?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study investigates the endogeneity among foreign direct investment, economic growth, and stock market development, along with the moderating role of political instability on the relationship among foreign direct investment, economic growth, and stock market development. The study employs selected macroeconomic variables data for the period of 1993–2016 with Auto Regressive Distributed Lag (ARDL) system and hierarchical regression approach for hypothesis testing. This study discovers that there are short-run and long-run association among economic growth, foreign direct investment, and stock market development. In the long run, only unidirectional relationship exists among economic growth, foreign direct investment, and stock market development. However, in the short-run, bidirectional relationship is evident between economic growth and stock market development. This study reveals that foreign direct investment partially mediates the relationship between economic growth and stock market development; and political instability negatively moderates the economic growth and stock market development nexus, the foreign direct investment and stock market development nexus, and the economic growth and foreign direct investment nexus. Therefore, this study suggests that political stability is a must for Bangladesh to achieve stock market development, to increase the foreign direct investment inflows, and to achieve long term sustainable growth.

PUBLIC INTEREST STATEMENT

This study examines the endogeneity among foreign direct investment, economic growth, and stock market development, along with the moderating role of political instability on the relationship among foreign direct investment, economic growth, and stock market development. The results show that there are short-run and long-run association among economic growth, foreign direct investment, and stock market development. In the long run, only unidirectional relationship exists among economic growth, foreign direct investment, and stock market development; whereas, in short run, bidirectional relationship exists between economic growth and stock market development. The results also suggest that political instability negatively moderates economic growth and stock market development nexus, foreign direct investment and stock market development nexus, and economic growth and foreign direct investment nexus. Therefore, the findings suggest that, in Bangladesh, political stability is necessary for stock market development and to increase the inflows of foreign direct investment.

1. Introduction

The role of financial development on economic growth can be traced with the seminal paper of Schumpeter (Citation1913) in economics and finance literature. After three decades, Robinson (Citation1952) suggested that financial development is one of the key factors that contribute to economic growth. Subsequent studies also support this relationship (inter alia: Demetrides & Hussein, Citation1996; Greenwood & Jovanovic, Citation1990; Lucas, Citation1988). Barro and Martin (Citation1995) argue that financial (stock market) development is endogenous, and it is considered as a part of economic growth. Moreover, it is argued that stock market development may stimulate economic growth and vice versa (Hoque & Yakoob, Citation2017; Levine, Citation1997; Levine & Sara, Citation1996; Levine & Zervos, Citation1998).

Theoretically, nexus between economic growth and finance is well accepted in the literature.Footnote1 However, this theory is valid in politically stable economies where entrepreneurs and investors have economic and business freedom. Hence, the relationship between the nature of growth and finance can be different in developing economies compared to developed economies, where economic and political turbulences are very common phenomena. In this regard, the statement of World Bank (Citation1993) and Yousif (Citation2002) suggests that the relationship among FDI, financial development, and economic growth may vary across countries due to the nature of economic and political condition, the policy implication efficiency and also depending on the development levels of financial institutions. Moreover, there might be imperceptible cultural or institutional factors that determine the nature and subsistence of relationship between stock markets and real economy. Therefore, it is important to understand the influence of political instability on the relationship between growth and finance of developing economies in order to formulate efficient policies. In this regard, the current study aims to address the question that how the political instability influences the relationship of growth and finance in developing economies.

Political instabilityFootnote2 plays an imperative role in the stock market operations and economic cycles (see Roe & Siegel, Citation2011). For example, with high political instability, it obvious that such unstable condition will create lack of confidence among the investors, which ultimately results in lower trading volume at stock market (Karolyi & Martell, Citation2010). Similarly, political unrests create barriers in business operations and delay foreign export; as a result, the overall output level of the economy also substantially declines within short period of time. In the same fashion, the political instability reduces foreign capital inflow, which is also an indicator that the economy is not suitable for investment. Hence, the political instability has negative effect on stock price, FDI, and economic output (inter alia: Ahmed & Pulok, Citation2013; Aisen & Veiga, Citation2013; Alesina, Özler, Roubini, & Swagel, Citation1996; Alesina & Perotti, Citation1996; An, Chen, Luo, & Zhang, Citation2016; Asteriou & Siriopoulos, Citation2000; Brada, Kutan, & Yigit, Citation2006; Liu, Shu, & Wei, Citation2017; William, Citation2017). Therefore, political instability can influence the endogenous relationship among foreign direct investment (FDI), economic growth, and stock market development.

With above-mentioned motivations, this study aims to investigate the moderating effect of political instability on the relationship among FDI, economic growth, and stock market development in a developing country, namely Bangladesh, where political instability is a very common phenomenon. In addition, there are several other rationales that motivated us to select Bangladesh as the sample country for this research. First, Bangladesh has been facing the political turbulences and violence since its independence (Ahmed & Pulok Citation2013). The main contributor behind this unstable political situation is the political strikes, which are locally known as Hartal.Footnote3 On the Hartal day, most business organizations, market places, and transportation do not operate fully because of the fear of attacks by the opposition political parties. Political strikes also negatively affect the stock market trading as the investors and other market participants are afraid to go to the stock market for trading. Therefore, the political unrests cause detrimental situation for investment and also for the overall operation of the stock market. This scenario can also be viewed as the loss of economic and business freedom. Hence, such turbulences and violence can significantly hamper the economic growth, FDI, and stock market development. For example, according to World Bank, in the financial year (FY) 2014/2015, about 1% of GDP (approx. $2.2 billion) loss took place due to political disturbance (Hussain, Citation2015).

Secondly, political unrests can subside the effectiveness of government, violate the law and order situation, and deteriorate the peace of the society. The coexistence of all these factors is necessary to create favourable investment environment and to improve the stock market performance. This assertation is also supported by La-Porta et al. (Citation2002). They suggested that political stability along with good governance is essential for the betterment of the economy and proper functioning of the stock market in order to attract investors. Therefore, it is necessary to understand how political instability in the economy affects the finance and growth nexus.

Third, the presence of political instability and violence in Bangladesh has also contributed to the lower level of confidence of international investors towards the country. For example, from year 2007 to 2009 and the year 2014 attracted the lowest domestic and international investments due to highly politically unstable situation during this time.Footnote4 Table provides the evidence of this lower amount of foreign and domestic investments in the country. Furthermore, export revenue from the garments sector is one of the major sources of foreign currency earnings for Bangladesh. This sector contributes almost 75% to the total export revenue of the country. So, any sort of political uncertainty can reduce the foreign buyers’ interest and can result the buyers to switch to the competitor countries, like Indonesia, India, or China; as the importers do not feel confident that the Bangladeshi sellers can maintain their promised delivery date due to political strikes and volatile situation.

Table 1. GDP Growth in recent political turbulent years

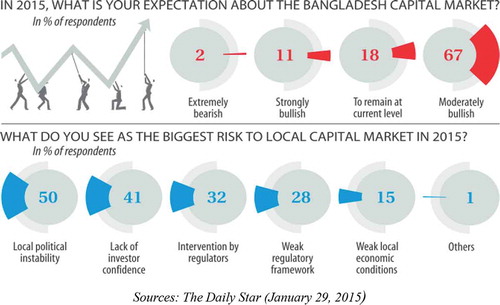

Fourth, according to the director of the Centre for Policy Dialogue (Bangladesh), Fahmida Khatun (Citation2015), “political stability is the key to the economic growth of Bangladesh” (The Daily Star, Citation2015). Economic growth ensures better allocation of resources in the capital market of the country, investments in technology and human capital, accumulation of capital and most importantly to attract foreign capital inflows, which is vital for the growth of any developing economy. Fifth, a survey conducted by Lanka-Bangla Securities on investor sentiments, presented in Figure , shows that most of the respondents feel political instability is the major source of risk for the capital market in Bangladesh, and it is also one of the main reasons for lower participation of foreign investors (Chowdhury, Citation2015).

Figure 1. Survey on investors sentiment.

This study has several theoretical and practical contributions. Firstly, the extant studies on the nexus among FDI, economic growth, and stock market development have been well documented in the context of both developed and emerging economies (inter alia: Duca, Citation2007; Jalil, Wahid, & Shahbaz, Citation2010; Levine & Zervos, Citation1998; Levine Citation2005; Yildirm, Ozdemir, & Dogan, Citation2013; Yousif, Citation2002), whereas a very little attention has been given to South Asian countries (inter alia: Sehrawat & Giri, Citation2015). Therefore, this study contributes to the literature by investigating this relationship focusing on a South Asian developing economy, Bangladesh. Secondly, in the context of Bangladesh there are a few studies that have focused on only the nexus between economic growth and stock market development, but according to our best knowledge much attention has not been given towards all three together in a single empirical study. The current study highlights this research gap focusing on the nexus among FDI, economic growth, and stock market development. As a result, this research brings all three endogenous growth indicators in one place, which can help investors and policy makers to understand the nature of economic growth in Bangladesh in the presence of political turbulence. Thirdly, studies on the effects of political instabilities on economic performances have ignored the moderating role of political instability on the relationship between economic growth and stock market development, relationship between economic growth and FDI, and relationship between FDI and stock market development (inter alia: Ahmed & Pulok, Citation2013; Aisen & Veiga, Citation2013; Alesina et al., Citation1996; Alesina & Perotti, Citation1996; An et al., Citation2016; Asteriou & Siriopoulos, Citation2000; Brada et al., Citation2006; Liu et al., Citation2017; William, Citation2017). Similarly, the existing empirical studies mainly focused on the endogenous relationship among economic growth, FDI, and stock market development, whereas, the moderating effect of political instability on these relationships has been given less attention (inter alia: Ang & McKibbin, Citation2007; Bengoa & Sanchez-Robles, Citation2003; Brambila-Macias & Massa, Citation2011; Bristy, Citation2014; Calderona & Lin, Citation2003; Chakraborty & Basu, Citation2002; Handa & Khan, Citation2008; Haque & Fatima, Citation2011; Hassan, Sanchez, & Yu, Citation2011; Hsiao &Hsiao, Citation2006; Iamsiraroj, Citation2016; Jalil et al., Citation2010; Kalaivani & Ibrahim, Citation2010; Li & Liu, Citation2005; Masuduzzaman, Citation2014; Nain & Kamaiah, Citation2014; Pan & Mishra, Citation2016; Rahman, Citation2015; Raza & Jawaid, Citation2014; Raza, Jawaid, Afshan, & Abd-Karim, Citation2015; Sahu & Dhiman, Citation2011; Sehrawat & Giri, Citation2015; Soumare & Tchana, Citation2015; Uddin, Shahbaz, Arouri, & Teulon, Citation2014; Uddin et al., Citation2014; Freckleton, Wright, & Craigwell, Citation2012; Yildirm, Ozdemir, & Dogan, Citation2013; Yousif, Citation2002). Therefore, according to our best knowledge this research is one of the first few studies that aim to investigate the moderating role of political instability on three relationships, for example: relationship between economic growth and stock market development, relationship between economic growth and FDI, and relationship between FDI and stock market development. Hence, the current study attempts to bridge the knowledge gap regarding the effects of political instability on the relationship of three very important macroeconomic variables. The findings uncover that political instability negatively moderates the endogenous relationship among economic growth and FDI and stock market development, suggesting that the existence of the political instability ultimately reduces the strength of the relationship; as a result, a country cannot achieve its desired level of economic growth, investment, and stock market development during the period of political unrest. Moreover, findings related to government policy and investment suggest that political stability is a key factor that attracts FDI and improves stock market development. Furthermore, the study results reveal that FDI partially mediates the relationship between economic growth and stock market development, which implies that the FDI inflows are important for economic growth and also for stock market development via economic growth. These findings imply that political stability is a vital factor for overall economic performance of Bangladesh. Therefore, political stability is a prerequisite for economic growth and capital market development.

The remaining of the paper is organized as follows. Section two reviews the existing literature and formulates the hypotheses for this current study. Section three discusses the empirical method for the analysis and the description of dataset with preliminary analysis. Section four depicts empirical results and findings. The final section includes closing remarks with future research directions.

2. Literature review and hypothesis development

2.1. Nexus of economic growth and stock market development

The notion endogeneity of finance and growth is first described by Levine (Citation1997). The theory indicates that the nature of the relationship can be unidirectional, bidirectional, or no relationship at all between stock market and growth (Yousif, Citation2002). The supply side theory suggests a unidirectional effect from stock market toward economic growth (Greenwood & Jovanovic, Citation1990; Hoque et al., Citation2017); on the other hand, the demand side theory indicates the unidirectional effects from economic advancement to stock market development (Demetriades & Hussein, Citation1996; Hoque et al., Citation2017). However, the feedback hypothesis proposes bidirectional effects between stock market development and economic growth (Bencivenga & Smith, Citation1991; Demetriades & Hussein, Citation1996; Greenwood & Smith, Citation1997) and the alternative hypothesis suggests no-relationship between financial market (stock market) and economic growth (Hoque et al., Citation2017; Lucas, Citation1988; Yousif, Citation2002).

The research on developed countries has been significantly documented with both unidirectional and bidirectional findings.Footnote5 However, the current study reviews only those studies, which focuses on developing and emerging country, to understand the nature of the relationship between capital market of a country and its economic growth. The research in the context of developing and emerging economies has also documented mixed findings, namely: unidirectional (inter alia: Ang & McKibbin, Citation2007; Brambila-Macias & Massa, Citation2011; Sehrawat & Giri, Citation2015; Yildirm et al., Citation2013), bidirectional (inter alia: Calderona and Lin, Citation2003; Hassan, Sanchez, & Yu, Citation2011; Jalil et al., Citation2010; Yildirm et al., 2013; Yousif, Citation2002), and no-relationship (inter alia: Nain & Kamaiah, Citation2014; Sahu & Dhiman, Citation2011). On the contrary, Pan and Mishra (Citation2016) reported a long-run negative association with the real sector of the economy with China’s A share market using ARDL model, which according to the authors is a proof of existence of irrational prosperity on the stock market and the bubbles in China’s financial sector. However, they could not find any short-term association between economic growth and stock market development.

In the context of Bangladesh, Handa and Khan (Citation2008) found existence of causal relationship between finance and economic growth, but the direction is from economic growth towards financial development (Grossman & Helpman, Citation1990). Uddin et al. (Citation2014) also reported similar findings, but the relationship exists only in the long-run. On the other hand, Bristy (Citation2014) and Masuduzzaman (Citation2014) found unidirectional effects of financial development on economic growth. Unlike others, using dynamic models, Haque and Fatima (Citation2011) did not find any linkage between stock market and economic growth. The mixed findings of the nature of relationship between growth and stock market development motivated the current research to further investigate the relation with new dataset. Therefore, this study hypothesizes as follow:

H1: Bidirectional causality exists between economic growth and stock market development.

2.2. Nexus of FDI and economic growth

Theoretically, there are several ways to explain the relationship between FDI and economic growth. The neoclassical growth theory claims that inflows of FDI accelerate the growth by allowing the increase in capital stock. From the perspective of endogenous growth theory, Shaw (Citation1973) and Romer (Citation1990) argue that economic growth can be increased with technological advancement by creating some positive externalities for the countries, as FDI can enrich the host countries by allowing access to advance technology that is not available in the host countries. Generally, when technology experts from the foreign countries invest in new projects, domestic investors can also participate and share the knowledge. Therefore, in brief, it can be said that FDI promotes economic growth and in case of FDI, it contributes more to developing countries than to developed economies (Johnson, Citation2006). On the other hand, growth of a country also promotes FDI inflows by showing the potentials for above average investment returns and prospective investment projects with lower labour and production costs.

Empirical research has found both bidirectional and unidirectional casual linkages between FDI and economic growth.Footnote6 Using the structured cointegration and VECM model, Chakraborty and Basu (Citation2002) found that the FDI does not cause GDP, but, GDP causes FDI. Bengoa and Sanchez-Robles (Citation2003) investigated the influences of FDI on growth and found that FDI and growth are positively and significantly correlated in Latin American countries. The results also indicate that the host countries must have stable economic conditions, adequate human capital, and financial liberalization (Bengoa & Sanchez-Robles, Citation2003). Employing simultaneous equation system techniques, Li and Liu (Citation2005) investigated the endogenity of FDI and growth for 84 countries for the period from year 1979 to 1989. They found that FDI and growth has indirect interactions, where FDI promotes economic growth through interaction terms like human capital exerts and technology, in developing countries. Using panel and time-series data, Hsiao and Hsiao (Citation2006) analysed the causality between FDI, GDP, and Exports for Eastern and South-eastern Asian countries. They observed that FDI has a direct unidirectional effect on GDP.

Esso (Citation2010) revisited the endogeneity between FDI and economic growth for ten (10) sub-Saharan countries. They found the existence of long-run relationship between FDI and economic growth in Angola, Cote d’Ivoire, Kenya, Liberia, Senegal, and South Africa. They also observed unidirectional effects of FDI on economic growth and economic growth to FDI; but the effects vary from country to country. Freckleton, Wright, and Craigwell (Citation2012) investigated the relationship between FDI and economic growth for both developing and developed countries. The results reflect that in both short- and long-run FDI promotes economic growth of developing and developed economies. Tekin (Citation2012) examined endogenity of FDI and growth from the view point of least developed countries and found the evidence that FDI Granger causes the GDP in Benin and Togo, and GDP Granger causes FDI in Burkina Faso, Gambia, Madagascar, and Malawi. Iamsiraroj (Citation2016) examined FDI and economic growth nexus for one hundred and twenty four (124) countries; the results indicated the existence of bidirectional relationship, where FDI has positive effects on growth and vice versa. Also, economic freedom and trade openness can stimulate GDP through FDI (Iamsiraroj, Citation2016).

Using the data from Bangladesh, few studies investigated the nexus between FDI and economic growth. Srinivasan, Kalaivani, and Ibrahim (Citation2010) used the cointegration and VECM approach to examine the relationship between GDP and FDI for SAARC countries. The results show that a long-run bidirectional relationship is evident between GDP and FDI for Bangladesh, India, Maldives, Nepal, Pakistan, and Sri Lanka. On the other hand, unidirectional causality exists in India’s case, which goes from GDP to FDI. Tabssum and Ahamed (Citation2014) examined the effects of domestic investment and FDI on economic growth, and reported that domestic investment is more significant than FDI for economic growth of the country. Rahman (Citation2015) showed that FDI and growth has negative correlation. The mixed findings of the causal relationship between FDI and growth encouraged us to further investigate the short- and long-run nature of relationships between the variables. Therefore, the current study hypothesizes that—

H2: There is a unidirectional causal effect on FDI from economic growth.

2.3. Nexus of FDI and stock market development

There are a few explanations for causal relationships between FDI and stock market development. Given that, FDI comes from developed countries where tradition of financing is via stock market. Therefore, FDI increases the possibility of listing of multinational companies in the host countries’ stock market (Alfaro, Chanda, Kalemli-Ozcan, & Sayek, Citation2010). This ultimately contributes in the development of stock market of the host country. Secondly, a well-functioning stock market attracts FDIs into the stock market portfolio, but investment inflows also depend on the level of business freedom and trade openness of the host country (Greenwood & Smith, Citation1997).

Empirical studies have shown mixed results on the nexus of FDI and stock market growth. Adam and Tweneboah (Citation2009) reported unidirectional causality from FDI to stock market development. Similarly, Kaleem and Shahabaz (Citation2009) found that in both short and long run FDI has a significant effect on stock market development. Using the Johansen cointegration test, Malik and Amjad (Citation2013) investigated the relationship between FDI and stock market development. They concluded that FDI simulates stock market development in the long run. Using VAR framework, Arčabić, Globan, and Raguž (Citation2013) investigated the causal relationship between FDI and stock market development in Croatia for the period of year 2001–2011. They found that, in the short run, FDI promotes stock market development.

Using the panel Granger causality model, Kholdy and Shariabian (Citation2005) found the existence of bidirectional association between financial markets and FDI in developed countries. Using ARDL bound testing cointegration approach Raza and Jawaid (Citation2014) examined the impact of FDI on stock market development in eighteen (18) Asian countries and confirmed the existence of bidirectional causal relationship of FDI and economic growth with stock market capitalization. Their study also suggests that there is a negative effect of FDI on stock market capitalization in the short run. Raza et al. (Citation2015) reported that FDI and economic growth have bidirectional relationship with stock market capitalization in Pakistan. Soumare and Tchana (Citation2015) used panel data to examine the causal relationship between financial market development and FDI. They reported that the bidirectional causality between FDI and stock market development is the indicator of the existence of a well-developed financial market in a developing country. Therefore, the study hypothesizes as follow:

H3: Bidirectional causality exists between stock market development and FDI.

2.4. Role of FDI on the relationship between stock market development and economic growth

FDI plays an important role in both economic growth and stock market development (Alfaro et al., Citation2010; Arčabić et al., Citation2013). In reality, economic growth attracts FDI to a country that again contributes towards improvement of stock market capitalization. Therefore, a good inflow of FDI ensures significant stock market development. However, FDI and economic growth also affect each other, because when the inflow of FDI in an economy increases, the economic growth of the country also boosts up. Therefore, the interaction between economic growth and FDI notably contributes towards stock market development. So, the current study hypothesises as follow—

H4: FDI mediates the relationship between economic growth and stock market development.

2.5. Role of the political instability on the relationship among FDI, economic growth, and stock market development

“Political instability can be viewed as instability of governments, regimes, and communities within a nation, and is likely to result from forcefully overthrowing or subjecting existing authorities to a high probability of involuntary removal” (Asteriou & Siriopoulos, Citation2000, p. 359). Political instability has strong negative effects on economic growth, FDI, and stock market development (Ahmed & Pulok, Citation2013; Aisen & Veiga, Citation2013; Alesina & Perotti, Citation1996; Gurgul & Lach, Citation2013). Therefore, political stability is required for increasing the capital inflow in stock market, to attract FDI and to stimulate economic growth.

Political instability and violence significantly affects the operation of a stock market (Roe & Siegel, Citation2011). During political unrest, investors may feel insecured to go outside and trade at stock market or brokerage house. They also feel anxious regarding the safety of their investment in a politically unstable economy. Similarly, news related to political unrests normally demotivates investors, and force them to withdraw their funds. As a result, during political unrests the trading volume and trade turnover in a stock market decline, which can cause stock price volatility and decline in the share prices (Karolyi & Martell, Citation2010). Such changes ultimately affect the stock market capitalization. In the same manner, political instability and violence affects the business operation of a company, which can result into lower production level along with delay in foreign export schedule. This type of scenario causes a downward pressure on firms’ profits and cash-flow and it negatively affects capitalization and growth of a stock market. All together these negative influences of political instability can eventually result in reduced economic output. Hence, it can be inferred that the presence of political instability negatively affects the economic growth and stock market development, which is presented in the form of testable hypothesis as follow:

H5: Political instability has dampening effects on the relationship between economic growth and stock market development.

Political stability is very crucial in attracting FDI to any country (Brada et al., Citation2006), as investors normally try to avoid unnecessary uncertainties related to investments. Furthermore, even when the economy grows at a desirable rate, political instability can trigger a negative state of mind among foreign investors and eventually can influence them to decide to not invest in a politically unstable country (Alesina et al., Citation1996); therefore, political turbulence negatively affects the relationship between economic growth and FDI. Moreover, in the same manner political instability negatively influences stock market development, as it discourages investors to invest in the market. Therefore, this study hypothesises as follow:

H6: Political instability moderates the relationship between economic growth and FDI.

H7: Political instability moderates the relationship between FDI and stock market development.

2.6. The conceptual research framework for the study

Based on formulated testable hypotheses, the current initiates two conceptual research models which are guide for conducting entire research. Figures and presents the conceptual framework for the study. The conceptual research model presented in Figure investigates the endogenous relationship among economic growth, FDI, and stock market development in Bangladesh and the conceptual research model enumerated in Figure examines the moderating effects of political instability on the relationship among FDI, economic growth, and stock market development in Bangladesh.

Figure 2. The conceptual model for endogeneity testing.

Figure 3. The conceptual model for meditation and moderation testing.

3. Dataset narratives and empirical methods

3.1. Data and variables used in the study

Like prior studies, this study uses GDP growth rate as a proxy for economic growth, and stock market capitalization as percentage of GDP is used as proxy for stock market development (Inter alia: Caporale, Howells, & Soliman, Citation2004; Enisan & Olufisayo, Citation2009; Massa, Citation2009; Shahabaz, Rehaman, & Muzaffar, Citation2015; Wongbangpo & Sharma, Citation2004). For the variable FDI, the yearly FDIs are also considered as percentage of GDP. For political instability,Footnote7 the World Bank’s (2011) country wise political stability index is used. The study also utilizes some selected macroeconomic variables of Bangladesh economy for the period from year 1993 to 2016, except for political instability. For political instability, data are available only from year 1996. Data are extracted from the website of Bangladesh Bank, World Bank, and Thompson Reuter’s DataStream.

3.2. Preliminary analysis

3.2.1. Descriptive statistics

Panel A and panel B of Table present the descriptive statistics and correlation matrix for the economic growth (growth), FDI, stock market development (SMD), and political instability (PI). The Kurtosis values and the Jarque-Bera test statistics indicate that the data are normally distributed. In addition, the data are positively skewed. The correlation among variables indicates that coefficients are within the cut-off value for regression, suggesting that there will be no multicollinearity issues in the regression models estimations.

Table 2. Summary statistics and correlation matrix

3.2.2. Unit root test

Before determining the regression models, it is necessary to check whether the time series are stationary. So, at first, we run unit root tests of Dickey and Fuller (Citation1979) and (Citation1981) and Phillips and Perron (Citation1988) to confirm, whether the series have unit root problem. Table demonstrates the estimates of Augmented Dickey Fuller (ADF) and Phillips Perron (PP) test at levels and at first differences of the data. At the level, all the variables have unit roots (by considering 5% level of significance). However, the variables have become stationary at the first difference. Also, none of the variables are trend stationary. Therefore, it can be said that all variables are stationary at same order that is at level one (I). The model does not have heteroscedasticity, as the regression between squared residuals and all independent variables from Heteroscedasticity White test (for both with cross terms and without cross terms) shows that the p value is more than 5%, which means the null hypothesis cannot be rejected, i.e. there is homoscedasticity.

Table 3. Unit root test results

3.3. Analytical framework and model estimation

3.3.1. The ARDL framework

The base case regression model for this study without moderation effect is as follow:

In the above Eq. 1, variable Growtht indicates the GDP growth rate in Bangladesh, FDIt is the FDI as percentage of GDP in period t, SMDt is the stock market capitalization as percentage of GDP in time period t, and Ut is the error term. We establish the above model by following traditional view that stock market development is an indicator of a country’s economy and an increase in FDI can flourish the economic growth.

We established the above regression model by considering the conventional view that the stock market and FDI are leading indicators of the economy of a country. The stock market has been regarded as a leading indicator of the economy. The traditional view believes that when the stock market experiences large growth the economy in the future is going to experience boom and vice versa (Comincioli, Citation1996). In the same way, theory suggests that FDI plays a vital role to modernize the economy and to promote growth in host countries, especially in developing countries, like: Bangladesh (Helpman & Grossman, 1990).

However, as stock market development is a leading indicator, lack of correlation between economic growth and stock market can be evident; moreover, the literature suggests that flourishing and growing economy increases the confidence of international investors and therefore higher GDP growth rate can also contribute towards increased FDI. To test these alternative views, we have formulated two additional equations by considering FDI and SMD as dependent variables. The equations are as follow:

Nevertheless, above Eqs. 1–3 cannot be estimated directly through Ordinary Least Square (OLS) method as it is the time series data. According to literature, OLS model can result in spurious regression results due to presence of unit root in the level form of the data set. Therefore, it is necessary to determine whether a long-run relationship exists among the variables in the model. For this purpose, the current study employs the bounds testing with Autoregressive Distributed Lag (ARDL) model proposed by Pesaran and Shin (Citation1998) and Pesaran et al. (Pesaran, Shin, & Smith, Citation2001). The ARDL model has several benefits over other conventional techniques of cointegration (e.g., Engle & Granger, Citation1987; Johansen & Juselius, Citation1990). First, it can be used irrespective of the order of the stationarity level of the data set, that is ARDL can be applied if the underlying variables are I(0), I(1) or a combination of both (Pesaran & Pesaran, Citation1997). Second, the ARDL procedure is statistically more significant approach to determine the cointegration relation in small samples to those of the Johensen and Juselius cointegration technique (Pesaran & Shin, Citation1998). Third, even if some of the regressors of the model are endogenous, the bounds testing approach can provide unbiased long-run estimates and valid t-statistics (Narayan, Citation2005). Fourth, the model can incorporate sufficient number of lags to capture the data generating process in a generic to specific modelling frameworks (Laurenceson & Chai, Citation2003). Fifth, from the ARDL model through a simple linear transformation, the error correction model (ECM) can be generated that integrates short-run adjustments with long-run equilibrium without loss of long-run information (Pesaran & Shin, Citation1999). The ARDL model consists of two basic steps for estimation of long-run relationship. The first step is to investigate the existence of the long-run relationships among all variables of the estimated equation. In the second step, the long-run and short-run models are estimated, provided that long-run cointegration is evident from the bounds testing. The ARDL framework for Eq. 1 is as follow:

In the above Eq. 4, α represents the drift component and Ut is white noise. The terms i and j represents the number of lags for the variables in the model, which is selected according to the optimal lag length criteria of SIC. Furthermore, the terms with summation signs represent the error correction dynamics and the second part of the equation with θi corresponds to long-run relationship. The following Eqs. 5 and 6 are formulated using the ARDL model to test the bidirectional influences of the variables FDI and SMD.

The above Eqs. 4–6 are error correction representations. So, in the next step the following error correction models are estimated.

where, represents the error correction term.

The coefficient of is expected to be negatively significant.

in the error correction models indicate the speed of adjustment to long-run equilibrium after a short-run shock. To ensure the goodness of fit of model, the diagnostic and stability tests are also performed. For the diagnostic test the serial correlation, normality and heteroscedasticity of the estimated model have been examined. Pesaran and Pesaran (Citation1997) suggested to use cumulative (CUSUM) and cumulative sum of squares (CUSUMSQ) for goodness of fit. The CUSUM and CUSUMSQ statistics are updated recursively and plotted against the break points. If the plots of CUSUM and CUSUMSQ statistics stay within the critical bands of 5% level of significance, the null hypothesis of stable coefficients in the given regression cannot be rejected.

3.3.2. Regression based on mediation and moderation models

In order to test mediation and moderation effects on the relationship among the endogenous variables of economic growth, stock market development, and FDI, we construct following econometric models.

where, Growtht indicates the GDP growth rate in Bangladesh, FDIt is the FDI as percentage of GDP in period t, SMDt is the stock market capitalization as percentage of GDP in time period t, indicates rate of political instability index of Bangladesh in time period t, and Ut is the error term.

4. Empirical results and discussions

4.1. Bound testing for cointegration

After establishing the order of integration, we have tested the long-run relationship among the variables. Before examining the existence of cointegration the optimal lag length has been chosen using Akike Information Criteria (AIC), Schawrz Byesian (SW), and Hannan Quinn (HQ) criteria. The optimal lag length for the model of the current study is 2 (see appendix table 1A). ARDL model estimates (p + 1)k regression equations to obtain optimal lags for each variable, where p is the maximum number of lags required and k is the number of regressors in the regression equation. There are four methods to decide the optimal ARDL model, for example: Akaike Information Criterion (AIC), Schwartz Bayesian Criterion (SBC), Hannan-Quinn Criterion, and adjusted R-squares. Based on a balanced consideration of almost all the aspects, such as, coefficient significance, goodness of fit of the model, serial correlation, and model stability the best models for Eqs. 4–6 are chosen.

Next, the study estimates the F-statistics for cointegration test using the optimal lag length for each model. The results of F-statistics for the optimal lag length are presented in Table . Table shows that the computed value of F-statistic for model A (5.39) and model C (4.91) which are greater than the upper bound value of F-statistic at 5% level of significance. Hence, we can reject the null hypothesis of no long-run relationship for in ARDL model A (Eq. 4) and C (Eq. 6). Therefore, we conclude that long-run relationship exists among the variables in model A and C. Furthermore, the existence of no-cointegrating relationship in ARDL model B (Eq. 5) suggests that no further analysis is necessary for this model.

Table presents the long-run coefficients of model A and C. The outputs of model A indicate the existence of positively significant impact of FDI on growth, while SMD has negative but significant effect on growth. The positive relationship between FDI and economic growth is expected, as foreign capital inflows bring economic prosperities to the economy of a country (see Hoque & Yakob, Citation2017). However, the negative relation between growth and SMD is not expected; as, a well-functioning stock market should positively influence economic growth. Nevertheless, this finding is consistent with those of Pan and Mishra (Citation2016) for Chinese stock market and economic growth. This negative relationship can also be true for Bangladesh, as for a very long period stock market of the country is not performing up to the desired level. In addition, this outcome is also an existence of irrational risk taking behaviour of investors and investors’ perceptions due to the politically unstable situation in Bangladesh. Moreover, from Model C in Table , we find that in the long run only FDI influences stock market development significantly, which is also expected, because foreign capital inflows and foreign investors’ participation increase capital inflows to the stock market and hence results in stock market growth.

Table 5. Long-run coefficients from the estimated ARDL models

Table presents the error correction representations of ARDL models A and C. As we can observe from the model outputs that the coefficient ECM (−1) terms consist correct signs for both the models. The error correction representations of model A indicate that in short run both FDI and SMD significantly affect growth. From error correction representations of model C, we detect that, in short run both growth and FDI significantly influences stock market development.

Table 6. Error correction representations of the selected ARDL models

Both the long- and short-run coefficients indicate that stock market development and economic growth affects each other. These findings suggest the existence of a bidirectional relationship between stock market and economic growth that supports our hypothesis H1. This finding is also supported by extant studies (inter alia: Calderona & Lin, Citation2003; Jalil et al., Citation2010; Hassan, Sanchez, & Yu, Citation2011; Yildirm, 2013; Yousif, Citation2002) . Furthermore, we find short- and long-run unidirectional relationship from FDI to growth. Therefore, the hypothesis H2 is also supported. This result is also supported be the findings of several past empirical studies (inter alia: Esso, Citation2010; Hsiao & Hsiao, Citation2006; Tabssum & Ahamed, Citation2014; Wright & Craigwell, 2012). Moreover, FDI is found to promote the SMD in both short and long run. This finding indicates the existence of positively significant unidirectional relationship from FDI to SMD. Hence, this finding does not support our hypothesis H3. The unidirectional causal effect from FDI to SMD is expected, but causal effect from SMD to FDI is also desirable. Though, the existence of unidirectional relationship between FDI and SMD is supported by prior studies (Adam & Tweneboah, Citation2009; Kaleem & Shahabaz Citation2009; Malik & Amjad, Citation2013), this type of causal relationship is an indicator of underperforming stock market in Bangladesh; which fails to attract foreign capital inflows and increase foreign investors’ participation.

4.2. Regression-based mediation and moderation test

Table presents the results for mediation and moderation effects. To measure the moderation and mediation impacts, the study has employed SPSS with PROCESSFootnote8 written by Andrew F. Hayes and Preacher (Citation2013). Built in models 1 and 4 of PROCESS, have been used to test the moderation and mediation effects, respectively.

Table 7. Regression results for meditation and moderations

Model D estimates direct effects of FDI and economic growth on stock market development, and also estimates indirect effect of economic growth via FDI on stock market development. The results show that economic growth has negative impact on stock market development, which is partially consistent with ARDL estimation. The findings also show that there are positively significant direct effects of FDI and economic growth on stock market. These findings are in line with ARDL estimation. The findings also suggest that there is indirect impact of economic growth on stock market development, which is channelled through FDI. This finding implies that the relationship between economic growth and stock market development is partially mediated by FDI. Therefore, the finding supports the hypothesis H4, which implies that FDI is an important factor for promoting stock market more efficiently and effectively.

Model E estimates the moderating effects of political instability on the relationship between economic growth and stock market development and like model A, this model also shows that economic growth has negative effect on stock market development. Moreover, the findings indicate that political instability negatively influences the stock market development. The negative effects of political instabilities on stock market development are consistent with those findings of Asteriou and Siriopoulos (Citation2000) and Roe and Siegel (Citation2011). In terms of moderating effects of political instability, the findings show that the interaction between economic growth and political instability has negative effect on stock market development. This finding indicates that the politically unstable situation dampens the relationship of economic growth and stock market development. Hence, this finding supports the hypothesis H5, which inferred that political instability limits the economic growth in promoting stock market development. Perhaps, the presence of political instability contributes to the negative relationship between economic growth and stock market development. The findings are consistent with last 10 years’ economic and political conditions of Bangladesh. Though, the economy of Bangladesh is growing yearly by more than 5%, but stock market is not performing very well after the crash in the year 2010–2011 (Azad, Azmat, Fang, & Edirisuriya, Citation2014).

The model F estimates moderating effects of political instability on the relationship between economic growth and FDI. The findings show that political instability has negative impact on FDI, which in line with Brada et al. (Citation2006) and Williams (Citation2017). The findings also show that economic growth has positive effect on FDI. Furthermore, the coefficient of interaction term of political instability and economic growth is appeared significantly negative. This result uncovers that political instability negatively moderates the relationship between economic growth and FDI. This finding supports the hypothesis H6, which infers that even though economic growth gives positive signal to foreign investors to invest in the economy, the presence of political instability demotivates the foreign investors. Therefore, in the past decade, Bangladesh observed lower FDI growth rate compared to earlier.

Model G estimates moderating effects of political instability on the relationship between FDI and stock market. The positive impact of FDI on stock market development is expected, whereas the impact of political instability is negatively significant for SMD. As the main intention of this model is to identify the moderating role of political instability on the relationship between FDI and stock market development, the estimation outputs show that moderating effect of political instability is negative on the relationship between FDI and stock market development; hence, this finding supports the hypothesis H7. Therefore, according to the findings it can be deduced that presence of political instability does not allow FDI to promote stock market development.

5. Concluding remarks

This study was an initial attempt to investigate the long-run and short-run equilibrium relationships among economic growth, FDI and stock market development by considering the issue of causality among the variables along with the moderating role of political instability in Bangladesh. In order to capture both long-run cointegration and short-run dynamics of the relationships, we employed the ARDL model with bound testing approach instead of the ordinary Johansen cointegration analysis. In short-run FDI and SMD significantly influences growth, and also growth and FDI significantly influences stock market development. However, in the long run only FDI influences stock market development significantly. On the other hand, stock market development and economic growth affects each other in the long run but the sign of the relationship is not expected, implying that exploring the sources of economic growth is a complicated topic and sometimes country specific situations can contribute towards a deviation of the empirical results from the theoretical assumptions. Moreover, short- and long-run unidirectional relationship from FDI to growth and the absence of causality from SMD to FDI indicates that the stock market of Bangladesh is not able to attract foreign investors. One plausible explanation for this outcome can be weak and fragile stock market fundamentals. The stock market of Bangladesh is comparatively new and it is dominated by individual small investors. As the stock markets of Bangladesh are inefficient in the weak form (Mobarek, Mollah, & Bhuyan, Citation2008), the returns in the market are nonrandom and the investors can generate abnormal returns through a competitive informational advantage and speculation. Market manipulations are also very common phenomenon in such market (Azad, Azmat, Fang, & Edirisuriya, 2014). All these stock market phenomena of the country together contribute towards the lack of interest of the foreign investors, and therefore economy fail to attract FDI. The regulatory bodies related to the capital market must take necessary steps to improve the overall governance of the stock market and to protect the investors’ interests, in order to increase the domestic and foreign capital inflows.

The empirical results reveal that there is existence of negative direct and moderating effects of political instability in Bangladesh on the relationship between economic development and stock market, relationship between economic development and FDI, and relationship between stock market and FDI. Thus, the empirical results suggest that the presence of political unrest reduces the strength of the relationships among the examined macroeconomic variables. These findings have some major policy implications. Firstly, the quantitative results of the study imply that the existence of political instability is one of the major causes that limit the economic advancement of Bangladesh. Therefore, the government of Bangladesh should focus more on the achievement of political stability for a sustainable economic growth rate of the country. Secondly, to attract more FDI the government needs to focus on the development of the capital market of the country. A developed and well-functioning capital market draws the attention of domestic and foreign investors’ in the form of increased portfolio investment and institutional participation in a stock market. Thirdly, in order to increase FDI and to develop the stock market Bangladesh needs to ensure that the investors’ rights are protected and the stock market is not negatively influenced due to political turbulence. If the government of Bangladesh can successfully address the root causes of political instability and try to mitigate its negative effects, while designing and implementing the economic policies, only then the country can grow at a rate that is sustainable.

Furthermore, the results reveal that FDI partially mediates the relationship between economic growth and stock market development. Therefore, it can be inferred that FDI inflows are important for economic growth and also FDI contributes towards the stock market development of the country. Thus, based on the overall empirical finding, this study once again suggest that political stability is a vital factor for overall economic performance of Bangladesh. Thus, it a necessary condition for economic performance; otherwise, the economy can achieve its desired goal and performance.

Nevertheless, this study focuses mainly on the interaction effects of political instability, on the relationship between economic growth and stock market development, the relationship between economic growth and FDI, and finally on the relationship between stock market development and FDI. However, there are several influential factors that can moderate and mediate these relationships, for example: governance quality, economic freedom, investment freedom, legal framework, etc. Hence, future studies can explore the nature and extent of the moderating influence of these factors on the relationship between economic growth and stock market development, between growth and FDI, and on the relationship between stock market development and FDI.

Additional information

Funding

Notes on contributors

Mohammad Enamul Hoque

Mohammad Enamul Hoque is a Doctoral Candidate at UKM-GSB, Universiti Kebangsaan Malaysia. His research interests are in the areas of asset pricing, monetary economics, Financial consumer’s behaviour, and Applied Economics and Finance. His works are appeared in the Service Industries Journal, Journal of Islamic Marketing, and Cogent Economic and Finance.

Tahmina Akhter

Tahmina Akhter is an Assistant Professor at Faculty of Business, University of Dhaka and a Doctoral Candidate at UKM-GSB, Universiti Kebangsaan Malaysia. Her research interests are in the areas of Corporate Finance, Financial Markets, and Applied Economics and Finance.

Noor Azuddin Yakob

Noor Azuddin Yakob is an Associate Professor at UKM-GSB, Universiti Kebangsaan Malaysia. His research interests are in the areas of Corporate Finance, Financial Markets, and Behavioural Finance. He has published his works in the Cogent Economic and Finance, Journal of Asset Management, International Business & Economics Research Journal, International Journal of Science and Research, Capital Market Review, and Jurnal Pengurusan.

Notes

1. “Theoretically and practically, it has been considered that growth is the soul of macroeconomics, and capital market is the pulse of an economy. Stock market serves as a platform for companies to raise equity capital for investment and capital expenditure (Levine & Zervos, Citation1998). It also plays a significant role in industrial and economic growth. Furthermore, a well-functioning stock market makes macroeconomy more efficient (Engle, Ghysels, & Sohn, Citation2013). Certainly, from the opposite direction, macroeconomic variables also enhance stock market performance (Seetanah, Citation2008). Additionally, macroeconomic policy and financial market liberalization make the stock market better functioning and efficient” (Hoque & Yakob, Citation2017, p. 4).

2. According to Asteriou & Siriopoulos (Citation2000, p. 359), “Political instability can be viewed as instability of governments, regimes, and communities within a nation, and is likely to result from forcefully overthrowing or subjecting existing authorities to a high probability of involuntary removal.”

3. “These strikes, locally known as hartals, are organized by opposition political parties and interest groups in Bangladesh as a form of protest against the government. These strikes typically last an entire working day although the duration could either be shorter or longer. While hartals trace their roots to earlier episodes of civil disobedience against colonialism in South Asia, their prevalence in Bangladesh has increased dramatically in recent years. Hartals are especially costly because they are used to coercively shut down factories, roads, ports, as well as all private and public institutions. The requirement that such activities/institutions be halted is enforced by the threat of violence” (Ahsan & Iqbal, Citation2014).

4. World Bank Report on Bangladesh development updates (April 2015).

5. See literature for developed countries, for example, Levine and Zervos (Citation1998); Levine (2005); Duca (Citation2007).

6. See (Borenszteina, Gregorio, & Lee, Citation1998; De Mello, Citation1999; Dutt, Citation1997), among others for literature before 2000s.

7. According to Kaufmann et al. (Citation2010, p. 4) “Political stability and absence of violence capturing perceptions of the likelihood that the government will be destabilized or overthrown by unconstitutional or violent means, including politically motivated violence and terrorism.” However, in study we used political instability because the score on this index presents negative scores for Bangladesh, and that negative scores is referred as political instability.

8. PROCESS is a programming language installed in SPSS for Mediation and Moderation Test. The PROCESS written based 76 developed models for both moderation and mediation. The good thing about PROCESS is it care covariates of dependent variables and mediator/moderator.

Related Research Data

References

- Adam, A., & Tweneboah, G. (2009). Foreign direct investment and stock market development: Ghana’s evidence. International Research Journal of Finance and Economics, 26, 178–185.

- Ahmed, M. U., & Pulok, M. H. (2013). The role of political stability on economic performance: The case of Bangladesh. Journal of Economic Cooperation and Development, 34(4), 61–100.

- Ahsan, R. N., & Iqbal, K. (2014). Political strikes and its impacts on trade: Evidence from Bangladeshi transaction-level export data. International Growth Center: Working paper.

- Aisen, A., & Veiga, F. J. (2013). How does political instability affect economic growth? European Journal of Political Economy, 29, 151–167. doi:10.1016/j.ejpoleco.2012.11.001

- Alesina, A., Özler, S., Roubini, N., & Swagel, P. (1996). Political instability and economic growth. Journal of Economic Growth, 1(2), 189–211. doi:10.1007/BF00138862

- Alesina, A., & Perotti, R. (1996). Income distribution, political instability and investment. European Economic Review, 40, 1203–1228. doi:10.1016/0014-2921(95)00030-5

- Alfaro, L., Chanda, A., Kalemli-Ozcan, S., & Sayek, S. (2010). How does foreign direct investment promote economic growth? Exploring the effects of financial markets on linkages. Journal of Development Economics, 91(2), 242–256. doi:10.1016/j.jdeveco.2009.09.004

- An, H., Chen, Y., Luo, D., & Zhang, T. (2016). Political uncertainty and corporate investment: Evidence from China. Journal of Corporate Finance, 36, 174–189. doi:10.1016/j.jcorpfin.2015.11.003

- Ang, J., & McKibbin, W. (2007). Financial liberalization, financial sector development and growth: Evidence from Malaysia. Journal of Development Economics, 84(1), 215–233. doi:10.1016/j.jdeveco.2006.11.006

- Arčabić, V., Globan, T., & Raguž, I. (2013). The relationship between the stock market and foreign direct investment in Croatia: Evidence from VAR and cointegration analysis. Financial Theory and Practice, 37(1), 109–126. doi:10.3326/fintp.37.1.4

- Asteriou, D., & Siriopoulos, C. (2000). The role of political instability in stock market development and economic growth: The case of Greece. Economic Notes, 29(3), 355–374. doi:10.1111/ecno.2000.29.issue-3

- Azad, A. S, Azmat, S, Fang, V, & Edirisuriya, P. (2014). Unchecked manipulations, price–volume relationship and market efficiency: Evidence from emerging markets. Research in International Business and Finance, 30, 51–71.

- Barro, R. J, & Sala-i-Martin, X. (1995). Economic growth. New York: McGraw Hill.

- Bencivenga, V. R., & Smith, B. D. (1991). Financial intermediation and endogenous growth. Review of Economic Studies, 58, 195–209. doi:10.2307/2297964

- Bengoa, M., & Sanchez-Robles, B. (2003). Foreign direct investment, economic freedom and growth: New evidence from Latin America. European Journal of Political Economy, 19(3), 529–545. doi:10.1016/S0176-2680(03)00011-9

- Borenszteina, E., Gregorio, J. D., & Lee, J.-W. (1998). How does foreign direct investment affect economic growth. Journal of International Economics, 45(1), 115–135. doi:10.1016/S0022-1996(97)00033-0

- Brada, J., Kutan, A., & Yigit, T. (2006). The effects of transition and political instability on foreign direct investment inflows. Economics of Transition, 14(4), 649–680. doi:10.1111/ecot.2006.14.issue-4

- Brambila-Macias, J., & Massa, I. (2011). Finance-growth nexus: Evidence from a top global reformer. Applied Financial Economics, 21, 529–544. doi:10.1080/09603107.2010.533997

- Bristy, H. J. (2014). Impact of financial development on exchange rate volatility and long-run growth relationship of Bangladesh. International Journal of Economics and Financial Issues, 4(2), 258–263.

- Calderon, C., & Lin, L. (2003). The direction of causality between financial development and economic growth. Journal of Development Economics, 72(1), 321–334. doi:10.1016/S0304-3878(03)00079-8

- Caporale, G., Howells, P., & Soliman, A. (2004). Stock market development and economic growth: The causal linkage. Journal of Economic Development, 29(1), 33–50.

- Chakraborty, C., & Basu, P. (2002). Foreign direct investment and growth in India: A cointegration approach. Applied Economics, 34(9), 1061–1073. doi:10.1080/00036840110074079

- Chowdhury, S. 2015. Political turmoil biggest risk to stockmarket. Dhaka: Thedailystar. Retrieved from http://www.thedailystar.net/political-turmoil-biggest-risk-to-stockmarket-62128

- Comincioli, B. (1996). The stock market as a leading indicator: An application of granger causality. University Avenue Undergraduate Journal of Economics, 1(1), 1.

- De Mello, L. J. (1999). Foreign direct investment‐led growth: Evidence from time series and panel data. Oxford Economic Papers, 51(1), 131–151. doi:10.1093/oep/51.1.133

- Demetrides, P., & Hussein, K. (1996). Does financial development cause economic growth? Time-series evidence from 16 countries. Journal of Development Economics, 51(2), 387–411. doi:10.1016/S0304-3878(96)00421-X

- Dickey, D., & Fuller, W. (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association, 74, 427–431.

- Dickey, D., & Fuller, W. (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica: Journal of the Econometric Society, 49, 1057–1072. doi:10.2307/1912517

- Duca, G. (2007). The relationship between the stock market and the economy: Experience from international financial marketsinternational financial markets. Bank of Valletta Review, 36(3), 1–12.

- Dutt, A. K. (1997). The pattern of direct foreign investment and economic growth. World Development, 25(11), 1925–1936. doi:10.1016/S0305-750X(97)00081-8

- Engle, R. F., & Granger, C. W. (1987). Co-integration and error correction: representation, estimation, and testing. Econometrica: journal of the Econometric Society, 251–276.

- Engle, R. F., & Ghysels, E., & Sohn, B. (2013). Stock marketvolatility and macroeconomic fundamentals. Review ofEconomics and Statistics, 95(3), 776–797.https://doi.org/10.1162/REST_a_00300

- Enisan, A. A., & Olufisayo, A. O. (2009). Stock market development and economic growth: Evidence from seven sub-Sahara African countries. Journal of Economics and Business, 61, 162–171. doi:10.1016/j.jeconbus.2008.05.001

- Esso, L. (2010). Long-run relationship and causality between foreign direct investment and growth: Evidence from ten african countries. International Journal of Economics and Finance, 2(2), 168. doi:10.5539/ijef.v2n2p168

- Freckleton, M., Wright, A., & Craigwell, R. (2012). Economic growth, foreign direct investment and corruption in developed and developing countries. Journal of Economic Studies, 39(6), 639–652. doi:10.1108/01443581211274593

- Greenwood, J., & Jovanovic, B. (1990). Financial development, growth, and the distribution of income. Journal of Political Economy, 98, 1076–1110. doi:10.1086/261720

- Greenwood, J., & Smith, B. (1997). Financial markets in development and the development of financial marketsdevelopment of financial markets. Journal of Economic Dynamics and Control, 21(1), 145–181. doi:10.1016/0165-1889(95)00928-0

- Grossman, G. M, & Helpman, E. (1990). Trade, innovation, and growth. The American Economic Review, 80(2), 86–91.

- Gurgul, H., & Lach, Ł. (2013). Political instability and economic growth: Evidence from two decades of transition in CEE. Communist and Post-Communist Studies, 46(2), 189–202. doi:10.1016/j.postcomstud.2013.03.008

- Handa, J., & Khan, S. R. (2008). Financial development and economic growth: A symbiotic relationship. Applied Financial Economics, 18(13), 1033–1049. doi:10.1080/09603100701477275

- Hassan, M. K., Sanchez, B., & Yu, J.-S. (2011). Financial development and economic growth: New evidence from panel data. The Quarterly Review of Economics and Finance, 51(1), 88–104. doi:10.1016/j.qref.2010.09.001

- Hauqe, M., & Fatima, N. (2011). Influences of stock market on real economy: A case study of Bangladesh. The Global Journal of Finance and Economics, 8(1), 49–60.

- Hayes, A. (2011). My macros and code for SPSS and SAS.

- Hayes, A. F., & Preacher, K. J. (2013). Conditional process modeling: Using structural equation modeling to examine contingent causal processes.

- Hoque, M. E., & Yakob, N. A. (2017). Revisiting stock market development and economic growth nexus: The moderating role of foreign capital inflows and exchange rates. Cogent Economics & Finance, 5(1), 1329975. doi:10.1080/23322039.2017.1329975

- Hsiao, F. S., & Hsiao, M.-C. W. (2006). FDI, exports, and GDP in East and Southeast Asia—Panel data versus time-series causality analyses. Journal of Asian Economics, 17(6), 1082–1106. doi:10.1016/j.asieco.2006.09.011

- Hussain, Z. (2015). Bangladesh development update April. (2015). Bangladesh development update. World Bank. Retrieved from http://documents.worldbank.org/curated/en/2015/04/24323972/bangladesh-development-update-april-2015

- Iamsiraroj, S. (2016). The foreign direct investment–Economic growth nexus. International Review of Economics & Finance, 42(1), 116–133. doi:10.1016/j.iref.2015.10.044

- Jalil, A., Wahid, N., & Shahbaz, M. (2010). Financial development and growth: A positive, monotonic relationship: Empirical evidences from South Africa. MPRA Paper No: 27668.

- Johnson, A. (2006). The effects of FDI inflows on host country economic growth. The Royal Institute of technology. Centre of Excellence for studies in Science and Innovation http://www.infra.kth.se/cesis/research/publications/workingpapers

- Johansen, S., & Juselius, K. (1990). Maximum likelihood estimation and inference on cointegration—With applications to the demand for money. Oxford Bulletin of Economics and Statistics, 52(2), 169–210. doi:10.1111/j.1468-0084.1990.mp52002003.x

- Kalaivani, M, & Ibrahim, P. (2010). FDI and economic growth in the ASEAN countries: Evidence from cointegration approach and causality test. IUP Journal of Management Research, 9(1), 38.

- Kaleem, R., & Shahbaz, M. (2009). Impact of foreign direct investment on stock market development: The case of Pakistan. Cambridge, United Kingdom: 9th Global Conference on Business and Economics, Cambridge University.

- Karolyi, G., & Martell, R. (2010). Terrorism and the stock market. International Review of Applied Financial Issues and Economics, 2, 285–314.

- Kaufmann, D., Kraay, A., & Mastruzzi, M. (2010). The worldwide governance indicators: Methodology and analytical issues. World Bank Policy Research Working Paper 5430.

- Khatun, F. (2015, December 29). Political stability is the key to growth in Bangladesh. East Asia Forum. Retrieved from http://www.eastasiaforum.org/2015/12/29/political-stability-is-the-key-to-growth-in-bangladesh/

- Kholdy, S., & Sohrabian, A. (2005). Financial markets, FDI, and economic growth: Granger causality test in panel data models. Working Paper, California State Polytechnic University.

- La Porta, R, Lopez‐de‐Silanes, F, Shleifer, A, & Vishny, R. (2002). Investor protection and corporate valuation. The Journal of Finance, 57(3), 1147–1170.

- Laurenceson, J., & Chai, J. C. (2003). Financial reform and economic development in China. Edward Elgar Publishing.

- Levine, R. (1997). Financial development and economic growth: Views and agendas. Journal of Economic Literature, 35, 688–726.

- Levine, R. (2005). Finance and growth: Theory and evidence. In A. Philippe & N. Steven (Eds.), Handbook of economic growth (pp. 865–934). Amsterdam: Elsevier.

- Levine, R., & Sara, Z. (1996). Stock market development and long-run growth. The World Bank Economic Review, 10, 2. doi:10.1093/wber/10.2.323

- Levine, R., & Zervos, S. (1998). Stock markets, banks, and economic growth. American Economic Review, 88(3), 537–558.

- Li, X., & Liu, X. (2005). Foreign direct investment and economic growth: An increasingly endogenous relationship. World Development, 33(3), 393–407. doi:10.1016/j.worlddev.2004.11.001

- Liu, L. X., Shu, H., & Wei, K. J. (2017). The impacts of political uncertainty on asset prices: Evidence from the Bo scandal in China. Journal of Financial Economics, 125(2), 286–310. doi:10.1016/j.jfineco.2017.05.011

- Lucas, R. (1988). On the mechanics of economic development. Journal of Monetary Economics, 22(1), 3–42. doi:10.1016/0304-3932(88)90168-7

- Malik, I. A., & Amjad, S. (2013). Foreign direct investment and stock market development in Pakistan. Journal of International Trade Law and Policy, 12(3), 226–242. doi:10.1108/JITLP-02-2013-0002

- Massa, I. (2009). Stock markets in Africa: Bidding for growth amid global turmoil. Overseas Development Institute.

- Masuduzzaman, M. (2014). Workers’ remittance inflow, financial development and economic growth: A Study on Bangladesh. International Journal of Economics and Finance, 6(8), 247–267. doi:10.5539/ijef.v6n8p247

- Mobarek, A, Mollah, A. S, & Bhuyan, R. (2008). Market efficiency in emerging stock market: Evidence from Bangladesh. Journal of Emerging Market Finance, 7(1), 17–41.

- Nain, M., & Kamaiah, B. (2014). Financial development and economic growth in India: Some evidence from non-linear causality analysis. Economic Change and Restructuring, 47(4), 299–319. doi:10.1007/s10644-014-9151-5

- Narayan, P. K. (2005). The saving and investment Nexus for China: Evidence from cointegration tests. Applied Economics, 37(17), 1979–1990. doi:10.1080/00036840500278103

- Pan, L., & Mishra, V. 2016. Stock market development and economic growth: Empirical evidence from China. Monash University, Department of Economics.

- Pesaran, B., & Pesaran, M. H. (2009). Microfit 5.0. Oxford: Oxford University Press.

- Pesaran, H. H., & Shin, Y. (1998). Generalized impulse response analysis in linear multivariate models. Economics Letters, 58(1), 17–29. doi:10.1016/S0165-1765(97)00214-0

- Pesaran, M. H., & Pesaran, B. (1997). Working with Microfit 4.0: Interactive econometric analysis;[Windows version]. Oxford University Press.

- Pesaran, M. H., & Shin, Y. (1999). An autoregressive distributed-lag modelling approach to cointegration analysis. Econometric Society Monographs, 31, 371–413.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. doi:10.1002/(ISSN)1099-1255

- Phillips, P. C., & Perron, P. (1988). Testing for a unit root in time series regression. Biometrika, 75(2), 335–346.

- Rahman, A. (2015). Impact of foreign direct investment on economic growth: Empirical evidence from Bangladesh. International Journal of Economics and Finance, 7(2), 178–185. doi:10.5539/ijef.v7n2p178

- Raza, S., & Jawaid, S. (2014). Foreign capital inflows, economic growth and stock market capitalization in Asian countries: An ARDL bound testing approach. Quality & Quantity, 48(1), 375–385. doi:10.1007/s11135-012-9774-4

- Raza, S. A., Jawaid, S. T., Afshan, S., & Abd-Karim, M. Z. (2015). Is stock market sensitive to foreign capital inflows and economic growth?. Journal of Chinese Economic and Foreign Trade Studies, 8(3), 142–164. doi:10.1108/JCEFTS-03-2015-0012

- Robinson, J. (1952). The Generalization of the General Theory. In The Rate of Interest and Other Essays. London: MacMillan.

- Roe, M., & Siegel, J. (2011). Political instability: Effects on financial development, roots in the severity of economic inequality. Journal of Comparative Economics, 39(3), 279–309. doi:10.1016/j.jce.2011.02.001

- Romer, P. (1990). Endogenous technological change. Journal of Political Economy, 98(1), 71–102. doi:10.1086/261725

- Sahu, N. C., & Dhiman, D. H. (2011). Correlation and causality between stock market and macro economic variables in India: An empirical study. IPEDR, 3, 281–284.

- Schumpeter, J. A. (1913). The theory of economic development. Cambridge, MA: Harvard University Press.

- Seetanah, B. (2008). Financial development and economicgrowth in an ARDL approach. Applied Economics Letter, 44, 43–50.

- Sehrawat, M., & Giri, A. (2015). Financial development and economic growth: Empirical evidence from India. Studies in Economics and Finance, 32(3), 340–356. doi:10.1108/SEF-10-2013-0152

- Shahabaz, M., Rehaman, I., & Muzaffar, T. (2015). Re-visiting financial development and economic growth Nexus: The role of capitalization in Bangladesh. South African Journal of Economics, 83(2), 452–472. doi:10.1111/saje.12063

- Shaw, E. S. (1973). Financial deepening in economic development.

- Soumaré, I., & Tchana, F. T. (2015). Causality between FDI and financial market development: Evidence from emerging markets. The World Bank Economic Review, 29(1), S205–S216. doi:10.1093/wber/lhv015

- Srinivasan, P., Kalaivani, M., & Ibrahim, P. (2010). An empirical investigation of foreign direct investment and economic growth in SAARC nations. Journal of Asia Business Studies, 5(2), 232–248. doi:10.1108/15587891111152366

- Tabassum, N., & Ahmed, S. P. (2014). Foreign direct investment and economic growth: Evidence from Bangladesh. International Journal of Economics and Finance, 6(9), 117–135. doi:10.5539/ijef.v6n9p117

- Tekin, R. B. (2012). Economic growth, exports and foreign direct investment in least developed Countries: A panel Granger causality analysis. Economic Modelling, 29(3), 868–878. doi:10.1016/j.econmod.2011.10.013

- Thedailystar. 2015. Infrastructure, political stability key to high growth: Analysts. Dhaka: Author. Retrieved from. http://www.thedailystar.net/infrastructure-political-stability-key-to-high-growth-analysts-29703

- Uddin, G. S., Shahbaz, M., Arouri, M., & Teulon, F. (2014). Financial development and poverty reduction nexus: A cointegration and causality analysis in Bangladesh. Economic Modelling, 36(1), 405–412. doi:10.1016/j.econmod.2013.09.049

- Williams, K. (2017). Foreign direct investment, economic growth, and political instability. Journal of Economic Development, 42(2), 17.

- Wongbangpo, P., & Sharma, S. (2004). Stock market and macroeconomic fundamental dynamic interactions: ASEAN-5 countries. Journal of Asian Economics, 13(1), 27–51. doi:10.1016/S1049-0078(01)00111-7

- World Bank. (1993). The Asian miracle: Economic growth and public policy. New York: Oxford University.

- Yildirm, S., Ozdemir, B. K., & Dogan, B. (2013). Financial development and economic growth Nexus in emerging European economies: New evidence from asymmetric causality. International Journal of Economics and Financial Issues, 3(3), 710–722.

- Yousif, K. (2002). Financial development and economic growth: Another look at the evidence from developing countries. Review of Financial Economics, 11(1), 131–150. doi:10.1016/S1058-3300(02)00039-3