?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper provides evidence on the moderating effects of institutions on the marginal effects of human capital, financial development, and macroeconomic policies on foreign direct investment (FDI) inflows, based on large panel data of 124 developing countries—spanning from 2002 to 2018—and generalised method of moments (GMM) estimators. The findings suggest that only financial development has a positive and significant direct effect on FDI inflows to developing countries. Importantly, improving the quality of institutions moderates the marginal effect of human capital on FDI inflows. Drawing on these findings, policymakers in developing countries are advised to undertake a set of reforms to upgrade the quality of institutions, improve financial institutions and markets, and scale up investments in human capital.

PUBLIC INTEREST STATEMENT

Policymakers in the Global South are drawn at foreign direct investments (FDI) for they are instrumental to economic growth and industrialization. However, confronted with a plethora of determinants, sometimes confusing, policymakers are still puzzled concerning the lever to act on to attract FDI inflows. To respond to such a pressing need, we assess the effects of human capital, financial development, and macroeconomic policies—called economic fundamentals—on FDI inflows in developing countries and evaluate the extent to which institutions strengthen the effects of the very economic fundamentals. We find that advancing the financial market would attract more foreign investors. Our findings also harmer that ameliorating the quality of institutions reinforces the effect of human capital on FDI inflows. Therefore, there is a need for fast-tracking financial development and investing in human capital in developing countries. More to the point, Policymakers in the Global South are advised to undergo institutional reforms to improve government effectiveness and reduce corrupt practices.

1. Introduction

Among foreign capitals, foreign direct investment (FDI) is the most relevant for developing countries since it comprises 39 % of their external funding (World Investment Report Citation2018| UNCTAD, s. d.) and catches policymakers’ attention. Several reasons underscore why policymakers are particularly drawn to FDI inflows. First, greater inflows of FDI could provide additional funding to fill the gap between the great need for investments and the lack of sufficient resources—unlocking the potential of host countries to finance the Sustainable Development Goals (SDGs). Second, multinational firms are engines of technologies and knowledge transfer (Guadalupe et al., Citation2012), as well as contributors to host countries’ physical capital accumulation and economic growth (Jude & Levieuge, Citation2016). Multinational firms have also been described as agents of industrialization (Haraguchi et al., Citation2019). Policymakers are drawn to FDI because it ultimately triggers the integration of the Global South into the world economy (Alguacil et al., Citation2011). However, given the plethora of FDI’s determinants advanced by researchers, policymakers remain confused about which attractors work best.

This paper aims to clear the confusion and provide developing countries’ policymakers with policy tools to attract FDI inflows. Since Lucas’s (Citation1990) paradox, insufficient investment in human capital is stressed as the root of scanty FDI inflows to developing countries. Drawing on that, theoretical clarifications incorporate international capital market imperfections (sovereign risk and asymmetric information) and cross-countries heterogeneities in fundamentals affecting productivity (Alfaro et al., Citation2008). These fundamentals are institutional and economic. The latter include human capital, financial development, and macroeconomic policies. This paper is chiefly concerned with these fundamentals. To that end, it first analyses the effect of financial development, human capital, and macroeconomic policies on FDI inflows in developing countries.

Economic fundamentals are relevant to FDI inflows in several respects. A well-developed financial market would benefit multinationals, since it allocates optimal resources to the best investment projects, ensures the monitoring of investments, diversifies risks and performs the function of savings collection (Levine, Citation2005). Such a market allows the manufacturing industry to blossom (Beck, Citation2002) and for multinationals to expand their exports (Manova et al., Citation2015). Additionally, a well-developed financial market can ease the financing of multinationals’ production costs (Desbordes & Wei, Citation2017). However, in some cases, a thriving financial market may breed multinationals’ exit. For instance, the entry of new firms with the only objective to serve the domestic market may cause a surge in the intermediate goods’ prices, leading to a decline in the multinational firms’ production (Bilir et al., Citation2014). From a theoretical perspective, human capital is regarded as a relevant ingredient to multinational firms’ attraction. According to Zhang and Markusen (Citation1999) skills and educational levels affect both the level and the nature of FDI (Dunning, Citation1977, Citation1988), such that a decline in the availability of skilled labour would precipitate FDI inflows towards zero. In attempting to unpack the underlying reasons for the somewhat negligible foreign capital flows to developing countries, Lucas (Citation1990) points to the low level of human capital. Furthermore, Alfaro et al. (Citation2008)—building on Lucas (Citation1990)—concede that the insufficient inflows of foreign capital to developing countries may be attributable to the dearth of quality human capital, the shallowness of the financial market, the institutional bottlenecks and the inadequacy of macroeconomic policies. Their assertion is that the heterogeneity of fiscal policies may lead to a substantial difference in the capital-labour ratio. For instance, high taxes and inflation reduce the marginal productivity of capital, ultimately affecting the capital-labour ratio. An unstable macroeconomic environment, fuelled by higher inflation, renders the business environment unpredictable, slows down resource allocation, hampers investment decisions, and reduces entrepreneurs’ capacity to anticipate returns on investments.

Furthermore, this paper assesses the nexuses between institutional and economic fundamentals. To be specific, it investigates the modulating effects of institutions on the FDI-human capital, FDI-financial development, and FDI-macroeconomic policies relationships. Institutions are rules and constraints that modulate the behavior of individuals in a society (North, Citation1990). They represent the governance infrastructure within countries and are instrumental to economic development (Acemoglu et al., Citation2001; Robinson et al., Citation2005). Better institutions are compatible with protected property rights and low levels of transaction costs. With these attributes, good institutions have the promise to shape the capital structure of multinational firms’ subsidiaries (Kesternich & Schnitzer, Citation2010). Another perspective perceives a higher institutional distance between the host country and the foreign investors’ source countries to be a deterring factor to FDI inflows (Cezar & Escobar, Citation2015) as the institutional difference increases firms’ production costs. That said, how do the institutional fundamentals relate to the host countries’ economic fundamentals in such a way that improving institutions would strengthen financial market development, human capital, and macroeconomic policies?

Levine (Citation1997) has conceptually attributed financial markets’ development to good institutions, since the latter limits market frictions and promotes access to information. Financial markets operate smoothly with judiciary efficiency and political stability. Put in historical perspective, Beck and Levine (Citation2003) theorise that countries whose ancient colonists originate from states with legal traditions that protect property rights, have well-developed financial markets. Acemoglu et al. (Citation2001) attribute countries’ financial underdevelopment (development) to the extractive (inclusive) institutions set by the colonists some years ago. Besides financial development, Acemoglu et al. (Citation2001) have advanced the same argument to explain the heterogeneities in human capital by the differences in institutions. From their perspective, states with higher (lower) human capital productivity are rooted in inclusive (extractive) institutions. Ehrlich and Lui (Citation1999) hold that corruption deters human capital development since, in countries plagued by such an institutional impediment, the time that governments spend on fighting corruption comes at the cost of investing in human capital. In defining a conceptual framework to link human capital to institutions, the takeaway insight of Klomp and de Haan (Citation2013) is that human capital get nurtured well in democracies than in autocracies. Yet, under the yoke of political instability, governments are more likely to draw higher revenues from seigniorage, which is inflation-fueling (Cukierman et al., Citation1992). In autocratic regimes with weak institutional infrastructures, the absence of the central bank’s independence and transparency (Loungani & Sheets, Citation1995; Walsh, Citation1995), coupled with the use of repression and public spending for personal purposes, feed high inflation (Fatton, Citation1992).

In this study, exploring data on a large sample of 124 developing countries spanning from 2002 to 2018, we used three identification strategies: (1) the two-step system generalised method of moments (GMM) estimator alongside the Windmeijer Bias-Corrected Robust VCE (variance-covariance matrix of the estimators); (2) the two-step GMM estimator of Arellano and Bover (Citation1995); and (3) the instrumental variable approach. We utilised the first identification strategy in our baseline estimates and employed the two others in our robustness checks. In the baseline estimates, we measured the quality of institutions by the index of institutions computed with the principal component analysis (PCA) methodology based on the World Bank’s Worldwide Governance Indicators (WGI). To integrate the contribution of each institutional measure of the WGI, we reran the baseline estimates with each institutional variable of the WGI. For robustness checks, we employed an alternative index of institutions computed, based on the political risks from the International Country Risk Guide (ICRG). Our robustness checks also involved subperiod analyses. Based on system GMM, we further estimated the empirical model before and after the 2008 financial crisis to gauge the extent to which the pattern of the determinants of FDI had been affected by the financial crisis.

Our research contributes to the literature in several fashions. First, though we are not the first to evaluate the direct effect of financial development, human capital, and macroeconomic policies, we are placed among a handful of studies to assess these three relevant economic fundamentals’ variables concurrently. The integration of these three factors in the same analysis allows for a comparative analysis. Our results consistently show that financial development is the most important economic fundamental, with a direct effect on FDI inflows to developing countries. Second, few studies have been dedicated to the effects of macroeconomic policies on FDI, and only a few studies concerning the modulating role of institutions on the FDI-macroeconomic policies exist. We barely found studies on the moderating effects of institutions on the FDI-macroeconomic nexus. In the present study, we payed specific attention to macroeconomic policies measured by inflations and external debts and found that the effects of inflations and external debts on FDI were insensitive to the quality of institutions. Third, previous studies concerning the modulating effect of institutions muddle developing and developed countries. This kind of confusion may drive inconclusiveness, since “developing” and “developed” are highly heterogeneous concepts. Furthermore, the results of such studies may be arduous to implement in developing countries since they draw on an economic framework unspecific to developing countries. Implementing such results as economic policies may lead to catastrophe. To avoid this, we based our analysis on a large panel data of 124 developing countries spanning from 2002 to 2018, which also allowed us to control for time-invariant unobservable country-specific characteristics. We were thus able to exploit the heterogeneities that the panel data offered. Resting on this, our findings can be used by policymakers in developing countries. Fourth, we barely found in the literature a study that investigated the modulating effects of institutions on a range of variables including human capital, financial development and macroeconomic policies simultaneously. Most of them have led the focus on the effect of institutions on either human capital or financial development in a way that it is difficult to assert that institutions have a greater modulating effect on the FDI-human capital nexus than on FDI-financial development nexus, or another way around. There is a need to conduct such a simultaneous analysis to allow for comparisons. From that exploration, our analysis shows that, though human capital and financial development have more direct effects on FDI in developing countries, improving the quality of institutions only improves the marginal effect of human capital on FDI inflows.

The remaining part of the paper unfolds as follows: section 2 provides a snapshot of the empirical literature. Section 3 outlines the methodology utilised. Section 4 presents the main findings. Section 5 concludes the paper and proposes some suggestions as policy implications.

2. Empirical literature review

2.1. Evidence on the direct effects of institutions, human capital, financial development, and macroeconomic policies on FDI

Institutions are important to foreign investors as they affect the business environment, transaction costs and production costs. Good institutions reflect the capacity of governments to enforce property rights (Calvo et al., Citation1996), which tend to be more secure in democracies (Harms & Ursprung, Citation2002). For instance, in a rule of law regime, political stability guarantees the protection of capital (Jensen, Citation2003). Contrarily, inadequate institutions are harmful to FDI inflows as they act as higher taxes on multinationals (Buchanan et al., Citation2012). By increasing uncertainty, political instability threatens capital accumulation (Henisz, Citation2009) and deters FDI inflows (Busse & Hefeker, Citation2007; Gastanaga et al., Citation1998). Based on this, Alfaro et al. (Citation2008) remarks that low institutional quality explains why developing countries attract low FDI inflows. Based on panel data of 150 countries spanning from 2000 to 2016, Tag (Citation2021) documents that countries with independent and impartial judiciaries and with better-enforced property rights attract more FDI. Similar results have been found by Contractor et al. (Citation2020), Du et al. (Citation2008), Staats and Biglaiser (Citation2012), and Jain (Citation2001) and Mauro (Citation1996) find that corruption deteriorates the business environment and harms investment. Staats and Biglaiser (Citation2012) conclude that American multinationals are inclined to locate themselves in countries with an impartial judiciary and strong rule of law. On a panel of 83 developing countries, Akhtaruzzaman et al. (Citation2017) found that a high risk of capital expropriation deterred FDI. Aziz (Citation2018), Cai et al. (Citation2019), Peres et al. (Citation2018), and Sabir et al. (Citation2019) have all recently confirmed the positive correlation between institutions and FDI inflows.

However, goods institutions are not always beneficial to host countries in terms of FDI inflows. For instance, multinational firms may discard institutions when they are interested in host countries’ natural resources (Wheeler & Mody, Citation1992) or when they opt for horizontal strategies (Poelhekke & Ploeg, Citation2010). Sometimes, foreign investors may even prefer investing in autocratic countries than in democratic ones; first, in an autocratic regime where multinationals are friendly with leaders, the multinationals benefit from lower taxes and protection against high wages (O’Donnell, Citation1978). Second, in such a regime the multinationals may take advantage of the mismatch between marginal labour productivity and real wages (Greider, Citation1998). Another reason why foreign investors may be interested in autocratic regimes is that democratic regimes are more inclined towards protective and competitive industrial policies. A recent study by Gossel (Citation2018) found that FDI was positively correlated with corruption in Sub-Saharan African because corruption was used to overcome higher transaction costs fuelled by a weak institutional framework. Some empirical studies—such as those by Kurul (Citation2017), and Asiedu and Lien (Citation2011)—document a non-linear effect of institutions on FDI inflows. Institutions are found to be negatively correlated with FDI inflows when below a threshold level of institutions (Kurul, Citation2017) or above a threshold level of natural resources (Asiedu & Lien, Citation2011).

Empirical evidence on the direct effects of financial development on FDI is mixed; no clear line has emerged. For instance, while Buch et al. (Citation2014), Agbloyor et al. (Citation2013), Donaubauer et al. (Citation2016), Desbordes and Wei(Citation2017), Islam et al. (Citation2020) and Nguyen and Lee (Citation2021) find a positive effect between financial development and FDI, Fernández-Arias and Hausmann (Citation2011), as well as Manova (Citation2013), report a negative effect. Financial development may have a detrimental effect on FDI inflows because a well-developed financial market may reinforce competition, leading to higher intermediate goods’ prices and low multinationals’ production. In this inconclusive setting, Kinda (Citation2009), and Dutta and Roy (Citation2011) find no effect between financial development and FDI whatsoever.

The line of inconclusiveness also manifests itself when it comes to the empirical direct effect of human capital on FDI inflows, though theories on the issues are less contentious. Noorbakhsh et al. (Citation2001), Cleeve et al. (Citation2015), and Kheng et al. (Citation2017) express that investing in human capital would increase FDI inflows in developing countries. Dutta and Osei‐Yeboah (Citation2013)and Islam et al. (Citation2020) even find a negative impact of human capital on FDI inflows, while Schneider and Frey (Citation1985), and Kinda (Kinda, Citation2009) report no effect. According to a largely shared idea, multinationals discard the quality of human capital in developing countries when engaged in horizontal FDI and when interested in cheaper natural resources and labour forces (Kinda, Citation2009).

Empirical evidence has demonstrated that macroeconomic instability is deleterious to FDI inflows. Policy uncertainty has been found to reduce FDI inflows (Canh et al., Citation2020; Zhu et al., Citation2019). A recent study by Nguyen and Lee (Citation2021), based on a large sample of 116 countries from 1996 to 2017, found that policy uncertainty reduced FDI inflows. Asiedu (Citation2005), Dutta et al. (Citation2017), and Sabir et al. (Citation2019) discovered a negative correlation between inflation and FDI inflows. Yet studies on the direct effect of macroeconomic policies (inflation) have reached the inconclusiveness line, since some studies—such as Rădulescu and Druica (Citation2014), and Naanwaab and Diarrassouba (Citation2016)—have reported a positive correlation between inflation and FDI.

From the survey of the literature, it is evident that the direct effects of institutions, human capital, financial development, and macroeconomic policies on FDI are not conclusive. Several reasons underlie this inconclusiveness. First, the heterogeneities in the methodologies employed, the time horizon considered, and the sample of countries may drive such an outcome. Second, the variety of metrics used to capture institutions, human capital, financial development and macroeconomic policies may drive such a plurality of conclusions. It is worth mentioning that the time frame in which studies are based matters too. For instance, as institutions produce direct effects over a longer duration, a shorter time frame would possibly lead to institutions having zero effects on FDI inflows.

2.2. Evidence for the modulating effects of institutions

Considering the inconclusiveness of studies on the direct effects of human capita; financial development; and macroeconomic policies on FDI inflows, some attempts have been made to fathom such inconclusive outcomes. In these attempts, institutions are regarded as vital factors to give meaning to the role of financial development and human capital in FDI inflows. Indeed, Dutta and Roy (Citation2011), based on a panel of 97 countries, found that higher political stability favours financial market development. A recent study by Islam et al. (Citation2020) confirms such a result on a panel of 79 developed and developing countries. Regarding the modulating effect of institutions on the FDI-human capital nexus in developing countries, Dutta and Osei‐Yeboah (Citation2013), and Naanwaab and Diarrassouba (Citation2016), on a panel of 137 developed and developing countries from 1995 to 2010, and Dutta et al. (Citation2017)—on a panel of 107 countries over the period 1984 to 2009—concluded that institutions enhanced the effect of human capital on FDI inflows.

Three remarks emerge. First, few studies have been concerned with the empirical investigations of the modulating effect of institutions on FDI-financial development and on FDI-human capital nexus. Second, studies on the modulating effect of institutions on FDI-macroeconomic policies are scant. Third, most of the existing studies have muddled both developed and developing countries in their investigations and have only analysed to which extent institutions modulate either the effects of financial development or human capital, instead of dealing with the three nexuses simultaneously.

3. Research methodology

3.1. Empirical model

Drawing on the theoretical model of Cezar and Escobar (Citation2015) and the empirical models of Dutta and Osei‐Yeboah (Citation2013); Dutta and Roy (Citation2011); and Islam et al. (Citation2020), FDI inflows () in a country

at a given time

(

) is modelled as a function of economic fundamentals including human capital (

), financial development (

) and macroeconomic policies (inflation (

), public external debt (DEBT_GDP)), institutions (

) and a set of control variables (

) which include the gross domestic product (GDP), domestic investment (

), trade openness (OPEN), population (TOTAL_POPU) and the United States of America’s (USA) economic growth (GDP_CUSA) to capture external shock. To apprehend the nexuses between institutions and economic fundamentals, we interact institutions with human capital, financial development, inflation, and external debt. EquationEquation (1)

(1)

(1) represents the explicit form of our empirical model.

is the error term that can be decomposed into unobserved time-invariant heterogeneities

, and idiosyncratic error components

,

,

and

are parameters to be estimated.

The variables of interest are the interactions. Their coefficients, say , are expected to be positive—irrespective of the sign of

which may be positive or negative, based on the economic fundamental considered. For instance, the total effect of human capital on FDI inflows is obtained by taking the first derivative of Equationequation (1)

(1)

(1) with respect to

. The very total effect is, thus, the sum of the direct effect of human capital (

) and its indirect effect conditional on the institutional level (

).

A positive suggests that improving the quality of institutions would strengthen the effect of human capital on FDI inflows. The same reasoning can be made with respect to financial development and macroeconomic policies’ variables. In this analysis, while we report the marginal effects of economic fundamentals’ variables on FDI inflows, we also provide their graphical representation.

3.2. Variable choice justification and expected signs

Dependent variable

We measure FDI by net FDI inflows in the percentage of GDP. This metric sums up equity capital reinvested, earnings and other long-term and short-term capital recorded in the balance of payments. We are aware that this metric lacks the capacity to disentangle the types of FDI. However, it is suitable for our analysis since we aim to fathom the determinants of FDI flows wholly. We are neither interested in FDI’s nature nor in the sector of investment. It would be erroneous to underestimate surveys aiming at sectoral analysis of FDI. However, we are unable to carry out such an analysis due to sectoral data unavailability, particularly among African countries, that represent a non-negligible part of our data set. Finally, we rely on net FDI inflows to measure FDI, as this metric has been widely used by researchers (Asiedu, Citation2005; Aziz, Citation2018; Cleeve et al., Citation2015; Nguyen & Lee, Citation2021; Tag, Citation2021).

Explanatory variables of interest

Our main explanatory variables include human capital, financial development, macroeconomic policies and institutions. Financial development has often been measured by domestic credit to the private sector as a percentage of GDP along with stock market capitalisation and monetary aggregate (Agbloyor et al., Citation2013; Choong & Lim, Citation2009; Kaur et al., Citation2013; Kurul, Citation2017; Law et al., Citation2018; Soumaré & Tchana Tchana, Citation2015; Tsagkanos et al., Citation2018). The aforementioned indicators only measure the size of the financial market and, thus, have limitations. For instance, a large financial market may be inaccessible and inefficient and may not contribute to financial development (Aizenman et al., Citation2015). Furthermore, each metric may lead to a different result as it only expresses a portion of financial development (Soumaré & Tchana Tchana, Citation2015). Financial development in itself is a multidimensional and complex concept that goes beyond financial market size as it accounts for both access and efficiency of financial institutions and markets (Svirydzenka, Citation2016). Complying with this, financial development is measured by the financial development index developed by the International Monetary Fund (IMF). This metric is computed with two others—namely, the financial market index and the financial institutions’ index. A value closer to 1 would indicate a well-developed financial market.

We measure macroeconomic (instability) policy by the inflation rate. Inflation rate is widely used in the literature as a proxy for macroeconomic instability. At a higher level, inflation creates exchange rate and price volatility (Azam, Citation1999) which limits foreign capital inflows. In addition to the inflation rate, we also use external debt stocks expressed as a percentage of gross national income (GNI) to gauge macroeconomic policies. Drawing on Alguacil et al. (Citation2011) and Jallab et al. (Citation2008), we argue that a higher external debt or fiscal deficit creates uncertainty that discourages the entrance of multinationals. Overall, both metrics capture host countries’ macroeconomic backgrounds. While the inflation rate best reflects uncertainty instilled by monetary policies, the external debt ratio demonstrates the state of fiscal policies.

In the literature, secondary school enrolment rate (Alfaro et al., Citation2009) and primary school completion rate (Lee & Lee, Citation2016) are used to capture a country’s human capital stock. Given the extent of missing data in the secondary school enrolment rate in most developing countries in the sample, we have proxied human capital by primary school enrolment rate.

We proxy institutions by the World Bank’s Worldwide Governance Indicators (WGIs), developed by Kaufmann et al. (Citation1999). In measuring the level of decision-making and political risk (Akhtaruzzaman et al., Citation2017), these indicators are constructed with a range of cross-country surveys and expert polls. The six WGIs are: (1) control of corruption; (2) regulatory quality; (3) government effectiveness; (4) political stability and absence of violence; (5) the rule of law; and (6) voice and accountability. These institutional indicators have been widely cited in the literature (Fon et al., Citation2021; Islam et al., Citation2020; Kurul, Citation2017). The “control of corruption” index expresses the extent to which political power is exercised for private purposes and how the state is captured by elites and private interest groups. The “regulatory quality” index expresses the government’s ability to formulate and implement policies that ensure the private sector’s development. “Government effectiveness” measures the quality of public service and its independence from political pressures; the quality of public policy formulation and implementation; and the credibility of the government’s commitment to these policies. The rule of law is concerned with the extent to which agents or citizens abide by the laws of society—in particular, contracts, property rights, the police force, the courts, and so on. “Political stability and the absence of violence” measures the likelihood that the government will be destabilised by unconstitutional means. The “voice and accountability” index demonstrates the extent to which citizens participate in the election of their government, express their freedom of speech and association, and so on. The WGIs range from −2.5 to 2.5. A value closer to 2.5 reflects good institutions. Given that the WGIs are highly correlated, one cannot integrate them in the same equation without running into multicollinearity. One also cannot discriminate among them without truncating salient aspects of institutions (Kurul, Citation2017). We therefore construct an institutional index as recommended by Buchanan et al. (Citation2012) and Globerman and Shapiro (Citation2002)—and widely used in the literature (Islam et al., Citation2020; Kurul, Citation2017). For our robustness analysis, we construct a second institutional index with the political risk indicators of the International Country Risk Guide (ICRG) as an alternative measure of institutions. These indicators have also been used widely in the literature (Aziz, Citation2018; Busse & Hefeker, Citation2007; Cai et al., Citation2019; Gossel, Citation2018; Islam et al., Citation2020; Mina, Citation2012), and include (1) government stability; (2) socio-economic conditions; (3) investment profile; (4) internal conflict; (5) external conflict; (6) corruption; (7) military in politics; (8) religious tension; (9) law and order; (10) ethnic tension; (11) democratic accountability; (12) and bureaucracy quality. The first five range from 0 to 12, whereas the latter seven range from 0 to 6. A higher level of any of these indicators would indicate low political risk and better-quality institutions.

Control variables

Investment is one of our control variables and has been included for several reasons. First, when information is asymmetric, decisions made by domestic investors provide information to foreign investors (McMillan, Citation1999). Moreover, a higher level of investment is indicative of higher capital productivity (Ndikumana & Verick, Citation2008). In the second place, investment in infrastructure improves economic growth according to the endogenous growth theory (Barro, Citation1990). Empirical studies—such as Kinda (Citation2009), Lautier and Moreaub (Citation2012), and Ndikumana and Verick (Citation2008)—report a positive effect of domestic investment on FDI. We measure domestic investment by gross fixed capital formation in percentage of GDP, as done in the literature (Lautier & Moreaub, Citation2012).

A large market may attract foreign investors as it helps raise the investors’ turnovers. In the literature, the size of the market is proxied by GDP (Busse & Hefeker, Citation2007) and GDP per capita (Alfaro et al., Citation2008; Naanwaab & Diarrassouba, Citation2016). These two indicators are also used to capture economic development (Cleeve et al., Citation2015; Lautier & Moreaub, Citation2012). In this paper, we use GDP. We also use the population size not only as a proxy for market size but also as a proxy for labour, as foreign investors are interested in cheaper labour available in developing countries compared to the industrialised world.

Our fourth control variable is trade openness, proxied by trade in the percentage of GDP due to the unavailability of data on trade policy (Yiheyis, Citation2013). On the theoretical ground, the effect of trade openness on FDI depends on the type of FDI. FDI and trade are complementary (substitutable) for vertical (horizontal) FDI (Brun & Gnangnon, Citation2017). Empirical investigations remain in line with the ambiguous effects of FDI on trade. Positive effects (Brun & Gnangnon, Citation2017; Cleeve et al., Citation2015), negative effects (Blomstrom & Kokko, Citation1997) and neutral effects (Blancheton & Opara-Opimba, Citation2010) have been reported in the literature.

Capital inflows are not only shaped by internal economic fundamentals but also by external pull and push factors (Fratzscher, Citation2012). Global risk also matters for FDI inflow (Kurul, Citation2017). For instance, FDI is more likely to flow into countries with higher interest rates or higher productivity (Boateng et al., Citation2015). As FDI moves North-South, a higher perspective of economic growth in developed countries may prevent foreign capital from moving towards the South. To capture the external factors that may affect FDI inflows in developing countries, we introduced the logarithm of GDP per capita growth in the USA. We expect that an increase in the USA’s economic growth will reduce the flow of capital to developing countries. The contrary is also expected.

below provides a summary of the variables used in the empirical model, their names, measurement, source and expected signs.

Table 1. Variable description and expected signs

3.3. Identification strategies

To simplify model (1), we allowed X to be the vector for all explanatory variables, including inflation; external debt; financial development; human capital; population; trade openness; gross domestic product; the USA’s economic growth rate; and institutions.

Where

The transformed Equationequation (3)(3)

(3) is a typical dynamic model, for it includes the first lag of the dependent variable in the set of the explanatory variables. The integration of the lagged FDI in the model allows the modelling of partial adjustment. Therefore,

reflects the speed of adjustment. Nonetheless, the presence of a lagged dependent variable (

) and the cross section-specific unobserved heterogeneities make it impossible to estimate the model (3) by ordinary least square (OLS)—that is, the fixed-effects model or random-effects model. Since

is a function of

,

is also a function of

, leading to a correlation between

and

in Equationequation (3)

(3)

(3) . Furthermore, the presence of the time-invariant unobservable heterogeneities can be correlated with the explanatory variable

, rendering the hypothesis

invalid. Therefore, the explanatory variable is endogenous. Thus, an OLS estimate would be biased and inconsistent even if

are not serially correlated.

To resolve the second issue, one needs to take the first difference of Equationequation (3)(3)

(3) .

Though the time-invariant fixed effects are removed in Equationequation (4)(4)

(4) ,

is still correlated with

in Equationequation (4)

(4)

(4) to the extent that

contains the error term lagged by one period. To overcome this, one needs to establish a satisfactory instrument for

. Based on Anderson and Hsiao (Citation1981) (), we must instrument

by

or

. However, the instrumental variable method of Anderson and Hsiao (Citation1981) has been subject to criticism since it does not explore all potential orthogonality conditions and may produce inefficient estimates (Das, Citation2019). The GMM estimator of Arellano and Bond (Citation1991) uses more instruments made of the pass values of

, as well as predetermined and exogenous variables. Therefore, the following moment conditions are used to compute the difference estimator.

To account for large autoregressive parameters and ratio of the variance of the cross section-specific effect to the variance of idiosyncratic error, we use the system GMM estimator of Blundell and Bond (Citation1998). The system GMM in EquationEquation (7)(7)

(7) combines the level equation (EquationEquation 3

(3)

(3) ) and the transformed equation (Equation 4).

Where .

Therefore, the above moment conditions are applicable to the system GMM. This is relevant to the estimation because the Equation in levels resorts to the lagged differences of explanatory variables as instruments under the conditions that the error term is not serially correlated and .

In addition to the common Arellano and Bond-type orthogonality conditions from EquationEquation (5)(5)

(5) and EquationEquation (6)

(6)

(6) , the system GMM employs the two following moment conditions on the level equation.

We estimate our empirical model with the two-step system GMM estimators. Since the estimated asymptotic standard errors of the two-step GMM estimator are downward biased (Windmeijer, Citation2005), we use the two-step estimator alongside the Windmeijer Bias-Corrected Robust VCE (variance-covariance matrix of the estimators) in the final step. In GMM practice, as a common rule, the number of instruments must be inferior to the number of groups. Since the system GMM generates more instruments, we apply Roodman’s (Citation2006) approach, which consists of reducing the number of instruments with the “collapse” command available in stata 16. To inspect serial correlation and instruments validity, the Arellano-Bond test and the Hansen test were performed. The former tests the null hypothesis of the absence of second-order autocorrelation of error term; the latter tests the null hypothesis of the joint validity of instruments. In both cases, the null hypothesis is not rejected if the p-value associated with each test is greater than 5%.

3.4. Principal component analysis techniques

For a full exploration of information within the institutional variables, we compute two indices based on the PCA, which is a non-parametric and multivariate approach used to extract relevant information from a set of correlated variables. The PCA uses an orthogonal transformation to convert a set of original correlated variables to principal components, representing a set of values of uncorrelated variables. Let be the institutional variables from the original dataset. Applied to the institutional variables, the PCA include the

components

, starting from a linear combination

of the initial institutional indicators. The PCA covers the maximum variance of the

components. In equating the sum of the squared factor loading, the variance proportion of the original institutional variable covers the first k factors. The sum of the squared factor loading is equal to one if all of the components are maintained. We use a correlation matrix to compute the index by solving the equation

, where

and

, respectively represent the eigenvalue and eigenvector;

is the identity matrix; and

is the correlation matrix of the institutional variables in the initial dataset. We consider eigenvalues greater than one, as suggested by Kaiser (Citation1961), and employ the PCA to compute the two indexes of institutions with ICRG’s political indicators and the Word Bank’s WGIs.

4. Results

4.1. Institutional index based on principal component analysis

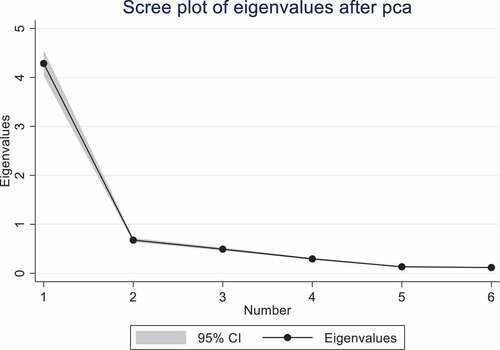

Results on the computation of the index of institutions based on the WGI (INST1) are reported in the annex (). After the computation of the six (06) eigenvalues, only one eigenvalue with a value of 4.286 was found to be greater than one and explained 71.4% of the total variance. shows the plot of the eigenvalues after the PCA.

Figure 1. Scree plot of the eigenvalues after PCA (WGI).

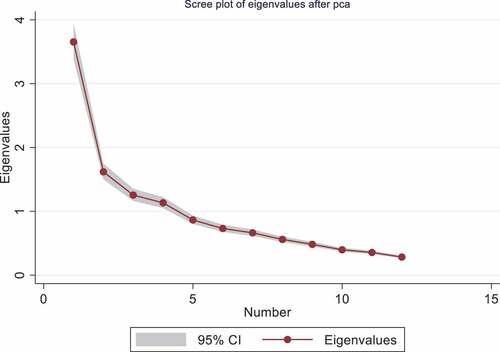

For the twelve (12) institutional indicators of ICRG, four (04) eigenvalues were greater than one and explained 63.8% of the variation. These eigenvalues were 3.653, 1.619, 1.254 and 1.133, which, respectively, explained 30.4 %, 13.5 %, 10.4 % and 9.4 % of the total variance. below presents the plot of the eigenvalues after PCA regarding the ICRG’s institutional indicators. The remaining results concerning the computation of the institutional index (INST2) are reported in the annex ().

Figure 2. Scree plot of the eigenvalues after PCA (ICRG).

4.2. Data and summary statistics of main variables

The data employed in this paper are panel data of 124 developing countries over 17 years, from 2002 to 2018. The initial database comprises of all 135 developing countries. Owing to data unavailability, the final database is reduced to 124 countries (The list of the countries is avaible in Table C1). The time dimension commences in the year 2002 due to the unavailability of annual institutional data before 2002, though the WGI commenced in 1996. To obtain consistent results, we limited all the variables in our dataset to this span, including institutional data of ICRG. reports the descriptive statistics of the main variables. shows that, among our variables of interest, only institutional variables and the external debt as a percentage of the GDP (macroeconomic policies) are positively correlated with net FDI inflow (percentage of GDP), inflation and human capital. Financial development indicators are not significantly correlated with FDI. Regarding the control variables, trade openness and domestic investment are positively correlated with FDI, whereas population is negatively correlated. However, we take these correlations with caution since we are mainly interested in the causal impact of the variable of interest on FDI inflows.

Table 2. Descriptive statistics of the main variables

Table 3. Correlation matrix

4.3. The effects of economic fondamentals on FDI inflows and the catalytic role of institutions

4.3.1. Results based on the institutional index computed with the WGI

reports estimates of the effects of economic fundamentals and institutions on FDI inflows as well as the effects of interactions of economic fundamentals and institutions; institutions being measured by the index of institutions computed with WGIs. Column (1) to Column (5) of report results with only one interaction while Column (6) reports results with the four interactions altogether. For each Column, the p-values associated with AR (2) and Hansen’s test are greater than 5%. While the first-order autocorrelation is tolerated in GMM practice, our results indicate that there is no second-order autocorrelation and that the instruments used are valid. Therefore, post-estimation tests ascertain the validity of estimates in .

Table 4. The effects of economic fundamentals on FDI inflows in developing countries - the modulating effect of institutions—measure of institutions: the index of institutions (WGI)

Columns (1) to (3) report results with interactions of institutions and financial development indicators, including financial development index, financial institutions index and financial market index. None of the coefficients of the interactions is significant, though. Additionally, the coefficients of the interactions of institutions and macroeconomic policies variables—namely, inflation and public external debt—are not significant. However, in column (5) the parameter attached to the interaction of institutions and human capital is significant at the 10% level. The significance levels of the interactions in Column (1) to Column (4) when all interactions are included in the same regression are also consistent with results reported in Column (5) of . Overall, our results indicate that institutions do not modulate the effects of financial development and macroeconomic policies on FDI inflows in developing countries. However, they do for human capital.

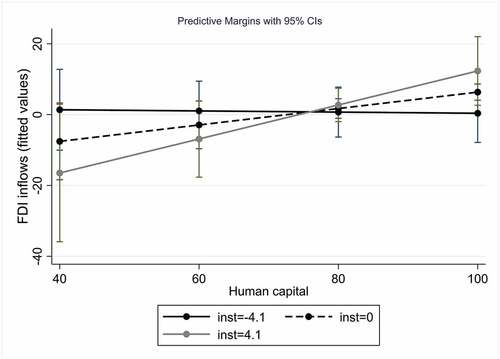

demonstrates the plot of the marginal effects of human capital on FDI inflows at different levels of institutions. When the index of institutions is −4.1 (worse institutions), the marginal effects are flat. The constancy of the marginal effects conveys that investing in human capital in a worse institutional environment do not attract any foreign investors. However, as institutions improve—that is, a higher index of institutions (0 and 4.1)—the marginal effects’ curve slopes upward—that is, investment in human capital has more pronounced effects on FDI inflows.

Figure 3. Marginal effects of human capital with the index of institutions (WGI).

Besides the results on the interactions, the coefficient of human capital is significant in most of the columns of , at 5% and 10% levels. Not only do institutions modulate the effects of human capital on the FDI inflows, but investments in human capital also have great potential to attract FDI inflows. These findings are consistent with Cleeve et al. (Citation2015), Kheng et al. (Citation2017), Okafor et al. (Citation2015), and Noorbakhsh et al. (Citation2001), who all report a direct positive effect of human capital. Moreover, our results regarding the modulating effect of institutions on the marginal effects of human capital on FDI inflows fall on the same line as Dutta and Osei‐Yeboah (Citation2013), Naanwaab and Diarrassouba (Citation2016), and Dutta et al. (Citation2017).

Financial development indeed has a positive direct effect on FDI inflows. The coefficient of the financial development variable in Columns (1), (4), (5) and (6) of is significant at the 1% level. Furthermore, the coefficients related to the index of financial institutions (Column 2) and the index of financial market (column 3) are respectively significant at 5 % and 10 % level. Such results indicate that improvements in both the financial market and financial institutions attract foreign investors. Our findings remain in line with Islam et al. (Citation2020), and Nguyen and Lee (Citation2021).

Regarding macroeconomic policies, while external public debt has no direct effect on FDI inflow, inflation indeed has. The parameter associated with inflation is positive and significant in most of the columns of . Though opposed to Kinda (Citation2009), Dutta et al. (Citation2017), and Sabir et al. (Citation2019), the positive effect of inflation on FDI inflows is in line with Rădulescu and Druica (Citation2014) , and Naanwaab and Diarrassouba (Citation2016). This finding is straightforward even if it falls outside of our expectations. For instance, the relaxation of the monetary policy can encourage investments in infrastructures which may, ultimately, attract foreign investors despite higher inflation that may follow. Furthermore, an expansionary fiscal policy that triggers inflation may stimulate investment and consumption and cause an increase in in the interest rate. Foreign investors may, thus, be attracted by a higher return on capital and higher demand for their products.

The coefficient of the logarithm of GDP is negative and significant at the 1% level in the first column. This outcome is also consistent in the subsequent columns. It indicates that higher economic growth in the host countries is associated with a lower level of FDI inflow. Though in sharp contradiction to our expectations, this finding is in line with the allocation puzzle hypothesis demonstrated by Gourinchas and Jeanne (Citation2013) according to which countries with higher productivity growth attract less FDI inflows. The reason for this is that countries with lower productivity growth impose taxes on financial saving, leading to insufficient national saving compared to investment needs. Consequently, these countries are more likely to turn to foreign capitals. However, our results contradict findings reported by Busse and Hefeker (Citation2007), Lautier and Moreaub (Citation2012), and Cleeve et al. (Citation2015).

From our estimates, we also found that the coefficient of the population was positive and significant in most of the equations estimated in . A growth in developing countries’ populations appears to be a source of opportunities for foreign investors. A large population offers not only a sizeable market for foreign investors but also provides them with cheaper labour. This finding falls in the same line with Asiedu (Citation2005) and Mottaleb and Kalirajan (Citation2010) who find that market size do attracts foreign investors.

As expected, the coefficient of the logarithm of the economic growth rate in the USA is positive and significant across the six columns of . We explain this by the fact that significant economic growth in the USA appears to be closely associated with a decrease in the USA interest rate, leading to a flow of foreign investments in developing countries in search of higher returns. Contrary to our expectations, the effects of domestic investment, institutions, and trade openness on FDI inflows are not significant.

The takeaway of this first analysis is that (1) human capital has both a direct and indirect effect (through institutions) on FDI inflows; (2) financial development and macroeconomic policies (inflation) have only a direct effect on FDI inflows; and (3) while host countries’ populations and the USA’s economic growth have a positive impact on FDI inflows, developing countries with lower productivity growth attract more foreign capital. We inspect the robustness of these findings in the following sub-sections.

4.3.2. The effect of human capital on FDI inflows: Which institution plays a catalytic role?

From the baseline estimates in Column 6 of , institutions are found to modulate the effect of human capital on FDI inflows. We now turn to find out which of the six WGIs best explains this outcome. To that end, we rerun our empirical model where institutions are measured by each World Bank’s institutional metric instead of an index of institutions. The results of these exercises are reported in . From Column (1) to column (6), institutions are measured by control of corruption; government effectiveness; political stability and absence of violence; regulatory quality; the rule of law; and voice and accountability. From an econometric perspective, these estimations are valid, since the probabilities associated with the Hansen and AR (2) denote that, instruments are valid and that there is no second-order autocorrelation. Overall, the results reported in are consistent with the baseline results in . The coefficients of the logarithm of GDP; the USA’s GDP per capita growth; the total population; and the financial development index are all significant.

Table 5. The effects of economic fundamentals on FDI inflows in developing countries - the modulating role of institutions - measure of institutions: the World Bank’s WGIs

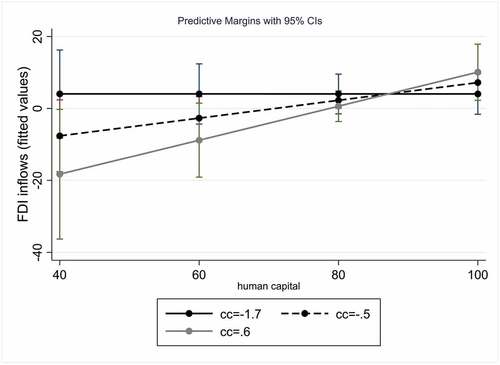

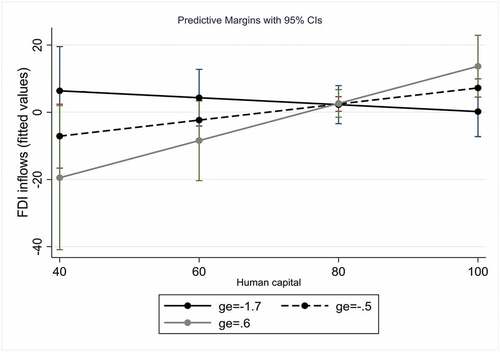

The results demonstrate that the coefficients of the interactions of human capital—with control of corruption on one hand, and effectiveness of government on the other—are positive and significant at the 10% level. Of the six institutional metrics, control of corruption and government effectiveness modulate the effect of human capital on FDI inflows. The marginal effects of human capital on FDI inflows plotted in demonstrate that a huge investment in human capital when the score of the control of corruption is −1.7 has no effect on FDI inflows; however, the marginal effect of human capital on FDI inflow becomes an increasing function of institutions when the score of control of corruption is −0.5 and 0.6. A similar pattern for the effectiveness of government is reported in . In conclusion, a country’s capacity to combat the use of public services for private end, and its ability to formulate, implement and commit to policies are relevant in enhancing the effect of human capital on FDI inflows.

Figure 4. Marginal effects of human capital as a function of control of corruption.

Figure 5. Marginal effects of human capital as a function of government effectiveness.

4.3.3 Robustness checks

In this section we perform a series of robustness checks. We first conduct a subperiod analysis around the 2008 financial crisis. Our baseline estimation is re-estimated for both the sub-periods 2002–2007 and 2008–2018. Further, we employ alternative identification strategies—that is, the instrumental variable approach and the two-step Arellano–Bond GMM estimator. We also use an alternative proxy of institutions; here, the quality of institutions has been measured with political risk indicators from ICRG.

Robustness check with subsample analysis

The 2008 financial crisis has had a huge impact on capital inflows’ allocation around the globe (Dornean et al., Citation2012) and have changed their determinants (Fratzscher, Citation2012; Zoungrana & tanToé, Citation2018). For instance, according to Fratzscher (Citation2012), during the financial crisis, FDI inflows were determined by push factors, whereas in the aftermath FDI inflows were driven by pull factors. A recent study by Zoungrana and tanToé (Citation2018) demonstrates that the 2008 financial crisis had chased out market-seeking investors and had appealed to resource-seeking investors. Accordingly, we hypothesise that the pattern of FDI determinants may vary substantially pre- and post-2008 crisis. We thus performed a subperiod analysis around 2008 to check not only our baseline results but also to what extent the effects of this external shock manifested in our estimates. The results concerning the period before the crisis and the period after the crisis are reported in Columns (2) and Column (3) of , respectively. The pattern of the determinant of FDI inflows before and after the crisis is slightly different. Before the crisis, human capital, domestic investment, and population growth were the main drivers of FDI inflows. We learn from this estimation that, prior to the financial crisis, foreign investors were not sensitive to financial market development in the host countries and to external shocks, such as sudden economic growth in the USA.

Table 6. The effects of economic fundamentals f on FDI inflows in developing countries - the modulating role of institutions—robustness analysis:subperiod analysis, Othogonal difference GMM and instrumental variable approach

After the crisis, the pattern of the determinant of FDI was consistent with our baseline estimates, which were reported again in column (1) of . Economic growth in the host countries; economic growth in the USA; population growth; and inflation are determinants of FDI. What is also consistent with our baseline results is the significance of the coefficient of the interaction of institutions and human capital. Still, the quality of institutions modulates the effect of human capital on FDI inflows. We also consistently found that the effects of financial development and macroeconomic policies were not significantly modulated by institutions.

Robustness check with alternative identification strategies: Instrumental variable approach and Difference GMM

The results concerning the two-step GMM, based on the forward orthogonal alongside the Windmeijer Bias-Corrected Robust VCE, are reported in Column (4) of . As one can notice, the results are consistent with the baseline estimates. Most importantly, institutions modulate the effect of human capital on FDI inflows. Furthermore, improving the quality of institutions does not strengthen the effects of financial development and macroeconomic policies on FDI inflows significantly.

We also regressed the empirical model with the instrumental variable approach. Since we consistently found that institutions modulated the effect of human capital on FDI inflows, we focused on human capital by instrumenting it on two external instruments—namely, arable land and infantile mortality rate—following Dutta and Osei-Yeboah (Citation2013). The results are consistent with our baseline estimate. While institutions modulate the effect of human capital on the FDI inflows to developing countries, we consistently find no such modulating effect with financial development and macroeconomic policies.

Robustness check with Political Risk Indicators of ICRG

We performed the same analysis that we did in column (6) of and to summarise the gist of our baseline estimates. Here, however, institutions are measured by political risk indicators from ICRG. In the first column, institutions are measured by the index of institutions computed with the PCA (INST2). In the subsequent columns, institutions are measured, respectively, by government stability; socio-economic condition; investment profile; internal conflict; external conflict; corruption; military in politic; religious tension; law and order; ethnic tension; democratic accountability; and bureaucracy quality.

The results of the two-step system GMM are reported in . They are consistent with the baseline results, apart from the fact that the effect of investment became significant, while the direct effect of human capital was no longer significant. Nonetheless, our main results are again confirmed: the marginal effect of human capital on FDI inflow is a positive function of institutional quality. Still, institutions do not significantly modulate the effects of macroeconomic policies and financial development on FDI inflows. The subsequent columns confirm the modulating effect of institutions on human capital and demonstrate that socio-economic condition; investment profile; external conflict; military in politics; and religious tension play significant roles in this respect.

Table 7. The effects of economic fundamentals on FDI inflows in developing countries - the modulating effect of institutions—robustness checking with an alternative measure of institutions

All things considered, after the robustness checks performed on our baseline estimates, we consistently found that, among economic fundamentals of interest, only financial development had a positive direct effect on FDI inflows. We also consistently found that institutions only modulated the effect of human capital on FDI inflows.

5. Conclusions

Considering the lack of financial resources in developing countries and the role of FDI in development, policymakers in developing countries believe that FDI would play a significant role in attaining SDGs. Still, policymakers are puzzled by the multiplicity of arguments advanced by social scientists. To supply policymakers with tools to attract multinationals, this paper set two goals. First, it analysed the direct effects of human capital (HCAP), macroeconomic policies (MP) and financial development (FD) on FDI inflows; second, it assessed the moderating role of institutions on the FD-FDI, MP-FDI and HCAP-FDI nexuses. Using a panel data of 124 developing countries spanning from 2002 to 2018, the paper employed the two-step system GMM alongside the Windmeijer Bias-Corrected Robust VCE. For robustness checks, it used three strategies. First, the empirical model was estimated with the instrumental variable approach and two-step GMM, based on the forward orthogonal deviations. Second, a subsample analysis was performed before and after the 2008 financial crisis. Third, the political risk indicators of ICRG were utilised as alternative institutional metrics of the WGIs. The findings of this paper underscore that financial development has a positive and significant direct effect on FDI inflows. Most importantly, though no evidence on the modulating effect of institutions on FD-FDI and MP-FDI nexuses exists, institutions moderate the effect of human capital on FDI inflows in developing countries positively. This paper has shed light on the contentious issue that foreign investors are only interested in the cheaper labour forces and natural resources in developing countries. Contrary to that common perception, we found that multinationals also consider human capital and the financial market. These findings have implications for policies aimed at attracting FDI in developing countries. In that respect, we suggest that policymakers undertake a massive investment in human capital and develop their financial markets. To reap the full benefits of their investment in human capital, policymakers ought to undertake institutional reforms to root out corrupt practices and conflicts (external and religious), as well as maintain a friendly investment profile and strengthen government effectiveness.

Author contributions

This paper is part of a Ph. D dissertation by Gildas Kadoukpè MAGBONDE, under the supervisions of Professor Mamadou Abdoulaye Konté. Though the conceptualization, the methodology, and the analysis are drafted and wrote by Gildas Kadoukpè MAGBONDE, Professor Mamadou Abdoulaye Konté supervised each of the sessions, provided advice to improve them, and contributed to the editing too. The two authors have agreed to publish the manuscript.

Availability of data

Data used in these studies are available and can be supply upon request.

Code availability

Stata codes used in this article are available and can be provided upon request

Acknowledgements

We are grateful to Laboratoire de Recherche en Economie de Saint-Louis (LARES) of Gaston Berger University who offers space, internet, and resources to conduct and finalized this paper.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Gildas Kadoukpè Magbondé

Gildas Kadoukpè Magbondé holds an MA in Applied Macroeconomics, an MA in Political Science from the University of Abomey-Calavi (Benin), and an MA in International and Development Economics from the University of Namur (Belgium). He’s currently a Ph.D. Student in applied macroeconomics at Gaston Berger University (Senegal). His doctoral research focuses on foreign direct investments (FDI), institutions, structural transformation, and economic growth in developing countries. In addition, Gildas Kadoukpè MAGBONDE shows a keen interest in microeconomic issues such as poverty and impact evaluations of public interventions.

Mamadou Abdoulaye Konté is a professor of economics at Gaston Berger University. He currently cumulates the position of the head of the Economic Department and the head of doctoral training in Economics. He got a master’s degree from Paris Dauphine University (France) and Ph. D from Panthéon Sorbonne University (France) in the field of quantitative economics and finance. Up to date, Professor Mamadou Abdoulaye KONTE has more than ten publications in the field of economics, finance, and applied mathematics.

References

- Acemoglu, D., Johnson, S., & Robinson, J. A. (2001). The colonial origins of comparative development: An empirical investigation. American Economic Review, 91(5), 1369–36. https://doi.org/10.1257/aer.91.5.1369

- Agbloyor, E. K., Abor, J., Adjasi, C. K. D., & Yawson, A. (2013). Exploring the causality links between financial markets and foreign direct investment in Africa. Research in International Business and Finance, 28 C , 118–134. https://doi.org/10.1016/j.ribaf.2012.11.001

- Aizenman, J., Jinjarak, Y., & Park, D. (2015). Financial development and output growth in developing Asia and Latin America: A comparative sectoral analysis. In NBER working papers. NBER Working Papers). National bureau of economic research, Inc. No 20917. https://ideas.repec.org/p/nbr/nberwo/20917.html

- Akhtaruzzaman, M., Berg, N., & Hajzler, C. (2017). Expropriation risk and FDI in developing countries: Does return of capital dominate return on capital? European Journal of Political Economy, 49 C , 84–107. https://doi.org/10.1016/j.ejpoleco.2017.01.001

- Alfaro, L., Kalemli-Ozcan, S., & Sayek, S. (2009). FDI, Productivity and financial development. The World Economy, 32(1), 111–135. https://doi.org/10.1111/j.1467-9701.2009.01159.x

- Alfaro, L., Kalemli-Ozcan, S., & Volosovych, V. (2008). Why doesn’t capital flow from rich to poor countries? An empirical investigation. The Review of Economics and Statistics, 90(2), 347–368. https://doi.org/10.1162/rest.90.2.347

- Alguacil, M., Cuadros, A., & Orts, V. (2011). Inward FDI and growth: The role of macroeconomic and institutional environment. Journal of Policy Modeling, 33(3), 481–496. https://doi.org/10.1016/j.jpolmod.2010.12.004

- Anderson, T. W., and Hsiao, Cheng 1981 Estimation of Dynamic Models with Error Components Journal of the American Statistical Association 76 355 598–606 https://doi.org/10.2307/2287517

- Arellano, M., & Bond, S. (1991). Some tests of specification for panel data : Monte carlo evidence and an application to employment equations. Review of Economic Studies, 58(2), 277–297. https://doi.org/10.2307/2297968

- Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68(1), 29–51. https://doi.org/10.1016/0304-4076(94)01642-D

- Asiedu, E. (2005). Foreign direct investment in Africa: The role of natural resources, market size, government policy, institutions and political instability (SSRN Scholarly Paper ID 717361). Social Science Research Network. https://doi.org/10.2139/ssrn.717361

- Asiedu, E., & Lien, D. (2011). Democracy, foreign direct investment and natural resources. Journal of International Economics, 84 1 , 99–111. https://doi.org/10.2139/ssrn.1726587

- Azam, J.-P. (1999). Institutions for macroeconomic stability in Africa. Journal of African Economies, 8(suppl_1), 6–29. https://doi.org/10.1093/jafeco/8.suppl_1.6

- Aziz, O. G. (2018). Institutional quality and FDI inflows in Arab economies. Finance Research Letters, 25 C , 111–123. https://doi.org/10.1016/j.frl.2017.10.026

- Barro, R. J. (1990). Government spending in a simple model of endogenous growth. Journal of Political Economy, 98(5), 103–125. Scopus. https://doi.org/10.1086/261726

- Beck, T., & Levine, R. (2003). Legal institutions and financial development (SSRN Scholarly Paper ID 476083). Social Science Research Network. https://papers.ssrn.com/abstract=476083

- Beck, T. (2002). Financial development and international trade: Is there a link? Journal of International Economics, 57(1), 107–131. https://doi.org/10.1016/S0022-1996(01)00131-3

- Bilir, K., Chor, D., & Manova, K. (2014). Host-country financial development and multinational activity. In NBER working papers. NBER Working Papers). National Bureau of Economic Research, Inc. No 20046. https://ideas.repec.org/p/nbr/nberwo/20046.html

- Blancheton, B., & Opara-Opimba, L. (2010). Foreign direct investment in Africa: What are the key factors of attraction aside from natural resources? In Cahiers du GREThA (2007-2019) (N o 2010–14; Cahiers Du GREThA (2007-2019)). Groupe de recherche en economie théorique et appliquée (GREThA). https://ideas.repec.org/p/grt/wpegrt/2010-14.html

- Blomstrom, M., & Kokko, A. (1997). How foreign investment affects host countries (Policy Research Working paper Series No 1745). The World Bank. https://econpapers.repec.org/paper/wbkwbrwps/1745.htm

- Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143. https://doi.org/10.1016/S0304-4076(98)00009-8

- Boateng, A., Hua, X., Nisar, S., & Wu, J. (2015). Examining the determinants of inward FDI : evidence from Norway. Economic Modelling, 47 C , 118–127. https://doi.org/10.1016/j.econmod.2015.02.018

- Brun, J., & Gnangnon, S. K. (2017). Does trade openness contribute to driving financing flows for development? (WTO Staff Working Paper ERSD-2017-06). World trade organization (WTO), Economic research and statistics division. https://econpapers.repec.org/paper/zbwwtowps/ersd201706.htm

- Buch, C. M., Kesternich, I., Lipponer, A., & Schnitzer, M. (2014). Financial constraints and foreign direct investment: Firm-level evidence. Review of World Economics, 150(2), 393–420. https://doi.org/10.1007/s10290-013-0184-z

- Buchanan, B. G., Le, Q. V., & Rishi, M. (2012). Foreign direct investment and institutional quality: Some empirical evidence. International Review of Financial Analysis, 21, 81–89. https://doi.org/10.1016/j.irfa.2011.10.001

- Busse, M., & Hefeker, C. (2007). Political risk, institutions and foreign direct investment. European Journal of Political Economy, 23(2), 397–415. https://doi.org/10.1016/j.ejpoleco.2006.02.003

- Cai, H., Boateng, A., & Guney, Y. (2019). Host country institutions and firm-level R&D influences: An analysis of European Union FDI in China. Research in International Business and Finance, 47, 311–326. https://doi.org/10.1016/j.ribaf.2018.08.006

- Calvo, G. A., Leiderman, L., & Reinhart, C. M. (1996). Inflows of capital to developing countries in the 1990s. Journal of Economic Perspectives, 10(2), 123–139. https://doi.org/10.1257/jep.10.2.123

- Canh, N. P., Binh, N. T., Thanh, S. D., & Schinckus, C. (2020). Determinants of foreign direct investment inflows: The role of economic policy uncertainty. International Economics, 161, 159–172. https://doi.org/10.1016/j.inteco.2019.11.012

- Cezar, R., & Escobar, O. (2015). Institutional distance and foreign direct investment (SSRN Scholarly Paper ID 2700089). Social Science Research Network. https://doi.org/10.2139/ssrn.2700089

- Choong, C.-K., & Lim, K.-P. (2009). Foreign direct investment, financial development, and economic growth: The case of Malaysia. Macroeconomics and Finance in Emerging Market Economies, 2(1), 13–30. https://doi.org/10.1080/17520840902726227

- Cleeve, E. A., Debrah, Y., & Yiheyis, Z. (2015). Human capital and FDI inflow : An assessment of the African case. World Development, 74(C), 1–14. https://doi.org/10.1016/j.worlddev.2015.04.003

- Contractor, F. J., Dangol, R., Nuruzzaman, N., & Raghunath, S. (2020). How do country regulations and business environment impact foreign direct investment (FDI) inflows? International Business Review, 29(2), 101640. https://doi.org/10.1016/j.ibusrev.2019.101640

- Cukierman, A., Edwards, S., & Tabellini, G. (1992). Seigniorage and Political Instability. American Economic Review, 82(3), 537–555 https://www.alexcuk.sites.tau.ac.il/_files/ugd/179175_3f2ced27c95a493cbbd0b5855e0c0dae.pdf?index=true.

- Das, P 2019 Limited Dependent Variable Model Springer. Econometrics in Theory and Practice: Analysis of Cross Section, Time Series and Panel Data with Stata 15.1

- Desbordes, R., & Wei, S.-J. (2017). The effects of financial development on foreign direct investment. Journal of Development Economics, 127 C , 153–168. https://doi.org/10.1016/j.jdeveco.2017.02.008

- Donaubauer, J., Neumayer, E., & Nunnenkamp, P. (2016). Financial market development in host and source countries and its effects on bilateral FDI. In kiel working papers (No 2029; Kiel Working Papers). Kiel Institute for the World Economy (IfW). https://ideas.repec.org/p/zbw/ifwkwp/2029.html

- Dornean, A., Işan, V., & Oanea, D.-C. (2012). The impact of the recent global crisis on foreign direct investment. Evidence from Central and Eastern European countries. Procedia Economics and Finance, 3, 1012–1017. https://doi.org/10.1016/S2212-5671(12)00266-3

- Du, J., Lu, Y., & Tao, Z. (2008). Economic institutions and FDI location choice: Evidence from US multinationals in China. Journal of Comparative Economics, 36(3), 412–429. https://doi.org/10.1016/j.jce.2008.04.004

- Dunning, J. H. (1977). Trade, location of economic activity and the MNE: A search for an eclectic approach. In B. Ohlin, P.-O. Hesselborn, & P. M. Wijkman ( Éds.), The international allocation of economic activity: Proceedings of a Nobel Symposium held at Stockholm (pp. 395–418). Palgrave Macmillan UK. https://doi.org/10.1007/978-1-349-03196-2_38

- Dunning, J. H. (1988). Explaining International Production. HarperCollins Publishers Ltd.

- Dutta, N., Kar, S., & Saha, S. (2017). Human capital and FDI: How does corruption affect the relationship? Economic Analysis and Policy, 56, 126–134. https://doi.org/10.1016/j.eap.2017.08.007

- Dutta, N., & Osei‐Yeboah, K. (2013). A new dimension to the relationship between foreign direct investment and human capital: The role of political and civil rights. Journal of International Development, 25(2), 160–179. https://doi.org/10.1002/jid.1739

- Dutta, N., & Roy, S. (2011). Foreign direct investment, financial development and political risks (SSRN Scholarly Paper ID 2206384). Social Science Research Network. https://papers.ssrn.com/abstract=2206384

- Ehrlich, I., & Lui, F. T. (1999). Bureaucratic corruption and endogenous economic growth. Journal of Political Economy, 107(S6), S270–S293. https://doi.org/10.1086/250111

- Fatton, R. (1992). Predatory rule: State and civil society in Africa. Lynne Rienner.

- Fernández-Arias, E., & Hausmann, R. (2011). International initiatives to bring stability to financial integration. In IDB publications (Working Papers). IDB publications (Working Papers)). Inter-American development bank. No 1304. https://ideas.repec.org/p/idb/brikps/1304.html

- Fon, R. M., Filippaios, F., Stoian, C., & Lee, S. H. (2021). Does foreign direct investment promote institutional development in Africa? International Business Review, 30(4), 101835. https://doi.org/10.1016/j.ibusrev.2021.101835

- Fratzscher, M. (2012). Capital flows, push versus pull factors and the global financial crisis. Journal of International Economics, 88(2), 341–356. https://doi.org/10.1016/j.jinteco.2012.05.003

- Gastanaga, V. M., Nugent, J. B., & Pashamova, B. (1998). Host country reforms and FDI inflows: How much difference do they make? World Development, 26(7), 1299–1314. https://doi.org/10.1016/S0305-750X(98)00049-7

- Globerman, S., & Shapiro, D. (2002). Global foreign direct investment flows: The role of governance infrastructure. World Development, 30(11), 1899–1919. https://doi.org/10.1016/S0305-750X(02)00110-9

- Gossel, S. J. (2018). FDI, democracy and corruption in Sub-Saharan Africa. Journal of Policy Modeling, 40(4), 647–662. https://doi.org/10.1016/j.jpolmod.2018.04.001

- Gourinchas, P-O, and Jeanne, O 2013 Capital Flows to Developing Countries: The Allocation Puzzle The Review of Economics Studies 80 4 1484–1515 https://doi.org/10.1093/restud/rdt004

- Greider, W. (1998). One world, ready or not: The manic logic of global capitalism. Simon & Schuster.

- Guadalupe, M., Kuzmina, O., & Thomas, C. (2012). Innovation and foreign ownership. American Economic Review, 102(7), 3594–3627. https://doi.org/10.1257/aer.102.7.3594

- Haraguchi, N., Martorano, B., & Sanfilippo, M. (2019). What factors drive successful industrialization? Evidence and implications for developing countries. Structural Change and Economic Dynamics, 49 C , 266–276. https://doi.org/10.1016/j.strueco.2018.11.002

- Harms, P., & Ursprung, H. (2002). Do civil and political repression really boost foreign direct investments? Economic Inquiry, 40(4), 651–663. https://doi.org/10.1093/ei/40.4.651

- Henisz, W. J. (2009). The institutional environment for multinational investment. Economic Institutions of Strategy 26 , 425–458.

- Islam, M., Khan, M., Popp, J., Sroka, W., Oláh, J., Popp, J., & Popp, J. (2020). Financial development and foreign direct investment-the moderating role of quality institutions. Sustainability, 12(9), 3556. https://doi.org/10.3390/su12093556

- Jain, A. K. (2001). Corruption: A Review. Journal of Economic Surveys, 15(1), 71–121. https://doi.org/10.1111/1467-6419.00133

- Jallab, M. S., Gbakou, M. B. P., & Sandretto, R. (2008). Foreign direct investment, macroeconomic instability and economic growth in MENA countries. In Working papers. Université de Lyon. (No 0817; Working Papers). Groupe d’Analyse et de Théorie Economique Lyon St-Étienne (GATE Lyon St-Étienne). https://ideas.repec.org/p/gat/wpaper/0817.html

- Jensen, N. M. (2003). Democratic governance and multinational corporations: Political regimes and inflows of foreign direct investment. International Organization, 57(3), 587–616. https://doi.org/10.1017/S0020818303573040

- Jude, C., & Levieuge, G. (2016). Growth effect of foreign direct investment in developing economies: The role of institutional quality. The World Economy. 40. https://doi.org/10.1111/twec.12402

- Kaiser, H. F. (1961). A note on Guttman’s lower bound for the number of common factors. British Journal of Statistical Psychology, 14(1), 1–2. https://doi.org/10.1111/j.2044-8317.1961.tb00061.x

- Kaufmann, D., Kraay, A., & Zoido-Lobaton, P. (1999). Governance matters. Policy research working paper series. The World Bank. (N o 2196; Policy Research Working Paper Series). https://ideas.repec.org/p/wbk/wbrwps/2196.html.

- Kaur, M., Yadav, S. S., & Gautam, V. (2013). Financial system development and foreign direct investment: A panel data study for BRIC countries. Global Business Review, 14(4), 729–742. https://doi.org/10.1177/0972150913501607

- Kesternich, I., & Schnitzer, M. (2010). Who is afraid of political risk? Multinational firms and their choice of capital structure. Journal of International Economics, 82(2), 208–218. https://doi.org/10.1016/j.jinteco.2010.07.005