?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The banking industry is the engine of economic activities of the modern day financial systems. As such, banks play a very significant part in supporting economic growth through the efficient allocation of resources and risk diversification in an environment of optimal interest rate spread. Therefore, the understanding of the impact of interest rate spread on the banking system efficiency demands that an empirical inquiry of this nature be conducted. In this paper, we seek to empirically investigate the impact of interest rate spread on the banking system efficiency in South Africa for the period from 2000Q1 to 2017Q3 by employing the nonlinear autoregressive distributed lags framework. Evidence from this study suggests the presence of asymmetries in the interest rate spread behavior. Specifically, in the long run, we find a significant negative relationship between banking efficiency and a positive shock to interest rate spread. Furthermore, a negative shock to interest rate spread improves banking efficiency by about 0.3% in the long run. The results of this study further suggest that economic growth and real exchange rate are significant factors that positively influence the banking system efficiency and nonperforming loans retard the efficiency of the banking system in South Africa.

PUBLIC INTEREST STATEMENT

The banking system efficiency plays a critical role in the health of the financial and economic spheres of a country. Evidence from this study suggests that economic growth and real exchange rate positively influence the efficiency of the South African banking system. However, it is further found that a positive change in interest rate spread decelerates banking efficiency in the long run and nonperforming loans have a negative effect on the efficiency of the banking system in South Africa. A negative shock to interest rate spread improves banking efficiency in South Africa in the long run. These findings could be generalized to other economies in the region in order to tighten the regulatory and supervisory oversight of the banking system such that stability and efficiency could be realized in this important industry.

1. Introduction

The South African financial system has in the past decade been put through some significant tests by external shocks such as the calamitous effects of the 2007 financial crisis, volatility in the international commodity prices and the general decrease in the global growth outlook. Kganyago (Citation2016) argue that, despite the slight economic recovery from the recent global financial crisis, the South African financial system has faced further challenges from widening interest rate spread and from the ongoing fragility in the international financial markets. Nonetheless, one point needs to be made clearly. The South African financial system safely weathered the contagion and catastrophic effects of the recent financial crisis because of its resilience and efficiency that are highly consistent with the more stringent global regulatory reforms and regulations (Maredza & Ikhide, Citation2013). Hence, the banking system in South Africa is ranked amongst the top-class banking systems of the world and therefore is of key systemic importance in the growth and development of the country.

It is an overarching fact that banks play an important role in the economies of developing countries, South Africa in particular, by improving the living standards of the citizenry through the provision of financial services. Pinnington and Shamloo (Citation2016) aver that the intermediation functions of banks include, among others, offering of a repository for savings and transforming them into illiquid assets, clearing and settlement systems, efficient distribution of financial resources between savers and borrowers and other financial products that deal with risk and market uncertainty. Principally, banking institutions are in existence because they are a direct response to the fact that information is costly. Thus, banks and other financial institutions specialize in the screening of the credit worthiness of borrowers and rendering continuous monitoring function such that borrowers honor their obligations (Were & Wambua, Citation2014). The profit or the reward that banks and other financial institutions get from offering these financial services is the spread between lending and deposit rates. This process is best known as maturity transformation and it is at the core of modern banking and forms the central part of this particular study.

As outlined in the outset, banks are institutions of confidence and contribute to the growth and development of an economy. Therefore, given the banking system–economic growth link, Tabak and Souto (Citation2010) maintain that potentially large interest rate spread could negatively affect the efficient intermediation functioning of banks and the economy in general. Consequently, the productivity of banking institutions and the growth path of the economy will decelerate. These factors provide sufficient motivation to undertake this study in order to provide policy makers and the government with precise, more directed and evidence-based empirical results on the impact of interest rate spread on the banking system efficiency in South Africa.

In addition, this paper is of relevance because the impact of widening interest rate spread is topical among central bankers and its appeal to the body of knowledge on banking gives a new perspective and deepens the understanding of how interest rate spread impacts the banking system efficiency in South Africa in a number of ways. For one, majority of previous studies (Chauyeau & Couppey, Citation2000; Kumbirai & Webb, Citation2010; Maredza & Ikhide, Citation2013) have emphasized the determination of competition and productivity in the banking system with less attention focused on how this industry is affected with interest rate spread. Furthermore, unlike previous studies which used the general Vector Error Correction (VEC) approach (Chauyeau & Couppey, Citation2000; Okeahalam, Citation2006, Smets, Citation2014), this study employs the nonlinear autoregressive distributed lags (NARDL) framework to empirically examine the impact of interest rate spread on the banking system efficiency in South Africa. We content that the adopted econometric framework, that is the NARDL model, is most appropriate as it allows the estimation of potential long- and short-run asymmetries in interest rate spread to inform policy formulation in the banking sector dynamics.

Given the introduction in the first section, this paper proceeds as follows: the overview of the South African banking system and interest rate spread is provided in Section 2. Section 3 provides the relevant literature consulted in relation to this study. The methodology and the econometric techniques employed in carrying out this study are presented in Section 4. Section 5 reports the empirical results and the last section provides the conclusion and policy implications of the study.

2. Overview of the South African banking system and interest rate spread

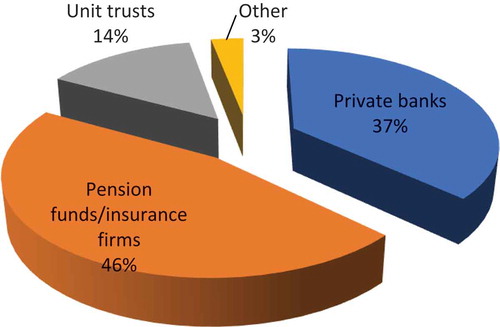

The economy of South Africa is fabricated by a large financial sector that is greatly sophisticated, well developed and highly regulated. The total market value of the assets within the financial sector, in December 2016, averaged 298% of GDP (South African Reserve Bank [SARB], Citation2016), surpassing those of other nations in the region and other developing countries. Kganyago (Citation2016) maintains that the biggest portion of the South African financial system is consumed by the commercial banks, with assets of around 112% of GDP. However, rapid growth in nonbank financial sector, for instance insurance companies and pension funds, has seen the share of commercial banks assets declining since 2008. At the end of 2016, the share of total financial assets of commercial banks in South Africa dropped by 72% between 2009 and 2016 (SARB, Citation2016). Figure shows the proportion of financial assets in South Africa.

Figure 1. The proportion of financial assets in South Africa in December 2016.

Source: SARB (Citation2016).

The majority of banking assets are domestic, with a share of 95% and most major banks in South Africa contracted their operations to developed economies and non-African emerging market economies (Banking Association of South Africa [BASA], Citation2016). According to Figure , a large proportion of the financial assets in South Africa are consumed by pension funds or insurance companies. This segment consumes about 46% of the total financial sector assets in South Africa (SARB, Citation2016). The second largest financial sector that occupies the financial assets in South Africa is the private banking sector with 37% portion of the total assets. Unit trusts, that is institutions that pool money from various investors to invest in assets such as shares, property and bonds, consume 14% of the total financial assets in South Africa. Other segments consume only 3% of the total financial sector assets (SARB, Citation2016).

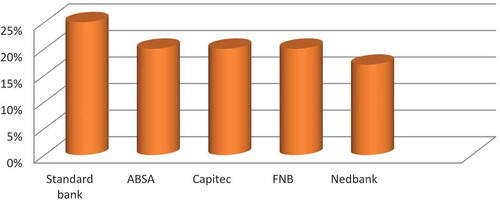

Kganyago (Citation2016) asserts that South Africa has a world class banking system because of its observance to the international banking regulation frameworks. This has seen a steadily increasing number of foreign players acquiring stakes in major banks in South Africa. Furthermore, Kganyago (Citation2016) argues that the South African banking sector is highly concentrated and compares favorably to the developed economies. The South African banking sector comprises 15 branches of foreign banks, 36 foreign bank representatives, 6 foreign controlled banks, 10 locally controlled banks and 3 mutual banks (SARB, Citation2016). The last quarter of 2016 reviewed that about 91% of the total banking sector assets was represented by the five major banks, also known as the “Big Five,” in South Africa, namely Standard bank, Capitec, FirstRand bank (FNB), ABSA and Nedbank (BASA, Citation2016). Generally, the number of banks in South Africa has been declining over the years. Locally controlled banks sorely decreased from 18 to 10 between 2010 and 2016, with branches of foreign banks increasing to 15 in 2016, from 13 in 2009 (SARB, Citation2016). This trend could be attributable to factors such as liquidations, mergers or amalgamations of financial institutions.

The major banks in South Africa are defined by the proportion of the market share that each financial institution consumes within the financial system. Figure exhibits the market share of the five largest banks in South Africa. Figure clearly indicates that the five major banks dominate the banking sector in South Africa. Standard bank has the largest market share with an average of 25%, followed by ABSA with about 22% market share of the banking sector. FNB and Nedbank follow with an average of 20% and 18%, respectively (BASA, Citation2016). The market share of these five major banks in South Africa shows not much difference between each bank and this indicates the concentration and competitiveness of the banking sector in South Africa. According to Maredza and Ikhide (Citation2013), concentration is the extent to which a large portion of the out of a particular market is produced by few firms in the industry.

Figure 2. The market share of major banks in South Africa in December 2016.

Source: SARB (Citation2016).

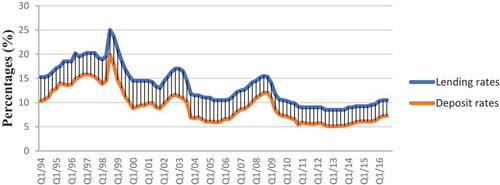

In South Africa, according to Aron and Muellbauer (Citation2012), the lending rate refers to the commercial banks’ prime overdraft rate. It is a benchmark rate priced at 3.5 basis points above the repurchase rate (SARB, Citation2016). This rate is used by banks to price the lending rates offered to clients at either above or below the benchmark rate. Figure shows trends in the lending and deposit rates in South Africa for the period 1994Q1–2016Q4.

Figure 3. Lending and deposit rates in South Africa 1994Q1–2016Q4.

Source: SARB (Citation2016).

According to Figure , the lending rate in South Africa has remained unchanged during 2016 at about 10% from an average of 9% in 2014. The lending rate averaged 12% from 1994 until 2017, reaching an all-time high of 26% in August 1998 and a record low of 5% during the apartheid era in September 1950 (SARB, Citation2017).

The deposit rates in South Africa, according to Figure , follow a consistently similar pattern with the lending rates. It can be seen from Figure that deposit rates fluctuate below the lending rates. The deposit interest rate showed an increase of 1.02% between 2015 and 2016 financial years (SARB, Citation2016). These deposits averaged 11% since the first quarter of 1994 to the last quarter of 2016, reaching an all-time peak of 19% in 1990 and a record low of 5% in the third quarter of 2013 (SARB, Citation2017). The deposits in South Africa, according to Kganyago (Citation2016), are composed of six different forms, namely current, savings, call, fixed and notice, Negotiable Certificate of Deposit (NCDs) and repos.

3. Literature review

Previous studies on the impact of interest rate spread on the banking system efficiency are very few not only in the context of South Africa but across all the developing economies. Majority of the available studies put more emphasis on the determination of productivity and competition within the banking system. In a study conducted by Okeahalam (Citation2006) for the 61 banking branches in South Africa, the results indicated that the productive efficiency of these banks was 83%. These results implied that financial institutions could reduce their costs by 17% without significant changes of their output mix. Similarly, using the parametric stochastic frontier, Ncube (Citation2009) concluded that the cost and profit efficiencies of the major four banks in South Africa averaged 55% and 92%, respectively.

In another study, Kumbirai and Webb (Citation2010) used financial ratios to analyze the profitability, credit quality and liquidity of the five major banks in South Africa and concluded that the South African financial system successfully weathered the effects of the 2008 financial crisis because of adequate capitalization and profitability. Similar results were obtained by Chauveau and Couppey (Citation2000) for the five major banks in South Africa using the data envelopment analysis techniques. Their study examined the technical efficiency of the selected banks and their results show the lack of significant problems of productive inefficiency. Likewise, Maredza and Ikhide (Citation2013) used a two-stage methodology framework to measure the efficiency and productivity changes of the four major commercial banks in South Africa. Their first stage results pinpointed to the fact that there was a noticeable but mild deviation of total factor productivity and efficiency measures during the 2008 financial crisis. The evidence from their second stage analysis, which used the censored Tobit model, show that the financial crisis was a major cause of bank inefficiency with a decrease of 16.96% compared to the precrisis era. The above cited previous studies provide detailed understanding on the determination of productivity and how competition and financial crises affect the efficient functioning of the banking system. However, limited attention has been focused on the empirical understanding of the impact of interest rate spread on the banking system efficiency in the context of South Africa.

4. Methodology

This study attempts to investigate the impact of interest rate spread on the banking system efficiency in South Africa by employing the NARDL framework. We specify the following asymmetric long-run equation of the banking system efficiency:

Given formulation (1), is a measure of economic growth,

signifies the total banking assets (a measure of bank size, used as a proxy of the capitalization of the South African banking system) and nonperforming loans as a proportion of total gross loans are captured by

.

represents the real exchange rate (ZAR/US$),

denotes the error-correction term and the subscripts

–

represent the cointegrating vectors or vectors of the long-run parameters to be estimated, respectively. In formulation (1),

and

represent partial sums of positive and negative changes in interest rate spread (lending minus deposit rates).

According to Shin, Pesaran and Smith (Citation2011), and O'Donnell (Citation2010), formulation (1) can be specified in an ARDL setting along the line of Pesaran and Shin (Citation1999) and Pesaran, Shin and Smith (Citation2001) as follows:

where all variables are as defined above, p, q, r, s and t are lag orders. It is important to note here that and

measure the short-run influences of a positive shock and a negative reduction to interest rate spread on banking total assets, respectively. As such, over and above the asymmetric long-run relation between interest rate spread and banking efficiency, the asymmetric short-term impact of interest rate spread changes is also captured.

4.1. Data and expected a priori

The data utilized for econometric estimation in this study were extracted from two sources within the Quantec data base, namely the Statistics South Africa and the SARB for the period from 2000Q1 to 2017Q3. The banking system efficiency of South Africa and the data thereof are represented by the five major banks with a share of about 91% of the total banking sector assets in the country. The conventional economic theory posits that growth in output improves the intermediation functioning of the banking system (Walsh, Citation2003); thus, the coefficient of GDP is expected to be positive. The coefficient of IRS is predicted to be either negative or positive depending with the elasticity of the variable. The quality of loans is captured by the variable NPL and an increase in this variable is expected to reflect inefficiencies in the banking industry. As such, the sign of the coefficient of NPL is expected to be negative. Since higher interest rates have a tendency to attract foreign capital and as a result cause the exchange rate to rise, therefore, the sign of REXR is expected to be positive.

4.2. Estimation techniques

This paper is an empirical attempt to establish the impact of interest rate spread on the banking system efficiency in South Africa using the NARDL methodology. The plausible feature of the NARDL approach to cointegration is that this method is applicable irrespective of whether the variables are I(0) or I(1) but with none that are I(2). Therefore, in order to render the validity of the computed F-statistics in the tests of cointegration, it is important to conduct tests of unit root such that no I(2) variables are involved in the analysis. To this end, we employ the widely used Augmented Dickey-Fuller (ADF) and Philips-Peron (PP) tests of unit root to analyze the unit root properties of the vectors. Based on the estimated NARDL, we employ the bounds test approach of Pesaran et al. (Citation2001) and Shin et al. (Citation2011) to test for the presence of cointegration among the vectors. This method of cointegration will be carried out using the Wald F-test based on the null hypothesis that all the long-run coefficients are jointly equal to zero. Having established the cointegration of variables, the final step of our empirical analysis involves the utilization of the NARDL framework to examine the short- and long-run estimates of the model specified in Equation (2).

5. Empirical results and discussion

Given the precondition of the bounds test approach that no variables should be I(2), we first subject each series to the ADF and PP tests of unit root to determine the unit root properties of the variables under the assumption of constant and trend terms. Evidence from unit root tests reported in Table suggest that the variables are I(1) processes except for the variable of nonperforming loans which is I(0). This means that all the other variables are nonstationary at level but become stationary in their first difference form.

Table 1. The results of unit root tests

Since the tests indicate that none of the variables are I(2), we confidently proceed to the bounds testing approach. The results displayed in Table indicate that a long-run relationship exists among the vectors when the regression model is normalized in banking total assets. This compelling evidence is indicated by the computed F-statistic of 7.69% exceeding the upper critical value of 4.69%, at the 5% level of significance. In the same manner, according to the diagnostic results reported in Table , all the diagnostic tests fail to exhibit any evidence of the violation of the classical linear regression model assumptions, that is the model estimated in Equation (2), according to Brooks (Citation2008), Gujarati (Citation2004) and Keho (Citation2017), does not have any problem of serial correlation, no Autoregressive Conditional Heteroskedasticity (ARCH) effect and non-normality in residuals. The results of the bounds F-statistics are reported in Table .

Table 2. ARDL cointegration test results

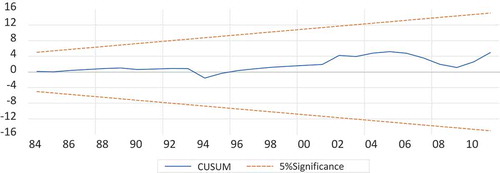

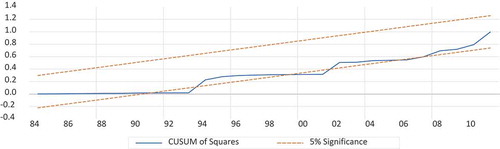

The stability of the estimated model was tested using the Cumulative Sum (CUSUM) and the CUSUM of Squares methods as shown in Figures and , respectively. The former test provides evidence that the model is stable as the graph is within the critical region at the 5% level of significance. However, the CUSUM of Squares graph indicates that the cumulative sum of squares is somewhat unstable as the graph is not strictly within the 5% significance lines. This is suggestive of parameter instability which is not desirable for the model.

Figure 4. The CUSUM test.

Source: Author’s computation using E-views 10 Econometric Software.

Figure 5. The CUSUM of Squares test.

Source: Author’s computation using E-views 10 Econometric Software.

Having established the long-run relationship between the variables, we further estimate the long-run impact of economic growth, interest rate spread, nonperforming loans and real exchange rates on the banking total assets in South Africa using the NARDL approach. The results of the long- and short-run estimates are disclosed in Table .

Table 3. Long- and short-run estimates of the ARDL method

The results of the NARDL approach indicate that all the estimated coefficients, in exception of nonperforming loans, are statistically significant in explaining the South African banking system and have expected signs. As stated earlier, the banking system efficiency of South Africa is proxied by the total banking assets of the five major commercial banks. The results indicate that a positive long-run relationship exists between economic growth, real exchange rate and total banking assets in South Africa both in the short and long run. In other words, ceteris paribus, a 1% change in output growth and real exchange rate will ignite an average of 30.7% and 17.9% increase in banking assets, respectively. These results authenticate the theory of interest rates and conform with previous findings of Chauyeau and Couppey (Citation2000), Okeahalam (Citation2006) and Ncube (Citation2009). As highlighted earlier, although majority of these studies emphasized the determination of efficiency and productivity in banking system, their results were slightly higher than those of this study, for example, Ncube (Citation2009) concluded that a unit increase in output increases bank capacity by almost 42%.

Another important finding of this study is that there is empirical evidence of a negative relationship between nonperforming loans and total banking assets in South Africa both in the short and long term. Importantly, Table exhibits evidence that a positive shock to interest rate spread retards the growth in total banking assets. More specifically, the presence of asymmetry is observed both in the short and long run in respect to a positive and a negative change in interest rate spread. In the long term, a positive unit change in interest rate spread ignites an average of about −0.12% decrease in banking capitalization. A negative shock to interest rate spread improves banking efficiency by about 0.3% in the long run. Moreover, a 10% decrease in nonperforming loans will translate to a 10.9% decrease in the total banking assets in South Africa. In a way, these results corroborate with the findings of Maredza and Ikhide (Citation2013). As stated earlier, their second stage regressions indicated that all the other bank-specific factors were significant except for interest rate. Their findings further concluded that nonperforming loans negatively and significantly impact the efficiency of banks. This is acceptable given that a rise in the quantity of nonperforming loans impedes the growth of bank assets. A negative relationship between bank assets and interest rate spread is inevitable in the case of South Africa since, according to Ncube (Citation2009) and Maredza and Ikhide (Citation2013), large banks tend to achieve high efficiency levels and reduced costs of operations since the deceleration of cost efficiency as indicated by an increase in interest rate spread decreases the overall productive efficiency of commercial banks.

6. Conclusion and policy implications

In this paper, we have empirically investigated the impact of interest rate spread on the banking system efficiency in South Africa by utilizing the NARDL framework on quarterly time series data from 2000Q1 to 2017Q3. The stationarity properties of the vectors were performed using the ADF and the PP tests of unit root. We employed the NARDL method of cointegration to examine the long-run relationship between the variables. The results suggest that a compelling long-run relationship exists among the variables and all the tests of normality, heteroscedasticity and correlation indicate that the estimated model does not have any problem of serial correlation, no ARCH effect and non-normality in residuals. The empirical evidence from this study suggests that economic growth and the real exchange rate are significant factors that positively influence the efficiency of the South African banking system. From the analysis, we find evidence for the presence of asymmetries in the long term as well as in the short run. More specifically, in the long run, a positive shock to interest rate spread tends to decelerate the growth in banking assets. A negative shock to interest rate spread improves banking efficiency by about 0.3% in the long run. Furthermore, this study also found that nonperforming loans slow the efficiency of the banking system. The monetary authorities and the government in South Africa should be mindful of the need to strictly adhere to the international regulations of commercial banks such that the gap between the deposit and lending rates could be optimally narrowed to achieve efficiency in the banking system. This endeavor will also uptick economic growth and strengthen the value of the domestic currency with more directed efforts of keeping the rate of inflation with the desired range of 3–6%.

Notwithstanding the promising results, this study faces some limitations. For one, the empirical analysis was conducted using total banking assets of the major South African commercial banks as a proxy of the efficiency of the banking system. An area of fruitful research in the future could be of utilizing other econometric techniques that can absorb the entire variables of the South African banking sector. This is important for many reasons. First, the empirical analysis employed in this study could have omitted some important variables that have a significant impact on the banking system efficiency or the endogeneity of some of the utilized explanatory variables. Therefore, this study could be extended by modeling other variables such as macro-prudential banking regulation and the stock market shares to explain the South African banking system efficiency. This will be of relevance given the need to maintain optimal interest rate spread, protect the quality of loans and enhance a health financial and economic environment in South Africa.

Acknowledgments

We thank three unidentified referees for helpful comments and suggestions on the initial draft of this paper. The usual disclaimer applies and the views expressed in this paper are the sole responsibility of the author.

Additional information

Funding

Notes on contributors

Varaidzo batsirai Shayanewako

Varaidzo Batsirai Shayanewako is a prospective Doctor of Economics at the University of Fort Hare and an Economics Lecturer in the Department of Economic & Business Sciences at Walter Sisulu University. He earned his master’s in Economics and a Cum Laude (Distinction) in Honours Economics at the University of Fort Hare. His research interests focus on applied econometrics, monetary economics, public finance, banking and finance. Shayanewako has publications in internationally accredited journals such as the Journal of Economics and Behavioural Studies (ISBN 2018, 2220-6140); Journal of Developing Areas (JDA) (ISSN 1548-2278); Journal of African Economies (JAE) (ISSN 0963-8024), Journal of Global Economics, among others.

Asrat Tsegaye

Asrat Tsegaye is an Adjunct Professor of Economics at the University of Fort Hare, Department of Economics, South Africa. He holds a PhD in economics from the University of Kent at Canterbury, UK. He has lectured and researched in several countries in Africa, including Zimbabwe, Botswana, and South Africa. His research interest is in the area of International trade problems and policies, monetary and finance issues.

References

- Aron, J., & Muellbauer, J. (2012). Review of monetary policy in South Africa since 1994. Journal of African Economies, 16(5), 705–744. doi:10.1093/jae/ejm013

- Banking Association of South Africa (BASA). (2016). Contributions to a technical committee to review the spread between the repo and prime rate. Cape Town, February, 286–314. Retrieved from http://www.banking.org.za/

- Brooks, C. (2008). Introductory to econometrics for finance. Cambridge: Cambridge University Press.

- Chauyeau, C. A., & Couppey, K. (2000). The role of bank capital in the propagation of shocks. Journal of Economic Dynamis and Control, 6, 555–576.

- Gujarati, D. N. (2004). Basic econometrics (4th ed.). New York: McGraw Hill.

- Keho, Y. (2017). The impact of trade openness on economic growth: The case of Cote d’Ivoire. Cogent Economics and Finance, 5, 133–820. doi:10.1080/23322039.2017.1332820

- Kganyago, L. (2016). The South African banking sector - an overview of the past 5 years, Dec 2015. Retrieved February 13, 2018, from http://www.reservebank.co.za/

- Kumbirai, G., & Webb, R. (2010). Putting the New Keynesian model to test. Journal of International Finance, 4, 135–143.

- Maredza, A., & Ikhide, S. I. (2013). Measuring the operational efficiency of commercial banks in Namibia. South Africa Journal of Economics, 76(4), 586–595.

- Ncube, M. (2009, November 11–13). Efficiency of the banking sector in South Africa. Fourth African Economic Conference on fostering development in an era of financial and economic crisis. Ethiopia: Addis Ababa.

- O’Donnell, C. J. (2010). Measuring and decomposing agricultural productivity and profitability change. Australian Journal of Agricultural and Resource Economics, 54(4), 527–560. doi:10.1111/j.1467-8489.2010.00512.x

- Okeahalam, C. C. (2006). Production efficiency in the South African banking sector. A stochastic analysis. International Review of Applied Economics, 20, 103–114. doi:10.1080/02692170500362819

- Pesaran, H., & Shin, Y. (1999). An autoregressive distributed lag modelling approach to cointegration in Econometrics and Economic theory in the 20th century. The Ragnar Frisch Centennial Symposium Cambridge University Press, USA, chapter. 4 (pp. 371–413).

- Pesaran, M. H., Shin, Y., & Smith, R. P. (2001). Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American Statistical Association, 94(446), 621–634. doi:10.1080/01621459.1999.10474156

- Pinnington, J., & Shamloo, M. (2016). Limits to Arbitrage and deviations from covered sectors. The American Economic Review, 104(2), 379–421.

- Shin, Y., Pesaran, M. H., & Smith, R. J. (2011). Pooled estimation of long-run relationships in dynamic heterogeneous panels. UK: Department of Applied Economics University of Cambridge.

- Smets, F. (2014). Financial stability and monetary policy, how closely interlinked? International Journal of Central Banking, 10, 264–300.

- South African Reserve Bank (SARB). (2016). Annual economic report 2016, Bank Supervision Department (pp. 1–113). Retrieved February 13, 2018, from http://www.reservebank.co.za/

- South African Reserve Bank (SARB). (2017). Annual economic report 2017, Bank Supervision Department, 90th Anniversary (pp. 1–173). Retrieved February 13, 2018, from http://www.reservebank.co.za/

- Tabak, M., & Souto, T. (2010). Financial intermediation costs in low-income countries: The role of regulatory, institutional and macroeconomic factors. International Monetary Fund, Canada, WP/12/140.

- Walsh, C. E. (2003). Monetary theory and policy (2nd ed.). UK: MIT Press.

- Were, M., & Wambua, J. (2014). What factors drive interest rate spread of commercial banks? Empirical evidence from Kenya. Review of Development Finance, 4(2014), 73–82. doi:10.1016/j.rdf.2014.05.005