?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the role of economic policy uncertainty (EPU) in influencing firm performance and leverage as a form of financing decisions, in the presence of herding in the emerging markets of Brazil, Russia, India, China and South Africa (BRICS). This study contributes to our understanding of how businesses in emerging markets make financial decisions during uncertain times as well as the role of policy development in influencing firm performance and corporate decisions. The increase or decrease in EPU is determined by the way policymakers or investors act and the consequences of their decisions. EPU is, in fact, a market characteristic that brings changes in prices and returns. Therefore, investors and policymakers should be aware of it to prevent any negative effects. A steady and predictable economic policy is critical to economic growth. We investigate how firms rationalise making leverage financing decisions during times of economic policy uncertainty and if so, if herding is present in these decisions. Our data spans the Top 80 listed firms in each respective country from the beginning of June 2002 to the end of June 2017. Russian, Indian and South African results show that EPU is significant in determining leverage financing decisions and that an increase in EPU leads to herding in such decisions. We find contrary results in Brazilian and Chinese firms. Our results imply that when leverage decisions are made, both the political climate as well as competitor movement data must be considered in determining a firm’s “ideal” capital structure.

PUBLIC INTEREST STATEMENT

Governments in emerging countries (BRICS) often generate economic policies, regulations, and laws that guide the direction of listed and unlisted firms in those countries. During times of disagreements on economic policies among policy makers, the degree of uncertainty among listed firms may further be amplified. It is normal to then see firms change the operation of their businesses, how they finance their businesses and how firms in similar industries imitate what lead firms are doing. Economic policy uncertainty has an impact on business and affects the profit for many firms, which together may lead to economic activity slowdown. Our results imply that when debt decisions are made in firms, both the political climate as well as competitor movement data must be considered in determining a firm’s “ideal” capital structure.

1. Introduction

Governments tend to initiate and implement economic policies, regulations, and laws that guide the directions of firms. BRICS listed firms such as Ambev, Sberbank, Reliance, PetroChina and Anheuser-Busch InBev respond by changing the operations of their businesses when governments change or modify these economic policies, regulations and laws. This is done in order to maintain a strong and healthy economy by adapting to the changes that have been made to work in the firm’s favour. Zhang et al. (Citation2015) state that due to the way policy decisions are made and the implementation process, economic policies typically cause a large extent of uncertainty, which could impose insightful impacts on the financial market and companies’ behaviours such as understating or overstating a decision that has been made. Cao et al. (Citation2013) concur with Zhang et al. (Citation2015) that policy uncertainty in business environments is caused by the time taken to implement new policies.

Uncertainty is an equivocal yet broad notion, which tends to be in the minds of a diverse group of people such as clients, company executives and policymakers, about possible future outlooks. Bloom (Citation2014) addressed questions about economic uncertainty and found that increments in uncertainty are both an instinct emerging from terrible news shocks that begin and amplify recessions by rising further as growth slows down. The author further states that during periods when policy makers have disagreements on economic policies, the degree of uncertainty may be greater than before (Bloom, Citation2014).

There are three factors that motivate the research undertaken in this study. First, there is a lack of research on the role of politics on firm capital structure decisions in emerging markets. Second, there is a lack of research about corporate decisions in relation to herding in emerging markets due to policy uncertainty; and third, there is no published study that has been done that scrutinises a combination of capital structure, politics and herding in emerging markets. This study will contribute to sharing new knowledge with other researchers in different and relevant fields; and will further determine other relationships that link with policy uncertainty in emerging markets. It is argued that while literature on policy uncertainty and capital structure exists in developed markets, much literature has not been published widely in the area of policy effects, capital structure and herding behaviour in emerging markets.

The terms policy uncertainty, political uncertainty and economic policy uncertainty are used interchangeably in the subsequent literature. Uncertainty in all the three terms may refer to the economic risk, investing, government policy, tax, regulatory regime or uncertainty over electoral outcomes that may affect the economy in a positive or negative way.Footnote1

It is common that large firms are not wrong about the rational or irrational capital structure decisions that they make and thus make it easier for smaller firms that have less experience to mimic their decisions. Cao et al. (Citation2013) show that in making financial decisions, firms that are less exposed to political risk and have low access to public debt markets, are less sensitive to fluctuations in political uncertainty. Leary and Roberts (Citation2014) found that firms make capital structure decisions by reacting to the capital structure decisions of other firms, as opposed to variations in firm-specific determinants. The authors further conclude that there is existing evidence suggesting that herding behaviour matters for capital structure decisions.

This study examines the role of EPU in influencing firm performance and leverage as a form of financing decision, as well as the effect of herding in these emerging markets, particularly Brazil, Russia, India, China and South Africa (BRICS). While literature on political uncertainty and capital structure exists in developed markets (which will be discussed in the literature review), this study aims to bring in emerging markets and link herding towards capital structure decisions in the presence of policy uncertainty. This argument points more towards EPU impacting leverage, which in turn will minimise the effect of herding. While past capital structure research focused on both leverage and equity, this study will focus more on leverage. It is believed that emerging markets look more towards leverage financing as it may be cheaper than equity and more convenient to undertake. The term capital structure will thus be used because of past literature being explained and to explain the different financing decisions.

An investigation of the effect of policy uncertainty in capital structure together with herding may provide twofold benefits. First, benefits will accrue to the body of knowledge about the role of economic policy in influencing firm performance and corporate decisions in emerging markets. The results of this study may assist to see how the BRICS countries will behave in the presence of herding and policy uncertainty in the future when they are forecasted to be the leading emerging group of the world.

Secondly, benefits will also accrue to firms and policy makers. Firm leaders may want to know how policy uncertainty influences the majority of corporate decisions, forecasts and the mechanisms of herding in order to understand and make positive appropriate capital structure decisions. The knowledge on policy uncertainty may benefit emerging markets as a whole in the quest to improve the quality of corporate information and timing of decision making to better meet the needs of the economy and policy makers.

1.1. Hypotheses testing

Our primary and secondary hypotheses are thus set as follows:

Primary Hypothesis

H0: There is no significant relation with economic policy uncertainty being a factor in determining firm leverage financing decisions.

H1: There is a significant relation with economic policy uncertainty being a factor in determining firm leverage financing decisions.

Secondary Hypothesis

H0: There is no significant relation with less economic policy uncertainty leading to little or no herding towards firm leverage financing decisions.

H1: There is a significant relation with more economic policy uncertainty leading to herding towards firm leverage financing decisions.

We will measure policy-related economic uncertainty for all the BRICS countries using an index developed by Baker et al. (Citation2016) based on frequency counts of newspaper articles. Similar to the EPU index developed for the USA, the same methodology applies to the BRICS countries according to individual country newspaper coverage. The effect of herding will be tested to determine how it impacts the outcome of the leverage equation (see methodology) with and without the inclusion of EPU.

This study is organised as follows. Section 2 reviews the literature. Section 3 presents the methodology which is employed in the study, along with the data and the sampling selection of the data. Section 4 details the results, and Section 5 concludes.

2. Literature review

2.1. A review of capital structure literature

Modigliani and Miller (Citation1958) created the capital structure irrelevancy theorem which suggests that valuating a firm is not an important factor in the way a company makes financing decisions in terms of debt and equity. The authors developed a theory that helps us understand how taxes and financial distress affect a firm’s financing decision. They wrote two propositions under the assumption of no taxes where the first proposition (capital structure irrelevance) states that a firm’s market value is not affected by capital structure choice. The second proposition (higher financial leverage) states that financial leverage is directly proportional to the cost of equity. When taxes are introduced, the value of the firm is improved by the tax shield, referred to as the trade-off theory of leverage (Modigliani & Miller, Citation1958). This proposition states that the actual cost of debt is less than the nominal cost of debt because of tax benefits. The trade-off theory supports the notion that a company can finance its assets with debt, as long as the cost of financial distress exceeds the value of tax benefits. Subsequent models of capital structure have been introduced based on the Modigliani-Miller propositions.

2.2. Performance of peer firms

Peer firms play a pivotal part in forming various corporate policies, and the conduct of peer firms may matter for capital structure. Ongoing empirical work demonstrates that a financially critical determinant of a firm’s capital structure average is the leverage ratios based on the industry (Leary & Roberts, Citation2014). The authors’ objective is to distinguish how, and why peer firm conduct matters for capital structure. Managers think about the financing choices and qualities of companion firms as instructive for their own financing choices. For instance, when peers of a firm raise their leverage ratios, it is often higher than it usually would have been had peer data not been available (Leary & Roberts, Citation2014). In like manner, the authors note that firms may think about the development prospects or financial wellbeing of their peers in deciding their own capital structure. In this way, peer firms’ impacts on capital structure happen when the activities or qualities of associate firms unequivocally enter a company’s financing target work (Leary & Roberts, Citation2014).

Leary and Roberts (Citation2014) state that any connection between an organisation’s financial strategies and the activities or qualities of their companions can be attributed to two reasons. The primary reason depends on the endogenous determination of firms into peer groups or an “overlooked basic factor”. This determination brings about firms from a similar peer group confronting comparable institutional situations and having comparable attributes, for example, generational legacies and investment opportunities. Leary and Roberts (Citation2014) state that the second reason is that organisations’ financial strategies are somewhat determined by a reaction to their peers. This reaction can work through two channels: activities or attributes. The first emerges when firms react to financial policies of peer firms. The second emerges when firms react to changes in the attributes of their companions such as profitability and risk (Leary & Roberts, Citation2014).

The authors’ results demonstrate that capital structures are essentially affected by their peers. Leverage is unequivocally adversely identified with equity shocks from peer firms. Deciding to issue debt and equity, respectively, comes with a negative and a positive relationship with respect to equity shocks from peer firms (Leary & Roberts, Citation2014). These findings are robust to a large group of estimation and endogeneity concerns.

Zeckhauser et al. (Citation1991) propose that managers that free-ride in information attainment or relative performance assessment may prompt herding behaviour in capital structure decisions. The authors remark that when a firm’s own signal is noticeable and optimisation is exorbitantly costly or tedious to implement, managers may sanely put more weight on the choices of others than trusting their own information. This is particularly likely when different firms (managers) in the business are seen as having more skill.

The authors’ results demonstrate that smaller market share; non-dividend paying and unrated firms in terms of debt are more sensitive to their peers’ actions than are their counterparts. These findings propose that herding behaviour is most grounded among those firms with the best learning thought processes and perhaps the best need to increase reputation (Leary & Roberts, Citation2014).

2.3. Policy uncertainty and capital structure

Capital structure is an important concept when thinking about companies’ injection of funds or diversification of investments. Investing equity or debt capital into domestic or international companies can influence not only the profitability of the company, but also if the company survives the adversities of the economy, such as a recession. Even though previous studies have found a negative influence of political uncertainty on corporate investment decisions, Cao et al. (Citation2013) are adamant that there is still a limited understanding of how political uncertainty affects a company’s financing decisions.

In addition to the above results, Cao et al. (Citation2013) also study the relationship of political uncertainty and firms’ access to open debt markets and find that intertemporal capital structure changes are less delicate to political uncertainty for firms who can access open debt markets (Cao et al., Citation2013). The author’s remark that this is in line with Faulkender and Petersen (Citation2006), where firms without access to open debt markets will probably be fiscally guarded (Cao et al., Citation2013). They explain that the financial frictions are additionally reinforced by the firms’ cash-holding choices in response to changes in the level of political uncertainty (Cao et al., Citation2013). If increasing money-related frictions caused by high political uncertainty is the hidden driver for firms’ financing choices, the authors see an expansion in cash holdings by the firm as a buffer against monetary resistances during times of moderately high political uncertainty (Cao et al., Citation2013). They thus find a substantial and positive connection between political uncertainty and cash holdings, recommending that directors build up cash reserves possessions to alleviate the external financial imperatives produced by political uncertainty (Cao et al., Citation2013).

Zhang et al. (Citation2015) show that due to policy decision-making and execution processes, economic strategies commonly produce a high degree of uncertainty, which could force significant effects on the market and firm practices. They note that political uncertainty has a supply and demand aspect. The fundamental premise behind the supply curve is that uncertainty in economic policies will weaken the external financing condition (Zhang et al., Citation2015). At the point when EPU increases, the information asymmetry amongst borrowers and banks would turn out to be extreme and temporary, as firms’ future income would be more unstable, leading to a higher default probability (Zhang et al., Citation2015). Both effects can prompt higher external financing expenses, and firms looking for financial flexibility would, for the most part, bring down their leverage ratios. In support of this idea, Zhang et al. (Citation2015) argue that experimental investigations on the USA money-related market show that the risk premium of municipal bonds is increased by EPU (Gao and Qi, Citation2012). They also argue that EPU decreases the average leverage ratio of firms (Cao et al., Citation2013), and forces extra costs and more stringent non-value terms on bank credit contracts at both total and firm level. In contrast, the demand effect refers to when firms decrease the demand of financing in face of increasing EPU (Zhang et al., Citation2015). Earlier research shows that when firms face high policy uncertainty, they will be more preservationist in settling on investment choices (Bernanke, Citation1983) and bring down their investment level (Gulen & Ion, Citation2016). The two effects create a negative relationship between EPU and firms’ capital structure; however, it is hard to quantify the impact. Zhang et al. (Citation2015) select Chinese-listed firms to test the above hypotheses. The authors see it essential to test whether the hypothesised relationship between EPU and capital structure choices holds in this emerging market or not (Zhang et al., Citation2015). They find that on average, the leverage ratio is negatively related with EPU and this negative impact is more noteworthy for firms from sectors with higher capitalisation, are non-state claimed, or have no earlier banking relationship. Further, they provide evidence that the negative relationship between capital structure and EPU is sourced from the weakening of outside financing conditions caused by EPU (Zhang et al., Citation2015). Lastly, Zhang et al. (Citation2015) demonstrate that firms’ utilisation of credit is positively identified with EPU, implying that firms have a tendency to change their financing structure as a reaction to the uncertainty of economic policy. The findings from Zhang et al. (Citation2015) add to the literature in various ways. To begin with, the authors provide an “out-of-sample” test on the relationship between EPU and firm capital structure decisions, and additionally shed light on this subject by demonstrating that Chinese firms have a tendency to change their financing choices amongst debt and credit during times of EPU (Zhang et al., Citation2015). Tran (Citation2019) shows that cultural characteristics impact the risk-seeking behaviour of corporates across countries. The author finds that EPU is negatively related to corporate risk-seeking behaviour and that cultural effects impact this finding. In particular, cultures that are individualistic in nature weaken risk-seeking behaviour, whereas cultures with a tendency to avoid uncertainty make this effect stronger. This is quite an interesting finding in relation to the scope of our study, as apart from legal systems, it can be inferred that the BRICS countries’ differing cultures would also be a factor in our interpreting our results. Khan et al. (Citation2020) examine EPU on US firms during the period of 1985 to 2017. They find that EPU negatively impacts the speed of capital structure adjustment. They further find asymmetry—EPU is more pronounced for under-levered firms.

2.4. Measuring EPU

Zhang et al. (Citation2015) study the effect of EPU on capital structure decisions in China using the policy uncertainty index developed by Baker et al. (Citation2016). Baker et al. (Citation2016) developed this index because of occurrences that intensified concerns regarding policy uncertainty such as, the Eurozone crises, the global financial crisis and policy disputes in the USA that were biased. The authors believed that policy uncertainty caused such crises in different parts of the world and hence wanted to prove that by measuring the EPU. The reports from Federal open market committee (Citation2009) and International Monetary Fund (Citation2012b, Citation2013) concur with Baker et al. (Citation2016). The reports suggest that uncertainty in the fiscal, monetary and regulatory policies of the USA and European countries contributed to a steep economic decline between 2008 and 2009 as well as the slow recoveries subsequently (Baker et al., Citation2016).

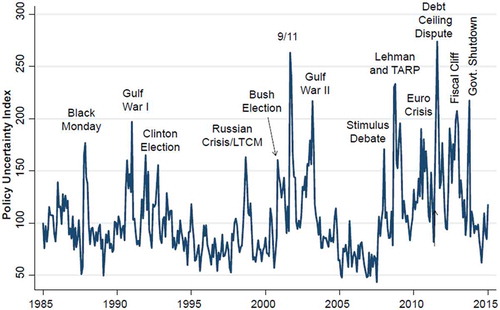

In order to measure EPU, the authors constructed this index by building three types of elements and then aggregated them to obtain the index displayed in Figure . The first element includes monthly data, information and news articles from media coverage of policy uncertainty, predominantly from 10 largest newspapers of that specific country, containing “uncertain” or “uncertainty”, “economic” or “economy”, and (or) policy-relevant terms (Baker et al., Citation2016). Baker et al. (Citation2016) state that the raw monthly count of articles that meet the search criteria is scaled by the number of articles in the same paper enclosing the word “today” (Baker et al., Citation2016). From these papers, a normalised index is then created inclusive of all monthly news articles conversing about EPU. Baker et al. (Citation2016) state that the more news articles there are about EPU, the more a higher level of EPU concerning households and businesses is reflected.

Figure 1. Index of Economic Policy Uncertainty for the USA, 1985 to 2014.

The second element reflects the list of tax code provisions set to expire over the next 10 years. Baker et al. (Citation2016) find that most of these provisions encompass “temporary” tax measures that generate a level of uncertainty for businesses and households, as the provisions often get rapidly reformed or prolonged after a political battle. Using data on the projected revenue impact of the scheduled expirations, found in the annual reports produced by the Congressional Budget Office (CBO), the authors constructed a discounted sum of dollar-weighted future tax code expirations (Baker et al., Citation2016). This index gives the direction that the tax codes will take in the future as a measure of the level of uncertainty and has become an essential source of uncertainty for businesses and households.

The third element of the policy-related uncertainty index contains differences among economic forecasters about inflation and government expenditures. Indices of uncertainty about policy-related macroeconomic variables are constructed by using the differences between professional forecasters’ predictions about where the levels of the Consumer Price Index, Government Expenditures, and State and Local Expenditures will be in the future. Baker et al. (Citation2016) used data from the Federal Reserve Bank of Philadelphia, which surveyed approximately fifty professional analysts. They found that differences of opinion are shown by larger forecast differences, which suggests more confusion about future developments (Baker et al., Citation2016). On the contrary, smaller forecast differences indicate less uncertainty.

Baker et al. (Citation2016, p. 5) state that

“Specifically, we compute the interquartile range of four-quarter-ahead forecasts of federal government purchases of goods and services, scaled by the median four-quarter ahead forecast of the same quantity. We then multiply by a 5-year backward-looking moving average for the ratio of nominal federal purchases to nominal GDP. These steps yield a sub-index of forecaster disagreement about federal government purchases. After obtaining an analogous sub-index of disagreement for state and local purchases, we sum the two sub-indexes, weighting by the relative size of their purchases”.

In order to obtain an index of EPU, all the three elements are aggregated, giving a 50% weight to the news-based element, as it is the most extensive measure amongst all three elements. Equal weights are then given to the scheduled tax code expiration element and the economic forecasters’ disagreement element. However, it was agreed upon that the news-based approach to measuring uncertainty comes with its flexibility to quantify the extent to which policy-related uncertainty accounts for overall economic uncertainty (Baker et al., Citation2016). Therefore, an index of EPU based on newspaper coverage frequency is developed for the USA (Baker et al., Citation2016) and the same has applied for each of the BRICS countries found on the website www.policyuncertainty.com.

South African data were not available on the website www.policyuncertainty.com and an alternative similar index from Brogaard and Detzel (Citation2015) was used for South Africa in this study. Brogaard and Detzel (Citation2015) tested how EPU impacts asset prices and created an index similar to that of Baker et al. (Citation2016) using the Access World News database. The sample consisted of 21 countries based on having a stock market with a market capitalisation of more than 500 USD billion at the beginning of 2011. Brogaard and Detzel (Citation2015) used similar keyword search as the Baker et al. (Citation2016) paper but extended it to international scenery. The measure that was used also focuses only on the news component due to data availability issues of the other two components of the Baker et al. (Citation2016) measure (Brogaard & Detzel, Citation2015). The frequency of country-related EPU is then normalised by the total number of articles about South Africa each month.

During times of uncertainty, it is observed by many studies that investors tend to mimic the actions of other investors. This herding behaviour, can also however, be observed in the decisions taken by managers of firms, as discussed below.

2.5. A review of herding literature

Zeckhauser et al. (Citation1991) analysed the yearly ratios of debt to equity for 200 largest firms over a time period of 20 years. Over that time frame, there was a constant general increase in the debt-equity ratios through extensive heterogeneity across industries and firms. This example may be explained by a cost-of-modification model—if returns from the movement are linear, the expenses of adjustment increase, and if the parameters are steady for the period under study, at that point each firm would modify a settled sum for each period paying little attention to the behaviour of different firms (Patel et al., 1991).

The authors’ capital structure herding migration model offers a different explanation with additional relationships of why firms herd. Assume, for the period studied, that there is a linear per unit advantage from moving the debt-equity ratio towards its ideal value, however there is a quadratic disadvantage for deviations from the group (the satisfaction of herding is linear, whereas the dissatisfaction of not herding is greater (quadratic)). Under this scenario, Patel et al. (1991) suggest that the company’s optimal ratio will be a weighting of its very own past ratio in addition to the industries expected (future) ratio. The average firm’s ratio is substituted by its lagged value; as its contemporaneous value may show a positive relationship as a result of the regular shocks that impact the market estimation of equity across firms in an industry (Patel et al., 1991). The authors say that a herd migration trend is shown by a significant positive sign on the industry ratio. The authors found that for 3 of the 10 industries that were studied, less than 15% of the firms shows such tendencies significantly (Patel et al., 1991). Brendea and Pop (Citation2019) examine herding behaviour in the Romanian market and find that firms herd to the mean debt ratio within industries, often at the detriment of moving away from their individual capital structures. Romanian firm’s capital structure is thus determined not just by firm-specific characteristics, but also those of the industry they are in.

2.6. Summary

Two capital structure models have gained prominence in the literature - a static trade-off framework and the pecking order framework. After explaining all aspects of the static trade-off and pecking-order theories, it was found that investors seem to be content with static trade-off theory as it yields the best internal debt ratio. It has been shown that when investors become uncertain about the market, share prices are lower and that following a high economic uncertainty period, share prices plummet. This explains that policy uncertainty can have long-term effects on investment level.

The literature review is consistent with the understanding of political elections being likely to discourage foreign investment due to policy uncertainty, creating uncertainty about the stable exchange rate policy and making incentives around fixed currency regimes. Policy uncertainty affects the way a firm is financed. The literature review shows that during periods of increased policy uncertainty, under-leveraged firms are more likely to maintain low debt ratios for lengthy periods and that investor herding behaviour exists in both developed and developing countries. The EPU index is used to measure EPU by building three types of elements and then aggregated them to obtain the index. Emerging markets such as the BRICS countries also are affected by policy uncertainty. These are among the largest countries on their continents and may possibly best epitomise the priorities and apprehensions of their regions. Below is the theoretical framework diagram that differentiates the existence of EPU. In the presence of EPU, there is often a tendency for firms to cluster together in their decisions. The left-hand side panel of Figure shows that when EPU is considered, the decision to raise additional debt or additional equity is not consistent across firms. In contrast, when EPU is not considered, one would expect firms to decide on their optimal capital structure independent of any external factors.

Figure 2. A firm’s capital structure with and without uncertainty.

3. Data and methodology

3.1. Data

The sample firms are selected based on Top 80 listed firms by market capitalisation, as of June 2017, in their respective country stock exchanges. A total of 370 firms will be sampled over a period of 15 years from the beginning of June 2002, the year after the five countries were noted to be emerging at a faster rate than others, to the end of June 2017. Russia’s available and accessible listed firm information on both the MOEX website and Bloomberg is limited to the Top 50 firms. These firms will be split into two sub-groups of the first 40 listed firms and the next 40 listed firms, however, in the case of Russia it will be first 25 listed firms and the next 25 listed firms. This is achieved by including a dummy variable in the regression, which will be discussed later.

Performance at the beginning of the period is determined to be different to the end of the sample period because of the variability of factors such as economic policy uncertainty, financial incidents and listing at various points. The Top 80 firms are chosen consequently by way of mitigating the industry sector biasness found in fewer firms chosen. A total of 370 firms were sampled over a period of 15 years from the beginning of June 2002, the year after the five countries were noted to be emerging at a faster rate than others, to the end of June 2017. The sample period is suited for data availability on all the five stock exchanges.

The annual financial statements of the BRICS-listed companies are used to examine the effect of economic policy uncertainty on leverage financing decisions. The financial statement information is sourced from Bloomberg and annual data are used to discover more time-series variations, as per Leary and Roberts (Citation2014). All the monthly closing share data (including dividends) are obtained from the I-Net Bridge database, Global Financial Data and Bloomberg; accounting data are sourced from both Bloomberg and the McGregor Bureau of Financial Analysis database; and the EPU index from Baker et al. (Citation2016), available at www.policyuncertainty.com as well as Brogaard and Detzel (Citation2015). The interested reader is directed to these articles for details on each country’s EPU.

Based on previous studies on capital structure, financial industry firms that are specially regulated will be excluded as they usually have high leverage ratios. Special treatment or particular transfer firms which are observed due to their reduced operating performances, according to their exchanges that they are listed on, will also be excluded. Firms that are listed and delisted during the sample period will be accounted for their listed period on the exchange, that is, if a firm was listed at the start of the study period and delisted in the middle, this implies that the return will be 0% after delisting. The same goes for firms that were listed in the middle of the period, their returns at the beginning of the study period will be 0%. Moreover, dual-listed firms will be excluded from the sample as they create a reasonable amount of clutter in analysing results. In this case, there are two dual-listed companies in all five countries. Glencore is dual-listed on both the JSE and HKSE, while United Company RUSAL is dual listed on HKSE and MOEX.

Each country will have its own monthly risk-free rates obtained as the 91-day Treasury Bill Rates from Bloomberg. To achieve the objective of this study, regressions will be run on eViews using the dynamic Generalised Method of Moments (GMM) model. Percentage changes in the variables will be used in the regressions while levels of variables will be used as a robustness check.

3.2. Testing for economic policy uncertainty (EPU) and leverage

3.2.1. Measuring leverage

In line with Zhang et al. (Citation2015), the same index incorporating data for each relevant country will be used in Brazil, Russia, India and South Africa. The sample will be split into top half and bottom half of each country’s Top 80 (50), based on the market capitalisation of the firms. Zhang et al. (Citation2015) show the impact of EPU on capital structure by using the following empirical model:

Where Leverage is the monthly book leverage ratio, defined as total debt to total assets, and the indices i and t correspond to firm and month, respectively. EPU represents the economic policy uncertainty index where the optimal lag can be empirically tested. The EPU index of Baker et al. (Citation2016) is monthly based, thus EPU will be annualised and changes in EPU will be used in this equation as opposed to levels.

X presents a set of control variables such as firm size, firm age, profitability, sales growth rate (∆Sales) and tangibility. The month fixed effect (which refers to the month of the firm’s financial year end (FYE)) and industry fixed effect are included in the model to control for overall macroeconomic factors over time, seasonality in corporate financing decisions and industry characteristics. Lastly, ε is the error term.

Total debt can be split into short-term debt plus long-term debt using the following model:

Where DT is the total debt that is split into DS and DL, which is the short-term debt and the long-term debt respectively. AT is denoted as the total assets.

Then the short-term and long-term debt values are calculated as follows:

3.3. Testing for herding

Herding behaviour is seen as the difference between the firm’s debt ratio and industry’s debt ratio (as per Welch, Citation2002),

where is the difference between industry debt ratio (

) and firm debt ratio (

) and is a herding parameter that changes over time,

. When

, then

which means that there is no herding. When

, it suggests the perfect herding towards the industry debt ratio in the sense that all the firm debt ratios move in the same direction and with the same magnitude as the industry debt ratio. In general, when

, some degree of herding exists in the market determined by the magnitude of

. This measure is calculated across the entire sample.

The effect of herding will be tested to determine how it impacts the outcome of the leverage equation without the inclusion of EPU.

EquationEquation (1) will be expanded upon by adding the herding factor in Equationequation (5)

to form Equationequation (7)

.

Where hm,t is the herding factor calculated in equation (15). All other variables and factors remain the same, as explained in equation (11).

3.4. Robustness checks

The leverage results will be checked for robustness using both book and market value. Leary and Roberts (Citation2014) used the change in market leverage as the dependent variable in all equations, which incorporated all firm-specific and peer firm averages used as control variables. Robustness will be checked by repeating this analysis for the level of market leverage, the level of book leverage as well as the change in book leverage. It is expected that the book leverage and the change in book leverage move in the same direction as the market leverage even though the market leverage is higher than firm leverage. This implies that for firms to decide on the target leverage, market-to-book ratio is one of the variables which need to be taken into account.

Another robustness check is to consider the CAPM in equilibrium, where it is meant to reflect a different effect of herding using firm betas and the market beta. It is an important and widely used model for evaluating the risk of a portfolio of assets obtained through leverage with respect to market risk and, in this case, with respect to firms within specific countries. Using this approach, it can be explored in a more detailed way whether the degree of herding has increased or decreased significantly over time.

Consider the following CAPM in equilibrium,

Where ri,t and rm,t are the excess returns on asset i and the market at time t, respectively, βi,m,t is the systematic risk measure, and Et is conditional expectation at time t (Hwang & Salmon, Citation2004). When herding is present towards the market portfolio and the equilibrium relationship no longer holds, both the beta and the herding expectation of asset i’s return will be biased. Assumed is the following relationship that holds in the presence of herding towards the market (Hwang & Salmon, Citation2004);

Where and

are the market’s biased short-run conditional expectation on the excess returns of asset i and its beta at time t, and hm,t is a herding parameter that changes over time, where hm,t ≤ 1.

is assumed to be given and thus hm,t is conditional on market fundamentals (Hwang & Salmon, Citation2004).

When hm,t = 0, =

which means that there is no herding and the equilibrium CAPM applies. When hm,t = 1,

= 1 which is the beta on the market portfolio and the expected excess return on the individual asset will be the same as that on the market portfolio (Hwang & Salmon, Citation2004). So, an hm,t of 1 suggests perfect herding towards the market portfolio, in the sense that all the individual assets move in the same direction with the same magnitude as the market portfolio. In general, when 0 < hm,t < 1, some degree of herding exists in the market determined by the magnitude of hm,t (Hwang & Salmon, Citation2004). Therefore, the herding factor can be calculated this way:

The effect of herding on returns will be tested to determine how it impacts the outcome of making leverage finance decisions in the leverage equation. Therefore, the herd measure is not assumed to be affected by market-wide mispricing like bubbles, but is designed to capture cross-sectional herd behaviour only within the market (Hwang & Salmon, Citation2004).

These checks examine how the leverage and herding factors behave when the regression specification is modified. If the coefficients are plausible and robust, this is commonly interpreted as evidence of structural validity.

4. Results

Table is a summary of the BRICS countries’ statistically significant regressors from the four regressions on both the OLS and GMM estimations. The regressions are: the effect of EPU on Leverage (A), the effect of EPU on Short-Term Leverage (B), the effect of EPU on Long-Term Leverage (C) and the effect of EPU and Herding on Leverage (D).

Table 1. Summary of overall BRICS Results—OLS and GMM Estimations

Table 2. Comparison of the herding effects

Brazil shows firm age to be significant in A, B and C but insignificant in the presence of the herding factor in D of the OLS estimations. This implies that in Brazil, the age of a firm matters and affects the leverage decisions during uncertainty periods. In contrast, all the Brazilian variables are insignificant in A, B, C and D of the GMM estimations.

Russia shows that all else equal, the dependent variables of A, B, C, and D and their initial values are significant in both the OLS and GMM regressions. In D (OLS Estimations), Russia considers a firm’s market capitalisation, a firm’s age and the degree of uncertainty to herd a leverage decision from specific firms.

India shows that all else equal, the dependent variables of A, B and C, and their initial values are significant in the OLS regressions while all the Indian variables are insignificant in A, B and C of the GMM estimations. Regression D of both the OLS and GMM seems to consider a firm’s market capitalisation, how profitable a firm is and the degree of uncertainty to herd a leverage decision from specific firms.

China presents the dependent variables of A, B, C, and D and their initial values to be significant in the OLS regressions while the dependent variables of B and C of the GMM Regressions are the only variables that are significant. In order for a Chinese firm to imitate another firm’s leverage decision making in the market, how profitable a firm is stands a very important question to answer so as to make that decision as shown in D of the OLS regressions.

South Africa shows that all else equal, the dependent variables of A, B, C, and D and their initial values are significant in both the OLS and GMM regressions. In order to make a short-term leverage decision, B of the OLS estimations, a South African firm considers a firms age, market capitalisation, sales level, the degree of uncertainty and the firms’ initial level of short-term leverage. Regression D of the OLS seems to consider a firms market capitalisation, sales level, how profitable a firm is, how tangible the assets of the firm are and the degree of uncertainty to herd a leverage decision from specific firms in the market.

The Top 40 variable is insignificant in both the OLS and GMM estimations for all the countries. This implies that being in the Top 40 does not affect the determination of leverage during policy uncertainty.

Overall, in Table , the OLS model is a better and clearer estimate of the relationship than the GMM model. All countries (except China) consider market capitalisation (profitability) before making the decision to herd in the market during policy uncertainty. South Africa and Russia consider most of the variables before making the decision to herd in the market during policy uncertainty. In conclusion, during times of economic policy uncertainty, firms make leverage financing decisions on their own not considering other factors but in the short-term and in the presence of herding, other factors are considered before making the leverage financing decisions.

4.1. Discussion of results

4.1.1. Brazil

Given that EPU in Brazil is high mostly due to corruption,Footnote2 it is expected that firms will lower their leverage ratios. Both OLS and GMM estimations show EPU to be statistically insignificant in explaining the overall leverage, short-term leverage and long-term leverage without the presence of herding as shown in Table . This implies that the change in EPU does not affect the debt decisions of Brazilian firms. Akey and Lewellen (Citation2017) state that Brazilian firms can also hedge against EPU by vigorously trying to impact the policy-making process. This means that Brazilian firms have a more grounded incentive to take part in the political procedure than comparable, policy-neutral firms. The herding effect is statistically significant and is positively related to the leverage ratio of firms using OLS estimations, while statistically insignificant and negatively related to the leverage ratio of firms using GMM estimations. This corresponds with Hwang and Salmon (Citation2004) having found proof of herding towards the market portfolio both when the market is rising and when it is falling. EPU is statistically insignificant in the presence of herding.

Brazilian firms rely more on leverage financing as it may be cheaper than equity and more convenient to undertake. The banking system in Brazil is more reliable, although interest rates are high when one considers borrowing funds. Overall, this implies that firms will decrease their leverage ratio when there is policy uncertainty in the market and borrow more when the market is stable again. In the presence of herding however, whether leverage increases or decreases due to herding, EPU still remains negatively related to leverage. The results are as expected, as EPU has a negative relationship with leverage financing decisions (Zhang et al., Citation2015).

4.1.2. Russia

Changes in EPU are statistically insignificant in the determination of overall firm leverage as well as long-term leverage meeting prior theoretical expectations of negative signage. EPU is found to be statistically insignificant in the determination of firm short-term leverage but does not meet prior theoretical expectations because of a positive relationship. In the presence of herding, EPU is statistically significant and has the expected sign and this makes it consistent with the findings of Zhang et al. (Citation2015), which show that increased EPU will cause firms to deleverage. Herding is statistically significant and positively related to leverage.

Given that when the degree of EPU in Russia increases, it is expected that firms are likely to decrease their leverage ratios like Brazil. Banks constitute a large share of Russia’s financial system but are poorly established. Nonetheless, capital from Russian banks is made available over short-term periods which prevent the possibility of long-term investments being funded from the banks. Overall, EPU is statistically insignificant in determining leverage and the relationship between the two variables varies given the market shocks, funding availability and restrictions within the Russian financial system. During times of economic policy uncertainty, Russian firms decrease their borrowings and herd their financing decisions towards the market.

4.1.3. India

Both OLS and GMM estimations are consistent with each other where EPU is statistically insignificant in explaining the overall leverage, short-term leverage and long-term leverage without the presence of herding. In the presence of herding, EPU and herding variables are statistically significant. This corresponds with Hwang and Salmon (Citation2004) having found proof of herding towards the market portfolio both when the market is rising and when it is falling. Although statistically insignificant, the differenced EPU term is inconsistent with prior expectations of a negative relation to leverage in both the OLS and GMM estimations.

Overall, a positive change in EPU would result in firms increasing their borrowing level and this is due to different financing sources that may be coming at a cheaper rate during a crisis. This is in contrast with the findings of Akey and Lewellen (2015) and Zhang et al. (Citation2015). India’s financial system is seen as a diversified system as sources of financing come from different streams in the country such as a growth in the participation of the private sector and nonbank intermediaries. This implies that firms will increase their leverage ratio when there is policy uncertainty in the market and borrow less when the market is stable again. In the presence of herding however, whether leverage increases or decreases due to herding, EPU still remains positively related to leverage. The results are not as expected based on the hypothesis stated in this research and are in contrast with what Zhang et al. (Citation2015) found. During times of economic policy uncertainty, Indian firms find other cheaper alternative borrowing mechanisms to finance their firms’ operations.

4.1.4. China

Both OLS and GMM estimations show EPU to be statistically insignificant in explaining the overall leverage, short-term leverage and long-term leverage without the presence of herding, but does not meet prior theoretical expectations because of a positive relationship. The differenced EPU term is consistent with prior expectations of a negative relation to short-term leverage in the OLS estimation. In the presence of herding, EPU is statistically insignificant yet does not meet prior theoretical expectations because of a positive relationship in the presence of herding. Herding is statistically significant but positive relationship in the OLS estimations while in the GMM estimations herding is statistically insignificant in the presence of herding but has a negative relationship. This corresponds with Hwang and Salmon (Citation2004) having found proof of herding towards the market portfolio both when the market is rising and when it is falling.

China’s financial system is bank-dominated and given the ratio of credit to GDP surpassing the benchmarks by wide margins, China appears to have the largest banking system in the world. Though there are private and publicly owned banks, there seems to be no significant competition among them. Given that when the degree of EPU in China increases, it is expected that firms are likely to decrease their leverage ratios. The overall results show a positive relationship on average which is in contrast with the expectations. This may be due to the diversity and flexibility of different finance sources available in both short-term and long-term periods.

This means that during times of economic policy uncertainty, Chinese firms are policy-neutral firms, which does not make them susceptible to hedge against EPU. Chinese firms increase their borrowing levels during times of economic policy uncertainty, which is in contrast with Zhang et al. (Citation2015).

4.1.5. South Africa

The OLS estimator shows that EPU is statistically insignificant in explaining the overall leverage and long-term leverage without the presence of herding, however, meets prior theoretical expectations of having a negative sign. EPU is statistically significant in explaining the short-term leverage but does not meet prior theoretical expectations. In the presence of herding, EPU and herding are statistically significant but do not meet prior theoretical expectations.

The GMM estimator shows that EPU is statistically insignificant in explaining the overall leverage, short-term leverage and long-term leverage without the presence of herding, but does not meet prior theoretical expectations. In the presence of herding, EPU is statistically insignificant and meets prior theoretical expectations of a negative signage, while herding is statistically significant but does not meet prior theoretical expectations.

Given that when the degree of EPU in South Africa increases, it is expected that firms are likely to decrease their leverage ratios. Looking at the overall results, though insignificant but they on average meet the prior theoretical expectations of a negative relationship with leverage. Corruption and a sense of uncertainty in the country has had a big impact on the economy and causing a decline its economic growth. Corrupt individuals use state resources for their own personal use, which bankrupts the country to fulfil its cause. Although most banking assets and liabilities are domestic and expanding into Africa, foreign assets minimally exist, and most bank liabilities are domestic, short-term, and wholesale. The largest source of funding comes from domestic credit while short-term credit from non-bank financial institutions and corporations forms a minimal part of financial assets, which have been gradually growing in the country.

Overall, during times of economic policy uncertainty, firms decrease their borrowing levels, which is consistent with the findings of Akey and Lewellen (2015) and Zhang et al. (Citation2015). Sum (Citation2012) agrees with the above and further says that during periods with high policy uncertainty, credit availability may become limited because banks may have low confidence and fear in the markets, which is the case in South African results. Firms show that during times of economic policy uncertainty herding is present relative to market conditions. This corresponds with Hwang and Salmon (Citation2004) having found proof of herding towards the market portfolio both when the market is rising and when it is falling. Seetharam and Britten (Citation2013) concur with the above as they additionally discovered that herding behaviour seems to rise before a market contraction. The caveat of this study is that Akey and Lewellen (2015) and Zhang et al. (Citation2015) used Baker et al. (Citation2016) to measure EPU while for South Africa, EPU was measured according to Brogaard and Detzel (Citation2015) instead. Nevertheless, results were in accordance with developed economies, demonstrating the high level of advancement in South Africa’s monetary-related markets.

4.2. Robustness

4.2.1. Market-to-Book leverage analysis

Overall, Russia, India and China robustness outcomes show no significant difference in moving from market leverage to market-to-book leverage. In other words, leader firms’ financial policies appear insensitive to the return shocks of follower firms. Change in market leverage matters for Brazil and South Africa even though market-to-book ratio is not one of the variables which need to be considered for all the BRICS countries.

4.2.2. CAPM herding effect

The summary in Table 2 shows both significant and insignificant herding effect results from the OLS estimations and the CAPM estimations. The CAPM herding effects are less than the OLS herding estimates except for Brazil. The OLS shows that all the BRICS countries’ herding effects are statistically significant at a 5% significance level whereas the CAPM results show only Brazil as having a significant herding effect. The comparison between the two models shows that the OLS estimation expresses a true reflection of the countries’ herding effects as well as being aligned to the expectations drawn from the literature review.

4.2.3. Robustness summary

The market-to-book leverage analysis and the CAPM herding analysis, as the two robustness checks were implemented to determine how the EPU and CAPM herding impacts the outcome of making leverage finance decisions in the leverage equation when the regression is modified. The robust checks have shown that firstly, for firms to decide on the target leverage, market-to-book ratio is not one of the variables which need to be taken into account for all the BRICS countries. Secondly, even though a CAPM analysis is an important and widely used model for evaluating the risk of a portfolio of assets obtained through leverage with respect to market risk, the robust check has shown to yield insignificant CAPM herding effects. In conclusion, the results from the two robust checks are not plausible and robust, and this is understood as evidence of structural invalidity.

5. Conclusion

This study examines the role of economic policy uncertainty (EPU) in influencing firm performance and leverage as a form of financing decisions, in the presence of herding in the emerging markets of Brazil, Russia, India, China and South Africa (BRICS). The increase or decrease EPU is determined by the way policymakers or investors act and the consequences of their decisions.

Using a recently available Economic Policy Uncertainty (EPU) measure for the BRICS countries, the relationship between EPU and BRICS firms’ capital structure choices is explored from June 2002 to 2017. The change in EPU in Brazil, Russia and South Africa yields a negative relationship to the firms’ leverage ratios, as expected, which means that during times of economic policy uncertainty, the firms in those countries decrease their borrowing levels. However, in India and China, the change in EPU is found to be statistically significant though the sign is not what is expected by the theory. This implies that the change in EPU does not affect the debt decisions of the firms in these two countries. Both countries have several alternative sources of leverage financing available. The negative relationship is vast for firms that borrow on a short-term basis mainly from local banks in Brazil, Russia and South Africa. This means that firms in these countries are more prone to react when there is uncertainty and more so it is evident that they tend to mimic other firms in the presence of uncertainty. Firms in India and China on the other hand take the opportunity of cheaper debt when there is uncertainty in the market. Firms in both countries have a variety and flexible sources of finance, which means they are able to increase leverage in times of uncertainty. This implies that the countries are not intimidated by EPU but rather use it to their advantage in growing their businesses knowing that EPU is only temporary in the market.

In developed countries, firms are likely to delay their debt issuance during times of high policy uncertainty as they value financial flexibility. Cao et al. (Citation2013) confirm this with the results found in their study, that suggest policy uncertainty has a first-order effect on firms’ financing decisions by increasing financial conflicts. They also show that firms that have lower political risk exposure and access to public debt markets are less sensitive to changes in policy uncertainty when determining capital structures and show that firms hold more cash during periods of high policy uncertainty (Cao et al., Citation2013). This is evidence that emerging countries react to EPU but some react more than others.

The outcomes of this study contribute to the body of knowledge in a number of ways. Firstly, like Zhang et al. (Citation2015), this study gives an “out-of-sample” investigation on the role of policy uncertainty and the presence of herding in determining financing decisions in the BRICS countries as the future leading emerging group of the world. Secondly, this study shows that firms in these countries have a tendency of changing their financing structure as a reaction to policy uncertainty in the presence of herding or not. This shows that emerging markets still require financial support in order to be stable in times of uncertainty. Thirdly, this study likewise adds to the growing literature that considers the impact of uncertainty and herding on corporate financing decisions in emerging countries.

This study tried to answer the questions through the primary and secondary hypotheses: During times of economic policy uncertainty, how do firms rationalise making leverage financing decisions; and do they herd their leverage financing decisions towards what the market or other firms have decided? Russian, Indian and South African results reject the primary and secondary null hypotheses and conclude that there is a significant relation with EPU being a factor in determining firm leverage financing decisions and that there is a significant relation with more EPU leading to herding towards firm leverage financing decisions, respectively. Brazilian and Chinese results fail to reject the primary and secondary null hypotheses and conclude that there is no significant relation with EPU being a factor in determining firm leverage financing decisions and that there is no significant relation with less EPU leading to little or no herding towards firm leverage financing decisions, respectively.

In summary, EPU has an impact on business. It affects the profit for many companies, and this is the reason of investment delays or less consumption, which together may lead to economic activity slowdown. EPU leads to financial and economic problems that could harm countries and their citizens that could contribute, otherwise, to sustainable growth. EPU is, in fact, a market characteristic that brings changes at the prices and returns levels. Investors and policymakers should be aware of it to prevent EPU consequences. In this manner, financial markets could find more stability.

Additional information

Funding

Notes on contributors

Prudence Makololo

Prudence Makololo is an Investment Professional and a PhD candidate from the University of Witwatersrand. She obtained her MCom in Finance from the University of the Witwatersrand and her area of interest is behavioural finance and emerging markets.

Yudhvir Seetharam

Yudhvir Seetharam is the Head of Analytics, Insights and Research at a major South African bank; and a Senior Lecturer in Finance from the University of the Witwatersrand. His area of research is in quantitative behavioural finance. Yudhvir is an editor for Cogent Economics and Finance.

Notes

1. Policy uncertainty (also called regime uncertainty) is a class of economic risk where the future path of government policy is uncertain, raising risk premia and leading businesses and individuals to delay spending and investment until this uncertainty has been resolved. Policy uncertainty may refer to uncertainty about monetary or fiscal policy, the tax or regulatory regime, or uncertainty over electoral outcomes that will influence political leadership.

2. Article “Brazil’s political and economic future remain uncertain” with Dr Sabatini’s commentary, retrieved from https://www.pacificcouncil.org/newsroom/brazil%E2%80%99s-political-and-economic-future-remain-uncertain

References

- Akey, P., & Lewellen, S. (2017). Policy uncertainty, political capital, and firm risk-taking. SSRN Electronic Journal 22, 2017. doi:10.2139/ssrn.2758395

- Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4), 1593–21. doi:10.1093/qje/qjw024

- Bernanke, B. S. (1983). Irreversibility, uncertainty, and cyclical investment. The quarterly journal of economics, 98(1), 85–106. doi:10.2307/1885568

- Bloom, N. (2014). Fluctuations in uncertainty. The Journal of Economic Perspectives, 28(2), 153–175. https://doi.org/10.1257/jep.28.2.153

- Brendea, G., & Pop, F. (2019). Herding behavior and financing decisions in Romania. Managerial Finance, 45(6), 716–725. https://doi.org/10.1108/MF-02-2018-0093

- Brogaard, J., & Detzel, A. (2015). The asset pricing implications of government economic policy uncertainty. Management Science, 61(1), 3–18. https://doi.org/10.1287/mnsc.2014.2044

- Cao, W., Duan, X., & Uysal, V. B. (2013). Does political uncertainty affect capital structure choices? Working paper. University of Oklahoma.

- Faulkender, M., & Petersen, M. A. (2006). Does the source of capital affect capital structure? The Review of Financial Studies, 19(1), 45–79. https://doi.org/10.1093/rfs/hhj003

- Federal open market committee. (2009). Minutes of the December 2009 meeting. http://www.federalreserve.gov/monetarypolicy/fomcminutes20091216.htm

- Gao, P., & Qi, Y. (2012). Political uncertainty and public financing costs: Evidence from US municipal bond markets. working paper. doi:10.2139/ssrn.2024294

- Gulen, H., & Ion, M. (2016). Policy uncertainty and corporate investment. Review of Financial Studies, 29(3), 523–564. https://academic.oup.com/rfs/article/29/3/523/1887688

- Hwang, S., & Salmon, M. (2004). Market stress and herding. Journal of Empirical Finance, 11(4), 585–616. https://doi.org/10.1016/j.jempfin.2004.04.003

- International Monetary Fund. (2012b, October). World economic outlook: Coping with high debt and sluggish growth. IMF Press.

- International Monetary Fund. (2013, April). World economic outlook: Hopes, realities, risks. IMF Press.

- Khan, M. A., Qin, X., & Jebran, K. (2020). Uncertainty and leverage nexus: Does trade credit matter? Eurasian Business Review, 10(3), 355–389. https://doi.org/10.1007/s40821-020-00159-5

- Leary, M. T., & Roberts, M. R. (2014). Do peer firms affect corporate financial policy? The Journal of Finance, 69(1), 139–178. https://doi.org/10.1111/jofi.12094

- Modigliani, F., & Miller, M. H. (1958). The cost of capital, corporation finance and the theory of investment. The American Economic Review, 48(3), 261–297. https://d1wqtxts1xzle7.cloudfront.net/30867396/modiglianiandmiller1958.pdf?1362598952=&response-content-disposition=inline%3B+filename%3DThe_Cost_of_Capital_Corporation_Finance.pdf&Expires=1599899845&Signature=F2mqjnBRq66AZI177PB3MBvaQxaFPfg0uJ5-2tccKp~a2ZBYRwaYTlIb7l7bwpKkHJPWslLlYD0d-iOmbHl1FgVPHIFfecUZajEIvcN5xR2KRGzOIgUhPTSfbE6zFftGdYsR7VfuXckxsLLClG50K5O54fp1984Kmmuwph~~b7YDzYLD7YMFbC5tNb5FjRF5bisabwx9vyVJlV3bGe-FsJjkQXf7-zNPT0GMBi6wPHMKCvfsuEXid8ffZh9CneJnnDfNnJAOIiug-79CDk13UaZO-8QXPgIb7ImzPFH3eDlj7RWxQ1tvAR6U-yV4pQTaIabDoqZD0OAdAS7uaWYH2w__&Key-Pair-Id=APKAJLOHF5GGSLRBV4ZA

- Seetharam, Y., and Britten, J. (2013). An Analysis of Herding Behaviour during Market Cycles in South Africa. Journal of Economics and Behavioral Studies, 5(2), 89–98. doi:10.22610/jebs.v5i2

- Sum, V. (2012). The Impulse Response Function of Economic Policy Uncertainty and Stock Market Returns: A Look at the Eurozone. SSRN Electronic Journal, 12(3), 100–105. doi:10.2139/ssrn.2088700

- Tran, Q. T. (2019). Economic policy uncertainty and corporate risk-taking: International evidence. Journal of Multinational Financial Management, 52, 100605. https://doi.org/10.1016/j.mulfin.2019.100605

- Welch, I. (2002). Columbus’ egg: The real determinant of capital structure. NBER Working Paper No. 8782. National Bureau Of Economic Research.

- Zeckhauser, R., Patel, J., & Hendricks, D. (1991). Nonrational actors and financial market behavior. Theory and Decisions, 31(2–3), 257–287. https://doi.org/10.1007/BF00132995

- Zhang, G., Han, J., Pan, Z., & Huang, H. (2015). Economic policy uncertainty and capital structure choice: Evidence from China. Economic Systems, 39(3), 439–457. https://doi.org/10.1016/j.ecosys.2015.06.003