Abstract

Studies noticed that individuals’ cognitive, psychological, and behavioral limitations always have some influence in their everyday decision making. And the financial decisions are no exceptions. Perhaps it can be affirmed that individual financial decisions do have cognitive influence. This is also true with the Indian households. This study has briefly identified one such component i.e. mental accounting system and has explored the presence of mental accounting influence in households’ financial decisions. The study also establishes mental accounting as a second-order construct by using a hierarchical latent variable model. Partial Least Square Structural Equation Model (PLS-SEM) has been used to analyze and validate the scales. The analysis has been done with 452 responses collected using a survey method through a structured questionnaire given to Indian households. The study essentially analyses the influence of mental accounting in the financial decisions of households. This study aims at extending the knowledge of behavioral finance among the scholars of consumer behavior and personal finance, as well as the financial service providers.

PUBLIC INTEREST STATEMENT

Recent research demonstrates that people often make financial decisions that are not based on logic but are influenced by their emotions and heuristics. This can be seen when people purchase stocks at higher prices based on speculation, and sell it at a lower price due to panic and lack of confidence, and make losses. Behavioral finance helps us to understand why people do not make their financial decisions in the way that rational choice models predict and help us explore the biases which influence our financial decisions. The present study identified one such component i.e. mental accounting system and explored the presence of mental accounting influence in households’ financial decisions. The current study also establishes mental accounting as a second-order latent variable construct. The analysis results support the prevalence of mental accounting systems in personal financial planning. The study extends the knowledge of behavioral finance among scholars of consumer behavior and also to the financial service providers in the Indian context.

1. Introduction

The term behavioral finance is defined as an individual’s psychological effects on financial decisions. The most essential reason to study behavioral finance is the limitation of traditional finance in explaining various antecedents of investors’ financial decisions. Behavioral finance does not overshadow the existence of any finance theory, but it merges those with cognitive psychology and provides a complete model of human behavior in the process of decision making (Thaler, Citation2005).

Behavioral decision making has been an area of interest for economists for many years, in which, the cognitive component of behavioral decisions i.e. mental accounting has been studied in various concepts of financial decision making and cognitive evaluation of economic outcomes (Thaler, Citation1988; Thaler, Citation1990). Individual households’ financial decision making is influenced by their implicit mental accounting characteristics (Thaler, Citation1985). The understanding of the mental accounting process helps an individual to appreciate that their financial choices are not unbiased.

Mental accounting is a process whereby people code, categorize, and evaluate their economic outcomes (Thaler, Citation1980). It describes that the subjective framing of the utility of a transaction divides income and expenditure into different cognitive accounts based on the source and the frequency (Gourville & Soman, Citation1998; Prelec & Loewenstein, Citation1998; Thaler, Citation1985, Citation1999). The main importance of the theory is that it helps in explaining individual economic behavior. An individual’s intension to control expenditure and increase savings causes the formation of mental accounts and is beneficial to the investors with imperfect self-control (Statman, Citation1999). Individuals typically use mental accounts as a self-control device.

The main objective of this study is to explore the presence of mental accounting systems among Indian households. The rest of the paper is organized as follows: Section 2 presents a brief review of mental accounting studies; section 3 discusses the methodology including questionnaire design, sampling and data collection; section 4 presents a brief analysis of the data. Section 5 and 6 conclude the study with brief discussions on the analysis results, study limitations, and practical implications.

2. Literature review

The mental accounting concept has been extensively studied in the area of individual psychology of various financial decisions. The present section discusses in brief about various studies conducted to understand the influence of mental accounting in individuals’ financial decisions.

The behavioral life-cycle hypothesis provides a better understanding of the relationship between consumer behavior and decision making (Shefrin & Thaler, Citation1988). The life cycle hypothesis proposes that individuals flatten their consumption to maximize utility over the lifetime (Ando & Modigliani, Citation1963). But recent studies differ in that understanding and support individual decision making influenced by “rule of thumb” or also known as mental accounting strategy (Bernheim et al., Citation2001). Mental accounting is the process of dividing assets into designated specific purpose accounts (Shefrin & Thaler, Citation1992).

It is a cognitive form of bookkeeping to keep a track of transactions of money and to keep control of spending (Thaler, Citation1985). Thus, Individuals saving behavior are associated with the behavioral life cycle hypothesis (Rabinovich & Webley, Citation2007). The Behavioral Life-Cycle Hypotheses (BLCH) proposes that the individuals’ various forms of wealth are not substitutes to each other i.e. households’ retirement savings, pension, or home equity has a comparatively less marginal propensity to consume (MPC) than other forms of wealth (Thaler, Citation1990). In the process of mental accounting, people cognitively divide their assets into three accounts, i.e. current income, current wealth, and future income. Based on that, they treat their account as non-fungible, and the marginal propensity to consume (MPC) of each account is different. The MPC is more for the current income account than current assets, and it’s almost zero when the money is stored in a future income account (Karlsson et al., Citation1997; Shefrin & Thaler, Citation1988).

Further, studies also mention that within each category, people again segregate the income based on the source of money, where marginal propensity again differs, such as marginal propensity to consume income from a lottery win or a gift is higher than money received as overtime pay or bonus (Maital & Maital, Citation1994; Thaler, Citation1990). It influences the individual’s saving and spending decisions and is helpful in restrain spending by allotting budget limits in certain categories (Heath & Soll, Citation1996). Studies support the influence of mental accounting rules in consumption and saving decisions (Feldman, Citation2010; Shefrin & Thaler, Citation1988). Mental accounting leads to impulsive investment behavior and substantiates the disposition effect (Ko & Huang, Citation2012). Studies also used the survey data to analyze and support the evidence of mental accounts in individual financial decisions (Shefrin & Thaler, Citation1988; Winnett & Lewis, Citation1995).

Other than the components of the behavioral life-cycle hypothesis, the present study also considered mental budgeting as one of the components to study the process of mental accounting among individual households. There is enough amount of literature that supports the role of mental budget in saving and consumption decisions. For more than half a decade, studies recognize the consumer’s tendency to divide wages into different categories with the allocation of different expenses. Wright (Citation1940) evaluated the unemployment workers’ study in the 1930s and described that they used to make small envelopes or chins pitches in the cupboard to put their small amounts of money. In another study of Rainwater et al. (Citation1959) describe the study of the household in the 1950s where they use the process of “tin can accounting”, where they mention that households put their money in different tin cans labeled with different expenditure. These studies provide the information of households’ allocation of funds into separate accounts through envelopes, various drawers, or tin canes [The above-mentioned references are cited from the paper of Heath and Soll 1996].

Studies support this process of creating groups and labelling resources and the effect of grouping on personal satisfaction (Thaler, Citation1994). Many researchers claim that individuals create mental budgets and allocate their income to those budgets (Heath & Soll, Citation1996; Thaler, Citation1990, Citation1999). Mental budgeting affects individual behavior and consumption decision (Heath, Citation1995; Heath & Soll, Citation1996). It is a cognitive form of book-keeping that individuals use to keep track of expenses and to control consumption and mental accounting as a self-control device that consumers employ to prevent excess spending on consumption (Cheema & Soman, Citation2006).

Thus, to analyze the formation and influence of mental accounting towards Indian households’ financial decision making process study has considered four concepts. The first concept is mental budgeting, which explains the concept of cognitive segregation of money based on different expenditures, like food, clothing, etc. The other three mental accounting concepts are considered from the concept of behavioral life cycle hypotheses i.e. current income, current assets, and future income.

The present study shares its contribution to behavioral finance literature by exploring the existence and influence of the mental accounting system among Indian households’ financial decision making process. As mentioned, households follow various cognitive evaluations before making financial decisions or dealing with financial matters. The present study considered and evaluated the existence and influence of mental accounting in Indian households’ financial decisions. The below section discusses the methodology used for the conduction of the study.

2.1. Conceptual background

The four concepts explained by Thaler (Citation1985), i.e. segregation of gains, integration of small losses, segregation of small losses from higher gains, and integration of gains received on the same day, have given birth to the new theory of consumer behavior. Each of these anecdotes violates the standard economic theory and establishes an example of different types of behavior that get induced by the mental accounting system. The concept of mental accounting proposes a theory of consumer choice which is based on consumer behavior (Thaler, Citation1985).

Therefore to explain the mental accounting system among Indian households, we use the concept of reference point, which is defined as perceived gains and losses. The reference point in metal accounting also explains the impact of “framing effect” in choices.

The study uses vignettes methodology to understand the existence of a mental accounting system among Indian households. For many years, vignettes methodology has been used to investigate various phenomena in the domain of social studies, behavioral studies, health sciences, etc. (Alexander & Becker, Citation1978; Bachmann et al., Citation2008). Vignettes are the stories of individuals, or situations used in various psychological studies, and are considered as a reference for perception, beliefs, and attitude (Hughes, Citation1998). Through vignettes, some hypothesized situations are created, and participants are asked to respond to those situations to fabricate the understanding of certain real-life scenarios (Rahman, Citation1996). While taking the guidelines from the past literature (Thaler, Citation1985, Citation1999), the present study constructed few vignettes, and responses have been collected for each of them.

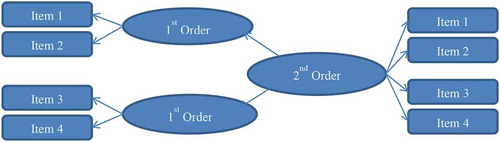

As mentioned in the literature review segment, the study considers three concepts from the behavioral life cycle hypothesis (BLCH) i.e. current Income, current assets, and future income, and another concept i.e. mental budgeting is used to measure the influence of mental accounting among Indian households (Mahapatra et al., Citation2019). The definition of each component has been derived from the understanding of past literature on mental accounting. The statements to measure each concept are prepared based on the described definition (see Annexure 1and 2). Based on previous literature, the conceptual framework of the study proposes mental accounting to be the second-order factor of current income, current asset, future income, and mental budgeting (see Figure ).

Figure 1. Conceptual frame work.

The mental accounting influence among Indian households has been measured by using a scale of 15 items (Mahapatra et al., Citation2019). The scale includes five items to measure mental budgeting, two items for current income, and four items for current assets and future income scale each (Mahapatra et al., Citation2019). The original scale includes three items to measure the concept of future income of BLCH, but we included one more item i.e. “I always make a point to keep aside some amount of money from my salary for meeting my future requirements” (see Annexure 3). The respondents were requested to answer their view on a five-point scale ranging from 1 (strongly agree) and 5 (strongly disagree).

3. Methodology

3.1. Data collection

The main objectives of the study are to explore the presence of mental accounting systems among Indian households’ financial decisions and to establish mental accounting as a second-order construct of mental budgeting, current income, current assets, and future income. The current study considers earning members of the family as the population of the study and mainly conducted in Hyderabad—Secunderabad twin cities. To represents a whole India sample, the respondents are selected mainly from the defense personal, employees of pharmaceutical companies, IT companies, banks, and educational institutes. The study uses an online and offline survey method to collect data. A structured questionnaire has been created using “Google form” and mailed to 1000 respondents and a hardcopy of the same was distributed to 625 respondents. A total of 512 respondents reverted (online and offline together) with responses. Finally, 60 responses were deleted due to missing values and analysis has been done with the 452 responses.

The current study uses the PLS-SEM method to analyze a hierarchical latent variable model to establish mental accounting as a second-order latent construct of four first-order latent constructs i.e. mental budgeting, current income, current assets, and future income. The increasing use of PLS-SEM can be observed in the field of strategic management (Hair et al., Citation2012). Modeling of a second-order construct with more than one reflective first-order construct can be seen in the measurement of the social capital construct (Koka & Prescott, Citation2002).

The PLS-SEM model has the highest statistical power and it’s suitable for a complex model with a smaller sample size (Hair et al., Citation2011, Citation2013). Cohen (Citation1992) provides the minimum sample size table for statistical power analysis in multiple regressions. The table of a minimum sample size of Cohen (Citation1992) including with the number of independent variables (i.e. maximum number of arrowheads pointed at explanatory variable) in a structural model. As per the table, the minimum sample size for the present study with four independent variables at 80% statistical power at a 5% significance level with minimum R-square of 0.25 is 65. Whereas, the study considers a sample size of 310, which is considered being the higher side of the minimum requirement.

3.2. Sample profile

A brief profile of the sample indicates that the male participants (62.2%) are more than female (37.8%). Almost 89.3% of them are between the age group of 25 years to 45 years. However, 10.6% of respondents are between the ages of 45 years to 55 years. It also can be noticed that most of the respondents are postgraduates (58.2%) with a private job (68.4%). A large number of the respondents (36.3%) indicate their annual family income to be in the bracket of Rs.4 lakhs to Rs.6 Lakhs, and 29.4% of them fall in the income bracket of Rs.6 lakhs to Rs.9 lakhs (see Table ).

Table 1. Socio-demographic profile of the entire sample

3.3. Methods

The methodology used to understand the mental accounting system among Indian households has been done in two steps viz. understanding mental accounting through vignettes and assessing mental accounting through scale items. The subsequent sections discuss the same.

3.4. Step 1: Understanding mental accounting through vignettes

Vignettes are hypothetical scenarios. Vignettes studies are extensively used in the field of medical-psychology and complex social science issues (Bachmann et al., Citation2008; Jensen et al., Citation2019; Schoenberg & Ravdal, Citation2000). The method has been used to explore the influence of social cognitive bias among young investors (Baeckström et al., Citation2018), in awareness and attitude studies (Schoenberg & Ravdal, Citation2000), in collecting data on various sensitive topics like mental health (Barter & Renold, Citation2000). Vignettes have become a fashionable tool in qualitative research methodology, especially in psychology, sociology, and cross-sectional analysis (Richman & Mercer, Citation2002). This approach offers flexibility in designing unique measurement instruments specific to contemporary attention (Schoenberg & Ravdal, Citation2000). The method is useful in collecting information with minimum available resources (Wilson & While, Citation1998).

The current study uses a series of vignettes statements (statements) to illustrate the influence of the mental accounting system in individual decisions which violates the concept of economic principle (Thaler, Citation1985, Citation1999). Studies proposed mental accounting influence on valuing gains and losses differently and described four principals of evaluating gains and losses by an individual i.e. (a) Segregation of gains (b) Integration of losses (c) Integration of gains received in the same day and (d) Segregation of small gains from larger losses (Thaler, Citation1985, Citation1999).

The current study evaluates each concept of mental accounting phenomena by using a small paragraph describing the situation usually known as “vignette”. Each situation describes “A” and “B” as a separate person. However, out of 452, only 416 respondents provided their views on each situation. The present study uses the rate of recurrence to analyze the preference of respondents for each of the scenarios given to them. The vignettes are prepared by taking reference from the past literature (Thaler, Citation1994, Citation1999). The below segment provides a brief explanation of each vignette.

Segregation of gains: As mentioned above, individuals induced with mental accounting systems segregate gains incurred in small pieces. To evaluate the same, respondents were asked to indicate their views on the following situation (see Table ).

Table 2. Responses of vignettes on segregation of gains

The analysis indicates that, though both Mr. A and Mr. B, ultimately had a profit of Rs.300, almost 57% of the respondents felt Mr. B would be happier than Mr. A. This indicates that, people segregate small losses from bigger gains and support the induction of mental accounting phenomena in pursuing financial outcomes.

Integrating small loss: The stimulation of mental accounting concept in the evaluation of households financial outcomes has also be observed through their tendency towards integrating losses, to evaluate the same, the following scenario has been used and respondents pen down their opinion by clicking the appropriate option (see Table ).

Table 3. Responses of vignettes on the integration of small losses

The analysis indicates Mr. A to be more upset than Mr. B, despite having the same amount of tax repercussion. According to a majority of respondents, the fact that Mr. A received two separate notices made him unhappy as compared to Mr. B, who received a single notice, despite the net loss being the same. The result proves the mental accounting phenomena of integrating losses and stipulates the formation of a mental accounting system among individual households while evaluating financial outcomes.

Segregating small losses from larger gains: The study also analyses the households evaluating financial outcomes based on the mental accounting phenomena i.e. segregating small losses from larger gains. To evaluate the same, below mentioned scenario has been used and responses have been analyzed (see Table ).

Table 4. Responses of vignettes on segregation of small losses from larger gains

The results conclude that almost 45.4% of respondents agree for Mr. A to be more upset than Mr. B. Though Mr. A and Mr. B spend an amount (of Rs. 2000), but in the case of Mr. A, he incurs a loss of Rs. 5000 and gets a bonus of Rs. 3000. As mentioned, mental account induces segregating of small gains from larger losses; the above results support the same and indicate the existence of a mental accounting system among Indian households.

Integrating gains received on the same day: The mental accounting phenomenon of “integrating of gains received in the same” has also been assessed among Indian households through the vignettes (see Table ).

Table 5. Responses of vignettes on the integration of gains received on the same day

Here, Mr. A received the gains in two different lucky draws, but Mr. B receives the same amount of gains in a single draw. The analysis result implies Mr. A to be happier than Mr. B. This indicates that an individual integrates the gains received on the same day, and supports the evidence of the mental accounting system among Indian households.

The present study also uses a few statements to analyze the existence of mental accounting influence in the financial decisions of Indian households. The below section discusses the same.

3.5. Step 2: Assessing mental accounting through scale items

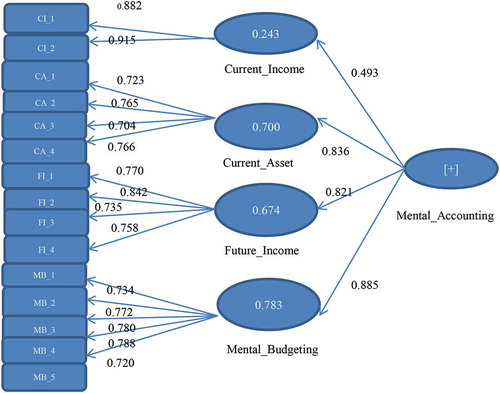

Partial Least Square Structural Equation Model (PLS-SEM) has been considered a suitable method to analyze the proposed model. Considering a sample of 452, an SEM analysis has been done to establish the model. The present study uses a hierarchical construct model to depict mental accounting as the second-order (Bradley & Henseler, Citation2007) of mental budgeting, current income, current assets, and future income (see Figure ).

Figure 2. Second order factor model; hierarchical component model (HCM).

In the conceptualization of a higher-order construct, the hierarchical latent variable model helps in matching the concept of predictor and criterion variables (Johnson et al., Citation2012). However, the conceptualization of a multidimensional scale can be derived through the theoretical relationship (Johnson et al., Citation2012; Polites et al., Citation2012). Hierarchical latent variables models are the representation of multidimensional constructs that are related to a similar level of concept (Chin, Citation1998). In recent years an increasing trend of the PLS-SEM model can be observed for the analysis of the hierarchical latent variable with reflective measures (Wetzels et al., Citation2009).

The hierarchical latent variable model in SEM helps in the assessment of the reliability and validity of the higher-order construct (Edwards, Citation2001; Fornell & Larcker, Citation1981; MacKenzie et al., Citation2011). The current study uses a repeated indicator approach of PLS-SEM to model hierarchical latent variable (Lohmöller, Citation1989). For example, in the current study second-order latent variables i.e. mental accounting consists of four first-order latent constructs i.e. mental budgeting, current income, current assets, and future income. Further, these four first-order constructs are the manifestation of fifteen variables. Therefore the model is specified with all nineteen manifest variables.

4. Analysis of the data

To establish the reliability and validity of the mental accounting measurement scale, the present study uses Partial Least Square (PLS) using SmartPLS 3.0, adopting the latent structural equations modeling technique. As PLS-SEM does not have any constraints on sample size and residual distributions (Chin, Citation1998; Fornell & Bookstein, Citation1982; Hair et al. Citation2016), the present study found it to be the best-suited approach for the analysis (see Figure ).

Figure 3. SEM analysis of the model.

To analyze the reliability of the mental accounting scale, the study first considers PLS outer loadings and composite reliability. And to analyze the validity of the scale study uses convergent validity and discriminant validity. PLS outer loadings give the factor loadings of each item. A greater than 0.70 value of factor loadings and composite reliability is considered to be acceptable (Fornell & Larcker, Citation1981) (see Table ).

Table 6. PLS Outer Model Loadings and P values

The Validation of the measurement model has been done through the elimination of items with less than 0.7 loadings, and the process of refinement resulted in a reduced number of items in each scale (see Table ).

Table 7. Number of items in each scale

The composite reliabilities of the four components of the mental accounting scale are more than adequate (>0.8) (Hair et al., Citation2013). The convergent validity of the scale is measured through the average variance extracted (AVE) value of each scale and a value greater than 0.5 (Hair et al., Citation2013) is considered to be satisfactory to persuade convergent validity. The discriminant validity of the scales has been analyzed through the Fornell-Lucker criteria i.e. the square root of the average variance extracted (AVE) should be larger than the inter-construct correlations (Agarwal & Karahanna, Citation2000; Fornell & Larcker, Citation1981) (see Table ).

Table 8. Reliability and validity of the scales

To satisfy discriminant validity, the study also checks for cross-loadings i.e. the loadings of each item should be more on a particular construct than any other construct. The absence of cross-loadings among the items verifies that one item is explaining more variance of a particular construct than any other construct (Henseler et al., Citation2009). The present study verifies the absence of cross-loadings among the items and satisfies the discriminant validity of the construct (see Table ).

Table 9. Cross-loadings

5. Discussion

The present study analyzes and validates the measurement scale of mental accounting and also empirically establishes and validates that mental accounting as the second-order factor of four constructs i.e. mental budgeting, current income, current assets, and future income. The results are in line with the behavioral life cycle hypothesis (BLCH) (Thaler, Citation1990) and support the existence of a mental accounting system among Indian households. The study has established the existence of mental accounting in different financial choices in two ways. Firstly, the study uses the vignettes method to understand the four concepts i.e. segregation of gains, integration of small losses, segregation of small losses from higher gains, and integration of gains received in the same day (Thaler, Citation1985), to explain the uses of the reference point in individual perception of gains and losses. Secondly, the concept of BLCH has been used to expose the mental accounting system in individual differences in financial choices.

The current study replicates the use of reference points in mental accounting theory in the Indian context. The four concepts of segregation and integration of gains and losses have shown clear evidence of the mental accounting system among Indian households. We further extend the scope of the study to investigate and establish the influence of mental accounting in individual financial decision making of Indian households (Mahapatra et al., Citation2019).

The mental accounting concepts developed here highlight the presence of differences in the individual choices of saving and spending money. The items used in the survey highlight the individual’s tendency for different mental conventions for the defining of payments (Prelec & Loewenstein, Citation1998).The results establish the presence of the mental accounting system among Indian households and reinforce the role of psychological processes that drive financial decisions.

Understanding of mental accounting can potentially improve the households’ financial decision making, which would ultimately increase savings and welfare, and would result in well-organized financial planning. Individuals’ financial planning decisions are associated with self-control (Mahapatra & Mishra, Citation2020). Studies support the association of self- control with financial behavior (Howlett et al., Citation2008; Mahapatra & Mishra, Citation2020; Vohs & Faber, Citation2007).

Mental accounting helps to improve self-control (Griesdorn et al., Citation2014). As proposed by Shefrin and Thaler (Citation1988), money earmarked with an emergency fund will lower the propensity to consume. Self-control can be imposed by the Government or Financial Institution on long term saving, by limiting the access to withdrawal with penalties (Griesdorn et al., Citation2014). Longer time horizon savings plans can be observed mostly among households with higher self-control (Rabinovich & Webley, Citation2007). Self-control is influenced by mental accounting and saving rules (Rha et al., Citation2006). The concept of self-control and self-regulation are similar (Griesdorn et al., Citation2014), therefore mental accounting influences the self-regulation of individuals towards financial decisions.

An individual without self-regulation is more impulsive in spending than the individual with deeper self-regulation (Vohs & Faber, Citation2007). Behavioral life cycle variables increase the saving likelihood which combined with self-regulation will have an increased impact on the propensity to save (Rha et al., Citation2006).

The study would be useful for the investors in checking and controlling their self-driven mental accounting process and would result in more savings and less unnecessary spending. It may also prove helpful in understanding investors’ preferences and might provide aid to the financial professionals in understanding customer cognitive perception for profiling their customers.

6. Limitation and future guidelines

The study used a purposive sampling method and targeted salaried employees. The present study only considered the presence of a mental accounting system among Indian households and presented the measurement scale of the same. The study can further be extended to analyze the influence of the mental accounting system in various financial decisions i.e. managing cashflow, investment decisions, insurance planning, retirement planning, etc. Further understanding of research-based choices and investors’ preferences can also be explained.

correction

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

Notes on contributors

Mousumi Singha Mahapatra

Mousumi Singha Mahapatra is an assistant professor at the Institute of Public Enterprise (IPE), Hyderabad. She is having a Ph.D degree in the area of behavioral finance and personal financial planning. She has more than nine years of research and teaching experience. Her broad areas of research interests include household finance, personal financial planning, behavioral finance, financial well-being, risk tolerance, financial attitude, money attitude, risk attitude, and financial satisfaction.

Ramkumar Mishra

Ramkumar Mishra is the Senior Professor and the Director of IPE is a widely recognized expert in public enterprise management. Previously he worked as a visiting fellow at London Business School, International Teachers program (Management) SDA Bocconi, Milan, Italy, and taught at the University of Broad ford. He is a member of several international study teams. He is a Non-Executive Director on some Public and Private Enterprise Boards in India. His areas of interest include Corporate Governance, International Management, International Finance, Public-Private Partnership, Restructuring, and Environmental Administration.

References

- Agarwal, R., & Karahanna, E. (2000). Time flies when you’re having fun: Cognitive absorption and beliefs about information technology usage. MIS Quarterly, 24(4), 665–17. https://doi.org/10.2307/3250951

- Alexander, C. S., & Becker, H. J. (1978). The use of vignettes in survey research. Public Opinion Quarterly, 42(1), 93–104. https://doi.org/10.1086/268432

- Ando, A., & Modigliani, F. (1963). The “life cycle” hypothesis of saving: Aggregate implications and tests. The American Economic Review, 53(1), 55–84. https://www.jstor.org/stable/1817129

- Bachmann, L. M., Mühleisen, A., Bock, A., Ter Riet, G., Held, U., & Kessels, A. G. (2008). Vignette studies of medical choice and judgement to study caregivers’ medical decision behaviour: Systematic review. BMC Medical Research Methodology, 8(1), 50. https://doi.org/10.1186/1471-2288-8-50

- Baeckström, Y., Silvester, J., & Pownall, R. A. (2018). Millionaire investors: Financial advisors, attribution theory and gender differences. The European Journal of Finance, 24(15), 1333–1349. https://doi.org/10.1080/1351847X.2018.1438301

- Barter, C., & Renold, E. (2000). ‘I wanna tell you a story’: Exploring the application of vignettes in qualitative research with children and young people. International Journal of Social Research Methodology, 3(4), 307–323. https://doi.org/10.1080/13645570050178594

- Bernheim, B. D., Skinner, J., & Weinberg, S. (2001). What accounts for the variation in retirement wealth among US households? American Economic Review, 91(4), 832–857. https://doi.org/10.1257/aer.91.4.832

- Cheema, A., & Soman, D. (2006). Malleable mental accounting: The effect of flexibility on the justification of attractive spending and consumption decisions. Journal of Consumer Psychology, 16(1), 33–44. https://doi.org/10.1207/s15327663jcp1601_6

- Chin, W. W. (1998). The partial least squares approach to structural equation modeling. Modern Methods for Business Research, 295(2), 295–336.

- Cohen, J. (1992). A power primer. Psychological Bulletin, 112(1), 155. https://doi.org/10.1037/0033-2909.112.1.155

- Edwards, J. R. (2001). Multidimensional constructs in organizational behavior research: An integrative analytical framework. Organizational Research Methods, 4(2), 144–192. https://doi.org/10.1177/109442810142004

- Feldman, N. E. (2010). Mental accounting effects of income tax shifting. The Review of Economics and Statistics, 92(1), 70–86. https://doi.org/10.1162/rest.2009.11892

- Fornell, C., & Bookstein, F. L. (1982). Two structural equation models: LISREL and PLS applied to consumer exit-voice theory. Journal of Marketing Research, 19(4), 440–452. https://doi.org/10.1177/002224378201900406

- Fornell, C., Larcker, D. F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Journal of Marketing Research; 18(3), 382–388. DOI:10.1177/002224378101800313

- Gourville, J. T., & Soman, D. (1998). Payment depreciation: The behavioral effects of temporally separating payments from consumption. Journal of Consumer Research, 25(2), 160–174. https://doi.org/10.1086/209533

- Griesdorn, T., Lown, J. M., DeVaney, S. A., Cho, S. H., & Evans, D. (2014). Association between behavioral life-cycle constructs and financial risk tolerance of low-to moderate-income households. Journal of Financial Counseling and Planning, 25. http://search.ebscohost.com/login.aspx?direct=true&db=bth&AN=102199834&site=ehost-live

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2), 139–152. https://doi.org/10.2753/MTP1069-6679190202

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2013). Partial least squares structural equation modeling: Rigorous applications, better results and higher acceptance. Long Range Planning, 46(1–12), 1–12. https://doi.org/10.1016/j.lrp.2013.01.001

- Hair, J. F., Sarstedt, M., Pieper, T. M., & Ringle, C. M. (2012). The use of partial least squares structural equation modeling in strategic management research: A review of past practices and recommendations for future applications. Long Range Planning, 45(5–6), 320–340. https://doi.org/10.1016/j.lrp.2012.09.008

- Hair, Jr., J. F., Sarstedt, M., Matthews, L. M. and Ringle, C. M. (2016). Identifying and treating unobserved heterogeneity with FIMIX-PLS: Part I – method. European Business Review, 28(1),. 63–76. https://doi.org/10.1108/EBR-09-2015–0094

- Heath, C. (1995). Escalation and de-escalation of commitment in response to sunk costs: The role of budgeting in mental accounting. Organizational Behavior and Human Decision Processes, 62(1), 38–54. https://doi.org/10.1006/obhd.1995.1029

- Heath, C., & Soll, J. B. (1996). Mental budgeting and consumer decisions. Journal of Consumer Research, 23(1), 40–52. https://doi.org/10.1086/209465

- Henseler, J., Ringle, C. M., & Sinkovics, R. R. (2009). The use of partial least squares path modeling in international marketing. In New challenges to international marketing (pp. 277–319). Emerald Group Publishing Limited. https://doi.org/10.1108/S1474-7979(2009)

- Howlett, E., Kees, J., & Kemp, E. (2008). The role of self‐regulation, future orientation, and financial knowledge in long‐term financial decisions. Journal of Consumer Affairs, 42(2), 223–242. https://doi.org/10.1111/j.1745–6606.2008.00106.x

- Hughes, R. (1998). Considering the vignette technique and its application to a study of drug injecting and HIV risk and safer behaviour. Sociology of Health & Illness, 20(3), 381–400. https://doi.org/10.1111/1467-9566.00107

- Jensen, E. J., Stum, M., & Jackson, M. (2019). What makes inheritance fair in stepfamilies? Examining perceptions and complexities. Journal of Divorce & Remarriage, 60(3), 234–252. https://doi.org/10.1080/10502556.2018.1488123

- Johnson, R. E., Rosen, C. C., Taing, M. U., Taing, M. U., & Taing, M. U. (2012). Recommendations for improving the construct clarity of higher-order multidimensional constructs. Human Resource Management Review, 22(2), 62–72. https://doi.org/10.1016/j.hrmr.2011.11.006

- Karlsson, N., Garling, T., & Selart, M. (1997). Effects of mental accounting on intertemporal choice. https://nbn-resolving.org/urn:nbn:de:0168-ssoar-399008

- Ko, K. J., & Huang, Z. (2012). Persistence of beliefs in an investment experiment. The Quarterly Journal of Finance, 2(1), 1250005. https://doi.org/10.1142/S201013921250005X

- Koka, B. R., & Prescott, J. E. (2002). Strategic alliances as social capital: A multidimensional view. Strategic Management Journal, 23(9), 795–816. https://doi.org/10.1002/smj.252

- Lohmöller, J. B. (1989). Predictive vs. structural modeling: Pls vs. ml. In Latent variable path modeling with partial least squares (pp. 199–226).

- MacKenzie, S. B., Podsakoff, P. M., & Podsakoff, N. P. (2011). Construct measurement and validation procedures in MIS and behavioral research: Integrating new and existing techniques. MIS Quarterly, 35(2), 293–334. https://doi.org/10.2307/23044045

- Mahapatra, M. S., & Mishra, R. K. (2020). Role of self-control and money attitude in personal financial planning. The Indian Economic Journal, 0019466220933408. https://doi.org/10.1177/0019466220933408

- Mahapatra, M. S., Raveendran, J., & De, A. (2019). Building a model on influence of behavioural and cognitive factors on personal financial planning: A study among Indian households. Global Business Review, 20(4), 996–1009. https://doi.org/10.1177/0972150919844897

- Maital, S., & Maital, S. L. (1994). Is the future what it used to be? A behavioral theory of the decline of saving in the West. The Journal of Socio-economics, 23(1–2), 1–32. https://doi.org/10.1016/1053-5357(94)90018-3

- Polites, G. L., Roberts, N., & Thatcher, J. (2012). Conceptualizing models using multidimensional constructs: A review and guidelines for their use. European Journal of Information Systems, 21(1), 22–48. https://doi.org/10.1057/ejis.2011.10

- Prelec, D., & Loewenstein, G. (1998). The red and the black: Mental accounting of savings and debt. Marketing Science, 17(1), 4–28. https://doi.org/10.1287/mksc.17.1.4

- Rabinovich, A., & Webley, P. (2007). Filling the gap between planning and doing: Psychological factors involved in the successful implementation of saving intention. Journal Of Economic Psychology, 28(4), 444–461. https://doi.org/10.1016/j.joep.2006.09.002

- Rahman, N. (1996). Caregivers’ sensitivity to conflict: The use of the vignette methodology. Journal of Elder Abuse & Neglect, 8(1), 35–47. https://doi.org/10.1300/J084v08n01_02

- Rainwater, L., Coleman, R. P., & Handel, G. (1959). Workingsman’s Wife: Her Personality, World and Life Style. Oceana.

- Rha, J. Y., Montalto, C. P., & Hanna, S. D. (2006). The effect of self-control mechanisms on household saving behavior. Journal of Financial Counseling and Planning, 17, 2. https://www.afcpe.org/wp-content/uploads/2018/10/vol-1722-self-control-mechanisms.pdf

- Richman, J., & Mercer, D. (2002). The vignette revisited: Evil and the forensic nurse. Nurse Researcher (Through 2013), 9(4), 70. https://doi.org/10.7748/nr2002.07.9.4.70.c6199

- Schoenberg, N. E., & Ravdal, H. (2000). Using vignettes in awareness and attitudinal research. International Journal of Social Research Methodology, 3(1), 63–74. https://doi.org/10.1080/136455700294932

- Shefrin, H. M., & Thaler, R. H. (1988). The behavioral life‐cycle hypothesis. Economic Inquiry, 26(4), 609–643. https://doi.org/10.1111/j.1465-7295.1988.tb01520.x

- Shefrin, H. M., & Thaler, R. H. (1992). Mental accounting, saving, and self-control. In G. Loewenstein & J. Elster (Eds.), Choice over time (pp. 287–330). Russell Sage Foundation. (A previous version of this chapter was published in “Economic Inquiry,” Oct 1988) https://psycnet.apa.org/record/1993-97149-012

- Statman, M. (1999). Behaviorial finance: Past battles and future engagements. Financial Analysts Journal, 55(6), 18–27. https://doi.org/10.2469/faj.v55.n6.2311

- Thaler, R. (1980). Toward a positive theory of consumer choice. Journal of Economic Behavior & Organization, 1(1), 39–60. https://doi.org/10.1016/0167-2681(80)90051-7

- Thaler, R. (1985). Mental accounting and consumer choice. Marketing Science, 4(3), 199–214. https://doi.org/10.1287/mksc.4.3.199

- Thaler, R.H. (1988). Anomalies: The ultimatum game. Journal of Economic Perspectives, 2(4), 195–206. https://doi.org/10.1257/jep.2.4.195

- Thaler, R. H. (1990). Anomalies: Saving, fungibility, and mental accounts. The Journal of Economic Perspectives, 4(1), 193–205. https://doi.org/10.1257/jep.4.1.193

- Thaler, R. H. (1994). Psychology and savings policies. The American Economic Review, 84(2), 186–192. https://www.jstor.org/stable/2117826

- Thaler, R. H. (1999). Mental accounting matters. Journal of Behavioral Decision Making, 12(3), 183. https://doi.org/10.1002/(SICI)1099-0771(199909)12:3<183::AID-BDM318>3.0.CO;2-F

- Thaler, R. H. (Ed.). (2005). Advances in behavioral finance (Vol. 2). Princeton University Press.

- Vohs, K. D., & Faber, R. J. (2007). Spent resources: Self-regulatory resource availability affects impulse buying. Journal of Consumer Research, 33(4), 537–547. https://doi.org/10.1086/510228

- Wetzels, M., Odekerken-Schröder, G., & Van Oppen, C. (2009). Using PLS path modeling for assessing hierarchical construct models: Guidelines and empirical illustration. MIS Quarterly, 33(1), 177–195. https://doi.org/10.2307/20650284

- Wilson, B., & Henseler, J. (2007). Modeling Reflective Higher-Order Constructs using Three Approaches with PLS Path Modeling: A Monte Carlo Comparison. In M. Thyne, & K. R. Deans (Eds.), ANZMAC 2007: Conference proceedings and refereed papers (pp. 791–800). Dunedin: ANZMAC. https://research.utwente.nl/en/publications/modeling-reflective-higher-order-constructs-using-three-approache

- Wilson, J., & While, A. E. (1998). Methodological issues surrounding the use of vignettes in qualitative research. Journal of Interprofessional Care, 12(1), 79–86. https://doi.org/10.3109/13561829809014090

- Winnett, A., & Lewis, A. (1940). Household accounts, mental accounts, and savings behaviour: Same old economics rediscovered? Journal of Economic Psychology, 16(3), 431–448. https://doi.org/10.1016/0167-4870(95)00019-K

- Wright, B. E. (1940). The unemployed worker. Yale University Press.