?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aimed to investigate the nexus between the level of environmental financial accounting practices (EFAP) and cost of capital. The population of this study is 1.188 firm-year observations. However, we excluded 408 firm-year with less than 2 years of information to calculate EFAP, 73 firm-year without sufficient financial accounting information to calculate the cost of capital and 35 firm-year without sufficient financial accounting information to calculate control variables. Finally, this paper used a sample of 672 firm-year observations of listed companies on the Vietnam stock market for 5 years from 2013 to 2017. Two-stage regressions with the lag term are adopted to address econometric issues and to improve the accuracy of the regression coefficients. The results show that Vietnamese firms with higher EFAP performance can rapidly reduce their cost of capital. The findings also indicate that capital structure does not play a moderating role to evaluate the relationship between EFAP and the cost of capital.

PUBLIC INTEREST STATEMENT

This paper aims to analyze the level of environmental financial accounting practices (EFAP) and its impact on cost of capital. This study is essential because lack of empirical studies on the relationship between EFAP and cost of capital in the emerging markets context. In practice, the levels of disclosure accounting information did not meet the demand for information on environmental financial accounting as expected by stakeholders. Therefore, this research was conducted for raising awareness about the importance of EFAP in Vietnam stock market and promotion for EFAP. This paper not only extends prior research with the relationship between EFAP performance and cost of debt capital, but also considers the effect of EFAP performance on cost of equity. These research findings are important for emerging markets since Vietnamese firms’ external financing is mainly from debt resources, and the empirical results provide a useful way for firms to improve their cost of capital.

1. Introduction

According to Nguyen (Citation2019), many large corporations in the world such as Formosa, British Petroleum Corporation (BP), Volkswagen’s largest automobile manufacturing group have collapsed due to fraud in information disclosure related to environmental protection. It is also a warning bell for businesses to raise awareness of environmental protection and publicize environmental information to related parties. Lately years, there has been a growing concern about the accountability of companies in reporting relevant environmental information. Generally, companies are expected to disclose environmental accounting information in their report for performance and reputation. According to Spasić and Stojanović (Citation2013), companies’ pressure for accountability in reporting comes from various reasons including demands from pressure groups such as investors and consumers, and directives from United Nation’s and European Community’s (EU). Accordingly, management can no longer continue to treat the conventional stewardship objective, as the only acknowledged standard of business operation.

Because of the importance of the practice and publication of environmental accounting information, recent studies related to the necessity of environmental accounting practices are receiving great attention from researchers in the world. These studies have argued that corporate environmental performance can improve the satisfaction of all stakeholders, enhance the corporate brand image, and even mores increase firm value and lower the cost of capital. According to Lin and Dong (Citation2018), firms with higher prior history of positive corporate environmental performance are less likely to file for bankruptcy when they are in deep financial distress and are more likely to experience accelerated recovery from distress. According to Cai, Cui, and Jo (Citation2016) and Fuadah et al. (Citation2019), firms with better environmental performance as less risky, and provide evidence suggesting that corporate environmental performance is positively related to firm value. Similarly, Al‐Hadi et al. (Citation2019) show that corporate environmental performance is associated with a positive valuation effect, and in their meta-analysis of prior quantitative research, Poddi and Vergalli (Citation2016) conclude that there is a positive association between corporate social or environmental responsibility and corporate financial performance. According to Oikonomou et al. (Citation2014), environmental performance can be regarded as a manner in their business decisions and processes, along with the strength of their relationships with various corporate stakeholders. Ghoul et al. (Citation2011) found that investment in improving responsible employee relations, environmental policies, and product strategies contributes substantially to reducing firms’ cost of equity. (Yeh et al., Citation2019) show that Chinese firms with higher environmental responsibility performance can rapidly reduce their cost of debt capital. Xu et al. (Citation2015) found that investments in improving environmental responsibility performance towards investors make the greatest contribution to reducing firms’ equity financing costs, and the cost of capital effects of environmental responsibility performance is more significant in recessions than in economic booms. Salvi et al. (Citation2018) indicated that firms with better environmental responsibility performance face significantly lower capital constraints. Similarly, some pioneer research also documents that strong environmental responsibility performance can lower the cost of equity capital (Oikonomou et al., Citation2014; Salvi et al., Citation2018), cost of debt capital (Jha & Cox, Citation2015), and credit spreads (Ghoul et al., Citation2011). According to Ghoul et al. (Citation2011), firms with better environmental responsibility performance exhibit cheaper equity financing and reducing firms’ cost of equity. However, these studies have been carried out in developed countries in the world, where there are differences in business characteristics of enterprises, characteristics of capital structure (CS) and financial market compared to Vietnam.

The importance of practicing environmental accounting in Vietnamese enterprises is also receiving increasing attention from both businesses and researchers. The research of Nguyen and Tran (Citation2019) indicated that the level of disclosure of environmental accounting information positive affects the financial performance of businesses both now and in the future. The research of Nguyen (Citation2019) investigated that there is close relationship between the level of environmental financial accounting practices (EFAP) and corporate financial risk of current year and following years. Similarly, Nguyen (Citation2019) showed that corporate environmental performance is associated with a positive valuation effect, and there is a positive association between corporate social or environmental responsibility and corporate financial performance. According to Nguyen (Citation2019) and Nguyen et al. (Citation2017), the disclosure levels of environmental accounting information of Vietnamese firms tend to increase. However, these levels of disclosure environmental information did not meet the demand for information on environmental accounting as expected by stakeholders. Even though the number of studies on EFAP is high, an empirical examination of the relationship between EFAP and cost of capital in the emerging markets context is limited. The lack of empirical studies on this issue could be one of the factors in explaining why companies listed on the Vietnam securities market are less concerned or involved in promoting their EFAP to various stakeholder groups. Therefore, our research was conducted for raising awareness about the importance of environmental accounting practices of listed companies in Vietnam stock market and promotion for EFAP.

The remainder of the paper is structured as follows. Section 2 presents theoretical background and research hypotheses. Section 3 describes our sample and research methodology. Section 4 presents the empirical results and robustness tests. Section 5 discusses the findings and provides a conclusion.

2. Literature review and hypothesis development

2.1. Literature review

Many studies in the literature have demonstrated that the financial system, including banking and capital markets, provides an important mechanism for assisting enterprises to raise capital. Vietnam is a small and partially open economy where the financial markets and institutional developments are still far behind the developed countries. Vo and Ellis (Citation2017) indicated that compared with developed markets, Vietnam’s capital market is relatively new and growing quickly. In recent years, with the trend of global integration, Vietnam’s financial market creates a more competitive business environment toward equal opportunity for private, foreign owned, state owned and privatized firms in getting fund in financial markets. In the last two decades, the Vietnamese government sets prioritizes in promoting financial liberalization and facilitating constant institutional reforms. Under the efficiency market hypothesis, Vo (Citation2016) argues that Vietnam’s stock market exhibits weak efficiency, indicating that investors in Vietnam react slowly when they receive related information from the market. In addition, many scholars have found that investors exhibit different reactions to good and bad news releases (Vo & Ellis, Citation2017). Dang et al. (Citation2018) find that investor’s adjustment speed is slow in response to good news released in the stock markets of Vietnam, illustrating that when investors receive good news, they may react slowly. It supports the conclusion that Vietnam’s capital market presents weak efficiency. Therefore, to account for such weak efficiency, this study employs a lag term in the regression to describe the current market status.

Companies with higher financial performance generally tend to disclose environmental accounting information. Vietnam firms are paying attention to the release of information on environmental indicators, but these have not been logically stated based on the assessments of stakeholders (Nguyen et al., Citation2017). Nguyen (Citation2019) shows that the difference in EFAP between western countries and Vietnam is the driving force, whereby stakeholders and state-owned holders in western and Vietnam respectively elicit this driving force. Thus, CEOs in Vietnam put less effort into EFAP in both state ownership and private companies. To develop EFAP in Vietnam’s market, the government began to formulate EFAP-related regulations and practices in state ownership companies (Nguyen et al., Citation2017). In 2015, Ministry of Finance issued Circular 155/2015/TT-BTC on guidelines for information disclosure on securities market. Vietnamese firms list on securities market are required to report related impact of the company on the environment. Besides, Vietnamese firms are also encouraged to publish environmental information according to global standards for sustainability reporting.

Signaling theory is useful for describing behavior when two parties (individuals or organizations) have access to different information. Typically, one party, the sender, must choose whether and how to communicate (or signal) that information, and the other party, the receiver, must choose how to interpret the signal. Accordingly, signaling theory holds a prominent position in a variety of management literatures, including strategic management, entrepreneurship, and human resource management are (Connelly et al., Citation2011). Mavlanova et al. (Citation2012) argue that when some investors have more private information than others, information asymmetry occurs in the capital market. To reduce the cost of capital, corporations exert great effort at reducing information asymmetry. Therefore, lower information asymmetry in the capital market leads to a lower cost of capital (Walker, Citation2010).

The signaling theory can offer one solution to information asymmetry. Mavlanova et al. (Citation2012) used a signaling timeline to explain the signaling process between the signaler and receiver. To reduce information asymmetry, the signaler conveys a signal to the receiver. After the receiver observes and interprets this signal, he or she makes a decision and transmits it to the signaler. In this study, the signaler is a firm that conveys EFAP as a signal to the receivers, who are investors. After investors receive and interpret this signal, they make their investment decision and decide how much payment they require, which is the feedback. EFAP can signal cooperation information, which concerns governments, businesses, and society, to investors (Mahoney et al., Citation2013). Hahn and Kühnen (Citation2013) find that firms transmit corporate governance-related information to potential investors to reduce their information asymmetry and investment risk. Corporate executives can deliver non-financial messages to potential investors. EFAP performance can reduce the cost of capital for firms through information transmission, such as signaling (Connelly et al., Citation2011).

2.2. Hypothesis development

Mavlanova et al. (Citation2012) showed that the cost of equity perfectly correlates with the conditional expected stock return, book-to-market values and excess stock returns to different dimensions of socially responsible performance. Increasing corporate socially responsible can reduce equity financing cost (Mahoney et al., Citation2013), firms with better social responsibility performance face significantly lower capital constraints. Previous research (Dutta & Nezlobin, Citation2017) suggests that effective corporate governance and stricter disclosure standards can decrease a firm’s cost of equity capital through a reduction in agency and information asymmetry problems. Connelly et al. (Citation2011) also report that both better stakeholder engagement and transparency around CSR performance are important in reducing capital constraints. They specifically argue that better access to finance can be attributed to (1) reduced agency costs due to enhanced stakeholder engagement and (2) reduced informational asymmetry due to increased transparency. Ghoul et al. (Citation2011) demonstrate that investment in improving responsible employee relations, environmental policies, and product strategies contributes substantially to reducing firms’ cost of equity. Similarly, Xu et al. (Citation2015) find that better corporate social responsibility practices can lower the cost of equity capital in China’s capital market. Therefore, our first hypothesis is as follows.

H1: Firms with higher EFAP performance have a lower cost of equity capital.

According to information asymmetry between corporation management and outside investors, Connelly et al. (Citation2011) reveal that corporations give priority to raising capital through debt financing. In addition, Rosa et al. (Citation2018) found a negative relationship between corporate social performance and interest rate, and a positive relationship between corporate social performance and debt rating. Thus, corporate social performance has a positive role in reducing the cost of debt capital. Moreover, firms with better corporate social performance are more attractive to lenders in terms of leverage allowance. Goss and Roberts (Citation2011) concluded that when corporations raise more capital through debt financing, information asymmetry may further increase and raise the cost of capital. In other words, when debt holders control most of the capital resources, they may also have access to private information for making investing decisions. Outside investors who have less access to private information may ask for a higher return on investments in a corporation. Huang et al. (Citation2017) provided that lenders are more sensitive to social responsibility concerns in the absence of security. Thus, banks are more willing to provide attractive loan terms to socially responsible firms. Yeh et al. (Citation2019) showed that Chinese firms with higher social responsibility performance can rapidly reduce their cost of debt capital. Therefore, our second hypothesis is as follows.

H2: Firms with higher EFAP performance have a lower cost of debt capital.

According to the signaling theory, to reduce the cost of capital, corporations exert great effort at reducing information asymmetry. Therefore, lower information asymmetry in the capital market leads to a lower cost of capital. CS choices also reflect a firm’s cost of capital when the decision is affected by information asymmetry. We infer that information asymmetry creates an incentive for corporations to raise capital through debt financing (Dutta & Nezlobin, Citation2017; Ghoul et al., Citation2011; Jha & Cox, Citation2015; Yeh et al., Citation2019) indicates that when firms encounter higher information asymmetry, they tend to raise capital through debt financing. When firms raise their capital through debt financing with higher information asymmetry among insiders and outside investors, it potentially leads to a higher cost of equity capital. Therefore, we predict that firms with a lower debt ratio that disclose social information can reduce cost of equity capital. Combining the above predictions of the theoretical models, we conclude the following hypotheses.

H3a: Higher EFAP performance reduces the cost of equity capital more effectively in firms with a lower debt ratio in Vietnam’s market.

H3b: Higher EFAP performance reduces the cost of debt capital more effectively in firms with a lower debt ratio in Vietnam’s market.

3. Research methodology

3.1. Sample and source of data

We rely on a sample of companies must meet two criteria: (i) having a complete set of annual accounting data for the 5 years 2013–2017; (ii) companies must disclose environmental accounting information in their annual report or sustainability report. The final sample for this study was unbalanced table data, as shown in Table .

Table 1. Research sample selection criteria

Although the number of companies selected for research is not large compared to the total number of companies listed on the Vietnam Stock Exchange at that time. However, with the binding of standards and the convenience of data collection, the research team used the above research data. The sample size chosen by the author with 672 observations is reasonable (Joe et al., Citation2014).

3.2. Variable measurements

3.2.1. Level of environmental financial accounting practices (EFAP)

According to the Global Reporting Initiative (GRI), Sustainable Development Report Guidelines, the total number of items for disclosure of mandatory environmental accounting information is 34 items in the 12 relevant fields as Table .

Table 2. Items for mandatory environmental information disclosure

Depends on how the company has published relevant information on the annual report for assessing the scored for the level of EFAP according the Table .

Table 3. Method to assess the levels of environmental financial accounting practices

EFAP is calculated according to the weighted approach, depending on the quality of the information provided to assess the score for each item, then averaged for each category and calculated the level of environmental financial accounting practice. The formula is as follows: The level of environmental financial accounting practice of firms X = (Yi is the score of information item i published by firm X).

3.2.2. Cost of equity capital and cost of debt capital

To measure financial cost of equity capital, we apply the capital asset pricing model (CAPM) (Da et al., Citation2012; Fama & French, Citation2004; Nasr et al., Citation2011). The cost of equity capital is calculated by this formula:

where COE: cost of equity capital, : individual stock return in year t,

risk-free rate in year t,

: m Market return in year t,

excess return of individual stock,

—

market factor, β: systematic risk.

We follow Kang and Shin (Citation2016) to calculate cost of debt; a company must determine the total amount of interest it is paying on each of its debts for the year. Then it divides this number by the total of all debt outstanding. The formula is as follows:

For example, a company has a 1 USD million loan with a 5% interest rate and a 200,000 USD loan with a 6% rate. It has also issued bonds worth 2 USD million at a 7% rate. The interest on the first two loans is 50,000 USD and 12,000 USD, respectively, and the interest on the bonds equates to 140,000 USD. The total interest for the year is 202,000 USD. As the total debt is 3.2 USD million, the company’s cost of debt is 6.31%.

In this study, we adopt the debt ratio, which is calculated by dividing total liability by both total liabilities and stockholders’ equity, as the capital (CS) variable. A high ratio implies that firms raise more capital through debt financing than through equity. According to Fama and French (Citation2004), firms obtaining capital through debt financing may increase the information asymmetry between insiders and outside investors. We expect that firms with higher ratios encounter higher information asymmetry, and that the CS positively moderates the relationship between EFAP performance and the cost of capital. We classify CS into high debt financing firms and lower debt financing firms based on each year’s median. The results show that if CS is higher than the CS median, then the value is 1 and 0 otherwise.

3.2.3. Control variables

There have been quite a number of studies on the factors affecting the cost of capital such as (Öztekin, Citation2015; Xue et al., Citation2017) these studies showed that many factors affecting the cost of capital such as the financial leverage, return on asset, management competence, company size, cash flow, the ratio of the market value to book value of total, quick ratio, business cycle, listing period, independent auditing. In order to examine the relationship between social responsibility practice and cost of capital, previous studies have also used control variables besides independent variables such as: The percentage of state capital, financial leverage, cash flow, the ratio of the market value to book value of total, debt ratio, independent auditing (Ghoul et al., Citation2011; Godfrey et al., Citation2009; Oikonomou et al., Citation2014; Yeh et al., Citation2019). These studies have demonstrated that business size, financial leverage, listing period, independent auditing, cash flow, the ratio of the market value to book value of total, cash ratio have significantly affect on cost of capital. Besides that due to data collection limitations, this study of the authors will include seven control variables to consider the relationship between EFAP and COC including: business size (SIZE); financial leverage (LEV); market to book ratio (MTB); return on assets (ROA); cash flow from operations (OFO); cash ratio (CR); net loss (Loss). They are measured as in Table :

Table 4. The way to evaluated the control variables

3.3. Data analysis technique

To examine the relationship between the level of EFAP and cost of capital, two following stage regressions are adopted to verify our Hypotheses 1 and 2. These regressions employ a lag term to describe the current Vietnam’s capital market, weak efficiency.

Regression 1: The association between EFAP performance and cost of equity capital.

The regression shows relationship between EFAP performance and cost of equity using the ordinary least squares (OLS), fixed effects model (FEM), and random effects model (REM). We use 1 or 2 years ahead cost of equity and current period of EFAP performance to capture the effect of lagged 1 year and lagged 2 years of EFAP performance on cost of equity, respectively. To choose the most appropriate method among three models include OLS, FEM, and REM, research conducted the Breusch-Pagan Lagrange test, Hausman test, and F-test.

Regression 2: The association between EFAP performance and cost of debt capital.

The regression shows relationship between EFAP performance and cost of debt capital using the OLS, FEM, and REM. We use 1 or 2 years ahead cost of debt and current period of EFAP performance to capture the effect of lagged 1 year and lagged 2 years of EFAP performance on cost of debt, respectively. The study also conducted Breusch-Pagan Lagrange test, Hausman test, and F-test, to choose the most suitable model to measure this relationship.

In order to verify the moderate effect of CS, we modify our Equations (1) and (Equation2(2)

(2) ) into EquationEquations (3

(3)

(3) ) and (Equation4

(4)

(4) ), with the empirical model as follows:

The regressions show relationship between EFAP performance and cost of equity capital, cost of debt capital considering the role of CS. We use 1 and 2 years ahead cost of both equity and debt capital and current period of EFAP performance to capture the effect of lagged 1 year and lagged 2 years of EFAP. We employ the debt ratio as the proxy for CS and implement two-way interactions into our regression model for the cost of both equity and debt capital.

Here, CS represents a dummy variable that equals 1 if financial leverage is over 50% and zero otherwise. EFAP_CS is an interaction term between EFAP performance and CS. The moderating effect of CS can be observed from the coefficient of the cross term (β3). If the coefficient is significant in β3, then the slope between EFAP and the cost of capital will vary between firms with a high debt ratio and those with a low debt ratio.

4. Empirical results and discussion

4.1. Descriptive statistics

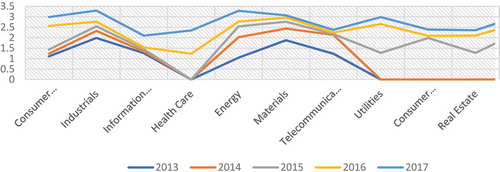

Figure gives an overview of the level of EFAP by listed companies in Vietnam from 2013 to 2017. During the study period, the number of listed companies does not only evidence increasing market volatility with disclosure of environmental accounting information (from 18 companies in 2013 to 295 companies in 2017), but also by Indicator level of EFAP, which is a good sign demonstrating that Vietnam firms are paying attention to the release of information on environmental indicators. This is shown by the mean value of the EFAP indicators are growing steadily every year. However, the data also show that the level of EFAP between different industries is different; some companies focus on investing heavily in information and indicators, but this information has not been logically stated based on the assessments of stakeholders.

Figure 1. The level of the environmental financial accounting practices of listed companies for the period 2013–2017 according to the industry.

Table presents basic statistical describing parameters of independent variables and dependent variables. According to Tauchen(Citation1986) condition for estimation of reliability for performing regression analysis is n > 200. According to Joe et al. (Citation2014), there should be 15–20 observations for a variable to be estimated. Combined with these principles, the sample size chosen by the authors with 672 observations is reasonable, this result guarantee reliability. According to the number on Table , the level of EFAP is 2.034 and range from 0.000 to 3.298. The size of the business ranges from 10.201 to 19.988, indicating that the size of the firms in the sample differs widely. The mean of cost of equity (debt) is 28.4% (10.2%), implying that external equity financing is more expensive than external debt financing.

Table 5. Statistical analysis

Table presents the results of the correlation coefficient test between the variables and the results of the multi-collinearity test. The purpose of the correlation analysis is to examine the tendency of the relationship between independent variables and dependent variables in the model. The level of EFAP is negatively correlated with cost of equity or cost of debt (−0.075 and −0.024), which means that the higher the level of EFAP, the lower cost of equity or cost of debt. However, to confirm whether the results are accurate or not, we need to conduct multivariate regression analysis.

Table 6. Correlation and multi-collinearity test

Table also shows the results of the multi-collinearity test, the results show that at the same time, the correlated pairs are less than 0.8 and the VIF of the independent variable is less than 5, which proves that there is not multi-collinearity. In addition, in order to increase the reliability of the regression results, the study conducted to examine whether there was a change in variance in the research model through the use of the White’s General test. The test results show that the p value is greater than 0.05, so with a significance level of 5% the H0 hypothesis on the uniformity of the variance is acceptable. That is, the pattern does not exist in the phenomenon of variance. With the above analysis, we assert that appropriate research data to perform multivariate regression analysis to examine the relationship between the level of EFAP and cost of capital.

4.2. Discussion

4.2.1. The association between EFAP performance and cost of equity capital

The results in Table show that both the lagged 1 year and lagged 2 years of EFAP performance are negatively and significantly associated with cost of equity. Thus, the level of EFAP of enterprises listed on the Vietnam stock market influences the cost of equity. Overall, our results preliminarily support that the performance of EFAP can lower the cost of equity capital, therefore supporting our Hypothesis 1.

Table 7. Regression results

4.2.2. The association between EFAP performance and cost of debt capital

Table results indicate that, in the case of lagged 1 year of EFAP performance, the OLS model is best suited, in the case of lagged 2 years of EFAP performance, the FEM model is sub-merged with the significance level of 5%. The results in Table show that performance of EFAP can lower the cost of debt capital, therefore supporting our Hypothesis 2.

Table 8. Regression results

4.2.3. The association between EFAP performance, cost of capital and capital structure

Table shows that the coefficient of the interaction term CS and EFAP is positive, but not significantly associated with cost of equity capital. These results illustrate that EFAP performance does not help firms, whereas higher debt ratios can effectively reduce their cost of equity capital. Thus, CS does not play a moderating role between EFAP performance and the cost of equity capital. This result does not support Hypothesis 3a. To validate these findings further, we adopt the cost of debt capital as our dependent variable to investigate the moderating role of CS. Model 3 and Model 4 (in Table ) examine that the coefficients of the interaction term CS and EFAP have no significant relation with the cost of debt capital. The results reveal that CS does not play a moderating role between EFAP performance and the cost of debt capital. Thus, Hypothesis 3b is not supported.

Table 9. The effect of EFAP performance on capital cost considering the role of capital structure

5. Conclusion and recommendations

Research results have shown that there exists a relationship between the level of EFAP and the cost of capital of enterprises in listed companies on the Vietnamese stock market. This result is similar to previous studies. However, in addition to this study, there have been new points compared to previous studies such as (1) research has examined the impact of the level of EFAP on cost of capital. As a result, lagged 1 year and 2 years of EFAP performance is negatively and significantly associated with both cost of equity and cost of debt, so we conclude that performance of EFAP can lower the cost of both equity and debt capital. (2) We use CS as a moderator to evaluate the relationship between EFAP and the cost of capital, the findings present that CS does not play a moderating role between EFAP performance and the cost of equity capital, it means that, the higher EFAP performance do not reduce the cost of equity and debt capital more effectively in firms with a lower debt ratio in Vietnam’s market. The results again confirm the benefits and implications of implementing environmental accounting. In other words, in the current context, EFAP not only helps enterprises comply with the law, improve their image but also helps businesses reduce the transaction costs to obtain external funding. From the research results, the research team proposed some recommendations to the Vietnam as follows:

First, the need to raise awareness of corporate environmental responsibility and the benefits of disclosing detailed environmental accounting information to the financial performance of the business. Some businesses say that if they focus on environmental protection activities, transparency of environmental accounting information is costly, reducing profits, it is a misconception. The results of this study showed that the firms with higher EFAP performance have a lower cost of both equity and debt capital. Therefore, the practice and disclosure of environmental accounting information is necessary, help businesses avoid legal complications to improve the image and reduce cost of capital.

Second, in the Vietnamese context, the reporting of primary environmental accounting information is still voluntary and free of any general pattern, with only large companies reporting responsibility. The number of companies reporting social responsibility is very low. Research results are the basis for encouraging organizations to change views when making annual reports as well as the content of disclosure in their annual report should not be too focused on the indicators. Financial results achieved during the year that ignored the environmental performance achieved. Because, together with the trend of green development of the world, investors are more interested in the information related to the implementation of corporate social responsibility. Consequently, with the implementation of environmental responsibility, the disclosure of this information to investors is also a way to attract their attention.

Third, the results also show that, in addition to the level of disclosure of environmental accounting information, other factors such as business size, financial leverage, market to book ratio, return on assets, cash flow from operations, cash ratio, net loss also affect the cost of capital. Therefore, in order to achieve the most efficient use of capital, in addition to the factors of practice and information disclosure, enterprises should consider the influence of other factors on the cost of capital. Since then, there is a reasonable adjustment plan to improve the efficiency of capital use, bringing the highest economic efficiency to businesses.

Basing on the quantitative and qualitative research methodology, this study provides an alternative way to lower Vietnamese firms’ cost of capital by investigating the relationship between EFAP performances and cost of capital. The results indicate that better EFAP performance can effectively lower the cost of capital. Firms can implement EFAP as a mechanism to lower their cost of capital by conveying a sustainable development commitment and social responsibility to creditors. On the other hand, creditors can decide whether to assist sustainable firms to lower their cost of capital by observing firms’ EFAP performance. Besides that the result of research also showed that the firms with a lower debt ratio, practice of environmental accounting has no much meaning in reducing the cost of capital. From the research results, the team has made several recommendations to promote the level of EFAP in the future. The article has enriched the sources of research on environmental accounting as well as contributed to improve EFAP in the future. However, one limitation is that we adopt Vietnam capital market data to investigate the relationship between EFAP and cost of capital. Whether, there is any difference between Vietnam and other countries in Southeast Asia such as Indonesia, India, or Thailand is still an unanswered question. Nevertheless, we consider these to be suggestive for further research in the future.

Citation information

Cite this article as: Environmental accounting practices and cost of capital of enterprises in Vietnam, Nguyen Huu Anh, Nguyen La Soa & Ha Hong Hanh. Cogent Economics and Finance (2020), 8: 1790964.

Acknowledgements

The authors would like to thank anonymous reviewers for their supportive comments and suggestions.

Additional information

Funding

Notes on contributors

Nguyen Huu Anh

Nguyen Huu Anh is an Associate Professor of Accounting, Dean of the School of Accounting and Auditing (SAA) at National Economics University (NEU) in Vietnam. His research interests include market based accounting research, and corporate finance. He is the author and co-authors of more than 50 research papers in different peer and refereed journals. He is also the author and co-authors of several text books in accounting and business.

Nguyen La Soa

Nguyen La Soa is a senior lecturer of accounting in the SAA at the National Economics University (NEU), Vietnam. She obtained her PhD (2017) from Academy of Finance, Vietnam. Her research interests are in environmental accounting and finance.

Ha Hong Hanh

Ha Hong Hanh is a senior lecturer of accounting in the SAA at the National Economics University (NEU), Vietnam. She obtained her PhD (2018) from the NEU, Vietnam. Her research interests are in qualitative and quantitative analysis in accounting information system and auditing.

References

- Al‐Hadi, A., Chatterjee, B., Yaftian, A., Taylor, G., & Hasan, M. M. (2019). Corporate social responsibility performance, financial distress and firm life cycle: Evidence from Australia. Accounting and Finance, 59(2), 961–17. https://doi.org/10.1111/acfi.12277

- Cai, L., Cui, J., & Jo, H. (2016). Corporate environmental responsibility and firm risk. Journal of Business Ethics, 139(3), 563–594. https://doi.org/10.1007/s10551-015-2630-4

- Connelly, B. L., Certo, S. T., Ireland, R. D., & Reutzel, C. R. (2011). Signaling theory: A review and assessment. Journal of Management, 37(1), 39–67. https://doi.org/10.1177/0149206310388419

- Da, Z., Guo, R.-J., & Jagannathan, R. (2012). CAPM for estimating the cost of equity capital: Interpreting the empirical evidence. Journal of Financial Economics, 103(1), 204–220. https://doi.org/10.1016/j.jfineco.2011.08.011

- Dang, N. H., Pham, D. C., & Vu, T. B. H. (2018). Effects of financial statements information on firms’ value: Evidence from Vietnamese listed firms. Investment Management and Financial Innovations, 15(4), 210–218. https://doi.org/10.21511/imfi.15(4).2018.17

- Dutta, S., & Nezlobin, A. (2017). Information disclosure, firm growth, and the cost of capital. Journal of Financial Economics, 123(2), 415–431. https://doi.org/10.1016/j.jfineco.2016.04.001

- Fama, E. F., & French, K. R. (2004). The capital asset pricing model: Theory and evidence. Journal of Economic Perspectives, 18(3), 25–46. https://doi.org/10.1257/0895330042162430

- Fuadah, L. L., Arisman, A., Wardani, R. S., & Yunita, A. (2019). Corporate social responsibility mediates corporate govermance index and financial performance indonesia. Academy of Accounting and Financial Studies Journal, 23(1), 1–8. https://doi.org/https//doi.10.1257/0895330042162430

- Ghoul, S. E., Guedhami, O. C. Y., Kwok, C., & Mishara, D. R. (2011). Does corporate social responsibility affect the cost of capital? Journal of Banking & Finance, 35(9), 2388–2406. https://doi.org/10.1016/j.jbankfin.2011.02.007

- Godfrey, P. C., Merrill, C. B., & Hansen, J. M. (2009). The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management. Strategic Management Journal, 30(4), 425–445. https://doi.org/10.4236/ib.2013.53B039

- Goss, A., & Roberts, G. S. (2011). The impact of corporate social responsibility on the cost of bank loans. Journal of Banking & Finance, 35(7), 1794–1810. https://doi.org/10.1016/j.jbankfin.2010.12.002

- Hahn, R., & Kühnen, M. (2013). Determinants of sustainability reporting: A review of results, trends, theory, and opportunities in an expanding field of research. Journal of Cleaner Production, 59(1), 5–21. https://doi.org/10.1016/j.jclepro.2013.07.005

- Huang, J., Duan, Z., & Zhu, G. (2017). Does corporate social responsibility affect the cost of bank loans? Evidence from China. Emerging Markets Finance and Trade, 53(7), 1589–1602. https://doi.org/10.1080/1540496X.2016.1179184

- Jha, A., & Cox, J. (2015). Corporate social responsibility and social capital. Journal of Banking & Finance, 60(2), 252–270. https://doi.org/10.1016/j.jbankfin.2015.08.003

- Joe, Hair, F., Christian, Ringle, M., & Sarstedt., M. (2014). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice., 19(2), 139–152. https://doi.org/10.2753/MTP1069-6679190202

- Kang, W., & Shin, J. (2016). Derivation of corporate debt pricing model and its empirical implications. Asia-Pacific Journal of Financial Studies, 45(3), 439–462. https://doi.org/10.1111/ajfs.12135

- Lin, K. C., & Dong, X. (2018). Corporate social responsibility engagement of financially distressed firms and their bankruptcy likelihood. Advances in Accounting, 43(1), 32–45. https://doi.org/10.1016/j.adiac.2018.08.001

- Mahoney, L. S., Thorne, L., Cecil, L., & LaGore, W. (2013). A research note on standalone corporate social responsibility reports: Signaling or greenwashing? Critical Perspectives on Accounting, 24(4–5), 350–359. https://doi.org/10.1016/j.cpa.2012.09.008

- Mavlanova, T., Benbunan-Fich, R., & Koufaris, M. (2012). Signaling theory and information asymmetry in online commerce. Information & Management, 49(5), 240–247. https://doi.org/10.1016/j.im.2012.05.004

- Nasr, H. B., Boubakri, N., & Cosset, J.-C. (2011). The political determinants of the cost of equity: Evidence from newly privatized firms. Journal of Accounting Research, 50(3), 605–646. https://doi.org/10.1111/j.1475-679X.2011.00435.x

- Nguyen, L. S. (2019). Relationship between environmental financial accounting practices and corporate financial risk: Evidence from listed companies in Vietnams securities market. Asian Economic and Financial Review, 9(2), 285–298. https://doi.org/10.18488/journal.aefr.2019.92.285.298

- Nguyen, L. S., & Tran, M. D. (2019). Disclosure levels of environmental accounting information and financial performance: The case of Vietnam. Management Science Letters, 9(4), 557–570. https://doi.org/10.5267/j.msl.2019.1.007

- Nguyen, L. S., Tran, M. D., Nguyen, T. X. H., & Le, Q. H. (2017). Factors affecting disclosure levels of environmental accounting information: The case of Vietnam. Accounting and Finance Research, 6(4), 255–264. https://doi.org/10.5430/afr.v6n4p255

- Oikonomou, I., Brooks, C., & Brooks, C. (2014). The effects of corporate social performance on the cost of corporate debt and credit ratings. Financial Review, 49(1), 49–75. https://doi.org/10.1111/fire.12025

- Öztekin, Ö. (2015). Capital structure decisions around the world: Which factors are reliably important? Journal of Financial and Quantitative Analysis, 50(3), 301–323. https://doi.org/10.1017/S0022109014000660

- Poddi, N. C. L., & Vergalli, S. (2016). Corporate social responsibility and firms’ performance: A strategic graphical analysis. Journal of International Business and Economics, 4(1), 1–12. https://doi.org/10.15640/jibe.v4n1a1

- Rosa, F., Liberatore, G., Mazzi, F., & Terzani, S. (2018). The impact of corporate social performance on the cost of debt and access to debt financing for listed European non-financial firms. European Management Journal, 36(4), 519–529. https://doi.org/10.1016/j.emj.2017.09.007

- Salvi, A., Petruzzella, F., & Giakoumelou, A. (2018). Does sustainability foster the cost of equity reduction? The relationship between corporate social responsibility (CSR) and riskiness worldwide. African Journal of Business Management, 12(12), 381–395. https://doi.org/10.5897/AJBM2018.8562

- Spasić, D., & Stojanović, M. (2013). Sustainability reporting –- Theoretical framework and reporting practive in the serbian oil industry. Economics and Organization, 10(3), 231–244. https://doi.org/org/665.6/.7:005.71]:651.78

- Tauchen, G. (1986). Finite state markov-chain approximations to univariate and vector autoregressions. Economics Letters, 20(2), 177–181. https://doi.org/10.1016/0165-1765(86)90168-0

- Vo, X. V. (2016). Determinants of capital structure in emerging markets: Evidence from Vietnam. Research in International Business and Finance, 40(1), 105–113. https://doi.org/10.1016/j.ribaf.2016.12.001

- Vo, X. V., & Ellis, C. (2017). An empirical investigation of capital structure and firm value in Vietnam. Finance Research Letters, 22(1), 90–94. https://doi.org/10.1016/j.frl.2016.10.014

- Walker, K. (2010). A systematic review of the corporate reputation literature: Definition, measurement, and theory. Corporate Reputation Review, 12(4), 357–387. https://doi.org/10.1057/crr.2009.26

- Xu, S., Liu, D., & Huang, J. (2015). Corporate social responsibility, the cost of equity capital and ownership structure: An analysis of Chinese listed firms. Australian Journal of Management, 40(2), 245–276. https://doi.org/10.1177/0312896213517894

- Xue, H., Zhang, S., Su, Y., & Wu, Z. (2017). Factors affecting the capital cost of prefabrication – A case study of China. Sustainability, 9(9), 1–22. https://doi.org/10.3390/su9091512

- Yeh, -C.-C., Lin, F., Wang, T.-S., & Wu, C.-M. (2019). Does corporate social responsibility affect cost of capital in China. Asia Pacific Management Review. Revised 15 January 2019, Accepted 1 April 2019, Retrieved May 12 2019, from https://doi.org/10.1016/j.apmrv.2019.04.001