?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The Gambia as one of the LDCs has made so many efforts to industrialize its economy. The Gambia Investment and Export Promotion Agency, GIEPA, was formed to develop Free Zones in selected locations to enable investors to operate in a more macroeconomic friendly environment. Despite all efforts, the Gambia economy suffers from limited availability of foreign exchange, weak agricultural output, a slowdown in their major investment—tourism, high inflation, a huge fiscal deficit, and a huge domestic debt burden. This study identified the determinants of domestic private investment in the Gambia. The study employed the ARDL Co- integration method to analyze a long-run equilibrium model of private investment. Exchange rate, credit to private sector, external debts, Real Interest Rate, Real Exchange Rate, Inflation, among others were identified as exogenous variables. Findings show that high exchange rate increased the real cost of import especially capital goods thereby making investment very costly. Financing of huge debts also inhibited private investment in the Gambia. Aggregate Demand Condition, Real Interest Rate, Real Exchange Rate, Inflation all performed below expectation. Credit to the private sector has not contributed effectively to boost private investment in the Gambia due to insufficient credit. The study therefore suggests an exchange rate policy that will be favorable to reduce cost of imported capital goods. The Gambia should look inward for the supplying of raw materials locally or promote investment in the areas where the required raw materials are available locally as stated by the comparative advantage theory.

Jel:

PUBLIC INTEREST STATEMENT

African economies are referred to as underdeveloped; at times developing, to minimize the inferiority complex when compared with developed economies of the world. The truth is that most African economies have the characteristic of the less developed economy. Such characteristics as low level of investment in the private sector, huge debt when compared to their revenues, high rate of inflation and poverty, are well pronounced in the Gambian economy which this paper studied. For these economies to achieve industrialization, private investment must be improved and stabilized. Findings from this study identified exchange rate as increasing the real cost of capital goods imports thereby making private investment very costly. Debt financing was found to have inhibited investment leaving few investible funds in the domestic economy and that affects the performance of private investors. In the end appropriate recommendations have been forwarded in this paper.

1. Introduction

The Gambia economy falls under the group of the Least Developed Countries (LDCs). The LDCs are the world´s most impoverished and vulnerable countries. They are a group of countries that have been classified by the United Nations as “least developed” in terms of their low gross national income (GNI), weak human assets and high degree of economic vulnerability. Most of the LDCS are located in Sub-Sahara Africa and the Latin America.

One major characteristic of the LDCs is the poor contributions of the private sector to their economies. The private sector in various economies across the globe had been known to contribute more meaningfully to economic growth than the public sector. This can be explained in the direction of lesser corruption in the private sector than in the public sector. (Seruvatu & Jayaraman, Citation2001). The Gambian economy has over the years tried to promote its private sector in many ways. For example, Gambia offers attractive incentive packages to investors under its Gambia Investment Promotion Act.

The UNDP report on the Gambia economy for 2019 also identified some efforts of the Gambia government to promote private investment over the years. As a strategy for promoting industrialization through export, the Gambia Investment and Export Promotion Agency, GIEPA, developed Free Zones in selected locations to enable investors to operate in a more macroeconomic friendly environment. Conditions for this development include transactions in these Free Zones to be denominated in foreign currencies, nationals of Gambia must be employed and trained, at least 70% of output must be exported in foreign markets and the scheme must contribute positively to form domestic productive capital. Gambia also issued Licenses and holders enjoyed incentives. This includes taxes and duties exemption; goods produced within or imported into any of the zones enjoy exemption of customs duty, excise duty and sales taxes; no import duty on capital equipment; no corporate tax or income tax for the first ten years in the case of trading activities in the zones, tax shall be pegged at a rate not exceeding 6% per annum thereafter, a full relieve from municipal tax payment among other incentives. All these were meant to encourage domestic private investment, hence industrialize Gambia (African Economic Outlook, Citation2019).

Despite all these applauded efforts, the Gambian economy faces a limited availability of foreign exchange, weak agricultural output, slowed tourism, high inflation, high fiscal deficit and high domestic debt burden which are detrimental to the growth of private sector investment. The government of the Gambia is making efforts to reverse these economic situations to normalcy. But have the efforts yielded any positive results on the private sector is major question to ask.

A review by the African Economic Outlook (Citation2019) revealed that imports of goods to the Gambia increased significantly from USD 303.81million in 2013 to USD 359.1million in 2014. This was attributed to increase in imports of goods such as sugar, rice, and meat and edible meat offal. Imports increased to USD 347.9 million in 2016. In like manner, imports of services increased from USD 65.3 million to USD 69.4 million in 2014. Total imports of goods and services increased from USD 369.4 million in 2013 to USD 428.5 million in 2014. The result of this was that trade deficit increased from USD 171.7 million (19.1% of GDP) in 2013 to USD 235.6 million (28.6% of GDP) in 2014. Remittances also increased in 2014 to USD 50.1 million (6.1% of GDP) from USD 48.7 million (5.4% of GDP) in 2013. Foreign direct investment (FDI) declined from USD 85.7 million (9.5% of GDP) in 2013 to USD 76.8 million (9.3% of GDP) in 2014. It recorded a debt equivalent to 81.80 percent of the country’s Gross Domestic Product in 2018 and 82.5% in 2019. Gambia’s debt profile also remains a challenge in that it negatively impacts the economy. It crowds out private-sector lending, given that financial institutions invest heavily in the risk-free treasury instruments as opposed to lending to the productive sectors. (African Economic Outlook, Citation2019)

The questions now are, what determines sustainable private investment in the Gambia? And how can Gambia achieve its industrialization objective given these determinants? What role has economic growth rate played in determining private investment in the Gambia? That is can we attribute the poor private investment condition to the slow economic growth rate in the Gambia? This study therefore seeks to identify the major determinants of private sector investment in the Gambia. Based on the Investment theory, some factors which are considered as shift factors in the investment function, such as business outlook of the economy, debt financing, etc., can also play important roles in determining private investment by either stimulate or dampen it. Such factors were included in this study as control variables.

2. Review of literature

Verma and Wilson (Citation2005) explored inter-dependency between private investment sectoral savings and real GDP. They used time series data applying Johansen cointegration approach to examine the long-run relationship and VECM (vector error correction mechanism) to check the short-run dynamics amongst variables. The research concluded that private investment, sectoral savings and gross domestic product (GDP) are positively related. On the basis of empirical consideration, De Gregorio (Citation2009) suggests that in developing countries, private investment is determined mainly by the level of domestic output, real interest rate, public investment, credit available for investment and exchange rate.

Verma (Citation2007) analyzed the endogenous impact of investment. The main objectives of the study were to conduct unit root test which endogenously determines a break in the time senses. ARDL (Autoregressive Distributed Lag) approach was used to analyze long-run relationship and error correction mechanism (ECM) for short-run relationship. The study took each variable as dependent and the rest of the variables as independent and then examined the relationship between them. The analysis concluded that GDP and gross domestic savings have a positive and significant relationship with private investment.

Sajid and Sarfraz (Citation2008) investigated the causal relationship between private investment and exchange rate. Their study used the cointegration technique and vector error correction model to examine causality between investment and exchange rate. Their results showed that there is long run as well as a short run equilibrium relationship between private investment and exchange rate.

Fripong and Marbuah (Citation2010) employed modern time series econometric techniques, the cointegration and error correction techniques using an ARDL model to measure the determinants of private investment. Their study revealed in the short-run, public investment, inflation, real interest rate, openness, real exchange rate and a regime of constitutional rule, are determinants of private investment in Ghana. They noted that in the long-run, private investment is significantly determined by, real output, inflation, external debt, real interest rate, openness and real exchange rate. They suggested a macroeconomic policy regime that will boost private investment.

Karagoz (Citation2010), in his study, aimed to determine the factors which affect private investments in the long-run in Turkey. The study estimated the long-run private investment equation using the bounds test (ARDL) approach to co-integration. Estimated coefficients of their variables showed that in the long-run real GDP, real exchange rate, ratio of private sector credit to GDP, private external debt, inflation, and trade openness have significant impacts on private investments.

Muhammad and Khan (Citation2013) analyzed the factors that play an important role in determining private investment in Pakistan. The econometric tests undertaken supported the view that private sector output, net capital inflows to the private sector, total sources of funds and past capital stock have all been significant determinants of private investment rates in Turkey. According to their findings, changes in the volume of bank credit also have a positive effect. They suggested that if the sector is squeezed for credit then there will be a reduction in the level of private investment with adverse impacts on the productivity of the private sector. This implies there is a “crowding out” effect indicating that most of the physical and financial resources are utilized by public sector, thereby exerting a negative influence on private investment.

Ayeni (Citation2014), investigated the determinants of private investment in Nigeria. The study used the ARDL (Autoregressive Distributed Lag) Cointegration approach to check the existence of a long-run relationship in Nigeria. The result suggested that aggregate demand condition in the economy (GDP), real interest rate, real exchange rate, inflation rate and credit to private sector have not been able to contribute effectively or boost private investment in Nigeria as they all show signs contrary to expectations. However, the study suggested that the government, while improving the macroeconomic conditions conducive to boost investment, should also create a conducive political environment to boost private sector investment.

Abate (Citation2016), conducted a study with the main objective of investigating and analyzing factors that determine domestic private investment in Ethiopia. They used the framework of VAR and VECM using annual data. Their results showed that public investment, real GDP, exchange rate and credit have positive effect on private investment in the long-run. In the short run, they identified exchange rate and inflation as having positive and negative effects respectively on private investment. Hence, to promote the performance of private sector in the country, they recommended measures that can improve real income of people and attract private investment. Such measures as basic infrastructural development, a stable investment environment and macroeconomic and political stability among others.

Bonga and Nyoni (Citation2017) systematically reviewed the determinants of private investment which has been significantly low for the past three decades in Zimbabwe. Their results showed that GDP and public investment are the most powerful factors that affect private investment in Zimbabwe. The study recommended that gross domestic product, public investment, interest rate and other macroeconomic indicators used in the study should be improved upon to have productive effect on the private sector investment.

3. Theoretical framework and model specification

This section draws its argument from the Acceleration theory of investment economics, an article shared online by Nipun (Citation2018). The article discussed two macroeconomic principles, namely the multiplier and the acceleration. The multiplier theory is silent about the effects of induced investment, an investment caused by the growth of national income. When the national output increases, investment is expected to increase. Such investment, which depends on national income or its rate of change, is the argument of induced investment. Nipun (Citation2018)

The Acceleration principle is one principle that explains more the implications of induced investment. It tells more about how total output or income can bring about additional investment spending. Simply put it explains why the increase in national income often results in a more than proportionate increase in investment spending. Also, why the amount of investment in an economy does not depend on the absolute level of business activity but on whether the activity level is increasing or decreasing.

So, if there is a change in the national income or output of an economy, it tends to induce a change in investment. The acceleration there is that a little change in national income or output in such economy will lead to a greater (accelerated) change in investment in the economy. It describes an accelerated effect on investment of a small change in the demand for or output, that is increase in sales of consumer goods in such economy. Moreover, for the purpose of this study, certain variables were introduced to complement the simple acceleration theory following other factors that determine investment or the nature of the response of investment to change in output as argued by Friedman. These factors are:

Lags in Investment: Investment lags behind the change in income. Capital adjustment theory argued that business firms’ reaction to the changes in output may not be instantaneous but follows a partial adjustment process to close the gap between the actual and desired change in capital stock. This is like saying investment model follows an autoregressive scheme. This justifies the use of ARDL model for this study.

Business monetary outlook: This also is in line with Hollis argument. Business outlook has two monetary indicators that show whether a rise in demand is sustainable or temporary. These are the rate of inflation and the exchange rate which has direct link with imported raw materials for the industries. This is why these two variables are included in our model.

Industry Capacity limits: Capacity limits of industries are a direct function of the demand outlook of the economy proxied by the real growth rate.

Inventory Investment: Usually, inventory investment is the investment in stocks of goods that business hold to make out delivery and sales. This varies proportionately with sales and output and can be used as a factor in the simple accelerator model. This is captured by inclusion of the real interest rate variable in this study.

In specifying the model, private investment (PRI) is made a function of seven other explanatory variables identified from theoretical and empirical literature. These variables are to proxy the following macroeconomic conditions: Aggregate demand, competitive condition, liquidity constraint, uncertainty/instability. Data used ranges between 1980 and 2019 base on availability on some variables. Data for this study were sourced from World Bank Indicators 2019. The model is specified explicitly as follows:

The model is specified implicitly as follows:

Where

PINV = Private Investment;

RGDP = Real Gross Domestic Product (proxy for demand conditions in the economy);

GNE = Government expenditure on investment (a proxy for Public investment);

CRPS = Credit to Private Sector (proxy for liquidity constraints);

INFR = Rate of inflation (proxy for macroeconomic uncertainties/instability);

EDT = Average interest on new external debt;

RINT = Real Interest Rate (proxy for User Cost of Capital);

REXR = Real Exchange Rate

4. Empirical findings and discussion

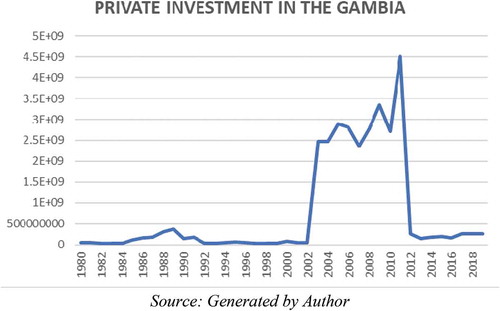

Trend in private investment in the Gambia is shown in Figure . Investment in the private sector seems to be very insignificant in the Gambia economy until 2002 when it started increasing. This steady increase was witnessed between 2002 and 2003 and could not be sustained leading to an oscillatory increase.

Figure 1. Trend in private investment.

Table presents the time series property of the variables in the model for this study. The ADF Unit root test shows that CPRS, EXD, INFR and RINT were all stationary at their levels, while GNE, PINV, REXR and RGDP are all stationary at first difference. Since the variables have a mixed order of integration between I (0) and I (1), this suggests that the condition for Johansen Cointegration technique is not met, hence we resort to the ARDL, Bound Test Cointegration Technique to test for the long equilibrium in the model.

Table 1. Theoretical A-priori expectations

Table 2. Unit root test (level and first difference)

The technique involves first estimating the model using ARDL and testing for the existence of cointegration among the variables. The result of the Bound Cointegration test is reported in Table . From Table , the F-statistic that the joint null hypothesis of lagged level variables (i.e. variable addition test) of the coefficients is zero is rejected at the 5% significance level. Further, since the calculated F-statistic (5.1311), exceeds the upper bound of the critical value bound at 1% (4.26) the null hypothesis of no cointegration (i.e. long-run relationship) in the private investment model is rejected indicating the existence of a long-run equilibrium relationship in the model. The short-run dynamicsor cointegrating equation and the long-run equation are presented in Tables and respectively.

Table 3. ARDL Bound Cointegration Test

Table 4. Results of the Short-Run ARDL (1, 2, 0, 3, 1, 1, 2, 1) model of private investment in the Gambia

Table 5. Results of the long-run ARDL (1, 2, 0, 3, 1, 1, 2, 1) model of private investment in the Gambia

The short-run dynamics in Table is interpreted in two dimensions. First is the error correction mechanism or cointegrating coefficient. It is negative (−1.085383) and highly significant considering the probability value (0.0006). This negative value implies that the endogenous variable, Private Investment in the Gambia, is truly deficient and in disequilibrium, the set of the exogenous variables is trying to correct the disequilibrium over time. The adjustment is towards the right direction to restore equilibrium in Private Investment over time. The speed of the adjustment is captured by the magnitude of the ECM coefficient (1.085383). This implies about 10.8% only of the disequilibrium in private investment was restored in the short-run. This is a very slow speed of adjustment.

The second interpretation of Table is the short-run marginal impact of individual variables based on expected a priori assumptions. A look at the probability values of the variables shows that all are significant except Real GDP coefficient. In the short-run real interest rate and inflation rate exert negative effects on private investment in the Gambia economy. Theories suggest that when inflation rate is high, private investment is negatively affected, that is it falls. As regard to real interest rate two schools of thought tried to explain the relationship with private investment. The neoclassical investment model treats real interest rate as a component of user cost of capital, therefore if affects private investment negatively. Another argument is that when real interest rate is high, flow of bank credits increases as people want to save more, this tends to complement private sector savings and increase investment.

A negative coefficient of real interest rate witnessed in the Gambia implies user cost of capital effect. It is expected that RGDP exerts a positive effect on private investment. The effect of real GDP on private investment in the short-run, even though positive, is not significant in the Gambia economy. Real exchange rate affects private investment positively in the short run. Theoretically, the real exchange rate can influence the level of private-sector investment either positively or negatively. Negatively as it is one of the components that determines the real cost of imports. When a currency is devalued, real cost of purchasing imported capital goods tends to increase, this reduces profitability in the private sector and a fall in investment resorts. Conversely, real currency devaluation can have a positive impact on investment in sectors producing internationally traded goods, as it increases competitiveness and export volumes. Thus, the effect of real exchange rate on private investment in the Gambia is one of increasing the cost of imported capital goods, thereby reducing profitability and discouraging private investment. The short-run effect of credit to private sector is also positive. Increasing credit by the banking sector to the private sector is likely to boost private sector investment.

The effect of government national expenditure on investment on public investment is positive and significant in the short-run. There are different school of thoughts on the relationship between public and private investment. One postulates that public investment can crowd-out private investment if deficits and interest rates are high (i.e. the Ricardian Equivalence Theorem) and there is competition for certain scarce resources (e.g. skilled labor, raw materials, etc.). The other postulates that public investment can serve as a catalyst to private investment through external economies, like the provision of infrastructure (e.g. transport, communication, irrigation projects, etc.). In the Gambia economy, public investment is acting as a crowding-in catalyst to private investment.

The effect of external debt financing on private investment seems to be positive in the short-run but this could not be sustained as it is negative in the long-run.

The existence of huge debt and financing of such may inhibit investment in many indebted countries because the possibility that confiscatory future taxation could be used to finance future debt service, which leaves few investible funds in the domestic economy and may affect the behavior of private investors. A look at the R2 shows that about 86% of the variations in private investment are jointly explained by changes in the set of determining variables in the short-run.

Table presents the long-run ARDL model of Private investment in the Gambia. All variables are significant except inflation rate and external debt. Real GDP exerts a significant negative effect on private investment, contrary to the prior expectation. Real exchange rate exerts a negative effect on private investment in the long-run meaning that it plays the role of increasing the user cost of capital. Real interest rate was negative in the short-run but positive in the long run. A higher real interest rate increases the flow of bank credits, which complements the private sector savings and facilitates private capital formation and hence private investment. Effect of inflation rate on private investment is not significant in the long-run. Credit to private sector maintains its positive effect in the long-run. However, the effect of external debt is negative in the long run as expected, while government expenditure on investment exerts a positive effect on private investment in the long-run.

5. Conclusion

This paper identified what determines sustainable private investment in the Gambia. A major question is whether the poor private investment in the country can be attributed to the slow economic growth rate in the country. Findings revealed that exchange rate, among others, as increasing the cost of import of capital into the country. This high cost of production makes investment very costly thereby discouraging private investment in the Gambia. Other factors that have slowed private investment down in the Gambia are the huge debt and the financing of such. Credit to private sector is low and has not been able to contribute effectively to boost investment in the sector. The study can therefore conclude that exchange rate and the low credit to private sector are the two major factors that have hindered private sector investment in the Gambia.

5.1. Recommendations

A new Cabinet paper on the Gambia’s National Investment Policy (2019–2024) to promote industrialization and value addition was recently instituted in the Gambia. The aim is to promote and facilitate investment so as to grow the economy. It also aimed to create gainful employment for its labor population. The policy, among other things, is aimed at diversifying export in the Gambia economy and open up Gambia to foreign markets. Public investment and infrastructural development were all targeted in the proposed policy to bring about industrialization of the Gambia.

For Gambia to achieve this feat in industrialization especially through private investment, some key macroeconomic indicators must be taken care of. Findings from this study identified the exchange rate as increasing the real cost import especially capital goods thereby making investment very costly. An exchange rate policy that will be favorable to reduce cost of imported capital goods must be put in place. In the alternative, Gambia can look inward to supplying raw materials locally or promote investment in the areas where the required raw materials are available locally. The existence of huge debt and financing of such in the Gambia has inhibited investment in many indebted countries because of the possibility that confiscatory future taxation could be used to finance future debt service, which leaves few investible funds in the domestic economy and may affect the behavior of private investors. Gambia government must first pursue debt restructuring of cancellation before their goal to promote industrialization through private investment can be achieved. High inflation rate credit to private sector by banks in the Gambia played important role in promoting few manufacturing firms in the Gambia because there are few banks in the Gambia. Unfortunately, government spending on public investment has been insignificant to allow private investment to enjoy economies of scale. Government of the Gambia should spend more on infrastructural development that will attract private investors into the economy.

Additional information

Funding

Notes on contributors

Raphael Kolade Ayeni

Raphael Kolade Ayeni has his First Degree in Agric. Economics from the University of Ibadan, Nigeria, Master’s Degree in Economics, and his PhD in Economics both from University of Ado Ekiti, Nigeria (now Ekiti State University). He was a teacher both at high school and College of Education for 10 years. Moreover, he has been lecturing at Undergraduate and Graduate programs at Ekiti State University, Ado Ekiti for the last 16 years. He had also served as head of department in the same University. He is currently on national assignment in the University of Gambia, under the Technical Aid Corps as an Associate Professor in Economics. He has published more than thirty articles in both national and international journals. He has also organized workshops and conferences on Research and Econometrics for both graduate students and Bureau of Statistics worker in the Gambia.

References

- Abate, Y. (2016). Determinants of domestic private investment in Ethiopia during 1971 to 2014: An empirical analysis. The International Journal Research Publication, 5(9), 86–11.

- African Economic Outlook. (2019). African Development Bank.

- Ayeni, R. K. (2014). Macroeconomic determinants of private sector investment - An ARDL approach: Evidence from Nigeria. Global Advanced Research Journal of Management and Business Studies, 3(2), 82–89. http://garj.org/garjmbs/index.htm

- Bonga, W. G., & Nyoni, T. (2017). An empirical analysis of the determinant of private investment in Zimbabwe. Dynamic Research Journals: Journal of Economic and Finance (DR-JEF), 2(4), 25–84.

- De Gregorio, J. (2009, June 4th). Global confidence crisis – The value of waiting and the coordination failure revisited. Keynote speech, Governor. Central Bank of Chile.

- Fripong, J. M., & Marbuah, G. (2010). The determinant of private sector investment in Ghana: An ARDL approach. European Journal of Social Sciences, 15(2), 250–261.

- Karagoz, K. (2010). Determining factors of private investments: An empirical analysis for Turkey. Sosyoekonomi Journal, Sosyoekonomi Society, (1).

- Muhammad, T. M., & Khan, S. (2013). The determinants of private investment and the relationship between public and private investment in Pakistan (Paper No. 49301). Retrieved August 26, 2013, from. 17:18 UTC. https://mpra.ub.uni-muenchen.de/49301/MPRA

- Nipun, S. (2018). Acceleration theory of investment economics. https://www.economicsdiscussion.net/investment/acceleration-theory-of-investment-economics/26064

- Sajid, G. M., & Sarfraz, M. (2008). Saving and economic growth in Pakistan: An issue of causality. Pakistan Economic and Social Review, 46(1), 17–36.

- Seruvatu, E., & Jayaraman, T. K. (2001). Determinants of private investment in Fiji. Working Paper, 2001/02. Economics Department, Reserve Bank of Fiji, 1–39.

- Verma, R. (2007). Savings, investment and growth in India: An application of ARDL bound testing approach. South Asia Economic Journal, 8(1), 87–98. https://doi.org/10.1177/139156140600800105

- Verma, R., & Wilson, E. J. (2005), A multivariate analysis of saving, investment and growth in India. Economic Working Papers, 05-24. University of Wollongong Research Online, 1–23.