?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper aims at understanding the implication of pension debt on fiscal policy in Tanzania. The paper employed a modified projected benefit obligation (PBO) approach for a period between 2010 and 2018. The results of the paper indicate a mismatch between benefit payments and members’ contributions, in that outflows are found to exceed inflows for a large part of the examined period, which tends to imply that pensions adequacy is questionable, and that the system cannot be sustained for a longer period if no rescue is put in place immediately. Further, drawing from the computed life expectancy of pensioners, it is indicative that the size of the retirement age cohort will continue to enlarge over time; which would result in increasing pension obligations. Since increased pension expenditure would not be fully covered from the existing pension assets, the Government as a guarantor would be required to cover the matured pension obligations through its annual fiscal budget. Unfortunately, looking at the current National Debt sustainability report pension debt is not part of the proposed national debt. Following these findings, and since neither increasing the contribution rate nor the retirement age may not be sustainable options, the reduction of accrual rate is the most suitable option the government is recommended to implement so as to rescue the current situation. However, in a long run, the paper recommends the government to undertake a systemic pension reform, which would change the entire pension system from a defined benefits scheme to a defined contributions scheme.

PUBLIC INTREST STATEMENT

As people develop through their lifetime, they have an expectation that a time will come when they will be able to retire. Many employers also take the view that, while their employees are working, they should be building up an entitlement to a pension when they retire. This paper opens up the understanding of readers about the challenges faced by Tanzanian pensioners on the observed mismatch between benefit payments and members’ contributions, in that outflows are found to exceed inflows which tends to imply that pensions adequacy is questionable, and that the pension system in Tanzania cannot be sustained for a longer period if no rescue is put in place immediately. However, in a long run, the government is advised to undertake a systemic pension reform, which would change the entire pension system from a defined benefits scheme to a defined contributions scheme.

1. Introduction

While most of the countries around the world in an attempt to honour their monetary obligations focus on conventional public internal and external debt, they tend to a greater extent assessing and reporting public guarantees that form a large chunk of public liabilities (Kelley, Citation2014: Splinter, Citation2017). Such guarantees include obligations implicit in guarantees of bank deposits, export schemes, rural credit programs, home Mortgages and student loans (Kane & Palacios, Citation1996; Sane & Thomas, Citation2015). Because of the challenges and complexities in measuring and monitoring such hidden liabilities there has been a genuine concern about the way these may affect macroeconomic variables. Among such liabilities, there are public and private pension liabilities, which fall under the government guarantee. In Tanzania, according to the PSSSF Act, public pensions are guaranteed by the government (URT, Citation2018).

Globally, many states differ in the way they honor the obligations associated with old age pension. Some government finances, their pension obligation through the current budget (Sweden. Japan and Canada) while other countries such as USA, UK and Swiss Government build up reserves to finance matured pension obligations (Bovenberg & Petersen, Citation1992; Palacios, Citation1996). Building up reserves would assist to ease the financial burden to the government when pension obligation falls due. In practice, the inclusion of implicit pension debt to the stock of public debt would enable the government to arrive at a better measure for the public Debt.

In essence, pension liability reflects three interrelated developments. First, governments increased worries about inter-temporal balance or lack thereof of their fiscal accounts in a globalized world. Second, many countries have started to reform their pension systems since the 1990s; and, many of such reforms involved a shift from unfunded, defined benefits schemes to a multi pillar schemes with a fully funded component in order to ensure sustainability of the social security system’s inability of the social security system, see also (Beltrametti & Della Valle, Citation2011; Holzmann, Citation1998). Finally, the estimated pension debt serves as an indicator of whether reforms have been effective in improving the Government’s balance sheet.

In this respect, the estimated pension debt, provide a better performance indicator as insisted by Palacios et al. (Citation2004) that estimate about the initial and reform—induced changes in pension debt are paramount during restructuring of a pension system so as to have a clear understanding of the extent of pension obligations. The level of pension debt is normally employed as a tool to gauge against the matured benefit payment obligations; meanwhile, the importance of assessing pension debt emanates from the fact that as a country plans for its macroeconomic interventions, it also needs to understand the magnitude of the and the type of reforms required to address the debt.

It is through the pension debt analysis where the government could be assured of the effectiveness of its reforms both during the short- and long-run period. Moreover, pension debt is usually taken into consideration when establishing a new scheme, especially a defined benefits scheme. The purpose of assessing pension liabilities before establishing any pension scheme is to ensure that benefit payments do not cause unnecessary pressure from any potential increase in tax burden to future population.

The Public Debt includes external and domestic debt. The domestic debt, according to the Ministry of Finance reports include Treasury bills, Treasury Bonds, special Bonds, Overdrafts, liquidity papers and other guarantees. Hence, in Tanzania, public debt does not include pension debt as one of the components, (MOF, Citation2018). Further, most of the pension schemes were established without taking into consideration the impact of the p ension debt to the national debt. Meanwhile, the analysis of public debt seems to be missing in the actuarial valuations in Tanzania. This has resulted in a situation that some of the schemes are already creating a fiscal burden due to mismatches between cash inflows and outflows whose impact to the Government obligation could hardly be established. It could be noted, however, that pension obligations are certain and obvious (United Nations Children’s Fund (Citation2019); Alaedini (Citation2013)). It follows, therefore that, macroeconomic policy should not be limited to the traditional public debt as advocated by Rizzo (Citation1999) and Hills (Citation1984). This is due to the fact that pension debt created during the process of administering pensions should be managed such that pension assets and maturing pension debt obligations are harmonized (Schwarz & Demirgue-Kunt, Citation1999).

There has been a growing concern about the funding status of defined benefit pension plans both in Tanzania, and globally. There are a large number of employees in both private and public sectors who dearly depend so much on defined benefit pension plan for their retirement. Unfortunately, defined pension plans currently seem much less secure than initially anticipated and many current and future retirees might receive less than expected out of their pensions. Apparently, this is the concern of so many prospective retirees in Tanzania. A study which may throw light on the status of the Government pension debt may be useful to the prospective pensioners, Government and pension stakeholders and may serve as an important input to MTFF model (Suescun, Citation2020). This paper, therefore, aims at coming up with an empirical evidence of the growing pension debt burden in order to inform macroeconomic policies in Tanzania. The paper also informs policy makers on the implementation of pension policy reforms on the development of social protection policy that addresses SDGs (United Nations Children’s Fund, Citation2019), Five Years Develop plan, and vision 2025. Also, the paper uses actuarial models to assess the financial sustainability of Tanzania’s pension plan. The actuarial projection results could provide positive policy implications for Tanzania’s structural and incremental reforms on the pension system, as well as offering experiences for other developing countries under similar circumstances.

The reminder of this paper is organized as follows; section two presents the introduction. While section two discusses the theoretical and empirical literature on pension debt, section three presents the methodology used in the paper. The analytical evidence of the paper is provided in section four before we conclude and provide policy recommendations in the final.

2. Theoretical underpinning

2.1. Pension debt concept

There are a number of methods of calculating pension debt, such as Accumulated Benefit Obligation (ABO), Projected Benefit Obligation (PBO), Entry Age Normal (EAN), and Projected Value of Benefits (PVB). The Accumulated Benefit Obligation (ABO) or termination liability is based on the fact that any pension fund, which currently has active members, they have a benefit package, which has already been promised to members and has been accrued even if the scheme is closed and no more new registration of members. In this case, the ABO is not influenced by uncertainty future salaries because cash flows associated with the ABO are based completely on the information known today (Bodie, Citation1990).

The application of ABO has been criticized as a very narrow measure of liabilities because it considers the accrued liability focusing on current salary and years of service. While in a typical pension scheme, a member accrues the right to pension retirement that equals a replacement of his/her final (or late-career) salary times years of service with the employer. If salary increases with years of his/her career for a given member, the member’s ABO grows in a curved shape with years of service. Thus, the ABO postpones a large share of accrued benefit rights until late in the member career’s life. The newly accrued liability under the ABO rises pungently towards retirement (Ibid).

A broader measure than the ABO is the Projected Benefit Obligation (PBO), which applies to project future wage increases in calculating today’s pension debt without taking in consideration future years of career. An even broader concept is the Projected Value of Benefits (PVB), which discounts a full projection of what current workers are expected paid if their wage grows (Treynor (Citation1976), Bulow (Citation1982), and Bodie (Citation1990)). Graphical presentation shows that ABO gives low provision of pension debt; many governments would prefer ABO due to the fact that it undermines the level of the public debt. However, regardless the method of assessing the pension debt, in long run they yield the same results. The application of ABO makes the government more conservative and less cautious on the debt burden.

2.2. Theoretical perspective

2.2.1. The theory of pension underfunding

A pension plan is “underfunded” and the government deems not “fiscally sound” if it lacks the assets to pay all of the future liabilities, and this clearly predicts the future trouble the degree of which can be clearly measured conveniently by unfunded liability, and since the liabilities of any pension system are typically large compared to the size of the budget, the unfunded part of that liability often seems immense, Robert et al. (Citation2004). The blames for pension underfunding are shared among both the employer and the government, but a great share of the blames is pushed to the government.

According to Robert et al. (2004), this problem is accelerated by government’s discretion to change the pension formula and thereby partially default on their liabilities. While this could create a distinction between government bonds and pension promises, this is a matter of degree; it may be easier to default on pension promises than bonds, but neither is without cost. On the one hand, it is highly unrealistic to assume that the pension obligations can be avoided altogether. There are few recorded cases of complete default on pension liabilities even in extreme cases. Rather, the argument holds that usually the government finds it easier to reduce its pension liability than to default or restructure its official public debt. Indeed, the frequent number of cost saving revisions to defined benefit formulas in public schemes over the last few decades seems to confirm this assertion (e.g., see Schwarz & Demirgue-Kunt, Citation1999). The true extent to which pension promises are more “flexible” will depend on an assessment of the ability of the government to reduce benefits, which in turn, will depend on the political and social environment. The public’s perception of their “entitlement” to the payments, the ease with which they can observe the changes to often-complex benefit formulas, and the average age of the population are among the factors that are likely to determine how much room a government has to manoeuvre.

2.2.2. Life-cycle hypothesis (LCH)

The fiscal policy implication of the pension debt is contextualized in the Life-Cycle Hypothesis (LCH) of savings and consumption. The LCH assumes that consumption and saving behaviour is predicated on the individual’s position in the life cycle. At a young age, those entering the labour force are assumed to have relatively low incomes and low saving rates, with the likelihood of dis-saving to meet their current consumption; whereas at the other end, for those in retirement, their income is assumed to decrease (Baranzin, Citation2005). During the middle working years, an income is assumed to rise sharply relative to consumption, to peak, and then start to decline.

Thus, savings tend to be positive in this period. Accordingly, the LCH predicts a decrease in savings as aging ultimately takes effect (Modigliani, Citation1966, Citation1986; Modigliani & Sterling, Citation1983). For an economy, the LCH hypothesizes a specific relationship between savings and age. The economy would be negatively affected if pension assets were to be insufficient and failed to finance pension payments. The arising pension liability would have to be borne by the government, with the attendant fiscal implications.

According to the life-cycle theory of consumption and saving, individuals try to maximize the utility deriving from their entire life-cycle consumption (ibid.) Explains further that consumption must be continuous, even if income through the life-cycle is discontinuous; and saving primarily finance consumption during retirement. Thus, LCH is consistent with the principle of pension schemes, which requires that a stream of income to a retiree should be adequate enough to enable the retiree to afford a decent life. In this regard, a pension scheme is one of the important components of financing consumption during the retirement period

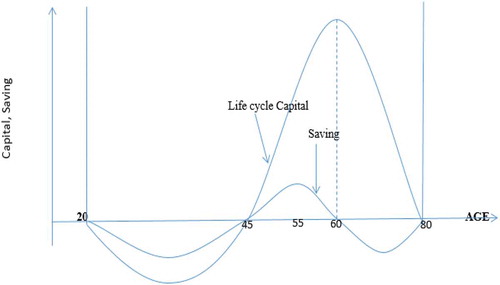

The discussed Life-Cycle Hypothesis is depicted in Figure . The figure shows that at the age of 20 when a typical young Tanzanian is assumed to start earning from employment, she begins without any savings up to the age of 45. This 20–45 age cohort is assumed to earn less income than it spends; hence, it is likely to be surviving on borrowing or on financial assistance from close relatives. Between the ages 46 and 60, a Tanzanian worker is assumed to earn surplus income over and above his or her current expenditure as to afford to save, and saving reaches a maximum at the age of 60, the statutory retirement age. At the age of 60 and above, retirees live on retirement benefits, which is a form of dis-saving from their forced savings in pension schemes. The Pension Funds would experience rising incomes from members’ contributions when their members are in the late forties and in the fifties. Thus, if the system is in equilibrium and pension benefits are actuarially neutral, the pension debt will be bearable and the system will remain sustainable.

2.3. Empirical literature

The empirical literature on the relationship between pension debt and its fiscal implications is scanty, and a majority of the studies undertaken are on developed economies. This study contributes to reducing the gap of the dearth of empirical studies on the relationship in developing countries.

Romp and Beetsma (Citation2020) studied the sustainability of pension arrangements basing on voluntary individual participation and the cost of their collapse. Results of the study indicated that the need for making participation mandatory is limited when the promised return on the contribution to the arrangement is set optimally, because the cost of a permanent loss of the intergenerational risk-sharing benefits is sufficiently large to make a collapse of these optimal arrangements unlikely. Romp analysis applied three important components, namely a PAYG pension scheme, a pension fund with a minimum return on contributions, but without a buffer, and a fund with a minimum return and a buffer. The study found practical implications for pension policies, as financial and demographic developments they prompt enhanced supervisory scrutiny. And when asset returns are sufficiently large, the reserves create some adequate fund, which could be use lower the contributions.

Splinter (Citation2017) examined fiscal stress to the state legislators to either raise taxes or cut spending. The study indicated that states could cut their pension contributions at seven times the rate of other spending in response to fiscal stress. Further the cumulative impact of state under-contributions due to fiscal stress explained about 4% of the mid-2008 actuarial underfunding. The study revealed that States did not pay actuarially required contributions in order to mitigate fiscal stress. Similarly, study findings revealed that investment returns explained little underfunding. However, much underfunding appeared to be caused by insufficient employee and actuarially required by government contributions to keep up with growing pension liabilities.

Sane and Thomas (Citation2015) examined the contribution and persistence in contributing to the national, voluntary, defined contributory pension programme, where the government provides the incentive of matching contributions of a minimum amount (USD 16). The study applied data from a financial services firm where 12% of customers (37,000 individuals) chose to participate in the scheme. Findings show that about 50% of members reached the minimum level of co-contribution, but that participants persist in contributing even if they failed to contribute the minimum amount in a given year. The study concluded on the willingness of the informal sector player to participate in a state-run voluntary pension programme in an emerging market where access to formal finance is limited.

Kelley (Citation2014). Studied a public choice approach to the problem of unfunded pension liabilities and adopts the methodology of Congleton and Shughart (Citation1990) to model underfunding of public pension plans using the median voter theorem, and the theory of “capture” by special interest groups. The study combined the two models using panel data from 2001 to 2009. The findings of the study showed strong description for the current levels of unfunded liabilities; implying that both median voter preferences and special interest group affect political outcomes. Further, the study found that the special interest group model slightly outperformed the median voter model Hurd et al. (Citation1993) calculated unfunded pension liabilities of seven industrialized countries, including Canada, France, Italy, United Kingdom, USA and [former] West Germany. The study applied the Accrued Benefit Obligation (ABO) approach to the 1990 data set and projected pension liabilities up to 2015. In projecting the pension liabilities, the ABO approach considers future wage growth, mortality rates and existing public pension reserves.

The study found that accrued pension obligations were in general more than twice the public debt, with variation in results across countries. For example, the study found that the accrued benefit obligations relative to the gross debt were, for Canada, 121% of the GDP against 96% of the GDP; for France, 216% of the GDP against 48% of the GDP; and for the UK, 156% against 46% of the GDP.

Chand et al. (Citation1996) sought to establish the pension debt for eight OECD countries, including Canada, France, Italy, Japan, Sweden, the United States, the United Kingdom, and [former] West Germany. The study used the Projected Benefits Obligations (PBO) approach, which computes the present liability accruing to pensioners and insured members. The study found that the pension liability as a percentage of the GDP was 94% in Canada; 265% in France; 357% in Italy; 166% in Japan; 31% in Sweden; 117% in the UK; and 106% in the USA.

Kune (Citation1996) calculated pension liabilities from Pension Obligations (PBO) and Accrued Benefits Obligation (ABO) approaches, for twelve European Union countries using 1990 data, assuming the maximum period of the projection to be 40 years. The study covered beneficiaries who were over 25 years old, including beneficiaries of survivors’ benefits. The current value of average real pension was calculated without taking into consideration future increase in life expectancy.

With the PBO approach, the study found that the implicit pension debt as a ratio of the GDP for the respective countries was as follows: Belgium, 101%; Denmark, 117; for France, 112%; Greece, 245%; Iceland, 78%; Italy, 207%; the UK, 95%, and [former] West Germany, 186%.

With the Accrued Benefit Obligation (ABO) approach, the study found that the pension liability as a ratio of the GDP were slightly lower in all countries as follows: Belgium, 75%; Denmark, 87%; France, 83%; Greece, 185%; Iceland, 55%; the UK, 68%; and [former] West Germany, 138%.

Holzmann et al. (Citation2004) estimate pension liabilities with a Pension Reform Option simulation toolkit (PROST) using data for the 1999/2000 period for 35 low- and middle-income countries, including only North African countries from Africa. Brazil was found to have the highest pension debt of 500% of GDP. By using a higher discount rate of 5%, the pension debts of 18 countries out of 35 countries were found to be higher than their national incomes. In addition, the study also established that moving from wage-based benefits to price indexation of benefits reduced the pension debt by 15 to 20%.

Mark et al. 2010 Analyzed wage growth by age, as well as the age-service distribution of workers, based on CAFRs from the 10 states with the largest pension liabilities. They assumed that a 65-year-old worker with 45 years of service would earn 100,000. USD They also applied a 3.5% inflation rate, a 2% benefit formula, a 3% fixed cost of living adjustment (COLA), an 8% discount rate, and death probabilities taken from the RP2000 combined mortality. Results showed that The EAN for active workers was about 0.4 USD trillion larger than the ABO for active workers using taxable money rates and 1.0 USD trillion using Treasury rates. Salary risk reduces the difference between the EAN and the ABO to 0.3 USD-$0.8 trillion. Assets in state pension funds were worth approximately 1.94 USD trillion as of June 2009. Also, for comparison, total state non-pension debt was 1.00 USD trillion and total state tax revenues were 0.78 USD trillion in 2008. They concluded that governments are much more likely to default on payments above 36 and beyond the ABO than they are to default on the ABO it. The cash flows above and beyond those associated with the ABO should therefore be discounted at a higher rate to reflect that greater default risk. Second, the cash flows that are not recognized in the ABO vary with wage growth, which may be correlated with pricing risk factors.

Holzmann (Citation1999) investigated the implicit pension debt to estimate the impact of the future path under an unreformed system in the OECD. The study assessed variations of the new implicit pension debt and found that reforms substantially had different paths. The change from wage to price indexation (with insurable wage growth of 2%) was found to have only mild effects on financial balance of the scheme. However, with respect to pension debt, a shift from wage to price indexation resulted in almost half of the reduction of the pension debt (that is, about 30% of GDP on a typical matured OECD pension scheme).

As already pointed out, the literature of pension debt in Africa is very scarce. Sundeep (Citation2008) carried out a descriptive analysis of the pension system in Kenya and concluded that the pension reforms needed to be deepened and broadened; and institutional structures of the pension system needed to be strengthened.

Robalino and Bogomolova (Citation2006) assessed the pension debt for 6 countries in the Middle East and North Africa (MENA) region. Using a World Bank Pension Reform Options Simulation Toolkit (PROST), the study found pension debts to be in the range of 50% to 100% of the GDP, which was higher than the explicit public debt. In addition, large schemes were found to have negative pension assets.

To sum up, the review of the literature indicates that most of the estimates of pension liability have been undertaken in developing countries, which point to a dire need to undertake more studies on developing countries. Secondly, the approaches taken by the studies varied; as well, the results were different. As such, the available evidence is still contentious, which justifies a need for additional empirical evidence.

3. Methodology

3.1. Measurement of variables and data type

Two common approaches to pension debt are the Accrued Benefits Obligations (ABO) approach (Hurd et al., 1993; Kune, Citation1996) and the Projected Benefits Obligations (PBO) approach (Chand et al., 1996; Kune, Citation1996). Of these two, the study has adopted the PBO approach, as explained earlier.

The fiscal implications of the pension debt are investigated by using “projected liability,” which is described as the present value of the expected cash inflows to current members on the basis of their contributions up to a certain specified period. This definition entails the likelihood that “current” members could die before reaching the pensionable age. Hence, a model for mortality of members and pensioners as developed in Isaka (Citation2017).

The computations of pension debt are based on pension expenditures, which relates to long-term benefits (pensions only) of two pension schemes the National Social Security Fund (NSSF) and the Public Services Social Security Fund (PSSSF) which was a merger of the then Parastatal Pension Fund (PPF), Local Authority Pension Fund (LAPS) and Private Sector Pension Fund (PSPF). This approach is taken because pension payments are a long-term liability (accrued benefits) of the schemes and have fiscal implication of the government. Administrative costs of the schemes were obtained from the audited account reports of the pension funds for a period of 5 financial years (2009/10–2019/20). The demographic data were obtained from the National Bureau of Statistics (NBS) and from the database of pension schemes.

Projections of annual demographic data were carried out using the Excel program up to 2045, on the assumption that fertility of the general population will remain unchanged (URT, Citation2013b). The choice of 2045 was for the reason that a young person who joined the pension scheme in 2015 at the age of 25 may retire voluntarily in 2045 or mandatory in 2050.

3.2. Data sources

Data for wage growth were calculated based on the wage bill data reported by the NBS (URT, Citation2018). No assumptions were made on indexation of benefits because at present, the approach is not mandatory for the schemes to follow or use. However, in assessing improvements in the adequacy, the indexation rate developed in Paper 3 was used in the analysis. The discount rate used is 5%, which is equivalent to the penalty charged by the schemes on delayed contributions. The replacement rate used is 67%, which is a simple average of the rates used by the pension schemes covered by the study.

Each cohort of existing old-age pensioners was followed through with the life expectancy, as developed in Isaka (Citation2017). Total costs in each year are a sum of payments for all cohorts and the administrative costs for all cohorts. Growth in membership is simulated by using a 5-year average obtained from the Funds. Surplus or deficit is obtained by deducting costs from total income, whereas the latter is an aggregate of both contributions and investment incomes.

3.3. Analytical approach

3.3.1. The approach

This paper employs a modified projected benefit obligation (PBO) approach which considers survival probabilities of scheme members and pensioners. The approach has been adopted because it has been popular in the literature on the estimation and assessment of pension liabilities. However, in the reviewed literature, studies that have used this approach (for example, Chand et al., 1996; Kune, Citation1996) assume that pension schemes continue to exist until the last member dies, barring for new entrants into the schemes. These studies compute the present values of anticipated benefits to current participants; i.e., they invoke the closed group method. In Tanzania, however, the pension system is open to new members.

Following Beltrametti and Della Valle (Citation2011), pension debt is computed as the present value of benefits that a pension system has to pay to its current members on the basis of their pension (rights) that has accrued prior to the year for which the Implicit Payment Debt (IPD) is calculated.Footnote1

3.3.2. The working definition

Various definitions of pension liability are common in literature. They include; first; the present value of pension accrued at a particular time, to be paid in the future on the basis of accrued rights (liabilities), where neither future contributions nor the accrual of new rights on the basis of the contributions is considered. Second; projected liabilities of the current members and pensioners assuming that pension schemes will continue to exist until the last contributor dies, while new entrants are not allowed; and that both the future contributions of the existing members and their new rights are allowed under current rules. This is referred to as the closed group method of calculating liabilities. Third, the present value of contributions and pensions of new workers under current rules including an option that allows for the inclusion of children who are not yet part of the labour force.

Calculations of pension benefits in Tanzania are made on the basis of future wages where in schemes use either the last salary paid or a 5-year average salary, and the flow of future contributions is used to finance a pension debt (PD) that has already accrued. In a balanced case, the net present value of PD is zero; which means that liabilities (L) are cancelled out with implicit assets (A) at time t, such that:

Where A (t) is implicit assets at time t, L (t) and PD (t) are liabilities and pension debt at at time t, respectively.

Following Settergren et al. (Citation2006), the pension debt PD, that is pension liability (PL) is generated by dividing pension debt by contributions per time (t) as follows;

Where:

C = pension contribution rate; S = salary of members;

= members at age

;

= Discount factor;

survival rate; (t) = maximum age;

is variable of integration; α = Pension indexation;

= Retirees;

Population growth trend;

= replacement rate when there is no-indexation, i.e. (α = 0); EquationEquation 5.2

(5)

(5) can be restated as:

Such that PD

Where

By substituting 5 and 6 the following is obtained

On the asset side income (including both contributions and investment income) features as an important component of social security assets. By that approach, the pension debt (PD) is obtained as:

In a simplified form EquationEquation 5.8(5)

(5) can be restated as:

Generally, the pension system is sustainable if the PD, as expressed in Equationequation 8(8)

(8) , is less or equal to zero (PD

, and becomes insolvent when PD > 0. In the case of insolvency, the pension liability would no longer be pension implicit debt; rather, it would become pension explicit debt. Prudence, in the case of insolvency, would require the Government to include the existing pension obligations in its budget.

4. Empirical results and discussion

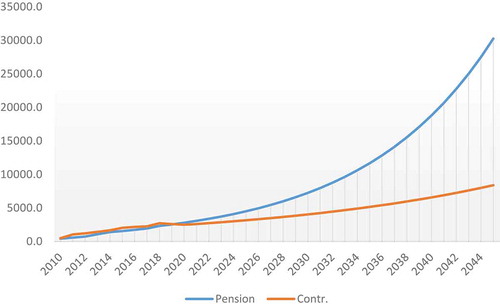

Empirical results, pointed out that actual pension expenditure, which was TZS 426 Billion in 2010 would increase to TZS 2,793 Billion in 2020. The projections from this study denoted that pension expenditure would surpassed members’ contributions in 2020 Figure . However, since there is adequate investments income, there would be a cushion to payment of pension obligation, without necessarily require Government intervention. Further projections of the pension debt denoted that pension expenditure would expand theatrically from 2021 onwards and in 2025 pension expenditure would enlarge to TZS 4,498 Billion, this amount would outweigh both contributions income (TZS 3,160 Billion) and investment income (TZS 1,165 Billion).

Figure 2. Pension expenditure vs contribution income

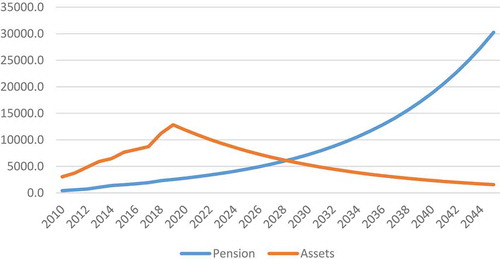

Considering the assets side of the pension system, results show that assets of the pension system have started to be depleted in 2020, and, by 2030, the situation would be worsened even further when total pension debt outweigh the level of pension assets. The study projection shows that with status quo, pension assets would be depleted in 2031, whereby pension expenditure (TZS 7,968 Billion) would surpass total pension assetsFootnote2 (TZS 5,796 billion) Figure .

Figure 3. Pension expenditure vs pension assets

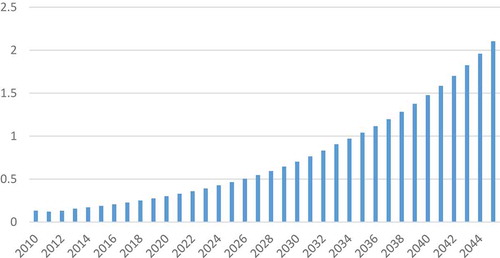

Apropos to the pay as you go rate (PAYG), results project an increase. For instance, in 2010, the PAYG was 12%, this was considered as healthy situation because pension contribution rate 20%. However, with an upsurge in pension expenditure PAYG is projected to rise very rapidly up to 50% in 2022 (Figure ). With such a high rise in PAYG, the pension system would be expensive to run due to the fact that member would be required to contribute more than 50% of their salaries to pay for pension contribution. As a result, this would make the pension system expensive and in some cases unaffordable.

Figure 4. Pay-as-you-Go rate (PAYG)

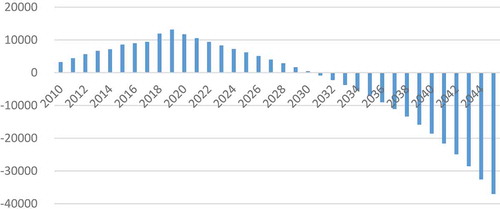

Exploring the reserves’ side, projections show that pension expenditure is swelling drastically, and, less amount is remained for investments as a result investment income would decrease over time. This decrease in investments coupled with multiplying pension expenditure would result to depletion of pension reserves as exhibited by Figure . In theory, under the partially funded DB system, reserves ought to be adequate to make the scheme sustainable for least 30 years. However, that is an ideal situation, which is contrary to the pension system in Tanzania. Assuming the status quo, reserves are projected to be negative, to the tune of TZS 852 billion in 2031 (Figure ). Inadequacy of reserves debilitates against improvement in the benefits. Hence, the outcry of members for the benefits to be improved may not be resolved in the short-to-medium terms. To restore the balance may demand the government to intervene and salvage the situation.

Figure 5. Pension reserves

With negative reserves, any increase in membership to pension schemes will cause more debt rather than the solving the problem. Hence, keeping the system open is likely to worsen the long-term financial position of the pension system. Hence, more burden to the tax payers due to the fact that pension liability would become an explicit debt to the Government. However, an increase in the amount of contributions would make the system viable subject to the institution of actuarially neutral benefit factors.

Hence, basing on results of the pension expenditure and its projections, in order for the pension system to become sustainable, the Government may choose to either increase the contribution rate to the existing cohort or reduce pension benefits package or both basing on actuarial recommendation. Such a policy may come with economic consequences in terms of negative effects on the welfare of either scheme members or retirees or both, which would be contrary to the philosophy and the practical objectives of the schemes. As such, the policy is likely to be unpopular and politically sensitive. A compromise option may be for the Government to set aside funds for the payment of the pension debt (liabilities) as they falls due.

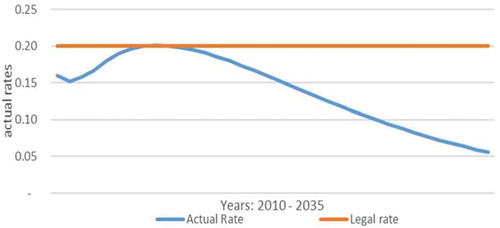

Analysis of contributions by members shows that the actual level has remained below the statutory requirement of pension contributions for most of the examined period. Whereas the statutory level is 20% of a member’s salary, the analysis shows that the amount contributed during the examined period was on average about 15%, and is projected to fall even further in the future (Figure ).

Figure 6. Actual contributions and legal contribution rate

Even if the level of legal contributions was to increase exponentially, the actual contributions are projected to remain at low levels, since they are projected to increase linearly (Figure ). The low levels of actual contributions could be accounted by lack of compliance with regard to remittance of contributions. This could also be explained by Pre—1999 PSPF debt, which was a result of conversion of the non-Contributory Pay as you go pension scheme to a contributory pension fund. Further, low level of actual contribution rate could be caused by the under disclosure of actual salary, which could be deducted by the employers to remit contributions. Another reason could be the presence of inactive members; this could also attributed by that fact that some employers do not register all of the employees to the pension schemes. Another problem that resulted to lower level of contributions was the payment of premature withdrawals, where some members upon receipt of withdrawal benefits do not disclose about new employment. Hence, due to lack of adequate inspection and enforcement the scheme would remain with dormant members, the case, which was common to NSSF and PPF.

Low levels of contributions not only erode the ability of the schemes to directly meet their matured obligations but also they constrain the capacity of the schemes to invest, which affect negatively investment income. Hence, by constraining the cash flow, non-compliance renders the pension system ineffective and ultimately leads to its failure to meet maturing obligations. In this regard, pension schemes should be more innovative and institute mechanisms that enforce compliance to ensuring contributions are collected on time.

5. Concluding remarks

The main objective of this paper was to analyze the pension debt in Tanzania, with a view to assess its fiscal implications and system sustainability. The results indicated a mismatch between benefit payments and members’ contributions, in that outflows were found to exceed inflows for a large part of the examined period, which tends to imply that pensions adequacy cannot be improved in the present circumstances. Relative to the inflows received from pensioners, the benefit payments are so high that the system cannot be sustained. With such level contributions, the study found that pension assets will tend to decrease over time, and would be depleted by 2023 if no immediate efforts are taken to restore sustainability.

Further, drawing from the computed life expectancy of pensioners, it is indicative that the size of the retirement age cohort will continue to enlarge over time; which would result in increasing pension obligations. Consequently, the pension liability was projected to increase exponentially over time due to the fact that currently the pension system is very generous, the pension factors are actuarially high, which threaten the sustainability of the pension system.

The findings of the study show also that pay as you go rates would rise from 12% in 2010 to more than 50% in 2022. At the rate of 12%, the study found the system to be affordable. However, with the pay as you go rate rising to 50%, the pension system was found to be unaffordable. High pay as you go rates would make pension plans very expensive, which would discourage new members to enrol and constrain the system further.

Furthermore, projections show that pension liability as a percentage of GDP would rise dramatically from 2020 onwards due to maturity of pension obligations. This rise will tend to have adverse effects on the system because pension assets would be insufficient to support pension expenditure. Since increased pension expenditure would not be fully covered from the existing pension assets, the Government as a guarantor would be required to cover the matured pension obligations through its annual fiscal budget. Unfortunately, looking at the National Debt sustainability report of 2018, pension debt has not been included.

Following these findings, the government could take immediate action, such as pension parametric reforms which may involve either of the following options; reducing accrual rates, increasing contribution rates or increasing retirement age. Since contributions are already on the higher side as compared with other countries in the region, this may make labour expensive, hence less competitive. Reduction of accrual rate is the most suitable because already the scheme offers generous and unsustainable factors. However, it is a tricky process that requires strong political commitment, transparency, sensitization, and involvement of stakeholders.

Furthermore, the Government should undertake a systemic reform, which would change the entire pension system from a Defined Benefits Scheme to a Defined contributions scheme. This will probably remove the intergenerational burden of the contributors and would reduce from the tax payers who would be required to finance pension of the small segment of the population who formally employed. There is a need to conduct another study using Medium Term Fiscal Framework FMM-MTFF. The Medium-Term Fiscal Framework FMM-MTFF model, is a dynamic stochastic general equilibrium model developed to support the implementation of a Medium-Term Fiscal Framework (MTFF) in emerging market and developing economies Suescun (Citation2020). As Tanzania is in the process of reforming its pension system, it is expected that findings of this study will serve as important inputs to MTFF to quantify the scale of the fiscal challenges, and provide medium-term macro fiscal projections and to evaluate the quantitative implications of past social security reforms carried out in Tanzania.

Additional information

Funding

Notes on contributors

Josephat Lotto

Josephat Lotto is a Senior Lecturer in Finance and Corporate Governance at the Institute of Finance Management in Tanzania. He graduated with a PhD in Corporate Governance and Financial Strategies from the UK in 2012. He also holds MSc in Finance, MBA and CPA (T). Josephat’s research interest lies at the heart of Corporate Governance and Financial strategies where the current paper forms a part of the research agendas around the broad theme. He has published over 30 research papers in various academic journals and he is a reviewer of several academic journals published by some reputable publishing houses such as Wiley & Sons, Inc, Taylor & Francis Group which publishes quality peer-reviewed journals under the Routledge; Multidisciplinary Digital Publishing Institute (MDPI), Elsevier, IEEE Access and Springer Nature. Such Journals include; International Journal of Finance and Economics, African Journal of Economics and Management Studies, Development Policy Review, The European Journal of Finance, Sustainability Journal and International Advances in Economics.

Notes

1. For the definition of IPD see Robalino and Bogomolova (Citation2006).

2. It should be noted that this analysis has not taken in consideration of administrative income of the pension schemes. If administration income is considered, the situation becomes even worse

References

- Ajwad, M. I., Abels, M., Novikova, M., & Mohamed, M. A. (2018). Financing social protection in Tanzania. World Bank.

- Alaedini, P. (2013). Qualitative assessment of conditional cash transfer and complementary components under the productive social safety net project: Institutional, capacity, and strategic issues (Report prepared for TASAF). https://www.tasaf.org/index.php/reports/studies/235-qualitative-assessment-ofconditional-cash-transfer-and-complimentary-components-under-the-productivesocial-safety-net-project

- Andersen, P. K., Borgan, O., Gill, R. D., & Keiding, N. (1993). Statistical models based on counting processes. Springer – Verlag.

- Baranzin, M. (2005). Modiglian’s life cycle theory of saving fifty years later. PSL Quarterly Review, 58, 233–16.

- Beltrametti, L., & Della Valle, M. (2011). Does the implicit debt mean anything after all? (JEL.H55, H63). Department of Economics, University of Genoa.

- Bodie, Z. (1990). The ABO, the PBO and pension investment policy. Financial Analysts Journal, 46(5), 27–34. https://doi.org/10.2469/faj.v46.n5.27

- Bovenberg, L., & Petersen, C. (1992). Public debt and pension policy. Fiscal Studies, 13(3), 1–14. https://doi.org/10.1111/j.1475-5890.1992.tb00180.x

- Bulow, J. I. (1982). What are corporate pension liabilities? Quarterly Journal of Economics, 97(3), 435–452. https://doi.org/10.2307/1885871

- Chand, S., and Jaeger, A.. (1996). Aging Population and Public Pension Scheme. Occasion Paper No.147. Washington, DC: IMF. doi:10.5089/9781557756206.084

- Congleton, R. D, and Shughart, W F., (1990). The Growth of Social Security: Electoral Push or Political pull? Economic Enquiry, 28(1), 109–132. doi:10.1111/ecin.1990.28.issue-1

- Hills, J. (1984). Public assets and liabilities and the presentation of budgetary policy in the public finance in perspective (Report Series No.8). Institute for Fiscal Studies.

- Holzmann, R., (1998). Financing the transition (Social Protection Discussion Paper No. 9814). The World Bank.

- Holzmann, R. (1999). On the economic benefits and fiscal requirements of moving from unfunded to funded pensions. In M. Buti, D. Franco, & L. Pench (Eds.), The welfare state in Europe (pp. 139–196). Edward Elgar. http://documents.worldbank.org/curated/en/999381538657815182/Financing-Social-Protection-in-Tanzania

- Hurd, M., Michaud, P-C.., and Rohwedder, S. (1993). The Displacement Effect of Public Pensions on the Accumulation of Financial Assets. Fiscal Studies, 33(2), 107–128. doi:10.1111/fisc.2012.33.issue-1

- Isaka, I. C. (2017). Social security in Tanzania; “Pension system adequacy and its fiscal implication. A Thesis Submitted in Fulfilment of the Requirements for the Degree ofDoctor of Philosophy (Economics) of the University of Dar es Salaam.

- Kane, C., and Robert, P. (1996). The implicit Pension Debt. Finance and Development. Washington, DC: IMF.

- Kelley, D. (2014). The political economy of unfunded public pension liabilities. Public Choice, 158(1), 21–38. https://doi.org/10.1007/s11127-012-0049-3

- Kune, J. (1996). The hidden liability, meaning and consequences. The CBP Seminal Series, The Hague (mimeo).

- Modigliani, F. (1966). The life cycle hypothesis of saving, the demand for wealth and the supply of capital, social research. PCI, ProQuest Information and Learning Company.

- Modigliani, F., & Sterling, A. (1983). Determinants of private saving with special reference to the role of social security, cross-country tests. In F. Modigliani & R. Hemming (Eds.), The determinants of national saving and wealth (pp. 24–55). St. Martins Press.

- Modigliani, F. (1986). Life-cycle, individual thrift, and the wealth of nations. American Economic Review, 76(3), 297–313.

- MOF. (2018). Tanzania National Debt Sustainability Analysis. Ministry of Finance and Planning Report, Dar Es Salaam, Tanzania

- Palacios, R. (1996). Averting the Old-Age Crisis. Technical Annex. Washington, DC: World Bank.

- Palacios, R., Holzmann, R., & Zviniene, A., (2004). Implicit pension debt (Issues, Measurement and Scope in An International Perspective. Social Protection Discussion Paper No.0403). WB Washington, DC.

- Rizzo, I. (1999). The hidden debt financial and monetary (Policy Studies, No.19 Dordrecht – Boston- London). Kluwer Academic Publishers.

- Robalino, D., & Bogomolova, T. (2006). Implicit pension debt in the Middle East and North Africa (Magnitude and Fiscal Implication. Working Paper Series No.46). World Bank.

- Romp, W., & Beetsma, N. R. (2020, April). Sustainability of pension systems with voluntary participation. CEPR, CESifo, Netspar, Tinbergen Institute.

- Sane, R., & Thomas, S. (2015). In search of inclusion: Informal sector participation in a voluntary, defined contribution pension system. Journal of Development Studies, 51(10), 1409–1424. https://doi.org/10.1080/00220388.2014.997220

- Schwarz, A., & Demirgue-Kunt, A. (1999). Taking stock of pension reforms around the world (Social Protection Discussion Paper No. 9917 the WB Washington, DC).

- Settergren, O., Mikula, D., & Lundberg, K. (2006). “Non-financial defined contribution pension schemes in a changing pension world” volume 2 gender, politics and financial stability. Ed. Robert Holzmann, Edward Palmer and David Robalino.

- Splinter, D. (2017). State pension contributions and fiscal stress*. Journal of Pension Economics and Finance, 16(1), 65–80. https://doi.org/10.1017/S1474747215000189

- Suescun, R. (2020). A tool for fiscal policy planning in a medium-term fiscal framework: The FMM-MTFF model. Economic Modelling, 88, 431–446. Inter-American Development Bank, 1300 New York Avenue, N.W., United States. https://doi.org/10.1016/j.econmod.2019.09.053.

- Sundeep, R. (2008). Analytical review of pension system in Kenya. Mimmeo.

- Treynor, J. L. (1976). The principles of corporate pension finance. The Journal of Finance, 32(2), 627–638. https://doi.org/10.2307/2326796

- United Nations Children’s Fund. (2019): Activities, tools and resources to support implementation of UNICEF’s 10 action areas in Social Protection:) UNICEF, October 2019 PD/GUIDANCE/2019/004: Down loaded on 22nd August 2020.

- URT. (2013b). Population distribution by age and sex. National Bureau of Statistics, Ministry of Finance, Dar Es Salaam and Chief Government Statistician, President’s Office, Finance, Economy and Planning.

- URT. (2018). Public Service Social Security Act No. 2 of 2018.

- Werding, M. (2006). Implicit pension debt and the role of public pensions for human capital accumulation, an assessment for Germany. IFO Institute for Economic Research and CESifo.