?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Regional economies seek to promote growth through industrialisation and literature suggests that developing the financial system, integrating the financial system within a sound institutional framework can promote industrial output. This study fills the gap by examining the impact of financial development and regional financial integration on ECOWAS’ industrial sector. This study assesses whether regional financial integration and financial development have a stronger effect on the growth of the industrial sector of ECOWAS member countries that have high level of institutional quality than it does in countries with lower level. Major findings from the study reveals that deepening regional financial integration can only enhance the industrial output of ECOWAS member countries that has sound institutional quality framework; this is important and is a strong enhancing factor for member countries experiencing low industrial sector output. Credit to the private sector alone both for countries with low industrial output and countries with high industrial output does not improve the level of industrial performance. However, for countries that have low industrial output with a stronger institutional quality framework, increases in credit to the private sector will increase the level of industrial output compared to countries with a higher level of industrial output. Increasing the level of money in circulation alone does not improve industrial sector performance; the quantum channeled as credit to the private sector does. An improved institutional framework must be set in place together with an enhanced flow of credit to the private sector in ECOWAS.

PUBLIC INTEREST STATEMENT

Enhancing the industrial sector is crucial to ensuring sustained economic growth of an economy. This is not different for the Economic Community of West African States (ECOWAS). Regional economies seek to achieve this by developing a robust and integrated financial system under a sound institutional framework. This study examines the effect of integrating the financial system which is robust under a strong institutional framework on the industrial sector output of ECOWAS region. The result from the study shows that integrating the financial system and ensuring more credit to the private sector can only enhance the industrial output of ECOWAS member countries when there is a robust institution. This is very important for group of countries experiencing low industrial sector output. A robust institutional framework and enhanced credit to the private sector must be continually pursued by ECOWAS to engender industrial growth.

1. Introduction

Economies globally have continued to pursue growth objectives and the continuous improvement in the welfare of their citizens. To do this end, several policies have been designed with respect to strengthening her institutions, creating an enabling environment for firms to thrive and ensuring that funds are readily available for investors. Despite these great resounding measures, most of the African economies have found themselves behind the pecking order among the global competitors. The need to foster common development and economic prosperity has been pursued since in the 1970s with the creation of the Economic Community of West African state by a group of initially 16 West African economies but now 15. The Economic Community of West African States (ECOWAS) is a regional organisation made up of 15 West Africa member countries established in 1975 for the purpose of enhancing economic integration in all fields of activity of the constituting countries (ECOWAS, Citation2016). This organisation and its economic arrangement seeks to devise strategies that can foster economic prosperity by ensuring equality and inter-dependence of member states, self-reliance, promote inter-state cooperation, harmonisation and integration of programmes among others (ECOWAS, Citation2016). The centrality of major activities that can facilitate the achievement of this target is the design of well-articulated policies and measures that will foster massive productions within each country thereby strengthening the industrial sector. As opined by Rostow in his stages of growth theory, the major driver in stimulating development (take-off) must include substantial growth of the industrial sector of the economy as well resource mobilisation in financing such investments (Todaro & Smith, Citation2015). The implication of this is that developing economies must thrive to seek for ways of promoting her industrial sector base as this will ensure sufficient production and input of other sectors to substantially grow and enjoy prosperity.

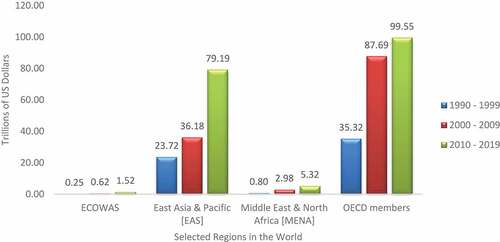

Despite the policies of ECOWAS, its member countries have not been able to experience breakthroughs in their industrial sector and the economy at large. Figure shows that the industry value added between 1990 and 2019 for each decade has not reached the mark of 2 trillion US dollars, compared to OECD member countries that increased from 35.32 trillion USD between 1990–1999 to 99.55 trillion USS between 2010 and 2019. Even the middle east and North Africa countries are also faced with similar challenges only that between 2000 and 2009, it crossed 2 trillion mark.

Figure 1. Comparison of industry value-added of selected regions in the world in current US$.

This becomes obvious that ECOWAS member countries must continue to develop strategies that can ensure improvement in the industrial sector performance. Economic literature (Ahmed, Citation2016; Edison et al., Citation2002; Garretsen et al., Citation2004; Guiso et al., Citation2004) have suggested that poor mobilization of financial resources in the form of weak financial development framework is a major factor militating against the progress of economic growth in developing economies. Schumpeter (Citation1911) in his groundbreaking research emphasised the role of the bank as the major financier of industrial activities; this implies that the development of financial institutions is a prerequisite for economic growth and development. Banks and financial institutions can thus mobilise financial resources in the form of credit to the industrial sectors towards increasing production. This can then lead to we testing a hypothesis that financial development can be a veritable tool of enhancing the industrial sector of any economy.

As financial development plays a critical role within each economy in fostering economic growth and improvement in the industrial sector, the coming together of the financial systems of regional economies to form regional financial integration can be of great deal. There have been significant although gradual reforms in the financial system of developing economies that suggests the emergence of regional financial integration. Such policies focus on financial market liberalization, privatization, technical modernization, improvement in internal and external monitoring mechanisms, revisions of investment codes to enhance foreign participation, and implementation of various institutional and regulatory changes (Ahmed, Citation2016). Literature (Ahmed, Citation2016; Ekpo & Chuku, Citation2017) suggests that weak financial development and financial integration could be an inhibiting factor promoting the success of African economies. Financial integration empowers member countries to take the advantage of the “systemic scale economies” which accrues to larger financial systems.

It is against this backdrop that this study seeks to examine the impact of financial development on the industrial output of ECOWAS member countries. Specifically, the study examines the impact of broad money supply on industrial output, the impact of credit to private sector on industrial output, the effect of regional financial integration on industrial output, the effect of institutional quality on industrial output and the interactive effect of institutional quality together with financial development on industrial sector output in ECOWAS. The study also examines the interactive effect of institutional quality together with regional financial integration on industrial sector output in ECOWAS region. The study tests the null hypotheses that broad money supply, credit to private sector, regional financial integration, institutional quality does not have significant effect on industrial output in ECOWAS. Also, another null hypothesis tested is that institutional quality does not significantly determine the effect which financial development and regional financial integration has on industrial sector output in ECOWAS region. In expanding the frontier of knowledge, we propose that financial development and regional financial integration may not be sufficient in improving the industrial sector performance within ECOWAS, improvement in institutional quality within the region can be a propelling force. Fergusson (Citation2006) noted that differences in institutions explain the fundamental causes of differences in the long-run economic performance of countries. We apply this to the ECOWAS region and thus examines if there is a stronger impact of financial development and regional financial integration on the industrial output of ECOWAS member countries with the presence of strong institutions?

The study contributes to knowledge in two areas. First, studies have examined how regional financial integration impacts on economic growth in Africa (Ekpo & Chukwu, Citation2017; Ahmed, Citation2016) and in WAMZ (Adedokun et al., Citation2020). Studies have also examined the impact of financial development on economic growth (Ahmed, Citation2016; Ibrahim & Alagidede, Citation2018). However, there is scanty literature to the best of our knowledge that have examined the impact of financial development and regional financial integration on industrial sector performance, the closest was the study by Ibrahim and Vo (Citation2020) but considered economic integration and sectoral outcomes in Sub-Saharan Africa. This study takes a deeper approach by narrowing its impact to the critical sector of the economy—the industrial sector. Also, the study is novel as the scope of the study covers ECOWAS member countries, which other studies have not taken into consideration. More importantly, the study extends the frontier of knowledge by examining the role institutional quality plays in determining the effect which financial development and regional financial integration has on industrial sector output in ECOWAS region. Other studies (Ahmed, Citation2016; Ekpo & Chuku, Citation2017) that secondarily considered institutions, regional financial development and growth did not consider it as a mediating role but only considered an aspect of institution. Our study constructs an index that factors all the six measures of institution and also further examines two critical aspects of such measure—control of corruption and regulatory quality.

The study covers all the ECOWAS member countries which are Benin, Burkina Faso, Cabo Verde, Cote d’Ivoire, The Gambia, Ghana, Guinea, Guinea-Bissau, Liberia, Mali, Niger, Nigeria, Senegal, Sierra Leone and Togo and the data will span through the period 1996–2019 as institutional quality indicators were only available from 1996.

The remaining part of this paper is organised into four sections. Section two examines theoretical and empirical issues surrounding the theme of the study while section three critically analyses the methods to follow in achieving the objective. The section three also includes model specification. Section four analyses the data and present the findings of the study while the fifth section concludes and presents the policy implication of the study.

2. Literature review

There is scanty literature that have examined the impact of financial development on industrial sector performance; regional financial integration and industrial sector performance and institutional quality and industrial sector performance. Major empirical evidence only provides the linkage between these tripartite variables and economic growth. Thus, major reviews in this section focus mainly on financial development, regional financial integration, institutions and economic growth.

Empirically, Ekpo and Chuku (Citation2017) examined the impact of regional financial integration on economic activity in Africa. The study employed the interest rate differentials to proxy regional financial integration as well as the state-space model which is the gap between the capital stock index and a benchmarked weighted dominant capital market index. Employing the System Generalised Methods of Moments (SYS-GMM), the study found evidence of regional financial integration impacting positively and significantly on economic growth in African countries. Although the study’s central focus is Africa, the number of countries (17 African countries were selected out of over 50 member countries) employed is not substantial and a true representative of African countries. Also, within Africa, there are about nine monetary integration unions in Africa (EAC, SACU, SADC, COMESA, CEMAC, UMA, CFA, WAEMU and ECOWAS), each of these has unique monetary and economic integration they pursue, examining regional financial integration across the entire continent can be affected by institutional rigidities present in each union thus impacting on the result of the studies.

Ahmed (Citation2016) examined the impact of the integration of the financial markets and financial development on economic growth in Africa. The study employed the dynamic system GMM to achieve its objectives using 30 Sub-Saharan African countries, a partial representation of Africa as a whole. The study found that international financial market integration enhances the economic growth of member states through the enhancement of the depth of the domestic financial system. The study focused attention on the extent of the development of the stock market as a measure of financial development and considered international financial integration without considering first how the regional financial integration can be achieved before international financial market integration. The exploratory investigation conducted by Ehigiamusoe and Lean (Citation2018) suggests that integration results into more competitive market in which firms can have access to greater technological spillovers which then engender economic growth. They also concluded that financial integration has significant impact on economic growth.

Ibrahim and Vo (Citation2020) examined the impact of economic integration on sectoral values and the mediating role financial development plays in 28 selected sub-Saharan African countries between the periods 1985 and 2015. The study employed the Generalised Methods of Moments and the sectors considered are the industry, services and Agriculture. Other integration measures considered are trade integration and financial integration. The study however used financial globalization measures to proxy financial integration. Our study relies on the interest rate differential which is not a dejure nor defacto measure of financial integration. The result from their study support the hypothesis that economic integration enhances industrial, services and agricultural output. Amongst the measures of economic integration, trade integration is found to be more robust and impactful.

Mendoza et al. (Citation2009) examined the global imbalances among industrial nations, the degree of financial integration and the role of financial development in this puzzle. Using the dynamic stochastic general equilibrium, the study found that increases in international financial integration is a major cause of global imbalances as both the industrial and developing countries differ with their level of financial development. Many of the countries that have deeper financial markets borrow much from abroad to invest in very risky assets. Fergusson (Citation2006) examined the role which financial development plays in the impact which financial institutions have on economic development using the expository style of investigation by analysing the past research work that have been done in this area. The study found that through larger and better financial markets, financial institutions can positively enhance economic development.

Huang et al. (Citation2014) examined the impact of financial development volatility on industrial sector growth volatility. Using panel data regression estimation technique, the result from the study shows that financial development volatility impacts heavily on the volatility of industrial sectors especially for those that rely on the external source of financing. The study noted that the volatility that increases industrial volatility comes from both volatilities in the banking sector as well as volatility in the stock market. A similar study examined by Patrick (Citation1966) found that financial development is critical to the growth of the economy for underdeveloped economies. In the studies of Marcelin and Mathur (Citation2014), the authors examined the impact of institutional frameworks available in an economy on financial development and employed a descriptive style of investigation. The result from the study shows that some critical institutional measures is needed to enhance financial development. The findings by Lothian (Citation2006) corroborate the role of the institution on capital flows and financial integration. Lothian noted that institutional factors—good policy, the pursuit of price stability—are critical in enhancing capital flows and financial integration.

Ibrahim and Alagidede (Citation2018) examined the impact of financial development on economic growth in 29 sub-Saharan African countries using the systems generalised methods of moments. The findings from the study show that financial development enhances economic growth; however, the extent of its impact is dependent on the simultaneous growth of real and financial sectors. In a similar study, Ibrahim (Citation2020) examined the impact of trade integration as well as financial integration on the structural transformation of 32 selected African countries, using the threshold regression estimation technique. The study found that financial integration and trade integration does not on its own but jointly explains the cross-country differences in the African level of structural transformation. The study concluded that trade integration will be enhanced when non-tariff bottlenecks have been addressed.

Guiso et al. (Citation2004) examined the effect of financial development on the business prospects of local firms within an integrated financial market. In their studies, financial development was measured using the probability at which a local firm or household is excluded from the credit market system. Microdata were collected for about 8000 households and models were estimated using the ordinary least square regression and instrumental variable technique. The result from the study suggests that financial development enhances improved economic conditions as this tends to increase the establishment of businesses, enhance growth and competition. The result also found that local small businesses benefit more from financial development than the high industrial economies.

Neusser and Kugler (Citation1998) examined the impact of financial development on manufacturing growth of OECD member countries. The individual country analysis was conducted using the VAR causality framework and cointegration analysis. The result reveals that most countries’ financial development stance improves the manufacturing productivity of many OECD member countries. The study found that using homogeneous analysis, long-run causality is associated between financial development and total factor productivity. However, differences in impact level between countries suggest a more complex picture that is apparent from cross-sectional evidence. The studies by Garretsen et al. (Citation2004) examined the impact of financial development and legal institutions on economic growth in a group of countries with common laws and civil law. The study employed panel data regression and found that societal norms are important factors that explain financial development measured by stock market capitalization while it does not impact when measured by the ratio of credit to the private sector to GDP. The study also found that including formal institutions enhance economic activities.

Masten et al. (Citation2008) examined the non-linear growth effect of financial development on economic growth and also examined if financial integration enhances the level of impact. The study focused on European countries and employed the generalized methods of moments estimation technique. The result from the study shows that the developing economies in Europe gained more from financial development and in overall, gains from regional financial integration is enhanced at higher levels of financial development. The study also noted that monetary integration within Europe is a major determinant of financial integration. Also, Friedrich et al. (Citation2013) examined the reasons why financial integration has varying impacts on economic growth in emerging European countries. Using the panel OLS and the quantile regression, the study found that financial integration has a larger and significant impact on the economic growth of emerging countries that are more politically integrated than the developed economies.

Xu and Tan (Citation2020) examined the impact of financial development and the industrial structure on natural resource utilization in China. The study employed the robust generalized least squares and results from the study revealed that the industrial structure of the economy has negative impact on the efficiency of natural resources utilization while financial development has positive impact on the natural resource use.

3. Research methods and procedure

This research design of the study used is quantitative style of investigation by analysing secondary data retrieved from world bank database. A model is developed in achieving the objective while the model is estimated using fixed effect panel regression and quantile regression estimation technique. This section specifies the model to be employed in analysing the objectives stated earlier in section one. Following the objectives that are to examine the impact of financial development on the industrial output of ECOWAS member countries, examine the effect of regional financial integration on the industrial output of ECOWAS member countries, and examine the extent of the impact of financial development and regional financial integration on the industrial output of ECOWAS member countries considering the countries’ institutional frameworks. To achieve this, the relevant models to be estimated in this study are specified.

In modeling, the study begins by developing the measures of regional financial integration. The financial markets can be said to be integrated when prices are unique. For this to occur, the assets that have common cash flows and risk profiles must have a common price as well as returns. Thus, we seldom say that the degree of differences between the returns or prices of assets that are unique explains the extent of financial segmentation within the region and the extent to which their convergence implies regional financial integration (Ekpo & Chukwu, Citation2017). From empirical literature (Adam et al., Citation2002; Baele et al., Citation2004; Bekaert et al., Citation2005; Vo, Citation2009), four measures have been developed as indicators of financial integration; these are the indicators based on intertemporal decisions among households and firms, measures based on institutional differences in financial regulations, measures of credit and the bond market integration and the measures based on stock market integration.

Feldstein and Horioka (Citation1980) suggest that the first measure will not provide evidence of regional financial integration as there exists no correlation between domestic savings and corporate savings. The first measure suggests that integration arises due to the relationship between the household’s savings and investment. The measure of regional financial integration based on institutional differences (both the dejure and the defacto measures) contains binary responses, which only explain either the presence of severe capital controls or not (Beck et al., Citation2013). Empirical evidence from East Asia and Africa (Ajayi & Ndikumana, Citation2014) suggest that these measures wrongly capture the degree of regional financial integration as there are capital control measures, but the increasing rate of illicit financial flows debunks any of such measures. More comfortably, measures that rely on the risk, price and returns of economy-wide assets are commonly used as measure of regional financial integration, such as the interest rate differentials and the extent of differences in regional stock markets (Ekpo & Chukwu, Citation2017; Adam et al., Citation2002; Donadelli & Gufler, Citation2021). The unavailability and limited development of stock markets in the ECOWAS region limit the ability to use the differences in the stock market as a measure of regional financial integration. Also, the interest rate differential measure is a more appropriate one to use as this helps to capture the overall risk and expected returns of economy-wide assets within the region.

In applying the interest rate differentials measure, we employ a variant of the capital asset pricing model and follow the studies by Ekpo and Chukwu (Citation2017); De Nicolo and Juvenal (Citation2014) state that for N countries in the region, with an expected return on investment in country as

, the expected returns for a partially integrated country is given as

where is the returns on investment in the country i,

is the perceived likelihood that an economy is integrated which has a boundary

,

is the return on a value-weighted regional portfolio. When

converges towards one, then the convergence in expected excess returns can be said to be an implication of increased regional integration. Thus, the degree of regional financial integration can be measured as the gap between the market excess return of a country from a measure of central tendency of the distribution of market excess returns of all the countries in the region (Ekpo & Chuku, Citation2017). Thus, we can specify that

EquationEquation (2)(2)

(2) implies that regional financial integration is measured as the quadratic difference between a country’s interest rate spread and an equally weighted average spread for countries in the region.

is the interest rate spread (lending rate—deposit rate) of country i at time t while

is the average spread for countries in the region. Interest rate is preferred as the bank’s interest rate mirrors the macro- and the microeconomic risks and opportunities in an economy and can thus be treated as the price of risk. The lower the quadratic value, the greater or more deepened regional financial integration is while the higher it is, the more segmented the market is.

There are six measures of institutional quality as developed by Kaufmann et al. (Citation2010); these are control of corruption; government effectiveness; political stability; voice and accountability; regulatory quality and rule of law. To capture the level of institutional quality, we employ the principal component analysis to generate the institutional quality index. That is;

EquationEquation (3)(3)

(3) can be further specified in the master equation for the principal component analysis (Esbensen, Citation2009) as:

where T is the score matrix, E is the residual matrix, P is the loading matrix, are the column of T,

is the column of P and a = 1, …, A is the principal component index from each of the variables instone, insttwo, instthree, instfour, rq and cc. The particular principal component that is large and relatively greater than one is used for the matrix rotation and development of the institutional quality index (insq). The studies of Shehnaz et al. (Citation2018) provide empirical evidence on the relevance of controlling for corruption as an important institutional measure for enhanced industrial sector performance while the studies by Suzigan et al. (Citation2020) show that regulation is important in determining the extent of industrialisation in Brazil. With Brazil as an emerging economy and likened to countries in the ECOWAS region, this study especially analyses the impact of control of corruption and regulatory quality on industrial sector performance. That is, aside from the institutional quality index, the study also x-trays how control of corruption and regulatory quality will influence industrial sector performance.

Having calculated the regional financial integration measure (rinteg) and estimates the institutional quality index (insq), we can then specify our model that captures our objectives. We start by specifying the impact of financial development and regional financial integration on industrial output performance. Industrial output performance is measured by the industrial value-added while we acknowledge other measures of financial development, two main measures of financial development are used here; the first is financial development that is measured by the ratio of broad money supply to output (fdm) and the ratio of credit to the private sector to output (fdp; Arestis & Demetriades, Citation1997; De Gregorio & Guidotti, Citation1995). The former measures the public angle of financial development while the second measures the aspect of private financial development. Following the studies by Ibrahim and Vo (Citation2020) with modifications, we specify that

where X are list of control variables which are labour force, capital formation, inflation rate and exchange rate. Labour and capital formation are the fundamental inputs employed in the industrial sector while the inflation rate measures the changes in domestic prices of industrial products while the exchange rate measures the international prices of industrial products. Thus, Equationequation (5)(5)

(5) is further written as:

EquationEquation (6)(6)

(6) can be written in econometrics form as:

We further extend Equationequation (7)(7)

(7) model by examining how control of corruption and regulatory framework will have an impact on industrial sector performance; this is stated as:

We extend the model of Equationequation (9)(9)

(9) by re-estimating the model however with little modification by introducing institutional quality index, removing control of corruption and regulatory framework; then we examine how this will have an impact on industrial sector performance. The model is specified as:

To examine the impact of financial development and regional financial integration on the industrial output of ECOWAS member countries in the presence of strong institutions, we modify Equationequation (9)(9)

(9) by interacting institutional quality with the measures of financial development and regional financial integration; this is stated as:

The apriori expectations of the coefficients in Equationequations 7(7)

(7) , Equation8

(8)

(8) , Equation9

(9)

(9) and Equation10

(10)

(10) for counterpart explanatory variables remain unchanged and thus, the variable definition, measurement, apriori expectation, and source of data are presented in .

Table 1. Variable definition and measurement

In order to estimate Equationequations 7(7)

(7) , Equation8

(8)

(8) , Equation9

(9)

(9) and Equation10

(10)

(10) , there are econometrics tests that must be conducted. Firstly, a descriptive statistic is conducted on each variable employed as described in ; this helps to explain the nature and pattern of variables employed. Subsequently, the pairwise correlation matrix will be estimated in order to determine the degree of relationship associated with the explanatory variables employed in the regression result. The purpose of conducting the correlation is to ensure that there is no presence of strong or perfect multicollinearity associated with the regression result.

Before estimating the regression result, the Hausman (Citation1978) test for an efficient estimator between the random effects and the fixed effects is estimated. The Hausman test compares an estimator say which is the fixed effect model that is known to be consistent with an estimator

which is the random effect that is efficient under the assumption being tested. The null hypothesis is that

indeed is an efficient (and consistent) estimator of the true parameters.

After establishing if the fixed effect model is a fully efficient specification of the individual effect or it’s the random effect that follows a normal distribution, we will further examine the possibility of cross-sectional dependence associated with the regression model. There are vast economic literature (Baltagi, Citation2005; M. H. Pesaran, Citation2004; Robertson & Symons, Citation2000) that suggests that panel data series exhibits some level of cross-sectional dependence in the errors. This is because of the greater presence of common shocks. Increases in economic cooperation and financial integration of entities within the region suggests the existence of strong interdependence among cross-sectional units and this implies the existence of cross-sectional dependence (De Hoyos & Sarafidis, Citation2006). With the presence of cross-sectional dependence, the estimates are likely to become inefficient depending on the degree of correlations across the cross-sections. The study after testing for cross-sectional dependence will employ the standard fixed effect estimation technique and estimate it using the robust standard errors by Driscoll and Kraay (Citation1998). They developed a standard error that makes the fixed effect estimator efficient even if the cross-sectional dependence is caused by the presence of unobserved common factors. To do this, we shall be employing the xtscc command as developed by Hoechle (Citation2006). To perform the cross-sectional dependence test, the study employs the M. H. Pesaran (Citation2004) method which has a mean of exactly zero for fixed values of time and number of cross-sections, making it valid despite the presence of small sample bias. The study corroborates the M. H. Pesaran (Citation2004) cross-sectional dependence test with the Frees (Citation2004) method which supplies the Q distribution, a weighted sum of two distributed random variables that depends on the size of T.

The cross-sectional dependence test validates if there is cross-sectional dependence across various cross-sections. With this, the study will further employ the M.H. Pesaran (Citation2003) second-generation panel unit root test which is applicable when there is no evidence of heterogeneity in the cross-sections and thus, allows for cross-sectional correlations (Hurlin et al., Citation2007). After this, the study employs the Kao (Citation1999) residual-based test for cointegration in order to examine the possibility of having a long-run relationship existing among economic fundamentals. The Kao approach assumes that the nuisance parameters are the same for all panel units (homogeneous short-run dynamics).

Subsequent to the tests conducted as aforementioned, the study will employ the fixed effect regression estimation technique with Driscoll and Kraay efficient standard errors to estimate Equationequations 7(7)

(7) , Equation8

(8)

(8) , Equation9

(9)

(9) , and Equation10

(10)

(10) . The fixed effect controls for omitted variable bias and is based on the assumption that the individual-specific effects are correlated with the independent variables. For robustness check and to examine how financial development and regional financial integration can affect ECOWAS member countries that produce low industrial output, we shall be employing the quantile regression by estimating the impact of the explanatory variables on the industrial output level of the first quantile distribution (q.25), second quantile (q.50) and the third quantile distribution (q.75). The quantile regression will help us to compare the magnitude of the impact of financial development, regional financial integration, and institutional quality on the industrial output of economies within the region that has the low industrial output from those with a high level of industrial output. The short-run dynamic fixed effect regression is employed for robustness check and also corroborates the cointegration test performed using the Kao residual cointegration method.

4. Data presentation and analysis of result

This section presents the data employed in achieving the research objective stated in the introductory section of the paper. To begin with, the section describes the statistical features of the variables employed for the 15 ECOWAS member countries; this is then followed by a correlation matrix to understand the degree of relationship among the explanatory variables employed. The next section conducts the relevant pre-estimation tests that are needed such as the cross-sectional dependence test, the Hausman test, panel unit root test and the cointegration test. Subsequently, the regression result is then presented and the results discussed.

5. Descriptive analysis of variables

From , we can see that the panel series are unbalanced due to the unavailability of all data points for the whole periods of the member countries. Control of corruption on average was −0.61 for the 15 countries and this is rated low as it ranges from −2.5 to 2.5, this implies that the region has not fared well with respect to controlling for corruption. The performance for control of corruption is not significantly different from that of regulatory quality as it maintained an average of −0.62, although some economies faired better in terms of controlling for corruption than regulatory quality at some point as the maximum value for the former was 1.14 and 0.13 for the latter. The extent of integration within the region on average, measured by the quadratic difference between the interest rate spread and the region’s average was 40.12, although it was once low as 0.06 was recorded as the minimum value, this was also high as 234.59 was recorded. The result also shows that on average, 8.41 billion US dollars was the industry value added to GDP while some economies within the region contributed as much as 111 billion US dollars in a single year.

Table 2. Descriptive statistics of variables employed

The extent of the availability of broad money in ratio to the output of the region was on average 27.35%, thus the financial development measured by the degree of broad money to GDP is a little higher than a quarter of the region’s output. Also, the ratio of credit made available for the private sector in relation to the output maintained an average of 14.86% and this was as high as 65.74% for one period. An average of 6.66 million people makes up the labour force of each country within the region yearly and one of the economies for a single year had a maximum of 63.2 million labour force. The inflation rate averaged 7.25% for each member country while the level of the exchange rate was highly volatile for each member country.

6. Principal component analysis for institutional quality index

The next thing to do is to use the principal component analysis in deriving the institutional quality index from the various measures of the level of institutional quality as retrieved from the world governance indicators; these variables are control of corruption, government effectiveness, political stability and absence of violence, regulatory quality, rule of law, voice and accountability. The eigenvalue reported from of the principal component analysis reveals that component 1 is the acceptable eigenvalue that is adequate for the construction of the index as the value 4.734 is greater than 1. The constructed index is used as the measure of institutional quality.

Table 3. Principal component eigen values & proportion for institutional quality index

7. Pairwise correlation of variables

We further employed the Pearson correlation matrix to understand the degree of the relationship existing among the explanatory variables. The result as presented in Table reveals that there is no perfect multicollinearity that is associated with the regression results as the pairwise correlation result of perfect relationship (−1, +1) does not exist in the model; the only perfect relationship is between insq and cc and as expected, the cc is a component of the measure of the institutional quality index (insq) as computed using the principal component analysis.

Table 4. Correlation matrix of variables employed

8. Hausman test result of fixed effect estimation

This section presents the result of the Hausman test in order to detect any possible violation of using random-effects modeling assumption as against the fixed effects.

The Hausman H has a distributed chi-Square statistic which tests the null hypothesis that the random effect model is appropriate as against the alternative hypothesis that the fixed effect is appropriate and so, the coefficients obtained under the fixed effect is efficient. From Table , the result reveals that the chi-square statistics for the four models to be estimated are all statistically significant at atleast 5% level of significance with models one, two and three significant at 1% while the fourth model is significant at 5%. Thus, we reject the null hypothesis that the difference in coefficients are not systematic and the individual -level effect are adequately modeled by a random-effect model. Thus, the fixed effect estimation technique is preferred over the random effect method.

Table 5. Hausman test result for models

9. Cross-sectional dependence test

With increasing financial integration of countries and other financial entities, we must examine the possibility of having a substantial cross-sectional dependence in the errors and this is because of the common shocks that become part of the error term. With this, the cross-sectional dependence test conducted using the M. H. Pesaran (Citation2004) and the Frees (Citation2004) as discussed in the previous section is presented in Table .

Table 6. Cross-sectional dependence test

The result from Table tests the null hypothesis that there is cross-sectional independence in the errors as against the alternative hypothesis that there is cross-sectional dependence associated with the error terms. Using the M. H. Pesaran (Citation2004) statistics for the four models, the result shows that for model one, three and four are statistically dependent at 1%, 5% and 5% level of significance respectively and thus, we can reject the null hypothesis of cross-sectional independence and accept the alternative and conclude that the cross-sectional dependence in the errors is not altered. For the second model, the result of the M. H. Pesaran (Citation2004) statistics does support that there is cross-sectional independence associated with the error term. However, this will be further validated using the Frees (Citation2004) statistics that provide for time series within the panel that is less than or equal to 30. Using the Frees (Citation2004) statistic, the result shows that for the first model, the critical value from the Frees’ Q is less than the statistic both at 1%, 5% and 10% level of significance. Thus, the rejection of the null hypothesis using the M. H. Pesaran (Citation2004) is corroborated with the Frees (Citation2004) approach and the rejection of the presence of no cross-sectional dependence is rejected. For the second model, the Frees statistics is greater than the critical value of the Q distribution both at 1%, 5% and 10% level of significance. We can conclude that there is cross-sectional dependence associated with the errors in the second model. For the third and fourth models, the result of the Frees’ method corroborates with the conclusion of Pesaran’s method and we can therefore conclude that there is cross-sectional dependence associated with the error terms.

10. Panel unit root test result

With the presence of cross-sectional dependence associated with the error terms for the four models, it becomes paramount that we estimate the panel unit root test using those methods that allow for cross-sectional dependence and the factor structure which is the class of the second-generation test. The approach adopted is thus the M.H. Pesaran (Citation2003) panel unit root test. Given that the second generation tests are still under development, the M.H. Pesaran (Citation2003) that can be easily estimated with STATA. The null hypothesis of series possessing unit root in the presence of cross-sectional dependence of the error terms is tested as against the alternative hypothesis of stationarity associated with the series.

The M.H. Pesaran (Citation2003) Z[t-bar] statistics at level for all the variables employed are not statistically significant even at 10% level of significance except for inflation rate, exchange rate, and regulatory quality. The conclusion is that inflation rate, exchange rate, and regulatory quality are stationary at level as their Z[t-bar] statistics is statistically significant at 1%, 5%, and 10% respectively. We further test for the possibility of having the other non-stationary variables at level becoming stationary at first difference. Employing the M.H. Pesaran (Citation2003) method, the result shows that all the other variables (industrial value-added, financial development as measured by the extent of broad money, financial development measured by the extent of credit to the private sector, regional financial integration, capital employed and regulatory quality) are stationary at first difference as their probability values are less than 1% while the institutional quality index is also stationary at first difference but statistically significant at 5%. The result from Table thus reaffirms that in the presence of cross-sectional dependence associated with the error terms, the series employed possess stationary properties.

Table 7. Panel unit root test by Pesaran

11. Kao cointegration test result

The presence of cross-sectional dependence and evidence of stationarity at both level and first difference necessitates the test for the presence of a long-run cointegrating relationship associated with the models. The study estimates a dynamic fixed effect panel regression and the evidence of stability and convergence in the error correction term implies the presence of cointegration in the regression model. However, for robustness check in ensuring that cointegration exists, the study performs the Kao (Citation1999) residual-based test for cointegration and the result as reported in Table shows that the modified Dickey-Fuller t statistics, Dickey-Fuller t statistics and the Augmented Dickey-Fuller t statistics are statistically significant at 5%. This because their probability values are all less than 5% and we can thus reject the null hypothesis of no cointegration associated with the regression result and accept the alternative and we conclude that cointegration exists in the models estimated.

Table 8. Kao test for cointegration

12. Regression result

The regression result from Table shows the impact of financial development measured by the ratio of broad money to GDP on industrial sector development. It also shows the impact of financial development measured by the ratio of credit to the private sector to GDP on industrial output. The result further examines the impact of regional financial integration on the industrial sector performance of the ECOWAS region. The result also demonstrates how institutional quality affects industrial performance with special emphasis on the extent of controlling for corruption and how strong the regulatory environment is. Further empirical investigation tried to see how effective financial development with a strong institution will impact on industrial sector performance of member countries in ECOWAS.

Table 9. Long-run fixed effect panel regression result with Driscoll and Kraay efficient standard errors and quantile regression

The first model considers the impact of financial development and regional financial integration on industrial sector performance in the ECOWAS region. From the result, there is a negative but statistically insignificant impact of financial development proxied by the ratio of broad money supply to GDP on industrial output. The implication of this is that the level of broad money supply within the economy does not have a significant impact on industrial output. However, the credit to the private sector has a positive but insignificant impact. The result also shows that increases in regional financial integration do not improve the industrial sector performance within the region. The implication of this is that the state of ECOWAS member countries’ financial integration does not improve the level of industrial output.

Considering models two, three, and four, the sign and level of significance of the impact of financial development as measured by broad money and credit to the private sector on industrial output remains the same with model one as discussed above; also, regional financial integration alone does not strengthen the industrial output. Model two considers the implication of strengthening the level of institutions on the industrial performance within the region. The level of institutional quality is measured by control of corruption and regulatory quality. The result reveals that the level of corruption within the region has not enhanced the industrial output as there is a negative and insignificant impact of the extent of controlling for corruption on industrial output. However, the result shows that the regulatory quality framework within the region has a positive and significant impact on industrial sector performance. Model three is a bit different from model two as it considers the impact of the overall level of institution on industrial sector output; this result shows that ECOWAS member countries generally have a weak institutional framework and this does not have a significant impact on industrial sector performance. The empirical evidence of this assertion is revealed in model three as the coefficient of the institutional quality index is positive but statistically insignificant.

We further modeled our study to examine the interaction between the measures of financial development and institutional quality. We examined the interactive effect of institutional quality and financial development measured by broad money on industrial output; the interactive effect of credit to private sector and institutional quality on industrial sector performance and we then examined whether financial regionalization will have a stronger effect on industrial sector performance with high levels of institutional quality. From model four as presented in Table , the result shows that financial development as measured by the ratio of broad money to GDP does not have a stronger effect with member countries with high levels of institutional quality. Also, the result shows that countries that have better institutional quality frameworks cannot influence industrial sector performance within the region despite greater regional financial integration; this is evident as the impact in model four of the interactive effect between institutional quality and regional financial integration is positive and statistically significant.

We continue to understand the nature and extent of the impact of our variables by employing the quantile regression to examine if the findings aforementioned above are different for countries with different levels of industrial output. Comparing the coefficient of credit to the private sector in the lower quantile and the upper quantile, the result shows that they are both negative, statistically significant and the same; this implies that credit to the private sector alone both for countries with low industrial output and countries with high industrial output does not improve the level of industrial performance. The result shows that the coefficient of the interaction between credit to the private sector is positive and statistically significant at 1% and this is higher for the lower quantile (0.043) than the upper quantile (0.016). The implication of this result shows that for countries that have low industrial output, increases in financial development (measured by the ratio of credit to the private sector to GDP) with a stronger institutional quality framework will increase the level of industrial output compared to countries with a higher level of industrial output. Also, the interaction between the ratio of broad money to GDP and institutional quality has the same declining effect for countries with low industrial output to countries with high industrial output; only that this effect is negative. The implication of this is that the negative impact of increasing the ratio of broad money to GDP on industrial output is worse for member countries with low industrial output compared to countries with high industrial output. Model four shows that regional financial integration and the presence of strong institutions enhance industrial sector performance. The result also shows that regional financial integration with stronger institutional quality has a higher positive impact on industrial output for countries with lower industrial productivity than those with higher industrial relevance. The result mirrors the findings of Boyd and Smith (Citation1996) concerning growth which predicts that international financial integration will only have a stronger effect on the growth of countries with well-developed financial system and high institutional quality than those with low levels.

Other control variables to a considerable extent conform to apriori expectations. The result shows that labour force within the region has a positive and significant impact on industrial output for all seven models. Also, the result reveals that capital formation within the region has a positive and significant impact on industrial output for all the seven models. The exchange rate has a positive and significant impact on industrial output for the fixed effect regression implying that the depreciation or devaluation of the currency promotes industrial sector performance. However, for countries with high industrial output, it is the appreciation of the currency that enhances their industrial sector performance. Also, the result reveals that stable price level promotes industrial performance as higher prices swifts away increases in the value of our industrial product.

The coefficient of determination for the four models shows that a considerable larger proportion of variation in industrial output is explained by the explanatory variables put together; 67.9% of variations in industrial output is explained by the explanatory variables in model one, it was 70% in model two but declined to 68.7% and 69.9% in model three and four respectively. For the Pseudo R-squared in the quantile regression, considerable values of 0.77, 079 and 0.81 for the first quantile, second quantile, and third quantile are adequate. For robustness check, we examined the equivalence of the quantile estimates across quantiles (q.25, q.50, and q.75). The result shows the f-statistics of the coefficient of the interaction between financial development and institutional quality is significant and this implies that we reject equality of the estimated coefficients for the three quantiles and we conclude that the coefficients are statistically significant.

The error correction terms in Table conforms to the apriori expectation. The error correction terms are negative, statistically significant and between zero and one non-inclusive; the implication of this is that convergence to the long-run equilibrium is achieved in the event of any possible disequilibrium in the short run, this shows that the equations are cointegrated in the long run. The short-run coefficients of financial development as measured by the ratio of credit to the private sector to GDP and the ratio of broad money supply to GDP in all the three models are negative and this implies that in the short run, financial development does not stimulate increase in industrial sector performance. However, the more financially the region is integrated, the higher their industrial sector performance. Also, institutional quality does not improve the industrial sector performance of ECOWAS member countries.

Table 10. Short run dynamic fixed effect regression result

13. Conclusion and policy recommendation

This study examines if financial development in the presence of an enhanced institutional framework significantly increases industrial sector performance. The study further examines if greater regional financial cooperation and well developed institutional framework can enhance the industrial sector performance. Relevant preliminary statistics reveal that the credit to the private sector provided annually on average within each country’s financial system is not adequate to stimulate industrial activities; although the volume of money in circulation with respect to the output it can purchase is relatively higher as expected than the part of the money that is provided to the private sector in form of credit. More importantly, the region’s extent of financial integration is weak when measured with the interest rate spread. The study also found out that controlling for corruption and regulatory quality as a measure of the institutional framework within the region has performed below average within the periods of study; this is evident as their average performance is not up to the benchmark average.

The further conclusion drawn from this study reveals that increases in the ratio of broad money to output do not significantly enhance industrial sector performance among ECOWAS member countries. Although the increases in credit to the private sector alone enhances industrial sector performance, this is not statistically significant. The study also concludes that increases in regional financial integration improve the industrial sector performance within the region; the more ECOWAS member countries are financially integrated, the greater the level of industrial output. Controlling measures put in place to fight corruption within the region have not enhanced the industrial sector performance. Enhancing the regulatory quality framework within the region improves industrial sector performance. Enhanced and strict adherence to policy regulations improves industrial sector performance within the region.

The study concludes that enhancing the greater supply of broad money (a measure of financial development) does not have a stronger effect on industrial output despite member countries with high levels of institutional quality; this implies that irrespective of the state of institutional quality within the region, increases in broad money supply is not effective in stimulating industrial output. The adverse impact of increasing broad money on industrial output is worse for member countries experiencing low industrial output performance compared to countries with high industrial output.

Regional financial integration with stronger institutional quality has a higher positive impact on ECOWAS member countries that has low industrial productivity than those with higher industrial output. Thus, regional financial integration and institutional quality is important and a strong enhancing factor for member countries experiencing low industrial sector productivity; it can increase the industrial sector activity of those countries with slow growth rate.

Credit to the private sector alone both for countries with low industrial output and countries with high industrial output does not improve the level of industrial performance. However, for countries that have low industrial output with a stronger institutional quality framework, increases in credit to the private sector will increase the level of industrial output compared to countries with a higher level of industrial output. Increasing the level of money in circulation alone does not improve industrial sector performance; the quantum channeled as a credit to the private sector does. The flow of funds as a credit to the private sector is a major factor for regional financial integration.

Other conclusions from the study infer that labour force and capital formation are significant and baseline factors that also improve the industrial sector performance. The exchange rate has a positive and significant impact on industrial output and thus, the depreciation or devaluation of the currency promotes industrial sector performance. However, for countries with high industrial output, it is the appreciation of the currency that enhances their industrial sector performance.

The policy implication of this study is that greater regional financial integration and a robust institutional framework can engender industrialisation among ECOWAS regional countries. ECOWAS as a regional body must seek to develop policies that will improve the institutional framework of regions, design collaborative programmes that will enhance shared knowledge across the financial institutions in the region. For ECOWAS as a region to achieve greater regional financial integration, an improved institutional framework must be set in place and there must be an enhanced flow of credit to the private sector. The monetary authority of each regional country must as a matter of urgency develop policy measures that can individually spur credit to the private sector, this is important to increase industrial output. For ECOWAS as a region to benefit from continental integration such as the African Continental Free Trade Area (AfCFTA) agreement and compete on a global scale, the sub-region must strengthen the industrial policies and seek to improve their industrial performance for them to compete also on a global scale. This study did not consider the impact of financial integration and financial development on other cirtical sectors of the economy such as the agricultural sector. Future research should consider the impact of regional financial integration and financial development on agricultural sector performance in ECOWAS region.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Acknowledgement

This research acknowledges the M.Sc. programme joint collaboration effort by Agricultural Research and Innovation Fellowship for Africa (ARIFA), coordinated by the Forum for Agricultural Research in Africa-FARA in partnership with the Tertiary Education Trust Fund (TETFund) and the Universidade Federal de Viçosa (UFV) in Brazil.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Onyebuchi Iwegbu

Onyebuchi Iwegbu is a Lecturer of the Department of Economics, University of Lagos. He is currently an Assistant Research Fellow of the Centre for Economic Policy Analysis and Research (CEPAR), University of Lagos. His continuous development in research has attracted several research grants and consultancy services to his profile. Onyebuchi has research interest in Development Macroeconomics and Development Finance.Kainu Justine has 18 years of experience in the Nigerian financial industry. He is a Fellow of the Chartered Institute of Bankers of Nigeria (CIBN) and Institute of Chartered Accountants of Nigeria (ICAN). He also holds MSc. Economics, MBA and BSc. Business Administration. Kainu is currently a PhD, Economics student at Babcock University, Ogun State.Leonardo Chaves Borges Cardoso is an Associate Professor in the Department of Agricultural Economics at Universidade Federal de Viçosa, Brazil. His research Interests include Energy Economics, Inequality, Crime, and other topics in Development Economics. One of his recent studies examines biofuels policies and fuel demand elasticities in Brazil.

Kainu Justine

Onyebuchi Iwegbu is a Lecturer of the Department of Economics, University of Lagos. He is currently an Assistant Research Fellow of the Centre for Economic Policy Analysis and Research (CEPAR), University of Lagos. His continuous development in research has attracted several research grants and consultancy services to his profile. Onyebuchi has research interest in Development Macroeconomics and Development Finance.Kainu Justine has 18 years of experience in the Nigerian financial industry. He is a Fellow of the Chartered Institute of Bankers of Nigeria (CIBN) and Institute of Chartered Accountants of Nigeria (ICAN). He also holds MSc. Economics, MBA and BSc. Business Administration. Kainu is currently a PhD, Economics student at Babcock University, Ogun State.Leonardo Chaves Borges Cardoso is an Associate Professor in the Department of Agricultural Economics at Universidade Federal de Viçosa, Brazil. His research Interests include Energy Economics, Inequality, Crime, and other topics in Development Economics. One of his recent studies examines biofuels policies and fuel demand elasticities in Brazil.

References

- Adam, K., Jappelli, T., Menichini, A., Padula, M., & Pagano, M. (2002). Analyse, compare, and apply alternative indicators and monitoring methodologies to measure the evolution of capital market integration in the European Union. University of Salerno, Italy.

- Adedokun, A. S., Yameogo, C. E. W., & Osode, O. E. (2020). International financial integration, macroeconomic performance and poverty reduction in WAMZ countries. Journal of Economic Studies, 17(1), 1–25 https://nauecojournals.com/index.php/stage/pdfreader/110/.

- Ahmed, A. D. (2016). Integration of financial markets, financial development and growth: Is Africa different? Journal of International Financial Markets, Institutions and Money, 42 1 , 43–59. 2016. http://dx.doi.org/10.1016/j.intfin.2016.01.003

- Ajayi, S. I., & Ndikumana, L. (2014). Capital flight from Africa: Causes, effects, and policy issues. Oxford University Press.

- Arestis, P., & Demetriades, P. (1997). Financial development and economic growth: Assessing the evidence. The Economic Journal, 107(442), 783–799. https://doi.org/10.1111/j.1468-0297.1997.tb00043.x

- Baele, L., Ferrando, A., Hordahl, P., Krylova, E., & Monnet, C. (2004). Measuring European financial integration. Oxford Review of Economic Policy, 20(4), 509–530. https://doi.org/10.1093/oxrep/grh030

- Baltagi, B. H. (2005). Econometric analysis of panel data (3rd ed.). Wiley.

- Beck, T., Claessens, S., & Schmukler, S. (2013 In G. Caprio, T. Beck., S. Claessens & S.L. Schmukler (eds.)). . The Evidence and Impact of Financial Globalization (Elsevier), (pp. 1–12) doi:10.1016/C2011-0-08962-7.

- Bekaert, G., Harvey, C., & Ng, A. (2005). Market integration and contagion. The Journal of Business, 78(1), 39–69. https://doi.org/10.1086/426519

- Boyd, J.H. & Smith, B.D. (1996). The co-evolution of the real and financial sectors in the growth process. World Bank Economic Review, 10(2), 371– 396

- De Gregorio, J., & Guidotti, P. E. (1995). Financial development and economic growth. World Development, 23(3), 433–448 doi:10.1016/0305-750X(94)00132-I.

- De Hoyos, R., & Sarafidis, V. (2006). Testing for cross-sectional dependence in panel-data models. The Stata Journal, 6(4), 482–496. https://doi.org/10.1177/1536867X0600600403

- De Nicolo, G., & Juvenal, L. (2014). Financial integration, globalization, and real activity. Journal of Financial Stability, 10 (C) , 65–75. https://doi.org/10.1016/j.jfs.2013.04.004

- Donadelli, M., & Gufler, I. (2021). Consumption smoothing, risk sharing and financial integration. The World Economy, 44(1), 143–187. https://doi.org/10.1111/twec.12996

- Driscoll, J., & Kraay, A. C. (1998). Consistent covariance matrix estimation with spatially dependent data. Review of Economics and Statistics, 80(4), 549–560. https://doi.org/10.1162/003465398557825

- ECOWAS. (2016). Fundamental principles and achievement of ECOWAS. from https://www.ecowas.int/about-ecowas/fundamental-principles/

- Edison, H. J., Levine, R., Ricci, L., & Slok, T. (2002). International financial integration and economic growth. Journal of International Money and Finance, 21(6), 749–776. https://doi.org/10.1016/S0261-5606(02)00021-9

- Ehigiamusoe, K. U., & Lean, H. H. (2018). . Economics Discussion Paper No (Kiel Institute for the World Economy). 2018-51. http://www.economics-ejournal.org/economics/discussionpapers/2018-51

- Ekpo, A., & Chuku, C. (2017). . African Development Bank Working Paper, No 291 (African Development Bank Group).

- Esbensen, K. H. (2009 In S. Brown, R. Taulor, & R. Walczak (eds.), Comprehensive Chemometrics:). . Chemistry, Molecular Sciences and Chemical Engineering, 211–226. https://doi.org/10.1016/B978-044452701-1.00043-0

- Feldstein, M., & Horioka, C. (1980). Domestic savings and international capital flows. Journal of Banking & Finance, 90 (358) , 314–329 doi:10.2307/2231790.

- Fergusson, L. (2006). Institutions for financial development: What are they and where do they come from? Journal of Economic Surveys, 20(1), 27–43. https://doi.org/10.1111/j.0950-0804.2006.00275.x

- Frees, E. W. (2004). Longitudinal and panel data: Analysis and applications in the social sciences. Cambridge University Press.

- Friedrich, C., Schnabel, I., & Zettelmeyer, J. (2013). Financial integration and growth — Why is emerging Europe different? Journal of International Economics, 89(2), 522–538. https://doi.org/10.1016/j.jinteco.2012.07.003

- Garretsen, H., Lensink, R., & Sterken, E. (2004). Growth, financial development, societal norms and legal institutions. Journal of International Financial Markets, Institutions and Money, 14(2), 0–183. https://doi.org/10.1016/j.intfin.2003.06.002

- Guiso, L., Sapienza, P., & Zingales, L. (2004). Does local financial development matter? The Quarterly Journal of Economics, 119(3), 929–969. https://doi.org/10.1162/0033553041502162

- Hausman, J. A. (1978). Specification tests in econometrics. Econometrica, 46(6), 1251–1271. https://doi.org/10.2307/1913827

- Hoechle, D. (2006). . In The Stata Journal 7 (3) 281–312 . .

- Huang, H., Fang, W. S., & Miller, S. M. (2014). Does financial development volatility affect industrial growth volatility? International Review of Economics and Finance, 29 (1) , 307–320. https://doi.org/10.1016/j.iref.2013.06.006

- Hurlin, C., Mignon, V., Sykes, R. N., Hurlin, C., Owen, C., & Harrison, N. K. (2007). Second generation panel unit root tests. Copd, 4(4), 305–312. halshs-00159842. https://doi.org/10.1080/15412550701595716

- Ibrahim, M. (2020). Effects of trade and financial integration on structural transformation in Africa: New evidence from a sample splitting approach. Physica A: Statistical Mechanics and Its Applications, 556(15), 124841. https://doi.org/10.1016/j.physa.2020.124841

- Ibrahim, M., & Alagidede, P. (2018). Effect of financial development on economic growth in Sub Saharan Africa. Journal of Policy Modeling, 40(6), 1104–1125. https://doi.org/10.1016/j.jpolmod.2018.08.001

- Ibrahim, M., & Vo, X. V. (2020). Effect of economic integration on sectorial value added in sub–saharan Africa: Does financial development matter? The Journal of International Trade & Economic Development, 29(8), 934–951. https://doi.org/10.1080/09638199.2020.1767682

- Kao, C. (1999). Spurious regression and residual-based tests for cointegration in panel data. Journal of Econometrics, 90(1), 1–44. https://doi.org/10.1016/S0304-4076(98)00023-2

- Kaufmann, D., Kraay, A., & Mastruzzi, M. (2010). . World Bank Policy Research Working Paper No. 5430 (Word Bank Group), http://papers.ssrn.com/sol3/papers.cfm?Abstract_id=1682130.

- Lothian, J. R. (2006). Institutions, capital flows and financial integration. Journal of International Money and Finance, 25(3), 358–369. https://doi.org/10.1016/j.jimonfin.2006.01.001

- Marcelin, I., & Mathur, I. (2014). Financial development, institutions and banks. International Review of Financial Analysis, 31 (1) , 25–33. https://doi.org/10.1016/j.irfa.2013.09.003

- Masten, A. B., Coricelli, F., & Masten, I. (2008). Non-linear growth effects of financial development: Does financial integration matter? Journal of International Money and Finance, 27(2), 295–313. https://doi.org/10.1016/j.jimonfin.2007.12.009

- Mendoza, E. G., Quadrini, V., & Ríos‐Rull, J. (2009). Financial integration, financial development, and global imbalances. Journal of Political Economy, 117(3), 371–416. https://doi.org/10.1086/599706

- Neusser, K., & Kugler, M. (1998). Manufacturing growth and financial development: Evidence from OECD countries. Review of Economics and Statistics, 80(4), 638–646. https://doi.org/10.1162/003465398557726

- Patrick, H. T. (1966). Financial development and economic growth in underdeveloped countries. Economic Development and Cultural Change, 14(2), 174–189. https://doi.org/10.2307/1152568

- Pesaran, M. H. (2003). A simple panel unit root test in the presence of cross section dependence. Mimeo, University of Southern California.

- Pesaran, M. H. (2004). General diagnostic tests for cross section dependence in panels. Cambridge Working Papers in Economics No. 0435, University of Cambridge, Faculty of Economics

- Robertson, D., & Symons, J. (2000). Factor residuals in SUR regressions: Estimating panels allowing for cross sectional correlation. CEP Discussion Papers dp0473, Centre for Economic Performance, LSE.

- Schumpeter, J. (1911). Theorie der wirtschaftlichen entwicklung (The theory of economic development). Duncker & Humblot.

- Shehnaz, N. K., Kaleem, A. M., & Tayyaba, I. (2018). Impact of infrastructure and institutional quality on industrial sector of Pakistan. Pakistan Economic Review, 1(2), 70–82 https://www.ajol.info/index.php/ajer/article/view/192194/181308.

- Suzigan, W., Garcia, R., & Feitosa, P. H. A. (2020). Institutions and industrial policy in Brazil after two decades: Have we built the needed institutions? Economics of Innovation and New Technology, 29(7), 799–813. https://doi.org/10.1080/10438599.2020.1719629

- Todaro, M. P., & Smith, S. C. (2015). Economic development (12th ed.). Pearson.

- Vo, X. V. (2009). International financial integration in Asian bond markets. Research in International Business and Finance, 23(1), 90–106. https://doi.org/10.1016/j.ribaf.2008.07.001

- World Development Indicator. (2021). 2021 world development indicators. from https://databank.worldbank.org/source/world-development-indicators#

- Xu, L., & Tan, J. (2020). Financial development, industrial structure and natural resource utilization efficiency in China. Resources Policy, 66, 101642. https://doi.org/10.1016/j.resourpol.2020.101642