?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper investigates the effect of oil price shocks on government expenditures on the health and education sectors in Saudi Arabia. Using a quarterly dataset 1990Q1–2017Q2 and employing a non-linear autoregressive distributed lag (NARDL) model, our research shows evidence of a non-linear relationship between oil prices and government expenditures in Saudi Arabia, where a negative oil price shock would have a statistically significant different impact in the long run compared to a positive shock. We build upon our empirical findings and draw some policy recommendations for Vision 2030 of Saudi Arabia.

PUBLIC INTEREST STATEMENT

Previous research stresses on the fact that large and unanticipated changes in energy prices could have significant negative effects on oil-dependent economies. An important channel through which low oil prices are expected to affect key economic variables in oil-rich countries is government revenues. Sharp and continuous drops in government revenues would certainly harm government development plans. This paper contributes to the existing literature by studying whether the impact of oil price increases and decreases would have different impacts on government expenditures on the education and health sectors in Saudi Arabia, a major oil exporting country. Our results show that although oil price drops are expected to hit both sectors, government spending on the health sector may suffer relatively more compared to the education sector. It is important to diversify funding sources on both sectors to offset any negative impacts drops on oil prices would have on both sectors.

Competing Interest

The authors declare that they have no conflict of interests.

1. Introduction

The oil price plummet of 2014 has revived academic and policy interests in understanding the relationship between oil prices and macroeconomic performance, especially of oil exporting countries. A large body of literature already exists focuses on how oil price volatility affects different aspects of the economy in both developed and developing countries. This research stresses on the fact that large and unanticipated changes in energy prices could have significant negative effects on oil-dependent economies. However, recent drops in oil prices, which seems to become a norm till date, stimulated researchers’ appetite to study new possible equilibria at low oil price levels.

An important channel through which low oil prices are expected to affect key economic variables in oil-rich countries is government revenues. A sharp and continuous drops in government revenues would certainly harm government development plans, especially in countries such as Saudi Arabia. In a country like Saudi Arabia wherein oil revenues account for more than 80% of total government revenues, it would not be surprising to see how the 2014 price crash coupled with high levels of government spending have been draining the Saudi government’s budget. As a result and given the currently low oil prices, fiscal deficit in Saudi Arabia has become more than $118 billion in 2016 (about 16% of GDP).

This paper sheds light on possible implications of negative oil price shocks on government expenditures in the health and education sectors. This is an important issue for policy makers in oil dependent economies in general and in Saudi Arabia in particular for several reasons. The Saudi government has recently adopted a comprehensive reform program articulated in the National Transformation Plan (NTP) Vision 2030 which aims at diversifying the economy away from oil within 15 years. The plan envisages the liquidation of the state-owned oil company (ARAMCO) to fund wide-ranging public investments. The privatization of Aramco through an Initial Public Offering (IPO) which produces 90% of government’s revenues is mainly to raise funds for the newly introduced reform program.

This ambitious plan focuses on three major areas. Firstly, it seeks to triple non-oil revenues by the end of the decade through levying indirect taxes and fees on public services. This includes the introduction of a value-added-tax (VAT) and developing non-oil sectors such as mining, tourism and education. Secondly, it aims to cut public spending by reducing subsidies, rationalizing public investment and reducing the public wage bill by 5%. These measures are expected to inject about $53 billion into the Saudi government’s budget by 2020. Thirdly, it aims to diversify both national wealth and investment portfolio abroad.

A major concern here is that low oil prices may push policy makers, in Saudi Arabia as well as in other oil exporting countries, to make difficult choices which could have serious implications on the welfare of Saudi people. Hence, our paper derives its significance from the weight of oil revenues in the kingdom of Saudi Arabia, and its important role in financing the government needs and improving the well-being of households. More specifically, we focus on the implications of oil price negative shocks on health and education sectors given the important role investments in human capital have to play to deliver on economic development. In addition, we justify our choice of sectors by the importance of human capital to economic growth. The 2030 Vision of Saudi Arabia which aims to diversify the economy away from being heavily dependent on oil includes mega projects especially in transportation and infrastructure. However, a crucial element of success for any economic transformation plan is not only the amount of labour but also the quality of this labour (human capital) which is maintained through `good’ education and health systems.

Thus, the primary objective of the current study is to explain the interrelationship between oil prices and government expenditures on health and education sectors in the Saudi economy. In particular, we empirically estimate the relationship between oil prices and government expenditures on health and education over the last three decades. Unlike most of the existing literature that assumes linearity, we employ a non-linear autoregressive distributed lag (NARDL) model to disentangle the effects of positive and negative shocks to oil prices on government expenditures.

The remainder of this paper is organized as follows. Section 2 presents a brief overview of the literature. Section 3 provides a background on oil price changes and the evolution of government expenditures in Saudi Arabia. Section 4 presents the dataset and the econometric model. Section 5 summarizes the empirical results. Finally, section 6 concludes.

2. Literature review

The impact of oil price on government spending has always been an open question in empirical research. Much of this research highlights the role of government revenues as a key channel through which oil prices affect fiscal policy choices in oil dependent economies. For example, a recent study by El Anshasy and Bradley (Citation2012), who employ a GMM estimation in a panel of 16 oil exporting countries over the period of 1957–2008 concludes that higher oil prices induce a larger government size in the long run. However, their results show that, in the short run, government expenditures rise relatively less proportionately to the oil revenue increase. Similar results are reported in Garkaz, Azma, and Jafari (Citation2012), who find a statistically significant impact of oil export revenues on government expenditures in Iran.

Hamdi and Sbia (Citation2013) study the dynamics among oil revenues, government spending, and growth in Bahrain. The authors find that oil revenues remain the principal source for growth and the main channel through which government spending is financed. Dizaji (Citation2014) examines the effects of oil shocks on government expenditures and government revenues in Iran. The author finds that causality runs from oil revenues to government total expenditures. Their results also reveal that the contribution of oil revenue shocks in explaining the government expenditures is stronger than the contribution of oil price shocks. Akanbi and Sbia (Citation2017) find empirical evidence of the effects of fiscal policy on the current accounts of oil exporting countries. Medina (Citation2016) study the impacts of commodity price shocks on fiscal policy indicators in Latin American and find that fiscal aggregates rise in response to positive shocks to commodity prices.

As a major oil exporting country, there is no doubt that changes in oil prices would have profound implications on the Saudi economy. There is already a large body of literature explains the relationship between oil and economic growth in Saudi Arabia. Kireyev (Citation1998), for example, argues that economic activities in the non-oil sector are correlated with oil prices through government spending. The findings in Al-Hakami (Citation2002) support a causal relationship between GDP and government expenditure in Saudi Arabia. A more recent study by Al-Nakib (Citation2015) shows that the recent oil price slump is likely to slow growth and widen fiscal deficit in the Saudi economy. Mseddi and Benlagha (Citation2017) show a bidirectional causality between oil consumption and economic growth. Finally, Hemrit and Benlagha (Citation2018) argue that the volatility of oil prices results in large fluctuations which increases the economy’s reliance upon the petroleum sector.

A major shortcoming in the previous literature, which we address in this study, is the linearity assumption of oil price shocks. To the best of our knowledge, none of the existing studies investigate the asymmetric impacts of oil price shocks on government expenditures in Saudi Arabia. In addition, the majority of the existing work tends to focus on total government expenditures while we study the impact of oil price shocks on government expenditures at a disaggregated level. More specifically, unlike the majority of the existing literature, we investigate the impacts of both negative and positive shocks to oil prices on government expenditures on the health and education sectors in Saudi Arabia.

3. Oil prices and government expenditures in Saudi Arabia

3.1. Oil price changes and the Saudi economy

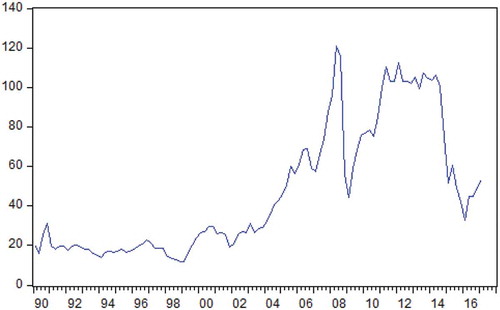

World oil prices have always been volatile showing a varying degree of rise and fall over time. Oil price volatility is usually dependent on variant global economic factors. However, since there are only a few big players controlling the vast majority of oil supply, this volatility is not only determined by economic factors but also geopolitical conditions play a very important role. OPEC, which acts as a club for big oil players, has been always playing a crucial role in determining oil prices through its influence on global oil supply and demand. Over the two decades prior 2014, oil prices had been characterized by an upward trend where it increased from $28.1 per barrel in 2003 to the highest level of $109.45 per barrel in 2012 a trend which came to an end with a sharp drop starting from 2014 until it reached as low as $26.94 per barrel in 2016. Figure presents oil price changes during the period 1990Q1–2017Q2.

Figure 1. Oil price between 1990Q1 and 2017Q2.

Figure shows crude oil price in US dollars per barrel. The data comes from Datastream hit WDQ76AAZA.

The supply side is perceived, to a far extent, to be the key driver of pushing crude oil price downward by more than 50% since 2014. The low value of the price elasticity of international demand for oil results in similar movements (in direction) in export revenues, and in the Saudi economy this is very true.

Saudi Arabia is an oil-based economy with strong government controls over major economic activities. Given its possession of about 16% of the world’s proven petroleum reserves and its rank as the largest exporter of petroleum, Saudi Arabia plays a leading role in OPEC. The petroleum sector accounts for roughly 87% of budget revenues, 42% of GDP, and 90% of export earnings. In order to diversify its economy and create more jobs for nationals, Saudi Arabia has recently been promoting the growth of its private sector. Although there are over 6 million foreign workers, mainly concentrated in the oil and services sectors, high unemployment rates, especially among youth, remain a cause of concern in Saudi Arabia. For this reason, Saudi officials are particularly focused on employing its large youth population, which generally lacks the education and technical skills that the private sector needs.

In 2015, the Kingdom incurred a budget deficit estimated at 13% of GDP, and it faces a deficit of $87 billion in 2016, which was financed by bond sales and drawing down reserves. Although the Kingdom can finance high deficits for several years by drawing down its considerable foreign assets or by borrowing, it has announced plans to cut capital spending in 2016. Some of these plans to cut deficits include introducing a value-added tax and reducing subsidies on electricity, water, and petroleum products. More recently, the government has approached investors about expanding the role of the private sector in the health care, education and tourism industries. While Saudi Arabia has emphasized their goals of diversification for some time, current low oil prices may force the government to make more drastic changes ahead of their long-run time line.

3.2. Education sector performance in Saudi Arabia

Education in Saudi Arabia is segregated by sex and divided into three separately administered systems: general education for boys, education for girls and traditional Islamic education (for boys). The Ministry of Education, established in 1952, presides over general education for boys, and education for girls comes under the jurisdiction of the General Presidency for Girls’ Education. Both sexes follow the same curriculum and take the same annual examinations.

The objectives of the Saudi educational policy are to ensure that education becomes more efficient, to meet the religious, economic and social needs of the country and to eradicate illiteracy among Saudi adults. There are several government agencies involved with planning, administrating and implementing the overall governmental educational policy in Saudi Arabia. The Ministry of Education sets overall standards for the country’s educational system (public and private) and also oversees special education for the handicapped. Early in 2003, the General Presidency for Girls’ Education was dissolved and its functions taken over by the Ministry, to administer the girls’ schools and colleges, supervise kindergartens and nursery schools and sponsor literacy programs for females. Adjusted net enrolment rate, in primary was 96.5, while in lower secondary for both sexes 73.2, in 2014. The Ministry of Higher Education is responsible for policy development and funding for the higher education sector.

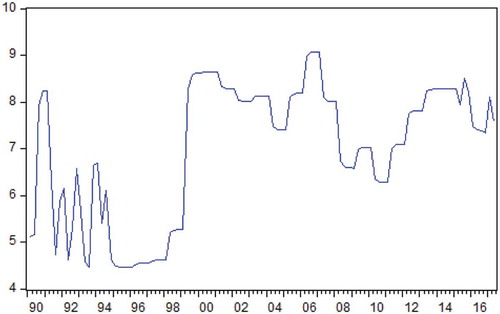

In 2012, the King Abdullah scholarship program was extended with the aim of helping a further 50,000 Saudis graduate from the world’s top 500 universities by 2020. According to data from the Institute for International Education, in the 2012/13 academic year there were a total of 44,586 tertiary-level Saudi students in the United States, an almost 100% increase from 2010/11 and a 12-fold increase from 2005. Expenditure on education as a percentage of total government increased from 4.3% in 1995 to 8.2% in 2014, it reached 9% in 2006. Figure shows the evolution of government expenditures on education (as percentage of total government expenditures) between 1990 and 2017.

3.3. Health sector performance in Saudi Arabia

The Healthcare sector in Saudi Arabia is primarily managed and financed by the Government through the Ministry of Health (MOH) and number of semi-public organization who specifically operate hospitals and medical services for their employees.

In terms of main achievements incidence rate of measles marked by decreased between 2006 (3.4–0.6 per 100,000 population) in 2015. Also between 2006 and 2015 over all immunization coverage increase from 95% to more than 97%.

Life expectancy in KSA for the year 2015 (74.3 years) exceeds the regional average by 6 years and exceed the global average by 4 years. Crude death rate (per 1000 population) is (3.9) which is lower than the regional rate (6.3) and almost half of the global rate. Infant mortality rate (per 1000 live births) among Saudis for year 2014 (7.4) is 83% less than the regional rate (44) and 80% less than the global rate (37) (www.moh.gov.sa).

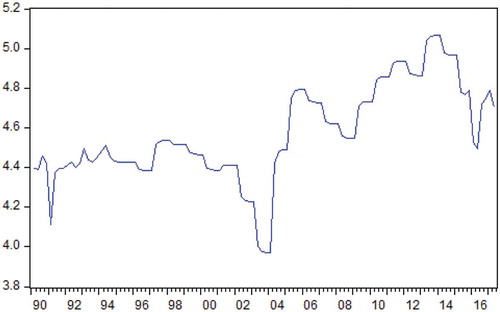

The financial allocation for the ministry of health as a part of government budget is the cornerstone of health resources. Ministry of health depends on a considerable percentage from total governmental budget throughout the 6 years development plan. It is clear from the data about Government expenditure on health as a percentage of (GDP), as it increased from 2.9% in 1995 to 4.6% in 2014, while as a percentage of total government expenditure it fluctuated between 3.9% up to 4.9% during the period 1995–2012 and reached 5.0% in 2013. It reached 62 billions SR in 2015 mounting to 7.25% of total governmental budget and equivalent to increment 2 billion SR (0.23%) from 2014 allocated resources. Figure shows the evolution of government expenditures on health (as a percentage of total government expenditures) between 1990 and 2017.

Figure 2. Government expenditure on education as % of total government expenditure 1990Q1–2017Q2.

Figure 3. Government expenditure on health as % of total government expenditure 1990Q1–2017Q2.

Regarding health and medical education, within the frame of government general strategy, ministry of health aims at upgrading the quality of Saudi human resources and put a plan to improve scientific efficiency of the national personnel to encourage them to get specialized in different health and medical fields, with concentration on developing training inputs, practical implementations and development of regulations governing training, local and broad scholarships.

4. Data and methodology

Our quarterly dataset 1990Q1 and 2017Q2, which comes from Datastream, includes data for oil price, government expenditures on education and health (as percentage of total government expenditures). Table presents the descriptive statistics of the dataset.

Table 1. Descriptive statistics

To empirically investigate the relationship between oil price shocks and government expenditures, we employ an asymmetric version of the autoregressive distributed lag ARDL model (Pesaran & Shin, Citation1998; Pesaran, Shin, & Smith, Citation2001). ARDL models are known to be of good performance, especially in small samples, and flexible with the integration prosperities of the regressors. The model is extended by Shin, Yu, and Greenwood-Nimmo (Citation2014) for the non-linear case, in which the impacts of positive and negative changes are allowed to be asymmetric using partial sum decompositions. The asymmetric co-integrating relationship can be expressed as follows:

where is government expenditures,

and

are the partial sum process of positive and negative changes in oil prices

and

is the error term. In Eq. 1,

and

denote the related asymmetric long-term parameters and

can be decomposed as:

and

are the partial sum process of positive (+) and negative (

) changes in

, which are defined as shown below:

The error correction model can be formally expressed as follows:

where is the error term,

and

are the asymmetric long-run parameters (Greenwood-Nimmo & Shin, Citation2013; Shin et al., Citation2014).

To test for the cointegrating relationships in the model, Shin et al. (Citation2014) employ the cointegration bound test () of Pesaran et al. (Citation2001), which is based on a modified F-test. The

tests for the null hypothesis of no cointegration

(i.e. the coefficients of the lagged level variables are jointly equal zero). Pesaran et al. (Citation2001) report two critical bounds; upper and lower. To reject the null hypothesis, and therefore concludes the existence of cointegration, the test statistics (

) should be greater than the upper bound, providing evidence of a long-run equilibrium relationship. If the

statistic is smaller than the lower bound, we then fail to reject the null hypothesis and a conclusion of no cointegration is made. If the

value lies between the critical bounds, the test is inconclusive. To test for asymmetries, the null hypothesis of no long- and short-run asymmetry is tested using Wald test.

5. Empirical results

A prominent feature of ARDL models is that individual series are allowed to be integrated of order zero and/or one. However, for the computed F-statistics to be valid it is important to ensure that there is no I(2) series included in the model. To test for the integration properties of individual series, we employ the Augmented Dickey Fuller (ADF) test for unit root (Dickey & Fuller, Citation1981). The ADF test results, see Table , show that all series are I(1) where we reject the null hypothesis only (p value ) when series are in the first difference form (D.Educ, D.Health & D.Oil).

Table 2. Augmented Dickey-Fuller unit root tests

Before we proceed to estimate our asymmetric ARDL model, we first estimate a linear ARDL model. We adopt a simple specification throughout the paper, in which the dependent variable is regressed on its own lagged values as well as the lagged values and first difference of oil prices. We follow a general to specific approach to determine the appropriate lag order. For the diagnostic tests, we apply Pesaran et al. (Citation2001) test for cointegration, Breusch Godfrey LM test for autocorrelation, Breusch Pagan Heteroscedasticity test, Ramsey test for specification errors, and the cumulative sum of recursive residuals for coefficient stability.

The results from the symmetric ARDL models for government expenditures on education and health are reported in Table alongside a number of diagnostic tests. The statistics (9.281 and 16.573) are relatively high which suggests the presence of long run relationships between oil prices and government expenditures. The adjustment coefficient is negative and significant (at the 1% level) in both models which ensures convergence towards long-run equilibrium. The speed of adjustment though seems to be very slow.

Table 3. ARDL estimated coefficients

Standard errors in parentheses. * , **

, ***

.

Pesaran et al. (Citation2001) test for cointegration with the null hypothesis of no cointegration.

and

refer to Breusch Godfrey LM test for autocorrelation and Breusch Pagan Heteroscedasticity test, respectively.

Ramsey test for specification errors

The ARDL results also show that government expenditures (on both education as well as on health) are positively related to oil prices in the long run. More specifically, a 1 per cent change in oil prices will lead to a 0.58 and 0.059 per cent change in government expenditures on education and health, respectively, in the long run. However, this coefficient is found to be statistically significant (at the 1% level) only in the case of education. Moreover, both models seem to pass the diagnostic tests, see the lower section of Table and Figure . In particular, we find no evidence of serial correlation () and heteroscedasticity (

) as we fail to reject the null hypothesis in both tests. In addition, Figure , which reports cumulative sum of recursive residuals along with the 95% confidence intervals, shows evidence of coefficient stability.

Figure 4. Cumulative sum of recursive residuals.

However, since that the ARDL model is symmetric, it implicitly assumes no difference (in size) between the impact of positive and negative oil price shocks on government expenditures. Such assumption, if not true, can lead to a misspecification problem. Thus, we extend the analysis to investigate the asymmetric impact of oil price shocks on government expenditures as explained in section 4.

Table reports our NARDL estimation alongside its diagnostic tests. The null hypothesis of no long- and short-run asymmetry is tested using Wald test and the computed test statistics are denoted as and

for the long- and short runs, respectively. In the short-run, the results reveal no significant difference in the impact of a negative shock than a positive shock for oil prices on government expenditures. The Wald test statistic

equals 1.591 and 2.610 and none of which is statistically significant at the 5% level. That is, negative shocks on oil prices will not have a significantly different short run impact (in sign and magnitude) on government expenditures than positive shocks. On the long run, however, the impact is significantly different. The Wald test statistic

equals 10.021 and 15.471 and both are statistically significant at 1% level. Such results strongly suggest that asymmetries need to be accounted for when studying the impact of changes in oil prices on government expenditures and, therefore, restrict the findings of symmetric models. In the case of Saudi Arabia, it is evident that a linear model for explaining the oil prices-government expenditures relationship will most likely be mis-specified.

Table 4. Dynamic asymmetric estimation of oil prices on government expenditures on Education and Health

Moreover, the cointegration test on the unrestricted (asymmetric) model fails to reject the null hypothesis with equal to 16.988 and 10.695 exceeding the upper bound the critical value. We thus find evidence of a long-run cointegrating relationship between the examined variables. The results, in Table , also show the estimated long run coefficients of the effects of positive (

) and negative (

changes in oil prices on government expenditures. The long run impact of positive and negative shocks to oil prices is statistically significant. More specifically, a 1 per cent increase in oil prices would lead to 0.611% and 0.624% increases in government expenditures on education and health, respectively. However, a 1 per cent drop in oil prices would lead to a drop in government expenditures on education and health by 0.564% and 0.801%, respectively. Both effects (positive and negative changes) are statistically significant at 1% or 5% level.

According to the results reported in Table , the asymmetric impacts of oil price shocks on government expenditures in Saudi Arabia is a long-run phenomena. Therefore, to obtain an even better fit of the dynamic interactions between oil price and government expenditures, we re-estimate our NARDL model after imposing a zero restriction on the short-run asymmetries allowing for only long-run asymmetry.

Table shows our NARDL estimation for constrained short-run asymmetries and unrestricted long-run asymmetries. This means while the effects of positive and negative shocks to oil prices on government expenditures are identical in the short run, they are not in the long-run. A similar specification is adopted in Atil, Lahiani, and Nguyen (Citation2014) and Alsamara, Mrabet, Dombrecht, and Barkat (Citation2017) for Saudi Arabia. Our empirical results confirm that the significant symmetric short-run and asymmetric long-run effects of oil price shocks on government expenditures. Our estimated coefficients of L.Oil(+) and L.Oil (-) (partial sums decompositions) are statistically significant at 5% or 1% level. This result suggests that an increase (decrease) in oil price will raise (reduce) government expenditures on the education and health sectors. The long-run coefficients of positive and negative changes of oil price are 0.674 and 0.516, respectively. This means that a 1% increase in oil price causes a 0.674% rise in government expenditures on education. Moreover, a 1% decrease in oil prices causes a 0.516% reduction in government expenditures on education. Similarly, in the case of the health sector, while a 1% increase in oil prices leads to a 0.637 increase in government expenditures, a 1% decrease in oil price would lead to a 0.814 drop in government expenditures.

Table 5. NARDL estimation with only the long-run asymmetries

So far, we find that oil price shocks have statistically significant impacts on government expenditures on the education health sectors. These effects seem to be asymmetrical in the long run but symmetrical in the short run. Thus, in the long run, while the effects of a positive oil shock outweigh the effects of a negative shock in the case of the education sector, the negative effects are found to be larger in the case of health expenditures. This could be interpreted according to our priori where government revenues are expected to increase when oil prices increase. However, there seem to be conflicted results in the long-run asymmetric impacts of oil price shock on the education and health sectors. Perhaps, this can be explained by longer term commitments of the Saudi multi-billion dollar scholarship program for young Saudis to study abroad. These types of programs are usually accompanied with political support and are integrated in long-run development plans of transforming the economy. So, in times of low oil price, there may be smaller room for significant drops in previously announced and politically supported education expenditures compared to the case with the health sector.

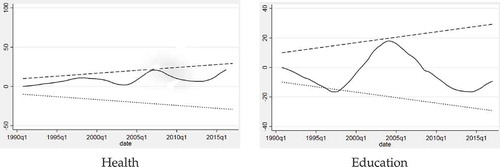

To show the adjustment process and the period of disequilibrium caused by a shock to oil prices, we use the NARDL estimates to produce the cumulative dynamic multiplier. The dynamic multiplier explains the adjustment process from the initial equilibrium to the new equilibrium point that results from a positive or negative shock. According to Shin et al. (Citation2014), the dynamic multiplier can still depict any possible asymmetries exist in the adjustment path even if no evidence of short run asymmetry is found. This is due to the fact that the adjustment path is not determined only by long run parameters but also on the error correction coefficients and the dynamics of the model itself.

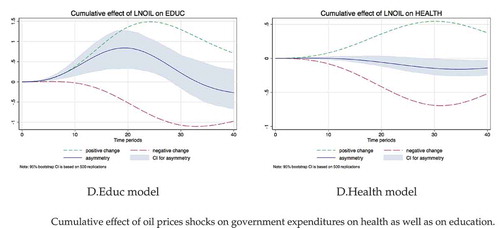

Figure illustrates the dynamic effects of positive and negative changes in the examined oil prices shocks on government expenditures on education and health, respectively. The dynamics of the oil prices cumulative multiplier shows that a positive shock to oil prices would have a greater impact on government expenditures on education compared to a negative shock to oil prices. However, the magnitude of the impact of a negative shock to oil prices would have a greater impact on government expenditures on health compared to a positive shock. This indicates that the negative shock moves government expenditures on health to a lower equilibrium point on the long-run. Moreover, in both models the dynamics of positive and negative shocks are straightforward and show no significant differences on the short run. In addition, it is worth noting how the impact dies out gradually and the new equilibrium is reached after nearly eight years. The overall conclusion, though, is that when oil prices drop, government expenditures on education and health would not reacts immediately. However, the negative shock to the same variable would have a stronger consequences on government spending in the long run, especially in the health sector.

Figure 5. Cumulative dynamic multiplier.

6. Conclusion

This paper examines the asymmetric impact of oil price shocks on government expenditures on the education and health sectors. We employ a non-linear autoregressive distributed lag (NARDL) model to examine the relationship between oil prices and government expenditures in Saudi Arabia; a major oil exporting country. The key findings in this study point to empirical evidence of the asymmetric impact of oil price shocks on government expenditures, especially in the long-run. In particular, our results support the non-linearity proposition wherein positive shocks to oil prices would have statistically different impacts on government spending compared to negative shocks. However, our findings lend support to such asymmetries only in the long run. Moreover, our results show that negative shocks to oil prices would have relatively greater long-run impacts on government expenditures on health compared to positive shocks. In addition, the effect of positive oil prices shocks on government spending on education are found to exceed the magnitude of negative shocks on the same variable.

An important policy lesson could be learned from our results. Although negative oil price shocks are expected to hit both sectors in the long run, government spending on the health sector may suffer relatively more compared to the education sector. Therefore, it is important to diversify funding sources on both sectors (education and health) in the long run to offset any negative impacts oil prices drops would have on government expenditures. Thus, dealing with oil price shocks and uncertainty is a key challenge facing Saudi Arabia and it is important that strong fiscal buffers are built-up in periods of high oil prices to help cushion government spending when oil prices are low. Expanding the role of private investment in the education and health sectors can also mitigate the effects of oil price shocks. Using sovereign wealth funds was shown by Mohaddes and Raissi (Citation2017) to may have weathered the effects of the recent oil shock in the short-run but this is not a sustainable solution in the long run. In this regard, our results confirm the findings in Abdel-Latif and El-Gamal (Citation2018) in that oil exporting countries such as Saudi Arabia need to transform their economies away from oil dependence.

The underlying research materials (data and codes) for this article can be accessed at https://doi.org/10.17632/vybc47sknf.1

Additional information

Funding

Notes on contributors

Hany Abdel-Latif

Dr Hany Abdel-Latif is a lecturer in Economics at Swansea University, UK, where he teaches Econometrics and International Economic Policy. He obtained a PhD in Economics from Swansea University and MSc in International Economics from City, University of London. His research interest is in Applied Economics, especially in the areas of Macroeconomics, Political Economy, Development, Financial and Labour Economics. His research appears in reputable refereed journals. He is a research associate at the Economic Research Forum (ERF) and acts as an external consultant for a number of international institutions. Dr Abdel-Latif is also the founder and managing director of The Economic Society which is an online network that supports teaching and learning Economics.

References

- Abdel-Latif, H., & El-Gamal, M. (2018). Antecedents of war: The geopolitics of low oil prices and decelerating financial liquidity. Applied Economics Letters, 1–5. doi:10.1080/13504851.2018.1494802

- Akanbi, O. A., & Sbia, R. (2017). Investigating the twin-deficit phenomenon among oil-exporting countries: Does oil really matter?. Empirical Economics, 1–20.

- Al-Hakami, A. O. (2002). Analyzing the causal relationship between government expenditure and revenues in Saudi Arabia, employing co-integration and granger causality models. Public Adminstration, 42, 475–493.

- Al-Nakib, O. (2015). Saudi Arabia: Economy resilient but growth slowing amid the oil price slump. Macroeocnoic Outlook. Economic Update series, NKB Saudi Arabia.

- Alsamara, M., Mrabet, Z., Dombrecht, M., & Barkat, K. (2017). Asymmetric responses of money demand to oil price shocks in Saudi Arabia: A non-linear ardl approach. Applied Economics, 49(37), 3758–3769. doi:10.1080/00036846.2016.1267849

- Atil, A., Lahiani, A., & Nguyen, D. K. (2014). Asymmetric and nonlinear pass-through of crude oil prices to gasoline and natural gas prices. Energy Policy, 65, 567–573. doi:10.1016/j.enpol.2013.09.064

- Dickey, D. A., & Fuller, W. A. (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica: Journal of the Econometric Society, 49, 1057–1072. doi:10.2307/1912517

- Dizaji, S. F. (2014). The effects of oil shocks on government expenditures and government revenues nexus (with an application to iran’s sanctions). Economic Modelling, 40, 299–313. doi:10.1016/j.econmod.2014.04.012

- El Anshasy, A. A., & Bradley, M. D. (2012). Oil prices and the fiscal policy response in oil-exporting countries. Journal of Policy Modeling, 34(5), 605–620. doi:10.1016/j.jpolmod.2011.08.021

- Garkaz, M., Azma, F., & Jafari, R. (2012). Relationship between oil revenues and government expenditure using wavelet analysis method: Evidence from iran. Economics and Finance Review, 2(5), 52–61.

- Greenwood-Nimmo, M., & Shin, Y. (2013). Taxation and the asymmetric adjustment of selected retail energy prices in the UK. Economics Letters, 121(3), 411–416. doi:10.1016/j.econlet.2013.09.020

- Hamdi, H., & Sbia, R. (2013). Dynamic relationships between oil revenues, government spending and economic growth in an oil-dependent economy. Economic Modelling, 35, 118–125. doi:10.1016/j.econmod.2013.06.043

- Hemrit, W., & Benlagha, N. (2018). The impact of government spending on nonoilgdp in Saudi Arabia (multiplier analysis). International Journal of Economics and Business Research, 15(3), 350–372. doi:10.1504/IJEBR.2018.091050

- Kireyev, A. (1998). Key issues concerning non-oil sector: Saudi Arabia recent economic development issue (vol. 48, pp. 29–33). Washington, D.C.: International Monetary Fund.

- Medina, L. (2016). The effects of commodity price shocks on fiscal aggregates in Latin America. IMF Economic Review, 64(3), 502–525. doi:10.1057/imfer.2016.14

- Mohaddes, K., & Raissi, M. (2017). Do sovereign wealth funds dampen the negative effects of commodity price volatility? Journal of Commodity Markets, 8, 18–27. doi:10.1016/j.jcomm.2017.08.004

- Mseddi, S., & Benlagha, N. (2017). Linkage between energy consumption and economic growth: Evidence from Saudi Arabia. The Empirical Economics Letters, 16(10), 1993–1101.

- Pesaran, M. H., & Shin, Y. (1998). An autoregressive distributed-lag modelling approach to cointegration analysis. Econometric Society Monographs, 31, 371–413.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. doi:10.1002/(ISSN)1099-1255

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ardl framework. In Festschrift in Honor of Peter Schmidt (pp. 281–314). New York, NY: Springer.