fail as state-owned/quasi state-owned banks (regional developments banks). The establishment of the IDIC marks the beginning of a new regime in the banking industry. Economic agents should evaluate assets of banks (loans, securities, assets) with 100% surety of the state (state-owned banks and regional development banks should suffer least downward correction, in contrast to private banks) (private national banks and foreign and joint venture banks) the value of which should suffer heavy downward correction due to relatively higher potential risk.

Thus, the trend in bank assets shows differential trajectory by type of ownership, as theory posits. Nonetheless, there is a catch. The two periods used in the study to examine the trend of bank assets, that is, prior to and in the wake of IDIC establishment, also marked the two periods when banks were exposed to relatively low inflation and high inflation, respectively, induced by Government of Indonesia policy that implemented a 114% hike in fuel prices. In fact, the second phase of fuel price hikes was effected in October 2005, 1 month after the establishment of IDIC in September 2005.