?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Historically, oil has been the main source of earnings in the Saudi Arabian economy. Different from other symmetric oil price shock studies, the aim of this paper is to test the impacts of symmetric oil price shocks on government expenditure-real exchange rate nexus and ultimately, to check the conformity of symmetric oil price shock findings to those prevailing in literature. To achieve this endeavor, autoregressive distributed lag (ARDL) and structural vector autoregressive (SVAR) have been employed for the period of 1970 to 2018. The goal of carrying out ARDL and SVAR together is to consolidate and strengthen the consistency of the results obtained from both approaches. Our models’ findings support the short-run appreciation of the real exchange rate as a reaction to symmetric oil price shocks and to real government expenditure. The latter finding, though is consistent with Dutch disease predictions. However, in the long-run symmetric oil price shocks negate the real exchange rate. The directional map of causality is as follows: symmetric oil price shocks impact the total earnings of the Saudi government and hence, government spending. Thereafter, the composition of expenditure causes an appreciation of the real exchange rate. Policymakers should consider oil price fluctuations as a source of disturbance to government earnings. Solutions could be carried out by benefiting from other countries' experience.

PUBLIC INTEREST STATEMENT

The aim of this paper has been to test empirically the impacts of symmetric oil price shocks and real government expenditure on real exchange rate in an oil-based economy. The findings of this research revealed the existence of a positive impact of symmetric oil price shocks on the real exchange rate, while exists negative impacts in the long run. Furthermore, real government expenditure shocks have impacted the real exchange rate positively. The findings are consistent with Dutch disease literature. This study employed ARDL and SVAR approaches for the sake of confirming and conformity of the findings. As a major oil-producing country, Saudi policymakers are susceptible to fluctuations of oil prices because the slump in government earnings will hinder the aggregated efforts of maintaining stable economic prosperity and employment. Thus, knowing sources of economic disruption helps in planning future expenditure on local sectors such as education, health, and capital formation.

1. Introduction

Oil earnings play a major role in the solidity of the Saudi economy nowadays. One of the prominent characteristics of the Saudi Arabian economy is its heavy reliance on oil export earnings and a high degree of openness, making it sensitive to external shocks. Thus, a vulnerable issue for Saudi policymakers is the reality of fluctuating oil prices in global markets. However, government expenditures' impact on exchange rate is a long story with an open end. Undoubtedly, government expenditure looked at as a savior in critical cases, such as in the recent global financial crisis, which is not that far behind. Just as important, in a resource-dependent country, oil price shocks can significantly influence government revenue and expenditure where growth in government revenue tends to accelerate the expansion of non-oil sectors. Furthermore, government expenditure may also induce inflation, leading to appreciation of the local currency (the real effective exchange rate). In this case, competitiveness in traded sectors would be at risk (Khadan, Citation2016).

The linkage between oil prices and exchange rates is thoroughly discussed in the literature. In this relationship, one channel of transmission is the terms of trade. Trade was related to the nominal exchange rate but did not have a direct impact on it (Raji et al., Citation2018). Beckmann et al. (Citation2017) identified some theoretical channels between oil prices and exchange rates. Terms of trade are focused on real exchange rates, wealth, and portfolios, assumed that effects flow from the nominal exchange rates to the oil prices. However, the channel of expectations allows a bidirectional causality between oil prices and exchange rates. Accordingly, government expenditure shocks affect output and private consumption jointly with real appreciation of exchange rate (De Castro & Fernández, Citation2013). Moreover, using rational expectations, unexpected and expected government spending shocks tend to appreciate the German real and nominal exchange rates for the period 1975: 2–1989: 4 (Koray & Chan, Citation1991). After pioneering work to identify the relationship between variations in oil prices and exchange rates, the next wave of studies focused on discerning the specific influence of oil prices on exchange rate variability (Muhammad et al., Citation2012). In like manner, the role of political and legal institutions is addressed in the literature. The co-variations between oil prices and real exchange rates depend on the institutional differences for oil-producing countries (Rickne, Citation2009; Moshiri, Citation2015).

After the collapse of fixed exchange rates in 1971, Saudi Arabia pegged its currency (the Riyal) to the US dollar. However, in 1975, the Saudi government pegged the Riyal to the Special Drawing Right (SDR) until May 1981, when it reverted to the US dollar. Although the nominal exchange rate is not altered, it changes from time to time to reflect changes in the inflation rate.

The primary objective of this study is to widen the scope of analysis thereby testing empirically the impacts of symmetric oil price shocks and government expenditure on the real exchange rate. In this paper, it is proposed (hypothesized) that symmetric oil price shocks and government expenditures affect the real exchange rate positively (appreciation) in the short run and symmetric oil price shocks negatively in the long run. The current study contributes to the literature by shedding light on the impacts of symmetric oil price shocks and real government expenditure on the real exchange rate in an open oil-based economy covering the period of 1970–2018. The uniqueness of this study stems from the fact that it incorporates ARDL and SVAR models to strengthen and consolidate findings. However, the handful of related studies have concentrated on the association between oil price, oil revenue, government expenditure, and economic growth; see, for example, Al Rasasi and Banafea (Citation2016); and Al Rasasi et al. (Citation2018).

Furthermore, in economic literature, the impact of oil price shocks and government expenditure have tended to appreciate the real exchange rates in oil-producing countries. Thus, the outcomes of this research will be valuable for policymakers, researchers, and others who are interested in understanding the impacts of oil price fluctuations and government expenditure on real exchange rates in the context of a major oil-producing country. Because of Saudi government’s earnings are dominated by windfalls, policymakers can arrange for suitable ways and means to encounter the impacts of oil price shocks and maintain stable real exchange rate. Thus, stable real exchange rate will be reflected on the value of imports and hence, inflation. Inflation surreptitiously affects the value of saving (investment) and causes the redistribution of income and assets. On the other hand, taking precautionary measures against oil price fluctuations will mitigate the slump in government earnings to keep aggregated efforts of maintaining stable economic prosperity and employment. The expected research findings are as follows, symmetric oil price shocks and government expenditure will influence the real exchange rate positively in the short run. However, in the long run, only symmetric oil price shocks influence the real exchange rate negatively. Furthermore, the causality test asserts that symmetric oil price shocks will exert pressure on government expenditure which, in turn, will cause the real exchange rate to appreciate.

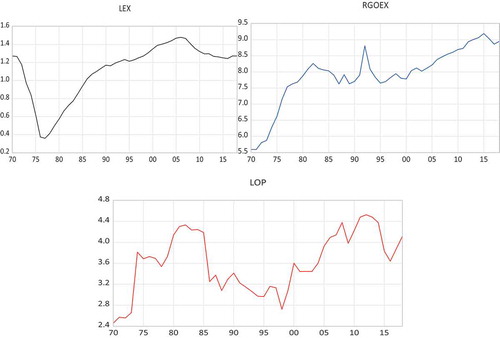

Afterward, Figure reflects the direction of real government expenditure, real exchange rate, and symmetric oil prices. It is interesting to note the presence of positive directional movements of the real exchange rate and symmetric oil price with real government expenditure. Besides, the negative directional movements of the real exchange rate with symmetric oil prices.

The remainder of this paper is structured as follows. Section 2 reviews theoretical and empirical oil price shock literature. Section 3 develops ARDL and SVAR models. Section 4 presents the estimation of ARDL and SVAR models, their interpretations, and the discussion of the empirical findings. Section 5 presents the conclusion and some policy suggestions based on the research outcomes.

Figure 1. Log real exchange rate, real government expenditure, and real OPEC basket oil price.

2. Review of related and empirical literature

The potency of fiscal policy in stabilizing the economy has been well documented in the literature. Under flexible exchange rates, an increase in government expenditure will lead to an increase in interest rate and hence, an appreciation of the exchange rate. On the contrary, Karras (Citation2011) points out that, under fixed exchange rates, preventing appreciation of exchange rates requires expansionary monetary policy to further the expansion of government expenditure. He asserts that fiscal policy is more potent under fixed exchange rates than under flexible ones. Using rational expectations, Koray and Chan (Citation1991) found that anticipated and unanticipated government spending caused the real and nominal exchange rates to appreciate. Rickne (Citation2009) illuminated the role of well-developed political and legal institutions in the relationship between oil prices and real exchange rates in oil-exporting countries and found that co-variation between oil prices and real exchange rates was conditional on political and legal institutions. In another interesting study, Adedokun (Citation2018) tested the impacts of oil shocks (prices and revenues) on the dynamic relations between government revenue and expenditure and their impacts on macroeconomic variables. He concluded that oil shocks did not predict variations in government expenditure in the short run but did predict oil revenue in the short and long run. Alternatively, exchange rates tend to respond asymmetrically to shocks in the crude oil market. For instance, Khadan (Citation2016) found that energy shocks had a positive and immediate effect on growth, but this growth was not sustained. Thus, the negative energy revenue shocks had a greater adverse impact on government expenditure. This finding is attributed to the reduction in capital expenditure. Besides, Cakrani et al. (Citation2013) revealed a positive relationship between government spending and the overvaluation of real exchange rates in Albania. It has been argued that a country as an oil exporter (importer) may experience exchange rate appreciation (depreciation) because of an oil price increase (Tasar, Citation2018,; Raji et al., Citation2018). However, when USD depreciates, oil prices will go up due to higher demand.

Other studies have explored the effects of government expenditure shocks on exchange rates in various contexts and country settings. According to De Castro and Fernández (Citation2013), government expenditure shocks affected output and private consumption jointly. Further, appreciation of Spanish exchange rate resulted from the persistence of the nominal exchange rate and higher relative prices. Miyamoto et al. (Citation2016) used panel data from 125 developing and developed countries and concluded that increasing government expenditure (military spending) caused the real exchange rate to depreciate and consumption to fall in underdeveloped countries, while in developed economies, it was the other way around. Nwosa (Citation2017) found a positive and significant relationship between fiscal policy and the exchange rate in Nigeria.

There have also been studies to probe the impacts of oil price changes and exchange rates in the context of oil-producing countries. Koh (Citation2017) used data for 40 oil-producing countries from 1973 to 2010 and found that countries with fixed exchange rates are experiencing adverse effects from oil price changes and tended to encounter a small and delayed depreciation. Meanwhile, under flexible exchange rates, depreciation was immense. Accordingly, Narayan et al. (Citation2008) examined the relationship between oil price and the Fijian dollar-USD exchange rate using data from 2000 to 2006. They employed GARCH and EGARCH models and found that an increase in oil prices led to an appreciation of the exchange rate. Further, Al-mulali and Sab (Citation2011) discovered that the UAE dirham-USD exchange rate was not an appropriate measure and oil price increases engender liquidity which in turn causes inflation. Moreover, Muhammad et al. (Citation2012) examined the link between oil prices and exchange rate in Nigeria using daily data. Applying generalized autoregressive conditional heteroscedasticity (GARCH) and the exponential (EGARCH) techniques, they confirmed the depreciation of the Nigerian naira-US dollar exchange rate.

In a similar vein, Brahmasrene et al. (Citation2014) examined the dynamic short-run and long-run relationships between US-imported oil prices and exchange rates using monthly data from January 1996 to December 2009. They found that in the short run a unidirectional causality runs from exchange rate to oil prices. Moreover, in the long run, causality runs from oil prices to the exchange rate. Nonetheless, Osuji (Citation2015) examined the impact of oil price changes on the USD-Naira exchange rate using daily data from January 2008 to December 2014. He discovered that the relative oil price significantly affected the exchange rate. Moreover, the evidence indicated the existence of unidirectional causality running from oil prices to exchange rate.

Along the same lines, Babatunde (Citation2015) examined the impact of oil price changes on the exchange rate in Nigeria. He found that an increase/decrease in oil price resulted in a depreciation/appreciation of the exchange rate. In the same manner, Atems et al. (Citation2015) pointed out that oil supply shocks had no effects on exchange rates, while global aggregated demand and oil-specific demand tended to result in exchange rate appreciation. Furthermore, Hashimova (Citation2017) showed that the fall in oil prices caused the depreciation of Azerbaijan’s currency. In contrast, Baghestani and Toledo (Citation2019) confirmed that oil price movements predict the direction in the real exchange rate up to 3 months for Canada, Mexico, and the US. Furthermore, in linking 65 major currencies, Wen and Wang (Citation2020) indicated that the US dollar and the Euro are the major transmitters of volatility. Therefore, volatilities are sensitive to international economic fundamentals. As a result, oil exports, among other related variables, cause volatility transmission across world markets.

Further elaborating on this topic, Garcia et al. (Citation2018) found that increases/decreases in spot oil prices caused appreciation/depreciation in the peso/USD exchange rate. However, future prices had no effect on the exchange rate. Accordingly, Raji et al. (Citation2018) indicated a unidirectional effect from oil price to the foreign exchange rate, and an increase in oil price led to an appreciation in the Nigerian naira-USD exchange rate. On the other hand, Samhi and Mohamed (Citation2018) concluded that variations in the Algerian dinar against the US dollar tended to depreciate the dinar. Mohammed et al. (Citation2019) examined the relationship between oil prices and the Nigerian naira-USD exchange rate using daily data and found that an increase in oil prices led to an increase in the naira-USD exchange rate. By the same token, Nusair and Olson (Citation2019) tested the impacts of oil price shocks on exchange rates in seven Asian countries Indonesia; Japan; Korea; Malaysia; Philippines; Korea, and Thailand. They found a symmetric effect on exchange rate depends on each country’s currency status. With the preceding analyses in mind, Olayungbo (Citation2019) examined the relative Granger causal impacts of oil price on exchange in Nigeria and did not find a Granger causal relationship between oil price and exchange rate. Equally, Yiew et al. (Citation2019) confirmed the existence of asymmetric co-integration between oil prices and exchange rates. Contrary to previous findings, Kaushik et al. (Citation2014) suggested that oil price changes did not affect the real exchange rate in India. Conversely, Tasar (Citation2018) asserted that causality is running from oil price shocks to the exchange rate in Romania.

Empirical studies that dealt with the Saudi case are numbered. Aleisa and Dibooğlu (Citation2002) examined sources of real exchange rate volatility in Saudi Arabia using monthly data from January 1980 until February 2000. They segregated changes into real and nominal and discovered that real shocks significantly affected real exchange movements. Additionally, they found that oil production shocks were responsible for the real exchange rate variations. Furthermore, Abdel-Latif et al. (Citation2018) examined the impacts of oil price shocks on government health and education expenditure in Saudi Arabia. They found a non-linear relationship between oil price shocks and government expenditure. Moreover, long-run negative oil price shocks affected government expenditures, especially in the health sector, while long-run positive oil price shocks provided economic benefits. Therefore, it did not lead to increased expenditures on health. Accordingly, Nouria et al. (Citation2018) examined the influence of oil price movements on the exchange rates in some of the MENA countries (Egypt, Jordan, Morocco, Qatar, Saudi Arabia, Tunisia, and the UAE). They concluded that an increase in oil prices caused an appreciation of exchange rates in Saudi Arabia and Tunisia. However, the drop in oil prices depreciated the exchange rates only in Saudi Arabia. Furthermore, a rise in oil prices led to exchange rate fluctuations in Tunisia and Saudi Arabia.

All in all, there is no consensus amongst economists that oil price shocks and government expenditure impact real exchange rates positively. However, Narayan et al. (Citation2008), Nouria et al. (Citation2018), Garcia et al. (Citation2018), Mohammed et al. (Citation2019), Tasar (Citation2018), and Baghestani and Toledo (Citation2019) found that oil price shocks affect real exchange rates positively (appreciation). On the other hand, government expenditure tends to appreciate real exchange rates, Nwosa (Citation2017) and Cakrani et al. (Citation2013) concluded that rise in government expenditure appreciates exchange rates. Though, in this paper, symmetric oil price shocks tend to appreciate the real exchange rate in short run and negatively in long run. Additionally, real government expenditure appreciates the real exchange rate in the short and long run.

Having reviewed literature, this paper contributes to the existing literature by adding evidence of thorough and deep analysis of the impact of symmetric oil price shocks and real government expenditure on the real exchange rate for a major oil-producing country. The impacts of symmetric oil price shocks and government expenditure on the real exchange rate are susceptible and vital for policymakers. It assists them in identifying sources of disturbance to government revenues and help overcome the government’s budget imbalance. Afterward, addressing the conformity of our economic findings to researchers’ outcomes is an addition.

3. Research methodology

3.1. The ARDL model

Following Adedokun (Citation2018) as a starting theoretical foundation, an eclectic model has been developed and adopted to test the impacts of symmetric oil price shocks and real government expenditure on the real exchange rate. The model is constructed as a log-linear ad hoc model specified to include the following variables:

where LEXt is the real bilateral Riyal-USD exchange rate, calculated according to the following formula: LEXt = log (Riyal*US CPI/Saudi CPI). LOPt is the OPEC basket real oil price; RGOEXt is the real government expenditure and Ut is an error term. According to Dutch disease literature, an increase in oil price would cause a positive impact on the real exchange rate. However, a rise in government expenditure would also cause an appreciation of the exchange rate. The latter is called the spending effect.

The autoregressive distributed lag (ARDL) was first introduced and applied by Pesaran and Shin (Citation1999) with the characteristic that not all variables are required to be stationary at I (0) or I (1). One major advantage of this test is that it is based on a single ARDL equation rather than on a VAR as in the Johansen approach. As a result, the number of estimated parameters is reduced. In contrast, unlike Johansen’s model, several restrictions can be easily imposed on each separate variable. The ARDL test does not require pre-testing for the order of integration (Khalil and Dombrecht Citation2011). Furthermore, this approach collapses in the case of an integrated stochastic trend. Thus, the ARDL (p, q) model can be specified as the unrestricted error correction version as follows:

where Гti with t = 1, 2, and 3 represents short-run dynamic coefficients. The ARDL model includes the log real bilateral exchange rate, the real log government expenditure, and the log real OPEC oil price basket. Similarly, α1 to α3 represent the long-run relationships, while Г1 to Г3 represent the short-run dynamics of the model. As has been noted, because of the existence of long-run relationships among the variables LEXt, RGOEXt, and LOPt, bound testing is performed, which depends on an F-test to examine the possibility of co-integration (long-run relationships) among the variables. If the F-value is higher than the upper bound, we reject H0 and conclude that there are co-integrated variables, such that:

H0: α1 = α2 = α3 = 0

By the same token, if the F-value is less than the lower bound, H0 is accepted, and the variables are not co-integrated. So, in the case of no long-run relationships among the variables:

H1: α1 ≠ α2 ≠ α3 ≠ 0

The error correction model of ARDL is shown in Equationequation (3)(3)

(3) . The speed of adjustment is represented by δ1. Eventually, the short-run correction model relationships presented in this analysis are specified as follows:

Testing for ECM is desirable because it reveals the speed of adjustment and the way the variables converge toward long-run equilibrium. If the expected ECMt-1 with δ1 is negative and significant, the variations between the dependent and independent variables are easily corrected to stable long-run relationships. The negative percentage of disequilibrium of the past year will return to long-run equilibrium in the following year. Hence, the explanatory variables will converge to long-run equilibrium at a certain speed, given by the magnitude of δ1.

3.2. Structural vector autoregression (SVAR)

Vector autoregressive (VAR) plays a pivotal role in describing the dynamic behavior of economic and financial determinants of time series. Consequently, VAR forecasts are flexible because they are built on the prospect of the future path of a variable. In addition, VAR is used for structural deduction and policy-making analysis. Following the economic literature (e.g., Su et al. Citation2016) that addresses the impacts of oil price structural shocks on the government-exchange rate nexus, a reduced form VAR model can be specified as follows:

where yt is the 3-vector of endogenous variables that includes the percentage change in OLPt, RGOEXt, and LEXt. β is the 3-vector of intercept coefficients to be estimated. et is a 3-vector of innovations, which may be contemporaneously correlated but are uncorrelated with their own lagged values and uncorrelated with all the right-hand side variables. It is assumed further that et is related to fundamental oil price shocks ℇt according to et = A0−1 ℇt. EquationEquation (4)(4)

(4) can be rewritten as the VAR oil price shocks structural model as follows:

Given the vector autoregressive model (VAR), the impulse response function (IRF) measures the reaction of one variable to a shock coming from another variable. The advantage of using VAR in the case of exchange rates, real government expenditure, and symmetric oil prices is that the variables are dynamic and can be evaluated without referring to causality (Beckmann et al., Citation2017). On the other hand, structural vector autoregressive (SVAR) can easily and precisely distinguish between different shocks.

where ai are matrices in lag operator H, such that HK xt = Xt—Kj aij is estimated coefficient j, aij = HK is the sum of the moving average coefficients for K = 1, 2, …, ρ, where ρ is the degree of polynomial aij (H). It is the optimal lag operator of the VAR. ℇtLOP, ℇtRGOEX, and ℇtLEX are structural shocks. Utilizing Cholesky decomposition in an identified structural VAR, it could be implemented according to the above structure. The long-run restrictions that are imposed are as follows:

Government expenditure and the exchange rate do respond to symmetric oil price shocks contemporaneously. Thus, a12 = a13 = 0. Studies have mentioned that oil price causes an appreciation or depreciation of the exchange rates in oil-based economies (see, e.g., Narayan et al., Citation2008; Hashimova, Citation2017; and Nouira et al. 2018). On the other hand, government expenditure will respond positively to symmetric oil price changes.

Oil price does not respond to government expenditure nor to exchange rate shocks.

Exchange rate responds to symmetric oil price shocks and government expenditure shocks contemporaneously. Hence, a23 = a13 = 0, which is consistent with Dutch disease theory (Corden, Citation1984).

4. Results and discussion

4.1. Descriptive statistics

Before indulging into analysis of results, descriptive statistics are presented. It is useful to explore the meaningfulness of the impacts of symmetric oil price shocks on government expenditure-real exchange rate nexus thereby different statistical measurements of the variables. Table reports the summary statistics of the variables of this study.

Table 1. Results of descriptive statistics of government expenditure (GOEX), oil prices (OP), and real exchange rate (EX) for the period of 1970–2018

From Table , the average value of government expenditure is (32,399.70) in millions of Saudi Riyals (local currency). For example, in 2015, government expenditure reached the peak with a value of 1,140,603 million reflecting an increase of 190 times the government expenditure value in 1970. After 2015, the value fluctuated enormously to reflect the unstable movements in the world oil market. Similarly, the average oil price is 43.33 USD with the maximum of 92.4 USD in 2014. Though the minimum oil price is 11.67 USD in 1970. Between 1970 and 2018 the oil market experienced ups and downs due to political instability. Furthermore, the average real exchange rate is 3.17 (Saudi riyal per US dollar) with a maximum of 4.39 in 2006 and a minimum of 1.43 in 1977. Equally important, the standard deviation of the variables GOEXt, OPt, and EXt is 295,012.6, 22.98, and 0.831, respectively. This means that the most volatile is GOEXt (295,727), while the least volatile is EXt with (0.831). The variables GOEXt and OPt are positively skewed while EXt is negatively skewed. The higher positive skewness could be attributed to higher incremental values of the variable. On the other hand, the steepness measure is with the coefficient of 3.72 for GOEXt, 2.45 for OPt, and 2.13 for EXt. Finally, J-B suggests the probability of less than 5% for the variable GOEXt and normally distributed. However, OPt and EXt may not normally distribute with probability greater than 5%. Data used in this paper are sourced from the Saudi Arabian Monetary Agency (SAMA), yearly statistics 2019, and International financial statistics (IFS).

4.2. The unit root test

Kaushik et al. (Citation2014) explain the importance of using stationary data, where the use of non-stationary data can yield spurious outcomes. An augmented Dicky–Fuller test is performed in this form:

where Xt is the variable under consideration, ∆ is the first difference operator, t is a time trend, and εt is a stationary random error term. If the null hypothesis δ = 0 is not rejected, the variable series contains a unit root and is non-stationary. The optimal lag length in Equationequation (6)(6)

(6) is identified by ensuring that the error term is a white noise error term. In addition to the augmented Dicky–Fuller test, a Phillips-Perron test is also conducted to ensure the stationarity of the series. The Phillips-Perron test uses non-parametric correction to deal with any correlation in error terms.

The aim of this test is to check whether a linear combination of integrated variables becomes stationary over a long-run period. If this happens, then there is co-integration among variables. Unit root tests, ADF, and PP are applied. Levels and first differences are included for each test. Table shows that for the ADF test, none of the variables LOPt, RGOEXt, and LEXt are stationary at the level. The reason is that the values of the test statistics for the variables are less than the critical values of the ADF statistics (Jibir & Aluthge, Citation2019). Results indicate that the null hypothesis of non-stationarity cannot be rejected at all levels. Nevertheless, all variables become stationary at the first difference and the ADF test statistics’ values are greater than the critical values at 1%, 5%, and 10% level of significance. Thus, the results indicate that LOPt, RGOEXt, and LEXt are stationary at the first difference and cannot be rejected. To repeat, the stationary properties of the variables according to ADF and PP tests confirm that all the variables are not integrated of order zero I (0). However, all variables (LOPt, RGOEXt, and LEXt) are integrated of the order one I (1). This suggests a random walk trend. At the integrated level of one, all variables are significant, ranging between 1% and 5% level of significance.

Table 2. Augmented-Dickey Fuller and Phillips-Perron tests

In addition, applying the PP test allowed for results in line with ADF test. The outcomes of the ADF and PP tests confirm that the variables are of order I (1), which paves the way to introduce and apply the ARDL approach.

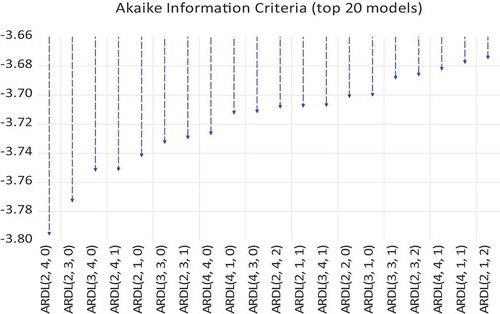

Considering the foregoing analysis, the strength of Akaike information criterion over other criteria is based on the following fact, 20 different ARDL models are performed. The lower value of AIC is selected, that is (2, 4, 0) which gives the lowest values of AIC. Moreover, Figure illustrates the strength of the selected model criteria.

Figure 2. The strength of model selection criteria.

4.3. The ARDL regression model

The autoregressive distributed lag (ARDL) approach is particularly useful in analyzing economic scenarios in small data samples. In these instances, a change in one variable will bring about changes in another variable, and changes in variables may not be immediate but will be distributed over time. Likewise, ARDL is built on several assumptions that there is no autocorrelation; there is no heteroscedasticity in the data (variance and mean are constant), and the data must be stationary. Therefore, ARDL is useful for determining long-run relationships among variables.

The estimation results are presented in Table . Symmetric oil price shocks are statistically insignificant at the 5% level. Ten percent increase in the symmetric oil price shocks leads to 0.11% appreciation of the real exchange rate, while 10% increase in the symmetric oil price shocks lagged one year causes a 0.53% depreciation in the exchange rate and is statistically significant at 5% level. However, the coefficient of depreciation of the real exchange rate is consistent with the findings of Muhammad et al. (Citation2012) and Smahi and Mohamed (Citation2018). On the contrary, 10% increase in symmetric oil price shocks lagged three years causes 0.64% appreciation of the exchange rate which is in line with predictions of Dutch disease theory. Furthermore, it is statistically significant at 5% level. Also, the results from Table point out that 10% increase in real government expenditure induces 0.40% appreciation of the exchange rate. This finding is statistically significant at the 5% level and consistent with Dutch disease literature (spending effect). As expected earlier, the ARDL coefficients of independent variables reflected the right signs. To be specific, a priori expectations of positive impacts of symmetric oil price shocks and real government expenditure on the real exchange rate are conspicuous.

Table 3. VAR lag order selection criteria

Table 4. The ARDL regression with dependent variable LEX

On the other hand, the adjusted R-square of 0.99 suggests that 99% of variations in the dependent variables is well explained by the independent variables. The probability of the F-test is statistically significant indicating that the regressors jointly and significantly influence the regression. The D-W statistic is 2.02, suggesting the absence of the first-order autocorrelation.

To sum, symmetric oil price shocks and real government expenditure had the expected signs. However, the impact of symmetric oil price shocks on the real exchange rate is somewhat low. This suggests that, according to the causality test, LOPt does Granger cause RGOEXt;, and in turn, RGOEXt does Granger cause LEXt. Thus, based on earlier results, the significant effect of the symmetric oil price shocks on the real exchange rate is not spontaneous but materializes after 3 years.

To consolidate earlier findings, fully modified ordinary least square (FMOLS) is introduced. FMOLS is a non-parametric approach that works on correcting autocorrelations between independent variables and the error term. Besides, it corrects heteroscedasticity. Accordingly, the results obtained from the fully modified ordinary least square (FOLS) test are presented in Table . The findings are consistent with the results obtained from ARDL. A 10% change in symmetric oil price shocks causes 3.5% depreciation of the real exchange rate. Symmetric oil price shock coefficient is statistically significant at 5%. Furthermore, 10% increase in real government expenditure, RGOEXt, would cause a 3.0% appreciation of the real exchange rate. Thus, RGOEXt is statistically significant at the 5% level. It is important to note that FMOLS confirms long-run co-integration coefficients.

Table 5. FMOLS estimates with dependent variable LEX

4.4. The ARDL short-run, long-run, and bounds testing

Based on Table , short-run values of the coefficients are not statistically significant, except the symmetric oil price shocks lagged 2 years. However, the negative sign indicates a depreciation of the real exchange rate. The error correction model has a negative sign and is significant at the 1% level. This points out the existence of long-run relationships among the variables LEXt, RGOEXt, and LOPt. The speed of adjustment of short-run variables to the long-run equilibrium for the error correction model, ECM−1, is a bit low and is 8%. This finding indicates that the last period’s disequilibrium is corrected at a speed of 8% annually, and though suggesting a convergence of our model’s variables to long-run equilibrium at a speed of 8% a year. The low speed of adjustment is justified on the grounds that the volatility of oil prices affects the total government oil earnings, and in turn, affects the internal and external demand of goods and services which will impact the exchange rate. Equally important, in examining the long-run results, Table , one notices that symmetric oil price shocks cause 40% of the depreciation of the real exchange rate, and real government expenditure accounts for 50% of the appreciation of the real exchange rate. Both LOPt and RGOEXt coefficients are statistically significant at the 5% level. Therefore, appreciation caused by government expenditure tends to influence domestic prices, which in turn impacts terms of trade.

Table 6. The ARDL error correction dependent variable LEX

Table 7. Long-run estimates with dependent variable LEX

To ensure the consistency of the model, several statistical tests have been performed. The model passed the serial correlation test. From Table , Breusch-Godfrey serial correlation LM test with probability value of (0.2172) indicates the rejection of the null hypothesis of the presence of serial correlation. Subsequently, for the bound testing, Table shows that the F-statistic value is about 3.58%, which is greater than the upper bound at the 10% level. This suggests the rejection of the null hypothesis that there exists no co-integration among all variables. For the normality test, Table shows that there is no heteroscedasticity.

Table 8. Serial correlation LM test

Table 9. F-bBounds test

Table 10. Heteroskedasticity test

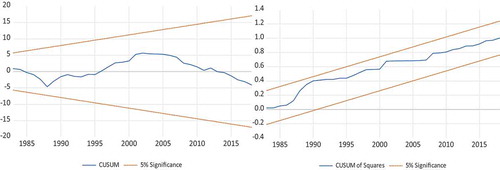

Furthermore, to check the stability of the model, the CUSUM and CUSUMQ tests are implemented. It was determined that the long-run coefficients and short-run dynamics of the ARDL estimates are stable. Thus, Figure shows the stability of the model.

Figure 3. Stability test of the model.

4.5. Variance decomposition

The relative importance of shocks is usually determined through variance decomposition. In fact, variance decomposition reveals the effects of one variable on the remaining variables of the structural vector autoregression (SVAR). Table shows the percentage of forecast error variance for each shock. About 31% of the variations in symmetric oil price shocks LOPt explained by its own shocks in the first year. As time passes, it diminishes to about 11% by the end of the tenth year. Just as important, the response of symmetric oil price shocks to real government expenditure RGOEXt and to the real exchange rate (LEXt) is almost negligible after the period of the tenth year. Similarly, the response of RGOEXt to symmetric oil price shocks has risen from 5% to about 62% after the tenth year. In contrast, the response of RGOEXt to LEXt is about 19% by the end of the tenth year. It is interesting to note that the response of LEXt to symmetric oil price shocks increased from 4% in the first year to a striking magnitude of 74% after the time span. The positive influence of the symmetric oil price shocks on LEXt reveals an appreciation of the real exchange rate LEXt. However, 29% of the contribution to variations in LEXt is attributed to its own shocks in the first year. After that, it started to diminish till the end of the period.

Table 11. Variance decomposition

All in all, it is easy to observe that between 74% and 76% of variations in the real exchange rate, LEXt, is explained by the symmetric oil price shocks, LOPt, and the real government expenditure, RGOEXt, respectively. These conclusions strongly support the ARDL and FMOLS findings.

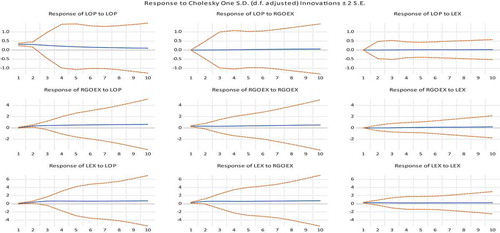

4.6. Impulse response function

Figure reports the impulse response of innovations of symmetric oil price shocks, real government expenditure, and real exchange rate over a ten-year horizon. One standard deviation of oil price shocks to LEXt is positive and continues to be positive in the long run; one standard deviation of real government expenditure to the real exchange rate LEXt is positively significant and continues to be significant in the long run; one standard deviation of the real exchange rate LEXt to LEXt is positive (22%–29%) and continues to be positive in the long run; and finally, one standard deviation of symmetric oil price shocks to government expenditure is positively significant and continues to be so in the long run. Consequently, one standard deviation of symmetric oil price shocks, LOPt, and real government expenditure shocks, RGOEXt, to the real exchange rate, LEXt, are positive and long-run lasting.

Figure 4. Responses of RGOEXt, LEXt to symmetric oil price shocks LOPt.

4.7. The discussion

Having specified the baseline model, which relied on the work of Adedokun (Citation2018), supporting data are sourced from Saudi Arabian monetary agency (SAMA) yearly statistics and from international financial statistics (IFS). An ad hoc model has been formulated to test the impacts of symmetric oil price shocks and government expenditure on the real exchange rate. The real exchange rate is regressed against real government expenditure and symmetric oil price. All variables are transformed into log-linear form.

To perform this analysis, an autoregressive distributed lag and structural autoregressive models are tested to see how much real exchange rate is impacted by the symmetric oil price shocks and the real government expenditure. Prior to executing these tests, the unit root test is launched. At the integrated level of one, all variables are statistically significant at 1% and 5% level, respectively. On the other hand, the ARDL model test shows that 10% increase in symmetric oil price shocks leads to an appreciation of the real exchange rate by 0.11%. However, a rise in real government expenditure by 10% would cause an appreciation of the real exchange rate by 0.40%. Of equal importance, in the long run, and other things equal, 10% increase in symmetric oil price shocks would lead to a 3.5% to 4% depreciation of real exchange. Nevertheless, 10% rise in real government expenditure would cause between 3% to 5% appreciation of the real exchange rate in the long run.

Furthermore, the analysis of SVAR tends to confirm the findings stemmed from the ARDL model test. It is worthwhile to note that between 74% and 76% of variations in the real exchange rate, LEXt, are explained by the symmetric oil price shocks, LOPt, and the real government expenditure, RGOEXt, respectively. Our results are consistent with researchers’ findings in economic literature where positive oil price shocks tend to appreciate/depreciate the real exchange rates (Tasar, Citation2018,; Raji et al., Citation2018). Besides, the impulse response function, IRF confirms that one standard deviation of symmetric oil price shocks, LOPt, and real government expenditure shocks, RGOEXt, to the real exchange rate, LEXt, is significantly positive and long-run lasting.

In addition, the speed of convergence from short-run to long-run equilibrium is 8% and warranted on the basis that the impacts of symmetric oil price shocks on the real exchange rate via the effects of government expenditure take time. Furthermore, statistical robustness tests revealed the stability of the model and no serial correlations.

At last, the results obtained in this research are in line with the findings of Muhammed et al. (2012); Brini et al. (Citation2016), Nouria et al. (Citation2018), Raji et al. (Citation2018), Garcia et al. (Citation2018), Tasar (Citation2018), Mohammed et al. (Citation2019), and Babatunde (Citation2015), and others.

5. Conclusion and policy recommendations

The impact of symmetric oil price shocks on exchange rates is not yet a settled issue among economists. In economic literature, studies have concluded both appreciation and depreciation of real exchange rates due to symmetric and a symmetric oil price shocks. Different from other symmetric oil price shock studies, this work analyzed and estimated the effects of symmetric oil price shocks and real government expenditure on the real exchange rate for the period of 1970 until 2018. Eclectic ARDL and SVAR models were developed and tested. Additional FMOLS test is carried out to widen and strengthen the quality of research outcomes. The ADF and PP tests showed stationary time series at the first difference. Furthermore, error correction and bounds test revealed a clear and concise long-run relationships among the variables LOPt, RGOEXt, and LEXt.

The major hypothesis of this study was that symmetric oil price shocks and real government expenditure affect the real exchange rate positively and therefore, found to be inclined to Dutch disease theory. The ECMt-1 is statistically negative at a 1% level, and the error correction model reveals (0.08%) yearly speed of adjustment from the short run to the long-run equilibrium. This is somewhat low, indicating that the adjustment process from the short run to the long run takes a considerable time. The justification for low adjustment process is that, according to the causality test, the symmetric oil price shocks affect the government’s oil income and then, expenditure. Hence, the expenditure’s impacts will be transmitted into the real exchange rate. On the contrary, the coefficient of symmetric oil price shocks lagged 3 years revealed a negative and statistically significant impact on the real exchange rate (depreciation).

The results obtained from ARDL, SVAR, and FMOLS are in line with those in the economic literature, that is the oil price shocks appreciate/depreciate the real exchange rates. By the same token, government expenditure appreciates/depreciates the real exchange rates. The IRFs indicate that the response of the real exchange rate to symmetric oil price shocks and government expenditure shocks causes obvious stable appreciation of the real exchange rate over time. It is worthwhile to note too, that between 74% to 76% of the variations in the real exchange rate, LEXt is brought about by the symmetric oil price shocks and the real government expenditure RGOEXt, respectively.

The outcomes are pivotal for policymakers, local and foreign investors, and researchers. According to Brahmasrene et al. (Citation2014), policymakers and investors could benefit from these findings on the basis that imported US oil price fluctuations tend to follow exchange rate variations in the short run, while currency fluctuations follow oil price fluctuations in the long run. As a result, oil prices play a role in modeling the exchange rates (Babatunde, Citation2015). Accordingly, moving to flexible exchange rates and establishing oil funds could serve as fiscal buffers (Koh, Citation2017) to reduce and soften the hard impacts of oil price fluctuations. Saudi Vision 2030 motivated substantial efforts to accelerate the steps toward increasing sources of government income to maintain stable economic growth. The stable real exchange rate will be reflected on the value of imports and hence, inflation. Furthermore, taking precautionary measures against oil price fluctuations will mitigate the slump in government earnings and assist in the aggregated efforts of maintaining stable economic prosperity and employment. Designing a detailed roadmap within a designated time framework is necessary to help local and global economies avoid the pitfalls of oil price variations.

This research is limited to the Saudi Arabian economy and carried out despite some limitations. Lack of historical quarterly data for the 70s and early 80s. However, further development of this research is possible by testing the impacts of asymmetric oil price shocks on real exchange rates. Further extension is possible by applying Hodrick–Prescott filtering approach to test for the effects of oil price and government expenditure volatility on the real exchange rates. Furthermore, it is worthwhile to include Gulf Cooperation Countries (GCC): Oman, United Arab Emirates, Qatar, Kuwait, and Bahrain. These economies share the same economic, cultural, and structural environments.

Disclosure statement

No potential conflict of interest was reported by the author.

Additional information

Funding

Notes on contributors

Abdulaziz Hamad Algaeed

Abdulaziz Hamad Algaeed is an associate professor of economics at Dar Al-Uloom University. Prior to joining the current institution, he served as a faculty member of the department of economics at Imam Mohammed bin Saud University. He appointed as a member of supreme economic council for two years. Now he is a member of the advisory committee of capital market authority (CMA). His area of interest is macroeconomics, financial economics, and econometrics. He published several articles in reputable journals.

References

- Abdel-Latif, H., Osman, R., & Ahmed, H. (2018). Asymmetric impacts of oil price shocks on government expenditure: Evidence from Saudi Arabia. Cogent Economics & Finance, 6(1), 1512835. https://doi.org/10.1080/23322039.2018.1512835

- Adedokun, A. (2018). The effects of oil shocks on government expenditure and government revenue nexus in nigeria (with exogeneity restrictions). Future Business Journal, 4(2), 219–18. https://doi.org/10.1016/j.fbj.2018.06.003

- Al Rasasi, M., & Banafea, W. (2016). The effects of oil price shocks on the Saudi Arabian economy. The Journal of Energy and Development, 41(½), 31–45.

- Al Rasasi, M., Qualls, J., & Alghamdi, S., Oil revenues and economic growth in Saudi Arabia, “SAMA Working Paper WP/17/8”, 2018.

- Aleisa, E., & Dibooğlu, S. (2002). Sources of real exchange rate movements in Saudi Arabia. Journal of Economics and Finance, 26(1), 101–110. https://doi.org/10.1007/BF02744455

- Al-mulali, U., & Sab, N. (2011). The impact of oil prices on the real exchange rate of the Dirham: A case study of the United Arab Emirates (UAE). OPEC Energy Review, 35(4), 384–399. https://doi.org/10.1111/j.1753-0237.2011.00198.x

- Atems, B., Kapper, D., & Lam, E. (2015). Do exchange rates respond to asymmetrically to shocks in the crude oil market? Energy Economics, 49, 227–238. https://doi.org/http://dx.doi.10.1016/j.eneco.2015.01.027

- Babatunde, M. (2015). Oil price shocks and exchange rate in Nigeria. International Journal of Energy Sector Management, 9(1), 2–19. https://doi.org/10.1108/IJESM-12-2013-0001

- Baghestani, H., & Toledo, H. (2019). Oil prices and real exchange rate in the NAFTA region. American Journal of Economics and Finance, 48(C), 253–264. https://doi.org/10.1016/j.najef.2019.02.009

- Beckmann, J., Czudaj, R., & Arora, V., The relationship between oil prices and exchange rates: Theory and evidence, “US Department of Energy Working Paper Series”, June 2017. Washington, DC: Independent statistics and analysis. U.S. department of energy. www.eia.gov.

- Brahmasrene, T., Huang, J., & Sissoko, Y. (2014). Crude oil prices and exchange rates: Causality, variance decomposition, and impulse response. Energy Economics, 44, 407–412. https://doi.org/http://dx.doi.10.1016/j.eneco.2014.05.011

- Brini, R., Jemmali, H., & Farroukh, A. (2016). Macroeconomic impacts of oil price shocks on inflation and real exchange rates: Evidence from MENA economies. Topics in Middle Eastern and African Economies, 18(2), 170–185.

- Cakrani, E., Resulaj, P., & Koprencka, L. (2013). Government spending and real exchange rate: Case of Albania. European Journal of Sustainable Development, 2(4), 303–310. https://doi.org/10.14207/ejsd.2013.v2n4p303

- Corden, W. M. (1984). Booming sector and Dutch disease economics: Survey and consolidation. Oxford Economic Papers, 36(3), 359–380. https://doi.org/10.1093/oxfordjournals.oep.a041643

- De Castro, F., & Fernández, L. (2013). The effect of fiscal shocks on the exchange rate in Spain. The Economic and Social Review, 44(2), 151–180.

- Garcia, S., Saucedo, E., & Velasco, A. (2018). The effects of oil prices on the spot exchange rate (MXN/USD) a VAR analysis for Mexico: 1991–2017. Análisis Económico, 33(84), 33–56.

- Gosh, S. (2011). Examining crude oil price-exchange rate nexus for India during the period of extreme oil price volatility. Applied Energy, 88, 1886-1889. https://doi.org/10.1016/j.apenergy.2010.10.043

- Hashimova, K., The effect of oil price fluctuations on the exchange rate of Azerbaijan: Assessment of the ears 2014–2017, “Center for Economic and Social Development”, December 2017. www.cesd.az.

- Jibir, A., & Aluthge, C. (2019). Modelling the determinants of government expenditure in Nigeria. Cogent Economics & Finance, 7(1), 1–23. https://doi.org/10.1080/23322039.2019.1620154

- Karras, G. (2011). Exchange-rates regimes, and the effectiveness fiscal policy. Journal of Economic Integration, 26(1), 29–44. https://doi.org/10.11130/jei.2011.26.1.29

- Kaushik, N., Raja, N., & Upadhyaya, K. (2014). Oil price and real exchange rate: The case of India. International Business and Economic Research Journal, 13(4), 809–814.

- Khadan, J., An econometric analysis of energy revenue and expenditure shocks on economic growth in Trinidad and Tobago, “IDB Working Papers”, No. IDB-WP-764, 2016.

- Khalil, S., & Dombrecht, M. (2011). The auto-regressive distributed lag approach to co-integration testing: Application to OPT inflation. PMA Working papers, WP/11/03.

- Koh, W. C. (2017). Oil price shocks and macroeconomic adjustment in oil-exporting countries. International Economic Policy, 14(2), 187–210. https://doi.org/10.1007/s10368-015-0333-z

- Koray, F., & Chan, P. (1991). Government spending, and the exchange rate. Applied Economics, 23(9), 1551–1558. https://doi.org/10.1080/00036849100000208

- Miyamoto, W., Nguyen, T., & Shermirov, V., The effects of government spending on real exchange rates: Evidence from military spending panel data, “Federal Reserve Bank of Boston Working Papers”, No. 14–16, 2016.

- Mohammed, D., Afangideh, J., & Ogundele, O. (2019). Oil price and exchange rate nexus-evidence from Nigeria. International Journal of Accounting and Financial Reporting, 9(1), 298–316. https://doi.org/10.5296/ijafr.v9i1.14386

- Moshiri, S. (2015). Asymmetric effects of oil price shocks in oil-exporting countries: The role of institutions. OPEC Energy Review, Vl. 39(2), 222–246. https://doi.org/10.1111/opec.12050

- Muhammad, Z., Suleiman, H., & Kouhy, R. (2012). Exploring oil price-exchange rate nexus for Nigeria. OPEC Energy Review, 36(4), 383–395. https://doi.org/10.1111/j.1753-0237.2012.00219.x

- Narayan, P., Narayan, S., & Prasad, A. (2008). Understanding the oil price-exchange rate nexus for the Fiji Islands. Energy Economics, 30(5), 2686–2696. https://doi.org/10.1016/j.eneco.2008.03.003

- Nouria, R., Amor, H., & Rault, C., Oil price fluctuations and exchange rate dynamics in the MENA region: Evidence from non-causality-in-variance and asymmetric non-causality tests, “CESIFO Working Paper Series”, No., 7201, 2018. www.CESifo‐group.org/wp.

- Nusair, S., & Olson, D. (2019). The effects of oil price shocks on Asian exchange rates: Evidence from quantile regression analysis. Energy Economics, 78, 44–63. https://doi.org/10.1016/j.eneco.2018.11.009

- Nwosa, P. (2017). Fiscal policy and exchange rate movement in Nigeria. Acta Universitatis Danubius Œconomica, 13(3), 115–127. journals.univ-danubius.ro/index.php/oeconomica/article/view/3958/4162

- Olayungbo, D. (2019). Effects of global oil price on exchange rate, trade balance, and reserves in Nigeria: A frequency domain causality approach. Journal of Risk and Financial Management, 12(43), 1–14. https://doi.org/10.3390/jrfm12010043

- Osuji, E. (2015). International oil prices and exchange rate in Nigeria: A causality analysis. International Journal of Academic Research in Economics and Management Sciences, 4(3), 11–22. https://doi.org/10.6007/IJAREMS/v4-i3/1798

- Pesaran, H., & Shin, Y. (1999). An auto-regressive distributed lag modeling approach to co-integration analysis. In Strom, S. (Ed.), chapter 11 in econometrics and economic theory in the 20th century Ragnar Frisch symposium (pp. 371-413). Cambridge: Cambridge University press.

- Raji, J., Abdulkadir, R., & Badru, B. (2018). Dynamic relationship between Nigeria-US exchange rate and crude oil price. African Journal of Economics and Management Studies, 9(2), 213–230. https://doi.org/10.1108/AJEMS-06-2017-0124

- Rickne, J., Oil prices and real exchange rate movements in oil-exporting countries: The role of institutions, “Research Institute of Industrial Economies, IFN Working Paper”, No., 810, 2009.

- Smahi, A., & Mohamed, K. (2018). Can oil prices forecast the exchange rate?: Evidence from Algeria. American Journal of Economics, 8(4), 202–208. https://doi.org/10.5923/j.economics.20180804.03

- Su, X., Zhu, H., You, W., & Ren, Y. (2016). Heterogenous effects of oil shocks on exchange rates: Evidence from quantile regression approach. Springer Plus, 5(1), 1187. https://doi.org/10.1186/s40064-016-2879-9

- Tasar, I. (2018). Asymmetric relationship between oil price and exchange rate: The case of Romania. The Journal of International Social Sciences, 28(1), 143–154.

- Wen, T., & Wang, G. (2020). Volatility connectedness in global foreign exchange markets. Journal of Multinational Financial Management, 54(C), 100617. https://doi.org/10.1016/j.mulfin.2020.100617

- Yiew, T., Yip, C., Tan, Y., Habibullah, M., & Khadijah, C. (2019). Can oil prices predict the direction of exchange rate movements? An empirical and economic analysis for the case of India. Economic Research, 32(1), 812–823. https://doi.org/10.1080/1331677X.2018.1559746