?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to measure the performance of actively-managed Saudi Arabia mutual funds during the COVID-19 outbreak and examines the potential impact of COVID-19 growth on the measured performance. The authors apply the Fama and French five-factor model to measure the risk-adjusted performance of a selected sample of 79 mutual funds. Mutual funds in Saudi Arabia outperformed the market with a significant positive alpha of 0.15%. The panel data regression technique identified the impact of growth in new confirmed cases and fatalities with fund-specific variables on mutual fund performance. The findings suggest that new confirmed cases had a significant and negative impact on mutual fund unadjusted returns and risk-adjusted returns. The significant positive impact of growth in COVID-19 fatalities on fund performance may have been interpreted as positive news by the market participants as the actual mortality rate was lower than previous forecast. Moreover, the study found that even individually, most mutual fund managers were not able to minimise the impact of the COVID-19 outbreak on mutual fund returns compared to the market portfolio. This study examines the potential impact of growth in COVID-19 cases as a new factor affecting mutual fund performance which helps investors to understand the behaviour of mutual fund performance during the COVID-19 crisis. It also provides evidence on how mutual fund performance reacted to the COVID-19 outbreak when compared to the overall market performance reaction. Moreover, this is the first study that applied the Fama and French five-factor model to estimate the mutual funds’ risk-adjusted performance.

Public interest statement

This paper is classified under humanities and social sciences. It focuses on a broad debate in the area of finance between the traditional finance theory which assumes that mutual fund managers may not outperform the overall market as all investors are rational in their investment decisions, and behavioural finance theory that hypothesises that groups of investors are not always rational which allows the possibility of mutual fund managers to outperform the benchmark index. Therefore, this research assesses the potential value that financial analysts and mutual fund managers add over passive investment to mutual funds’ subscribers. Furthermore, this paper investigates the impact of the COVID-19 outbreak on mutual fund performance. It shows how mutual funds have managed to alleviate the impact of the COVID-19 outbreak on funds’ returns.

1. Introduction

The performance of active mutual funds has been a debated issue in the area of finance for a long time with no decisive conclusion. Several seminal studies in this field have found that mutual funds outperformed their benchmarks (Grinblatt & Titman, Citation1993; Kosowski et al., Citation2006; Wermers, Citation2000), whereas other influencing studies have found mutual funds underperformed their benchmarks (Carhart, Citation1997; Fama & French, Citation2010; Malkiel, Citation1995). Kosowski (Citation2011) and Moskowitz (Citation2000) studied mutual fund performance during recessions. They showed evidence that mutual funds generally outperform their benchmarks during recessions, which suggests that active managers deliver returns when investors need them the most. The superior mutual fund performance during financial crises may be the reason why investors continue to subscribe to mutual funds despite the existence of some other evidence that supports the underperformance of mutual funds.

The recent global outbreak of COVID-19 has erupted economic uncertainty in international financial markets. Globally, most cities imposed stay-at-home orders to contain the spread of the virus causing severe losses to most business sectors. Brent prices plunged more than 65% during the first quarter of 2020, and the U.S. crude oil futures collapsed below zero for the first time in history (Sheppard et al., Citation2020). The World Bank Group (Citation2020) evaluated a decline of 5.2% in the overall world gross domestic production (GDP). Studies have shown that the COVID-19 outbreak has a significant impact on stock price returns (Al-Awadhi et al., Citation2020; Erdem, Citation2020; Mazur et al., Citation2021; Rahman et al., Citation2021), market volatility (Engelhardt et al., Citation2021; Gao et al., Citation2021), and market liquidity (Zaremba et al., Citation2021).

Mutual fund performance in such market critical conditions reveals fund managers’ skills in allocating assets during high discrepancies in stock prices. Pástor and Vorsatz (Citation2020) undertook the first study on the performance of equity mutual funds in the U.S. during the COVID-19 crisis. Their results indicate that most mutual funds underperformed their benchmarks. Mirza et al. (Citation2020) confirmed the underperformance of most categories of European investment funds to their benchmarks during the COVID-19 crisis, except for social funds that remarkably outperformed their benchmarks.

In the context of the Saudi securities exchange market, most studies have focused on mutual fund performance during normal market conditions (Ashraf, Citation2013; BinMahfouz & Hassan, Citation2012) with limited studies during exceptional market conditions. The spread of COVID-19 posed serious obstacles in terms of economic indicators. The government of Saudi Arabia imposed movement restrictions, such as suspension of airlines, elimination of tourism programs, and cultural and religious events. They then shifted to complete lockdowns and curfew during periods of high growth in new confirmed cases. The real GDP dropped by 4.1% (General Authority for Statistics, Citation2020), exceeding the World Bank Group (Citation2020) previous forecast of −3.8%. Accordingly, the Tadawul All Share Index (TASI)—the main index of the Saudi equity market—plunged by approximately 30% between January and April 2020. There is no evidence in the literature about the performance of mutual funds operating in Saudi Arabia during the COVID-19 crisis. The current study fills this gap and it is the first study to apply the recent Fama and French (Citation2015) five-factor model to measure the risk-adjusted performance of Saudi mutual funds. This study extends the literature on mutual fund performance and assists investors of mutual funds in their investment decisions during the COVID-19 crisis or any similar crisis in the future.

The main purpose of this study is as follows. First, estimate the Fama and French (Citation2015) five-factor model to measure the risk-adjusted performance of active equity mutual funds during the COVID-19 pandemic. The findings contribute to the ongoing debate on active investment strategy as it provides evidence of mutual fund performance during a critical investment period. The application of the Fama and French (Citation2015) five-factor model on the Saudi mutual funds adds to the capital asset pricing literacy as this is the first study that measures the risk-adjusted performance as the recent model incorporates five risks factors, namely, market risk premium, size, value, profitability, and investment. Second, identify the potential impact of both growths in COVID-19 new confirmed cases and fatalities on the unadjusted returns and risk-adjusted returns across equity mutual funds. Third, examine the ability of individual mutual fund managers to alleviate the consequences of the COVID-19 outbreak on the fund performance in comparison to the market portfolio. This objective helps investors to understand the behaviour of mutual fund managers who protect their wealth from the consequences of the COVID-19 pandemic compared to the market portfolio. Measuring the impact of factors related to the COVID-19 crisis on mutual fund performance in the Middle East’s largest market has received less attention in the literature, necessitating further investigation. Thus, testing how fund performance has been impacted by the COVID-19 crisis helps in understanding the behaviour of mutual fund performance and the importance of equity mutual funds as an alternative for building a personal investment portfolio during pandemics.

This paper is further divided into the following sections. The second section proceeds with a literature review, while the third section presents data collection and methodology. The final section provides the result discussion and conclusion.

2. Literature review

2.1. Performance measurement models and their application on Saudi funds

Previous studies have used several models to investigate mutual fund performance and its relationship with respective benchmark indices. Jensen’s (Citation1968) alpha risk-adjusted performance measure uses Sharpe (Citation1964) capital asset pricing model (CAPM) that draws the relationship between a portfolio’s expected return and systematic risk. Several key studies have claimed that CAPM suffers from theoretical and empirical flaws (Campbell & Vuolteenaho, Citation2004; Fama & French, Citation2004). These studies have indicated that the single-risk factor model fails to capture all related risk factors that affect an asset’s expected returns. Therefore, the single-risk factor model underestimates the expected returns of portfolios, particularly those focused on value and small-cap stocks.

Fama and French (Citation1993) extended the CAPM model by introducing two additional risk factors: size and value. The size factor captures the risk of the systematic outperformance of small companies on big companies, and the value factor captures the risk of the systematic outperformance of high book/market on low book/market stocks. The Fama and French (Citation1993) three-factor model reinforced the explanatory power of CAPM by 70–90%. Moreover, the Fama and French (Citation1993) three-factor model generates alphas that are closer to zero. The Carhart (Citation1997) four-factor model includes momentum as a fourth factor that captures the Jegadeesh and Titman (Citation1993) momentum anomaly. The average returns of winners minus the average returns of losers capture the market anomaly of persistence in returns for firms with high returns in the previous year and persistence in returns for firms with lower returns in the previous year.

Fama and French (Citation2015) discovered patterns in the returns of stock portfolios related to profitability and investment that cannot be explained by the three-factor model. Therefore, Fama and French (Citation2015) extended the Fama-French three-factor model by adding two new factors to capture the risk of profitability and investment. The five-factor model has up to 94% explanatory power (Fama & French, Citation2015). Fama and French (Citation2017) applied the five-factor model on the stock markets of four regions: North America, Europe, and the Asia Pacific,Footnote1 while Japan stands alone. They constructed the portfolios of the five-factor model for each region as one market. Although investment factors were redundant in Europe and Japan, asset pricing tests confirmed that the five-factor model captures the pattern in average returns better than the three-factor model. Foye (Citation2018) conducted a comprehensive test of the Fama-French five-factor model in emerging markets and found that the five-factor model outperformed the three-factor model in five markets in Eastern Europe and five markets in Latin America. Asian markets did not generate significant premiums for profitability or investment. The aforementioned literature has demonstrated the superior performance of the Fama and French (Citation2015) five-factor model compared to the previous models in estimating portfolios’ expected returns in developed and some emerging markets.

Several studies have applied the CAPM and variant extended models on domestic-oriented mutual funds in Saudi Arabia. Merdad et al. (Citation2010) measured mutual fund performance managed by HSBC between 2003 and 2010. Using the CAPM, Islamic-law compliant mutual funds underperformed TASI by an alpha of −0.32%, compared to −0.17% for conventional mutual funds throughout the sample period. BinMahfouz and Hassan (Citation2012) applied the CAPM and Fama and French (Citation1993) three-factor models to measure mutual fund performance between 2005 and 2010. Their results show that the risk-adjusted performance based on the single-factor and three-factor models did not seem to be statistically significant for Islamic mutual funds and their conventional counterparts. Ashraf (Citation2013) used the CAPM on Islamic and conventional mutual funds using a data set from 2007 to 2011 and found that the investment in Islamic funds in the Saudi market generates positive and significant risk-adjusted performance. However, the results indicate that the Jensen’s alphas of their conventional counterparts are insignificant. AlRahahleh and Bhatti (Citation2017) used the CAPM and Carhart (Citation1997) four-factor model to investigate the performance of Saudi mutual funds between 2007 and 2016. Both the models have demonstrated that mutual funds in Saudi Arabia outperformed the benchmark (TASI) recording positive and significant alphas for all of the investigated funds throughout the sample period. Alsubaiei (Citation2021) measured Saudi mutual fund performance by the single-factor, three-factor, and Carhart-four-factor models. While the single-factor and three-factor models generated statistically insignificant alphas, mutual funds have produced 0.012% positive and a significant alpha when measured by the Carhart-four-factor model.

Only a few studies have examined the performance of Saudi-based mutual funds during exceptional market conditions. Using subsample periods, AlRahahleh and Bhatti (Citation2017) measured the performance of Saudi mutual funds during different market volatility conditions (low, medium, and high-volatility). Mutual funds outperformed the main market index only when the market was recording low-volatility conditions. Mutual funds did not generate significant performance when the market was volatile (medium to high). Although Merdad et al. (Citation2010) found a negative performance of HSBC mutual funds during the full sample period, both Islamic-law compliant and conventional mutual funds generated significant positive alphas of 0.33% and 0.38%, respectively, during the global financial crisis of 2008–2010. However, no study has focused on mutual fund performance during the COVID-19 outbreak and its economic consequences, which has created uncertainty in Saudi Arabia’s economy and requires special attention. Thus, this study is the first to consider measuring mutual fund performance during a specific critical investment period. It is also the first study to transcend the issues in the former performance measurement models by applying the recently-developed Fama and French (Citation2015) five-factor model to measure Saudi mutual fund performance.

2.2. Factors that impact mutual fund performance and the COVID-19 pandemic

Several factors impact mutual fund performance in Saudi Arabia. However, most studies on the performance of Saudi mutual funds have compared the performance of Islamic-law compliant mutual funds to that of conventional mutual funds. These studies have excessively focused on the impact of compliance with Islamic law on fund performance. Examples of such studies include Ashraf (Citation2013), BinMahfouz and Hassan (Citation2012), and Merdad et al. (Citation2010). The inconsistent findings in previous studies may be due to differences in model selection and sample period. In a study that examined several factors potentially affecting mutual fund performance, Alsubaiei (Citation2019) found that mutual fund performance has significant positive relationships with fund flows, size, and management fees and significant negative relationships with fund age and oil price volatility.

The unprecedented wide-ranging economic repercussions of the COVID-19 pandemic have disrupted normal operations in all economic sectors. Among others, the global equity market has been considered to be one of the most impacted sectors in the global economy. This motivated most researchers to uncover the impact of COVID-19 on stock pricing behaviour (Al-Awadhi et al., Citation2020; Erdem, Citation2020; Mazur et al., Citation2021; Rahman et al., Citation2021; Xu, Citation2021). Using various approaches, such as panel data analysis techniques, vector autoregression model, and event study methodology to identify this impact, most of the research found that the stock returns have been negatively affected by the COVID-19 pandemic. Moreover, Engelhardt et al. (Citation2021); Gao et al. (Citation2021) identified evidence of the impact of COVID-19 on stock market volatility, and Zaremba et al. (Citation2021) showed that responses to COVID-19 affected market liquidity in emerging markets. Corbet et al. (Citation2021) demonstrated that Chinese designated COVID-19 and influenza indicators have substantially affected Chinese financial markets, gold prices, the oil futures market, and the cryptocurrency market.

Other studies focused on the dynamic interaction in relationships between different markets and correlation dynamics between stock returns amid the COVID-19 pandemic. Elgammal et al. (Citation2021) documented evidence of bidirectional return spillover effects between equity and gold markets, and return spillover effects from energy returns to equity and gold returns, whereas Ajmi et al. (Citation2021) found bidirectional return spillover effects between energy market and equity market. More importantly, both studies found that return transmission relationships become more intense during the COVID-19 outbreak. As such, So et al. (Citation2021) analysed the relationship between Hong Kong’s stock returns in four recent financial crises. Unlike the previous three financial crises, the increase in systemic risk in the financial system during the COVID-19 outbreak led to a substantial increase in the stock returns’ connectedness. Generally, these findings indicate the possibility of mutual fund managers’ diversification opportunities being limited during the COVID-19 crisis.

A growth in COVID-19 cases impacts most stock returns in the Saudi market. Similar to all other countries, the government of Saudi Arabia introduced counter-spread measures, such as tightening or easing human movement and lockdown against COVID-19 depending on new confirmed cases. These measures negatively affected the operational performance of the stock market. By confirming the negative impact of COVID-19, Alzyadat and Asfoura (Citation2021) recorded that TSAI returns is negatively associated with the growth of new confirmed cases. The ongoing research in this area is considering the impact of both changes in the number of cases as well as the number of fatalities due to COVID-19. Atassi and Yusuf (Citation2021) investigated how both indicators affect market performance and found that the overall market responded significantly and negatively to an increase in new confirmed cases, and insignificantly and positively to the growth in fatalities. To the best of our knowledge, no a previous study has attempted to investigate the effect of the COVID-19 outbreak on mutual fund performance.

Equity-investment fund managers employ their expertise to change the compositions of their investments to reflect changing economy and market conditions to manage the risk of their portfolio. By changing the compositions of the funds, they aim to provide the best diversification and achieve superior performance for their investors (Bodie et al., Citation2010, p. 84). Thus, fund managers have implemented a similar approach to minimise the adverse impact of COVID-19 on the funds’ performances. Therefore, the growth in new cases of COVID-19 may not affect the performance of equity mutual funds significantly. However, considering the significant size of energy companies in the Saudi stock market with the evidence of more intensified return transmission relationships between the equity market and energy market during COVID-19 by Elgammal et al. (Citation2021) and the existing evidence of the impact of growth in COVID-19 cases on the overall Saudi market by Alzyadat and Asfoura (Citation2021) and Atassi and Yusuf (Citation2021) may reflect a potential impact of the spread of COVID-19 in Saudi Arabia on mutual fund performance, which has not yet been unearthed. Therefore, this study first builds on the methodologies of the recent studies in asset pricing models, including Fama and French (Citation2015, Citation2017); Foye (Citation2018) to measure mutual fund performance in Saudi Arabia. Then builds on the previous studies that investigated factors affecting mutual fund performance in Saudi Arabia, including Alsubaiei (Citation2019), Ashraf (Citation2013), BinMahfouz and Hassan (Citation2012), and Merdad et al. (Citation2010), and it considers the potential impact of the growth of COVID-19 cases on mutual fund performance to examine the potential impact of growth in COVID-19 cases, Islamic-law compliance, management fee, age of funds, and size of funds on the Saudi mutual fund performance that is estimated by the recent Fama-French five-factor model.

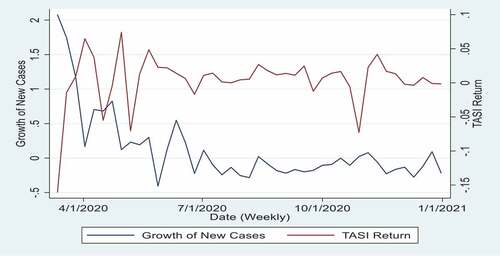

Figure shows the returns of the main index of the Saudi market (TASI) and the growth of COVID-19 new confirmed cases. It displays that the Saudi stock market was more sensitive to the growth of COVID-19 new confirmed cases during the earlier stages of the virus spread in the country. The figure shows that during the early weeks of the pandemic in Saudi Arabia, both the growth of COVID-19 new confirmed cases and TASI returns experienced severe fluctuations in opposite directions. After July 2020, the variants were in an opposite relationship but adopted less intense fluctuations. Our inferences in Figure are consistent with previous findings of Alzyadat and Asfoura (Citation2021) who measured the effect of COVID-19 on the main market index and found that the adverse market reaction was stronger during the early stage of the COVID-19 pandemic.

Figure 1. Response of TASI returns to the growth of COVID-19 new confirmed cases from March 2020 to December 2020. The authors estimated and analysed the variants in this figure.

3. Data and methodology

3.1. Data

This study used several secondary data sources to collect the required data. COVID-19 data in Saudi Arabia (number of confirmed new cases and fatalities) were obtained from the Ministry of Health’s COVID-19 daily report and the daily cases numbers were converted to weekly cases. Data for fund net asset values (fund trading prices) and financial ratios were collected from the Refinitiv-Eikon database. Out of the 254 existing public funds in Saudi Arabia, this study concentrated on 79 locally-oriented equity funds. The sampling processes excluded non-equity funds, funds that did not invest locally, and consolidated funds. This study relies on weekly returns to avoid the noise in the daily data. The study provides 43-time series return observations for each fund from March 5th to December 31st, 2020. The returns of 1-month SAMA billsFootnote2 were taken as the risk-free rate of returns, which is extracted from the website of the Saudi Central Bank.

3.2. Methodology

This study predicts that the economic repercussions of the COVID-19 outbreak have negatively affected mutual fund performance. The impact of the COVID-19 outbreak is measured based on the change in weekly new infections (CWI) and the change in weekly fatalities (CWF). To test the hypothesised impact of the COVID-19 outbreak on mutual fund performance, this study applies the model in Equationequation 1(1)

(1) .

Panel data regression analysis is the most appropriate approach. As the COVID-19 outbreak occurred over a relatively long period, the use of panel data analysis technique allows for identifying the impact of the outbreak over time and across funds. Furthermore, panel data regression models control for both time-series and cross-sectional variation in the data. Thus, it minimises estimation bias issues that could arise from heteroskedasticity and multicollinearity (Baltagi, Citation2008). To identify the best approach for the estimation of Equationequation 1(1)

(1) , the study performed the Chow (Citation1960) test to compare pooled-OLS model and fixed-effect model; Breusch and Pagan (Citation1980) Lagrange multiplier test to compare pooled-OLS model and random-effect model; and Hausman (Citation1978) test to compare fixed-effect model and random-effect model. These procedures of tests indicate the pooled-OLS regression estimation approach as the most appropriate approach to investigate the impact of the COVID-19 on mutual fund performance. However, to test the robustness, we also estimated Equationequation 1

(1)

(1) using a two-way fixed effects model controlling for both the fund-and-time fixed-effect dummy variables along with the main independent variables, CWI and CWF. The study estimated the models with heteroskedasticity robust standard errors.

where is mutual fund returns (unadjusted return calculated or risk-adjusted return estimated) for “ith” fund at week “t”, and the unadjusted return performance and the risk-adjusted return performance are determined based on Equationequations 2

(2)

(2) and Equation4

(4)

(4) , respectively.

is the intercept. The main explanatory variables, CWI and CWF, are calculated separately based on Equationequation 3

(3)

(3) given the growth rate and show how the COVID-19 cases fluctuated in the country.

is a vector of explanatory variables that are used to control the fund-specific variables. It includes management fee, size of the fund, age of the fund, and a dummy variable to represent compliance with Islamic law. The management fee is the annual fee paid by the subscribers to managers as a percentage of their investments. The natural logarithm of total net assets (TNA) held by a fund is taken to proxy the size of the fund. Age is the number of years elapsed from the inception of a fund. Islamic-law compliant is a dummy variable given 1 for funds defined as Islamic-law compliant by Tadawul (Saudi Securities Exchange), and 0 otherwise.

The unadjusted return for the mutual funds and the market (TASI) can be calculated using the equation given below.

where R represents unadjusted returns of the fund and market. Ln is the natural logarithm and P is the price of “ith” funds and the market index at time “t”. is dividends for fund i at week t (only applied in the calculation of funds’ return).

A modified version of the above equation has been used to measure the changes in COVID-19 cases (new infections and fatalities). The equation is separately estimated for the weekly change in infections (CWI) and the weekly change in fatalities (CWF).

To calculate the risk-adjusted return, it is necessary to isolate the other sources of risk that generally affect fund returns. Therefore, this study uses Fama and French (Citation2015) five-factor model to measure the risk-adjusted return performance of mutual funds operating in Saudi Arabia. EquationEquation 4(4)

(4) reproduces the five-factor model that measures the variability in fund returns that consider the risks of market risk premium, size, value, profitability, and investment. The study separately estimated the ordinary least squares regression model for each equity mutual fund to calculate the weekly risk-adjusted performance of funds.

where is the fund’s risk premium measured as fund excess return recorded by the ith fund for the period “t” over the risk-free return;

is the market risk premium measured as market excess return (TASI) over the risk-free return; αi represents the excess returns of fund i over the market;

is the risk-free rate of returns defined as returns of 1-month SAMA bills; β 1 to β 5 are the estimated coefficients, which exhibit each fund’s risk exposure on each factor that identified the sensitivity of the returns of fund i to the market risk and other risk factors: size (SMB), value (HML), profitability (RMW), and investment (CMA). SMBt is the difference of returns on small and big diversified portfolios, HMLt is the differences of returns of high and low book-to-market portfolios, RMW is the difference of returns of portfolios of robust and weak profitability, and CMA is the difference of return on stock portfolios of conservative and aggressive firms. εi,t represents an error term.

The Fama and French (Citation2015) five-factor model needs to construct portfolios by sorting the return on size, value, profitability, and investment of each observed stock in the market. Therefore, stocks are sorted into two size groups (big and small), three value groups (low, medium, and high), three profitability groups (robust, medium, and weak), and three investment groups (conservatives, medium, and aggressive). Stocks with a market capitalisation above the median of TASI capitalisation are classified big and those below are classified small. By obtaining the 30th and 70th percentile of the book-to-market ratio, operating profitability ratio, and investment growth ratios, stocks below the 30th percentile are identified as low value, weak profitability, and conservative stocks, respectively; above 70th percentile are classified as high valued, robust profitability, and aggressive investment stocks, respectively; and between 30th and 70th as the medium in each sorting.

The study formed 18 portfolios from the above stock classifications to construct the risk factors. To construct size and value factors, six portfolios (big-low, big-medium, big-high, small-low, small-medium, and small-high) were formed based on the intersection of the two size groups and the three book-to-market groups. Mimicking the same steps that are used for the size and value factors, six portfolios (big-weak, big-medium, big-robust, small-weak, small-medium, and small-robust) were formed for the size and profitability factors. Another six portfolios (big-conservatives, big-medium, big-aggressive, small-conservatives, small-medium, and small-aggressive) were formed for the size and the investment factors. The SMB is calculated as the average of the three joint size factors produced in each previous sorting. Then, the value-weighted return of portfolios was taken as the corresponding values of each factor in the model. Table shows the values for the risk factors that were identified.

Table 1. Measurements of the risk factors in the Fama and French (Citation2015) five-factor model

4. Descriptive statistics

Tables present the descriptive statistics and the pairwise correlations of the test variables, respectively. During the COVID-19 period from 5th March to 31 December 2020, equity mutual funds gained an average unadjusted return of 0.41% compared to 0.35% for the overall market (TASI) and experienced a slightly lower standard deviation of 3.07% compared to the market’s 3.76%. On average, mutual fund managers in Saudi Arabia provided their investors with higher returns associated with lower risk compared to the market during the COVID-19 crisis. The average of CWI and CWF was 12.26% and 10.06%, respectively. The pairwise-correlation coefficients for variables show that there is no significant multicollinearity between the dependent variables.

Table 2. Summary statistics of the main variables

Table 3. Pairwise correlations between mutual fund returns and other variables

Table presents the descriptive statistics of risk factors that were used as the explanatory variables in the Fama and French (Citation2015) five-factor model (EquationEquation 4(4)

(4) ). TASI’s average risk premium during the sample period was 0.34%. The size factor indicates that, on average, a portfolio that invests in small firms outperforms a portfolio that concentrates on big firms by 0.1%. The mean of investment factor suggests that holding a portfolio of conservative firms would outperform a portfolio that contains aggressive firms by 0.03%. The value factor indicates that a portfolio of value firms underperforms a portfolio of growth firms by 0.55%, and the profitability factor shows that a portfolio of robust profitability firms also underperforms a portfolio of weak profitable firms by approximately 0.06%. The estimated correlations’ coefficient for factor variables revealed that there is no significant multicollinearity among them.

Table 4. Summary statistics of the weekly Fama-French five-factor model, March 2020 to December 2020

5. Empirical analysis

Table summarises the estimated Fama-French five-factor model given in Equationequation 4(4)

(4) . The estimated R square shows that the model explains approximately 75% of the equity mutual fund returns. The estimated coefficient for the market risk premium (TASIRP) shows a significant positive relationship with the mutual fund return. The estimated market systematic risk revealed that the 1% increase in market excess return leads to a 0.68% increase in mutual fund return, indicating that funds are less volatile than the overall market return. The results also show that the size and the value factors have a significant positive association and the profitability factor has a significant negative association with fund returns. Furthermore, Table also records a statistically significant alpha coefficient of 0.15% on mutual fund returns in Saudi Arabia during the study period. Mutual funds gaining a significant and positive risk-adjusted return of 0.15% contribute to the theory of superior mutual fund performance during financial crises in developed markets (Kosowski, Citation2011; Moskowitz, Citation2000). It also supports the findings of a better performance of Saudi Arabian mutual funds during a financial crisis (Merdad et al., Citation2010). More importantly, the findings show evidence that mutual funds can still generate significant positive risk-adjusted returns even after controlling for two additional risk factors of profitability and investment that have never been considered in previous studies. As the results of the current study show that the profitability risk factor is statistically significant, this factor may play a dominant role in Saudi mutual funds’ expected returns which necessitate considering it in future research for precise performance measurement. However, the results contradict other studies by Mirza et al. (Citation2020); Pástor and Vorsatz (Citation2020), which reported that mutual funds are significantly underperforming their benchmarks in developed markets during the COVID-19 pandemic. The contradiction with these studies may be attributed to the classification of market development as Huij and Post (Citation2011) demonstrated better performance of mutual funds operating in emerging markets compared to those operating in developed markets.

Table 5. OLS-regression of the fund excess return on the Fama-French five-factor model, March 2020 to December 2020

Table presents the estimated pooled-OLS regression model given in Equationequation 1(1)

(1) , which investigates the impact of CWI, CWF, and controlling variables on mutual fund unadjusted returns. The selection of independent variables for estimation includes the following: (1) only CWI in the model; (2) both CWI and other fund-specific variables in the model; (3) only CWF in the model; and (4) both CWF and other fund-specific variables in the model. As shown in Table , CWI had a significant negative effect of −3.12% on the mutual fund unadjusted returns in models (1) and (2). The association between CWI and unadjusted returns does not change estimations with CWI in model (2) even after including the controlling variables. These results confirm the significant and negative effect of the COVID-19 outbreak on the mutual fund unadjusted returns. The extended analysis of the impact of the COVID-19 outbreak on individual mutual funds’ unadjusted returns is discussed later in this paper. The significant positive effect of Islamic-law compliance on mutual fund performance during the COVID-19 crisis is consistent with Merdad et al. (Citation2010) findings of better performance of Islamic-law compliant mutual funds during the financial crisis due to higher compensations for riskier holdings by these mutual funds. Furthermore, this study found that the age of funds has a significant positive effect on the mutual fund performance during the COVID-19 crisis, indicating a better performance of long-time experienced managers during the financial crisis, and this is in contrast to the negative effect of funds’ age documented by Alsubaiei (Citation2019) in the long-time framework study.

Table 6. Pooled-OLS regression of funds unadjusted return on CWI and CWF

In contrast to the findings of the regression that used CWI as an explanatory variable, the regression that sought the association of CWF on unadjusted return reordered a positive association between unadjusted return and the CWF. As explained by Bodie et al. (Citation2010), forward-looking investors use current information to predict future market conditions. Therefore, it can be assumed that investors in the market have predicted the CWF based on the CWI in advance according to the available wide-world average mortality rate of 2.36% (Worldometers Citation2021). Investors immediately react to CWI, expecting a similar mortality rate in the future. However, the actual mortality rate in Saudi Arabia which started developing 3 weeks following the infection was 1.60% (Worldometers Citation2021), which was remarkably lower than what was initially assumed. Therefore, the positive coefficients recorded for the CWF may be evidence that the market is adjusting its overestimation of fatalities in advance and reacting to it as positive news.

Table shows the pooled-OLS regression estimation of Equationequation 1(1)

(1) that quantifies the impact of CWI, CWF, and control variables on the mutual fund risk-adjusted returns. The following independent variables were chosen for the estimation procedure: (1) only CWI model; (2) both CWI and other controlling variables model; (3) only CWF model; and (4) both CWF and other controlling variables model. Similar to the findings of the unadjusted return, the CWI was significant and had a negative impact on the mutual fund risk-adjusted returns. On average, for every 1% increase in new cases, fund risk-adjusted performances declined by approximately 0.0063%. The results remained consistent even after adding fund-specific controlling variables. This study did not find sufficient evidence on the impact of other controlling variables on the mutual fund risk-adjusted returns during the study period except for Islamic-law compliant mutual funds which are generally compensated for holding riskier equities (Merdad et al., Citation2010). The CWF impacts the mutual fund risk-adjusted performance at a 10% significance level as shown in models (3) and (4).

Table 7. Pooled-OLS regression of fund risk-adjusted returns on growth in CWI and CWF

The results of this study provide unprecedented evidence confirming the impact of the spread of COVID-19 cases as a new factor negatively impacting equity mutual funds’ unadjusted and risk-adjusted returns in Saudi Arabia. The current findings are consistent with previous studies of Alzyadat and Asfoura (Citation2021); Atassi and Yusuf (Citation2021) that measured the impact of the COVID-19 outbreak on the Saudi main market index and sub-indices. The negative impact of the COVID-19 outbreak across mutual funds shows evidence of low-resilient in mutual funds unadjusted and risk-adjusted returns to the economic restrictions associated with the spread of COVID-19. This significant and negative association could have resulted due to the counter-assets choices made by the fund managers to overcome the negative effect of COVID-19. The general characteristics of holdings can be inferred from the coefficient signs in Table . The significant positive SMB indicates mutual funds’ net exposure to small-cap stocks (Omri et al., Citation2019), which were indeed affected significantly and negatively during the COVID-19 crisis. The net exposure to small-cap stocks by Saudi mutual funds during the crisis could be a reason for the negative impact of the increase in COVID-19 cases on risk-adjusted returns across mutual funds. However, no information is publicly available on managers’ specific equities selection behaviour to verify this claim.

To conduct a robustness test for estimations of Equationequation (1)(1)

(1) , we replaced the fund-level controlling variables with fund-fixed effects and time-fixed effects dummy variables. Table shows the estimated results of the model, which confirms that CWI continued to have a significant negative impact on both mutual fund unadjusted return and mutual fund risk-adjusted performance. Moreover, the results show that the impact of CWF continued to be significant and positive. The results in Table confirm that the above estimations in Table and Table are not biased due to the omitted variables.

Table 8. Entity-and-time fixed effect regression model of funds unadjusted return, and funds risk-adjusted return on CWI and CWF

After documenting the negative impact of the COVID-19 outbreak across mutual funds’ performances, the study focuses on the success of individual mutual fund managers to alleviate the consequences of the COVID-19 outbreak on fund performance under their management in comparison to market portfolio (passive-investment strategy). Such an analysis identifies the existence of individual funds that constructed crisis-defensive portfolios. Therefore, the study tests the impact of growth in COVID-19 new confirmed cases on the unadjusted returns of individual mutual funds, and then test if this potential impact on individual mutual funds is significantly different from the impact on returns of the market portfolio (TASI).

The regression model given in Equationequation 5(5)

(5) is employed to regress TASI returns on CWI, and regress mutual fund returns separately on CWI. The estimated regression coefficients of each fund are post hoc combined with estimated TASI regression coefficients using Weesie (Citation1999) seemingly unrelated estimation approach. The estimated regression slope of TASI returns on CWI is −0.0338 and significant at the 99% significance level. This slope is used as a benchmark to distinguish the funds with significantly different slopes. The estimated regression slopes of the 79 mutual funds on CWI range between −0.00296 and −0.0617, and they are significant at least on a 95% significance level. To identify the funds that were impacted by the COVID-19 outbreak significantly different than the market portfolio, the study performs Wald test of H0:

=

that rejects the null hypothesis if Clogg et al. (Citation1995) Z–score in Equationequation (6)

(6)

(6) is larger than the appropriate

threshold. Table summarises the final outcomes of coefficients equality.Footnote3 In the table, funds with slope coefficients that are significantly higher than the slope of the overall market (−0.0338) are counted in the first row, not significantly different are counted in the second row, and significantly lower are reported in the third row.

Table 9. The impact of COVID-19 outbreak on returns of the market and the 79 mutual funds

where is the fund and TASI unadjusted returns calculated in Equationequation 1

(1)

(1) at week t,

is the intercept of the model, the independent variable

is CWI, and

is the error term.

and

are the estimated regression slopes of ith fund returns and TASI returns on growth in COVID-19 cases respectively.

and

are the standard error of the estimated slopes, respectively.

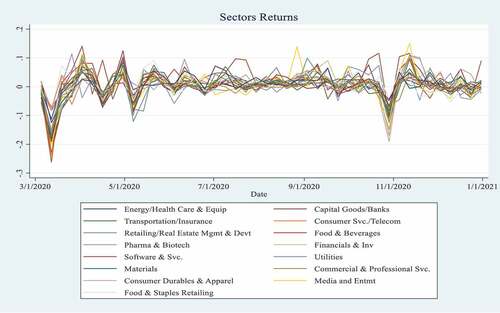

The growth in COVID-19 cases negatively impacted the return for all 79 funds in the sample. The responses of most mutual funds’ (71 out of 79) returns to CWI do not significantly differ from the response of the main market portfolio. The well-diversified holdings of stocks across all industries by most mutual funds may be the reason for the equal negative impact of COVID-19 on funds and the overall market. Industries’ return movement in the Saudi Arabia stock market presented in Figure displays strong correlations between the returns of most industries during the COVID-19 crisis.Footnote4 It is evident that irrespective of the industries or stocks, COVID-19 brought similar impacts on the performance of every investment. The higher connectedness of stock returns during the COVID-19 crisis compared to three other crises was confirmed in the Hong Kong stock market (So et al., Citation2021).

Figure 2. Time series returns’ movements for all sectors in the Saudi market from March 5th to December 31st, 2020. The authors estimated and analysed the variants in this figure.

Out of 79 mutual funds, five funds were able to beat the market in managing the probable negative impact of COVID-19. These funds are mainly invested in essential goods and services industries, such as food production, food and staples retailing, utilities, and health care equipment and services. These industries are considered essential in every situation such as a pandemic and natural disasters. Therefore, stocks in these industries may not have suffered during the COVID-19 times compared to other industries. Consequently, even without rebalancing their portfolios, such funds could have faced the minimum impact of COVID-19. In addition, actions taken by mutual fund managers could also have reduced the negative impact of COVID-19. This indicates that only mutual funds invested in essential services may provide investors with capital-defensive investment options during a pandemic era. Non-essential industries and services were heavily impacted by health measures introduced to mitigate the spread of COVID-19. Three funds that mainly invested in energy, commercial and professional services, and real estate management and development stocks recorded a significantly higher negative impact compared to the overall market. The current findings may assist subscribers to mutual funds to allocate their investments during pandemics or similar natural disasters. However, they must also consider their long-term and short-term investment goals. Although mutual funds excessively invested in non-essential industries were impacted more during COVID-19, and those invested in essential industries and services were less impacted, the stock market always generously compensates riskier investments.

6. Conclusion

The outbreak of COVID-19 has impacted economic activities globally and most financial markets have witnessed severe uncertainty. This study measured the unadjusted return and risk-adjusted performance of actively-managed mutual funds during the COVID-19 crisis. On average, mutual funds in Saudi Arabia gained an unadjusted return of 0.414% compared to an unadjusted return for the main market (TASI) of 0.352%. This study is the first to apply the Fama and French (Citation2015) five-factor model to measure the risk-adjusted performance of active mutual funds in Saudi Arabia. The model is strongly significant and explains approximately 75% of the equity mutual fund returns variation. Most importantly, the mutual funds gained a significant positive alpha of 0.15% and it shows the solid mutual fund performance during the COVID-19 period.

After measuring the performance of active mutual funds, this study used panel data analysis to measure the impact of CWI and CWF on unadjusted return performance and risk-adjusted performance of equity mutual funds. The findings suggest that CWI had a significant and negative impact on unadjusted returns and risk-adjusted returns. However, CWF cases had a significant and positive impact on unadjusted returns as fatalities seemed to be lesser than previous expectations. Only a few individual mutual funds provided investors with capital-defensive investment options during the pandemic and focused their investments on sectors of essential goods and services, including food production, food and staples retailing, utilities, and health care equipment and services. Future research may conduct advanced analysis of the connectedness between stocks during COVID-19 (So et al., Citation2021) or the spillovers between multiple financial markets (Ajmi et al., Citation2021; Elgammal et al., Citation2021) in the Saudi context and then link between these potential intensified contagions and equity mutual fund performance.

correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Acknowledgements

A special acknowledgement to two anonymous reviewers for their valuable comments which significantly improved our paper and to Mr. Asim Alshaikhmubarak for providing daily numbers of new confirmed cases and fatalities of COVID-19 in a manageable file.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Haidar Alqadhib

Haidar Alqadhib is a lecturer at King Faisal University and a PhD Candidate at Victoria University, Australia. He obtained his M.S. in Finance from Texas A&M University-Commerce, USA. He has taught principles of financial management 1 & 2, financial markets & institutions, and banks management. Haidar’s research interests focus on investments funds, assets pricing, and financial markets and institutions.

Nada Kulendran

Nada Kulendran is an Honorary Fellow at Victoria University, Melbourne, Australia. He obtained his PhD from Monash University, Australia. He has extensive experience in teaching statistics, economics, and financial risk management subjects in multiple countries. His area of expertise includes econometric modelling, financial markets forecasting, and volatility forecasting. He has made a sustained contribution in his area of research that resulted in the publication of research articles in high impact journals

Lalith Seelanatha

Lalith Seelanatha is serving as a lecturer in finance at School of Business. He is teaching in both postgraduate and undergraduate Programs in the school and doing research in banking, and finance.

Notes

1. North America includes stocks from the US and Canada; Europe includes stocks from Austria, Belgium, Den- mark, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, and the United Kingdom; and Asia Pacific includes stocks from Australia, New Zealand, Hong Kong, and Singapore.

2. SAMA bills are the Saudi central bank’s treasury bills.

3. The individual regression results and regression coefficients’ equality tests are available upon request.

4. Table A1 in the appendix also presents the correlation coefficients of the Saudi sectors’ indices returns during the COVID-19 crisis.

References

- Ajmi, H., Arfaoui, N., & Saci, K. (2021). Volatility transmission across international markets amid COVID 19 pandemic. Studies in Economics and Finance, 38(5), 926–22. https://doi.org/10.1108/SEF-11-2020-0449

- Al-Awadhi, A., Alsaifi, K., Al-Awadhi, A., & Alhammadi, S. (2020). Death and contagious infectious diseases: Impact of the COVID-19 virus on stock market returns. Journal of Behavioral and Experimental Finance, 27(1), 1003–1026. https://doi.org/10.1016/j.jbef.2020.100326

- AlRahahleh, N., & Bhatti, I. (2017). Mutual funds performance in Saudi Arabia. <https://cma.org.sa/en/Market/Documents/MF_in_KSA_en.pdf>

- Alsubaiei, B. 2019, ‘Mutual fund flows and performance in Saudi Arabia: analysis of how new factors impact fund flow and performance’, PhD thesis, Loughborough University.

- Alsubaiei, B. (2021). Do stock market risk factors explain mutual fund returns? Evidence from Saudi Arabia. The Scientific Journal of King Faisal University: Humanities and Management Sciences, 23(1), 1–7. https://doi.org/10.37575/h/mng/210044

- Alzyadat, J., & Asfoura, E. (2021). The effect of COVID-19 pandemic on stock market: An empirical study in Saudi Arabia. The Journal of Asian Finance, Economics and Business, 8(5), 913–921. https://doi.org/10.13106/jafeb.2021.vol8.no5.0913

- Ashraf, D. (2013). Performance evaluation of Islamic mutual funds relative to conventional funds. International Journal of Islamic and Middle Eastern Finance and Management, 6(2), 105–121. https://doi.org/10.1108/17538391311329815

- Atassi, H., & Yusuf, N. (2021). The effect of COVID-19 on investment decisions in Saudi stock market. The Journal of Asian Finance, Economics and Business, 8(6), 797–807. https://doi.org/10.13106/jafeb.2021.vol8.no6.0797

- Baltagi, B. (2008). Econometric analysis of panel data (Third ed.). John Wiley & Sons Ltd., West Sussex.

- BinMahfouz, S., & Hassan, K. (2012). A comparative study between the investment characteristics of islamic and conventional equity mutual funds in Saudi Arabia. The Journal of Investing, 21(4), 128–143. https://doi.org/10.3905/joi.2012.21.4.128

- Bodie, Z., Kane, A., & Marcus, A. (2010). Essentials of Investments (8th edn ed.). McGraw-Hill.

- Breusch, T., & Pagan, A. (1980). The Lagrange multiplier test and its applications to model specification in econometrics. The Review of Economic Studies, 47(1), 239–253. https://doi.org/10.2307/2297111

- Campbell, J., & Vuolteenaho, T. (2004). Bad beta, good beta. American Economic Review, 94(5), 1249–1275. https://doi.org/10.1257/0002828043052240

- Carhart, M. (1997). On persistence in mutual fund performance. The Journal of Finance, 52(1), 57–82. https://doi.org/10.1111/j.1540-6261.1997.tb03808.x

- Chow, G. C. (1960). Tests of equality between sets of coefficients in two linear regressions. Econometrica: Journal of the Econometric Society, 28(3), 591–605. https://doi.org/10.2307/1910133

- Clogg, C. C., Petkova, E., & Haritou, A. (1995). Statistical methods for comparing regression coefficients between models. American Journal of Sociology, 100(5), 1261–1293. https://doi.org/10.1086/230638

- Corbet, S., Hou, Y. G., Hu, Y., Oxley, L., & Xu, D. (2021). Pandemic-related financial market volatility spillovers: Evidence from the Chinese COVID-19 epicentre. International Review of Economics & Finance, 71(1), 55–81. https://doi.org/10.1016/j.iref.2020.06.022

- Elgammal, M., Ahmed, W., & Alshami, A. (2021). Price and volatility spillovers between global equity, gold, and energy markets prior to and during the COVID-19 pandemic. Resources Policy, 74(1), 102334. https://doi.org/10.1016/j.resourpol.2021.102334

- Engelhardt, N., Krause, M., Neukirchen, D., & Posch, P. (2021). Trust and stock market volatility during the COVID-19 crisis. Finance Research Letters, 38(1), 101873. https://doi.org/10.1016/j.frl.2020.101873

- Erdem, O. (2020). Freedom and stock market performance during Covid-19 outbreak. Finance Research Letters, 36(1), 101671. https://doi.org/10.1016/j.frl.2020.101671

- Fama, E., & French, K. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1), 3–56. https://doi.org/10.1016/0304-405X(93)90023-5

- Fama, E., & French, K. (2004). The capital asset pricing model: Theory and evidence. Journal of Economic Perspectives, 18(3), 25–46. https://doi.org/10.1257/0895330042162430

- Fama, E., & French, K. (2010). Luck versus skill in the cross‐section of mutual fund returns. The Journal of Finance, 65(5), 1915–1947. https://doi.org/10.1111/j.1540-6261.2010.01598.x

- Fama, E., & French, K. (2015). A five-factor asset pricing model. Journal of Financial Economics, 116(1), 1–22. https://doi.org/10.1016/j.jfineco.2014.10.010

- Fama, E., & French, K. (2017). International tests of a five-factor asset pricing model. Journal of Financial Economics, 123(3), 441–463. https://doi.org/10.1016/j.jfineco.2016.11.004

- Foye, J. (2018). A comprehensive test of the Fama-French five-factor model in emerging markets. Emerging Markets Review, 37 , 199–222. https://doi.org/10.1016/j.ememar.2018.09.002

- Gao, X., Ren, Y., & Umar, M. (2021). To what extent does COVID-19 drive stock market volatility? A comparison between the US and China. Economic Research-Ekonomska Istraživanja, forthcoming , 1–21. https://doi.org/10.1080/1331677X.2021.1906730

- General Authority for Statistics. (2020). Gross Domestic Product. viewed 28/06/2021 <https://www.stats.gov.sa/sites/default/files/Gross%20Domestic%20Product%20annual%202020%20EN.pdf>

- Grinblatt, M., & Titman, S. (1993). Performance measurement without benchmarks: An examination of mutual fund returns. Journal of Business, 66(1), 47–68. https://doi.org/10.1086/296593

- Hausman, J. (1978). Specification tests in econometrics. Econometrica, 46(1), 1251–1272. https://doi.org/10.2307/1913827

- Huij, J., & Post, T. (2011). On the performance of emerging market equity mutual funds. Emerging Markets Review, 12(3), 238–249. https://doi.org/10.1016/j.ememar.2011.03.001

- Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance, 48(1), 65–91. https://doi.org/10.1111/j.1540-6261.1993.tb04702.x

- Jensen, M. (1968). The performance of mutual funds in the period 1945–1964. The Journal of Finance, 23(2), 389–416. https://doi.org/10.1111/j.1540-6261.1968.tb00815.x

- Kosowski, R. (2011). Do mutual funds perform when it matters most to investors? US mutual fund performance and risk in recessions and expansions. The Quarterly Journal of Finance, 1(3), 607–664. https://doi.org/10.1142/S2010139211000146

- Kosowski, R., Timmermann, A., Wermers, R., & White, H. (2006). Can mutual fund “stars” really pick stocks? New evidence from a bootstrap analysis. The Journal of Finance, 61(6), 2551–2595. https://doi.org/10.1111/j.1540-6261.2006.01015.x

- Malkiel, B. (1995). Returns from investing in equity mutual funds 1971 to 1991. The Journal of Finance, 50(2), 549–572. https://doi.org/10.1111/j.1540-6261.1995.tb04795.x

- Mazur, M., Dang, M., & Vega, M. (2021). COVID-19 and the march 2020 stock market crash. Evidence from S&P1500. Finance Research Letters, 38(1), 101690. https://doi.org/10.1016/j.frl.2020.101690

- Merdad, H., Hassan, K., & Alhenawi, Y. (2010). Islamic versus conventional mutual funds performance in Saudi Arabia: A case study. Journal of King Abdulaziz University: Islamic Economics, 23(2), 161–198. https://doi.org/10.4197/Islec.23-2.6

- Mirza, N., Naqvi, B., Rahat, B., & Rizvi, S. K. A. (2020). Price reaction, volatility timing and funds’ performance during Covid-19. Finance Research Letters, 36(1), 101657. https://doi.org/10.1016/j.frl.2020.101657

- Moskowitz, T. J. (2000). Mutual fund performance: An empirical decomposition into stock-picking talent, style, transactions costs, and expenses: Discussion. The Journal of Finance, 55(4), 1695–1703. https://doi.org/10.1111/0022-1082.00264

- Omri, A., Soussou, K., & Goucha, N. (2019). On the post-financial crisis performance of Islamic mutual funds: The case of Riyad funds. Applied Economics, 51(18), 1929–1946. https://doi.org/10.1080/00036846.2018.1529403

- Pástor, Ľ., & Vorsatz, M. B. (2020). Mutual fund performance and flows during the COVID-19 crisis. The Review of Asset Pricing Studies, 10(4), 791–833. https://doi.org/10.1093/rapstu/raaa015

- Rahman, M., Amin, A., & Al-Mamun, M. (2021). The COVID-19 outbreak and stock market reactions: Evidence from Australia. Finance Research Letters, 38(1), 101832. https://doi.org/10.1016/j.frl.2020.101832

- Sharpe, W. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance, 19(3), 425–442. https://doi.org/10.1111/j.1540-6261.1964.tb02865.x

- Sheppard, D., McCormick, M., Raval, A., Brower, D., & Lockett, H. (2020). ‘US oil price below zero for first time in history’, Financial Times, 21 April 2020, https://www.ft.com/content/a5292644-958d-4065-92e8-ace55d766654

- So, M. K., Chu, A. M., & Chan, T. W. (2021). Impacts of the COVID-19 pandemic on financial market connectedness. Finance Research Letters, 38(1), 101864. https://doi.org/10.1016/j.frl.2020.101864

- Weesie, J. (1999). Seemingly unrelated estimation and the cluster-adjusted sandwich estimator. Stata Technical Bulletin, 52(1), 37–47. https://www.stata-press.com/journals/stbcontents/stb52.pdf

- Wermers, R. (2000). Mutual fund performance: An empirical decomposition into stock‐picking talent, style, transactions costs, and expenses. The Journal of Finance, 55(4), 1655–1695. https://doi.org/10.1111/0022-1082.00263

- World Bank Group. (2020). June 2020 Global Economic Prospects. <https://www.worldbank.org/en/publication/global-economic-prospects>

- Worldometers 2021, Coronavirus Cases, Worldometers website, 28/July/2021, <https://www.worldometers.info/coronavirus/#countries>

- Xu, L. (2021). Stock Return and the COVID-19 pandemic: Evidence from Canada and the US. Finance Research Letters, 38(1), 101872. https://doi.org/10.1016/j.frl.2020.101872

- Zaremba, A., Aharon, D. Y., Demir, E., Kizys, R., & Zawadka, D. (2021). COVID-19, government policy responses, and stock market liquidity around the world: A note. Research in International Business and Finance, 56(1), 101359. https://doi.org/10.1016/j.ribaf.2020.101359

Appendix

Table A1. Summary statistics for weekly returns for 20 sectors’ indices in the Saudi stock exchange (TASI) between 5th March and 31st Dec 2020